India–Republic of Korea CEPA: Assessment and Future Path

Abstract

:1. Introduction

2. Literature Review

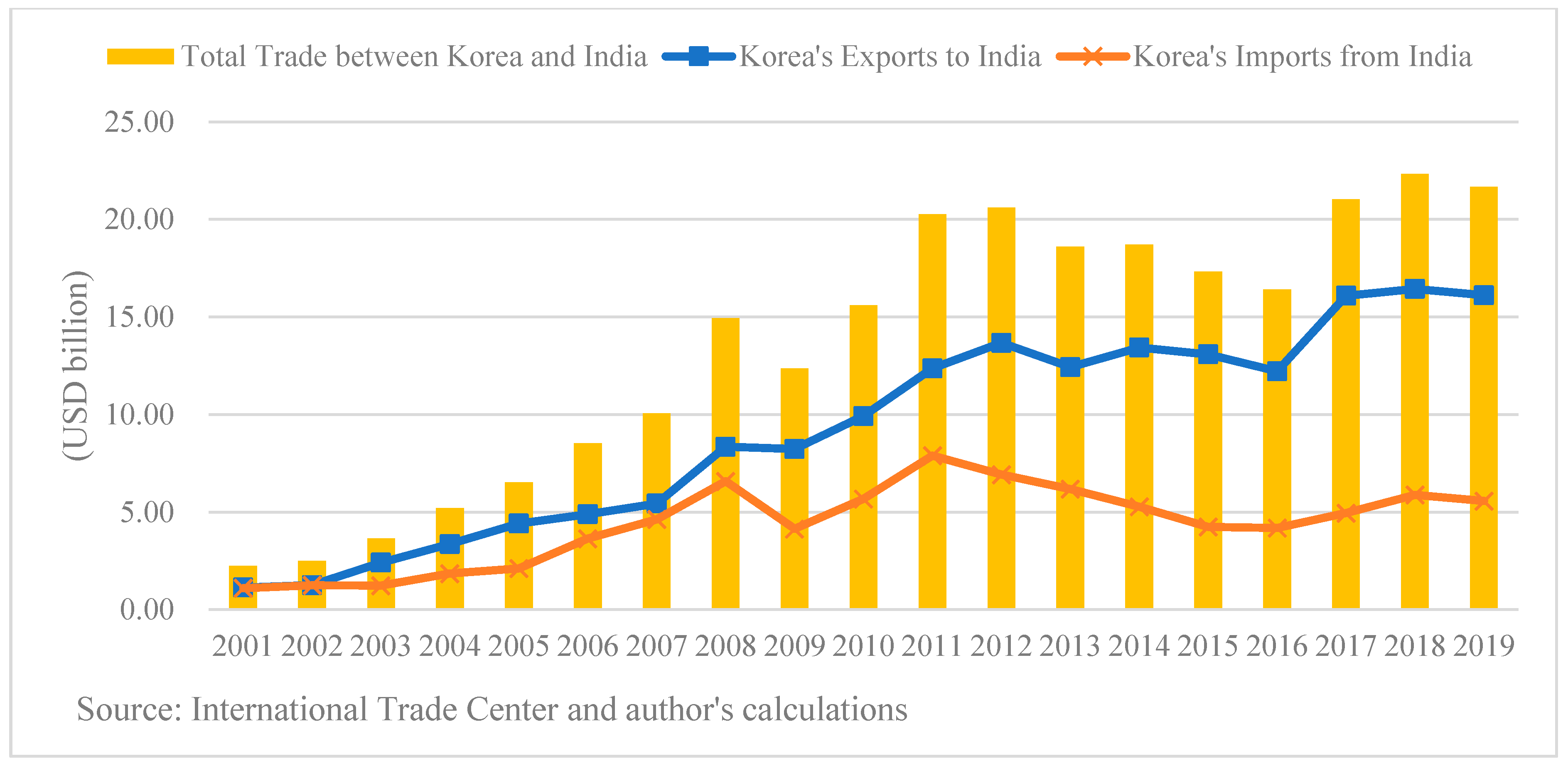

3. Trade Relations between India and the ROK

4. Identifying Comparative Advantage between the ROK and India

4.1. Theoretical Framework

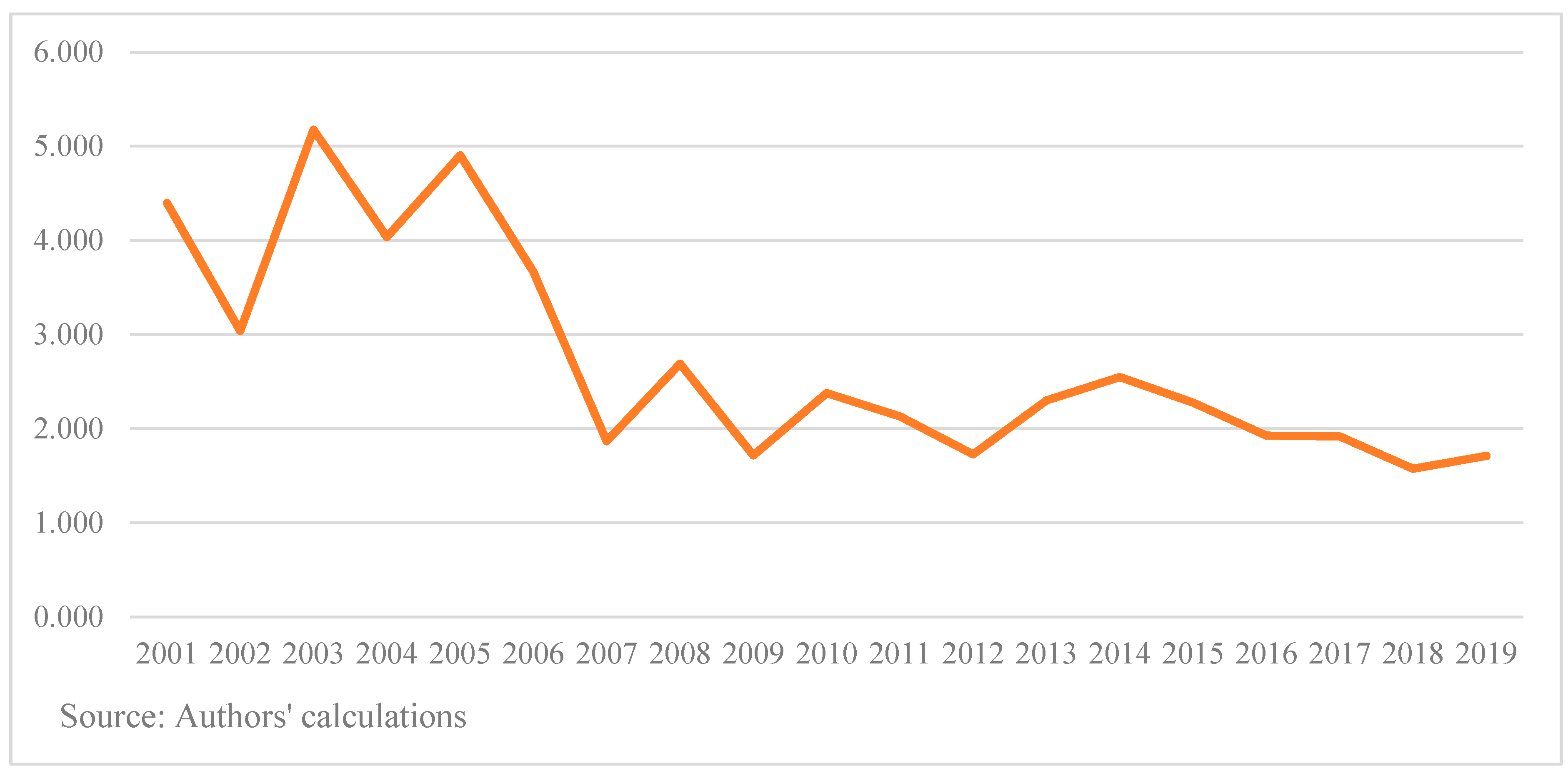

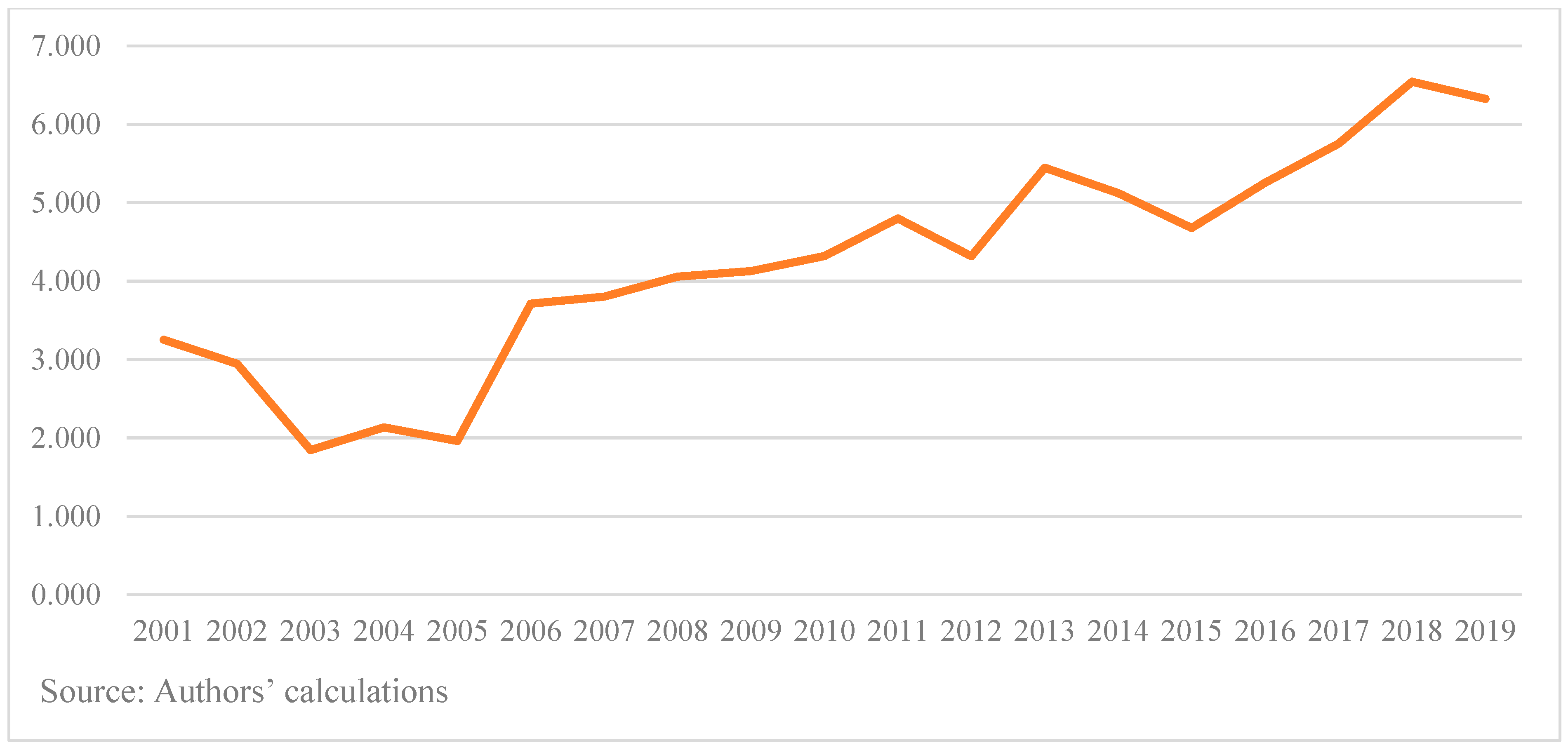

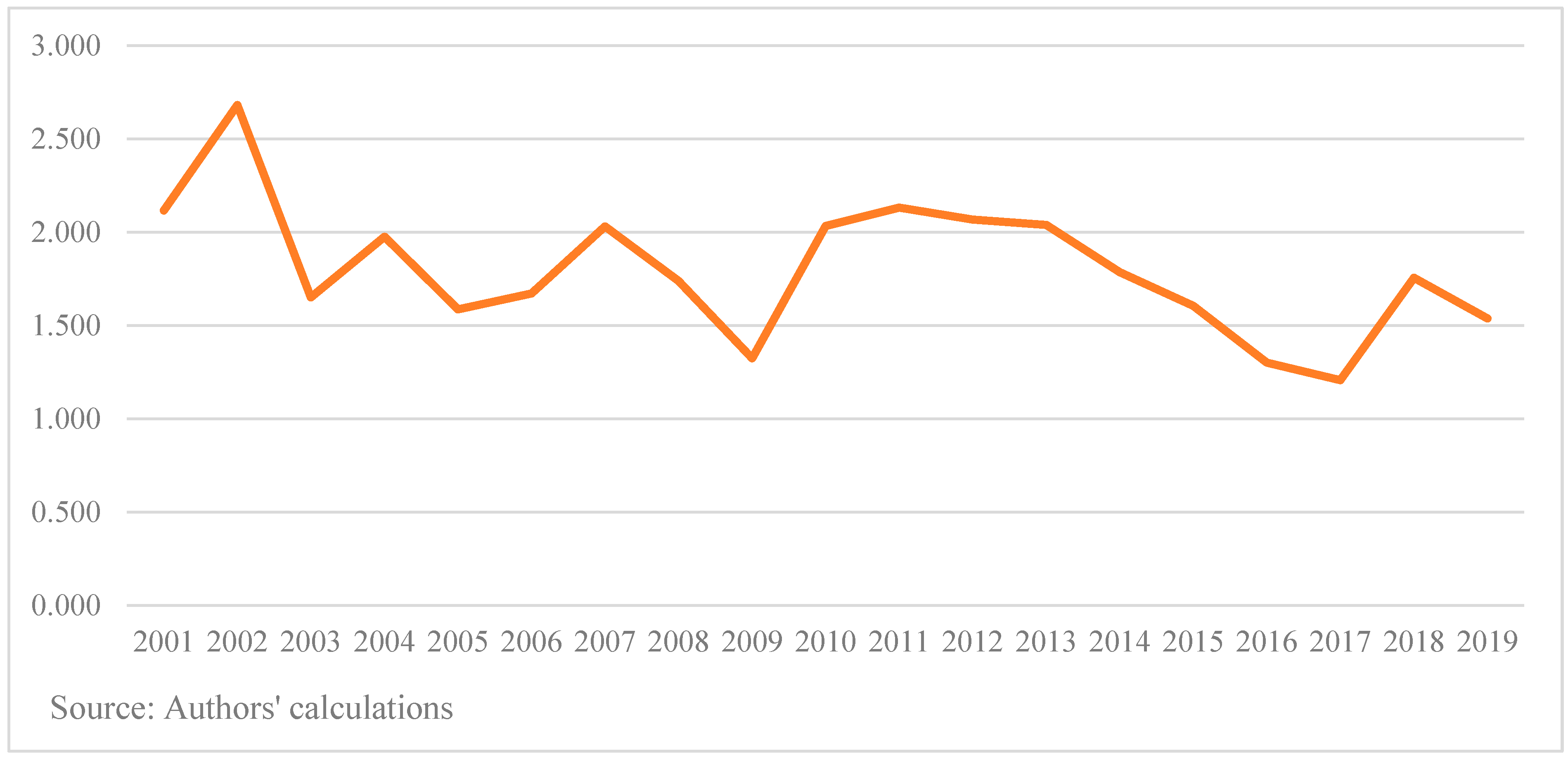

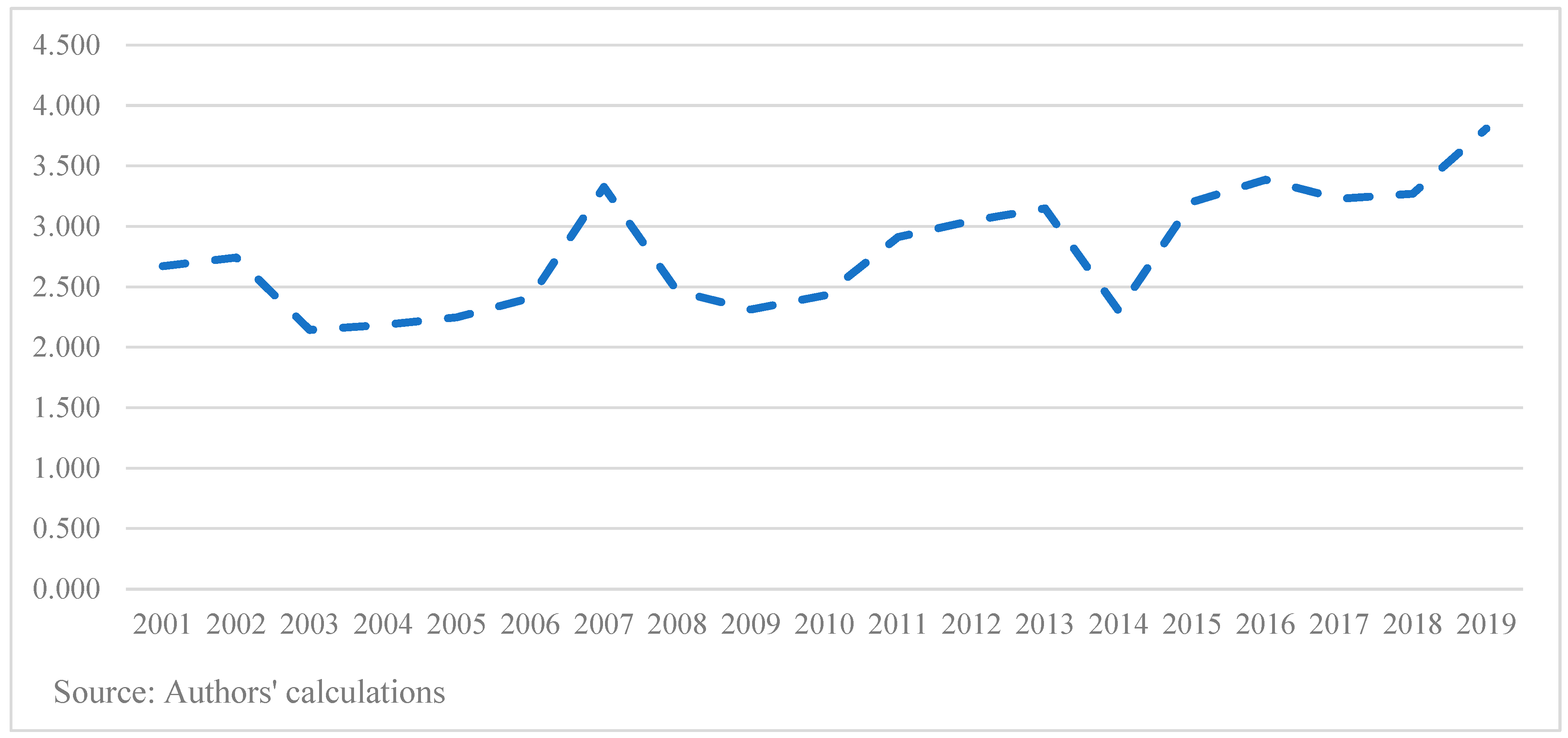

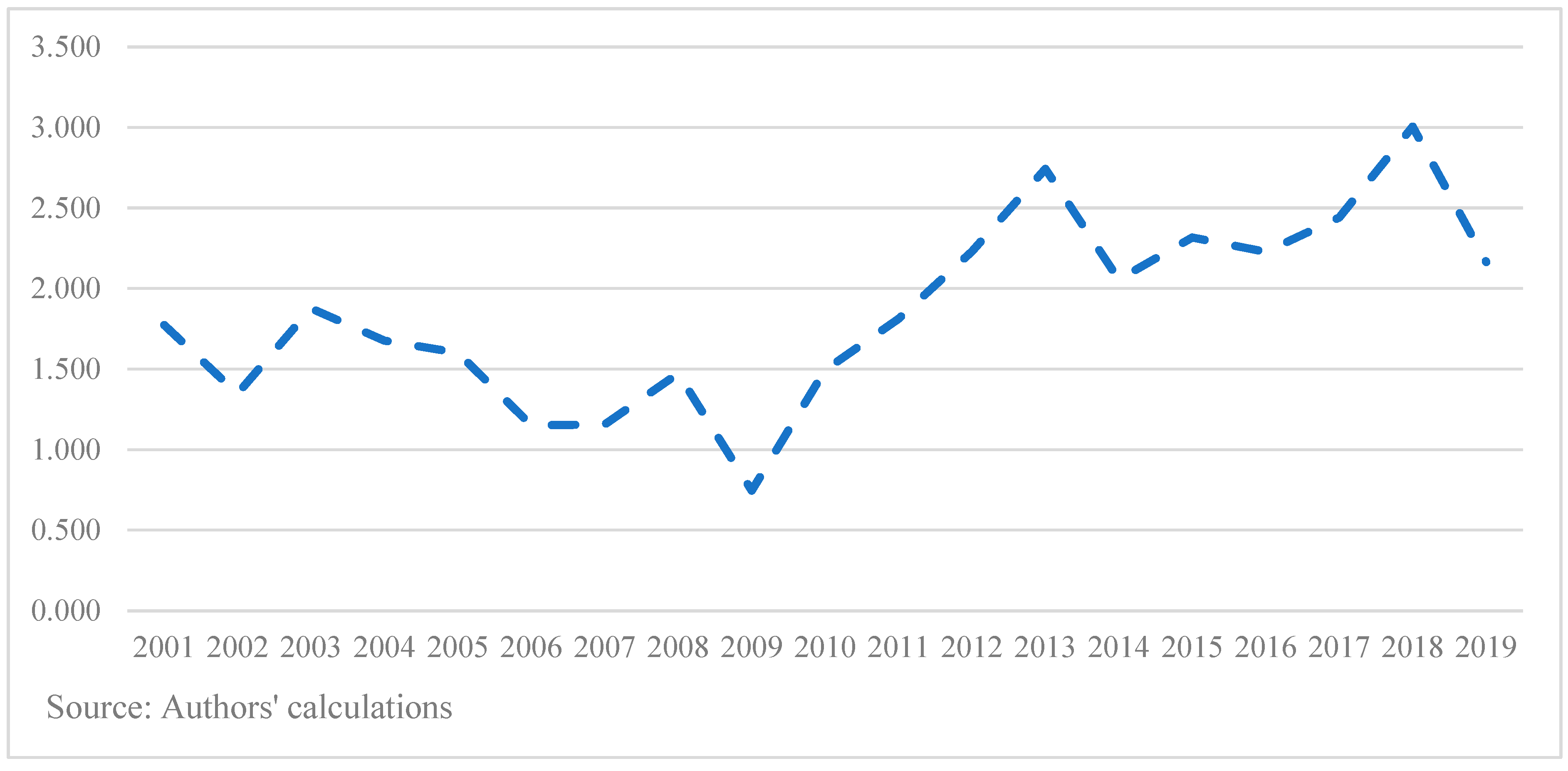

4.2. MCA Results and Analysis

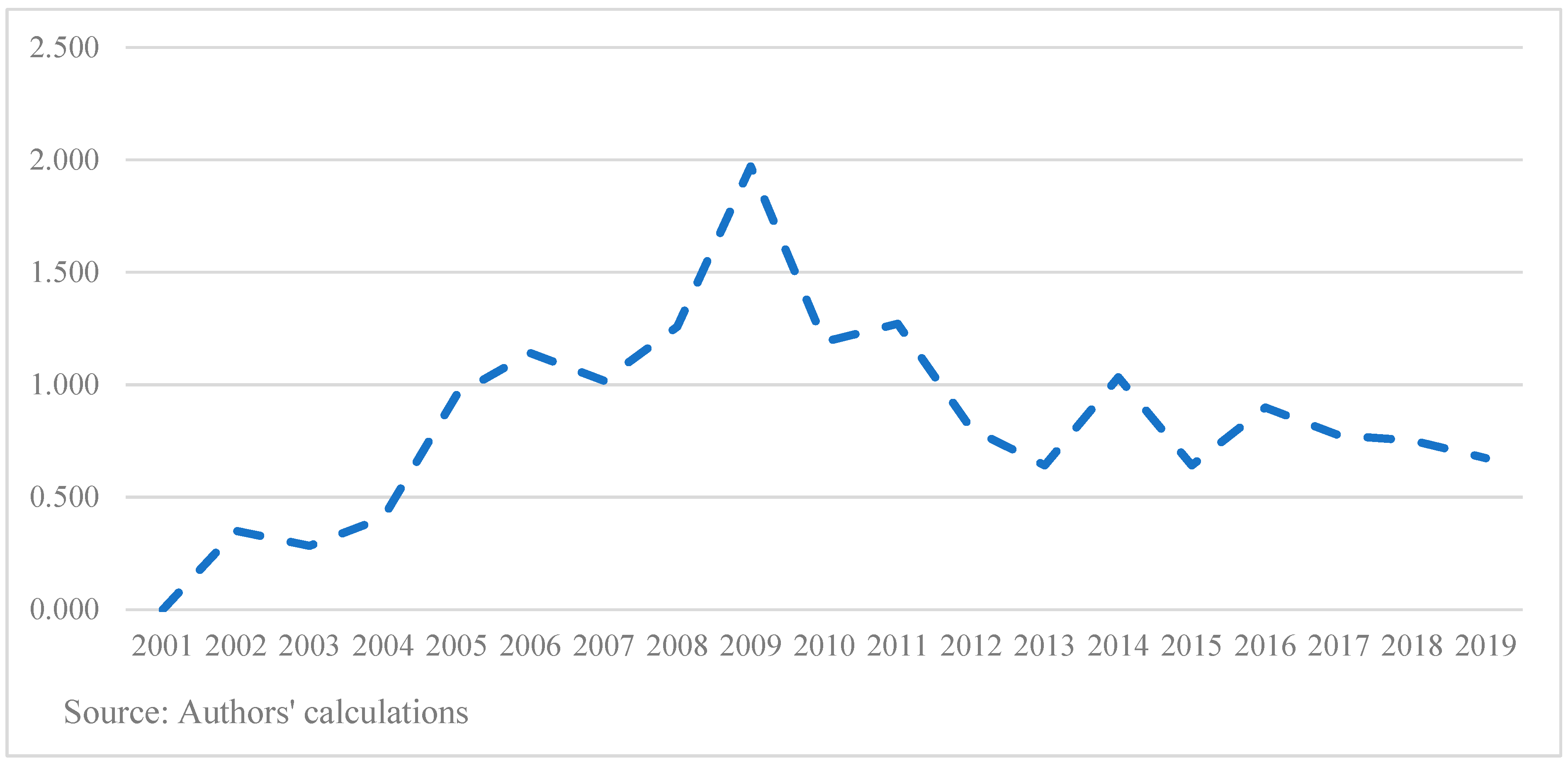

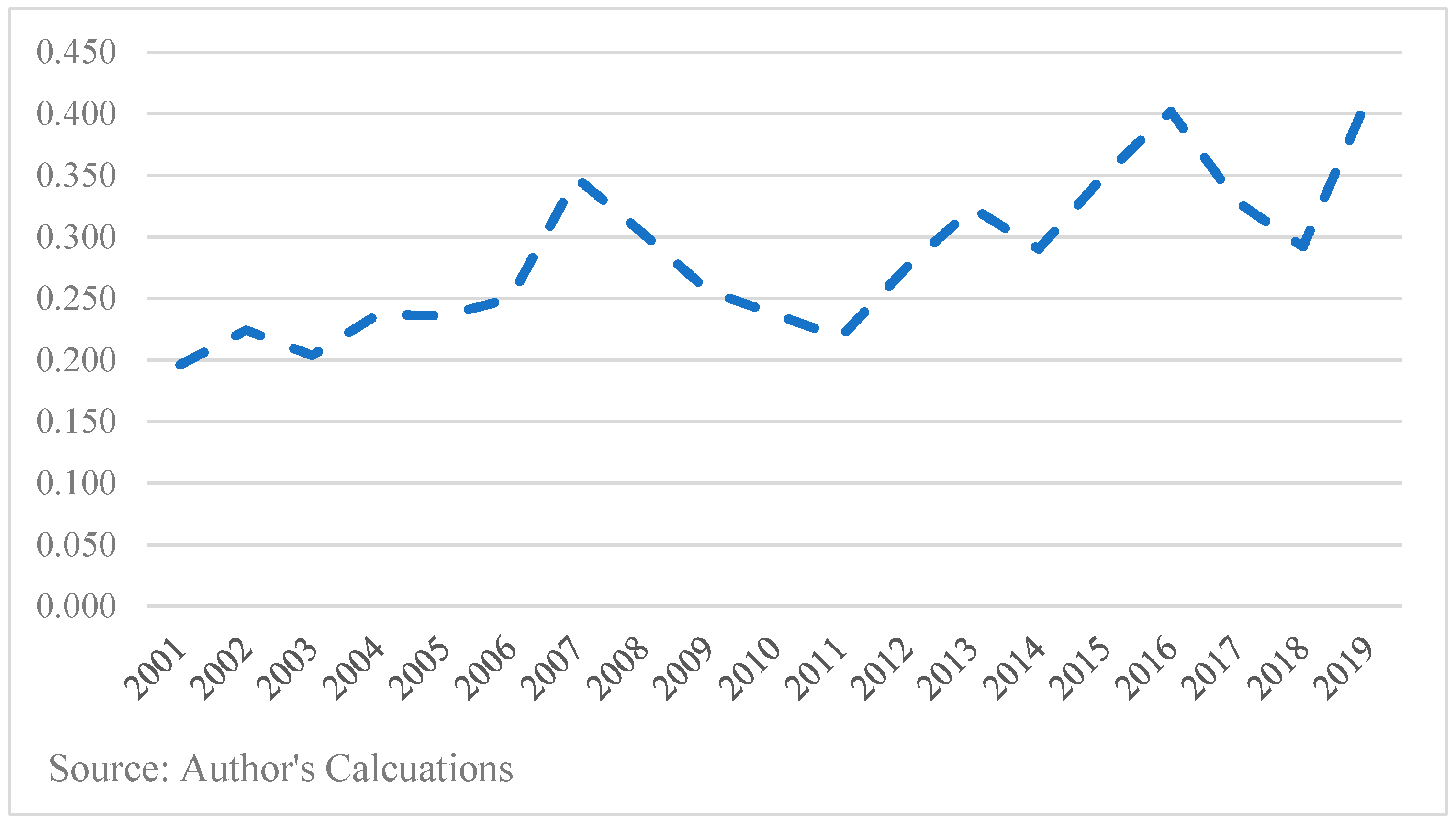

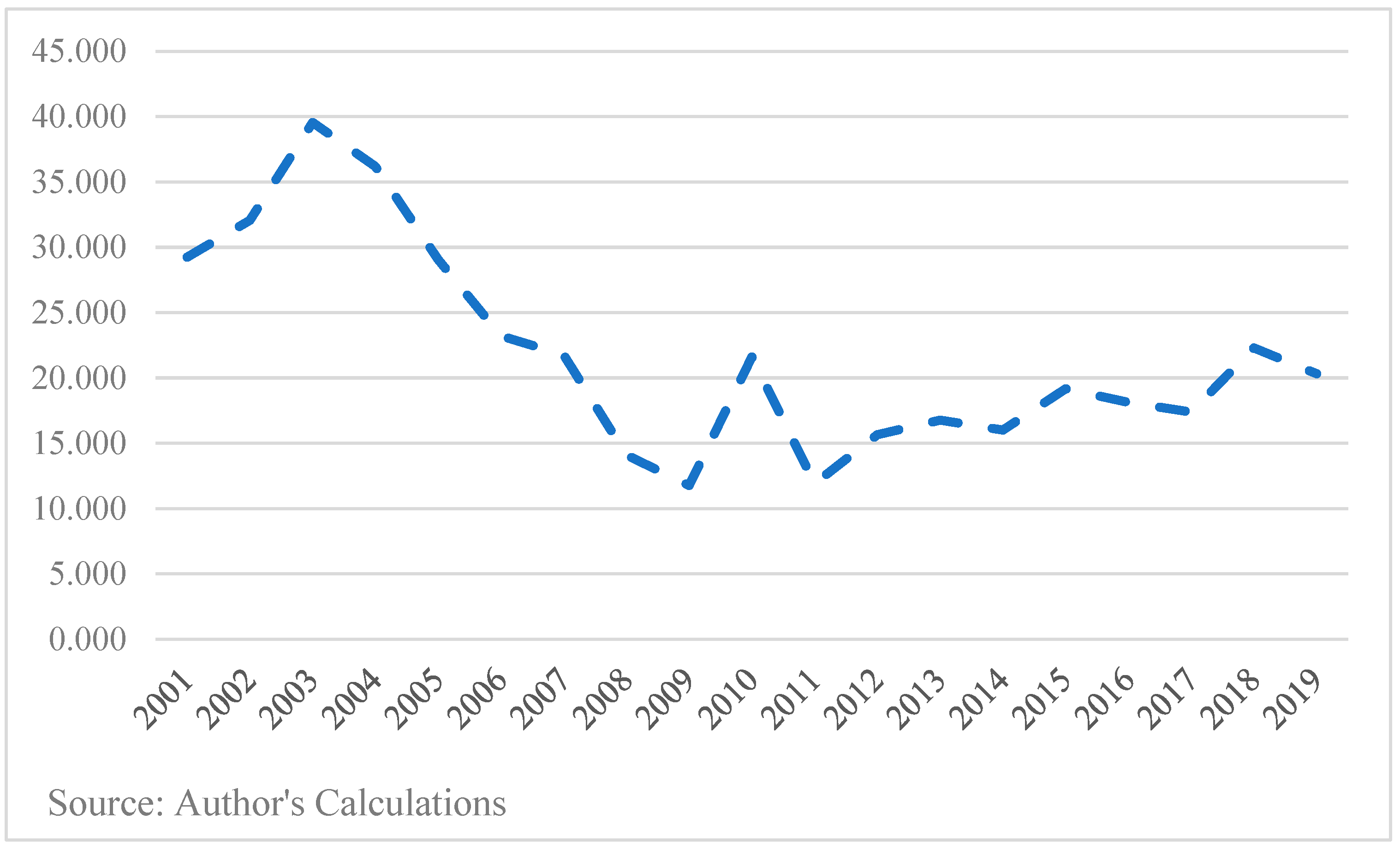

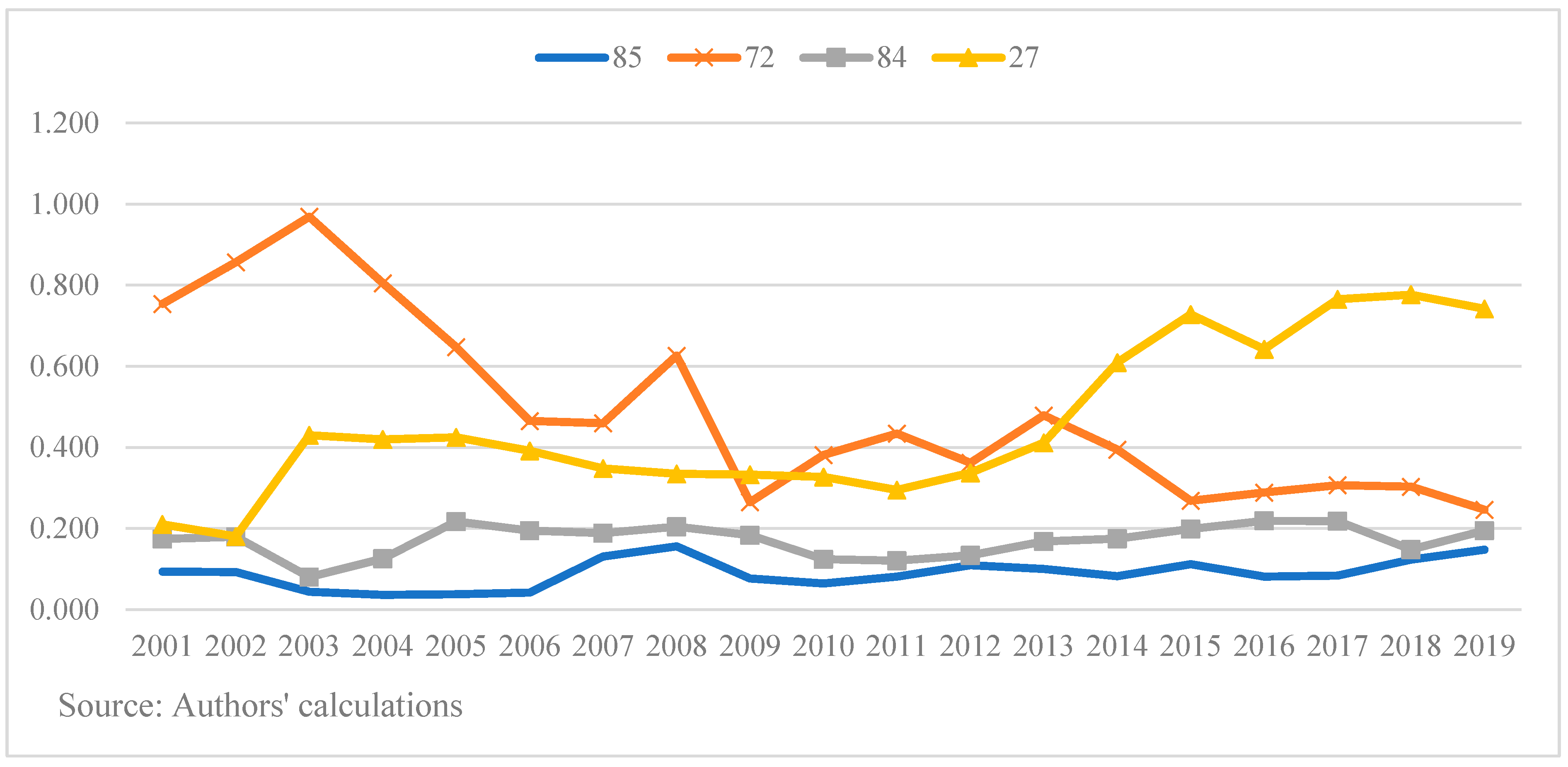

4.3. Grubel–Lloyd Index Results and Analysis

5. Services Trade

Analyzing the Comparative Advantage for Service Trade

6. Trade Policy Framework

6.1. Tariffs

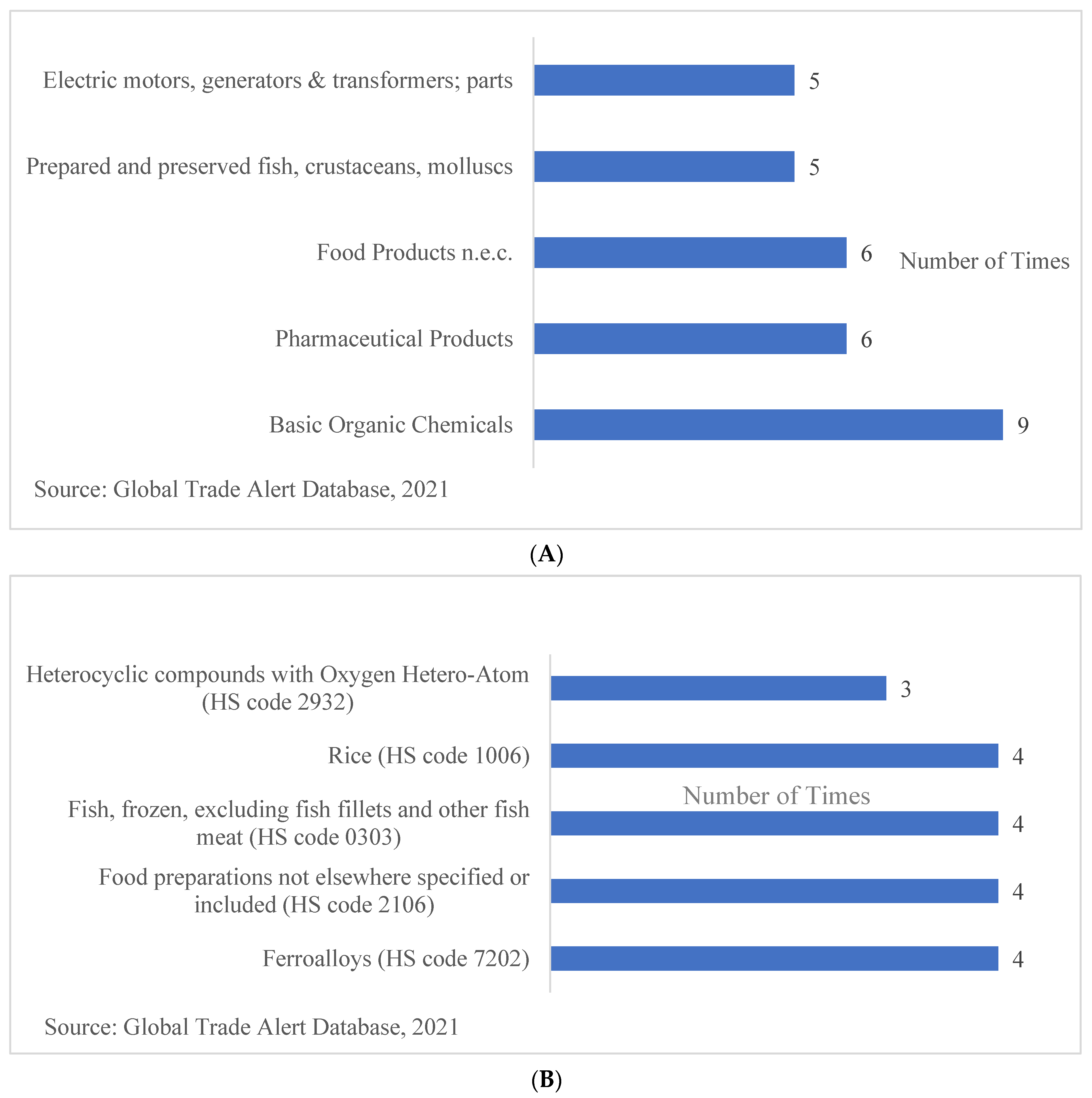

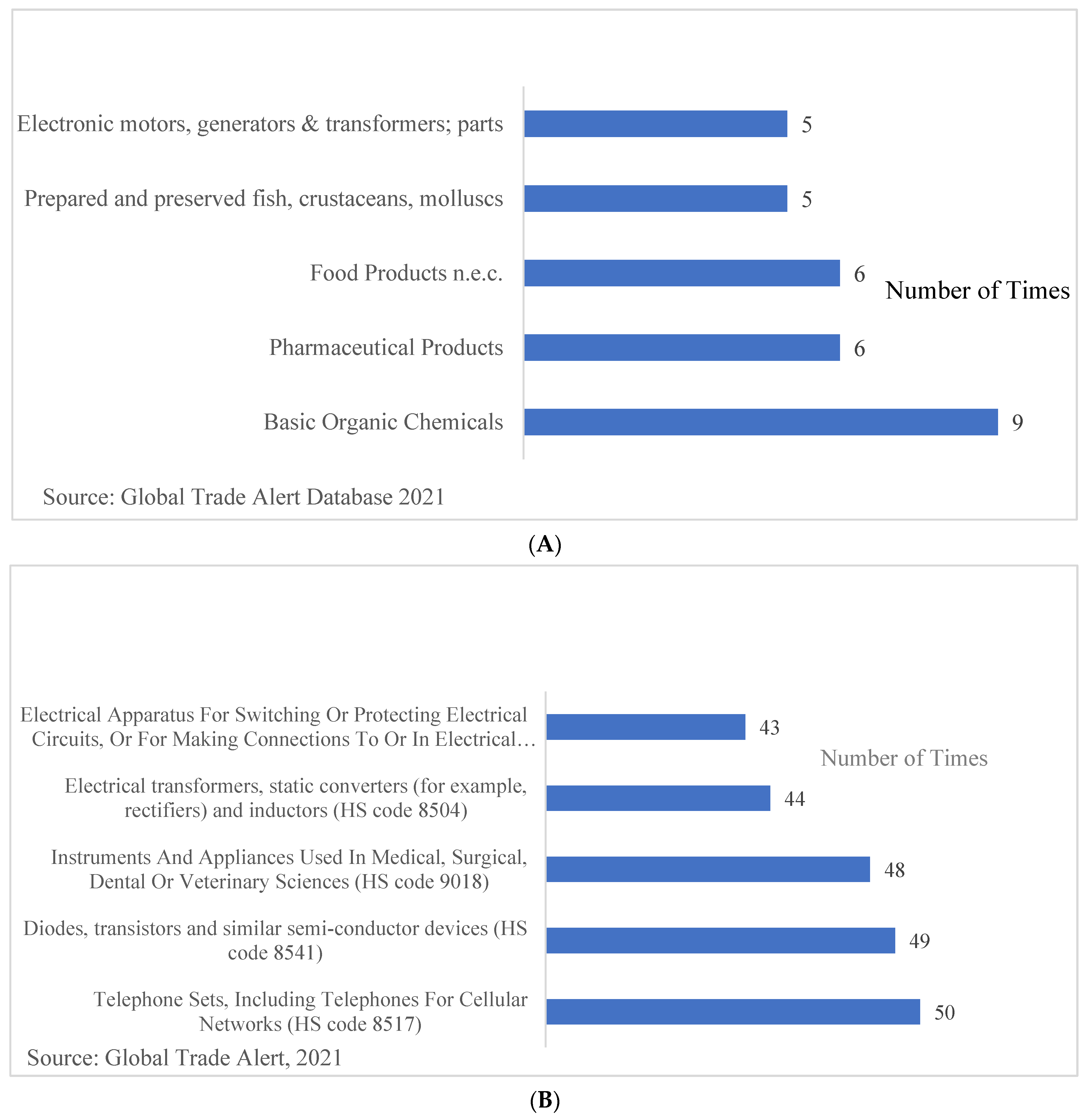

6.2. NTMs

7. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

Appendix A

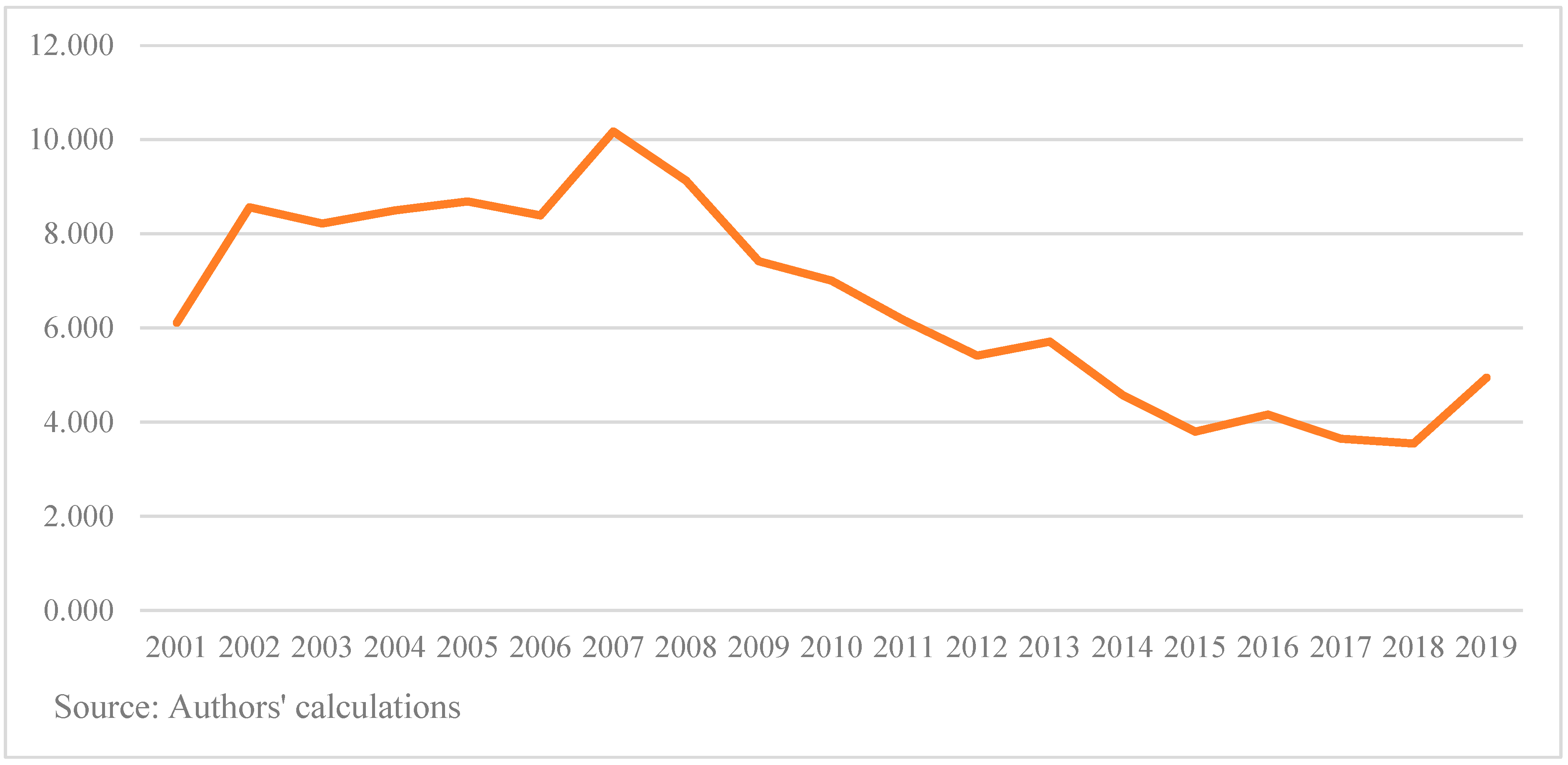

| MCA of Korea’s Goods Export to India | |||||||||

| HS Code 85 | HS Code 72 | HS Code 84 | HS Code 39 | HS Code 29 | HS Code 87 | HS Code 27 | HS Code 90 | HS Code 73 | |

| 2001 | 4.397 | 3.251 | 2.117 | 3.512 | 1.338 | 6.112 | 0.000 | 1.443 | 2.365 |

| 2002 | 3.037 | 2.945 | 2.683 | 3.851 | 1.143 | 8.563 | 0.000 | 1.641 | 3.370 |

| 2003 | 5.176 | 1.848 | 1.650 | 3.118 | 0.757 | 8.219 | 0.002 | 1.141 | 2.185 |

| 2004 | 4.035 | 2.135 | 1.976 | 2.754 | 0.744 | 8.496 | 0.001 | 1.057 | 2.293 |

| 2005 | 4.904 | 1.962 | 1.586 | 3.466 | 0.935 | 8.685 | 0.000 | 1.030 | 1.903 |

| 2006 | 3.668 | 3.712 | 1.671 | 3.038 | 0.837 | 8.391 | 0.232 | 0.944 | 1.607 |

| 2007 | 1.866 | 3.802 | 2.031 | 2.934 | 1.152 | 10.176 | 0.250 | 1.197 | 3.356 |

| 2008 | 2.690 | 4.056 | 1.739 | 3.636 | 1.270 | 9.129 | 0.248 | 1.387 | 4.241 |

| 2009 | 1.716 | 4.128 | 1.325 | 3.558 | 1.384 | 7.414 | 0.384 | 1.335 | 1.837 |

| 2010 | 2.379 | 4.319 | 2.033 | 3.945 | 2.045 | 7.003 | 0.221 | 1.749 | 2.408 |

| 2011 | 2.130 | 4.797 | 2.132 | 4.038 | 2.181 | 6.160 | 0.207 | 1.665 | 1.905 |

| 2012 | 1.729 | 4.317 | 2.068 | 3.996 | 2.225 | 5.411 | 0.173 | 1.412 | 2.201 |

| 2013 | 2.301 | 5.446 | 2.039 | 4.513 | 2.762 | 5.708 | 0.141 | 1.594 | 2.541 |

| 2014 | 2.550 | 5.122 | 1.786 | 3.955 | 2.026 | 4.576 | 0.186 | 1.500 | 2.258 |

| 2015 | 2.277 | 4.678 | 1.605 | 3.383 | 1.181 | 3.794 | 0.193 | 1.455 | 2.299 |

| 2016 | 1.927 | 5.252 | 1.301 | 3.105 | 1.259 | 4.160 | 0.218 | 1.207 | 1.832 |

| 2017 | 1.918 | 5.753 | 1.208 | 3.006 | 1.450 | 3.644 | 0.196 | 1.150 | 2.156 |

| 2018 | 1.577 | 6.543 | 1.756 | 3.681 | 1.564 | 3.544 | 0.166 | 1.384 | 2.111 |

| 2019 | 1.712 | 6.324 | 1.538 | 3.390 | 1.741 | 4.940 | 0.161 | 1.416 | 2.102 |

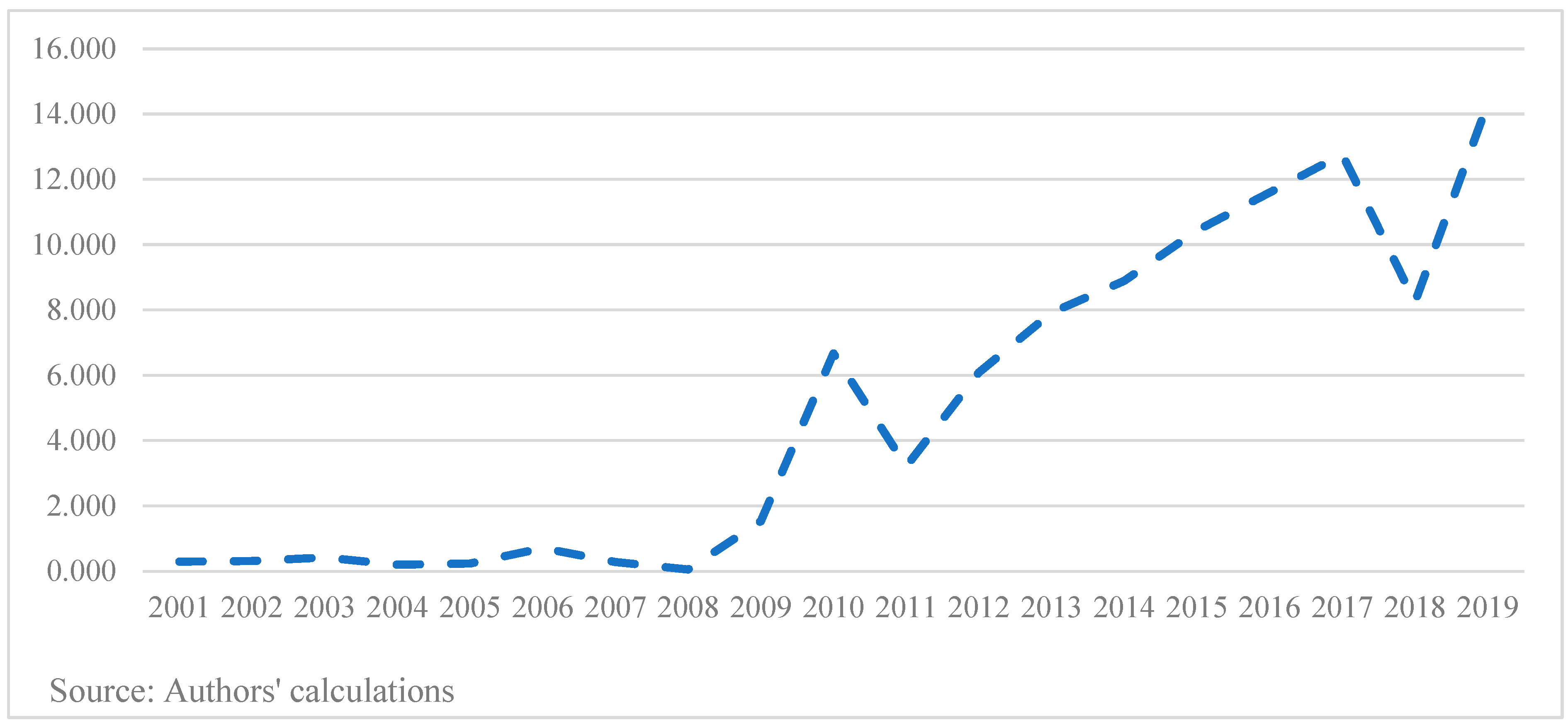

| MCA of India’s Goods Export to Korea | |||||||||

| HS Code 76 | HS Code 27 | HS Code 29 | HS Code 72 | HS Code 84 | HS Code 52 | HS Code 85 | HS Code 23 | HS Code 26 | |

| 2001 | 0.293 | 0.000 | 2.671 | 1.773 | 0.196 | 29.243 | 0.099 | 20.907 | 4.308 |

| 2002 | 0.313 | 0.350 | 2.743 | 1.347 | 0.224 | 32.065 | 0.058 | 23.593 | 5.620 |

| 2003 | 0.422 | 0.283 | 2.144 | 1.877 | 0.204 | 39.553 | 0.059 | 22.695 | 7.387 |

| 2004 | 0.195 | 0.407 | 2.185 | 1.676 | 0.237 | 36.176 | 0.068 | 19.122 | 5.808 |

| 2005 | 0.235 | 0.954 | 2.248 | 1.602 | 0.236 | 29.067 | 0.066 | 13.615 | 5.701 |

| 2006 | 0.705 | 1.141 | 2.407 | 1.151 | 0.250 | 23.205 | 0.047 | 26.476 | 4.273 |

| 2007 | 0.280 | 1.018 | 3.326 | 1.156 | 0.348 | 21.756 | 0.070 | 24.086 | 4.936 |

| 2008 | 0.057 | 1.258 | 2.462 | 1.472 | 0.303 | 14.093 | 0.095 | 15.558 | 0.780 |

| 2009 | 1.533 | 1.971 | 2.313 | 0.746 | 0.256 | 11.781 | 0.068 | 5.669 | 1.685 |

| 2010 | 6.670 | 1.191 | 2.429 | 1.494 | 0.237 | 21.613 | 0.057 | 7.492 | 0.402 |

| 2011 | 3.209 | 1.271 | 2.911 | 1.812 | 0.218 | 11.904 | 0.100 | 8.234 | 0.680 |

| 2012 | 6.084 | 0.803 | 3.045 | 2.230 | 0.275 | 15.662 | 0.119 | 13.409 | 0.338 |

| 2013 | 7.919 | 0.641 | 3.148 | 2.742 | 0.323 | 16.761 | 0.112 | 14.637 | 0.523 |

| 2014 | 8.888 | 1.033 | 2.302 | 2.056 | 0.290 | 16.010 | 0.118 | 10.000 | 0.444 |

| 2015 | 10.433 | 0.641 | 3.202 | 2.316 | 0.350 | 19.162 | 0.129 | 9.558 | 0.155 |

| 2016 | 11.598 | 0.898 | 3.385 | 2.227 | 0.402 | 18.121 | 0.139 | 5.381 | 0.012 |

| 2017 | 12.766 | 0.775 | 3.228 | 2.440 | 0.328 | 17.392 | 0.124 | 5.313 | 0.813 |

| 2018 | 8.234 | 0.752 | 3.269 | 3.005 | 0.292 | 22.296 | 0.197 | 7.285 | 0.885 |

| 2019 | 14.323 | 0.674 | 3.810 | 2.165 | 0.415 | 20.310 | 0.211 | 7.644 | 0.923 |

| Grubel–Lloyd Index | |||||||||

| From Korea to India | From India to Korea | ||||||||

| HS Code 85 | HS Code 72 | HS Code 84 | HS Code 27 | HS Code 85 | HS Code 72 | HS Code 84 | HS Code 27 | ||

| 2001 | 0.093 | 0.754 | 0.174 | 0.210 | 0.062 | 0.538 | 0.099 | 0.580 | |

| 2002 | 0.092 | 0.857 | 0.179 | 0.180 | 0.051 | 0.630 | 0.109 | 0.000 | |

| 2003 | 0.044 | 0.969 | 0.080 | 0.430 | 0.015 | 0.748 | 0.084 | 0.065 | |

| 2004 | 0.036 | 0.805 | 0.126 | 0.419 | 0.023 | 0.682 | 0.084 | 0.022 | |

| 2005 | 0.038 | 0.647 | 0.217 | 0.425 | 0.022 | 0.637 | 0.113 | 0.000 | |

| 2006 | 0.042 | 0.465 | 0.195 | 0.391 | 0.026 | 0.409 | 0.139 | 0.691 | |

| 2007 | 0.131 | 0.460 | 0.188 | 0.348 | 0.064 | 0.378 | 0.153 | 0.803 | |

| 2008 | 0.156 | 0.626 | 0.205 | 0.335 | 0.063 | 0.566 | 0.150 | 0.657 | |

| 2009 | 0.077 | 0.265 | 0.183 | 0.333 | 0.063 | 0.259 | 0.191 | 0.635 | |

| 2010 | 0.064 | 0.381 | 0.124 | 0.327 | 0.035 | 0.390 | 0.114 | 0.714 | |

| 2011 | 0.081 | 0.434 | 0.121 | 0.295 | 0.064 | 0.424 | 0.088 | 0.625 | |

| 2012 | 0.109 | 0.362 | 0.134 | 0.337 | 0.083 | 0.402 | 0.091 | 0.867 | |

| 2013 | 0.100 | 0.479 | 0.168 | 0.411 | 0.074 | 0.498 | 0.143 | 0.814 | |

| 2014 | 0.082 | 0.394 | 0.175 | 0.610 | 0.065 | 0.392 | 0.147 | 0.736 | |

| 2015 | 0.112 | 0.268 | 0.199 | 0.728 | 0.059 | 0.277 | 0.145 | 0.894 | |

| 2016 | 0.081 | 0.289 | 0.219 | 0.642 | 0.070 | 0.296 | 0.197 | 0.969 | |

| 2017 | 0.084 | 0.307 | 0.218 | 0.765 | 0.056 | 0.302 | 0.207 | 0.942 | |

| 2018 | 0.123 | 0.303 | 0.148 | 0.777 | 0.106 | 0.298 | 0.121 | 0.954 | |

| 2019 | 0.148 | 0.247 | 0.195 | 0.742 | 0.113 | 0.222 | 0.159 | 0.981 | |

| 1 | The number in the parentheses refers to the HS Code at the six-digit tariff line. |

| 2 | The rules of origin, as the name suggests, determines from which country the products originate from. It is important as tariffs and NTMs in several cases depend upon a national source of a product. |

| 3 | Intra-industry trade can be of the horizontal intra-industry type which is trading in products which are similar in quality, for instance, the ROK exporting and importing automobiles from India. IIT can also be of a vertical intra-industry type where trade in high- and low-quality technology intensive items happens (Krugman 1981). |

| 4 | https://www.ideasforindia.in/topics/trade/india-s-trade-protectionism-and-low-productivity-vicious-cycle.html (accessed on 3 January 2022). |

| 5 | In September 2014, the Indian government announced the policy “Make in India” to establish India as the global manufacturing hub. Moreover, “Atmanirbhar Bharat Abhiyan” was also introduced in May 2020 for India’s self-reliance and economic revival in the time of the COVID-19 pandemic. |

| 6 | We selected nine items for the analysis because it is necessary to discuss iron and steel in this study. India has imposed anti-dumping on iron and steel from Korea (The Economic Times 2020). |

| 7 | Based on the definition of the World Trade Organization, commercial services include manufacturing services on physical inputs owned by others, maintenance and repair services, transport, travel, construction, insurance and pension services, financial services, charges for the use of intellectual property, telecommunications, computers and information services, other business services, and personal, cultural, and recreational services. (https://www.wto.org/english/res_e/statis_e/technotes_e.htm, accessed on 10 June 2021). |

| 8 | We chose six items as opposed to the five most important items as vehicles, the sixth most important item, are extensively exported by the ROK to India. |

| 9 | We are looking at the broad trend of India–Korea trade relations and hence we did not go for a higher degree of product disaggregation (beyond the HS Codes two-digit level). |

| 10 | Basically, the RCA and MCA are similar concepts. In some papers, the RCA has been employed to analyze the comparative advantage in a specific market, rather than measuring the comparative advantage in the world market. Please refer to Kuzmenko et al. (2022) for the RCA. |

| 11 | Theoretically, country a’s import from b is the same as country b’s export to a. Generally, exports are recorded on the FOB while imports are recorded on the CIF basis which could contribute to the difference. Therefore, we strictly follow this formula. |

| 12 | We also calculated the RSCA (Revealed Symmetric Comparative Advantage) and found that the RSCA exhibits a similar result with the use of the MCA. Hence, we do not report that in this article. |

| 13 | According to the WTO, other business services include trade-related services, operational leasing (rentals), and miscellaneous business, professional, and technical services such as legal, accounting, management consulting, public relations services, advertising, market research and public opinion polling, research and development services, architectural, engineering, and other technical services, agricultural, mining, and on-site processing (https://www.wto.org/english/res_e/statis_e/technotes_e.htm, accessed on 10 June 2021). |

| 14 | A: Manufacturing services on physical inputs owned by others; B: Maintenance and repair services n.i.e.; C: Transport; D: Travel; E: Construction; F: Insurance; G: Financial services; H: Charges for the use of intellectual property n.i.e.; I: Telecommunications, computer, and information services; J: Other business services; K: Personal, cultural, and recreational services. |

| 15 | Trade policy measures pertain to merchandized trade; therefore, in this section, we examine tariffs and NTMs impacting merchandise tradable items. The government measures impacting services trade are not available. |

References

- Ahmed, Shahid. 2011. India-Korea CEPA: An Assessment. Korea and the World Economy 12: 45–98. [Google Scholar]

- Balassa, Bela. 1965. Trade Liberalisation and “Revealed” Comparative Advantage. The Manchester School 33: 99–123. [Google Scholar] [CrossRef]

- Banik, Nilanjan. 2001. An Analysis of India’s Exports during the 1990s. Economic and Political Weekly 36: 4222–30. [Google Scholar]

- Banik, Nilanjan, Debashis Chakraborty, and Sampada Kumar Dash. 2021. IPR Waiver in Vaccines and Opportunities for India: What Does the Data Show? UNESCAP Working Paper. Bankok: United Nations Economic and Social Commission for Asia and the Pacific. [Google Scholar]

- Burange, L. G., Sheetal J. Chaddha, and Poonam Kapoor. 2010. India’s Trade in Services. The Indian Economic Journal 58: 44–62. [Google Scholar] [CrossRef]

- Cho, Choongjae, Young Chul Song, Jung-Mi Lee, and Chi Hyun Yun. 2018. An Analysis of the Competitiveness and Difficulties in Korea’s Export to India; Research Paper 18-15; Sejong: Korea Institute of International Economic Policy. (In Korean)

- Cho, Jun-Hyon. 2012. The Change and Tendency of TSI of Korean Industries after Korea-India CEPA. Journal of Industrial Economics and Business 25: 1559–85. (In Korean). [Google Scholar]

- Cho, Mee Jin, and Bo Young Choi. 2019. The Analysis on the Use of Korea-India CEPA. Journal of International Trade and Industry Studies 24: 51–75. (In Korean). [Google Scholar]

- Chuang, Yih-Chyi. 1998. Learning by doing, the technology gap, and growth. International Economic Review 39: 697–721. [Google Scholar] [CrossRef]

- Danna-Buitrago, Jenny P., and Remi Stellian. 2021. A New Class of Revealed Comparative Advantage Indexes. Open Economies Review 2021: 1–27. [Google Scholar] [CrossRef]

- Dash, Ranjan Kumar Das, and P. C. Parida. 2013. FDI, services trade and economic growth in India: Empirical evidence on causal links. Empirical Economics 45: 217–38. [Google Scholar] [CrossRef]

- Feder, Gershon. 1983. On exports and economic growth. Journal of Development Economics 12: 59–73. [Google Scholar] [CrossRef]

- Feenstra, Rober C. 1998. Integration of trade and disintegration of production in the global economy. Journal of Economic Perspectives 12: 31–50. [Google Scholar] [CrossRef] [Green Version]

- Gereffi, Gary. 1999. International trade and industrial upgrading in the apparel commodity chain. Journal of International Economics 48: 37–70. [Google Scholar] [CrossRef]

- Government of India (GOI). 2021. Brief on India-Korea Economic and Commercial Relations. Available online: https://www.indembassyseoul.gov.in/page/india-rok-trade-and-economic-relations/#:~:text=1.,mark%20for%20the%20first%20time.&text=Korea’s%20total%20FDI%20to%20India,2020%20stands%20at%20%246.94%20billion (accessed on 12 December 2021).

- Grubel, Herb, and Peter John Lloyd. 1975. Intra-Industry Trade: The Theory and Measurement of International Trade in Differentiated Products. New York: Wiley. [Google Scholar]

- Gupta, Apoorva, Ila Patnaik, and Ajay Shah. 2018. Exporting and Firm Performance: Evidence from India. NIPFP Working Paper No. 243. New Delhi: NIPFP. [Google Scholar]

- International Trade Center (ITC). 2020. Available online: https://intracen.org/resources/tools?it%5B126%5D=126 (accessed on 12 November 2021).

- Kemeny, Thomas, and David Rigby. 2012. Trading away what kind of jobs? Globalization, trade and tasks in the US economy. Review of World Economics 148: 1–16. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Kim, Nam Doo, Yongkul Won, Chaiwook Chun, and Hoon Chung. 1997. Changing Patterns of East Asia’s Trade and Direct Investment and a Policy Agenda; Seoul: Korea Institute of International Economic Policy, pp. 97–109. (In Korean)

- Kim, Tae-Heon. 2009. An Empirical Study on the Export Competitiveness of Korean Automobiles in the Local Chinese Market. International Area Studies Review 13: 583–611. (In Korean). [Google Scholar]

- Krugman, Paul R. 1981. Intraindustry Specialization and the Gains from Trade. Journal of Political Economy 89: 959–73. [Google Scholar] [CrossRef]

- Kuzmenko, Elena, Lenka Rumankova Irena Benesova, and Lubos Smutka. 2022. Czech Comparative Advantage in Agricultural Trade with Regard to EU-27: Main Developmental Trends and Peculiarities. Agriculture 12: 217. [Google Scholar] [CrossRef]

- Lee, Soon Chul. 2019. The Effect of the Korea-India CEPA and 3rd FTAs on the Bilateral Trade between Korea and India. Journal of International Trade and Industry Studies 24: 49–79. (In Korean). [Google Scholar]

- Nath, Hiranya K., and Binoy Goswami. 2018. India’s comparative advantages in services trade. Eurasian Economic Review 8: 323–42. [Google Scholar] [CrossRef]

- Pailwar, Veena, and Nirav R. Shah. 2009. Revealed comparative advantages for India in services trade. International Journal of Trade and Global Markets 2: 109–27. [Google Scholar] [CrossRef]

- Plouffe, Michael. 2017. Firm heterogeneity and trade-policy stances evidence from a survey of Japanese producers. Business and Politics 19: 1–40. [Google Scholar] [CrossRef] [Green Version]

- Sauve, Pierre, and Aaditya Mattoo, eds. 2003. Domestic Regulation and Service Trade Liberalization. Washington, DC: World Bank Publications. [Google Scholar]

- Shukla, Srijan. 2021. India’s Trade Protectionism and Low-Productivity Vicious Cycle. Available online: https://www.ideasforindia.in/topics/trade/india-s-trade-protectionism-and-low-productivity-vicious-cycle.html (accessed on 4 January 2022).

- The Economic Times. 2020. India imposes anti-dumping duty on certain steel products from China, Vietnam, Korea. The Economic Times, June 23. [Google Scholar]

- World Bank. 2020. World Development Indicators 2014. Washington, DC: The World Bank. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

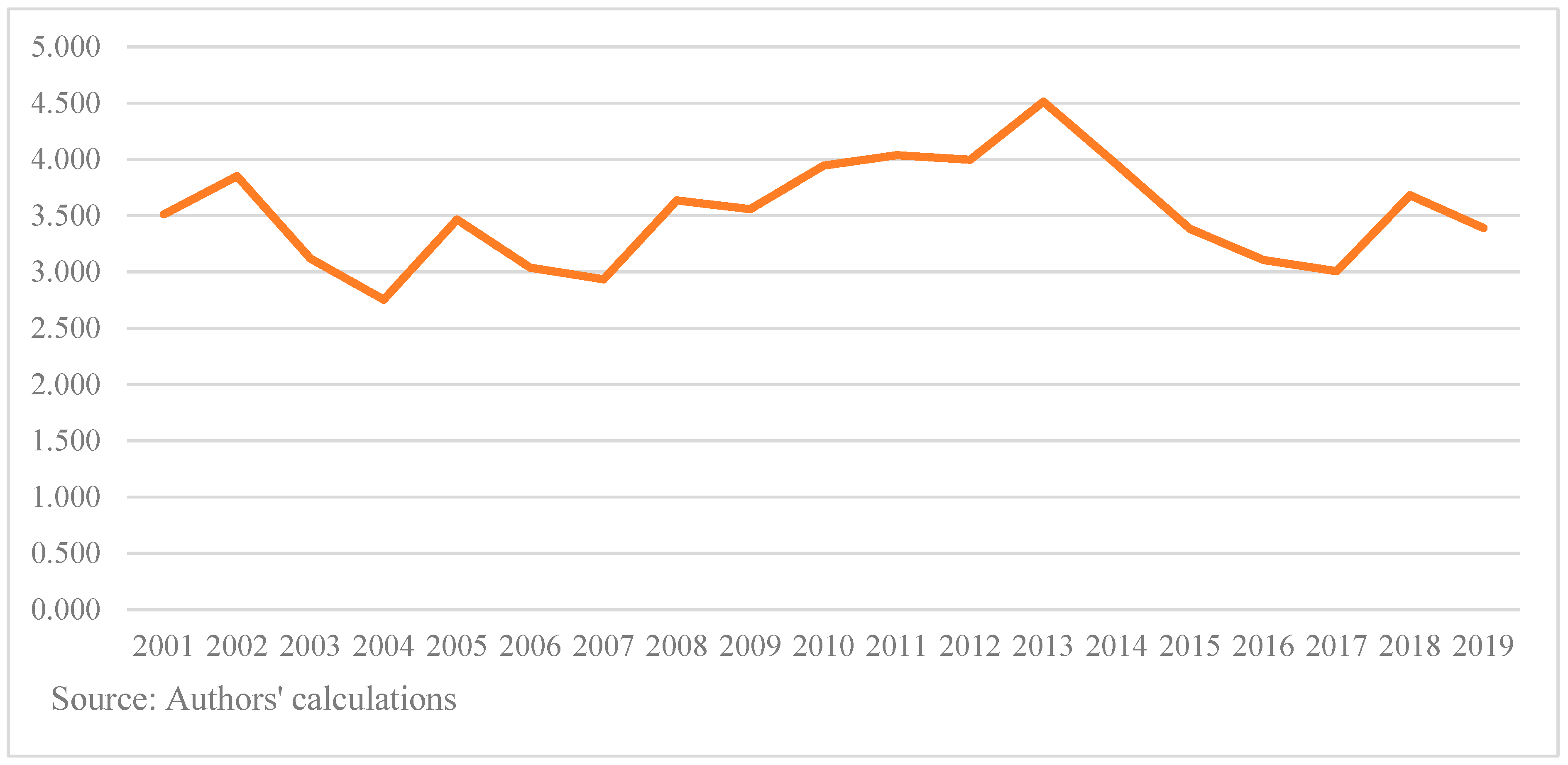

| ROK’s Exports to India (USD mil) | Growth Rate of ROK’s Exports to India (%) | ROK’s Export to the World (USD mil) | Share of India in ROK’s Total Exports (%) | India’s Exports to ROK (USD mil) | Growth Rate of India’s Exports to ROK (%) | India’s Exports to the World (USD mil) | Share of ROK in India’s Total Exports (%) | |

|---|---|---|---|---|---|---|---|---|

| 2001 | 1136 | 150,430 | 0.8 | 457 | 43,878 | 1.0 | ||

| 2002 | 1256 | 10.6 | 162,466 | 0.8 | 623 | 36.2 | 50,097 | 1.2 |

| 2003 | 2409 | 91.8 | 193,817 | 1.2 | 663 | 6.4 | 59,360 | 1.1 |

| 2004 | 3363 | 39.6 | 253,844 | 1.3 | 970 | 46.2 | 75,904 | 1.3 |

| 2005 | 4412 | 31.2 | 284,418 | 1.6 | 1519 | 56.7 | 100,352 | 1.5 |

| 2006 | 4891 | 10.9 | 325,457 | 1.5 | 2321 | 52.8 | 121,200 | 1.9 |

| 2007 | 5437 | 11.2 | 371,477 | 1.5 | 2462 | 6.1 | 145,898 | 1.7 |

| 2008 | 8350 | 53.6 | 422,003 | 2.0 | 3773 | 53.2 | 181,860 | 2.1 |

| 2009 | 8229 | −1.4 | 363,531 | 2.3 | 3772 | 0.0 | 176,765 | 2.1 |

| 2010 | 9922 | 20.6 | 466,380 | 2.1 | 3634 | −3.7 | 220,408 | 1.6 |

| 2011 | 12,362 | 24.6 | 555,208 | 2.2 | 4549 | 25.2 | 301,483 | 1.5 |

| 2012 | 13,675 | 10.6 | 547,854 | 2.5 | 4076 | −10.4 | 289,564 | 1.4 |

| 2013 | 12,426 | −9.1 | 559,648 | 2.2 | 4495 | 10.3 | 336,611 | 1.3 |

| 2014 | 13,437 | 8.1 | 573,091 | 2.3 | 4794 | 6.7 | 317,544 | 1.5 |

| 2015 | 13,085 | −2.6 | 526,900 | 2.5 | 3603 | −24.9 | 263,889 | 1.4 |

| 2016 | 12,213 | −6.7 | 495,465 | 2.5 | 3464 | −3.8 | 260,963 | 1.3 |

| 2017 | 16,084 | 31.7 | 573,716 | 2.8 | 4378 | 26.4 | 295,862 | 1.5 |

| 2018 | 16,441 | 2.2 | 605,169 | 2.7 | 4817 | 10.0 | 323,997 | 1.5 |

| 2019 | 16,111 | −2.0 | 542,333 | 3.0 | 4653 | −3.4 | 323,250 | 1.4 |

| ROK’s Exporting Commodities to India | India’s Exporting Commodities to the ROK | |

|---|---|---|

| 1 | HS Code 85: Electrical machinery and equipment and parts thereof (18.1%) | HS Code 76: Aluminum and articles thereof (17.9%) |

| 2 | HS Code 72: Iron and steel (15.5%) | HS Code 27: Mineral fuels, mineral oils, and products of their distillation (17.0%) |

| 3 | HS Code 84: Machinery, mechanical appliances, nuclear reactors, and boilers (14.3%) | HS Code 29: Organic chemicals (9.6%) |

| 4 | HS Code 39: Plastics and articles thereof (10.5%) | HS Code 72: Iron and steel (6.7%) |

| 5 | HS Code 29: Organic chemicals (7.2%) | HS Code 84: Machinery, mechanical appliances, nuclear reactors, and boilers (4.3%) |

| 6 | HS Code 87: Vehicles other than railway or tramway rolling stock, and parts and accessories thereof (6.2%) | HS Code 52: Cotton (4.0%) |

| 7 | HS Code 27: Mineral fuels, mineral oils, and products of their distillation (4.8%) | HS Code 85: Electrical machinery and equipment and parts thereof (3.8%) |

| 8 | HS Code 90: Optical, photographic, cinematographic instruments (3.2%) | HS Code 23: Residues and waste from the food industries; prepared animal fodder (3.4%) |

| 9 | HS Code 73: Articles of iron or steel (1.9%) | HS Code 26: Ores, slag, and ash (2.8%) |

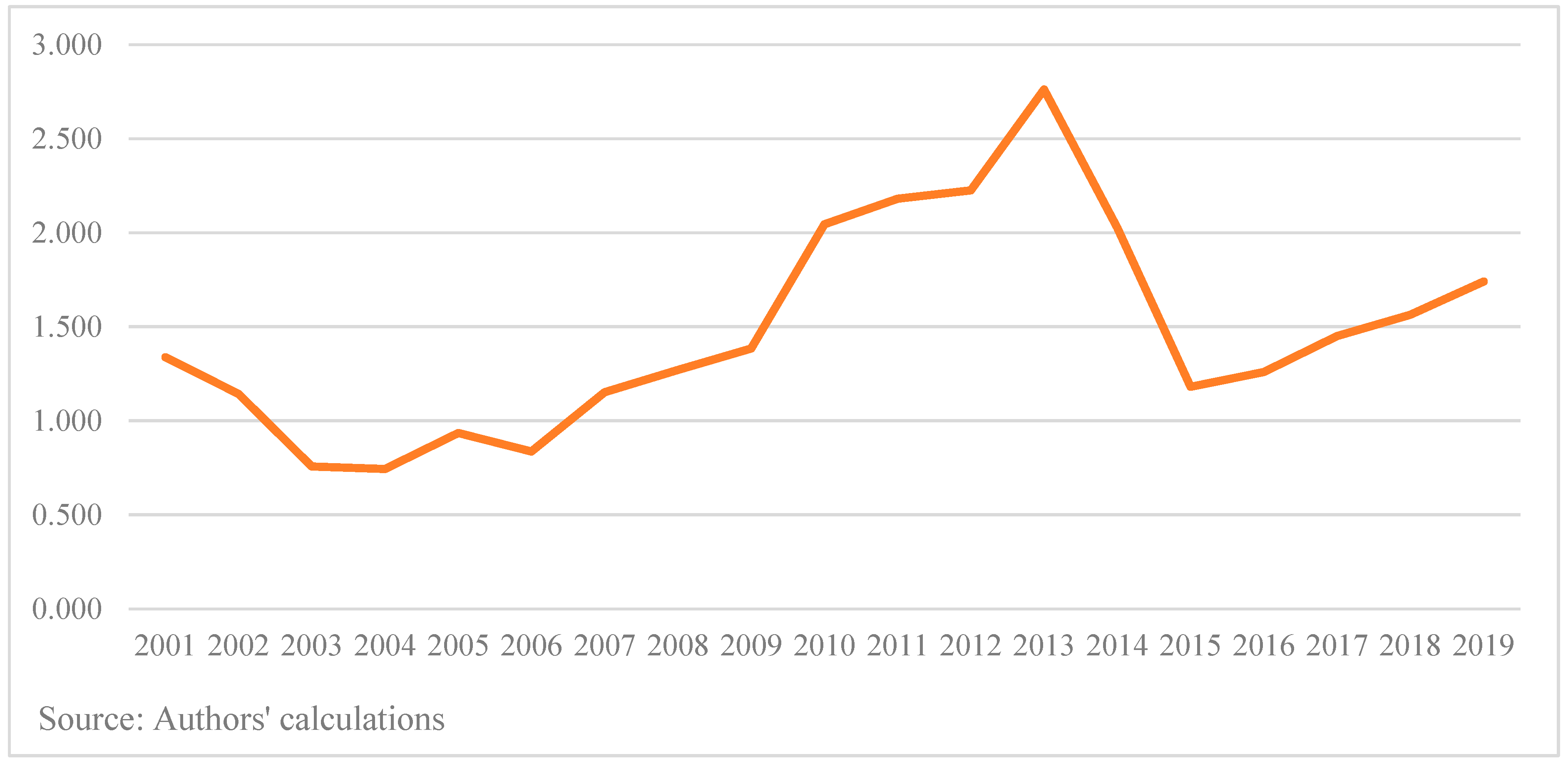

| ROK’s Export of Commercial Services to India (USD mil) | ROK’s Export of Commercial Services to the World (USD mil) | Share of India in ROK’s Commercial Services Export (%) | India’s Export of Commercial Services to ROK (USD mil) | India’s Export of Commercial Services to the World (USD mil) | Share of ROK in India’s Commercial Services Export (%) | |

|---|---|---|---|---|---|---|

| 2005 | 1179 | 49,312 | 1.52% | 948 | 51,851 | 1.83% |

| 2006 | 897 | 55,503 | 1.62% | 1405 | 69,166 | 2.03% |

| 2007 | 1179 | 69,793 | 1.69% | 1677 | 86,235 | 1.94% |

| 2008 | 1654 | 89,839 | 1.84% | 2185 | 105,668 | 2.07% |

| 2009 | 1391 | 71,427 | 1.95% | 1983 | 92,484 | 2.14% |

| 2010 | 1703 | 81,932 | 2.08% | 2288 | 116,563 | 1.96% |

| 2011 | 1860 | 89,365 | 2.08% | 2652 | 137,906 | 1.92% |

| 2012 | 2066 | 101,899 | 2.03% | 2669 | 145,016 | 1.84% |

| 2013 | 2020 | 102,116 | 1.98% | 2728 | 148,699 | 1.83% |

| 2014 | 2260 | 110,757 | 2.04% | 3019 | 156,601 | 1.93% |

| 2015 | 2052 | 96,443 | 2.13% | 2854 | 155,701 | 1.83% |

| 2016 | 2001 | 93,893 | 2.13% | 2934 | 161,221 | 1.82% |

| 2017 | 2104 | 88,720 | 2.37% | 3500 | 184,621 | 1.90% |

| 2018 | 2160 | 97,957 | 2.21% | 3778 | 204,258 | 1.85% |

| 2019 | 2271 | 101,473 | 2.24% | 3965 | 213,702 | 1.86% |

| 2005 | 2010 | 2015 | 2017 | 2019 | |

|---|---|---|---|---|---|

| A. Manufacturing services on physical inputs owned by others | 3 | 5 | 8 | 7 | 6 |

| B. Maintenance and repair services n.i.e. | 0 | 0 | 11 | 14 | 21 |

| C. Transport | 374 | 735 | 665 | 536 | 518 |

| D. Travel | 124 | 323 | 435 | 468 | 564 |

| E. Construction | 122 | 384 | 360 | 319 | 267 |

| F. Insurance and pension services | 2 | 8 | 11 | 18 | 12 |

| G. Financial services | 7 | 17 | 18 | 28 | 34 |

| H. Charges for the use of intellectual property n.i.e. | 17 | 42 | 107 | 136 | 134 |

| I. Telecommunications, computer, and information services | 8 | 35 | 140 | 212 | 238 |

| J. Other business services | 91 | 147 | 278 | 345 | 348 |

| K. Personal, cultural, and recreational services | 1 | 7 | 18 | 22 | 29 |

| Total commercial services | 748 | 1703 | 2052 | 2104 | 2271 |

| Share of India in ROK’s total services exports | 1.5% | 2.1% | 2.1% | 2.4% | 2.2% |

| 2005 | 2010 | 2015 | 2017 | 2019 | |

|---|---|---|---|---|---|

| A. Manufacturing services on physical inputs owned by others | 0 | 0 | 15 | 11 | 22 |

| B. Maintenance and repair services n.i.e. | 0 | 0 | 2 | 3 | 3 |

| C. Transport | 154 | 355 | 340 | 430 | 509 |

| D. Travel | 253 | 517 | 714 | 1000 | 1062 |

| E. Construction | 2 | 4 | 9 | 15 | 19 |

| F. Insurance and pension services | 17 | 39 | 38 | 50 | 49 |

| G. Financial services | 13 | 77 | 66 | 58 | 60 |

| H. Charges for the use of intellectual property n.i.e., | 6 | 5 | 15 | 22 | 28 |

| I. Telecommunications, computer, and information services | 229 | 642 | 811 | 842 | 956 |

| J. Other business services | 273 | 632 | 823 | 1039 | 1222 |

| K. Personal, cultural, and recreational services | 2 | 18 | 22 | 27 | 36 |

| Total commercial services | |||||

| Share of ROK in India’s total services exports | 1.8% | 2.0% | 1.8% | 1.9% | 1.9% |

| A | B | C | D | E | F | G | H | I | J | K | |

|---|---|---|---|---|---|---|---|---|---|---|---|

| 2005 | - | - | 0.911 | 1.612 | 16.302 | 0.044 | 0.648 | 2.035 | 0.436 | 0.539 | 0.766 |

| 2006 | - | - | 0.867 | 1.521 | 20.032 | 0.077 | 0.512 | 1.969 | 0.663 | 0.488 | 2.402 |

| 2007 | - | - | 0.843 | 1.459 | 28.400 | 0.058 | 0.451 | 1.193 | 0.459 | 0.571 | 1.819 |

| 2008 | - | - | 0.920 | 1.503 | 30.568 | 0.049 | 0.283 | 0.830 | 0.331 | 0.357 | 0.813 |

| 2009 | - | - | 0.771 | 1.658 | 24.148 | 0.014 | 0.214 | 0.987 | 0.425 | 0.357 | 0.090 |

| 2010 | - | - | 0.977 | 1.912 | 24.014 | 0.099 | 0.156 | 1.069 | 0.601 | 0.358 | 0.104 |

| 2011 | - | - | 0.748 | 1.812 | 27.093 | 0.062 | 0.139 | 1.248 | 0.881 | 0.428 | 1.668 |

| 2012 | 12.505 | 1.234 | 0.726 | 1.928 | 33.133 | 0.047 | 0.202 | 0.708 | 0.811 | 0.386 | 1.330 |

| 2013 | 13.835 | 0.000 | 0.668 | 2.090 | 25.529 | 0.079 | 0.120 | 0.754 | 0.960 | 0.426 | 0.975 |

| 2014 | 15.546 | 0.993 | 0.636 | 1.843 | 28.059 | 0.092 | 0.184 | 0.792 | 1.241 | 0.524 | 0.623 |

| 2015 | 16.488 | 2.029 | 0.724 | 1.668 | 21.410 | 0.120 | 0.329 | 1.215 | 2.097 | 0.530 | 0.748 |

| 2016 | 7.872 | 2.068 | 0.666 | 1.766 | 21.739 | 0.107 | 0.240 | 1.290 | 2.067 | 0.547 | 0.764 |

| 2017 | 11.130 | 1.829 | 0.623 | 1.683 | 17.296 | 0.190 | 0.320 | 1.384 | 2.317 | 0.646 | 0.680 |

| 2018 | 11.802 | 1.252 | 0.584 | 1.722 | 11.131 | 0.131 | 0.600 | 1.235 | 2.176 | 0.599 | 0.694 |

| 2019 | 6.271 | 1.278 | 0.574 | 1.843 | 10.326 | 0.133 | 1.117 | 1.272 | 1.856 | 0.566 | 0.734 |

| A | B | C | D | E | F | G | H | I | J | K | |

|---|---|---|---|---|---|---|---|---|---|---|---|

| 2005 | 0.000 | 0.000 | 0.461 | 1.024 | 0.142 | 1.447 | 3.450 | 0.079 | 34.837 | 1.290 | 0.885 |

| 2006 | 0.000 | 0.000 | 0.478 | 0.864 | 0.188 | 1.327 | 2.133 | 0.021 | 13.754 | 1.530 | 0.643 |

| 2007 | 0.000 | 0.000 | 0.438 | 0.877 | 0.136 | 1.493 | 1.498 | 0.047 | 16.794 | 1.544 | 0.892 |

| 2008 | 0.000 | 0.000 | 0.425 | 1.014 | 0.118 | 2.076 | 1.420 | 0.045 | 18.848 | 1.371 | 1.116 |

| 2009 | 0.000 | 0.000 | 0.559 | 1.146 | 0.117 | 2.005 | 0.803 | 0.045 | 17.122 | 1.058 | 3.824 |

| 2010 | 0.000 | 0.000 | 0.491 | 1.156 | 0.073 | 1.855 | 1.687 | 0.023 | 18.674 | 1.131 | 1.180 |

| 2011 | 0.000 | 0.000 | 0.581 | 1.210 | 0.060 | 3.068 | 1.531 | 0.052 | 17.974 | 1.021 | 0.378 |

| 2012 | 0.022 | 1.057 | 0.550 | 1.160 | 0.072 | 2.277 | 1.166 | 0.047 | 18.844 | 1.102 | 0.678 |

| 2013 | 0.023 | 6.284 | 0.534 | 1.105 | 0.066 | 1.825 | 1.514 | 0.057 | 16.967 | 1.104 | 1.026 |

| 2014 | 0.083 | 0.637 | 0.559 | 1.115 | 0.102 | 2.344 | 1.542 | 0.079 | 15.464 | 1.054 | 0.961 |

| 2015 | 0.067 | 0.221 | 0.447 | 1.097 | 0.135 | 1.769 | 1.494 | 0.058 | 11.247 | 1.128 | 1.284 |

| 2016 | 0.051 | 0.228 | 0.466 | 1.046 | 0.221 | 1.565 | 1.361 | 0.064 | 10.752 | 1.165 | 1.364 |

| 2017 | 0.043 | 0.229 | 0.507 | 1.125 | 0.197 | 1.461 | 1.063 | 0.081 | 8.689 | 1.107 | 1.322 |

| 2018 | 0.075 | 0.196 | 0.506 | 1.096 | 0.227 | 1.842 | 1.187 | 0.089 | 10.013 | 1.156 | 1.351 |

| 2019 | 0.073 | 0.150 | 0.541 | 1.139 | 0.187 | 1.143 | 0.868 | 0.088 | 8.955 | 1.109 | 1.175 |

| India’s Exports to ROK | Number of Tariffs Lines | Average Tariffs (%) | Maximum Average Tariffs (%) |

| Petroleum oils and oils from bituminous minerals | 6 | 0.5 | 3 |

| Aluminum; unwrought (not alloyed) | 1 | 0 | 0 |

| Ferro-alloys; ferro-chromium | 1 | 0 | 0 |

| Zinc; unwrought (not alloyed) | 1 | 0 | 0 |

| Oil-cake and other solid residues | 1 | 0 | 0 |

| ROK’s Exports to India | Number of Tariffs Lines | Average Tariffs (%) | Maximum Average Tariffs (%) |

| Electronic integrated circuits | 1 | 0 | 0 |

| Petroleum oils and oils from bituminous minerals | 9 | 4.94 | 6 |

| Vehicle parts and accessories, nec | 1 | 5 | 5 |

| Vehicle parts; gearboxes and parts thereof | 1 | 7.5 | 7.5 |

| Vinyl chloride, other halogenated olefin polymers | 1 | 7.5 | 7.5 |

| Existing Tariffs (%) | Simulated Tariffs (%) | Current Trade (USD mil) | Simulated Trade Value (USD mil) | |

|---|---|---|---|---|

| India’s exports to ROK | ||||

| Petroleum oils and oils from bituminous minerals | 0.5 | 0 | 1206.07 | 1234.36 |

| ROK’s exports to India | ||||

| Petroleum oils and oils from bituminous minerals | 4.94 | 0 | 704.86 | 747.67 |

| Vehicle parts and accessories, nec | 5 | 0 | 325.82 | 344.08 |

| Vehicle parts; gearboxes and parts thereof | 7.5 | 0 | 308.10 | 331.09 |

| Vinyl chloride, other halogenated olefin polymers | 7.5 | 0 | 306.83 | 333.99 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Banik, N.; Kim, M. India–Republic of Korea CEPA: Assessment and Future Path. Economies 2022, 10, 104. https://doi.org/10.3390/economies10050104

Banik N, Kim M. India–Republic of Korea CEPA: Assessment and Future Path. Economies. 2022; 10(5):104. https://doi.org/10.3390/economies10050104

Chicago/Turabian StyleBanik, Nilanjan, and Misu Kim. 2022. "India–Republic of Korea CEPA: Assessment and Future Path" Economies 10, no. 5: 104. https://doi.org/10.3390/economies10050104

APA StyleBanik, N., & Kim, M. (2022). India–Republic of Korea CEPA: Assessment and Future Path. Economies, 10(5), 104. https://doi.org/10.3390/economies10050104