An Approach to the Evaluation of the Quality of Accounting Information Based on Relative Entropy in Fuzzy Linguistic Environments

1

School of Business Administration, China University of Petroleum-Beijing, Beijing 102249, China

2

China National Institute of Standardization, Beijing 100191, China

*

Author to whom correspondence should be addressed.

Entropy 2017, 19(4), 152; https://doi.org/10.3390/e19040152

Submission received: 13 March 2017

/

Revised: 24 March 2017

/

Accepted: 28 March 2017

/

Published: 5 April 2017

Abstract

:There is a risk when company stakeholders make decisions using accounting information with varied qualities in the same way. In order to evaluate the accounting information quality, this paper proposed an approach to the evaluation of the quality of accounting information based on relative entropy in fuzzy linguistic environments. Firstly, the accounting information quality evaluation criteria are constructed not only from the quality of the accounting information content but also from the accounting information generation environment. Considering that the rating values with respect to the criteria are in linguistic forms with different granularities, the method to deal with the linguistic rating values is given. In the method, the linguistic terms are modeled with the 2-tuple linguistic model. Relative entropy is used to calculate the information consistency, which is used to derive the weight of experts and criteria. Finally, the example is given to illustrate the feasibility and practicability of the proposed method.

1. Introduction

With economic development, accounting information is increasingly important. The quality of the accounting information of each company is different since accounting practitioners’ professional ability and professional ethics vary greatly within companies. The quality of accounting information affects the decision-making of investors and the interests of creditors. Moreover, it is related to the efficiency of the market operation and the results of national economic regulation and control.

According to the official data of the China Securities Regulatory Commission, as of September 2016, there are 2952 listed companies in China (A shares and B shares). Although these financial reports have been authenticated by the third party auditors, it is hard to discriminate between “pass” and “fail” for the accounting information through the audit reports [1]. The personalized needs of different users cannot be satisfied by the evaluation results of accounting information quality from auditors.

The evaluation attributes of accounting information quality are the premise for implementing the evaluation. Many studies are based on the design of attributes for evaluating accounting information quality. For example, Xu and Cai designed the quantitative attributes [2]. Wu and Liu pointed out that attributes should include quantitative attributes and qualitative attributes [3]. Zheng and Lin constructed an accounting information quality evaluation system based on the supervision of the government and the public. From the perspective of investor protection [4], Bai constructed an accounting information quality evaluation system with 13 attributes in three levels according to the three dimensions of company accounting information generation [5]. Wang and Wan constructed the evaluation attribute system of accounting information quality with the background of big data [6]. Li and Shi think that the quality of accounting information should include the quality of accounting information disclosure and the quality of accounting information content [7]. Zang and Zhang constructed the evaluation attribute system including the three aspects of the company accounting system, the company internal management, and the external supervision situation [8].

These researchers made valuable contributions to the evaluation of accounting information quality. However, the impact of the accounting information generation environment on the quality of information is ignored. They only pay attention to the final financial results of economic operation. The environmental impact on the quality of information is extensive. It affects the reliability and relevance of the information. Moreover, it also has influence not only on the data at a point in time, but on the data for a long period of time.

The appropriate evaluation method is the key for deriving the result of the accounting information quality evaluation. Li and Shi use the expert scoring method to score the expert’s weight and the company’s qualitative attributes and calculate the sample company’s accounting information quality score [7]. Zang and Zhang applied the fuzzy evaluation method to quantitatively analyze the attribute system and determined the attribute weight by an analytic hierarchy process (AHP) [8]. In contrast, Xu et al. used principal component analysis to weight each attribute [2]. Shyi-Ming et al. applied the triangular fuzzy number method to resolve group decision problems [9]. Chen and Yang evaluated the company’s credit state and analyzed the sensitivity of its consensus degree by their method [10].

The linguistic terms in these methods are mostly modeled with triangular fuzzy numbers. When using the triangular fuzzy numbers to deal with the linguistic evaluation information, the linguistic terms needs to be first transformed into the manipulation machine format. Since the computing results cannot be matched to the initial linguistic terms, the retranslation step is used to express the results in the initial expression domain [11]. There often exists a loss of information in these processes. Moreover, in these methods, the preferences of experts and the weights of experts are neglected. The linguistic terms given to experts for expressing their preferences are with the same granularity without the consideration of the preferences of experts. The more specialized experts will give more precise information with greater granularity. The weights of experts are not the same in the evaluation. The 2-tuple linguistic model is a method that is used to deal with the linguistic evaluation information. Yong Liu, Yong-Jie Xing, and Chen Xing applied the method of 2-tuple linguistic dynamic multiple attribute decision making with entropy weight to evaluate the risk of projects and virtual enterprises [12,13]. The key to solving the multi-attribute group decision-making problem is to determine the weight. Multiple attribute group decision making problems with interval-valued hesitant fuzzy sets can be solved by variable power geometric operators based on entropy weights [14]. Also, scholars have proposed combining the method of entropy and attribute impact loss for determining the weights [15]. Moreover, inter-relationships among attributes [16] are emphasized by computing the partition Bonferroni mean. Additionally, Estrella et al. proposed a software tool called Flintstones [17] that was developed to implement linguistic computational models such as the 2-tuple linguistic model.

In order to resolve the above-stated problems, in this paper, we proposed the approach to the evaluation of the quality of accounting information based on relative entropy in fuzzy linguistic environments. Firstly, the evaluation attributes are constructed. Not only are the comprehensive attributes constructed based on the research results of the existing literature on the accounting information content quality, but it also constructs the attributes from the environmental aspects. Secondly, the method for dealing with the linguistic evaluation information is proposed. The 2-tuple linguistic model is used to deal with the linguistic evaluation information. With the 2-tuple linguistic model, the loss of information is avoided since no retranslation process is needed. The smaller the relative entropy is, the more consistent the information is. So the relative entropy is used to measure the information similarity and the weight of experts [18,19]. Moreover, due to the difference in the background and the level of knowledge of the evaluator, linguistic decision analysis problems based on multi-granularity linguistic term sets are common [20,21]. In this study, linguistic term sets with multi-granularity are provided. Experts can choose the linguistic term sets they prefer to give their opinions.

The contribution of this paper is mainly reflected in two aspects of the attributes and methods, which are summarized as the following four points. First, on the basis of extensively studying the existing literature about the evaluation attributes of accounting information quality, this paper integrates the evaluation attributes and improves the system of accounting information quality evaluation attributes. Then, it proposes that the evaluation system should contain the accounting information generation environment factors, because the environment affects the correlation as well as the reliability of the financial information. In addition, the relative entropy is used to calculate the consistency between the individual evaluator and the evaluator group instead of the traditional method of calculating the consistency, to make up for the shortcomings of information confusion. Lastly, it is necessary to make the multi-granularity linguistic information uniform since different evaluators may use different linguistic term sets due to their own expertise and the degree of familiarity with the evaluated company.

The structure of the rest of this paper is as follows: Section 2 reviews the Two-tuple linguistic model. In the following section, the evaluation attributes are constructed from the aspects of accounting information content quality and accounting information generation environment quality. Section 4 presents the method to deal with the linguistic information based on relative entropy. Section 5 provides an illustrative application. Section 6 concludes the paper.

2. Related Works

2.1. 2-Tuple Linguistic Model

Due to the complexity and uncertainty of objective things and the fuzziness of human thoughts, some attributes are more suitable for evaluation in linguistic form. For the evaluation of linguistic information, Spanish professor Herrera proposed a 2-tuple semantic information evaluation method [11]. In the model, the linguistic information is represented by a linguistic term and a real number, which is continuous in its domain. No approximation process is needed to translate between the manipulation machine format and the initial linguistic format, and the loss of information is avoided. It is more precise than the method based on the extension principle [22]. In the following, the 2-tuple linguistic model is briefly reviewed.

The 2-tuple semantics representation model represents linguistic information by means of a 2-tuple , where is a linguistic label and is a numerical value that represents the value of the symbolic translation.

Definition 1.

Definition 2.

Let , where denotes the granularity of set , and is the result of a symbolic aggregation operation, and then the 2-tuple that expresses the equivalent information is obtained with the following function:

where , round is the usual rounding operation, has the closest attribute label to , and is the value of the symbolic translation [11,23,24].

Definition 3.

Definition 4.

Definition 5.

Definition 6.

- (1)

- If then is bigger than ;

- (2)

- If then

- (a)

- if then is bigger than ;

- (b)

- if then is equal to ;

- (c)

- if then is smaller r than .

Definition 7.

2.2. Relative Entropy

The concept of entropy was introduced by Clausius in 1865, and the second law of thermodynamics was expressed in the form of an isolated system entropy law [28]. Boltzmann and Planck [29] gave the microscopic statistical formula of entropy, and used entropy to represent the disorder degree of a system. In 1948, Shannon [30] extended statistical entropy to the theory of information and established the system theory of communication coding. In 1951, Kullback and Leibler proposed the concept of relative entropy [31].

The relative entropy, also known as the Kullback–Leibler divergence [32], is a measure of the distance between two probability distributions of a variable. Given two probability distributions X and Y over a discrete variable, let , , then the relative entropy is defined as follows [24]:

where X = (…, ), Y = (,…,) are the two discrete probability distributions. Relative entropy is not strictly a distance; typically, X represents the true distribution of the data, and Y represents the theoretical distribution of the data, the simulated distribution, or the approximate distribution of X. The relative entropy has non-negativity (that is, D(X||Y)) and asymmetry (that is, D(X||Y) ≠ D(X||Y) [33,34].

It is not difficult to prove that when the discrete probability distributions of X and Y are exactly the same, the relative entropy of X is smaller than that of Y. The smaller the relative entropy is, the greater the similarity between X and Y is, so we can use the relative entropy to measure the similarity between X and Y.

3. Construction of Evaluation Attributes of Accounting Information Quality

The evaluation attributes are constructed from the content of the accounting information and the environment in which the accounting information is generated, which is shown in Table 1.

3.1. Evaluation Attributes of Accounting Information Content

3.1.1. Reliability

Reliability is the basic quality characteristic of accounting information. It is the foundation and core requirement of accounting information quality characteristics. Reliability refers to the information provided by the company that stakeholders can trust [35]. Accounting information with reliability characteristics needs to meet the following conditions:

Firstly, it reflects all the content that it intends to reflect or should reflect correctly, presents an impartial economic result, and the content can be verified.

Secondly, it reflects the entire content to be reflected or should reflect correctly, present economic results impartially, and be able to withstand verification. It can be extracted from the reliability that the main factors affecting the reliability are no error, integrity, neutrality, verifiability, and prudence.

(1) No error

The existence of errors in accounting information means that it does not reflect the truth. No error states that the company’s accounting information should be consistent with the situation or phenomenon it is expressing, and if the information does not meet the requirements of no error, reliability cannot be guaranteed [36].

(2) Integrity

For accounting information to be reliable, the information must be complete and comprehensive under the principle of importance and cost-benefit. The omission of information can lead to decision-making errors [37], and the deliberate omission of information means concealment and fraud [38].

(3) Neutrality

The description of neutrality in SFAC (Statements of Financial Accounting Concepts) No. 2 is that accounting information is compiled and reported in a way that is not biased towards the intended aim [35]. Neutrality requires an objective reflection of the facts and all information should be communicated in an unbiased manner, meaning that investors’ decisions and actions cannot be deliberately affected. For accounting information to meet the requirements of reliability, it should first meet the requirements of neutrality.

(4) Verifiability

Verifiability means that independent accounting information users with similar capabilities can use the same method to achieve the same result. Verifiability is the ability to replicate reproduction. In order to convince the users that the accounting information is no error and unbiased, the information should be verifiable [39]. Users of independent accounting information with different knowledge should obtain the same or similar results with the same information, so that information users can believe that the information is a reliable reflection of the economic facts [40].

(5) Prudence

The principle of prudence, also known as the principle of robustness, states that when the economic business has different accounting methods and procedures, the methods and procedures that minimize the impact on stakeholders should be selected [41]. It also means reasonably estimating possible losses and expenses. Prudence is the prudent attitude of making estimates and judgments under uncertain conditions [40].

3.1.2. Correlation

The key to whether accounting information is useful to users is whether accounting information is relevant to decision-making and whether it helps to improve decision-making. Relatively significant accounting information can help decision-makers to judge past decision-making, and correct or confirm past forecasts, which has a confirmatory value (determination value). Furthermore, accounting information with the relevant characteristics should also have predictive value and help users to predict future financial status, operating results, and cash flows of the company. At the same time, lagging information to the user’s decision-making value will be greatly reduced or will even lose value; only timely information is relevant information. Therefore, the factors that affect the correlation include the determination value, predictive value, and betimes [42].

(1) Confirmatory value

When the information can confirm or correct the past assessment or judgment, it can be concluded that the information has a certain value [43]. Confirmatory value means that the accounting information can correct or confirm the previous forecast. Therefore, the accounting information with confirmatory value allows decision-makers to assess the current financial situation and the results of the assessment can be used as a reference when making the same decision in the future.

(2) Predictive value

Accounting information can help the user to predict the outcome of past, present, and future events, and obtain the ability to make a difference in decision making [43]. Predictive value states that accounting information, as useful input information, can help decision makers to predict cash flow or profitability, rather than accounting information itself as a practical forecast. There is a mutually reinforcing relationship between confirmatory value and predictive value. If you know the outcome of an event, it will help to improve the accuracy of decision-makers in predicting similar future events. Without understanding the past, predictions will lose their premise; if they do not care about the future, understanding the past will be meaningless [44].

(3) Betimes

Information is valuable when it is available to decision makers before losing the ability to influence decision-making [45]. The quality requirements of betimes mainly include the timely collection of accounting information of the economic operations, the processing of accounting information within the prescribed time limit, the timely preparation of financial reports, and the timely transmission of accounting information. Sometimes increasing the correlation of information by increasing betimes can compromise the quality of information reliability [45].

3.1.3. Constraints

(1) Importance

SFAC No. 2 regards importance as one of the constraints of accounting information quality characteristics [45]. The simplest way to judge the importance of information is to ask whether the presence or absence of the accounting information affects the investors’ decision-making. The reason for importance as a constraint is that importance is associated with all other quality characteristics [46]. This information is important if the underreporting and misreporting of particular information can influence the decision made by the information users based on the financial information. Importance depends not only on the size of the amount of the information but also on the nature of the information. The importance level is different for different accounting subjects [47].

(2) Cost-benefit principle

The provision of accounting information states that in the production of benefits there will also be a certain cost at the same time. The principle of cost-effectiveness is a general principle in economic activities [48]. Moreover, economic activities only take place when the benefits are greater than the costs incurred. However, in some cases, some accounting information quality characteristics have to be sacrificed in order to reduce costs [49].

3.1.4. Third Party Opinion

(1) Type of audit opinion

Taking into account the audit opinion issued by certified public accountants, they can be seen as a diagnosis of the published company financial information, and the third party audit opinion can be the comprehensive attributes for evaluation of the accounting information content quality [50].

(2) Illegal record

At the same time, when illegal behavior appears in the company, government departments as regulators will exercise their duties and levy appropriate punishment to the company. The illegal announcement released by the government can also be used as an evaluation standard of the accounting information content quality [51].

3.2. Evaluation Attributes of Accounting Information Environment

The formation and disclosure of accounting information is just like the manufacturing of products. Many factors affect the quality of accounting information. Generally, the accounting information generation environment includes the internal environment and the external environment. Internal environments include corporate governance and internal control, and external environments include the third-party audit environment and the regulatory environment.

3.2.1. Internal Environment

The internal environment ensures the normal operation of companies, and the internal conditions achieve the objectives and the sum of the internal atmosphere. As the main influence factor of the accounting information generation environment, the internal environment should focus on two aspects of internal control and corporate governance.

(1) Internal control

The Committee of Sponsoring Organizations of the Treadway Commission defines internal controls as procedures that are implemented by the board of directors, managers, and others of the company to provide reasonable assurance as to: the efficiency and effectiveness of operations, the reliability of financial reporting, and compliance with applicable laws and regulations [52]. Internal control includes five elements: control environment, risk assessment, control activities, information, and communication and supervision. Because the internal control can ensure the reliability of financial reporting, internal control helps to guarantee that companies provide high-quality accounting information.

(2) Corporate governance

Corporate governance has three basic characteristics. Firstly, corporate governance is the institutional arrangement that regulates the owners, the board of directors, and the management. Secondly, corporate governance is a system of internal and external checks and balances to ensure accountability of all of its stakeholders and to carry out business activities in various regions in a socially responsible way. Thirdly, the purpose of corporate governance is to help all employees and to implement procedures and activities to ensure that the company’s assets are properly managed. Scientific corporate governance institutions and good governance environment is conducive to company staff performing their duties and forming a good corporate culture [53].

3.2.2. External Environment

A good company external environment can urge the company to continuously improve the quality of accounting information. The external environments of accounting information are mainly the external audit environment and external supervision environment.

(1) External audit environment

Independence is the soul of external auditing. Auditing reports issued by qualified external auditors can provide stakeholders with a reasonable assurance about the quality of the company accounting information. The focus of the external audit environment is the qualifications of the auditors, the audit staff’s professional quality and ethics, the rotation of the firm on a regular basis, and the quality control level of the firm [54].

(2) External supervision environment

External supervision is mainly based on national laws and regulations for public officials to assess the behavior of companies. The external supervision mainly investigates the performance of the duties of government departments and trade associations.

4. Method to Deal with the Linguistic Evaluation Information Based on Relative Entropy in the Fuzzy Linguistic Environment

Let be the set of evaluators, and be the attribute set in the th level. Suppose that , are the values which take the form of the granularity linguistic variable used to calculate the weight of evaluators and the weight of attributes respectively, given by the evaluators ,with respect to the attribute in the th level .

The procedures are given as follows:

(1) Uniform multi-granularity linguistic information

Step 1. The linguistic evaluation set with different granularity is transformed into the basic linguistic evaluation set , where is the granularity of the basic linguistic evaluation set.

(2) Determine the Weight of Evaluators

Step 2. Standardize the evaluation values provided by the evaluator. Let be the standardized data, which take the form of granularity linguistic variables, given by the evaluators , with respect to the attribute in the -th level .

Step 3. Compute the relative entropy of the evaluator relative to all other evaluators, with respect to the attribute in the th level , by the equation:

Step 4. Compute the relative similarity of evaluator in relation to the attribute in the -th level . Because the smaller the relative entropy is, the greater the similarity is, the similarity degree can be obtained by the following equation:

Step 5. According to the authority of the individual evaluator and the relative similarity of individual evaluators in the group, we can obtain the comprehensive weight of an individual evaluator in relation to the attribute in the -th level . Calculate the comprehensive weight of individual evaluators for the attributes by the following equation:

Let and be the important coefficient of the individual evaluator opinion and the important coefficient of the similarity of the evaluator group opinion, respectively, and be the importance of the individual evaluator opinion.

- (a)

- If , it means that the individual evaluator opinion is more important;

- (b)

- If , it means that the similarity of the evaluator group opinion is more important;

- (c)

- If , it means that the individual evaluator opinion is as important as the similarity of the evaluator group opinion.

The values of , , and are determined by decision makers. For the convenience of discussion, this paper sets and .

(3) Determine the Weight of Attributes

Step 6. The linguistic evaluation set with different granularity is transformed into the basic linguistic evaluation set , where is the granularity of the basic linguistic evaluation set.

Step 7. Standardize the data which is used to calculate the importance of attributes. Suppose that is the standardized data, which take the form of the granularity linguistic variable, given by the evaluators , with respect to the attribute in the -th level .

Step 8. Compute the relative entropy of the evaluator relative to all other evaluators, with respect to the attribute in the -th level , by the equation:

Step 9. Compute the relative similarity of evaluator in relation to the attribute in the -th level .

Step 10. Calculate the comprehensive weight of the attributes of the individual evaluator in relation to the attribute in the -th level , according to the information of attribute weight by the decision makers and the relative similarity of attributes in the group.

Likewise, let = = 0.5 and .

(4) Determine the Final Evaluation Results

Step 11. Calculate the evaluation value and the results of the attributes’ importance in the n-th level

Step 12. Aggregate the evaluation value and the attribute importance result of the n-th level to the (n − 1)-th level

This step is repeated until the evaluation result of the first level is obtained.

5. Application of the Accounting Information Quality Evaluation

Consider an automobile manufacturing company. The production covers light truck, medium truck, heavy truck, light bus, and medium-sized passenger cars, and a full range of commercial vehicles and the core components of the engine. It is trans-regional, cross-sector, cross-ownership, and a state-controlled listed company.

Considering job level, gender, and age quality, 30 financial workers are invited in the study and give their opinions with respect to the evaluation attributes.

5.1. Calculate the Evaluation Results

The following is the application of the method of multi-granularity two-tuple semantic information evaluation based on relative entropy according to the results of the survey of 30 questionnaires, to evaluate the quality of accounting information of case company:

Step 1. Uniform multi-granularity linguistic information.

The information used to calculate the weight of the evaluators is multi-granularity data and includes 3 granularity sets, 5 granularity sets, and 9 granularity sets:

- (1)

- : (poor), : (medium), : (good);

- (2)

- : (poorer), : (poor), : (medium), : (good), : (better);

- (3)

- : (awful), : (poorest), : (poorer), : (poor), : (medium), : (good), : (better), : (best), : (excellent).

The 9 granularity set is used as the basic linguistic term set. The results of the conversion of the granularity are shown in Table 2 by Equations (2), (4), (6), and (9):

For a better understanding, a simple example is given below. The evaluation value of the predictive value , which is an attribute belonging to the system of accounting information quality evaluation attributes, is (medium). The process of transforming it into the 9-granularity basic linguistic term set is as follows by Equations (2), (4), (6), and (9).

It is not difficult to determine that and = 1 by Equations (2) and (6).

Step 2. Determine the evaluation value in the third level. Standardize the evaluation values using Equation (12), compute the relative entropy using Equation (13), compute the relative similarity using Equation (14), compute the comprehensive weight of the individual evaluator using Equation (15), and obtain the evaluation value in the third level using Equation (21). The results are shown in Table 3.

Step 3. Determine the results of the attributes’ importance in the th level. Standardize the evaluation values using Equation (17), compute the relative entropy using Equation (18), compute the relative similarity using Equation (19), compute the comprehensive weight of the individual evaluator using Equation (20), and obtain the evaluation value in the third level by Equation (22). The results are shown in Table 3.

Step 4. According to the evaluation result of the third level from Steps 2 and 3, aggregate the evaluation value and the attributes’ importance results in the third level to the second level using Equations (23) and (24).

Step 5. Similar to step 4, aggregate the evaluation value and the attributes’ importance results in the second level to the first level according to the data from Table 3.

Step 6. Obtain the final evaluation result according to the data from Table 4 and Equation (23): (L7, −0.50).

5.2. Analyze the Evaluation Results

(1) Analyze the Importance Degree of Attributes

Analyze the degree of importance of the attributes according to Table 4. Comparing the accounting information content with the environment of information generation, the importance of the accounting information content quality is higher than that of the information generating environment, but the difference is not significant, which indicates that more and more financial officers are already aware of the importance of the environment for information quality.

The ranking of the importance degree of attributes in the second level is third party opinion, reliability, correlation, and constraints. Third party opinion ranked first because it is made up of the type of audit opinion and compliance, which are the prerequisites for a company to ensure the quality of financial information and are also the minimum requirements for the stakeholders. From the constraints in the last one, we can predict that the implementation of the cost-effectiveness principle is not in place and the awareness of financial officers is failing.

(2) Analyze the Evaluation Results of the Case Company

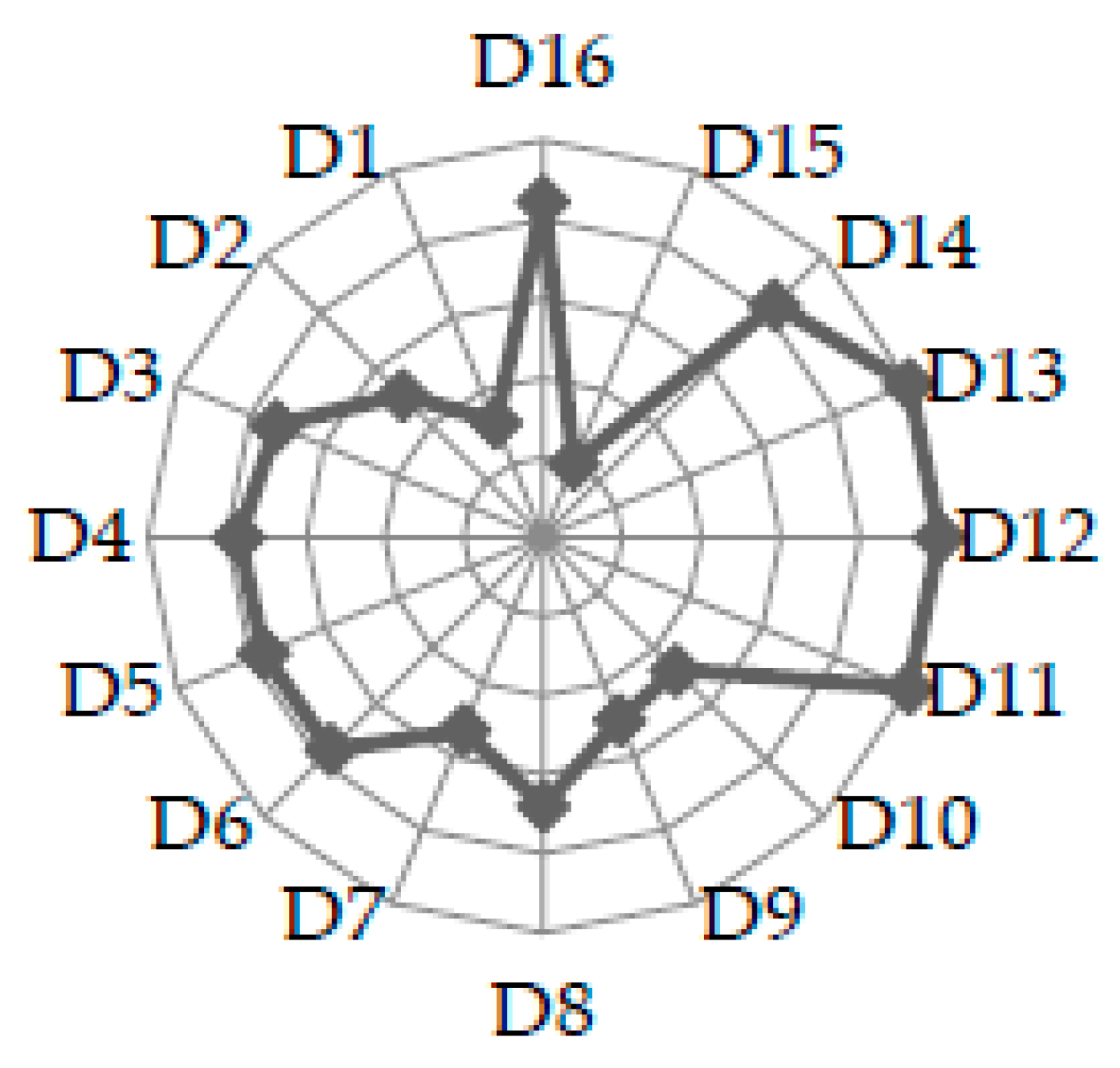

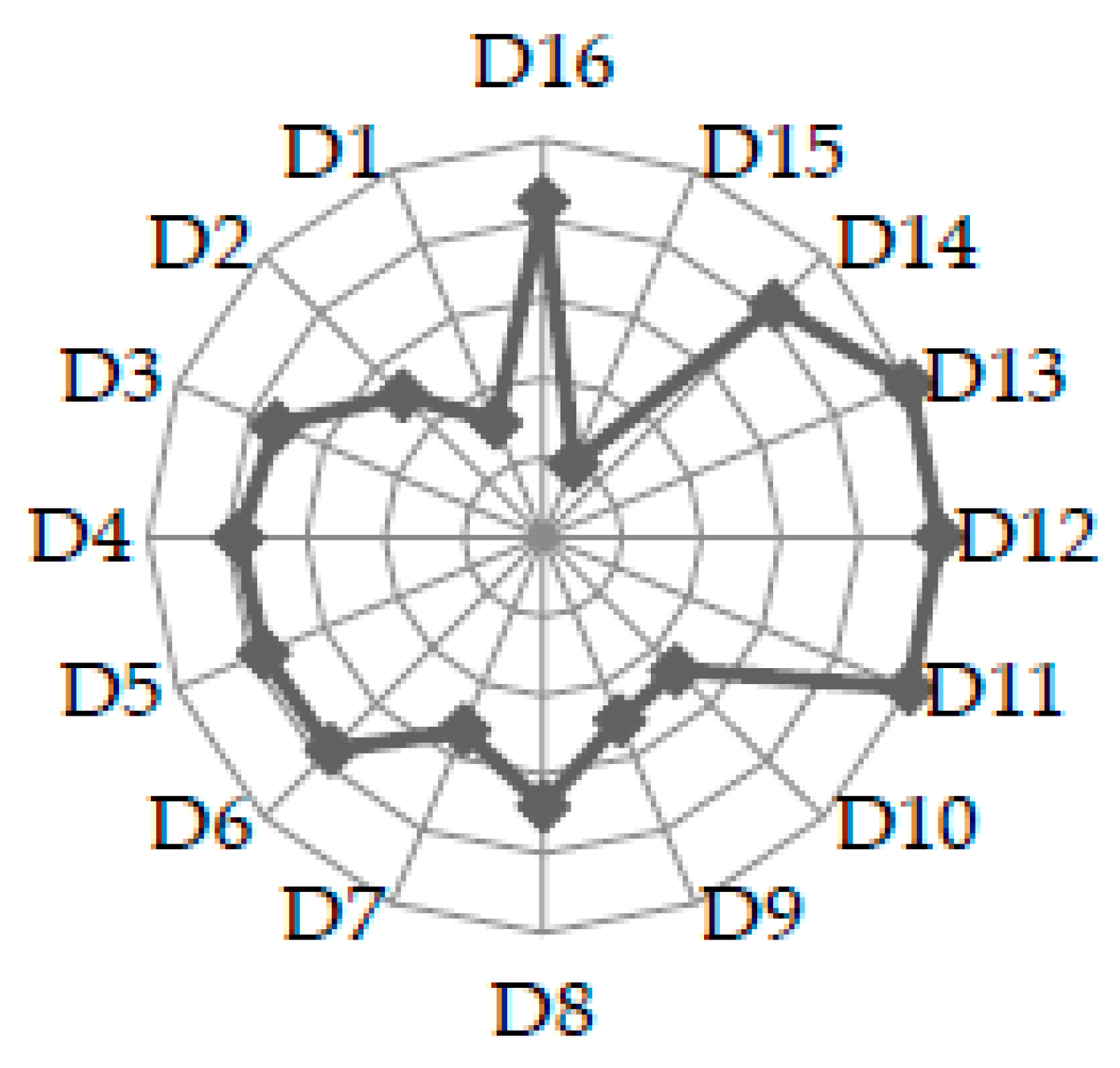

First, we analyze the third-level attributes’ evaluation value. Figure 1 is a radar chart of the evaluation value in the third level, according to Table 3.

Figure 1 shows that the evaluation value of the external auditor and the predictive value are the lowest, which indirectly verifies the results of the analysis of the importance of attributes. The financial officers think that the predictive value is not important subconsciously, leading to case company accounting information that has little effect on stakeholder prediction. At the same time, we can also see that the third party audit agency hired by the case company does not have a very good practicing quality and qualification level. The evaluation value of the audit opinion type, compliance, and internal control are the highest, because these data are the premise of a company ensuring the quality of financial information and are the stakeholders’ minimum requirements for companies. Therefore, the vast majority of companies should reach this level. Moreover, the evaluation value of the confirmatory value, verifiability, importance, and cost-benefit principle is lower, which should cause concern for the financial managers in the case company.

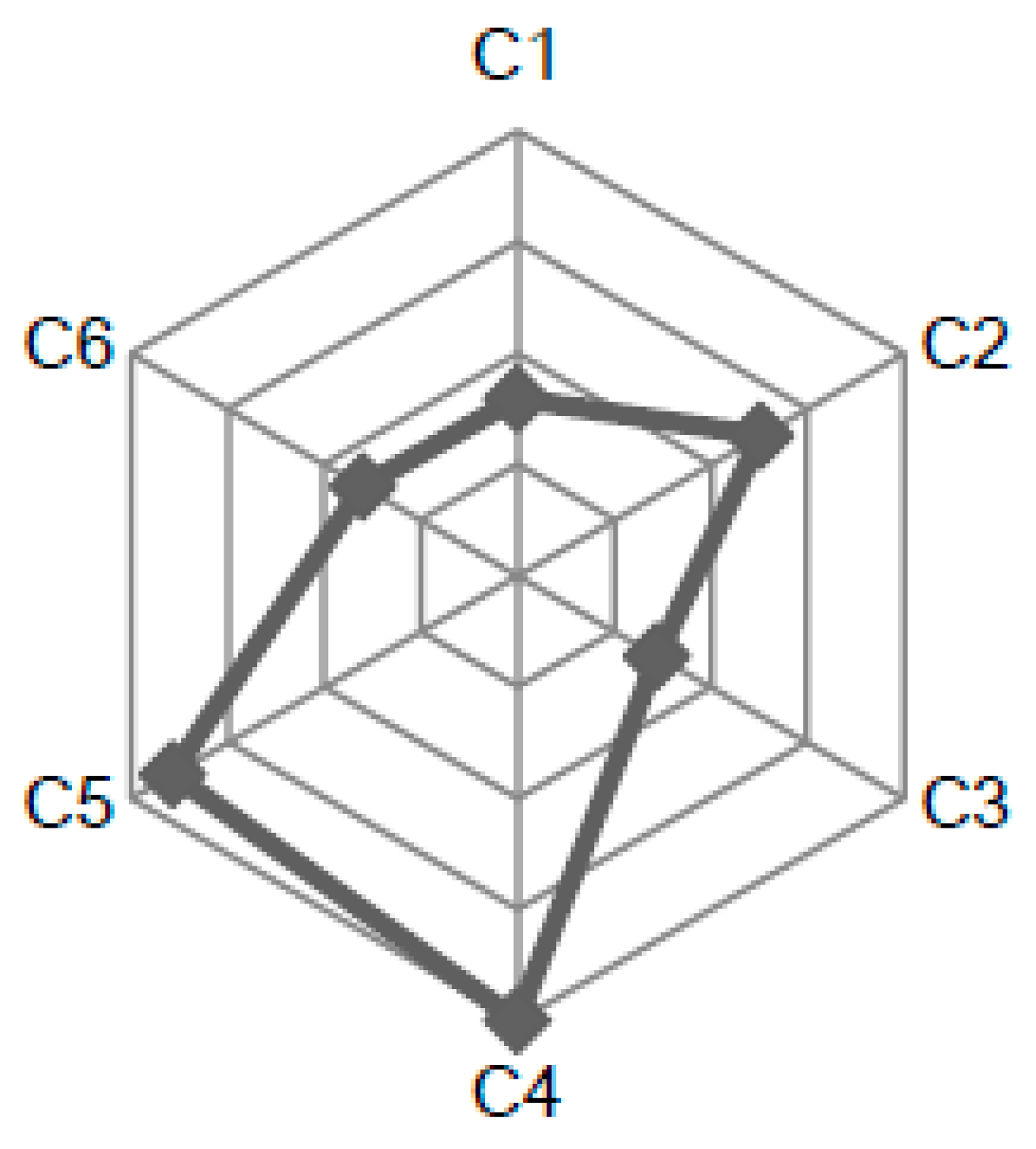

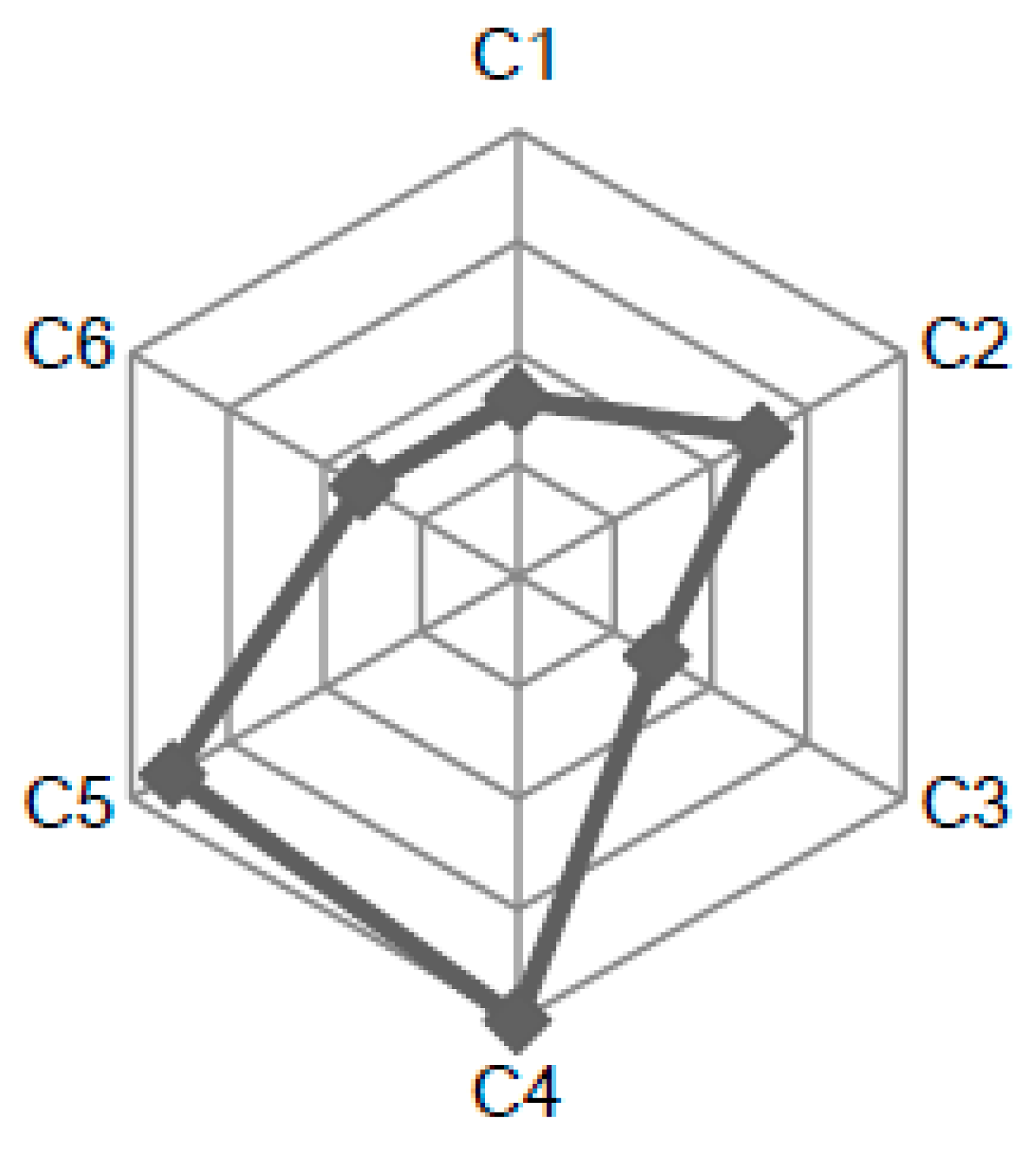

Second, we analyze the second-level attributes’ evaluation value. Figure 2 is a radar chart of the evaluation value in the second level based on Table 3. Figure 2 shows that the evaluation of the accounting information quality in the case company has a higher score in the internal environment and third party opinion, which is to the company’s advantage, and should continue to be maintained. However, we should also pay attention to the problems in correlation, external environment, and constraints, because the company officers do not pay enough attention to them. Additionally, the third party audit institution is weak. Also, the employees do not form awareness of cost saving.

(3) Suggestion

Regarding suggestions to the case company, first of all, due to the lower evaluation value of constraints in the second level, it is recommended that the company distinguish between important information and unimportant information to raise awareness of cost control.

Secondly, improve the correlation of the accounting information quality, especially to improve the predictive value and confirmatory value of the accounting information. Finally, hire a strong, reputable accounting firm to help the company improve the quality of accounting information. At the same time, the company should continue to improve the professional competence of financial officers and strengthen internal oversight.

Regarding suggestions about the external environment, first, the third party audit institutions should constantly improve their professional quality, improve professional competence, maintain independence, and strengthen audit quality control. Second, the government regulatory departments should conscientiously perform their duties of supervision, reduce illegal acts of companies, improve the comparability of financial information between companies, and purify the capital market.

6. Conclusions

The quality of accounting information is important for company stakeholders to make decisions. In this paper, the quality evaluation of accounting information is studied. Firstly, the comprehensive evaluation criteria for the quality of accounting information is constructed. The accounting information generation environment involves corporate governance, internal control, and the external regulatory environment. The influence of the environment on accounting information is extensive and complex. Therefore, besides the accounting information contents, the accounting information generation environment in the construction of the accounting information quality evaluation criteria must be considered. In the proposed method, which is used to deal with linguistic evaluation information with multi-granularities, the 2-tuple model is used to represent the linguistic terms. It is more precise for processing linguistic evaluation information without the loss of information. The relative entropy is used to calculate the consensus of opinions, which is used to obtain the weights of the criteria and experts. The illustrated example shows that the proposed approach is feasible and is fit for the evaluation of the quality of accounting information.

Acknowledgments

The research is supported by the National Natural Science Foundation of China under Grant No. 71101153, 71571191, 71301152, 91646122, Humanity and Social Science Youth Foundation of Ministry of Education in China (Project No. 15YJCZH081, 13YJC790112) and Science Foundation of China University of Petroleum, Beijing (No. 2462015YQ0722), National Key Research and Development Plan under Grant No. 2016YFF0202604.

Author Contributions

Ming Li and Xiaoli Ning conceived and designed the study; Mingzhu Li, Xiaoli Ning, Yingcheng Xu and Ming Li wrote the paper. All authors have read and approved the final manuscript.

Conflicts of Interest

The authors declare no conflict of interest.

References

- Sun, G.G.; Yang, J.F.; Zheng, W.J. Financial Report Quality Assessment: Theoretical Framework, Key Concepts and Operational Mechanism. Account. Res. 2013, 3, 27–35. [Google Scholar]

- Xu, H.; Xiao, N.; Cai, M.R. The Quality of Accounting Information in Evaluation Index System. Res. Econ. Manag. 2012, 11, 122–128. [Google Scholar]

- Wu, M.T.; Liu, Y.; Shi, Y. Ealuation of Enterprises’ Accounting Information Quality based on Projection Pursuit Model. J. Liaoning Technol. Univ. 2012, 4, 383–385. [Google Scholar]

- Zheng, R.Z.; Lin, Z.A. On the Construction of Accounting Information Quality Evaluation Index System—Based on Government Supervision. Commun. Financ. Account. 2008, 8, 26–27. [Google Scholar]

- Bai, P. A Study on the Measurement System of the Accounting Information Quality in the Perspective of Investor Protection. Ph.D. Thesis, Huazhong University of Science and Technology, Wuhan, China, 2012. [Google Scholar]

- Wang, X.J.; Wan, Y.H. The Construction of Enterprise Accounting Information Quality Evaluation Index System under Large Data—Based on Fuzzy Comprehensive Evaluation Method. Financ. Account. Mon. 2015, 14, 74–77. [Google Scholar]

- Li, L.Q.; Shi, P. The Index System of the Enterprise’s Accounting Information Quantity and It’s Comprehensive Evaluation. J. Taiyuan Univ. Technol. 2005, 3, 52–56. [Google Scholar]

- Zang, X.Q.; Zhang, X.X. Research on Fuzzy Comprehensive Evaluation of Accounting Information Quality of Listed Companies. Stat. Decis. 2008, 23, 173–175. [Google Scholar]

- Chen, S.M. Aggregating Fuzzy Opinions in the Group Decision-making Environment. Cybern. Syst. 1998, 29, 363–376. [Google Scholar] [CrossRef]

- Chen, X.; Yang, X. Multiple Attributive Group Decision Making Method based on Triangular Fuzzy Numbers. Syst. Eng. Electron. 2008, 30, 278–282. [Google Scholar]

- Herrera, F.; Martínez, L. A 2-tuple fuzzy linguistic representation model for computing with words. IEEE Trans. Fuzzy Syst. 2000, 8, 746–752. [Google Scholar]

- Liu, Y. Method for 2-tuple Linguistic Dynamic Multiple Attribute Decision Making with Entropy Weight. J. Intell. Fuzzy Syst. 2014, 27, 1803–1810. [Google Scholar]

- Yong-Jie, X.; Chen, X. Model for Evaluating the Virtual Enterprise’s Risk with 2-tuple Linguistic Information. J. Intell. Fuzzy Syst. 2016, 31, 193–200. [Google Scholar]

- Xiong, S.H.; Chen, Z.S.; Li, Y.L. On Extending Power-Geometric Operators to Interval-Valued Hesitant Fuzzy Sets and Their Applications to Group Decision Making. Int. J. Inf. Technol. Decis. Mak. 2016, 15, 1055–1114. [Google Scholar] [CrossRef]

- Edmundas, K.Z.; Valentinas, P. Integrated Determination of Objective Criteria Weights in MCDM. Int. J. Inf. Technol. Decis. Mak. 2016, 15, 267–283. [Google Scholar]

- Dutta, B.; Guha, D. Partitioned Bonferroni Mean based on Linguistic 2-tuple for Dealing with Multi-attribute Group Decision Making. Appl. Soft Comput. 2015, 37, 166–179. [Google Scholar] [CrossRef]

- Estrella, F.J.; Espinilla, M.; Herrera, F. Flintstones: A fuzzy linguistic decision tools enhancement suite based on the 2-tuple linguistic Model and Extensions. Inf. Sci. 2014, 280, 152–170. [Google Scholar] [CrossRef]

- Tan, M.; Shi, Y.; Yang, J.C. Decision Making Method of Multi-Granularity Uncertain Language Group Based on Similarity. Comput. Sci. 2016, 3, 262–265. [Google Scholar]

- Zhang, Z.; Guo, C.H. A Multi-granularity Uncertain Linguistic Group Decision-making Method based on Relative Entropy. Dalian Univ. Technol. 2012, 6, 921–927. [Google Scholar]

- Xu, Z.; Wang, H. Managing Multi-granularity Linguistic Information in Qualitative Group Decision Making: An Overview. Granul. Comput. 2016, 1, 21–35. [Google Scholar] [CrossRef]

- Morente-Molinera, J.A.; Pérez, I.J.; Ureña, M.R. On Multi-granular Fuzzy Linguistic Modeling in Group Decision Making Problems: A Systematic Review and Future Trends. Knowl.-Based Syst. 2015, 74, 49–60. [Google Scholar] [CrossRef]

- Li, M.; Jin, L.; Wang, J.; Ding, D.; Liu, O.; Li, M. A new MCDM method combining QFD with TOPSIS for knowledge management system selection from the user’s perspective in intuitionistic fuzzy environment. Appl. Soft Comput. 2014, 21, 28–37. [Google Scholar] [CrossRef]

- Herrera, F.; Martínez, L. An Approach for Combining Linguistic and Numerical Information based on 2-tuple Fuzzy Linguistic Representation Model in Decision-making. Int. J. Uncertain. Fuzziness Knowl.-Based Syst. 2000, 8, 539–562. [Google Scholar] [CrossRef]

- Herrera, F.; Martínez, L.; Sanchez, P.J. Managing Non-homogeneous Information in Group Decision Making. Eur. J. Oper. Res. 2005, 166, 115–132. [Google Scholar] [CrossRef]

- Herrera, F.; Martinez, L. A Model based on Linguistic 2-tuples for Dealing with Multi-granularity Hierarchical Linguistic Contexts in Multi-expert Decision-making. IEEE Trans. Syst. Man Cybern. Part B Cybern. 2001, 31, 227–234. [Google Scholar] [CrossRef] [PubMed]

- Zhang, Z.; Guo, C. A Method for Multi-granularity Uncertain Linguistic Group Decision Making with Incomplete Weight Information. Knowl.-Based Syst. 2012, 111–119. [Google Scholar] [CrossRef]

- Jiang, Y.; Fan, Z.; Ma, J. A Method for Group Decision Making with Multi-granularity Linguistic Assessment Information. Inf. Sci. 2008, 178, 1098–1109. [Google Scholar] [CrossRef]

- Clausius, R. Ueber verschiedene für die Anwendung bequeme Formen der Hauptgleichungen der mechanischen Wrmetheorie. Ann. Phys. 1865, 125, 353–400. [Google Scholar] [CrossRef]

- Ellis, R.S. The Theory of Large Deviations: From Boltzmann’s 1877 Calculation to Equilibrium Macrostates in 2D Turbulence. Phys. D Nonlinear Phenom. 1999, 133, 106–136. [Google Scholar] [CrossRef]

- Shannon, C.E. A Mathematical Theory of Communication. Bell Syst. Tech. J. 1948, 27, 379–423. [Google Scholar] [CrossRef]

- Kullback, S.; Leibler, R.A. On Information and Sufficiency. Ann. Math. Stat. 1951, 22, 79–86. [Google Scholar] [CrossRef]

- Zhu, H.; Fu, Z.Z.; Li, Z.M. A New Image Thresholding Method Based on Relative Entropy. In Proceedings of the IEEE 2002 International Conference on Communications, Circuits, Systems and West Sino Expositions, Chengdu, China, 29 June–1 July 2002; pp. 634–638. [Google Scholar]

- Kleeman, R. Measuring Dynamical Prediction Utility Using Relative Entropy. J. Atmos. Sci. 2002, 59, 2057–2072. [Google Scholar] [CrossRef]

- Vedral, V. The Role of Relative Entropy in Quantum Information Theory. Rev. Mod. Phys. 2001, 74, 197–234. [Google Scholar] [CrossRef]

- Financial Accounting Standards Board (FASB). Concepts Statements No. 2, Qualitative Characteristics of Accounting Information; Financial Accounting Standards Board: Norwalk, CT, USA, 1980. [Google Scholar]

- Joyce, E.J.; Libby, R.; Sunder, S. Using the FASB’s Qualitative Characteristics in Accounting Policy Choices. J. Account. Res. 1982, 20, 654–675. [Google Scholar] [CrossRef]

- Accounting Principles Board (APB). Statement No. 4; Accounting Principles Board: Norwalk, CT, USA, 1970; pp. 85–105. [Google Scholar]

- International Accounting Standards Committee (IASC). Framework for the Preparation and Presentation of Financial Statements; International Accounting Standards Committe: London, UK, 1989. [Google Scholar]

- American Institute of Certified Public Accountants (AICPA). Improving Business Reporting—A Customer Focus; American Institute of Certified Public Accountants: Durham, NC, USA, 1994; pp. 20–25. [Google Scholar]

- Accounting Standards Board (ASB). Statement of Principles for Financial Reporting; Accounting Standards Board: London, UK, 1999. [Google Scholar]

- Maltby, J. The Origins of Prudence in Accounting. Crit. Perspect. Account. 2000, 11, 51–70. [Google Scholar] [CrossRef]

- Jonas, G.J.; Blanchet, J. Assessing Quality of Financial Reporting. Account. Horiz. 2008, 14, 353–363. [Google Scholar] [CrossRef]

- Ge, J.S.; Chen, S.D. Study on Assessment of the Quality of Financial Reporting. Account. Res. 2001, 11, 9–18. [Google Scholar]

- Wolk, H.I.; Dodd, J.L.; Rozycki, J.J. Accounting Theory: Conceptual Issues in a Political and Economic Environment. Accountancy 2004, 40, 2515–2522. [Google Scholar]

- Whittred, G.P.; Zimmer, I.R. Timeliness of Financial Reporting and Financial Distress. Account. Rev. 1984, 59, 287–295. [Google Scholar]

- Reed, P. The Trueblood Report: An Analyst’s View. Financ. Anal. J. 2005, 31, 32–41. [Google Scholar]

- International Accounting Standards Board (IASB). The Conceptual Framework for Financial Reporting; International Accounting Standards Board: London, UK, 2010. [Google Scholar]

- Financial Accounting Standards Board (FASB). Preliminary Views: Conceptual Framework for Financial Reporting: Objective of Financial Reporting and Qualitative Characteristics of Decision-Useful Financial Reporting Information; Financial Accounting Standards Board: Norwalk, CT, USA, 2006. [Google Scholar]

- International Accounting Standards Board/ Financial Accounting Standards (IASB/FASB). Exposure Draft (ED). The Objective of Financial Reporting and Qualitative Characteristics and Constraints of Decision-Useful Financial Reporting Information; International Accounting Standards Board: London, UK, 2008. [Google Scholar]

- Karjalainen, J. Audit Quality and Cost of Debt Capital for Private Firms: Evidence from Finland. Int. J. Audit. 2011, 15, 88–108. [Google Scholar] [CrossRef]

- Francis, J.; Schipper, K. Have Financial Statements Lost Their Relevance. J. Account. Res. 1999, 37, 319–352. [Google Scholar] [CrossRef]

- Committee of Sponsoring Organizations (COSO). Internal Control-Integrated Framework. 2013. Available online: https://www.coso.org/Documents/990025P-Executive-Summary-final-may20.pdf (accessed on 23 March 2017).

- Bhojraj, S.; Sengupta, P. Effect of Corporate Governance on Bond Ratings and Yields: The Role of Institutional Investors and the Outside Directors. J. Bus. 2003, 76, 455–475. [Google Scholar] [CrossRef]

- Chow, C. The Demand for External Auditing: Size, Debt and Ownership Influence. Account. Rev. 1982, 57, 272–291. [Google Scholar]

Figure 1.

Evaluation Value of the Third Level.

Figure 2.

Evaluation Value of the Second Level.

{kind=link}

{kind=link}

Table 1.

The Quality Evaluation Attributes of Accounting Information.

| First Level | Second Level | Third Level | Attributes Description | Type |

|---|---|---|---|---|

| Accounting Information Content Evaluation | Correlation | Predictive value | The information is helpful for investors to predict the possibility that the event will happen or not in the future | Linguistic |

| Confirmatory value | The information can help investors to understand the impact of past management decisions on the company’s current financial situation | Linguistic | ||

| Betimes | Provide information in a timely manner | Linguistic | ||

| Reliability | Integrity | The information shows all the truth, no omission | Linguistic | |

| Neutrality | The information conveys the fact in an unbiased way | Linguistic | ||

| No error | The information is consistent with the facts | Linguistic | ||

| Verifiability | A third party with sufficient knowledge to use the same data can get similar results | Linguistic | ||

| Prudence | Not over-estimating earnings, not underestimating losses | Linguistic | ||

| Constraints | Importance | The existence of the information will affect the investor’s decision-making | Linguistic | |

| Cost-benefit principle | The cost of providing accounting information should not be greater than the benefits it generates | Linguistic | ||

| Third Party Opinion | Type of audit opinion | The type of audit opinion represents the extent to which the certified public accountants guarantee the quality of accounting information of the company | Numeric | |

| Compliance | The government examines the financial reports of the Company in form and content | Numeric | ||

| Information generation environment evaluation | Internal environment | Internal Control | The company has formed a good control environment, established a smooth information channel of communication, and control activities have been implemented and supervision | Numeric |

| Corporate Governance | The company set up a scientific governance institution, the formation of good governance environment and the management layer has played a role | Linguistic | ||

| External environment | External Auditor | The qualifications of the auditors, the quality of the auditors, and the rotation of the accounting firm. | Numeric | |

| External supervision | The soundness of laws and regulations, and the intensity of law enforcement by regulatory agencies | Linguistic |

Table 2.

The transformation of the multi-granularity linguistic term set.

| 3 Granularity Set Transform into 9 Granularity Set | |||||||

| Before transformation | () | () | () | ||||

| After transformation | () | () | () | ||||

| 5 Granularity Set Transform into 9 Granularity Set | |||||||

| Before transformation | () | () | () | () | () | ||

| After transformation | () | () | () | () | () | ||

Table 3.

The second level and third level evaluation results.

| Second Level Attributes | Evaluation Value | Importance of Attributes | Third Level Attributes | Evaluation Value | Importance of Attributes |

|---|---|---|---|---|---|

| Correlation | (, −0.41) | (, −0.46) | Predictive value | (, −0.43) | (, 0.45) |

| Determined value | (, −0.48) | (, −0.38) | |||

| Betimes | (, −0.35) | (, −0.45) | |||

| Reliability | (, −49) | (, −0.44) | Integrity | (, −0.15) | (, −0.18) |

| Neutrality | (, −0.17) | (, 0.36) | |||

| No error | (, −0.20) | (, −0.36) | |||

| Verifiability | (, −0.35) | (, 0.44) | |||

| Prudence | (, 0.39) | (, −0.48) | |||

| Constraints | (, 0.44) | (, −0.47) | Importance | (, −0.49) | (, −0.32) |

| Cost-benefit principle | (, 0.37) | (, 0.38) | |||

| Third Party Opinion | (, 0) | (, −0.26) | Type of audit opinion | (, 0) | (, −0.25) |

| Compliance | (, 0) | (, −0.27) | |||

| Internal environment | (, −0.42) | (, −0.47) | Internal Control | (, 0) | (, −0.42) |

| Corporate Governance | (, 0.14) | (, 0.49) | |||

| External environment | (, −0.40) | (, −0.50) | External Auditor | (, 0) | (, −0.48) |

| External supervision | (, 0.23) | (, 0.48) |

Table 4.

The first level evaluation results.

| First Level Attributes | Evaluation Value | Importance of Attributes |

|---|---|---|

| Information Content Evaluation | (, 0.41) | (, −0.41) |

| Information generation environment | (, −41) | (, −0.48) |

© 2017 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Li, M.; Ning, X.; Li, M.; Xu, Y. An Approach to the Evaluation of the Quality of Accounting Information Based on Relative Entropy in Fuzzy Linguistic Environments. Entropy 2017, 19, 152. https://doi.org/10.3390/e19040152

AMA Style

Li M, Ning X, Li M, Xu Y. An Approach to the Evaluation of the Quality of Accounting Information Based on Relative Entropy in Fuzzy Linguistic Environments. Entropy. 2017; 19(4):152. https://doi.org/10.3390/e19040152

Chicago/Turabian StyleLi, Ming, Xiaoli Ning, Mingzhu Li, and Yingcheng Xu. 2017. "An Approach to the Evaluation of the Quality of Accounting Information Based on Relative Entropy in Fuzzy Linguistic Environments" Entropy 19, no. 4: 152. https://doi.org/10.3390/e19040152

Note that from the first issue of 2016, this journal uses article numbers instead of page numbers. See further details here.