The Impact of Government Policy on Macro Dynamic Innovation of the Creative Industries: Studies of the UK’s and China’s Animation Sectors

Abstract

:1. Introduction

2. Theories of the Macro Dynamic Innovation System and Innovation Policy

2.1. Innovation as System and Ecosystem

2.2. Government Innovation Policy

3. Research Design and Methodology

4. Findings and Discussion

4.1. The Macro Innovation System of the Animation Industry

4.2. Government Policies in the U.K’s and China’s Animation Industries

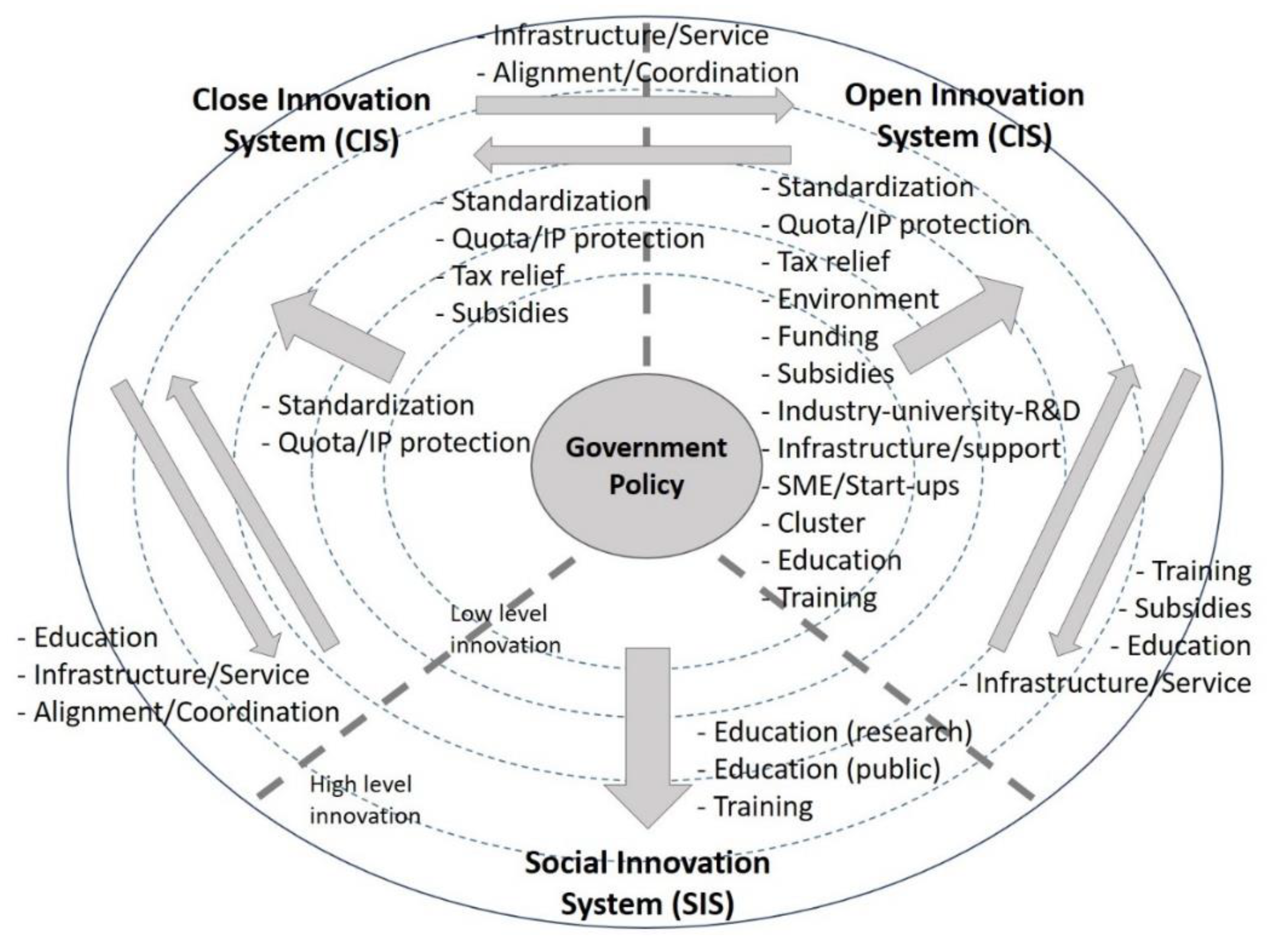

4.3. Dynamic View of the Macro Innovation System

5. Conclusions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- Giarini, O. The globalization of service in economic theory and economic practice: Some conceptual issues. In Trading Services in the Global Economy; Cuadrado-Roura, J.R., Rubalcaba-Bermejo, L., Bryson, J.R., Eds.; Edward Elgar: Cheltenham, UK, 2002; pp. 58–77. [Google Scholar]

- DCMS. Creative Industries Mapping Documents 1998; DCMS: London, UK. Available online: https://www.gov.uk/government/publications/creative-industries-mapping-documents-1998 (accessed on 4 August 2019).

- DCMS. Creative Industries Mapping Documents; DCMS: London, UK, 2001. Available online: https://www.gov.uk/government/publications/creative-industries-mapping-documents-2001 (accessed on 4 August 2019).

- UNCTAD. Creative Economy Bucks the Trend, Grows Despite Slowdown in Global Trade. 2019. Available online: https://unctad.org/en/pages/PressRelease.aspx?OriginalVersionID=499 (accessed on 4 August 2019).

- Lumina. UK Animation on the Rise. 2017. Available online: http://luminasearch.com/research/animation-on-the-rise/ (accessed on 4 August 2019).

- Messerlin, P.; Parc, J. The effect of screen quotas and subsidy regime on cultural industry: A case study of French and Korean film industries. J. Int. Bus. Econ. 2014, 15, 57–73. [Google Scholar]

- Yun, J.J. How do we conquer the growth limits of capitalism? Schumpeterian dynamics of open innovation. J. Open Innov. Technol. Mark. Complex. 2015, 1, 1–20. [Google Scholar] [CrossRef] [Green Version]

- Yun, J.J.; Liu, Z. Micro and macro dynamics of open innovation with quadruple-helix. Sustainability 2019, 11, 3301. [Google Scholar] [CrossRef] [Green Version]

- Chesbrough, H. Open Innovation: The New Imperative for Creating and Profiting from Technology; Harvard Business School Press: Cambridge, MA, USA, 2013. [Google Scholar]

- Chesbrough, H.; Brunswicker, S. A fad or a phenomenon?: The adoption of open innovation practices in large firms. Res. Technol. Manag. 2014, 57, 16–25. [Google Scholar]

- Ayob, N.; Teasdale, S.; Fagan, K. How social innovation ‘came to be’: Tracing the evolution of a contested concept. J. Soc. Policy 2016, 45, 635–653. [Google Scholar] [CrossRef] [Green Version]

- Bogers, M.; Chesbrough, H.; Moedas, C. Open innovation: Research, practices, and policies. Calif. Manag. Rev. 2018, 60, 5–16. [Google Scholar] [CrossRef]

- Moore, J.F. Predators and prey: A new ecology of competition. Harv. Bus. Rev. 1993, 71, 75–86. [Google Scholar]

- Adner, R. The Wide Lens: A New Strategy for Innovation; Penguin: London, UK, 2012. [Google Scholar]

- Beraud, P.; du Castel, V.; Cormerais, F. Open innovation, economy of contribution and the territorial dynamics of creative industries. J. Innov. Econ. 2012, 10, 81–105. [Google Scholar] [CrossRef]

- Dahlander, L.; Gann, D.M. How open is innovation? Res. Policy 2010, 39, 699–709. [Google Scholar] [CrossRef]

- Ma, L.; Qian, C.; Liu, Z.; Zhu, Y. Exploring the innovation system of the animation industry: Case study of a Chinese company. Sustainability 2018, 10, 3213. [Google Scholar] [CrossRef] [Green Version]

- Santagata, W. Cultural districts, property rights and sustainable economic growth. Int. J. Urban Reg. Res. 2002, 26, 9–23. [Google Scholar] [CrossRef]

- Banks, M.; Hesmondhalgh, D. Looking for work in creative industries policy. Int. J. Cult. Policy 2009, 15, 415–430. [Google Scholar] [CrossRef]

- Edler, J.; Georghiou, L. Public procurement and innovation: Resurrecting the demand side. Res. Policy 2007, 36, 949–963. [Google Scholar] [CrossRef]

- Ma, L.; Jiang, M.; Yu, K.; Gan, J. A Study on Regional Innovation Policy under Innovation Paradigm 30: A Case of Jiangsu Province in China. In Proceedings of the 2016 Portland International Conference on Management of Engineering and Technology (PICMET 2016), Honolulu, HI, USA, 4–8 September 2016; pp. 1055–1064. [Google Scholar]

- OECD. Demand-Side Innovation Policies; OECD Publishing: Paris, France, 2011. [Google Scholar]

- Qu, L.; Li, Y. Research on industrial policy from the perspective of demand-side open innovation: A case study of Shenzhen new energy vehicle industry. J. Open Innov. Technol. Mark. Complex 2019, 5, 31. [Google Scholar] [CrossRef] [Green Version]

- Almgren, R.; Skobelev, D. Evolution of technology and technology governance. J. Open Innov. Technol. Mark. Complex 2020, 6, 22. [Google Scholar] [CrossRef] [Green Version]

- Li, F.; Butel, L.; Wang, P. Innovation policy configuration—A comparative study of Russia and China. Policy Stud. 2017, 38, 311–338. [Google Scholar] [CrossRef]

- Schot, J.; Steinmueller, W.E. Three frames for innovation policy: R&D, systems of innovation and transformative change. Res. Policy 2018, 47, 1554–1567. [Google Scholar]

- Grillitsch, M.; Hansen, T.; Coenen, L.; Miorner, J.; Moodysson, J. Innovation policy for system-wide transformation: The case of strategic innovation programmes (SIPs) in Sweden. Res. Policy 2019, 48, 1048–1061. [Google Scholar] [CrossRef]

- Phills, J.A.; Deiglmeier, K.; Miller, D.T. Rediscovering social innovation. Stanf. Soc. Innov. Rev. 2008, 6, 34–43. [Google Scholar]

- Flew, T. Global Creative Industries; Polity Press: Cambridge, UK, 2013. [Google Scholar]

- Ritman, A. U.K. Film Industry Sees Record Spending from Hollywood Production in 2016. The Hollywood Reporter. 2017. Available online: https://www.hollywoodreporter.com/news/uk-film-industry-sees-record-spending-hollywood-productions-2016-968843 (accessed on 12 September 2019).

- Santoro, G.; Bresciani, S.; Papa, A. Collaborative modes with Cultural and Creative Industries and innovation performance: The moderating role of heterogeneous sources of knowledge and absorptive capacity. Technovation 2020, 92–93, 102040. [Google Scholar] [CrossRef]

- Chandra, T. Mapping knowledge management system within literatures of creative industry. J. Manag. Inf. Decis. Sci. 2019, 22, 213–222. [Google Scholar]

- Li, F. The digital transformation of business models in the creative industries: A holistic framework and emerging trends. Technovation 2020, 92–93, 102012. [Google Scholar]

- Landoni, P.; Dell’era, C.; Frattini, F.; Petruzzelli, A.M.; Verganti, R.; Manelli, L. Business model innovation in cultural and creative industries: Insights from three leading mobile gaming firms. Technovation 2020, 92–93, 102084. [Google Scholar]

- Salvador, E.; Simon, J.; Benghozi, P. Facing Disruption: The Cinema Value Chain in the Digital Age. Int. J. Arts Manag. 2019, 22, 25–40. [Google Scholar]

- Yamada, J.; Yamashita, M. Entrepreneurs’ Intentions and Partnership Towards Innovation: Evidence from the Japanese Film Industry. Creat. Innov. Manag. 2006, 15, 258–267. [Google Scholar] [CrossRef]

- Lassen, A.H.; Maureen, M.; Ljungberg, D. Knowledge-intensive entrepreneurship in manufacturing and creative industries: Same, same, but different. Creat. Innov. Manag. 2018, 27, 284–294. [Google Scholar] [CrossRef]

- Hotho, S.; Champion, K. Small businesses in the new creative industries: Innovation as a people management challenge. Manag. Decis. 2011, 49, 29–54. [Google Scholar] [CrossRef] [Green Version]

- Mossig, I. Regional Employment Growth in the Cultural and Creative Industries in Germany 2003–2008. Eur. Plan. Stud. 2011, 19, 967–990. [Google Scholar] [CrossRef]

- Innocenti, N.; Lazzeretti, L. Do the creative industries support growth and innovation in the wider economy? Industry relatedness and employment growth in Italy. Ind. Innov. 2019, 26, 1152–1173. [Google Scholar] [CrossRef]

- Potts, J. Why creative industries matter to economic evolution. Econ. Innov. New Technol. 2009, 18, 663–673. [Google Scholar] [CrossRef] [Green Version]

- Boix-Domenech, R.; Soler-Marco, V. Creative service industries and regional productivity. Pap. Reg. Sci. 2017, 96, 261–279. [Google Scholar] [CrossRef]

- Oyekunle, A.O.; Sirayi, M. The role of creative industries as a driver for a sustainable economy: A case of South Africa. Creat. Ind. J. 2018, 11, 225–244. [Google Scholar]

- Klement, B.; Strambach, S. Innovation in Creative Industries: Does (Related) Variety Matter for the Creativity of Urban Music Scenes? Econ. Geogr. 2019, 95, 385–417. [Google Scholar] [CrossRef]

- Feuls, M. Understanding culinary innovation as relational: Insights from Tarde’s relational sociology. Creat. Innov. Manag. 2018, 27, 161–168. [Google Scholar] [CrossRef]

- Zhou, J.; Li, J.; Jiao, H.; Qiu, H.; Liu, Z. The more funding the better? The moderating role of knowledge stock on the effects of different government-funded research projects on firm innovation in Chinese cultural and creative industries. Technovation 2020, 92–93, 102059. [Google Scholar] [CrossRef]

- Lee, N.; Drever, L. The Creative Industries, Creative Occupations and Innovation in London. Eur. Plan. Stud. 2013, 21, 1977–1997. [Google Scholar] [CrossRef]

- Liu, H.; Silva, E. Examining the dynamics of the interaction between the development of creative industries and urban spatial structure by agent-based modelling: A case study of Nanjing, China. Urban Stud. 2018, 55, 1013–1032. [Google Scholar] [CrossRef]

- Lee, C.B. Cultural Policy and Governance: Reviewing Policies Related to Cultural and Creative Industries Implemented by the Central Government of Taiwan Between 2002 and 2012. Rev. Policy Rep. 2015, 32, 465–484. [Google Scholar] [CrossRef]

- Comunian, R.; Taylor, C.; Smith, D. The Role of Universities in the Regional Creative Economies of the UK: Hidden Protagonists and the Challenge of Knowledge Transfer. Eur. Plan. Stud. 2014, 22, 2456–2476. [Google Scholar] [CrossRef] [Green Version]

- Braun, V.; Clarke, V. Using thematic analysis in psychology. Qual. Res. Psychol. 2006, 3, 77–101. [Google Scholar] [CrossRef] [Green Version]

- BFI. Screen Business: How Screen Sector Tax Reliefs Power Economic Growth across the U.K. 2018. Available online: https://www.bfi.org.uk/sites/bfi.org.uk/files/downloads/screen-business-full-report-2018-10-08.pdf (accessed on 20 September 2019).

- British Council. U.K. Animation. 2018. Available online: http://film.britishcouncil.org/docs/UKAnimationCatalogue_1528804727.pdf (accessed on 20 September 2019).

- ANIMATION UK. The UK’s Animation Sector: In Profile. 2018. Available online: https://www.animationuk.org/subpages/the-uks-animation-sector-in-profile/?section=industry (accessed on 20 September 2019).

- LIAF. About the London International Animation Festival. 2019. Available online: http://www.liaf.org.uk/about/ (accessed on 20 September 2019).

- CGB (Chinabaogao.com). Analysis of the Development Process and Profit Model of China’s Animation Industry. 2018. Available online: http://market.chinabaogao.com/it/041I303512018.html (accessed on 20 September 2019).

- Liu, Z. The current business performance of the Chinese animation industry: Key structure and emerging themes. Int. J. Cult. Creat. Ind. 2015, 2, 42–53. [Google Scholar]

- Alpha Animation. About Alpha Animation. 2019. Available online: https://www.gdalpha.com/about/index.html (accessed on 20 September 2019).

- Sohu. Interpretation of the Revenue of Major Animation Companies in China. 2018. Available online: http://www.sohu.com/a/230105371_115832 (accessed on 28 September 2019).

- DCMS. 2010 to 2015 Government Policy: Media and Creative Industries. 2015. Available online: https://www.gov.uk/government/publications/2010-to-2015-government-policy-media-and-creative-industries/2010-to-2015-government-policy-media-and-creative-industries (accessed on 29 September 2019).

- GOV.UK. Corporation Tax: Creative Industry Tax Reliefs. 2018. Available online: https://www.gov.uk/guidance/corporation-tax-creative-industry-tax-reliefs (accessed on 29 September 2019).

- Askci.com. Comic Industry Policy Summary and Interpretation in Different Parts of China. 2018. Available online: http://www.askci.com/news/finance/20180115/162850116068.shtml (accessed on 20 September 2019).

{kind=link}

{kind=link}

| Paper | Key Findings |

|---|---|

| Klement and Strambach [44] | Policies need to analyze not only aggregate data but also the composition of regional symbolic knowledge bases, which are related or not directly related to the creative industries. |

| Feuls [45] | Innovation in the creative industries is not a linear development process, but a culinary system involving relations of everyday practices that define and transform its value. |

| Zhou et al. [46] | Central government-funded research projects show an inverted U-shaped effect on both firms’ radical innovation and incremental innovation in the creative industries. Local government-funded projects have an inverted U-shaped effect on firms’ incremental innovation, but no significant effects on firms’ radical innovation. |

| Lee and Drever [47] | Policies need to integrate creative occupations into firms across the whole economy. |

| Liu and Silva [48] | More open job market information can result in more rapid geographical clustering of the creative firms. It can accelerate innovation through knowledge and information spill-over. |

| Lee [49] | Cultural values promoted by government policy can support the creative industries and stimulate other new industries. |

| Comunian et al. [50] | Universities traditionally play an important role in the triple helix innovation. However, there are important institutional and professional challenges for universities to develop an explicit and sustainable role as new actors in the creative economies. |

| Category | Sub-Category |

|---|---|

| Supply-side | S1: Public funded R&D and mission-led research [21,26] S2: Fiscal/financial support and subsides [25,26] S3: Favorable tax treatment [21,26] S4: Establishing science hubs and industry clusters [21,26] S5: Supporting SMEs and start-ups [25,26] S6: Infrastructure support, e.g., improving research centers [21,25] S7: Education for research careers [26] S8: Personnel training [21] |

| Demand-side | D1: Stimulating private demand for innovation [22] D2: Public procurement [22,25] D3: Pre-commercial procurement [22] D4: Innovation inducement prizes [22] D5: Industry–university–R&D institution collaboration [22] D6: Standardization and regulation [22,25] |

| Environmental-side | E1: Law, finance, tax systems to improve the environment [21,25,29] E2: Content regulations, quota, IP protection [25,27,29] E3: Administrative, sharing platforms, infrastructure and service support [17,21,25] E4: User-involvement as producers, legitimates, and demand contributors [26] E5: Improving alignment and cross-sectorial coordination [26,27] E6: Promotion of entrepreneurship and innovation culture [26,29]. E7: Soft-law and governance, leading to self-regulation [29] E8: Public education of the industry values with the aim of sustainability [29] |

| Value Chain | Closed Innovation System (CIS) | Social Innovation System (SIS) | Open Innovation System (OIS) |

|---|---|---|---|

| Creation/design | Large firms conducting R&D internally; Large firms leading the industry, with SMEs under the roof; IP protection and management; Co-developing products with long-term supply partners; Backward integration with creation/design studios. | General stakeholder involvement (non-for-profit organizations, industry, university, government); Products featuring social needs; Social innovation and collective creation. | Triple Helix innovation with university involvement, e.g., the UK screen industry; Crowd sourcing and innovation events; Open innovation based on digital platforms, led by large companies; Knowledge spillover effect. |

| Manufacturing/production | In-house production; Long-term collaboration; Outsourcing with strict control. | Industrial association and NGOs’ involvement for standardization and social concerns. | Outsourcing and subcontracting with multiple partners; Co-production among large firms and SMEs on digital platforms. |

| Distribution/marketing | Distribution through major online and offline media, e.g., TV, Amazon; Market and monetary value delivery. | Marketing with social events; Social media and social networks e.g., YouTube, Twitter, Facebook | Distribution through various interactive forms, e.g., Netflix, Amazon, YouTube, Twitter, Facebook; Crowd voting and user engagement; Using social media and social networks. |

| Communication/service | Cross sector integration, e.g., animation IP further expanding towards the gaming industry, consumer products, theme parks, hotel businesses, with IP control | Services featuring social needs and community engagement; Considering user experience in product development and expansion; Festivals to encourage communication | User-content creation; University entrepreneurs; Product spillover effect. |

| Government Policy Instruments (S, D, E) with Detailed Content | Impact on Macro Innovation Systems (CIS, SIS, OIS) |

|---|---|

| 2002. The Enterprise Act: Reviews mergers in the media industry, to make sure that one owner does not control a disproportionately large share of the industry [60]. | This regulation standardizes practices of large firms in the media industry. (D6 → CIS) |

| 2003. The Communications Act: It is the primary means by which the digital industries are regulated. It set up Ofcom’s (UK’s communications regulator) full powers [60]. | This centralized policy standardizes the practices of the digital industry. (D6 → CIS) |

| 2010. The Digital Economy Act: Measures to protect the rights of copyright owners online; the Initial Obligations Code for rights holders and ISPs (internet service providers) on how to deal with internet piracy; the code for the functioning of the mass notification system, which will require certain internet ISPs to participate and will clarify the voluntary role copyright owners will play [60]. | The regulations aim to ensure IP protection, standardize practices on digital platforms, and benefit large firms and SMEs with IPs. Through measurements and benchmarks, IP management can be more efficient and effective. (E2 → CIS) |

| 2011–2012. Funding the British Film Institute (BFI), the UK’s lead agency for film, to support film production, distribution, education, audience development, and market research [60]. | From 2011 to 2012, the government funding of BFI amounted to GBP 20 million, greatly supporting education, training, and market research, and engaging more people in the film industry. (S7, S8, E8 → SIS) |

| 2011. Setting up the Creative Industries Council: to provide regular dialogue between the government and the industry. The council focuses on areas where there are barriers to growth facing the sector, such as access to finance, skills, export markets, regulation, IP and infrastructure [60].) | The Creative Industrial Council is an informal forum. It breaks the barrier between sectors and companies, engaging large companies and SMEs to generate knowledge together, and provides infrastructure and service support. (D6, E1, E2, E3, E5 → OIS) |

| 2011. The Media Ownership (Radio and Cross Media) Order: Giving media businesses the freedom to enter new markets, particularly local TV [60]. | This policy can encourage more companies, including SMEs, to deliver products to the market smoothly. It also promotes product spillover effects through media. (E3 → OIS) |

| 2012. Funding the BFI Film Academy Network: the BFI delivers film-related courses at different locations in the UK. It aims to provide everyone with the opportunity to build a lifelong relationship with film; to create clear progression paths for talented young people; to ensure that film is celebrated and explored in formal education [60]. | In late 2012, the BFI received money from the Department for Education to create the BFI Film Academy Network. The government action further contributes to education, market research, the distribution of the film industry, public awareness of film knowledge and skills, and social engagement. (S2, S7, S8 → SIS) |

| 2012. The Local Digital Television Programme Services Order: Creating a local TV licensing regime [60]. | This policy can improve infrastructure and public services. (E3 → SIS) |

| 2013. The multiplex operator (responsible for building and maintaining the technical infrastructure needed to broadcast local TV services) license was awarded to Ofcom. This is a significant milestone in moving the launch of each local TV channel forward [60]. | It shows infrastructure support to facilitate the distribution of the animation industry. It also stimulates the market at a local level by expanding TV program accessibility. (E3 → SIS) |

| 2013 Creative industry tax reliefs: A group of 8 Corporation Tax reliefs that allow qualifying companies to claim deductions when calculating their taxable profits [61]. | It highlights the importance of the creative industries, with favorable tax policies provided. (S3, E1 → OIS) |

| 2013. Animation Tax Relief (ATR): Companies can claim ATR on an animation program if: the program passes the cultural test or qualifies as an official co-production; the program is intended for broadcast; at least 51% of the total core expenditure is on animation; at least 10% of the total production costs relate to activities in the UK [61]. | With the ATR policy, the number of animation studios, including most SMEs, will grow. (S3, E1 → OIS) |

| 2014. Children’s Television Tax Relief (CTR): Companies can claim CTR if: the program passes the cultural test or qualifies as an official co-production; the program is intended for broadcast; the program must be for children, specifically, the primary audience is expected to be under the age of 15; at least 10% of the total production costs relate to activities in the UK [61]. | CTR is an extension of high-end television and animation relief. It promotes original designs, and collaboration between media and animation companies. Meanwhile, it also contributes to children’s education and public service improvement. (E3, E8 → SIS; S3, E1, E5 → OIS) |

| 2014. Video Games Tax Relief (VGTR): Companies can claim VGTR if: the video game is British; the video game is intended for supply; at least 25% of core expenditure is incurred on goods or services that are provided from within the European Economic Area (EEA) [61]. | This policy encourages product spillover effects, from animation movies to the game industry and related services. It also facilitates alliances among animation studios and game software companies to co-create IP. (S3, E1, E5 → OIS) |

| 2014 Interaction of VGTR and Research and Development (R&D) tax relief: Where video game SMEs’ R&D tax relief is claimed on a project, large companies can make claims under the large scheme [61]. | This policy supports the original R&D activities of the video game industry, which is closely related to the animation industry. It provides benefits to both large firms and SMEs. (S3, E1 → OIS; S3, E1 → CIS) |

| Government Policy Instruments (S, D, E) with Detailed Content | Impact on Macro Innovation System (CIS, SIS, OIS) |

|---|---|

| 2000. Notice on strengthening the introduction and broadcasting of animated cartoons. All TV stations must broadcast 10 min of animated cartoons every day, with 60% being domestic-made [62]. | This is centralized regulation, with the aim of promoting original productions in general. (E2 → OIS) |

| 2002. The development plan of the film and television animation industries during the “10th Five-Year Plan” period. It highlights the industry paths of nationalization, popularization and industrialization [62]. | This policy continuously addresses the importance of the animation industry at the strategic level, promoting innovation and public support of the animation industry. (E2 → OIS) |

| 2004. Notice on subject planning of domestic TV animations. The Beijing animation channel, Shanghai cartoon TV, and Hunan Golden Eagle cartoon TV are approved as animation channels [62]. | This policy shows infrastructure support. With animation-featuring TV channels, animation products can be distributed to the mass market. It also links animation producers with distributors for collaboration. (E3 → OIS) |

| 2005. Notice on tax policy issues concerning the autocratic reform of cultural institutions into enterprises. Enterprises engaged in animation-related creation, production, and distribution can be exempted from the corporate income tax [62]. | As a typical supply-side policy, the tax exemption scheme supports the creation of knowledge. SMEs (due to almost no large companies existing) including software, comic book, animation and service companies, can be more actively engaged in innovation and creating IPs. (S3 → OIS) |

| 2005. Specific measures to promote the development of animation creation in China. Encouraging TV houses to broadcast domestic animation during 17:00 and 21:00. The total amount of domestic animation broadcasting should not be less than 60% [62]. | This policy has, in general, supported original production, with protection from competition from foreign products conferred. (E3 → OIS) |

| 2006. Some opinions on supporting the development of the domestic animation industry The central government set up special funds to support the development of original animation works. It encourages social capital to enter the animation industry. Enterprises that open up their own production of animation products can enjoy exemption of the value-added tax and the corporate income tax. Eligible SMEs which develop technology innovation can apply for SMEs’ science and technology fund [62]. | This is one of the most important policies regarding the Chinese animation industry. SMEs’ innovation is encouraged with resource sharing, learning, and exchange. Direct funding and favorable tax programs result in more companies involved in original R&D and technology innovation. Social capital further provides chances for SMEs in addition to government funds. (S1, S2, S3, S5 → OIS) |

| 2006–2012. Creating animation industry parks across China, with support from local governments. Examples are Supplementary opinions on encouraging and supporting the development of animation and game industry (Hangzhou government), Measures for fund management for the development of animation industry in Xiamen (Xiamen government), Preferential policies for Beijing digital entertainment industry base (Beijing government) [62]. | These series of local government policies are to respond to central government guidance on the development of the animation industry’s focus on supply support. Direct funding to R&D projects, subsidies to SMEs, alliances between the industry and universities, training, research center establishment, administration and service improvements, and clusters are new themes of innovation. University–industry collaboration is supported by many local governments. (S1, S2, S3, S4, S5, S6, S7, S8, D5, E3 → OIS) |

| 2008. Management measures for the recognition of animation enterprises. The standards and procedures for the identification of animation enterprises are stipulated [62]. | With the number of SMEs increasing, this policy helps industry convenience and standardization. (D6 → OIS; D6 → CIS) |

| 2009. Notice of the State Administration for Industry and Commerce of the Ministry of Culture on the special rectification of the animation market. The protection of animation derivatives, trading products, key animation products, and other regulatory work are deployed [62]. | Trends of resource integration, and product and brand convergence aiming at high quality and value-added activities are formed based on this regulation. (D6, E2 → CIS) |

| 2011. Notice on the business tax policy of value-added tax to support the development of the animation industry. This extended the relevant tax incentives until the end of 2012 and brought animation copyright trading into the scope of preferential treatment [62]. | Apart from continuously supporting the animation industry’s innovation and production, this policy highlighted IP protection, driving the movement towards closed innovation and resource integration. (S3 → CIS) |

| 2012. The “12th five-Year Plan” for creative industries. The animation industry is listed as one of the 11 key industries. It is proposed that “by 2015, the value added of the animation industry will exceed 30 billion yuan, creating 5–10 domestic animation brands and key animation enterprises with strong competitiveness and influence in the world.” [62] | This policy indicates a strategic change from OISs towards CISs with the resource integrating, funding and promoting of leading companies. Through M&A and collaboration, leading large firms are gradually formed which have control of value chains, technology and IPs. (S2, E2 → CIS) |

| 2013. National animation brand construction and protection plan. Identifying 20 animation brands including the “Happy goat and grey wolf” and announcing the standards of mobile animation [62]. | The identification and rewarding of top animation brands shows government support on leading large companies. With brand promotion, the supply chain can be further integrated. With mobile infrastructure support, the public can engage with the industry more easily. (S2 → CIS, S6, E3 → SIS) |

| 2017. The Ministry of Culture’s planning for cultural development and reform in the 13th Five-Year Period. Promoting China’s International Network Culture Expo, China’s International Animation and Games Fair and other key creative industries events. Supporting original animation production and brands featuring the national culture, and promoting mobile phone animation standards [62]. | The policy shows the importance of cross-sectorial communication and information exchange. Through events, it also involves service agencies and society. (E5, E8 → SIS) |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Liu, Z. The Impact of Government Policy on Macro Dynamic Innovation of the Creative Industries: Studies of the UK’s and China’s Animation Sectors. J. Open Innov. Technol. Mark. Complex. 2021, 7, 168. https://doi.org/10.3390/joitmc7030168

Liu Z. The Impact of Government Policy on Macro Dynamic Innovation of the Creative Industries: Studies of the UK’s and China’s Animation Sectors. Journal of Open Innovation: Technology, Market, and Complexity. 2021; 7(3):168. https://doi.org/10.3390/joitmc7030168

Chicago/Turabian StyleLiu, Zheng. 2021. "The Impact of Government Policy on Macro Dynamic Innovation of the Creative Industries: Studies of the UK’s and China’s Animation Sectors" Journal of Open Innovation: Technology, Market, and Complexity 7, no. 3: 168. https://doi.org/10.3390/joitmc7030168

APA StyleLiu, Z. (2021). The Impact of Government Policy on Macro Dynamic Innovation of the Creative Industries: Studies of the UK’s and China’s Animation Sectors. Journal of Open Innovation: Technology, Market, and Complexity, 7(3), 168. https://doi.org/10.3390/joitmc7030168