3.1. Sensitivity of Investment Demand to Feed-in Tariffs Prices for Onshore Wind Electricity Generation from Renewable Energy Sources Projects

The analysis begins by quantifying the corresponding PI, using the set of parameters and equations defined in

Section 2.1. The benchmark project for this section concerns an interconnected (mainland) wind farm with an installed capacity of 3.6 MW (e.g., consisting of two wind turbines with a nominal capacity of 1.8 MW, each). The contributions of each capital source to the initial investment expenditure are assumed as follows:

- ▪

Until 2006: A 40% public subsidy (grant) of the total eligible RES-E investment cost, equity capital equal to 40% of the total investment cost and 40% subsidy of the interest of the loan (20%) obtained for the purpose of financing the investment;

- ▪

From 2006 to 2010: A 40% public subsidy and equity capital equal to 25% of the total investment cost;

- ▪

From 2010 onwards: The equity capital covers 25% of the total investment cost. The rest is covered by a loan (75%), and the FIT are increased by 20%

It is also assumed that the investors secure a loan with a 10 year duration and a 7% interest rate. The cost of equity is 10%. According to data from the Greek operator of electricity market [

22], the average annual capacity factor for interconnected wind RES-E farms is 25%. Furthermore, the operating and maintenance cost is assumed to be equal to 3.7% of the total investment cost per annum. The depreciation expense is assumed to be equal to 5% of the total investment cost per annum. We assume that the corporate tax rate remains at 25% during the project’s operation and that inflation rises at the rate of 2% annually. The project duration is 20 years, and the salvage value is assumed to be zero.

The values of the PI for the years from 2001 to 2012 are presented in

Table 8 (note: the value 12.7 in 2001 means that the MIRR was 12.7%).

Table 8.

The profitability index (PI) for an interconnected onshore wind farm from 2001 to 2012.

Table 8.

The profitability index (PI) for an interconnected onshore wind farm from 2001 to 2012.

| Profitability Index (PI) for an Interconnected on Shore Wind Farm from 2001 to 2012 |

|---|

| Year | 2001 | 2002 | 2003 | 2004 | 2005 | 2006 | 2007 | 2008 | 2009 | 2010 | 2011 | 2012 |

| PI | 12.7 | 12.7 | 13.7 | 15.0 | 14.8 | 13.5 | 13.6 | 14.0 | 14.1 | 14.9 | 15.0 | 15.1 |

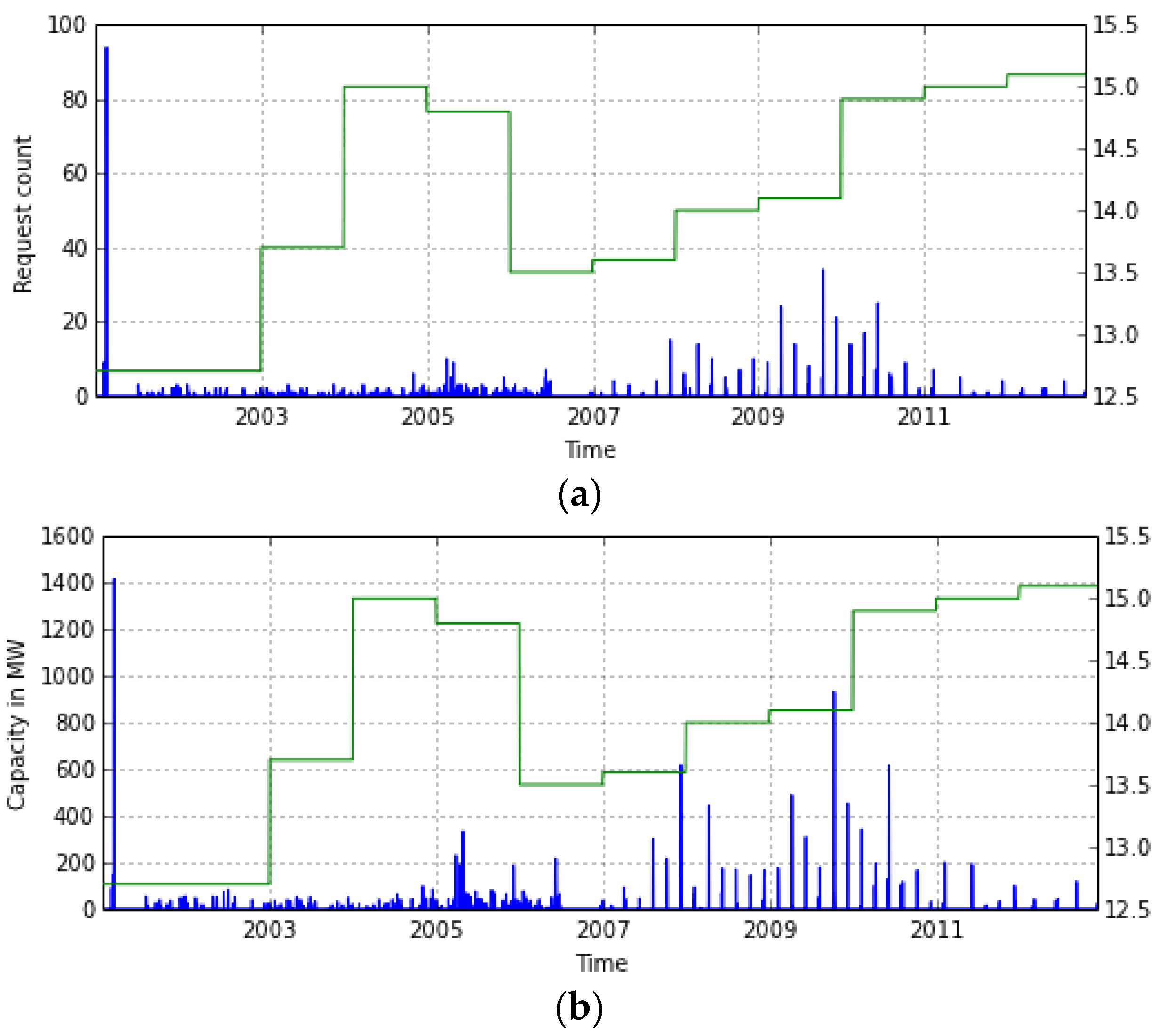

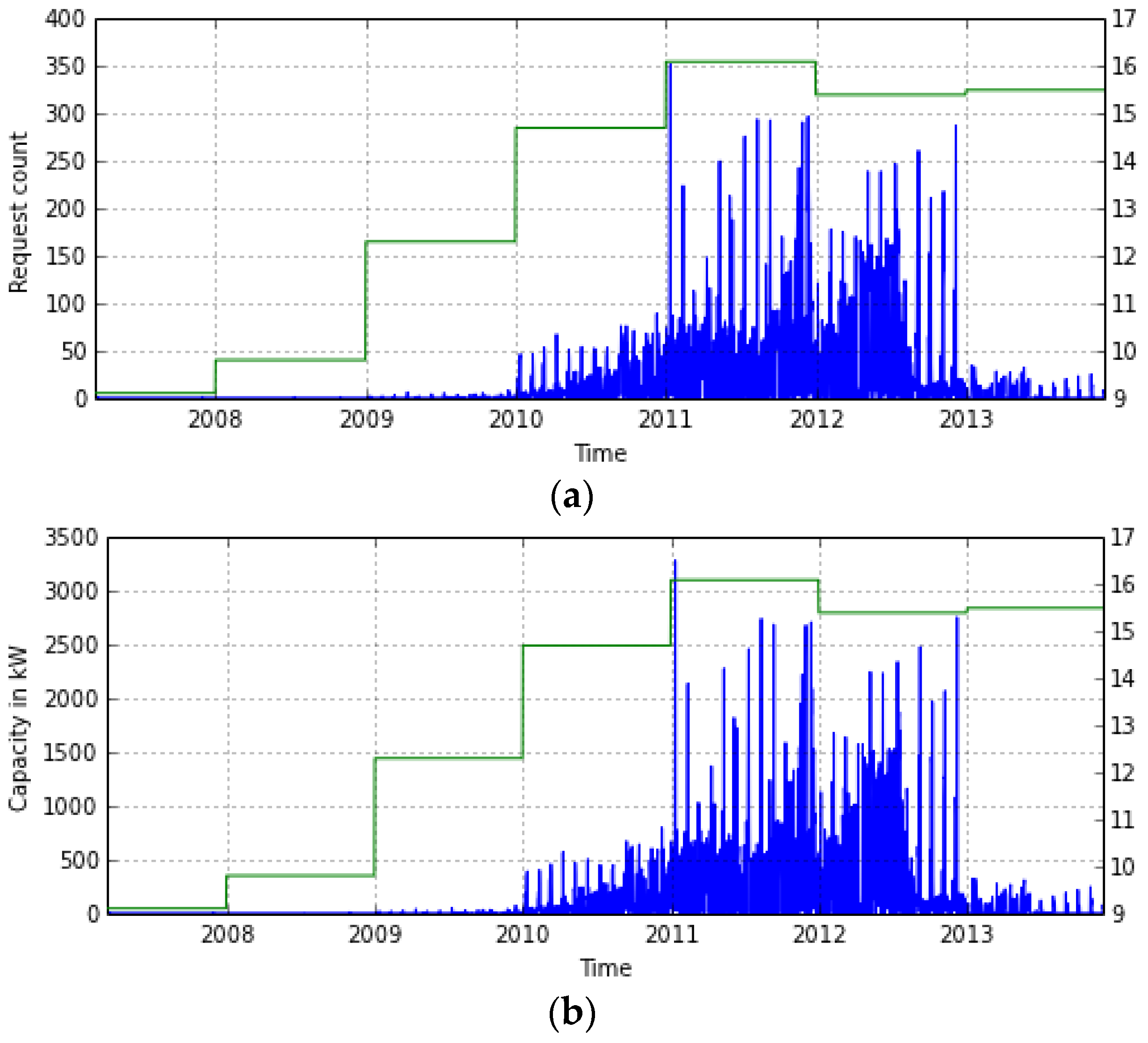

The evolution of demand, measured both in terms of the number of projects requesting a production license and in terms of the corresponding cumulative capacity, and the PI (as a piecewise linear curve) for interconnected wind RES-E investments from 2001 to 2012 are depicted in the next figure.

It is evident that the PI becomes relevant only after the enactment of Law 3468/2006 (June 2006), which set new administrative procedures for the promotion of RES-E and simplified the licensing procedures, and Law 3522/2006 (December 2006), which allowed investors to receive an upfront payment of up to 50% of the granted subsidy.

At the same time, the years 2011 and 2012 are an interesting case, since although the PI was higher than ever, the demand for new investments was very low. Furthermore, production licenses for wind RES-E projects of a total capacity of 260 MW were unilaterally cancelled by the investors who owned them; the French utility, electricite de France (EDF) alone owned and cancelled production licenses for 100MW of wind RES-E. The main reason for this loss of interest has been the low rate of the actual capacity additions. Although many of the projects that have acquired a production license would not materialize for various reasons (licensing, financial, etc.), the allocated grid connectivity offers had covered in many areas the limit for the safe operation of the grid.

The data suggest that increased financial incentives were utilized to counterbalance institutional deficiencies in permitting and interconnecting wind RES-E projects. An RES-E support policy measure is efficient if it induces a strong demand for investments in RES-E deployment with the minimum level of public expenditures. However, the rate of actual capacity additions has a reinforcement effect on the willingness to invest. No matter how attractive the PI is, if the success rate of the RES-E projects that acquire a production license is significantly low and/or the lead time to obtain all necessary permits is significantly high, either the willingness to invest diminishes or the size of the pool of the potential investors reduces to only the most capable to handle the authorization procedures.

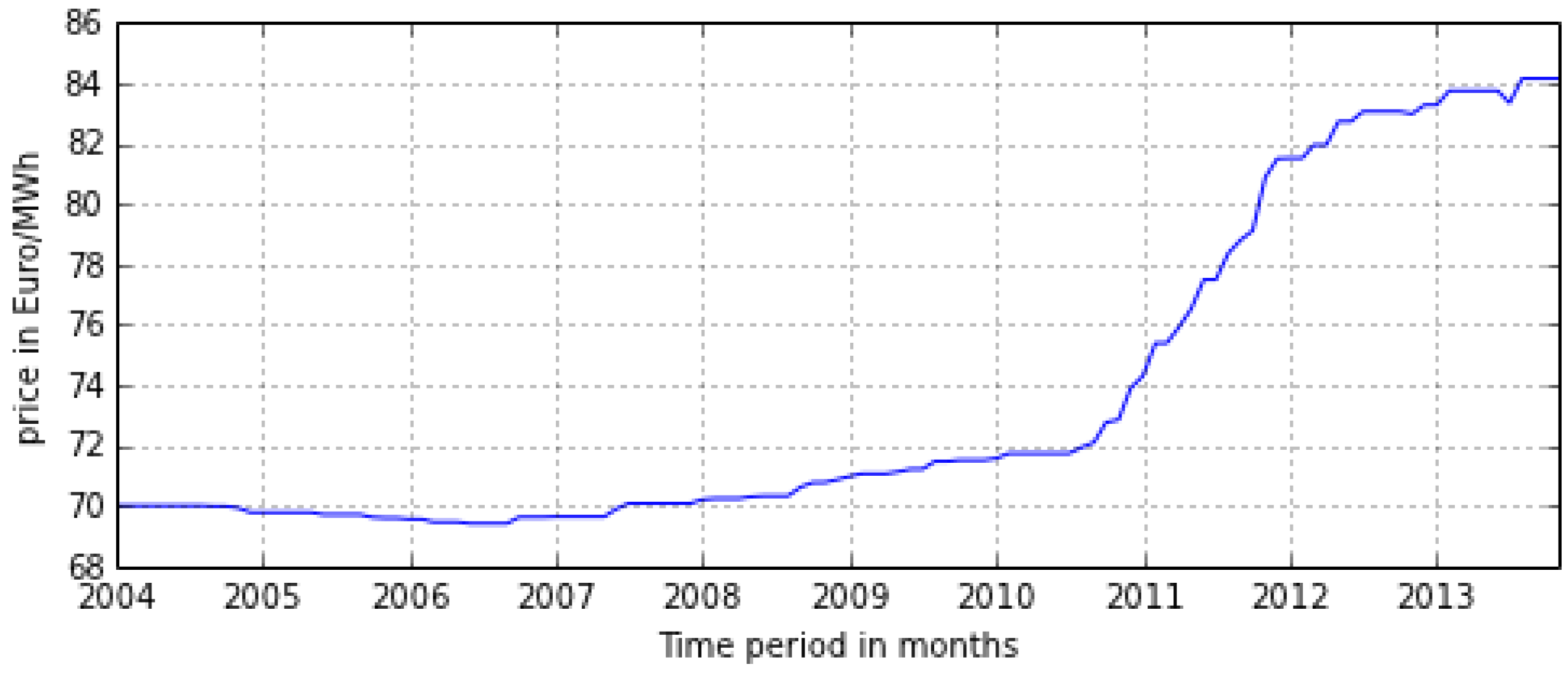

A higher than necessary PI negatively affects the efficiency of the support measures in proportion to the number of projects that manage to receive the fiscal support. Consequently, an alternative way to explore the data is to examine the actual weighted monthly average price of wind RES-E generation. In order to quantify the FIT cost per RES-E unit installed, we must know both the time evolution of the RES-E capacity additions, as well as the time when each RES-E installation in operation attained its connection offer.

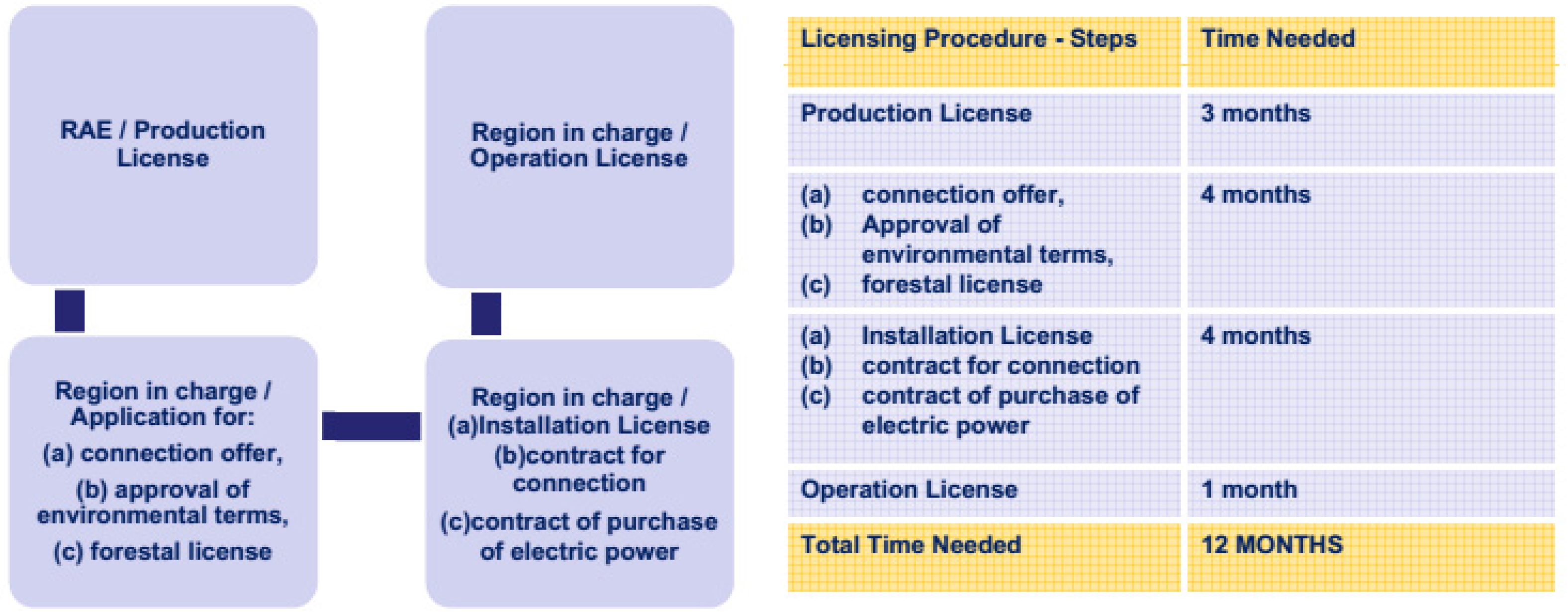

Due to data unavailability regarding the dates when RES-E projects in operation actually attained their connection offers, i.e., the dates when the FIT size was fixed, the analysis in this paper was based on the realistic assumption that after the enactment of Law 3851/2010, the average time elapsed between the attainment of the connection offer and the attainment of the operation license for a wind RES-E project was 9 months, whereas before Law 3851/2010, it was 18 months, since large-scale RES-E plants required permissions from 32 public-sector entities on a central, regional, prefectural and local level, leading to a licensing procedure that could exceed in practice 24 months.

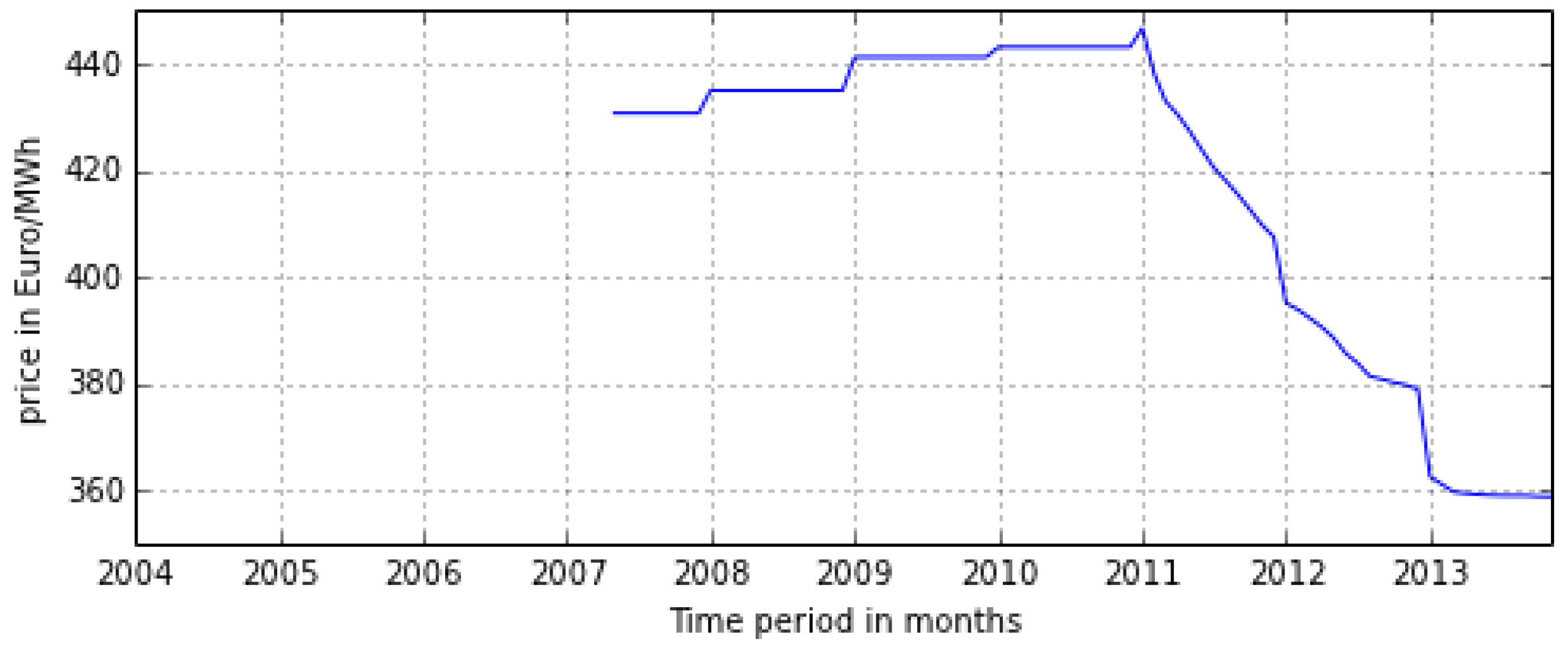

The estimated evolution of the generation-weighted (in €/MWh) monthly average wind power price for the same period is presented in

Figure 2.

Figure 2.

Evolution of demand and PI for interconnected wind RES-E investments. (a) Number of operation license requests for interconnected onshore wind RES-E during January 2001 to December 2012; and (b) capacity that corresponds to the operation license requests for interconnected onshore wind RES-E during January 2001 to December 2012.

Figure 2.

Evolution of demand and PI for interconnected wind RES-E investments. (a) Number of operation license requests for interconnected onshore wind RES-E during January 2001 to December 2012; and (b) capacity that corresponds to the operation license requests for interconnected onshore wind RES-E during January 2001 to December 2012.

An increasing cost for RES-E remuneration makes sense only if financial incentives start at a significantly low level and become progressively stronger so that less efficient sites are explored. However, the difference between the planned, according to the Greek NREAP, and the actual installed capacity suggests that this does not characterize the case of Greece. In particular, from 2010to 2013, the installed capacity increased from 1320 MW to 1784 MW, whereas the NREAP goal envisioned an increase from 1327 MW to 3112 MW.

3.2. Sensitivity of Investment Demand to Feed-in Tariff Prices for Photovoltaic Electricity Generation from Renewable Energy Sources Projects

The analysis begins by quantifying the corresponding PI, using the set of parameters and equations defined in

Section 2.1. In this subsection, two benchmark projects will be employed: one for an interconnected (mainland) utility-scale project and one for a residential system installation. The first benchmark project concerns a 1MW installation. The initial investment expenditure corresponds to:

- ▪

Until 2006: A40% public subsidy (grant) of the total eligible RES-E investment cost, equity capital equal to 40% of the total investment cost and 40% subsidy of the interest of the loan (20%) obtained for the purpose of financing the investment;

- ▪

From 2006 to 2010: A40% public subsidy and an equity capital equal to 25% of the total investment cost;

- ▪

From 2010 onwards: The equity capital covers 25% of the total investment cost. The rest is covered by a loan (75%), since PV plants were excluded from the national investment incentive law.

Fantidis

et al. [

23] have calculated the long-term monthly mean values of solar radiation and the monthly average daily clearness index over 46 areas in Greece. For the profitability calculations, the average annual capacity factor is taken to be 22%, and the annual efficiency decrease is 0.5%. Furthermore, the operating and maintenance cost is assumed to be equal to 1% of the total investment cost per annum, and the depreciation expense is assumed to be equal to 5% of the total investment cost per annum. We assume that the corporate tax rate remains at 25% for the duration of the PV’s operation. The cost of equity is 10%, and the price level (inflation) rises at the rate of 2% per annum. It is also assumed that the initial installation cost (€/Wp) is 1.5times the PV module price for the corresponding year. Finally, it is assumed that the investors secure a loan with a 10year duration and a 7% interest rate. The values of the PI for the years from 2005 to 2012 are presented in

Table 9.

Table 9.

The PI for a 1MW PV plant from 2005 to 2012.

Table 9.

The PI for a 1MW PV plant from 2005 to 2012.

| PI for a 1 MW PV Plant from 2005 to 2012 |

|---|

| Year | 2005 | 2006 | 2007 | 2008 | 2009 | 2010 | 2011 | 2012 |

| PI | 3.9 | 15.3 | 14.8 | 15.8 | 18.6 | 19.6 | 21.7 | 21.2 |

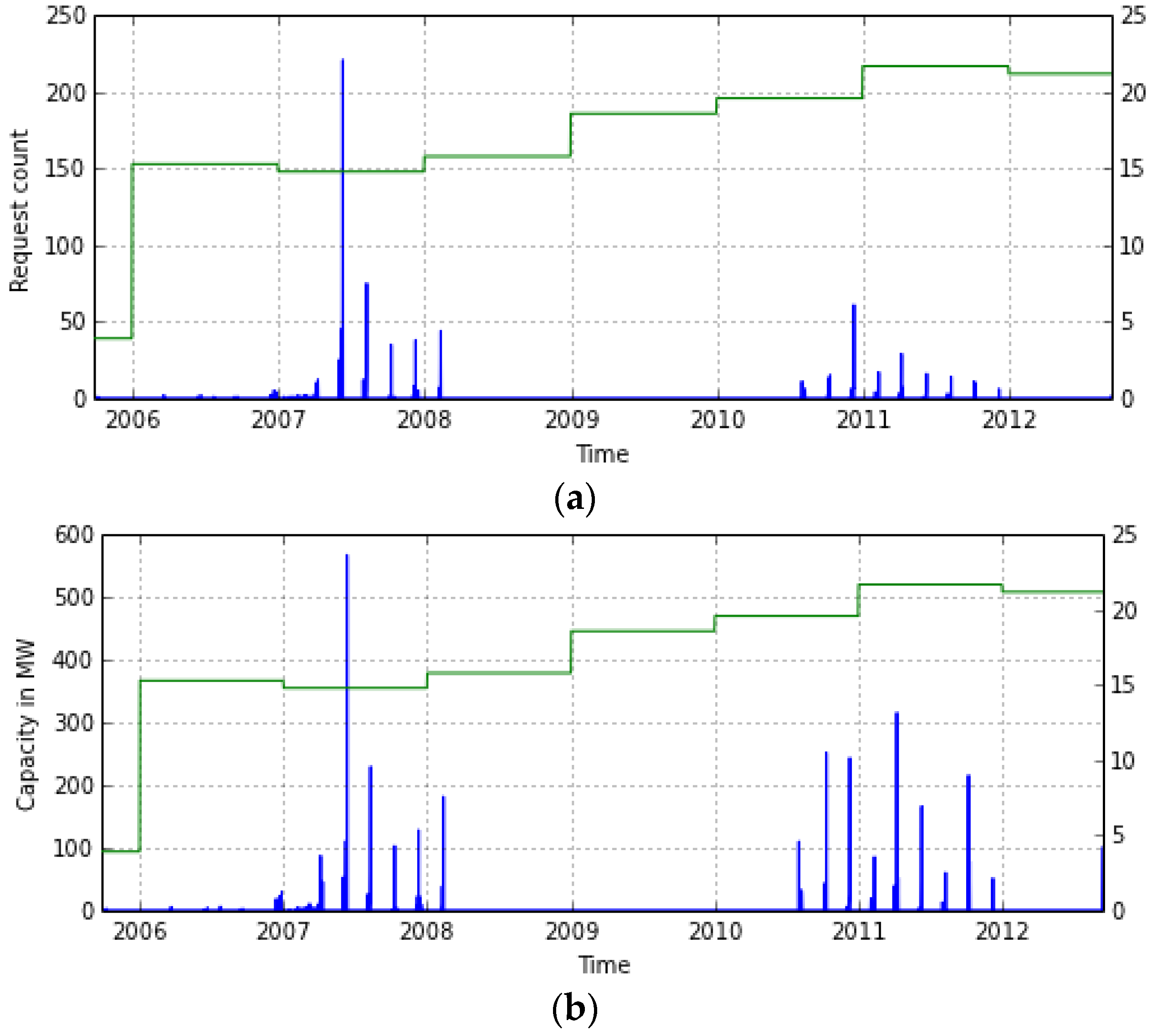

The evolution of demand, measured both in terms of capacity and in terms of the number of projects requesting a production license, and the PI for PV investments of capacity equal to or greater than 1MW from 2006 to 2012 investments is depicted in

Figure 3 and

Figure 4.

Figure 3.

Generation-weighted average wind power price for the period from January 2004 to November 2013.

Figure 3.

Generation-weighted average wind power price for the period from January 2004 to November 2013.

The FIT scheme that was established in Greece in 2006 provided strong price incentives for PV RES-E investments. However, in order to make the grid restrictions explicit, but also to control the overall cost for the consumers, the national RES implementation program set an upper limit on the PV capacity per administrative region. The surge of applications for operation licenses exceeded by far the limits set by the program, leading to a halt of any further submission of PV applications to the regulatory authority of energy (RAE) in 2008.

In light of these developments, the scheme voted on in January 2009 provided for the capacity limits to be scrapped. At the same time, Law 3734/2009 did not allow buying or selling production licenses or approvals prior to the grid connection of a PV station. This led to the deterioration of hundreds business plans of PV investors, who, eventually, lost their interest. In fact, the trading of licenses was one of the most determinant factors of the PV market development until then [

24]. The demand for investments increases considerably only during 2010 and 2011 due to the Law 3851/2010, which provided for a highly improved permitting procedure. It also provided a signal of increased market share for new RES-E investments by stating that the contribution of the electrical energy produced by RES-E to the gross electrical energy consumption should reach a share of at least 40% by 2020. However, time-consuming grid connection procedures a result of the limited capacity of the grid, have been a major barrier for PV deployment in Greece.

Figure 4.

Evolution of demand and the PI for PV investments of capacity equal to or greater than 1 MW. (a) Number of operation license requests for 1 MW and greater PV RES-E during September 2005 to September 2012; and (b) capacity that corresponds to the operation license requests for 1 MW and greater PV RES-E during September 2005 to September 2012.

Figure 4.

Evolution of demand and the PI for PV investments of capacity equal to or greater than 1 MW. (a) Number of operation license requests for 1 MW and greater PV RES-E during September 2005 to September 2012; and (b) capacity that corresponds to the operation license requests for 1 MW and greater PV RES-E during September 2005 to September 2012.

The assumption behind the estimation of the annual FITs paid for PV RES-E production is that capacity additions that took place before 2011 had locked their remuneration in 2007 FITs, whereas for capacity additions that took place from 2011 onwards, the average time elapsed between the attainment of the connection offer and the attainment of the operation license was 24 months. According to LAGIE data [

25], approximately 40% of the PV installations with a capacity greater than 10 kWp are also less than 100 kWp. It is assumed that this percentage remained steady throughout the horizon of the analysis. The estimated evolution of the generation-weighted (in €/MWh) monthly average PV power price is presented in

Figure 5.

Figure 5.

Generation-weighted average PV power price for the period from January 2004 to November 2013.

Figure 5.

Generation-weighted average PV power price for the period from January 2004 to November 2013.

Figure 5 represents a case of overshooting, where very attractive support was provided for the diffusion of PV, leading to the actual installed capacity being far higher than that planned; from 2010 to 2013, the installed capacity increased from 184 MW to 2055 MW, whereas the NREAP goal envisioned an increase from 153 MW to 836 MW. A side effect of the target overshooting was locking the electricity system with older PV technological options that were (cost-wise) inferior; a significant number of PV installations attained their connection offer until 2010, but they were actually built during 2012 and 2013.

The benchmark project for the calculation of the residential systems’ PI is based on a system with capacity equal to 9 kWp. The initial investment expenditure corresponds to the equity capital, covering 50% of the total investment cost. The rest is covered by a loan with a 10 year duration and a 7% interest rate. The cost of equity is assumed to be 15%. The operating and maintenance cost is assumed to be equal to 2% of the total investment cost per annum. According to data from LAGIE, the average annual capacity factor for rooftop PV installations is 15%. The annual efficiency decrease has been assumed to be 0.5%. Until 2010, 20% of the total PV cost (capped at 700€) is deducted from the investors’ annual taxable income. From 2010 onwards, the FIT for small rooftop PV systems of up to 10 kWp is guaranteed for 25 years, and the revenues from selling electricity are tax free. The values of the PI for the years from 2007 to 2013 are presented in

Table 10.

Table 10.

The PI for rooftop PV systems of up to 10 kWp from 2006 to 2013.

Table 10.

The PI for rooftop PV systems of up to 10 kWp from 2006 to 2013.

| PI for Rooftop PV Systems of up to 10 kWp from 2006 to 2013 |

|---|

| Year | 2007 | 2008 | 2009 | 2010 | 2011 | 2012 | 2013 |

| PI | 9.1 | 9.8 | 12.3 | 14.7 | 16.1 | 15.4 | 15.5 |

Since residential installations do not require the attainment of production licenses, the requests for grid connection were used as a proxy for demand. The demand for investments, measured both in terms of capacity and in terms of the number of projects requesting grid connection, is depicted in

Figure 6.

Figure 6.

Evolution of demand and PI for rooftop PV investments from 2007 to 2013. (a) Number of grid connection requests for rooftop PV systems during March 2007 to December 2013; and (b) capacity that corresponds to grid connection requests for rooftop PV systems during March 2007 to December 2013.

Figure 6.

Evolution of demand and PI for rooftop PV investments from 2007 to 2013. (a) Number of grid connection requests for rooftop PV systems during March 2007 to December 2013; and (b) capacity that corresponds to grid connection requests for rooftop PV systems during March 2007 to December 2013.

Regarding residential systems’ installations, PV investors, even if they were private owners, were fiscally considered as enterprises and had therefore to submit value added tax declarations periodically, while at the same time, the revenues from solar electricity were taxed as regular income, i.e., in the order of 25%–40%. This led practically to zero residential system installations until 2010.

An interesting observation is that although the expected profitability of the rooftop PV installations remained constant during 2012 and 2013, the rate of deployment in 2013 was significantly lower. Following the line of thought that searches in unobservable factors for explanations for such discontinuities, one should consider that 2013 was a year when a discussion began about the need to tax the revenues from rooftop PV installations (this discussion was fueled by a series of press articles that highlighted that the PV deployment rate was very high in particularly high-income areas of Greece), and rooftop PV owners were asked to pay a retrospective levy on their revenues; it is likely that these events increased the perceived risk of investing in rooftop PV.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}