Purpose: FinTech research has grown rapidly, but few studies have measured the levels of scientific collaboration among authors, institutions, and nations. This study aimed to reveal the status and levels of scientific collaboration in this field. The results will help scholars to combine their knowledge and resources to generate new ideas that may not have been possible if they worked alone and enable them to work more efficiently, resulting in higher-quality results for all parties.

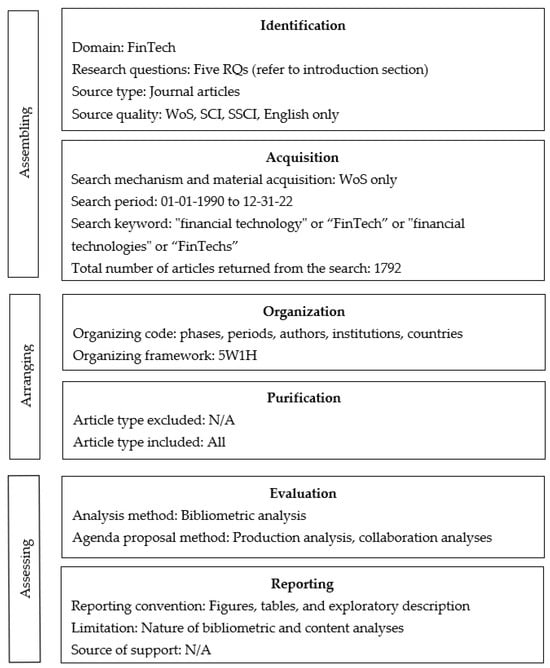

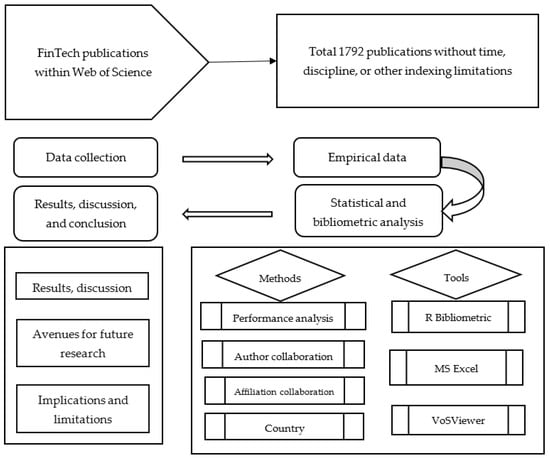

Design/methodology/approach: Research papers in the FinTech field indexed in the Web of Science databases from 1999 to 2022 were included in the research dataset. Using R-bibliometrix and VOS viewer (Visualisation of Similarities viewer), co-authorship networks were drawn. Additionally, some measures of the co-authorship network were assessed, such as the links, total link strength, total number of articles, total citations, normalized total citations, average year of publication, average citations, and average normalized normal citations. Beyond bibliometric analyses, this research gathers other statistics for analysis to gain further insights.

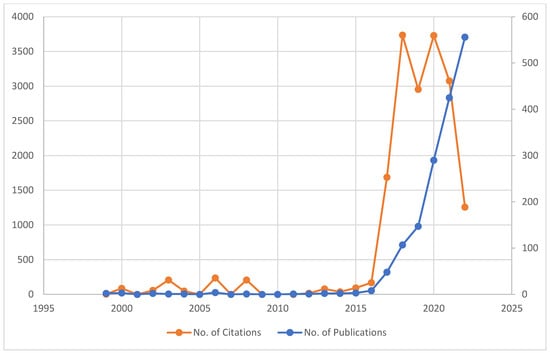

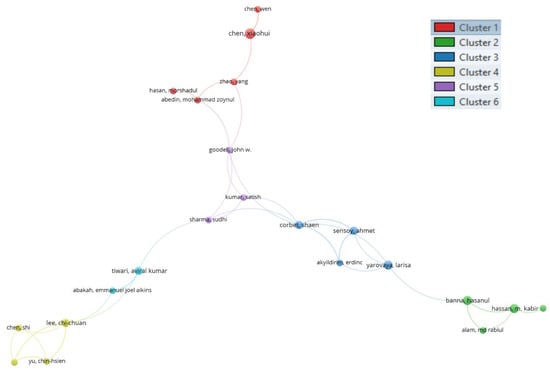

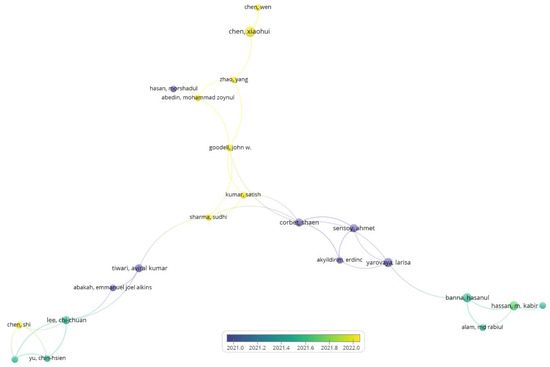

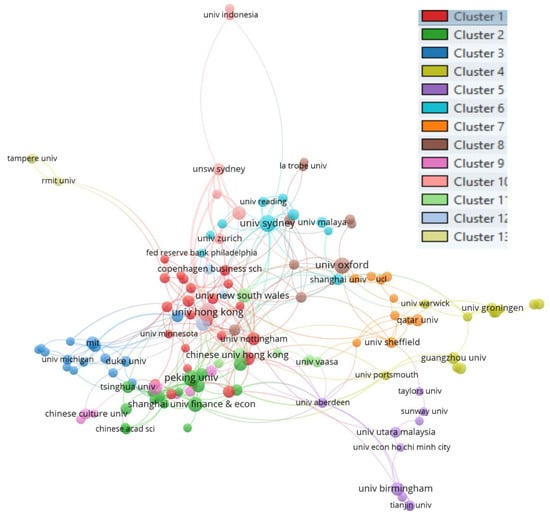

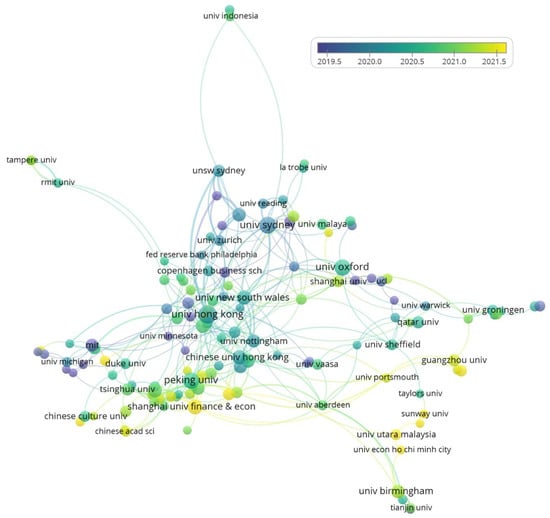

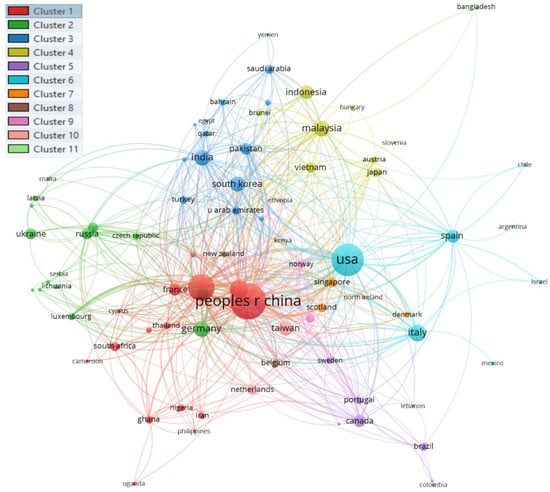

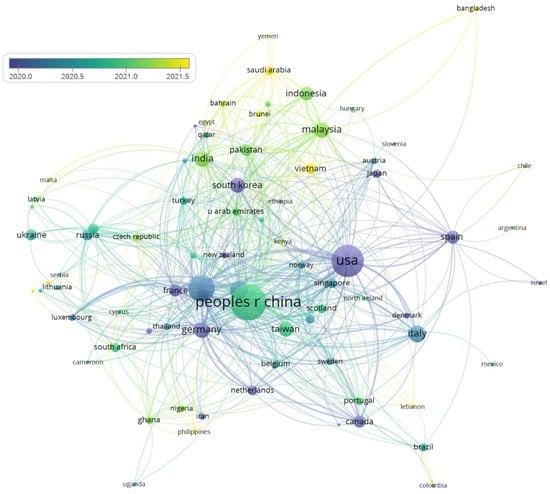

Result: A total of 1792 publications were identified, and a number of these revealed an increase in the forms of collaboration, including collaboration among authors and institutions. Three lists of the most collaborative authors, institutions, and countries were compiled. The top authors, affiliations, and countries were ranked according to their total links, citations, average citations, and annual normalized citations. There were six distinct clusters of collaboration among authors, thirteen among affiliations, and eleven among countries. In terms of author collaborations, the links and total link strength had three nodes and four nodes, respectively. John Goodell, Chi-Chuan Le, and Shaen Corbet were the top three collaborative authors. In terms of affiliations, the two strength attributes were 8 and 12 nodes, with Sydney University, Hong Kong University, and the Shanghai University of Finance and Economics topping the list. In terms of collaboration among countries, these two attributes had 14 and 34 nodes. Three of the most collaborative countries were England, the People’s Republic of China, and the United States.

Originality/value: In contrast with previous systematic literature reviews, this study quantitatively examines the collaboration status in the FinTech field on three levels: authors, affiliations, and countries.

Full article

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}