A 15 Year Ecological Comparison for the Market Dynamics of Minnesota Community Pharmacies from 2002 to 2017

Abstract

:1. Introduction

1.1. Background

1.2. Objectives

2. Methods

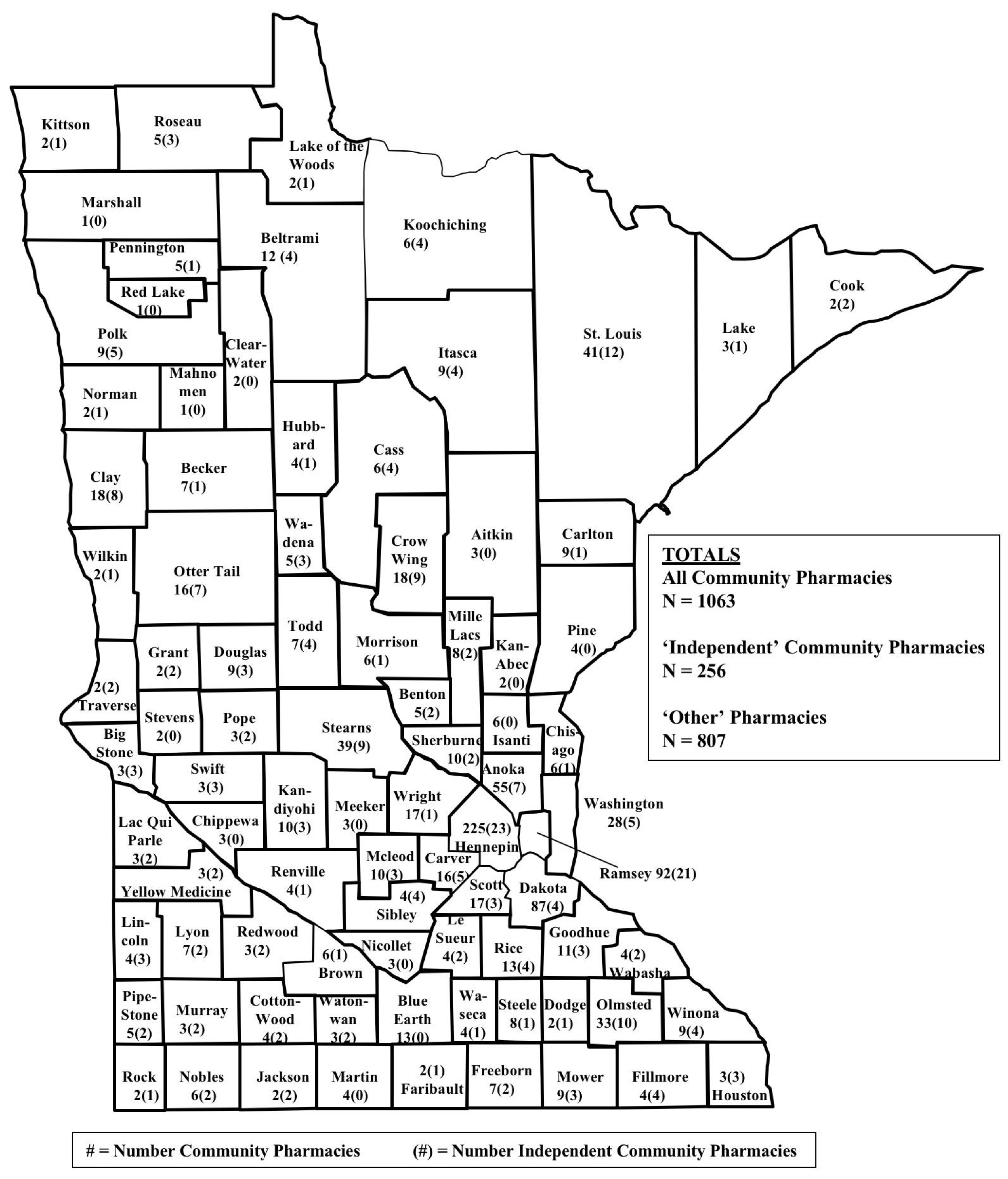

2.1. Data Sources

2.2. Data Analysis

2.3. Study Objective 1

2.3.1. Dependent Variables

- All community pharmacies: Per the state of Minnesota, an “established place(s) in which prescriptions, drugs, medicines, chemicals, and poisons are prepared, compounded, dispensed, vended, distributed, or sold to or for the use of non-hospitalized patients and from which related pharmaceutical care services are provided [24]”.

- Independent community pharmacies: A community pharmacy owned as a single entity or as part of an organization comprising of 10 or fewer community pharmacies.

- Chain community pharmacies: Any community pharmacy owned as part of an organization comprising of more than 10 community pharmacies.

2.3.2. Independent Variables

2.4. Study Objective 2

Variables

- Single entity: A business organization comprised of one pharmacy in a local market that would be classified under ‘Independent community pharmacies’ for objective 1.

- Small chain: A business organization comprised of 2–10 community pharmacies under common ownership (typically located in a local market) that would be classified under ‘Independent community pharmacies’ for objective 1.

- State/regional chain: A business organization comprised of greater than 10 community pharmacies under common ownership; distributed throughout Minnesota or the Midwest Region (Iowa, Illinois, Indiana, Kansas, Michigan, Minnesota, Missouri, North Dakota, Nebraska, Ohio, South Dakota, Wisconsin) and that would be classified under ‘Chain community pharmacies’ for objective 1.

- National chain: greater than 10 community pharmacies under common ownership; typically comprised of more than 1000 community pharmacies nationwide, located in most of the 50 states, and that would be classified under ‘Chain community pharmacies’ for objective 1.

- Health & Personal Care: establishment is considered a pharmacy that also has a “front end”. A relatively large amount of square footage is devoted to the pharmacy and over-the-counter products. Revenue from the pharmacy and over-the-counter product sales is relatively large. The typical reason for patronizing the business is to “go to the pharmacy.” Locational convenience is a primary patronage motive. This type of pharmacy has also been known as a retail pharmacy.

- Mass merchandiser: establishment is considered a big box retail store that also has a “pharmacy.” A relatively small amount of square footage is devoted to the pharmacy and over-the-counter products. Revenue from the pharmacy and over-the-counter product sales is relatively small. The typical reason for patrons to visit the business is to “go to the big box retailer.” Retail shopping convenience is a primary patronage motive.

- Supermarket: establishment is considered a grocery store that also has a “pharmacy.” A relatively small amount of square footage is devoted to the pharmacy and over-the-counter products. Revenue from the pharmacy and over-the-counter product sales is relatively small. The typical reason for patronizing the business is to “go to the grocery store.” Grocery shopping convenience is a primary patronage motive.

- Clinic/medical center: establishment is considered a clinic that also has a “pharmacy”. A relatively small amount of square footage is devoted to the pharmacy and over-the-counter products. Revenue from the pharmacy and over-the-counter product sales is relatively small. The typical reason for patronizing the business is to “go to the clinic”. In some cases, the pharmacy is a stand-alone business but is still considered to be closely associated with the clinic or medical center that is nearby. In many cases, the pharmacy name is the same as the clinic name (XYZ Clinic, XYZ Medical Center, XYZ Pharmacy). Health care visit convenience is a primary patronage motive.

- Specialty: establishment is considered a specialty business. Typically, all of the square footage is devoted to the pharmacy. Revenue for this business typically comes completely from the specialty services offered by the pharmacy. The typical reason for patronizing the business is to “receive unique pharmaceutical services” to meet patient care needs. Examples of specialty pharmacies include those focused upon renal services, compounding, veterinary pharmacy, long-term care, oncology, infusion, nuclear, outpatient treatment centers, HIV medication services, specialty pharmaceuticals. Need for specialty services is a primary patronage motive.

3. Results

4. Discussion

Study Limitations

5. Conclusions

Author Contributions

Acknowledgments

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

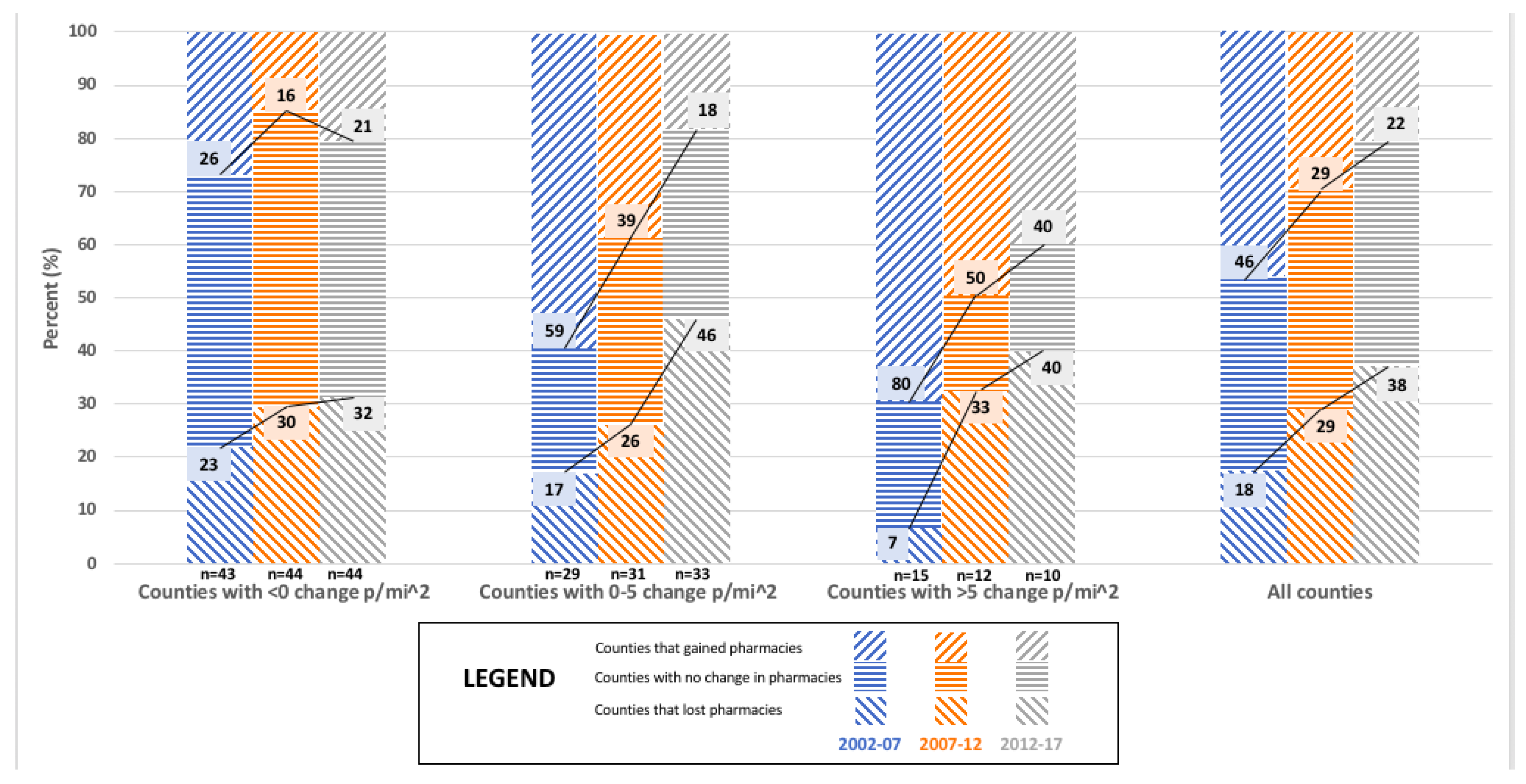

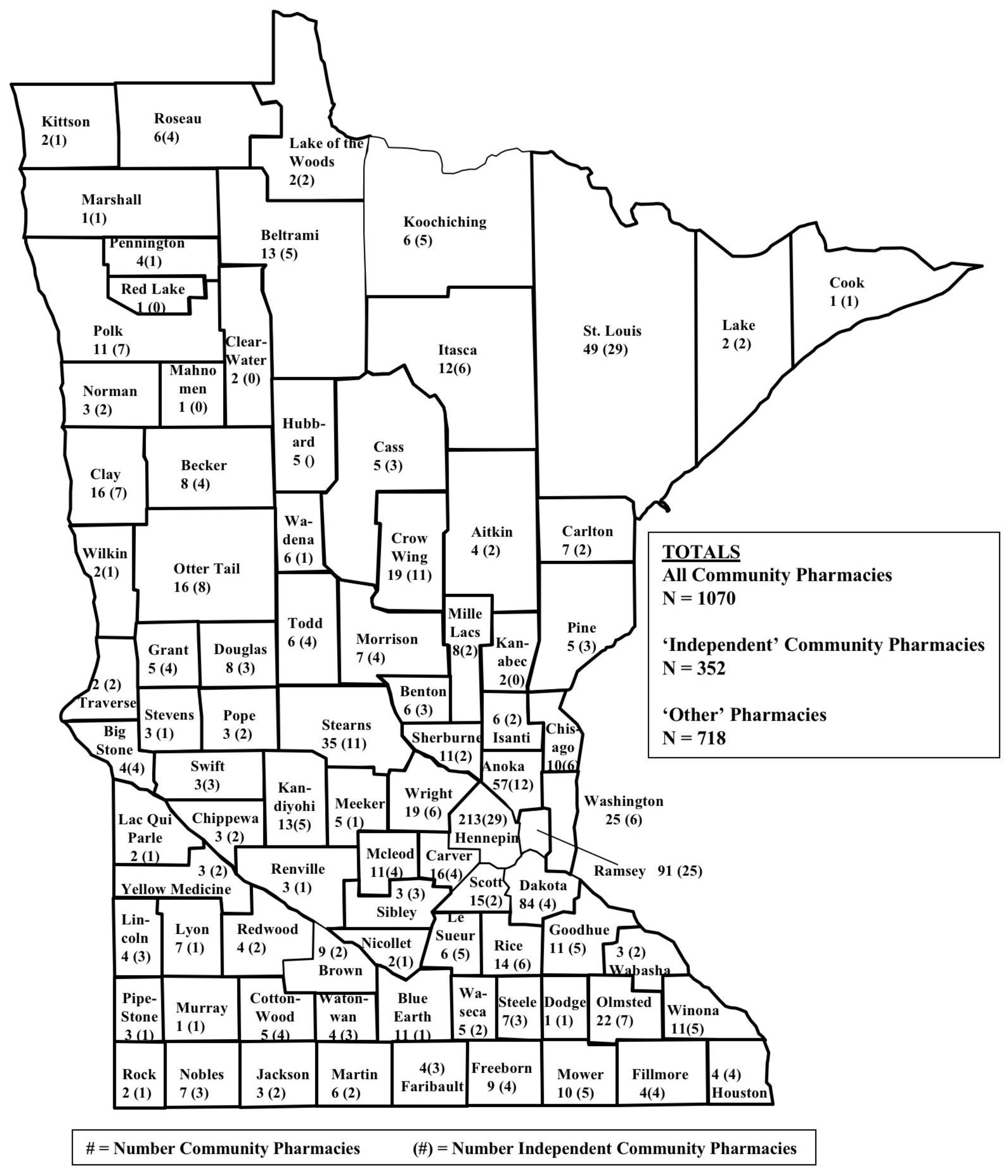

| Pharmacy Category Market Dynamic | Counties with <0 p/mi2 Change | Counties with 0–5 p/mi2 Change | Counties with >5 p/mi2 Change | Overall |

|---|---|---|---|---|

| N = 43 | N = 29 | N = 15 | N = 87 | |

| All community pharmacies | ||||

| Lost pharmacies | 23% | 17% | 7% | 18% |

| Stayed the same | 51% | 24% | 13% | 36% |

| Gained pharmacies | 26% | 59% | 80% | 46% |

| p = 0.002 | ||||

| Independent pharmacies | ||||

| Lost pharmacies | 56% | 41% | 80% | 55% |

| Stayed the same | 23% | 35% | 13% | 25% |

| Gained pharmacies | 21% | 24% | 7% | 20% |

| p = 0.185 | ||||

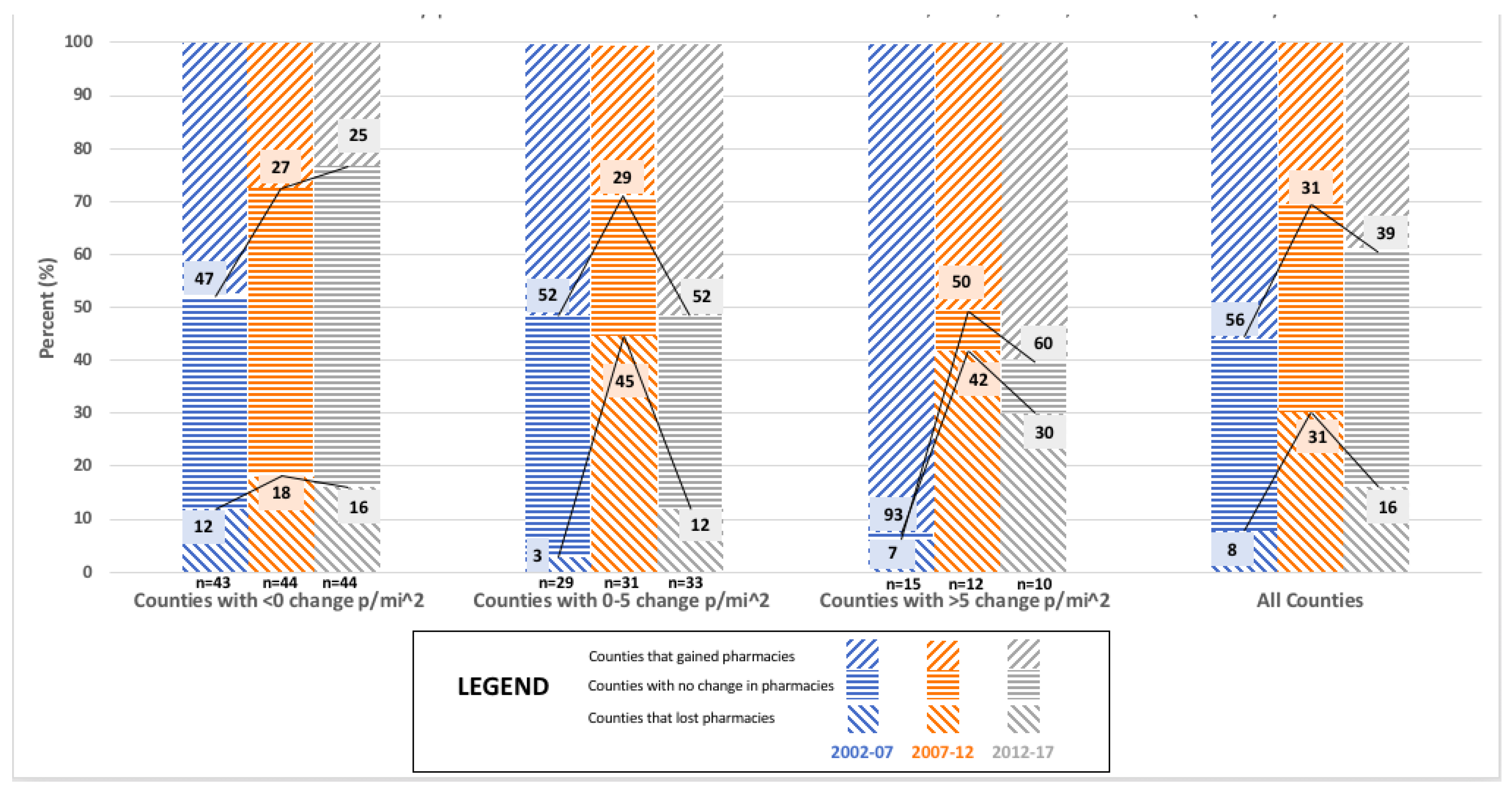

| Chain pharmacies | ||||

| Lost pharmacies | 12% | 3% | 7% | 8% |

| Stayed the same | 42% | 45% | 0% | 36% |

| Gained pharmacies | 47% | 52% | 93% | 56% |

| p = 0.014 |

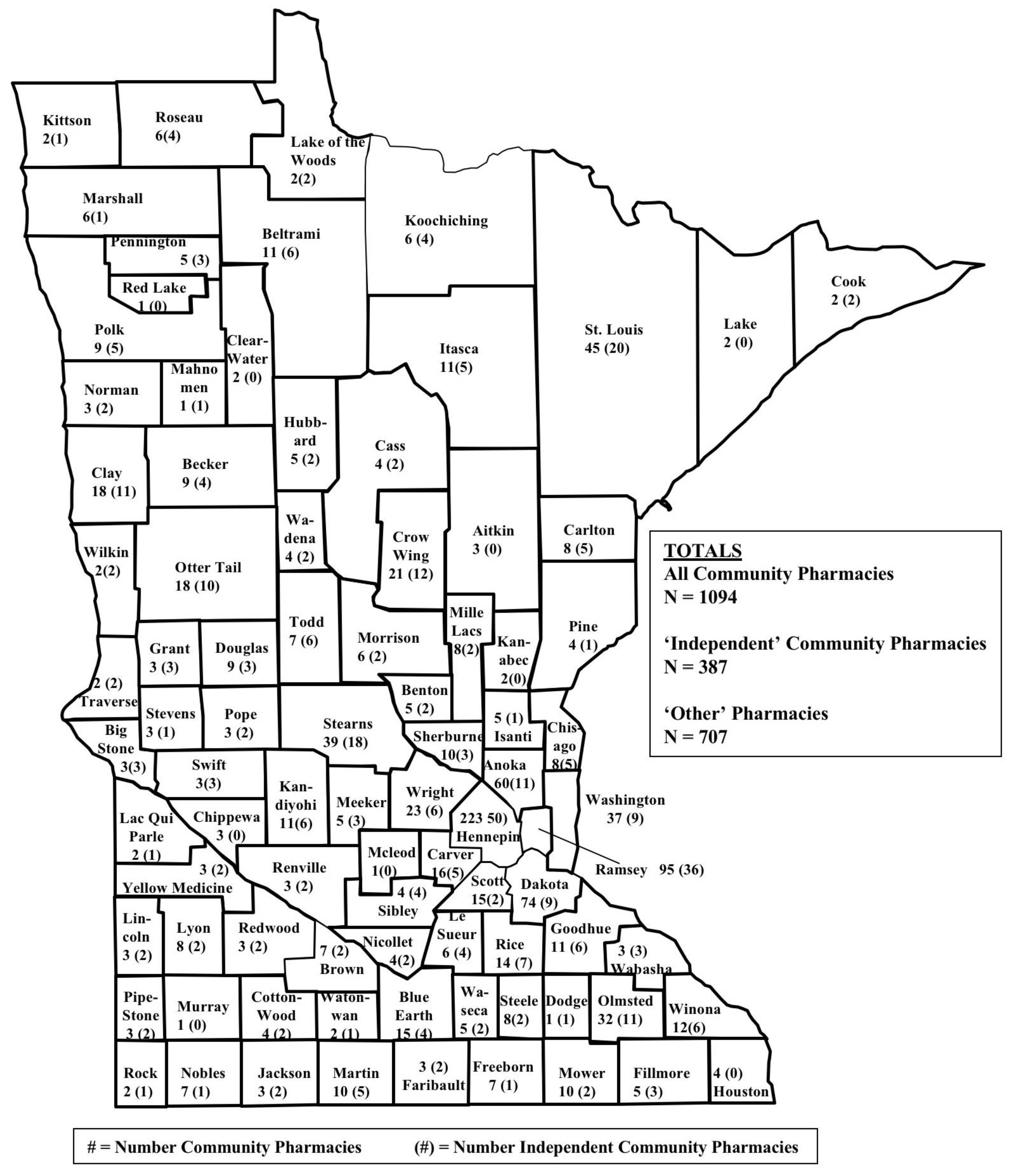

| Pharmacy Category Market Dynamic | Counties with <0 p/mi2 Change | Counties with 0–5 p/mi2 Change | Counties with >5 p/mi2 Change | Overall |

|---|---|---|---|---|

| N = 44 | N = 31 | N = 12 | N = 87 | |

| All community pharmacies | ||||

| Lost pharmacies | 30% | 26% | 33% | 29% |

| Stayed the same | 55% | 36% | 17% | 43% |

| Gained pharmacies | 16% | 39% | 50% | 29% |

| p = 0.052 | ||||

| Independent pharmacies | ||||

| Lost pharmacies | 43% | 23% | 25% | 33% |

| Stayed the same | 39% | 19% | 17% | 29% |

| Gained pharmacies | 18% | 58% | 58% | 38% |

| p = 0.005 | ||||

| Chain pharmacies | ||||

| Lost pharmacies | 18% | 45% | 42% | 31% |

| Stayed the same | 54% | 26% | 8% | 38% |

| Gained pharmacies | 27% | 29% | 50% | 31% |

| p = 0.009 |

| Pharmacy CategoryMarket Dynamic | Counties with <0 p/mi2 Change | Counties with 0–5 p/mi2 Change | Counties with >5 p/mi2 Change | Overall |

|---|---|---|---|---|

| N = 44 | N = 33 | N = 10 | N = 87 | |

| All community pharmacies | ||||

| Lost pharmacies | 32% | 46% | 40% | 38% |

| Stayed the same | 48% | 36% | 20% | 40% |

| Gained pharmacies | 21% | 18% | 40% | 22% |

| p = 0.349 | ||||

| Independent pharmacies | ||||

| Lost pharmacies | 43% | 61% | 80% | 54% |

| Stayed the same | 36% | 27% | 10% | 30% |

| Gained pharmacies | 21% | 12% | 10% | 16% |

| p = 0.234 | ||||

| Chain pharmacies | ||||

| Lost pharmacies | 16% | 12% | 30% | 16% |

| Stayed the same | 59% | 36% | 10% | 45% |

| Gained pharmacies | 25% | 52% | 60% | 39% |

| p = 0.022 |

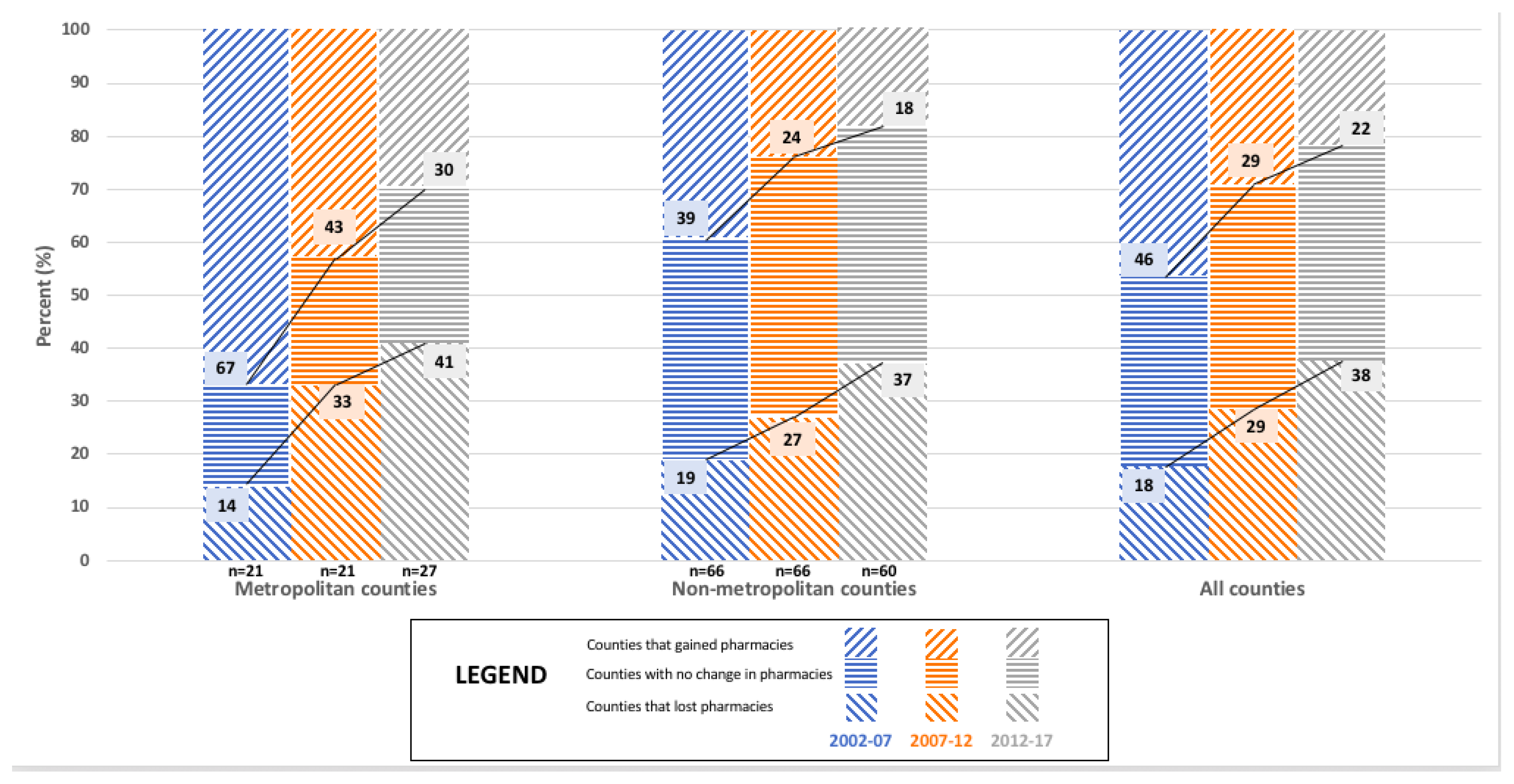

| Pharmacy CategoryMarket Dynamic | Metropolitan Counties | Non-Metropolitan Counties | Overall |

|---|---|---|---|

| N = 21 | N = 66 | N = 87 | |

| All community pharmacies | |||

| Lost pharmacies | 14% | 19% | 18% |

| Stayed the same | 19% | 41% | 36% |

| Gained pharmacies | 67% | 39% | 46% |

| p = 0.083 | |||

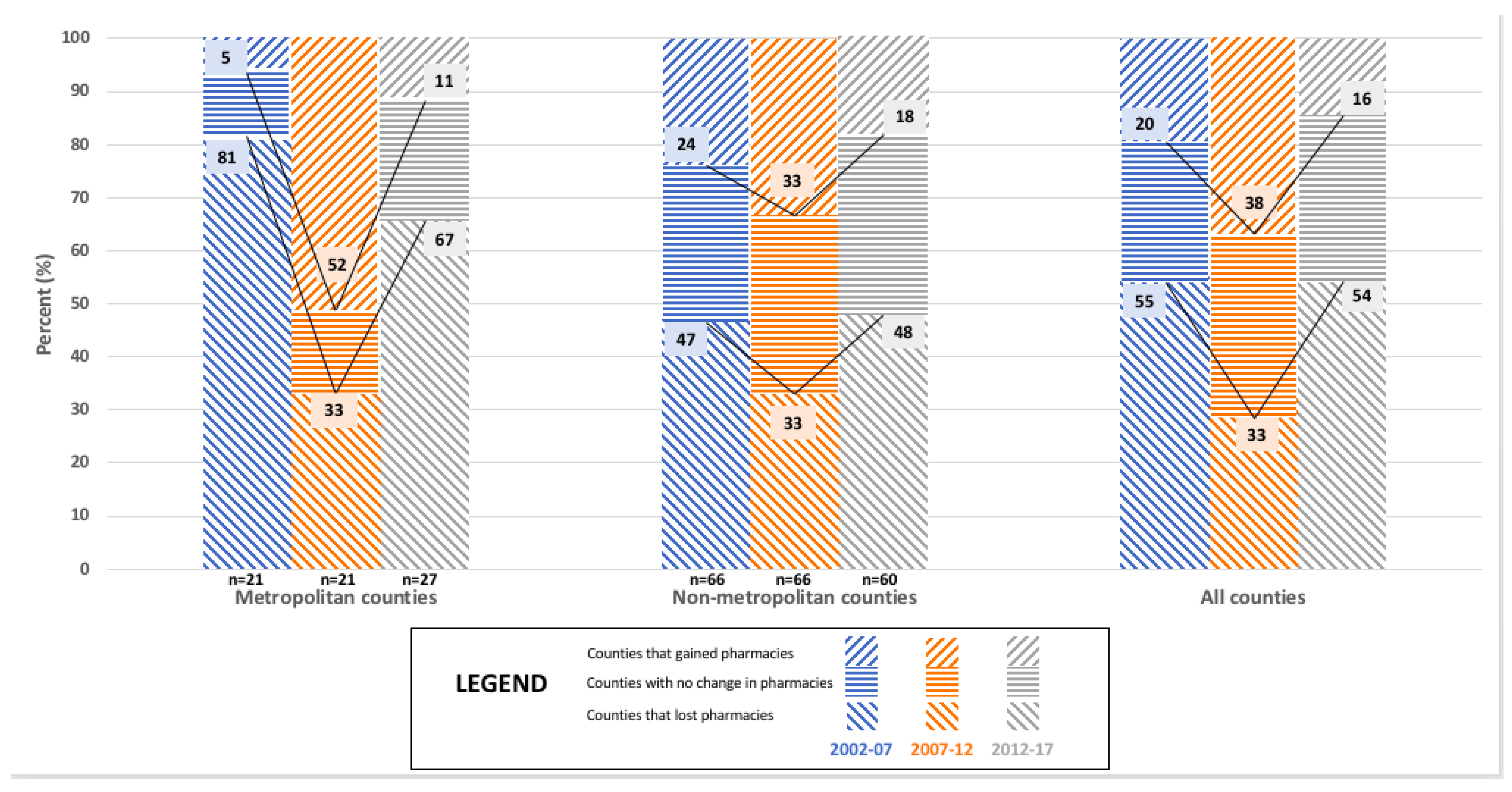

| Independent pharmacies | |||

| Lost pharmacies | 81% | 47% | 55% |

| Stayed the same | 14% | 29% | 25% |

| Gained pharmacies | 5% | 24% | 20% |

| p = 0.021 | |||

| Chain pharmacies | |||

| Lost pharmacies | 5% | 9% | 8% |

| Stayed the same | 19% | 41% | 36% |

| Gained pharmacies | 76% | 50% | 56% |

| p = 0.108 |

| Pharmacy CategoryMarket Dynamic | Metropolitan Counties | Non-Metropolitan Counties | Overall |

|---|---|---|---|

| N = 21 | N = 66 | N = 87 | |

| All community pharmacies | |||

| Lost pharmacies | 33% | 27% | 29% |

| Stayed the same | 24% | 49% | 43% |

| Gained pharmacies | 43% | 24% | 29% |

| p = 0.111 | |||

| Independent pharmacies | |||

| Lost pharmacies | 33% | 33% | 33% |

| Stayed the same | 14% | 33% | 29% |

| Gained pharmacies | 52% | 33% | 38% |

| p = 0.171 | |||

| Chain pharmacies | |||

| Lost pharmacies | 48% | 26% | 31% |

| Stayed the same | 24% | 42% | 38% |

| Gained pharmacies | 29% | 32% | 31% |

| p = 0.138 |

| Pharmacy CategoryMarket Dynamic | Metropolitan Counties | Non-Metropolitan Counties | Overall |

|---|---|---|---|

| N = 27 | N = 60 | N = 87 | |

| All community pharmacies | |||

| Lost pharmacies | 41% | 37% | 38% |

| Stayed the same | 30% | 45% | 40% |

| Gained pharmacies | 30% | 18% | 22% |

| p = 0.323 | |||

| Independent pharmacies | |||

| Lost pharmacies | 67% | 48% | 54% |

| Stayed the same | 22% | 33% | 30% |

| Gained pharmacies | 11% | 18% | 16% |

| p = 0.282 | |||

| Chain pharmacies | |||

| Lost pharmacies | 19% | 15% | 16% |

| Stayed the same | 22% | 55% | 45% |

| Gained pharmacies | 59% | 30% | 39% |

| p = 0.013 |

References

- Gaither, C.A.; Schommer, J.C.; Doucette, W.R.; Kreling, D.H.; Mott, D.A. Final Report of the 2014 National Sample Survey of the Pharmacist Workforce to Determine Contemporary Demographic Practice Characteristics and Quality of Work-Life; American Association of Colleges of Pharmacy: Arlington, VA, USA, 2015; Available online: https://www.aacp.org/sites/default/files/finalreportofthenationalpharmacistworkforcestudy2014.pdf (accessed on 7 May 2018).

- Bureau of Labor and Statistics. Occupational Employment and Wages, May 2017: 29-1051 Pharmacists. Occup. Employ. Stat. 2017, 9. Available online: https://www.bls.gov/oes/current/oes291051.htm (accessed on 7 May 2018).

- Cranor, C.W.; Christensen, D.B. The Asheville Project: Short-term outcomes of a community pharmacy diabetes care program. J. Am. Pharm. Assoc. 2003, 43, 149–159. Available online: http://www.ncbi.nlm.nih.gov/pubmed/12688433 (accessed on 8 May 2018). [CrossRef]

- Isetts, B.J.; Schondelmeyer, S.W.; Artz, M.B.; Lenarz, L.A.; Heaton, A.H.; Wadd, W.B.; Brown, L.M.; Cipolle, R.J. Clinical and economic outcomes of medication therapy management services: The Minnesota experience. J. Am. Pharm. Assoc. 2003, 48, 203–211. [Google Scholar] [CrossRef] [PubMed]

- Bacci, J.L.; McGrath, S.H.; Pringle, J.L.; Maguire, M.A.; McGivney, M.S. Implementation of targeted medication adherence interventions within a community chain pharmacy practice: The Pennsylvania Project. J. Am. Pharm. Assoc. 2014, 54, 584–593. [Google Scholar] [CrossRef] [PubMed]

- Qato, D.M.; Daviglus, M.L.; Wilder, J.; Lee, T.; Qato, D.; Lambert, B. “Pharmacy Deserts” Are Prevalent In Chicago’s Predominantly Minority Communities, Raising Medication Access Concerns. Health Aff. 2014, 33, 1958–1965. [Google Scholar] [CrossRef] [PubMed]

- Qato, D.M.; Zenk, S.; Wilder, J.; Harrington, R.; Gaskin, D.; Alexander, G.C. The availability of pharmacies in the United States: 2007–2015. van Wouwe JP, ed. PLoS ONE 2017, 12, e0183172. [Google Scholar] [CrossRef] [PubMed]

- Schommer, J.C.; Singh, R.L.; Cline, R.R.; Hadsall, R.S. Market dynamics of community pharmacies in Minnesota. Res. Soc. Adm. Pharm. 2006, 2, 347–358. [Google Scholar] [CrossRef] [PubMed]

- Schommer, J.C.; Yusuf, A.A.; Hadsall, R.S. Market dynamics of community pharmacies in Minnesota, U.S. from 1992 through 2012. Res. Soc. Adm. Pharm. 2014, 10, 217–231. [Google Scholar] [CrossRef] [PubMed]

- Minnesota Board of Pharmacy. Pharmacy Immunization Practice in Minnesota; Minnesota Board of Pharmacy: Minneapolis, MN, USA, 2016; Volume 2, Available online: www.health.state.mn.us/divs/idepc/immunize/hcp/protocols/ (accessed on 8 May 2018).

- Baroy, J.; Chung, D.; Frisch, R.; Apgar, D.; Slack, M.K. The impact of pharmacist immunization programs on adult immunization rates: A systematic review and meta-analysis. J. Am. Pharm. Assoc. 2016, 56, 418–426. [Google Scholar] [CrossRef] [PubMed]

- Salazar, D. Turning the Tide: Community Pharmacy Grapples with the Opioid Epidemic. Drug Store News 2018, 1. Available online: https://www.pharmacist.com/article/turning-tide-community-pharmacy-grapples-opioid-epidemic (accessed on 8 May 2018).

- National Association of Boards of Pharmacy. NABP Issues Policy Statement Supporting the Pharmacist’s Role in Increasing Access to Opioid Overdose Reversal Drug; National Association of Boards of Pharmacy: Mount Prospect, IL, USA, 2014; Available online: http://www.nabp.net/news/nabp-issues-policy-statement-supporting-the-pharmacist-s-role-in-increasing-access-to-opioid-overdose-reversal-drug (accessed on 8 May 2018).

- Smolen, A. Role of the Pharmacist in Proper Medication Disposal. US Pharm. 2011, 36, 52–55. [Google Scholar]

- Rickles, N.M.; Skelton, J.B.; Davis, J.; Hopson, J. Cognitive memory screening and referral program in community pharmacies in the United States. Int. J. Clin. Pharm. 2014, 36, 360–367. [Google Scholar] [CrossRef] [PubMed]

- Staudt, A.M.; Amtower, J.E.; George, J.; Daniels, N.C.; Allou, J.N.; Laswell, E.; Ballentine, J. The Correlation of Free Health Screenings at Community Pharmacies on Diabetes. Innov. Pharm. 2017, 8. [Google Scholar] [CrossRef] [Green Version]

- DeLoach, L.A.; Leonard, C.E.; Galdo, J.A. Specialty Pharmacy: What’s the Impact on Community Practice? US Pharm. 2016, 41, 35–40. Available online: https://www.uspharmacist.com/article/specialty-pharmacy-whats-the-impact-on-community-practice (accessed on 8 May 2018).

- Carrion, A.; Martin, T.S. The Affordable Care Act and the Pharmacist. US Pharm. 2015, 40, 33–38. [Google Scholar]

- Melody, K.; McCartney, E.; Sen, S.; Duenas, G. Optimizing care transitions: The role of the community pharmacist. Integr. Pharm. Res. Pract. 2016, 5, 43–51. [Google Scholar] [CrossRef] [PubMed]

- Pringle, J.L.; Rucker, N.L.; Domann, D.; Chan, C.; Tice, B.; Burns, A.L. Value-Based Incentives in Community Pharmacy. Am. J. Pharm. Benefits 2016, 8, 22–29. [Google Scholar]

- Minnesota Department of Health. Minnesota Board of Pharmacy. 2018. Available online: https://mn.gov/boards/pharmacy/ (accessed on 8 May 2018).

- US Census Bureau. Statistical Abstract of the United States; United States Department of Commerce: Washington, DC, USA. Available online: https://www.census.gov/history/www/reference/publications/statistical_abstracts.html (accessed on 7 May 2018).

- Minnesota State Demographic Center (SDC). Available online: https://mn.gov/admin/demography/ (accessed on 8 May 2018).

- The Office of the Revisor of Statutes. Minnesota Administrative Rules; Part 6800.0100; Minnesota Legislature: St. Paul, MN, USA, 2011; Volume 3. Available online: https://www.revisor.mn.gov/rules/?id=6800.0100 (accessed on 8 May 2018).

- Welch, D.; Burritt, C.; Coleman-Lochner, L. Retail’s Big Box Era at an End. Financ. Post 2012, 6. Available online: http://business.financialpost.com/news/retail-marketing/retails-big-box-era-at-an-end (accessed on 8 May 2018).

| Pharmacy Category Market Dynamic | 2002–2007 | 2007–2012 | 2012–2017 |

|---|---|---|---|

| All community pharmacies | |||

| Lost pharmacies | 18% | 29% | 38% |

| Stayed the same | 36% | 43% | 40% |

| Gained pharmacies | 46% | 29% | 22% |

| Independent pharmacies | |||

| Lost pharmacies | 55% | 33% | 54% |

| Stayed the same | 25% | 29% | 30% |

| Gained pharmacies | 20% | 38% | 16% |

| Chain pharmacies | |||

| Lost pharmacies | 8% | 31% | 16% |

| Stayed the same | 36% | 38% | 45% |

| Gained pharmacies | 56% | 31% | 39% |

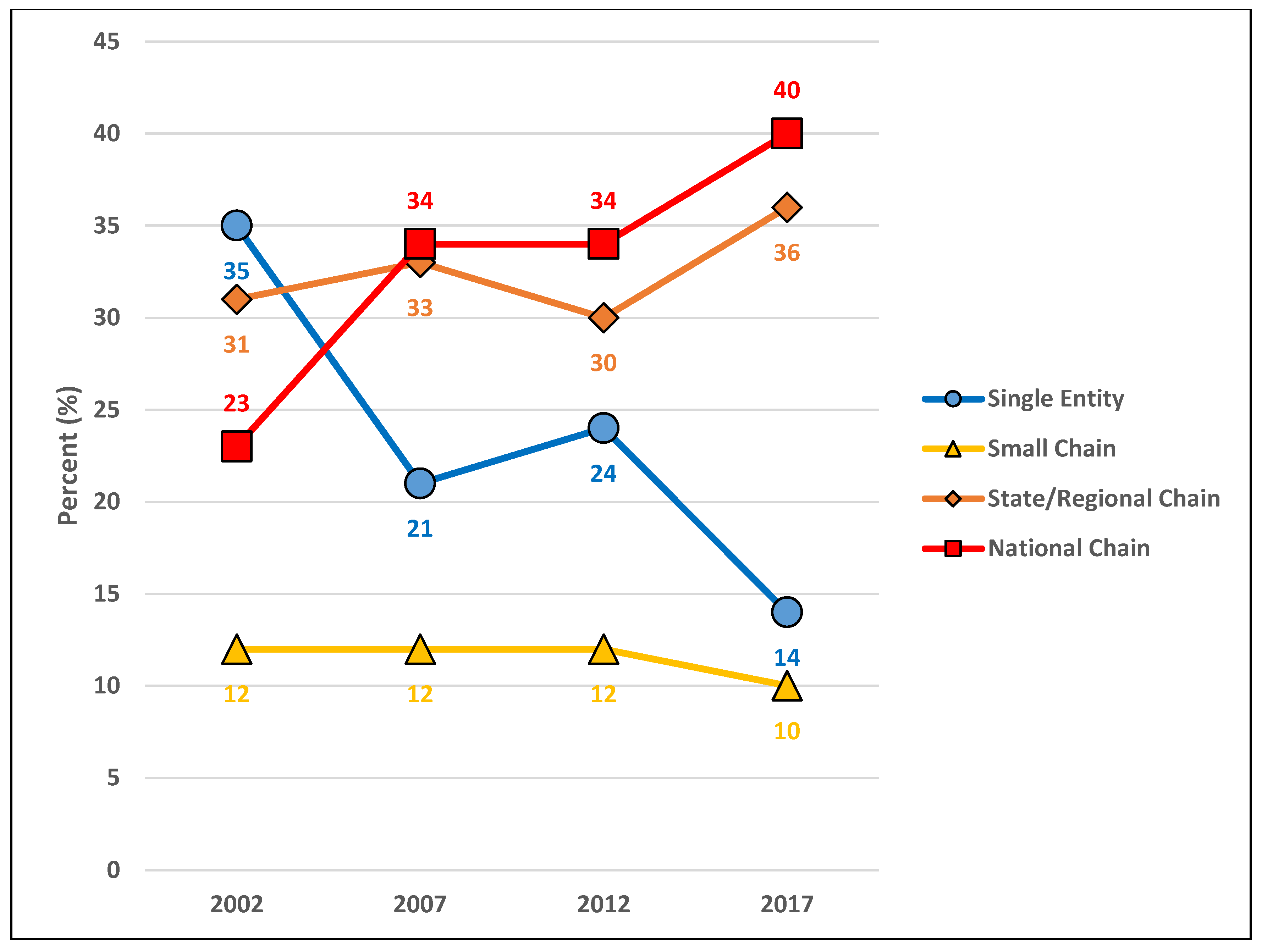

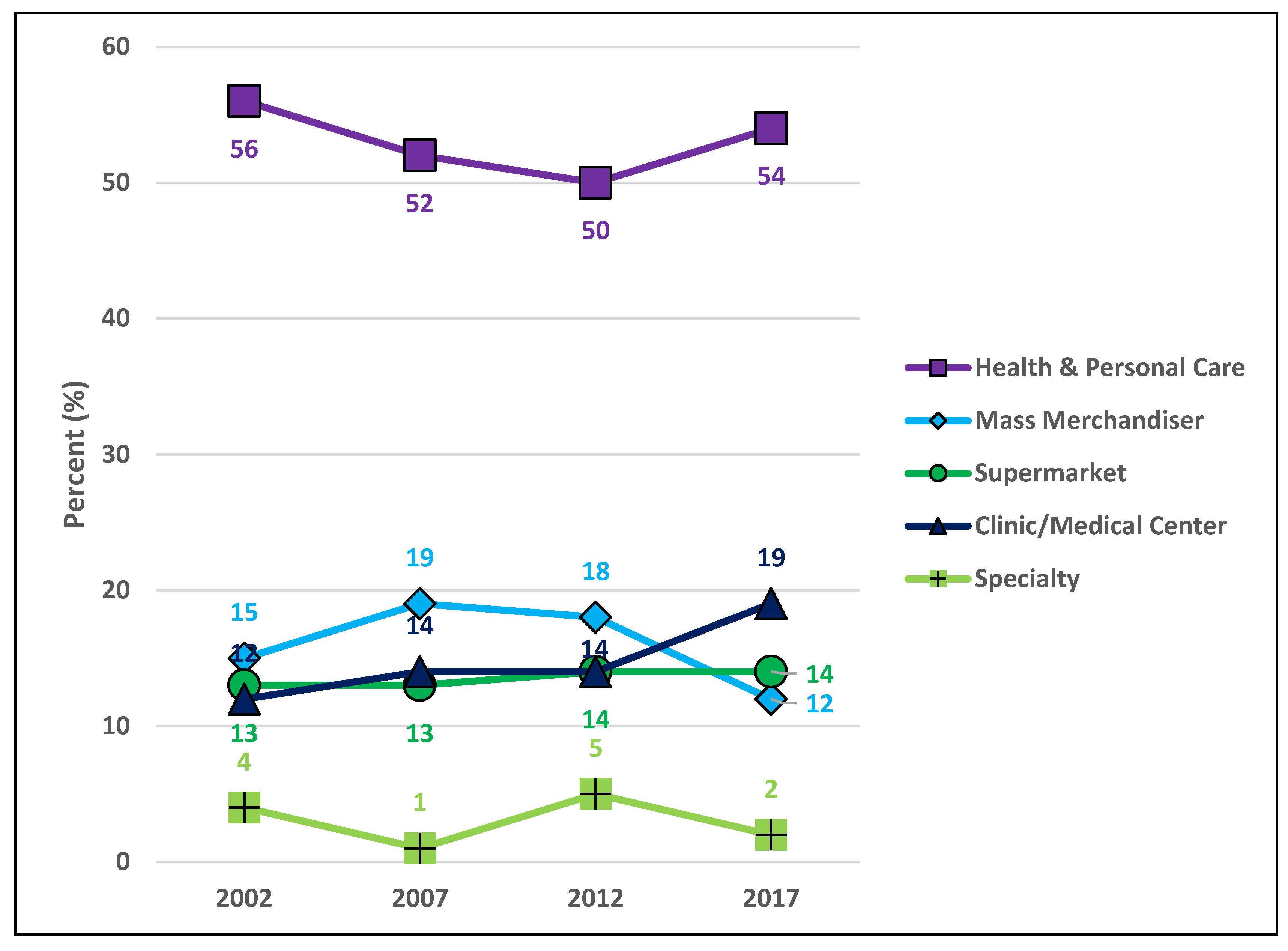

| Business Organization Structure | Pharmacy Type | 2002 | 2007 | 2012 | 2017 |

|---|---|---|---|---|---|

| N = 996 | N = 1070 | N = 1094 | N = 1063 | ||

| Single entity | Health & Personal Care | 281 (28%) | 185 (17%) | 199 (18%) | 127 (12%) |

| Mass merchandiser | 0 (0%) | 0 (0%) | 0 (0%) | 0 (0%) | |

| Supermarket | 0 (0%) | 0 (0%) | 0 (0%) | 0 (0%) | |

| Clinic/medical center | 36 (4%) | 32 (3%) | 28 (3%) | 19 (2%) | |

| Specialty | 29 (3%) | 10 (1%) | 33 (3%) | 5 (1%) | |

| Total | 346 (35%) | 227 (21%) | 260 (24%) | 151 (14%) | |

| Small chain | Health & Personal Care | 98 (10%) | 97 (9%) | 91 (8%) | 83 (8%) |

| Mass merchandiser | 0 (0%) | 0 (0%) | 0 (0%) | 0 (0%) | |

| Supermarket | 0 (0%) | 0 (0%) | 0 (0%) | 0 (0%) | |

| Clinic/medical center | 20 (2%) | 26 (2%) | 30 (3%) | 17 (2%) | |

| Specialty | 2 (<1%) | 2 (<1%) | 6 (1%) | 5 (1%) | |

| Total | 120 (12%) | 125 (12%) | 127 (12%) | 105 (10%) | |

| ALL INDEPENDENTS (=Single entity +Small chain) | 466 (47%) | 352 (33%) | 387 (35%) | 256 (24%) | |

| State/regional | Health & Personal Care | 99 (10%) | 120 (11%) | 63 (6%) | 66 (6%) |

| chain | Mass merchandiser | 13 (1%) | 0 (0%) | 17 (2%) | 0 (0%) |

| Supermarket | 127 (13%) | 139 (13%) | 155 (14%) | 150 (14%) | |

| Clinic/medical center | 61 (6%) | 96 (9%) | 83 (8%) | 162 (15%) | |

| Specialty | 5 (1%) | 0 (0%) | 12 (1%) | 5 (1%) | |

| Total | 305 (31%) | 355 (33%) | 330 (30%) | 383 (36%) | |

| National chain | Health & Personal Care | 81 (8%) | 152 (14%) | 201 (18%) | 294 (28%) |

| Mass merchandiser | 144 (14%) | 209 (20%) | 173 (16%) | 127 (12%) | |

| Supermarket | 0 (0%) | 0 (0%) | 0 (0%) | 0 (0%) | |

| Clinic/medical center | 0 (0%) | 0 (0%) | 0 (0%) | 0 (0%) | |

| Specialty | 0 (0%) | 2 (<1%) | 3 (<1%) | 2 (<1%) | |

| Total | 225 (23%) | 363 (34%) | 377 (34%) | 423 (40%) | |

| ALL CHAIN (=State/regional chain + National chain) | 530 (53%) | 718 (67%) | 707 (65%) | 807 (76%) |

© 2018 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Olson, A.W.; Schommer, J.C.; Hadsall, R.S. A 15 Year Ecological Comparison for the Market Dynamics of Minnesota Community Pharmacies from 2002 to 2017. Pharmacy 2018, 6, 50. https://doi.org/10.3390/pharmacy6020050

Olson AW, Schommer JC, Hadsall RS. A 15 Year Ecological Comparison for the Market Dynamics of Minnesota Community Pharmacies from 2002 to 2017. Pharmacy. 2018; 6(2):50. https://doi.org/10.3390/pharmacy6020050

Chicago/Turabian StyleOlson, Anthony W., Jon C. Schommer, and Ronald S. Hadsall. 2018. "A 15 Year Ecological Comparison for the Market Dynamics of Minnesota Community Pharmacies from 2002 to 2017" Pharmacy 6, no. 2: 50. https://doi.org/10.3390/pharmacy6020050

APA StyleOlson, A. W., Schommer, J. C., & Hadsall, R. S. (2018). A 15 Year Ecological Comparison for the Market Dynamics of Minnesota Community Pharmacies from 2002 to 2017. Pharmacy, 6(2), 50. https://doi.org/10.3390/pharmacy6020050