How Does Good Governance Relate to Quality of Life?

Facultad de Economía y Empresa, University of Oviedo, Av. Cristo, s/n, 33006 Oviedo, Spain

*

Author to whom correspondence should be addressed.

Sustainability 2017, 9(4), 631; https://doi.org/10.3390/su9040631

Submission received: 1 February 2017

/

Revised: 30 March 2017

/

Accepted: 12 April 2017

/

Published: 17 April 2017

Abstract

:This paper explores the relationship between the practices of good governance and the quality of life at the municipal level in Spain. A composite indicator of the quality of life of 393 Spanish municipalities in 2011 is estimated using varied statistical information. For this purpose, we follow a benefit of the doubt approach based on Data Envelopment Analysis. Then three dimensions of good governance are considered: transparency, participation, and accountability. The results show a significant positive relationship between quality of life and participation and financial accountability. However, transparency seems to be unrelated to quality of life.

1. Introduction

With the turn of the century, several external emerging challenges have promoted important reforms at the public local level of government. Municipalities had to cope with increasing fiscal pressures, exacerbated after the financial crisis and with increasing demands from the media and from citizens. This situation has fostered the need for extending collaboration among multiple policy-making agents, taking sustainability and concern about the needs of future generations to the center of the debate [1]). As a result, conventional local management models have been extended to include good public governance principles. Good governance has become a central topic in the discussion of economic and political development [1,2,3,4,5].

The initial efforts of international institutions, such as the International Monetary Fund and the World Bank in the 1990s, aimed to relate good governance to the “manner in which power is exercised in the management of a country’s economic and social resources for development” [2]. However, the concept today is more complex and includes the role of multiple stakeholder structures and processes, which influence the outcomes of public policies. According to Bovaird and Löffler [6] (p. 316), good governance can be defined as “the negotiation by all the stakeholders in an issue (or area) of improved public policy outcomes and agreed governance principles, which are both implemented and regularly evaluated by all stakeholders”.

Good governance is about the interaction between governments and other social organizations, the relationship with citizens, decision-making, and accountability. Governments have a key role in this network, since good governance implies managing public affairs in a transparent, accountable, participatory, and equitable manner [7]. Determining the quality of governance requires the measurement of two achievements: (1) improvements in public policy outcomes, and (2) improvements in respect of principles of governance. Of course, both aspects are strongly related and can be considered two sides of the same coin. As noted by Bovaird and Löffler [8], the quality of good governance can be inferred from the achievement of key quality of life domains and by how far each of the key governance principles has been honored.

However, it is unclear how these aspects relate to each other in practice. Does transparency improve governance? Does quality of life relate to government efficiency or accountability? Are those regions with more civic engagement the ones in which good governance has promoted more welfare? The aim of this article is to analyze the relationship between quality of life conditions in municipalities and three key governance principles: transparency, participation, and financial accountability.

The paper is structured as follows. Section 2 reviews the importance of quality of life (QoL) as a performance indicator of social progress, indicating the dimensions that must be assessed and including a proposal for measuring QoL in Spanish municipalities. Section 3 explores the relationship between good governance and the quality of life in municipalities, introducing some testable hypothesis. Section 4 briefly describes the methodology to construct the composite indicators of QoL. Section 5 presents the empirical results, and concluding remarks are included in a final section.

2. Quality of Life (QoL) As a Measure of Social Progress in Municipalities

According to Bovaird and Loffler [1] (p. 16), local governance is “the set of formal and informal rules, structures, and processes which determine the ways in which individuals and organizations can exert power over the decisions (made by other stakeholders) which affect their welfare at the local level”. Consequently, good local governance should be accompanied by the achievement of high levels of social, economic, and environmental welfare, through the cooperation and interaction of multiple stakeholders (local authorities, business, voluntary sector, media, etc.).

Verifying the existence of good local governance requires assessing the impacts or outcomes of public policies, that is, the effect of public policies on the quality of life of the citizens (something that goes beyond the mere outputs or services provided). For instance, better governance should improve physical safety, for which it is necessary to reduce crime (outcome), but this cannot be assured simply by increasing the number of police hours (output). Citizens and other stakeholders are interested in measuring the success of public interventions in terms of the changes they bring in the quality of life, rather than by the quality of the activities themselves. However, as Rotberg [9] indicates, governance is tangible, and measuring performance can best be done by using publicly available objective data.

In turn, measuring the quality of life of the citizens is far from being an easy task. Traditionally, aggregated macroeconomic figures have been used in order to track the progress of societies. However, using aggregated macroeconomic variables oversimplifies the problem. The flaws of conventional measures, such as the Gross Domestic Product (GDP), are well-known to economists and social scientists [10]. Instead, alternative socio-economic variables that complement GDP and are informative about the degree of human development in society are needed [11]. These measures should be based on considering the multiple dimensions that account for all the factors that contribute to welfare and sustainability in modern societies.

Many different institutions have taken the challenge of developing statistics in order to measure the quality of life of the citizens in recent years. The European Commission and the OECD have proposed different frameworks for measuring the quality of life in countries [12]. At the local level (municipalities), information is still not very well developed. The Urban Audit Project (UAP) contains very valuable information about the largest European cities, but the sample size is not large enough to perform a comprehensive internal analysis of any European country. However, many researchers have overcome these difficulties and have found ways to estimate QoL indexes in municipalities [13]. We can cite [14] or [15] for the US, [16] for Japan, or [17] for Europe. However, there are not many examples of specific estimations of quality of life in municipalities within specific countries in Europe. Recent examples are [18] for Italy, [19] for Estonia, and [20] for the Czech Republic. As for Spain, [21,22,23,24,25,26,27,28], have done so for different territories of the country. More recently, González et al. [12] and Cárcaba et al. [29] have tracked the evolution of municipal QoL in Spain between 2001 and 2011. This research builds on the methodological proposal for the measurement of the QoL in Spain contained in these two references. The proposal includes the use of seven dimensions, which correspond with the most influential proposals in the recent literature (see [12] for details). Namely, the seven dimensions are: Material Living Conditions, Health, Education, Environment, Economic and Physical Safety, Social Interaction, and Personal Activities. This multidimensional approach to evaluate the quality of life is difficult to implement in practice, since the statistical information required at the local level is not readily available in Spain. However, from this specification of dimensions, we were able to collect data for all the municipalities with populations over 20,000 in 2011 by combining different data sources, typically including microdata. The total sample includes 393 municipalities, which cover around 65% of the Spanish population. We collected two subindicators for each of the seven dimensions considered. Therefore, we use a battery of 14 subindicators in order to construct a single composite indicator of the quality of life.

Let us briefly describe the subindicators employed (a full description of these indicators can be found in [12]). The first dimension represents the material living conditions, which is approximated by the Average Socioeconomic Condition (ASC), which informs about the social status of the individuals in the census, and by a housing variable that reflects the Quality of the Dwellings (QD). The second dimension (Health) is represented by two variables that measure Excess Mortality (EM) and Avoidable Mortality (AM). The first of these measures how much higher or lower the death rate of the population is than expected given the age structure. The second measures the number of deaths that can be considered avoidable given current medical and preventive practices [30]. It includes deaths that could be avoided by a good functioning of health services and also deaths which are strongly related to bad habits such as smoking or alcoholism. In order to compute this indicator, we used the list of avoidable causes of death identified by Gispert et al. [30] and counted all the deaths that can be attributed to one or several of those causes during the year. Then, the AM indicator is the sum of these avoidable deaths, divided by the total population of the municipality.

Third, we use the Overall Level of Education (OLE) and the population with higher education (UD) as the two subindicators of the Education dimension. The Environment dimension is approximated by two air pollutants that represent a high concern for the World Health Organization [31]. These are the Particulate Matter (PM10) and the Ozone (O3). Economic safety is measured by the Unemployment Rate (UR), while physical safety is measured by the Crime Rate (CRI). In turn, the Social Interaction dimension is represented by the percentage of the population that is engaged in Volunteering Activities (VA) and by the number of Cultural and Social Facilities (CSC). Finally, the last dimension (Personal Activities) is approximated by the Commercial Market Share (CMS), which is a measure of consumption and commercial activity, and with the Commuting Time (CT), a variable strongly related to QoL [32].

In Section 4 we explain how these 14 subindicators are combined or aggregated in order to produce a composite indicator of the QoL. This composite indicator will reflect improvements in the QoL as the subindicators considered improve and must be comparable across municipalities. We will propose the construction of a QoL frontier, in which the best municipalities (in terms of QoL) act as referents or benchmarks of the remaining municipalities.

3. Good Governance Principles and Quality of Life in Municipalities

As we have just seen, quality of life is a complex and multidimensional concept. The same applies to the notion of good governance. The United Nations Development Program [33] identified nine principles of good governance, which have influenced subsequent academic literature [4,6,34]:

- ■

- Participation: all men and women should have a voice in decision-making, either directly or through legitimate intermediate institutions representing their interests.

- ■

- Rule of law: legal frameworks should be fair and enforced impartially.

- ■

- Transparency: this is built on the free flow of information. Processes, institutions, and information must be directly accessible to concerned users, and enough information should be provided to allow for effective understanding and monitoring.

- ■

- Responsiveness: institutions and processes must aim at serving all the stakeholders.

- ■

- Consensus orientation: good governance must be able to mediate conflicting interests in order to reach a broad consensus on what is in the best interest of the group.

- ■

- Equity: all men and women must have opportunities to improve or maintain their quality of life.

- ■

- Effectiveness and efficiency: processes and institutions should produce results that satisfy needs, making the best possible use of resources.

- ■

- Accountability: decision-makers in government, the private sector, and civil society organizations must be held accountable to the public, as well as to institutional stakeholders.

- ■

- Strategic vision: leaders and the public must have a broad and long-term perspective on good governance and human development, along with a sense of what is needed for such development.

These principles interact with each other in complex ways, reinforcing each other, and cannot be developed in isolation. For instance, better access to information fosters transparency, but also civic engagement and effective decision-making. Civic engagement feeds the flow of information and increases legitimacy in decision-making. Legitimacy, in turn, encourages participation. In order to be equitable, institutions must be transparent and follow the rule of law.

Measuring these characteristics of good governance is far from straightforward. In this paper, we focus on the assessment of the relationship between the quality of life in Spanish municipalities and three of these dimensions, namely transparency, participation, and financial accountability, which can be measured with available municipal data.

3.1. Transparency

Many different definitions of transparency have been formulated within the literature about good governance. All of them highlight the same fundamental attributes. Transparency implies that information is available and accessible to those affected by government decisions (stakeholders), and that this information is reliable and comes in an understandable format. Thus, availability, accessibility, reliability, and understandability are the necessary constituents of transparency.

According to Vishwanath and Kaufmann [35], transparency implies an appropriate flow of timely and reliable economic, social, and political information, which must be accessible to all relevant stakeholders. In the public sector, transparency implies an openness of the governance system through clear processes and procedures and easy access to public information for citizens [4]. Pietrowski and Van Ryzin [36] define governmental transparency as the ability to find out what is going on inside a public sector organization through avenues such as open meetings, access to records, or the proactive posting of information on websites. With these elements, any stakeholder may obtain reliable information about the activities of the municipality that are a concern for him or her and is able to understand and interpret this information.

Transparency in the public sector has been the object of analysis in numerous papers, which also examine its drivers (see, for instance, [37,38,39,40,41,42]. Some research has focused specifically on the relationship between transparency and governance, studying the role of information disclosure in shaping a better government, improving the design of public policy (help identifying goals), or reducing corruption [43,44,45,46,47].

In general, research highlights the critical importance of accessibility of government information as a necessary condition for good governance. However, there may also be some drawbacks with transparency. For instance, Bac [48] notes that high transparency increases the probability of detecting corruption or wrongdoing, but it may also increase the visibility of key decision-makers, thereby placing stronger incentives to establish “connections” for corruption. Ref. [49] shows that the transparency of the political system does not unambiguously improve efficiency: transparency of revenues can be counterproductive because it endogenously leads to increased wasteful spending. Bauhr and Grimes [50] show how an increase in transparency in highly corrupt countries tends to breed citizen resignation rather than indignation.

However, transparency in public management is a requirement for building social capital and for human development. This does not imply a direct effect on the quality of life of the citizens, since transparency alone would not lead to this outcome. However, without transparency public management tends toward inefficiency by the lack of control. Back in 1913, Louis Brandeis referred to this when writing “Sunlight is said to be the best of disinfectants; electric light is the most efficient policeman” [51]. Without transparency, there is no way in which citizens may exercise informed political choice. Therefore, transparency is crucial for effective participation leading to social development and welfare improvement. Transparency adds clarity and accountability to public administration, which otherwise is prone to corruption. Therefore, it should relate to the improvements in the quality of life of the citizens. This leads to our first testable hypothesis:

Hypothesis 1.

Higher transparency implies better governance and should result in higher quality of life in the municipality.

To measure the degree of Transparency we employ the index constructed by the NGO Transparency International for the biggest Spanish municipalities. This NGO has the objective of fighting corruption by pursuing greater transparency and the realization of the principles of accountability by monitoring the performance of key institutions. Access to information is seen as the best tool in the fight against misbehavior in public administration. Unfortunately, only 110 municipalities are listed in the report of Transparency International. For this reason, this first hypothesis of this paper will only be tested in a reduced subsample of the complete sample.

3.2. Participation

According to Arnstein [52], citizen participation is a reflection of citizen power. Extensive participation grants access to decision-making, involving people in the economic, political, cultural, and social processes that affect them. The way to approach participation has gradually turned from a citizenship obligation to a citizenship primary right, which commits not only citizens, but also civil society, state agencies, and institutions [53]. The institutionalization of participation has occurred through regular election processes, council hearings, and, more recently, participatory budgeting. Nowadays, participatory governance means a convergence of social and political participation and the scaling up of participatory methods, state-civil partnerships, decentralization and devolution, participatory assessment, and other factors [54].

The types of participation are varied, ranging from being mere spectators who receive information about some policy or project, to the effective involvement in the negotiation of public policies; from voting for elected representatives at regular intervals, to engaging in legal or even illegal protest. Participation is not only having the mechanisms to participate, but using them effectively. According to Fung [55], the modes of participation vary along three dimensions—scope of participation, mode of communication and decision, and extent of authority—addressing three important problems of democratic governance: legitimacy, justice, and effective governance.

Citizens’ participation in community decision-making implies better governance. Citizen involvement in policy-making makes people feel more responsible for public matters and increases public engagement, encourages people to listen to a diversity of opinions, and thus promotes mutual understanding, and contributes to greater legitimacy of decisions [56]. The link between participation and policy outcomes is a core tenet of much of the scholarly literature. Political participation affects the type of policies that the government implements, leads to different policy outcomes, and leads to superior social outcomes because of participation’s role in aggregating information and preferences [57,58,59]. As such, its effect on the quality of life of the citizens must be positive, which leads to our second testable hypothesis:

Hypothesis 2.

Higher participation of citizens implies better governance and should result in higher quality of life in the municipality.

We measure civic participation by the voter turnout in the municipal elections of 2011.

3.3. Financial Accountability

According to the UNDP [33], good governance implies the existence of an accountable government. Decision-makers in government are accountable to the public, and different stakeholders may hold the government and its representatives accountable for different issues (safe keeping of inputs, efficiency of operations, or compliance with laws). Not surprisingly, accountability in public administration also has different views. In a narrow sense, it can be defined as ‘the obligation to explain and justify conduct’ [60]. However, accountability is normally invoked in a broader sense which involves honesty, legality, efficiency, or good administration [61,62,63]. In this paper, we focus on the financial side of accountability.

In Concepts Statement nº 1, the Governmental Accounting Standards Board (GASB) states that governmental financial reporting should provide information to assist users in assessing accountability. While it is only one of multiple sources of information, financial reporting plays a major role in fulfilling the government’s duty to be publicly accountable in a democratic society. That document also notes that financial information can be used to assess a state or local government’s financial condition, that is, its financial position and its ability to continue to provide services and meet its obligations as they come due [64] (par. 34).

As such, the mere existence of financial information is an exercise of accountability. However, it is also required that this information evidences appropriate use of financial resources, budgetary execution, liquidity and solvency, indebtedness, cost of the services, and goals achieved. In this sense, the accumulation of public debt or the lack of liquidity implies a non-responsible use of public resources. This leads to our third hypothesis.

Hypothesis 3.

Financial accountability, as represented by measures of financial condition, implies better governance and should result in higher quality of life in the municipality.

In this paper, financial accountability will be measured by two measures which are commonly used to evaluate the quality of financial management in local governments. The first one is the cash surplus of the municipality in 2011. In the Spanish accounting regulation, the cash surplus (remanente de tesorería) is defined as a variable that has the aim of showing the cumulative surplus/deficit of the current and the previous yearly budgets. It is an extended opinion within public managers that this indicator is a good proxy of the quality of financial management in the local entity [65], as it considers the cumulative effect of the decisions taken in relation to the assignment of public resources. The cash surplus is useful because it allows financial reporting users to assess the balance of the financial activity, showing the financial capacity or financial need of the entity at the end of the period. This is a specific magnitude in the Spanish accounting regulation that can be considered the main indicator of financial health [66]. The second indicator of financial accountability is the debt per capita of the municipality in 2011. Debt is also a stock variable that reflects the cumulative effect over time of budgetary slippage in the municipality, and it can be considered a negative indicator of good governance.

4. Estimating Quality of Life Scores in Municipalities

In order to estimate the QoL scores, we used the 14 subindicators mentioned in Section 2. These subindicators must now be aggregated into a single composite indicator, reflecting the overall QoL conditions of the municipality under analysis. For the aggregation of this information, many possible methodologies have been suggested in the literature [67], from equal weighting (i.e., direct sum of all the subindicators after some normalization) to factor analysis. In this paper, we follow the methodology described in [12], which is based on the Benefit of the Doubt (BoD) approach originally developed by Melyn and Moesen [68]. The BoD approach proposes to compute a weighted sum of the subindicators of QoL and then tries to find the most favorable weights for each municipality, that is, the ones that maximize the QoL score. In doing so, the score obtained can be understood as the maximum possible score that can be obtained under any possible linear aggregation method. Data Envelopment Analysis (DEA) finds exactly this structure of the most favorable weights. DEA is a mathematical programming technique that was originally proposed by Charnes et al. [69] to measure efficiency in production. It has also been widely used in the estimation of QoL indexes (see [70] for an extensive review of the literature).

However, the application of DEA to the computation of QoL scores must be done with caution. Sharpe and Andrews [71] noted that this technique may produce unrealistic results by giving unreasonable weights to the variables employed. By searching for the BoD weights, many variables may receive null weights simply because their values are low [72], and the method tries to maximize the QoL score. This is the reason why it is convenient to introduce weight constraints within the DEA mathematical program, in order to constrain this flexibility and disparity of weights. Introducing weight constraints limits the BoD properties of the technique, but improves consistency and comparability of the scores. The cost of it is that weight restrictions also imply some sort of value judgement. In this paper, we aim to use weight constraints to correct the inconsistencies of unconstrained DEA while, at the same time, imposing minimum external value judgement. The starting point of the proposed methodology is the formulation of a QoL frontier using the ratio form specification of the original DEA program, which computes the BoD score of QoL:

where xim is the input m in city i, yis is the output s in city i, vm is the weight of subindicator m, and us is the weight of subindicator s and j of any city included in the sample. Inputs can be thought of as indicators that should be reduced in order to improve QoL conditions (unemployment, for instance) and outputs as indicators that should be increased (education, for instance). The program minimizes the ratio of input to output value using a reference value (of 1) as the minimum. The alternative interpretation of maximizing the ratio of output to input value using a reference value (of 1) as the maximum or frontier value is more widespread and straightforward. Thus, the weights of inputs and outputs are selected for each municipality so as to minimize that ratio, thereby obtaining a value that refers to 1 in comparison with the rest of the municipalities. A value equal to 1 implies that it is possible to find weights that place the municipality on the frontier, so that no other municipality with those same weights can obtain a better ratio.

This mathematical program matches the original formulation of DEA and is perfectly consistent with the BoD philosophy. However, it is problematic for a number of reasons. First, it forces the researcher to establish which variables are to be considered as inputs and which ones as outputs. In the context of QoL measurement, this is something essentially arbitrary, as it depends on how these variables are defined and measured. To avoid this problem, we preferred to convert all the subindicators to output variables, regardless of their original definition in the database. Our original variables come in the form of outputs and inputs. In order to transform all of them into dimensionless outputs, we applied the “distance to the group leader” normalization used by Cherchye et al. [73], dividing all output variables by their maximum and dividing the minimum of all input variables by their values. See [12] for more details on this way of normalizing. After this normalization is done, all the resulting subindicators take values within the (0,1) interval. Values closer to 1 indicate better QoL conditions, while values closer to 0 indicate worse QoL conditions regarding that subindicator. With all the variables transformed this way, we can compute the BoD composite indicator of QoL solving the next linear program for each municipality [74]:

This program is equivalent to the original DEA formulation, for the case that all variables are outputs. In this case, the mathematical program finds the weights that maximize the aggregated value of the normalized outputs and compares this value with the rest of the municipalities giving the maximum a reference value of 1. The QoL of the municipality under analysis (i) must be interpreted in relation with this maximum of 1. The municipalities obtaining a value equal to 1 will be placed on the QoL frontier and, therefore, will act as referent for the rest of the municipalities, which will be below the frontier even with their best possible set of weights (BoD). The optimal value of the objective function will reflect the distance from the municipality to the QoL frontier in proportional terms.

The second issue with this methodology is the absolute freedom to select the most favorable weights. This implies differences in the weights of the municipalities which compromise comparability of the scores, since the weights under which those scores are computed may be completely different. For this reason, we included some constraints within the mathematical program in order to restrict the acceptable range of weights that municipalities can take in the computation of the QoL score. This way, we still allow for some BoD, since the municipalities can select their most favorable weights, but only within a range that can be considered acceptable. At a minimum, this implies ruling out null weights. We go much further in order to restrict considerably the acceptable range of weight variation. Although there are many possible ways to restrict weights in DEA, we followed the Wong and Beasley [75] procedure of delimiting the weight shares of each subindicator with the following constraints:

This procedure introduces the 14 restrictions into the DEA program in the form of weight shares, one per subindicator. This is, we restrict the relative importance that each weight may have in the total weighting of the QoL score. This way of introducing constraints maintains the units’ invariance property [74] and produces results which are halfway between the complete weight flexibility of BoD and equal weighting. Our proposal is to obtain a weighting method that gets in-between complete BoD flexibility and equal weighting (no flexibility at all). This amounts to providing 50% flexibility and imposing 50% common weighting. Given that we have 14 subindicators, the limits to impose 50% common weighting for all municipalities imply ranging from 3.571% to 10.714%. Since all the 14 indicators must have at least a weight of 3.571%, the total common weight is equal to 3.571% × 14 = 50%. Equal weighting would be in the middle of the imposed range (7.143%). We provide 50% variation around this reference to half (3.571%) or one and a half (10.714%). We also tried with alternative limits for the weighting constraints, as shown in González et al. (2016). The results are quantitatively and qualitatively similar under all the specifications.

5. Results

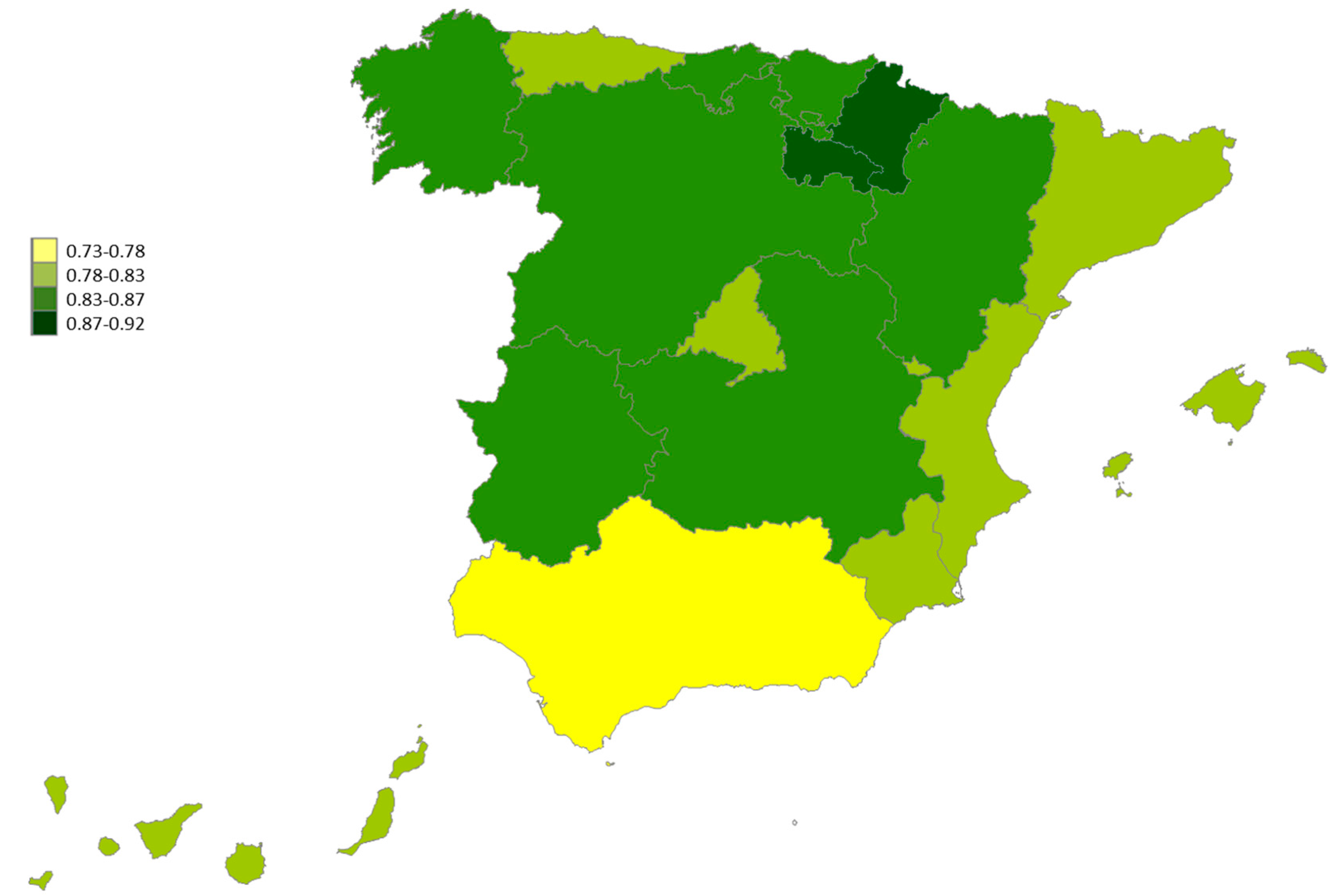

A complete description of the QoL scores and its geographical distribution across the territory can be found in [12]. In this paper, we summarize these results by showing the distribution of averages per region in Figure 1. Central-North municipalities show the highest QoL scores, while Southern municipalities (including the Canary Islands) achieve the lowest scores. While there is no relationship between city size and QoL, the biggest cities (Madrid and Barcelona) obtain only moderate scores. This means that, comparatively, they do not score as high in the combination of dimensions considered as other smaller municipalities included in the sample.

The focus of this paper is on how this distribution of QoL relates to the distribution of good governance practices over the sample. Table 1 shows descriptive statistics of the variables that will be used in our empirical analysis. In regards to the QoL, transparency, participation, and accountability variables, we added some demographic control variables that may also relate to QoL: population density per square kilometer, population average age, and population growth. average QoL is 0.77, which means that the average municipality is 23% down with respect to the municipalities with the best quality of life. The worst municipality in terms of QoL only reaches 38.5% of the maximum attainable. The transparency index ranges from 15 to 100, with 70.91 being the average. Participation and accountability variables were normalized to vary between 0 and 1. We appreciate more dispersion in accountability than in participation, especially in the variable debt per capita. In turn, the demographic control variables show important variation within the sample.

Table 2 shows the results of the regression analysis of QoL on the governance variables. We estimated three different models. The first two include the variable Transparency and therefore are run on the reduced sample (110 observations) for which this variable is available. The first model includes regional dummies, while the second one does not. The region excluded is Andalucia. Therefore, all the coefficients must be interpreted in comparison to Andalucia. The reason to control for regional dummies is that some competencies that are important for determining QoL conditions (such as health or education) are the responsibility of the regional governments. Finally, the third model is run on the entire sample (393 observations), without the variable Transparency. The results are very stable across models. As we can observe, Transparency does not relate significantly to the quality of life of the municipalities, while Participation and Accountability (Cash Surplus) present a positive and significant relationship in the three specifications estimated. In contrast, Debt Per Capita does not relate significantly to QoL in any of the models. The control variable population density correlates negatively with QoL, although it is not significant in the full sample. In contrast, population age has a positive and significant effect in the full sample. There is no effect of population growth on the quality of life.

By construction, the QoL index is bounded within the (0,1] interval. Thus, we cannot assume that the dependent variable of our model (the QoL score) varies freely from “−infinity” to “+infinity”, as is done in conventional OLS estimation. Instead, the distribution of the QoL score is truncated within the (0,1] interval. For this reason, we repeated the estimations using a truncated model, specifying these limits as the truncation points. The results, shown in Table 3, are qualitatively very similar. There is no effect of Transparency, and we also find a robust positive effect of Participation and Accountability (Cash Surplus), and no significant effect of Debt Per Capita. The effects of the control variables are also similar, but the relations are more intense in terms of statistical significance.

In sum, our results provide strong support for Hypothesis 2 (the role of Participation in QoL), some support for Hypothesis 3 (the role of Accountability in QoL), and no support for Hypothesis 1 (the influence of Transparency in QoL). However, transparency is only measured within the subsample of the largest municipalities. In turn, Hypothesis 3 is only validated with one of the variables (Cash Surplus), which is claimed by experts to be the single most important variable in order to approximate financial accountability in Spanish local governments [65]. We find no significant effect of Debt Per Capita, a variable that also relates to financial accountability. Additionally, regional dummies seem to capture important differences in the QoL of the municipalities, as expected. Regarding the control variables, ageing and population density seem to have a relationship with the QoL (although in opposite directions), while population growth seems to be unrelated. In principle, this last result may seem counterintuitive, since we could expect that migration flows would tend to favor the municipalities with a higher QoL. This is the traditional idea of Tiebout [76], that people would vote with their feet. However, these migration flows may also have the effect of reducing perceived QoL among existing residents, which might explain the lack of a positive relationship.

6. Concluding Remarks

The ultimate goal of society should be to improve the welfare of the citizens and contribute to human development. The focus of public policy on aggregate macroeconomic measures such as the GDP is therefore misplaced. Other social aspects of well-being should be considered, such as health, crime, leisure, a clean environment, etc. Quality of life indexes aim to complement macroeconomic figures with socio-economic figures summarizing welfare in society. Institutions such as the European Union or the OECD have taken the challenge of developing measures of well-being capable of guiding policy-making. However, most efforts are oriented towards comparing the evolution of countries. Much less work has been done in measuring the quality of life at the local level of analysis. In this paper, we have combined information on seven dimensions that relate to the quality of life at the municipal level in Spain. In order to represent these seven dimensions, we have carefully collected 14 subindicators covering economic concerns, but also health, education, safety, environment, or personal activities. Our sample covers 65% of the Spanish population with a total of 394 municipalities. A considerable effort has been made in order to find meaningful indicators that cover those dimensions for a big sample.

The major goal of our paper was to examine how QoL related to good governance, understood here as one of its drivers. We believe this is especially important at the local level of the public administration. We used measures of three aspects of good governance in order to check for the existence of such relationships. First, we employed the index of transparency developed by International Transparency for 2011 in order to account for the degree of information disclosure in local public affairs. Second, we used voter turnout as a measure of participation in local politics. Finally, we used two measures of the financial condition (cash surplus and debt per capita) as indicators of financial accountability. Our results show a significant positive relationship between participation and financial accountability (when measured by the cash surplus indicator) and the quality of life. However, we did not find a significant relationship between quality of life and transparency or debt per capita.

These results point to interesting relationships between local government good governance practices and the quality of life of the citizens. In particular, the results highlight the importance of citizen participation and financial accountability. This evidence stresses the importance of deepening the degree of citizen participation in decision-making at the municipal level. Some Spanish cities have already taken the challenge of taking participation a step further from simply voting every four years. For instance, the local government of Madrid has recently established a procedure for participatory budgeting that will help decide how to spend 100 million euros during 2017. If participation leads to better assignment of these resources to meet the real needs of the citizens, it is clear how this can result in improvement in the QoL. In the case of Barcelona, 5% of the budget is decided by these participation procedures. In addition, many more cities are taking the challenge of opening up to citizen participation. In 2015, the Spanish Federation of Municipalities and Provinces (FEMP) created the Network of Local Governments for Transparency and Citizen Participation in order to foster transparency and participation in decision-making. Today, some 200 municipalities are members of this network and, therefore, demonstrate an adherence to these practices of good governance. Unfortunately, this represents only 2.5% of the municipalities in Spain. The results in this paper provide new evidence favoring the generalization of these practices.

The fact that our results do not confirm any relationship between transparency and the quality of life is worrying. We strongly believe that there must be some relationship between these variables, at least in the long-run. Two limitations of our empirical study may partially explain this lack of evidence. First, we only have data on transparency for a reduced subsample of 110 municipalities, which may condition this result. Second, the index elaborated by International Transparency only accounts for the most formal aspects of transparency, which most of the municipalities satisfy. That is, the great majority of the municipalities in the sample score high in the variable transparency. Future research should make an effort to develop and incorporate better measures of transparency, which should be available for a larger sample. Additionally, future research should also consider additional dimensions of good governance which were not accounted for in this paper due to data limitations. These efforts will surely deepen our understanding of the underlying relationships between good governance practices and the quality of life of the citizens.

Acknowledgments

This research was financed by the Spanish “Ministerio de Economía y Competitividad”, project code: MINECO CSO2013-43359-R and co-financed with ERDF funds. The authors gratefully acknowledge all the institutions that provided access to restricted access data without which this study would not have been possible: “Instituto Nacional de Estadística”, “Ministerio del Interior”, “Departament d’Interior-Generalitat de Catalunya”.

Author Contributions

Ana Cárcaba is the main author of this paper. She designed the research and worked out the hypotheses. Eduardo González contributed with the estimation of the QoL indexes and writing. Juan Ventura did the revision of literature and main writing of the final manuscript. Rubén Arrondo is responsible for the econometric analysis of the data.

Conflicts of Interest

The authors declare no conflict of interest.

References

- Bovaird, T.; Löffler, E. Moving from excellence models of local service delivery to benchmarking of ‘good local governance’. Int. Rev. Adm. Sci. 2002, 68, 9–24. [Google Scholar] [CrossRef]

- World Bank. Proceedings of the World Bank Annual Conference on Development Economics 1992; Supplement to The World Bank Economic Review and The World Bank Research Observer; World Bank: Washington, WA, USA, 1991. [Google Scholar]

- Weiss, T.G. Governance, good governance and global governance: Conceptual and actual challenges. Third World Q. 2000, 21, 795–814. [Google Scholar] [CrossRef]

- Kim, P.; Halligan, J.; Cho, N.; Oh, C.; Eikenberry, A. Toward Participatory and Transparent Governance: Report on the Sixth Global Forum on Reinventing Government. Public Adm. Rev. 2005, 65, 646–654. [Google Scholar] [CrossRef]

- Grindle, M. Good Governance: The Inflation of an Idea; Planning ideas that matter; Harvard Kennedy School: Cambridge, MA, USA, 2012; pp. 259–282. [Google Scholar]

- Bovaird, T.; Löffler, E. Evaluating the quality of public governance: Indicators, models and methodologies. Int. Rev. Adm. Sci. 2003, 69, 313–328. [Google Scholar] [CrossRef]

- Santiso, C. Good Governance and Aid Effectiveness: The World Bank and Conditionality. Georget. Public Policy Rev. 2001, 7, 1–22. [Google Scholar]

- Bovaird, T.; Löffler, E. Assessing the quality of local governance: A case study of public services. Public Money Manag. 2007, 27, 293–300. [Google Scholar] [CrossRef]

- Rotberg, R.I. Good governance means performance and results. Governance 2014, 27, 511–518. [Google Scholar] [CrossRef]

- Stiglitz, J.; Sen, A.; Fitoussi, J.P. Mismeasuring Our Lives: Why GDP Doesn’t Add up; The New York Press: New York, NY, USA, 2010. [Google Scholar]

- Ranis, G.; Stewart, F. Economic Growth and Human Development. World Dev. 2000, 28, 197–219. [Google Scholar] [CrossRef]

- González, E.; Cárcaba, A.; Ventura, J. Weight Constrained DEA Measurement of the Quality of Life in Spanish Municipalities in 2011. Soc. Indic. Res. 2017. [Google Scholar] [CrossRef]

- Ballas, D. What makes a happy city? Cities 2013, 32, 39–50. [Google Scholar] [CrossRef]

- Becker, R.A.; Denby, L.; McGill, R.; Wilks, A.R. Analysis of data from the Places Rated almanac. Am. Stat. 1989, 41, 169–186. [Google Scholar] [CrossRef]

- Marshall, E.; Shortle, J. Using DEA and VEA to evaluate quality of life in the Mid-Atlantic states. Agric. Resour. Econ. Rev. 2005, 34, 185–203. [Google Scholar] [CrossRef]

- Hashimoto, A.; Ishikawa, H. Using DEA to evaluate the state of society as measured by multiple social indicators. Socio-Econ. Plan. Sci. 1993, 27, 257–268. [Google Scholar] [CrossRef]

- Morais, P.; Camanho, A. Evaluation of Performance of European cities with the aim to promote quality of life improvements. Omega 2011, 39, 398–409. [Google Scholar] [CrossRef]

- Bigerna, S.; Polinori, P. Quality of life in major Italian cities: Do local governments cost efficiency contribute to improve urban life style? An introductory analysis. Econ. Policy Energy Environ. 2013, 3, 121–144. [Google Scholar] [CrossRef]

- Poldaru, R.; Roots, J. A PCA-DEA approach to measure the quality of life in Estonian counties. Socio-Econ. Plan. Sci. 2014, 48, 65–73. [Google Scholar] [CrossRef]

- Murgaš, F.; Klobučnik, M. Municipalities and regions as good places to live: Index of quality of life in the Czech Republic. Appl. Res. Qual. Life 2016, 11, 553–570. [Google Scholar] [CrossRef]

- González, E.; Cárcaba, A.; Ventura, J. The importance of the geographic level of analysis in the assessment of the Quality of Life: The case of Spain. Soc. Indic. Res. 2011, 102, 209–228. [Google Scholar] [CrossRef]

- Martin, J.C.; Mendoza, C. A DEA approach to measure the Quality of Life in the municipalities of the Canary Islands. Soc. Indic. Res. 2013, 113, 335–353. [Google Scholar] [CrossRef]

- Royuela, V.; Suriñach, J.; Reyes, M. Measuring QoL in small areas over different periods of time: Analysis of the province of Barcelona. Soc. Indic. Res. 2003, 64, 51–74. [Google Scholar] [CrossRef]

- Zarzosa, P. La Calidad de Vida en los Municipios de Valladolid; Diputación Provincial de Valladolid: Valladolid, Spain, 2005. (In Spanish) [Google Scholar]

- López, M.E.; Sánchez, P. La medición de la calidad de vida en las comarcas gallegas. Revista Galega de Economía 2009, 18, 1–20. [Google Scholar]

- Murias, P.; Martínez, F.; Miguel, C. An economic well-being index for the Spanish provinces: A Data Envelopment Analysis approach. Soc. Indic. Res. 2006, 77, 395–417. [Google Scholar] [CrossRef]

- Jurado, A.; Perez-Mayo, J. Construction and evolution of a multidimensional well-being index for the Spanish regions. Soc. Indic. Res. 2012, 107, 259–279. [Google Scholar] [CrossRef]

- Navarro, J.M.; Artal, A. Foot voting in Spain: What do internal migrations say about Quality of Life in the Spanish municipalities? Soc. Indic. Res. 2015, 124, 501–515. [Google Scholar] [CrossRef]

- Cárcaba, A.; González, E.; Ventura, J. Social progress shift in Spanish municipalities (2001–2011). Appl. Res. Qual. Life 2017. [Google Scholar] [CrossRef]

- Gispert, R.; Arán, M.; Puigdefábregas, A. Grupo para el Consenso en la Mortalidad Evitable La mortalidad evitable: Lista de consenso para la actualización del indicador en España. Gaceta Sanitaria 2006, 20, 184–193. [Google Scholar] [CrossRef] [PubMed]

- World Health Organization WHO. Air Quality Guidelines for Particulate Matter, Ozone, Nitrogen Dioxide and SULFUR DIOXIDE. GLOBAL UPDATE 2005 (Summary of Risk Assessment); World Health Organization, Regional Office for Europe: Copenhagen, Denmark, 2006. [Google Scholar]

- Stutzer, A.; Frey, B.S. Stress that doesn’t pay: The commuting paradox. Scand. J. Econ. 2008, 110, 339–366. [Google Scholar] [CrossRef]

- United Nations Development Program (UNDP). Governance and Sustainable Human Development; UNDP Governance policy Paper; UNDP: Norwalk, CA, USA, 1997. [Google Scholar]

- Graham, J.; Amos, B.; Plumptre, T. Principles for good governance in the 21st century. Policy Brief 2003, 15, 1–6. [Google Scholar]

- Vishwanath, T.; Kaufmann, D. Towards Transparency in Finance and Governance; World Bank-Economic Development Institute: Washington, WA, USA, 1999; SSRN 258978. [Google Scholar]

- Piotrowski, S.J.; Van Ryzin, G.G. Citizen attitudes toward transparency in local government. Am. Rev. Public Adm. 2007, 37, 306–323. [Google Scholar] [CrossRef]

- Smith, K.A. Voluntarily reporting performance measures to the public a test of accounting reports from US Cities. Int. Public Manag. J. 2004, 7, 19. [Google Scholar]

- Laswad, F.; Fisher, R.; Oyelere, P. Determinants of voluntary Internet financial reporting by local government authorities. J. Account. Public Policy 2005, 24, 101–121. [Google Scholar] [CrossRef]

- Cárcaba, A.; García, J. Determinants of online reporting of accounting information by Spanish local government authorities. Local Gov. Stud. 2010, 36, 679–695. [Google Scholar]

- Guillamón, M.D.; Bastida, F.; Benito, B. The determinants of local government’s financial transparency. Local Gov. Stud. 2011, 37, 391–406. [Google Scholar] [CrossRef]

- Del Sol, D.A. The institutional, economic and social determinants of local government transparency. J. Econ. Policy Reform 2013, 16, 90–107. [Google Scholar] [CrossRef]

- García-Sánchez, I.M.; Frías-Aceituno, J.V.; Rodríguez-Domínguez, L. Determinants of corporate social disclosure in Spanish local governments. J. Clean. Prod. 2013, 39, 60–72. [Google Scholar] [CrossRef]

- Kaufmann, D.; Mehrez, G.; Gurgur, T. Voice or Public Sector Management? An Empirical Investigation of Determinants of Public Sector Performance Based on a Survey of Public Officials; World Bank Research Working Paper; World Bank Group: Washington, WA, USA, 2002. [Google Scholar]

- Kaufmann, D.; Kraay, A. Growth without Governance; World Bank Policy Research Working Paper, 2928; World Bank Group: Washington, WA, USA, 2002. [Google Scholar]

- Islam, R. Does more transparency go along with better governance? Econ. Politics 2006, 18, 121–167. [Google Scholar] [CrossRef]

- Bastida, F.; Benito, B. Central government budget practices and transparency: An international comparison. Public Adm. 2007, 85, 667–716. [Google Scholar] [CrossRef]

- Lindstedt, C.; Naurin, D. Transparency is not enough: Making transparency effective in reducing corruption. Int. Political Sci. Rev. 2010, 31, 301–322. [Google Scholar] [CrossRef]

- Bac, M. Corruption, connections and transparency: Does a better screen imply a better scene? Public Choice 2001, 107, 87–96. [Google Scholar] [CrossRef]

- Gavazza, A.; Lizzeri, A. Transparency and economic policy. Rev. Econ. Stud. 2009, 76, 1023–1048. [Google Scholar] [CrossRef]

- Bauhr, M.; Grimes, M. Indignation or resignation: The implications of transparency for societal accountability. Governance 2014, 27, 291–320. [Google Scholar] [CrossRef]

- Brandeis, L.D. What publicity can do. Harpers Weekly, 20 December 1913; 10–13. [Google Scholar]

- Arnstein, S.R. A ladder of citizen participation. J. Am Inst. Plan. 1969, 35, 216–224. [Google Scholar] [CrossRef]

- Hickey, S.; Mohan, G. Relocating participation within a radical politics of development. Dev. Chang. 2005, 36, 237–262. [Google Scholar] [CrossRef]

- Hickey, S.; Mohan, G. Participation—From Tyranny to Transformation? Exploring New Approaches to Participation in Development; Zed Books: London, UK, 2004. [Google Scholar]

- Fung, A. Varieties of participation in complex governance. Public Adm. Rev. 2006, 66 (Suppl. 1), 66–75. [Google Scholar] [CrossRef]

- Michels, A.; De Graaf, L. Examining citizen participation: Local participatory policy making and democracy. Local Gov. Stud. 2010, 36, 477–491. [Google Scholar] [CrossRef]

- Pateman, C. Participation and Democratic Theory; Cambridge University Press: Cambridge, UK, 1970. [Google Scholar]

- Knack, S. Social capital and the quality of government: Evidence from the states. Am. J. Political Sci. 2002, 46, 772–785. [Google Scholar] [CrossRef]

- Martin, S. Engaging with citizens and other stakeholders. In Public Management and Governance, 2nd ed.; Bovaird, T., Löffler, E., Eds.; Roudledge: London, UK, 2009; pp. 279–296. [Google Scholar]

- Bovens, M. Analysing and assessing accountability: A conceptual framework1. Eur. Law J. 2007, 13, 447–468. [Google Scholar] [CrossRef]

- Johnson, N. Defining Accountability. Public Adm. Bull. 1974, 17, 3–13. [Google Scholar]

- Stewart, J.D. The role of information in public accountability. In Issues in Public Sector Accounting; Hopwood, A., Tomkins, C., Eds.; Philip Allan: London, UK, 1984; pp. 13–34. [Google Scholar]

- Glynn, J. Public Sector Financial Control and Accountability; Blackwell: Oxford, UK, 1987. [Google Scholar]

- Governmental Accounting Standards Board (GASB). Concepts Statement No. 1, Objectives of Financial Reporting; GASB: Norwalk, CA, USA, 1987.

- Brusca, M. The usefulness of financial reporting in Spanish local governments. Financ. Account. Manag. 1997, 13, 17–34. [Google Scholar]

- Pina, V. Principios de análisis contable en la Administración Pública. Span. J. Financ. Account. 1994, 24, 379–432. [Google Scholar]

- Nardo, M.; Saisana, M.; Saltelli, A.; Tarantola, S.; Hoffman, A.; Giovannini, E. Handbook on Constructing Composite Indicators: Methodology and User Guide; OECD Statistics Working Paper Series; OECD: Paris, France, 2005. [Google Scholar]

- Melyn, W.; Moesen, W. Towards a Synthetic Indicator of Macroeconomic Performance: Unequal Weighting When Limited Information Is Available; Public Economics Research Paper 17; CES, KU Leuven: Leuven, Belgium, 1991. [Google Scholar]

- Charnes, A.; Cooper, W.W.; Rhodes, E. Measuring the Efficiency of Decision Making Units. Eur. J. Oper. Res. 1978, 2, 429–444. [Google Scholar] [CrossRef]

- Mariano, E.B.; Sobreiro, V.A.; Rebelatto, D.A. Human development and Data Envelopment Analysis: A structured literature review. Omega 2015, 54, 33–49. [Google Scholar] [CrossRef]

- Sharpe, A.; Andrews, B. An Assessment of Weighting Methodologies for Composite Indicators: The Case of the Index of Economic Well-Being; Centre for the Study of Living Standards (CLS) research report No. 2012-10; CLS: Ottawa, ON, Canada, 2012. [Google Scholar]

- Vidoli, F.; Mazziotta, C. Robust weighted composite indicators by means of frontier methods with an application to European infrastructure endowment. Stat. Appl. Ital. J. Appl. Stat. 2011, 23, 259–282. [Google Scholar]

- Cherchye, L.; Moesen, W.; Puyenbroeck, T. Legitimately diverse, yet comparable: On synthesizing social inclusion performance in the EU. J. Common Mark. Stud. 2004, 42, 919–955. [Google Scholar] [CrossRef]

- Cherchye, L.; Moesen, W.; Rogge, N.; Puyenbroeck, T. An introduction to benefit of the doubt composite indicators. Soc. Indic. Res. 2007, 82, 111–145. [Google Scholar] [CrossRef]

- Wong, Y.-H.B.; Beasley, J.E. Restricting weight flexibility in Data Envelopment Analysis. J. Oper. Res. Soc. 1990, 41, 829–835. [Google Scholar] [CrossRef]

- Tiebout, C.M. A pure theory of local expenditures. J. Political Econ. 1956, 64, 416–424. [Google Scholar] [CrossRef]

Figure 1.

Distribution of the average Quality of Life (QoL) in the Spanish regions in 2011.

{kind=link}

Table 1.

Descriptive statistics.

| Average | Min | Max | SD | |

|---|---|---|---|---|

| QoL | 0.773 | 0.385 | 1.0 | 0.08 |

| Transparency | 70.91 | 15 | 100 | 24.5 |

| Participation | 0.803 | 0.576 | 1.0 | 0.09 |

| Accountability (Cash Surplus) | 0.585 | 0.032 | 1.0 | 0.11 |

| Accountability (Debt per Capita) | 0.211 | 0.0 | 1.0 | 0.13 |

| Pop. Density | 1790.2 | 25.88 | 21,757.5 | 2930.2 |

| Pop. Age | 39.5 | 33.2 | 47.7 | 2.61 |

| Pop. Growth | 0.237 | −0.111 | 1.16 | 0.22 |

Table 2.

Regression results (dependent variable QoL).

| Coeff. | t-Value | Coeff. | t-Value | Coeff. | t-Value | |

|---|---|---|---|---|---|---|

| Constant | 0.301 | 1.74 * | 0.278 | 2.18 ** | 0.259 | 3.16 *** |

| Transparency | −0.0003 | −1.05 | 0.0002 | 0.63 | - | - |

| Participation | 0.365 | 3.09 *** | 0.289 | 3.93 *** | 0.161 | 3.76 *** |

| Accountability (Cash Surplus) | 0.157 | 2.66 *** | 0.189 | 2.92 *** | 0.059 | 1.82 * |

| Accountability (Debt PC) | 0.055 | 1.07 | 0.024 | 0.47 | 0.042 | 1.02 |

| Pop. Density | −0.00005 | −2.37 ** | −0.00005 | −2.38 ** | −0.000005 | −0.34 |

| Pop. Age | 0.002 | 0.60 | 0.005 | 1.62 | 0.009 | 5.07 *** |

| Pop. Growth | 0.024 | 0.56 | −0.061 | −1.31 | −0.014 | −0.67 |

| Aragon | 0.134 | 3.70 *** | ||||

| Asturias | 0.022 | 0.51 | ||||

| Baleares | 0.060 | 1.09 | ||||

| Canarias | −0.005 | −0.19 | ||||

| Cantabria | 0.051 | 0.86 | ||||

| Castilla y Leon | 0.068 | 2.26 ** | ||||

| Castilla-Mancha | 0.029 | 0.89 | ||||

| Cataluña | 0.076 | 3.14 *** | ||||

| C. Valenciana | −0.048 | −1.83 * | ||||

| Extremadura | 0.041 | 0.95 | ||||

| Galicia | 0.075 | 2.30 ** | ||||

| Madrid | 0.028 | 1.16 | ||||

| Murcia | 0.012 | 0.36 | ||||

| Navarra | 0.150 | 2.53 ** | ||||

| País Vasco | 0.104 | 3.00 *** | ||||

| La Rioja | 0.108 | 1.83 * |

* Significance level 0.1; ** Significance level 0.05; *** Significance level 0.01.

Table 3.

Truncated regression results (dependent variable QoL).

| Coeff. | t-Value | Coeff. | t-Value | Coeff. | t-Value | |

|---|---|---|---|---|---|---|

| Constant | 0.339 | 2.25 ** | 0.274 | 2.27 ** | 0.252 | 3.09 *** |

| Transparency | −0.0002 | −0.94 | 0.0002 | 0.77 | - | - |

| Participation | 0.330 | 3.26 *** | 0.259 | 3.68 *** | 0.154 | 3.61 *** |

| Accountability (Cash Surplus) | 0.142 | 2.80 *** | 0.172 | 2.78 *** | 0.055 | 1.69 * |

| Accountability (Debt PC) | 0.056 | 1.28 | 0.022 | 0.46 | 0.041 | 1.27 |

| Pop. Density | −0.00005 | −2.65 *** | −0.00005 | −2.69 *** | −0.000005 | −0.42 |

| Pop. Age | 0.002 | 0.69 | 0.005 | 2.02 ** | 0.009 | 5.28 *** |

| Pop. Growth | 0.021 | 0.58 | −0.061 | −1.39 | −0.013 | −0.61 |

| Aragon | 0.147 | 4.18 *** | ||||

| Asturias | 0.024 | 0.64 | ||||

| Baleares | 0.058 | 1.24 | ||||

| Canarias | −0.004 | −0.19 | ||||

| Cantabria | 0.053 | 1.05 | ||||

| Castilla y Leon | 0.071 | 3.46 *** | ||||

| Castilla-Mancha | 0.036 | 1.31 | ||||

| Cataluña | 0.071 | 3.46 *** | ||||

| C. Valenciana | −0.043 | −1.97 ** | ||||

| Extremadura | 0.049 | 1.33 | ||||

| Galicia | 0.078 | 2.80 *** | ||||

| Madrid | 0.021 | 1.02 | ||||

| Murcia | 0.014 | 0.50 | ||||

| Navarra | 0.153 | 2.90 *** | ||||

| País Vasco | 0.104 | 3.50 *** | ||||

| La Rioja | 0.114 | 2.18 ** |

* Significance level 0.1; ** Significance level 0.05; *** Significance level 0.01.

© 2017 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Cárcaba, A.; González, E.; Ventura, J.; Arrondo, R. How Does Good Governance Relate to Quality of Life? Sustainability 2017, 9, 631. https://doi.org/10.3390/su9040631

AMA Style

Cárcaba A, González E, Ventura J, Arrondo R. How Does Good Governance Relate to Quality of Life? Sustainability. 2017; 9(4):631. https://doi.org/10.3390/su9040631

Chicago/Turabian StyleCárcaba, Ana, Eduardo González, Juan Ventura, and Rubén Arrondo. 2017. "How Does Good Governance Relate to Quality of Life?" Sustainability 9, no. 4: 631. https://doi.org/10.3390/su9040631

Note that from the first issue of 2016, this journal uses article numbers instead of page numbers. See further details here.