1. Introduction

The European Commission (EC) has set targets for 2020 including a 20% reduction in greenhouse gas emissions (from 1990 levels), a 20% increase of the share of renewable energy sources (RES), and a 20% improvement in energy efficiency [

1]. In 2014, renewable energy sources represented 29% of energy generation in the EU [

2] and they are continuing to grow. The increasing penetration of intermittent and non-controllable decentralized renewable energy sources is causing serious stability problems in the EUs electricity distribution and transmissions networks. This is resulting in high costs for ancillary services in many EU countries and grid operators frequently having to curtail RES generation or to limit further penetration of RES in congested areas. Therefore, there is a need for more flexibility to increase/decrease energy demand when required by the transmission/distribution system operator. Demand Response (DR) represents the most suitable and immediately available way to provide this flexibility due to its wide applicability and cost-effectiveness when compared to other technologies (e.g., storage) or measures (e.g., grid reinforcement). Globally DR could support the penetration of RES on the energy network, mitigate capacity issues on distribution networks, maximize local self-consumption and reduce the required generators margins procured by Transmission System Operators (TSOs), Distribution System Operators (DSOs), and Balance Responsible Party (BRPs) to guarantee grid stability [

3]. DR systems help grid operators and consumers by enabling the shifting or reduction of energy use while compensating participating consumers for their contribution. A DR provider (i.e., aggregator) acts as an intermediary between the grid operator and energy consumers. When the grid operator has difficulties with matching national energy demand, a notification is sent to the DR provider. The DR provider identifies from its portfolio of customers those that can participate. The selected customers receive a request to reduce their energy demand, either manually or automatically, and in return receive financial compensation for their participation [

4].

DR programs in the form of agreements between single large energy consumers (i.e., energy-intensive industrial sites) and grid operators have been in place for some time. However, these programs have failed to work for small- and medium-scale energy consumers [

3]. Blocks of Buildings (BOB) might provide the right scale to participate in DR-programs because when compared to single buildings, they offer more flexibility in timing of energy usage, local energy generation, and energy storage with potentially exploitable assets and synergies. To test this potential, the EC-funded project DR-BOB (GA No. 696114) seeks to integrate existing technologies to create a scalable solution that enables DR operations in buildings consisting of different blocks. These technologies are a Decentralized Energy Management System (DEMS

®) provided by Siemens, a Local Energy Manager (LEM) from Teesside University (outcome of the IDEAS EU-funded project), and a Consumer Portal (CP) that was developed based on the GridPocket EcoTroks

TM (GridPocket SAS, Sophia-Antipolis, France) tool. The integration of these technologies enables real-time optimization of the local energy production, consumption, and storage to maximize economic profit, minimize CO

2 emissions, and comply with DR requests. The DR-BOB solution is intelligent in the sense that it is automated and can adapt to fluctuation in the energy demand or production, subject to dynamic price tariffs and changing weather conditions. The solution is developed and then implemented infour4 pilot sites: the University of Teesside in Middlesbrough (UK), blocks of office buildings in the Montaury district of Anglet (FR), the Fondazione Poliambulanza hospital in Brescia (IT), and the Technical University of Cluj-Napoca (RO). To ensure market penetration, the integration and implementation activities are accompanied by the development of appropriate and innovative Business Models, able to capture the value of the DR-BOB solution for both the potential customer segments and the solution providers.

Following this introduction,

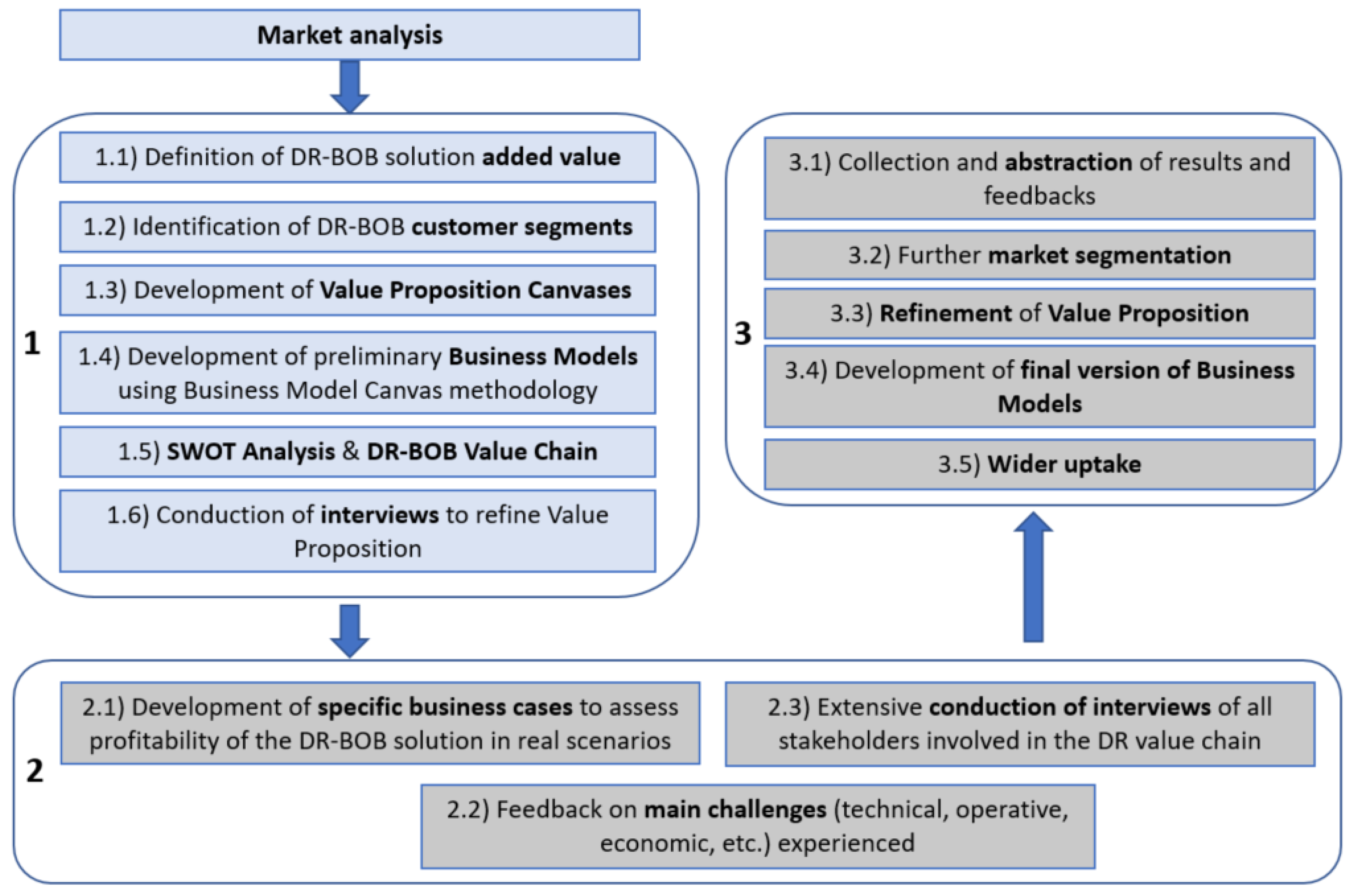

Section 2 describe the challenges encountered when approaching the business modelling activities, while

Section 3 reports the resulting 3-phase methodology for business model development. Then,

Section 4 and

Section 5 focus on the activities completed to date (phase 1), which led to the first version of business models.

Section 6 describes the next step, which will involve the implementation in the pilot buildings and the development of pilot-focused cost-benefit analysis. Finally,

Section 7 reports the key findings resulting from the completion of phase 1.

5. Identified Customer Segments and Business Models

The analysis of the added value of the DR-BOB solution was then sharpened to target specific customer segments and identify business opportunities. This led to the development of two Business Models, both addressing the ambitions and the value offering of a “DR-BOB solution provider”, but each targeting different costumer segments and different market conditions. The DR-BOB solution provider can be considered as a technology provider, but it focused here on the provision of the DR-BOB products and services. Business Models have been developed using the Osterwalder’s canvas methodology [

10]. To further clarify customer needs and shape the DR-BOB solution value proposition, the business models have been further refined using the Value Proposition canvas methodology [

11].

The first Business Model targets BOB owners with different capabilities and in different market conditions:

BOB owners in fully developed DR markets with enough capacity (in terms of available flexibility) to directly participate in explicit DR schemes;

BOB owners in fully developed DR markets without enough capacity (in terms of available flexibility) to directly participate in explicit DR schemes and participating through an aggregator;

BOB owners in partially developed and undeveloped DR markets doing implicit DR or predictive building management.

The second Business Model targets aggregators, which exist only in fully-developed DR market contexts.

In Business Model 1, the technology provider sells the solution directly to BOB owners (or other stakeholders that could be associated with BOB such as municipalities, district managers, local Distribution Network Operators, or intermediaries like ESCOs (Energy Service Companies). The BOB owner gets the opportunity to improve its controllability on the building and, based on the specific market conditions, reduce its energy bill through implicit and explicit DR (with or without an aggregator). In addition, the solution enables predictive maintenance (due to the great amount of data managed) and is able to involve building occupants. In terms of revenue streams, two approaches are identified: product-based and service-based. The choice of one or the other is a function of the market maturity level, of the specific conditions of the BOB, and of the willingness of the DR-BOB solution provider to include building management in its service offering.

For the product-based revenue stream, the DR-BOB solution provider sells the solution directly to the BOB Owner, together with all installation services required to make it fully operative (e.g., integration with existing BEMSs and control systems, implementation and calibration of algorithms, communication between components, support with DR schemes, etc.). Then, the provider also sells maintenance and customer support services, which include regular upgrades to both hardware and software, problem fixing, etc. These additional services are typically sold through annual contracts at a fixed rate based on building size and complexity. This approach is typical of BEMS providers.

The second case uses a service-based approach that is typical of ESCOs. In this case, the revenue for the DR-BOB solution provider does not come from the direct sale of products and limited services, but from part of the revenue that the BOB Owner gets from the utilization of the DR-BOB solution. In this sense, the provider installs the DR-BOB tool in the BOB and provide all services (installation, maintenance, customer support, etc.) without any direct compensation but is paid as a result of cost-saving and revenue obtained from energy efficiency measures and implicit and explicit DR programs. The two parties sign a contractual agreement (which in the case of ESCOs is called Energy Saving Performance Contract—ESPC) that specifies duration of the service, compensation, obligations, etc. Differently from the product-based approach, in this second case, the DR-BOB solution provider is investing in the implementation of DR-BOB in the BOB and expects to get a return from that. This means that the provider is directly interested in how the building is managed and the solution is used. Therefore, it is likely to provide consulting and knowledge to maximize the benefits. In this sense, it is likely that the BOB Owner might decide to externalize facility management services in favor of the DR-BOB solution provider. The BOB Owner would reduce its operative costs and maximize the impact of the DR-BOB solution utilization. The provider would be able to fully control and maximize the profitability of its investment and strengthen its relationship with the end customers.

In the second Business Model, the solution is provided to aggregators that use the DR-BOB solution (in particular, the Siemens’ DEMS®) to extend their portfolio of flexibility providers and then participate in explicit DR schemes. Other stakeholders that could take the roles of aggregators in future are ESCOs, retailers and DSO, if supported by regulations. The main revenue for the DR-BOB solution provider should come from the direct sale of the DEMS and LEMs and CPs (to be then installed in BOBs) and from a limited number of associated services (e.g., training to the aggregators, installation of the DEMS and upgrades). This because the provision of services associated to the BOB, such as installation of LEM and CP, customer support, and maintenance and upgrades, should be part of the agreement between the aggregator and the BOB Owner and should not involve directly the DR-BOB solution provider.

In fully developed DR markets, it is the aggregator who is interested in enabling DR in BOBs and the one sending DR requests to its clients. In spite of this, it is likely that the aggregator will sub-contract some of these services to the solution provider or other professionals due to their higher experience, although always keeping the direct relationship with the end user. This is even more probable in emerging DR markets, where new aggregators will lack the resources for the implementation of the solution in buildings.

However, unlike Business Model 1, it is unlikely that the aggregator will want to establish a service-based agreement with the DR-BOB solution provider and compensate it with part of the revenue obtained from participation in explicit DR schemes. Direct sale seems the only viable option.

6. Implementation in Use Cases

The development and deployment of DR technologies and programs is driven by business opportunities related to improvements in the electricity network or market-based opportunities [

12]. Within the former group, the opportunities lie in the possibility of using flexibility in existing energy markets (day-ahead, balancing and ancillary service, capacity, etc.) to provide services to market players and network operators [

8]. Many studies have already proven the effectiveness of such business opportunities and models through simulation and empirical assessment of DR programs applied to existing markets [

13,

14] and also refer to the building sector [

15]. In DR-BOB, the scope is not to create/test new DR schemes, but simply to check the applicability and profitability of existing ones using flexibility provided by Blocks of Buildings. It is also in scope of the project to assess the appeal and techno-economic convenience of values of flexibility other than the use in energy markets. To do so the business models developed in the already-completed phase 1 will be implemented in the four project’s pilot sites to assess effectiveness and profitability of the DR-BOB solution in real cases. This will also provide feedbacks on technical issues, occupants’ engagement, impact on end users’ comfort conditions, constraints in specific buildings, etc.

Demonstration activities at each pilot will involve the following three steps.

- (1)

Collection of historical data for the creation of a reliable baseline (for both consumption and environmental data), including eventual upgrades to the buildings’ monitoring and control systems;

- (2)

Installation and set-up of the DR-BOB solution;

- (3)

Running of the DR-BOB solution for a given observation period (up to one year).

During the final step, the building energy/facility manager will receive and implement DR requests. These will be triggered based on real and/or emulated events (using a market emulator developed as part of the project) and existing DR and tariff schemes. Building occupants will be asked to provide feedback on other aspects of the solution, such as impact on building management comfort conditions, their work load, etc. Full description of the DR-BOB scenarios can be found in [

16], with key aspects summarized below.

6.1. UK Pilot Site—Teesside University

The demonstration activities at Teesside University will involve four explicit DR schemes and one implicit one, as reported in the following

Table 1.

The scenarios will globally involve up to 700 kW of flexible capacity, mainly deriving from the HVAC system and the CHP of the university. Scenario 3 will also heavily involve building occupants. All explicit DR schemes are established by the UK TSO (UK National Grid) [

17].

6.2. French Pilot Site—Montaury District (Anglet)

In this group of office buildings, the demonstrations will involve two implicit and two explicit DR schemes, as reported in the following

Table 2.

Main assets involved are heat pumps and office equipment. This pilot sites also include a DR action on gas consumption.

6.3. Italian Pilot Site—Fondazione Poliambulanza hospital (Brescia)

Demonstration activities at the hospital will involve 3 implicit and one explicit DR scheme. This because explicit DR programs are not yet available in Italy.

Table 3 reports the DRs scenarios implemented.

The scenarios will involve up to 350 kW of flexible assets. Some events will be triggered by a dynamic tariff, obtained as a combination of energy costs for generating heat, coolth and electricity through a trigeneration plant (CCHP) and the hospital’s gas and electricity import tariffs. Scenario 2 will heavily involve the members of the hospital’s administration staff, who will be required to switch off non-essential office equipment.

6.4. Romanian Pilot Site—Technical University of Cluj-Napoca

As in Italy, Romania has not yet established explicit DR schemes. As a consequence, scenarios for this pilot site will emulate some explicit DR conditions, as summarized in

Table 4.

The two scenarios implemented in the university will involve up to 100 kW of flexible capacity and will directly engage students in the DR actions.

6.5. Methodology for Cost-Benefit Analysis

A detailed cost-benefit analysis will be carried out for each pilot site, with the aim of assessing the profitability of the implementation of the DR-BOB solution. The scope of the analysis will be limited to the boundaries of the four blocks of buildings and it will not take into consideration, in phase 2, the impact of the DR-BOB solution on the electricity network and the benefits in case of extensive deployment.

Costs will be divided into Capital Expenditures (CAPEX) and Operational Expenditures (OPEX). The former will include the total cost for purchasing, installing, and configuring the DR-BOB hardware and software components, as estimated by the project partners that developed them. CAPEX will also include the additional costs for improving the monitoring and control capabilities of the buildings and enabling an effective deployment of the DR-BOB solution. To this aim, the project provided for the development of a dedicated methodology for assessing the DR Technology Readiness Level (DRTRL) of a building [

18]. All pilots were assessed and categorized based on this methodology, which also gave an indication of the required additional metering and control equipment to be installed to achieve the appropriate readiness level. Information about OPEX will be collected during the observation period by recording direct and indirect costs for running the DR-BOB solution; this includes either human resources, licenses for DR-BOB software or other tools (e.g., Building Management Systems), maintenance activities resulting from DR-BOB, etc.

Benefits will be obtained from the economic results of the DR actions during the observation period (either triggered by real or emulated events). The LEM and DEMS are programmed based on existing DR schemes and settlement processes. In most cases, these involve the calculation of a dynamic baseline (based on historical data and current weather and occupancy conditions) and the comparison with the consumption observed during the DR event. Results for each DR instance will be recorded and visualized on the CP, and their cumulation will provide the total cost-saving and revenue during the observation period.

Reliability and consistency of results will be also ensured by adequate replicability assessments to make sure all flexible assets and all DR opportunities are taken into account when calculating overall benefits due to DR.

Furthermore, estimation of benefits will also include those deriving from improvements in building management and operation of assets and from the increased participation of building occupants in energy-related activities.

Table 5 summarizes the data to be recorded for use in the cost-benefit analysis at each pilot site.

The collected cost and benefit information will be then used to calculate cashflows and extract relevant economic indicators (payback time, NPV, IRR) associated to the implementation of the DR-BOB solution in each block of buildings. Finally, as part of phase 3, the results of the cost-benefit analysis will be abstracted and scaled up at national and European levels to see the potential impact of the DR-BOB solution on the various EU DR markets and arrive to the final version of the business models. This will be done in compliance with well-established methodologies for cost-benefit analysis of smart grid projects [

19,

20].

{kind=link}