Risks 2024, 12(5), 83; https://doi.org/10.3390/risks12050083 - 20 May 2024

Abstract

In this research, we consider cyber risk in insurance using a quantum approach, with a focus on the differences between reported cyber claims and the number of cyber attacks that caused them. Unlike the traditional probabilistic approach, quantum modeling makes it possible to

[...] Read more.

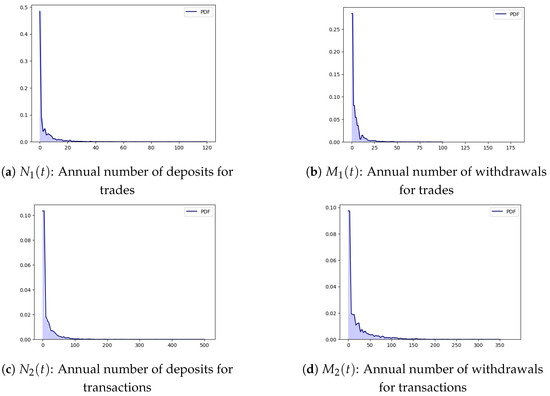

In this research, we consider cyber risk in insurance using a quantum approach, with a focus on the differences between reported cyber claims and the number of cyber attacks that caused them. Unlike the traditional probabilistic approach, quantum modeling makes it possible to deal with non-commutative event paths. We investigate the classification of cyber claims according to different cyber risk behaviors to enable more precise analysis and management of cyber risks. Additionally, we examine how historical cyber claims can be utilized through the application of copula functions for dependent insurance claims. We also discuss classification, likelihood estimation, and risk-loss calculation within the context of dependent insurance claim data.

Full article

(This article belongs to the Special Issue Advancements in Actuarial Mathematics and Risk Theory)

►

Show Figures

Figure 1

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}