Risk Culture during the Last 2000 Years—From an Aleatory Society to the Illusion of Risk Control

1

DZ BANK AG, F/TM, Frankfurt 60265, Germany

2

House of Finance, Goethe University, Frankfurt 60323, Germany

Int. J. Financial Stud. 2017, 5(4), 31; https://doi.org/10.3390/ijfs5040031

Submission received: 7 October 2017

/

Revised: 8 November 2017

/

Accepted: 12 November 2017

/

Published: 1 December 2017

(This article belongs to the Special Issue Finance, Financial Risk Management and their Applications)

Abstract

:The culture of risk is 2000 years old, although the term “risk” developed much later. The culture of merchants making decisions under uncertainty and taking the individual responsibility for the uncertain future started with the Roman “Aleatory Society”, continued with medieval sea merchants, who made business “ad risicum et fortunam”, and sustained to the culture of entrepreneurs in times of industrialisation and dynamic economic changes in the 18th and 19th century. For all long-term commercial relationships, the culture of honourable merchants with personal decision-making and individual responsibility worked well. The successful development of sciences, statistics and engineering within the last 100 years led to the conjecture that men can “construct” an economical system with a pre-defined “clockwork” behaviour. Since probability distributions could be calculated ex-post, an illusion to control risk ex-ante became a pattern in business and banking. Based on the recent experiences with the financial crisis, a “risk culture” should understand that human “Strength of Knowledge” is limited and the “unknown unknown” can materialise. As all decisions and all commercial agreements are made under uncertainty, the culture of honourable merchants is key to achieve trust in long-term economic relations with individual responsibility, flexibility to adapt and resilience against the unknown.

{kind=link}

1. Introduction—Cultures of Risk

For many years, risk management in the financial industry was dominated by the question, how to calculate “severity times probability”. This understanding of “risk” has been applied for three centuries, since Abraham de Moivre formulated in his book (1718) “The Doctrine of Chances: Or, a Method of Calculating the Probabilities of Events in Play” [quote, emphasis by the authors]:

The Risk of losing any Sum is […] the product of the Sum adventured multiplied by the Probability of the Loss.

However, risk extents a weighted probability, as de Moivre pointed out by the single word “adventured”. Without an “adventurer”, there would be no human awareness for the uncertainty of the future. Risk requires individual decision-making in the present and a conscious perception of the future consequences1.

Risk is more than a calculation of a probability distribution—risk is a social phenomenon2 of culture(s). Those can be cultures of a profession (e.g., mediaeval merchants), a time (e.g., Roman empire), a region (e.g., Amsterdam in 17th century), a social position (such as Ulrich Beck’s “Risikogesellschaft”, a “World Risk Society” of the 20th century), a high reliability organisation (HRO, e.g., a hospital), or a general awareness for collectively relevant large-scale technology (such as nuclear power; see, e.g., Jonas 1979 and Bechmann 1993).

On the one side, risk research in economics and in banking focussed on the mathematical aspects of calculating risk capital. After the financial crisis, there was a shift to the issues of good corporate governance and incentive structures as root for mis-conduct by employees. On the other side, the phenomenon “risk” was discussed from different perspectives, as shown by Althaus (2005) in his work about the epistemological status of risk in scientific disciplines. Current examples for the wide spectrum of perspectives about “risk” include:

- The discussion about “risk-taking” starting many years ago from the perspective of psychology (Kahneman and Lovallo 1993) and bank ownership structure (Saunders et al. 1990) to pre-crisis discussions about asymmetric information (Sinn 2003) and competition (Boyd and De Nicoló 2005) to a post-crisis focus on remuneration and incentive pay (Efing et al. 2015; Martynova et al. 2015);

- Darwin College Lecture Series “Risk” of University of Cambridge in 2010;

- Conference on “Kulturen des Risikos im Europa des Mittelalters und der Frühen Neuzeit” (Cultures of Risk in Europe in Mediaeval and Early Modern Times) 2017 in Munich;

- Book “The Illusion of Risk Control: What Does it Take to Live with Uncertainty?” by Gilles Motet (eds. 2017) with focus on “safety culture” in high risk industries.

The term “Kulturen des Risikos“ (Cultures of Risk) was introduced by Herfried Münkler (2010) with a positive connotation of “cultures of risk” compared to “worlds of safety” [original quote3]:

“Kulturen des Risikos trauen sich im Umgang mit dem Gefährlichen und Bedrohlichen mehr zu als Welten der Sicherheit. Kulturen des Risikos sind darauf angelegt, hinter jeder Gefahr auch eine Chance zu sehen. [...] Welten der Sicherheit beruhen auf dem impliziten Versprechen einer sicheren Welt und befördern auf diese Weise Erwartungen, an denen sie schließlich gemessen werden. Dabei stellt sich dann mit großer Regelmäßigkeit heraus, dass sie diesem Versprechen nicht wirklich genügen …”.

This explanation points to a link between “cultures of risk” and the “worlds of safety”. Promises of a safe and simple world will regularly end-up as an illusion of risk control due to unpredicted risk events, while active risk-taking in our complex world results in a mixture of unpredicted success, calculated outcome, and possible failure. This ambivalence of “risk versus safety” led to the development of the idea of resilience to develop systems with an intrinsic dynamical capability to adapt to unpredicted changes and still maintain function.

Taking into account some simplification, this paper aims at providing a synthesis of different perspectives about risk and culture developed along the historical perspective, how “risk” was described and managed in trade and finance4. After a review of the current definitions of the term in the risk management of banks, different phases of the historical development will be discussed:

- An aleatory society with diversification of economical endeavours in the Roman society

- Ad risicum et fortunam: individual decision-making and responsibility of medieval merchants

- Dutch Tulipmania with rational gamblers in times of war and plague in the 17th century

- Adventurers and entrepreneurs in the dynamic economic development of the 18th and 19th century

- Scientific Management in the 20th century and faith in clockwork-like models

- Volatility, Uncertainty, Complexity and Ambiguity (VOCA) in the 21st century

This tour de force integrates the social, cultural and historical aspects of “risk” with the position of individual decision makers such as merchants, entrepreneurs, managers, and bankers.

2. Definitions of “Risk Culture” and Honourable Merchants

The Financial Stability Board (FSB 2014) wrote in its “Guidance on Supervisory Interaction with Financial Institutions on Risk Culture” in 2014 [quote, emphasis by the author]:

A sound risk culture consistently supports appropriate risk awareness, behaviours and judgements about risk-taking within a strong risk governance framework. A sound risk culture bolsters effective risk management, promotes sound risk-taking, and ensures that emerging risks … are recognised, assessed, escalate and addressed in a timely manner. Risk culture … evolves over time in relation to the events that affect the institution’s history (such as mergers and acquisitions) and to the external context within which the institution operates.

One year later, the Basel Committee on Banking Supervision (BCBS 2015) published its guidelines “Corporate Governance Principles for Banks”, in which ”risk culture” was defined as [quote, emphasis by the author]:

… norms, attitudes and behaviours related to risk awareness, risk-taking and risk management, and controls that shape decisions on risks. Risk culture influences the decisions of management and employees during the day-to-day activities and has an impact on the risks they assume.

In the same year, German banking supervisory authority BaFin summarised quite shortly in the title of an expert article (Steinbrecher 2015):

These definitions describe “risk culture” as good corporate processes, conscious decision-making and responsibility of banks as organisations5. In other words, this is the 21st century version of the culture of honourable merchants with personal decision-making, individual responsibility, and good conduct6 in long-term commercial relationships based on pragmatic rationality. Mika Kallioinen summarized this as “The Bond of Trade” (Kallioinen 2012).Risk culture: Requirements of responsible corporate governance

De Molina (1597), a scholar of the school of Salamanca, already mentioned responsible conduct of merchants four centuries ago:

[bankers commit] “mortally sin if they dedicate themselves to the type of transactions where they run the risk (danger) of getting involved in a situation where they will be unable to pay for the deposits. For example, if they send such a great amount of merchandise across sea that in case of shipwrecking, or the ship being caught by pirates, it is not possible for them to pay for the deposits, not even by selling their assets. And they not only mortally sin when the business ends badly, but also even if it were to end favorably.”

Nevertheless, a careful separation is required to avoid a blending of commercial (risk) culture and criminal behaviour, corruption, fraud or betrayal. Every company with some thousand people knows the truth that there will be potential criminals and fraudsters, drug addicts, or cheaters of the type of “rogue traders”. In any culture, one will find criminal behaviour of individuals, small gangs or, respectively, organised crime; and criminal activities belong to public prosecutors7.

As early as 450 BC, the Law of the Twelve Tables (“Leges Duodecim Tabularum”) was the foundation of Roman law. This version of law comprised seven tables about civil and commercial law, and in each case, one for criminal, public and sacred law plus two supplements. Commercial law was always a basis for the society of a market economy—but never was simple. However, Rome will also be the first example for the development of a “risk culture” during the ages.

3. An Aleatory Society—Rome

The idea to explain the perception of risk in old Rome as “Aleatory Society” was elaborated by the English classicist Mary Beard (2011) during a Darwin College Lecture about “Risk and the humanities: Alea iacta est.” The term “Aleatory Society” was coined by Nicholas Purcell (1995) to explain the use of dice (in Latin: alea) as a “cultural map” to create analogies between success and/or failure with the dice versus success and/or failure in other aspects of life such as economy. Mary Beard extended this view and argued that [quote]:

“Romans used the imaginary of dicing actively to parade (and so, in a sense, manage) uncertainty. […] the luck of the board game became a way of seeing, classifying and understanding what in our terms might be thought of as risk.”

At first glance, it might look a little odd that a whole society should have taken dicing as a “tool” to deal with risk and uncertainty. However, today’s perspective is based on four hundred years of probability calculus. To impose our perspective about risk and uncertainty on societies of the past would be misleading, and we should avoid thinking about the Roman society as a pure fatalistic one, in which each event was attributed to a “whim of the gods” by passive people, as Bernstein (1996) wrote.

The late Roman Republic and the Roman Empire were a rather efficient market economy and had—for the time two thousand years ago—a quite developed banking system. Peter Temin (2012) elaborated about the Roman market economy and reported one example that, according to Plutarch, Cato the Elder (Cato Major; 234 BC to 149 BC) lend money for underwriting of ships, but demanded that the borrowers form a large association with at least fifty members, representing as many ships, in which he would take one (of fifty) shares. This double diversification with a pool of 50 ships divided to 50 shareholders is a rather modern approach of financial risk management.

For the first century AD, Jones (2006) presented the case of “The Bankers of Puteoli”, a town near Naples, which draws on an archive of wax tablets published in 1999. At that time, Puteoli was a major shipping centre, as Ostia, the port of Rome at the mouth of the Tiber, was not able to take the huge 300 ton grain ships from Egypt and North Africa. The case concerns the medium sized banking house of the Sulpicii between 35 and 55 AD. One part of their business consisted of short-term loans, and those loans took place at auction sales—such auctions were a large part of the activity of a forum of a Roman city. The other part of the business concerned grain dealing (“commodities”). Due to wind and sea in the Mediterranean, ships from Alexandria arrived in early June. Thus, prices were different in April/May (“uncertainty” = future contracts) to June, when the ships had arrived (“certainty” = spot market for the residuum).

Of course, neither Senator Cato nor the Sulpicii, probably freemen, applied dice for a “calculation of probabilities”. Nevertheless, both were engaged in “risky” economic transactions and had to develop an understanding about the basics of sea trade and commodity markets. As the data represent three generations of the banking house of the Sulpicii, their bank ran a quite sustainable business. In an Aleatory Society, an important thing one could learn from gambling is the lesson that life is unpredictable—you cannot always win, losses are to be accepted, and one should not invest all money in a single game. Obviously, the Sulpicii were able to manage the unpredictable future of business even without the term “risk” and without a better calculus for probabilities than dice. Beard (2011) put it in a nutshell that [quote]: “Rome was a culture that look danger in the eye”.

4. Ad Risicum et Fortunam—Medieval Sea Merchants

The term “risk” can be found in many European languages from the beginning of the 16th century: for example, in German, the first appearance8 was probably in 1507 as “uff unser rysigo” (at our risk; Wilhelm 2013). Nonetheless, this is somehow misleading, as the lingua franca—the language of the merchants and of commercial contracts—was Medieval Latin in the Middle Ages.

Classical Latin did not contain the term “risk”, only danger (“periculum”) or—and with an ambivalent context—luck (“fortuna”). A term for “risk” emerged in the context of Mediterranean maritime trade—traditionally dominated by Italian city republics continuing Roman legacy. One example is Amalfi, a new city not known in Roman times, but just across the gulf of Naples some ten miles from Puteoli, which was a maritime power and trading place. In the 8th and 9th century, when Mediterranean trade revived and while Venice was in its infancy, it dominated the Italian trade with the East trading, i.e., grain, salt and slaves, together with the town of Gaeta. Later, Venice became one of the dominant Italian city republics, and since the middle of the 12th century, North Italian merchants were engaged in long distance sea trade across the Mediterranean.

They rediscovered Roman contracts such as “limited” partnerships known as “colleganza” in Amalfi and Venice (documented from 976 on; see Pryor 1977)—and “commenda” elsewhere in Europe (e.g., in Genoa, Pisa, Marseilles, and Toulouse; see Puga and Trefler 2014). They had replaced the ancient “sea loan” contracts already at the end of the 11th century (Madden 2012). Due to the practical use in maritime trade, there were many similarities9 and amalgamations. The “commenda” seems to stretch back to Roman roots via a link in the Byzantine “chreokoinonia” (χρεοκοινωνία) used by merchants in Constantinople (documented only in the Rhodian Sea Law of the seventh or eighth century; see Pryor 1977 and Letsios 1996), whereas the “colleganza” seem to be an Italian development.

During the Italian Renaissance, the differentiation between individual roles and responsibilities in a “colleganza” or “commenda” with (active) travelling merchant and (passive) sedentary merchants triggered that merchants distinguish between risk and danger:

- “Risicum” was used in the context of individual (commercial) conscious decision under uncertainty, but with the responsibility to accept or cover the (financial) consequences and damages;

- “Periculum” or, respectively, “fortunam” were used for exogenous (natural) forces, with the merchant could not be aware of and which could be covered by a contract, i.e., something unrelated to the individual decision making of a professional and experienced sea merchant.

This development is described by Benjamin Scheller (2017) as “The Birth of Risk”. The next step took place in the fourteenth century with maritime insurance business moving away from the coastal cities and with a concentration in Florence. Merchants began to specify the “risk” factors concerning their spatial and temporal dimensions and to determine their price.

Giovanni Ceccarelli (2015) summarised this progress in a talk with the title about “Renaissance risk takers: culture and practice in Florentine society”. Consequently, a “merchant culture” emerged in the Italian Renaissance, which differed very much from previous hierarchical societies:

- Risk was regarded as an outcome of individual decisions, for which the decision maker has the responsibility (in contrast to hierarchical “tribal” societies).

- Risk was interpreted as intertemporal interaction depending on a clear understanding of a “progressing time” with a development from the present and the future (in contrast to the older “steady-state” societies, in which everything was pre-ordained by religion or sovereign).

- Risk was handled as a commercial product, which could be rationally traded, insured or hedged for a certain price (one of the current core functions of a bank; see Baecker 1991).

As a calculable and transferable commercial product10, “risk” was part of communication, law, social relations and cultural context of the Renaissance merchant society11. The “Birth of Risk” triggered that merchants decided consciously, what they took “uff unser rysigo”. This merchant culture was also the root of the “honourable merchant”—not in the sense of a “moral” category but as a fully rational approach to establish long-term and recurrent business relations across the whole Mediterranean.

In the Zibaldone da Canal, a merchant manual with a Venetian origin dating a little after 1320, one can find the instruction [quote according to translation by (Dotson 1994, 2002)]:

Cheat not rich man nor poor—since you know not what you may encountera man may buy other things—but not fortune12.

Until the end of the 15th century, this development spread out in Europe along the merchants’ network(s) in Europe, where merchants were independent enough (see Fouquet 2010):

- from Italy to Marseilles, Toulouse, Barcelona and Spain;

- with branches of Italian merchant houses in Bruges as “clearing house for northern Europe, and from Bruges to Antwerp and later to Amsterdam;

- from the fairs of the Champagne to Cologne, to Frankfurt and to Southern Germany;

- with merchants—e.g., Jakob Fugger—learning the business in Venice or other Italian cities

- to London and to the Hanseatic League and further to the Baltics.

This development was regional, but also temporal: from the South to the North over some centuries. In parallel, the first documented crisis of merchant houses/merchant banks happened: the crash of the Buonaccorsi, Peruzzi and other merchant families in Florence in 1342/1343, the banking crash in Barcelona in 1381–1383, and the breakdown of merchant families in Rothenburg, Donauwörth and Nürnberg during 1408–1440, as summarized by Fouquet (2010).

There was a highly dynamical—and unpredictable—development during the Middle Ages in a complex network with gateway hubs, long-distance network makers and users of those networks with regional products. As it was usually too risky to carry cash13 for a “delivery versus payment” across Europe, different forms of institutional and relational trust emerged. For example, the Hanseatic League had centralised register of debts since 1270, in which single contracts between merchants were recorded to support the general principles of “good faith and trust” or “bona fide” (see, e.g., Ziegler 1994). In other cases, merchant had a long-term exchange of letters over decades without ever meeting face to face, which provides a relational bond between honourable and enabled them to settle single deliveries in their books mutually by netting14.

Maybe the last step in this development can be seen in Luca Pacioli’s (1494) work on the double-entry system of book-keeping in Europe “Particularis de computis et scriptuis”, which was a stepping-stone to the Modern Age. Accounts receivable and accounts payable were a mapping of an unknown and risky future to the present of the merchants’ business.

5. The Dutch “Tulpmania”—Rational Gamblers in Risky Times (The 17th Century)

A number of changes happened from the Middle Ages to the 16th century: from the discovery of the maritime routes to Asia and the Americas and political changes in Europe to demographic movements and development in the first European “industries” such as English wool production or central European mining. Overall, the centre of European economic leadership shifted to the Netherlands in the so-called “Golden Age”, which De Vries and van der Woude (1997) described as “The First Modern Economy”. Besides a productive local agriculture and a technically advanced industry, the Netherlands established modern public finance, efficient capital markets, and the modern corporation—with the start of the Dutch East India Company (VOC, Vereenigde Oost-Indische Compagnie) and the West Indian Company (WIC). This advancement is rather unique, as it happened during very “risky” times:

- The Dutch Revolt (Eighty Years’ War from 1566/1568 to 1648; in Dutch “Tachtigjarige Oorlog“) against Spanish supremacy with independency de-facto in 1609 and de-jure in 1648

- The Thirty Years’ War in Germany (1618–1648)

- The Bubonic plague in coastal cities in Northern Europe from 1617 to 1630 and isolated outbreaks, e.g., in Amsterdam in summer 1635 to 1637

- The onset of the European “Little Ice Age” in the mid-sixteenth century (continuing to the mid-nineteenth century)

During this time, self-governing cities in the Netherlands—fighting for the independency—(re-)invented financial futures in grain (after the Romans) and employed futures in many other commodities (e.g., herring) important for the European economies. However, there was a razor thin line between gambling prohibited by law, financial futures for hedging (permitted), and short-selling/future trading not for hedging condemned as immoral gambling.

According to a common narrative, the Netherlands were also responsible for the first economic bubble in history: the Dutch “Tulpmania” of 1636/1637. However, in recent studies of detailed price data, Garber (1989), Day (2004) and Thompson (2007) concluded that the “Tulipmania” was an artefact, but not an economic bubble.

Peter Garber focussed on the outbreak of Bubonic plague in Amsterdam (together with other risks of war and climate), which shifted priorities of the common people: They could either die unpredictably due to external “danger” or take individual “risk” in gambling. Because gambling was illegal, people used the tulip market to buy futures without money and sell futures without assets. Serious tulip traders were not engaged in those trades (done in taverns and bars) until the last month before the final crash (Garber 1989).

Thompson (2007) elaborated the implicit conversion of ordinary tulip futures contracts into tulip options (contracts that could be cancelled for a small premium) in an imperfect attempt by some public officials15. Probably, both developments added up as roots for the Tulipmania, which was simply a temporary period during which the prices in future contracts had been legally converted into option prices, which simplified the way to misuse the tulip market for gambling.

It seems that there was no “-mania” at all, but rather rational behaviour of different agents:

- Professional tulip merchants traded in an efficient market, in which the spot and future prices were determined by supply and demand with plague and wars as exogenous factors.

- The common people used the opportunity of the changed “regulation” of the tulip market as a valve for their desire to gamble in times of plague and wars.

Both types of behaviour have to be regarded as rational and risk-aware, but in different ways for different social groups. Although the beginning of the 17th century was a time before a theory of probability was developed, traders and gamblers were aware of the “risk”. The Netherlands of this time represented a risk-aware culture with rational agents—depending on the individual perception of risk according to the social situation.

6. Adventurers and Entrepreneurs—Industrialisation and Non-Equilibrium

In the second half of the 17th century and first half of the 18th century, the concept of probability developed and was based on ideas about gambling (but not about economy at all):

- The “gambler’s dispute” of Chevalier de Méré led to an exchange of letters between Blaise Pascal and Pierre de Fermat, in which principles of probability were formulated in 1654.

- Christiaan Huygens published the earliest book on probability “De ratiociniis in ludo aleae” (On Reasoning in Games of Chance) in 1657.

- Gerolamo Cardano wrote the “Liber de Ludo Aleae” (Book on Games of Chance) sometime in the mid-1500s, although it was unpublished until 1663.

- Jakob Bernoulli’s book “Ars Conjectandi” was published posthumous in 1713.

- Abraham de Moivre wrote the “Doctrine of Chances” in 1718.

In parallel, politics, economy and society in Europe experienced fundamental changes during the 18th century:

- New social, political, and economical concepts, e.g., by Adam Smith and David Hume, which laid the basis of an open society of free individuals;

- New worlds to be discovered (e.g., self-government of “New Amsterdam” in 1652, which was renamed by the English later in 1664 to New York);

- New technologies, e.g., with the steam engine (i.e., with James Watt’s patent in 1781) and railroads (later at the beginning of the 19th century).

All those developments were interconnected in a highly dynamic world far from equilibrium. Nonetheless, this “new world” opened ways for adventurers and entrepreneurs to develop industrialisation and to implement science into innovations. Maybe, the best description can be taken from a company’s name, which was already chartered in 1407: the English “Company of Merchant Adventurers”16.

In a world with opportunities in regions where “no men gone before”, those merchants, adventurers and entrepreneurs took the risk of their individual decision-making. There were a number of controversial and, of course, criminal characters in those years, who used those opportunities to pull naive people over the barrel. In parallel, a number of economic bubbles appeared (see Brunnermeier and Schnabel 201517): the Mississippi bubble of John Law’s Mississippi Company in 1719–1720, the crisis of the East India Company in 1772, East India Company and the Latin America Mania in 1824–1825 to the English Railway Mania in 1840, the German “Gründerkrise” in 1872–1873, the Chicago real estate boom in 1881–1883, et cetera. However, this was a time of industrial, economic development.

The “risk culture” of such a disequilibrium was pointed out by Bernard Mandeville (1705) in “The Fable of The Bees” as “Private Vice, Public Benefit”18. The interaction between independent agents led to a dynamical search process in the market with a positive social result. No calculating authority—neither gods, nor sovereigns—are required for the emergence of the market and the rules of business between the merchants. Von Hayek (1944, 1982) described this development as spontaneous order:

- The risk culture was to embrace risks = size opportunities—and all consequences such as crashes, insolvencies and bubbles were part of the development far from equilibrium.

- However, sellers and buyers had to manage their own risks and take (or sometimes not) their responsibilities. At least, there was no help from a “last resort”.

- In the long run, the economic development generates benefits for the society in general.

Although the calculus of probability was available (first in history) at that time, probability calculations were applied to gambling with fixed rules, but not to the dynamical development of an economy in on-equilibrium. This changed in the 20th century.

7. Scientific Management and the Clockwork as Paradigm (The 20th Century)

At the beginning of the 20th century, scientists such as Henri Poincaré still accepted the complexity of the economies with limited rationality and limited knowledge. One example is the comment of Poincaré (1908) to Bachelier’s thesis [quote]:

Another example is Poincaré’s comment to Walras [as quoted in Ingrau and Israel 1990]:When men are close to each other, they no longer decide randomly and independently of each other, they each reacts to the others19.

… you regard men as infinitely selfish and infinitely farsighted. The first hypothesis may perhaps be admitted in a first approximation, the second may call for some reversion.

This can be seen as an end-point of separated perspectives about the calculation of probabilities in gambling (with fix rules and no development) versus the dynamical development of the economy, in which interaction of agents generates a non-deterministic system far from equilibrium. The beginning of the 20th century marked a threshold to a cultural atmosphere, which arose from the successes of sciences, mathematics and engineering, with believe in a “mechanical” clockwork-like world.

This new conception of economics can be illustrated by three examples:

- Marie-Esprit-Léon Walras’ “Éléments d’économie politique pure” of (Walras 1874), which was influenced by Antoine Augustin Cournot (1801 to 1877) and the French rationalism, or Cartesian constructivism—adopted after the 1954 translation by William Jaffé in the General Equilibrium Theory of Arrow and Debreu (1954) and McKenzie (1959).

- Louis Bachelier’s “Théorie de la Spéculation” (Bachelier 1900; adopted after Leonard Jimmie Savage translated Bachelier to English and Paul Samuelson promoted his ideas in the 1950s).

- Frederick Winslow Taylor’s “Principles of Scientific Management” of (Taylor 1911; with the rapid adaption of his ideas, e.g., by Henry Ford in the production of Ford Model T in 1918).

Those concepts developed between the 1870s and the 1950s adopted the developments of mechanics and mathematics and were all successful milestones in economics to solve allocation problems for the first time on a quantitative basis. Nevertheless, those ideas focussed on an economy with no dynamics, i.e., no innovation, no globalisation and no exogenous factors such as technology or demographics. Although they came from different fields, they represent an assumption of a “clockwork” economy around an equilibrium. Economics was seen through the glasses of Cartesian constructivism, in which risk could arise only as statistical derivations from pre-defined concepts and ex-post prescribed processes.

This “culture of mechanics”—to be distinguished from sciences with the approach of falsification—triggered a development in the second half of the 20th century. The risk culture focussed on paradigm of a “clockwork” world, in which all developments followed fixed rules with calculable outcome. The individual responsibility of an honourable merchant shifted to the background. As one could calculate probability mathematically, an illusion to “control” risk future developed in business and banking. Economic agents were always fully rational, processes were always as designed, plans were always fulfilled, and “uncertainty” was seen as a measurable variance to the predefined parameters only.

Without going into detail, even “heretic” theories such as Benoit Mandelbrot’s (2004) idea about a “fractal behaviour” of the financial market did not question the “rational” approach, but discussed the way how to calculate probabilities. It may be a sheer coincidence, but, Wang et al. (2009) published a paper in which they described that a Brownian motion (of special colloids) does not show a Gaussian distribution, but an exponential one. As Brownian motion and Gaussian distribution were usually used as synonyms in economics, this experiment pointed out that we should be aware of quick associations without experimental evidence.

Walter Schachermayer (2016) provided an intriguing story, how visions of a “calculable economy” was misused at the end of the 20th century to provide simple figures for complex situations [quote]:

The CEO of J.P. Morgan, Dennis Weatherstone, asked the bank’s quants in the wake of the 1987 crash to come up with a short daily summary of the market risk facing the bank. He wanted one single number every day at 4:15 pm which indicates the risk exposure of the entire bank. By that time the quants, i.e., the quantitative financial analysts, disposed of mathematical models for “market risk”, such as the above considered price movements of stocks, options etc. Stochastic models were used to calculate the distribution of total profits or losses from these sources during a fixed period, i.e., the consecutive 10 business days. The “value at risk” was then defined as the 1% quantile of this distribution, i.e., the smallest number M 2 R such that the probability of the total loss being bounded by M; is at least 99%. This was the famous “4:15 number”.

Numbers like this were used without a clear understanding of the limitations—i.e., the assumptions of the central limit theorem and the independency of processes. The risk culture at the end of the 20th century had developed into an “illusion of control” with simple numbers to describe complex situations. The more people were involved in decision-making along defined and prescribed processes, the less somebody saw himself as responsible. Responsibility was “distributed” within a process, a unit, a company or a society: There are policy-makers, model-makers, parameter-makers, process-makers, system-makers, external consultants, analysts, reviewers, auditors, et cetera, but no more decision-makers with individual responsibility.

March and Shapira (1987) pointed out the difference between theoretical models—classical decision theory—and real-world behaviour of decision-makers according to studies:

“Let other managers participate in your decision.” and “believe that risk is manageable”.

The risk culture of an honourable merchant with individual responsibility (taken by a person or a firm20) deteriorated to “you have to dance as longs as the music plays”21. This was a phase transition from a market economy with individual agents and individual responsibility to a collective behaviour—herd behaviour—with a substitution of responsibility by theoretical models. The financial crisis put an end to this, or in the words of Meryn King (2016): The financial crisis marked “The End of Alchemy”.

8. Parenthesis about the Tails of the Unexpected

In a conference about “The Credit Crisis Five Years On: Unpacking the Crisis” in 2012, the chief economist of the Bank of England, Andrew G Haldane spoke about: “Tails of the unexpected”. In his speech he postulated that the Knightian “unknown unknown” cannot be calculated at all. However, there is a continuous transition from the “known” to the “unknown unknown”, which can be illustrated by the power law distribution22 for the severity S and frequency F of (operational) risk events: F(S) proportional to S −λ.

For the purpose of this paper, a good summary was given by Haldane (2012) to illustrate the connection between small “calculable” risk events and disasters: the development of forest fires in two different situations:

- One would imagine an area where trees are naturally and randomly growing with occasional lightning strikes that could cause a fire. Over longer time, the forest will develop into a “critical” state: Most of the time, fires are small and contained, but, on rare occasions, a random lightning strike can cause the forest to be lost.

- A forester takes concern for the expected yield of the forest with a trade-off. A more densely filled forest makes for superior expected yield, but it also exposes the forest to higher fire risk. The forester will build firebreaks: larger in number where lightning strikes, and fewer where they are rare. This arrangement maximises expected yield. However, it will also result in occasional “systemic” forest fires as the scrub will be removed, which typically leads to small fires in free nature, which clean the forest naturally from time to time.

A living forest is a rather complex, interactive structure, although it consists of simple elements such as trees and scrub. While the first situation can be characterised as self-organized criticality (“SOC”, see Bak et al. 1987), the second one correspond to highly optimised tolerance (“HOT”, see compilation by Carlson and Doyle 2002).

Both concepts were taken into account in the development of the theory of “high reliability organisation”, originally discussed by Rochlin et al. (1987). They wrote in the introduction [quote, emphasis by the authors]:

“Recent studies of large, formal organizations that perform complex […] tasks under conditions of tight coupling and severe time pressure have generally concluded that most will fail spectacularly at some point, with attendant human and social costs of great severity. The notion that accidents in these systems are “normal” that is, to be expected given the conditions and risks of operation, appears to be as well grounded in experience as in theory.”

In a nutshell, complex organisation cannot avoid risk. Things will go wrong, and accidents are quite normal. The consciousness that tail risk cannot be calculated and high severe risk event will happen at some point in time is antagonistic to the belief of “clockwork” economy with fixed rules and ex-ante planned results. Especially, the trigger for a catastrophic risk event can be very small and can have an incalculable23 impact.

One intriguing example of an external impact on a highly complex system may be one statement of Clinton (1995) [quote]: “Make it easy for people to own their own homes and enjoy the rewards of family life and see their work rewarded.” This vision for a general homeownership—independent of actual financial capabilities—can be regarded as one trigger24 of the US subprime mortgage crisis two decades later. Starting from the political vision, the U.S. mortgage industry changed from traditional on balance sheet mortgages to a long and fragmented chain from underwriting, banks as intermediators, aggregation by government-sponsored institution, securitisation into Asset-backed Securities, repacking into Collateralised Debt Obligations (CDO), re-repacking, et cetera. The non-predictable development ended with three results: disregard of assumption in the idealised models (with independent events instead of a synchronised domestic home market), replacement of individual responsibility by formal distributed processes and oblivion that the future is uncertain.

9. From Sir Karl R. Popper to the Concept of Resilience

Since the 1990s, it would have been easy to think outside the box, and one example maybe a U.S. Marine Corps (1997) manual with the guideline:

In the heat of battle, plans will go awry, instructions and information will be unclear and misinterpreted, communications will fail, and mistakes and unforeseen events will be commonplace.

Risk in the sense of the unpredictability of the future cannot be “removed” or “reduced” by models or plans—neither in the heat of battle, nor in the economy.

Sir Karl R. Popper (1991) pointed out this basic principle of uncertainty in the quote:

All Life is Problem Solving.

The quote is a summary of his concept of “critical rationality”, i.e., the concept to regard all theories or models as temporal knowledge and to accept future uncertainty and evidence-based revision of assumptions. If we understand Sir Karl R. Popper right, we have to be prepared to solve unexpected problems and should not “put all money” in models with limitations and assumption.

McChrystal (2016) supported this perspective from a different perspective, how military conflicts in time of VUCA (volatility, uncertainty, complexity, ambiguity) develop:

… complex phenomena happened and how they might happen, but they can’t tell us when and where it will happen.

Consequently, McChrystal proposes an organisational approach of “team of teams”, which is based upon adaptive entities with a high flexibility to react to unforeseen events to cope with “uncertainty”25.

The 21st century has to be prepared for complexity far from equilibrium and, consequently, a “culture of resilience” is required26. Niklas Luhmann (1968) pointed out that “trust is a mechanism for a reduction of (social) complexity”. Different to use of the term “complexity” in computational sciences, Luhmann’s “complexity” describes the situation of a decision-maker to anticipate the future, in which his commercial counterparties are free to make their decision about different options at any time. In Luhmann’s view, trust depends on experiences made in the past with those counterparties and facilitates to bridge the gap to the uncertain future, in which the counterparties are free to choose their options at any time. This concept re-captures ideas elaborated more than hundred years ago by Simmel (1908) that [quote, translated by the author]:

trust [is] a hypothesis of future behaviour, which is stable enough to base upon practical actions

Although Luhmann’s concept seems quite trivial, without trust (based on past experiences) and responsibility (for future consequences), two important issues of risk-taking emerge:

- the responsibility for the intertemporal gap between present decisions and future consequences (leading to moral hazard of decision-makers in the classical principal-agent-situation and to problematic impact of incentive pay on risk-taking);

- the responsibility for “faceless” decisions, if such decision-making is distributed along a chain of formal approval processes.

In a recent paper, Shapira and Zingales (2017) analyzed such “normal wrongdoing” and coined the term “faceless crime”. They drilled down one well-documented case (the emissions of a toxic chemical by DuPont over decades) and pointed out that without individual responsibility and accountability, a collective of decision-making will search for an optimum for that collective, especially when decision-making and consequences are separated by a time lag due to a long-term information asymmetry and distributed approval.

10. Strength of Knowledge and the Importance of Our Ignorance

Human “Strength of Knowledge” is limited and the “unknown unknown” can materialise anytime. The distinction between “risk” (a situation where each possible outcome is known and can be assigned a probability) and “uncertainty” (a situation where probabilities and perhaps even the set of outcomes is unknown) was made by Frank Knight (1921), and referred to by a wealth of authors including Keynes (1921) and King (2016). This leads to a more detailed approach to risk following distinction (see Aven 2010, 2012; Milkau 2013) taking into account our “Strength of Knowledge” (SoK):

- Historical loss data defined by R0 = {E, L, N; SoK = 1} with type of OpRisk event E, loss L, recorded number of events N. For aggregated events, a statistical measurement error can be added Ri = {Ei, Li, Ni, σi; SoK = 1}.

- Measured risk R = {E, L, Ps; SoK} with a Bayesian interpretation of Ps as subjective measure of uncertainty under the conscious assumption of a “repeatable game”.

- Estimation of (future) risk R* = {E, L, Pf*, U(Pf*), SoK} with an uncertainty for the probability U(Pf) based on the Strength of Knowledge SoK about the expected future, i.e., the question whether the “game” is fully repeatable.

- Uncertainty of future (extrapolated) risk by replacing the frequency-interpreted probability Pf by the uncertainty U(SoK) itself, giving a risk perspective RU = {E, O, U(SoK)}27, which is aligned to the new ISO 31000 definition of risk (see Purdy 2010) with a shifted emphasis to the uncertain achievement of an objective O.

- The “unknown unknown”, i.e., the risk of possible disasters: RDesaster = (Disaster, O, SoK << 1) about which no knowledge is available.

In contrast to the illusion at the end of the 20th century that risk can be “controlled” by calculating simple numbers, SoK puts the focus on “The Importance of Our Ignorance” (von Hayek 1967). As Renn et al. (2011) pointed out [quote]: “But many risks are not simple and cannot be calculated as a function of probability and effects.” The approach shown above has the advantage to include other classifications of risk with categories of volatility, uncertainty, complexity, and ambiguity.

This comes with the disadvantage to lose the simplicity of Abraham de Moivre (1718) formula to calculate risk in gambling with fixed rules. Of course, in fully defined circumstances—as in continuously repeated games with fixed rules, i.e., with a continuity from the past to the future (in average)—the future will follow the pattern of the past and probabilities can be calculated. Those methods have been proven as very efficient in many other areas including banking.

However, even in a Gaussian distribution, severe tail events can occur at any time—now or later. Under the condition of a power law distribution, situation can occur even without a mean value for the total loss (in cases with λ < 1), and extreme events can contribute the majority of total loss.

During dynamic developments, systems far from equilibrium can be deterministic, but not calculable. Finally, in systems with possible phase transitions (e.g., from independent agents to herd behaviour), the switch can be unpredictable. This limited knowledge can be the key to an understanding that the future is non-calculable and any decision has to be made under uncertainty.

11. Digitization and Epistemic Uncertainty

David Spiegelhalter (2011) pointed out in a lecture [quote]:

But when we start acknowledging our inability to represent the full complexity of the real world using mathematical models, we are faced with leaving the safe land of quantifiable uncertainty and entering (possibly hostile) environment of disputed sciences, ill-understood possibilities and deep uncertainty.

Accepting our ignorance about the future or, respectively, our epistemic uncertainty comes with a natural resistance, because many people prefer a secure and predictable future and like to trade personal responsibility for paternalism. Such a behaviour is not restricted to “conservative” social groups, but can be found in rather “digital” communities, too. One example is the discussion about “Code is Law” in cases where so-called smart contracts are deployed on an immutable blockchain to automate contractual agreements (see, e.g., Milkau et al. 2016).

Such “smart contracts” are simply software scripts running in a distributed computer network. Given: (a) that the partners of the contractual relationship agreed to write the contract in this special language—and not in English, Swahili or Esperanto; and (b) the applicable law they agreed on—i.e., law of Delaware, of the Netherlands, or of China—allows electronic contracts, there is no magic in a smart contract. A smart contract is just a documentation of the mutual agreement.

Protagonists of a digital “Code is Law” would point out that such a smart contract could automatically enforce all future actions, like payments or, in case of a default, a restitution of the traded object. Even in unforeseen situations, the code of the smart contract would be completely prescriptive and enforce all actions in the future, as they were documented in the past.

In such a world of “Code is Law”, no uncertainties would exist, as all conditions (if–then–else) and were fixed immutably ex-ante. Nevertheless: What happens if one partner files under Chapter 11 (or any equivalent in the chosen law) and this possibility was not included in the code? Simply ignore Chapter 11 and make the payment after all? Of course, the rules of Chapter 11 apply to all account and all payments independent from the technical systems (traditional bank account or blockchain tokens). Man-made law to solve disputes and courts have the task to make judgements—especially in unexpected cases.

The discussion about “Code is Law” illustrates the human desire for predictability and for a simple clockwork-like world. In parallel, it demonstrates the wish to build up an illusion of control and to substitute individual responsibility with a technical “clockwork”. Finally, it shows how the future is predicted merely as simple extrapolations of today and how much we ignore the possibility of (unforeseen) developments in society, business and law.

12. Conclusions

We live in a complex world, in which risk is inescapable. Even a natural phenomenon, classically understood as an exogenous “danger” or act of god, can trigger a “risk”: Where people for example decide to settle down in lowland regions, which are usually flooded by a hurricane, et cetera, their decision-making results in a high risk for individuals and the society.

From the historical perspective applies in this paper, a correlation—of course without evidence for causality—can be seen between the development of the probability calculus and the perception of risk:

- The more statistical methods became available to calculate probabilities, the less understanding of the social aspect of risk remained.

- The more trust in numbers or model developed, the less responsibility was taken for the future consequences of current individual decisions.

Risk is the human perception of the intertemporal gap between current decision-making and future consequences, i.e., the gap between the present and the future28. As a human perception, Risk depends on the social system we live in—in a pre-ordained world there is no risk, but only the will of gods or sovereigns. Luhmann (1991) pointed out [quote from the English translation including the emphasis (Luhmann 1993)]:

The outside world itself knows no risks, for it knows neither distinction, nor expectations, nor evaluations, nor probabilities—unless self-produced by observer systems in the environment of other systems.

One example for such a social system was the community of independent merchants over centuries making decision under uncertainty and taking the (individual) responsibility for future uncertainty. This community developed continuously from the Roman “Aleatory Society” via the Italian city republics and the merchants in the Middle Ages to the adventurers of the industrialisation and to the entrepreneurs at the beginning of the 20th century.

Without any doubt, there was a very successful development of statistics and use of quantitative models in risk management. In the world we live in, nobody would not be capable of handling everyday problems, like commuting to the workplace or making decision for personal life, without generalizing and extrapolating from experiences. Statistical reasoning can be regarded as an attempt to formalize such mental activities and provide a professional framework to support decision making under uncertainty. The fact that some poorly understand the assumptions and limitations of statistical approaches, and that results are unduly generalized, does not imply that such endeavours are vain. A vast number of technical and business decisions are based on—well-understood—statistical concepts: from fatigue analysis of airplane wings to credit card fraud management.

Nevertheless, exactly those successes stimulated a conjecture that men can plan economical systems, design distribution of resources, and predict the future “clockwork” behaviour. The financial crisis (and incidents from nuclear power to hurricanes) made clear that complex systems are no clockworks and that every decision about the future is uncertain and not calculable. Additionally, it became clear that human decisions: (i) conserve beliefs; (ii) overestimate individual experiences; and (iii) attribute history to the will of human beings (March 1994)—we all are biased.

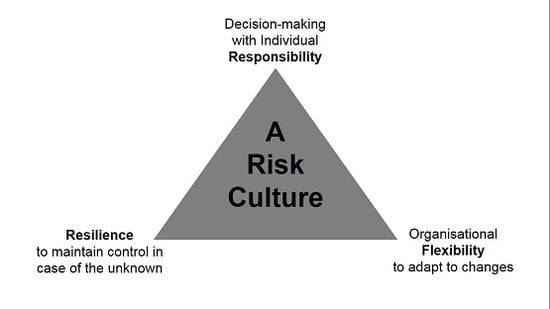

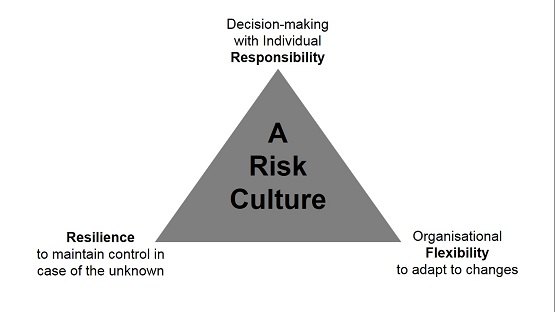

To take care for our human ignorance about the future, a sound risk culture should include:

- Responsibility for the decisions made under uncertainty, including the “risk” to admit mistakes afterwards;

- Flexibility for future development with adaptive “Team of Teams” in times of VUCA and for situations far from equilibrium;

- Resilience practice (Walker and Salt 2012) “to build capability to absorb disturbance and maintain function” including the monitoring of “precursors”, i.e., early warning signals within time series of risk-parameters, which indicate some imminent unknown unknown.

In that sense, the Roman and Mediaeval merchants showed more understanding of the uncertain future and—in parallel—more individual responsibility compared to people at the beginning of the 21st century who put all their money in one game and believed in predictability of the future, but ignored the assumptions and limitation of all model made by men and women.

Acknowledgments

The author thanks two unknown reviewers and Ritva Tikkanen, University of Gießen, for valuable comments and discussion.

Conflicts of Interest

The author declares no conflict of interest. The opinion expressed in this paper is his individual one and does not represent the company or academic institutions he is engaged with.

References

- Althaus, Catherine E. 2005. A disciplinary perspective on the epistemological status of risk. Risk Analysis 25: 567–88. [Google Scholar] [CrossRef] [PubMed]

- Arrow, Kenneth, and Gerard Debreu. 1954. The Existence of an Equilibrium for a Competitive Economy. Econometrica 22: 65–290. [Google Scholar] [CrossRef]

- Arthur, W. Brian. 2014. Complexity Economics. In Complexity and the Economy. Oxford: Oxford University Press, pp. 1–29. [Google Scholar]

- Aven, Terje. 2010. Misconceptions of Risk. Chichester: John Wiley & Sons. [Google Scholar]

- Aven, Terje. 2012. The risk concept—Historical and recent development trends. Reliability Engineering and System Safety 99: 33–44. [Google Scholar] [CrossRef]

- Bachelier, Louis. 1900. Théorie de la Spéculation. Annales Scientifiques de l’École Normale Supérieure 3: 21–86. [Google Scholar] [CrossRef]

- Baecker, Dirk. 1991. Womit Handeln Banken?—Eine Untersuchung zur Risikoverarbeitung in der Wirtschaft. Frankfurt: Suhrkamp Taschenbuch. [Google Scholar]

- Bak, Peter, Chao Tang, and Kurt Wiesenfeld. 1987. Self-organized criticality: An explanation of the 1/f noise. Physical Review Letters 59: 381–84. [Google Scholar] [CrossRef] [PubMed]

- Basel Committee on Banking Supervision (BCBS). 2015. Guidelines—Corporate Governance Principles for Banks. July. Available online: http:www.bis.org/bcbs/publ/d328.htm (accessed on 28 August 2017).

- Beard, Mary. 2011. Risk and the humanities: Alea iacta est. In Risk. Darwin College Lectures. Edited by Layla Skinns, Michael Scott and Tony Cox. Cambridge: Cambridge University Press. [Google Scholar]

- Bechmann, Gotthard, ed. 1993. Risiko und Gesellschaft: Grundlagen und Ergebnisse Interdisziplinärer Risikoforschung. Opladen: Westdeutscher Verlag. (In German) [Google Scholar]

- Bernstein, Peter L. 1996. Against the Gods: The Remarkable Story of Risk. New York: John Wiley & Sons. [Google Scholar]

- Boyd, John H., and Gianni De Nicoló. 2005. The Theory of Bank Risk Taking and Competition Revisited. The Journal of Finance 60: 1329–43. [Google Scholar] [CrossRef]

- Brunnermeier, Markus K., and Isabel Schnabel. 2015. Bubbles and Central Banks: Historical Perspectives. CEPR Discussion Paper No. DP10528. Available online: https://ssrn.com/abstract=2592370 (accessed on 4 September 2017).

- Caranda, Ramón. 1987. Carlos V y sus Banqueros, Editorial Crítica. Madrid: Barcelona. [Google Scholar]

- Carlson, Jean M., and John Doyle. 2002. Complexity and robustness. Proceedings of the National Academy of Sciences of the United States of America 99: 2538. [Google Scholar] [CrossRef] [PubMed]

- Ceccarelli, Giovanni. 2015. Renaissance Risk Takers: Culture and Practice in Florentine Society. Talk Given at December 2. Available online: www.uni-due.de/graduiertenkolleg_1919/wagnisse (accessed on 2 September 2017).

- Clinton, William J. 1995. Remarks on the National Homeownership Strategy. June 5 The American Presidency Project. Available online: www.presidency.ucsb.edu/ws/?pid=51448 (accessed on 21 August 2017).

- Cohn, Alain, Michel Maréchal, and Christian Zünd. 2016. Civic Honesty across the Globe. Paper presented at the SITE Summer Workshops 2016, Session 8: Psychology and Economics, Stanford University, August 24–26; Available online: https://site.stanford.edu/2016/session-8 (accessed on 17 September 2017).

- D’Aveni, Richard A. 1998. Waking up to the New Era of Hypercompetition. The Washington Quarterly 21: 183–95. [Google Scholar] [CrossRef]

- Daft, Richard L., and Robert H. Lengel. 1983. Information Richness: A New Approach to Managerial Behavior and Organization Design. College Station: Texas A&M University. [Google Scholar]

- Day, Christian C. 2004. Is There a Tulip in Your Future? Ruminations on Tulip Mania and the Innova-tive Dutch Futures Markets. Journal des Economistes et des Etudes Humaines 14: 151–70. [Google Scholar] [CrossRef]

- De Moivre, Abraham. 1718. The doctrine of Chance. W. Pearson, London as extended English version of De Mensura Sortis, Phil. Trans. Roy. Soc No. 329, January, February, March 1711, reprinted with a commentary by O. Hald. International Statistical Review 52: 229–62. [Google Scholar]

- De Molina, Luis. 1597. Tratado sobre los cambios. Cuenca; reprint: Instituto de Estudios Fiscales, Madrid, ICI, 1990; translation: “Treatise on Money”, Translation by Jeannine Emery, with Introduction by Francisco Gómez Camacho. Journal of Markets & Morality 8: 161–323. [Google Scholar]

- De Soto, Jesús Huerta. 1996. New Light on the Prehistory of the Theory of Banming and the School of Salamanca. The Review of Austrian Economics 9: 59–81. [Google Scholar] [CrossRef]

- De Vries, Jan, and Ad van der Woude. 1997. The First Modern Economy: Success, Failure, and Perseverance of the Dutch Economy, 1500–1815. Cambridge: Cambridge University Press. [Google Scholar]

- Dotson, John E. 1994. Merchant Culture in Fourteenth Century Venice: The Zibaldone da Canal. Tempe: Medieval & Renaissance Texts & Studies, Center for Medieval & Early Renaissance Studies. [Google Scholar]

- Dotson, John E. 2002. Fourteenth Century Merchant Manuals and Merchant Culture. In Merchant’s Books and Mercantile Pratiche from the Late Middle Ages to the Beginning of the 20th Century. Edited by Markus A. Denzel, Jean Claude Hocquet and Harald Witthöft. Stuttgart: Franz Steiner, vol. 163, pp. 75–88. [Google Scholar]

- Douglas, Mary, and Aaron Wildavsky. 1982. Risk and Culture: An Essay on the Selection of Technical and Environmental Dangers. Berkeley: University of California Press. [Google Scholar]

- Thompson, Earl A. 2007. The tulipmania: Fact or artifact? Public Choice 130: 99–114. [Google Scholar] [CrossRef]

- Efing, Matthias, Harald Hau, Patrick Kampkötter, and Johannes Steinbrecher. 2015. Incentive pay and bank risk-taking: Evidence from Austrian, German, and Swiss banks. Journal of International Economics 96: 123–40. [Google Scholar] [CrossRef]

- Elliott, E. Donald. 1983. Risk and Culture: An Essay on the Selection of Technical and Environmental Dangers. Faculty Scholarship Series. Paper 2192. Available online: http://digitalcommons.law.yale.edu/fss_papers/2192 (accessed on 3 October 2012).

- Fouquet, Gerhard. 2010. Netzwerke im internationalen Handel des Mittelalters—eine Einleitung. In Netzwerke im Europäischen Handel des Mittelalters, Vorträge und Forschungen. Edited by Gerhard Fouquet and Hans-Jörg Gilomen. Ostfildern: Jan Thorbecke Verlag, vol. 72, pp. 9–20. (In German) [Google Scholar]

- Financial Stability Board (FSB). 2014. Guidance on Supervisory Interaction with Financial Institutions on Risk Culture. Available online: www.financialstabilityboard.org/wp-content/uploads/140407.pdf (accessed on 3 October 2012).

- Garber, Peter M. 1989. Tulipmania. Journal of Political Economy 97: 535–60. [Google Scholar] [CrossRef]

- Haldane, Andrew. 2012. Tails of the unexpected. Speech Given at “The Credit Crisis Five Years On: Unpacking the Crisis” Conference, University of Edinburgh Business School, June 8–9; Available online: www.bankofengland.co.uk/ (assessed on 28 October 2012).

- Jonas, Hans. 1979. Das Prinzip Verantwortung. Versuch einer Ethik für die Technologische Zivilisation. Frankfurt: Insel Verlag. (In German) [Google Scholar]

- Jones, David. 2006. The Bankers of Puteoli: Finance, Trade and Industry in the Roman World. Gloucestershire: Tempus Publishing Ltd. [Google Scholar]

- Kahan, Dan M. 2012. Cultural Cognition as a Conception of the Cultural Theory of Risk. Handbook of Risk Theory. New York: Springer, pp. 725–59. [Google Scholar]

- Kahneman, Daniel, and Dan Lovallo. 1993. Timid Choices and Bold Forecasts: A Cognitive Perspective on Risk Taking. Management Science 39: 17–33. [Google Scholar] [CrossRef]

- Kallioinen, Mika. 2012. The Bonds of Trade: Economic Institutions in Pre-Modern Northern Europe. Cambridge: Cambridge Scholars Publishing, Newcastle upon Tyne. [Google Scholar]

- Keynes, John Maynard. 1921. Treatise on Probability. London: Macmillan & Co. [Google Scholar]

- King, Mervyn. 2016. The End of Alchemy: Money, Banking, and the Future of the Global Economy. London: Little, Brown Book Group. [Google Scholar]

- Knight, Frank H. 1921. Risk, Uncertainty and Profit. New York: Harper. [Google Scholar]

- Letsios, Dimitrios G. 1996. Νόμος ‘Ροδίων Ναυτικός—Das Seegesetz der Rhodier—Untersuchungen zu Seerecht und Handelsschiffahrt in Byzanz. Zeitschrift der Savigny-Stiftung für Rechtsgeschichte: Romanistische Abteilung 117: 624ff. [Google Scholar]

- Luhmann, Niklas. 1968. Vertrauen. Ein Mechanismus der Reduktion sozialer Komplexität. Stuttgart: Enke, (English version: Trust and Power, Wiley, 1979). [Google Scholar]

- Luhmann, Niklas. 1991. Soziologie des Risikos. Berlin: De Gruyter. [Google Scholar]

- Luhmann, Niklas. 1993. Risk: A Sociological Theory. Berlin and New York: De Gruyter. [Google Scholar]

- Madden, Thomas F. 2012. Venice: A New History. London: Viking/Penguin. [Google Scholar]

- Mandelbrot, Benoit. 2004. The (Mis)Behavior of Markets: A Fractal View of Risk, Ruin, and Reward. New York: Basic Books. [Google Scholar]

- Mandeville, Bernard. 1705. The Fable of The Bees: Or, Private Vices, Public Benefits (first published as the poem "The Grumbling Hive: Or, Knaves turn’d Honest" in 1705 and as book in 1714). Available online: hppt://pedagogie.ac-toulouse.fr/philosphie/textesdephilosophes.htm#mandeville (accessed on 29 July 2017).

- March, James G. 1994. Primer on Decision Making: How Decisions Happen. New York: The Free Press. [Google Scholar]

- March, James G., and Zur Shapira. 1987. Managerial Perspectives on Risk and Risk Taking. Management Science 33: 1404–18. [Google Scholar] [CrossRef]

- Marković, Dimitrije, and Claudius Gros. 2014. Power laws and self-organized criticality in theory and nature. Physics Reports 536: 41–74. [Google Scholar] [CrossRef]

- Martynova, Natalya, Lev Ratnovski, and Razvan Vlahu. 2015. Bank Profitability and Risk-Taking, IMF Working Papers, No. 15/249. Washington, DC, USA: International Monetary Fund, November 25.

- Maschke, Erich. 1984. Das Berufsbewußtsein des mittelalterlichen Fernkaufmanns. In Die Stadt des Mittelalters, Vol. 3 (Wirtschaft und Gesellschaft). Darmstadt: Wissenschaftliche Buchgesellschaft. (In German) [Google Scholar]

- McKenzie, Lionel W. 1959. On the Existence of General Equilibrium for a Competitive Economy. Econometrica 27: 54–71. [Google Scholar] [CrossRef]

- McChrystal, Stanley. 2016. Team of Teams: New Rules of Engagement for a Complex World. London: Penguin. [Google Scholar]

- McCormick, Roger, and Chris Stears. 2016. Conduct Costs Project Report 2016. CCP Research Foundation CIC. Available online: conduct-costs-project-report-2016.pdf (assessed on 29 July 2017).

- Mehr, Ralf. 2008. Societas und Universitas: Römischrechtliche Institute im Unternehmensgesellschaftsrecht vor 1800. Köln and Weimar: Böhlau Verlag. (In German) [Google Scholar]

- Milkau, Udo. 2011. Systemic Risk Seen from the Perspective of Physics. The Capco Institute Journal of Financial Transformation 31: 73–82. [Google Scholar]

- Milkau, Udo. 2013. Adequate Communication about Operational Risk in the Business Line. The Journal of Operational Risk 8: 35–57. [Google Scholar] [CrossRef]

- Milkau, Udo, Frank Neumann, and Jürgen Bott. 2016. Development of Distributed Ledger Technology and a First Operational Risk Assessment. The Capco Institute Journal of Financial Transformation 44: 20–30. [Google Scholar]

- Moretti, Franco, and Dominique Pestre. 2015. Bankspeak: The Language of World Bank Reports, 1946–2012. Stanford: Pamphlets of the Stanford Literary Lab, No. 9. March. [Google Scholar]

- Münkler, Herfried. 2010. Strategien der Sicherung: Welten der Sicherheit und Kulturen des Risikos. In Sicherheit und Risiko—Über den Umgang mit Gefahr im 21. Jahrhundert. Edited by Herfried Münkler, Matthias Bohlender and Sabine Meurer. Bielefeld: Transcript Verlag. [Google Scholar]

- Nehlsen-von Stryk, Karin. 1986. Die venezianische Seeversicherung im 15. Jahrhundert. Münchener Universitätsschriften, Juristische Fakultät: Abhandlungen zur rechtswissenschaftlichen Grundlagenforschung 64: 239. [Google Scholar]

- Oltedal, Sigve, Bjørg-Elin Moen, Hroar Klempe, and Torbjørn Rundmo. 2004. Explaining risk perception. An evaluation of cultural theory. Trondheim: Norwegian University of Science and Technology 85: 1–33. [Google Scholar]

- Pacioli, Luca. 1494. The Rules of Double-Entry Bookkeeping—Particularis de Computis et Scriptuis. (Origianallxy Published as the 11th Treatise of Section Nine of the Summa de Arithmetica, Geometria, Proportioni et Proportionalia. Venice 1494). Leipzig: IICPA Publications. [Google Scholar]

- Poincaré, Henri. 1908. Science et Méthode. Paris: Flammarion. [Google Scholar]

- Popper, Karl R. 1991. Alles Leben ist Problemlösen (All Life is Problem Solving). In Karl R.Popper. Alles Leben ist Problemlösen. Munich and Berlin: Piper. [Google Scholar]

- Pryor, John H. 1977. The Origins of the Commenda Contract. Speculum 52: 5–37. [Google Scholar] [CrossRef]

- Puga, Diego, and Daniel Trefler. 2014. International Trade and Institutional Change: Medieval Venice's Response to Globalization. The Quarterly Journal of Economics 2014: 753–821. [Google Scholar] [CrossRef]

- Purcell, Nicholas. 1995. Literate games: Roman society and the game of alea. In Studies in Ancient Greek and Roman Society. Edited by Robin Osborne. Cambridge: Cambridge University Press. [Google Scholar]

- Purdy, Grant. 2010. ISO 31000:2009—Setting a New Standard for Risk Management. Risk Analysis 30: 881–86. [Google Scholar] [CrossRef] [PubMed]

- Reinhart, Carmen M., and Kenneth S. Rogoff. 2009. Time Is Different: Eight Centuries of Financial Folly. Princeton: Princeton University Press. [Google Scholar]

- Renn, Ortwin, Andreas Klinke, and Marjolein van Asselt. 2011. Coping with Complexity, Uncertainty and Ambiguity in Risk Governance: A Synthesis. AMBIO 40: 231–46. [Google Scholar] [CrossRef] [PubMed]

- Rochlin, Gene I., Todd R. La Porte, and Karlene H. Roberts. 1987. The Self-Designing High-Reliability Organization: Aircraft Carrier Flight Operations at Sea. Naval War College Review, issue Autumn 1987. Available online: www.projectwhitehorse.com/pdfs/Self_Designing_-_LaPort.pdf (accessed on 20 September 2017).

- Saunders, Anthony, Elizabeth Strock, and Nickolaos G. Travlos. 1990. Ownership Structure, Deregulation, and Bank Risk Taking. The Journal of Finance 45: 643–54. [Google Scholar] [CrossRef]

- Schachermayer, Walter. 2016. Mathematics and Finance. In Mathematics and Society, 7th European Congress of Mathematics & Congress of the European Mathematical Society. Edited by Wolfgang König. July 18–22, Zürich: European Mathematical Society Publishing House, pp. 37–50. [Google Scholar]

- Scheller, Benjamin. 2017. The Birth of Risk. Contingency and Mercantile Practice in Mediterrenean Sea Trade in the High and Later middle Ages. Historische Zeitschrift 304: 305–31. [Google Scholar]

- Shapira, Roy, and Luigi Zingales. 2017. Is Pollution Value-Maximizing? The DuPont Case. Stigler Center for the Study of the Economy and the State, University of Chicago Booth School of Business New Working Paper Series No. 13. , September. Available online: research.chicagobooth.edu/-/media/research/stigler/pdfs/workingpapers/13ispollutionvaluemaximizingsep2017.pdf (accessed on 29 October 2017).

- Simmel, Georg. 1908. Soziologie—Untersuchungen über die Formen der Vergesellschaftung. Berlin: Duncker & Humblot, Kapitel V: Das Geheimnis und die geheime Gesellschaft. pp. 256–304. Available online: http://socio.ch/sim/soziologie/soz_5.htm (accessed on 7 November 2017).

- Sinn, Hans-Werner. 2003. Risk Taking, Limited Liability and the Competition of Bank Regulators. Finanzarchiv 59: 305–29. [Google Scholar] [CrossRef]

- Slovic, Paul. 2000. The Perception of Risk. New York: Earthscan. [Google Scholar]

- Spiegelhalter, David. 2011. Quantifying uncertainty. In Risk. Darwin College Lectures, No. 24. Edited by Layla Skinns, Michael Scott and Tony Cox. Cambridge: Cambridge University Press. [Google Scholar]

- Steinbrecher, Ira (BaFin). 2015. Risk culture: Requirements of responsible corporate governance. Available online: www.bafin.de/SharedDocs/Veroeffentlichungen/EN/Fachartikel/2015/ fa_bj_1508_risikokultur_en.html (accessed on 28 August 2017).

- Taylor, Frederick Winslow. 1911. Principles of Scientific Management. New York: Harper & Brother. [Google Scholar]

- Temin, Peter. 2012. Roman Market Economy. Princeton Economic History of the Western World. Princeton: University Press Group Ltd. [Google Scholar]

- U.S. Marine Corps. 1997. “Warfighting”, Fleet Marine Force Manual. Available online: www.dtic.mil/doctrine/jel/service_pubs/mcdp1.pdf (accessed on 25 August 2012).

- van der Linden, Sander. 2016. A Conceptual Critique of the Cultural Cognition—Thesis. Science Communication 38: 128–38. [Google Scholar] [CrossRef]

- von Hayek, Friedrich A. 1967. The Theory of Complex Phenomena. Studies in Philosophy, Politics and Economics. London: Routledge & Kegan Paul, pp. 22–42. [Google Scholar]

- von Hayek, Friedrich A. 1944. The Road to Serfdom. London: George Routledge & Sons. [Google Scholar]

- von Hayek, Friedrich A. 1982. Law, Legislation and Liberty. London: Routledge and Kegan Paul. [Google Scholar]

- von Petersdorff, Winand. 2017. Warum gibt es in Texas so wenig Deiche. FAZ, September 19. [Google Scholar]

- Walker, Brian, and David Salt. 2012. Resilience Practice. Washington: Island Press. [Google Scholar]

- Walras, Marie-Esprit-Léon. 1874. Éléments D’économie Politique Pure. (English Traslation as: Elements of Pure Economics by William Jaffé). American Economic Association and the Royal Economic Society. Toronto: Thomas Nelson & Sons. [Google Scholar]

- Wang, Bo, Stephen M. Anthony, Sung Chul Baea, and Steve Granick. 2009. Anomalous yet Brownian. Proceedings of the National Academy of Sciences of the United States of America 106: 15160–64. [Google Scholar] [CrossRef] [PubMed]

- Wilhelm, Eva-Maria. 2013. Italianismen des Handel sim Deutschen und Französischen—Wege des frühneuzeitlichen Sprachkontakts. Berlin and Boston: Walter de Gruyter. [Google Scholar]

- Ziegler, Uwe. 1994. Die Hanse. Bern, Munich and Vienna: Scherz Verlag. [Google Scholar]

| 1 | A similar idea—that risk is perceived and/or prioritised aligned to the social network somebody is connected to—is the starting point of the so-called “cultural theory of risk” set forth by Douglas and Wildavsky (1982). Unfortunately, the further development of this approach focussed on how political discussion of and public disagreement about environmental risks (from pollution to nuclear power) depended on social groups in the U.S. with certain worldviews. Therefore, this approach has received critique from the beginning (e.g., Elliott 1983; Oltedal et al. 2004; van der Linden 2016), but was continued in the idea about “Cultural Cognition” (Kahan 2012). Another approach was given by Slovic (2000) with his work on “The Perception of Risk”, which accessed social and political risk taking. |

| 2 | |

| 3 | Translation by the author: “Cultures of risk dare to do more in handling dangerous and perilous situations compared to worlds of safety. Cultures of risk are designed to see an opportunity together with some danger. [...]. Worlds of safety are based on the implicit promise of a ‘safe world’ and promote experiences to be measured to. In the course of this, the fact emerges with large regularity that such “worlds of safety” cannot fulfil the promises”. |

| 4 | As will be discussed later in this paper, the activities of mediaeval merchants created merchant banking and merchant banking developed into financial services. |

| 5 | The notion “governance” first showed up in the 1980s according to Renn et al. (2011). A recent study by Moretti and Pestre (2015) for the use of “governance” in World Bank Reports between 1946 and 2012 showed no use before 1990, but [quote]: “then increased its presence to the point that it is now as frequent as ‘food’, ten times more than ‘law’, and a hundred times more frequent than ‘politics’”. |

| 6 | In an unpublished working paper (see Cohn et al. 2016), Alain Cohn, Michel Maréchal and Christian Zünd conducted nation-wide field experiments in 30 countries and approximately 250 cities around the globe to collect a behavioural measure of civic honesty. They found a significant correlation between civic honesty and economic prosperity. Additionally, civic honesty correlated positively with trust in the society. |

| 7 | Nevertheless, criminal behaviour and prosecution can fall apart: The Conduct Costs Project Report 2016 (McCormick and Stears 2016) for the banks with highest conduct costs reported a grand total of GBP bn 252 for 2011–2015 and (one year overlapping) GBP bn 197 for 2008–2012, which roughly results in “annual conduct costs” of GBP bn 40 over one decade. A lion’s share of GBP bn 11 p.a. comes from fines to Bank of America according to this report. A majority of those fines were to settle allegations for selling “toxic” mortgages to investors. This legacy came from the acquisition of Countrywide, the US largest mortgage lender, by Bank of America in 2008—in the high noon of the subprime crisis to save Countrywide from default, i.e., to stabilize the financial system in the US. Would any bank do the same again? |

| 8 | Other terms were used in parallel depending from region to region for “risk” in the Medieval Germany: for example, “aresche” and “wagnis” in Southern Germany or “aventiure”/”eventhure” in the Hanseatic League (see Maschke 1984 and references therein). |

| 9 | Parallel types of contracts for cooperation were: (i) the “Wedderlegginge” developed in the 13th century in the Hanseatic League (Mehr 2008), as well as the ‘isqa developed by Jewish merchants and the qirād developed by Muslim merchants (Pryor 1977). The same challenge to “manage” risk in long-distance trade resulted in the same principle solutions. |

| 10 | “Piui rixego e piui prexio” as written in Venice 1457 (Nehlsen-von Stryk 1986). |

| 11 | A similar but also different development was the “Hanse” (Hanseatic League, from the 12th to the 16th century with some later survival). Different to the Italian merchant cities, the Hanse started with cross-country (legal) contracts—sponsored by Henry the Lion (1129/1130 or 1133/1135 to 1195)—with Gotland (1161), Sweden (1174) Novgorod (1189). |

| 12 | This was a different “business“ culture compared to the conclusion of D’Aveni (1998), which he made concerning so-called “hypercompetition” between US and Japanese companies in the late 20th century [quote]: “Clearly, in business, chivalry is dead. Western firms, having begun the process of becoming lean, must now become mean.” |

| 13 | Even keeping money in vaults of banks could have been very risky, as documented in the case of confiscation of precious metals from vaults of banks in Seville by Charles V (Carlos V) in 1545 (Caranda 1987 and De Soto 1996). |