1. Introduction

The COVID-19 pandemic has significantly hit the global economy and posed serious challenges to governments all over the world. In 2020, global GDP fell by 3.41% (y.o.y) compared to 2019. The current crisis differs from the Asian Financial Crisis of 1998 (AFC) in terms of disruption as the AFC impacted economies mostly through a shortfall in demand, with direct supply-side disruption found only in the banking and finance sectors. Rather than crisis shock itself, the economic recession drove the real sector disruption during the financial crisis (

Baldwin and Mauro 2020). This time, the shocks of the health crisis directly harmed the demand and supply sides by hindering the production of industry as the result of mobility restrictions to contain the virus’s spread.

The COVID-19 pandemic has brought economic contraction in almost all regions in Indonesia, particularly Java and Sumatra. The deeper contraction in Java is explained by the rapid increase in daily new infections as a result of greater testing rates in major provinces such as DKI Jakarta and East Java (

Sparrow et al. 2020). The high infection rate in provinces with relatively large economies is inevitable since their high population density, mobility, and connectivity provide ideal circumstances for the virus to thrive (

Hsu 2020). In Indonesia, provinces with high human interaction activities have been significantly hit by the strict mobility restrictions during the pandemic, such as Bali that is primarily reliant on tourism. On the other hand, some provinces are surviving the economic contraction surprisingly well, as seen by positive economic growth in 2020. These provinces are based primarily on natural resources rather than human interaction activities.

Many businesses, particularly in the Java region as the epicenter of economic activities, are cutting off costs by temporarily shutting down operations and laying off workers. As a result, Statistics Indonesia (BPS) recorded that 2.69 million people lost their job in 2020. High employment losses translate into lower household income, resulting in the poverty rate jumping to 9.78% in 2020 from 9.41% in 2019, which reflects the short-term immediate income effects due to mobility restrictions. The contraction mostly affects the most vulnerable segments of society, namely the near-poor and informal sector workers in urban areas (

Sparrow et al. 2020).

To dampen the impact on the most vulnerable group, the Government of Indonesia (GoI) has allocated around 30% of the total national economic recovery (PEN) funds in 2020 for social protection and consumption programme. The heavy additional expenditures for dealing with the crisis have brought exceptional challenges to the GoI since they also faced massive revenue shortfalls. The impact of the crisis on fiscal balance is fully reflected in the figures of the State Budget (APBN) and its policy. The APBN was already amended twice in 2020, in April (Presidential Decrees No. 54 of 2020) and in June (Presidential Decrees No. 72 of 2020). The GoI slashed central government revenue from Rp2233 trillion in the first version of APBN to only Rp1700 trillion in the latest APBN. On the other hand, the central government expenditure significantly increased from Rp2540 to Rp2739 trillion following the massive amount of stimulus for recovery programmes. The revised budget reflected a gloomy outlook for the economy as revenues continue to decrease, while expenditures increase. As a result, Indonesia faced the first ever-widening budget deficit since the AFC, at 6.09% of GDP in 2020. The high deficit has pushed the GoI to undertake extraordinary reforms of its budget policy as the President had passed a decree to allow budget deficits to exceed the threshold of 3% as stipulated by Law No. 17 of 2003. The temporarily lifted reform of the budget deficit is allowed until the end of the 2022 fiscal year.

In the spirit of bringing the deficit back under the threshold, while also financing the national economic recovery, the GoI has taken several measures. In the first budget amendment, the government already tried to recover some amount of money to finance the national economic recovery by re-evaluating central government expenditure. The strategy includes reducing the amount of central capital funds allocated to ministries and central government institutions. The government has also evaluated the efficiency of health and education spending to find the least efficient spending. Moreover, the central government has also pushed the local governments to re-evaluate their spending in the spirit of finding the most efficient structure of the Local Budgets (APBD) during the COVID-19 pandemic.

Indonesia has implemented substantial decentralized administration of local government since 2001, which allows local governments to play a stronger role in managing their APBD. Local governments are required to develop the APBD and present it to their Regional House of Representatives (DPRD) for approval each year. Before implementing APBD, local governments must also obtain approval from the Ministry of Home Affairs. Similar to most countries, the decentralized system in Indonesia utilizes intergovernmental transfers from central to provincial governments in order to ensure local governments have sufficient resources to deliver to the public. The tax is collected by the central government, and it is distributed to local governments through transfers. There are three major components of transfers, namely the General Allocation Fund (DAU), Special Allocation Fund (DAK), and Revenue Sharing Fund (DBH).

In times of COVID-19, countries around the world have adopted countercyclical fiscal policy to minimize the socio-economic impact of the COVID-19 pandemic (

International Monetary Fund 2020). The central government mandated local governments to evaluate and minimize their spending following the reduction in intergovernmental fiscal transfer from 34% of the total expenditure to only 28% on the revised national budget. The central government has also shifted the allocation of intergovernmental fiscal transfers from DAU into DAK as well as the village fund (

dana desa). However, the implementation of budget policies at the provincial level has been in turmoil as the budget policy for all provinces has been implemented with the same encounter, regardless of their specific condition. The central government policy required local governments to refocus the local budget to handle the COVID-19 pandemic under the Ministry of Home Affairs Decree (Permendagri No. 20 of 2020), including the re-allocation of DAK to finance certain health services. Local governments have also been pushed to reallocate their goods and services expenditure as well as capital expenditure in their APBD. Despite the tight measurement for the local budget, unfortunately, there are not many funds allocated by the local governments.

Qibthiyyah (

2021) found that the revised budgets in some provinces, to some extent, are even lower than previously planned. As of May 2020, the amount of reallocated budget from local government has only amounted to Rp85 trillion or far below the expectations. The main reason why regions have disregarded directives from the central government is mainly due to their poor ability to manage financial matters, coupled with the severe contraction of local revenue due to COVID-19.

Local governments have also faced budget shortfalls following the contraction in local own-source revenue (PAD) due to the lower economic activity. Local governments face a harder situation than central government because their options for additional sources of income are limited (

Halimatussadiah et al. 2020). As a result, the crisis has put immense pressure on APBD across provinces. Local governments are not being agile in responding with fiscal adjustment during the crisis, as during the normal situation, the local budgets are relatively secure and rely heavily on central transfer. Facing revenue shortfalls, local budget management measures will vary among provinces because of the distinct number of COVID-19 cases, diverse fiscal capacity, different capability to reach budget efficiency, and varied opportunities to develop alternative sources of income.

However, there have only been a few discussions about the effect of the COVID-19 pandemic on local budget conditions in the existing literature. Adding to the literature, we explore the responses of the local governments to the pandemic using three major fiscal indicators at the provincial level, namely, fiscal capacity index, solvency ratio, and level of autonomy. We examine the linkage between fiscal indicators with the macroeconomic conditions of each province in the first period of the pandemic in 2020. We also analyse ways of reshaping local budgets in the medium-to-long-term since governments must find the most efficient policy to manage their budgets to boost economic growth in the long-term. Thus, two main contributions of this paper are to investigate how local governments have responded to fiscal challenges during COVID-19 and how medium-to-long-term approaches can be used to reshape the local budgets following the pandemic.

Our paper is organized as follows. The first section is an introduction. The second section reviews the existing literature related to the urgency of countercyclical fiscal policy, ways of managing the local budget during the crisis, and the need to achieve fiscal sustainability. The data and methodology used in this paper are then demonstrated in the third section. The fourth section presents the results of the analysis, followed by the strategies towards fiscal sustainability in the fifth section and the conclusion in the sixth section.

2. Literature Review

Countries around the world grapple with the economic impact brought by the COVID-19 pandemic by using fiscal and monetary policies. In times of economic volatility, states assume social and fiscal responsibilities by implementing expenditure policies directed at mitigating the adverse effects of negative economic cycles on the general welfare of citizens (

International Monetary Fund 2009). In accordance with the countercyclical role of the state, government spending should be increased during contractionary periods and decreased during expansionary periods (

Sharp 1958).

Learning from history, the countercyclical fiscal policy role of the state can be seen in the increased state expenditure during the Great Depression of 1929 until early 1930s where the aim was to stimulate economic recovery while also protecting the citizens from stagnating into deplorable poverty (

Snell 2009). Spending in the United States was at its highest when economic activity was at its lowest, based on the 1929 constant prices (

Sharp 1958). Moreover, during the 2009 Global Financial Crisis, we can see how government intervention, in their countercyclical role of adopting stimulus packages, can cushion the economy against financial shocks. This demonstrates the state’s countercyclical role in keeping the supply and demand sides of the economy afloat when periodic economic volatility undermines the general population’s financial position.

Unlike advanced countries, emerging markets have historically pursued procyclical fiscal policies on both the spending and the revenue sides. Indonesia is no exception; when the economy performs well, the government commonly increases its spending in the following year and vice versa. This procyclicality is merely because emerging markets’ limited access to international credit markets in bad times coupled with political incentives and institutional weaknesses in good times tend to encourage “excessive” public spending (

Riascos and Vegh 2003). Put differently, the textbook recommendation of saving on sunny days for rainy days is rarely followed in emerging markets.

COVID-19 has created a global recession where millions of workers are now unemployed, overall household incomes and expenses have declined, many companies and various business organizations have stopped paying their workers and have laid off millions of workers, net exports have declined, and as a result, the aggregate spending has shifted downwards in recent months. This has the potential to triple the country’s challenges of unemployment, poverty, and inequality if state institutions are incapable of implementing countercyclical policies effectively by directing capacity and resources to minimize the impact of the pandemic and resuscitating the economy for inclusive growth (

Khambule 2021). This has led countries across the globe, developed and underdeveloped, to adopt countercyclical measures to minimize the socio-economic impact of the COVID-19 pandemic (

International Monetary Fund 2020).

In the United States, the revenue transfers to local governments played an instrumental role in the state’s spending structure and supplemented the revenues of local governments. The payments played a countercyclical role by offsetting the local government-burdened revenue structure (

Gordon 2012). This was important as local governments have limited tax bases and often rely on revenue streams, and they faced harder challenges during times of economic volatility, rendering them unable to finance their services. Without an improved financial base, local governments will have to lower their spending in relation to a decline in their revenues; yet the central government has the power to increase its spending even in the face of an economic downturn due to its diverse revenue structures (

Snell 2009). A similar scenario also happened in Indonesia, where the major source of local revenue still comes from intergovernmental transfer by approximately 60% on average in 2019. Yet, several transfers from the central government come with a specific target and objective, making the allocation less flexible than it could be.

As an early response, the Government of Indonesia issued the Ministry of Home Affairs Decree (Permendagri No. 20 of 2020) on a guideline to provinces and local governments, which is more on re-allocating spending items, to ensure that provinces and local governments have sufficient funding to manage the COVID-19 pandemic in their respective region. Although there is a need to allocate more funds to handle the COVID-19 health crisis, in some provinces and local governments, the revised budget to some extent is lower than previously planned (

Qibthiyyah 2021). However, there may be a condition in which operating costs of provincial and/or local government-related services and/or revenues was expected to decline.

Many works of literature have identified that local government needs to maintain their spending, increase infrastructure spending especially to health sectors, and avoid tax during an economic crisis. Another way the local government can weather the economic storm is using the fund balances, often referred to as rainy-day funds. According to

Lauth (

2003), the local governments that can cope most successfully with economic downturns are the ones that have planned ahead and taken proactive measures to insulate themselves during the economic “booms,” making the “busts” more manageable. They have achieved this, among other ways, by diversifying their local economy and revenue streams, maintaining large fund balances, and carefully assessing their policy mission and goals (

Scorsone and Plerhoples 2010).

Afonso (

2013) also found that some of the local governments in the United States began preparing for a recession several years before it hit. Some of them reported that they were less affected by the recession because of long-term planning, which meant that they started making cuts before the effects of the recession manifested, allowing them to build up their fund balances. Hence, proactive planning by fund balances mechanism is crucial.

At the end of the day, a fund balance mechanism is only an enabling environment for local governments to adopt a contracting fiscal policy. Nevertheless, countercyclical fiscal policies, such as giving stimulus for the health sector, social protection, and incentives for the business sector, are only effective in the short term. Furthermore, the government needs to find more sources of financing to reduce their fiscal burden, popularly by issuing bonds. In consequences, the issuance cost—the increasing debt-to-GDP ratio—is another fiscal problem. This is an inevitable condition that is faced by the government amid the COVID-19 situation, which also means that the government is shifting their current costs to a long-term burden (

Zen and Kimura 2020). Thus, achieving fiscal sustainability in the future by planning their budget for debt repayment is becoming crucial for the government.

For the local provincial and district and/or city government, measuring whether a local government will achieve fiscal sustainability is harder due to the nature of fiscal sustainability analysis. Based on

Burnside (

2005) and

Marks (

2004), fiscal sustainability explains the condition to assess a government’s ability to service its debt obligations without explicitly defaulting on them. However, until now, no local government has issued debt of its own. In the time of COVID-19, most local governments applied for debt to the central government, increasing the burden on central government to find sources of financing. In addition, the local government budget heavily depends on central government transfers. Thus, maintaining expenditure and generating revenue is the only key to achieving budget sustainability and building up a more resilient budget for any future shocks.

The dependency of the local government budget on the central government puts pressure for central government to perform well. Once the COVID-19 crisis has been resolved and the economy has recovered and resumed its normal growth trajectory, the central government must prioritize maintaining sustainable fiscal policies in order to assist the local government to also achieve it. An increase in government debts should be followed by a debt repayment schedule which will increase future government expenditure. According to

Asimakopoulos and Karavias (

2016);

Forte and Magazzino (

2016), and

Hajamini and Falahi (

2018), an increase in government expenditure relative to GDP is often associated with higher economic growth, but only up to a point. Beyond that point, as the government expenditure to GDP ratio rises, the opportunity cost of government expenditure increases, contributing to a less optimal allocation of resources in the economy; meaning that the relationship between the ratio of government expenditure to GDP and GDP growth turns negative.

In the long-term, the government should adopt a neoclassical policy by reducing spending and raising taxes to control the fiscal deficit and further increases in debt and debt burden. Older empirical literature also links the success and persistence of fiscal consolidations in emerging market countries to the extent that the government reduces current expenditure and adjusts revenue (

Adam and Bevan 2003).

Vegh et al. (

2018) found that fiscal consolidation, in which policy is swift when the economy improves, leads to higher economic growth in the long run. When the central government achieves this condition, the local government benefits as well, resulting in better fiscal conditions for local governments.

Since previous literature emphasizes the importance of implementing countercyclical fiscal policy during the crisis and appropriately managing the budget, as well as maintaining fiscal sustainability to have a more resilient fiscal framework to weather any future shocks, there are only a few studies on local government responses to the local budget during the COVID-19 crisis. As a result, we attempt to add value to the recent literature by examining the local budget conditions during the COVID-19 crisis in Indonesia as a decentralized nation and suggesting several strategies that should be implemented by local government to achieve fiscal sustainability.

4. Results

To analyse the ability of local government in managing the impact of COVID-19, we provided several fiscal indicators and combined them with macroeconomic variables during the pandemic and pre-pandemic. First, we employed fiscal capacity index provided by the Ministry of Finance (MoF) to observe the provinces’ ability in generating fiscal revenue and maintaining fiscal stability. Substantially, the fiscal capacity index provides a slight yet notable vision of the overall ability and capacity of the local government budget. The major source of local revenue still comes from the intergovernmental transfer by approximately 60% on average in 2019. Yet, several transfers from the central government come with a specific target and objective, making the allocation less flexible than it could be. Aside from central government transfers, improved performance in generating fiscal revenue will be the key to a robust and promising fiscal capacity.

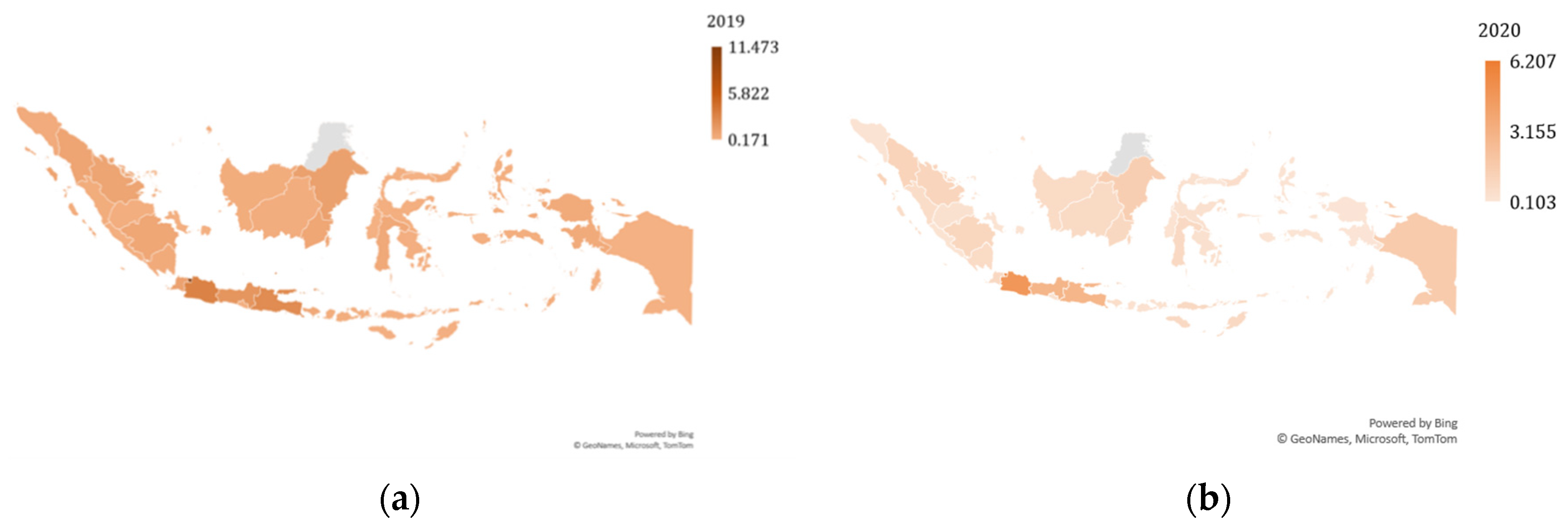

The fiscal capacity index in 2020 showed a similar pattern compared to its figure before the pandemic (

Figure 1) even though the value was decreased due to the lower economic activity during the outbreak. The mapping of fiscal capacity index and economic growth in 2020 (

Figure 2) shows that provinces with a higher fiscal capacity index have good achievement in generating their local own-source revenue, which is also mainly driven by economic activities. In contrast, other provinces with limited revenue-generating capabilities continue to rely heavily on fiscal transfers from the central government. On the contrary, provinces that enjoyed growth during the pandemic, such as Papua, West Nusa Tenggara, and Central Sulawesi, are primarily contributed to by agriculture and fishery, as well as mining sectors that remained operating during the outbreak. Unfortunately, with the small proportion of local own-source revenue and additional spending to manage the pandemic’s impact, the growth was not translated into a broader fiscal space.

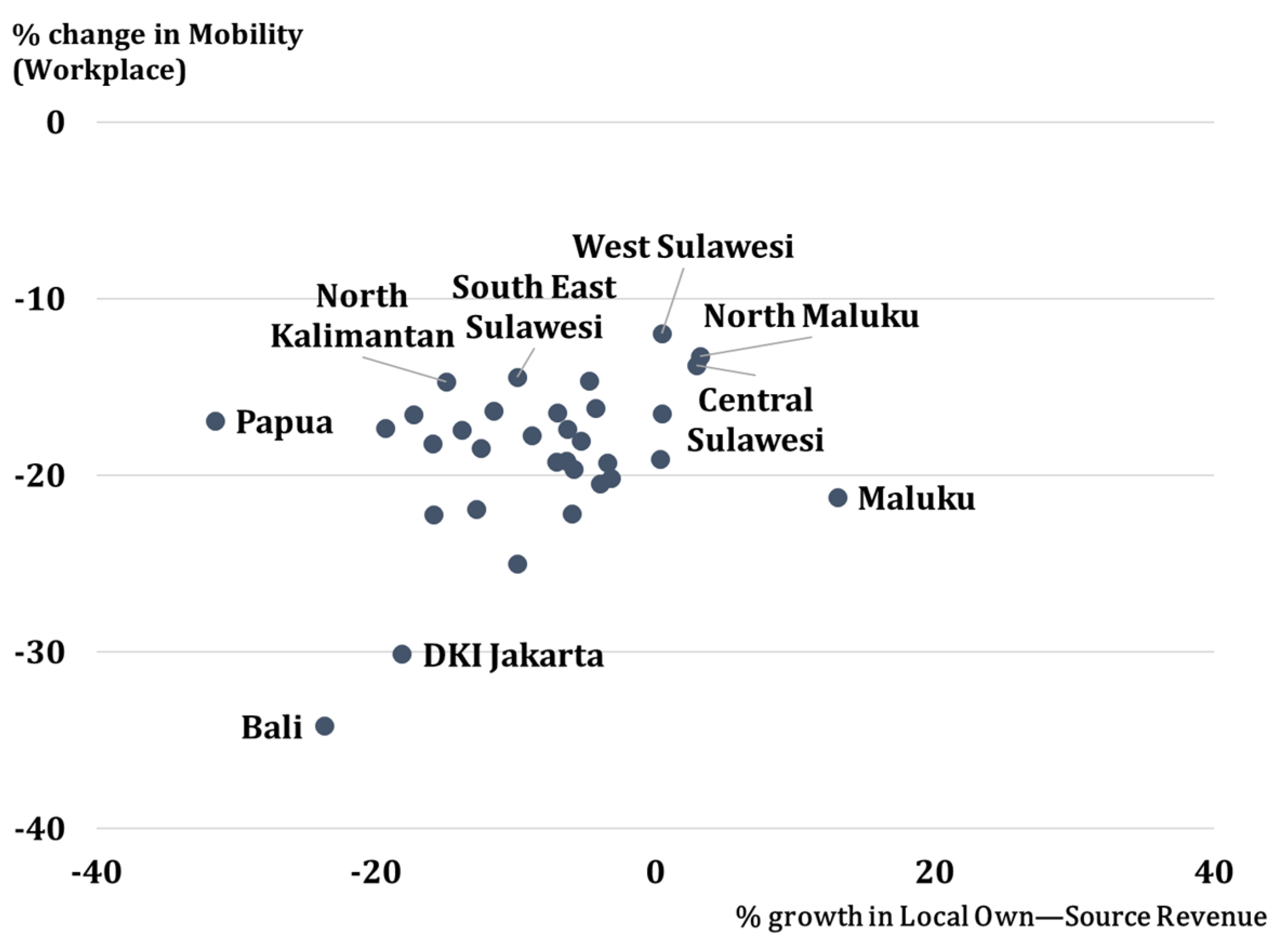

Reg—GDP Growth Looking deeper, we compare the growth of local own-source revenue with the intensity of people’s mobility during the COVID-19 period using data from Google Mobility Index for the overall year in 2020 (

Figure 3 and

Figure 4). During the early COVID-19 period, the intensity was persistently recorded as being in negative territory. Lower mobility corresponded to slower growth in local own-source revenue, the majority of which comes from consumption-activity taxes such as restaurant tax and hotel tax, as well as fuel tax. Among all provinces, Papua was acknowledged as the main loser in the arena that recorded an immense decline of local own-source revenue. Looking at other provinces, Bali and DKI Jakarta reported the most notable changes in mobility, both for recreation and workplace, relative to other provinces. The events were parallel with the negative growth of local own-source revenue generated by the two provinces.

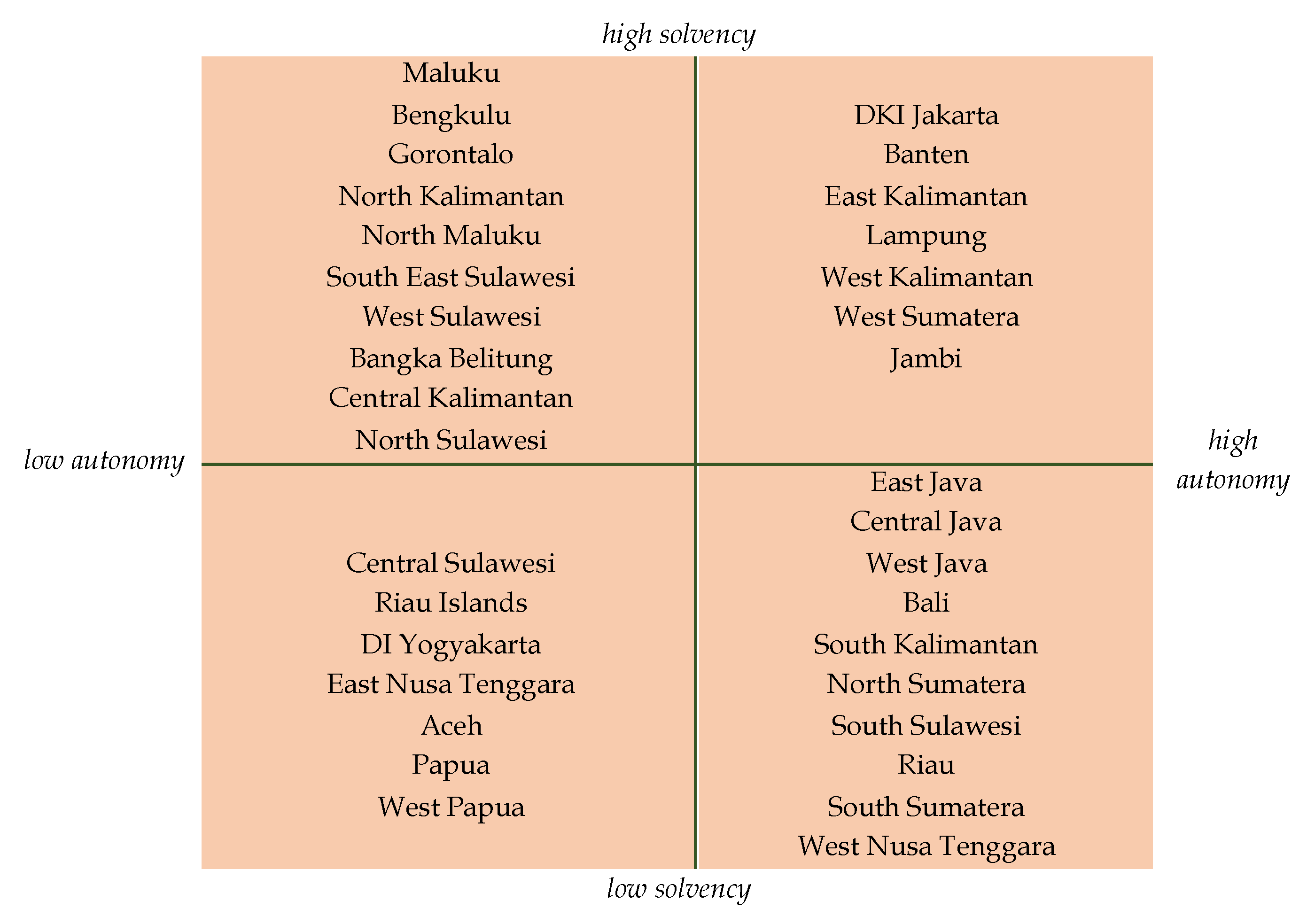

The next indicator that we used in mapping local budget capability was the solvency ratio to look further into the ability of local government in managing their budget. We combined the solvency ratio with the level of autonomy to develop an analysis and occupy the linkage between the two variables. We concluded from the proportion of local own-source revenue to total revenue. The proportion implies that the bigger the amount, the higher the level of autonomy. In other words, the provinces with a greater proportion play a better role in generating revenue from other sources, making them less reliant on central government transfers.

Referring to

Figure 5, provinces are divided into four quadrants based on their level of solvency and level autonomy. DKI Jakarta and several other provinces are defined by high solvency and autonomy. Other provinces with a similar fiscal capacity index pattern, such as West Java and East Java, are known to have a lower solvency ratio. We may conclude that, despite their higher level of autonomy and ability to generate local own-source revenue, certain provinces may need to put more effort into managing spending allocation.

Maluku and North Maluku are two eastern Indonesian provinces that are considered to be rather reliant on central government transfers. Aceh, along with Papua and West Papua, share the same attitude, as the province has received an additional fiscal transfer in the form of a special autonomy fund (Dana Otsus) since the beginning of the decentralization era. Despite their high reliance on central government transfers, Maluku and North Maluku have managed to form a more solvent budget than other dependent provinces.

As many people are aware, Indonesia has been implementing a decentralization system since the new-order regime fell in the late 1990s. It is believed that the system will improve economic and social conditions because local governments will be able to instantly capture local needs (

Bardhan 2002). However, it is also believed that local governments are more resilient to economic shocks because they are still dependent on central government for intergovernmental transfers (

Wolkoff 1987). During the unprecedented moment of COVID-19, and the central government’s stance at its vulnerable point, the local budget was also negatively affected. Therefore, a firm fiscal stance is needed to finance the emergency measures triggered by the pandemic. With the limited fiscal space and government transfers during the pandemic era, an alternative source of income and a better-spending scenario are critical.

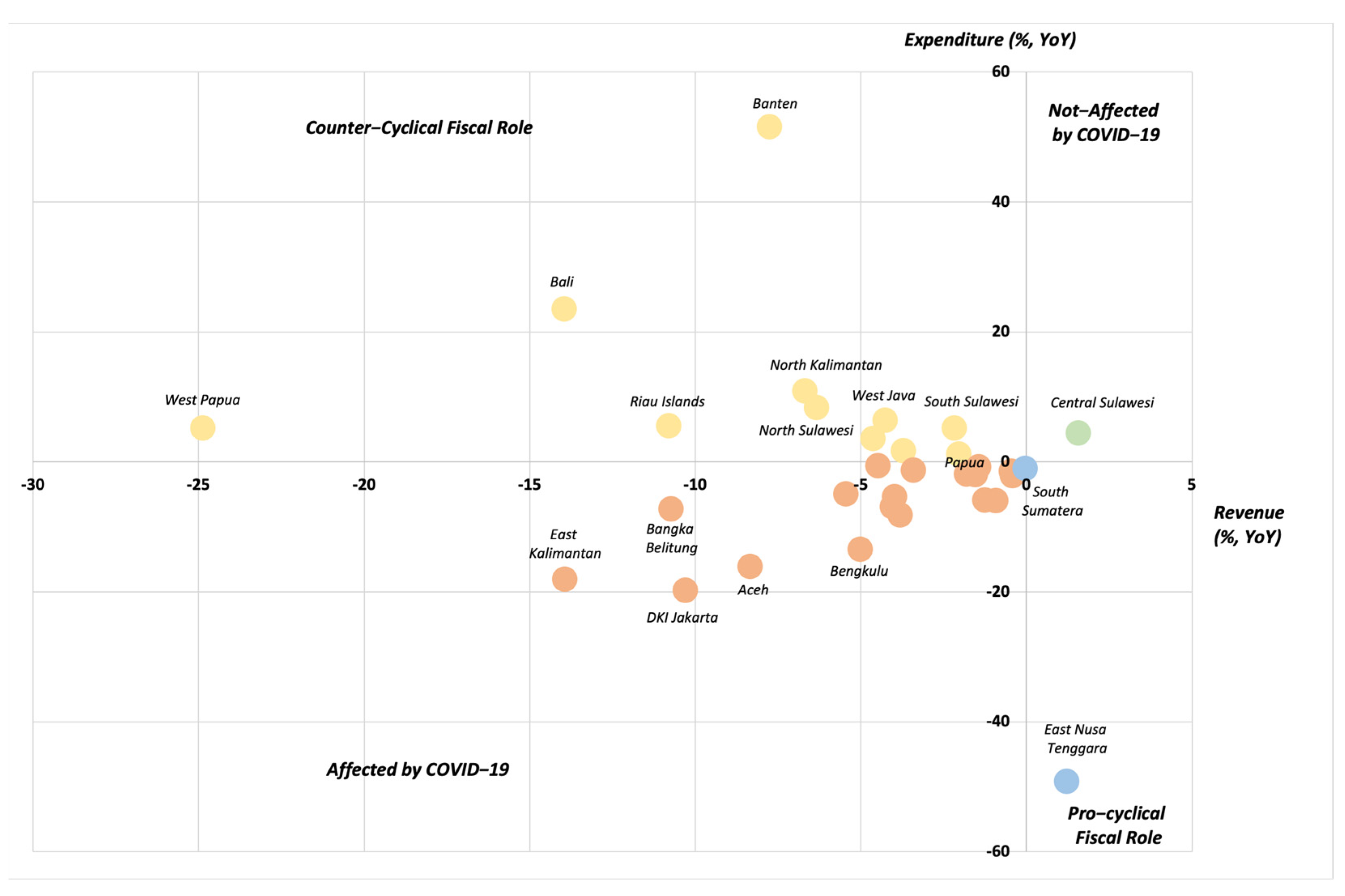

Furthermore, this study evaluates how local governments are dealing with the COVID-19 crisis (

Figure 6) by mapping provinces into four categories based on changes in revenues and expenditures during 2020 (the first period of pandemic) compared to 2019 (the pre-crisis period). The first category is the provinces that are not affected by COVID-19, marked by an increase in both revenue and expenditure. The second category is the provinces that implemented a countercyclical fiscal policy during the pandemic, indicated by a decrease in their revenue, but which successfully managed to increase their expenditure. The third category is the provinces that are affected by the COVID-19, shown by a decrease in both revenue and expenditure. This indicates that the local budget was contracted since they could not manage to implement a countercyclical fiscal policy during these bad times through increased spending. The last category is the provinces that implemented a procyclical fiscal policy during the pandemic, marked by an increase in revenue, but experienced a contraction in expenditure side.

From the mapping of fiscal conditions, only Central Sulawesi, which has a local budget, is not affected by the pandemic. Whereas 20 provinces in Indonesia appear to have fiscal constraints, we categorized these as the provinces that are affected by COVID-19 since they have not taken any policies to overcome the pandemic. The average of both government revenue and expenditure of provinces in the third category decreased by 8.2% and 6.5%, respectively, in 2020. The decline in the revenue was mainly due to an 8.4% decrease in average local own-source revenue, especially in the Java and Bali regions with high pandemic rates, and a 2.9% decrease in intergovernmental transfer. Meanwhile, decline in government expenditures occurred in both goods and services and capital expenditures, which fell 8.7% and 16.9%, respectively, for reallocation to weather the impact of COVID-19.

Eleven provinces were identified as having implemented a countercyclical fiscal policy. The increase in local government spending was caused by the high increase in social assistance and health expenditures in 2020 as a response to COVID-19. Only two provinces, South Sumatera and East Nusa Tenggara, implemented a procyclical fiscal policy. Based on the regional fiscal matrix for 2020, most provinces in Indonesia are severely affected by the pandemic and they face difficulty to absorb the local budget and reallocate spending effectively to overcome the crisis. The root cause of this problem is a weak fiscal management capacity. According to

Morgan and Trinh (

2017), in some developing countries, weak revenue management capacity causes local governments to not fully use their rights to collect their taxes. In terms of budget efficiency, several spending areas may be eliminated from the local budget, especially those that are inefficient, such as business travel spending. Local governments mostly spend more on personnel-related expenditures rather than capital expenditures, which currently devours 70% of total spending; thus the concept of better spending must be prioritized because the quality of spending remains deficient.

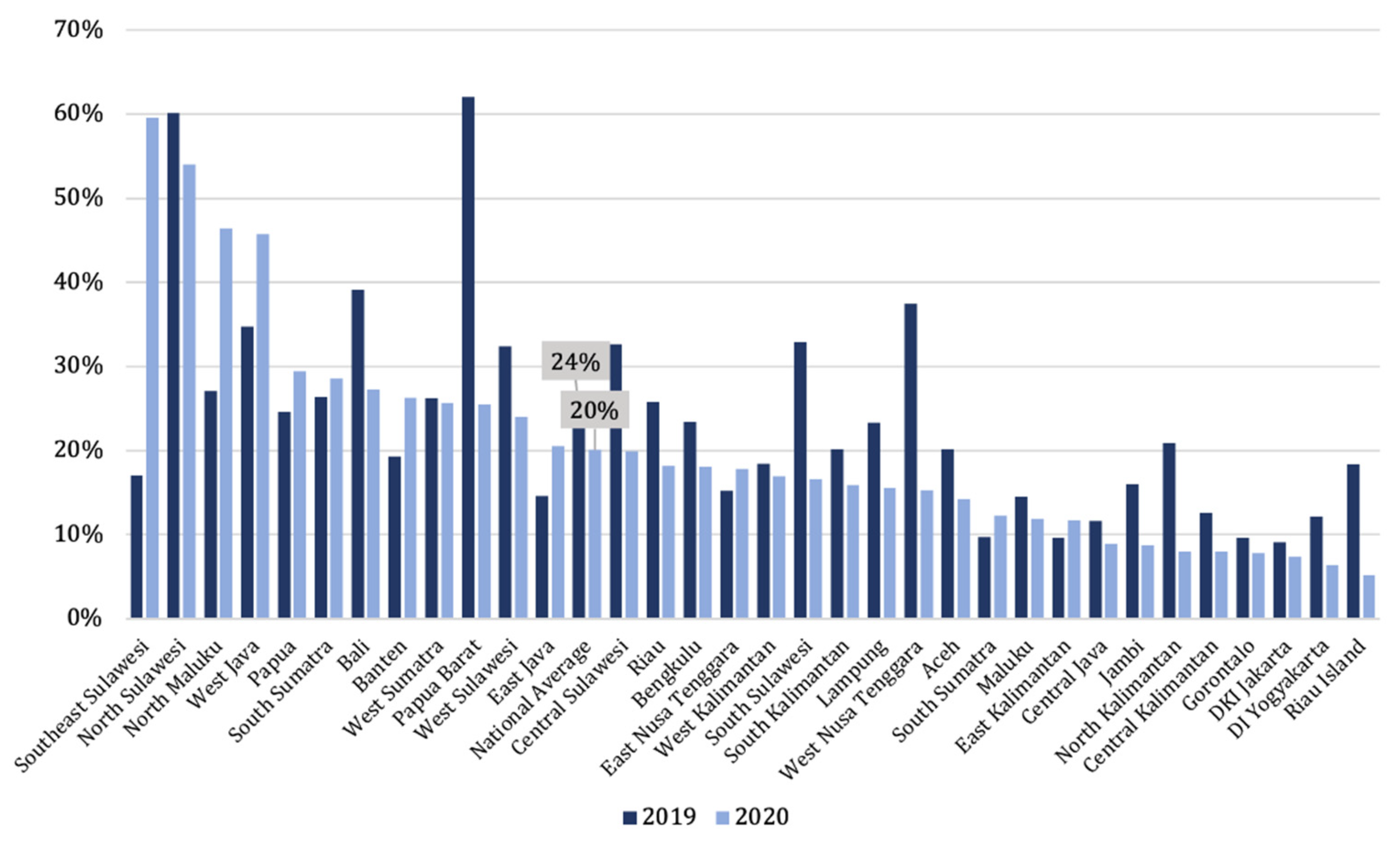

In facing the health crisis, the readiness of a country can be seen, for example from the health expenditure budget and the number of health facilities. We also examined how prepared Indonesia is in facing the pandemic based on the contribution of health expenditure on total expenditure and the availability of health facilities at a provincial level. Data for 2019 show that the proportion of health spending is still low: less than 20% in all provinces, with a national average of 9%. South Kalimantan, Aceh, and DKI Jakarta are three provinces with the highest proportion of health spending. On the other hand, the health expenditure only contributed to 3% of the total expenditure in DI Yogyakarta, Central Java, West Java, and West Papua.

However, the distribution of health facilities is not necessarily influenced by the proportion of the health expenditure budget. There is an uneven geographical distribution of health facilities, where the western part of Indonesia has more health facilities than the eastern part. The

World Bank Group (

2018) even found that the median distance to a health facility on Java is about 5 km, but the median distance in the eastern provinces is up to 30 km, and 18% of Indonesians travel for more than one hour to reach a public hospital. The disparity in health facilities is one of the serious problems faced by Indonesia, even before the COVID-19 pandemic. Therefore, improvements in health facilities in Indonesia are urgently needed to control the outbreak, or at least to be prepared if another wave of pandemics occurs. Although several provinces have increased their budgets, most local governments have reduced their health capital expenditures, which can be used to build health centres and facilities, as can be seen in

Figure 7. In 2020, the average ratio of health capital expenditure decreased by 4% compared to the previous year. As a result, local governments, particularly in the eastern part of Indonesia, lack adequate infrastructure to cope with the pandemic.

The local governments have limited fiscal space to deal with the health infrastructure problem during the outbreak. Local governments are experiencing a decrease in both local own-source revenue and transfer from the central government due to the pandemic (

Halimatussadiah et al. 2020). Furthermore, the central government’s response of building emergency hospitals around Indonesia drives local governments to neglect their problem. In consequence, local governments focused only on increasing their expenditure for health workers by 3% on average, while the other component of health expenditure for goods and services remained steady. Hence, the issue of overcrowding patients in regional hospitals is not surprising.

The COVID-19 outbreak provides the right momentum for local governments to refocus their health budget on capital expenditure to manage the pandemic situation as well as to reduce disparities in health infrastructure between regions in Indonesia. With an adequate health facility and infrastructure, the local government will have better resilience on their regional health system if a similar situation reoccurs in the future. Therefore, increasing local governments’ health capital expenditure will not only be a short-term effective spending but also an investment for the future.

5. Strategies toward Fiscal Sustainability

Fiscal policy is an important lever to contain the pandemic, mitigate the economic effects, and facilitate a rapid recovery. Immediate concern should be focused on finding strategies towards fiscal sustainability for local government while rebuilding fiscal resiliency over the medium term, thus appropriate responses can be prepared for another crisis. Next, this paper proposes several recommendations for the local government to achieve better and sustainable fiscal policy in the aftermath of the crisis.

5.1. Emergency Spending for Crisis, Climate Change, and Disaster Resilience Programme

Fiscal decentralization has led to a large variation in regional fiscal capacity (

Park and Maher 2020). We found that limited capability of several Indonesian local governments to generate revenue has hindered their ability to respond to the pandemic. Different geographical conditions and characteristics between regions also create large potential for future threats from climate change and disaster, including other health outbreaks. The circumstances force local governments take an active role in mitigating future economic losses by reprioritizing regional planning and budgeting. Local governments must build up financial reserves during periods of economic expansion to build much stronger financial resilience in facing difficult times and to fund climate change mitigation and disaster resilience programs. Local governments can build up financial reserves in a variety of ways, including the provision of idle funds, also known as emergency spending, and the utilization of fund balances. According to

Qibthiyyah (

2021), before 2020, emergency spending of Indonesian provincial governments was generally less than 0.1% of total spending; however, in 2020, emergency spending increased to an average of 3.32% of total spending with high allocation occurred in Java regions.

5.2. Diversification to Broaden the Source of Revenue

Taxes play an important role, both in terms of revenue levels and of tax structure, which may need to be adapted for a post-COVID-19 era (

OECD 2020). This suggests policymakers to implement tax policy reform, particularly by modifying local tax revenue systems with some new sources of local tax revenues, as well as increasing tax bases and tax rates from existing regional taxes or central government taxes distributed to regions. The government can focus on raising revenues from tax bases that are least detrimental to growth, such as forestry, plantation, and mining property tax (PBB P3) which is still collected centrally and distributed to the regions. Another potential source of local taxes is income tax, with the ‘Opsen’ scheme

2 depending on economic conditions such as those in the US and Europe. To boost tax revenues and broaden tax bases, local governments should be given the authority to collect income taxes. Furthermore, local governments can unleash their higher local revenue potential by implementing tax and administrative breaks for taxes paid to the provincial government, managing local-owned assets and other sources of income, and imposing environmental-related taxes under provincial authority such as fisheries retribution and surface water taxes.

5.3. A Concessional Loan from Government-Related Institutions

Local governments can benefit the soft loans from government-related institutions (e.g., PT. SMI and/or Regional Owned Enterprises or ROEs) which offer long tenor, relaxed terms, and low-interest rates. In providing budget support, it is crucial to observe the local’s repayment capacity. If the local government has an improper debt refinancing mechanism and continues to run budget deficits, it will limit the growth potential and put further challenges on fiscal resilience and stability. PT. SMI, as one of the special mission vehicles (SMV) under the MoF, has disbursed around Rp19.1 trillion in regional loans to 28 local governments during 2020 to accelerate regional economic recovery.

5.4. Developing Municipal Bonds

To finance public infrastructure provisions, local governments can issue municipal bonds. For investors, municipal bonds are highly attractive, since they are tax-exempted, meaning that their returns are not subjected to tax. Besides benefiting the local government as an alternative long-term financing source for capital expenditures, provinces that develop municipal bonds will improve fiscal decentralization and local autonomy as well as fiscal management through more prudent and transparent debt management.

Under the Minister of Finance Regulation No. 111 of 2012, municipal bonds can only be issued in the domestic capital market in Rupiah. The bonds issued are also only in the form of revenue bonds, which are bonds backed by revenue from a specific project such as a toll road. Jakarta, Aceh, West Java, and Central Java provinces, as well as Banyuwangi district (in East Java Province), have expressed interest in issuing municipal bonds and/or Sukuk. However, due to bureaucratic hurdles that the bonds issuance plans should be approved by the legislative, up to now, no regions have issued municipal bonds. Nevertheless, the new job creation law (Law No. 11 of 2020) removes the requirement for regional administrations to seek legislative approval before issuing a municipal bond. Since the jobs law provided a “breakthrough” for bureaucratic issues related to municipal bonds issuance, there are numerous opportunities for local governments to issue municipal bonds anytime soon.

5.5. Better Fiscal Governance and Coordination

Well-functioning fiscal governance can contribute to mitigating fiscal risks by strengthening efficiency, accountability, and transparency, as well as maintaining fiscal space (

Kim et al. 2020). If the local government lacks good fiscal governance, it will lead to inefficient spending, increase fiscal deficit, and, in the worst scenario, it may hinder economic development. Furthermore, the APBD should be aligned with the regional medium-term development plan (RPJMD). The integration will improve fiscal responsibility and spending efficiency. The central government can coordinate with local governments to plan for future macroeconomic and fiscal constraints, as well as budget ceilings. If necessary, the central government can provide technical capacity building to the local government to design and formulate the annual APBD comprehensively following the medium-term plan and monitor the projects taken under the programme will be implemented in good quality.

5.6. Increasing Capital Expenditure to Induce Economic Growth

Another potential solution for having strong fiscal resiliency is to increase capital expenditures in the short term after the COVID-19 subsides to accelerate local economic recovery and to induce long-term economic growth. Indonesia’s economy is plagued by a range of “infrastructure gaps”, where many regions lack physical infrastructure or have infrastructure that falls short of quality standards, owing largely to under-investment. For example, many hospitals and public health facilities in remote provinces lack 24-h access to clean water and electricity. Along with rapid industrialization and urbanization, infrastructure needs have soared and both central and local Indonesian governments have struggled to build infrastructure at the required pace. Amid pandemic, the local governments have been overwhelmed as they should reallocate capital expenditure to handling the outbreak and postpone the infrastructure development. In the aftermath of the COVID-19 pandemic, infrastructure development contributes to recovery by creating jobs, opening new markets, and increasing efficiencies. It is also critical to generate new infrastructure funding and attract private sector participation through blended financing, public–private partnership (PPP), and corporate social responsibility (CSR).

5.7. Increasing Soft Infrastructure to Have Higher Resiliency and as a Preparation for Facing Another Potential Crisis

The COVID-19 pandemic may lead to a learning crisis and negatively affect Indonesia now and in the future. School closures may exacerbate existing disparities in access to education, directly affecting poor and vulnerable students, especially in remote areas, to achieving knowledge and skills due to limited internet access (

Halimatussadiah et al. 2020). To promote local economic growth, local government needs to increase their productive spending on soft infrastructure such as education and ICT. Local government may also unleash their local own-source revenue to fund scholarships for their society especially regional medical personnel to improve both the quality of human development and the level of public health. However, these are difficult measures based on political and financial standpoints in part because of legal restrictions such as tax and expenditure limitations, mandatory spending dictated by state governments, and balanced budget requirements (

Chapman 2009).

6. Conclusions

The COVID-19 crisis has put immense pressure on local government budgets across provinces, hence jeopardizing local budget resilience. The responses of the local government in managing their budget varied across provinces following the distinct number of COVID-19 cases, diverse fiscal capacity, different capability to reach budget efficiency, and varied opportunities to generate alternative sources of income. This paper found that most provinces in Indonesia were affected by the COVID-19 pandemic with the average of both government revenue and expenditure decreasing by 8.2% and 6.5%, respectively, in 2020.

Despite a higher number of fiscal capacity index, several provinces particularly in Java and Bali recorded a decrease in fiscal capacity due to sluggish economic activity, hence they experienced a shortfall in tax revenue, while at the same time needing to implement countercyclical mitigative fiscal policy during these difficult times. On the other hand, several other provinces, which are mainly contributed to by primary sectors, enjoyed economic growth during the pandemic. Unfortunately, with the small proportion of local own-source revenue, higher dependence on intergovernmental transfer and external grant financing, as well as higher needs of expenditure to cushion the impact of the pandemic, the growth may not be translated into a broader fiscal space in the local budget. Notwithstanding, this condition will in reverse change once the economy starts to recover, for provinces with low economic diversification to generate higher local-generated income, will, in turn, suffer worse to accelerate the economic recovery when the COVID-19 pandemic ends.

In the end, several recommendations for local governments to rebuild stronger fiscal resiliency are provided: (1) prepare emergency spending for crisis, climate change, and disaster resilience programs, (2) broaden sources of local-owned revenue, (3) benefit from concessional loans from government-related institutions, (4) develop municipal bonds, (5) improve fiscal governance and strengthen coordination among different levels of government, (6) increase capital expenditure, and (7) increase soft infrastructure to improve resiliency and as a preparation for another potential crisis.

Since the COVID-19 pandemic is not yet over at the time of this research, and unlike the previous crises that impacted globally, this study provides insights for international readers and scholars through the implications and responses of local government at the subnational level in a decentralized economy in managing a local budget during the COVID-19 pandemic, and proposes several strategies for achieving fiscal resilience in the aftermath of the crisis. However, future studies are needed to provide more rigorous empirical and technical methods. As the fiscal condition in Indonesia is complex, with many administrative levels ranging from province, district, city, to village, this study may lack the necessary capacity to execute the local budget conditions in greater depth to cover all administrative levels, as well as quantitative aspects such as the impact of local governments’ inability to manage their fiscal policies during the pandemic on macroeconomic variables, particularly growth. Furthermore, when analysing the first period of the pandemic, we encountered several data constraints and anomalies. As a result, future research will undoubtedly be needed to conduct an analysis of the impact of the pandemic on the local budget over a longer time span, particularly from 2020 to 2022, and to draw important lessons from different countries on how they manage the local budget in times of COVID-19. Despite the numerous harms and challenges posed by this global pandemic, this study has provided a much-needed impetus for scholars and practitioners to reconsider the urgency to build resilient and sustainable fiscal policies not only at the national but also at the subnational levels.

,

, {kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}