Analysis of Environmental Accounting and Reporting Practices of Listed Banking Companies in Bangladesh †

1

Department of Sustainability Management, Inha University, Incheon 22212, Korea

2

College of Business Administration, Inha University, Incheon 22212, Korea

*

Author to whom correspondence should be addressed.

†

The concept of this paper was presented in the title of “Environmental Accounting Concept and Reporting Practice: Evidence from Banking Sector of Bangladesh” at 1st Dhaka International Business and Social Science Research Conference, Dhaka, Bangladesh, 20–21 January 2106 with Hossain, M. S. and Khan, S. This paper, however, is totally different in that it uses 20 banks data and use a scoring system to analyze current status of environmental information disclosure by Bangladeshi banks.

Sustainability 2017, 9(10), 1717; https://doi.org/10.3390/su9101717

Submission received: 9 August 2017

/

Revised: 8 September 2017

/

Accepted: 19 September 2017

/

Published: 26 September 2017

(This article belongs to the Section Economic and Business Aspects of Sustainability)

Abstract

:“Bangladesh faces many ecological challenges, including air and water contamination, land degradation, and waste management”. Bangladesh faces many ecological challenges, including air and water contamination, land degradation, and waste management. This study was designed to investigate the extent and nature of environmental accounting and reporting of listed banks in Bangladesh in 12 major categories. Information was collected from the annual reports of 20 banks listed on the Dhaka Stock Exchange for the period 2010 to 2014. The results indicate that the banks examined significantly disclosed environmental information for the 12 categories. The study found that banks disclosed the most environmental information for green banking and renewable energy categories, whereas they disclosed the least for environmental recognition and waste management categories. Furthermore, yearly comparison reveals that disclosure of environmental information increased sharply from 16% in 2010 to 83% in 2014. In addition, Bangladesh Bank’s recent fruitful initiatives on environmental disclosures were reviewed, and the findings of the 12 categories have managerial implications for policy makers in corporations as well as the government. It is recommended that professional accounting bodies of Bangladesh, along with international and government policy makers develop a separate conceptual framework for environmental accounting and reporting for the financial and non-financial sectors of the country.

1. Introduction

Some 3 million deaths a year are linked to exposure to outdoor air pollution. Indoor air pollution can be just as deadly. In 2012, an estimated 6.5 million deaths (11.6% of all global deaths) were associated with indoor and outdoor air pollution together. Nearly 90% of air-pollution-related deaths occur in low- and middle-income countries, with nearly 2 out of 3 occurring in WHO’s South-East Asia and Western Pacific regions. WHO’s air quality model confirms that 92% of the world’s population lives in places where air quality levels exceed WHO limits. Environmental risk factors, such as air, water and soil pollution, chemical exposures, climate change, and ultraviolet radiation, contribute to more than 100 diseases and injuries.[1]

Bangladesh is ranked fourth among countries with the worst urban air [2] and WHO’s statement above shows the vulnerability of the world environment, particularly South Asian countries [3,4]. Environmental accounting and reporting (EAR) create accountability for business entities [5,6,7,8] in terms of their efforts to protect the environment in their corporate decisions. In decision making, an organization considers different pressures from internal and external parties and attempts to legitimize the impact of its activities on the environment in the eyes of society and various pressure groups [8]. EAR plays an active role in preparing, presenting, and analyzing environmental information for interested parties [9].

Environmental information may be monetary or nonmonetary; currently, however, accountants are attempting to convert qualitative environmental information into quantitative information [10]. Environmental disclosure may be positive or negative, indicating whether the organization is environmentally friendly or destructive [9,11]. Moreover, nonfinancial information regarding economic, social, and environmental performance fosters stakeholders’ understanding of management responsibilities [12]. Furthermore, EAR, corporate sustainability reporting, and sustainability practices enhance a company’s image in the marketplace and among different stakeholders, thus encouraging top management to improve environmental conditions [7,8].

Exercises related to EAR reinforce corporate decision-making power and management stewardship [8,9]. The overall performance of an organization is evaluated based on not only financial results but also contributions toward protecting and improving the environment [13]. Thus, EAR has become an important consideration when investors and creditors assess risks associated with their investments [14]. Professional accountants and accounting bodies have already begun EAR and CSR reporting activities [15].

Bangladesh is a developing country, but a recent trend indicates that the country is moving toward a middle-income position [2]. Its economy depends mostly on the manufacturing and financial sectors [16]. The banking sector has had a positive contribution to and an influence on the economic development of the country. At present, Bangladesh faces several environmental problems, including water pollution, air pollution, land degradation, loss of biodiversity, poor waste management, coastal erosion, and poor chemical waste processing [2,13]. The banking sector can play a tremendous role in upgrading the present environmental situation of the country. Moreover, banks are the most recognized and significant financial organizations. They engage in financing for manufacturing as well as nonmanufacturing companies as financial intermediaries. Thus, banks are related both directly and indirectly to environmental issues. Recently, Bangladeshi banking companies have implemented international award-winning large-scale corporate social responsibility (CSR) programs [17]. Furthermore, Bangladeshi banks are practicing global sustainability reporting, with some banks preparing their sustainability reports according to the Global Reporting Initiative (GRI) [18]. Bangladesh Bank (central bank) has made a tremendous effort since 2008 to issue circulars related to social and environmental issues [19]. Moreover, it has played a major role in recent years with the issuance of a comprehensive circular regarding implementation of green policies by financial institutions (i.e., BRPD Circular No. 2). At present, Bangladesh Bank green policy guidelines provide the only mandatory framework in the history of Bangladesh’s financial organizations. Bangladesh Bank also began publishing an annual Green Banking review report on the financial sector in 2013 [20] describing the financial and nonfinancial green performance activities of banks. The banking sector in Bangladesh has also played a pivotal role in CSR and EAR reporting in recent years [21,22,23] thereby recognizing the connection between CSR functions and environmental issues. The current patterns have given a striking picture of environmental reporting (ER), or green reporting (GR) of Bangladeshi banks, but the emerging discussion is whether the major Bangladeshi banks have actually had any effects on EAR performance considering the country’s vulnerable environmental position. Many studies have been conducted on corporate ER of manufacturing companies in Bangladesh [9,24,25,26,27,28]. However, there is a dearth of study documenting banking companies’ EAR on major emerging environmental contents and EAR disclosure study is limited to the recent study on green disclosure of banks [29] except for a few studies on the GRI [17,18], CSR [21,28,29,30] and sustainability [22,23].

Furthermore, Bangladesh receives relatively less attention in studies about EAR compared to other developing countries. Furthermore, in Bangladesh, there is a lack of managerial commitment to the respective stakeholders concerned with societal activities [31]. The study provides preliminary evidence on EAR implementation in the banking sector of developing countries, such as Bangladesh. Specifically, it examines major activities of banking companies in 12 emerging categories of EAR disclosure. Another aim of this study is to overview the legal position of EAR. A limited study has been found on EAR disclosure along with legal provision and environmental financing in the Bangladeshi banking sector. Thus, this research would be unique in the banking sector analysis. Indeed, a study that investigates EAR disclosure of various banks from an emerging economy like Bangladesh will add a new dimension to the banking literature [31].

2. Legal Status of Environmental Accounting and Reporting in Bangladesh

Environmental pollution has been a common problem in Bangladesh in the last few decades. The major rivers of the country are in vulnerable positions, and in Dhaka, the capital, the Buriganga River is highly contaminated [13]. Air pollution is another very alarming situation for the country, particularly in Dhaka and Chittagong, a commercial center [1]. The Ministry of Environment and Forests of Bangladesh was established in 1989, and since then Government of Bangladesh has paid more attention to the environment because of pressure from various stakeholders, including national and international organizations [24]. In 1995, the United Nations Development Programme (UNDP) began supporting a National Environmental Management Action Plan; in the same year, the Bangladesh Environmental Conversion Act of 1995 was promulgated. The Act established new industries, which are required to obtain environmental clearance certificates from the Department of Environment, and the companies may be asked to disclose environmental information on demand [9,24,25]. In addition, the country’s EAR is influenced by other legislation, as shown in Table 1.

Clearly, there are strong legal positions on environmental issues in Bangladesh, and reporting of environmental information to the regulatory bodies is required. At present, however, there are no mandatory guidelines in corporate laws in Bangladesh to disclose corporate environmental information [24,25,30]. Table 1 lists numerous laws in Bangladesh to protect the environment. Nevertheless, why is Dhaka the most contaminated city in the world? A recent study of Belal et al. [13] clearly states the reasons for the environmental vulnerability of the country. The researchers pointed to political unwillingness, corporate unwillingness, a lack of sufficient manpower in related departments, and corruption as the prime reasons for contamination.

3. Theoretical Background and Literature Review

3.1. Theoretical Background

3.1.1. Stakeholder Theory and EAR Disclosure

Banks do the business in the society and their financial and non-financial activities receive huge amount of pressure from its various stakeholders including media, NGO, investors, government, customers, and shareholders [4,17,29,32,33,34]. Stakeholder theory is commonly and widely used as a rationale underlying active EAR disclosure. In particular, EAR disclosure assures stakeholders of organizations environmental performance, environmental investments and strategy [35]. According to the stakeholder theory, organization’s financial performance depends on its sound and faithful relationship with stakeholders. EAR information disclosure is considered a significant medium of an organization’s social and environmental responsibility. Freeman et al. [36] define the stakeholder theory as fundamentally a theory about how business works at its best, and how it could work. It is descriptive, prescriptive and instrumental at the same time it is managerial. It is about value creation and trade and how to manage business effectively (p. 9). Researchers found that socially irresponsible operation can have a negative influence on banks’ financial and nonfinancial performance such as share prices and brand reputation [17]. Today’s customers are increasingly interested to know bank’s social responsibility, social investment and CSR performance. Effective management is directly associated with good governance, and at the same time it ensures stakeholder expectation from the firm. Corporation is required to understand that sound and faithful relationship with its various stakeholders will lead to survival and financial success in the long-run [32,33,34].

In addition, stakeholders have supposition regarding EAR disclosure performance in connection with pollution prevention, bio-diversity, environmental management system, climate change disclosure, and effective and efficient utilization of natural resources [4,33,34,35]. Accordingly, corporation should report all of the EAR issues to its stakeholders in the name of annual reports, web sites, brochures, stand-alone CSR or sustainability reports [17,32]. Prior investigation specified that EAR has become an “action and support tool” for organizations to reach its stakeholders and to enhance overall performance and reputation [33,35,37]. Currently, banks in developing countries like Bangladesh are facing a great deal of challenges from stakeholders regarding environmental and ecological issues, especially from institutional investors [4,17,29]. Thus, we believe that stakeholder framework will make the banking companies more accountable for disclosing more and more EAR information to maintain positive relationship with the diverse stakeholders and to accelerate their environmental stewardship.

3.1.2. Legitimacy Theory and EAR Disclosure

Legitimacy theory explains and considers the relationship between organization and society [4,32,38]. Suchman [39] defines legitimacy as a generalized perception or assumption that the actions of an entity are desirable, proper, or appropriate within the same socially constructed system of norms, values, beliefs and definitions (p. 574). Legitimacy theory in the research can be divided into strategic and institutional [34,39]. Strategic legitimacy consists of resources and control which an organization uses to achieve social support over managerial performance [34,39]. Strategic legitimacy explains organizations’ desire and motivation for EAR, CSR and Sustainability issues. From the legitimacy perspective EAR reporting is an influential utensil of a company to communicate with society [4,33,34,38]. Legitimacy is important for every organization to manage its strong and reputed position and status in the society and to know the reactions of respondents from the society. For the legitimacy concern companies are interested in disclosing positive information rather than negative information [22]. Organizations in both developed and developing countries use publications and reports to mitigate pressure on controversial environmental decisions by which legitimacy is threatened [34]. Nowadays, organizations are very concerned about public perception of their prevailing environmental activities for that they consider EAR reporting is an emerging tool to gain societal support and reputation [33,34]. Therefore, legitimacy comprises social systems, norms, rules and meaning that can ensure companies responsibility and accountability on EAR. Moreover, legitimacy can create opportunities and attraction of economic resources to ensure the social and political support [4]. Prior research on legitimacy has documented the use of social disclosures in annual reports as tools to legitimize organizations. Many studies have found that EAR disclosures are commonly positive and self-praising, with a little bad and neutral news disclosed [17,22,34]. Therefore, we expect that Bangladeshi banking companies will disclose EAR information to cope with the legitimacy pressure from the societal exceptions.

3.2. EAR in Developing Countries

Although EAR is on the increase, few studies have explored sustainability, CSR, corporate ER, corporate social reporting, corporate human disclosure, and so on in developing countries [13,17,22,23,24,25,40,41,42,43,44,45]. Teoh et al. [46] conducted a study on environmental disclosure and financial performance of listed companies in Singapore, noting that environmental disclosures generally reflect firms’ better financial performance. Thus, there is a significant and positive relationship between the level of environmental disclosure and financial performance, indicating that firms with better prior financial performance make greater subsequent environmental disclosures. Fifka [47] investigated the prevailing literature on social and environmental reporting in different developing countries, pointing out that the number of studies on this subject has increased during the last decade because of people’s awareness of CSR, the environment, and sustainability. Moreover, a few scholars in developing countries like Malaysia, Bangladesh, India, and China perform research on the issue [47]. Furthermore, different studies indicate that, in most Asian countries, CSR and social, environmental, and sustainability reporting are not widely practiced and are generally limited to specific industries related to oil, chemicals, and steel [8,47,48]. Environmental and social aspects of the sustainability performance of Asian companies are less prevalent than they are for European companies [49].

Social and environmental reporting has increased over the past two decades in developed and developing countries [21,37,50,51]. Savage [12] made a study of 115 South African companies and found that approximately 50% of companies made social disclosures and 63% made environmental disclosures. Moreover, Tsang [52] conducted a study over 10 years of 33 listed companies in Singapore and found that 52% of these made social disclosures. A recent survey of KPMG [37] reported that corporate responsibility (CR), corporate environmental responsibility (CER), and CSR are now undeniably mainstream business practices worldwide; additionally, there has been a dramatic increase in CR reporting rates in the Asia-Pacific area over the past three years.

South Asian countries like India, Pakistan, Sri Lanka, and Bangladesh have a smaller number of companies that report corporate environmental and social information [8,53]. Oil, mineral, cement, automotive, and pharmaceutical companies are generally prepared for ER in the South Asia [54]. Gupta [14] examined annual reports of 23 listed companies in India and found that very few companies in India were voluntarily disclosing environmental issues in their annual reports. He also stated that a lack of environmental legislation behind poor environmental disclosures in annual reports is supported by a previous study [24,25]. In Malaysia, ER or CSR is in developing stages [55]. Dissanayake et al. [8] studied 60 listed companies of Sri Lanka and stated that ER was quite significant for larger firms. The study also revealed that companies were providing more social information than environmental information. Further, banking companies are providing more environmental information than other companies.

Although social and environmental reporting practices have gained momentum, such practices are apparently a new issue for financial institutions in Bangladesh [22,23,29]. Hossain and Chowdhury, Rahman and Muttakin, Dutta and Bose, Shil and Iqubal, Ullah and Rahman, Nurunnabi [4,9,21,26,56,57] have conducted studies on listed companies of Bangladesh—particularly, companies on the Dhaka and Chittagong stock exchanges—and have stated that companies were providing social information in their annual reports related to environmental, philanthropic, societal, and human resource aspects but in an unstructured manner. Another finding is that environmental information disclosure is very poor despite a rapid change in nature over the last five years [11,18,19,29]. Climate change is a very crucial issue for Bangladesh in relation to global warming. A recent empirical study that examined listed Bangladeshi companies on climate change reporting has shown very poor disclosure on climate change information; only 2.23% of companies report climate related information [4]. Even the oil and gas companies operating in Bangladesh disclose little environmental information in their annual reports [9]. The recent research has been performed by Belal et al. [13] in the new dimensional area of vulnerability and corporate environmental accountability in Bangladesh. The researchers reported much negligence in Bangladesh, particularly in terms of environmental performance and pollution. They argue that Bangladesh has incurred huge costs related to air and water pollution, public health, low groundwater levels, and river erosion; consequently, vulnerable people are losing their livelihoods. Further, the study reflects the real picture of our policy makers and business persons who speak out often on the environment but do little for environmental protection. This situation is also reflected in the controversial decision regarding the Rampal power plant and Ruppur atomic power plant [2,58,59]. The latest research investigated green banking disclosure and green policy implications for Bangladesh Banks, and it found an increasing information disclosure and a positive relationship between green banking policy and information disclosure [29]. Additionally, recent studies report mixed results on Bangladeshi banking and non-banking companies EAR disclosure [4,29].

4. Research Methodology

4.1. Sample and Data

The nature of the study is descriptive and based solely on information from secondary data sources of banking companies. The main sources of information are annual reports of listed companies on the Dhaka Stock Exchange (DSE). It is documented and widely accepted that the annual report is a common and popular means of communicating with stakeholders [24,44,47,60,61,62,63,64,65]. Thus, banking sector environmental disclosure is the key focus of the study. Twenty listed banks were selected (see Table 2) among 30 banking companies on the DSE (see Appendix A) based upon the availability of the annual reports from the website during the study period. Moreover, for a descriptive study, a minimum acceptable sample size was considered as 10% of the total population [44,66]. The sample size of the study represents 67% of the total population.

The selection of banking companies emanated from recent directives of Bangladesh Bank promoting CSR and green reporting [21]. Banking companies are leading in the disclosure of corporate social activities, social and environmental reporting, and sustainability reporting [8,21] and societal and philanthropic [8] activities. Besides, listed companies usually place importance on publishing quality reports for different stakeholders and meeting statutory requirements [6]. Annual reports of sample banks, Bangladesh Bank reports, relevant books, newspapers, the Internet, websites, and research works were also considered [17,60,63]. In addition, to confirm the legitimacy and credibility of each annual report on social and environmental issues, all sections of the annual reports (e.g., vision statement, mission statement, directors’ report, chairman’s report, and notes and explanations) were analyzed [51].

4.2. Data Collection Period

Bangladesh Bank issued a different circular in 2009 and the Government of Bangladesh enacted a financial act in 2010 regarding tax benefits of CSR [32]. Moreover, in 2011, Bangladesh Bank issued a circular requesting that all banks adopt a green banking policy in order to conserve and protect the environment. Finally, in 2013, Bangladesh Bank issued “Policy Guidelines for Green Banking”, presenting detailed reporting guidelines [66]. As a result; CSR, social and environmental, and green reporting initiatives in Bangladesh have reached a hallmark position since 2010. Therefore, annual reports for the period of five year from 2010 to 2014 were used in this study. As a result, 100 observations from the study period have been selected from 20 listed banks.

4.3. Research Method

As stated earlier, the nature of the study is descriptive. Most researchers rely on content analysis for social and environmental reporting (SER) disclosure, which is widely accepted, but this study used a general content analysis for methodical order and investigation of the contents reported in annual reports [17,21,29,69,70,71]. The study emphasizes the number of disclosures related to SER, whether presented in the annual report or not. To measure content disclosure of SER reporting, different researchers have used different types of measures. For example, Beattie and Jones [72,73] suggested numbers of words, sentences, pictures, graphs, and charts, whereas Zeghal and Ahmed [74] used the number of words only. Hackston and Milne [75] used the number of sentences; Gray et al. [64] used the number of pages; Rahman [47] used the number of lines; Kabir and Akinnusi [51] used the number of words; and Ullah and Rahman [21] used numbers of words, sentences, tables, graphs, and charts. Previous studies have concluded that there is no specific guidance in the CSR literature for choosing any measure for content analyses [28,51,75,76,77]. Broadly, the analysis in this study covered the content of selected areas of EAR information in the annual report rather than lines, words, graphs, et cetera. The methodology and content used in the study reflects that used in the prior research of Wiseman [78], Kabir and Akinnusi [51] and Ullah and Rahman [21] (Table 3). Further, the study involves analyzing the content of environmental disclosure in 12 major categories with specific coding (see Appendix B). The areas were selected based on previous research and present Bangladesh Bank green policy guidelines. The major areas or categories were used to measure the performance of the selected banks’ EAR. All selected categories relate to the environment, environmental investment, and environmental performance. Moreover, efforts of selected banks to reduce air pollution, water pollution, and save energy are known from their daily environmental practices, whereas waste management, renewable energy, environmental policy and green banking policy information are typically described in long-term environmental policies for investment purposes. The remaining areas are associated with environmental supervision. Therefore, the selected areas are considered components of banking companies’ environmental perspectives. As a result, CSR and SR related information is not included in our analysis [17]. The study incorporates a scoring system for the 12 categories to justify how many banks are providing information related to EAR. Accordingly, the EAR disclosure score index (EARS) of a selected company reflects the methodology used by Cooke, Ullah and Rahman [21,79]. For each category banks reporting environmental information were given a value of 1 (otherwise, 0) in a dichotomous procedure suggested by Clarkson et al [80]. EARS are sum of 12 categories for each bank and each year:

where, EARS = Environmental Accounting and Reporting Score for each bank for a given year; di = 1 if the item is reported, 0 otherwise.

In this study, general mathematical techniques and descriptive statistics were used; these included averages, percentages, and the EARS index. Furthermore, an analysis regarding the monetary or nonmonetary nature of disclosures was performed [51]. This method of measurement has been applied in several prior studies to quantify and describe disclosures [30,32,44,64,75].

5. Findings and Results

5.1. EAR Disclosure Performance Measurement

5.1.1. Environmental Projects and Finance

Most banks facilitating environmental projects (Table 4) show their concern for the environment and society. The most positive development is that a bank finances green projects at a zero rate of return. Every bank studied has financed projects associated with renewable energy, e-commerce, e-business, online banking, or waste management. Directly and indirectly banks have invested significant amount of money in different environmental projects since 2012. Total green financing amounted to BDT 2,70,921.53 million in 2012 and increased to BDT 4,35,877.09 million in 2014 [20,81]. The incremental increase of environmental project financing has a significant impact on the environment, as shown in the following example:

The Bank gives priority in disbursing environment-friendly investments like renewable energy, energy efficiency, waste management, alternative energy, recycling and recyclable products, green industry, safety and security of factories, clean water supply, etc. [82].

5.1.2. Environmental Disclosures in Selected Categories

Table 5 presents the information and scores in 12 categories of EAR. Six banks disclosed environmental information in all areas. Banks with the highest disclosure scores were BRAC, BAL, DBBL, IBBL, SEBL and UCB (please refer to Appendix A for meanings of abbreviations), whereas FSIBL, OBL and ShIBL disclosed the least amount of environmental information. Compared to the recent study by Ullah and Rahman [21] who reported that the most environmental information provided by banks in their annual reports was 40–50%, this study shows better performance by the Bangladeshi banking sector, with the average disclosure of environmental information at 85%. The effect of Bangladesh Bank’s green reporting guidelines (mandatory ER disclosure) is evident [20]. Furthermore, compared to other studies such as Azim et al. [83], Singh and Ahuja [61], Savage [12] Bose et al. [29] and Tsang [45] the present study indicates satisfactory results regarding environmental disclosures in annual reports.

Table 6 presents disclosure of EARS information for all banks for five years, showing that the category (please refer to Appendix B for meanings of EARS Coding) of green banking (C9) scored the highest followed by renewable energy (C4) and energy-saving (C5). The findings affirm the better environmental management performance of banking organizations, as suggested by the following statement in an annual report: “Around a third of the bulbs being used in this office are of energy-savings type. We are saving around 40% electricity (used for lighting purpose) by using the daylight in our Corporate Office” [84].

On the other hand, awards or appreciation for environmental activities (C7) scored the least, whereas waste management (C3) and air pollution & tree plantation initiatives jointly (C1 & C10), scored second and third from the bottom, respectively. Banking companies disclosed relatively little climate change and global warming (C12) information (i.e., 2.9 on average) despite the fact that Bangladesh is one of the most affected countries by the issue in the world [4]. Therefore, on average they disclosed 55% (TEARS 661 out of 1200) EAR disclosure during the study period. The findings indicate that banks have made insufficient movement on these issues. Additionally, the analysis found results consistent with the recent study [4,29].

5.1.3. Ranking of Banks

Table 7 provides the ranking of the banks based on the total EARS for five year period. Among the 20 banks, IBBL ranked highest (score of 55 out of 60) and FSIBL ranked the lowest (score of 14 out of 60) for disclosure of EAR information. Furthermore, scores for many banks like BAL, DBBL, IFIC were the same and there was only one point difference with each other in some cases. The results are inconsistent with the recent findings of Ullah and Rahman [21].

Table 8 presents the yearly information disclosed by banks for all categories. For the period 2010 to 2014, every bank published EAR information, with the most information disclosed in 2014 and the least in 2010. Banking companies’ gradually increasing EAR disclosure is the result of Bangladesh Bank green policy efforts [29]. Furthermore, the result of the study is supported by previous studies, such as Ullah and Rahman [21], Azim et al. [83], Masud and Kabir [31].

Table 9 presents and compares EAR disclosure trend of banking companies from 2010 to 2014. It shows that the average disclosure of EAR information is 3.167, with a minimum disclosure of 0 and a maximum disclosure of 7 items of the selected categories in 2010. The mean EAR disclosure of 2011 is 8.583, about 3 times higher than that of 2010, indicating that banking companies made more EAR information disclosure due to the Bangladesh Bank green policy. T-value testing the difference between mean disclosure in 2010 (3.167) and 4 year period 2011–2014 (12.979) is significant at less than 1% (t = 7.55). Non-parametric Wilcoxon two sample test result comparing two medians also shows the same result (z = 5.55). The mean information disclosures for 2012, 2013 and 2014 are 11.667, 15.167 and 16.500, respectively. Most significantly, in 2014 EAR disclosure increased to about 6 times higher than 2010. Overall descriptive statistics of EARS shows the increasing trend of the banks EAR during the study period. The result is consistent with the recent study on green reporting disclosure of Bangladeshi Banks [29]. The recent study revealed that the incorporation of regulatory framework by the central bank of Bangladesh positively and significantly influenced EAR disclosure practices in the financial sector of Bangladesh.

5.2. Environmental Disclosure in the Annual Reports

5.2.1. Disclosure and Nondisclosure of EAR Information

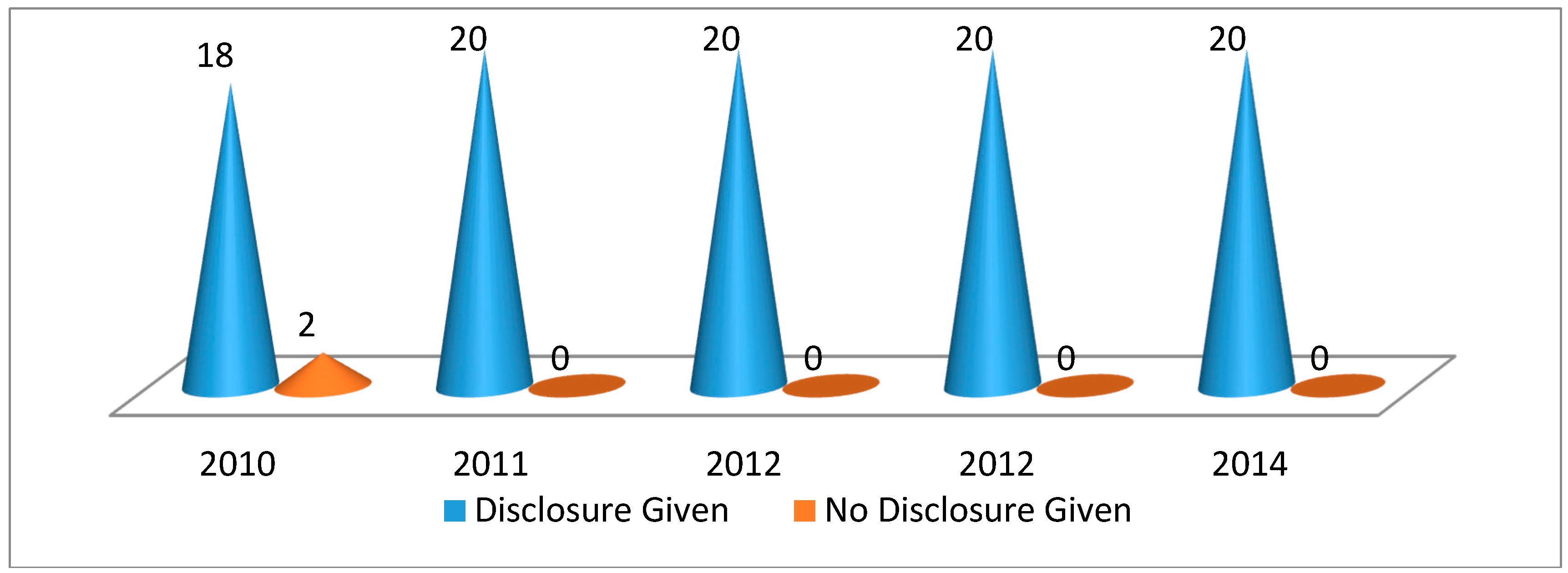

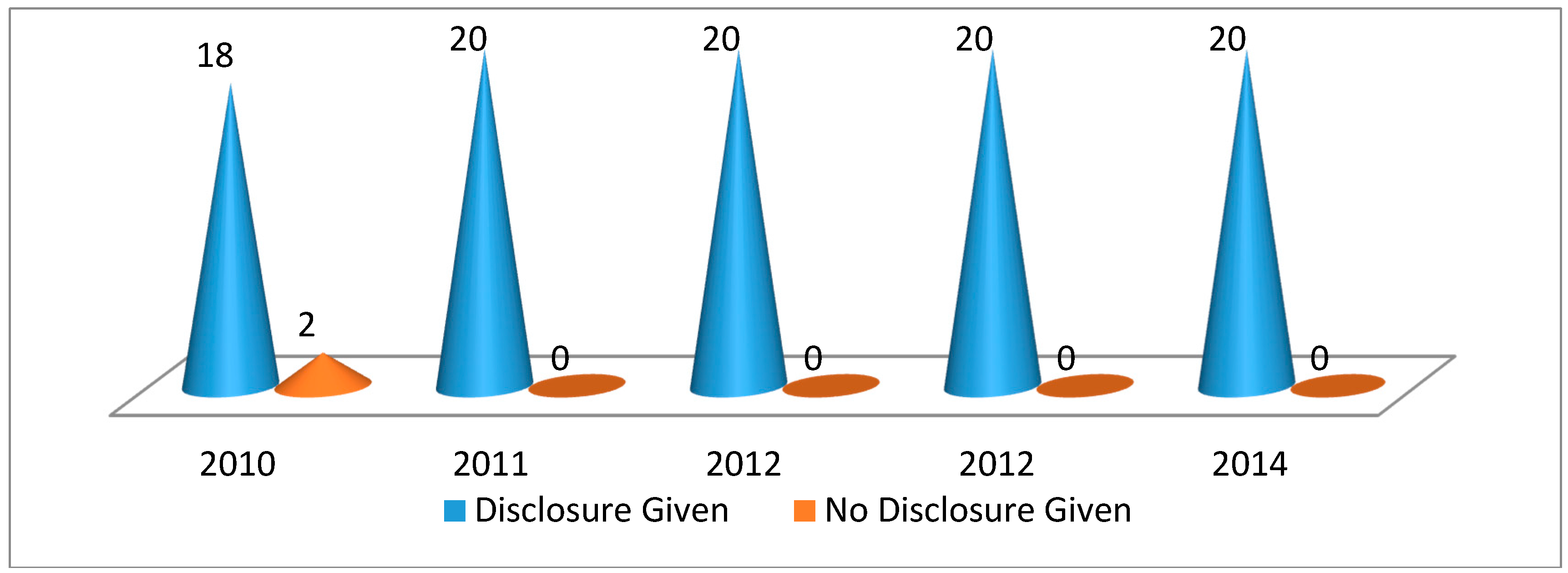

Figure 1 shows that almost all banks have disclosed environmental information except for two banks in 2010. The amount of information disclosure by each bank varies as can be seen in Table 7. The increase in disclosure from 2010 to 2011 seems to be the effect of Bangladesh Bank green policy efforts [29].

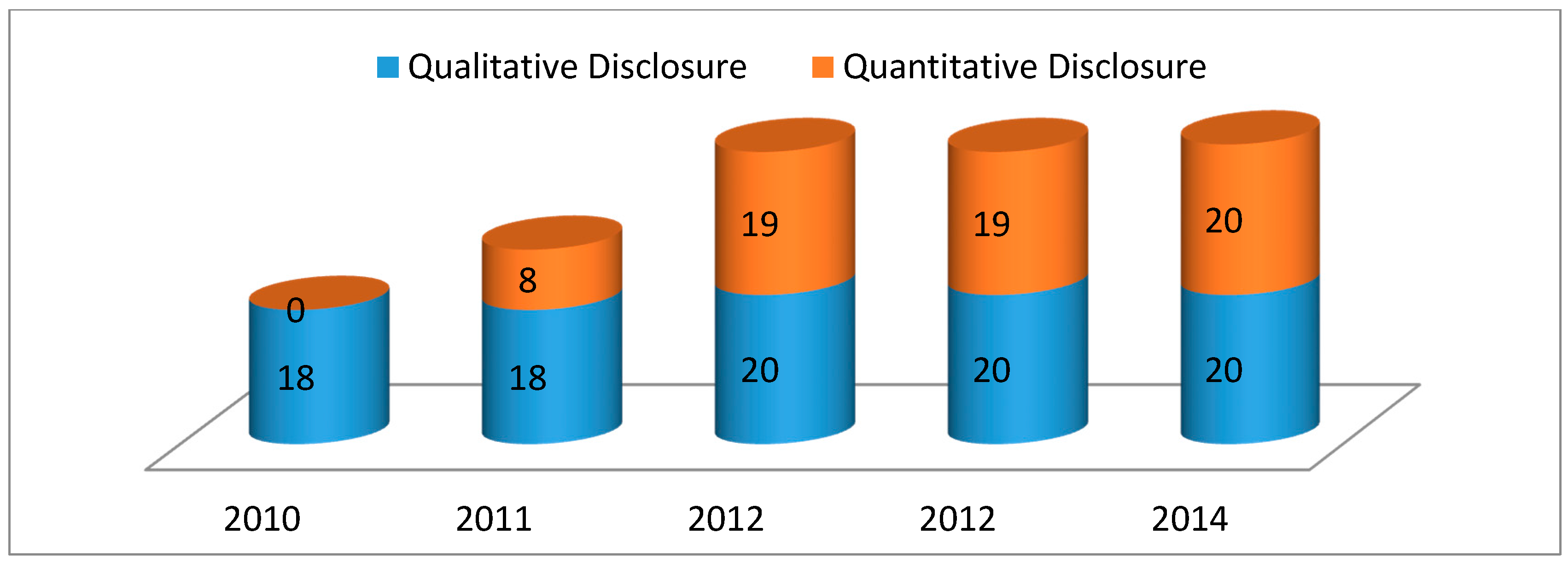

5.2.2. Qualitative and Quantitative EAR disclosure

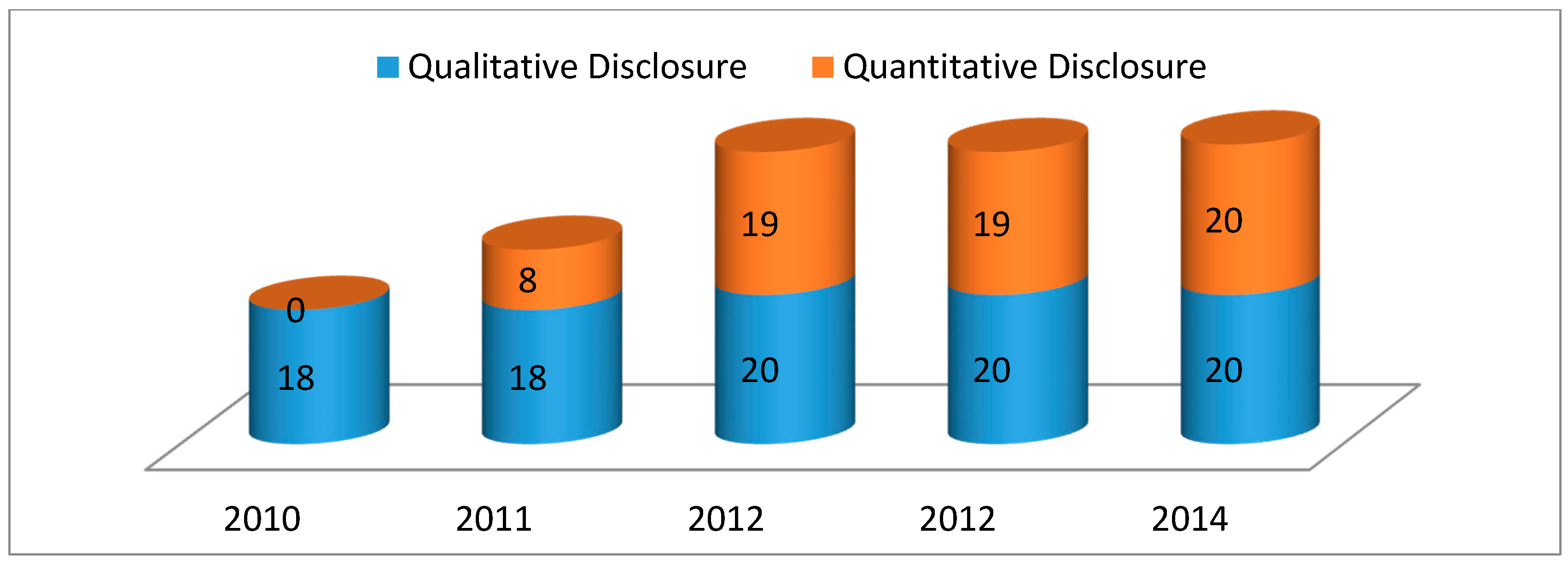

Figure 2 describes the mode for disclosing environmental information. The disclosure of environmental information has been increasing for both qualitative and quantitative information over time. In 2010, not a single bank disclosed quantitative information, but since 2011, the number of banks disclosing such information has been gradually increasing. In 2014, all 20 banks in the sample disclosed quantitative information. However, banking companies that disclose financial information on environmental issues do not provide any proper breakdown of environmental expenditures in their annual reports [14]. Some banks have given detailed information on environmental protection activities through charts and tables [14,21], and provided those information in both monetary and nonmonetary terms as well as phonetically through diagrams, graphs, and tables [21]. However, not many banks have reported quantitative/monetary information in their annual reports adequately. Further, there is a little consistency in the types of environmental information disclosed from year to year.

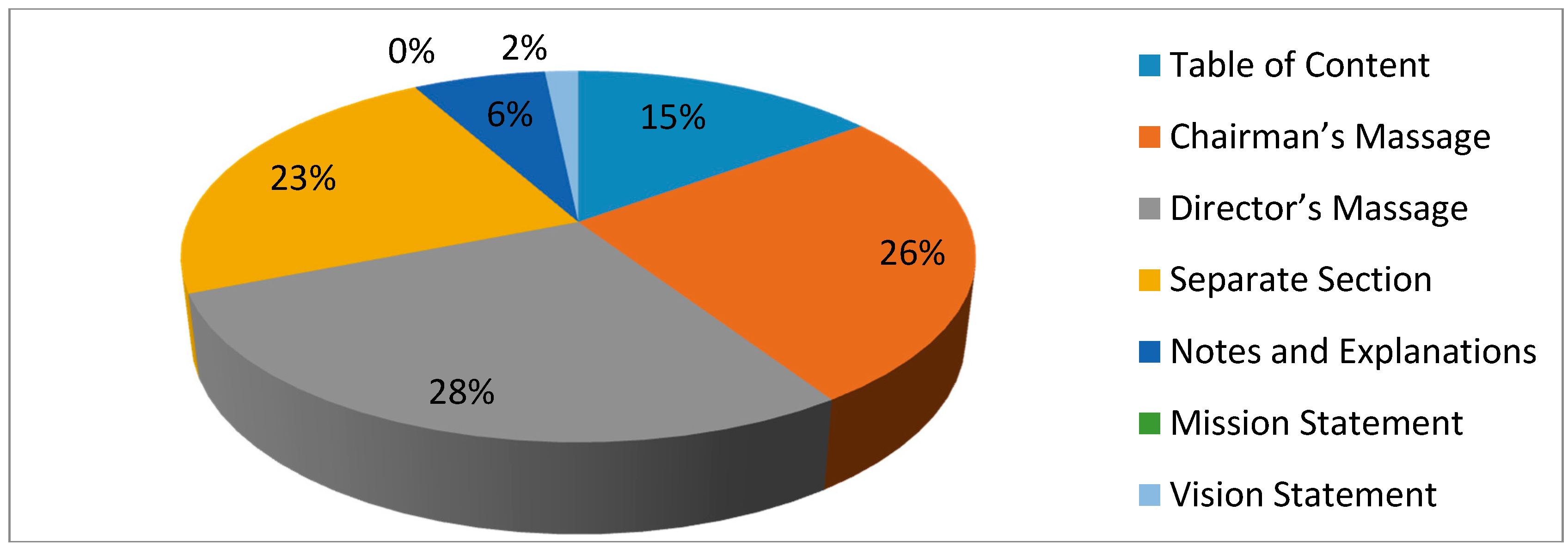

5.2.3. Environmental Information Disclosing Section

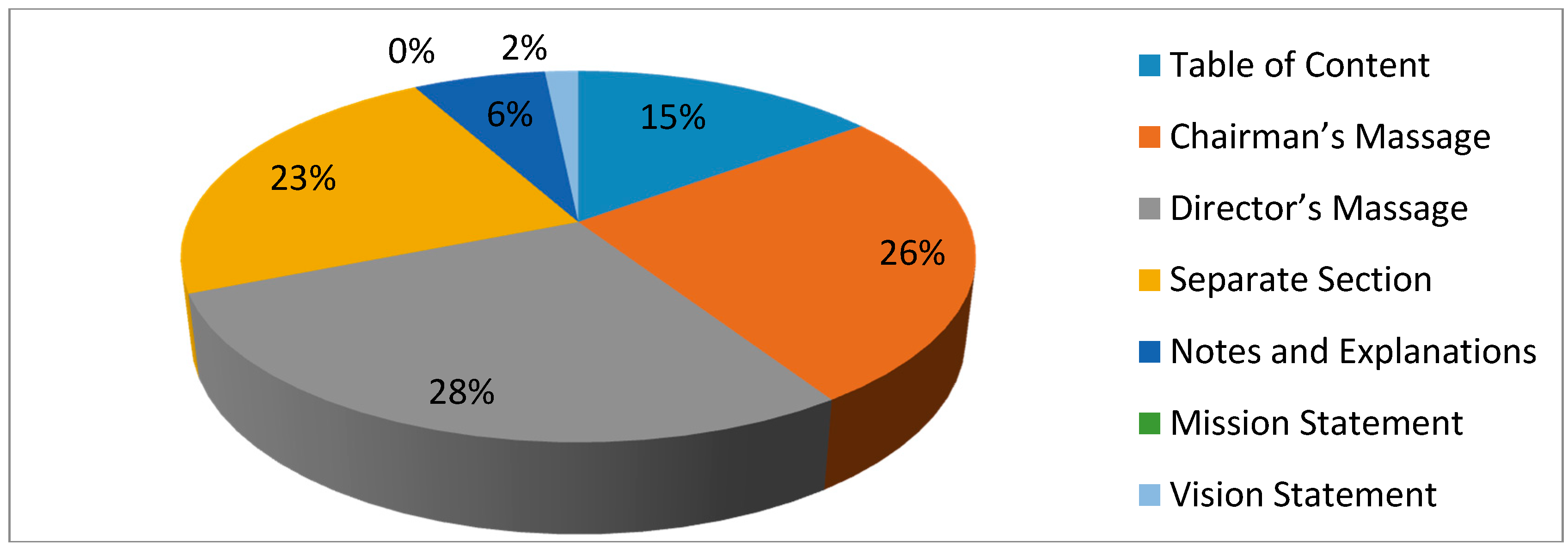

Environmental information can be disclosed in various sections in the annual report, such as the table of contents, financial statements, separate sections, and the chairman’s or director’s message [44]. From Figure 3, we see that most companies studied made environmental disclosures in the table of contents, separate sections, or chairman’s/director’s message. In fact, 71% of sample banks reported environmental information through separate environmental sections in the annual report. Only ten banks provided environmental information via footnotes in the annual report for the period 2012 to 2014. Some banking companies used other locations for environmental disclosure, such as the first page of the annual report, the vision statement, or booklets enclosed with annual reports. One bank used the vision statement only for disclosing information about the environment. Though every bank articulated a mission statement, none of the banks examined mentioned the environment in their mission statements.

6. Conclusions and Managerial Implications

The findings of the study reveal that environmental accounting concepts and reporting by listed Bangladeshi banking companies are still developing. The study involved an analysis of the annual reports of selected banks for the period 2010 to 2014 to examine how environmental issues are reported. A model with 12 categories for EAR disclosure scoring scheme was designed. These categories provide a better understanding of banking companies’ environmental policies and strategies. Bangladeshi banking companies promote diversified environmental functions throughout the country and contribute money for improvements to society and the environment. Banking companies support and disclose information mainly for green banking, renewable financing and energy savings, but they must focus more on waste, air, and water management strategies. To combat global warming and the country’s vulnerability in these areas, Bangladesh banks are becoming more focused on effective energy use. Thus, they should initiate more programs to build awareness among stakeholders and introduce awards to encourage individuals and organizations to work together toward creating a green Bangladesh. Organizations have environmental policies and separate departments for green or sustainable banking, representing a tremendous effort in the environmental sector. The framework of the 12 areas of EAR ensures a vivid picture of banks’ current EAR policies and strategies, and the resulting findings of the study will help policy makers and implementers reduce gaps in environmental investments and policy circulation. Presently, Bangladeshi banks are providing both qualitative and quantitative information in their reports. More than 90% of banking companies disclosed both financial and nonfinancial information for the study period. In addition, more than 70% of banking companies disclosed environmental information in a different section of the annual report, indicating the commitment of top management to EAR. Disclosing information in a separate section of the annual report as well as in the chairman’s or director’s message shows increased efforts in terms of EAR performance. However, the absence of EAR information from sample banks’ mission and financial statements shows a lack of long-term corporate policies and strategies. This study also explored the legal framework of EAR in Bangladesh. We observed that there are enough laws but a lack of political and organizational commitment in Bangladesh to compliance.

Furthermore, any disclosure creates corporate images for society and stakeholders [62,85]. As to increasing the corporate reputation, we believe Bangladeshi banking sectors will flourish because of their present practices and efforts aimed at sustainability. Stakeholders and legitimacy theories support a possible positive relationship between corporations’ EAR disclosure and their overall financial performances. EAR disclosure enhances banking companies’ long term environmental policy and strategy that attracts stakeholder’s engagement and social reputation. Also, EAR disclosure can secure legitimacy for banking companies from the society and diverse stakeholders.

The results of this study contribute to the existing knowledge on EAR in Bangladesh, mainly for management. The corporate manager is now able to identify the gap in environmental activities in 12 areas. The scoring model is used to collect EAR information in different years, comprehensively suggesting the strong and weak areas of the banks. This study also has implications for policy makers in Bangladesh’s government, especially regarding non-performing environmental laws. Moreover, the findings of this study should strongly motivate Bangladesh bank policy makers to review green banking guidelines. They also have a practical implication in terms of sustainability reporting. The results suggest that corporate laws of Bangladesh could be improved by including enough social and environmental provisions to ensure that social, environmental, CSR, human resource, climate change, and sustainability reporting and practices will become more holistic over time. It is also recommended that professional accounting bodies of Bangladesh, along with international and government policy makers, develop a separate conceptual framework on EAR for the financial and nonfinancial sectors of the country with specified objectives, assumptions, qualitative characteristics, and application consequences for companies.

Despite the important implications of this study, a limitation is the size of the sample. The analysis included only 20 listed companies. Additionally, the study is descriptive in nature. Further empirical research could be conducted to include all listed financial companies so that a significant hypothesis could be developed and tested.

Acknowledgments

This work is financially supported by Korea Ministry of Environment (MOE) as “Graduate School specialized in Climate Change”.

Author Contributions

Md. Abdul Kaium Masud carried out the empirical studies and literature review and drafted the manuscript; Seong Mi Bae participated in the design of the study and the statistical analysis; Jong Dae Kim helped to draft and review the manuscript and communicated with the editor of the journal. All authors read and approved the final manuscript.

Conflicts of Interest

The authors declare that they have no competing interests.

Appendix A

{kind=link}

{kind=link}

{kind=link}

Table A1.

List of Banks Selected for the Sample.

| Al-Arafah Islami Bank Ltd. (AAIBL) BRAC Bank Ltd. (BRAC) Bank Asia Ltd. (BAL) City Bank Ltd. (CBL) Dutch Bangla Bank Ltd. (DBBL) EXIM Bank Ltd. (EXIM) Eastern Bank Ltd. (EBL) First Security Islami Bank Ltd. (FSIBL) ICB Islami Bank Ltd. (ICB) IFIC Bank Ltd. (IFIC) | Islami Bank Bangladesh Ltd. (IBBL) Jamuna Bank Ltd. (JBL) Mercantile Bank Ltd. (MBL) One Bank Ltd. (OBL) Prime Bank Ltd. (PBL) South East Bank Ltd. (SEBL) Social Islami Bank Ltd. (SoIBL) Shahjalal Islami Bank Ltd. (ShIBL) Standard Bank Ltd. (SBL) United Commercial Bank Ltd. (UCB) |

Appendix B

Table A2.

Environmental Accounting & Reporting Score (EARS) Coding.

| EARS Code No. | EARS Code Items |

|---|---|

| C1 | Air pollution and control disclosure |

| C2 | Water pollution and control disclosure |

| C3 | Waste management and investment disclosure |

| C4 | Renewable energy and investment disclosure |

| C5 | Energy savings and improvements disclosure |

| C6 | Environmental, ecological and carbon management policy and strategy related disclosure |

| C7 | Award and appreciation for environmental initiatives and protections related disclosure |

| C8 | Separate department of environment, CSR and green banking disclosure |

| C9 | Green banking initiatives, policy, strategy and implementation disclosure |

| C10 | Tree plantation and forestry disclosure |

| C11 | Environmental awareness, training & education related disclosure |

| C12 | Climate change & global warming disclosure |

References

- World Health Organization. Available online: http://www.who.int/phe/publications/air-pollution-global-assessment/en/ (accessed on 1 October 2016).

- The Daily Star. Available online: http://www.thedailystar.net (accessed on 4 January 2016).

- Masud, M.A.K.; Hossain, M.S.; Khan, S. Environmental Accounting Concept and Reporting Practice: Evidence from Banking Sector of Bangladesh. Presented at the 1st Dhaka International Business and Social Science Research Conference, Dhaka, Bangladesh, 20–22 January 2016. [Google Scholar]

- Nurunnabi, M. Who cares about climate change reporting in developing countries? The market response to, and corporate accountability for, climate change in Bangladesh. Environ. Dev. Sustain. A Multidiscip. Approach Theory Pract. Sustain. Dev. 2015, 17. [Google Scholar] [CrossRef]

- Hubbard, G. Measuring organizational performance: Beyond the triple bottom line. Bus. Strateg. Environ. 2009, 18, 177–191. [Google Scholar] [CrossRef]

- Dilling, P.F. Sustainability reporting in a global context: What are the characteristics of corporations that provide high-quality sustainability reports-an empirical analysis? Int. Bus. Econ. Responsib. J. 2010, 9, 19–30. [Google Scholar] [CrossRef]

- Elijido-Ten, E. The impact of sustainability and balanced scorecard disclosures on market performance: Evidence from Australia’s top 100. J. Appl. Manag. Account. Res. 2011, 9, 59–73. [Google Scholar]

- Dissanayake, D.; Tilt, C.; Lobo, M.X. Sustainability reporting by listed companies in Sri Lanka. J. Clean. Prod. 2016, 30, 1–14. [Google Scholar] [CrossRef]

- Rahman, S.R.; Muttakin, M.B. Corporate Environmental Reporting Practices in Bangladesh—A Study of Some Selected Companies. Cost Manag. 2005, 33, 13–21. [Google Scholar]

- The SIGMA Guidelines-Toolkit: SIGMA Environmental Accounting Guide. SIGMA Project: London, UK, 2003. Available online: http://www.projectsigma.co.uk/Toolkit/SIGMAEnvironmentalAccounting.pdf (access on 20 September 2014).

- Bose, S. Environmental Accounting and Reporting in Fossil Fuel Sector: A Study on Bangladesh Oil, Gas and Mineral Corporation (Petrobangla). Cost Manag. 2006, 34, 53–67. [Google Scholar]

- Savage, A.A. Environmental Reporting: Stakeholders’ Perspective; Working Paper 94; University of Port Elizabeth: Port Elizabeth, South Africa, 1994. [Google Scholar]

- Belal, A.R.; Copper, S.M.; Khan, N.A. Corporate Environmental Responsibility and Accountability: What Chance in Vulnerable Bangladesh. Crit. Perspect. Account. 2015, 33, 44–58. [Google Scholar] [CrossRef]

- Gupta, V.K. Environmental Accounting and Reporting—An Analysis of Indian Corporate Sector. Available online: http://www.wbiconpro.com/110-Gupta.pdf or http://business.wesrch.com/mobile/paper-details/pdf-BU1H5H4B3ABQM-environmental-accounting-and-reporting (accessed on 10 December 2012).

- Confederation of Asia and Pacific Accountants. Annual Report 2009. Available online: http://www.capa.com.my/wp-content/uploads/2017/02/CAPA_AnnualReport_2009_FINAL.pdf (accessed on 22 September 2017).

- Government of Bangladesh. Annual Budget Published by the Ministry of Finance. 2015. Available online: http://www.mof.gov.bd (accessed on 10 July 2015).

- Khan, M.H.U.Z.; Islam, M.A.; Fatima, J.K.; Ahmed, K. Corporate sustainability reporting of major commercial banks in line with GRI: Bangladesh evidence. Soc. Responsib. J. 2011, 7, 347–363. [Google Scholar] [CrossRef]

- Khan, M.T.A. Sustainability Reporting under global reporting initiative. Cost Manag. 2016, 43, 4–17. [Google Scholar]

- Sayaduzzaman, M.; Masud, M.A.K. Corporate Social Responsibility Practices of Private Commercial Banks in Bangladesh: A Comparative Study. Cost Manag. 2012, 40, 34–39. [Google Scholar]

- Bangladesh Bank. Review of CSR Activities of Financial Sector. Published by Green Banking and CSR Department. 2013, 2014, 2015. Available online: https://www.bb.org.bd/pub/index.php (accessed on 2 November 2016).

- Ullah, M.H.; Rahman, M.A. Corporate social responsibility reporting practices in banking companies in Bangladesh: Impact of regulatory change. J. Financ. Report. Account. 2015, 13, 200–225. [Google Scholar] [CrossRef]

- Sobhani, F.A.; Arman, A.; Zianuddin, U. Revisiting the Practices of Corporate Social and Environmental Disclosure in Bangladesh. Corp. Soc. Responsib. Environ. Manag. 2009, 16, 167–183. [Google Scholar] [CrossRef]

- Sobhani, F.A.; Arman, A.; Zianuddin, U. Sustainability disclosure in annual reports and websites: A study of the banking industry in Bangladesh. J. Clean. Prod. 2011, 23, 75–85. [Google Scholar] [CrossRef]

- Belal, A.R. Environmental Reporting in Developing Countries: Empirical Evidence from Bangladesh. Eco-Manag. Audit. 2000, 7, 114–121. [Google Scholar] [CrossRef]

- Imam, S. Environmental Reporting in Bangladesh. Soc. Environ. Account. 1999, 19, 12–14. [Google Scholar] [CrossRef]

- Shil, N.; Iqubal, M. Environmental Disclosure-Bangladesh Perspective. Cost Manag. 2005, 33, 85–93. [Google Scholar]

- Hossain, M.; Islam, K.; Andrew, J. Corporate social and environmental disclosure in developing countries: Evidence from Bangladesh. In Proceedings of the Asian Pacific Conference on International Accounting Issues, Maui, HI, USA, 18 October 2006; Available online: http://ro.uow.edu.au/commpapers/179/ (accessed on 5 March 2014).

- Khan, M.H.U.Z. The Effect of Corporate Governance elements on Corporate Social Responsibility (CSR) Reporting: Empirical Evidence from Private Commercial Banks of Bangladesh. Int. J. Law Manag. 2010, 52, 82–109. [Google Scholar] [CrossRef]

- Bose, S.; Khan, B.Z.; Rashid, A.; Islam, S. What drives green banking disclosure? An institutional and corporate governance perspective. Asia Pac. J. Manag. 2017. [Google Scholar] [CrossRef]

- Khan, M.H.U.Z.; Halabi, A.; Samy, M. CSR Reporting Practice: A study of Selected Banking Companies in Bangladesh. Soc. Responsib. J. 2009, 5, 344–357. [Google Scholar] [CrossRef]

- Masud, M.A.K.; Kabir, H.M. Corporate social responsibility evaluation by different levels of management of Islamic banks and traditional banks: Evidence from banking sector of Bangladesh. Probl. Perspect. Manag. 2016, 14, 194–202. [Google Scholar] [CrossRef]

- Killic, M.; Kuzey, C.; Uyar, A. The impact of ownership and board structure on corporate social responsibility reporting in the Turkish banking industry. Corp. Gov. 2015, 15, 357–372. [Google Scholar] [CrossRef]

- Lu, Y.; Abeysekera, I.; Cortese, C. Corporate social responsibility reporting quality, board characteristics and corporate social reputation: Evidence from China. Pac. Account. Rev. 2015, 27, 95–118. [Google Scholar] [CrossRef]

- Comyns, B. Determinants of GHG reporting: An analysis of global oil and gas companies. J. Bus. Ethics 2014. [Google Scholar] [CrossRef]

- Villers, C.; Naiker, V.; Staden, C. The effects of board characteristics on firm environmental performance. J. Manag. 2011, 37, 1636–1663. [Google Scholar] [CrossRef]

- Freeman, R.; Harrison, J.; Wicks, A.; Parmar, B.; Colle, S. Stakeholder Theory: The State of the Art; Cambridge University Press: New York, NY, USA, 2010. [Google Scholar]

- KPMG. The KPMG Survey of Corporate Responsibility Reporting 2017. Available online: https://assets.kpmg.com/content/dam/kpmg/pdf/2015/08/kpmg-survey-of-corporate-responsibility-reporting-2013.pdf (accessed on 5 August 2015).

- Gray, R.H.; Owen, D.; Adams, C. Accounting & Accountability: Changes and Challenges in Corporate Social and Environmental Reporting; Prentice Hall: Upper Saddle River, NJ, USA, 1996. [Google Scholar]

- Suchman, M.C. Managing legitimacy: Strategic and institutional approaches. Acad. Manag. Rev. 1995, 20, 571–610. [Google Scholar]

- Masud, M.A.K.; Hossain, M.S. Corporate Social Responsibility Reporting Practices in Bangladesh: A Study of Selected Private Commercial Banks. IOSR J. Bus. Manag. 2012, 6, 42–47. [Google Scholar] [CrossRef]

- Sahay, A. Environmental reporting by Indian corporations. Corp. Soc. Responsib. Environ. Manag. 2004, 11, 12–22. [Google Scholar] [CrossRef]

- Azim, M.I.; Ahmed, S.; Islam, M.S. Corporate social reporting practice: Evidence from listed companies in Bangladesh. J. Asia Pac. Bus. 2009, 10, 130–145. [Google Scholar] [CrossRef]

- Belal, A.R.; Owen, D.L. The view of corporate managers on the current state of, and future prospects for, social reporting in Bangladesh: An engagement-based study. Account. Audit. Account. J. 2007, 20, 472–494. [Google Scholar] [CrossRef]

- Hoque, A.; Clarke, A.; Huang, L. Lack of Stakeholder Influence on Pollution Prevention: A Developing Country Perspective. Organ. Environ. 2016, 1–19. [Google Scholar] [CrossRef]

- Meena, R. Green banking as initiative for sustainable development. Glob. J. Manag. Bus. Stud. 2013, 3, 1181–1186. [Google Scholar]

- Teoh, H.Y.; Pin, F.W.; Joo, T.T.; Ling, Y.Y. Environmental Disclosures-Financial Performance Link: Further Evidence from Industrializing Economy Perspective. 2016. Available online: http://citeseerx.ist.psu.edu/viewdoc/summary?doi=10.1.1.202.164 (accessed on 30 September 2016).

- Fifka, M. The development and state of research on social and environmental reporting in global comparison. J. Betriebswirtsch. 2012, 62, 45–84. [Google Scholar] [CrossRef]

- Choi, J.S. An investigation of the initial voluntary environmental disclosures made in Korean semi-annual financial reports. Pac. Account. Rev. 1998, 11, 73–102. [Google Scholar]

- Baughn, C.C.; McIntosh, J.C. Corporate social and environmental responsibility in Asian countries and other geographical regions. Corp. Soc. Responsib. Environ. Manag. 2007, 14, 189–205. [Google Scholar] [CrossRef]

- Global Reporting Initiative. The 2016 Sustainability Leaders: A Globe Scan/Sustainability Survey. 2010–2016. Available online: https://www.globalreporting.org/Pages/default.aspx (accessed on 3 October 2016).

- Kabir, M.H.; Akinnusi, D.A. Corporate social and environmental accounting information reporting practices in Swaziland. Soc. Responsib. J. 2012, 8, 156–173. [Google Scholar] [CrossRef]

- Tsang, E.W.K. A longitudinal study of corporate social reporting in Singapore: The case of the banking, food and beverages and hotel industries. Account. Audit. Account. J. 1998, 11, 624–635. [Google Scholar] [CrossRef]

- Jamali, D.; Mishak, R. Corporate social responsibility (CSR): Theory and practice in a developing country context. J. Bus. Ethics 2007, 72, 243–262. [Google Scholar] [CrossRef]

- Rahman, S.R. Corporate social reporting in India-A view from the top. Glob. Bus. Rev. 2006, 7, 313–324. [Google Scholar] [CrossRef]

- Sawani, Y.; Mustaffa, M.Z.; Darus, F. Preliminary insights on sustainability reporting and assurance practices in Malaysia. Soc. Responsib. J. 2010, 6, 627–645. [Google Scholar] [CrossRef]

- Hossain, I.; Chowdhury, A. Environmental Reporting: A study of the listed companies in Bangladesh. Cost Manag. 2014, 42, 36–46. [Google Scholar]

- Dutta, P.; Bose, S. Corporate Environmental Reporting on the Internet in Bangladesh: An Exploratory Study. Int. Rev. Bus. Res. Pap. 2008, 4, 38–150. [Google Scholar]

- The Daily Prothom-Alo. Available online: http://www.prothom-alo.com (accessed on 5 January 2016).

- UNESCO. Available online: http://www.unescobkk.org/fileadmin/user_upload/library/OPI/Documents/UNESCO_in_the_news_2014/141130Sundarbans_may_lose_its_heritage_status__UNESCO.pdf (accessed on 10 October 2016).

- Guthrie, J.; Parker, L. Corporate Social Disclosure Practice: A Comparative International Analysis. Adv. Public Interest Account. 1990, 3, 159–175. [Google Scholar]

- Singh, D.R.; Ahuja, J.M. Corporate social reporting in India. Int. J. Account. Educ. Res. 1983, 18, 151–169. [Google Scholar]

- Adams, C.A. Internal organizational factors influencing corporate social and ethical reporting: Beyond current theorizing. Account. Audit. Account. J. 2002, 15, 223–250. [Google Scholar] [CrossRef]

- Adams, C.A.; Hill, W.Y.; Roberts, C.B. Corporate Social Reporting Practices in Western Europe: Legitimating Corporate Behavior? Br. Account. Rev. 1998, 30, 1–21. [Google Scholar] [CrossRef]

- Gray, R.; Kouhy, R.; Lavers, S. Corporate social and environmental reporting: A review of the literature and a longitudinal study of UK disclosure. Account. Audit. Account. J. 1995, 8, 47–77. [Google Scholar] [CrossRef]

- Islam, M.A.; Deegan, C. Motivations for an organization within a developing country to report social responsibility information: Evidence from Bangladesh. Account. Audit. Account. J. 2008, 21, 850–874. [Google Scholar] [CrossRef] [Green Version]

- Hossain, D.M.; Bir, A.T.; Tarique, K.M.; Momen, A. Disclosure of Green Banking Issues in the Annual Reports: A Study on Bangladeshi Banks. Middle East J. Bus. 2016, 7, 19–30. [Google Scholar] [CrossRef]

- Bangladesh Bank. Available online: https://www.bb.org.bd/fnansys/bankfi.php (accessed on 24 August 2017).

- Dhaka Stock Exchange. Available online: http://www.dsebd.org/companylistbyindustry.php?industryno=11 (accessed on 24 August 2017).

- Krippendorf, K. Content Analysis: An Introduction to Its Methodology; Sage: New York, NY, USA, 1980. [Google Scholar]

- Hossain, M.; Tan, L.; Adams, M. Voluntary disclosure in an emerging capital market: Some empirical evidence from companies listed on the Kuala Lumpur stock exchange. Int. J. Account. 1994, 29, 334–351. [Google Scholar]

- Ahmed, K.; Nicholls, D. The impact of non-financial company characteristics on mandatory compliance in developing countries: The case of Bangladesh. Int. J. Account. 1994, 29, 60–77. [Google Scholar]

- Beattie, V.; Jones, M.J. The use and abuse of graphs in annual reports: A theoretical framework and empirical study. Account. Bus. Res. 1992, 22, 291–303. [Google Scholar] [CrossRef]

- Beattie, V.; Jones, M.J. An empirical study of graphical format choices in charity annual reports. Financ. Account. Manag. 1994, 10, 215–236. [Google Scholar] [CrossRef]

- Zeghal, D.; Ahmed, S.A. Comparison of social responsibility information disclosure media used by Canadian firms. Account. Audit. Account. J. 1990, 3, 38–53. [Google Scholar] [CrossRef]

- Unerman, J. Methodology issues-reflections on quantification in corporate social reporting content analysis. Account. Audit. Account. J. 2000, 13, 667–681. [Google Scholar] [CrossRef]

- Milne, M.J.; Adler, R.W. Exploring the reliability of social and environmental disclosures content analysis. Account. Audit. Account. J. 1999, 12, 237–256. [Google Scholar] [CrossRef]

- Hackston, D.; Milne, M.J. Some determinants of social and environmental disclosures in New Zealand companies. Account. Audit. Account. J. 1996, 9, 77–108. [Google Scholar] [CrossRef]

- Wiseman, J. An evaluation of environmental disclosures made in corporate annual reports. Account. Organ. Soc. 1982, 7, 53–63. [Google Scholar] [CrossRef]

- Cooke, T.E. The impact of size, stock market listing and industry type on disclosure in the annual reports of Japanese listed corporations. Account. Bus. Res. 1992, 22, 229–237. [Google Scholar] [CrossRef]

- Clarkson, P.; Li, Y.; Richardson, G.; Vasvari, F. Revisiting the Relation between Environmental Performance and Environmental Disclosure: An Empirical Analysis. Account. Organ. Soc. 2008, 33, 303–327. [Google Scholar] [CrossRef]

- Bangladesh Bank. Annual Report on Green Banking. Green Banking Wing. 2012. Available online: https://www.bb.org.bd/pub/index.php (accessed on 2 November 2016).

- Islamic Bank Bangladesh Ltd. Annual Report, 2014. Available online: http://www.islamibankbd.com/abtIBBL/financial_report.php (accessed on 21 August 2017).

- Azim, M.I.; Ahmed, E.; D’Netto, B. Corporate social disclosure in Bangladesh: A study of the financial sector. Int. Rev. Bus. Res. Pap. 2011, 7, 37–55. [Google Scholar]

- Bank Asia Ltd. Annual Report, 2014. Available online: http://www.bankasia-bd.com/home/annual_reports (accessed on 21 August 2017).

- Gray, R. Social, environmental and sustainability reporting and organizational value creation? Whose value? Whose creation? Account. Audit. Account. J. 2006, 19, 793–819. [Google Scholar] [CrossRef]

Figure 1.

Total EAR information disclosure by banks.

Figure 2.

Types of EAR information.

Figure 3.

Disclosing section of EAR information.

Table 1.

Legal status of environmental reporting in Bangladesh.

| EAR Legal Status in Bangladesh | |

|---|---|

| 1. | Ministry of Environment and Forests |

| 2. | Forest Department |

| 3. | Department of Environment |

| 4. | Planning Commission |

| 5. | Bank Companies Act, 1991 |

| 6. | National Environment Policy, 1992 |

| 7. | Financial Institutions Act, 1993 |

| 8. | Securities and Exchange Commission Act 1993 |

| 9. | Financial Institutions Act, 1993 |

| 10. | Companies Act, 1994 |

| 11. | National Environmental Management Action Plan, 1995 |

| 12. | Environmental Conversion Act, 1995 |

| 13. | Environmental Conversion Rules, 1997 |

| 14. | Bankruptcy Act, 1997 |

| 15. | Ozone Depleting Substances Rules, 2004 |

| 16. | Environmental Court Act, 2010 |

| 17. | Climate Change Trust Act, 2010 |

| 18. | Credit Risk Management Industry Best Practices by Bangladesh Bank in 2010 |

| 19. | Environmental Risk Management Guidelines, 2011 |

| 20. | Policy Guidelines for Green Banking, 2011 |

| 21. | Finance Act (changes from time to time) |

| 22. | Bangladesh Biodiversity Act, 2012 |

| 23. | Securities and Exchange Rules |

| 24. | Bangladesh Bank Rules |

| 25. | Tax Ordinances |

| 26. | IFIC guidelines |

| 27. | IASC guidelines |

| 28. | FASB guidelines |

| 29. | BFRS guidelines |

Source: Masud and Kabir [31], and authors’ own compilation.

Table 2.

Sample selection process.

| Sample Selection Criteria | Banks |

|---|---|

| Total banks [67] | 57 |

| Banks not listed on Dhaka Stock Exchange (DSE) | (27) |

| Banks listed on DSE [68] | 30 |

| Banks with missing annual reports | (10) |

| Final sample banks | 20 |

Table 3.

Twelve categories of emerging environmental information.

| EAR Categories | Sources |

|---|---|

| Air pollution, water pollution, waste management, environmental policy, award for environmental protection, separate department of environment | Wiseman [76] |

| Green banking, tree plantation, environmental awareness training & education, renewable energy, climate change risk | Ullah and Rahman [21] |

| Energy-saving | Kabir and Akinnusi [51] |

Source: Developed by the authors.

Table 4.

Example of environmental project information.

| Name of Bank | Major Environmental Financing Areas |

|---|---|

| Islami Bank | Effluent Treatment Plant (ETP), biogas plants, solar home systems, solar panel trades, bio-fertilizer plants, tunnel kilns, installation of zigzag kilns, waste and hazardous disposal plants, waste paper recycling plants, waste battery recycling plants, LED bulb production, safe/clean water supply projects, improved cooking stoves, green projects (at zero rate of return), electricity generation from rice husks, rice bran oil production, e-commerce and e-business promotions, investing via online banking |

| Brac Bank | Solar energy, green projects, ETP, double hull oil tankers, environment-friendly brickfields, e-commerce and e-business promotions, investing via online banking |

| EXIM Bank | ETP, renewable energy, clean water supply, wastewater treatment plants, recycling of harmful waste, solid and hazardous waste disposal plants, biogas plants, bio-fertilizer plants, environment-friendly brickfields, e-commerce and e-business promotions, investing via online banking |

| Bank Asia | Renewable energy and carbon offset projects, reducing energy and resource consumption, solar home systems, consumption of water, solar energy, biogas, ETP, HHK projects, greenhouse gas emission projects, waste management, e-commerce and e-business promotions, investing via online banking |

| Prime Bank | ETP, HHK projects, solid waste management, energy and water management, renewable energy projects, green travel, and e-commerce and e-business promotions, investing via online banking |

Source: Annual reports of selected banks.

Table 5.

Sample banks’ total EAR disclosures in 12 categories 2010–2014.

| ER Categories/Banks | Disclosing EAR Information | Percentage (%) |

|---|---|---|

| AAIBL | 10 | 83 |

| BRAC | 12 | 100 |

| BAL | 12 | 100 |

| CBL | 9 | 75 |

| DBBL | 12 | 100 |

| EXIM | 11 | 92 |

| EBL | 11 | 92 |

| FSIBL | 8 | 67 |

| ICB | 9 | 75 |

| IFIC | 11 | 92 |

| IBBL | 12 | 100 |

| JBL | 9 | 75 |

| MBL | 10 | 83 |

| OBL | 8 | 67 |

| PBL | 10 | 83 |

| SEBL | 12 | 100 |

| SoIBL | 11 | 92 |

| ShIBL | 8 | 67 |

| SBL | 9 | 75 |

| UCB | 12 | 100 |

| Average | 10 | 85 |

Source: Developed by the authors.

Table 6.

Total EAR disclosure of sample banks 2010–2014.

| EARS Code/Banks | C1 | C2 | C3 | C4 | C5 | C6 | C7 | C8 | C9 | C10 | C11 | C12 |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| AAIBL | 2 | 2 | 0 | 4 | 5 | 4 | 0 | 3 | 5 | 1 | 4 | 3 |

| BRAC | 1 | 2 | 4 | 5 | 3 | 2 | 1 | 3 | 3 | 2 | 1 | 1 |

| BAL | 4 | 4 | 4 | 4 | 4 | 3 | 3 | 4 | 4 | 1 | 4 | 4 |

| CBL | 0 | 0 | 1 | 3 | 3 | 4 | 0 | 2 | 4 | 1 | 4 | 1 |

| DBBL | 3 | 3 | 3 | 4 | 3 | 3 | 3 | 3 | 5 | 5 | 3 | 5 |

| EXIM | 0 | 2 | 2 | 2 | 2 | 4 | 2 | 2 | 4 | 3 | 2 | 4 |

| EBL | 1 | 4 | 3 | 5 | 5 | 4 | 2 | 2 | 4 | 0 | 5 | 2 |

| FSIBL | 1 | 1 | 0 | 2 | 2 | 1 | 0 | 0 | 3 | 3 | 0 | 1 |

| ICB | 5 | 5 | 0 | 4 | 4 | 4 | 0 | 0 | 4 | 2 | 4 | 5 |

| IFIC | 4 | 4 | 0 | 5 | 4 | 4 | 1 | 4 | 4 | 4 | 5 | 4 |

| IBBL | 5 | 5 | 4 | 5 | 5 | 5 | 3 | 3 | 5 | 5 | 5 | 5 |

| JBL | 0 | 2 | 2 | 2 | 2 | 2 | 0 | 0 | 2 | 2 | 2 | 2 |

| MBL | 0 | 4 | 2 | 2 | 4 | 1 | 0 | 4 | 4 | 2 | 3 | 2 |

| OBL | 0 | 0 | 1 | 4 | 4 | 4 | 0 | 3 | 4 | 0 | 4 | 1 |

| PBL | 4 | 4 | 4 | 5 | 4 | 4 | 0 | 4 | 5 | 0 | 4 | 4 |

| SEBL | 2 | 2 | 2 | 2 | 3 | 2 | 2 | 3 | 2 | 3 | 2 | 1 |

| SoIBL | 1 | 1 | 0 | 3 | 2 | 3 | 3 | 3 | 3 | 2 | 2 | 1 |

| ShIBL | 0 | 0 | 0 | 4 | 4 | 3 | 0 | 3 | 4 | 1 | 4 | 2 |

| SBL | 4 | 4 | 0 | 5 | 5 | 4 | 0 | 4 | 4 | 0 | 4 | 5 |

| UCB | 3 | 4 | 3 | 5 | 5 | 5 | 3 | 4 | 4 | 3 | 5 | 5 |

| Total | 40 | 53 | 35 | 75 | 73 | 66 | 23 | 54 | 77 | 40 | 67 | 58 |

| Average EARS on Bank | 2.00 | 2.65 | 2.06 | 3.75 | 3.65 | 3.30 | 1.28 | 2.84 | 3.85 | 2.22 | 3.35 | 2.90 |

Source: Developed by the authors.

Table 7.

Ranking of sample banks based on EAR disclosure over five years.

| Rank | Bank Name | Total Disclosures | Rank | Bank Name | Total Disclosure |

|---|---|---|---|---|---|

| 1 | IBBL | 55 | 8 | EXIM | 29 |

| 2 | UCB | 49 | 9 | BRAC | 28 |

| 3 | BAL | 43 | 9 | MBL | 28 |

| 3 | DBBL | 43 | 10 | SEBL | 26 |

| 3 | IFIC | 43 | 11 | OBL | 25 |

| 4 | PBL | 42 | 11 | ShIBL | 25 |

| 5 | SBL | 39 | 12 | SoIBL | 24 |

| 6 | EBL | 37 | 13 | CBL | 23 |

| 6 | ICB | 37 | 14 | JBL | 18 |

| 7 | AAIBL | 33 | 15 | FSIBL | 14 |

Source: Developed by authors based on EAR scoring.

Table 8.

Yearly disclosure of EAR.

| EARS Categories | 2010 | 2011 | 2012 | 2013 | 2014 |

|---|---|---|---|---|---|

| C1 | 2 | 7 | 8 | 11 | 12 |

| C2 | 3 | 9 | 10 | 15 | 16 |

| C3 | 2 | 2 | 7 | 11 | 13 |

| C4 | 7 | 13 | 15 | 20 | 20 |

| C5 | 5 | 13 | 15 | 20 | 20 |

| C6 | 2 | 11 | 15 | 18 | 20 |

| C7 | 0 | 1 | 5 | 7 | 10 |

| C8 | 0 | 5 | 14 | 17 | 18 |

| C9 | 4 | 15 | 18 | 20 | 20 |

| C10 | 4 | 5 | 9 | 9 | 13 |

| C11 | 4 | 12 | 13 | 19 | 19 |

| C12 | 5 | 10 | 11 | 15 | 17 |

| Total Disclosure | 38 | 103 | 140 | 182 | 198 |

| Percentage (%) of EAR disclosure | 16 | 43 | 58 | 76 | 83 |

Source: Developed by the author.

Table 9.

EAR disclosure comparison 2010–2014.

| Year | Mean | Median | Std. Dev. | Minimum | Maximum | Mode |

|---|---|---|---|---|---|---|

| 2010 | 3.167 | 3.5 | 2.082 | 0 | 7 | 2 |

| 2011 | 8.583 | 9.5 | 4.562 | 1 | 15 | 13 |

| 2012 | 11.667 | 12 | 3.939 | 5 | 18 | 15 |

| 2013 | 15.167 | 16 | 4.629 | 7 | 20 | 20 |

| 2014 | 16.500 | 17.5 | 3.631 | 10 | 20 | 20 |

| 2011–2014 | 12.979 | 13 | 5.134 | 1 | 20 | 20 |

| Comparison between 2010 and 2011–2014 | t = 7.55 p = 0.001 | z = 5.55 p = 0.01 | ||||

© 2017 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Masud, M.A.K.; Bae, S.M.; Kim, J.D. Analysis of Environmental Accounting and Reporting Practices of Listed Banking Companies in Bangladesh. Sustainability 2017, 9, 1717. https://doi.org/10.3390/su9101717

AMA Style

Masud MAK, Bae SM, Kim JD. Analysis of Environmental Accounting and Reporting Practices of Listed Banking Companies in Bangladesh. Sustainability. 2017; 9(10):1717. https://doi.org/10.3390/su9101717

Chicago/Turabian StyleMasud, Md. Abdul Kaium, Seong Mi Bae, and Jong Dae Kim. 2017. "Analysis of Environmental Accounting and Reporting Practices of Listed Banking Companies in Bangladesh" Sustainability 9, no. 10: 1717. https://doi.org/10.3390/su9101717

Note that from the first issue of 2016, this journal uses article numbers instead of page numbers. See further details here.