To Facilitate or Curb? The Role of Financial Development in China’s Carbon Emissions Reduction Process: A Novel Approach

Abstract

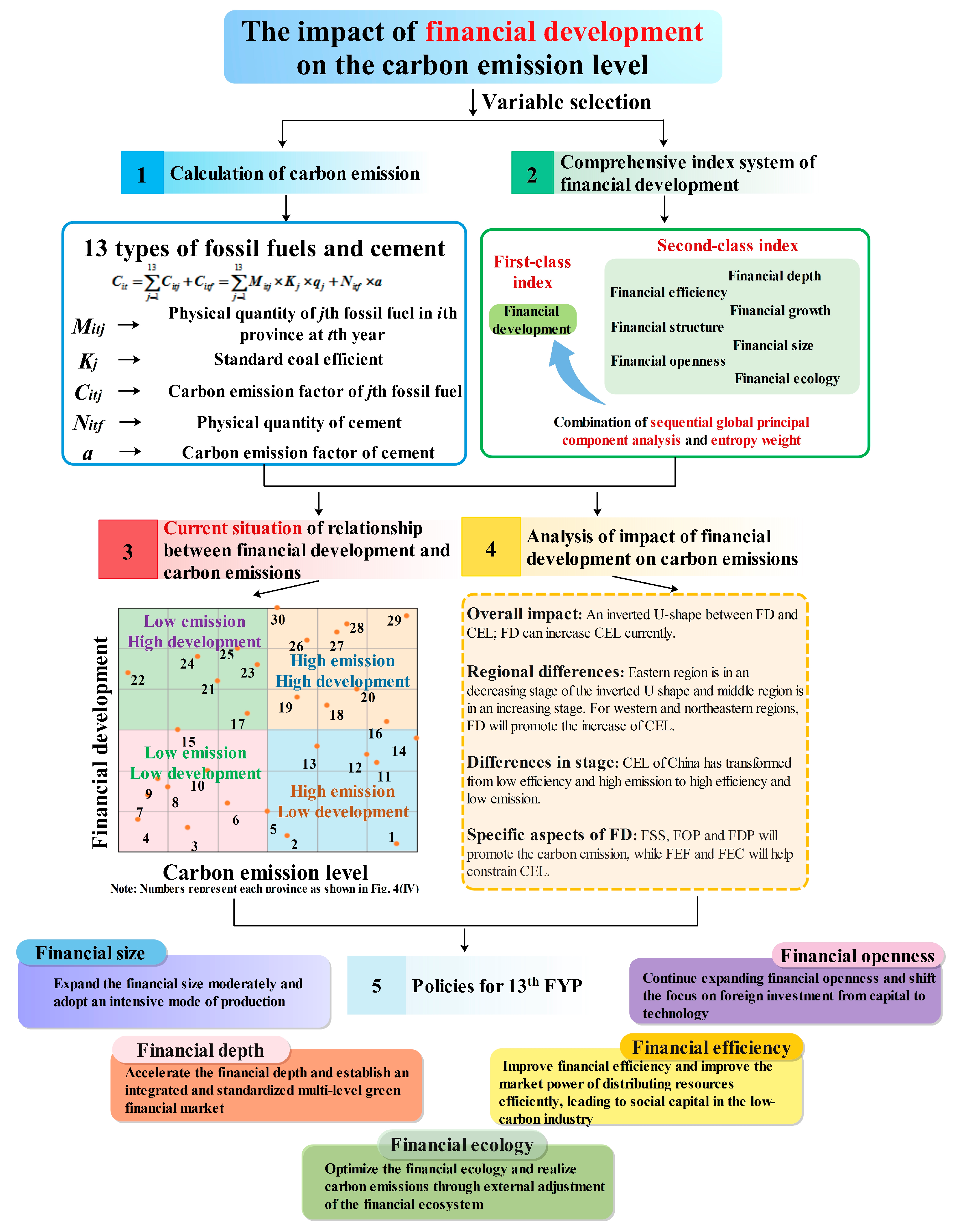

:1. Introduction

- (1)

- With environmental degradation and resource exhaustion, all countries face great pressure regarding carbon emissions. In total, 175 countries have signed the Paris Agreement, which is a positive and solid step towards jointly face one of the most important long-term challenges currently: climate change. As the largest carbon emitter, China’s efforts to reduce carbon emissions can notably contribute to mitigating global warming. Therefore, researching carbon emissions in China is of great significance. Additionally, the influences of many factors on carbon emissions, such as urbanization and population, have been clear. However, there are mixed conclusions on how financial development affects carbon emissions due to different research approaches, selected variables and so on. In fact, with the integration of the global economy and the rapid development of the financial industry, financial development has played an increasingly pivotal role in influencing carbon emissions. Thus, this research has great practical significance.

- (2)

- The approach of this paper in researching the relationship between carbon emissions and financial development is different from previous studies in the following aspects:

- ◆

- When measuring financial development, we creatively establish a comprehensive evaluation index system to represent it instead of a single variable. To the best of our knowledge, it is impossible to fully measure financial development by using only one index, which will have an influence on the reliability of the analysis results. Additionally, giving proper weight to each individual variable in the index system plays a pivotal role in deciding the effectiveness of the system. Therefore, this paper combines a sequential global principal component analysis and the entropy weight method to ensure that the correct weight is used, which can overcome subjectivity and leverage each method fully.

- ◆

- When calculating carbon emissions, this paper considers both the combustion of 13 types of fossil fuels and the production of cement, which can make the calculation of carbon emissions more accurate and comprehensive.

- ◆

- The ARDL approach is applied to investigate the long-run relationship between financial development and carbon emissions, and a dynamic panel error-corrected model is utilized to capture the short-run impact. Before estimation, we test whether each region is independent, after which a cross-section mean group (CMG), pooled mean group (CPMG) and dynamic fixed effect (CDFE) are applied to estimate the parameters in the equation.

- ◆

- The fourth feature of the proposed method is the application of the STIRPAT model. It has been proven to be effective in researching the influencing factors of carbon emissions, and one apparent advantage is that the model can be expanded to include the financial development index, apart from some common factors.

- ◆

- Apart from discussing the overall impact, we also divide China into different regions and stages to explore the regional and stage differences of the impact. Different from the time series data, the panel data can be more representative and effective in researching Chinese carbon emissions. Furthermore, we also discuss the impact of seven specific aspects of the financial development index system on the carbon emissions level.

- (3)

- Our research results not only provide the basis for policy makers in China to control carbon emissions but can also explain the relationship between financial development and carbon emissions in other developing countries in the world, such as India. Currently, financial development can facilitate carbon emissions, indicating that the wealth and scale effects are larger than the technology and structure effects. Moreover, the relationship is different in different regions and stages. With the extensive economic growth mode, financial development can lead to the increase of the carbon emissions level, and financial development will gradually show a tendency to constrain the carbon emissions level as the policies and economic structure change.

2. Literature Review

2.1. Methods to Measure the Influencing Factors of Carbon Emissions

2.2. Financial Development Indexes

2.3. Methods to Research the Relationship between Carbon Emissions and Financial Development

2.4. Nexus between Financial Development and Carbon Emissions

3. Methodology

3.1. Sequential Global Principal Component Analysis (SGPCA)

- Step 1

- Z-score normalization. The first step for processing the original data is to eliminate the dimension of data. The equation iswhere is the original data of the ith index and jth sample. and represent the mean and standard deviation of ith index, respectively.

- Step 2

- According to the normalized data matrix , calculate the correlation coefficient matrix .

- Step 3

- Calculate the eigenvalue and eigenvector of R. The eigenvalue is calculated based on the characteristic equation , which is the eigen-polynomial of . Solve and order , ranging in size:

- Step 4

- Calculate the contribution rate. The equation of the contribution rate and cumulative contribution rate is described in Equations (4) and (5) here:

- Step 5

- Calculate the principal component load matrix, which is the correlation coefficient between the principal component and the variable .

- Step 6

- Scores of the principal component can be obtained with the following equations.

3.2. Entropy Weight Method (EWM)

- Step 1

- Non-negative data processing. Equation (8) demonstrates that entropy is a type of calculation between the individual indicator and its corresponding , which is not related to the calculation between and . Therefore, there are no dimensional differences among the data, but the procedure requires non-negativity. The data processing of the large indicator and small indicator is listed in Equations (8) and (9), respectively:

- Step 2

- The proportion of the jth indicator of the ith scheme is

- Step 3

- The entropy of the jth indicator is:where , ln is the natural logarithm, . The constant k is relative to the sample size m, and in general, and .

- Step 4

- Calculate the difference coefficient of the jth indicator. For the jth indicator, a larger difference of indicator plays a larger role in evaluating the case:

- Step 5

- The entropy weight of the jth indicator is:

3.3. Combination of SGPLA and EWM

3.4. The Expanded STIRPAT Model

3.5. The Pooled Mean Group Estimator

4. Data and Variables

4.1. Calculation of Carbon Emissions in Each Province

4.2. Financial Development Index System (FDIS)

4.3. Other Variables

5. Empirical Results and Discussion

5.1. Current Situations of Carbon Emissions and Financial Development

5.1.1. Current Situations of Carbon Emissions in China

5.1.2. Current Situations of Financial Development in China

5.1.3. Results of the Clustering Analysis

5.2. Impact of Financial Development on Carbon Emissions

5.2.1. The Overall Impact

- (1)

- For the long-term impact, the coefficients of financial development on CEPC are 0.291, which is statistically significant. Additionally, the coefficient of FD2 is negative, which is −0.321, proving the inverted U-shape relationship between financial development and CEPC in China. The results indicate that, at the present stage, the development of finance is at the expense of the environment.

- (2)

- Compared with long-term influence, the short-term coefficient of FD on the CEPC is 0.375. The results show that the short-term influence degree is larger than the long-term impact; therefore, the inhibiting effect of the FD on CEL requires a long time to be realized. This conclusion is valuable because it suggests that policy makers consider the long-term influence when developing policies.

- (3)

- Finally, for the overall impact of other variables, the GDPPC can facilitate CEPC. The industrial structure contributes to CEPC with a coefficient of 0.310. The results fully reflect the characteristics of high output value and low production efficiency during the industrialization process.

5.2.2. The Impact on Different Regions

- (1)

- Eastern region. FD constrains CEL in the long term. That is, if the financial development increases 1%, CEPC decreases 0.374%. Meanwhile, the coefficient of FD2 is both negative and significant, indicating an inverted U-shape relationship between financial development and CEL [97]. Financial development in the eastern region tends to be mature, so it can constrain CEL. GDPPC can cause carbon emissions to increase, leading to a rise of energy consumption and demand. The results of other variables fully prove that the industrial process of the eastern region contains technological advancement and improvements in production efficiency, which are caused by the factor reallocation [19].

- (2)

- Middle region. The impact is statistically significant at the 1% level with positive coefficients of 0.391. The GDPPC increases CEPC with a coefficient of 0.326. The industrial structure has a significant and positive impact on CEL. In the short term, the coefficient is larger, indicating that the middle region needs time to achieve the carbon emissions reduction.

- (3)

- Western region. The long-term coefficient of FD on CEL in western region is negative and significant, but the absolute value, 0.461, is larger than the middle region. Thus, with the improvement of the financial development level, carbon emissions will increase at a greater magnitude than the middle region. The GDPPC can affect the carbon emissions level positively at the 1% level. The western region is in a start-up stage, and the region needs to improve the investment environment, increase openings, attract social capital and participate actively in western development and establishment.

- (4)

- North-eastern region. The influence is positive and significant and exceeds the middle region at a value of 0.698. The influence of other variables is similar to that in the western region. In the short term, the impact of FD on CEPC is 0.429. As a traditional industrial base, the north-eastern region has an extensive economic development pattern. The accumulated deep contradiction is gradually becoming obvious, causing low utilization efficiency in each resource and condition. Financial development proceeds at the cost of environment.

5.2.3. The Impact on Different Stages

- (1)

- During the 10th FYP (2001–2005), stimulated by industrialization, urbanization and internationalization, the Chinese economy achieved rapid expansion, and the industrial structure tended toward high input, energy consumption and pollution. At that time, financial development promoted CEL, and each 1% increase of financial development caused a 0.816% increase in CEPC. Therefore, financial development aggravates the carbon emissions in this stage because of the outdated production capacity, increase of enterprises with high energy consumption, lagging production technology and low production efficiency [18].

- (2)

- The 11th FYP was a transformative period for Chinese carbon emissions with remarkable progression of low-carbon development. The increase of carbon emissions was effectively alleviated, and the increasing tendency of CEL begins to decrease. Therefore, during this time, the economic development mode changes from an investment-led pattern to a science-led pattern. Financial development can promote CEL with a coefficient of 0.569. This confirms that although financial development can still increase carbon emissions, the impact effect greatly decreases. On the other hand, it shows that the strategies of energy conservation and emission reduction are effective and can contribute to low-carbon development.

- (3)

- The 12th FYP is a key stage for China to develop its low-carbon economy. China further adjusted its energy structure, established an energy system, changed the industrial structure, promoted the development of low-carbon industries, and developed low-carbon technology. During this time, FD promoted CEL with a lower impact magnitude, which indicates that the low-carbon development mode accelerated the independent innovation process. The expansion of financing channels, continuous perfection of the carbon trade mechanism and improvement of technological research abilities are beneficial for China in realizing a low-carbon economy.

5.2.4. The Impact of Different Aspects of Financial Development on CEL

6. Conclusions

Author Contributions

Conflicts of Interest

Abbreviations

| CEI | Carbon emission intensity |

| MG | Mean group |

| PMG | Pooled mean group |

| DFE | Dynamic fixed effect |

| FYP | Five-Year Plan |

| IDA | Index decomposing analysis |

| GMM | Generalized method of moment |

| LMDI | Logarithmic Mean Divisia Index |

| FE | Fixed effects |

| FGLS | Feasible generalized least squares |

| DK | Driscoll–Kraay standard errors |

| PCSE | Panel corrected standard errors |

| PLS | Partial least squares |

| SGPCA | Sequential global principal component analysis |

| FDIN | Financial development index |

| FDIS | Financial development index system |

| EWM | Entropy weight method |

| POP | Population |

| FIR | Financial interrelation ratio |

| UR | Urbanization |

| IS | Industrial structure |

| GDP | Gomestic gross products |

| TCE | Total carbon emission |

| CEI | Carbon emission intensity |

| CEPC | Carbon emission per capita |

| FSZ | Financial size |

| FST | Financial structure |

| FOP | Financial openness |

| FDP | Financial depth |

| FGR | Financial growth |

| FEF | Financial efficiency |

| FEC | Financial ecology |

| ARDL | Auto regressive distributed lag model |

| FD | Financial development |

| CEL | Carbon emission level |

| IPCC | Intergovernmental Panel on Climate Change |

| KMO | Kaiser-Meyer-Olkin |

| HE-HD | High emission-high development |

| HE-LD | High emission-low development |

| LE-HD | Low emission-high development |

| LE-LD | Low emission-low development |

| CD | Cross-sectional dependence |

Appendix A

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Time | Name of Policy | Related Contents |

|---|---|---|

| January 2017 | The Comprehensive Working Plan for Energy Conservation and Emission Reduction during the 13th Five Year Plan | Assign total energy consumption and intensity goals for each province (city and district), propose goals for primary industries and clarify the control plan for CO2 total discharge levels in each region. |

| June 2016 | Regulations of Industrial Energy Conservation | Emphasize a transaction system of energy use rights, clarify the management methods for energy saving and build a healthy and sound supervision system. |

| September 2014 | Action Plan for Transformation and Updating of Energy Conservation and Emission Reduction of Coal (2014–2020) | Until 2020, the average coal consumption power supply of newly built coal-fired generating units should be lower than 300 g/kWh. Transformational active units should be lower than 310 g/kWh. |

| April 2014 | Revise Environmental Protection Act | Highlight the cyclical utilization of resources and environmental improvement and protection to coordinate social and economic development and environmental protection. |

| September 2013 | Action Plan for the Control of Air Pollution | Increase the selected ratio of raw coal to 70%. |

| July 2012 | Revise Cleaner Production Promotion Law | Promote cleaner production, improve the utilization efficiency of resources, reduce and prevent pollution, and protect the environment. |

| August 2011 | Comprehensive Working Plan for Energy Conservation and Emissions Reduction during the 12th Five Year Plan | Aim to decrease carbon emissions intensity by 17% in 2015 compared to 2010 within the national economy and social development plan of the 12th Five Year Plan. |

| April 2010 | Revise Renewable Energy Law | Enhance the development and utilization of renewable energy and promote the rapid and orderly development of renewable energy industries. |

| April 2008 | Energy Conservation Law | Promote energy conservation, improve the utilization efficiency of energy and promote comprehensive, harmonious and sustainable development. |

| March 2006 | The 11th Five Year Plan | Aim to decrease energy consumption by 20% |

| August 2002 | Kyoto Protocol | Aim to decrease carbon emissions by 40–45% by 2020 compared to 2005. |

Appendix B

| Component | X1 | X2 | X3 | X4 | X5 | X6 | X7 | X8 | X9 | X10 | X11 |

| Principal component method | 0.0411 | 0.0330 | 0.0383 | 0.0362 | 0.0503 | 0.033 | 0.0682 | 0.072 | 0.0285 | 0.0355 | 0.0221 |

| Entropy weight method | 0.0398 | 0.0243 | 0.0456 | 0.0458 | 0.0494 | 0.0366 | 0.0485 | 0.0486 | 0.0398 | 0.0545 | 0.0486 |

| Average | 0.0405 | 0.0286 | 0.0419 | 0.0410 | 0.0498 | 0.0348 | 0.0583 | 0.0603 | 0.0342 | 0.0450 | 0.0354 |

| Component | X12 | X13 | X14 | X15 | X16 | X17 | X18 | X19 | X20 | X21 | X22 |

| Principal component method | 0.0175 | 0.0321 | 0.0369 | 0.0691 | 0.0696 | 0.0653 | 0.0646 | 0.0245 | 0.0668 | 0.0268 | 0.0684 |

| Entropy weight method | 0.0444 | 0.0481 | 0.0470 | 0.0401 | 0.0485 | 0.0483 | 0.0493 | 0.0483 | 0.0497 | 0.0492 | 0.0457 |

| Average | 0.0309 | 0.0401 | 0.0419 | 0.0546 | 0.0590 | 0.0568 | 0.0569 | 0.0364 | 0.0582 | 0.0380 | 0.0570 |

Appendix C. Cross-Sectional Dependence (CD), Panel Unit Root Test and Panel Cointegration Tests

| Variable | CD-Test | p-Value | Abs(corr) | Variable | CD-Test | p-Value | Abs(corr) |

|---|---|---|---|---|---|---|---|

| CEPC | 63.520 | 0.000 | 0.890 | FST | 52.350 | 0.000 | 0.775 |

| GDPPC | 75.430 | 0.000 | 0.976 | FOP | 53.880 | 0.000 | 0.719 |

| IS | 32.630 | 0.000 | 0.628 | FDP | 37.660 | 0.000 | 0.533 |

| FD | 53.970 | 0.000 | 0.692 | FGR | 48.700 | 0.000 | 0.626 |

| FD2 | 48.400 | 0.000 | 0.627 | FEF | 38.170 | 0.000 | 0.515 |

| FSZ | 75.040 | 0.000 | 0.962 | FEC | 22.210 | 0.000 | 0.361 |

| Variables in Levels | Variables in First Differences | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Constant w/o Trend | Constant w/Trend | Constant w/o Trend | Constant w/Trend | |||||||||

| No. lag | 1 | 2 | 3 | 1 | 2 | 3 | 1 | 2 | 3 | 1 | 2 | 3 |

| CEPC | 0.796 | 0.883 | 0.891 | 0.996 | 0.994 | 0.998 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 |

| GDPPC | 0.574 | 0.629 | 0.735 | 0.965 | 0.978 | 0.993 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 |

| IS | 0.072 | 0.139 | 0.168 | 0.471 | 0.669 | 0.705 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 |

| FD | 0.905 | 0.945 | 0.911 | 0.920 | 0.946 | 0.998 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 |

| FD2 | 0.918 | 0.936 | 0.900 | 0.972 | 0.963 | 0.977 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 |

| FSZ | 0.624 | 0.958 | 0.972 | 0.982 | 0.987 | 1.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 |

| FST | 0.946 | 0.998 | 0.999 | 0.703 | 0.996 | 0.999 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 |

| FOP | 0.874 | 0.889 | 0.903 | 0.641 | 0.993 | 0.817 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 |

| FDP | 0.318 | 0.856 | 0.774 | 0.621 | 1.000 | 0.999 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 |

| FGR | 0.568 | 0.626 | 0.888 | 0.825 | 0.945 | 0.991 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 |

| FEF | 0.838 | 0.851 | 0.998 | 0.617 | 1.000 | 0.995 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 |

| FEC | 0.302 | 0.492 | 0.517 | 0.806 | 0.885 | 0.793 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 |

| CEPC | GDPPC | IS | FD | FD2 | FSZ | FST | FOP | FDP | FGR | FEF | FEC |

|---|---|---|---|---|---|---|---|---|---|---|---|

| Gt | 0.428 (0.006) | 1.955 (0.975) | 6.242 (1.000) | 3.471 (1.000) | 0.601 (0.026) | 2.309 (0.000) | 0.631 (0.736) | 5.404 (0.000) | 6.140 (1.000) | 5.883 (0.000) | 1.208 (0.006) |

| Ga | −3.716 (0.000) | −5.510 (0.000) | −2.657 (0.004) | −6.692 (0.000) | −5.091 (0.000) | −5.468 (0.000) | −5.667 (0.000) | −3.399 (0.000) | −2.307 (0.011) | −3.681 (0.000) | −5.379 (0.000) |

| Pt | 0.815 (0.001) | −0.009 (0.096) | 4.420 (1.000) | 1.874 (0.070) | −0.776 (0.219) | −1.734 (0.042) | −2.589 (0.005) | 1.628 (0.048) | 4.616 (0.000) | 3.517 (0.000) | 0.676 (0.050) |

| Pa | −3.969 (0.000) | −5.407 (0.000) | −0.357 (0.010) | −3.214 (0.001) | −4.499 (0.000) | −7.197 (0.000) | −6.945 (0.000) | −2.991 (0.001) | −0.256 (0.009) | −2.805 (0.003) | −4.555 (0.000) |

Appendix D. Regional Division of China

| Region | Provinces |

|---|---|

| Eastern | Beijing, Tianjin, Hebei, Shanghai, Jiangsu, Zhejiang, Fujian, Shandong, Guangdong and Hainan. |

| Middle | Shanxi, Anhui, Jiangxi, Henan, Hubei and Hunan. |

| Western | Inner Mongolia, Guangxi, Chongqing, Sichuan, Guizhou, Yunnan, Xizang, Shaanxi, Gansu, Qinghai, Ningxia and Xinjiang. |

| Northeastern | Liaoning, Jilin and Heilongjiang. |

References

- Shahbaz, M.; Tiwari, A.K.; Nasir, M. The effects of financial development, economic growth, coal consumption and trade openness on CO2 emissions in South Africa. Energy Policy 2013, 61, 1452–1459. [Google Scholar] [CrossRef] [Green Version]

- Charfeddine, L.; Khediri, K.B. Financial development and environmental quality in UAE: Cointegration with structural breaks. Renew. Sustain. Energy Rev. 2016, 55, 1322–1335. [Google Scholar] [CrossRef]

- Zeng, S.; Liu, Y.; Liu, C.; Nan, X. A review of renewable energy investment in the BRICS countries: History, models, problems and solutions. Renew. Sustain. Energy Rev. 2017, 74, 860–872. [Google Scholar] [CrossRef]

- Wang, Y.; Yang, X.; Sun, M.; Ma, L.; Li, X.; Shi, L. Estimating carbon emissions from the pulp and paper industry: A case study. Appl. Energy 2016, 184, 779–789. [Google Scholar] [CrossRef]

- Carbon Trade, Global Carbon Project Issues the Carbon Emission Amount. Available online: http://www.tanjiaoyi.com/article-3258–1.html (accessed on 5 April 2016).

- CDIAC, Carbon Emission of Top 20 Countries in the World in 2013. Available online: http://cdiac.ornl.gov/trends/emis/top2013.tot (accessed on 5 April 2016).

- Meng, F.; Su, B.; Thomson, E.; Zhou, D.; Zhou, P. Measuring China’s regional energy and carbon emission efficiency with DEA models: A survey. Appl. Energy 2016, 183, 1–21. [Google Scholar] [CrossRef]

- Zeng, S.; Nan, X.; Liu, C.; Chen, J. The response of the Beijing carbon emissions allowance price (BJC) to macroeconomic and energy price indices. Energy Policy 2017, 106, 111–121. [Google Scholar] [CrossRef]

- CDIAC, Carbon Emission of China from 1978 to 2013. Available online: http://cdiac.ornl.gov/CO2_Emission/timeseries/national/China (accessed on 5 April 2016).

- Kim, J.; Park, K. Financial development and deployment of renewable energy technologies. Energy Econ. 2016, 59, 238–250. [Google Scholar] [CrossRef]

- Ziaei, S.M. Effects of financial development indicators on energy consumption and CO2 emission of European, East Asian and Oceania countries. Renew. Sustain. Energy Rev. 2015, 42, 752–759. [Google Scholar] [CrossRef]

- Xiong, L.; Qi, S.Z. Financial development and carbon emission of Chinese provinces: Based on STIRPAT model and dynamic panel data analysis. J. China Univ. Geosci. (Soc. Sci. Ed.) 2016, 16, 63–73. (In Chinese) [Google Scholar]

- Wang, Y.F.; Zhao, H.Y.; Li, L.Y.; Liu, Z.; Liang, S. Carbon dioxide emission drivers for a typical metropolis using input-output structural decomposition analysis. Energy Policy 2013, 58, 312–318. [Google Scholar] [CrossRef]

- Karmellos, M.; Kopidou, D.; Diakoulaki, D. A decomposition analysis of the driving factors of CO2 (carbon dioxide) emissions from the power sector in the European Union countries. Energy 2016, 94, 680–692. [Google Scholar] [CrossRef]

- Shahiduzzaman, M.; Layton, A. Decomposition analysis for assessing the United States 2025 emissions target: How big is the challenge? Renew. Sustain. Energy Rev. 2017, 67, 372–383. [Google Scholar] [CrossRef]

- Yan, Q.Y.; Zhang, Q.; Zou, X. Decomposition analysis of carbon dioxide emissions in China’s regional thermal electricity generation, 2000–2020. Energy 2016, 112, 788–794. [Google Scholar] [CrossRef]

- Li, A.J.; Zhang, A.Z.; Zhou, Y.X.; Yao, X. Decomposition analysis of factors affecting carbon dioxide emissions across provinces in China. J. Clean. Prod. 2017, 141, 1428–1444. [Google Scholar] [CrossRef]

- Zhou, Y.; Liu, Y.S.; Wu, W.X.; Li, Y.R. Effects of rural-urban development transformation on energy consumption and CO2 emissions: A regional analysis in China. Renew. Sustain. Energy Rev. 2015, 52, 863–875. [Google Scholar] [CrossRef]

- Zhang, C.G.; Zhou, X.X. Does foreign direct investment lead to lower CO2 emissions? Evidence from a regional analysis in China. Renew. Sustain. Energy Rev. 2016, 58, 943–951. [Google Scholar] [CrossRef]

- Wang, P.; Wu, W.S.; Zhu, B.Z.; Wei, Y.M. Examining the impact factors of energy-related CO2 emissions using STIRPAT model in Guangdong province, China. Appl. Energy 2013, 106, 65–71. [Google Scholar] [CrossRef]

- Li, H.N.; Mu, H.L.; Zhang, M.; Li, N. Analysis on influence factors of China’s CO2 emissions based on Path-STIRPAT model. Energy Policy 2011, 39, 6906–6911. [Google Scholar] [CrossRef]

- Wang, C.J.; Wang, F.; Zhang, X.L.; Yang, Y.; Su, Y.X.; Ye, Y.Y.; Zhang, H.G. Examining the driving factors of energy related carbon emissions using the extended STIRPAT model based on IPAT identity in Xinjiang. Renew. Sustain. Energy Rev. 2017, 67, 51–61. [Google Scholar] [CrossRef]

- Danish; Zhang, B.; Wang, B.; Wang, Z.H. Role of renewable energy and non-renewable energy consumption on EKC: Evidence from Pakistan. J. Clean. Prod. 2017, 156, 855–864. [Google Scholar]

- Park, S.; Lee, Y. Regional model of EKC for air pollution: Evidence from the Republic of Korea. Energy Policy 2011, 39, 5840–5849. [Google Scholar] [CrossRef]

- Haq, I.; Zhu, S.J.; Shafiq, M. Empirical investigation of environmental Kuznets curve for carbon emission in Morocco. Ecol. Indic. 2016, 67, 491–496. [Google Scholar] [CrossRef]

- Wang, Y.; Zhang, C.; Lu, A.T.; Li, L.; He, Y.M.; Tojo, J.; Zhu, X.D. A disaggregated analysis of the environmental Kuznets curve for industrial CO2 emissions in China. Appl. Energy 2017, 190, 172–180. [Google Scholar] [CrossRef]

- Ahmad, N.; Du, L.S.; Lu, J.Y.; Wang, J.L.; Li, H.Z.; Hashmi, M.Z. Modelling the CO2 emissions and economic growth in Croatia: Is there any environmental Kuznets curve? Energy 2017, 123, 164–172. [Google Scholar] [CrossRef]

- Shuai, C.Y.; Chen, X.; Shen, L.Y.; Jiao, L.D.; Wu, Y.; Tan, Y.T. The urbing points of carbon Kuznets curve: Evidences from panel and time-series data of 164 countries. J. Clean. Prod. 2017, 162, 1031–1047. [Google Scholar] [CrossRef]

- Liddle, B. What are the carbon emissions elasticities for income and population? Bridging STIRPAT and EKC via robust heterogeneous panel estimates. Glob. Environ. Chang. 2015, 31, 62–73. [Google Scholar] [CrossRef]

- Liddle, B. Population, affluence, and environmental impact across development: Evidence from panel cointegration modeling. Environ. Model. Softw. 2013, 40, 255–266. [Google Scholar] [CrossRef]

- Itkonen, J. Problems estimating the carbon Kuznets curve. Energy 2012, 39, 274–280. [Google Scholar] [CrossRef]

- Beak, J.; Kim, H.S. Is economic growth good or bad for the environment? Empirical evidence from Korea. Energy Econ. 2013, 36, 744–749. [Google Scholar] [CrossRef]

- Saboori, B.; Sulaiman, J. CO2 emissions, energy consumption and economic growth in Association of Southeast Asian Nations (ASEAN) countries: A cointegration approach. Energy 2013, 55, 813–822. [Google Scholar] [CrossRef]

- Ndoricimpa, A. Analysis of asymmetries in the nexus among energy use, pollution emissions and real output in South Africa. Energy 2017, 125, 543–551. [Google Scholar] [CrossRef]

- Goldsmith, R. Financial Structure and Development; Yale University Press: New Haven, CT, USA, 1969. [Google Scholar]

- McKinnon, R. Money and Capital in Economic Development; Brooking Institution: Washington, DC, USA, 1973. [Google Scholar]

- King, R.; Levine, R. Finance and growth: Schumpeter might be right. Quart. J. Econ. 1993, 108, 717–737. [Google Scholar] [CrossRef]

- Levine, R.; Zeroes, S. Stock markets, banks and growth. Am. Rev. 1998, 88, 537–558. [Google Scholar]

- Khan, M.S.; Senhadji, A. Financial development and economic growth: An overview. IMF Work. Pap. 2000, 209, 413–433. [Google Scholar] [CrossRef]

- Beck, T.; Levine, R. Stock markets, banks and growth: Panel evidence. SSRN Electr. J. 2002, 28, 423–442. [Google Scholar]

- Acharyya, J. FDI, growth and the environment: Evidence from India on CO2 emission during the last two decades. J. Econ. Dev. 2009, 34, 43–58. [Google Scholar]

- Coondoo, D.; Dinda, S. Causality between income and emission: A country-group specific econometric analysis. Ecol. Econ. 2002, 40, 351–367. [Google Scholar] [CrossRef]

- Chakraborty, D.; Mukherjee, S. How do trade and investment flows affect environmental sustainability? Evidence from panel data. Environ. Dev. 2013, 6, 34–47. [Google Scholar] [CrossRef]

- Acaravci, A.; Ozturk, I. On the relationship between energy consumption, CO2 emissions and economic growth in Europe. Energy 2010, 35, 5412–5420. [Google Scholar] [CrossRef]

- Shahbaz, M.; Hye, Q.M.A.; Tiwari, A.K.; Leitão, N.C. Economic growth, energy consumption, financial development, international trade and CO2 emissions in Indonesia. Renew. Sustain. Energy Rev. 2013, 25, 109–121. [Google Scholar] [CrossRef] [Green Version]

- Bekhet, H.A.; Matar, A.; Yasmin, T. CO2 emissions, energy consumption, economic growth and financial development in GCC countries: Dynamic simultaneous equation models. Renew. Sustain. Energy Rev. 2017, 70, 117–132. [Google Scholar] [CrossRef]

- Katircioglu, S.T.; Taspinar, N. Testing the moderating role of financial development in an environmental Kuznets curve: Empirical evidence from Turkey. Renew. Sustain. Energy Rev. 2017, 68, 572–586. [Google Scholar] [CrossRef]

- Shahzad, S.; Kumar, R.; Zakaria, M.; Hurr, M. Carbon emission, energy consumption, trade openness and financial development in Pakistan: A revisit. Renew. Sustain. Energy Rev. 2017, 70, 185–192. [Google Scholar] [CrossRef]

- Cole, M.A.; Elliott, R.J.R.; Fredriksson, P.G. Endogenous pollution havens: Does FDI influence environmental regulations? Scand. J. Econ. 2006, 108, 157–178. [Google Scholar] [CrossRef]

- He, J. Pollution haven hypothesis and environmental impacts of foreign direct investment: The case of industrial emission of sulfur dioxide (SO2) in Chinese provinces. Ecol. Econ. 2006, 60, 228–245. [Google Scholar] [CrossRef]

- Ibrahim, M.H.; Law, S.H. Social capital and CO2 emission—Output relations: A panel analysis. Renew. Sustain. Energy Rev. 2014, 29, 528–534. [Google Scholar] [CrossRef]

- Halkos, G.E.; Paizanos, E.A. The effect of government expenditure on the environment: An empirical investigation. Ecol. Econ. 2013, 91, 48–56. [Google Scholar] [CrossRef] [Green Version]

- Pesaran, M.H. A simple panel unit root test in the presence of cross-section dependence. J. Appl. Econ. 2007, 22, 265–312. [Google Scholar] [CrossRef]

- Adewuyi, A.O. Effects of public and private expenditures on environmental pollution: A dynamic heterogeneous panel data analysis. Renew. Sustain. Energy Rev. 2016, 65, 489–506. [Google Scholar] [CrossRef]

- Chang, S.C. Effects of financial developments and income on energy consumption. Int. Rev. Econ. Financ. 2015, 35, 28–44. [Google Scholar] [CrossRef]

- Zhang, Y.J. The impact of financial development on carbon emissions: An empirical analysis in China. Energy Policy 2011, 39, 2197–2203. [Google Scholar] [CrossRef]

- Komal, R.; Abbas, F. Linking financial development, economic growth and energy consumption in Pakistan. Renew. Sustain. Energy Rev. 2015, 44, 211–220. [Google Scholar] [CrossRef]

- Ang, J.B. What are the mechanisms linking financial development and economic growth in Malaysia? Econ. Model. 2008, 25, 38–53. [Google Scholar] [CrossRef]

- Sadorsky, P. The impact of financial development on energy consumption in emerging economies. Energy Policy 2010, 38, 38–53. [Google Scholar] [CrossRef]

- Shahhaz, M.; Lean, H.H. Does financial development increase energy consumption? The role of industrialization and urbanization in Tunisia. Energy Policy 2012, 40, 437–439. [Google Scholar]

- Coban, S.; Topcu, M. The nexus between financial development and energy consumption in the EU: A dynamic panel data analysis. Energy Econ. 2013, 39, 81–88. [Google Scholar] [CrossRef]

- Sadorsky, P. Financial development and energy consumption in central and eastern European frontier economies. Energy Policy 2011, 39, 999–1006. [Google Scholar] [CrossRef]

- Christopoulos, D.K.; Tsionas, E.G. Financial development and economic growth: Evidence from panel unit root and cointegration tests. J. Dev. Econ. 2004, 73, 55–74. [Google Scholar] [CrossRef]

- Shahbaz, M.; Hoang, T.H.V.; Mahalik, M.K.; Roubaud, D. Energy consumption, financial development and economic growth in India: New evidence from a nonlinear and asymmetric analysis. Energy Policy 2017, 63, 199–212. [Google Scholar] [CrossRef]

- IEA (International Energy Agency). World Energy Investment Outlook: Special Report; IEA: Paris, France, 2014. [Google Scholar]

- Best, R. Switching towards coal or renewable energy? The effects of financial capital on energy transitions. Energy Econ. 2017, 63, 75–83. [Google Scholar] [CrossRef]

- Sbia, R.; Shahbaz, M.; Hamdi, H. A contribution of foreign direct investment, clean energy, trade openness, carbon emissions and economic growth to energy demand in UAE. Econ. Model. 2014, 36, 191–197. [Google Scholar] [CrossRef] [Green Version]

- Zheng, D.; Shi, M.J. Multiple environmental policies and pollution haven hypothesis: Evidence from China’s polluting industries. J. Clean. Prod. 2017, 141, 295–304. [Google Scholar] [CrossRef]

- Shahbaz, M.; Solarin, S.A.; Mahmood, H.; Arouri, M. Does financial development reduce CO2 emissions in Malaysian economy? A time series analysis. Econ. Model. 2013, 35, 145–152. [Google Scholar] [CrossRef] [Green Version]

- Jalil, A.; Feridun, M. The impact of growth, energy and financial development on the environment in China: A cointegration analysis. Energy Econ. 2011, 33, 284–291. [Google Scholar] [CrossRef]

- Salahuddin, M.; Gow, J.; Ozturk, I. Is the long-run relationship between economic growth, electricity consumption, carbon dioxide emissions and financial development in Gulf Cooperation Council Countries robust? Renew. Sustain. Energy Rev. 2015, 51, 317–326. [Google Scholar] [CrossRef]

- Mulali, U.A.; Sab, C.N. The impact of energy consumption and CO2 emission on the economic and financial development in 19 selected countries. Renew. Sustain. Energy Rev. 2012, 16, 4365–4369. [Google Scholar] [CrossRef]

- Mulali, U.A.; Sab, C.N. The impact of energy consumption and CO2 emission on the economic growth and financial development in the Sub Saharan African countries. Energy 2012, 39, 180–186. [Google Scholar] [CrossRef]

- Dogan, E.; Seker, F. The influence of real output, renewable and non-renewable energy, trade and financial development on carbon emissions in the top renewable energy countries. Renew. Sustain. Energy Rev. 2016, 60, 1074–1085. [Google Scholar] [CrossRef]

- Ozturk, I.; Acaravci, A. The long-run and causal analysis of energy, growth, openness and financial development on carbon emissions in Turkey. Energy Econ. 2013, 36, 262–267. [Google Scholar] [CrossRef]

- Abbasi, F.; Riaz, K. CO2 emissions and financial development in an emerging economy: An augmented VAR approach. Energy Policy 2016, 90, 102–114. [Google Scholar] [CrossRef]

- Gokmenoglu, K.; Ozatac, N.; Eren, B.M. Relationship between industrial production, financial development and carbon emissions: The case of Turkey. Procedia Econ. Financ. 2015, 25, 463–470. [Google Scholar] [CrossRef]

- Boutabba, M.A. The impact of financial development, income, energy and trade on carbon emissions: Evidence from the Indian economy. Econ. Model. 2014, 40, 33–41. [Google Scholar] [CrossRef]

- You, W.H.; Zhu, H.M.; Yu, K.M.; Peng, C. Democracy, financial openness, and global carbon dioxide emissions: Heterogeneity across existing emission levels. World Dev. 2015, 66, 189–207. [Google Scholar] [CrossRef]

- Tang, C.F.; Tan, B.W. The impact of energy consumption, income and foreign direct investment on carbon dioxide emissions in Vietnam. Energy 2015, 79, 447–454. [Google Scholar] [CrossRef]

- Wang, S.J.; Li, Q.Y.; Fang, C.L.; Zhou, C.S. The relationship between economic growth, energy consumption, and CO2 emissions: Empirical evidence from China. Sci. Total Environ. 2016, 542, 360–371. [Google Scholar] [CrossRef] [PubMed]

- Wang, Y.F.; Ma, X.D.; Joyce, M.J. Reducing sensor complexity for monitoring wind turbine performance using principal component analysis. Renew. Energy 2016, 97, 444–456. [Google Scholar] [CrossRef]

- Zhang, M.; Su, B. Assessing China’s rural household energy sustainable development using improved grouped principal component method. Energy 2016, 113, 509–514. [Google Scholar] [CrossRef]

- Faed, A.; Chang, E.; Saberi, M.; Hussain, O.; Azadeh, A. Intelligent customer complaint handling utilising principal component and data envelopment analysis (PDA). Appl. Soft Comput. 2016, 47, 614–630. [Google Scholar] [CrossRef]

- Shannon, C.E. A mathematical theory of communication. Bell Syst. Tech. J. 1948, 27, 279–423. [Google Scholar] [CrossRef]

- Delgado, A.; Romero, I. Environment conflict analysis using an integrated grey clustering and entropy-weight method: A case study of a mining project in Peru. Environ. Model. Softw. 2016, 77, 108–121. [Google Scholar] [CrossRef]

- Wang, Q.; Wu, C.; Sun, Y. Evaluating corporate social responsibility of airlines using entropy weight and grey relation analysis. J Air Transp. Manag. 2015, 42, 55–62. [Google Scholar] [CrossRef]

- Zou, Z.H.; Yun, Y.; Sun, J.N. Entropy method for determination of weight of evaluating in fuzzy synthetic evaluation for water quality assessment indicators. J. Environ. Sci. 2006, 18, 1020–1023. [Google Scholar] [CrossRef]

- Chen, S.; Leng, Y.; Mao, B.; Liu, S. Integrated weight-based multi-criteria evaluation on transfer in large transport terminals: A case study of the Beijing south railway Station. Transp. Res. Part A Policy Pract. 2014, 66, 13–26. [Google Scholar] [CrossRef]

- Srivastav, R.; Simonovic, S. An analytical procedure for multi-site, multi-season streamflow generation using maximum entropy bootstrapping. Environ. Model. Softw. 2014, 59, 59–75. [Google Scholar] [CrossRef]

- Neill, O.; Liddle, B.; Jiang, L.; Smith, K.; Pachauri, S.; Dalton, M.; Fuchs, R. Demographic change and carbon dioxide emissions. Lancet 2012, 380, 157–164. [Google Scholar] [CrossRef]

- Binder, M.; Offermanns, C.J. International Investment Positions and Exchange Rate Dynamics: A Dynamic Panel Analysis. Discussion Paper. 2007. Available online: https://www.researchgate.net/publication/5002596 (accessed on 8 May 2016).

- China Energy Statistical Yearbook (2014), Regional Energy Balanced Sheet (Quantity). Available online: http://free.xiaze.com/nianjian/zgnytjnj2013/ (accessed on 5 April 2016).

- IPCC (Intergovernmental Panel on Climate Change). IPCC Guidelines for National Greenhouse Gas Inventories. Available online: http://www.ipcc-nggip.iges.or.jp/public/gl/guidelin/ch1ri.pdf (accessed on 8 May 2016).

- Li, K.; Qi, S.Z. Trade openness, economic growth and CO2 emission of China. Econ. Res. 2011, 11, 60–72. (In Chinese) [Google Scholar]

- Cement data, CEinet Statistics Database. Available online: http://db.cei.gov.cn (accessed on 8 May 2016).

- Sheng, P.F.; Guo, X.H. The long-run and short-run impact of urbanization on carbon dioxide emissions. Econ. Model. 2016, 53, 208–215. [Google Scholar] [CrossRef]

- Luintel, K.B.; Khan, M.; Gonzalez, R.L.; Li, G.G. Financial development, structure and growth: New data, method and results. J. Int. Financ. Mark. Inst. Money 2016, 43, 95–112. [Google Scholar] [CrossRef]

- Kim, S.H.; Lin, S.C.; Chen, T.C. Financial structure, firm size and industry growth. Int. Rev. Econ. Financ. 2014, 41, 23–39. [Google Scholar] [CrossRef]

- Lim, C.C.; Mcnelis, P.D. Income growth and inequality: The threshold effects of trade and finanical openness. Econ. Model. 2016, 58, 403–412. [Google Scholar] [CrossRef]

- Trabelsi, M.; Cherif, M. Capital account liberalization and financial deepening: Does the private sector matter? Q. Rev. Econ. Financ. 2017, 64, 141–151. [Google Scholar] [CrossRef]

- Luo, Y.; Tanna, S.; Vita, G.D. Financial openness, risk and bank efficiency: Cross-country evidence. J. Financ. Stab. 2016, 24, 132–148. [Google Scholar] [CrossRef]

- Riain, S.O.; Curry, E.; Harth, A. XBRL and open data for global financial ecosystems: A linked data approach. Int. J. Account. Inf. Syst. 2012, 13, 141–162. [Google Scholar] [CrossRef]

- Pesaran, M.H. General diagnostic tests for cross section dependence in panels. CWPE 2004, 7, 1240. [Google Scholar]

- Kim, D.H.; Lin, S.C.; Suen, Y.B. Dynamic effects of trade openness on financial development. Econ. Model. 2010, 27, 254–261. [Google Scholar] [CrossRef]

- Pesaran, M. A simple panel unit root test in the presence of cross-section dependence. J. Appl. Econ. 2003, 22, 265–312. [Google Scholar] [CrossRef]

- Baek, J. A new look at the FDI-income-energy-environment nexus: Dynamic panel data analysis of ASEAN. Energy Policy 2016, 91, 22–27. [Google Scholar] [CrossRef]

- Westerlund, J. Testing for error correction in panel data. Oxf. Bull. Econ. Stat. 2007, 69, 709–748. [Google Scholar] [CrossRef]

| Country | Year | Influencing Factors | Estimated Methods | Equation | Ref. |

|---|---|---|---|---|---|

| Factor Decomposition Model | |||||

| EU-28 | 2000–2012 | Level of activity, electricity intensity, electricity trade, efficiency of electricity generation and fuel mix | LMDI-I method with the use of logarithmic mean weight functions | [14] | |

| United States | 2005–2025 | CO2 intensity of energy use, energy intensity of output, structural change, GPD per capita, population | Kaya identity additive Logarithmic Mean Divisia Index (LMDI) method | [15] | |

| China | 2000–2012 | Energy structure, intensity, energy efficiency, economic development, population | Logarithmic Mean Divisia Index (LMDI) method | [16] | |

| China | 2001–2011 | Energy mix change, potential energy intensity change, economic activity, energy usage efficiency, energy saving technology change, GDP technical efficiency, GDP technology change | the multiplicative LMDI method | [17] | |

| STIRPAT model | |||||

| China | 1990–2012 | Percentages of population employed in secondary and tertiary industries, percentage of the population living in urban areas, shares of the added value of secondary and tertiary industry to the GDP, rural-urban income gap, the cultivated land area occupied by construction | Fixed effects (FE), the feasible generalized least squares (FGLS) and the linear regression with Driscoll–Kraay standard errors (DK) | [18] | |

| China | 1995–2010 | Population, GDP per capita, tertiary industry value, secondary industry output value, FDI, energy consumption | Fixed effects (FE), linear regression with Newey-West standard errors (N-W), panel-corrected standard errors (PCSE), and Driscoll-Kraay standard errors (DK), feasible generalized least squares (FGLS) | [19] | |

| China | 1980–2010 | Total population, urbanization level, GDP per capita, technology, industrialization, service, foreign trade degree, energy consumption structure | Ridge regression with biased estimates | [20] | |

| China | 1990–2008 | GDP per capita, industrial structure, population, urbanization rate, technology level, energy consumption | Partial least squares (PLS) regression, linear regression | [21] | |

| CKC/EEO model | |||||

| Morocco | 1971–2011 | GDP per capita, trade openness, electricity consumption per capita | Vector error correction mechanism (VECM) | [25] | |

| China | 2000–2013 | GDP per capita, energy intensity, urbanization level | Semi-parametric panel fixed effects regression supplemented with traditional parametric regression estimation method | [26] | |

| Croatia | 1992–2011 | GDP | Autoregressive distributed lag model (ARDL), dynamic ordinary least squares (DOLS), fully modified ordinary least squares (FMOLS) | [27] | |

| 164 countries | 1960–2011 | GDP per capita | Ordinary least squares (OLS) | [28] | |

| Korea | 1978–2007 | Income, energy consumption, electricity production (thermal power, nuclear) | Autoregressive distributed lag model (ARDL), ordinary least squares (OLS) | [32] | |

| Southeast Asian Nations | 1997–2009 | Real income per capita, energy use per capita | Autoregressive distributed lag model (ARDL), ordinary least squares (OLS) | [33] | |

| South Africa | 1971–2010 | Energy use, GDP per capita | Autoregressive distributed lag model (ARDL), ordinary least squares (OLS) | [34] | |

| Time | Countries | Carbon Emissions | Financial Development | Method | Relationship | Ref. |

|---|---|---|---|---|---|---|

| 1975–2011 | Indonesia | CO2 emission per capita | Real domestic credit to private sector per capita | Unit root/ARDL | Financial development condenses carbon emissions and inverted-U shaped relationship is confirmed between financial development and carbon emissions. | [45] |

| 1975–2011 | UAE | CO2 emission per capita | Domestic credit to private sector | Unit root/Co-integration | Find an inverted U-shaped relationship between financial development and CO2 emissions. | [2] |

| 1971–2011 | Malaysia | CO2 emission per capita | Real domestic credit to private sector per capita | ARDL/VECM | Financial development can play positive and significant role in combating environmental degradation in the country. | [69] |

| 1953–2006 | China | CO2 emission per capita | Ratio of deposit liabilities to nominal GDP, ratio of credit to private sector to nominal GDP, ratio of commercial bank assets to the sum of commercial bank and central bank assets, foreign assets plus the foreign liabilities as a share of GDP | ARDL | Financial development has led to a decrease in environmental pollution. | [70] |

| 1980–2012 | Gulf Cooperation Council Countries | CO2 emission per capita | Domestic credit available to the private sector as share of GDP | PVECM | Financial development was found to reduce CO2 emissions in the long-run; Financial development would continue to impact CO2 emissions little magnitude into the future. | [71] |

| 1980–2008 | 19 countries | CO2 emission per capita | Broad money, domestic credit provided by banking sector, and the domestic credit to private sector | Granger causality test | CO2 emission affected the financial development based on the long run causal relationship and the positive short run causal relationship. | [72] |

| 1980–2008 | Sub Saharan African countries | Carbon emissions | Broad money, the domestic credit to private sector | Granger causality test | CO2 emission had a long run impact and a positive causal relationship on the financial development. The financial development indicators had a positive causal relationship with the CO2 emission. | [73] |

| 1985–2011 | 40 countries | Carbon emissions | Domestic credit to private sector | EKC/PVECM | Increases in financial development decrease carbon emissions. | [74] |

| 1960–2007 | Turkey | CO2 emission per capita | Domestic credit to private sector | ARDL/Granger causality test/VEC | There is a long-run relationship between per capita carbon emissions and financial development. Financial development variable has no significant effect on per capita carbon emissions in the long run. | [75] |

| 1971–2011 | Pakistan | CO2 emission per capita | Financial intermediation development: Total Credit, Private Sector Credit; Stock market development: Stock market capitalization, Stocks traded/turnover; Foreign direct Investment | ARDL//VECM | CO2 emission per capita is co-integrated with financial development; Financial development contributes to the increase of CO2 emission; FDI had a unidirectional causal relationship with emissions. | [76] |

| 1960–2010 | Turkey | CO2 emission per capita | Real domestic credit to private sector per capita | Granger causality test | There is a unidirectional relationship between financial development and carbon emissions. | [77] |

| 1971–2008 | India | Carbon emission | Domestic credit to private sector | ARDL/Granger causality test | Financial development has a long-run positive impact on carbon emissions. There is a long-run unidirectional causality running from financial development to carbon emissions and energy use. | [78] |

| 1985–2005 | World | CO2 emission per capita | Financial openness | EKC/Quantile regression model | More financial openness does not appear to reduce the carbon emissions. | [79] |

| 1965–2008 | South Africa | CO2 emission per capita | Real domestic credit to private sector per capita | Unit root/ARDL/ECM | Banking sector development that is per capita access to domestic credit of private sector help to achieve lower CO2 per capita emissions. | [1] |

| 1994–2009 | China | Carbon emissions | Financial intermediation scale, financial intermediation efficiency, stock market scale, stock market efficiency, foreign direct investment | VAR/Granger causality test/VECM | The influence of financial intermediation scale is the largest with weaker efficiency’s influence. Stock market scale has relatively larger influence on carbon emissions with limited efficiency. FDI exerts the least influence on the change of carbon emissions. | [56] |

| 1976–2009 | Vietnam | CO2 emission per capita | Real financial direct investment per capita | Co-integration/Granger causality test | The FDI is found to be negatively affecting CO2 emissions. | [80] |

| 1989–2011 | 13 European/12 Asia and Oceania | Carbon emissions | The ratio of domestic credit to the private sector to GDP, and the stock traded turnover ratio | PVAR | CO2 shocks on both credit and stock markets are insignificant. | [11] |

| Criteria Level | Factor Level | Measuring Level |

|---|---|---|

| FSZ | Financial asset | X1: Gross of banking assets, Security assets and Premium income |

| Financial institutions | X2: Number of insurance and Security institutions | |

| Financial professionals | X3: Total number of financial professionals | |

| FST | Financial industrial structure | X4: Banking assets/Financial assets |

| Internal structure of banking industry | X5: Deposit/Loan | |

| FOP | Capital flow liberalization | X6: FDI/Total investment in fixed assets |

| Localization of foreign financial service | X7: Gross of FDI in financial industry | |

| FDP | Finacialization | X8: Gross of deposit and loan of financial institutes/GDP |

| Financial depth rate | X9: Financial assets/GDP | |

| Foreign direct investment depth rate | X10: FDI/GDP | |

| FGR | Financial increasing | X11: Increasing speed of RMB deposit of financial institutions |

| X12: Increasing rate of RMB deposit of residents | ||

| Capital formation speed | X13: Gross capital formation/GDP | |

| Insurance density | X14: Premium per capita | |

| Insurance depth | X15: Premium income/GDP | |

| FEF | Macroscopic allocation efficiency | X16: Transform rate of saving to investment |

| X17: Capital formation rate | ||

| Saving rate | X18:Saving/Disposal personal income | |

| Marginal productivity of capital | X19: GDP growth/Total fixed asset investment | |

| FEC | Institutional environment | X20: Variety of distribution |

| Intermediary services | X21: Rate of patent authorization and pending | |

| Social credit system | X22: Individual credit |

| Name | Variable Measure | Symbol | Expected Sign | Economic Implications |

|---|---|---|---|---|

| GDP per capita | GDP/total population | GDPPC | +/− | The influence is uncertain. According to EKC, carbon emissions would increase first with the rise of GDP per capita and then show a declining trend after a certain threshold value is reached. |

| Industrial structure | Total industrial output value/GDP | IS | +/− | The process of industrialization includes technological advancement, which can redistribute the production factors and improve the production efficiency. However, in the early stages of industrialization, the carbon emissions will increase. |

| Long-Run Coefficients | Short-Run Coefficients | |||||||

|---|---|---|---|---|---|---|---|---|

| CMG | CPMG | CDFE | CMG | CPMG | CDFE | |||

| GDPPC | 0.228 (0.452) | 0.214 *** (3.251) | 0.293 *** (7.320) | GDPPC | −0.491 (−0.273) | 0.293 (1.193) | 0.312 (0.685) | |

| IS | −1.393 ** (−1.982) | 0.344 *** (5.619) | 0.310 ** (2.020) | IS | 0.219 * (1.920) | 0.174 ** (2.327) | −0.258 (−0.531) | |

| FD | −0.729 (−0.308) | 0.986 * (1.830) | 0.291 *** (8.792) | FD | 0.154 (0.983) | −0.215 *** (−7.170) | 0.375 ** (2.290) | |

| FD2 | 2.175 (0.835) | 0.252 *** (3.714) | −0.321 *** (−4.832) | FD2 | −0.352 (−0.159) | 0.719 (1.024) | 0.907 (0.925) | |

| Error correction | −0.286 * (−1.992) | −0.491 ** (−2.218) | −0.219 *** (−3.890) | Constant | 0.912 (0.014) | 2.566 *** (4.376) | 4.474 *** (4.140) | |

| Number of obs | 390 | Hausman test | 1 | Prob ≥ 1.000 | ||||

| Number of groups | 30 | 2 | Prob ≥ 0.989 | |||||

| Log Likelihood | 881.343 | 3 | Prob ≥ 1.000 | |||||

| Eastern Region | Middle Region | Western Region | Northeastern Region | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| CMG | CPMG | CDFE | CMG | CPMG | CDFE | CMG | CPMG | CDFE | CMG | CPMG | CDFE | |||

| Long-run coefficients | GDPPC | 0.347 * (−1.832) | 0.314 ** (2.130) | 0.224 *** (3.261) | 0.329 * (1.922) | −0.131 (−0.840) | 0.326 ** (2.281) | 0.318 ** (2.175) | 0.205 *** (4.435) | 0.342 *** (7.123) | −0.279 *** (−4.328) | −0.273 ** (−2.251) | −0.125 *** (6.764) | |

| IS | −0.358 ** (−6.486) | −0.208 * (−1.945) | −0.352 ** (−2.471) | 0.246 *** (2.929) | −0.253 * (−1.842) | 0.510 (0.529) | 0.353 ** (2.334) | 0.411 (1.150) | 0.261 *** (4.205) | 0.622 ** (2.335) | 0.832 * (1.8192) | 0.741 *** (3.935) | ||

| FD | −0.335 * (−1.920) | 0.427 (1.207) | −0.374 *** (−3.238) | 0.521 *** (4.837) | −0.581 (−1.428) | 0.391 *** (4.519) | 0.613 ** (2.029) | 0.426 * (1.992) | 0.461 *** (4.298) | 0.633 * (1.826) | 0.741 *** (3.514) | 0.698 ** (2.279) | ||

| FD2 | −0.348 ** (−2.205) | −0.359 ** (−2.275) | −0.258 *** (−5.324) | −0.762 *** (−4.732) | 0.164 * (1.938) | −0.873 ** (−2.134) | −0.523 ** (−2.490) | −0.741 (−0.148) | −0.915 *** (−3.904) | −0.674 ** (−2.435) | −0.733 (−1.532) | −0.582 * (-1.973) | ||

| Error correction | 0.138 * (1.831) | −0.427 *** (−2.794) | −0.416 *** (−4.190) | −0.301 ** (−2.13) | −0.315 ** (−2.143) | −0.251 *** (−6.237) | −0.379 (−1.146) | −0.291 ** (−2.101) | −0.313 *** (−3.850) | −0.304 ** (−2.345) | −0.135 *** (−1.453) | −0.421 *** (−2.890) | ||

| Short-run coefficients | GDPPC | 0.136 * (1.841) | −0.142 (−1.219) | −0.115 * (−1.893) | −1.750 (−1.28) | −0.019 (−0.928) | −0.225 (−0.451) | 0.404 *** (2.845) | −0.897 (−1.320) | 0.461 ** (2.354) | 0.969 (1.354) | −0.437 * (−1.355) | 0.234 * (2.014) | |

| IS | 0.480 * (1.971) | 0.179 ** (1.324) | −0.261 ** (−2.436) | 0.220 ** (2.401) | −0.251 * (−1.840) | 0.391 (0.202) | −0.451 ** (−2.142) | 0.029 (0.640) | −0.361 * (−1.882) | 0.372 (1.462) | 0.401 ** (2.445) | 0.235 ** (2.133) | ||

| FD | −0.312 ** (−2.045) | −0.364 * (−1.813) | −0.334 ** (−2.201) | 0.254 *** (−5.605) | 0.829 (1.340) | 0.913 (0.251) | 0.542 *** (5.290) | 0.490 (0.270) | 0.516 ** (1.346) | 0.039 (0.904) | 0.910 (0.20) | 0.429 * (1.821) | ||

| FD2 | −0.231 * (1.841) | −0.532 ** (2.289) | −0.237 ** (−2.184) | −0.284 * (−1.784) | −0.841 (−1.129) | −0.418 (−0.582) | −0.031 (−0.340) | −0.158 ** (−2.184) | −0.917 * (−1.942) | −0.114 * (−1.801) | −0.994 (−0.301) | −0.151 * (−1.794) | ||

| Constant | −0.081 *** (−4.000) | 0.034 ** (2.163) | 0.083 *** (3.901) | 0.072 *** (4.132) | 0.262 ** (2.214) | 0.086 ** (2.245) | 0.031 ** (2.051) | −0.048 * (−1.910) | 0.071 *** (4.406) | 0.619 *** (3.410) | 0.381 ** (2.400) | 0.212 *** (4.137) | ||

| Number of obs | 130 | 78 | 143 | 39 | ||||||||||

| Number of groups | 10 | 6 | 11 | 3 | ||||||||||

| Hausman test | 1 | Prob ≥ 1.000 | Prob ≥ 1.000 | Prob ≥ 1.000 | Prob ≥ 1.000 | |||||||||

| 2 | Prob ≥ 0.990 | Prob ≥ 0.991 | Prob ≥ 0.993 | Prob ≥ 0.998 | ||||||||||

| 3 | Prob ≥ 1.000 | Prob ≥ 1.000 | Prob ≥ 1.000 | Prob ≥ 1.000 | ||||||||||

| 10th Five-Year Plan | 11th Five-Year Plan | 12th Five-Year Plan | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| CMG | CPMG | CDFE | CMG | CPMG | CDFE | CMG | CPMG | CDFE | |||

| Long−run coefficients | GDPPC | 0.235 * (1.941) | 0.248 ** (2.193) | 0.253 *** (4.972) | 0.258 ** (2.349) | 0.241 *** (4.153) | 0.292 *** (4.513) | 0.150 ** (2.214) | −0.112 *** (−2.839) | −0.142 *** (−3.514) | |

| IS | 0.624 ** (2.295) | 0.427 *** (4.512) | 0.720 ** (1.986) | 0.449 *** (3.395) | 0.316 * (1.912) | 0.552 ** (2.215) | 0.241 ** (2.127) | 0.051 (0.990) | 0.301 ** (2.198) | ||

| FD | 0.793 *** (4.417) | 0.774 ** (2.249) | 0.816 *** (2.995) | 0.5132 ** (2.310) | 0.414 *** (3.154) | 0.569 ** (2.114) | 0.325 ** (2.117) | 0.350 *** (5.214) | 0.257 *** (4.146) | ||

| FD2 | −0.418 ** (−2.251) | −0.162 (−0.829) | −0.298 ** (−2.263) | −0.172 (−1.880) | −0.203 (−0.619) | −0.283 (−0.354) | 0.682 (0.292) | −0.541 (−0.430) | 0.823 (0.514) | ||

| Error correction | −1.933 ** (−1.923) | −0.422 ** (−2.125) | −0.946 *** (−5.959) | −0.354 *** (−3.719) | −0.422 ** (−2.124) | −0.481 *** (−3.081) | −1.293 ** (−1.904) | −0.351 (−0.980) | −1.412 *** (−5.523) | ||

| Short−run coefficients | GDPPC | 0.301 (0.482) | 0.461 (1.201) | −0.439 *** (−4.329) | 0.719 (0.343) | 0.193 ** (2.273) | 0.415 (0.911) | −0.214 * (−1.892) | 0.183 ** (2.091) | −0.280 ** (−2.142) | |

| IS | 0.293 * (1.982) | 0.923 (0.924) | 0.142 * (1.842) | 0.993 (0.030) | 0.219 *** (2.906) | 2.327 (0.092) | −0.011 (−0.203) | −0.383 (−0.330) | −0.282 (−1.231) | ||

| FD | 0.192 * (1920) | 0.012 (1.021) | 0.169 * (1.981) | −0.264 (−0.239) | 0.335 (0.349) | −0.243 ** (−2.211) | −1.001 (−0.032) | 0.383 (0.590) | −0.342 * (−1.953) | ||

| FD2 | −0.213 (−0.781) | −0.258 * (−1.811) | −0.213 * (−1.851) | 0.232 * (1.914) | −0.914 (−1.228) | 0.839 (1.019) | 0.928 (1.348) | −0.830 (−0.921) | 0939 (1.282) | ||

| Constant | 0.021 * (1.892) | 0.355 (0.091) | −0.475 * (−1.920) | 0.439 (1.026) | −0.244 ** (−2.248) | 0.214 ** (2.044) | 0.312 (0.720) | −1.883 *** (−4.028) | 1.251 ** (2.122) | ||

| Number of obs | 120 | 120 | 90 | ||||||||

| Number of groups | 30 | 30 | 30 | ||||||||

| Hausman test | 1 | Prob ≥ 1.000 | Prob ≥ 1.000 | Prob ≥ 1.000 | |||||||

| 2 | Prob ≥ 0.989 | Prob ≥ 0.993 | Prob ≥ 0.991 | ||||||||

| 3 | Prob ≥ 1.000 | Prob ≥ 1.000 | Prob ≥ 1.000 | ||||||||

| Aspect | FSZ | FST | FOP | FDP | FGR | FEF | FEC | Error Correction | Constant |

|---|---|---|---|---|---|---|---|---|---|

| Overall impact | 0.369 *** (4.839) | −0.246 (−1.540) | 0.133 ** (2.168) | 0.221 *** (4.901) | −0.293 (−1.409) | −0.166 ** (−2.213) | −0.159 * (−1.798) | 0.382 *** (3.829) | −0.224 *** (−4.338) |

| Eastern region | −0.496 *** (−3.439) | −0.410 (−0.021) | −0.284 ** (−2.267) | −0.142 ** (−2.199) | 0.492 (1.503) | −0.398 *** (−4.839) | −0.451 *** (−4.223) | 0.528 *** (5.490) | −0.308 *** (−4.113) |

| Middle region | 0.313 *** (2.904) | 0.351 *** (4.982) | 0.192 *** (3.904) | 0.129 *** (5.701) | 0.929 (0.081) | 0.042 (1.233) | 0.148 *** (2.312) | 0.551 *** (4.391) | −0.218 ** (−4.492) |

| Western region | 0.235 ** (2.152) | −0.440 (−0.092) | 0.926 (1.450) | 0.105 * (−1.915) | −0.241 ** (−2.135) | 0.282 (0.010) | −0.195 ** (−1.982) | 0.345 *** (4.326) | −0.209 ** (−2.213) |

| Northeastern region | 0.193 ** (1.998) | 0.924 (0.241) | 0.326 *** (6.132) | 0.146 (0.021) | −2.410 (−0.199) | 0.335 *** (4.213) | −0.153 (−1.288) | 0.590 (1.095) | −0.037 *** (−5.192) |

| Region | Impact | Reasons |

|---|---|---|

| Financial Size [99] | ||

| Nationwide | + | 1. Energy-intensive enterprises with small investment risk and high revenues use the extensive product mode. 2. Lack of government support and investment in energy conservation and emission reduction technologies. 3. Financial institutions do not focus on the design of low-carbon products. |

| Eastern region | − | 1. The eastern region is a good location, and the financial size is in an early stage, so the costs of emission reduction are low. 2. The government guides carbon emissions positively, and the desire to reduce the emissions of companies in the eastern region is strong. |

| Middle region | + | |

| Western region | + | |

| North-eastern region | + | |

| Financial openness [100] | ||

| Nationwide | + | 1. The entry barrier for FDI in China is too low to ensure investment quality. The attraction for FDI is not sufficient, and the pursuit of FDI is blind. 2. The regulations are not perfect. |

| Eastern region | − | 1. The eastern region can attract good foreign investment with high technology. 2. FDI in the western region is limited. 3. The reasons for middle and north-eastern regions are the same as those nationwide. |

| Middle region | + | |

| Western region | / | |

| North-eastern region | + | |

| Financial depth [101] | ||

| Nationwide | + | 1. The resources of financial credit agencies are directed to departments with high energy consumption. 2. FDI transforms industries with high energy consumption and pollution in China. |

| Eastern region | − | 1. The technological advantage of the eastern region is obvious, and technology spill-over can offset the pollution. 2. In the eastern region, credit from financial institutions is placed in the green energy industry. |

| Middle region | + | |

| Western region | + | |

| North-eastern region | + | |

| Financial efficiency [102] | ||

| Nationwide | − | 1. Transformation rate of savings and deposits of financial institutions is high, and more financing can help change the product technology. 2. The financial environment for resident consumption improves, requiring low energy consumption products. |

| Eastern region | − | 1. The eastern region has an obvious technological advantage with a high transformation rate of capital use. The situation in the north-eastern region is the opposite. |

| Middle region | / | |

| Western region | / | |

| North-eastern region | + | |

| Financial ecology [103] | ||

| Nationwide | − | 1. Technological innovation decreases carbon emissions. 2. Improvement in quality of life enhances awareness of energy conservation and emission reduction. |

| Eastern region | − | 1. Insufficient control of technology innovation in the north-eastern region. 2. Awareness of carbon emissions reduction among residents is weak. |

| Middle region | − | |

| Western region | − | |

| North-eastern region | / | |

© 2017 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Xing, T.; Jiang, Q.; Ma, X. To Facilitate or Curb? The Role of Financial Development in China’s Carbon Emissions Reduction Process: A Novel Approach. Int. J. Environ. Res. Public Health 2017, 14, 1222. https://doi.org/10.3390/ijerph14101222

Xing T, Jiang Q, Ma X. To Facilitate or Curb? The Role of Financial Development in China’s Carbon Emissions Reduction Process: A Novel Approach. International Journal of Environmental Research and Public Health. 2017; 14(10):1222. https://doi.org/10.3390/ijerph14101222

Chicago/Turabian StyleXing, Tiancai, Qichuan Jiang, and Xuejiao Ma. 2017. "To Facilitate or Curb? The Role of Financial Development in China’s Carbon Emissions Reduction Process: A Novel Approach" International Journal of Environmental Research and Public Health 14, no. 10: 1222. https://doi.org/10.3390/ijerph14101222