Tensions in Aspirational CSR Communication—A Longitudinal Investigation of CSR Reporting

College of Business, Dublin Institute of Technology, Dublin 2, Ireland

Sustainability 2017, 9(12), 2202; https://doi.org/10.3390/su9122202

Submission received: 24 October 2017

/

Revised: 15 November 2017

/

Accepted: 15 November 2017

/

Published: 29 November 2017

(This article belongs to the Section Economic and Business Aspects of Sustainability)

Abstract

:A recent emergence of academic discourse within organisation and management scholarship is encouraging organisations to embrace the performative power of aspirational talk within corporate social responsibility (CSR) communication. However, there has been no empirical study to date to investigate the appropriateness of such encouragement. This paper analyses CSR reporting and underlying sensemaking processes to trace how far this academic departure from the dominant discourse of verification and standardisation is reflected and accepted within this practice. The process-focused, longitudinal study is based on a discursive analysis of Nestlé CSR reports, revealing the struggles between forward and backward facing statements, and tracing the discursive management of tensions between talk and action over a period between 2002 and 2016. The discursive analysis is complemented with findings from seven in-depth interviews with Nestlé senior managers and external non-governmental organisation (NGO) stakeholders to provide insights into the underlying organisational sensemaking. Three tension management phases are detected in the reporting shifting from ignoring aspiration to allowing for a dialectic interplay between aspiration and performance. The interview findings support the detection of the three phases, highlight the dialectic interplay between retrospective and prospective sensemaking as part of the iterative reporting, and underscore the importance of stakeholder involvement in the process.

1. Introduction

With the growing embrace of corporate social responsibility (CSR) and sustainability by companies over the past decades, the communication of such initiatives and programmes has increasingly become a substantial challenge for organisations. Consequently, CSR communication is now considered an integral element in building stakeholder support, managing corporate reputation [1], and gaining legitimacy [2,3], and has thus become increasingly relevant to companies investing in CSR programmes.

More recently, a debate has emerged amongst organisational and communication scholars as to whether communication of CSR should take place only in relation to completed and successful CSR, or also in relation to CSR aspirations [4,5,6,7], communication which announces intentions and plans for the future. This polarisation is reflected in the concepts of discursive opening and discursive closing [8]. Discursive opening refers to an environment where issues can be constitutively explored in a productive manner, while discursive closing captures the opposite, negating discussion and debate [8]. On a practical level, CSR communication can be divided into talk (CSR aspirations and intentions to take place in the future) and action (actual organisational CSR practice that has taken place in the past) [6], resulting in organisations having to decide if and how to balance these two elements. Previous research carried out by the author has highlighted that organisational actors experience this as a significant tension, at times even contradiction or paradox [9]. One mainstream communication tool where organisations are commonly faced with balancing talk and action are CSR reports. Within this communication genre, companies disclose CSR-related performance to their stakeholders [10,11], and more recently use the reports for strategic marketing and self-promotion purposes [12]. Thus, tension between talk and action is further reflected in the combination of informational (statement of facts and achievements using concrete language [13]) and promotional elements (idealised statements of what the company aspires to, usually expressed using vague language [7,14]) in the genre of CSR reporting, resulting in hybridity [15].

The academic concept of aspirational CSR talk is relatively recent, and empirical studies examining how this concept is lived and executed in managerial practice are only beginning to emerge [9]. While the transformative capacity of aspirational talk and discursive opening has been highlighted in previous conceptual studies [6,8], research has yet to account fully for the dynamics of using future-oriented CSR communication in an empirical context. This article seeks to address this research gap by taking a tensional approach rooted in paradox theory [16,17,18] to explore aspirational talk, and to demonstrate, by unfolding the tension between talk and action over time, that it is in fact the dialectic framing of the talk–action relationship by the organisation, in combination with stakeholder involvement, that acts as a driver for transformative change in CSR.

Furthermore, this article seeks to add to the emerging body of tension management conceptualisation and paradox theory within communication scholarship [3,19,20,21,22,23,24,25,26], answering calls to unfold tensions and paradoxes longitudinally [16] and illustrating organisational management of the talk–action tension over time. The temporal nature of this study is particularly suited to examine how organisational phenomena such as aspirational talk “emerge, change and unfold over time” [27] (p. 1) and thus adds to process research in management and organisation studies.

To achieve this, the research explores how the interplay/tension between talk and action develops, changes and evolves within the CSR reporting of an international multinational corporation over a 14-year period. This discursive analysis of CSR reporting is then further supplemented by in-depth interviews with Nestlé managers and other key NGO stakeholders to gain insights into the underlying tension management and sensemaking processes. A tensional approach is used to explore the relationship between talk and action and to shed light on the concept of aspirational talk. A general overview of the theoretical concepts informing this research is provided. Then the selection of the sample is explained, and an outline of the research methodology is provided. The manifestation of the talk–action tension in the CSR reports is demonstrated and is linked to the changing terrain of the broader CSR talk–action discourse. This reveals the clashes, but also reinforcement, between conflicting logics of discursive opening and closing in the processes of CSR reporting. The interview findings provide insights into the underlying mechanisms of tension management and organisational sensemaking. After the results are presented, the implications of the findings are discussed and recommendations for future research are developed.

2. Conceptual Foundation

2.1. CSR Communication and Aspirational Talk

CSR communication is considered an integral element of the CSR process to inform stakeholders about CSR initiatives [1] and in facilitating the sensemaking process of organisational members and their stakeholders [28]. While traditionally companies would engage in CSR communication to transmit information and to persuade their audiences, a shift from “traditional” to “alternative” underpinning can be observed in recent years [29], and CSR communication is viewed as a way of co-constructing sustainability/CSR and negotiating its meaning [30,31].

In line with this more constitutive theorising, an academic debate has emerged as to whether CSR communication should take place only in relation to completed and successful CSR, or also in relation to CSR aspirations [4,5,6,7]. This debate highlights two elements within the practice of CSR communication: talk (CSR aspirations and intentions) and action (actual organisational CSR performance), giving rise to “creative tensions” [32].

However, these tensions stemming from the practice of combining CSR talk and action can also be perceived by organisational actors as a paradoxical demand [9]. Often, organisations respond to this by aiming to suppress the paradox and thus reducing the performative potential of aspirational talk. These tensions and contradictions can stem from differences between what is said and what is done, or what is planned and what has been achieved. Due to the aspirational nature of this type of claim making, which does not necessarily find itself rooted in action, decoupling between talk and action may and does take place in some cases [33,34]. Most often, this decoupling in relation to CSR talk and action is viewed as problematic, potentially threatening legitimacy and credibility [35], with calls to focus on sustainability performance and achievements, rather than efforts and intentions [36]. This conflict causes organisations to be wary of making public claims about their CSR programmes for fear of being accused of greenwashing if differences between talk and action are observed [37,38,39] and if external stakeholders feel that the organisation is engaged in excessive self-promotion [40].

2.2. CSR Communication and Sensemaking

While CSR communication may be critiqued as being frequently used for strategic reasons and to persuade, rather than allowing for dialogic, two-way communication between organisations and stakeholders, it is important to highlight the underlying sensemaking processes to generate a more nuanced and balanced view. Sensemaking in the Weickean sense involves “turning circumstances into a situation that is comprehended explicitly in words and that serves as a springboard into action” [41] (p. 409). Cycling between retrospection (looking back and reflecting, focus on action) and prospection (looking into the future and determining a vision, talk), organisational sensemaking occurs. This process is described in more detail by Gioia and Thomas [42]:

“First, sensemaking occurs when a flow of organizational circumstances is turned into words and salient categories. Second, organizing itself is embodied in written and spoken texts. Third, reading, writing, conversing, and editing are crucial actions that serve as the media through which the invisible hand of institutions shapes conduct”.[42] (p. 365)

The process of sensemaking is aptly captured in Weick’s [43] sensemaking recipe of “how can I know what I think until I see what I say?” which emphasises retrospection. However, this version does not acknowledge the role of other stakeholders in this process. An extension of this recipe to include interactions with stakeholders is “how can I know who we are becoming until I see what they say and do with our actions?” [41] (p. 416). In the context of CSR communication, this view on organisational sensemaking is aligned with a two-way dialogic approach, in line with Morsing and Schultz’s [44] stakeholder involvement strategy, focusing on negotiation of corporate CSR action between the organisation and stakeholders.

2.3. Tensional Relationship between Talk and Action

Organisations engage in CSR communication to communicate their values in relation to CSR, to achieve legitimacy [45,46], to build credibility and trust and to strengthen their reputation [1,47,48,49,50]. On the one hand, communication of intentions, visions, and aspirational talk, while often vague, are important due to their performative potential [6] and mostly these ambitions and visions are formulated in an open-ended fashion, using a CSR as a journey metaphor [7]. However, the statement of ambitions and visions may leave organisations open to accusations of greenwashing if not backed up with hard facts [37,38]. This emphasises the need for organisations to communicate their CSR achievements in the form of concrete, verified, and measurable results to convince stakeholders of their commitment and follow through. The language used in making those claims is scientific, and the focus is on messaging that “sustainability has been achieved” [7] (p. 146), thus using a CSR as destination metaphor. Consequently, organisations must navigate this talk–action dichotomy in their CSR communication. Depending on how this tensional relationship is framed by the organisational actors, the responses can differ. A brief overview of tensional approaches in organisational literature will outline the various frames and strategic responses.

2.4. Tensional Approach

Paradox theory has been increasingly found useful to study organisational phenomena, and particularly in instances where tensions are amplified through a complex and rapidly changing environment [51,52] in which organisations are required to pursue multiple goals and integrate multiple voices [53,54] simultaneously. Consequently, there has been an increasing number of paradox studies [55] from a range of disciplines and paradigms [16]. The role of tensions and paradoxes has recently begun to attract attention in CSR and sustainability scholarship [56,57,58,59] and also within research exploring communicative dimensions there has been an emergence of tensional approaches to explore complex organisational concepts [19,20,22,23,24,25,26].

While paradox theory has been critiqued for lacking conceptual clarity [52], the detailed mapping of the field by Putnam et al. [16] has addressed this shortcoming. Their review provides a comprehensive outline of terms used to describe tensions, such as duality, dualism, contradiction, paradox, and dialectic. While a duality, for example, is defined as “interdependence of opposites in a both/and relationship that is not mutually exclusive or antagonistic duality” [16] (p. 5), contradictions are classified as “bipolar opposites that are mutually exclusive and interdependent such that the opposites define and negate each other” [16] (p. 6), and a paradox is demarcated as “contradictions that persist over time, impose and reflect back on each other, and develop into seemingly irrational or absurd situations” [16] (p. 8). When considering the talk–action relationship, talk and action are neither mutually exclusive opposites (as talk and action can coexist) nor do talk and action develop into absurd situations. The concept which captures the talk–action relationship most fittingly is dialectics, which is summarised as “interdependent opposites aligned with forces that push-pull on each other like a rubber band and exist in an ongoing dynamic interplay as the poles implicate each other” [16] (p. 7). Talk and action are in fact opposing poles that coexist, and are in dynamic interplay.

While the definitional concepts between contradiction, paradox, and dialectic are seen to be precise and tightly described, organisational responses in managing them appear in a similar vein. Organisations can adopt either a defensive or an active approach: while defensive approaches consist of either/or thinking, active approaches are centred on both-and or more-than thinking [16,52,60].

Defensive approaches are usually short-term as they tend to temporarily suppress the tension through techniques such as separation [61] and selection [62], without developing new ways of working with the tension [63]. Within this approach, either/or thinking is prevalent, where the organisation tends to choose between paradoxical agendas [64], resulting in each pole either being denied or privileged [62]. Alternatively, both poles are recognised, but they are separated spatially or temporally [61].

Active approaches, on the other hand, entail embracing the paradox, and exploring the tension “to generate creative insight and change” [65] (p. 170). They are divided according to both-and and more-than approaches [16]. Both-and approaches consist of paradoxical thinking [52] focused on reflecting on the paradox and seeking out differences, segmenting and then connecting poles [61], and integration and balance [52,62], which combines the two poles and neutralises tension in a middle of the road approach, but at the same time leaves both poles “unfulfilled in their totality” [62] (p. 76). More-than approaches represent ways of working with opposites through reframing and transcendence (also referred to as synthesis, [62]), which involves using the dynamic interplay between the two poles to form new perspectives by situating opposites in a novel relationship [16]. Within this type of thinking, opposites are equally valued and intertwined, and the focus is on the dynamic interplay between them. Specifically, reflective practice [66], centred on collaborative stakeholder dialogue, has been shown to use tension in a proactive manner which opens meaning, pinpoints options and helps develop organisational action.

2.5. Tensional Approaches and Aspirational CSR Communication

As outlined above, there are two types of approaches to dealing with tension: to embrace it, or to suppress it. Suppressing it in the aspirational CSR communication context, on the one hand, involves focusing on standardisation and quantification of achievements and reporting these in the form of verified facts, ultimately seeking discursive closure [8]. However, this drive towards recoupling of talk and action may, in fact, limit creativity around the development of CSR. Embracing tension, on the other hand, allows for the topic and practice of CSR to be constitutively explored. It permits temporary decoupling of talk and action that results in a deeper exploration of CSR issues and their solutions [6,67]. Organisations today are facing the challenge of how to navigate this talk–action tension.

This paper examines how the tensions and contradictions of communicating CSR aspirations and achievements develop over time and play out in the organisational activity of CSR reporting, thus addressing Putnam et al.’s [16] calls for longitudinal and process-based studies of paradox [27]. More specifically, this study seeks to shed light on how organisations respond to and discursively manage the tension between talk and action. It also addresses calls by academics to generate much-needed empirical data on the phenomenon of aspirational talk [6]. It adds to the growing body of research exploring organisational tension from a constitutive perspective, focusing on what language is doing in situations of competing demands [68]. As briefly discussed above, an embrace of tension is thought to help to discover resourceful solutions [69], and allows organisations to “generate creative insight and change” [65] (p. 170) and opens new possibilities [70], which are needed to solve the sustainable development challenge. This research aims to demonstrate just this by outlining the dynamics of the talk–action tension over time, the strategic responses and the overall impact.

2.6. CSR Reporting

To harness the full benefits of implementing CSR strategies with regard to reputation management and to address transparency concerns, organisations need to communicate their CSR efforts to their stakeholders and the public. Approaches to communication include website communication [71,72], social media [73,74], and annual company CSR reports [3]. Specifically non-financial CSR reports have become the “norm rather than exception” [75] (p. 7), and this type of voluntary reporting has become increasingly widespread [76,77,78,79]. CSR reports fulfill a variety of strategic aims: to demonstrate commitment to engage with stakeholders [80], to address issues of social accountability [81], and to respond to stakeholder pressure [82].

Due to its until recently voluntary nature (The EU Directive 2014/95/EU was introduced on 12 June 2016, making CSR reporting mandatory for companies with 500+ employees from fiscal year 2017–2018 [83].) and the variety of motivations and aims, the genre of CSR reporting is rather heterogeneous with regard to length, scope, and approach [84,85,86], using a range of definitions and indicators. To improve the quality of reporting, and to address concerns of skepticism and ward off government regulation, voluntary standardisation of CSR reporting and its content is taking place [87]. There has been a proliferation of a wide variety of CSR reporting guidelines in recent years: The United Nations Global Compact (UNGC) in 1999, the Global Reporting Initiative (GRI) in 2000, GRI’s G2 guidelines in 2002, GRI’s G3 guidelines in 2006, and the G4 in 2013. The implementation level of the GRI has been shown to increase the quality of CSR reporting and reduce policy–practice decoupling [88].

Further, there has been increasing pressure from governing bodies, media, competitors, and consumer protection societies for companies to report their CSR practices according to such voluntary reporting guidelines [89]. Whilst joining such initiatives may be beneficial for the organisations insofar as they develop their expertise [90], such initiatives are also likely to shape and control the discourses surrounding CSR, and more specifically discourses of CSR talk and action.

CSR reports are a mainstream channel for organisations to communicate their CSR activities and strategies to their stakeholders [2]. One way to look at CSR reports is to see them purely as tools to monitor and report social impact [91], but they can also be considered forms of self-representations [12]. Consequently, modern forms of CSR reporting can be viewed as a hybridised genre [15] as they “combine factual reporting with promotional discourse” [15] (p. 235), requiring organisations to combine action and talk, reinforcing the tensional element.

2.7. Discourse and Aspirational CSR Communication

Organisational practice, which in this case is CSR communication and more specifically CSR reporting, is performed within the context of discourses [92], collections of discursive practices and texts that determine “who and what is ‘normal,’ standard and acceptable” [93] (p. 544). The previous discussion has highlighted the pervasiveness of the dominant discourse centred on standardisation, quantification [94], and discursive closure [8] which is reproduced and normalised. At the same time, the recent emergence of an alternative discourse of aspirational talk and discursive opening is highlighted, which is challenging this view on the basis of it resulting in “repetitive micro-practices that stabilize social relations” [8] (p. 137). Adopting a process-based discursive approach to exploring organisational phenomena is particularly suited to highlight how discourses in relation to aspirational CSR talk emerge, develop, and change over time, taking into account the discursive struggles over meanings [95].

3. Materials and Methods

The aim of this study is to explore if and how the discursive management of the talk–action tension changes, adapts and evolves over time. An interpretivist, discursive lens is applied to longitudinally analyse how talk and action are discursively navigated in company CSR reports and how the organisation makes sense of this process to derive insights into the organisational learning processes around tension management.

3.1. Longitudinal Research on CSR Reporting

Longitudinal research examining CSR reporting is well established [84,96,97,98] and highlights that interesting insights can be generated from longitudinal studies. Most studies take a quantitative approach, for example tracking issues development or carrying out industry comparisons, and most of them are placed within accounting publications. However, there is also criticism of taking a purely quantitative approach [99], prompting a call for an interpretative longitudinal study focusing on how meaning is constructed [100]. In light of the research objective of this study, to uncover how the talk–action tensions unfold over time, and since tensions are often latent and hidden, a qualitative approach is prioritised to capture the richness of the research problem.

3.2. Methodological Approach

Building on research that celebrates linguistics and language—the so-called “linguistic turn”—this work provides an empirical, discursive investigation of the tensions associated with aspirational CSR communication, more specifically the tensions between talk and action, promotional and informational statements. This type of methodology supports the constitutive view of communication and the performative role of language. Whilst the primary aim of the paper is to examine the management of tensions between discursive opening/talk and discursive closure/action, this research also aims to outline the context within which these texts (CSR reports) are embedded, as well as providing insights into underlying organisational sensemaking processes. The research approach taken in this study is qualitative and discovery-driven to aid the identification of latent tensions. Qualitative content analysis provides the needed flexibility for analysing textual data and to interpret meaning [101,102,103].

3.3. Rationale for Sample Selection

For this type of study, a company had to be selected that had an extensive record of CSR reporting, ensuring a sufficiently large longitudinal research sample. Considering previous research on the impact of company nationality, size, degree of internationalisation, and industry context on CSR reporting [104,105], Nestlé was identified as a suitable research site. Nestlé is headquartered in Switzerland, had an annual turnover of CHF 88.8 billion and 335,000 employees in 2015, and operates in 189 countries [106]. It is considered a high CSR performer: with a Carbon Disclosure Leadership score of 100 A; Nestlé is the top rated food and beverage producer of the Dow Jones Sustainability Index, scoring more than double the average in its industry [107]; it is included on the FTSE4Good ranking [108], and is ranked second in the Oxfam Behind the Brands scorecard [109]. Further, Nestlé has experienced a number of reputational shocks over the years (e.g., the infant formula crisis in the late 1970s and 1980s, the KitKat Campaign by Greenpeace in 2010 to highlight palm oil use), making it a particularly interesting and contextually-rich case.

3.4. Data Collection

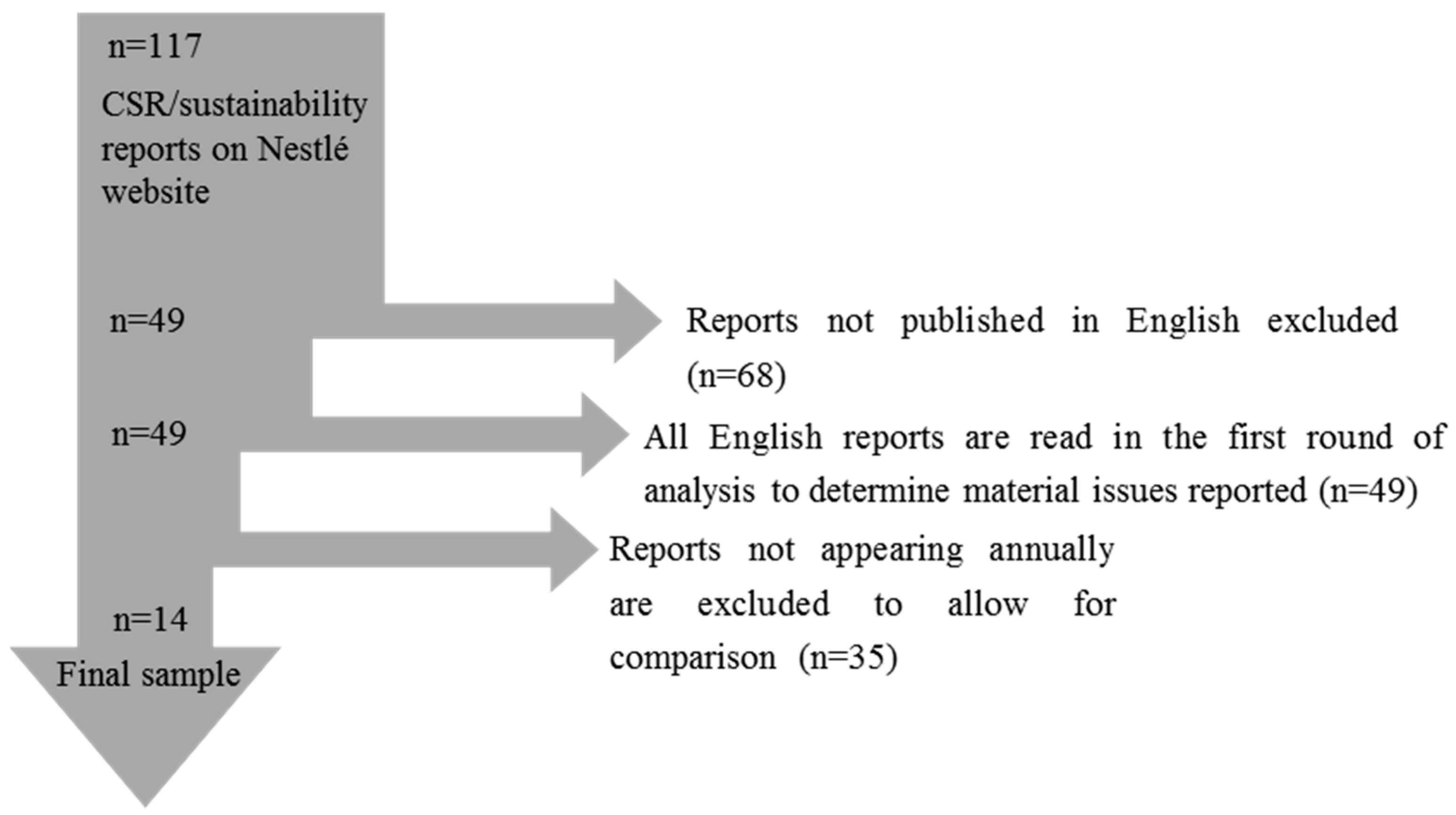

All publicly available CSR/sustainability-related reports were downloaded from the official Nestlé Creating Shared Value (CSV) website (http://www.Nestlé.com/csv/downloads), with the exception of the 2002 report which was not available on the CSV website and was downloaded from the Nestlé document library [110]. Overall, 117 reports published between 2002 and 2016 were available for download and were retrieved. Out of the 117 reports, those reports not published in English were excluded. This left 49 English-language reports. These consisted of full CSV reports, CSV summary reports, region-specific reports, operations-specific reports, policies, charters, and action plans. All 49 documents, totalling in excess of 3000 pages, were read to gain an understanding of the issues discussed and their general framing (see Table A1 in the Appendix A for a detailed overview of the reports included in the initial data scanning stage). To allow a longitudinal observation of the talk–action tension, the selection of reports was narrowed down to documents that were published on an annual basis, thereby focusing the study on the CSV annual reports, which have been published since 2008 (see Table A2). Further, the decision was made to include and analyse all full-length reports between 2002 and 2016 (there was no publication in 2007). This narrowing of data allowed for a 14-year longitudinal design to demonstrate how the interplay between talk and action has developed over time (see Figure 1). To contextualise the reports, the GRI guidelines were also included in the analysis to learn more about the reporting environment and recommendations during the same time period.

The documentary analysis focused on how the organisation was using words to navigate the tension between talk and action in its reporting. The analysis of how the tension between talk and action was discursively managed at the organisational level allowed for inferences to be made about the underling organisational processes. However, to allow for more rigorous claims to be made, it was decided to add interviews with Nestlé organisational members, as well as stakeholders outside the organisation to authenticate the results from the documentary analysis. In total, seven in-depth telephone interviews were carried out between July and September 2017, ranging from 35 min to 90 min. Experts from within and also from outside the organisation were chosen to provide a balanced overview of the viewpoints (see Table 1 for an overview of the interviewees). To get insights into the internal perspective, Nestlé managers with communication, operations and scientific affairs backgrounds were selected, who had the seniority, length of service and exposure within Nestlé to ensure sufficient knowledge of internal processes. To include the external stakeholder perspective, NGO actors were selected that had both positive, as well as negative interaction with the organisation. The inclusion of other stakeholder groups, such as consumers was considered, however, the decision was taken to not include them on the basis of Nestlé having a separate communication platform to interact with consumers in relation to sustainability, such as consumer websites and social media. Similarly, within the business-to-business context, the company communicates in the form of procurement policies and personal interactions. The interviews were audio recorded, transcribed and then coded with NVivo to substantiate the documentary analysis and to explore how the participants were making sense of the of the process and what the organisational learning over this time period had been.

3.5. Data Analysis

The analysis of the texts (CSR reports) was initially carried out inductively, to get a feel for the data. Therefore, the first step of the analysis consisted of close reading of the reports, which was repeated several times to get a feel for the structure and language of the reports, the issues reported, and the treatment of aspirational and performance-based communication The data was coded to categories, which were derived inductively [111].

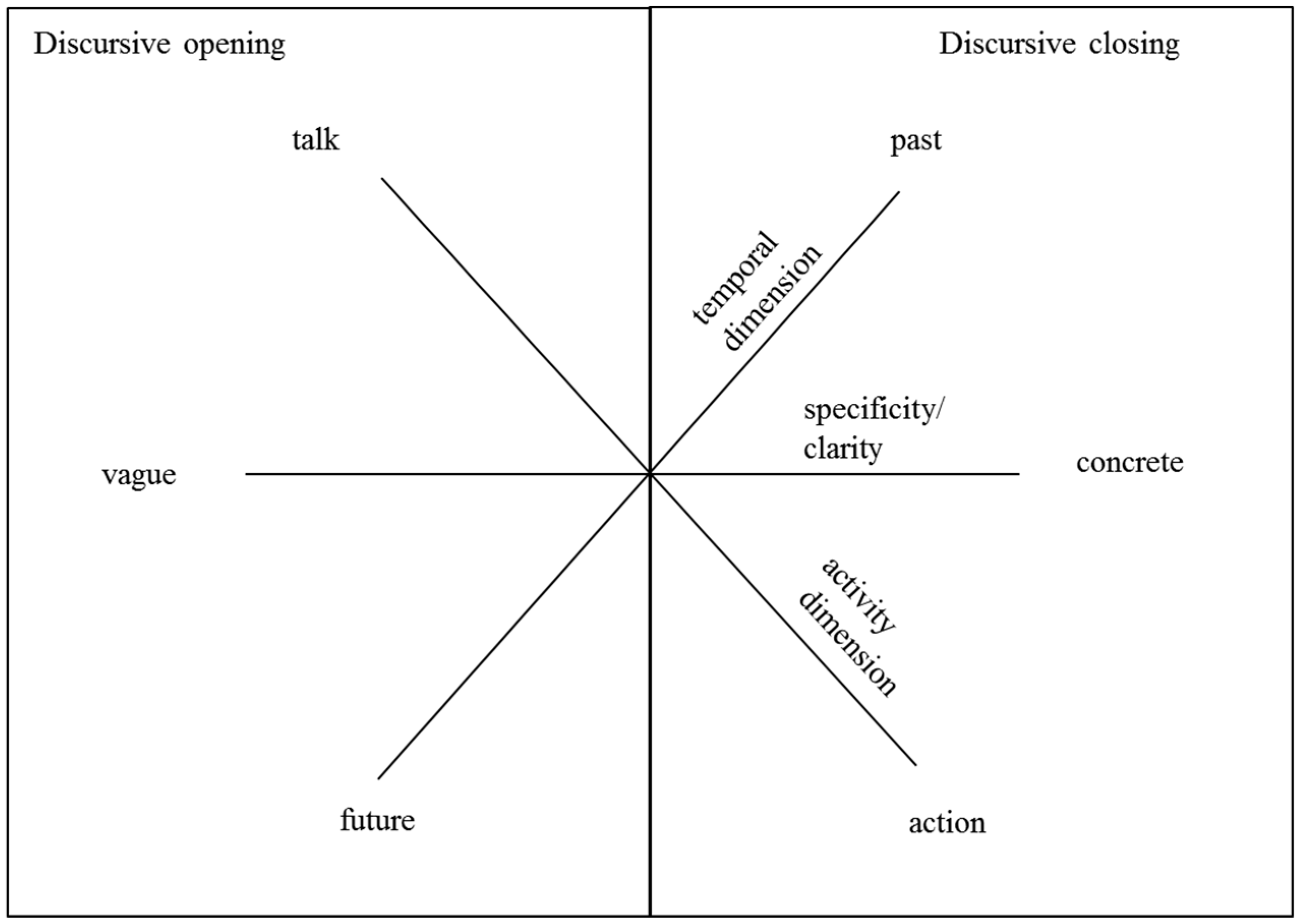

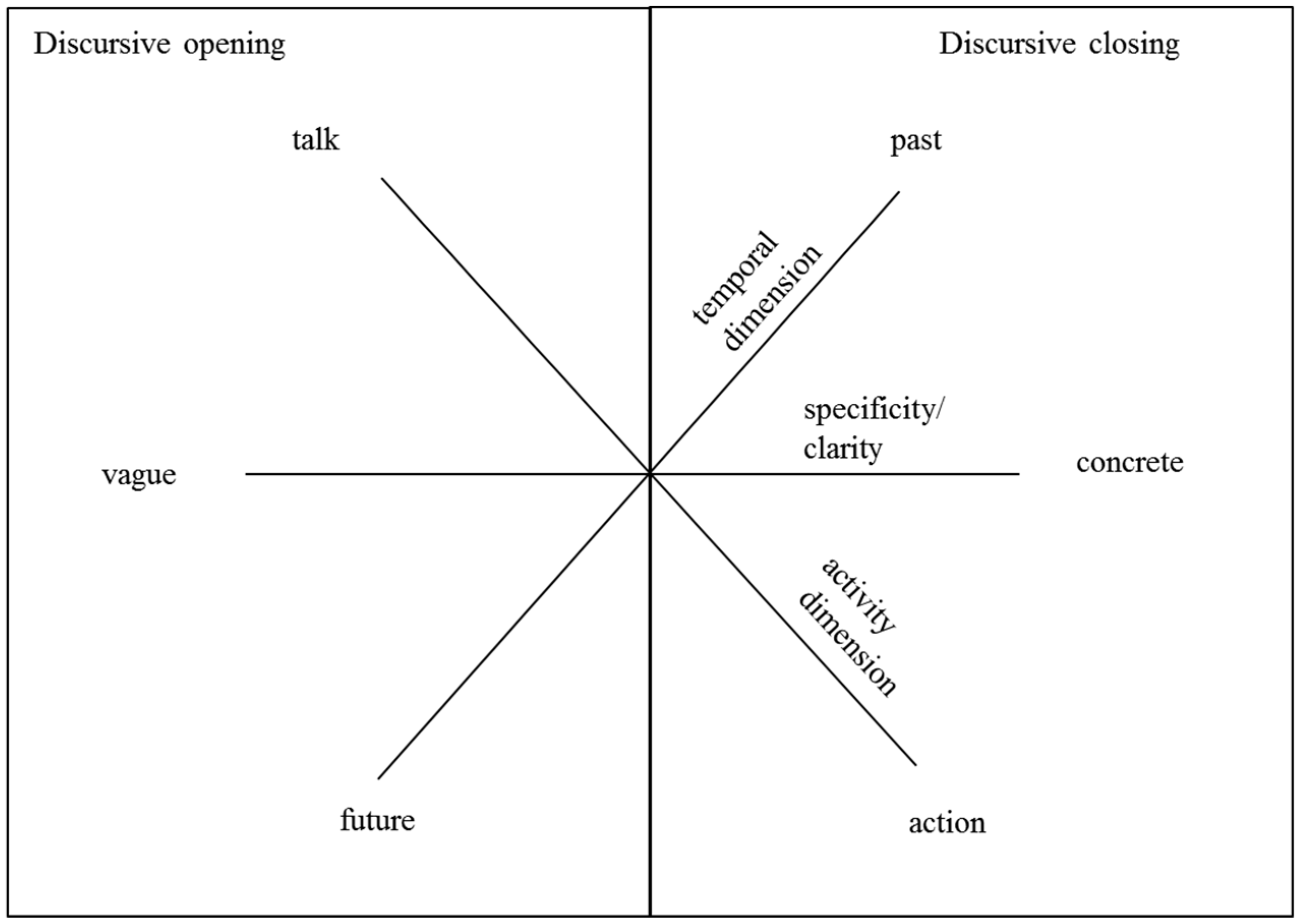

The second round of analysis consisted of coding the data according to theoretically derived concepts based on the literature pertinent to aspirational talk. The data was then manually analysed in NVivo to detect the interplay between talk and action, and to examine how far the reports reproduce and restructure existing discourses in relation to communicating aspirations and performance-focused reporting. With the aim of identifying discourses of aspiration and discourses of performance, the review of literature on aspirational talk yielded a range of opposing proxies to carry out the corpus analysis, focusing on action and talk (activity dimension), past and future (temporal dimension), and vagueness and clarity (specificity), which can be grouped into discursive opening and closing (Figure 2).

To examine the talk–action relationship in more detail, in-depth qualitative coding of the forward-looking statements and commitments was carried out. The aim was to uncover the various discursive strategies employed by Nestlé to manage this tension, and to observe the embrace of aspirational CSR communication. Based on the theoretical discussion, the organisational practice of CSR reporting can be considered a process of retrospective and prospective sensemaking, during which the organisation uses future and past related elements to establish its position on CSR and plan where it would like to move to. Consequently, it can be assumed that two discourses can be observed in the corpus: a discourse of aspiration and a discourse of performance.

This part of the analysis thus consisted of a detailed investigation of the texts to identify, structure and sequence discourses of aspiration and discourses of performance to see how their interplay changes, evolves, or adapts over time. Passages of text were coded in relation to the following proxies:

- (1)

- Aspiration: future-related claim, statement of vision, goal, target or plan.

- (2)

- Performance: past-related claim, review of performance, statement of organisational action.

An example of a passage coded to discourse of aspiration within the text is: “The report’s scope is ambitious, reflecting our determination to meet our responsibilities and play our part in addressing global challenges” [112] (p. 2), while the following passage is an example coded to discourse of performance: “In order to combat the causes of malnutrition, healthcare professionals around the world need relevant and up-to-date information. To help provide this, in 2005 we created the Nestlé Nutrition Institute. In just seven years, this independent, not-for-profit organisation has become the largest private publisher of nutritional information in the world. Its website currently attracts more than 170,000 registered users in nearly every country in the world” [112] (p. 15).

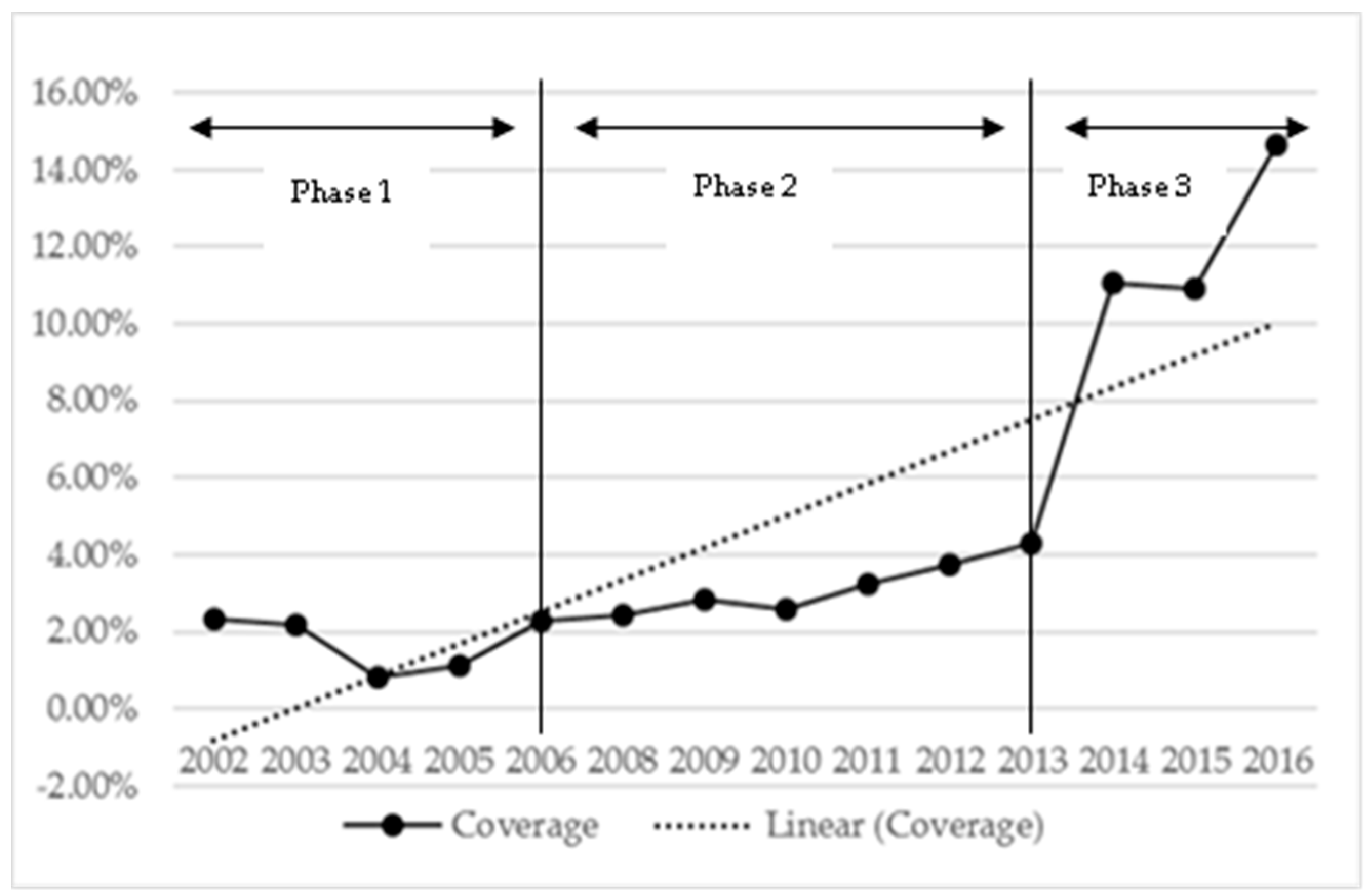

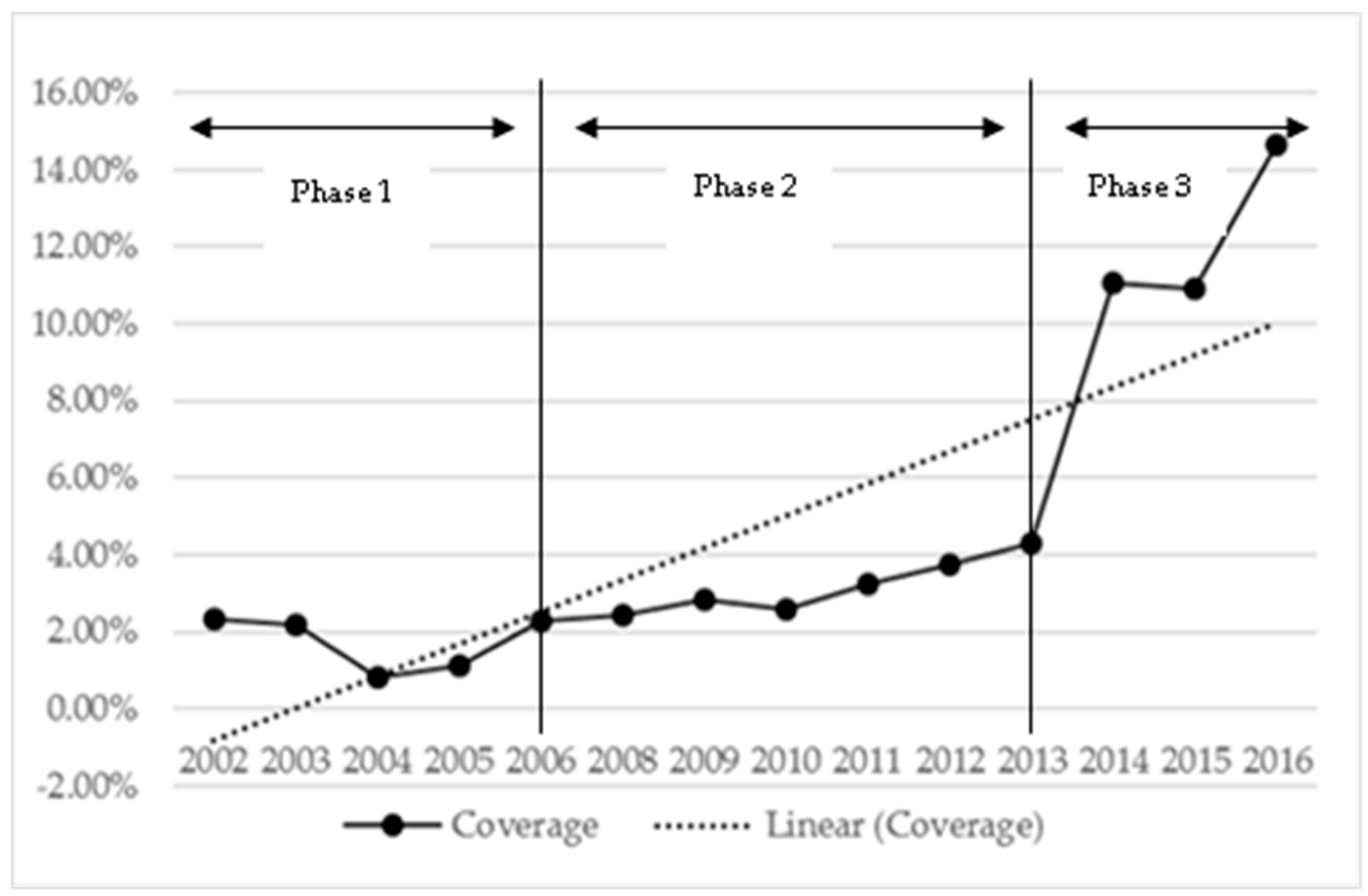

The data was coded and analysed within an interpretative, discursive vein, focusing on how language is used to discursively navigate the talk–action tension in the reports. In identifying different discursive strategies, which are described in detail in the results section using illustrative examples from the data, three main phases emerged in Nestlé’s reporting, elucidating how the talk–action interplay evolved. Phase 1 consists of reports published between 2002 and 2005, Phase 2 comprises reports published between 2006 and 2012, and Phase 3 consists of reports from dated 2013 to 2016. The overall quantitative analysis of the percentage coverage of passages coded to the discourse of aspiration supports the increasing embrace of discursive opening which can be observed in the sample (see Figure A1 in the Appendix B).

The coding of the interview data took place both deductively and inductively. In the preparation of the analysis grid for the extraction of information, both deductive and inductive approaches were used [113]. For the analysis, participant quotes were contrasted and interpreted, and then interlinked with the findings of the documentary analysis [114] further increasing the validity of the results [115]. Through the use of different categories (deductive, leaning on Weick’s theory of sensemaking and tension management in the documentary analysis), relevant passages were encoded and marked in the interviews, while new categories were also developed (inductive, focusing on stakeholder dialogue) during the analysis process.

4. Results

4.1. Findings of the Documentary Analysis

4.1.1. Phase 1 (Reports from 2002–2005)

In the earlier reports, Nestlé displays a defensive response to the talk–action tension: the tension is not acknowledged, and discursive strategies are developed to reduce the tension, by focusing on past performance and limiting aspiration. In the report published in 2002, for example, the discourse of performance is dominant and the only text element coded to the discourse of aspiration in the entire report is “Nestlé seeks to be a true partner in sustainable development” [116] (p. 8). Both the discourse of performance and the discourse of aspiration are rather vague, with little detail added: “Over 30 years ago in Moga, in northern India, support started with Nestlé providing loans at favourable rates to enable farmers to build their herds of cattle” [116] (p. 12).

In the report published in 2003, a slight increase in the inclusion of aspirations can be observed: here, any elements coded to the discourse of aspiration are phrased in reference to joint initiatives in which Nestlé is involved. Consequently, the aspiration is detached from the organisation, signifying a separation strategy: “Nestlé has committed to the Jimma agricultural research centre by assisting them to increase their scientific capacity in the coffee sector” [117] (p. 15). Simultaneously, a more detailed approach to performance reporting can be observed: “In 2002, the company bought about 110,000 tonnes of coffee directly from farmers and cooperatives. This was a 10% increase over the previous year” [117] (p. 6). A similar approach can be observed in the report issued the following year, where Nestlé voices organisational ambitions only in reference to the development of the coffee crop: “Nestlé Nespresso is committed to the progressive implementation of sustainable quality coffee practices” [118] (p. 28). Performance-related statements in these instances are kept vague, with no quantified elements: “Nestlé also supports a Coffee Training Centre in Ethiopia. Advice provided by Nestlé agronomists is free and there is no obligation on the farmer to then sell his coffee to Nestlé” [118] (p. 22). Similarly, in the report distributed in 2005 Nestlé voices hopes and ambitions for Africa’s development, with little or no reference being made to how Nestlé will support such development, once again separating the organisational and societal roles in sustainable development. Focus within this report is on emphasising Nestlé’s past and current activities pertinent to supporting Africa’s progress.

In Phase 1 reports, the tension is not really recognised, and is dampened through emphasising discursive closure and verification, while the organisation appears to be cautious about including aspirational statements. The analysis of the texts brings to light that the early reports in particular have a performance bias, and while some forward-looking passages are included, they are rather vague and focused on general sustainable development goals without giving insight into Nestlé’s aspiration for their organisational practice of CSR. Within these early reports, there is a predominant focus on detailing existing achievement and involvement, but also legitimating practices (in particular justification) can be observed to rationalise Nestlé’s business practices regarding its coffee purchasing practices and operations in Africa. The discourse of performance is prioritised, and the discourse of aspiration is minimised. Where aspiration can be observed, forward-facing claim making is vague and focused on the macro (societal) level rather micro (organisational) level with specific terms of reference of what this ambition means for Nestlé.

Tension Management in Phase 1

When conceptualised within tension management strategies, Phase 1 reports comprising reports published between 2002 and 2005, correspond to an either/or [16], dilemmic view of tension. Here, the organisation responds to the tension by selecting or separating the opposing poles [61,62]. Two specific strategies can be observed: one is privileging discourses of performance over aspiration and limiting statements of ambitions to a minimum (selection); the other is to separate aspirations away from the organisational level to the societal level by phrasing CSR commitments and imperatives within the societal perspective rather than the organisational (separation). Consequently, aspiration is muted and constrained, and forward-facing claims that may guide organisational decision making in a binding manner do not feature and help the organisation to raise the bar regarding CSR practice.

4.1.2. Phase 2 (Reports from 2006–2012)

The report published in 2006 signifies a departure from Phase 1 reporting: here, discourses of aspiration and performance begin to coexist. The tension is recognised, and to an extent embraced. Talk and action exist side by side, but the focus is short-term, and often vague. Interestingly, forward-facing statements within the 2006 report are often contained within expert contributions and endorsements (e.g., commentary by Mark Kramer from Harvard Business School, Chris Willie from Rain Forest Alliance, Ian Bretman from Fairtrade Foundation). This shift in how talk is increasingly integrated into the CSR reports coincides with Nestlé’s collaboration with Mark Kramer and the introduction of Porter and Kramer’s influential work reconceptualising CSR as creating shared value (CSV) [119], a framework which was adopted by Nestlé to guide its CSR policy. The following statement by Kramer highlights the reconceptualised relationship between discourses of performing and aspiration which can be observed in the Phase 2 reports: “the challenge for Nestlé moving forward is to demonstrate how well other achievements are replicated throughout its operations, and to move from incremental improvements to publicly committing to specific performance targets” [120] (p. 28).

This approach is continued in the 2008 report. The report, for example, opens with a CSR performance overview (as per GRI guidelines), a review of quantified CSR highlights, and an overview of the internal and external auditing processes. An example of general ambition to aid developing countries by carrying out value-added activities and reducing the transportation related emissions is “our principle is to manufacture, when possible, in countries from which we source commodities, rather than to export the raw materials” [121] (p. 12). This is immediately followed by a statement of accomplishment: “today, about half our factories are in the developing world, located primarily in rural areas, reflecting our long-term approach to investment and our ability to operate in diverse and complex environments”. This argument is then further strengthened by performance to date, where it is stressed that things have been done like this for a long time: “for example, Nestlé has operated in South Africa since 1927 and in Brazil since 1921. And we continue to manufacture coffee in Côte d’Ivoire despite the sporadic violence and civil unrest there over the last few years”.

The company goes on to highlight the embrace of environmental standards and adds quantified evidence, as well as quantified vision: “we are seeking external certifications for all our factories in line with ISO 14001, the internationally recognised environmental management system standard. This provides a common language and enables compliance to be demonstrated more easily to our stakeholders. 18% of our factories are certified to ISO 14001 and/or OHSAS 18001. We aim to certify 100% of our factories by 2010. 84% of our factories have been audited within the scope of our CARE programme” [121] (p. 12). This statement encapsulates Nestlé’s motivation for embracing a more scientific and verified approach in its reporting to facilitate more transparent and easier communication with its stakeholders, as well as signaling its commitment to further standardisation in the future. The discourse of performance is underscored by an emphasis on verification, resulting in verified performance.

While the report issued in 2010 is similarly performance focused; aspirations are increasingly beginning to feature. While some of the aspirations are separated and are voiced from the view of independent experts as is done in the 2006 report, others, which are voiced from the organisational perspective, are becoming increasingly specific. General sustainable development ambitions are broken down into organisational goals and more specific targets: “Over the last 10 years, Nestlé has supported the training of 100,000 cocoa and coffee farmers, and aims to support the training of a further 130,000 farmers over the next 10. Nestlé will also invest a minimum of CHF 460 million in its plant science and sustainability initiatives for coffee and cocoa by 2020, CHF 350 million of which will be spent on coffee” [122]. The organisation appears to be implementing Kramer’s advice of publicly committing to forward-looking performance targets [120]. The oscillation between discourses of aspiration and performance is also taking place spatially and textually: while aspirations are embedded in text, performance-related information is often detailed in streamlined tables. Within the Phase 2 reports, a clear structure of how the discourse or aspiration and performance are combined becomes apparent: text is structured into “our goals, actions and performance” for each sustainability category. While aspirations are quantified and broken down into smaller organisational goals, these goals tend to be limited to the short term.

Interestingly, this report, which signifies a move towards coexistence of discourses and aspiration, contains reference to stakeholders demanding a more performance-based approach to CSR reporting. The Bureau Veritas assurance statement in the Nestlé Creating Shared Value Update 2010 report advises that “stakeholders will expect future reporting in this area to be more performance orientated and as such Nestlé needs to focus its efforts in developing a methodology to measure the impacts (and benefits) … of the projects” [123] (p. 93), signaling a recommendation for increased verification and to develop methodologies to measure impact. This recommendation is then put into practice in the following years, where an increasing focus on measuring performance, development of metrics, quantification of performance, detailing of KPIs, and visual development from text to tables can be observed in the company’s reporting. Measurement and evidence-based reporting are included, verified through internal and external auditing.

Tension Management in Phase 2

In paradox strategy terms, the tension management in the Phase 2 reports represents an integration [62] and acceptance [61] approach. Rather than framing talk and action as a dilemma, prompting either/or responses that would result in favouring one pole over the other, the discourse of aspiration and performance are allowed to coexist in a both-and manner [16] and the tension is accepted. Talk and action are integrated and balanced in that “both ends of the continuum are legitimate at once, but remain unfulfilled in their totality” [62] (p. 76). Through merging talk and action, the individual poles are somewhat compromised. At times, the organisation shifts back and forth between the poles of talk and action, through different contexts. However, this vacillation appears to be disintegrating into separation [61] at times. The potential of aspirational talk is not fully harnessed.

4.1.3. Phase 3 (Reports from 2013–2016)

The year 2013 was pivotal for the company’s reporting approach. Based on stakeholder feedback, Nestlé decides to regularly publish forward-facing commitments as part of its CSR reporting. During its annual stakeholder engagement process, Nestlé is prompted to “provide greater disclosure in respect to forward-looking CSR targets” [112] (p. 40). Here, aspirations are conceptualised as forward-looking “commitments”. The choice of words signifies a shift from a slightly vague desire, dream, or ambition to something of an organisational pledge, promise, or even guarantee. These forward-facing goals are increasingly supplemented with quantified, medium- to long-term targets. So, while Nestlé is embracing a discourse of discursive opening, it simultaneously couples this with increased quantification of these aspirations.

Increased disclosure of future goals in this instance is interpreted as a prompt to also increase measurability and metrics associated with these goals. As a reason for this quantification of aspiration, Nestlé cites its capacity to “provide a clear sense of the strategic direction we are heading in and the standards to which we hold ourselves accountable” [124] (p. 3). Thus, there is a drive to combine aspiration and quantification simultaneously. While in Phase 2 the approach to this combination appears cautious, even apprehensive, in Phase 3 Nestlé becomes more confident in balancing talk and action. It also provides an interesting insight into how the organisation uses CSR reporting for retrospective and prospective sensemaking to guide strategic decision making. Evidence can be found in the report relating to the important process that reporting triggers internally and externally, and the practice of sustainability reporting is referred to as “no longer simply a collection of anecdotal stories and data, but rather a holistic exercise in internalising and improving a company’s commitment to sustainable development” [106] (p. 6).

Tension Management in Phase 3

Within Phase 3 reports, the tension seems to be actively managed. By handling aspirational talk in a more concrete, thought-out manner, the performativity potential of the talk–action dichotomy is more fully realised. Talk and action are enveloped in a clear strategic direction. Proactive management of the tension helps to transcend the paradox [62].

While the discourses of aspiration and performance conflict with each other, Nestlé seems to move towards a stage of transcendence by intertwining both discourses through concretising its abstract vision (Table 2). Not only does the organisation imagine where it would like to be regarding CSR, but it also breaks down the relevant steps needed to get there, which then act as a road map to help the organisation to transition towards that goal. The performative potential of an imagined vision and the concrete elements of performance targets are united and work in unison to fully harness the transformative potential of aspirational talk by triggering the sensemaking process and reflective practice [66].

In a dialogic fashion, together with its stakeholders, the organisation imagines the goal, assesses how this vision can be achieved, and then develops concrete goals and projections on which performance targets are based. Ultimately, the opposites of talk and action are intertwined with each other and tensions are used to develop actions, building on the performative qualities of aspirational talk. More specifically, the company transcends the tension through transforming the talk–action dichotomy into a new perspective [62] by using the actual linguistic features of discursive closing to formulate discourses of aspiration. Significant quantification, metrics and tables are used to present future-oriented information. This results in a synthesis [61] of discourses of aspiration and performance which are coupled with discursive closing and opening in a dialectical fashion, which bridges the opposing poles of the talk–action dilemma. Within the reporting, opposites are juxtaposed, the tension is reframed [60], and talk and action become encompassed in each other.

4.1.4. Meso Level Discourse and Interdiscursivity

Adopting a discursive approach requires the micro level analysis (at company level) to be situated in the meso level context (collaborative networks and compliance regime). As Nestlé has been reporting its CSR activities in accordance with the GRI guidelines since the 2007 report, the GRI guidelines G1, G2, G3, G3.1, and G4 were analysed as part of this research to determine the existing discourse in relation to the talk–action relationship within those reporting guidelines. Further, additional publications by the GRI, specifically in relation to future reporting, which includes a stance not included in the current G4 guidelines, were examined.

The GRI reports were analysed regarding recommendations on how to include a statement of visions and aspirations in reporting. The guidelines are very much grounded in a culture of performance-based reporting, favouring action over talk. The G3 [125] and G3.1 [126] guidelines both highlight that sustainable development “can seem more of an aspiration than a reality”, underscoring the dominant discourse of verification and quantification, implying a preference for closing of the gap between talk and action. This is also signaled by the GRI’s recommendation to “use organization-specific indicators (as needed) in addition to the GRI performance indicators to demonstrate the results of performance against goals”. Here, the GRI encourages organisations to express aspirations as goals to be reported on. The guideline suggests that organisational vision and ambition should be confined to the CEO statement at the beginning of the report.

With the publication of the G4 guidelines [127], a slight shift in the treatment of the talk–action tension can be observed. In this publication, reference is made to the role that CSR reporting plays in the organisational sensemaking process. Reporting is described as a process that “helps organizations to set goals, measure performance, and manage change in order to make their operations more sustainable” [127] (p. 3). In 2015, the GRI initiated research into the future of CSR reporting and produced a report with findings, Sustainability and Reporting 2025 [128]. As part of this research, several publications were issued, and forums held. Interestingly, while not mentioned in the published report, an interview extract can be found on the website discussing the “futurist’s view” at a forum event. In this interview with Amy Zalma, CEO of the World Future Society, the role of ambitions, visions, and aspirations in reporting is discussed, indicating a move towards discursive opening and increased inclusion of forward-looking commitments [129].

This emergence of the futurist’s perspective is likely to impact the next reissuing of GRI reporting guidelines due to the calls for an explicit focus on the future during this forum workshop, which highlights that “ways to incorporate longer-term forecasting and foresight into sustainability reporting could fruitfully shape the endeavor”. These shifts in thinking seem to be mirrored in Nestlé’s approach to reporting, which transitions from favouring discourses of performance to increasingly blending them with discourses of aspirations.

4.2. Findings from the Interviews

The objective of the interviews is two-fold: firstly, the participants are encouraged to discuss changes in the tension management over the observed reporting period to help the author compare and contrast the findings from the documentary analysis. Secondly, the participants are asked to share their own reflections on the reporting and tension management to deepen the author understanding of the underlying sensemaking processes. Additionally, importance of stakeholder processes throughout the reporting process emerges as an important theme.

4.2.1. Tension Management

Within the analysis of the question of how tension management between talk and action has developed within the reporting of the organisation, the internal respondents (#1, #2, #3), as well as the external respondents (#4, #5, #6) support the findings of the three phases detected in the documentary analysis. The focus on performance in Phase 1, representing discursive closure, is attributed by both internal and external respondents to the organisation’s Swiss culture (#1, #3, #4, #5, #6). Further, it is pointed out that this approach was thought to help the organisation deal with the contested nature of CSR and the lack of shared understanding of the concept amongst its stakeholders (#1). Another explanation provided for the focus on performance is the fear of not achieving its promise:

I was told, especially by the very senior managers of “Swiss origin”: that’s part of our culture. The Swiss culture is very much about “Do good, and people will notice that”.(#3)

They were very careful about not communicating about things which they had not really done yet. It is not just Nestlé. This is a Swiss thing.(#6)

Nestlé was somewhat reluctant to make promises, where there was a possibility it might not be able to reach or implement. That is the reason for the caution in the early years of the reporting.(#1)

A further explanation for the focus on the discourse of performance in the early reporting is the organisation’s reactive rather than proactive CSR management approach (#1, #4, #5, #6), mainly aimed at dealing with general reputational crises within the organisation and among their competitors after they had occurred.

In the beginning the reports were driven very much by societal controversies.(#1)

The transition towards Phase 2, where discursive opening is increasingly embraced but limited to the shorter term, is mainly attributed to the introduction of the Porter and Kramer’s Creating Shared Value (CSV) concept at the organisational level in 2006, as well as the introduction of the GRI Guidelines G3 (#1, #2, #2, #5, #7) and the UN Global Compact reporting guidelines (#1):

The introduction of the guiding principle of Creating Shared Value was an important milestone and game changer.(#1)

I don’t know who was first, who is the chicken and who is the egg here, was it Porter and Kramer or was it, Nestlé. In any case, Nestlé figured, if I'm not mistaken figured in our launch report, in the launch paper they figured as a case study, so it's interesting I think to refer to that. And to point to the importance of the creating shared value concept in Nestlé’s move from performance-based to aspirational reporting.(#5)

Further, the interview with the Operations Director provides insights into the impact of leadership during these phases. The interviewee (#2) attributes the approach of phase 2 to his role in the organisation and his approach to CSR management. Here, he highlights the importance of balancing talk and action, but clearly indicates a preference for performance:

But you know what I used to say in Nestlé we don’t walk the talk. In Nestlé, we talk the walk. And that was my rule. We talk walk, we do first, we create those conditions, we build those wastewater plants, we help farmers, we do all those things, and then we, or even better somebody else tells the story where we operate and so.(#2)

The transition towards Phase 3, where discursive opening and discursive closing are used simultaneously, and aspirational talk is stretched to the longer term, is supported by internal (#1, #2, #3) and external interviewees (#4, #5, #7). Multiple reasons for this are listed, such as NGO pressure (#1, #5) and changing stakeholder demands (#1), digitalisation and consequently higher confidence in data (#2), as well as meso structures, such as the United Nations Sustainable Development goals (#1) which are demanding longer term commitments.

But at least what I notice is that throughout the duration of the Behind the Brand's campaign of Oxfam (comment by the author: established 2013) their sustainability plans have adjusted to go more towards the aspirational. They have moved to a more aspirational way of formulating their societal responsibilities.(#5)

2013 probably also corresponds to world of digitalisation and the ability to have more confidence in the data, and also, we have more substance to tell.(#2)

One participant (#5) points out the crucial role credibility plays in the relationship between both talk and action. Here, he emphasises that the credibility of the aspirational statements is only as strong as the credibility of the performance statements, underscoring the importance of synthesis of both elements. Moreover, the performative qualities of the CSR report due to its public nature are discussed (#5), as well as the accountability it creates (#1):

Part of the recipe of a good due diligence process is that you go public with it, is that you come out somewhat of your closet of dealing with these things internally. And saying to the outside world what other challenges that you are meeting and partnering up with others, even with peers in a pre-competitive space to deal with those issues that you have.(#5)

Further, one internal interviewee (#1) points towards the importance of positive stakeholder feedback and consequent stakeholder dialogue as a consequence of transitioning towards more aspirational talk in their reporting. This has given the organisation more confidence in reporting on its ambitions, and has helped to convince critical internal stakeholders of this new CSR reporting approach, linking internal and external communication as part of the reporting process.

Interviewee #4 (external NGO perspective) provides some insights into why the organisation is utilising the technique of concretising the more abstract aspiration:

You need to have an ambitious goal, one that needs to be aspirational, but one that needs to be verifiable, and not only verifiable in its ultimate objective, but also in its interim stages.(#4)

The advantage of phase 3 reporting is described by one of Nestlé’s manager as “enabling the external world to look at what we are doing and how we are doing things” (#3), and providing a basis for ongoing stakeholder involvement.

The next step in the interview data analysis focuses on the organizational sensemaking around the talk–action management process.

4.2.2. Organisational Sensemaking

This section is based mainly on the interview data from the organisational members within Nestlé (#1, #2, #3), providing insights into the organisational sensemaking processes surrounding the management between talk and action.

The analysis of the data brings to the fore that the organisation oscillates between retrospective sensemaking, prospective sensemaking and enactment. Retrospective activities that the organisational members refer to are a review of past performance, key performance indicator (KPI) analysis (#2), measurement of sustainability indicators (#3), as well as the process of regularly compiling reports used for internal and external audiences (#1). Prospective activities consist of decisions relating to long-term vision and shorter-term sub targets (#1, #2, #3), which are described to take place in lengthy internal consultations to consider the feasibility and consequences (#2).

Most importantly, the interplay between retrospective and prospective sensemaking is described as an iterative process, which is continually reviewed (#2). One respondent specifically points out the internal reflection and auto communication that accompanies the breaking down of ambition across the various hierarchical functions, the definition of specific measures to achieve the aspiration (#1), while another senior manager stresses the importance of aligning sensemaking, talking and walking (#2):

That is the advantage, that you have to work on themes, break them down, for your own function, your brand, put a budget behind it. This creates a high level of accountability and concreteness. Our sustainability performance is used a lot as an instrument to create internal commitment.(#1)

I was able to align the thinking with the doing. That coherence is leadership. Find me a leader that aligns thinking, saying and doing, and you will see a great case for sustainability management.(#2)

However, it is also pointed out that internal audiences required some convincing to embrace the more aspirational communication (#1). Despite these internal criticisms, this specific senior manager, who has been overseeing the reporting over the entire time period of the reports analysed in this research, expresses his overall positive experience of Nestlé’s departure from the focus on performance towards a combination of both performance and aspiration due to the dialogic interactions it has created (#1).

The following analysis of the interviews will focus on the participants’ views on the link between stakeholder involvement and CSR reporting.

4.2.3. Stakeholder Dialogue/Involvement and CSR Reporting

While the documentary analysis in the previous section pinpoints stakeholder processes as reported by the organisation, the interviews are used to gain more insights from the perspective of key NGO stakeholders. As previously mentioned, one of the reasons the discourse of aspiration is progressively embraced by the organisation is due to stakeholder demands (#2), specifically from the NGO sector, indicating stakeholder responsiveness.

When the external interviewees were questioned in relation to Nestlé’s stakeholder involvement, a pivotal moment is referred to (#4, #5, #6)—the Greenpeace Nestlé KitKat campaign. This campaign highlighted the negative impact that Nestlé’s use of palm oil in its food products was having on deforestation and consequently of the habitat of the orangutans. The campaign, which was initiated in 2010, and aggressively targeted the company via social media, demonstrates how NGOs were becoming more effective and bolder in their campaigning.

I think all the alarms went off when Greenpeace targeted them, and Greenpeace really went at it. And so, it resulted in quite a shock, I think, for Nestlé which actually has made it to a degree easier for us to engage with Nestlé.(#5)

Interestingly, the NGO manager indicates how this crisis event has helped open Nestlé for dialogue. While all three NGO stakeholders comment on a changed approach within Nestlé (#4, #5, #6), two participants observe a distinct openness by Nestlé to engage in stakeholder dialogue (#4, #5). While two of the NGO stakeholders and one organisational stakeholder indicate that company CSR reports are used by them as a basis for discussion with stakeholders (#1, #4, #5) and to demonstrate transparency (#4), one NGO participant (#6) states that they primarily use the company reports to detect decoupling between what the organisation is reporting and actual practice. This respondent also comments that she does not believe in stakeholder talks and dialogue as currently practiced by Nestlé as they are too broad and general:

We are not going to change anything with that. It is actually a better use of our time to research on specific, come up with specific demands to a company like Nestlé.(#6)

This more active approach of researching specific demands and confronting the company has yielded some positive action on behalf of Nestlé (#6) to address these demands, and indicates similar responsiveness within Nestlé to this type of stakeholder interaction.

5. Discussion

Organisation scholars have made calls to explore aspirational CSR communication from an empirical perspective [6], and to investigate the transformative potential of discursive opening [8] within CSR and sustainability. CSR reports are a widely and frequently used means to communicate about organisational achievements, as well as intentions. Combining the sometimes opposing poles of talk and action poses difficulties due to the consequent tensions and clashes between organisational self-promotion and factual reporting style. Paradox scholars, on the other hand, have called for more research exploring how tension management evolves, changes, and adapts over time [16,27].

This longitudinal study of CSR and sustainability reporting reveals how the organisation discursively manages the talk–action tension, and traces the tension management strategies over a period of 14 years. The study finds evidence of three tensional approaches to navigating the often opposing poles of talk and action, transitioning from denial, to embrace, to transcendence, and thus supports the paradox literature view of tension management as a fluid and evolving practice. The analysis of the internal and external experts supports the existence of those three phases detected in the documentary analysis.

The empirical data demonstrates that, during the first phase, the organisation attempts to silence the tension by prioritizing a discourse of performance through opposition [61] and selection [62]. While this dualistic, either/or response can be seen as a mechanism to ward off criticisms of greenwashing [38], and appears to be rooted in the organizational culture of the examined organisation, it constrains aspiration, and omits the transformative potential that aspirational CSR communication can offer through stretch and align mechanisms involving communicating idealised versions of the organisation. However, as reporting progresses, and the organisation embraces a more active approach to managing CSR and involving stakeholders, the discourses of performance and aspiration begin to feature simultaneously—talk and action coexist, and integration [62] can be observed. Discursive mechanisms to manage this coexistence are focusing on aspiration in the shorter term, allowing the organisation to vacillate [61] between talk and action, though here again, the potential of aspirational talk is not fully harnessed.

In the third phase, the organisation manages to intertwine and synthesise [61] the two discourses of performance and aspiration. By discursively concretising vague aspiration, the organisation attempts to transcend [62] the clash between talk and action in its reporting. The forces of discursive opening and closing are simultaneously at play, and by transforming a vague ambition into a specific performance target, the organisation attempts to reduce any criticisms of greenwashing and makes its vision credible by “enabling the external world to look at what we are doing and how we are doing things” (#3). Thus, the organisation deftly manages the tension between talk and action by quantifying its aspiration, by blending linguistic elements of discursive closing with the discourse of aspiration. If considered in isolation, this might be viewed as discursive closure alone, preventing the performative capacity of discourses of aspiration. However, on closer examination, it seems that the organisation is simply “thinking out loud” and engages in reflexive practice [66] reflecting on where it would like to be and how it can get there.

By combining vague and concrete elements and by mixing discourses of aspiration and performance, the reporting becomes dynamic, and the opposites act as a “push-pull on each other like a rubber band” [16] (p. 7), which is significantly driven by the demands of material NGO stakeholders. Rather than conceptualising talk and action as a dilemma, requiring an either/or response, the organisation actively reimagines and reframes [60] the relationship between performance and aspiration as a dialectic process. The interplay between opposites—talk and action, aspiration and performance, vagueness and concreteness—gathers momentum as the various elements are synthesized [61], fueling the transformative potential of aspirational CSR. The tension between the opposites acts as a stimulant to the sustainability debate as “dynamic interplay of opposites becomes a source of energy, creativity, and dialogue” [16] (p. 11).

Table 3 summarises the above discussion of phases and contextualises them within the tension management approaches. It also indicates how the dichotomy between talk and action is navigated under the various paradox approaches and links the outcome to aspirational CSR communication.

The research unfolds the organisation’s increasingly refined approach to managing the talk–action tension, which evolves from either/or thinking, to both-and thinking, to a more-than approach in which the tension is embraced and managed through sensemaking [16,52,63].

At various points through the reports, evidence can be found highlighting the deeper organisational sensemaking processes that are triggered as part of the reporting practice. When reflecting on the role of reporting within the organisation, Nestlé finds that “it is no longer simply a collection of anecdotal stories and data, but rather a holistic exercise in internalising and improving a company’s commitment to sustainable development in a way that can be demonstrated to both internal and external stakeholders and shareholders alike” [106] (p. 6), which is in line with Weick’s notion of “how can I know what I say if I don’t see what I say?”. The interview findings provide even deeper insights into this sensemaking process, highlighting the dialectic interplay between retrospective and prospective sensemaking, which appear to be iterative, rather than linear. Both elements are shown to be in dialogue, with retrospection (what’s the story?) acting as a springboard for prospective articulations (now what?), and vice versa. So, sustainability is reported on, acting as a springboard for organisational action.

If the above cycle took place in isolation, the interplay between talk and action would never be challenged. However, in Nestlé it can be observed that talk–action sensemaking takes place in dialogue with stakeholders, which at times is shown to be tensional and conflictual [130], pointing towards a wider social and systemic sensemaking. Both internal and external stakeholders point towards a stakeholder responsiveness on behalf of the organisation. This stakeholder interaction extends the previously stated sensemaking recipe to “how can I know who we are becoming until I see what they say and do with our actions?” [41] (p. 416), pushing out the boundaries and fuelling the transformative potential of aspirational talk in an outward spiral-like fashion.

This study highlights the iterative nature of reporting, allowing for the exploration of aspiration and performance, which can indeed be a driver of change under boundary conditions of self-reflection and openness to embrace tension. The results of the documentary analysis and the analysis of the interview data point towards a continued redrafting of organisational CSR aspirations over the years, so that they become more comprehensive and responsive.

These findings have important implications for the scholarship and practice of CSR reporting, by countering claims that the activity of reporting will become obsolete [131,132]. Instead, this research reveals the reflective and reflexive capacity that reporting can have within the organisation.

Further, this research makes manifest the power struggles between external stakeholders and meso structures, such as the GRI reporting guidelines, which shape the reporting agenda and act as push and pull forces to focus on either performance or aspiration. The reports show evidence of the organisation acting on recommendations to include more performance-based reporting and the subsequent call to embrace a more future-oriented approach. However, it is also demonstrated that in the case of the organisation studied, which is considered a CSR leader by many, this responsiveness to stakeholders results in the organisation embracing aspirational talk ahead of the GRI guidelines thus starting to incorporate a futurist voice. It is important to keep in mind that the organisation selected for this analysis had experienced reputational crises in relation to its CSR. As the interview findings highlight, these shocks and rising skepticism, are found to have caused the organisation to seek more interaction and dialogue.

5.1. Contribution to Theory

This study explores at a detailed level how the practice of aspirational talk and the resulting tension between talk and action unfolded over a period of 14 years within the CSR reporting of a multinational corporation. The empirical insights into the discursive tension management broaden the understanding of the academic concept of aspirational talk at a practical level, and it is the first study to do so in an empirical context.

By applying a tensional approach to the concept of aspirational talk, the management of talk and action is explained in much detail, outlining the specific strategy of blending linguistic elements of discursive closing with the discourse of aspiration, while at the same time answering calls by academics to focus on systems/process-based studies to extend paradox theory by examining how tensions emerge and develop over time. The temporal nature of this study unfolds the discursive management of aspirational talk over time and thus adds empirical evidence to process research in management and organisation studies [27].

Christensen et al.’s [6] seminal work on aspirational talk focuses on the performativity of talk, and zooms in on the difference between talk and action that acts as a motivator to achieve more sustainable practice. This paper argues that the existing literature can be enriched by adopting a tensional approach to explore aspirational talk. It puts forth the view that depending on how the talk–action relationship is viewed, the transformative potential of aspirational talk is determined. An either/or approach to the talk–action relationship will constrain aspirational talk, while adopting a dialectic view of this relationship will yield the transformative effect of aspirational CSR communication, allowing for talk and action to coexist and keeping the gap between talk and action adroitly manageable [133].

This examination of the management of the talk–action tension contributes to the tension/paradox literature by highlighting how the dynamic interplay between talk and action helps to further the CSR agenda, thus underscoring the “developmental nature of dialectical systems” [16] (p. 57) and answers calls to research CSR communication through a lens of dialectics [19,21].

5.2. Contribution to Practice

Looking to the reporting practice of a large multinational that has experienced reputational ups and downs may prove useful for organisations currently grappling with how to include more aspirational CSR talk in their communication. The longitudinal examination in this instance highlights the inadequacy of attempting to moderate the tension by focusing on performance, as the potential of aspirational talk is not fully realised. Separation of aspiration and performance are also shown to have limited effectiveness as they are not stable states, and are only suited for the short term. Instead, a synthesis approach, combining both talk and action in a dialectic interplay, by taking a longer-term perspective, by being more specific in stating its aspirations, enables the organisation so match talk to action in a meaningful way.

The evidence from the analysis also suggests that the process of aspirational CSR reporting can indeed act as a site of sensemaking, allowing the organisation to engage in retrospective and prospective sensemaking processes. Practiced together, they allow the organisation to develop a strategic plan on how to achieve the organisational aspiration of becoming more sustainable. The specific case shows how the organisation abandons monologic, one-way reporting aimed at persuading (as observed in the earlier reporting) in favour of dialogic, two-way symmetric reporting (in Phase 3 reporting), which allows for this type of dialectic sensemaking.

Most importantly, it highlights the role of stakeholder involvement and responsiveness in this process. Rather than considering the CSR report a finished product, it should be used as a ground for discussion with stakeholders. This dialogue, allowing stakeholders to co-create the organisation’s CSR narrative allows demonstrates how greater acceptance of discursive opening can be yielded and used to drive CSR. This finding offers valuable insight to other organisations who have yet to embrace aspirational CSR by outlining how the talk–action tension may be navigated.

5.3. Limitations and Future Research