Evaluating Policy Frameworks and Their Role in the Sustainable Growth of Distributed Photovoltaic Generation

Abstract

:1. Introduction

2. Methodology Framework

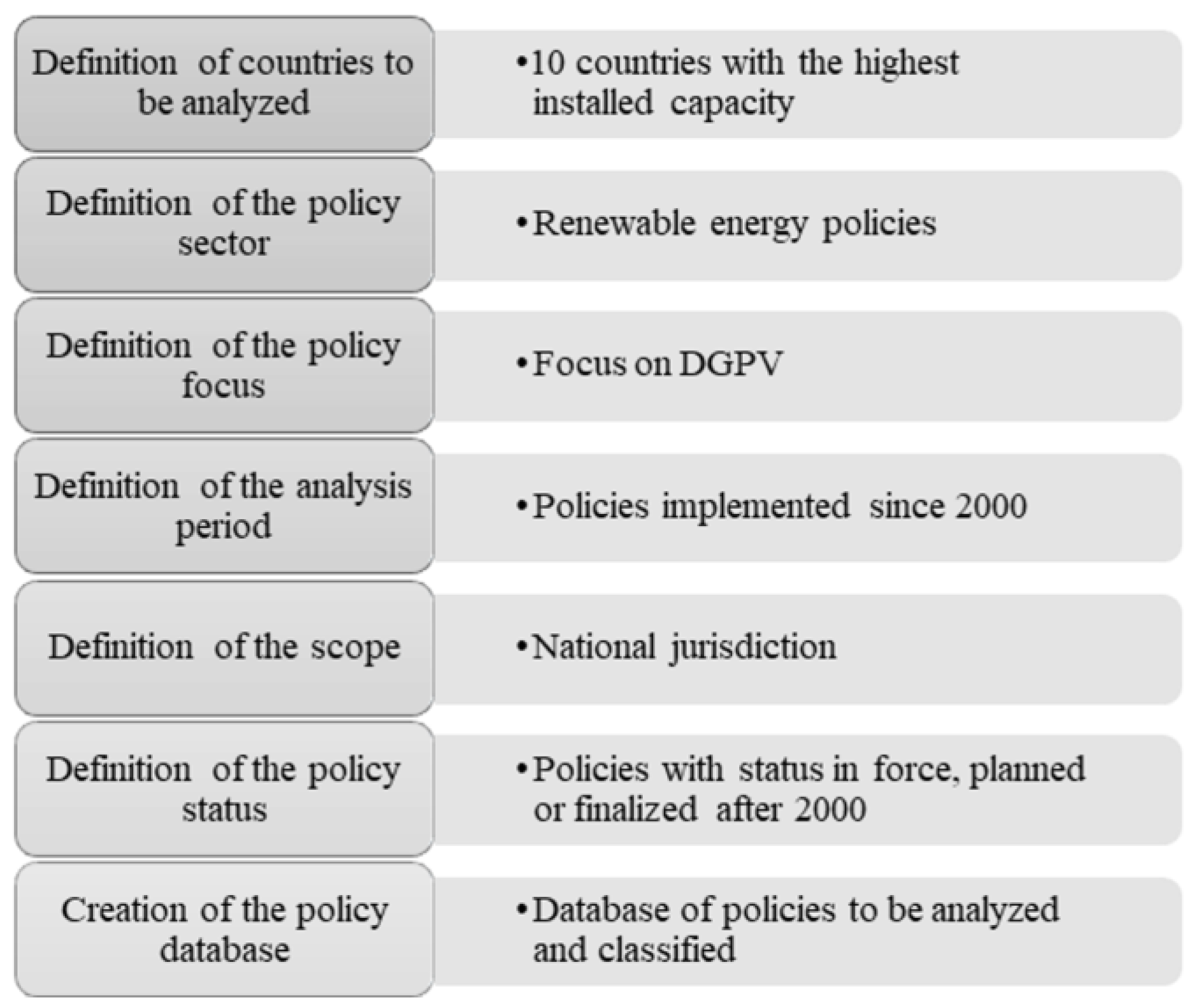

2.1. Stage One: Establishing the Analytical Framework for Energy Policy Evaluation

2.2. Methodological Approach for Stage Two: Assessing the Impacts of Selected Policies

3. Results and Discussion

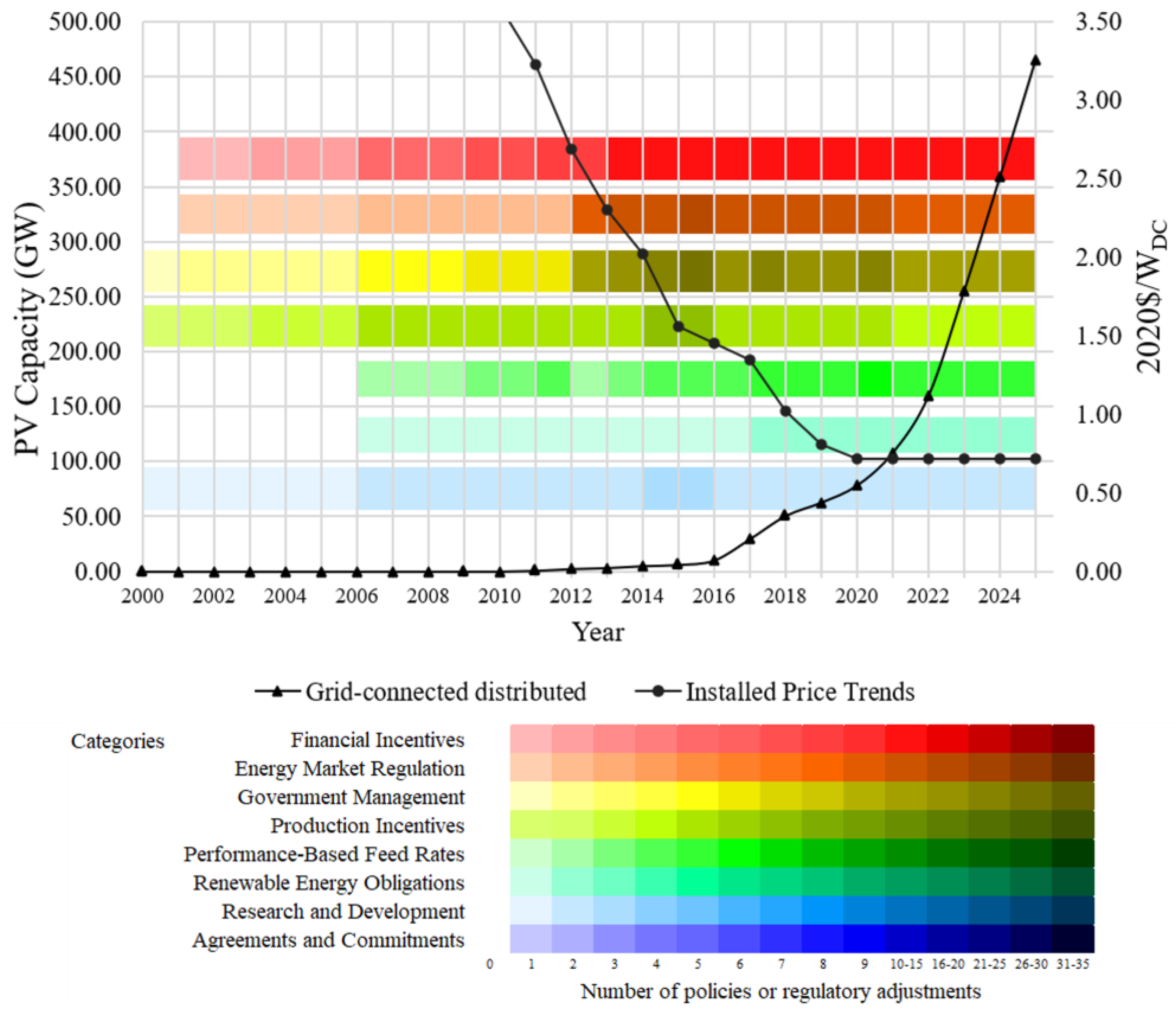

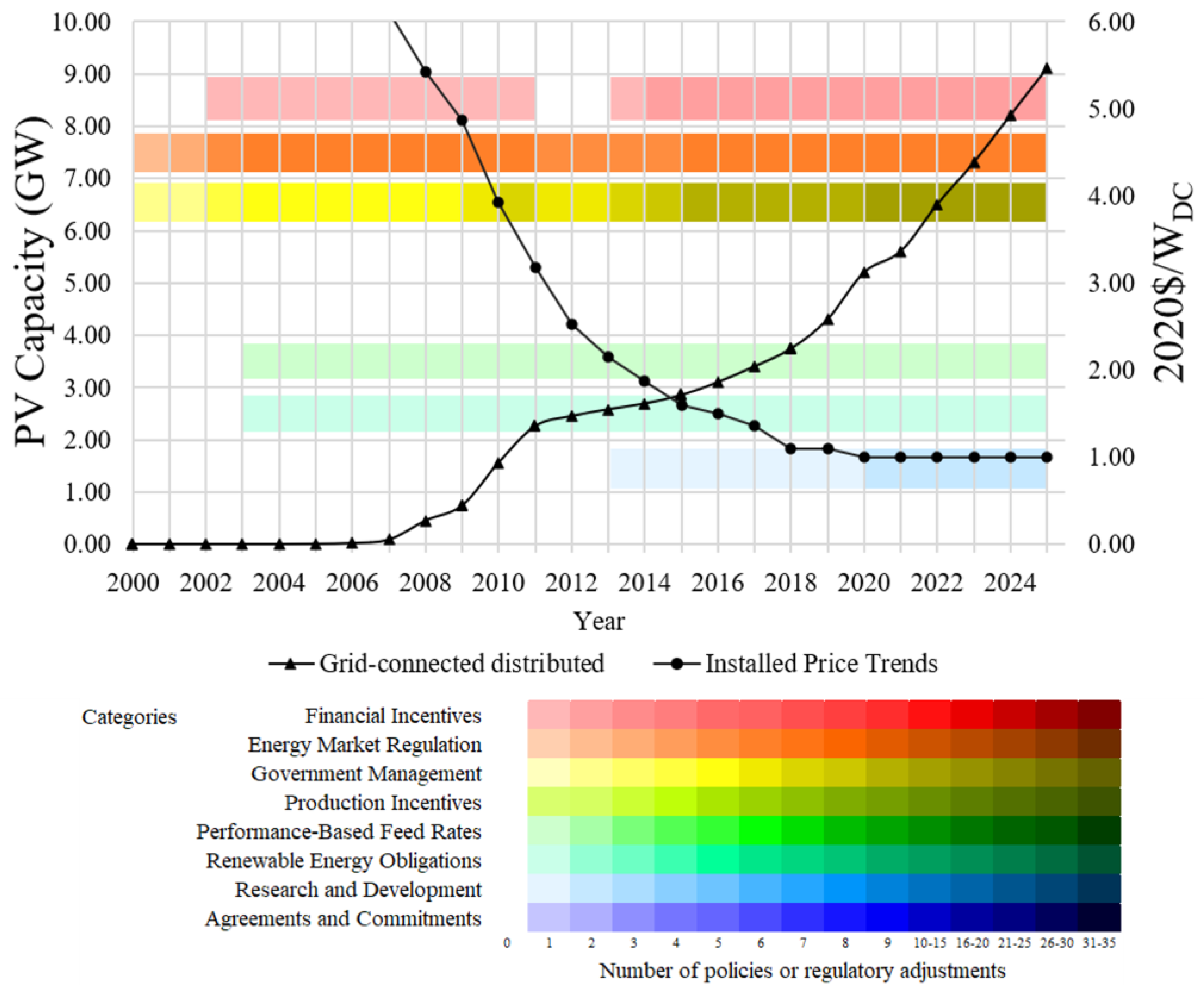

3.1. Mapping Policy Landscapes: Unveiling Categories, Trends, and Country-Specific Applications

3.2. Examining the Drivers of Distributed Solar: A Historical Analysis of Top 10 DGPV Leaders

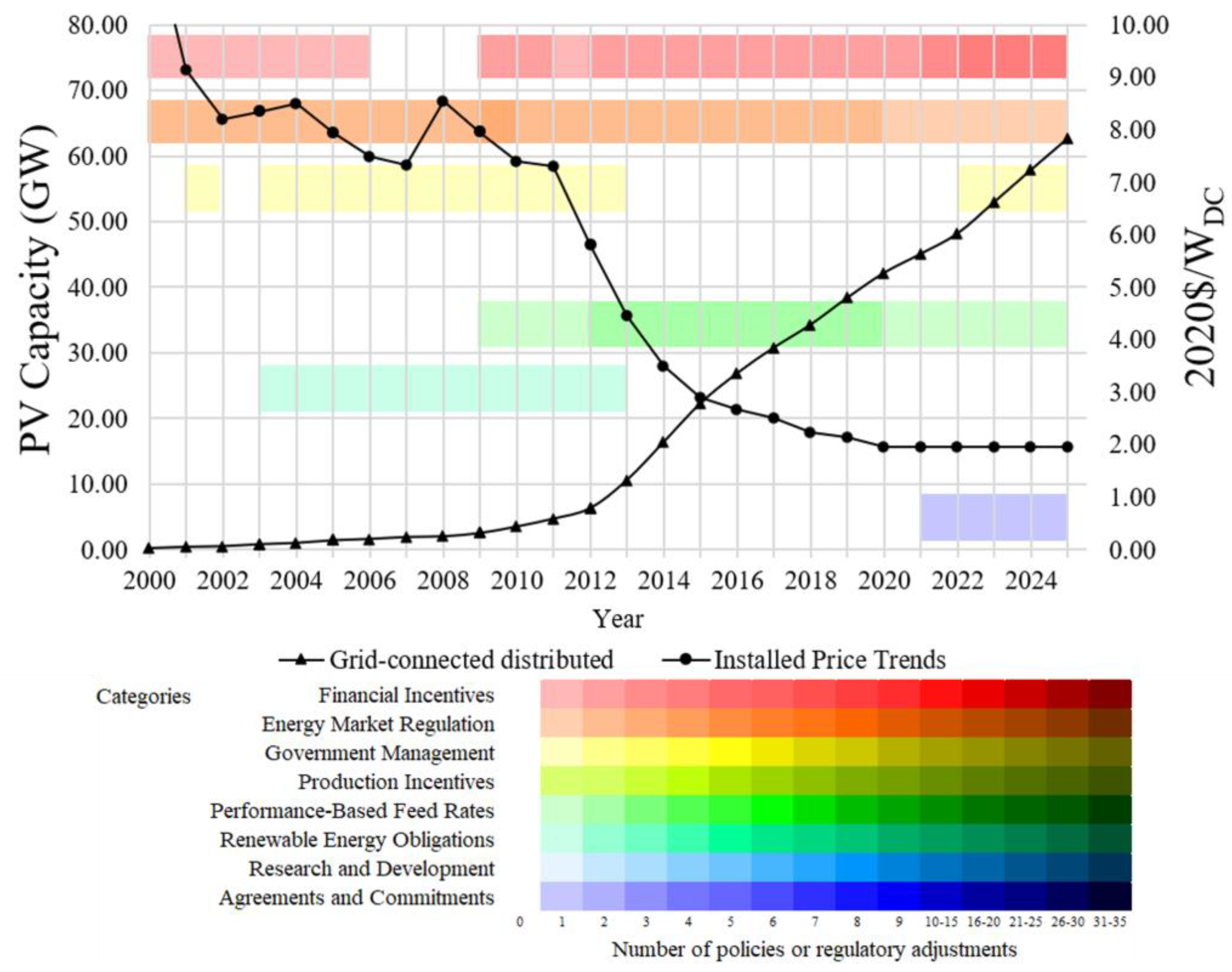

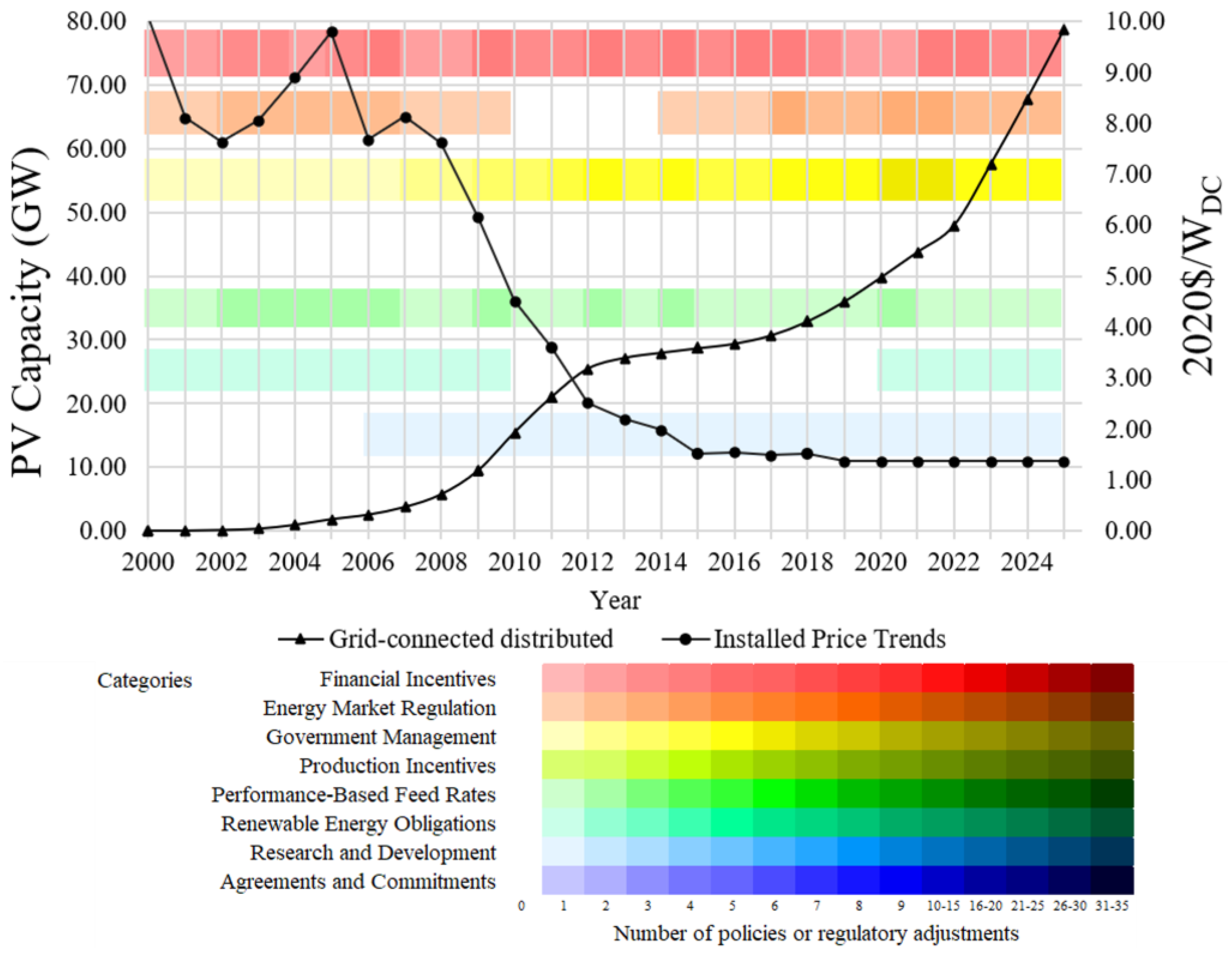

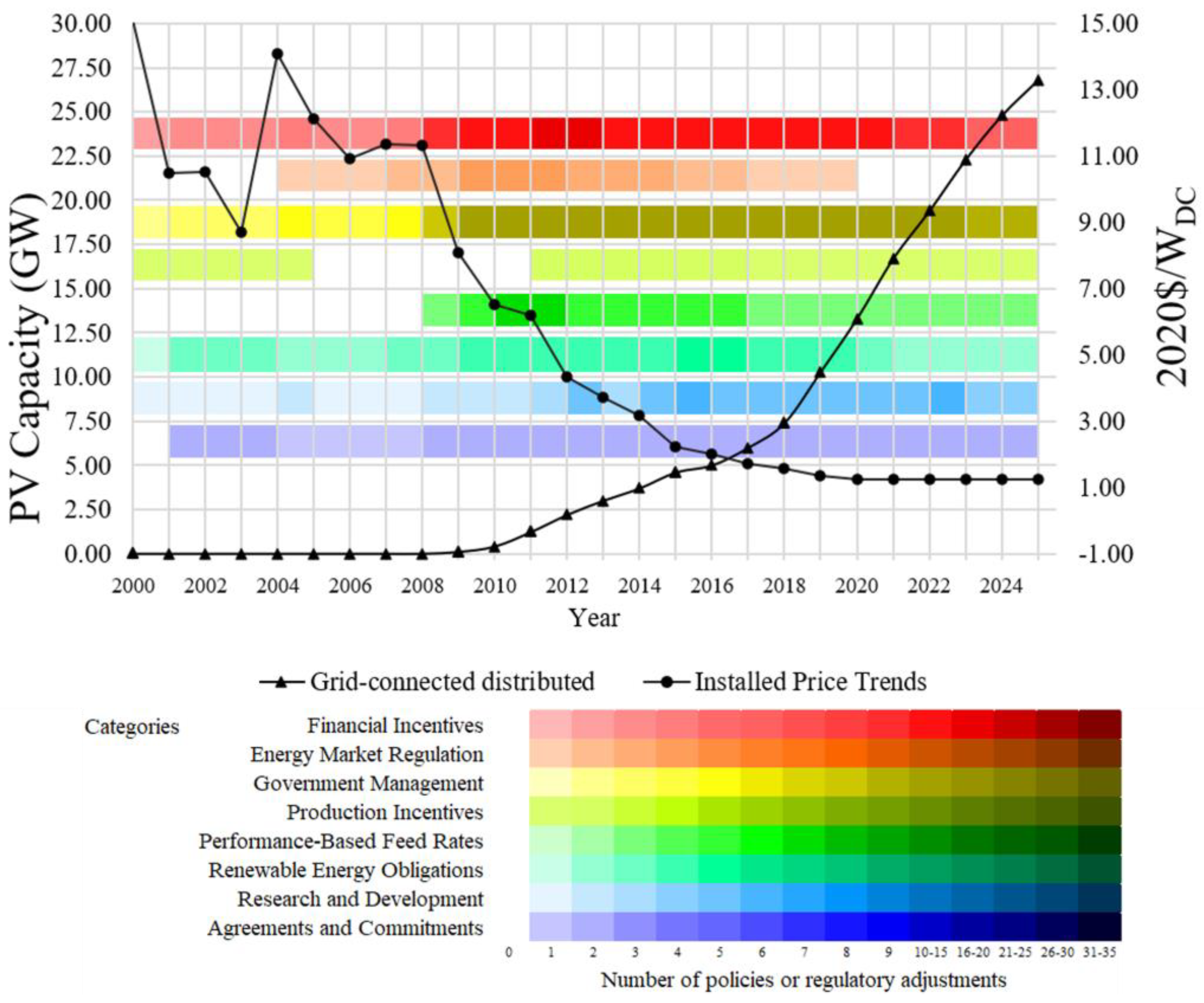

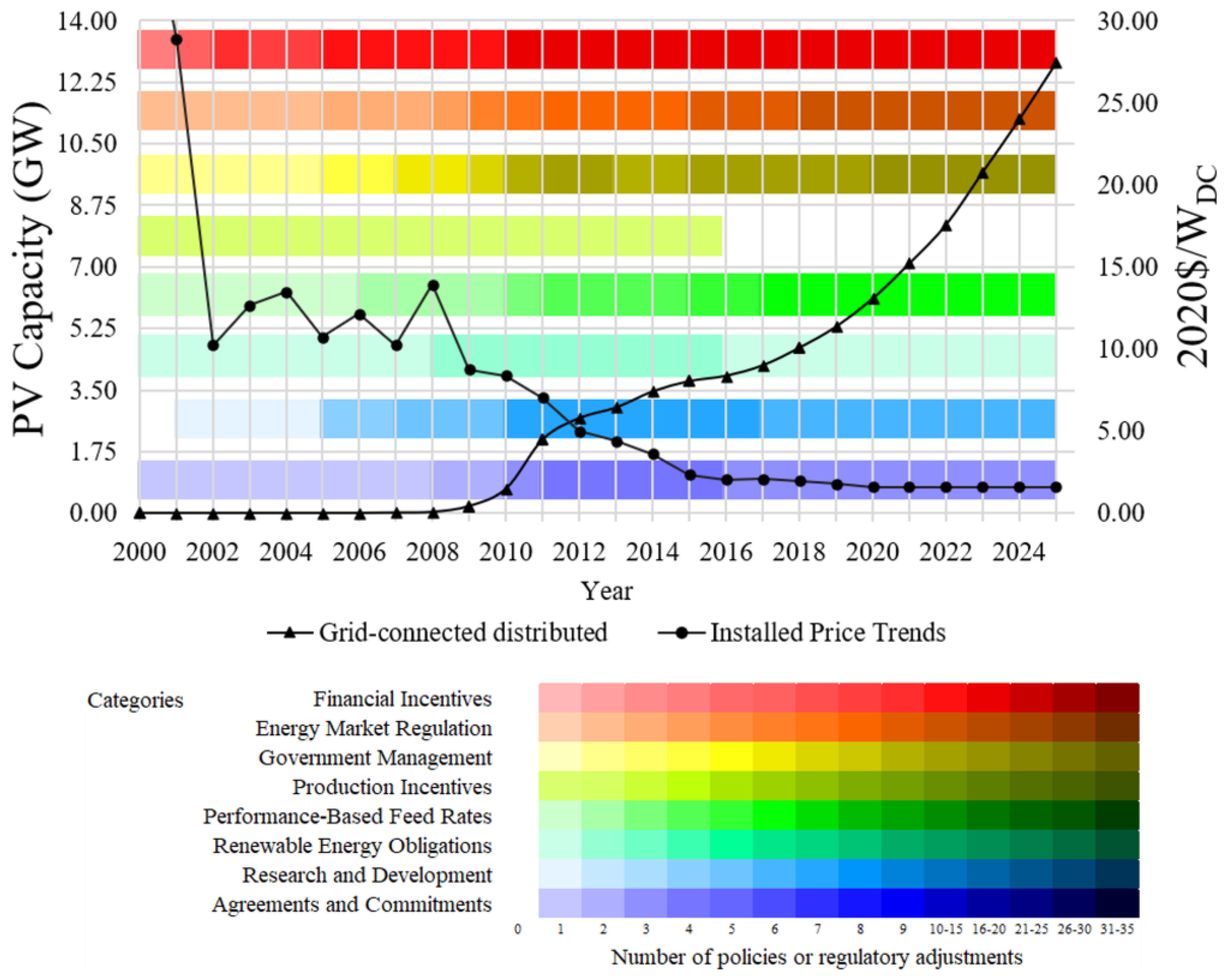

3.2.1. China

3.2.2. Japan

3.2.3. Germany

3.2.4. USA

3.2.5. Italy

3.2.6. Australia

3.2.7. Netherlands

3.2.8. India

3.2.9. France

3.2.10. Belgium

3.3. Mapping Renewable Energy Policies to Key Stakeholder Incentives

3.3.1. Prosumers

3.3.2. Integrators

3.3.3. Equipment and Component Manufacturers

3.3.4. Utilities

3.3.5. Research Institutions

3.4. Examining Policy Mechanisms Across Renewable Energy Maturity Stages

3.5. Aligning DGPV Policy Strategies with Socioeconomic Development

3.6. Exploring the Impact of Electricity Sector Scenarios on DGPV Incentive Mechanisms

4. Discussion and Policy Implications

5. Conclusions

Author Contributions

Funding

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- UNFCCC Kyoto Protocol—Targets for the First Commitment Period. Available online: https://unfccc.int/process-and-meetings/the-kyoto-protocol/what-is-the-kyoto-protocol/kyoto-protocol-targets-for-the-first-commitment-period (accessed on 20 September 2023).

- Song, X.; Wang, P. Effectiveness of Carbon Emissions Trading and Renewable Energy Portfolio Standards in the Chinese Provincial and Coupled Electricity Markets. Util. Policy 2023, 84, 101622. [Google Scholar] [CrossRef]

- Pichou, M.; Dussartre, V.; Lâasri, M.; Keppler, J.H. The Value of Distributed Flexibility for Reducing Generation and Network Reinforcement Costs. Util Policy 2023, 82, 101565. [Google Scholar] [CrossRef]

- Meflah, A.; Chekired, F.; Drir, N.; Canale, L. Accurate Method for Solar Power Generation Estimation for Different PV (Photovoltaic Panels) Technologies. Resources 2024, 13, 166. [Google Scholar] [CrossRef]

- IEA-PVPS. Trends in Photovoltaic Applications 2024, 1st ed.; International Energy Agency: Redfern, Australia, 2024; pp. 1–104. [Google Scholar]

- McGreevy, D.M.; MacDougall, C.; Fisher, D.M.; Henley, M.; Baum, F. Expediting a Renewable Energy Transition in a Privatised Market via Public Policy: The Case of South Australia 2004-18. Energy Policy 2021, 148, 111940. [Google Scholar] [CrossRef]

- Heilmann, E. The Impact of Transparency Policies on Local Flexibility Markets in Electric Distribution Networks. Util Policy 2023, 83, 101592. [Google Scholar] [CrossRef]

- IEA-PVPS. Trends in Photovoltaic Applications 2023, 1st ed.; International Energy Agency: Redfern, Australia, 2023; pp. 1–96. [Google Scholar]

- IRENA. Renewable Power Generation Costs in 2020, 1st ed.; International Renewable Energy Agency: Abu Dhabi, United Arab Emirates, 2021; pp. 2–180. [Google Scholar]

- IRENA; IEA; REN21. Renewable Energy Policies in a Time of Transition, 1st ed.; International Renewable Energy Agency (IRENA), International Energy Agency (IEA), and Renewable Energy Policy Network for the 21st Century (REN21): Redfern, Australia, 2018; pp. 1–112. ISBN 9789292600617. [Google Scholar]

- Yetkiner, H.; Berk, I. Energy Intensity and Directed Fiscal Policy. Econ. Syst. 2023, 47, 101070. [Google Scholar] [CrossRef]

- Gunkel, P.A.; Bergaentzlé, C.M.; Keles, D.; Scheller, F.; Jacobsen, H.K. Grid Tariff Designs to Address Electrification and Their Allocative Impacts. Util Policy 2023, 85, 101676. [Google Scholar] [CrossRef]

- Liu, Y.; Dong, K.; Dong, X.; Taghizadeh-Hesary, F. Towards a Sustainable Electricity Industry in China: An Appraisal of the Efficacy of Environmental Policies. Util Policy 2024, 86, 101700. [Google Scholar] [CrossRef]

- Ding, L.; Zhang, Z.; Dai, Q.; Zhu, Y.; Shi, Y. Alternative Operational Modes for Chinese PV Poverty Alleviation Power Stations: Economic Impacts on Stakeholders. Util Policy 2023, 82, 101524. [Google Scholar] [CrossRef]

- Ali, A.; Shahid, M.; Qadir, S.A.; Islam, M.T.; Khan, M.W.; Ahmed, S. Solar PV End-of-Life Waste Re-cycling: An Assessment of Mechanical Recycling Methods and Proposed Hybrid Laser and High Voltage Pulse Crushing Method. Resources 2024, 13, 169. [Google Scholar] [CrossRef]

- IRENA. Policies and Regulations for Private Sector Renewable Energy Mini-Grids, 1st ed.; International Renewable Energy Agency: Abu Dhabi, United Arab Emirates, 2016; pp. 1–112. ISBN 9789295111455. [Google Scholar]

- Neves, D.; Scott, I.; Silva, C.A. Peer-to-Peer Energy Trading Potential: An Assessment for the Residential Sector under Different Technology and Tariff Availabilities. Energy 2020, 205, 118023. [Google Scholar] [CrossRef]

- Schaffer, L.M.; Bernauer, T. Explaining Government Choices for Promoting Renewable Energy. Energy Policy 2014, 68, 15–27. [Google Scholar] [CrossRef]

- Jain, P.; Bardhan, S. Sustainable Energy Deployment in Developing Countries: The Role of Composition of Energy Aid. Econ. Syst. 2024, 48, 101195. [Google Scholar] [CrossRef]

- IEA. Renewables 2022, 1st ed.; International Energy Agency: Paris, France, 2022; pp. 1–159. [Google Scholar]

- IEA. Renewables 2019, 1st ed.; International Energy Agency: Paris, France, 2019; pp. 1–204. [Google Scholar]

- Brown, A.; Bunyan, J. Valuation of Distributed Solar: A Qualitative View. Electr. J. 2014, 27, 1040–6190. [Google Scholar] [CrossRef]

- Mandelli, S.; Mereu, R. Distributed Generation for Access to Electricity: “Off-Main-Grid” Systems from Home-Based to Microgrid. In Renewable Energy for Unleashing Sustainable Development, 1st ed.; Colombo, E., Bologna, S., Masera, D., Eds.; Springer: Cham, Switzerland, 2013; pp. 75–97. ISBN 978-331900284-2/978-331900283-5. [Google Scholar] [CrossRef]

- Oprea, S.V.; Bâra, A. Generative Literature Analysis on the Rise of Prosumers and Their Influence on the Sustainable Energy Transition. Util Policy 2024, 90, 101799. [Google Scholar] [CrossRef]

- Baliozan, P.; Mourad, S.; Morse, D.; Kim, S.; Friedrich, L.; Preu, R. Photovoltaic Development Standardizing Based on Roadmaps and Technology Readiness Levels. In Proceedings of the European Photovoltaic Solar Energy Conference and Exhibition, Munich, Germany, 24 June 2016. [Google Scholar] [CrossRef]

- Fischer, M.; Woodhouse, M.; Baliozan, P. International Technology Roadmap for Photovoltaics (ITRPV)—2023 Results, 15th ed.; VDMA e. V. Photovoltaics Equipment, a Sector Group of EMINT: Frankfurt am Main, Germany, 2024; pp. 1–82. [Google Scholar]

- Zhao, Y.; Tang, K.K.; Wang, L. li Do Renewable Electricity Policies Promote Renewable Electricity Generation? Evidence from Panel Data. Energy Policy 2013, 62, 887–897. [Google Scholar] [CrossRef]

- Marques, A.C.; Fuinhas, J.A.; Manso, J.P. A Quantile Approach to Identify Factors Promoting Renewable Energy in European Countries. Environ. Resour. Econ. 2011, 49, 351–366. [Google Scholar] [CrossRef]

- IEA Policies Database Solar PV National. Available online: https://www.iea.org/policies?jurisdiction=National&technology%5B0%5D=Solar%20PV (accessed on 21 August 2023).

- Batlle, C. A Method for Allocating Renewable Energy Source Subsidies among Final Energy Consumers. Energy Policy 2011, 39, 2586–2595. [Google Scholar] [CrossRef]

- Altenburg, T.; Engelmeier, T. Boosting Solar Investment with Limited Subsidies: Rent Management and Policy Learning in India. Energy Policy 2013, 59, 866–874. [Google Scholar] [CrossRef]

- Mir-Artigues, P.; Del Río, P. Combining Tariffs, Investment Subsidies and Soft Loans in a Renewable Electricity Deployment Policy. Energy Policy 2014, 69, 430–442. [Google Scholar] [CrossRef]

- Schmidt, J.; Wehrle, S.; Rusbeh, R. A Reduction of Distribution Grid Fees by Combined PV and Battery Systems under Different Regulatory Schemes. In Proceedings of the International Conference on the European Energy Market, EEM 2016, Porto, Portugal, 6–9 June 2016. [Google Scholar]

- de Castro Vieira, S.; Tapia Carpio, L.G. The Economic Impact on Residential Fees Associated with the Expansion of Grid-Connected Solar Photovoltaic Generators in Brazil. Renew Energy 2020, 159, 1084–1098. [Google Scholar] [CrossRef]

- Gautier, A.; Hoet, B.; Jacqmin, J.; Van Driessche, S. Self-Consumption Choice of Residential PV Owners under Net-Metering. Energy Policy 2019, 128, 648–653. [Google Scholar] [CrossRef]

- Jonh, J.S. Breaking: California’s NEM 2.0 Decision Keeps Retail Rate for Rooftop Solar, Adds Time-of-Use. Available online: https://www.greentechmedia.com/articles/read/Californias-Net-Metering-2.0-Decision-Rooftop-Solar-to-Keep-Retail-Payme (accessed on 28 May 2020).

- Rehman, W.U.; Bhatti, A.R.; Awan, A.B.; Sajjad, I.A.; Khan, A.A.; Bo, R.; Haroon, S.S.; Amin, S.; Tlili, I.; Oboreh-Snapps, O. The Penetration of Renewable and Sustainable Energy in Asia: A State-of-the-Art Review on Net-Metering. IEEE Access 2020, 8, 170364–170388. [Google Scholar] [CrossRef]

- Singla, A.; Singh, K.; Yadav, V.K.; Padhy, N.P. Development of Distributed Solar Photovoltaic Energy Market in India. In Proceedings of the IEEE Power and Energy Society General Meeting 2015, Denver, CO, USA, 26–30 July 2015. [Google Scholar]

- Biresselioglu, M.E.; Nilsen, M.; Demir, M.H.; Røyrvik, J.; Koksvik, G. Examining the Barriers and Motivators Affecting European Decision-Makers in the Development of Smart and Green Energy Technologies. J. Clean. Prod. 2018, 198, 417–429. [Google Scholar] [CrossRef]

- Carfora, A.; Pansini, R.V.; Romano, A.A.; Scandurra, G. Renewable Energy Development and Green Public Policies Complementarities: The Case of Developed and Developing Countries. Renew. Energy 2018, 115, 741–749. [Google Scholar] [CrossRef]

- Noblet, C.L.; Teisl, M.F.; Evans, K.; Anderson, M.W.; McCoy, S.; Cervone, E. Public Preferences for Investments in Renewable Energy Production and Energy Efficiency. Energy Policy 2015, 87, 177–186. [Google Scholar] [CrossRef]

- Sharma, N.K.; Tiwari, P.K.; Sood, Y.R. Solar Energy in India: Strategies, Policies, Perspectives and Future Potential. Renew. Sustain. Energy Rev. 2012, 16, 933–941. [Google Scholar] [CrossRef]

- Qadir, S.A.; Al-Motairi, H.; Tahir, F.; Al-Fagih, L. Incentives and Strategies for Financing the Re-newable Energy Transition: A Review. Energy Rep. 2021, 7, 3590–3606. [Google Scholar] [CrossRef]

- Salleh, S.F.; Roslan, M.E.; Isa, A.M.; Nair, M.F.B.; Salleh, S.S. The Impact of Minimum Energy Performance Standards (MEPS) Regulation on Electricity Saving in Malaysia. In Proceedings of the IOP Conference Series: Materials Science and Engineering, Kuching, Malaysia, 7–8 August 2017; 2018; 341, p. 012022. [Google Scholar] [CrossRef]

- Sonnenschein, J.; Van Buskirk, R.; Richter, J.L.; Dalhammar, C. Minimum Energy Performance Standards for the 1.5 °C Target: An Effective Complement to Carbon Pricing. Energy Effic. 2019, 12, 387–402. [Google Scholar] [CrossRef]

- Liu, C.; Li, N.; Zha, D. On the Impact of FIT Policies on Renewable Energy Investment: Based on the Solar Power Support Policies in China’s Power Market. Renew. Energy 2016, 94, 251–267. [Google Scholar] [CrossRef]

- Campoccia, A.; Dusonchet, L.; Telaretti, E.; Zizzo, G. An Analysis of Feed’in Tariffs for Solar PV in Six Representative Countries of the European Union. Sol. Energy 2014, 107, 530–542. [Google Scholar] [CrossRef]

- Pyrgou, A.; Kylili, A.; Fokaides, P.A. The Future of the Feed-in Tariff (FiT) Scheme in Europe: The Case of Photovoltaics. Energy Policy 2016, 95, 94–102. [Google Scholar] [CrossRef]

- Leiren, M.D.; Reimer, I. Historical Institutionalist Perspective on the Shift from Feed-in Tariffs to-wards Auctioning in German Renewable Energy Policy. Energy Res. Soc. Sci. 2018, 43, 33–40. [Google Scholar] [CrossRef]

- Goodarzi, S.; Aflaki, S.; Masini, A. Optimal Feed-In Tariff Policies: The Impact of Market Structure and Technology Characteristics. Prod. Oper. Manag. 2019, 28, 1108–1128. [Google Scholar] [CrossRef]

- Shrimali, G.; Tirumalachetty, S. Renewable Energy Certificate Markets in India-A Review. Renew. Sustain. Energy Rev. 2013, 26, 702–716. [Google Scholar] [CrossRef]

- Pineda, S.; Bock, A. Renewable-Based Generation Expansion under a Green Certificate Market. Renew. Energy 2016, 91, 53–63. [Google Scholar] [CrossRef]

- Wiser, R.; Barbose, G.; Holt, E. Supporting Solar Power in Renewables Portfolio Standards: Experience from the United States. Energy Policy 2011, 39, 3894–3905. [Google Scholar] [CrossRef]

- Bird, L.; Chapman, C.; Logan, J.; Sumner, J.; Short, W. Evaluating Renewable Portfolio Standards and Carbon Cap Scenarios in the U.S. Electric Sector. Energy Policy 2011, 39, 2573–2585. [Google Scholar] [CrossRef]

- Jo, J.H.; Hayden, J.; Noll, S. Feasibility and Consumer Benefits of Meeting the Renewable Portfolio Standard for Distributed Generation in Illinois. Int. J. Sustain. Build. Technol. Urban Dev. 2014, 5, 171–182. [Google Scholar] [CrossRef]

- Ma, J.; Xu, T. Optimal Strategy of Investing in Solar Energy for Meeting the Renewable Portfolio Standard Requirement in America. J. Oper. Res. Soc. 2023, 74, 181–194. [Google Scholar] [CrossRef]

- Chang, K.; Xue, C.; Zhang, H.; Zeng, Y. The Effects of Green Fiscal Policies and R&D Investment on a Firm’s Market Value: New Evidence from the Renewable Energy Industry in China. Energy 2022, 251, 123953. [Google Scholar] [CrossRef]

- Yu, F.; Guo, Y.; Le-Nguyen, K.; Barnes, S.J.; Zhang, W. The Impact of Government Subsidies and En-terprises’ R&D Investment: A Panel Data Study from Renewable Energy in China. Energy Policy 2016, 89, 106–113. [Google Scholar] [CrossRef]

- Chen, Z.; Sun, P. Generic Technology R&D Strategies in Dual Competing Photovoltaic Supply Chains: A Social Welfare Maximization Perspective. Appl. Energy 2024, 353, 122089. [Google Scholar] [CrossRef]

- Emili, S.; Ceschin, F.; Harrison, D. Product–Service System Applied to Distributed Renewable Energy: A Classification System, 15 Archetypal Models and a Strategic Design Tool. Energy Sustain. Dev. 2016, 32, 71–98. [Google Scholar] [CrossRef]

- Funkhouser, E.; Blackburn, G.; Magee, C.; Rai, V. Business Model Innovations for Deploying Distrib-uted Generation: The Emerging Landscape of Community Solar in the U.S. Energy Res. Soc. Sci. 2015, 10, 90–101. [Google Scholar] [CrossRef]

- O’Shaughnessy, E.; Barbose, G.; Wiser, R.; Forrester, S.; Darghouth, N. The Impact of Policies and Business Models on Income Equity in Rooftop Solar Adoption. Nat. Energy 2021, 6, 84–91. [Google Scholar] [CrossRef]

- Strupeit, L.; Palm, A. Overcoming Barriers to Renewable Energy Diffusion: Business Models for Customer-Sited Solar Photovoltaics in Japan, Germany and the United States. J. Clean. Prod. 2016, 123, 124–136. [Google Scholar] [CrossRef]

- Walters, T.; Esterly, S.; Cox, S.; Reber, T.; Rai, N. Policies to Spur Energy Access: Volume 1 Engaging the Private Sector in Expanding Access To Electricity, 1st ed.; National Renewable Energy Laboratory: Golden, CO, USA, 2015; pp. 1–83. [Google Scholar]

- Barbose, G.; Darghouth, N.; O’Shaughnessy, E.; Forrester, S. Tracking the Sun—Pricing and Design Trends for Distributed Photovoltaic Systems in the United States, 1st ed.; Lawrence Berkeley National Laboratory: Berkeley, CA, USA, 2023; pp. 1–45. [Google Scholar]

- IEA-PVPS. Trends in Photovoltaic Applications 2022, 1st ed.; International Energy Agency: Redfern, Australia, 2022; pp. 1–88. [Google Scholar]

- Zhang, L.; Qin, Q.; Wei, Y.M. China’s Distributed Energy Policies: Evolution, Instruments and Recommendation. Energy Policy 2019, 125, 55–64. [Google Scholar] [CrossRef]

- Peng, H.; Liu, Y. A Comprehensive Analysis of Cleaner Production Policies in China. J. Clean. Prod. 2016, 135, 1138–1149. [Google Scholar] [CrossRef]

- Zhao, X.; Zeng, Y.; Zhao, D. Distributed Solar Photovoltaics in China: Policies and Economic Performance. Energy 2015, 88, 572–583. [Google Scholar] [CrossRef]

- Yang, F.f.; Zhao, X.-g. Policies and Economic Efficiency of China’s Distributed Photovoltaic and Energy Storage Industry. Energy 2018, 154, 221–230. [Google Scholar] [CrossRef]

- Gosens, J.; Kåberger, T.; Wang, Y. China’s next Renewable Energy Revolution: Goals and Mechanisms in the 13th Five Year Plan for Energy. Energy Sci. Eng. 2017, 5, 141–155. [Google Scholar] [CrossRef]

- IEA. Renewables 2023, 1st ed.; International Energy Agency: Paris, France, 2023; pp. 1–96. [Google Scholar]

- Muhammad-Sukki, F.; Abu-Bakar, S.H.; Munir, A.B.; Yasin, S.H.; Ramirez-Iniguez, R.; McMeekin, S.G.; Stewart, B.G.; Sarmah, N.; Mallick, T.K.; Rahim, R.A.; et al. Feed-in Tariff for Solar Photovoltaic: The Rise of Japan. Renew. Energy 2014, 68, 636–643. [Google Scholar] [CrossRef]

- Myojo, S.; Ohashi, H. Effects of Consumer Subsidies for Renewable Energy on Industry Growth and Social Welfare: The Case of Solar Photovoltaic Systems in Japan. J. Jpn. Int. Econ. 2018, 48, 55–67. [Google Scholar] [CrossRef]

- Lauber, V.; Jacobsson, S. The Politics and Economics of Constructing, Contesting and Restricting Socio-Political Space for Renewables—The German Renewable Energy Act. Environ. Innov. Soc. Transit. 2016, 18, 147–163. [Google Scholar] [CrossRef]

- Ruf, H. Limitations for the Feed-in Power of Residential Photovoltaic Systems in Germany – An Overview of the Regulatory Framework. Sol. Energy 2018, 159, 588–600. [Google Scholar] [CrossRef]

- Proudlove, A.; Daniel, K.; Lips, B.; Sarkisian, D.; Shrestha, A. The 50 States of Solar (Q2 2016 Policy Review): A Quarterly Look at America’s Fast-Evolving Distributed Solar Policy and Regulatory Conversation, 1st ed.; NC Clean Energy Technology Center: Raleigh, NC, USA, 2016; pp. 1–9. [Google Scholar]

- DSIRE Programs. Available online: https://programs.dsireusa.org/system/program?state=US (accessed on 15 September 2023).

- IEA Policies Database Energy System of United States. Available online: https://www.iea.org/policies?technology=Solar PV&topic=Renewable Energy&year=desc&country=United States (accessed on 15 September 2023).

- Sarrica, M.; Biddau, F.; Brondi, S.; Cottone, P.; Mazzara, B.M. A Multi-Scale Examination of Public Discourse on Energy Sustainability in Italy: Empirical Evidence and Policy Implications. Energy Policy 2018, 114, 444–454. [Google Scholar] [CrossRef]

- Schwarz, J. Italy: Summary, Support Schemes. Available online: http://www.res-legal.eu/search-by-country/italy/summary/c/italy/s/res-e/sum/152/lpid/151/ (accessed on 2 February 2025).

- Antonelli, M.; Desideri, U. The Doping Effect of Italian Feed-in Tariffs on the PV Market. Energy Policy 2014, 67, 583–594. [Google Scholar] [CrossRef]

- Li, H.X.; Edwards, D.J.; Hosseini, M.R.; Costin, G.P. A Review on Renewable Energy Transition in Australia: An Updated Depiction. J. Clean. Prod. 2020, 242, 118475. [Google Scholar] [CrossRef]

- van Rooijen, S.N.M.; van Wees, M.T. Green Electricity Policies in the Netherlands: An Analysis of Policy Decisions. Energy Policy 2006, 34, 60–71. [Google Scholar] [CrossRef]

- Climate Policy Database. Available online: https://www.climatepolicydatabase.org/policies?country%5B%5D=434&decision_date=&high_impact=All&jurisdiction%5B%5D=893&policy_type%5B%5D=907&keywords= (accessed on 16 September 2023).

- Anciaux, S. Netherlands: Summary, Support Schemes. Available online: http://www.res-legal.eu/search-by-country/netherlands/summary/c/netherlands/s/res-e/sum/172/lpid/171/ (accessed on 2 February 2025).

- Srivastava, S. Policy Framework for Developing and Promoting Decentralised Renewable Energy Livelihood Applications, 1st ed.; F. No. 32/18/2020-SPV Division Government of India Ministry of New & Renewable Energy: New Delhi, India, 2021; pp. 1–19. [Google Scholar]

- Shidore, S.; Busby, J.W. What Explains India’s Embrace of Solar? State-Led Energy Transition in a Developmental Polity. Energy Policy 2019, 129, 1179–1189. [Google Scholar] [CrossRef]

- IEA Jawaharlal Nehru National Solar Mission (Phase I, II and III). Available online: https://www.iea.org/policies/4916-jawaharlal-nehru-national-solar-mission-phase-i-ii-and-iii?technology=DistributedPV (accessed on 16 September 2023).

- Kapoor, T. National Solar Mission Target of Grid Connected Solar Power Projects, 1st ed.; F. No. 30/80/2014-15/NSM Government of India Ministry of New & Renewable Energy: New Delhi, India, 2015; pp. 1–6. [Google Scholar]

- Vidalic, H. France: Summary, Support Schemes. Available online: http://www.res-legal.eu/search-by-country/france/summary/c/france/s/res-e/sum/132/lpid/131/ (accessed on 2 February 2025).

- Wilkin, B. National Survey Report of PV Power Applications in Belgium 2018, 1st ed.; International Energy Agency: Redfern, Australia, 2018; pp. 1–20. [Google Scholar]

- Mihaylov, M.; Rădulescu, R.; Razo-Zapata, I.; Jurado, S.; Arco, L.; Avellana, N.; Nowé, A. Comparing Stakeholder Incentives across State-of-the-Art Renewable Support Mechanisms. Renew. Energy 2019, 131, 689–699. [Google Scholar] [CrossRef]

- Huijben, J.C.C.M.; Podoynitsyna, K.S.; Van Rijn, M.L.B.; Verbong, G.P.J. A Review of Governmental Support Instruments Channeling PV Market Growth in the Flanders Region of Belgium (2006–2013). Renew. Sustain. Energy Rev. 2016, 62, 1282–1290. [Google Scholar] [CrossRef]

- Yang, Q. Do Vertical Ecological Compensation Policies Promote Green Economic Development: A Case Study of the Transfer Payments Policy for China’s National Key Ecological Function Zones. Econ. Syst. 2023, 47, 101125. [Google Scholar] [CrossRef]

- Andresen, S.; Agrawala, S. Leaders, Pushers and Laggards in the Making of the Climate Regime. Glob. Environ. Change 2002, 12, 41–51. [Google Scholar] [CrossRef]

- Inderberg, T.H.J.; Tews, K.; Turner, B. Is There a Prosumer Pathway? Exploring Household Solar Energy Development in Germany, Norway, and the United Kingdom. Energy Res. Soc. Sci. 2018, 42, 258–269. [Google Scholar] [CrossRef]

- De Boeck, L.; Van Asch, S.; De Bruecker, P.; Audenaert, A. Comparison of Support Policies for Resi-dential Photovoltaic Systems in the Major EU Markets through Investment Profitability. Renew. Energy 2016, 87, 42–53. [Google Scholar] [CrossRef]

- Parag, Y.; Sovacool, B.K. Electricity Market Design for the Prosumer Era. Nat. Energy 2016, 1, 1–6. [Google Scholar] [CrossRef]

- Yu, J.J.; Tang, C.S.; Shenc, Z.J.M. Improving Consumer Welfare and Manufacturer Profit via Government Subsidy Programs: Subsidizing Consumers or Manufacturers? Manuf. Serv. Oper. Manag. 2018, 20, 752–766. [Google Scholar] [CrossRef]

- Jansson, P.M. Net Metering PV Distributed Resources Benefits All Stakeholders on PJM. In Proceedings of the SOLAR 2016-American Solar Energy Society National Solar Conference 2016 Proceedings, San Francisco, CA, USA, 10–13 July 2016; pp. 194–200. [Google Scholar]

- Chen, J.; Wang, X. Climate Policy Uncertainty and the Chinese Sectoral Stock Market: A Multilayer Network Analysis. Econ. Syst. 2024; in press. [Google Scholar] [CrossRef]

- MIT. Utility of the Future, 1st ed.; Massachusetts Institute of Technology: Cambridge, MA, USA, 2016; pp. 1–382. ISBN 9780692808245. [Google Scholar]

- Shum, K.L.; Watanabe, C. An Innovation Management Approach for Renewable Energy Deployment–the Case of Solar Photovoltaic (PV) Technology. Energy Policy 2009, 37, 3535–3544. [Google Scholar] [CrossRef]

- Hassan, M.; Oueslati, W.; Rousselière, D. Environmental Taxes, Reforms and Economic Growth: An Empirical Analysis of Panel Data. Econ. Syst. 2020, 44, 100806. [Google Scholar] [CrossRef]

- Ma, H.; Oxley, L.; Gibson, J. China’s Energy Economy: A Survey of the Literature. Econ. Syst. 2010, 34, 105–132. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Related External Factor | Motivating Question |

|---|---|

| Which policy demonstrates the most significant impact on the trends in installation costs? |

| Which policy exerts the greatest influence on the expansion of installed capacity? |

| Among sector agents, which entity possesses the greatest capacity to drive the growth of DGPV, and which policy is best suited to enhance their capabilities? |

| What policies are most conducive to each stage of technology maturity? |

| What political strategies are optimal for aligning with the various phases of the nation’s development trajectory? |

| Based on the characteristics of the electricity sector, which policies are most suitable for promoting the penetration of DGPV? |

| Incentive Category | Types of Policies Considered in Each Category | Description | References |

|---|---|---|---|

| Direct Financial Incentives | Payments, finance, and taxation Loans/debt finance Payments and transfers Taxes, fees, and charges Tax credits and exemptions Grants | Direct financial incentives are monetary benefits provided by governments or utility companies to encourage the adoption and implementation of photovoltaic solar energy systems. These incentives can take the form of tax credits, rebates, subsidies, or grants and aim to lower the cost of installing and operating DGPV systems and make them more accessible and affordable for individuals and businesses. | [30,31,32,33,34] |

| Energy Market Regulation | Regulation Energy market regulation Net energy metering Time-of-use tariffs | Energy market regulation refers to the policies and rules established by governments or utility companies to govern the integration and participation of DGPV systems in the energy market. These regulations aim to promote the growth of renewable energy sources, encourage fair competition, and ensure the stability and reliability of the energy grid. Energy market regulation manages the buying and selling of energy, access to the grid priority, incentive for self-consumption, and demand control. | [35,36,37,38] |

| Government Management | Targets Plans and framework legislation Strategic plans/climate change strategies Information and education Awards/Education and training Equity Government-provided advice Technology roadmaps Public information Codes and standards Prescriptive requirements and standards | Government management is responsible for outlining the guidelines to be followed, setting GHG emission reduction and RE adoption goals, developing strategic plans for mitigating the effects of climate change, technological roadmaps, creating codes and reference standards, prescribing norms and qualitative requirements, as well as directly acting in the dissemination of knowledge to the public through public information, education and training projects, awarding of innovative projects, and democratization of energy seeking equity. | [39,40,41,42,43] |

| Production Incentives | Production motivation Minimum energy performance Standards (MEPS) Product-based MEPS | Production incentives refer to policies and mechanisms that aim to motivate and increase production. This can be achieved through various methods such as production motivation, Minimum Energy Performance Standards (MEPS), and product-based MEPS. Production motivation provides financial benefits to producers of DGPV systems. MEPS set a minimum energy efficiency level for DGPV systems, ensuring that the systems being used are of good quality. Product-based MEPS require that only DGPV systems that meet specific energy efficiency standards are sold and used. | [44,45] |

| Performance-Based Feed Rates | Performance-based payments Performance-based policies Feed-in tariffs/premiums | Performance-based feed-in tariffs (PBFITs) are a type of financial incentive in the energy market that reward power producers for the amount of electricity they generate and feed into the grid. Unlike traditional feed-in tariffs, which offer a fixed rate per kilowatt-hour produced, PBFITs vary based on the performance of the energy system, usually based on factors such as capacity factor, availability, or efficiency. | [46,47,48,49,50] |

| Renewable Energy Obligations | Renewable/non-fossil energy obligations Obligations on average types of sales/output Energy efficiency/fuel economy obligations Green certificates Renewable Portfolio Standard (RPS)/Renewable Purchase Obligation (RPO) | Renewable Energy Obligations (REOs) refer to the requirement for electricity suppliers to source a minimum proportion of their energy from renewable sources, as set by government mandates. This can be achieved through various schemes such as purchasing renewable energy directly, acquiring green certificates that represent renewable energy generation, or fulfilling obligations set by government agencies. The goal of REOs is to increase the adoption of renewable energy, promote investment in renewable energy production, and drive down the cost of renewable energy through economies of scale. | [51,52,53,54,55,56] |

| Research and Development | R&D Operational funding for institutions | Research and Development (R&D) involves the allocation of funds and resources for the improvement and advancement of photovoltaic technologies. This includes providing operational funding for institutions such as universities and research centers to carry out research and develop new solutions, increase the efficiency, reliability and scalability of photovoltaic systems, as well as reduce costs and increase their competitiveness in the energy market. | [57,58,59] |

| Agreements and Commitments | Negotiated agreements (public–private sector) PPA/Unilateral commitments (private sector) | Agreements and commitments encompass formal agreements and promises made by governments, organizations, or corporations. Such agreements and commitments can range from negotiated public–private partnerships to unilateral commitments to the private sector, providing a stable and predictable financial framework for the entities involved. This, in turn, enables them to secure funding and plan for future investments with greater confidence. | [60,61,62,63,64] |

| China | Japan | Germany | USA | Italy | Australia | Netherlands | India | France | Belgium | Total | |

|---|---|---|---|---|---|---|---|---|---|---|---|

| Direct Financial Incentives | 20 | 7 | 12 | 31 | 13 | 28 | 16 | 20 | 25 | 3 | 175 |

| Energy Market Regulation | 19 | 3 | 6 | 6 | 13 | 4 | 10 | 15 | 11 | 7 | 94 |

| Government Management | 37 | 3 | 12 | 41 | 18 | 23 | 13 | 32 | 22 | 11 | 212 |

| Production Incentives | 7 | 0 | 0 | 10 | 0 | 3 | 0 | 5 | 1 | 0 | 26 |

| Performance-Based Feed Rates | 10 | 2 | 7 | 0 | 8 | 7 | 4 | 7 | 7 | 1 | 53 |

| Renewable Energy Obligations | 2 | 1 | 2 | 1 | 3 | 6 | 3 | 9 | 2 | 1 | 30 |

| Research and Development | 3 | 0 | 1 | 16 | 5 | 11 | 3 | 6 | 8 | 2 | 55 |

| Agreements and Commitments | 0 | 1 | 0 | 7 | 1 | 3 | 4 | 1 | 4 | 0 | 21 |

| Total | 52 | 11 | 20 | 61 | 32 | 38 | 29 | 40 | 41 | 14 | 338 |

| China | Japan | Germany | USA | Italy | Australia | Netherlands | India | France | Belgium | Total | |

|---|---|---|---|---|---|---|---|---|---|---|---|

| Direct Financial Incentives | 8 | 1 | 2 | 13 | 6 | 14 | 7 | 8 | 15 | 1 | 75 |

| Energy Market Regulation | 2 | 2 | 2 | 2 | 8 | 4 | 6 | 11 | 6 | 6 | 49 |

| Government Management | 6 | 1 | 1 | 15 | 10 | 11 | 3 | 18 | 7 | 5 | 77 |

| Production Incentives | 5 | 0 | 0 | 2 | 0 | 0 | 0 | 0 | 1 | 0 | 8 |

| Performance-Based Feed Rates | 4 | 0 | 2 | 0 | 5 | 7 | 2 | 6 | 2 | 1 | 29 |

| Renewable Energy Obligations | 1 | 0 | 1 | 1 | 2 | 4 | 1 | 6 | 2 | 1 | 19 |

| Research and Development | 2 | 0 | 0 | 9 | 2 | 2 | 2 | 3 | 5 | 0 | 25 |

| Agreements and Commitments | 0 | 0 | 0 | 6 | 1 | 2 | 0 | 1 | 2 | 0 | 12 |

| China | Japan | Germany | USA | Italy | Australia | Netherlands | India | France | Belgium | Total | |

|---|---|---|---|---|---|---|---|---|---|---|---|

| Direct Financial Incentives | 7 | 1 | 4 | 22 | 2 | 3 | 7 | 8 | 9 | 1 | 64 |

| Energy Market Regulation | 2 | 2 | 0 | 4 | 2 | 0 | 6 | 11 | 2 | 6 | 35 |

| Government Management | 6 | 1 | 5 | 22 | 2 | 3 | 3 | 18 | 2 | 5 | 67 |

| Production Incentives | 5 | 0 | 0 | 6 | 0 | 1 | 0 | 0 | 1 | 0 | 13 |

| Performance-Based Feed Rates | 3 | 0 | 2 | 0 | 0 | 0 | 2 | 6 | 1 | 1 | 15 |

| Renewable Energy Obligations | 1 | 0 | 0 | 1 | 0 | 3 | 1 | 6 | 1 | 1 | 14 |

| Research and Development | 2 | 0 | 1 | 11 | 0 | 1 | 2 | 3 | 1 | 0 | 21 |

| Agreements and Commitments | 0 | 0 | 0 | 5 | 0 | 2 | 0 | 1 | 1 | 0 | 9 |

| Key Stakeholder | Prosumers | Integrators | Equipment and Component Manufactures | Utilities | Research Institutions |

|---|---|---|---|---|---|

| Direct Financial Incentives | 175 | 175 | 175 | - | - |

| Energy Market Regulation | 94 | - | - | 94 | - |

| Government Management | 212 | - | 212 | 212 | - |

| Production Incentives | - | 26 | 26 | - | - |

| Performance-Based Feed Rates | 53 | - | - | - | - |

| Renewable Energy Obligations | 30 | - | - | 30 | - |

| Research and Development | - | - | - | - | 55 |

| Agreements and Commitments | 21 | - | - | 21 | - |

| Development Phases | Initial Implementation Phase (TRL 1–3) | Initial Growth Phase (TRL 4–5) | First Major Growth Phase (TRL 6–7) | Mature Implementation Phase (TRL 8–9) |

|---|---|---|---|---|

| Direct Financial Incentives | 56 | 72 | 81 | 123 |

| Energy Market Regulation | 38 | 48 | 55 | 84 |

| Government Management | 63 | 71 | 85 | 160 |

| Production Incentives | 8 | 3 | 13 | 21 |

| Performance-Based Feed Rates | 21 | 26 | 24 | 39 |

| Renewable Energy Obligations | 16 | 18 | 16 | 27 |

| Research and Development | 22 | 24 | 28 | 42 |

| Agreements and Commitments | 9 | 14 | 16 | 19 |

| Total | 233 | 276 | 318 | 515 |

| Gross Domestic Product per Capita (mi) | 0 to 499 | 500 to 999 | 1000 to 1499 | 1500 to 1999 | 2000 to 3999 | 4000 to 9999 | 10,000 to 19,999 | 20,000 to 29,999 | 30,000 to 39,999 | 40,000 to 49,999 | 50,000 to 59,999 | 60,000 to 69,999 | 70,000 to 79,999 | Over 80,000 |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Direct Financial Incentives | 0 | 1 | 5 | 10 | 14 | 12 | 11 | 4 | 7 | 11 | 11 | 21 | 15 | - |

| Energy Market Regulation | 0 | 3 | 6 | 8 | 9 | 16 | 11 | 3 | 5 | 5 | 6 | 5 | 2 | - |

| Government Management | 0 | 3 | 10 | 15 | 17 | 26 | 20 | 3 | 7 | 11 | 13 | 22 | 11 | - |

| Production Incentives | 0 | 1 | 2 | 3 | 5 | 7 | 5 | 0 | 0 | 1 | 1 | 5 | 2 | - |

| Performance-Based Feed Rates | 0 | 1 | 3 | 4 | 5 | 5 | 5 | 1 | 2 | 3 | 2 | 4 | 5 | - |

| Renewable Energy Obligations | 0 | 1 | 3 | 5 | 5 | 2 | 2 | 1 | 1 | 2 | 2 | 3 | 5 | - |

| Research and Development | 0 | 1 | 2 | 3 | 4 | 3 | 2 | 1 | 3 | 4 | 4 | 9 | 6 | - |

| Agreements and Commitments | 0 | 0 | 1 | 1 | 1 | 0 | 0 | 1 | 1 | 2 | 2 | 3 | 2 | - |

| Human Development Index | 0.400 to 0.499 | 0.500 to 0.599 | 0.600 to 0.699 | 0.700 to 0.799 | 0.800 to 0.899 | 0.900 to 1.000 |

|---|---|---|---|---|---|---|

| Direct Financial Incentives | 0 | 3 | 14 | 12 | 5 | 11 |

| Energy Market Regulation | 0 | 5 | 9 | 16 | 4 | 6 |

| Government Management | 0 | 7 | 17 | 26 | 5 | 13 |

| Production Incentives | 0 | 1 | 5 | 7 | 0 | 1 |

| Performance-Based Feed Rates | 0 | 3 | 5 | 6 | 2 | 3 |

| Renewable Energy Obligations | 0 | 2 | 5 | 2 | 1 | 2 |

| Research and Development | 0 | 2 | 4 | 3 | 2 | 4 |

| Agreements and Commitments | 0 | 1 | 1 | 0 | 1 | 2 |

| Share of Renewables in Power Generation (%) | Under 0 | 0 to 9.99 | 10 to 19.99 | 20 to 29.99 | 30 to 39.99 | 40 to 49.99 | 50 to 59.99 | 60 to 69.99 | 70 to 79.99 | 80 to 89.99 | Over 90 |

|---|---|---|---|---|---|---|---|---|---|---|---|

| Direct Financial Incentives | - | 9 | 11 | 9 | 8 | - | - | - | - | - | - |

| Energy Market Regulation | - | 4 | 7 | 8 | 8 | - | - | - | - | - | - |

| Government Management | - | 7 | 14 | 14 | 11 | - | - | - | - | - | - |

| Production Incentives | - | 1 | 2 | 1 | 0 | - | - | - | - | - | - |

| Performance-Based Feed Rates | - | 2 | 4 | 4 | 3 | - | - | - | - | - | - |

| Renewable Energy Obligations | - | 2 | 2 | 2 | 2 | - | - | - | - | - | - |

| Research and Development | - | 3 | 4 | 3 | 2 | - | - | - | - | - | - |

| Agreements and Commitments | - | 2 | 2 | 1 | 2 | - | - | - | - | - | - |

| Net Electricity imports (GWh) | Under 0 | 0 to 9.99 | 10 to 19.99 | 20 to 29.99 | 30 to 39.99 | 40 to 49.99 | 50 to 59.99 | 60 to 69.99 | 70 to 79.99 | 80 to 89.99 | Over 90 |

|---|---|---|---|---|---|---|---|---|---|---|---|

| Direct Financial Incentives | 11 | 9 | 7 | 2 | - | - | - | - | - | - | - |

| Energy Market Regulation | 10 | 6 | 9 | 6 | - | - | - | - | - | - | - |

| Government Management | 17 | 13 | 11 | 9 | - | - | - | - | - | - | - |

| Production Incentives | 2 | 2 | 0 | 0 | - | - | - | - | - | - | - |

| Performance-Based Feed Rates | 4 | 2 | 3 | 1 | - | - | - | - | - | - | - |

| Renewable Energy Obligations | 3 | 2 | 2 | 1 | - | - | - | - | - | - | - |

| Research and Development | 3 | 3 | 2 | 1 | - | - | - | - | - | - | - |

| Agreements and Commitments | 2 | 2 | 2 | 0 | - | - | - | - | - | - | - |

| Direct Financial Incentives | Energy Market Regulation | Government Management | Production Incentives | Performance-Based Feed Rates | Renewable Energy Obligations | Research and Development | Agreements and Commitments | |

|---|---|---|---|---|---|---|---|---|

| Reduction in installation costs | X | X | X | |||||

| Growth in installed capacity | X | X | X | |||||

| The most influential stakeholder for sectoral growth: Prosumers | X | X | ||||||

| Technological maturity—Different stages of technology | X | X | X | |||||

| Socioeconomic factors—various phases of the nation’s development trajectory | X | X | ||||||

| Lowest shares of renewable energy | X | |||||||

| Highest shares of renewable energy | X | |||||||

| Various net imports ranging | X |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2025 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Schetinger, A.M.; de Lucena, A.F.P. Evaluating Policy Frameworks and Their Role in the Sustainable Growth of Distributed Photovoltaic Generation. Resources 2025, 14, 28. https://doi.org/10.3390/resources14020028

Schetinger AM, de Lucena AFP. Evaluating Policy Frameworks and Their Role in the Sustainable Growth of Distributed Photovoltaic Generation. Resources. 2025; 14(2):28. https://doi.org/10.3390/resources14020028

Chicago/Turabian StyleSchetinger, Annelys Machado, and André Frossard Pereira de Lucena. 2025. "Evaluating Policy Frameworks and Their Role in the Sustainable Growth of Distributed Photovoltaic Generation" Resources 14, no. 2: 28. https://doi.org/10.3390/resources14020028

APA StyleSchetinger, A. M., & de Lucena, A. F. P. (2025). Evaluating Policy Frameworks and Their Role in the Sustainable Growth of Distributed Photovoltaic Generation. Resources, 14(2), 28. https://doi.org/10.3390/resources14020028