Re-Examining the Effects of Official Development Assistance on Foreign Direct Investment Applying the VAR Model

Abstract

:1. Introduction

2. Literature Review

3. Materials and Methods

3.1. The Generalized Method of Moments (GMM) Estimation with Gravity Model

3.1.1. Estimation Equation

3.1.2. The GMM Estimation

3.2. Estimations with Panel VAR Model

3.2.1. Panel VAR Model

3.2.2. Panel Unit Root Test

3.2.3. Panel Granger Causality Test

3.2.4. Impulse Response Analysis

3.3. Data

4. Results

4.1. Results of GMM Estimation with the Gravity Model

4.1.1. Impact of ODA from All Donor Countries on FDI

4.1.2. Impact of ODA from Major Donor Countries on Their Own FDI

4.1.3. Impact of ODA from Each Major Donor Country on FDI

4.1.4. Impact of ODA from Each Major Donor Country on Their Own FDI

4.2. Results of Granger Causality Test with Panel VAR Model

4.2.1. Results of Panel Unit Root Tests

4.2.2. Results of Lag Length Selection

4.2.3. Results of Panel Granger Causality Test

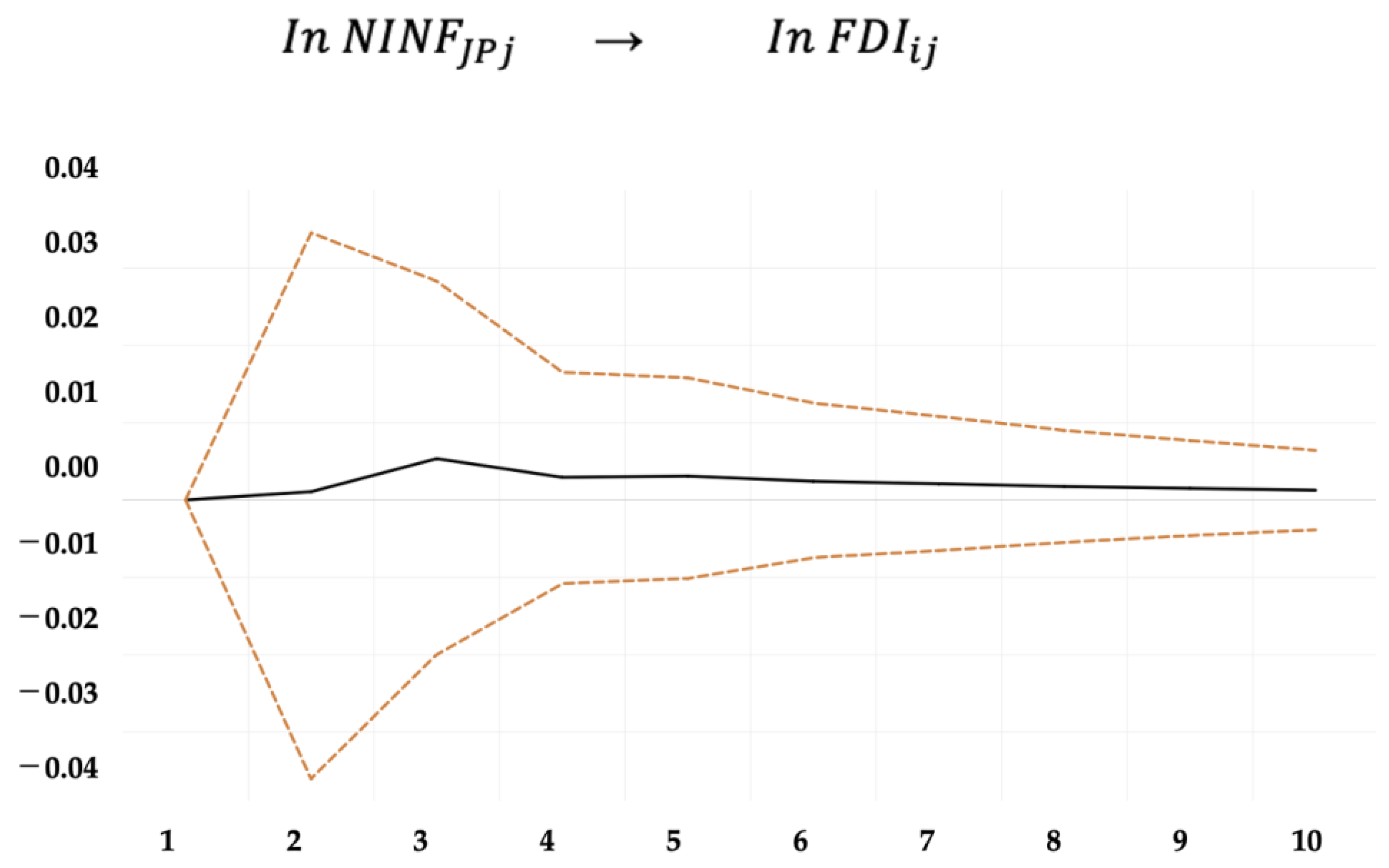

4.2.4. Results of Impulse Response Analysis

5. Discussion

5.1. Negative Effect of Japanese ODA for Non-Infrastructure Sectors on FDI from Major Donor Countries

5.2. Vanguard Effect of Japanese ODA

6. Conclusions

- Since only the GMM estimation result was significant and the results of the Granger causality test and impulse response analysis were not significant, it cannot be concluded that Japan’s ODA to non-infrastructure sectors had a negative impact on FDI.

- The vanguard effect of Japan’s ODA that previous studies (Kang et al. 2011; Kimura and Todo 2010) have pointed to was not significant since the 2000s.

- Since the 2000s, there have been no robust results showing that “ODA has affected on FDI”.

- It is suggested that the vanguard effect of Japanese ODA pointed out by previous studies appeared mainly in the 1990s and may not be sustainable.

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| 1 | Argentina | 17 | Mozambique |

| 2 | Brazil | 18 | Nigeria |

| 3 | Cambodia | 19 | Oman |

| 4 | Chile | 20 | Pakistan |

| 5 | China | 21 | Panama |

| 6 | Colombia | 22 | Peru |

| 7 | Egypt | 23 | Philippines |

| 8 | India | 24 | Saudi Arabia |

| 9 | Indonesia | 25 | South Africa |

| 10 | Iran | 26 | Thailand |

| 11 | Iraq | 27 | Trinidad Tobago |

| 12 | Kazakhstan | 28 | Tunisia |

| 13 | Malaysia | 29 | Turkey |

| 14 | Mauritius | 30 | Ukraine |

| 15 | Mexico | 31 | Uruguay |

| 16 | Morocco | 32 | Viet Nam |

References

- Akaike, Hirotogu. 1998. Information Theory and an Extension of the Maximum Likelihood Principle. In Selected Papers of Hirotugu Akaike. Edited by Emanuel Parzen, Kunio Tanabe and Genshiro Kitagawa. Springer Series in Statistics; New York: Springer, pp. 199–213. [Google Scholar] [CrossRef]

- Ali, Minhaj, Shujahat H. Hashmi, Muhammad R. Nazir, Ahmer Bilal, and Muhammad I. Nazir. 2021. Does Financial Inclusion Enhance Economic Growth? Empirical Evidence from the IsDB Member Countries. International Journal of Finance & Economics 26: 5235–58. [Google Scholar] [CrossRef]

- Arellano, Manuel, and Olympia Bover. 1995. Another Look at the Instrumental Variable Estimation of Error-Components Models. Journal of Econometrics 68: 29–51. [Google Scholar] [CrossRef]

- Aslan, Alper, Oguz Ocal, Baki Ozsolak, and Ilhan Ozturk. 2022. Renewable Energy and Economic Growth Relationship under the Oil Reserve Ownership: Evidence from Panel VAR Approach. Renewable Energy 188: 402–10. [Google Scholar] [CrossRef]

- Beladi, Hamid, and Reza Oladi. 2006. Does Foreign Aid Impede Foreign Investment? Economics Research Institute Study Paper 19: 1–31. [Google Scholar]

- Blonigen, Bruce A., and Jeremy Piger. 2014. Determinants of foreign direct investment. Canadian Journal of Economics/Revue canadienne d’économique 47: 775–812. [Google Scholar] [CrossRef]

- Blundell, Richard, and Stephen Bond. 1998. Initial Conditions and Moment Restrictions in Dynamic Panel Data Models. Journal of Econometrics 87: 115–43. [Google Scholar] [CrossRef]

- Cheng, Si, and Shaozhou Qi. 2021. The Potential for China’s Outward Foreign Direct Investment and Its Determinants: A Comparative Study of Carbon-Intensive and Non-Carbon-Intensive Sectors along the Belt and Road. Journal of Environmental Management 282: 111960. [Google Scholar] [CrossRef] [PubMed]

- Cipollina, Maria, Giorgia Giovannetti, Filomena Pietrovito, and Alberto F. Pozzolo. 2012. FDI and Growth: What Cross-Country Industry Data Say. The World Economy 35: 1599–1629. [Google Scholar] [CrossRef]

- Eaton, Jonathan, and Akiko Tamura. 1994. Bilateralism and Regionalism in Japanese and U.S. Trade and Direct Foreign Investment Patterns. Journal of the Japanese and International Economies 8: 478–510. [Google Scholar] [CrossRef]

- Efron, Bradley, and Robert J. Tibshirani. 1993. An Introduction to the Bootstrap. Monographs on Statistics and Applied Probability 57. New York: Chapman & Hall. Available online: https://m.kulib.kyoto-u.ac.jp/webopac/TY86157429 (accessed on 22 August 2022).

- Erdil, Erkan, and I. Hakan Yetkiner. 2009. The Granger-Causality between Health Care Expenditure and Output: A Panel Data Approach. Applied Economics 41: 511–18. [Google Scholar] [CrossRef]

- Garriga, Ana Carolina, and Brian J. Phillips. 2014. Foreign Aid as a Signal to Investors: Predicting FDI in Post-Conflict Countries. Journal of Conflict Resolution 58: 280–306. [Google Scholar] [CrossRef]

- Haini, Hazwan, and Pauline Tan. 2022. Re-Examining the Impact of Sectoral- and Industrial-Level FDI on Growth: Does Institutional Quality, Education Levels and Trade Openness Matter? Australian Economic Papers. n/a (n/a). Available online: https://doi.org/10.1111/1467-8454.12253 (accessed on 22 August 2022). [CrossRef]

- Harms, Philipp, and Matthias Lutz. 2006. Aid, Governance and Private Foreign Investment: Some Puzzling Findings for the 1990s*. The Economic Journal 116: 773–90. [Google Scholar] [CrossRef]

- Hsiao, Frank S. T., and Mei-Chu W. Hsiao. 2006. FDI, Exports, and GDP in East and Southeast Asia—Panel Data versus Time-Series Causality Analyses. Journal of Asian Economics 17: 1082–106. [Google Scholar] [CrossRef]

- Iamsiraroj, Sasi. 2016. The Foreign Direct Investment–Economic Growth Nexus. International Review of Economics & Finance 42: 116–33. [Google Scholar] [CrossRef]

- Iida, Kazuto. 2010. Development of Foreign Direct Investment and Establishment of Global Capital in Japan. Wagakoku ni okeru kaigai chokusetsu toushi no tenkai to global shihon no kakuritsu. Seikeironso 78: 1–39. (In Japanese). [Google Scholar]

- Irshad, Mohd, and Syed Hasan Qayed. 2022. Casual Nexus between Economic Growth, FDI and Employment: An Inquiry into BRICS and ASEAN. Theoretical and Applied Economics XXIX: 107–24. [Google Scholar]

- Japan External Trade Organization. 2014. FDI Flow (Based on Reports and Notifications, Gross). JETRO. Available online: https://www.jetro.go.jp/en/reports/statistics.html (accessed on 19 June 2022).

- Juodis, Artūras, Yiannis Karavias, and Vasilis Sarafidis. 2021. A Homogeneous Approach to Testing for Granger Non-Causality in Heterogeneous Panels. Empirical Economics 60: 93–112. [Google Scholar] [CrossRef]

- Kang, Sung Jin, Hongshik Lee, and Bokyeong Park. 2011. Does Korea Follow Japan in Foreign Aid? Relationships between Aid and Foreign Investment. Japan and the World Economy 23: 19–27. [Google Scholar] [CrossRef]

- Karakaplan, Ugur, Bilin Neyapti, and Selin Sayek. 2005. Aid and Foreign Direct Investment: International Evidence. Working Paper 2005/12. Discussion Paper. Available online: https://www.econstor.eu/handle/10419/83262 (accessed on 4 May 2021).

- Kaufmann, Daniel, Aart Kraay, and Massimo Mastruzzi. 2010. The Worldwide Governance Indicators: Methodology and Analytical Issues. SSRN Scholarly Paper ID 1682130. Rochester: Social Science Research Network. Available online: https://papers.ssrn.com/abstract=1682130 (accessed on 9 February 2022).

- Kim, Dai-Won, Jung-Suk Yu, and M. Kabir Hassan. 2018. Financial Inclusion and Economic Growth in OIC Countries. Research in International Business and Finance 43: 1–14. [Google Scholar] [CrossRef]

- Kimura, Hidemi, and Yasuyuki Todo. 2010. Is Foreign Aid a Vanguard of Foreign Direct Investment? A Gravity-Equation Approach. World Development 38: 482–97. [Google Scholar] [CrossRef]

- Levin, Andrew, Chien-Fu Lin, and Chia-Shang James Chu. 2002. Unit Root Tests in Panel Data: Asymptotic and Finite-Sample Properties. Journal of Econometrics 108: 1–24. [Google Scholar] [CrossRef]

- Liao, Hongwei, Yedi Chi, and Jiarui Zhang. 2020. Impact of International Development Aid on FDI along the Belt and Road. China Economic Review 61: 101448. [Google Scholar] [CrossRef]

- Ly-My, Dung, and Hyun-Hoon Lee. 2019. Effects of Aid for Trade on Extensive and Intensive Margins of Greenfield FDI. The World Economy 42: 2120–43. [Google Scholar] [CrossRef]

- Markusen, James R. 1984. Multinationals, Multi-Plant Economies, and the Gains from Trade. Journal of International Economics 16: 205–26. [Google Scholar] [CrossRef]

- Mihut, Marius Ioan. 2014. Plazza Acord and the ‘Explosion’ of the Japanese FDI. Procedia Economics and Finance 15: 721–29. [Google Scholar] [CrossRef]

- Ministry of Foreign Affairs of Japan. 1992. Japan’s Official Development Assistance Charter. June 30. Available online: https://www.mofa.go.jp/policy/oda/summary/1999/ref1.html (accessed on 19 June 2022).

- Ministry of Foreign Affairs of Japan. 2004a. Chapter 1 The Situation Surrounding Japan’s ODA and Revision of the ODA Charter. In Japan’s Official Development Assistance White Paper 2003 “Goals of the Revised ODA Charter”; Vol. Part I. The Revision of the “ODA Charter” and Japan’s New Approach. Available online: https://www.mofa.go.jp/policy/oda/white/2003/index03.html (accessed on 19 June 2022).

- Ministry of Foreign Affairs of Japan. 2004b. Chapter 2. Progress of 50 Years of ODA. In Japan’s Official Development Assistance White Paper 2004 “Accomplishments and Progress of 50 Years”; Part I. Accomplishments and Progress of 50 Years:37. Available online: https://www.mofa.go.jp/policy/oda/white/2004/index.html (accessed on 19 June 2022).

- Ministry of Foreign Affairs of Japan. 2004c. Japan’s Official Development Assistance Charter. Ministry of Foreign Affairs of Japan, November 30. Available online: https://www.mofa.go.jp/policy/oda/reform/charter.html (accessed on 19 June 2022).

- Ministry of Foreign Affairs of Japan. 2015. Cabinet Decision on the Development Cooperation Charter. Available online: https://www.mofa.go.jp/policy/oda/page_000138.html (accessed on 21 December 2020).

- Ministry of Foreign Affairs of Japan. 2016. Japanese Debt Relief Measures (Amount of Public Debt Forgiven) (Approximate Value). Wagakuni no saimu kyusai sochi (koteki saimu menjo-gaku) (gaisan-chi). Ministry of Foreign Affairs of Japan. Available online: https://www.mofa.go.jp/mofaj/gaiko/oda/seisaku/keitai/enshakan/saimuhouki.html (accessed on 12 February 2022). (In Japanese)

- Ministry of Foreign Affairs of Japan. 2021. ODA Budget. ODA yosan. Ministry of Foreign Affairs of Japan. Available online: https://www.mofa.go.jp/mofaj/gaiko/oda/shiryo/yosan.html (accessed on 21 September 2021). (In Japanese)

- Mishra, Bikash Ranjan, and Pabitra Kumar Jena. 2019. Bilateral FDI Flows in Four Major Asian Economies: A Gravity Model Analysis. Journal of Economic Studies 46: 71–89. [Google Scholar] [CrossRef]

- Morshed, Niaz, and Mohammad Razib Hossain. 2022. Causality Analysis of the Determinants of FDI in Bangladesh: Fresh Evidence from VAR, VECM and Granger Causality Approach. SN Business & Economics 2: 64. [Google Scholar] [CrossRef]

- Organisation for Economic Co-operation and Development (OECD). 2002. Foreign Direct Investment for Development: Maximising Benefits, Minimising. Available online: https://www.oecd.org/investment/investmentfordevelopment/foreigndirectinvestmentfordevelopmentmaximisingbenefitsminimisingcosts.htm (accessed on 20 December 2021).

- Organisation for Economic Co-operation and Development (OECD). 2020. “What Is ODA?” OECD. Available online: http://www.oecd.org/dac/financing-sustainable-development/development-finance-standards/What-is-ODA.pdf (accessed on 23 November 2020).

- Ouyang, Yaofu, and Peng Li. 2018. On the Nexus of Financial Development, Economic Growth, and Energy Consumption in China: New Perspective from a GMM Panel VAR Approach. Energy Economics 71: 238–52. [Google Scholar] [CrossRef]

- Pradhan, Rudra P., Mak B. Arvin, Neville R. Norman, and Samadhan K. Bele. 2014. Economic Growth and the Development of Telecommunications Infrastructure in the G-20 Countries: A Panel-VAR Approach. Telecommunications Policy 38: 634–49. [Google Scholar] [CrossRef]

- Razzaq, Asif, Hui An, and Sarath Delpachitra. 2021. Does Technology Gap Increase FDI Spillovers on Productivity Growth? Evidence from Chinese Outward FDI in Belt and Road Host Countries. Technological Forecasting and Social Change 172: 121050. [Google Scholar] [CrossRef]

- Rezitis, Anthony N. 2015. The Relationship between Agricultural Commodity Prices, Crude Oil Prices and US Dollar Exchange Rates: A Panel VAR Approach and Causality Analysis. International Review of Applied Economics 29: 403–34. [Google Scholar] [CrossRef]

- Rossi, Barbara, and Yiru Wang. 2019. VAR-Based Granger-Causality Test in the Presence of Instabilities. Economic Working Paper Series 1642: 15. [Google Scholar]

- Selaya, Pablo, and Eva Rytter Sunesen. 2012. Does Foreign Aid Increase Foreign Direct Investment? World Development 40: 2155–76. [Google Scholar] [CrossRef]

- Stock, James H., and Mark W. Watson. 2001. Vector Autoregressions. Journal of Economic Perspectives 15: 101–15. [Google Scholar] [CrossRef]

- Wang, Haijun, Hu Yang, Fengya Li, and Min Zhang. 2022. Does Foreign Aid Reduce the Country’s Risk of OFDI? The Chinese Experience. International Studies of Economics. July. Available online: https://doi.org/10.1002/ise3.20 (accessed on 31 July 2022). [CrossRef]

- Windmeijer, Frank. 2005. A Finite Sample Correction for the Variance of Linear Efficient Two-Step GMM Estimators. Journal of Econometrics 126: 25–51. [Google Scholar] [CrossRef]

- Wooldridge, Jeffrey M. 2012. Introductory Econometrics: A Modern Approach, 5th ed. Mason: Cengage Learning, p. 642. [Google Scholar]

| Variable | Description |

|---|---|

| ln FDIij | Log of real Foreign Direct Investment (FDI) flow from country i to j (BMD3: 2003–2013, BMD4: 2014–2020) from OECD.Stat |

| ln AID_Allj | Log of total real Official Development Assistance (ODA) gross disbursement flow from all DAC countries to j (CRS code 1000s − code 900s) from OECD.Stat |

| ln INF_Allj | Log of total real ODA for infrastructure gross disbursement flow from all DAC countries to j (CRS code 200s + 300s + 400s) from OECD.Stat |

| ln NINF_Allj | Log of total real ODA for non-infrastructure gross disbursement flow from all DAC countries to j (CRS code 500s + 600s + 700s) from OECD.Stat |

| ln AIDij | Log of total real ODA gross disbursement flow from country i to j (CRS code 1000s − code 900s) from OECD.Stat |

| ln INFij | Log of total real ODA gross for infrastructure disbursement flow from country i to j (CRS code 200s + 300s + 400s) from OECD.Stat |

| ln NINFij | Log of total real ODA for non-infrastructure gross disbursement flow from country i to j (CRS code 500s + 600s + 700s) from OECD.Stat |

| ln GDPi | Log of real GDP of donor country i from WDI |

| ln GDPj | Log of real GDP of recipient country j from WDI |

| ln GOVj | Log of Sum of 6 indicators of governance (level of voice and accountability, political stability, government effectiveness, regulatory quality, rule of law, and level of accountability) of country j from WGI |

| ln GNIpj | Log of real GNI per capita of country j from WDI |

| ln DISTij | Log of distance between country i and j from CASIO |

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | |

|---|---|---|---|---|---|---|---|---|

| Year | 2003–2013 | 2003–2013 | 2003–2013 | 2003–2013 | 2014–2020 | 2014–2020 | 2014–2020 | 2014–2020 |

| Dependent Variable | ln FDIij | ln FDIij | ln FDIij | ln FDIij | ln FDIij | ln FDIij | ln FDIij | ln FDIij |

| ln FDIij | 0.802 *** | 0.797 *** | 0.797 *** | 0.797 *** | 0.991 *** | 0.982 *** | 0.995 *** | 1.012 *** |

| (0.0806) | (0.0820) | (0.0819) | (0.0818) | (0.101) | (0.0864) | (0.0756) | (0.0666) | |

| ln AID_Allj | 1.89 × 10−5 | 0.000957 | ||||||

| (0.000286) | (0.000875) | |||||||

| ln INF_Allj | −5.92 × 10−5 | −7.93 × 10−5 | 0.00270 | 0.00112 * | ||||

| (0.000380) | (0.000281) | (0.00193) | (0.000672) | |||||

| ln NINF_Allj | −2.38 × 10−5 | −4.34 × 10−5 | −0.00186 | 0.000850 | ||||

| (0.000469) | (0.000362) | (0.00208) | (0.000690) | |||||

| ln GDPi | 0.00481 | 0.00528 | 0.00529 | 0.00527 | −0.0104 | −0.0100 | −0.00869 | −0.00840 |

| (0.00469) | (0.00463) | (0.00462) | (0.00470) | (0.00828) | (0.00713) | (0.00707) | (0.00719) | |

| ln GDPj | 0.00803 *** | 0.00697 ** | 0.00698 ** | 0.00697 ** | −0.00517 * | −0.00409 * | −0.00456 ** | −0.00414 * |

| (0.00274) | (0.00285) | (0.00279) | (0.00283) | (0.00281) | (0.00243) | (0.00227) | (0.00227) | |

| ln GOVj | 0.00182 *** | 0.00201 ** | 0.00201 ** | 0.00200 ** | 0.00342 | −0.00613 | −0.00220 | 0.00286 |

| (0.000651) | (0.000859) | (0.000847) | (0.000842) | (0.0114) | (0.0109) | (0.00987) | (0.00952) | |

| ln GNIpj | −0.00825 ** | −0.00859 ** | −0.00856 ** | −0.00856 *** | 0.000279 | 0.00321 | 0.00325 | 0.000901 |

| (0.00369) | (0.00338) | (0.00344) | (0.00324) | (0.00640) | (0.00552) | (0.00533) | (0.00529) | |

| ln DISTij | −0.00649 | −0.00737 | −0.00738 | −0.00729 | −0.000827 | 0.000103 | −0.000891 | −0.000873 |

| (0.00467) | (0.00510) | (0.00507) | (0.00505) | (0.00427) | (0.00321) | (0.00313) | (0.00302) | |

| Lag option | 14 | 13 | 13 | 13 | 11 | 11 | 11 | 11 |

| Arellano–Bond test | 0.119 | 0.119 | 0.119 | 0.119 | 0.246 | 0.244 | 0.242 | 0.242 |

| Hansen J test | 0.752 | 0.787 | 0.801 | 0.796 | 0.103 | 0.169 | 0.168 | 0.130 |

| VIF less than 10 | ○ | ○ | ○ | ○ | ○ | × | ○ | ○ |

| Observations | 1170 | 1170 | 1170 | 1170 | 600 | 600 | 600 | 600 |

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | |

|---|---|---|---|---|---|---|---|---|

| Year | 2003–2013 | 2003–2013 | 2003–2013 | 2003–2013 | 2014–2020 | 2014–2020 | 2014–2020 | 2014–2020 |

| Dependent Variable | ln FDIij | ln FDIij | ln FDIij | ln FDIij | ln FDIij | ln FDIij | ln FDIij | ln FDIij |

| ln FDIij | 0.797 *** | 0.797 *** | 0.793 *** | 0.795 *** | 1.031 *** | 0.973 *** | 0.964 *** | 1.051 *** |

| (0.0854) | (0.0895) | (0.0883) | (0.0889) | (0.0282) | (0.0964) | (0.106) | (0.0668) | |

| ln AIDij | 5.15 × 10−5 | 0.00170 | ||||||

| (0.000351) | (0.00206) | |||||||

| ln INFij | 0.000150 | 0.000142 | 0.00546 | 0.00662 | ||||

| (0.000333) | (0.000335) | (0.00558) | (0.00550) | |||||

| ln NINFij | 0.000105 | 9.23 × 10−5 | 0.000105 | 0.00107 | ||||

| (0.000256) | (0.000276) | (0.00184) | (0.00251) | |||||

| ln GDPi | 0.00601 | 0.00603 | 0.00606 | 0.00640 | −0.0116 ** | −0.00440 | −0.00793 | −0.00483 |

| (0.00552) | (0.00526) | (0.00617) | (0.00510) | (0.00549) | (0.00710) | (0.00826) | (0.00745) | |

| ln GDPj | 0.00676 ** | 0.00581 ** | 0.00544 ** | 0.00616 ** | −0.00223 | −0.00467 | −0.00509 | −0.00342 |

| (0.00282) | (0.00260) | (0.00265) | (0.00282) | (0.00221) | (0.00364) | (0.00388) | (0.00302) | |

| ln GOVj | 0.00204 *** | 0.00216 ** | 0.00176 ** | 0.00227 ** | 0.0104 | 0.00663 | 0.00809 | 0.0111 |

| (0.000787) | (0.000937) | (0.000845) | (0.000923) | (0.00922) | (0.0156) | (0.0165) | (0.0145) | |

| ln GNIpj | −0.00941 ** | −0.00906 ** | −0.00937 ** | −0.0100 ** | −0.00237 | 0.00538 | 0.00606 | −0.000899 |

| (0.00445) | (0.00457) | (0.00467) | (0.00465) | (0.00559) | (0.0134) | (0.0124) | (0.00848) | |

| ln DISTij | −0.00711 | −0.00791 | −0.00696 | −0.00748 | 0.00130 | −0.00207 | −0.000404 | −0.00253 |

| (0.00490) | (0.00516) | (0.00541) | (0.00500) | (0.00265) | (0.00391) | (0.00412) | (0.00392) | |

| Lag option | 14 | 13 | 13 | 13 | 12 | 11 | 11 | 11 |

| Arellano–Bond test | 0.119 | 0.118 | 0.119 | 0.119 | 0.239 | 0.256 | 0.253 | 0.265 |

| Hansen J test | 0.762 | 0.825 | 0.339 | 0.443 | 0.224 | 0.143 | 0.144 | 0.125 |

| VIF less than 10 | ○ | ○ | ○ | ○ | ○ | ○ | ○ | ○ |

| Observations | 1170 | 1170 | 1170 | 1170 | 600 | 600 | 600 | 600 |

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | |

|---|---|---|---|---|---|---|---|---|

| Year | 2003–2013 | 2003–2013 | 2003–2013 | 2003–2013 | 2014–2020 | 2014–2020 | 2014–2020 | 2014–2020 |

| Dependent Variable | ln FDIij | ln FDIij | ln FDIij | ln FDIij | ln FDIij | ln FDIij | ln FDIij | ln FDIij |

| ln FDIij | 0.790 *** | 0.704 *** | 0.778 *** | 0.808 *** | 1.002 *** | 0.989 *** | 1.002 *** | 1.005 *** |

| (0.0856) | (0.137) | (0.0880) | (0.0915) | (0.0413) | (0.0598) | (0.0622) | (0.0411) | |

| ln AIDFRj | 0.000701 | 0.000215 | ||||||

| (0.00124) | (0.00177) | |||||||

| ln AIDGMj | −0.000723 | 0.000431 | ||||||

| (0.00231) | (0.00212) | |||||||

| ln AIDJPj | 0.00171 | 0.000752 | ||||||

| (0.00138) | (0.00156) | |||||||

| ln AIDUKj | −0.000230 | 0.00174 | ||||||

| (0.000440) | (0.00305) | |||||||

| ln AIDUSj | −0.000989 | 0.00108 | ||||||

| (0.00138) | (0.00318) | |||||||

| ln INFFRj | −4.26 × 10−6 | 0.000643 | 0.00167 | 0.00163 | ||||

| (0.00252) | (0.00136) | (0.00156) | (0.00282) | |||||

| ln INFGMj | −0.00692 * | −0.000802 | 0.00210 | −4.18 × 10−5 | ||||

| (0.00377) | (0.00273) | (0.00173) | (0.00255) | |||||

| ln INFJPj | 0.00534 * | 0.00155 | 0.00106 | 0.00117 | ||||

| (0.00315) | (0.00162) | (0.00114) | (0.00184) | |||||

| ln INFUKj | −0.000241 | −0.000218 | −0.000920 | 0.00133 | ||||

| (0.000474) | (0.000457) | (0.00209) | (0.00263) | |||||

| ln INFUSj | 0.00166 | −0.000723 | −0.000364 | −0.00121 | ||||

| (0.00209) | (0.00138) | (0.00152) | (0.00288) | |||||

| ln NINFFRj | 0.000302 | 0.000601 | −0.000387 | 0.000864 | ||||

| (0.000458) | (0.000383) | (0.000653) | (0.000641) | |||||

| ln NINFGMj | 0.000179 | 0.000221 | −0.000746 | −0.000468 | ||||

| (0.000346) | (0.000466) | (0.000829) | (0.000810) | |||||

| ln NINFJPj | −0.000562 | −0.000746 ** | 0.000714 | 0.000885 | ||||

| (0.000450) | (0.000339) | (0.000710) | (0.000770) | |||||

| ln NINFUKj | 0.000350 | 0.000356 | 0.00145 * | −0.000178 | ||||

| (0.000356) | (0.000363) | (0.000785) | (0.000896) | |||||

| ln NINFUSj | 0.000531 | 9.65 × 10−5 | −0.000580 | −0.000117 | ||||

| (0.000547) | (0.000491) | (0.000644) | (0.00103) | |||||

| Lag option | 11 | collapse | 11 | 11 | 11 | 11 | 11 | 11 |

| Arellano–Bond test | 0.119 | 0.12 | 0.119 | 0.117 | 0.236 | 0.192 | 0.241 | 0.243 |

| Hansen J test | 0.256 | 0.093 | 0.13 | 0.106 | 0.313 | 0.507 | 0.366 | 0.245 |

| VIF less than 10 | × | × | × | ○ | ○ | ○ | ○ | ○ |

| Observations | 1170 | 1170 | 1170 | 1170 | 600 | 600 | 600 | 600 |

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | |

|---|---|---|---|---|---|---|---|---|

| Year | 2003–2013 | 2003–2013 | 2003–2013 | 2003–2013 | 2014–2020 | 2014–2020 | 2014–2020 | 2014–2020 |

| Dependent Variable | ln FDIFRj | ln FDIFRj | ln FDIFRj | ln FDIFRj | ln FDIFRj | ln FDIFRj | ln FDIFRj | ln FDIFRj |

| ln AIDFRj | 0.000204 | 0.00951 | ||||||

| (0.00327) | (0.00630) | |||||||

| ln INFFRj | −0.00132 | −0.00199 | 0.0164 | 0.0118 | ||||

| (0.00238) | (0.00252) | (0.0148) | (0.00742) | |||||

| ln NINFFRj | 0.000556 | 0.000414 | −0.00294 | 0.00167 | ||||

| (0.000764) | (0.000749) | (0.00388) | (0.00235) | |||||

| Lag option | collapse | collapse | collapse | collapse | 11 | 11 | 11 | 11 |

| Arellano–Bond test | 0.296 | 0.313 | 0.307 | 0.306 | 0.533 | 0.538 | 0.507 | 0.552 |

| Hansen J test | 0.997 | 1.000 | 1.000 | 1.000 | 0.599 | 0.985 | 0.537 | 0.778 |

| VIF less than 10 | ○ | ○ | ○ | ○ | ○ | ○ | ○ | ○ |

| Observations | 234 | 234 | 234 | 234 | 120 | 120 | 120 | 120 |

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | |

|---|---|---|---|---|---|---|---|---|

| Year | 2003–2013 | 2003–2013 | 2003–2013 | 2003–2013 | 2014–2020 | 2014–2020 | 2014–2020 | 2014–2020 |

| Dependent Variable | ln FDIGMj | ln FDIGMj | ln FDIGMj | ln FDIGMj | ln FDIGMj | ln FDIGMj | ln FDIGMj | ln FDIGMj |

| ln AIDGMj | −0.000835 | 0.00169 | ||||||

| (0.00202) | (0.00588) | |||||||

| ln INFGMj | −0.00193 | −0.00139 | 0.00206 | 0.00473 | ||||

| (0.00266) | (0.00214) | (0.00483) | (0.00425) | |||||

| ln NINFGMj | −0.000144 | −9.17 × 10−5 | 0.000665 | 0.000226 | ||||

| (0.000527) | (0.000510) | (0.00133) | (0.00165) | |||||

| Lag option | collapse | collapse | collapse | collapse | 11 | 11 | 11 | 11 |

| Arellano–Bond test | 0.454 | 0.718 | 0.478 | 0.645 | 0.685 | 0.692 | 0.707 | 0.661 |

| Hansen J test | 0.940 | 1.000 | 0.985 | 1.000 | 0.851 | 0.827 | 0.578 | 0.200 |

| VIF less than 10 | ○ | ○ | ○ | ○ | ○ | ○ | ○ | ○ |

| Observations | 234 | 234 | 234 | 234 | 120 | 120 | 120 | 120 |

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | |

|---|---|---|---|---|---|---|---|---|

| Year | 2003–2013 | 2003–2013 | 2003–2013 | 2003–2013 | 2014–2020 | 2014–2020 | 2014–2020 | 2014–2020 |

| Dependent Variable | ln FDIJPj | ln FDIJPj | ln FDIJPj | ln FDIJPj | ln FDIJPj | ln FDIJPj | ln FDIJPj | ln FDIJPj |

| ln AIDJPj | −0.00252 | 0.00291 | ||||||

| (0.00428) | (0.00309) | |||||||

| ln INFJPj | −0.00294 | −0.00563 | −0.00111 | 0.00381 | ||||

| (0.00332) | (0.00525) | (0.00679) | (0.00418) | |||||

| ln NINFJPj | 0.000147 | −6.90 × 10−6 | 0.00270 | 0.00234 | ||||

| (0.000341) | (0.000340) | (0.00450) | (0.00229) | |||||

| Lag option | collapse | collapse | collapse | collapse | 11 | 11 | 11 | 11 |

| Arellano–Bond test | 0.761 | 0.716 | 0.792 | 0.763 | 0.621 | 0.616 | 0.607 | 0.622 |

| Hansen J test | 0.944 | 1.000 | 0.981 | 0.992 | 0.195 | 0.450 | 0.308 | 0.327 |

| VIF less than 10 | ○ | ○ | ○ | ○ | ○ | ○ | ○ | ○ |

| Observations | 234 | 234 | 234 | 234 | 120 | 120 | 120 | 120 |

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | |

|---|---|---|---|---|---|---|---|---|

| Year | 2003–2013 | 2003–2013 | 2003–2013 | 2003–2013 | 2014–2020 | 2014–2020 | 2014–2020 | 2014–2020 |

| Dependent Variable | ln FDIUKj | ln FDIUKj | ln FDIUKj | ln FDIUKj | ln FDIUKj | ln FDIUKj | ln FDIUKj | ln FDIUKj |

| ln AIDUKj | 0.000381 | 0.00511 | ||||||

| (0.00105) | (0.00467) | |||||||

| ln INFUKj | 4.17 × 10−5 | 0.000337 | 0.00188 | 0.00648 * | ||||

| (0.00110) | (0.00108) | (0.00373) | (0.00372) | |||||

| ln NINFUKj | 0.000180 | 0.000595 | 0.000872 | 0.000708 | ||||

| (0.000844) | (0.000838) | (0.00175) | (0.00133) | |||||

| Lag option | collapse | collapse | collapse | collapse | 11 | 11 | 11 | 11 |

| Arellano–Bond test | 0.106 | 0.109 | 0.106 | 0.091 | 0.250 | 0.249 | 0.266 | 0.248 |

| Hansen J test | 0.876 | 0.992 | 0.892 | 0.945 | 0.435 | 0.581 | 0.339 | 0.257 |

| VIF less than 10 | ○ | ○ | ○ | ○ | ○ | ○ | ○ | ○ |

| Observations | 234 | 234 | 234 | 234 | 120 | 120 | 120 | 120 |

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | |

|---|---|---|---|---|---|---|---|---|

| Year | 2003–2013 | 2003–2013 | 2003–2013 | 2003–2013 | 2014–2020 | 2014–2020 | 2014–2020 | 2014–2020 |

| Dependent Variable | ln FDIUSj | ln FDIUSj | ln FDIUSj | ln FDIUSj | ln FDIUSj | ln FDIUSj | ln FDIUSj | ln FDIUSj |

| ln AIDUSj | −0.00334 | 0.0110 | ||||||

| (0.00694) | (0.0177) | |||||||

| ln INFUSj | 0.000596 | −0.00271 | −0.00757 | 0.00744 | ||||

| (0.00472) | (0.00802) | (0.0144) | (0.0192) | |||||

| ln NINFUSj | −0.00151 | −0.00190 | 0.00343 | 0.00659 | ||||

| (0.00125) | (0.00138) | (0.00392) | (0.00449) | |||||

| Lag option | collapse | collapse | collapse | collapse | 1 1 | 1 1 | 1 1 | 1 1 |

| Arellano–Bond test | 0.273 | 0.289 | 0.273 | 0.286 | 0.295 | 0.394 | 0.308 | 0.414 |

| Hansen J test | 0.992 | 0.999 | 0.989 | 0.991 | 0.338 | 0.481 | 0.509 | 0.570 |

| VIF less than 10 | ○ | ○ | ○ | ○ | ○ | ○ | ○ | ○ |

| Observations | 234 | 234 | 234 | 234 | 120 | 120 | 120 | 120 |

| 2003–2013 | ||

|---|---|---|

| Variable | Statistic | Prob. |

| ln FDIij | −27.180 | 0.000 |

| ln NINFJPj | −10.876 | 0.000 |

| 2003–2013 | ||||

|---|---|---|---|---|

| Variables | 0 | 1 | 2 | |

| ln FDIij | ln NINFJPj | 8.828754 | 8.150825 | 8.061585 * |

| 2003–2013 | ||

|---|---|---|

| Null Hypothesis: | F-Statistic | Prob. |

| ln NINFJPj does not Granger Cause ln FDIij | 0.1262 | 0.8815 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Ono, S.; Sekiyama, T. Re-Examining the Effects of Official Development Assistance on Foreign Direct Investment Applying the VAR Model. Economies 2022, 10, 236. https://doi.org/10.3390/economies10100236

Ono S, Sekiyama T. Re-Examining the Effects of Official Development Assistance on Foreign Direct Investment Applying the VAR Model. Economies. 2022; 10(10):236. https://doi.org/10.3390/economies10100236

Chicago/Turabian StyleOno, Saori, and Takashi Sekiyama. 2022. "Re-Examining the Effects of Official Development Assistance on Foreign Direct Investment Applying the VAR Model" Economies 10, no. 10: 236. https://doi.org/10.3390/economies10100236

APA StyleOno, S., & Sekiyama, T. (2022). Re-Examining the Effects of Official Development Assistance on Foreign Direct Investment Applying the VAR Model. Economies, 10(10), 236. https://doi.org/10.3390/economies10100236