Appendix A. Extended Model Description

A more detailed description of the macroeconomic and technology framework is given in the following to extend the understanding of underlying assumptions and model features. For the CGE model, the description follows the model structure shown in

Figure 2 and sectoral model codes are used from

Table 2. A detailed algebraic representation and information on the basic model parameterization can be found in Bednar-Friedl et al. [

40,

41].

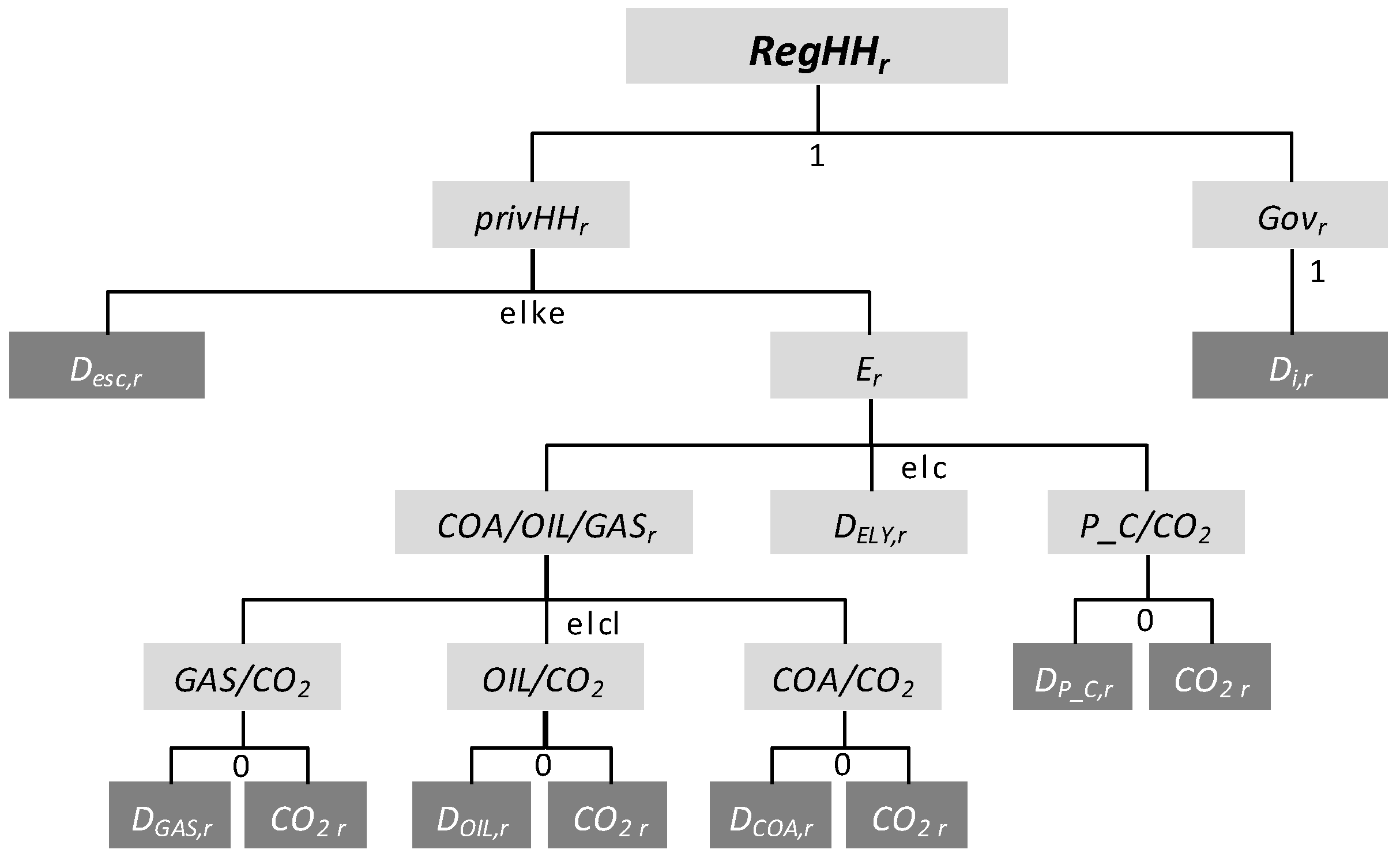

The income for the regional household (

RegHHr) in the CGE model is generated by the employment of the primary factors capital (

Kr), labor (

Lr), and natural resources (

Rr), as well as tax revenues. The regional household redistributes this income for the consumption of a representative private household (

pirvHHr) and the public consumption of the government (

Govr) with a unitary elasticity of substitution. Private consumption in each region is characterized by a constant elasticity of substitution between a material consumption bundle and an energy aggregate. Public consumption is modeled as a Cobb Douglas aggregate of an intermediate material consumption bundle. For this activity, a nested constant elasticity of substitution (CES) function with several levels is employed, which is shown in

Figure A1.

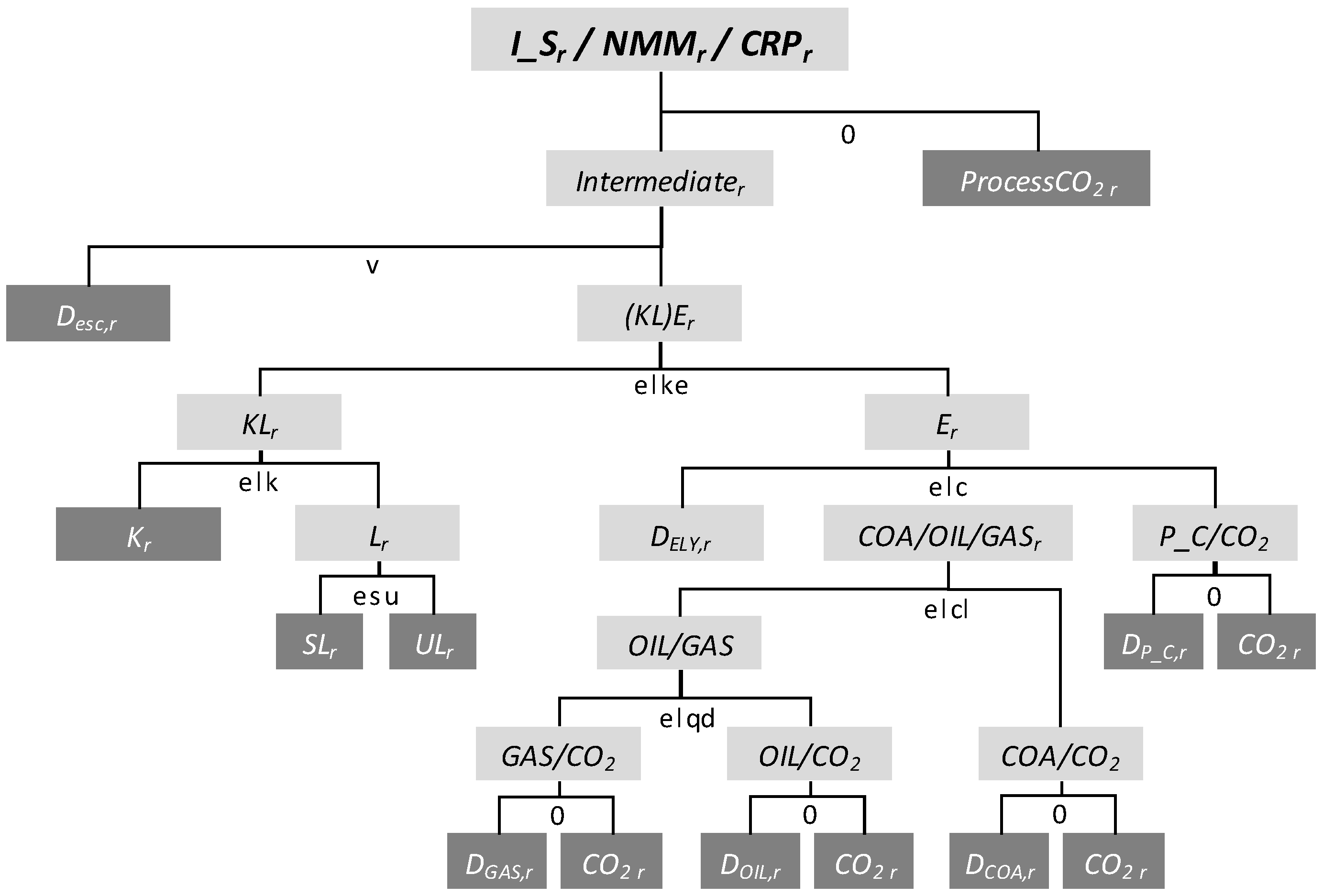

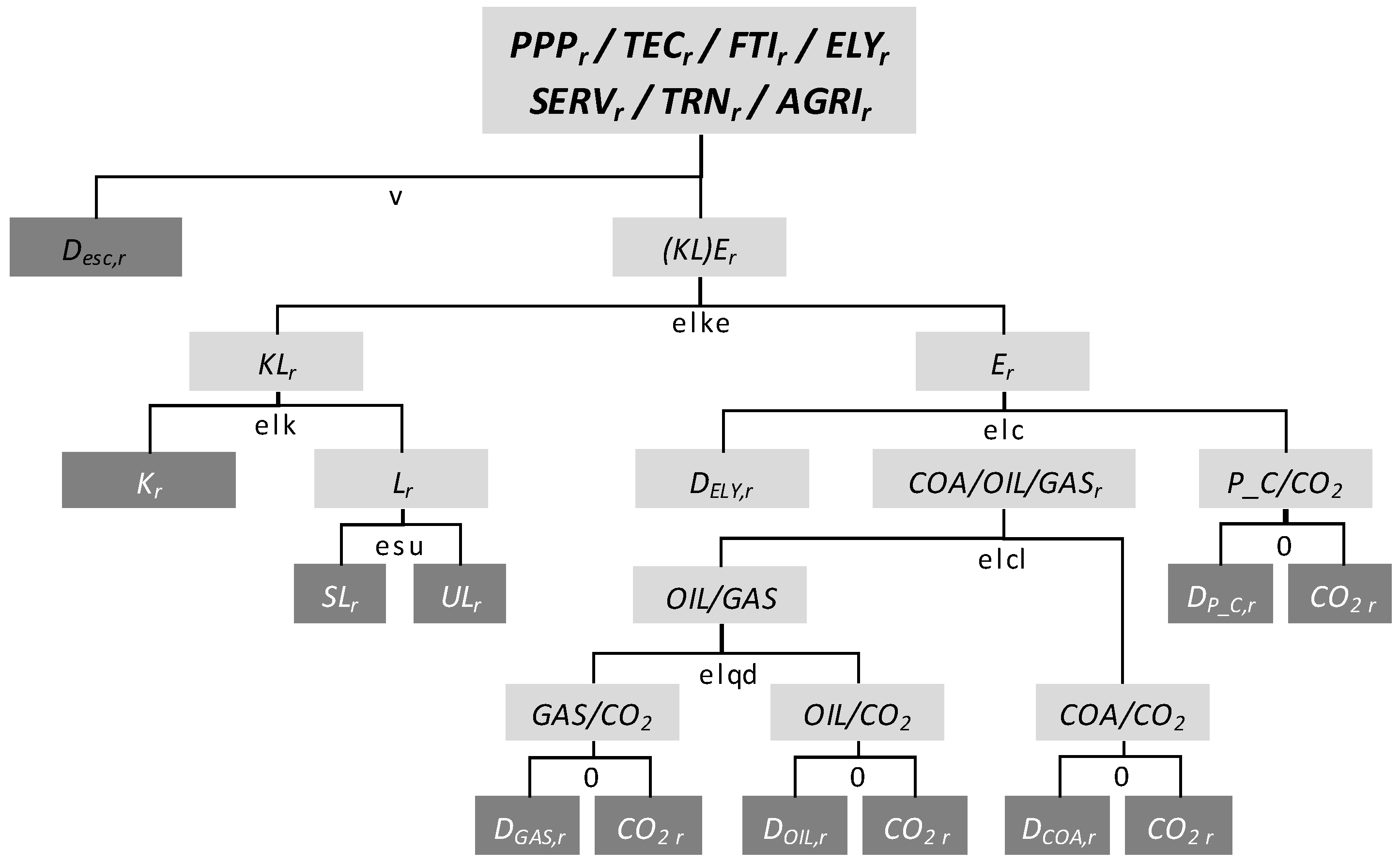

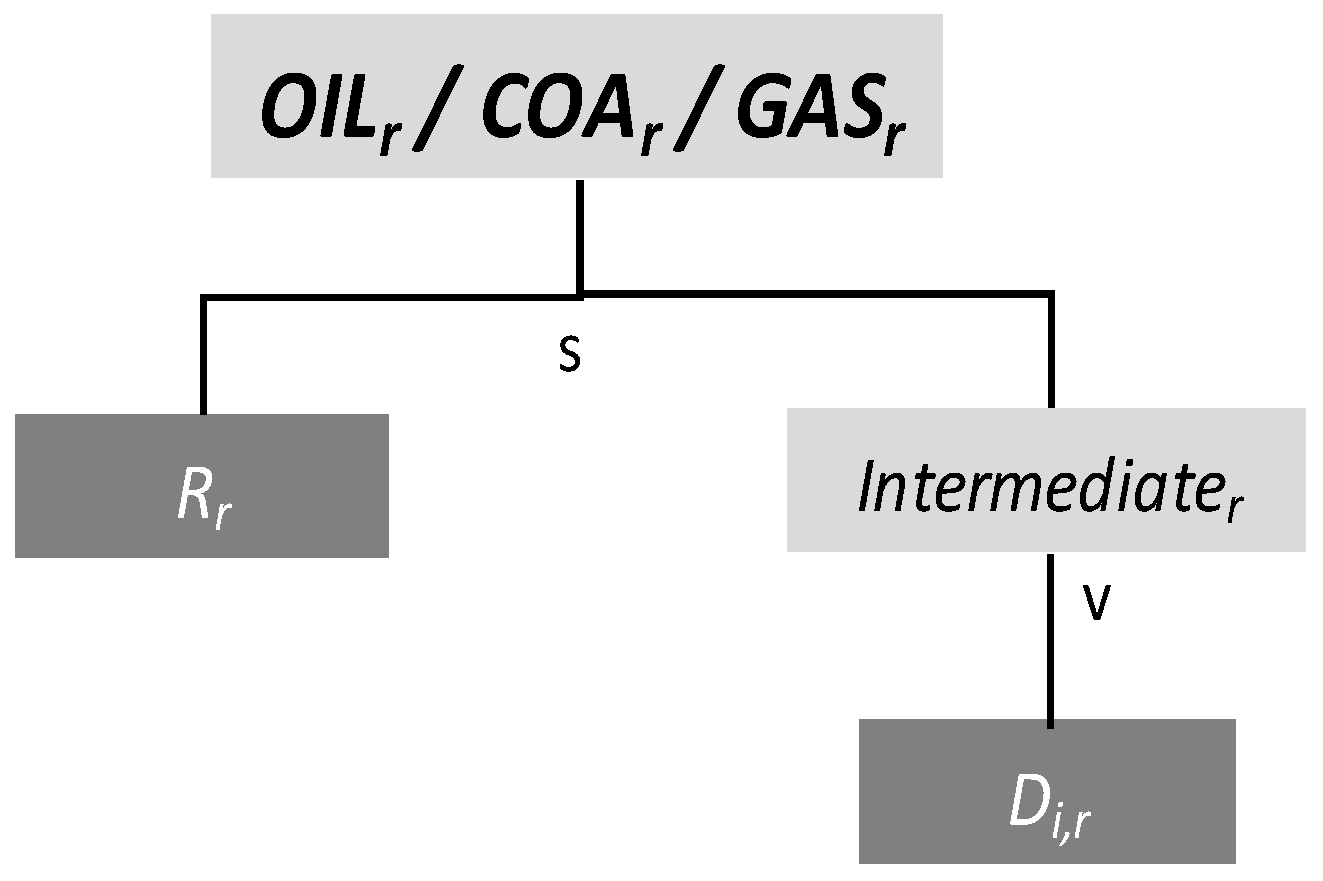

In the domestic production (

Yir), intermediate inputs and primary factors are used. The primary factors labor and capital are mobile across sectors within a region but immobile between regions. The natural resource (

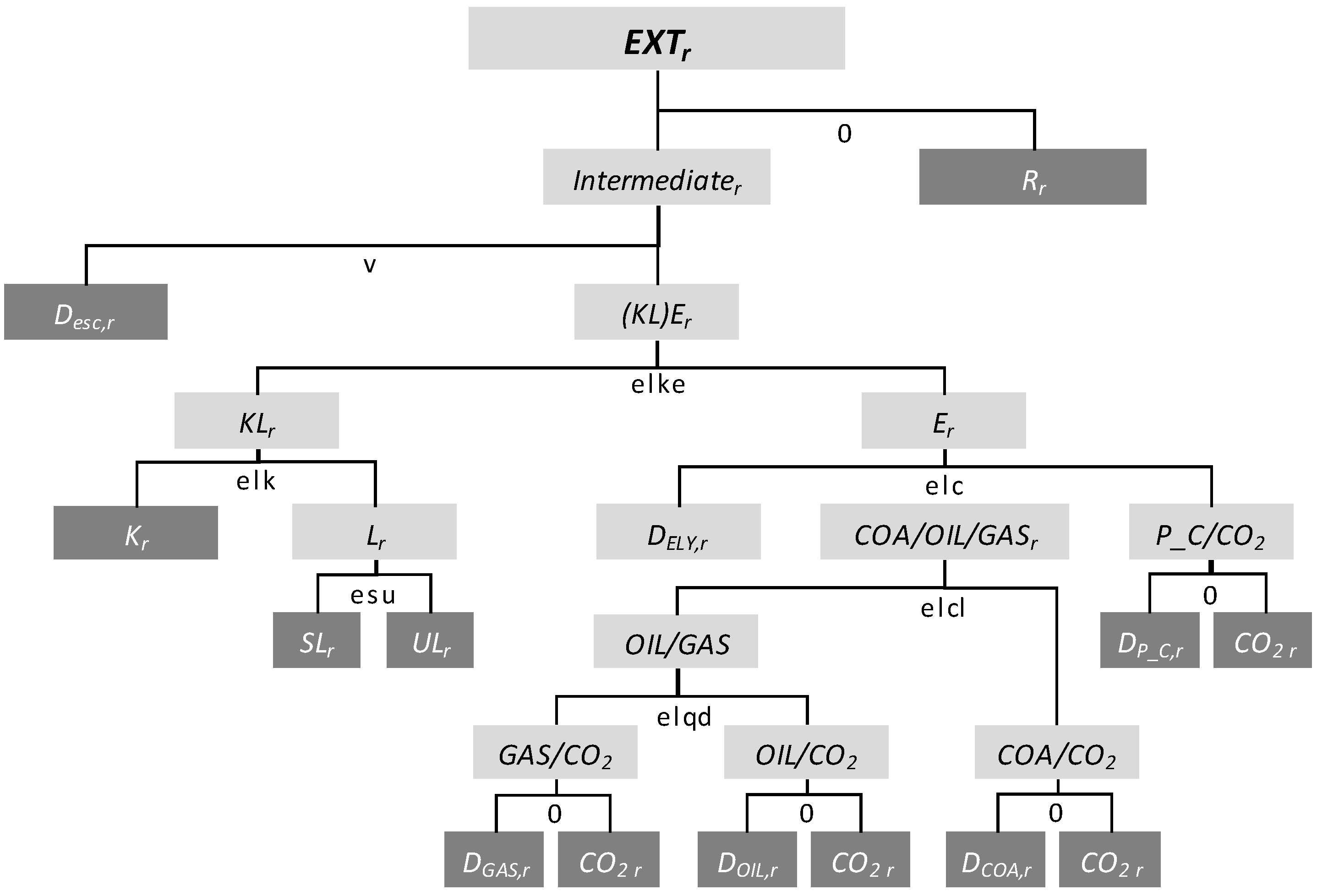

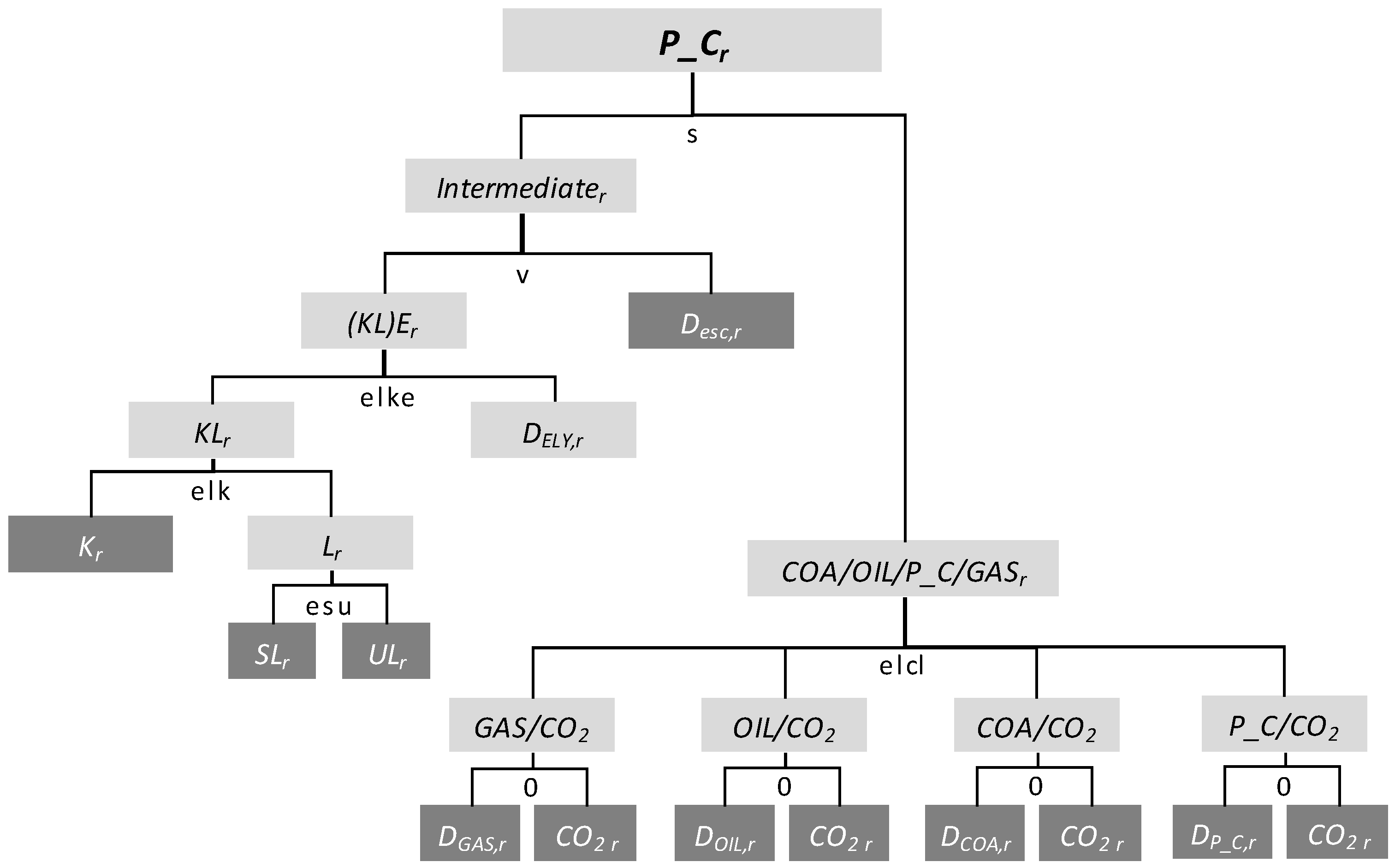

Rr) input is used only in the extraction of primary energy (COA, OIL, and GAS) and Other Extraction (EXT). Again, nested CES production functions are used for the representation of substitution possibilities in domestic production between the primary inputs (capital, labor, and natural resources), intermediate energy and material inputs as well as substitutability between energy commodities (primary and secondary). The domestic production activities Y

ir are differentiated in three nesting-types of production sectors: (i) non-resource using commodity production (comprising EIS and other NEIS sectors); (ii) resource using (primary energy) extraction sectors; and (iii) the production in the Petroleum sector. The first type of non-resource using production is further divided into production structures that produce process emissions (

Figure A2) and those that do not (

Figure A3). In addition, the second type of production sectors is represented by the structure of Coal, Crude Oil and Natural Gas production (

Figure A4) as well as the Other Extraction sector (

Figure A5). Finally, in the Petroleum sector (P_C) the fossil fuel inputs GAS, OIL, COA and P_C are nested in a Leontief type at the top nesting level to all other inputs (i.e., they are characterized by zero elasticity of substitution) such that production cannot substitute away from energy inputs (

Figure A6).

Figure A1.

Nesting structure of the regional household demand in the CGE model.

Figure A1.

Nesting structure of the regional household demand in the CGE model.

Figure A2.

Nesting structure of non-resource using sectors with combustion and process emissions in production in the CGE model.

Figure A2.

Nesting structure of non-resource using sectors with combustion and process emissions in production in the CGE model.

Figure A3.

Nesting structure of non-resource using sectors without process emissions in production in the CGE model.

Figure A3.

Nesting structure of non-resource using sectors without process emissions in production in the CGE model.

Figure A4.

Nesting structure of the resource using fossil fuel sectors without process emissions in production in the CGE model.

Figure A4.

Nesting structure of the resource using fossil fuel sectors without process emissions in production in the CGE model.

Figure A5.

Nesting structure of resource using Other Extraction sector without process emissions in production in the CGE model.

Figure A5.

Nesting structure of resource using Other Extraction sector without process emissions in production in the CGE model.

Figure A6.

Nesting structure of Petroleum (P_C) sector without process emissions in production in the CGE model.

Figure A6.

Nesting structure of Petroleum (P_C) sector without process emissions in production in the CGE model.

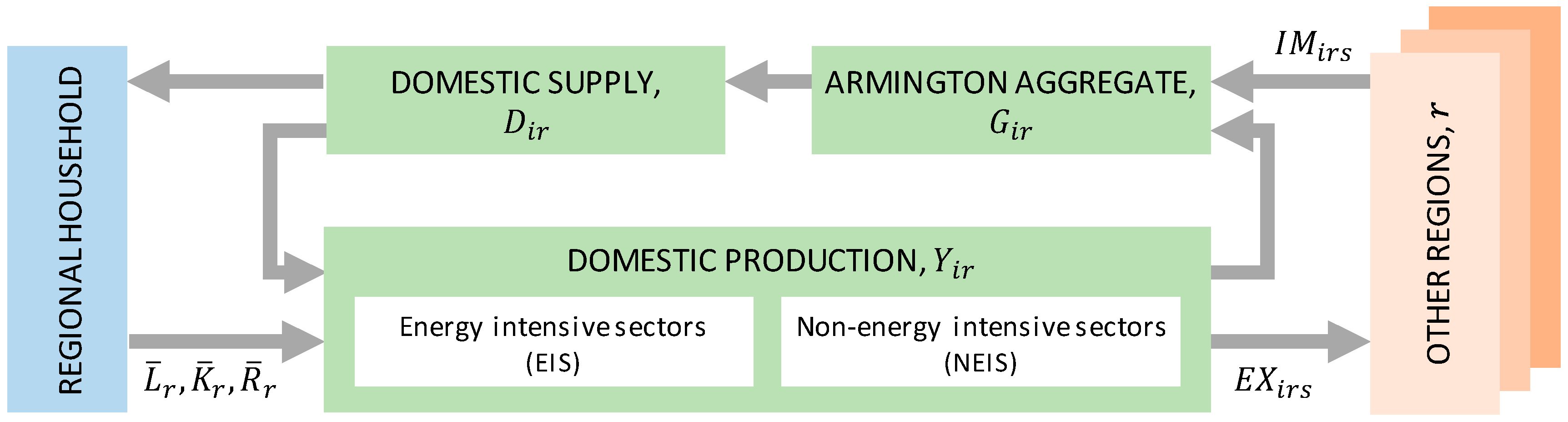

International trade between the 13 regions follows the Armington hypothesis [

58], according to which domestic and imported goods are treated as imperfect substitutes. The Armington aggregate

Gir is thus implemented as a CES function of domestic production

Yir and imported goods

IMirs. The output of the Armington aggregate enters the domestic supply

Dir, which in turn is used to satisfy final household demand and intermediate demand in production. Each sectoral import of one region from another region corresponds to the respective sectoral export flow of the other region, originating from its domestic production

Yir.

CO

2 emissions are covered in the CGE model both for production and consumption activities. They are differentiated into combustion and industrial process emissions. The combustion of fossil fuels is modeled as a fixed composite of fossil fuel input and CO

2 emission with a fuel specific carbon coefficient. In the three production sectors of Iron and Steel, Non-metallic Minerals and Chemicals industrial process emissions are covered by nesting emissions as Leontief input at the top level of the CES function nesting tree as shown in

Figure A2.

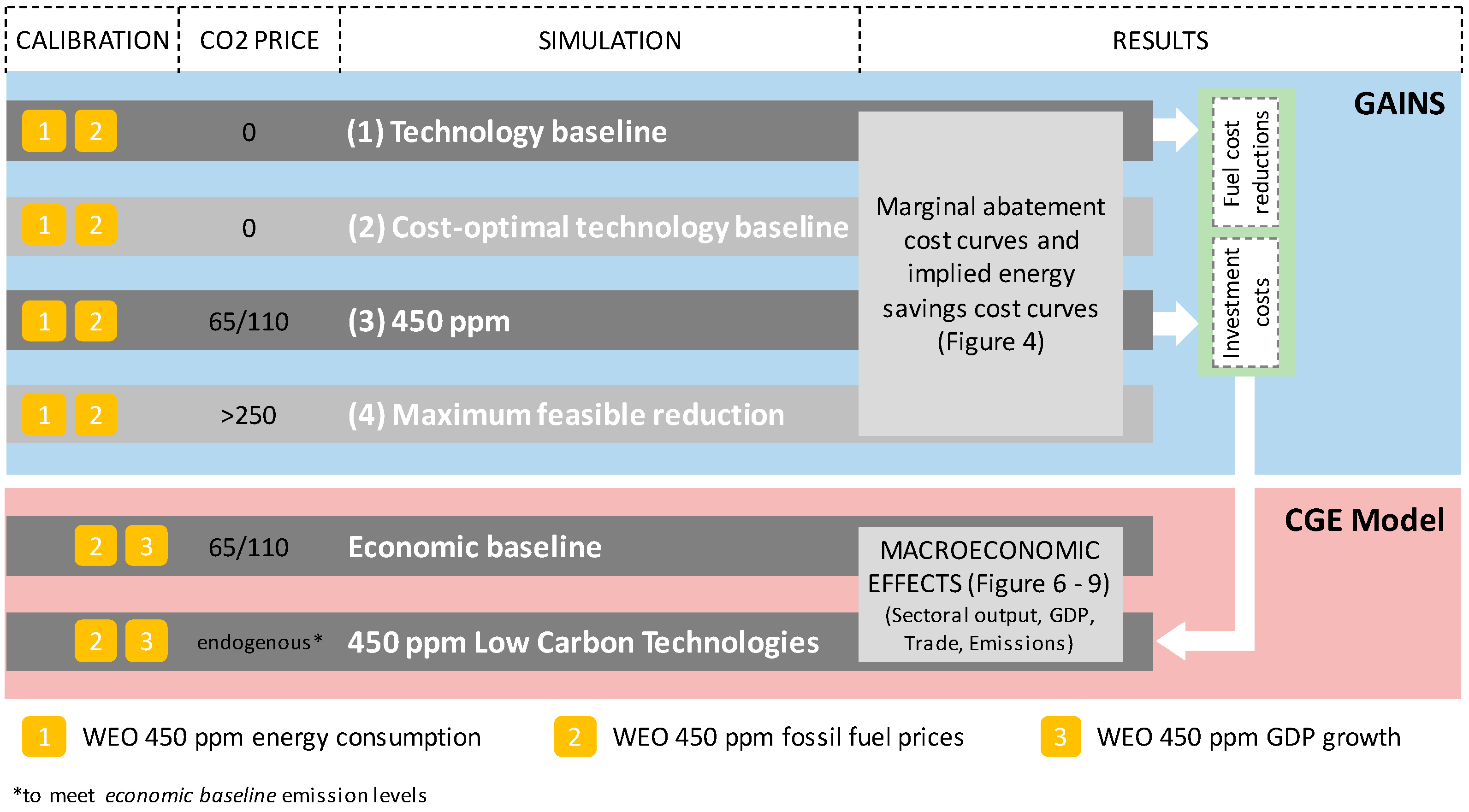

The GAINS model is an integrated assessment model of air pollution and GHG mitigation that covers all sectors of the economy in around 180 regions of the world. The model can be used in a number of different ways, with a focus on economy-wide or sectoral aspects. For example, it can be used calculate sectoral and national/regional/global emissions from an exogenously given energy scenario, such as the WEO. Most pertinent for the current context of industrial emissions, it can also be used to separate the WEO assumptions on projections of production volumes of industrial products from the corresponding average energy intensity per unit of product

for major products

in the energy intensive industries:

For the present purposes, further enrich the average energy-intensity

with independent analysis of energy efficiency and cost information of individual technologies, which can be grouped into technology packages. Thus,

can be expressed as resulting from a mix of technology packages

, each of which is represented by an implementation rate or weight

:

In practice, we define package for product as the set of technologies that describe energy intensity by product in the base year, i.e., for all products in the base year, and the other packages describe improvements in this efficiency: in particular, package 1 describes the implication for the average energy intensity across a region of switching off smaller, inefficient production facilities; package 2 represents the implications of reaching the national energy efficiency frontier (best practice at the national level) in all facilities; and package 3 represents reaching the international energy efficiency frontier. As more energy efficient technologies are adopted over time or as a result of a policy intervention, the weights (proxies for levels of implementation) of the more efficient technologies increase and the overall efficiency increases. Simultaneously, because each package is associated with a well-defined unit cost for implementation (which itself is a function of (annualized) investment costs, operating and maintenance costs and fuel costs saved), the change in implementation rates is associated with a change in implementation costs.

In a third step the GAINS model can be used to identify cost-effective strategies to respond to an exogenous policy intervention, in this case a carbon price. For this we set up a linear programming-optimization in which the objective that is minimized is the implementation costs of energy efficiency technologies summed over all subsectors and products, plus the carbon price revenues (carbon price times emissions). The independent variables in this optimization problem are the implementation rates of the efficiency packages, which are subject to the obvious constraint that they sum up to 100% for each product in each subsector, and may be subjective to additional constraints (for example, a share of installations may not be upgradable).

To illustrate the level of disaggregation and detail of input parameters,

Table A1 shows—for China—the historical and projected production numbers for the major products in the respective energy intensive industries (products not listed here are subsumed in a category “other” for each subsector, whose trend in production volumes is inferred from the value-added projections for the subsectors).

Table A1.

Statistical data and projection of production volumes of the industrial products modeled here for the case of China. Source: [

52] and own.

Table A1.

Statistical data and projection of production volumes of the industrial products modeled here for the case of China. Source: [52] and own.

| Sector/Product | Unit | 2005 | 2010 | 2020 | 2030 |

|---|

| Iron and Steel industry |

| Coke | 106 tons | 254.1 | 390.2 | 323.9 | 209.0 |

| Sinter and pellets | 106 tons | 427.8 | 642.2 | 521.0 | 448.3 |

| Pig iron | 106 tons | 343.8 | 516.1 | 418.7 | 360.3 |

| Basic oxygen steel | 106 tons | 295.4 | 443.2 | 359.6 | 309.4 |

| Electric arc steel | 106 tons | 57.6 | 86.4 | 70.1 | 60.3 |

| Casting rolling finishing | 106 tons finished products | 335.3 | 503.1 | 421.0 | 362.3 |

| Coal production and refineries |

| Coal production | 106 tons | 2204.7 | 2584.6 | 3729.2 | 4270.2 |

| Oil refineries | 106 tons oil input | 198.4 | 224.9 | 301.5 | 370.0 |

| Chemicals industry |

| Ammonia | 106 tons | 40.4 | 49.6 | 68.4 | 91.9 |

| Ethylene | 106 tons | 12.2 | 15.0 | 29.0 | 38.9 |

| Chlorine | 106 tons | 14.4 | 17.7 | 24.9 | 33.5 |

| Non-metallic mineral industry |

| Cement | 106 tons | 1065.8 | 1700.0 | 1456.2 | 1403.0 |

| Lime | 106 tons | 150.9 | 152.0 | 154.7 | 158.0 |

| Bricks | 106 tons | 1040.0 | 1460.0 | 1500.0 | 1500.0 |

| Non-ferrous metals industry |

| Primary aluminum | 106 tons | 8.5 | 12.5 | 14.5 | 13.0 |

| Secondary aluminum | 106 tons | 0.1 | 0.1 | 0.1 | 0.1 |

| Other metals—primary | 106 tons | 8.6 | 11.5 | 12.0 | 12.0 |

| Other metals—secondary | 106 tons | 8.6 | 11.5 | 12.0 | 12.0 |

| Pulp and Paper industry |

| Pulp from wood | 106 tons | 10.4 | 15.5 | 18.0 | 18.4 |

| Pulp from recovered paper | 106 tons | 6.9 | 15.5 | 33.5 | 34.1 |

| Paper and paperboard | 106 tons | 14.4 | 25.8 | 42.9 | 43.7 |

Table A2 shows, for two selected products/production processes of the Iron and Steel industry in China, the energy intensity for different energy carriers and the resulting total for the packages described above. Package 0 represents the average energy efficiency in 2005, and packages 1 to 3 represent clusters of technological measures that reduce the energy intensity at constant output.

Table A2.

Energy intensity per unit of output for two selected products in the Iron and Steel sector in China for different energy carriers.

Table A2.

Energy intensity per unit of output for two selected products in the Iron and Steel sector in China for different energy carriers.

| Energy Intensity (GJ per Unit) | Package 0 | Package 1 | Package 2 | Package 3 |

|---|

| Pig iron production |

| Fuels | 10.5 | 9.5 | 8.6 | 8.0 |

| Steam hot water | 0.0 | 0.0 | 0.0 | 0.0 |

| Electricity | 0.9 | 0.7 | 0.6 | 0.5 |

| Total | 11.4 | 10.2 | 9.2 | 8.5 |

| Electric arc steel |

| Fuels | 1.4 | 1.2 | 1.0 | 0.9 |

| Steam hot water | 0.0 | 0.0 | 0.0 | 0.0 |

| Electricity | 2.6 | 2.2 | 1.9 | 1.7 |

| Total | 4.0 | 3.4 | 2.9 | 2.6 |

Table A3 illustrates the corresponding cost parameters for the efficiency packages for these two processes. Since we are only interested in costs in addition to baseline costs, we only report investment costs over the Package 0 costs. Differences in operating and maintenance costs can also reflect productivity changes, and these have been reflected to the extent they are included in the more disaggregated marginal cost curves that assume constant output. Regional differences in investment costs are marginal.

Table A3.

Cost parameters for the energy efficiency packages discussed in the text above. Since no technological cost learning effect is assumed, these cost parameters are used also for 2030.

Table A3.

Cost parameters for the energy efficiency packages discussed in the text above. Since no technological cost learning effect is assumed, these cost parameters are used also for 2030.

| Efficiency Package/Cost Parameter | Unit | Package 0 | Package 1 | Package 2 | Package 3 |

|---|

| Pig iron production |

| Capital investments (INV) | $/unit | - | 4.1 | 30.5 | 73.0 |

| O + M (fixed) | % INV | - | 5.0% | 5.0% | 5.0% |

| Electric arc steel |

| Capital investments (INV) | $/unit | - | 7.1 | 16.4 | 54.0 |

| O + M (fixed) | % INV | - | 0.0% | 0.0% | 0.0% |

Finally,

Table A4 illustrates our assumed implementation rates of the different packages for selected products in the 2030

technology baseline for China. These implementation rates reflect the reduction in energy intensity autonomously and as a result of non-carbon policies in the

technology baseline. In conjunction with the above energy intensities and production volumes, they are consistent with the projected WEO 2009 baseline energy consumption. For India and Europe, processes and energy efficiency packages are not fundamentally different, rather the implementation rates are different (e.g., in Europe zero share for Package 0), reflecting different baseline intensities. Consequently, the remaining per unit potentials for further improvement differ by region. In addition, production volumes differ across regions and products. These differences, taken together, explain the differences in abatement cost curves across regions.

Table A4.

Examples of implementation rates of energy efficiency packages in China in the 2030 technology baseline for selected products of the Iron and Steel industry.

Table A4.

Examples of implementation rates of energy efficiency packages in China in the 2030 technology baseline for selected products of the Iron and Steel industry.

| Efficiency Package | Package 0 | Package 1 | Package 2 | Package 3 |

|---|

| Pig iron production | 50% | 35% | 10% | 5% |

| Electric arc steel | 60% | 30% | 10% | 0% |

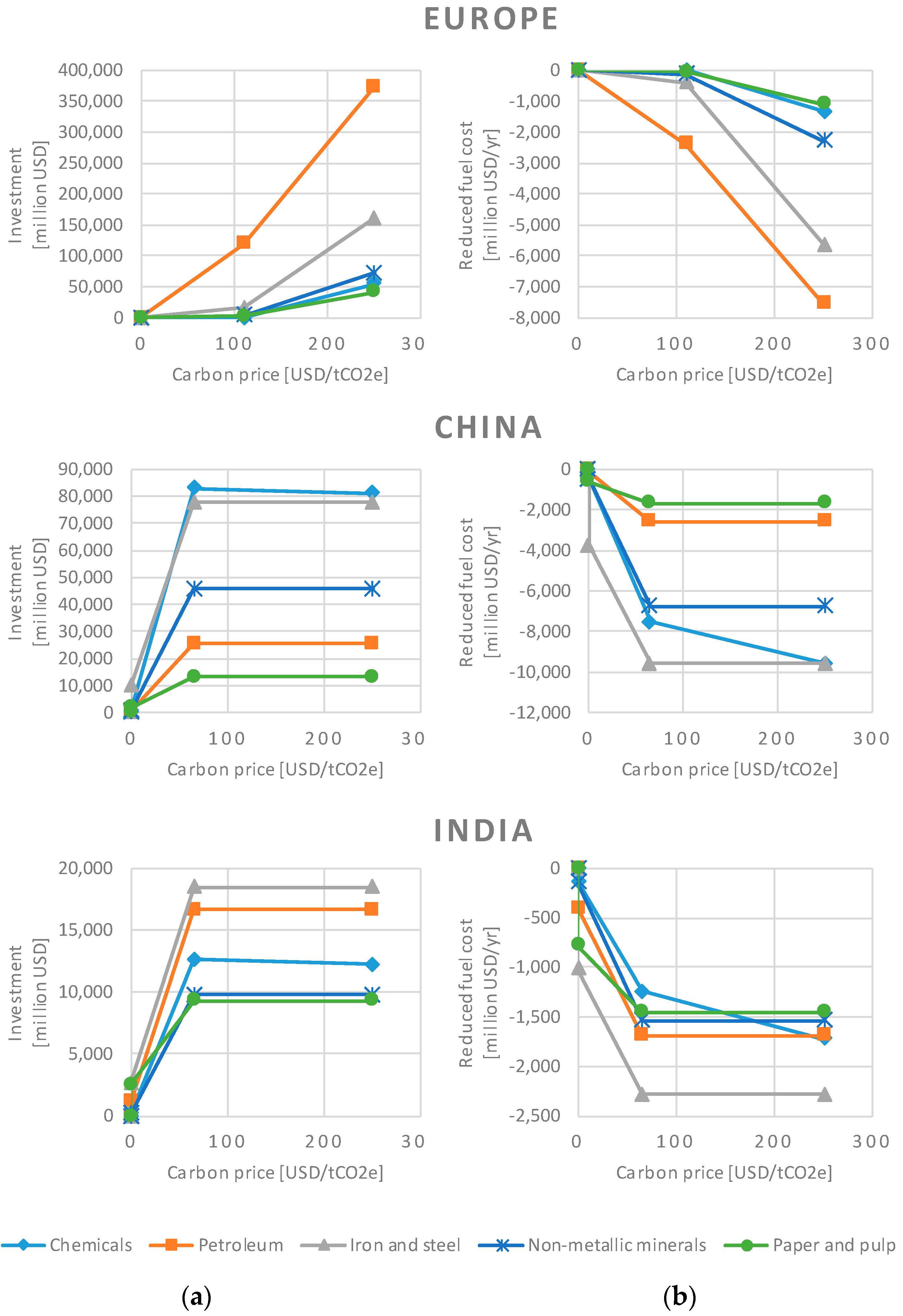

Note that the implied cost saving resulting from reduced energy intensity for the higher packages can be inferred from the above energy intensities (

Table A1), production volumes, implementation rates and scenario energy prices. Investment requirements are calculated from production volumes, implementation rates and unit investment costs. In the presence of a carbon price the implementation rates change, and the cost-effective levels are determined with an LP-optimization. The results of these calculations are summarized in

Figure 3 and

Figure 4.

Technology parameters listed in

Table A2,

Table A3 and

Table A4 were discussed with and reviewed by experts in Europe, India and China. In particular, for Europe the GAINS model has benefited from a peer review process in the run up to the policy assessment process leading to the Revision of the Gothenburg Protocol and the Thematic Strategy for Air Pollution of the EU, for both of which the GAINS model was the modeling tool of choice. Many parameters were directly taken or derived from the PRIMES model [

59]. For the India and China parts IIASA had subcontracted local experts to review the above methodology and to provide updated parameters. In addition, Zhang et al. [

56] provided input from own independent analyses. Cost figures have a local and a world market component (except in cases where no specific information was available), reflecting the fact that (parts of) the technologies are developed and manufactured locally, using local labor and resource costs, while other parts have to be purchased at world market prices. This, and different requirements for the technologies (e.g., different air pollution control requirements), explain cost differentials between technologies in different regions.

Autonomous technological improvement is already reflected in the WEO as decreasing average energy intensities for the individual products over time. In GAINS, this is represented by increasing implementation rates of the higher stage packages. No technological learning is assumed here, in the sense that the unit costs for the technology packages and their energy efficiency stay constant over time. While this may be a relatively conservative assumption, the impact of learning in these mature industries is considered relatively small, compared to younger industries such as those producing, for instance, computer hardware or solar PV modules.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}