Understanding the Generation of Value along Supply Chains: Balancing Control Information and Relational Governance Mechanisms in Downstream and Upstream Relationships

Abstract

:1. Introduction

2. Literature Review

2.1. Governance Mechanisms in Collaborative Supply Chains

2.1.1. TCE Perspective

2.1.2. RBV Perspective

2.2. Value Generation in Collaborative Supply Chains: A Multidimensional Approach

2.3. Effects of Firm Roles within Inter-Organisational Supply Chain Relationships

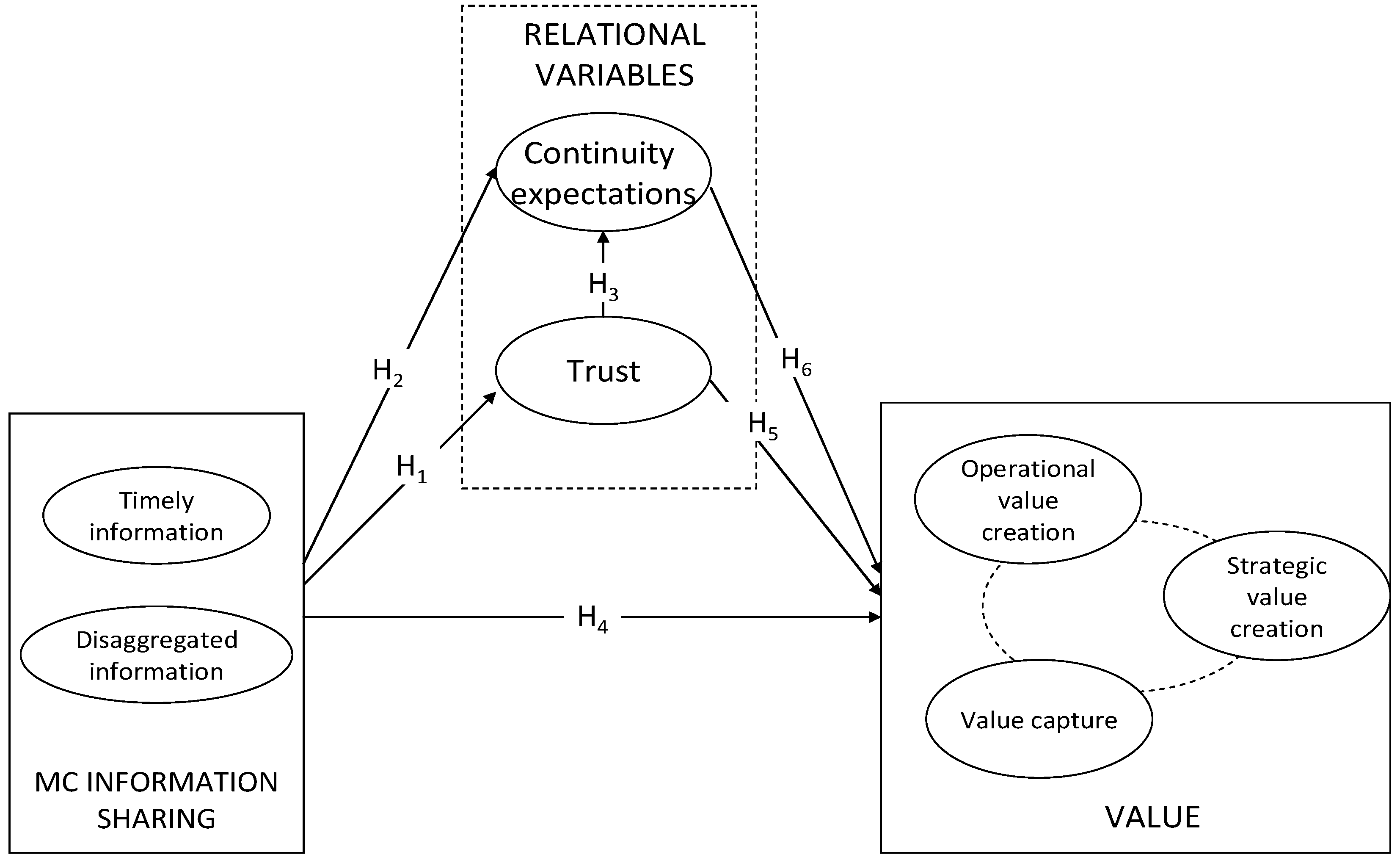

3. Model and Hypotheses

4. Research Methodology

4.1. Sample Design and Data Collection

4.2. Instrument Development

4.3. Nonresponse Bias

4.4. Common Method Bias

4.5. Measurement Model Results

4.6. Invariance Testing

4.7. Structural (Path) Model

5. Results

5.1. Results of Relational Variables

5.2. Results of Value Creation and Capture

6. Discussion and Conclusions

6.1. Managerial and Theoretical Implications

6.2. Limitations and Future Research

Acknowledgments

Author Contributions

Conflicts of Interest

Appendix A. Survey Items and Descriptives

{kind=link}

| MC Information Sharing (Timely) | Buyer Sample Mean (sd) | Supplier Sample Mean (sd) |

|---|---|---|

| TI1—Requested information arrives immediately upon request | 5.28 (1.03) | 5.06 (1.22) |

| TI2—There is no delay between an event and the reporting of relevant information to you | 5.29 (1.03) | 5.16 (1.24) |

| TI3—Reports are received frequently | 5.02 (1.13) | 4.88 (1.34) |

| TI4—Information requested by the partner is provided immediately upon request | 5.25 (1.29) | 5.38 (1.27) |

| TI5—There is no delay between an event and the provision of relevant information to the partner | 5.53 (1.09) | 5.55 (1.22) |

| TI6—Reports are provided frequently | 5.18 (1.13) | 5.50 (1.09) |

| MC Information Sharing (Disaggregated) | ||

| DI1—Information is received in forms that support a “what if?” analysis | 5.12 (1.17) | 5.22 (1.13) |

| DI2—Costs information received is separated into fixed and variable components | 3.87 (1.85) | 3.68 (1.69) |

| DI3—Information is provided in forms that support a “what if?” analysis | 5.24 (1.09) | 5.56 (1.08) |

| DI4—Costs information provided is separated into fixed and variable components | 4.02 (1.68) | 3.79 (1.68) |

| Trust | ||

| TR1—This partner is trustworthy | 5.72 (1.02) | 5.39 (1.29) |

| TR2—This partner is always honest with us | 5.63 (0.94) | 5.32 (1.31) |

| TR3—The partner is capable of providing quality products and services to us | 5.92 (0.89) | 5.61 (1.22) |

| TR4—This partner keeps promises it makes to our firm | 5.35 (1.15) | 5.27 (1.14) |

| TR5—This partner’s beliefs serve our specific need well | 5.77 (0.93) | 5.18 (1.16) |

| TR6—We trust this partner to keep our best interests in mind | 5.42 (1.20) | 5.34 (1.68) |

| Continuity Expectations | ||

| CE1—Your company expects that the relationship will continue over time | 6.02 (0.80) | 6.34 (0.85) |

| CE2—You believe that your partner expects the relationship to continue over time | 6.16 (0.84) | 5.96 (1.10) |

| CE3—Your company makes plans based on continuance | 5.82 (1.23) | 6.06 (1.18) |

| CE4—You believe that your partner makes plans based on continuance | 5.91 (0.94) | 5.13 (1.50) |

| Operational Value Creation | ||

| OV1—Please indicate the level of your firm’s performance in terms of overall product quality relative to your major industrial competitors | 5.18 (1.01) | 5.13 (0.91) |

| OV2—Please indicate the level of your firm’s performance in terms of average selling price relative to your major industrial competitors | 4.67 (1.09) | 4.76 (1.01) |

| OV3—Please indicate the level of your firm’s performance in terms of overall customer service level relative to your major industrial competitors | 4.99 (1.36) | 5.08 (1.27) |

| Strategic Value Creation | ||

| SV1—Please indicate the level of your firm’s performance in terms of research investment relative to your major industrial competitors | 4.65 (1.47) | 4.58 (1.40) |

| SV2—Please indicate the level of your firm’s performance in terms of ability to win resources relative to your major industrial competitors | 4.98 (1.21) | 4.55 (1.28) |

| SV3—Please indicate the level of your firm’s performance in terms of staff training programs relative to your major industrial competitors | 4.72 (1.23) | 4.56 (1.26) |

| Value Capture | ||

| VC1—Please indicate the level of your firm’s performance in terms of return on assets relative to your major industrial competitors | 4.66 (0.93) | 4.41 (1.22) |

| VC2—Please indicate the level of your firm’s performance in terms of market share relative to your major industrial competitors | 4.57 (1.39) | 4.56 (1.40) |

References

- Dyer, J.H.; Singh, H. The relational view: Cooperative strategy and sources of interorganizational competitive advantage. Acad. Manag. Rev. 1998, 23, 660–679. [Google Scholar]

- Corsten, D.; Kumar, N. Do suppliers benefit from collaborative relationships with large retailers? An empirical investigation of efficient consumer response adoption. J. Mark. 2005, 69, 80–94. [Google Scholar] [CrossRef]

- Huemer, L. Supply Management: Value creation, coordination and positioning in supply relationships. Long Range Plan. 2006, 39, 133–153. [Google Scholar] [CrossRef]

- Kähkönen, A.-K.; Lintukangas, K. The underlying potencial of supply management in value creation. J. Purch. Supply Manag. 2012, 18, 68–75. [Google Scholar] [CrossRef]

- Terpend, R.; Tyler, B.B.; Krause, D.R.; Handfield, R.B. Buyer-supplier relationships: Derived value over two decades. J. Supply Chain Manag. 2008, 44, 28–55. [Google Scholar] [CrossRef]

- Daugherty, P.J.; Richey, R.G.; Roath, A.S.; Min, S.; Chen, H.; Arndt, A.D.; Genchev, S.E. Is collaboration paying off for firms? Bus. Horiz. 2006, 49, 61–70. [Google Scholar] [CrossRef]

- Cao, M.; Zhang, Q. Supply Chain Collaboration: Impact on Collaborative Advantage and Firm Performance. J. Oper. Manag. 2011, 29, 163–180. [Google Scholar] [CrossRef]

- Walter, A.; Ritter, T.; Gëmunden, H.G. Value-creation in buyer-supplier relationships. Ind. Mark. Manag. 2001, 30, 365–377. [Google Scholar] [CrossRef]

- Möller, K.E.K.; Törrönen, P. Business suppliers’ value creation potential: A capability-based analysis. Ind. Mark. Manag. 2003, 32, 109–118. [Google Scholar] [CrossRef]

- Sanders, N.R. Pattern of information technology use: The impact on buyer–supplier coordination and performance. J. Oper. Manag. 2008, 26, 349–367. [Google Scholar] [CrossRef]

- Nyaga, G.N.; Whipple, J.M.; Lynch, D.F. Examining supply chain relationships: Do buyer and supplier perspectives on collaborative relationships differ? J. Oper. Manag. 2010, 28, 101–114. [Google Scholar] [CrossRef]

- Cannon, J.P.; Homburg, C. Buyer-seller relationships and customer firm costs. J. Mark. 2001, 65, 29–43. [Google Scholar] [CrossRef]

- Li, S.; Ragu-Nathan, B.; Ragu-Nathan, T.S.; Rao, S.S. The impact of supply chain management practices on competitive advantage and organizational performance. Omega 2006, 34, 107–124. [Google Scholar] [CrossRef]

- Dyllick, T.; Hockerts, K. Beyond the business case for corporate sustainability. Bus. Strategy Environ. 2002, 11, 130–141. [Google Scholar] [CrossRef]

- Wheeler, D.; Colbert, B.; Freeman, R.E. Focusing on value: Reconciling corporate social responsibility, sustainability and a stakeholder approach in a network word. J. Gen. Manag. 2003, 28, 1–28. [Google Scholar] [CrossRef]

- Perrini, F.; Tencati, A. Sustainability and stakeholder management: The need for new corporate performance evaluation and reporting systems. Bus. Strategy Environ. 2006, 15, 296–308. [Google Scholar] [CrossRef]

- Wu, M. Sustainability as Stakeholder Management. In Business and Sustainability: Concepts, Strategies and Changes; Critical Studies on Corporate Responsibility, Governance and Sustainability; Emerald: New York, NY, USA, 2012; Volume 3, pp. 221–239. [Google Scholar]

- Frankel, R.; Goldsby, T.J.; Whipple, J.M. Grocery industry collaboration in the wake of ECR. Int. J. Logist. Manag. 2002, 13, 1–16. [Google Scholar] [CrossRef]

- Daugherty, P.J. Review of logistics and supply chain relationships literature and suggested research agenda. Int. J. Phys. Distrib. Logist. Manag. 2011, 23, 14–26. [Google Scholar] [CrossRef]

- Bovet, D.; Martha, J. Value Nets: Breaking the Supply Chain to Unlock Hidden Profits; Wiley: New York, NY, USA, 2000. [Google Scholar]

- Möller, K.; Rajala, A.; Svahn, S. Strategic business nets-their type and management. J. Bus. Res. 2005, 58, 1274–1284. [Google Scholar] [CrossRef]

- Ulaga, W.; Eggert, A. Value-based differentiation in business relationships: Gaining and sustaining key supplier status. J. Mark. 2006, 70, 119–136. [Google Scholar] [CrossRef]

- Romano, P. Co-ordination and Integration Mechanisms to Manage Logistics Processes across Supply Networks. J. Purch. Supply Manag. 2003, 9, 119–134. [Google Scholar] [CrossRef]

- Noordewier, T.G.; John, G.; Nevin, J.R. Performance outcomes of purchasing arrangements in industrial buyer-vendor relationships. J. Mark. 1990, 54, 80–93. [Google Scholar] [CrossRef]

- Sanders, N.R.; Premus, R. Modeling the relationship between firm IT capability, collaboration, and performance. J. Bus. Logist. 2005, 26, 1–23. [Google Scholar] [CrossRef]

- Kulp, S.C.; Lee, H.L.; Ofek, E. Manufacturer benefits from information integration with retail customers. Manag. Sci. 2004, 50, 431–444. [Google Scholar] [CrossRef]

- Zhang, Q.; Vonderembse, M.A.; Lim, J. Value chain flexibility: A dichotomy of competence and capability. Int. J. Prod. Res. 2002, 40, 561–583. [Google Scholar] [CrossRef]

- Wang, E.T.G.; Wei, H. Interorganizational Governance Value Creation: Coordinating for Information Visibility and Flexibility in Supply Chains. Decis. Sci. 2007, 38, 647–674. [Google Scholar] [CrossRef]

- Heide, J.B.; Miner, A.S. The shadow of the future: Effects of anticipated interaction and frequency of contact on buyer-seller cooperation. Acad. Manag. J. 1992, 35, 265–291. [Google Scholar] [CrossRef]

- Grover, V.; Teng, J.; Fiedler, K. Investigating the role of information technology in building buyer-supplier relationship. J. Assoc. Inf. Syst. 2002, 3, 217–245. [Google Scholar]

- Kale, P.; Singh, H.; Perlmutter, H. Learning and protection of proprietary assets in strategic alliances: Building relational capital. Strateg. Manag. J. 2000, 21, 217–237. [Google Scholar] [CrossRef]

- Paulraj, A.; Lado, A.A.; Chen, I.J. Inter-organizational communication as a relational competency: Antecedents and performance outcomes in collaborative buyer-supplier relationships. J. Oper. Manag. 2008, 26, 45–64. [Google Scholar] [CrossRef]

- Williamson, O.E. Transaction cost economics: The governance of contractual relations. J. Law Econ. 1979, 22, 3–61. [Google Scholar] [CrossRef]

- Hopwood, A.G. Looking across rather than up and down: On the need to explore the lateral processing of information. Account. Organ. Soc. 1996, 21, 589–590. [Google Scholar] [CrossRef]

- Van der Meer-Kooistra, J.; Vosselman, E.G.J. Management control of interfirm trasactional relationships: The case of industrial renovation and maintenance. Account. Organ. Soc. 2000, 25, 51–77. [Google Scholar] [CrossRef]

- Anderson, S.W.; Dekker, H.C. Management control for market transactions: The relation between transaction characteristics, incomplete contract design, and subsequent performance. Manag. Sci. 2005, 51, 1734–1753. [Google Scholar] [CrossRef]

- Dekker, H.C. Control of inter-organizational relationships: Evidence on appropriation concerns and co-ordination requirements. Account. Organ. Soc. 2004, 29, 27–49. [Google Scholar] [CrossRef]

- Ring, P.S.; Van de Ven, A.H. Structuring cooperative relationships between organizations. Strateg. Manag. J. 1994, 13, 483–498. [Google Scholar] [CrossRef]

- Langfield-Smith, K.; Smith, D. Management control systems and trust in outsourcing relationships. Manag. Account. Res. 2003, 14, 281–307. [Google Scholar] [CrossRef]

- Nooteboom, B. Learning and governance in inter-firm relations. Rev. D’écon. Polit. 2004, 114, 55–76. [Google Scholar] [CrossRef]

- Han, G.; Dong, M. Sustainable regulation of information sharing with electronic data interchange by a trust-embedded contract. Sustainability 2017, 9, 964. [Google Scholar] [CrossRef]

- Caglio, A.; Ditillo, A. A review and discussion of management control in inter-firm relationships: Achievements and future directions. Account. Organ. Soc. 2008, 33, 865–898. [Google Scholar] [CrossRef]

- De Man, A.-P.; Roijakkers, N. Alliance governance: Balancing control and trust in dealing with risk. Long Range Plan. 2009, 42, 75–95. [Google Scholar] [CrossRef]

- Vosselman, E.; Van der Meer-Kooistra, J. Accounting for control and trust building in interfirm transactional relationships. Account. Organ. Soc. 2009, 34, 267–283. [Google Scholar] [CrossRef]

- Caniëls, M.J.C.; Gelderman, C.J. Purchasing strategies in the Kraljic matrix-A power and dependence perspective. J. Purch. Supply Manag. 2005, 11, 141–155. [Google Scholar] [CrossRef]

- Meehan, J.; Wright, G.H. Power priorities: A buyer-seller comparison of areas of influence. J. Purch. Supply Manag. 2011, 17, 32–41. [Google Scholar] [CrossRef]

- Yao, Y.; Dresner, M.; Palmer, J.W. Impact of boundary-spanning information technology and position in chain of firm performance. J. Supply Chain Manag. 2009, 45, 3–17. [Google Scholar] [CrossRef]

- Anderson, E.; Weitz, B. The use of pledges to build and sustain commitment in distribution channels. J. Mark. Res. 1992, 29, 18–34. [Google Scholar] [CrossRef]

- Kim, K.K.; Park, S.H.; Ryoo, S.Y.; Park, S.K. Inter-organizational information systems visibility in buyer-supplier relationships: The case of telecommunication equipment component manufacturing industry. Omega 2011, 39, 667–676. [Google Scholar] [CrossRef]

- Cox, A. The art of the possible: Relationship management in power regimes and supply chains. Supply Chain Manag. 2004, 9, 346–356. [Google Scholar] [CrossRef]

- Hakansson, H.; Lind, J. Accounting and network coordination. Account. Organ. Soc. 2004, 29, 51–72. [Google Scholar] [CrossRef]

- Cheung, M.S.; Myers, M.B.; Mentzer, J.T. Does relationship learning lead to relationship value? A cross-national supply chain investigation. J. Oper. Manag. 2010, 28, 472–487. [Google Scholar] [CrossRef]

- Priem, R.L.; Li, S.; Carr, J.C. Insights and new directions from demand-side approaches to technology innovation, entrepreneurship, and strategic management research. J. Manag. 2012, 38, 346–374. [Google Scholar] [CrossRef]

- Ganesan, S. Determinants of long-term orientation in buyer-seller relationships. J. Mark. 1994, 58, 1–19. [Google Scholar] [CrossRef]

- Morgan, R.M.; Hunt, S.D. The commitment-trust theory of relationship marketing. J. Mark 1994, 58, 20–38. [Google Scholar] [CrossRef]

- Uzzi, B. Social structure and competition in interfirm networks: The paradox of embeddedness. Adm. Sci. Quart. 1997, 42, 35–67. [Google Scholar] [CrossRef]

- Kim, K.K.; Park, S.H.; Ryoo, S.Y.; Park, S.K. Inter-organizational cooperation in buyer-supplier relationships. J. Bus. Rev. 2010, 63, 863–869. [Google Scholar]

- Bromiley, P.; Cummins, L.L. Transaction Costs in Organizations with Trust. In Research on Negotiation in Organizations; Bies, R., Sheppard, B., Lewicki, R., Eds.; JAI Press: Greenwich, UK, 1995. [Google Scholar]

- Eisenhardt, K.M. Control: Organizational and economic approaches. Manag. Sci. 1985, 31, 134–149. [Google Scholar] [CrossRef]

- Ouchi, W.G. A conceptual framework for the design of organizational control mechanisms. Manag. Sci. 1979, 25, 833–847. [Google Scholar] [CrossRef]

- Tomkins, C. Interdependencies, trust and information in relationships, alliances and networks. Account. Organ. Soc. 2001, 26, 161–191. [Google Scholar] [CrossRef]

- Mouritsen, J.; Thrane, S. Accounting, network complementarities and the development of inter-organisational relations. Account. Organ. Soc. 2006, 31, 241–275. [Google Scholar] [CrossRef]

- Mohr, J.; Spekman, R. Characteristics of partnership success: Partnership attributes, communication behaviour, and conflict resolution techniques. Strateg. Manag. J. 1994, 15, 135–152. [Google Scholar] [CrossRef]

- Seal, W.B.; Berry, A.; Cullen, J. Disembedding the supply chain: Institutionalized reflexivity and inter-firm accounting. Account. Organ. Soc. 2004, 29, 73–92. [Google Scholar] [CrossRef]

- Lindenberg, S. It takes both trust and lack of mistrust: The workings of cooperation and relational signalling in contractual relationships. J. Manag. Gov. 2000, 4, 11–33. [Google Scholar] [CrossRef]

- Cooper, R.; Slagmulder, R. Interorganizational cost management and relational context. Account. Organ. Soc. 2004, 29, 1–26. [Google Scholar] [CrossRef]

- Bouwens, J.; Abernethy, M.A. The consequences of customisation on management accounting system design. Account. Organ. Soc. 2000, 25, 221–241. [Google Scholar] [CrossRef]

- Chenhall, R.H.; Morris, D. The Impact of Structure, Environment, and Interdependence on the Perceived Usefulness of Management Accounting Systems. Account. Rev. 1986, 6, 16–35. [Google Scholar]

- Chenhall, R.H. Management control systems design within its organizational context: Findings from contingency-based research and directions for the future. Account. Organ. Soc. 2003, 28, 127–168. [Google Scholar] [CrossRef]

- Whipple, J.M.; Frankel, R.; Daugherty, P.J. Information support for alliances: Performance implications. J. Bus. Logist. 2002, 23, 67–82. [Google Scholar] [CrossRef]

- Anderson, E.; Narus, J.A. A model of distributor firm and manufacturer firms working partnership. J. Mark. 1990, 54, 42–58. [Google Scholar] [CrossRef]

- Grant, R. Prospering in dynamically-competitive environments: Organizational capability as knowledge integration. Org. Sci. 1996, 7, 375–387. [Google Scholar] [CrossRef]

- Chenhall, R.H.; Landfield-Smith, K. Multiple Perspectives of Performance Measures. Eur. Manag. J. 2007, 25, 266–282. [Google Scholar] [CrossRef]

- Barney, J.B. Firm resources and sustained competitive advantage. J. Manag. 1991, 17, 99–120. [Google Scholar] [CrossRef]

- Chen, H.; Daugherty, P.J.; Landry, T.D. Supply Chain Process Integration: A Theoretical Framework. J. Bus. Logist. 2009, 30, 27–46. [Google Scholar] [CrossRef]

- Young, G.; Sapienza, H.; Baumer, D. The influence of flexibility in buyer-seller relationships on the productivity of knowledge. J. Bus. Res. 2003, 56, 443–445. [Google Scholar] [CrossRef]

- Liao, Y.; Hong, P.; Rao, S.S. Supply management, supply flexibility and performance outcomes: An empirical investigation of manufacturing firms. J. Supply Chain Manag. 2010, 46, 6–22. [Google Scholar] [CrossRef]

- Hartmann, E.; De Grahl, A. The flexibility of logistics service providers and its impact on customer loyalty: An empirical study. J. Supply Chain Manag. 2011, 47, 63–85. [Google Scholar] [CrossRef]

- Dwyer, F.R.; Schurr, P.H.; Oh, S. Developing buyer-seller relationships. J. Mark. 1987, 51, 11–27. [Google Scholar] [CrossRef]

- Ehret, M. Managing the trade-off between relationships and value networks. Towards a value-added approach of customer relationship management in business-to-business markets. Ind. Mark. Manag. 2004, 33, 465–473. [Google Scholar] [CrossRef]

- Borys, B.; Jemison, D.B. Hybrid arrangements as strategic alliances: Theoretical issues in organizational combinations. Acad. Manag. Rev. 1989, 14, 234–249. [Google Scholar]

- Adner, R.; Zemsky, P. A demand-based perspective on sustainable competitive advantage. Strateg. Manag. J. 2006, 27, 215–239. [Google Scholar] [CrossRef]

- Priem, R.L. A consumer perspective on value creation. Acad. Manag. Rev. 2007, 32, 219–235. [Google Scholar] [CrossRef]

- Priem, R.L.; Swink, M. A demand-side perspective on supply chain management. J. Supply Chain Manag. 2012, 48, 7–13. [Google Scholar] [CrossRef]

- Aspara, J.; Tikkanen, H. Creating novel consumer value vs. capturing value: Strategic emphases and financial performance implications. J. Bus. Res. 2013, 66, 593–602. [Google Scholar] [CrossRef]

- DeSarbo, W.S.; Ebbes, P.; Fong, D.K.; Snow, C.C. Revisiting customer value analysis in a heterogeneous market. J. Model. Manag. 2010, 5, 8–24. [Google Scholar] [CrossRef]

- Madhok, A.; Li, S.; Priem, R.L. The resource-based view revisited: Comparative firm advantage, willingness-based isolating mechanisms and competitive heterogeneity. Eur. Manag. Rev. 2010, 7, 91–100. [Google Scholar] [CrossRef]

- Zander, I.; Zander, U. The inside track: On the important (but neglected) role of customers in the resource-based view of strategy and firm growth. J. Manag. Stud. 2005, 42, 1519–1548. [Google Scholar] [CrossRef]

- Mizik, N.; Jacobson, R. Trading off between value creation and value appropriation: The financial implications of shifts in strategic emphasis. J. Mark. 2003, 67, 63–76. [Google Scholar] [CrossRef]

- Prahinski, C.; Benton, W.C. Supplier evaluations: Communication strategies to improve supplier performance. J. Oper. Manag. 2004, 22, 39–62. [Google Scholar] [CrossRef]

- Cox, A. Business relationship alignment: On the commensurability of value capture and mutuality in buyer and supplier exchange. Supply Chain Manag. 2004, 9, 410–420. [Google Scholar] [CrossRef]

- Saccani, N.; Perona, M. Shaping buyer-supplier relationships in manufacturing contexts: Design and test of a contingency model. J. Purch. Supply Manag. 2007, 13, 36–41. [Google Scholar] [CrossRef]

- Mouritsen, J.; Hansen, A.; Hansen, C.O. Interorganizational controls and organizational competencies: Episodes around target cost management/functional analysis and open book accounting. Manag. Account. Res. 2001, 12, 221–244. [Google Scholar] [CrossRef]

- Normann, U.; Ellegaard, C.; Munkgaard, M. Supplier perceptions of distributive justice in sustainable apparel sourcing. Int. J. Phys. Distrib. Logist. Manag. 2017, 47, 368–386. [Google Scholar] [CrossRef]

- Frohlich, M.T.; Westbrook, R. Arcs of integration: An international study of supply chain strategies. J. Oper. Manag. 2001, 19, 185–200. [Google Scholar] [CrossRef]

- Dekker, H.C. Value chain analysis in interfirm relationships: A field study. Manag. Account. Res. 2003, 14, 1–23. [Google Scholar] [CrossRef]

- Kulp, S.C. The effect of information precision and information reliability on manufacturer-retail relationships. Account. Rev. 2002, 77, 653–677. [Google Scholar] [CrossRef]

- Subramani, M. How do suppliers benefit from information technology use in supply chain relationships? MIS Q. 2004, 28, 45–73. [Google Scholar]

- Fawcett, S.E.; Calantone, R.; Smith, S.R. An investigation of the impact of flexibility on global reach and firm performance. J. Bus. Logist. 1996, 17, 167–196. [Google Scholar]

- Amit, R.; Schoemaker, P.J. Strategic assets and organisational rent. Strateg. Manag. J. 1993, 14, 33–46. [Google Scholar] [CrossRef]

- Eisenhardt, K.; Martin, J. Dynamic Capabilities: What Are They? Strateg. Manag. J. 2010, 21, 1105–1121. [Google Scholar] [CrossRef]

- Pavlou, P.A. Institution-based trust in interorganizational exchange relationships: The role of online B2B marketplaces on trust formation. J. Strateg. Inf. Syst. 2002, 11, 215–243. [Google Scholar] [CrossRef]

- Doney, P.M.; Cannon, J.P. An examination of the nature of trust in buyer-seller relationships. J. Mark. 1997, 61, 35–51. [Google Scholar] [CrossRef]

- Kwon, I.-G.; Suh, T. Factors affecting the level of trust and commitment in supply chain relationships. J. Supply Chain Manag. 2004, 40, 4–14. [Google Scholar] [CrossRef]

- Mohr, J.; Fisher, R.J.; Nevin, J.R. Collaborative communication in interfirm relationships: Moderating effects of integration and control. J. Mark. 1996, 54, 36–51. [Google Scholar] [CrossRef]

- Heide, J.B.; Stump, R.L. Performance Implications of Buyer-Supplier Relationships in Industrial Markets: A Transaction Cost Explanation. J. Bus. Res. 1995, 32, 57–66. [Google Scholar] [CrossRef]

- Fiala, P. Information sharing in supply chains. Omega 2005, 33, 419–423. [Google Scholar] [CrossRef]

- Singh, K.; Mitchell, W. Growth Dynamics: The bidirectional relationship between interfirm collaboration and business sales in entrant and incumbent alliances. Strateg. Manag. J. 2005, 26, 497–521. [Google Scholar] [CrossRef]

- Anderson, E.; Weitz, B. Determinants of continuity in conventional industrial channel dyads. Mark. Sci. 1989, 8, 310–323. [Google Scholar] [CrossRef]

- Ryu, S.; Park, J.E.; Min, H. Factors of determining long-term orientation in interfirm relationships. J. Bus. Res. 2007, 60, 1225–1233. [Google Scholar] [CrossRef]

- Wallenburg, C.M.; Cahill, D.L.; Knemeyer, A.M.; Goldsby, T.J. Commitment and trust as drivers of loyalty in logistics outsourcing relationships: Cultural differences between the United States and Germany. J. Bus. Logist. 2011, 32, 83–98. [Google Scholar] [CrossRef]

- Palmatier, R.W. Interfirm relational drivers of customer value. J. Mark. 2008, 72, 76–89. [Google Scholar] [CrossRef]

- De Toni, A.; Nassimbeni, G. Buyer-supplier operational practices, sourcing policies and plant performance: Results of an empirical research. Int. J. Prod. Res. 1999, 37, 597–619. [Google Scholar] [CrossRef]

- Madhok, A. Reassessing the fundamentals and beyond: Ronald Coase, the transaction cost and resource-based theories of the firm and the institutional structure of production. Strateg. Manag. J. 2002, 23, 535–550. [Google Scholar] [CrossRef]

- Zeller, T.L.; Gillis, D.M. Achieving market excellence through quality: The case of Ford Motor Company. Bus. Horiz. 1995, 38, 23–30. [Google Scholar] [CrossRef]

- Krause, D.R.; Handfield, R.B.; Tyler, B.B. The relationships between supplier development, commitment, social capital accumulation and performance improvement. J. Oper. Manag. 2007, 25, 528–545. [Google Scholar] [CrossRef]

- Whipple, J.M.; Lynch, D.F.; Nyaga, G.N. A buyer’s perspective on collaborative versus transactional relationships. Ind. Mark. Manag. 2010, 39, 507–518. [Google Scholar] [CrossRef]

- Morris, M.; Carter, C.R. Relationship marketing and supplier logistics performance: An extension of the key mediating variables model. J. Supply Chain Manag. 2005, 41, 32–43. [Google Scholar] [CrossRef]

- Borgatti, S.P.; Foster, P.C. The network paradigm in organizational research: A review and typology. J. Manag. 2003, 29, 991–1013. [Google Scholar]

- Capaldo, A. Network structure and innovation: The leveraging of a dual network as a distinctive relational capability. Strateg. Manag. J. 2007, 28, 585–608. [Google Scholar] [CrossRef]

- Anderson, J.C.; Hakansson, H.; Johanson, J. Dyadic business relationships within a business network context. J. Mark. 1994, 58, 1–15. [Google Scholar] [CrossRef]

- Dillman, D.A. Mail and Internet Surveys: The Tailored Design Method; John Wiley & Sons: New York, NY, USA, 2000. [Google Scholar]

- Van der Stede, W.A.; Young, S.M.; Chen, C.X. Assessing the quality of evidence in empirical management accounting research: The case of survey studies. Account. Organ. Soc. 2005, 30, 655–684. [Google Scholar] [CrossRef]

- Abernethy, M.A.; Brownell, P. The role of budgets in organizations facing strategic change. Account. Organ. Soc. 1999, 24, 189–204. [Google Scholar] [CrossRef]

- Chen, J.I.; Paulraj, A.; Lado, A.A. Strategic purchasing, supply management and firm performance. J. Oper. Manag. 2004, 22, 505–523. [Google Scholar] [CrossRef]

- Narasimhan, R.; Nair, N. The antecedent role of quality, information sharing and supply chain proximity on strategic alliance formation and performance. Int. J. Prod. Econ. 2005, 96, 301–313. [Google Scholar] [CrossRef]

- Amstrong, J.S.; Overton, T.S. Estimating nonresponse bias in mail surveys. J. Mark. Res. 1977, 14, 396–402. [Google Scholar] [CrossRef]

- Rogelberg, S.G.; Stanton, J.M. Understanding and Dealing with Organizational Survey Nonresponse. Organ. Res. Methods 2007, 10, 195–209. [Google Scholar] [CrossRef]

- Blair, E.; Zinkhan, G.M. Non-response and generalizability in academic research. J. Mark. Sci. 2006, 34, 4–7. [Google Scholar] [CrossRef]

- Podsakoff, P.M.; MacKenzie, S.B.; Lee, J.-Y.; Podsakoff, N.P. Common method biases in behavioural research: A critical review of the literature and recommended remedies. J. Appl. Psychol. 2003, 88, 879–903. [Google Scholar] [CrossRef] [PubMed]

- Liao, Z.; Wong, W.K. The determinants of customer interactions with internet-enable e-banking services. J. Oper. Res. Soc. 2008, 59, 1201–1210. [Google Scholar] [CrossRef]

- Moslehpour, M.; Wong, W.K.; Aulia, C.K.; Pham, V.K. Repurchase intention of Korean beauty products among Taiwanese consumers. Asian Pac. J. Mark. Logist. 2017, 29, 569–588. [Google Scholar] [CrossRef]

- Hair, J.F.; Black, W.C.; Babin, B.R.; Anderson, R.E.; Tatham, R.L. Multivariate Data Analysis; Prentice-Hall: Upper Saddle River, NJ, USA, 2006. [Google Scholar]

- Steiger, J.H. Structural model evaluation and modification: An interval estimation approach. Multivar. Behav. Res. 1990, 25, 173–180. [Google Scholar] [CrossRef] [PubMed]

- Hu, L.T.; Bentler, P.M. Fit indices in covariance structure modeling: Sensitivity to underparameterized model misspecification. Psychol. Methods 1998, 3, 424. [Google Scholar] [CrossRef]

- Segars, A.H.; Grover, V. Strategic information systems planning success: An investigation of the construct and its measurement. MIS Q. 1998, 22, 139–163. [Google Scholar] [CrossRef]

- Doll, W.J.; Raghunathan, T.; Lim, S.J.; Gupta, Y.P. A confirmatory factor analysis of the user information satisfaction instruments. Inf. Syst. Res. 1995, 6, 177–188. [Google Scholar] [CrossRef]

- Bagozzi, R.P.; Yi, Y.; Phillips, L.W. Assessing construct validity in organizational research. Admin. Sci. Q. 1991, 36, 421–458. [Google Scholar] [CrossRef]

- Fornell, C.; Larcker, D.F. Evaluating structural equation models with unobservable variables and measurement error. J. Mark. Res. 1981, 18, 39–50. [Google Scholar] [CrossRef]

- Byrne, B.M. Structural Equation Modelling with EQS: Basic Concepts, Applications, and Programming; Lawrence Erlbaum Associates: New York, NY, USA, 2006. [Google Scholar]

- Baumgartner, H.; Steenkamp, J.-B. Multi-group latent variable models for varying numbers of items and factors with cross-national and longitudinal applications. Mark. Lett. 1998, 9, 21–35. [Google Scholar] [CrossRef]

- Das, T.K.; Teng, B.S. Trust, control, and risk in strategic alliances: An integrated framework. Organ. Stud. 2001, 22, 251–283. [Google Scholar] [CrossRef]

- Mayer, R.C.; Davis, J.; Schoorman, F.D. An integrative model of organizational trust. Acad. Manag. Rev. 1995, 20, 709–734. [Google Scholar]

- Hines, T.; McGowan, P. Supply chain strategies in the UK fashion industry—The rhetoric of partnership and realities of power. Int. Entrep. Manag. J. 2005, 1, 519–537. [Google Scholar] [CrossRef]

- Tan, K.C. Supply Chain Management: Practices, Concerns, and Performance Issues. J. Supply Chain Manag. 2002, 38, 42–53. [Google Scholar] [CrossRef]

- Köksal, D.; Strähle, J.; Müller, M.; Freise, M. Social sustainable supply chain management in the textile and apparel industry. A literature review. Sustainability 2017, 9, 100. [Google Scholar] [CrossRef]

- Varsei, M.; Christ, K.; Burrit, R. Distributing wine globally: Financial and environmental trade-offs. Int. J. Phys. Distrib. Logist. Manag. 2017, 47, 410–428. [Google Scholar] [CrossRef]

- Brusset, X. Does supply chain visibility enhance agility? Int. J. Prod. Econ. 2016, 171, 46–59. [Google Scholar] [CrossRef]

- Lee, H.; Kim, M.S.; Kim, K.K. Interorganizational information systems visibility and supply chain performance. Int. J. Inf. Manag. 2014, 34, 285–295. [Google Scholar] [CrossRef]

- Seuring, S.; Müller, M. From a literature review to a conceptual framework for a sustainable supply chain management. J. Clean. Prod. 2008, 16, 1699–1710. [Google Scholar]

- Canzaniello, A.; Hartmann, E.; Fifka, M.S. Intra-industry strategic alliances for managing sustainability-related supplier risks: Motivation and outcome. Int. J. Phys. Distrib. Logist. Manag. 2017, 47, 387–409. [Google Scholar] [CrossRef]

| Research | Interorganisational Performance | Research Details | ||

|---|---|---|---|---|

| Operational Value-Creation | Strategic Value-Creation | Value Capture | ||

| [8] (S) | Short-notice deliveries | Innovation, information, references to potential customers, reduction in dependency on other customers, access to third parties | Margin per profit, overall profit, number of deliveries, sales volume, profitability | 247 German suppliers (electronic, mechanical, chemical and vehicle industries) |

| [9] (S) | - | Product and process innovation, market information acquisition, access to other relevant factors in working environment | Direct profit, business volume, level of business, revenue guarantee | Theoretical approach |

| [90] (S) | Product quality, delivery performance, price, responsiveness to requests for changes, service support | - | - | Survey of 139 first-tier North American automotive suppliers |

| [25] (S) | Cost improvement, product quality, delivery speed | Innovation introduction | - | Survey of 245 US industrial firms |

| [6] (B) & (S) | Service level, flexibility, cycle time | Information visibility, end-customer satisfaction, inventory visibility | Business volume | Survey sent to The University of Oklahoma Logistics/Supply Chain Executive Panel (56 members) |

| [22] (B) | Product cost, product quality, delivery performance, service support, conformance to specifications | Personal interaction, know-how, time to market, reduction inventories | - | Interviews with 10 manufacturers in a variety of areas and survey of 118 + 228 purchasing managers |

| [10] (S) | Cost efficiency obtained from higher sales volumes | Improvements of processes, new product, learning about customers and markets, product enhancements, new business opportunities. | Profitability | 241 first-tier OEM suppliers in the computer industry |

| [32] (S) & (B) | Quality, cost, volume flexibility, delivery, response promptness, product conformance to specifications, reliability/dependability, customer order confirmation speed, customer complaint handling speed, delivery dependability | - | - | 232 United States firms (SIC 34–39). |

| [11] (B) & (S) | Order cycle times, order processing accuracy, delivery promptness | Forecast accuracy, satisfaction with the relationship | Profitability, market share, sales growth | 397 buyers and 290 suppliers (US manufacturing and service industries) |

| [44] (B) & (S) | Product quality, delivery performance, cost and price | Know-how, communication | - | 126 buyer units and 126 suppliers of 5 international manufacturing companies |

| [7] (B) or (S) | Quality (as relational collaborative advantage) | Innovation (as relational collaborative advantage) | Growth of sales, ROI, growth on ROI, profit margin on sales | 227 US managers with experience in supply chain management (SIC 25, 20, 34–28) |

| The Firm | Buyers (%/sd) | Suppliers (%/sd) |

|---|---|---|

| General machinery | 57 (54.81%) | 42 (46.66%) |

| Electrical and electronic machinery | 22 (21.15%) | 24 (26.67%) |

| Transportation equipment | 25 (24.04%) | 24 (26.67%) |

| Number of employees | 301.46 (1052.87) | 229.00 (1117.03) |

| Age of firm | 19.21 (15.72) | 19.38 (14.38) |

| ROA | 0.01 (0.13) | 0.05 (0.07) |

| ROE | 0.02 (1.06) | 0.07 (0.25) |

| The relationship | ||

| Volume of purchases/sales represented by the relationship (%) | 15.09 (14.50) | 17.71 (21.93) |

| Length of relationship (years) | 12.13 (8.32) | 11.42 (7.62) |

| Factor | Buyer Sample | Supplier Sample | ||||

|---|---|---|---|---|---|---|

| Factor Loadings (p-Value < 0.05) | CR (>0.7) | CFA Model Fit (Minimum Recommended Values) | Factor Loadings (p-Value) | CR (>0.7) | CFA Model Fit (Minimum Recommended Values) | |

| TI | TI2: 0.651 (0.000 ***) | 0.772 | X2 = 12.209, df = 8 X2/df: 1.526 (<3) GFI: 0.963 (>0.9) AGFI: 0.903 (>0.9) CFI: 0.978 (>0.9) RMSEA = 0.091 (<0.1) | TI2: 0.649 (0.000 ***) | 0.774 | X2 = 8.001, df = 8 X2/df: 1.000 (<3) GFI: 0.973 (>0.9) AGFI: 0.929 (>0.9) CFI: 1.000 (>0.9) RMSEA = 0.071 (<0.08) |

| TI3: 0.643 (0.000 ***) | TI3: 0.753 (0.000 ***) | |||||

| TI4: 0.705 (0.000 ***) | TI4: 0.629 (0.000 ***) | |||||

| TI6: 0.708 (0.000 ***) | TI6: 0.683 (0.000 ***) | |||||

| DI | DI2: 0.900 (0.000 ***) | 0.862 | DI2: 0.756 (0.000 ***) | 0.811 | ||

| DI4: 0.840 (0.000 ***) | DI4: 0.892 (0.000 ***) | |||||

| TR | TR2: 0.750 (0.000 ***) | 0.842 | X2 = 0.432, df = 2 X2/df: 0.216 (<3) GFI: 0.998 (>0.9) AGFI: 0.990 (>0.9) CFI: 1.000 (>0.9) RMSEA = 0.000 (<0.08) | TR2: 0.674 (0.000 ***) | 0.869 | X2 = 1.970, df = 2 X2/df: 0.985 (<3) GFI: 0.989 (>0.9) AGFI: 1.000 (>0.9) CFI: 1.000 (>0.9) RMSEA = 0.000 (<0.08) |

| TR3: 0.728 (0.000 ***) | TR3: 0.752 (0.000 ***) | |||||

| TR4: 0.730 (0.000 ***) | TR4: 0.902 (0.000 ***) | |||||

| TR5: 0.812 (0.000 ***) | TR5: 0.819 (0.000 ***) | |||||

| CE | CE1: 0.903 (0.000 ***) | 0.754 | CE1: 0.722 (0.000 ***) | 0.738 | ||

| CE3: 0.606 (0.000 ***) | CE3: 0.731 (0.000 ***) | |||||

| CE4: 0.603 (0.000 ***) | CE4: 0.633 (0.000 ***) | |||||

| OV | OV1: 0.767 (0.002 ***) | 0.728 | X2 = 9.336, df = 11 X2/df: 0.849 (<3) GFI: 0.976 (>0.9) AGFI = 0.938 (>0.9) CFI = 1.000 (>0.9) RMSEA = 0.000 (<0.08) | OV1: 0.991 (0.000 ***) | 0.756 | X2 = 29.249, df = 11 X2/df: 2.659 (<3) GFI: 0.919 (>0.9) AGFI = 0.793 (>0.9) CFI = 0.909 (>0.9) RMSEA = 0.100 (≤0.1) |

| OV3: 0.746 (0.004 ***) | OV3: 0.529 (0.015 **) | |||||

| SV | SV1: 0.865 (0.004 ***) | 0.805 | SV1: 0.835 (0.000 ***) | 0.821 | ||

| SV2: 0.753 (0.003 ***) | SV2: 0.715 (0.000 ***) | |||||

| SV3: 0.658 (0.007 ***) | SV3: 0.780 (0.000 ***) | |||||

| VC | VC1: 0.565 (0.004 ***) | 0.619 | VC1: 0.612 (0.000 ***) | 0.606 | ||

| VC2: 0.767 (0.007 ***) | VC2: 0.706 (0.000 ***) | |||||

| Buyer Sample | Supplier Sample | |||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| TI | DG | TR | CE | OV | SV | VC | TI | DG | TR | CE | OV | SV | VC | |

| TI | 1 | 0.374 | 0.653 | 0.520 | 0.282 | 0.346 | 0.434 | 1 | 0.410 | 0.352 | 0.361 | 0.328 | 0.320 | 0.396 |

| DG | 0.374 | 1 | −0.029 | 0.057 | 0.372 | 0.339 | 0.087 | 0.410 | 1 | −0.032 | 0.583 | 0.091 | 0.182 | 0.123 |

| TR | 0.653 | −0.029 | 1 | 0.714 | 0.125 | 0.244 | 0.254 | 0.352 | −0.032 | 1 | 0.362 | 0.203 | 0.032 | 0.281 |

| CE | 0.520 | 0.057 | 0.714 | 1 | 0.044 | 0.247 | 0.376 | 0.361 | 0.583 | 0.362 | 1 | 0.102 | 0.033 | 0.290 |

| OV | 0.282 | 0.372 | 0.125 | 0.044 | 1 | 0.312 | 0.118 | 0.328 | 0.091 | 0.203 | 0.102 | 1 | 0.449 | 0.425 |

| SV | 0.346 | 0.339 | 0.244 | 0.247 | 0.312 | 1 | 0.414 | 0.320 | 0.182 | 0.032 | 0.033 | 0.449 | 1 | 0.439 |

| VC | 0.434 | 0.087 | 0.254 | 0.376 | 0.118 | 0.414 | 1 | 0.396 | 0.123 | 0.281 | 0.290 | 0.425 | 0.439 | 1 |

| Max corr | 0.653 | 0.374 | 0.714 | 0.714 | 0.372 | 0.414 | 0.434 | 0.410 | 0.583 | 0.362 | 0.583 | 0.449 | 0.449 | 0.439 |

| √AVE | 0.680 | 0.871 | 0.756 | 0.718 | 0.756 | 0.764 | 0.674 | 0.680 | 0.827 | 0.791 | 0.696 | 0.793 | 0.764 | 0.674 |

| √AVE/max corr | 1.041 | 2.329 | 1.059 | 1.006 | 2.032 | 1.845 | 1.553 | 1.659 | 1.419 | 2.185 | 1.194 | 1.766 | 1.702 | 1.535 |

| Invariance | Χ2 (p) | df | Χ2/df | CFI | GFI | AGFI | RMSEA | ΔΧ2 (p) | ΔCFI |

|---|---|---|---|---|---|---|---|---|---|

| Configural | 381.903 (0.001) | 299 | 1.277 | 0.940 | 0.842 | 0.778 | 0.038 | - | - |

| Metric | 391.472 (0.000) | 312 | 1.255 | 0.942 | 0.839 | 0.783 | 0.036 | 9.569 (0.729) | 0.002 |

| Factorial | 393.496 (0.002) | 316 | 1.245 | 0.944 | 0.838 | 0.784 | 0.036 | 2.014 (0.733) | 0.002 |

| Structural | 418.478 (0.001) | 329 | 1.272 | 0.935 | 0.832 | 0.785 | 0.038 | 24.992 (0.023) | −0.009 |

| Direct Effects | Indirect Effects | Total Effects | |||||||

|---|---|---|---|---|---|---|---|---|---|

| H | Path | Buyer | Supplier | H | Path | Buyer | Supplier | Buyer | Supplier |

| H1 | TI→TR | 0.761 *** | 0.458 *** | - | - | - | - | 0.761 *** | 0.458 *** |

| H1 | DI→TR | −0.307 * | −0.226 + | - | - | −0.307 * | −0.226 + | ||

| H2 | TI→CE | −0.068 | 0.193 | H7 | TI→TR→CE | 0.638 *** | 0.145 * | 0.570 *** | 0.338 + |

| H2 | DI→CE | 0.132 | 0.172 | H7 | DI→TR→CE | −0.258 * | −0.071 + | −0.126 | 0.101 |

| H3 | TR→CE | 0.838 *** | 0.316 * | - | - | - | - | 0.838 *** | 0.316 * |

| H4 | TI→OV | −0.001 | 0.565 * | H7 | TI→{TR,CE}→OV | 0.104 | −0.148 | 0.103 | 0.417 * |

| H4 | TI→SV | 0.083 | 0.319 + | H7 | TI→{TR,CE}→SV | 0.173 + | −0.064 | 0.256 * | 0.255 + |

| H4 | TI→VC | 0.480 + | 0.242 | H7 | TI→{TR,CE}→VC | −0.007 | 0.155 + | 0.473 ** | 0.397 * |

| H4 | DI→OV | 0.392 * | −0.161 | H7 | DI→{TR,CE}→OV | −0.056 | 0.069 | 0.335 * | −0.092 |

| H4 | DI→SV | 0.308 * | 0.086 | H7 | DI→{TR,CE}→SV | −0.064 | −0.008 | 0.244 * | 0.078 |

| H4 | DI→VC | −0.066 | 0.016 | H7 | DI→{TR,CE}→VC | 0.035 | 0.025 | 0.031 | 0.041 |

| H5 | TR→OV | 0.240 | −0.313 + | H7 | TR→CE→OV | −0.117 | −0.005 | 0.124 | −0.318 + |

| H5 | TR→SV | 0.184 | −0.030 | H7 | TR→CE→SV | 0.049 | −0.047 | 0.233 + | −0.077 |

| H5 | TR→VC | −0.238 | 0.059 | H7 | TR→CE→VC | 0.256 | 0.120 + | 0.018 | 0.178 |

| H6 | CE→OV | −0.139 | −0.014 | - | - | - | - | −0.139 | −0.014 |

| H6 | CE→SB | 0.059 | −0.148 | - | - | - | - | 0.059 | −0.148 |

| H6 | CE→VC | 0.306 | 0.378 * | - | - | - | - | 0.306 | 0.378 * |

| Suppliers Value-Based Performance | Buyers Value-Based Performance | |||||

|---|---|---|---|---|---|---|

| OV | SV | VC | OV | SV | VC | |

| TI | Accounting for control | Accounting for control (weak) | Accounting for durable and stable relationships | - | Accounting for trust | Accounting for control |

| DI | - | - | - | Accounting for control | Accounting for control | - |

© 2017 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Ramon-Jeronimo, J.M.; Florez-Lopez, R.; Ramon-Jeronimo, M.A. Understanding the Generation of Value along Supply Chains: Balancing Control Information and Relational Governance Mechanisms in Downstream and Upstream Relationships. Sustainability 2017, 9, 1487. https://doi.org/10.3390/su9081487

Ramon-Jeronimo JM, Florez-Lopez R, Ramon-Jeronimo MA. Understanding the Generation of Value along Supply Chains: Balancing Control Information and Relational Governance Mechanisms in Downstream and Upstream Relationships. Sustainability. 2017; 9(8):1487. https://doi.org/10.3390/su9081487

Chicago/Turabian StyleRamon-Jeronimo, Juan Manuel, Raquel Florez-Lopez, and Maria Angeles Ramon-Jeronimo. 2017. "Understanding the Generation of Value along Supply Chains: Balancing Control Information and Relational Governance Mechanisms in Downstream and Upstream Relationships" Sustainability 9, no. 8: 1487. https://doi.org/10.3390/su9081487