Doing Good Again? A Multilevel Institutional Perspective on Corporate Environmental Responsibility and Philanthropic Strategy

Abstract

:1. Introduction

2. Theories and Hypotheses

2.1. Literature Review and Institutional Background

2.2. Corporate Environmental Responsibility and Corporate Philanthropy

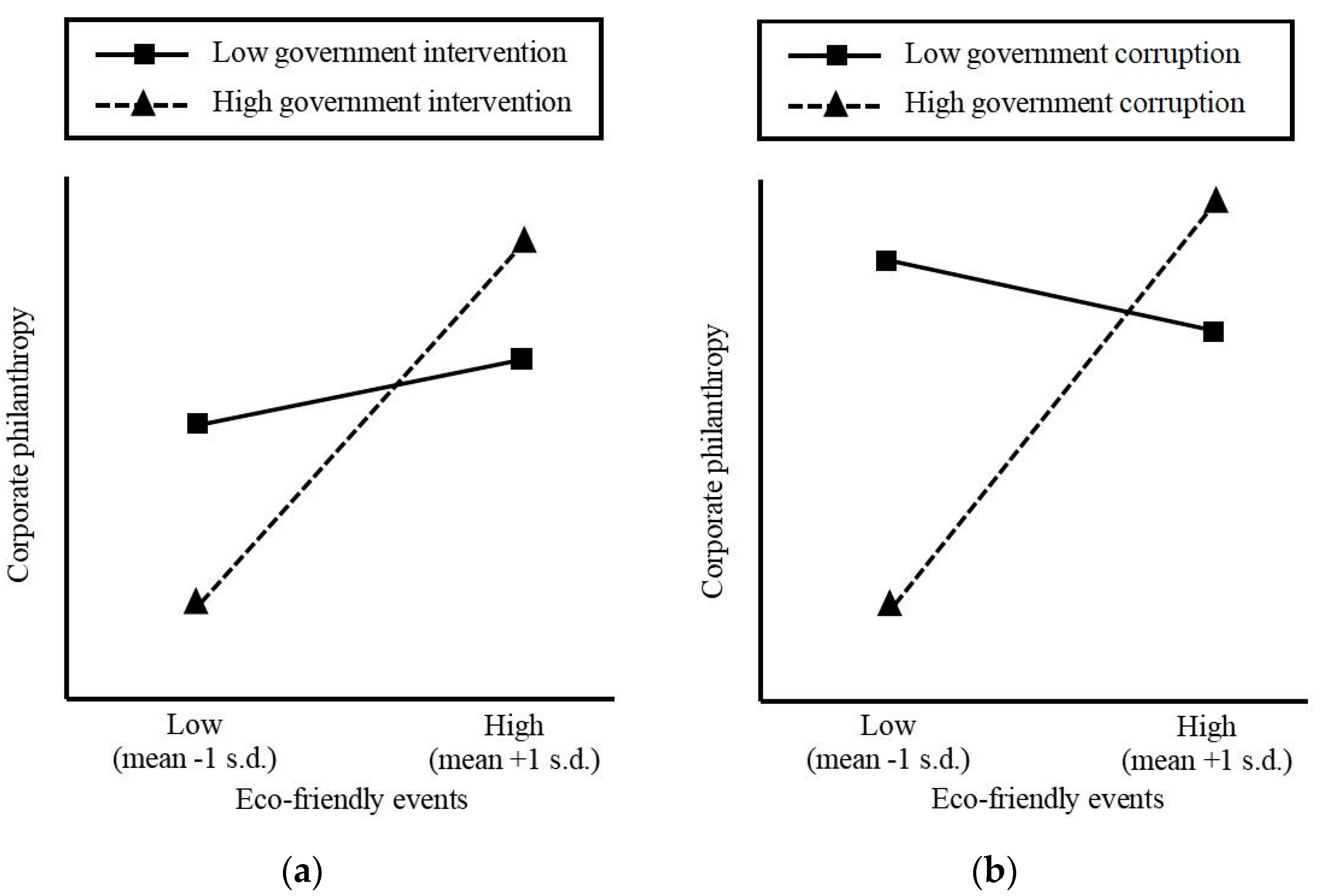

2.3. Moderation Effect of Government Intervention

2.4. Moderation Effect of Government Corruption

3. Data and Methodology

3.1. Sample and Data Collection

3.2. Measurement of Variables

3.2.1. Corporate Philanthropy (Named Donation)

3.2.2. Corporate Eco-Friendly Events (Named Environment)

3.2.3. Government Intervention (Named NERI)

3.2.4. Government Corruption (Named Corruption)

3.2.5. Control Variables

- (1)

- Firm size (named Firm size), measured as the logarithm of corporate total assets, has been proven to play an important role in corporate philanthropic behavior [47]. Larger firms have more resources to practice corporate philanthropy and tend to pay more attention to their reputations and shareholders’ attitudes [47,48,54].

- (2)

- Firm age (named Firm age), measured as the number of years from a firm’s foundation until the end of 2013. Older firms have been proven to be likelier to accumulate more resources from different channels and to practice corporate philanthropy. This is made possible by their more stable organizational structures and greater social relevance [17,20].

- (3)

- Leverage (named Leverage) measured as the percentage ratio of total debts to total assets [55].

- (4)

- (5)

- Corporate performance (named ROA), measured as the percentage value of Return to Assets (ROA). Previous studies have proved that firms with good financial performance are more likely to practice corporate philanthropy [17].

- (6)

- Regional GDP (named GDP), measured as the logarithm of Gross Domestic Product (GDP) at the provincial level in China [56].

- (7)

- Finally, we introduced Year dummy for each year from 2008 to 2013 into the regression.

3.3. Statistical Analysis

4. Results

4.1. Descriptive Statistics

4.2. Regression Analyses and Results

4.3. Robustness Checks

5. Discussion

5.1. Contributions and Implications

5.2. Limitations and Future Study Directions

6. Conclusions

Acknowledgments

Author Contributions

Conflicts of Interest

References

- Ameer, R.; Othman, R. Sustainability practices and corporate financial performance: A study based on the top global corporations. J. Bus. Ethics 2012, 108, 61–79. [Google Scholar] [CrossRef]

- Flammer, C. Corporate Social Responsibility and Shareholder Value: The Environmental Consciousness of Investors. Acad. Manag. J. 2011, 56, 758–781. [Google Scholar] [CrossRef]

- Perrini, F.; Tencati, A. Sustainability and stakeholder management: The need for new corporate performance evaluation and reporting systems. Bus. Strategy Environ. 2006, 15, 296–308. [Google Scholar] [CrossRef]

- Sharma, S.; Vredenburg, H. Proactive corporate environmental strategy and the development of competitively valuable organizational capabilities. Strateg. Manag. J. 1998, 19, 729–753. [Google Scholar] [CrossRef]

- Lyon, T.P.; Maxwell, J.W. Corporate social responsibility and the environment: A theoretical perspective. Rev. Environ. Econ. Policy 2008, 2, 240–260. [Google Scholar] [CrossRef]

- Portney, P.R. The (Not So) new corporate social responsibility: An empirical perspective. Rev. Environ. Econ. Policy 2008, 2, 261–275. [Google Scholar] [CrossRef]

- Rahman, N.; Post, C. Measurement Issues in Environmental Corporate Social Responsibility (ECSR): Toward a Transparent, Reliable, and Construct Valid Instrument. J. Bus. Ethics 2012, 105, 307–319. [Google Scholar] [CrossRef]

- Waddock, S.A.; Graves, S.B. The corporate social performance-financial performance link. Strateg. Manag. J. 1997, 18, 303–319. [Google Scholar] [CrossRef]

- Ambec, S.; Lanoie, P. Does it pay to be green? A systematic overview. Acad. Manag. Perspect. 2008, 22, 45–62. [Google Scholar]

- Dollinger, M.J. Environmental contacts and financial performance of the small firm. J. Small Bus. Manag. 1985, 23, 24. [Google Scholar]

- King, A.A.; Lenox, M.J. Does it really pay to be green? An empirical study of firm environmental and financial performance. J. Ind. Ecol. 2001, 5, 105–116. [Google Scholar] [CrossRef]

- Orlitzky, M.; Siegel, D.S.; Waldman, D.A. Strategic corporate social responsibility and environmental sustainability. Bus. Soc. 2011, 50, 1–28. [Google Scholar] [CrossRef]

- Stanwick, P.A.; Stanwick, S.D. The relationship between corporate social performance and organizational size, financial performance, and environmental performance: An empirical examination. J. Bus. Ethics 1998, 17, 195–204. [Google Scholar] [CrossRef]

- Du, X.Q. Is Corporate Philanthropy Used as Environmental Misconduct Dressing? Evidence from Chinese Family-Owned Firms. J. Bus. Ethics 2015, 129, 341–361. [Google Scholar] [CrossRef]

- Emerson, R.M. Power-dependence relations. Am. Sociol. Rev. 1962, 27, 31–41. [Google Scholar] [CrossRef]

- Pfeffer, J.; Salancik, G.R. The External Control of Organizations: A Resource-Dependency Perspective; Harper & Row: New York, NY, USA, 1978; pp. 76–90. [Google Scholar]

- Wang, H.; Qian, C. Corporate philanthropy and corporate financial performance: The roles of stakeholder response and political access. Acad. Manag. J. 2011, 54, 1159–1181. [Google Scholar] [CrossRef]

- Chiu, S.; Sharfman, M. Legitimacy, visibility, and the antecedents of corporate social performance: An investigation of the instrumental perspective. J. Manag. 2011, 37, 1558–1585. [Google Scholar] [CrossRef]

- Dickson, B.J. Red Capitalists in China: The Party, Private Entrepreneurs, and Prospects for Political Change; Cambridge University Press: Cambridge, UK, 2003; pp. 35–60. ISBN 052-1-81-817-6. [Google Scholar]

- Gao, Y.Q.; Hafsi, T. Government Intervention, Peers Giving and Corporate Philanthropy: Evidence from Chinese Private SMEs. J. Bus. Ethics 2015, 132, 433–447. [Google Scholar] [CrossRef]

- Koehn, D.; Ueng, J. Is philanthropy being used by corporate wrongdoers to buy good will? J. Manag. Gov. 2010, 14, 1–16. [Google Scholar] [CrossRef]

- Porter, M.E.; Kramer, M.R. The competitive advantage of corporate philanthropy. Harv. Bus. Rev. 2002, 80, 56–68. [Google Scholar] [PubMed]

- Haley, U.C. Corporate contributions as managerial masques: Reframing corporate contributions as strategies to influence society. J. Manag. Stud. 1991, 28, 485–510. [Google Scholar] [CrossRef]

- Godfrey, P.C.; Merrill, C.B.; Hansen, J.M. The relationship between corporate social responsibility and shareholder value: An empirical test of the risk management hypothesis. Strateg. Manag. J. 2009, 30, 425–445. [Google Scholar] [CrossRef]

- Brammer, S.; Millington, A. Corporate reputation and philanthropy: An empirical analysis. J. Bus. Ethics 2005, 61, 29–44. [Google Scholar] [CrossRef]

- Wang, H.; Choi, J.; Li, J.T. Too little or too much? Untangling the relationship between corporate philanthropy and firm financial performance. Organ. Sci. 2008, 19, 143–159. [Google Scholar] [CrossRef]

- Aguinis, H.; Glavas, A. What we know and don’t know about corporate social responsibility: A review and research agenda. J. Manag. 2012, 38, 932–968. [Google Scholar] [CrossRef]

- Li, S.; Song, X.; Wu, H. Political Connection, Ownership Structure, and Corporate Philanthropy in China: A Strategic-Political Perspective. J. Bus. Ethics 2015, 129, 399–411. [Google Scholar] [CrossRef]

- Li, W.; Zhang, R. Corporate Ownership Interference: Evidence Social Responsibility, Structure, and Political from China. J. Bus. Ethics 2010, 96, 631–645. [Google Scholar] [CrossRef]

- Schuler, D.A.; Rehbein, K.; Cramer, R.D. Pursuing strategic advantage through political means: A multivariate approach. Acad. Manag. J. 2002, 45, 659–672. [Google Scholar] [CrossRef]

- Xin, K.K.; Pearce, J.L. Guanxi: Connections as substitutes for formal institutional support. Acad. Manag. J. 1996, 39, 1641–1658. [Google Scholar] [CrossRef]

- Park, S.H.; Luo, Y. Guanxi and organizational dynamics: Organizational networking in Chinese firms. Strateg. Manag. J. 2001, 22, 455–477. [Google Scholar] [CrossRef]

- Steidlmeier, P. Gift Giving, Bribery and Corruption: Ethical Management of Business Relationships in China. J. Bus. Ethics 1999, 20, 121–132. [Google Scholar] [CrossRef]

- Shleifer, A.; Vishny, R.W. Politicians and firms. Q. J. Econ. 1994, 109, 995–1025. [Google Scholar] [CrossRef]

- Fan, J.P.; Wong, T.J.; Zhang, T. Politically connected CEOs, corporate governance, and Post-IPO performance of China’s newly partially privatized firms. J. Financ. Econ. 2007, 84, 330–357. [Google Scholar] [CrossRef]

- Fan, J.P.; Rui, O.M.; Zhao, M. Public governance and corporate finance: Evidence from corruption cases. J. Comp. Econ. 2008, 36, 343–364. [Google Scholar] [CrossRef]

- Jo, H.; Kim, H.; Park, K. Corporate environmental responsibility and firm performance in the financial services sector. J. Bus. Ethics 2015, 131, 257–284. [Google Scholar] [CrossRef]

- Wood, D.J.; Jones, R.E. Stakeholder mismatching: A theoretical problem in empirical research on corporate social performance. Int. J. Organ. Anal. 1995, 3, 229–267. [Google Scholar] [CrossRef]

- Zhang, R.; Zhu, J.; Yue, H.; Zhu, C. Corporate philanthropic giving, advertising intensity, and industry competition level. J. Bus. Ethics 2010, 94, 39–52. [Google Scholar] [CrossRef]

- Godfrey, P.C. The relationship between corporate philanthropy and shareholder wealth: A risk management perspective. Acad. Manag. Rev. 2005, 30, 777–798. [Google Scholar] [CrossRef]

- Du, X.Q.; Chang, Y.; Zeng, Q.; Du, Y.; Pei, H. Corporate environmental responsibility (CER) weakness, media coverage, and corporate philanthropy: Evidence from China. Asia Pac. J. Manag. 2016, 33, 551–581. [Google Scholar] [CrossRef]

- Wei, S.J. Why Is Corruption So Much More Taxing Than Tax? Arbitrariness Kills; National Bureau of Economic Research: Cambridge, MA, USA, 1997. [Google Scholar]

- Beck, P.J.; Maher, M.W. A comparison of bribery and bidding in thin markets. Econ. Lett. 1986, 20, 1–5. [Google Scholar] [CrossRef]

- Lien, D.H.D. A note on competitive bribery games. Econ. Lett. 1986, 22, 337–341. [Google Scholar] [CrossRef]

- Jiang, G.; Wang, H. Should earnings thresholds be used as delisting criteria in stock market? J. Account. Public Policy 2008, 27, 409–419. [Google Scholar] [CrossRef]

- Du, X.Q. Does Religion Matter to Owner-Manager Agency. J. Bus. Ethics 2013, 118, 319–347. [Google Scholar] [CrossRef]

- Brammer, S.; Millington, A. Firm size, organizational visibility and corporate philanthropy: An empirical analysis. J. Bus. Ethics 2006, 15, 6–19. [Google Scholar] [CrossRef]

- Adams, M.; Hardwick, P. An analysis of corporate donations: United Kingdom evidence. J. Manag. Stud. 1998, 35, 641–654. [Google Scholar] [CrossRef]

- Williams, R.J. Women on corporate boards of directors and their influence on corporate philanthropy. J. Bus. Ethics 2003, 42, 1–10. [Google Scholar] [CrossRef]

- Wang, X.L.; Fan, G.; Yu, J.W. Marketization Index of China’s Provinces: Neri Report 2016; Social Science Academic Press: Beijing, China, 2016; pp. 3–16. ISBN 978-7-52-010022-9. (In Chinese) [Google Scholar]

- Cull, R.; Xu, L.C. Institutions, ownership, and finance: The determinants of profit reinvestment among Chinese firms. J. Financ. Econ. 2005, 77, 117–146. [Google Scholar] [CrossRef]

- Jia, N. Are collective political actions and private political actions substitutes or complements? Empirical evidence from China’s private sector. Strateg. Manag. J. 2014, 35, 292–315. [Google Scholar] [CrossRef]

- Cole, M.A.; Elliott, R.J.R.; Zhang, J. Corruption, Governance and FDI Location in China: A Province-Level Analysis. J. Dev. Stud. 2009, 45, 1494–1512. [Google Scholar] [CrossRef]

- Roberts, P.W.; Dowling, G.R. Corporate reputation and sustained superior financial performance. Strateg. Manag. J. 2002, 23, 1077–1093. [Google Scholar] [CrossRef]

- Gao, Y.Q.; Hafsi, T. Political dependence, social scrutiny, and corporate philanthropy: Evidence from disaster relief. Bus. Ethics Eur. Rev. 2017, 26, 189–203. [Google Scholar] [CrossRef]

- Du, X.Q.; Jian, W.; Du, Y.; Feng, W.; Zeng, Q. Religion, the Nature of Ultimate Owner, and Corporate Philanthropic Giving: Evidence from China. J. Bus. Ethics 2014, 123, 235–256. [Google Scholar] [CrossRef]

- Oh, W.Y.; Chang, Y.K.; Cheng, Z. When CEO career horizon problems matter for corporate social responsibility: The moderating roles of industry-level discretion and blockholder ownership. J. Bus. Ethics 2016, 133, 279–291. [Google Scholar] [CrossRef]

- Ryan, T.Y. Modern Regression Analysis; Wiley: New York, NY, USA, 1997; pp. 97–105. [Google Scholar]

- Branco, M.C.; Rodrigues, L.L. Corporate social responsibility and resource-based perspectives. J. Bus. Ethics 2006, 69, 111–132. [Google Scholar] [CrossRef]

- Scott, W.R. Institutions and Organizations, 3rd ed.; Sage: Thousand Oaks, CA, USA, 2008; pp. 35–46. [Google Scholar]

- Zucker, L.G. Institutional theories of organization. Ann. Rev. Sociol. 1987, 13, 443–464. [Google Scholar] [CrossRef]

- Jamali, D.; Neville, B. Convergence versus divergence of CSR in developing countries: An embedded multi-layered institutional lens. J. Bus. Ethics 2011, 102, 599–621. [Google Scholar] [CrossRef]

- Schnietz, K.E.; Epstein, M.J. Exploring the Financial Value of a Reputation for Corporate Social Responsibility during a Crisis. Corp. Reput. Rev. 2005, 7, 327–345. [Google Scholar] [CrossRef]

- Williams, R.J.; Barrett, J.D. Corporate philanthropy, criminal activity, and firm reputation: Is there a link? J. Bus. Ethics 2000, 26, 341–350. [Google Scholar] [CrossRef]

{kind=link}

| Characteristics | Max | Min | Mean | Number of Observations | % of Total N |

|---|---|---|---|---|---|

| Donation | |||||

| Have | 1 | 1 | 1 | 8034 | 67.07 |

| Not have | 0 | 0 | 0 | 3944 | 32.93 |

| Donation amount (log) | 20.26 | 0 | 8.43 | 11,978 | 100 |

| Firm size (log) | 30.57 | 15.58 | 21.86 | 11,978 | 100 |

| Firm age | 33 | 1 | 13.05 | 11,978 | 100 |

| Leverage (%) | 1.27 | 0.01 | 0.45 | 11,978 | 100 |

| Stateshare | |||||

| Have | 1 | 1 | 1 | 3542 | 29.57 |

| Not have | 0 | 0 | 0 | 8436 | 70.43 |

| Stateshare amount (%) | 0.92 | 0 | 0.09 | 11,978 | 100 |

| ROA (%) | 0.94 | −0.10 | 0.05 | 11,978 | 100 |

| GDP (log) | 11.04 | 5.98 | 9.95 | 11,978 | 100 |

| Environment | |||||

| Have | 1 | 1 | 1 | 1763 | 14.72 |

| Not have | 0 | 0 | 0 | 10,215 | 85.28 |

| Environment amount | 0 | 672 | 1.39 | 11,978 | 100 |

| NERI | 11.80 | −0.30 | 7.60 | 11,978 | 100 |

| Corruption | 46.30 | 2.65 | 22.76 | 11,978 | 100 |

| Variables | Mean | SD | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 1 | Donation | 8.43 | 6.15 | 1 | |||||||||

| 2 | Firm size | 21.86 | 1.43 | 0.18 | 1 | ||||||||

| 3 | Firm age | 13.05 | 5.21 | −0.02 | 0.15 | 1 | |||||||

| 4 | Leverage | 0.45 | 0.22 | 0.08 | 0.52 | 0.28 | 1 | ||||||

| 5 | Stateshare | 0.09 | 0.18 | 0.03 | 0.20 | −0.07 | 0.12 | 1 | |||||

| 6 | ROA | 0.05 | 0.07 | 0.08 | −0.11 | −0.18 | −0.40 | −0.02 | 1 | ||||

| 7 | GDP | 9.95 | 0.76 | −0.02 | −0.04 | −0.01 | −0.12 | −0.20 | 0.07 | 1 | |||

| 8 | Environment | 1.39 | 9.26 | 0.05 | 0.18 | 0.02 | 0.05 | 0.01 | 0.01 | 0.01 | 1 | ||

| 9 | NERI | 7.60 | 1.89 | 0.04 | −0.02 | −0.09 | −0.07 | −0.06 | 0.07 | 0.58 | −0.01 | 1 | |

| 10 | Corruption | 22.76 | 6.64 | 0.01 | −0.10 | 0.10 | 0.07 | 0.01 | −0.08 | −0.03 | −0.03 | −0.03 | 1 |

| Variables | Model 1 β (SE) | Model 2 β (SE) | Model 3 β (SE) | Model 4 β (SE) | Model 5 β (SE) |

|---|---|---|---|---|---|

| Constant | −185.30 (207.13) | −170.39 (208.15) | −188.79 (207.38) | −172.04 (207.98) | −190.75 (207.17) |

| Firm size | 0.91 *** (0.05) | 0.89 *** (0.05) | 0.88 *** (0.05) | 0.88 *** (0.05) | 0.87 *** (0.05) |

| Firm age | −0.02 * (0.01) | −0.02 + (0.01) | −0.02 + (0.01) | −0.02 + (0.01) | −0.02 + (0.01) |

| Leverage | 0.50 (0.33) | 0.52 (0.33) | 0.54 (0.33) | 0.54 (0.33) | 0.55 + (0.33) |

| Stateshare | −0.68 * (0.32) | −0.67 * (0.32) | −0.67 * (0.32) | −0.67 * (0.32) | −0.66 * (0.32) |

| ROA | 9.35 *** (0.82) | 9.35 *** (0.82) | 9.33 *** (0.82) | 9.36 *** (0.82) | 9.33 *** (0.82) |

| GDP | −0.23 (0.77) | −0.19 (0.77) | −0.25 (0.77) | −0.18 (0.77) | −0.25 (0.77) |

| NERI | 0.75 *** (0.09) | 0.76 *** (0.09) | 0.75 *** (0.09) | 0.76 *** (0.09) | 0.75 *** (0.09) |

| Corruption | 0.18 *** (0.04) | 0.18 *** (0.04) | 0.18 *** (0.04) | 0.18 *** (0.04) | 0.18 *** (0.04) |

| Year dummy | Include | Include | Include | Include | Include |

| Environment | 0.01 + (0.01) | 0.02 ** (0.01) | 0.01 * (0.01) | 0.02 ** (0.01) | |

| Environment × NERI | −0.24 * (0.11) | −0.24 * (0.11) | |||

| Environment × Corruption | −0.21 * (0.10) | −0.21 * (0.10) | |||

| χ square | 729.24 (10) *** | 733.04 (11) *** | 737.10 (12) *** | 738.07 (12) *** | 742.22 (13) *** |

| ICC at province level | 0.39 | 0.39 | 0.39 | 0.39 | 0.39 |

| Variables | Model 1 β (SE) | Model 2 β (SE) | Model 3 β (SE) | Model 4 β (SE) | Model 5 β (SE) |

|---|---|---|---|---|---|

| Constant | −8.48 *** (1.34) | −8.20 *** (1.35) | −7.78 *** (1.35) | −8.11 *** (1.35) | −7.68 *** (1.36) |

| Firm size | 0.82 *** (0.05) | 0.81 *** (0.05) | 0.79 *** (0.05) | 0.80 *** (0.05) | 0.79 *** (0.05) |

| Firm age | −0.05 *** (0.01) | −0.05 *** (0.01) | −0.05 *** (0.01) | −0.05 *** (0.01) | −0.05 *** (0.01) |

| Leverage | 1.00 ** (0.32) | 1.02 ** (0.32) | 1.04 *** (0.32) | 1.03 *** (0.32) | 1.04 *** (0.32) |

| Stateshare | −1.77 *** (0.32) | −1.76 *** (0.32) | −1.76 *** (0.32) | −1.76 *** (0.32) | −1.75 *** (0.32) |

| ROA | 11.78 *** (0.81) | 11.78 *** (0.81) | 11.75 *** (0.81) | 11.78 *** (0.81) | 11.75 *** (0.81) |

| GDP | −0.10 (0.10) | −0.10 (0.10) | −0.11 (0.10) | −0.10 (0.10) | −0.11 (0.10) |

| NERI | −0.02 (0.04) | −0.02 (0.04) | −0.02 (0.04) | −0.02 (0.04) | −0.02 (0.04) |

| Corruption | 0.01 (0.01) | 0.01 (0.01) | 0.01 (0.01) | 0.01 (0.01) | 0.01 (0.01) |

| Year dummy | Include | Include | Include | Include | Include |

| Environment | 0.01 + (0.01) | 0.02 ** (0.01) | 0.01 + (0.01) | 0.02 ** (0.01) | |

| Environment × NERI | −0.30 ** (0.11) | −0.31 ** (0.11) | |||

| Environment × Corruption | −0.12 (0.10) | −0.12 (0.10) | |||

| F value | 110.08 *** | 102.46 *** | 96.17 *** | 95.74 *** | 90.27 *** |

| R square | 0.11 | 0.11 | 0.11 | 0.11 | 0.11 |

| Adjust R square | 0.11 | 0.11 | 0.11 | 0.11 | 0.11 |

© 2017 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Liu, W.; Wei, Q.; Huang, S.-Q.; Tsai, S.-B. Doing Good Again? A Multilevel Institutional Perspective on Corporate Environmental Responsibility and Philanthropic Strategy. Int. J. Environ. Res. Public Health 2017, 14, 1283. https://doi.org/10.3390/ijerph14101283

Liu W, Wei Q, Huang S-Q, Tsai S-B. Doing Good Again? A Multilevel Institutional Perspective on Corporate Environmental Responsibility and Philanthropic Strategy. International Journal of Environmental Research and Public Health. 2017; 14(10):1283. https://doi.org/10.3390/ijerph14101283

Chicago/Turabian StyleLiu, Wei, Qiao Wei, Song-Qin Huang, and Sang-Bing Tsai. 2017. "Doing Good Again? A Multilevel Institutional Perspective on Corporate Environmental Responsibility and Philanthropic Strategy" International Journal of Environmental Research and Public Health 14, no. 10: 1283. https://doi.org/10.3390/ijerph14101283