Entropic Data Envelopment Analysis: A Diversification Approach for Portfolio Optimization

,

,

Abstract

:1. Introduction

2. Literature Review

2.1. Data Envelopment Analysis (DEA)

2.2. Portfolio Selection

2.3. Entropy

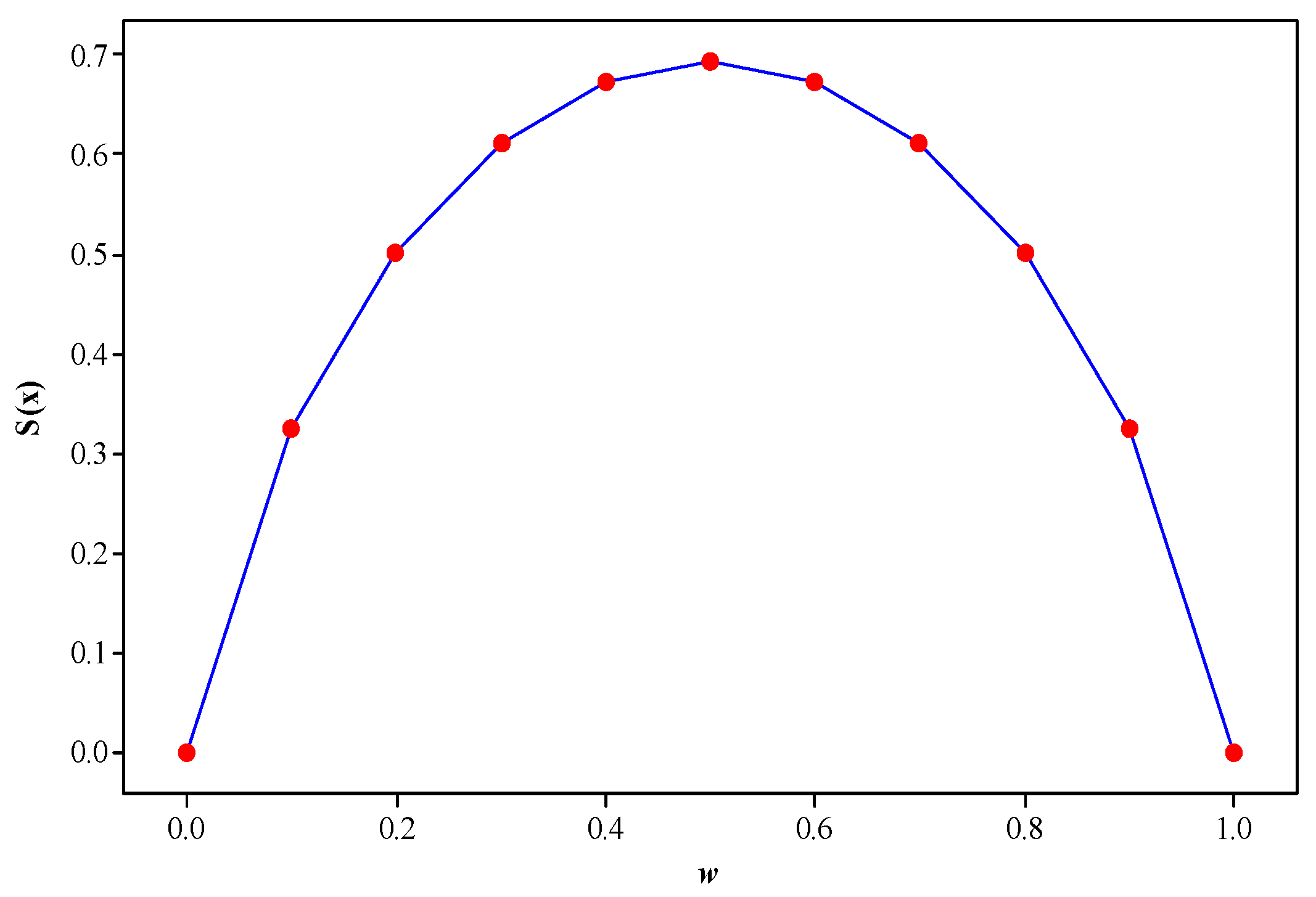

3. Proposed Method

4. Analysis and Results

5. Conclusions

Acknowledgments

Author Contributions

Conflicts of Interest

References

- Zopounidis, C.; Doumpos, M.; Fabozzi, F. Preface to the Special Issue: 60 Years Following Harry Markowitz’s Contributions in Portfolio Theory and Operations Research. Eur. J. Oper. Res. 2014, 234, 343–345. [Google Scholar] [CrossRef]

- Leung, P.L.; Ng, H.Y.; Wong, W.K. An improved estimation to make Markowitz’s portfolio optimization theory users friendly and estimation accurate with application on the US stock market investment. Eur. J. Oper. Res. 2012, 222, 85–95. [Google Scholar] [CrossRef]

- Levy, H.; Levy, M. The benefits of differential variance-based constraints in portfolio optimization. Eur. J. Oper. Res. 2014, 234, 372–381. [Google Scholar] [CrossRef]

- Kolm, P.; Tutuncu, R.; Fabozzi, F. 60 Years of portfolio optimization: Practical challenges and current trends. Eur. J. Oper. Res. 2014, 234, 356–371. [Google Scholar] [CrossRef]

- Markowitz, H. Mean-variance approximations to expected utility. Eur. J. Oper. Res. 2014, 234, 346–355. [Google Scholar] [CrossRef]

- Palczewski, A.; Palczewski, J. Theoretical and empirical estimates of mean–variance portfolio Sensitivity. Eur. J. Oper. Res. 2014, 234, 402–410. [Google Scholar] [CrossRef]

- Yu, J.R.; Lee, W.Y.; Chiou, W.J.P. Diversified portfolios with different entropy measures. Appl. Math. Comput. 2014, 241, 47–63. [Google Scholar] [CrossRef]

- Jobson, J.D.; Korkie, B. Estimation for Markowitz efficient portfolios. J. Am. Stat. Assoc. 1980, 75, 544–554. [Google Scholar] [CrossRef]

- Sheraz, M.; Dedu, S.; Preda, V. Entropy Measures for Assessing Volatile Markets. Procedia Econ. Financ. 2015, 22, 655–662. [Google Scholar] [CrossRef]

- Zhou, R.; Cai, R.; Tong, G. Applications of Entropy in Finance: A Review. Entropy 2013, 15, 4909–4931. [Google Scholar] [CrossRef]

- Abbassi, M.; Ashrafi, M.; Tashnizi, E. Selecting balanced portfolios of R&D projects with interdependencies: A Cross-Entropy based methodology. Technovation 2014, 34, 54–63. [Google Scholar]

- Bhattacharyya, R.; Hossain, S.; Kar, S. Fuzzy cross-entropy, mean, variance, skewness models for portfolio selection. J. King Saud Univ. Comput. Inf. Sci. 2014, 26, 79–87. [Google Scholar] [CrossRef]

- Zhou, R.; Zhan, Y.; Cai, R.; Tong, G. A Mean-Variance Hybrid-Entropy Model for Portfolio Selection with Fuzzy Returns. Entropy 2015, 17, 3319–3331. [Google Scholar] [CrossRef]

- Rodder, W.; Gartner, I.R.; Rudolph, S. An entropy-driven expert system shell applied to portfolio selection. Expert Syst. Appl. 2010, 37, 7509–7520. [Google Scholar] [CrossRef]

- Post, T.; Poti, V. Portfolio Analysis Using Stochastic Dominance, Relative Entropy, and Empirical Likelihood. Manag. Sci. 2017, 63, 153–165. [Google Scholar] [CrossRef]

- Post, T. Empirical Tests for Stochastic Dominance Optimality. Rev. Financ. 2017, 21, 793–810. [Google Scholar]

- Post, T.; Karabati, S. Portfolio Construction Based on Stochastic Dominance and Empirical Likelihood. SSRN 2017, 108, 541–569. [Google Scholar]

- Popkov, A.Y. Entropy model of the investment portfolio. Autom. Remote Control 2006, 67, 1518–1528. [Google Scholar] [CrossRef]

- Emrouznejad, A.; Tavana, M. Peformance Measurement with Fuzzy Data Envelopment Analysis; Springer: Berlin/Heidelberg, Germany, 2014. [Google Scholar]

- Azadi, M.; Jafarian, M.; Saen, R.F.; Mirhedayatian, S.M. A new fuzzy DEA model for evaluation of efficiency and effectiveness of suppliers in sustainable supply chain management context. Comput. Oper. Res. 2015, 54, 274–285. [Google Scholar] [CrossRef]

- Edirishinghe, N.; Zhang, X. Input/output selection in DEA under expert information, with application to financial markets. Eur. J. Oper. Res. 2010, 207, 1669–1678. [Google Scholar] [CrossRef]

- Lim, S.; Oh, K.; Zhu, J. Use of DEA cross-efficiency evaluation in portfolio selection: An application to Korean stock market. Eur. J. Oper. Res. 2014, 236, 361–368. [Google Scholar] [CrossRef]

- Rotela Junior, P.; Pamplona, E.O.; Rocha, L.C.; Valerio, V.E.; Paiva, A.P. Stochastic portfolio optimization using efficiency evaluation. Manag. Decis. 2015, 53, 1698–1713. [Google Scholar] [CrossRef]

- Branda, M.; Kopa, M. DEA models equivalent to general N-th order stochastic dominance efficiency tests. Oper. Res. Lett. 2016, 44, 285–289. [Google Scholar] [CrossRef]

- Rotela Junior, P.; Rocha, L.C.; Aquila, G.; Pamplona, E.O.; Balestrassi, P.P.; Paiva, A.P. Stochastic portfolio optimization using efficiency evaluation. Acta Sci. Technol. 2017, in press. [Google Scholar] [CrossRef]

- Post, T. Empirical Tests for Stochastic Dominance Efficiency. J. Financ. 2003, 58, 1905–1931. [Google Scholar] [CrossRef]

- Post, T.; Kopa, M. General Linear Formulations of Stochastic Dominance Criteria. Eur. J. Oper. Res. 2013, 230, 321–332. [Google Scholar] [CrossRef]

- Sharpe, W.F. A simplified model for portfolio analysis. Manag. Sci. 1963, 9, 277–293. [Google Scholar] [CrossRef]

- Khoveyni, M.; Guo, R.E.; Yang, G.I. Negative data in DEA: Recognizing congestion and specifying the least and the most congested decision making units. Comput. Oper. Res. 2017, 79, 39–48. [Google Scholar] [CrossRef]

- Ferreira, C.M.; Gomes, A.P. Introdução à Análise Envoltória de Dados—Teoria, Modelos e Aplicação; Editora UFV: Viçosa, Brasil, 2009. (In Portuguese) [Google Scholar]

- Charnes, A.; Cooper, W.W.; Rhodes, E. Measuring the efficiency of decision making units. Eur. J. Oper. Res. 1978, 2, 429–444. [Google Scholar] [CrossRef]

- Banker, R.D.; Charnes, A.; Cooper, W.W. Some Models for Estimating Technical and Scale Inefficiencies in Data Envelopment Analysis. Manag. Sci. 1984, 30, 1078–1092. [Google Scholar] [CrossRef]

- Emrouznejad, A.; Yang, G.I. A survey and analysis of the first 40 years of scholarly literature in DEA: 1978–2016. Soc. Econ. Plan. Sci. 2017. [Google Scholar] [CrossRef]

- Lampe, H.; Hilgers, D. Trajectories of efficiency measurement: A bibliometric analysis of DEA and SFA. Eur. J. Oper. Res. 2015, 240, 1–21. [Google Scholar] [CrossRef]

- Emrouznejad, A.; Parker, B.R.; Tavares, G. Evaluation of research in efficiency and productivity: A survey and analysis of the first 30 years of scholarly literature in DEA. Soc. Econ. Plan. Sci. 2008, 42, 151–157. [Google Scholar] [CrossRef]

- Liu, J.S.; Lu, L.Y.Y.; Lu, W.M.; Lin, B.J.Y. A survey of DEA applications. Omega 2013, 41, 893–902. [Google Scholar] [CrossRef]

- Liu, J.S.; Lu, L.Y.Y.; Lu, W.M.; Lin, B.J.Y. Data envelopment analysis 1978–2010: A citation-based literature survey. Omega 2013, 41, 3–15. [Google Scholar] [CrossRef]

- Toloo, M. On finding the most BCC-efficient DMU: A new integrated MIP–DEA model. Appl. Math. Model. 2012, 36, 5515–5520. [Google Scholar] [CrossRef]

- Jablonsky, J. Multicriteria approaches for ranking of efficient units in DEA models. Cent. Eur. J. Oper. Res. 2012, 20, 435–449. [Google Scholar] [CrossRef]

- Ghosh, S.; Yadav, V.K.; Mukherjee, V.; Yadav, P. Evaluation of relative impact of aerosols on photovoltaic cells through combined Shannon’s Entropy and Data Envelopment Analysis (DEA). Renew. Energy 2016, 105, 344–353. [Google Scholar] [CrossRef]

- Falagario, M.; Sciancalepore, F.; Constantino, N.; Pietroforte, R. Using a DEA-cross efficiency approach in public procurement tenders. Eur. J. Oper. Res. 2012, 218, 523–529. [Google Scholar] [CrossRef]

- Jha, D.K.; Shrestha, R. Measuring Efficiency of Hydropower Plants in Nepal Using Data Envelopment Analysis. IEEE Trans. Power Syst. 2006, 21, 1502–1511. [Google Scholar] [CrossRef]

- Markowitz, H. Portfolio selection. J. Financ. 1952, 7, 77–91. [Google Scholar] [CrossRef]

- Frankfurter, G.M.; Phillips, H.E.; Seagle, J.P. Performance of the Sharpe Portfolio selection model: A comparison. J. Financ. Quant. Anal. 1976, 11, 195–204. [Google Scholar] [CrossRef]

- Darolles, S.; Gourieroux, C. Conditionally fitted Sharpe performance with an application to hedge fund rating. J. Bank. Financ. 2010, 34, 578–593. [Google Scholar] [CrossRef]

- Ormos, M.; Zibriczky, D. Entropy-based financial asset pricing. PLoS ONE 2014, 12, e115742. [Google Scholar] [CrossRef] [PubMed]

- Fang, S.C.; Rajasekera, J.R.; Tsao, H.S.J. Entropy Optimization and Mathematical Programming; Kluwer Academic Publishers: Boston, MA, USA, 1997. [Google Scholar]

- Shannon, C.E. A mathematical theory of communication. Bell Syst. Tech. J. 1948, 27, 3–15. [Google Scholar] [CrossRef]

- Rocha, L.C.S.; Paiva, A.P.; Balestrassi, P.P.; Severino, G.; Rotela Junior, P. Entropy-based weighting for multiobjective optimization: An application on vertical turning. Math. Probl. Eng. 2015, 2015, 608325. [Google Scholar] [CrossRef]

- Kim, W.; Kim, J.; Mulvey, J.; Fabozzi, F. Focusing on the worst state for robust investing. Int. Rev. Financ. Anal. 2015, 39, 19–31. [Google Scholar] [CrossRef]

- Sharpe, W.F. Capital Assets Prices: A Theory of Market Equilibrium under Conditions of Risk. J. Financ. 1964, 19, 425–442. [Google Scholar] [CrossRef]

- Sharpe, W.F. The Sharpe Ratio. J. Portf. Manag. 1994, 21, 49–58. [Google Scholar] [CrossRef]

- Homm, U.; Pigorsch, C. Beyond the Sharpe Ratio: An application of the Aumann-Serrano index to performance measurement. J. Bank. Financ. 2012, 36, 2274–2284. [Google Scholar] [CrossRef]

- Auer, B.; Schuhmacher, F. Performance Hypothesis Testing with the Sharpe Ratio: The Case of Hedge Funds. Financ. Res. Lett. 2013, 10, 196–208. [Google Scholar] [CrossRef]

{kind=link}

| DMU | Portfolio 1 | Portfolio 2 | Portfolio 3 |

|---|---|---|---|

| DMU2 | 19.67% | 26.41% | 17.99% |

| DMU5 | - | 0.00% | 3.82% |

| DMU9 | - | 0.00% | 3.64% |

| DMU10 | 10.21% | - | - |

| DMU12 | 0.50% | 5.93% | 9.50% |

| DMU13 | - | 0.00% | 6.26% |

| DMU16 | 47.68% | 56.26% | 31.30% |

| DMU21 | 0.00% | 5.60% | |

| DMU26 | 7.90% | - | - |

| DMU28 | - | 0.00% | 2.31% |

| DMU52 | 0.89% | - | - |

| DMU55 | - | 0.00% | 7.83% |

| DMU57 | - | 11.39% | 11.76% |

| DMU58 | 13.16% | - | - |

| - | Portfolio 1 | Portfolio 2 | Portfolio 3 |

|---|---|---|---|

| Beta | 0.361 | 0.278 | 0.283 |

| Alpha | 1.851 | 1.861 | 1.083 |

| Expected Return | 0.900 | 0.890 | 0.890 |

| Standard deviation | 0.625 | 0.813 | 0.361 |

| Return | 2.751 | 2.751 | 1.973 |

| Sharpe Ratio | 2.978 | 2.289 | 3.002 |

| Number of Assets | 7 | 4 | 10 |

| Accumulated return | 14.08% | 13.36% | 16.97% |

© 2017 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Rotela Junior, P.; Rocha, L.C.S.; Aquila, G.; Balestrassi, P.P.; Peruchi, R.S.; Lacerda, L.S. Entropic Data Envelopment Analysis: A Diversification Approach for Portfolio Optimization. Entropy 2017, 19, 352. https://doi.org/10.3390/e19090352

Rotela Junior P, Rocha LCS, Aquila G, Balestrassi PP, Peruchi RS, Lacerda LS. Entropic Data Envelopment Analysis: A Diversification Approach for Portfolio Optimization. Entropy. 2017; 19(9):352. https://doi.org/10.3390/e19090352

Chicago/Turabian StyleRotela Junior, Paulo, Luiz Célio Souza Rocha, Giancarlo Aquila, Pedro Paulo Balestrassi, Rogério Santana Peruchi, and Liviam Soares Lacerda. 2017. "Entropic Data Envelopment Analysis: A Diversification Approach for Portfolio Optimization" Entropy 19, no. 9: 352. https://doi.org/10.3390/e19090352