Risk Assessment of China’s Overseas Oil Refining Investment Using a Fuzzy-Grey Comprehensive Evaluation Method

1

School of Business Administration, China University of Petroleum (Beijing), Beijing 102249, China

2

Energy Systems Research Center, The University of Texas at Arlington, Arlington, TX 76019, USA

3

Department of Agricultural, Food and Resource Economics, Rutgers, The State University of New Jersey, New Brunswick, NJ 08901, USA

4

Chongqing CISDI Engineering Consulting Co., Ltd., Chongqing 400010, China

*

Author to whom correspondence should be addressed.

Sustainability 2017, 9(5), 696; https://doi.org/10.3390/su9050696

Submission received: 3 February 2017

/

Revised: 25 April 2017

/

Accepted: 25 April 2017

/

Published: 28 April 2017

(This article belongs to the Section Energy Sustainability)

Abstract

:Following the “going out” strategy, Chinese oil and gas companies have been widely involved in investing and operating business abroad to mitigate the increasing energy imbalance between supply and demand. Overseas oil investment, characterized by high risks and high returns, plays a significant role in ensuring energy security and strengthening global competitiveness in China. However, compared with overseas upstream projects, the downstream oil refining investment is still in the preliminary development stage, with limited experience for references, which further increases the risk surrounding such multibillion-dollar ventures. Hence, it is significant to assess the investment risks so as to help investors be fully aware of them and then make optimal investment decisions. To this end, this paper successfully identifies the main risk factors, including the local investment environment risk, technical risk, organization management risk, health, safety and environment (HSE) and social responsibility risk, and economic risk. Then, a qualitative-quantitative comprehensive risk evaluation method, combining the fuzzy mathematics and the grey system theory, is proposed and applied to analyze the investment risks of one Chinese overseas oil refining project as a case study. The assessment results are basically in accordance with the practical conditions, which validate the reliability and reasonability of the proposed risk assessment model in regard to the overseas oil refining project. The findings of this research provide the theoretical foundation and practical methodology of the risk analysis for future investment in oil refining areas.

1. Introduction

The refining industry, as one of the basic industries supporting social and economic developments, is growing rapidly in China [1]. In 1993, China turned into a net oil importer for the first time, which stimulated refining enterprises to expand their investment activities in global oil fields under the encouragement of policy, namely ’utilizing two kinds of oil and gas resources and markets—at home and abroad‘ [2,3,4,5]. With over 80 projects spreading in 42 countries all over the world, Chinese overseas oil investment has been constantly growing in recent years [6]. The decline of global oil price since 2014 has led to a dramatic development tendency of the entire refining industry, and this has boosted the enthusiasm of Chinese oil companies for investing in foreign oil refining projects [7]. The evolving globalized business strategy of Chinese oil enterprises and strong support from the Chinese government has contributed to the development of overseas projects [8]. Known as upstream investment, overseas oil refining not only inevitably eases the domestic oil imbalance between supply and demand but also ensures energy security and political stability [9]. However, the investment in downstream refining is relatively less and still in its infancy compared with upstream overseas oil projects. The risk involved in overseas refining investment is complex due to uncertainties stemming from unstable investment environment, laws and legislation, and other factors [10]. Generally, host countries that receive Chinses investment in oil refining are generally abundant in oil and Chinese oil companies own projects in the upstream sector, which are mainly in the Middle East, Africa, Central Asia and South Africa [11]. Many of them are rated as high-risk countries such as Sudan, Libya, Chad, Niger and Iraq, because there exist complex geopolitical milieus, an unstable political situation and large differences in the market development status and laws and regulations. These factors may deter the development of the overseas refining investment projects. Hence, the overseas risk for refining investment should be identified and accessed to take appropriate measures to decrease the odds of the risk, ensure the successful progressing of the project, and achieve the expectation of the investment.

On reviewing the short investment history of China’s overseas refining projects, there are limited experiences for reference in the research and practice. Only a few studies are related to overseas oil refining projects, and no effective universal evaluation system has been proposed [12,13,14]. The methods used in project risk assessment can be divided into three types: qualitative evaluation, quantitative evaluation, and qualitative–quantitative evaluation [15]. Among the frequently-used evaluation methods expert judgement is mainly used for the qualitative assessment; the Monte Carlo simulation method and decision tree analysis are used for the quantitative assessment; and the analytic hierarchy process-based method, fuzzy comprehensive evaluation, and grey evaluation are used for the qualitative–quantitative assessment. Each of them has its own advantages and disadvantages (see Table 1), and is applicable for different situations [16,17,18,19,20,21]. The comparison of strong and weak points between those evaluation methods have been discussed, which indicates that the comprehensive evaluation method is superior to a single quantitative or qualitative evaluation method [22].

Considering risk assessment methods for overseas oil refining investments, there are none publicly available. When it comes to the overseas investment risk assessment, the fuzzy comprehensive evaluation method and grey evaluation method are widely applied [23]. However, it has been proven that the single fuzzy math-based method can lead to information loss, while sole application of the grey system theory cannot fully take advantage of the fuzziness of the evaluation criteria [24,25]. Both shortcomings can cause differences between evaluation results and practical situations [26]. In addition, the characteristics of the overseas refining investments are known as complexity and uncertainty, which can result in fuzziness and greyness when the investment risk is evaluated [27]. For example, the index of refining investment risk evaluation is hard to quantize with limited specific data. The expert judgement cannot totally grip all risk information. Therefore, the integrated fuzzy-grey model is put forward in this paper to make advantage of both methods, which provides a feasible method for assessing overseas refining investments risk and compensates for the academic shortage of overseas refining risk analysis. The prominent advantages of the fuzzy-grey method not only takes full consideration of fuzziness and greyness of experts but also effectively offsets impacts of subjective factors and avoids the difficulty in weight allocation due to excessive factors. In addition, this method only requires a small quantity of samples, and is featured by simple calculation, which can be easily accepted and mastered.

In this study, we contribute to the existing literature on the risk assessment of China’s overseas oil refining investment in two aspects. First of all, we identify five types of risks for overseas oil refining investment and choose 20 indicators that fully consider the potential risk abroad and reduce the repetition and tedium of excessive indices; this contributes to making our results more realistic and reasonable, thereby giving policymakers a better understanding of risk for overseas oil refining investment. Second, risk assessment of overseas refining investments is characterized as a complex problem with multi-criteria and fuzzy multi-attributes. To the best of our knowledge, we are the first to build an integrated model based on the fuzzy theory and the grey system theory to assess the risk level, which can weaken effects of similar information and reduce the subjective effects coming from expert judgement. The proposed model provides a feasible and publicly available method for assessing the overseas oil refining investment risk and enriches the study on overseas oil refining investment risk analysis.

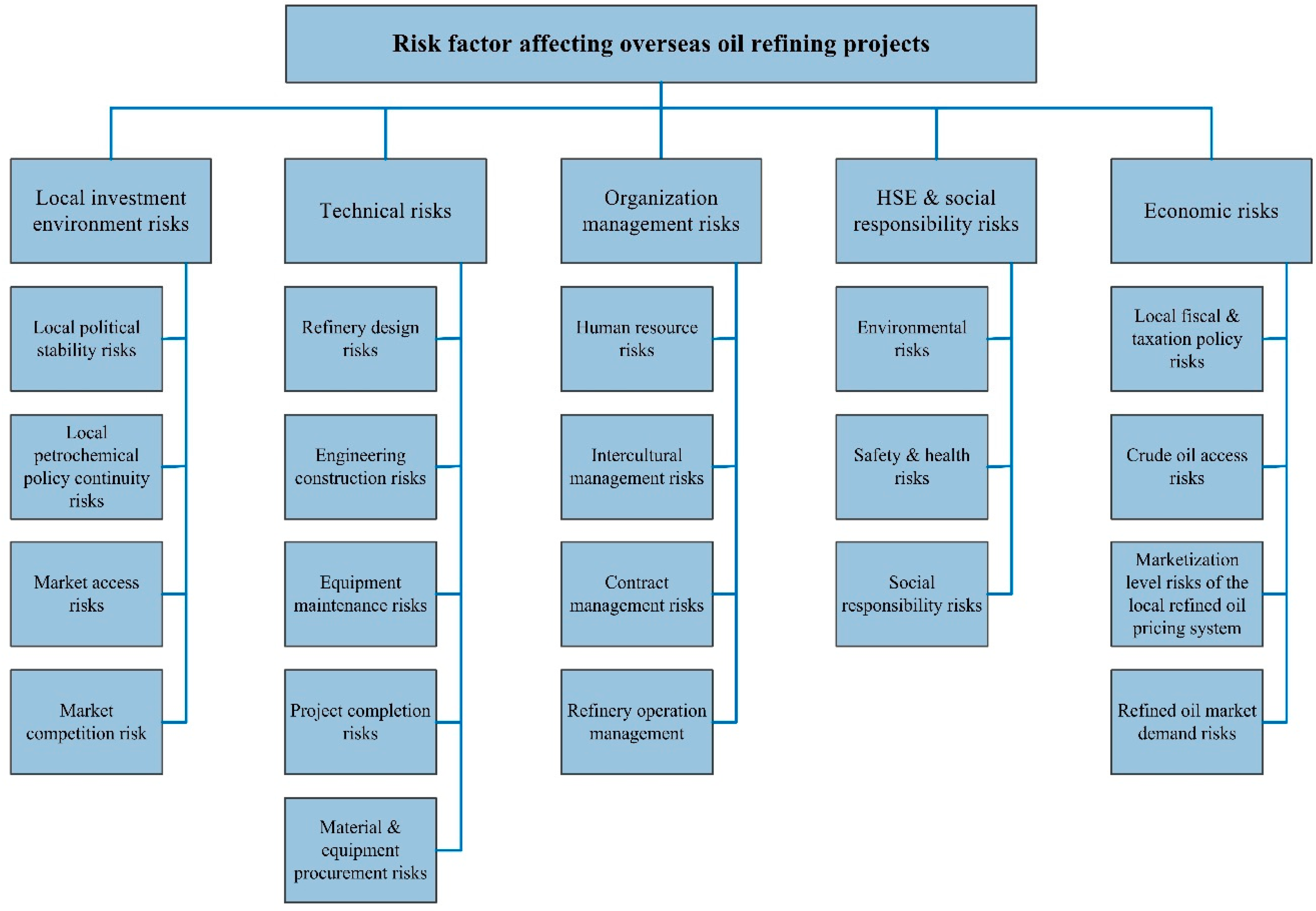

2. Risk Factor Analysis on Overseas Refining Investment

Based on this literature review, this paper views the investment risk of the overseas refining projects as the possible loss caused by uncertainty in the process of international investment. In this investment process, several uncertain factors impose tremendous risks, such as the complex geopolitical milieus, unstable political situation of local countries, and large differences in the market development status and laws and regulations. In addition, the risks are far higher than those of investment in domestic upstream projects [27]. In view of this, a risk factor analysis on overseas oil refining investment not only concerns successful project implementation, but also affects decision making for future investment [28]. This analysis lays the foundation for the build-up of the risk evaluation index system, as well as determining the risk performance. According to empirical results [1,2,5,6,7,8,9,10,11,12,13,14] and characteristics of overseas refining projects, we use the investment risk identification method as described by the Apex Oil Company [29] for reference, and identify five types of risks affecting the overseas refining projects, including the local investment environment risk, technical risk, organization management risk, health, safety and environment (HSE) and social responsibility risk, and economic risk. The specific categories are shown in Figure 1.

2.1. Local Investment Environment Risks

The local investment environment risk refers to the project risk factor that derives from the change of the situation of the foreign country when the oil company chooses to invest on oil refining projects in that country [10]. The overseas oil refining project is tightly related to the host country, and therefore it may encounter tremendous loss once the investment environment changes. The local investment environment risk mainly includes the local political stability risk, the petrochemical policy continuity risk, investment access risk, and market competition risk.

- Local political stability. This refers to the governing on the domestic political situation of the local government, which can be reflected in the regime change, war and civil strife. Local political instability imposes severe threats on overseas refining projects, which will lead to the high-risk level of the project from the initial stage of the investment [30].

- Policy continuity in the petrochemical industry. The invested overseas project has to strictly follow the local laws and regulations for the petroleum and petrochemical industries. The discontinuity in the petrochemical industry policy may cause damages to oil refining projects [31].

- Market access risk. This is defined as the permission of the host country for Chinese oil companies to participate in the local oil refining projects with few or no tariff barriers [32].

- Market competition risk. The market competition risk refers to the influence aroused by the competition from petroleum and petrochemical companies of other countries on the uncertainty of the project implementation. Fierce market competition indicates high risks [33].

2.2. Technical Risks

The technical risk refers to the risk that affects the overseas oil refining investment due to the technical uncertainty [34]. This kind of risks exist in many stages of the project, which mainly include the refinery design risk, material and equipment procurement risk, engineering construction risk, project completion risk, equipment maintenance risk, and safe production risk of the refinery plant.

- Refinery design risk. The successful commissioning of the overseas oil refining project greatly depends on the initial design of the refinery plant, which mainly consists of the selection of the refining process, determination of the production capacity, and arrangement of the main process unit and flare system [35].

- Engineering construction risk. This refers to the odds of engineering quality deviation from the expectation due to the limitation in the ground condition and subjective causes of the construction team during the building process of the refinery [36].

- Project completion risk. This risk refers to the uncertainty in the engineering construction stage and pilot production stage of the oil refinery project, and mainly occurs in the forms of engineering construction delay, cost overrun, and below-standard engineering quality [37].

- Equipment maintenance risk. The equipment may malfunction in its operation process, so that the equipment maintenance is needed to ensure the safe operation of the refinery after it runs for a period of time. The maintenance cost and shutdown loss constitute the equipment maintenance risk [38].

- Material and equipment procurement risk. This risk can be defined as the uncertainty deriving from inappropriate procurement budget that can cause the failure of engineering materials to meet the production requirement or exceed the budget. The procurement risk can increase the required investment of the project and prolong the duration of construction [39].

2.3. Organization Management Risks

The organization management risk refers to the risk that the overseas oil refining project cannot complete the expected goal due to defects in planning, organization, implementation and control rooted in the changes of the management system, management level, working system and so on [40]. Specifically, the organization management risk can be divided into the human resource risk, intercultural management risk, contract management risk, refinery operation and management risk, and coordination risk.

- Human resource management risk. The human resource is an important factor for the success of overseas projects. The comprehensive quality, professional proficiency, and education level of the project team member to a certain extent affects the overseas oil refining project [41].

- Intercultural management risk. When an oil company invests on an oil refining project in a foreign country, the project inevitably exists in a different cultural environment. The intercultural management risk means the probability of the project loss because of cultural misunderstandings and cultural conflicts [42].

- Contract management risk. The contract management risk refers to the probability of situations where the project suffers losses due to the omission of contract terms, ambiguous expression, inappropriate selection of contract types, or wrong choice of contracting forms during the entire process from the contract bidding of the oil refining project, through the contract conclusion, to the execution and termination [43].

- Refinery operation management risk. The refinery operation management risk describes the odds of the failure of the refinery operation to meet the expectation or the project loss due to the complexity and variability of the external environment and the limited cognitive and adaptive abilities of the administrator to the environment [44].

2.4. HSE and Social Responsibility Risks

The HSE and social responsibility risk is the risk of the project loss caused by influences from the health, safety and environment (HSE) as well as the social responsibility. This kind of risk exists in the stages of the project approval, design, construction and operation, and should be eliminated as completely as possible to ensure the evolution of the project from the project approval stage to the normal production stage [45].

- Environmental risk. The environmental risk mainly refers to the potential damage to surroundings. The oil refining company produces a mass of waste oil, industrial residues and waste water (known as the three wastes) and they tend to negatively impact the environment—causing vegetation deterioration, air pollution and geological alteration [46].

- The safety and health risk. The safety and health risk describes the probability of accidents such as loss of life and personal injuries, occupational diseases, property damage, workplace destruction during the construction and production of the refinery plant [47].

- The social responsibility risk. The social responsibility risk points to the odds of the refinery project damage due to the company’s lack of or inappropriate undertaking of social responsibilities and impacts on the sustainable development of the local society. The social responsibility risk often affects the reputation of the refinery and hence influences its sustainable development [48].

2.5. Economic Risks

The economic risk refers to the project financial loss due to the change in the economic factors related to the project and unpredictable events [49]. The occurrence of economic risk hampers the implementation schedule of the project, impacts its normal operation and even directly leads to the project failure. This kind of risks mainly roots in the change of local fiscal and taxation policies, the difficulty in crude oil access, crude oil price fluctuation, blockage of the refined oil distribution channel, marketization level of the refined oil pricing system and so on.

- Local fiscal and taxation policy risk. The potential change in the revenue of the refinery due to the variation in the local fiscal and taxation policy is defined as the local fiscal and taxation policy risk. This so-called change in the local fiscal and taxation policy includes the alteration of the interest rate, exchange rate and tax rate, which has effects on the income of the refinery [50].

- Crude oil supply risk. The crude oil access risk refers to the uncertainty originating from the impacted raw material supply for the refinery. Therefore, problems in the access to crude oil mean no raw materials for processing and failure to maintain production. The revenue of the refinery vanishes, which causes tremendous economic loss of the refinery [51].

- Refined oil market demand risk. This relates to the uncertainty in the local refined oil demand. The refined oil is associated with profits of the refinery. High local demand for the refined oil indicates good sales of the refined oil. On the contrary, weak market demand for the refined oil leads to slow distribution of the refined oil and dead product stock of the refinery [52].

- Marketization level risk of the local refined oil pricing system. The revenue of the overseas refinery is attributed to the sale of the refined oil, which greatly relies on the price of the refined oil. In terms of the overseas refining project, the host country often imposes limits on the refined oil price to protect the local stakeholder, which lowers the marketization level of the refined oil pricing system and leads to insecurity of the refinery revenue [53].

3. Methodology

3.1. Overarching Framework

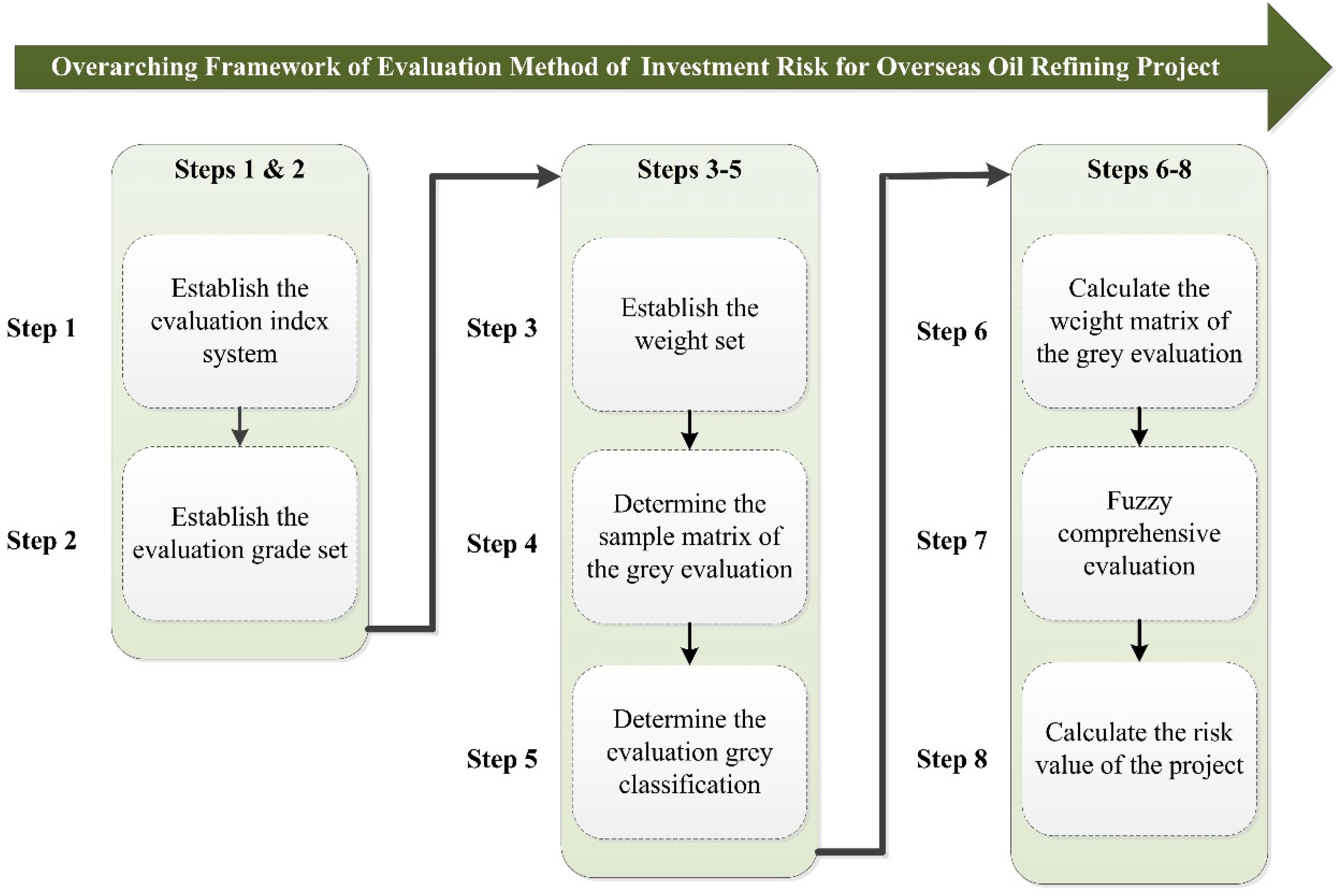

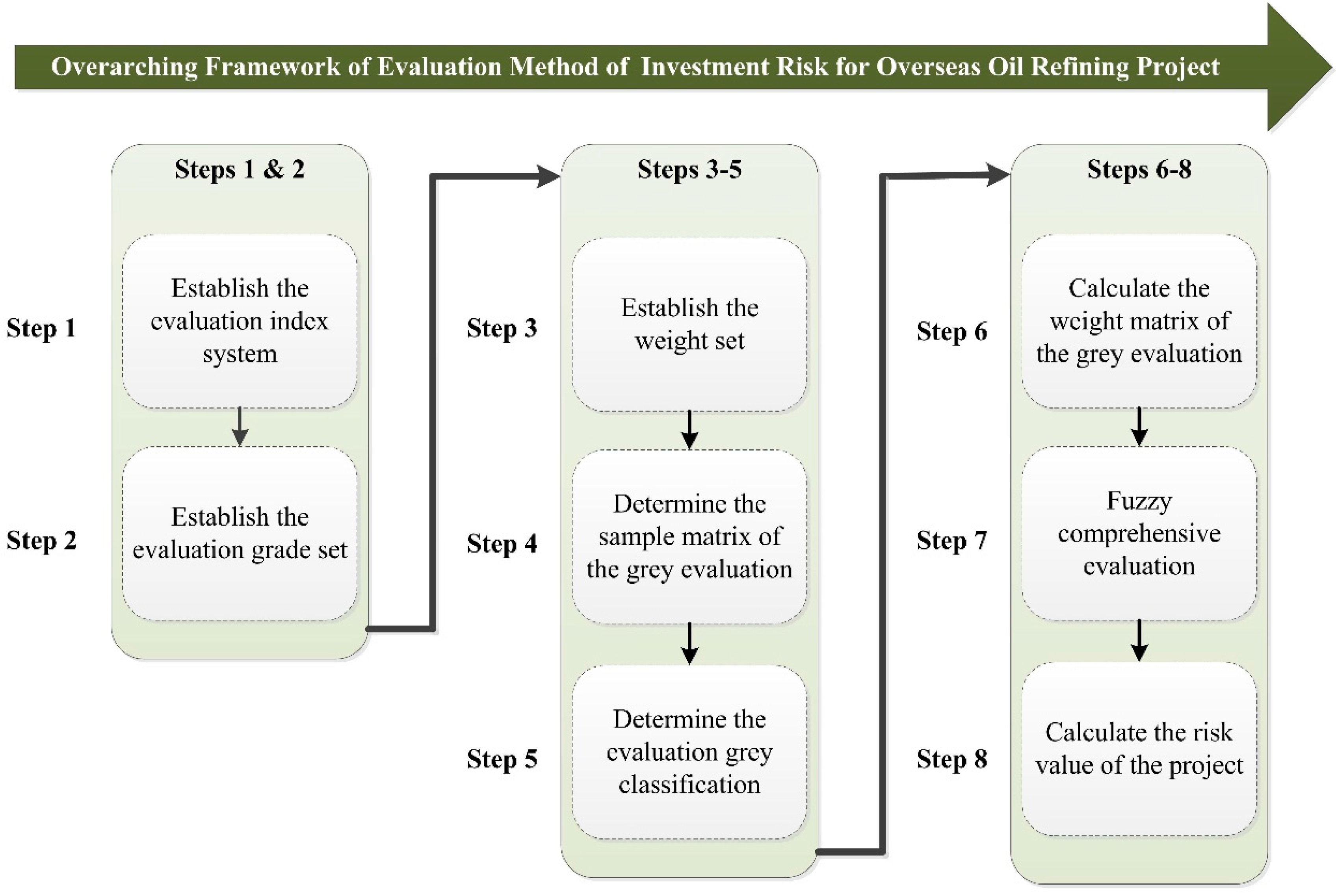

An appropriate evaluation method is required for scientific and reasonable assessment on the investment risk of the overseas oil refining project. Given that such projects involve multiple risks and the evaluation system possesses multiple evaluation indexes, most of which are hard to be determined through statistics, quantification of the evaluation index has to be completed with the help of the expert judgement [54]. Moreover, the rating of the risk, namely “high-risk” or “low-risk”, is fuzzy and greatly influenced by the subjective uncertainty, and thus accurate grading is hard to achieve [55]. For this reason, this paper combines the fuzzy comprehensive evaluation and the grey relational analysis to assess the investment risk of the overseas oil refining project [24,25]. As Figure 2 shows, an overarching framework of evaluation method of investment risk for overseas oil refining project is established.

3.2. Solution Method

The procedure of the investment risk assessment on the overseas oil refining project using the fuzzy-grey comprehensive evaluation method can be mainly concluded to the following eight steps [56]:

Step 1: Establish the evaluation index system. On the basis of the influential factor analysis in Sector 2, five primary indexes and 20 secondary indexes have been identified. The indexes and corresponding character symbols are shown in Table 2.

Step 2: Establish the evaluation grade set. The purpose of the fuzzy comprehensive evaluation is to determine the optimal evaluation result from the evaluation grade set, with all factors being comprehensively considered [57]. In this paper, the risk can be divided into five levels, namely low-risk, relatively low-risk, medium risk, relatively high-risk, and high-risk, with one, three, five, seven and nine points respectively assigned to each level of risks. It can also be described as .

Step 3: Establish the weight set. The evaluation index set should be developed, which is composed of some indexes for the criterion layer and factor layer. The analytical hierarchy process (AHP) is used to determine the weight distribution of the index system. In the AHP method, any of the two risk factors are compared to determine their relative importance, which is then used to calculate the weight of each risk factor in the whole evaluation system [58]. The weight set of the indicator in the criterion layer is defined as , mark . The weight set of the indicator in the factor layer is defined as , , where the value of j should be determined according to the quantity of the indicator in the factor layer of each criterion layer.

Step 4: Determine the sample matrix of the grey evaluation. It is assumed that the number of the experts is p, and each expert can give scores to the risk factor according to the scoring standard and his own experience. The grades that expert k gives to risk index is denoted as . The sample matrix for the grey evaluation can be determined on the basis of all the expert-based scoring results.

Step 5: Determine the evaluation grey classification. This step consists of calculating the weight matrix in grey leagues based on the grey system theory, which was pioneered by Deng et al. (1982) [25]. According to the risk grading standard in this paper, five grey classes are divided, respectively denoted as e = 1, 2, 3, 4 and 5 corresponding to the low-risk, relatively low-risk, medium-risk, relatively high-risk and high-risk. The linear whitenization weight function is adopted to describe the grey classification as below:

Grey class 1 (e = 1, low-risk): the grey number ◎ 1 ∈ [0,1,2], and the whitenization weight function is f1:

Grey class 2 (e = 2, relatively low-risk): the grey number ◎ 1 ∈ [0,3,6], and the whitenization weight function is f2:

Grey class 3 (e = 3, medium-risk): the grey number ◎ 1 ∈ [0,5,10], and the whitenization weight function is f3:

Grey class 4 (e = 4, relatively high-risk): the grey number ◎ 1 ∈ [0,7,14], and the whitenization weight function is f4:

Grey class 5 (e = 5, high-risk): the grey number ◎ 1 ∈ [0,9,∞], and the whitenization weight function is f5:

Step 6: Calculate the weight matrix of the grey evaluation. Using the values of the whitenization weight function and , the grey evaluation coefficient of index with regard to grey class e can be calculated as:

The total grey evaluation coefficient of index is:

Hence the experts’ grey evaluation weight of index in terms of grey class e can be defined as:

in the factor layer has a grey evaluation weight vector of . Then the grey evaluation weight matrix can be calculated through all the grey evaluation weight vectors of each index in the factor layer of each indicator in the criteria layer in the investment risk evaluation index system of overseas oil refining projects:

Step 7: Fuzzy comprehensive evaluation. The fuzzy evaluation model is adopted as the fuzzy arithmetic operator. Therefore, the risk assessment model can be expressed as:

The first-level fuzzy evaluation, namely the fuzzy comprehensive evaluation for factor i, can be described as:

Regarding the second-level fuzzy comprehensive evaluation, the evaluation result Mi of the first-level fuzzy comprehensive evaluation can be used as the single-element evaluation grade set to form the single-element evaluation matrix:

With the help of the matrix R and the weight set W, the second-level fuzzy comprehensive evaluation can be carried out as below:

Step 8: Risk value of the project can be determined on the basis of the evaluation grade set V:

4. Case Study

4.1. Background

The China National Petroleum Company (CNPC) of China, and the African country named C, have jointly developed a upstream-downstream integrated project. In terms of the downstream oil refining project, the CNPC invests US$60 million and holds 60% of the project shares, and the remaining 40% belongs to the government of the country C. The duration of the joint venture is 99 years, and the CNPC is responsible for the operation and management of the refinery. The designed crude oil processing capacity of this project is 2.5 million tons per year, which will be built in a two-stage schedule. The first-stage project, consisting of the refinery plant, power plant and petroleum product sales centre, delivers a capacity of one million tons per year, and annual production of 0.7 million tons of gasoline and diesel, 20,000 tons of kerosene, 25,000 tons of polypropylene, 60,000 tons of liquefied gas, and 40,000 tons of fuel oil. The refinery includes the production units, such as the atmospheric distillation, heavy oil catalytic cracking, catalytic reforming, hydrofining, gas fractionation, polypropylene, and petroleum product refining units, and the utility system. The crude oil for the refinery comes from the oil block H, owned by the subsidiary company of the CNPC in the country C. This refinery is the first oil refining project in country C, and the country depends on imported oil for all petroleum products. The build-up of this refinery can meet the domestic demand of the country for refined oil, and meanwhile allows for exports and boosts the development of the petroleum and petrochemical industries of the country. The design, construction, commissioning and operation of the refinery are all carried out by the CNPC, with all required materials and equipment first bought in China and then transported to the country C. In addition, all technical staff come from the CNPC.

4.2. Risk Assessment Results

(1) Weight distribution of evaluation indexes. In order to objectively decide the index significance of the proposed investment risk evaluation system of overseas oil refining projects, a questionnaire has been designed. The overseas oil refining market has long been monopolized by three big state-owned oil companies (SOCs), whose total market share exceeds 96% [3]; namely, the China National Petroleum Company (CNPC), China Petroleum and Chemical Corporation (Sinopec), and the China National Offshore Oil Corporation (CNOOC). Therefore, multiple experts of the China Petroleum Technology & Development Company, the Great Wall Drilling Company and the China National Oil & Gas Exploration & Development Company of the CNPC, the Sinopec Petroleum Exploration and Production Research Institute of the Sinopec, and the Research Institute of Economics and Technology of the CNOOC, who once participated overseas oil refining projects, have been surveyed in this present study. Moreover, experts were asked to grade the indexes with points from 1 to 5, and the average point of each index was taken as a reference for determining the evaluation index importance. In this paper, 100 copies of the questionnaires were issued, and 96 were returned (96%). However, a total of 91 useable surveys were produced as five questionnaires were invalid. Table 3 demonstrates the breakdown of the respondents in terms of gender, age, education and working years. The sample consists of 10 men (68%) and 6 women (32%). In total, 19% of respondents were aged 30 or under, 25% were aged 30–40 years old and the remaining 56% were aged 40 or over. In terms of the respondents’ education, the respondents tended to be well educated (87% of them have a graduate or doctor degree). The working years of almost 76% of respondents are more than 5 years. Thus, it can ensure the authority and accuracy of the index scoring results.

Furthermore, the results of the survey are provided in Table 4.

On the basis of the calculation results of the survey statistics and AHP approach, the weight coefficients of the evaluation index system are displayed in Table 5.

(2) Determination of the grey evaluation sample matrix. The evaluation sample matrix D was obtained by consulting ten experts that are familiar with this project.

(3) Calculation of the grey evaluation weight matrix. On the basis the of expert-based scoring and whitenization weight functions mentioned above, the grey evaluation coefficient of each risk index can be calculated. The calculation process of the index is shown below as an example:

Hence, the total evaluation coefficient of the index concerning each grey class can be calculated as:

The evaluation weights of the index in regards to each evaluation grey class are respectively:

Accordingly, the grey evaluation weight vector r11 of can be expressed as:

Similarly, the weight vectors of the rest factors belonging to the superior criterion index A, namely , , , , , …, and can all be calculated. Then, the grey evaluation weight matrix of the factors belonging to each criterion-layer index concerning each evaluation grey class, (i = A, B, C, D and E) can be constituted:

(4) Fuzzy comprehensive evaluation. The fuzzy comprehensive evaluation on the risk index of this project can be conducted using the shown formula.

MA = WA × RA = (0, 0.1347, 0.2823, 0.3260, 0.2570)

MB = WB × RB = (0, 0.2109, 0.3309, 0.2581, 0.2005)

MC = WC × RC = (0, 0.2258, 0.3060, 0.2621, 0.2061)

MD = WD × RD = (0, 0.1458, 0.3158, 0.3028, 0.2355)

ME = WE × RE = (0, 0.1057, 0.2972, 0.3265, 0.2707)

The evaluation matrix R for the secondary fuzzy comprehensive evaluation can be obtained with the help of :

The result of the comprehensive risk assessment of this project, M, is shown below:

M = W × R = (0, 0.1521, 0.3025, 0.3038, 0.2416)

The comprehensive assessment of the general risk of the project is:

That of the local investment environment risk is:

That of the technical risk is:

That of the organization management risk is:

That of the HSE and social responsibility risk is:

That of the economic risk is:

Therefore, the risk priority of the project is:

GE > GA > GD > GB > GC.

In order to better assess the results of the investment risk level, a scientific and effective division standard is developed (see Section 3.2). From 1 to 9, the risk value gradually increases. For instance, the overseas oil refining project marked with 1 represents low risk, and that with 9 means high risk. Therefore, the results of risk evaluation and ranking, 7 > GE > GA > G > GD > GB > GC > 5, indicate that the CNPC’s oil refining project in the country C belongs to the medium- to high-risk project in either the overall risk or five types of risks. Given the long-term characteristics of the project (99 years, also see Section 4.1), the decision-making of this project should maintain a clear sense of the dilemma and leave enough room in formulating policies to gradually reduce these risks. Moreover, the risk ranking also shows that the local investment environment risk and economic risk are the highest, and accordingly extra attention should be paid to monitor such risks. In fact, CNPC signed a refinery joint venture agreement with country C in September 2007, and the refining investment project was constructed in October 2009. At the end of June 2011, the first phase of the project was completed. During the construction process, investors were faced with difficulties such as poor construction conditions, lack of local skilled workers, serious transportation issues, and harsh weather conditions. After the construction was completed, the production was required to halt due to a disagreement on oil price with country C. In addition, refinery workers went on strikes for better conditions at one point. The project experience shows that the risk level of economic and local environment is the highest, which is in accordance with our results. In summary, compared with the annual reports of this project in the CNPC [59], our assessment results are basically in accordance with practical conditions, which proves the effectiveness of the proposed index system and evaluation model as well as consistency with reality.

5. Conclusions

The globalization of the oil refining business has become a necessity, as the strength of China’s oil company is continuously growing. Risks exist in the entire lifecycle of overseas investment in the oil refining projects, and are also affected by complex uncertainties. Quantitative risk level evaluation can not only help the investor understand the risk level and make the optimal investment decision, but also to some extent ensure the successful progress of the project. The purpose of this paper aims to establish a risk assessment model as well as guide the overseas investment for oil enterprises. Some main conclusions can be drawn, as follows.

(1) Risks affecting overseas oil refining investment can be divided into five categories: local investment environment risk, technical risk, organization management risk, HSE and social responsibility risk, and economic risk. Each category is identified by specific risk indicators including 20 second-grade indices. Based on the results of expert investigation and questionnaire, local investment environment risk and economic risk are considered as key factors affect the overseas refining investment.

(2) The risk level in the case of CPNC’s overseas oil refining investment project in the country C is relatively high. By employing the proposed fuzzy-grey comprehensive evaluation model, the overall score of the project is 6.2712, which falls in the scope of medium to high risk level. Specifically, the economic risk and the local investment environment risk are the two categories with highest scores (6.5186 and 6.4177), which should be fully realized and dealt with by investors in the future; the HSE and social responsibility risk takes third place (6.2549); the influence of the technical risk and the organization management risk is the lowest. The results are in accordance with reality, and prove the effectiveness of the proposed index system and risk assessment model in terms of overseas refining investments.

(3) Compared with typical risk assessment methods, the fuzzy-grey method effectively incorporates the benefits of fuzzy evaluation and grey evaluation methods and has been proven to be a useful risk assessment tool for overseas refining investment. It takes full consideration of the fuzziness and greyness of expert judgements and requires a small quantity of samples. It features simple calculations, which can be easily accepted and mastered.

Despite these advances in knowledge of risk factor identification, some important indicators, such as services [60,61], and subsidies [62], are not considered in this study. Therefore, it would be significant to add another factor to our evaluation model to explore the investment risk level of the Chinese oil companies for overseas oil refining projects in future research.

Acknowledgments

This paper is financially supported by the National Natural Science Foundation of China (No. 71273277) and the Key Projects of the Philosophy and Social Science Researches of Ministry of Education of China (No. 11JZD048). In addition, the authors thank the editors and the anonymous reviewers of this manuscript for their elaborate work.

Author Contributions

All of the authors have co-operated in the preparation of this work. Hui Li wrote the manuscript. Kangyin Dong and Renjin Sun made contributions to the design of the article. Xiaoyue Guo collected and analysed the data. A final review, including final manuscript revisions, was performed by Hongdian Jiang and Yiqiao Fan.

Conflicts of Interest

The authors declare no conflict of interest.

References

- Moro, L.F.L. Process technology in the petroleum refining industry—Current situation and future trends. Comput. Chem. Eng. 2003, 27, 1303–1305. [Google Scholar] [CrossRef]

- Su, M.; Zhang, M.; Lu, W.; Chang, X.; Chen, B.; Liu, G.; Hao, Y.; Zhang, Y. Ena-based evaluation of energy supply security: Comparison between the chinese crude oil and natural gas supply systems. Renew. Sustain. Energy Rev. 2017, 72, 888–899. [Google Scholar] [CrossRef]

- Dong, K.; Sun, R.; Li, H.; Zheng, S.; Yuan, B.; Chung, K.H. Weaker demand outlook, heightened regulations create uncertainty for chinese refiners. Oil Gas J. 2016, 114, 63–67. [Google Scholar]

- Dong, K.-Y.; Sun, R.-J.; Li, H.; Jiang, H.-D. A review of china’s energy consumption structure and outlook based on a long-range energy alternatives modeling tool. Petroleum Sci. 2016, 14, 1–14. [Google Scholar] [CrossRef]

- Fang, W.L.; Y.L.; An, H.Z. Views on global cooperation in oil-gas resource. Resour. Ind. 2011, 13, 43–46. (In Chinese) [Google Scholar]

- Len, C. China’s 21st century maritime silk road initiative, energy security and sloc access. Marit. Aff. 2015, 11, 1–18. [Google Scholar] [CrossRef]

- Mckinsey’s Energy Insights. Impact of Low Crude Prices on Refining. 2015. Available online: https://www.mckinseyenergyinsights.com/insights/impact-of-low-crude-prices-on-refining.aspx (accessed on 25 April 2017).

- Hong, E.; Sun, L. Dynamics of internationalization and outward investment: Chinese corporations’ strategies. China Q. 2006, 187, 610–634. [Google Scholar] [CrossRef]

- Houser, T. The roots of chinese oil investment abroad. Asia Policy 2008, 5, 141–166. [Google Scholar] [CrossRef]

- Li, H.; Dong, K.; Sun, R.; Yu, J.; Xu, J. Sustainability Assessment of Refining Enterprises Using a DEA-Based Model. Sustainability 2017, 9, 620. [Google Scholar] [CrossRef]

- Iea. Overseas Investments by Chinese National Oil Companies: Assessing the Drivers and Impacts. 2011. Available online: https://www.iea.org/publications/freepublications/publication/overseas_china.pdf (accessed on 25 April 2017).

- Huang, Y.Z. How to avoid the technical risk of overseas refining projects. Int. Petroleum Econ. 1999, 7, 37–41. (In Chinese) [Google Scholar]

- Milani, R.V.; Lavie, C.J. Another step forward in refining risk stratification. J. Am. Coll. Cardiol. 2011, 58, 464–466. [Google Scholar] [CrossRef] [PubMed]

- Guo, P.G.H.; Feng, W.K. Reflections on participation in international refining project cooperation. Econ. Anal. China’s Petroleum Chem. Ind. 2008, 10, 52–54. [Google Scholar]

- Felder, F.A. Risk modeling, assessment, and management. IIE Trans. 2005, 37, 586–587. [Google Scholar]

- Hughes, R.T. Expert judgement as an estimating method. Inf. Softw. Technol. 1996, 38, 67–75. [Google Scholar] [CrossRef]

- Li, P.; Chen, B.; Li, Z.; Zheng, X.; Wu, H.; Jing, L.; Lee, K. A monte carlo simulation based two-stage adaptive resonance theory mapping approach for offshore oil spill vulnerability index classification. Mar. Pollut. Bull. 2014, 86, 434–442. [Google Scholar] [CrossRef] [PubMed]

- Abbasitabar, F.; Zare-Shahabadi, V. In silico prediction of toxicity of phenols to tetrahymena pyriformis by using genetic algorithm and decision tree-based modeling approach. Chemosphere 2017, 172, 249–259. [Google Scholar] [CrossRef] [PubMed]

- Kokangül, A.; Polat, U.; Dağsuyu, C. A new approximation for risk assessment using the ahp and fine kinney methodologies. Saf. Sci. 2017, 91, 24–32. [Google Scholar] [CrossRef]

- Yu, C. Quantitative risk analysis method of information security-combining fuzzy comprehensive analysis with information entropy. BioTechnology 2014, 10, 12753–12761. [Google Scholar]

- Liu, H.-C.; Liu, L.; Liu, N. Risk evaluation approaches in failure mode and effects analysis: A literature review. Expert Syst. Appl. 2013, 40, 828–838. [Google Scholar] [CrossRef]

- Li, H.; Sun, R.; Lee, W.-J.; Dong, K.; Guo, R. Assessing risk in chinese shale gas investments abroad: Modelling and policy recommendations. Sustainability 2016, 8, 708. [Google Scholar] [CrossRef]

- Hsu, H.-M.; Chen, C.-T. Fuzzy credibility relation method for multiple criteria decision-making problems. Inf. Sci. 1997, 96, 79–91. [Google Scholar]

- Billaudel, P.; Devillez, A.; Lecolier, G.V. Performance evaluation of fuzzy classification methods designed for real time application. Int. J. Approx. Reason. 1999, 20, 1–20. [Google Scholar] [CrossRef]

- Julong, D. Introduction to grey system theory. J. Grey Syst. 1989, 1, 1–24. [Google Scholar]

- Guo, P.; Shi, P.-G. Research on fuzzy-grey comprehensive evaluation method of project risk. J. Xi’an Univ. Technol. 2005, 21, 106–109. [Google Scholar]

- Chen, Q. The principle and strategy for overseas refining and petrochemical projects development at the time of global recession. Petroleum Petrochem. Today 2011, 3, 2–6. [Google Scholar]

- Ramos, S.B.; Veiga, H. Risk factors in oil and gas industry returns: International evidence. Energy Econ. 2011, 33, 525–542. [Google Scholar] [CrossRef]

- Apex Oil Company. Available online: http://apexoil.com/ (accessed on 25 April 2017).

- Osabutey, D.; Obro-Adibo, G.; Agbodohu, W.; Kumi, P. Analysis of risk management practices in the oil and gas industry in ghana. Case study of tema oil refinery (tor). Eur. J. Bus. Manag. 2013, 5, 139–150. [Google Scholar]

- Busse, M.; Hefeker, C. Political risk, institutions and foreign direct investment. Eur. J. Political Econ. 2007, 23, 397–415. [Google Scholar] [CrossRef]

- Fia Maket Access Working Group, Market Access Risk Management Recommendations. 2010. Available online: https://secure.fia.org/downloads/market_access-6.pdf (accessed on 25 April 2017).

- Laksmana, I.; Yang, Y.-W. Product market competition and corporate investment decisions. Rev. Acc. Financ. 2015, 14, 128–148. [Google Scholar] [CrossRef]

- Zhang, B.S.; Wang, Q.; Wang, Y.J. Model of risk-benefit co-analysis on oversea oil and gas projects and its application. Syst. Eng. Theory Pract. 2012, 32, 246–256. (In Chinese) [Google Scholar]

- Markowski, A.S. Quantitative risk assessment improves refinery safety. Oil Gas J. 2002, 100, 56–63. [Google Scholar]

- Iqbal, S.; Choudhry, R.M.; Holschemacher, K.; Ali, A.; Tamošaitienė, J. Risk management in construction projects. Technol. Econ. Dev. Econ. 2015, 21, 65–78. [Google Scholar] [CrossRef]

- Kokkaew, N.; Wipulanusat, W. Completion delay risk management: A dynamic risk insurance approach. KSCE J. Civ. Eng. 2014, 18, 1599–1608. [Google Scholar] [CrossRef]

- Bigliani, R. Reducing Risk in Oil and Gas Operations; IDC Energy Insights: Framingham, MA, USA, 2013. [Google Scholar]

- Anvaripour, B.; Sa’idi, E.; Nabhani, N.; Jaderi, F. Risk analysis of crude distillation unit’s assets in abadan oil refinery using risk based maintenance. TJEAS J. 2013, 3, 1888–1892. [Google Scholar]

- Muralidhar, K. Enterprise risk management in the middle east oil industry: An empirical investigation across gcc countries. Int. J. Energy Sect. Manag. 2010, 4, 59–86. [Google Scholar] [CrossRef]

- Stephens, J.C.; Wilson, E.J.; Peterson, T.R. Socio-political evaluation of energy deployment (speed): An integrated research framework analyzing energy technology deployment. Technol. Forecast. Soc. Chang. 2008, 75, 1224–1246. [Google Scholar] [CrossRef]

- Li, S. Risk management for overseas development projects. Int. Bus. Res. 2009, 2, 193. [Google Scholar] [CrossRef]

- Pongsakdi, A.; Rangsunvigit, P.; Siemanond, K.; Bagajewicz, M.J. Financial risk management in the planning of refinery operations. Int. J. Prod. Econ. 2006, 103, 64–86. [Google Scholar] [CrossRef]

- Ribas, G.P.; Leiras, A.; Hamacher, S. Operational planning of oil refineries under uncertainty special issue: Applied stochastic optimization. IMA J. Manag. Math. 2012, 23, 397–412. [Google Scholar] [CrossRef]

- Spence, D.B. Corporate social responsibility in the oil and gas industry: The importance of reputational risk. Chic.-Kent Law Rev. 2011, 86, 59. [Google Scholar]

- Rezaian, S.; Jozi, S.A. Health-safety and environmental risk assessment of refineries using of multi criteria decision making method. APCBEE Procedia 2012, 3, 235–238. [Google Scholar] [CrossRef]

- Chauhan, N. Safety and Health Management System in Oil and Gas Industry; Wipro Technologies: Bangalore, India, 2013. [Google Scholar]

- Ledwidge, J. Corporate social responsibility: The risks and opportunities for hr: Integrating human and social values into the strategic and operational fabric. Hum. Resour. Manag. Int. Dig. 2007, 15, 27–30. [Google Scholar] [CrossRef]

- Paté-Cornell, M.E. Fire risks in oil refineries: Economic analysis of camera monitoring. Risk Anal. 1985, 5, 277–288. [Google Scholar] [CrossRef]

- Nakhle, C. Petroleum Taxation: Sharing the Oil Wealth: A Study of Petroleum Taxation Yesterday, Today and Tomorrow; Routledge: Oxford, UK, 2008. [Google Scholar]

- Nnadili, B.N. Supply and Demand Planning for Crude Oil Procurement in Refineries. Master’s Thesis, Massachusetts Institute of Technology, Cambridge, MA, USA, 2006. [Google Scholar]

- Zhang, G.; Zou, P.X. Fuzzy analytical hierarchy process risk assessment approach for joint venture construction projects in china. J. Constr. Eng. Manag. 2007, 133, 771–779. [Google Scholar] [CrossRef]

- Song, C.; Li, C. Relationship between chinese and international crude oil prices: A vec-tarch approach. Math. Probl. Eng. 2015, 2015, 842406. [Google Scholar] [CrossRef]

- Baker, E.; Keisler, J.M. Cellulosic biofuels: Expert views on prospects for advancement. Energy 2011, 36, 595–605. [Google Scholar] [CrossRef]

- Liu, H.-C.; Liu, L.; Bian, Q.-H.; Lin, Q.-L.; Dong, N.; Xu, P.-C. Failure mode and effects analysis using fuzzy evidential reasoning approach and grey theory. Expert Syst. Appl. 2011, 38, 4403–4415. [Google Scholar] [CrossRef]

- Bu, G.; Zhang, Y. Grey fuzzy comprehensive evaluation based on the theory of grey fuzzy relation. Syst. Eng. Theory Pract. 2002, 4, 141–144. [Google Scholar]

- Lee, M.-C. Information security risk analysis methods and research trends: Ahp and fuzzy comprehensive method. Int. J. Comput. Sci. Inf. Technol. 2014, 6, 29. [Google Scholar]

- Vargas, L.G. An overview of the analytic hierarchy process and its applications. Eur J. Oper. Res. 1990, 48, 2–8. [Google Scholar] [CrossRef]

- Cnpc Annual Report. Available online: http://www.cnpc.com.cn/en/ar2015/annualreport_list.shtml (accessed on 25 April 2017).

- Mas-Verdu, F.; Ribeiro Soriano, D.; Roig Dobon, S. Regional development and innovation: The role of services. Serv. Ind. J. 2010, 30, 633–641. [Google Scholar] [CrossRef]

- Dobón, S.R.; Soriano, D.R. Exploring alternative approaches in service industries: The role of entrepreneurship. Serv. Ind. J. 2008, 28, 877–882. [Google Scholar] [CrossRef]

- Soriano, D.R.; Peris-Ortiz, M. Subsidizing technology: How to succeed. J. Bus. Res. 2011, 64, 1224–1228. [Google Scholar] [CrossRef]

Figure 1.

Risk factor analysis of overseas oil refining investment. HSE: health, safety and environment.

Figure 1.

Risk factor analysis of overseas oil refining investment. HSE: health, safety and environment.

Figure 2.

Research framework of evaluation method in this study.

{kind=link}

{kind=link}

Table 1.

Advantages and disadvantages of typical risk assessment methods.

| Methods | Examples | Advantages | Disadvantages |

|---|---|---|---|

| Qualitative method |

|

|

|

| Quantitative method |

|

|

|

| Comprehensive method |

|

|

|

Source: Li et al. [22].

Table 2.

Investment risk evaluation index system of overseas oil refining projects.

| Goals | Criteria | Factors |

|---|---|---|

| Investment risks of overseas oil refining projects, G | Local investment environment risks, A | Local political stability risks, A1 |

| Local petrochemical policy continuity risks, A2 | ||

| Market access risks, A3 | ||

| Market competition risk, A4 | ||

| Technical risks, B | Refinery design risks, B1 | |

| Engineering construction risks, B2 | ||

| Equipment maintenance risks, B3 | ||

| Project completion risks, B4 | ||

| Material and equipment procurement risks, B5 | ||

| Organization management risks, C | Human resource risks, C1 | |

| Intercultural management risks, C2 | ||

| Contract management risks, C3 | ||

| Refinery operation management, C4 | ||

| HSE and social responsibility risks, D | Environmental risks, D1 | |

| Safety and health risks, D2 | ||

| Social responsibility risks, D3 | ||

| Economic risks, E | Local fiscal and taxation policy risks, E1 | |

| Crude oil access risks, E2 | ||

| Marketization level risks of the local refined oil pricing system, E3 | ||

| Refined oil market demand risks, E4 |

Table 3.

Demographic characteristics of the respondents (N = 91).

| Participant Characteristics | Frequency | % |

|---|---|---|

| Gender | ||

| Males | 62 | 68 |

| Females | 29 | 32 |

| Age | ||

| <30 | 17 | 19 |

| 30–40 | 23 | 25 |

| >40 | 51 | 56 |

| Education | ||

| Bachelor’s degree | 12 | 13 |

| Graduate degree | 48 | 53 |

| Doctorate degree | 31 | 34 |

| Working years | ||

| <5 | 22 | 24 |

| 5–10 | 29 | 32 |

| >10 | 40 | 44 |

Table 4.

Index scoring statistics.

| Index No. | Risk Index | Total Points | Average Points |

|---|---|---|---|

| A | Local investment environment risks | 387 | 4.2527 |

| B | Technical risks | 283 | 3.1099 |

| C | Organization management risks | 268 | 2.9451 |

| D | HSE and social responsibility risks | 341 | 3.7473 |

| E | Economic risks | 378 | 4.1538 |

| A1 | Local political stability risks | 391 | 4.2967 |

| A2 | Local petrochemical policy continuity risks | 336 | 3.6923 |

| A3 | Market access risks | 245 | 2.6923 |

| A4 | Market competition risk | 267 | 2.9341 |

| B1 | Refinery design risks | 210 | 2.3077 |

| B2 | Engineering construction risks | 210 | 2.3077 |

| B3 | Equipment maintenance risks | 243 | 2.6703 |

| B4 | Project completion risks | 191 | 2.0989 |

| B5 | Material and equipment procurement risks | 306 | 3.3626 |

| C1 | Human resource risks | 275 | 3.0220 |

| C2 | Intercultural management risks | 283 | 3.1099 |

| C3 | Contract management risks | 275 | 3.0220 |

| C4 | Refinery operation management | 257 | 2.8242 |

| D1 | Environmental risks | 312 | 3.4286 |

| D2 | Safety and health risks | 296 | 3.2527 |

| D3 | Social responsibility risks | 276 | 3.0330 |

| E1 | Local fiscal and taxation policy risks | 330 | 3.6264 |

| E2 | Crude oil access risks | 290 | 3.1868 |

| E3 | Marketization level risks of the local refined oil pricing system | 334 | 3.6703 |

| E4 | Refined oil market demand risks | 284 | 3.1209 |

Table 5.

The weight coefficients of the risk evaluation index system of overseas refinery investment.

Table 5.

The weight coefficients of the risk evaluation index system of overseas refinery investment.

| Criteria | Weights | Factors | Weights |

|---|---|---|---|

| Local investment environment risks, A | 0.2843 | Local political stability risks, A1 | 0.3967 |

| Local petrochemical policy continuity risks, A2 | 0.2721 | ||

| Market access risks, A3 | 0.1602 | ||

| Market competition risk, A4 | 0.1710 | ||

| Technical risks, B | 0.1391 | Refinery design risks, B1 | 0.1735 |

| Engineering construction risks, B2 | 0.1678 | ||

| Equipment maintenance risks, B3 | 0.1613 | ||

| Project completion risks, B4 | 0.1979 | ||

| Material and equipment procurement risks, B5 | 0.2995 | ||

| Organization management risks, C | 0.1287 | Human resource risks, C1 | 0.2507 |

| Intercultural management risks, C2 | 0.2646 | ||

| Contract management risks, C3 | 0.2432 | ||

| Refinery operation management, C4 | 0.2415 | ||

| HSE and social responsibility risks, D | 0.2012 | Environmental risks, D1 | 0.3622 |

| Safety and health risks, D2 | 0.3519 | ||

| Social responsibility risks, D3 | 0.2859 | ||

| Economic risks, E | 0.2467 | Local fiscal and taxation policy risks, E1 | 0.2683 |

| Crude oil access risks, E2 | 0.2342 | ||

| Marketization level risks of the local refined oil pricing system, E3 | 0.2656 | ||

| Refined oil market demand risks, E4 | 0.2319 |

© 2017 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Li, H.; Dong, K.; Jiang, H.; Sun, R.; Guo, X.; Fan, Y. Risk Assessment of China’s Overseas Oil Refining Investment Using a Fuzzy-Grey Comprehensive Evaluation Method. Sustainability 2017, 9, 696. https://doi.org/10.3390/su9050696

AMA Style

Li H, Dong K, Jiang H, Sun R, Guo X, Fan Y. Risk Assessment of China’s Overseas Oil Refining Investment Using a Fuzzy-Grey Comprehensive Evaluation Method. Sustainability. 2017; 9(5):696. https://doi.org/10.3390/su9050696

Chicago/Turabian StyleLi, Hui, Kangyin Dong, Hongdian Jiang, Renjin Sun, Xiaoyue Guo, and Yiqiao Fan. 2017. "Risk Assessment of China’s Overseas Oil Refining Investment Using a Fuzzy-Grey Comprehensive Evaluation Method" Sustainability 9, no. 5: 696. https://doi.org/10.3390/su9050696

Note that from the first issue of 2016, this journal uses article numbers instead of page numbers. See further details here.