Abstract

Digitalization has intensified globalization and economic interactivity between countries both developed and developing, increasing the complexity and lack of transparency in economic activities. The increase in digital transactions poses a remarkable challenge for tax authorities yet the digital economy is slowly replacing traditional commercialization and transactions. Conventional international tax legislation has not kept abreast with the growth and complexity of the digital economy and its accompanying challenges with respect to taxation. In view of the infant nature of digital tax legislation in African countries as well as the auspicious possibility of increasing tax revenue to fund public expenditure together with the probability of contradictory outcomes of digital tax policy, through a critical literature review this paper assesses digital taxation through direct digital service taxes (DSTs) in Africa. The findings were mixed. While the possibility of tax revenue maximization and improved economic growth were persuasive, the arguments pointing to negative externalities emanating from poor digital service tax policy design were equally pragmatic.

1. Introduction

The digital economy is growing tremendously globally, and the African continent is no exception, with digital multinational enterprises (MNEs) such as Amazon, Facebook, and Google having significant presence in the African digital space. United Nations Conference for Trade and Development (UNCTAD 2018) estimates Facebook to have more than 200 million users in Africa and approximately 21 million people in the African continent to regularly engage in online purchasing. Bunn et al. (2020) and UNCTAD (2019) allude to a significant growth in the use of smartphones in Sub-Saharan Africa from 10% to 30% between 2000 and 2019. In Kenya Philip et al. (2021) estimated the internet penetration to have reached 89.5% of the population in 2019. Despite this exponential growth in digital transactions and usage of digital services, taxing them remains a formidable task for African governments and their tax authorities. The expansion of the digital economy is linked to the Fourth Industrial Revolution (4IR) (Ojo 2022). The growth was further intensified by the COVID-19 pandemic that changed the way people interacted and how businesses operated, moving most processes to digitalization.

The COVID-19 pandemic led to disruptions in economies globally. The pandemic heavily affected economic sectors such as manufacturing, tourism, and mining among others, resulting in financial losses, job losses, and reductions in economic activity. These COVID-19-induced challenges translated to reduced taxation revenues for economies, compelling governments to look for alternative sources of revenue to finance public expenditure (Kelbesa 2020; Megersa 2020). In the African continent, the situation was further compounded by a high dependence on commodity sales and prices. The commodity prices are a function of supply and demand, which was heavily affected during the COVID-19-driven lockdowns.

The digital services sector gained momentum during the COVID-19 pandemic and seemed to be operating relatively flawlessly. For example, the volume and magnitude of mobile money transactions in Africa increased significantly during the COVID-19 pandemic intensity period. Clifford (2020) tables that in 2020, mobile money accounts widened by 12% to 562 million, and monthly functioning accounts increased to 161 million, signaling an 18% rise in SSA. The total volume of transactions rose by 15% to approximately 27 billion, and the value of mobile money transactions grew by 23% to USD 495 billion in the region. This was affirmed by Shapshack (2021) who submits that mobile money transactions in Africa were approximately USD 500 billion in value in 2020.

Many e-commerce businesses survived the COVID-19 mitigation response measures and performed well, reporting increases in demand, financial performance, and profitability. The increased economic activities led to new entrants into the market as well as expanded operations for already existing companies, thus stimulating employment creation, as the demand for goods and/or services heightened (Kelbesa 2020; Mekgoe and Hassam 2020). Contemporary tax debates and discussions on possible tax reforms have paid fundamental focus to the effect of the digitalization of the economy on domestic revenue generation. Political discussions have also centered on the need to consider the taxation of both traditional business operations and virtual operations. The digital economy appears to be an ideal source of untapped revenue for African nations. Therefore, the ideal avenue is to set up digital tax legislation to follow the seemingly lucrative incomes into the digital economy. The topic of digital services taxes has generated a lot of debate. Disputations surround the justification and the possible effects of their implementation (Munoz et al. 2022).

The Organization of Economic Cooperation and Development (OECD) has been working on guidelines towards the creation of harmonized digital taxes (OECD 2019, 2020, 2021) and the African Tax Administration Forum (ATAF) has been working towards issuing guidelines and offering guidance to African countries in designing their digital tax structure and frameworks (ATAF 2020). Considering these have been taking time before being released, some countries including African countries enacted their own digital taxes to be collected tax revenue while waiting for the finalization of the international and continental guidelines. New tax policies have also emerged, and these include digital services taxes and equalization levies to complement the traditional taxes and regulations such as transfer pricing legislation aimed at taxing digital transactions (Bunn et al. 2020). Clifford (2020) and Lees and Akol (2021) point out to increase in mobile money taxes in Africa. In some cases, political expediency might have overtaken consistent tax policy construction that adheres to the canons of taxation (Becker 2021; Bunn et al. 2020).

Notwithstanding the fact that various African Nations (South Africa, Zimbabwe, Uganda, Kenya, and Nigeria among others) have included digital transactions in their taxation scope through indirect taxes such as Value Added Tax (VAT) (Simbarashe 2020), direct digital services taxation or tax provisions remain scarcely implemented (Becker 2021). Currently, direct digital tax legislation is found in four African countries (Zimbabwe, Nigeria, Tunisia, and Kenya). These taxes are in their nascent stages of implementation as effective implementation dates range between the years 2019 and 2021. This area is therefore a novel area that is currently understudied but gaining recognition in academic and policy research in domestic revenue mobilization in the African content. Megersa (2020) submits that “literature on DST (particularly academic research) is very limited. The evidence base around the economic impacts (on consumers, businesses, and government revenue) is particularly scarce”. The researcher further points out that the evidence is even scantier for developing countries.

In view of the urgent need for more sources of domestic revenue generation, heightened by the COVID-19 pandemic, African revenue authorities need to focus on tapping tax revenues from the digital economy. This paper explores digital taxation through direct DSTs in African countries. It gives a general review of the current taxation frameworks targeting direct taxation of digital transactions. It identifies possible opportunities presented by digital taxation in the African context. The paper also outlines the challenges experienced in the implementation, administration, and enforcement of digital tax legislation. It also discusses implications and possible avenues to tap more tax revenue from the digital economy. Through a comprehensive literature review, the paper sought to make theoretical and practical contributions to the body of knowledge on digital taxation and policy efforts towards direct taxation of digital services or e-ecommerce activities. Firstly, as earlier outlined, digital taxation is still in its early stages of implementation in African countries, this article contributes to the ongoing debate on the possibility of increased domestic revenue mobilization through the enactment of direct digital tax legislation. The paper also explores the possible nature and structure of the legislation as well as the possible challenges to be surmounted together with the opportunities to be exploited. Secondly, unpacking the opportunities, challenges, and implications from the experiences of the African countries that have implemented direct digital taxes makes a practical contribution to policy construction as both policymakers, tax authorities, and governments can draw lessons from these experiences and address the shortcomings in improving current and future policies on DSTs.

Through literature review, the paper addresses the following questions:

- (a)

- What is the structure of direct DSTs taxes and their implementation in the African continent?

- (b)

- What are the opportunities and challenges of implementing direct DSTs in African countries?

- (c)

- What are the implications and lessons learned on the implementation of direct DSTs in Africa?

While the paper is a review article and review articles are often criticized for their lack of contribution or being a replication of previous studies (Mpofu 2021b; Xiao and Watson 2019), this paper also makes an additional contribution to the DSTs discussion by employing diverse source. Due to the infant nature of the subject area, the researchers widened the diversity of relevant literature by including working papers, conference papers and policy briefs. These were from development institutions such as ATAF, OECD, International Centre Tax and Development (ICTD), Institute Development Studies (IDS), Africa Portal and comments from accounting firms Deloitte, Price Waterhouse Coopers and Ernest and Young. The diversity of the literature and the fact that it encompassed views from various and relevant stakeholders that are knowledgeable of the DSTs was a key strength of this review article. While journal articles brought academic and theoretical cogency, literature from development bodies and accounting brought the practical side of DSTs implementation in Africa. Therefore, strengthening the ability of the article to contribute to both theory and practice.

This study carried out an evaluative synopsis and synthesis of arguments from previous recent research on DSTs. Digital service taxes are a new phenomenon that is still being debated among researchers, policymakers, tax bodies, and developmental bodies. In addition to informing readers on the current state of knowledge in this novel area, the paper puts into perspective the controversy surrounding the implementation of DSTs. This could possibly galvanize and provoke new conceptions that could be addressed by further research. For example, understanding the implications of DTSs could push policymakers to do an in-depth assessment of the possible costs and benefits of DSTs administration. This could accordingly ensure a reduction in negative effects on revenue generation, market structure, and on the digital divide as well as financial inclusion of vulnerable groups.

2. Literature Review

2.1. Digital Taxation Defined

There is no concise definition for the digital economy as the description is used to refer to various economic activities. Becker (2021) asserts that the digital economy includes platform-supported services such as Uber, online platforms such as Amazon, Facebook, and Google, trading electronic services such as e-books, video games, and films as well as online delivery of software and mobile-enabled technologies and applications. The fundamental feature of digitalization is that it enables companies to do business in places where they have no physical presence (Ismail 2020; Ndulu et al. 2021). Existing international tax laws were such that MNEs paid tax where production took place as opposed to the country where consumers were based. More countries are arguing for digital taxation through corporate tax to target users of digital services in the countries they are located (Asen and Bunn 2021). Countries worldwide are lobbying for efficiency in taxing digital transactions as a means of mobilizing revenue, especially in the face of the COVID-19-induced problems.

Defining digital taxes has equally been confusing and controversial. Researchers offer varying definitions for taxes and their nature and the structure varies with national contexts. What is referred to as digital taxes differs from one nation to the other. Kelbesa (2020) defines DSTs as direct taxes that are applied to non-residents with no physical presence in the taxing country but only have customers and users. Megersa (2020) and Bunn et al. (2020) contend that the nature and scope of digital taxes differ from one country to another. Countries have taken varying approaches to defining businesses that would be legally obligated to pay corporate taxes in their countries in relation to the customers accessing digital services within the countries’ borders. For example, India, Kenya, Nigeria, and Indonesia as examples (Kelbesa 2020). India proposed to tax digital businesses based on the significant economic presence test, though concise definitions and thresholds remain unclear. Indonesia proposed to levy tax on digital transactions based on the domestic market activity through digital means. The tax policy targets gross revenues from digital transactions. Kenya’s digital tax is levied on income accruing from digital marketplaces and similar to Indonesian tax; it targets the gross revenue from digital businesses. Nigeria on the other hand taxes online business profits to the extent that the profit is significantly linked to the economic presence in Nigeria. Bunn et al. (2020) posit, “Digital taxes include policies that specifically target businesses which provide products or services through digital means using a special tax rate or tax base”. These digital taxes include VAT on digital services, corporate tax on digital transactions, withholding taxes, and income taxes on digital transactions (de Lima Carvalho 2020; Kelbesa 2020; Kofler and Sinnig 2019; Low 2020). Others have split these into direct (digital services tax such as income taxes) and indirect digital taxes (consumption taxes such as VAT). Bunn et al. (2020) assert that “digital services taxes are gross revenue taxes with a tax base that includes revenues derived from a specific set of digital goods or services or based on the number of digital users within a country”. Most of the regulations have unclear and underdeveloped parts that would perhaps be cleared and ironed out for the controversies and ambiguities.

2.2. Digital Taxation and the International Context

Digital tax policies have targeted social media MNEs such as Facebook, Google, and Amazon, web-based services as well as other e-commerce marketplaces to widen the tax base by extending existing legislation to new players or directing new tax legislation specifically to new businesses and platforms that were previously not subjected to tax. For example, VAT policies have been reformed in countries such as Zimbabwe and South Africa to cater to expansion in products and services traded digitally, even in cases where companies have no physical presence in countries where they are offering a service to users. Corporate tax policies have been reformed to bring digital services into the tax net (Bunn et al. 2020). There is a need for international consensus on digital tax policy structures, implementation, and implications. The lack of international agreement would lead to contradictions and intersections in different countries’ individual tax laws resulting in double or over-taxation.

Owing to the concerns over the adequacy and appropriateness of commonly applied tax legislation in capturing the digital economy into the tax net, there have been concerns from both developed and developing countries on the need to bring digital transactions under the ambit of tax laws. The OECD is working on guidelines to be informed by the outcomes and conclusions of discussions with over 130 countries on how the concerns on the digital economy and taxation could be addressed (OECD 2020). Becker (2021) puts the countries at 141 countries in 2021. The organization is working towards consensus-driven solutions to the challenges of taxing the digital economy (Mekgoe and Hassam 2020; OECD 2019; Megersa 2020), by considering new business models and ways of distributing taxing rights in a way that also benefits consumer countries of digital services (Deloitte 2020). The OECD Action 1 on BEPS sought to address the taxation of digital transactions. This was in recognition of the fact that the digital economy was likely to bring more risks to BEPS and even fundamentally increase the prevailing BEPS risks. The BEPS Action 1 brought about the need for improved legislation on transfer pricing activities, permanent establishments, and controlled foreign entities’ operations to minimize the likelihood of new risks emerging or increasing in those general risks already in existence. The OECD two-pillar framework approach speaks to BEPS in relation to the digital economy. The OECD/G20 Inclusive Framework on BEPS addresses the key challenges of digitalization of the economy and distribution of taxing rights (Becker 2021; OECD 2020).

The OECD two-pillar framework aim at simplifying digital taxation and increasing tax compliance, reducing or preventing double taxation that could emerge due to unharmonized respective countries’ digital tax legislation as well as minimizing disputes. By countries agreeing on the legislation and committing to its implementation as well as having a consensus on the formulation of a transparent and acceptable dispute resolution mechanism, this would bring standardization to digital tax administration and enforcement. Pillar one of the Inclusive Framework addresses the fairer distribution of profits. The pillar targets MNEs operating in sectors other than the extractive and financial services sectors with a global turnover in excess of 20 billion and profit before tax exceeding 10%. The pillar further prescribes that a residual profit of 20 to 30% of the profit above 10% of revenue be distributed to market jurisdictions where the services or goods were consumed. Pillar 2 speaks to the introduction of a global minimum corporate tax of about 15% to protect the tax bases of individual countries and reduce harmful international tax competition. Despite the provisions of the two-pillar framework, there are still several challenges that remain unaddressed. For example, the sale of tangible goods through digital platforms (lack of digital presence in the country the goods are delivered), variations in thresholds for digital taxes, and the complexity that comes along with digital taxes, thus compromising the simplicity principle that the OECD ought to uphold (Megersa 2020). According to Latif (2019, 2020) due to the expansion of the digital economy, MNEs have generated profits in ways that have challenged the propensity of governments to mobilize tax revenues from this economy by relying on conventional international tax rules. The inadequacy of traditional international tax laws signaled the urgency of having novel and relevant digital economy-focused tax rules (Turina 2018, 2020).

Frustrated by the delay and the lack of consensus on the implementation of the multilateral OECD-driven DSTs framework, both developed and developing countries have introduced unilateral or country-specific DSTs. These taxes would possibly have different opportunities, challenges, and effects in developed and developing country contexts. The variations could be linked to the differences in political and economic setting, political and economic power imbalances, tax administration capacity, technology advancements as well as financial resources availability. The tax rates generally do not vary significantly for developed and developing countries as shown in Table 1, Table 2 and Table 3. DSTs are based on revenue similar to a turnover tax (TOT) used by tax administrators for the informal sector. Table 1 gives a snapshot of DSTs in developed countries.

Table 1.

Digital Services Taxes in Selected Developed Countries.

Table 2.

Digital taxes in selected non-African developing counties.

Table 3.

Direct DSTs implemented in African countries.

The structure of direct DSTs in developing and developing countries shares similarities in terms of the tax base (revenue) and high thresholds as well as that big technology giants are the targets. In addition, tax revenue mobilization and reduction of tax avoidance seem to be the driving motives for the implementation of DSTs globally, these taxes also suffer from similar criticism in both developed and developing countries. For example, in Australia, the taxes are advocated for based on revenue generation and the fact that the reliance on mobile and intangible assets by digital giants weakens the competitiveness of domestic companies, traditional media firms, and small digital firms. Even researchers focusing on developed countries link DSTs to the reclaiming of value created through market jurisdictions. The issue of value creation is problematic, especially how to measure it since there is no cash exchange involved. The taxes are also criticized for resulting in increases in input costs for businesses, weakening international competitiveness, and the possibility of creating trade wars (Hathorne and Breunig 2020; Lowry 2019). DSTs are also disapproved of in developed countries because of being discriminatory, unreasonable, burdensome, and targeted at constricting the United States’ e-commerce (Kennedy 2019). Noonan and Plekhanova (2020) criticize them for violating international trade agreements and leading to double taxation challenges in developed countries such as Spain and Britain. While developed and developing countries might share similar motives and criticisms, the opportunities and challenges of DSTs will differ in developed countries and African country contexts. The tax environment of developing and developed countries differ due to political and economic power differences, financial and technical resource capacities as well as other economic and social vulnerabilities affecting developing countries. African countries have a high informal sector, high levels of financial exclusion and digital inclusion as well as fragile technical and tax administration capacities. For example, challenges of DSTs relating to value creation as well as the increase in administrative and compliance costs might affect both developed and developing countries, the level, and impact would differ in line with capabilities capacities, and competencies

2.3. Digital Taxation in Developing Countries

Despite the possible challenges of digital taxes and their infant nature, a few developing countries (both African and non-African) have put in place digital taxes while waiting for the OECD digital tax proposal to be finalized. Table 2 gives a summary of direct DSTs in the selected non-African developing countries.

2.4. Digital Taxation in African Countries

There has been a consequential surge in internet usage in Africa, especially on digital services and social media platforms as well as cloud computing. As proclaimed by Becker (2021), with the increased growth in information, communication, and technology infrastructure and internet usage, the internet-linked population rose from 4.5 million to 526 million between 2000 and 2019 (signifying 39.3% connectivity and 11.5% of global internet-connected population). The suggested approach was released by the ATAF in September 2020 (African Tax Administration Forum (ATAF 2020)). This infers considerable growth in the digital economy and untapped tax base.

Several Sub-Saharan African countries are members of the OECD inclusive framework. These countries include South Africa, Angola, Kenya, Benin, Namibia, Mauritius, Nigeria, Togo, Sierra Leone, and Senegal. The ATAF has raised concerns on the relevance and contextual applicability of the OECD two-pillar framework to African countries. The Forum lacks or has minimal advantages for the application of the framework to the African continent as well as the likelihood of the ineffectiveness of the provisions in Africa. The organization further raises concerns on the complexity of the proposals, pointing out that the framework could result in inconsequential profits being re-allocated to smaller market jurisdictions similar to most of the African Nations (Becker 2021; Bunn et al. 2020). The ATAF proposes that the re-distribution of profits must be computed based on a proportion of the MNEs’ overall profit as opposed to its residual profit. This would arguably bring about simplicity and fairness in the re-allocation of profits. In cases where residual profit is to be retained the ATAF advocates for at least 35% of the residual profit to be shared with the market jurisdiction. The administration forum raised concern on the 15% proposed tax rate, suggesting that at least a 20% tax rate would be more beneficial to the African continent. The tax rate would productively protect African economies’ tax bases and reduce illicit financial flows from Africa (Becker 2021; OECD 2021).

The ATAF released a policy document named “Domestic Resource Mobilisation-Digital Services Taxation in Africa in 2020 as the forum continued working towards the development of a ‘Suggested Approach to Drafting Digital Services Tax Legislation’. This was done to guide African countries on the structure and framework for implementing DSTs that consider the unique challenges of the African continent (Becker 2021; Deloitte 2020; ATAF 2020).

The ATAF suggests a direct DST rate from 1% to 3% on the gross annual revenue from digital transactions accruing in market jurisdictions. (Becker 2020 The ATAF encourages countries to be proactive and not to solely wait for the OECD-driven solutions to the implementation of digital taxation systems, as these might take longer to be agreed on and disseminated for use. The delays might be costly, as significant revenues may remain untapped from the digital economy, therefore negatively affecting already economically vulnerable cash-strapped African governments (Becker 2021; Deloitte 2020). Despite the encouragement for proactiveness, the ATAF in its suggested approach points out the need for members to evaluate carefully whether they will be committed to repealing their national digital taxation systems in line with the requirements of the OECD international framework the consensus-driven digital taxation solutions. The framework requires that member countries who would have implemented their own individual country digital taxes to repeal them in favor of the OECD-directed ones (ATAF 2020).

According to Levin (2022) “one of the most efficient ways of promoting long-term inclusive development is to ensure domestic financing through a stable, broad-based and fair tax system”. African countries face challenges of weak domestic revenue mobilization due to aggressive tax planning, tax avoidance, and evasion by MNEs which are aided by the weaknesses in transfer pricing legislation (Oguttu 2016, 2017, 2020).

As pointed out earlier in the introduction, several African countries broadened the purview of indirect taxes such as VAT to encompass e-commerce activities, with only a minority enacting tax laws toward direct taxation of digital services offered to non-resident customers or consumers, who are not physically domiciled in the taxing country (Simbarashe 2020; Kabwe and van Zyl 2021). While in 2019 Egypt made indications towards the consideration of implementing a digital tax on social media and other advertising platforms, the actual possible implementation dates, and the nature as well as the structure of envisioned digital tax laws to be implemented remain hazy. South Africa has focused on the taxation of digital transactions indirectly through VAT; efforts to implement direct DSTs remain unclear. Perhaps the reduction in revenue and the overstretched public budgets necessitated by the COVID-19 pandemic might stimulate debates on the possibility of implementing direct digital taxes. Despite the enactment of digital taxation legislation, African countries must strike a balance between mobilizing tax revenue from digital transactions and the need to attract foreign direct investment to stimulate economic growth. Care must be taken to ensure that countries remain competitive in the global market environment and to guard against double taxation or double non-taxation of income received or accruing from the sale of digital goods and services. The individual countries’ digital taxation laws must take note of the nation’s unique economic and political environments, policies, and envisaged risks. It is also key for the countries to guard against promulgating novel tax policies that are distortive or go against the principles of a good tax system.

Table 3 gives a synopsis of the implementation of direct DSTs by a few African countries. While the above countries have implemented direct DSTs, most of the other African countries are hoping to do so in the future, with the notable ones being South Africa and Egypt. Though the possible implementation dates remain unknown the countries have had deliberation pointing towards the consideration to have direct digital taxes implemented (Becker 2021; Simbarashe 2020).

2.5. Opportunities, Challenges, and Implications Administering Direct DSTs

There has been intense debate among researchers on the opportunities, challenges, and implications of direct DSTs taxes in Africa (Munoz et al. 2022; Rukundo 2017). In relation to opportunities, most researchers allude to the revenue generation possibilities. Various researchers have alluded to the increase in tax revenue mobilization emanating from the implementation of digital taxes (Megersa 2020; Bunn et al. 2020; Deloitte 2020). Even though there is evidence to back the argument in developed countries (such as Australia) and the European Union, there is little evidence in the African context and much of it has been mixed, contradictory, and contested. In relation to VAT on digital sales, revenue was estimated to have increased by US$ 5 billion and in Australia, US$242 million was approximated to have been mobilized through taxation of digital services (Bunn et al. 2020; Megersa 2020).

Several researchers proffer various challenges facing African countries in implementing digital taxes (Ahmed and Gillwald 2020; Ndajiwo 2020; Philip et al. 2021; Rukundo 2020). While Rukundo (2020) emphasizes administrative challenges, Ahmed and Gillwald (2020) point to the design of digital tax systems that can lead to the taxes being regressive and Philip et al. (2021) allude to the weak or absence of enforcement frameworks, lack of awareness and tax avoidance and evasion strategies. Akpen (2020) states that the “ability to be everywhere and nowhere is the strength of the digital economy”, but that is also what makes its taxation problematic. Santoro et al. (2022) posit that digital tax administration is affected by difficulties in accessing quality data, political barriers, and the lack of digitization tax administration as well as poor technology in Africa. This is affirmed by Eliffe (2021) who refers to six challenges of mobilizing tax revenues from the digital economy. These are (1) the invisibility of digital transactions and the inability to tax them (2) the challenge of data availability in relation to the contributions made by digital users, the justifiability and measurement of value creation (3) the mobility of and dependence on intellectual property or assets (4) how to characterize digital incomes and transactions (5) the inadequacy of transfer pricing regulations to regulate the activities of MNES or even curb their tax avoidance and evasion challenges (6) the weaknesses in the residence based tax systems and the general trade competition by nations. Magwape (2022) alludes to the inadequacy of technical and financial resources characterizing African countries (under-resourced), the complexity of MNE transactions and digital transactions in general, and the weaknesses and slowness in adapting to the evolving international tax discourse. Nicholas et al. (2017) contend that the implementation of DSTs would be difficult to implement as they lack the necessary political support and cooperation from institutions such as financial institutions. In Tanzania, Liganya (2020) alludes to the lack of clear legislation towards taxing e-commerce activities.

Irimia et al. (2021) table the shortcomings of the DSTs structure in support of the criticism of the tax policy as well as its lack of acceptance by some stakeholders. These weaknesses include (1) the fact that the taxes are calculated on revenue leads effectively to rates that are high as no deductions are allowed. The tax does not take into consideration either profits or taxable income. (2) Direct DSTs inordinately affect businesses with high volume but low margin transactions and products. The total tax revenue might be seemingly high, yet the company makes very minimal profits. This could lead to vulnerability of companies and possible closure due to an overly heavy tax burden (3) Direct DSTs lead to companies having tax obligations even when there are incurring losses or generating low profits (4) The taxes could lead to race bottom. (5) The absence of deductions discourages investments that could produce high returns in the long-term (deductions such as interests (cost of capital) as well as capital allowances or allowances on capital expenditure and research and development often encourage investments. (6) The taxes could administratively be difficult in relation to long-term contacts. (7) DSTs could drive MNEs and their governments to engage in retaliatory behavior or trade wars. (8) The taxes could possibly lead to double taxation.

The implications are better articulated by Kofler (2021, p. 51) who asserts:

“While those turnovers based on specific taxes are heavily criticized as ‘bad policy’ from an economic perspective (regarding e.g., double burdens, impact on investment, innovation, welfare and growth, distortion of consumer choices and business decisions, benefits the older over digital technology, etc.), recent scholarship has found some potential sympathy for DSTs as a potentially appropriate taxation of location-specific rents”.

Etim et al. (2020) submit that the taxation of the digital economy will not only negatively affect the expansion of the digital economy and employment creation in African countries. The researchers argue that youths have been exploiting the digital space for employment in countries such as Nigeria, Kenya, Nigeria, and Zimbabwe with high unemployment. Taxation of these digital services, marketplaces, and e-commerce services might affect employment creation and perpetuate inequality and frustrate poverty reduction efforts. In Gabon, Katz (2015) raises the affordability implications of taxing the digital economy and in Nigeria, Isiandinso and Omoju (2019) raise concerns on employment generation, sustainable economic development, and welfare loss. Beebeejaun (2020), Kirsten (2019) and Ngeno (2020) also raise the unfavorable effect of taxing the digital economy in African countries.

3. Review Methodology

This paper focuses on digital taxation options available to African countries to broaden their tax bases in view of the expanding digital economy. The paper focuses on possible opportunities, constraints, and consequences of implementing direct DSTs. This paper employs a qualitative research methodology using a critical review approach. De Vos and El-Geneidy (2022) state that reviews are important for three key reasons. Firstly, they enable researchers to pinpoint novel connections in the body of knowledge and construct theoretical frameworks and conceptual models to inform research. Secondly, reviews help researchers highlight new possible avenues for a future researcher by spotlighting possible research gaps. The gaps could with respect to methodological, policy, and findings. Thirdly, review articles can help researchers to generate policy suggestions and to provide guidance for policy and practice. This review article concentrated on contributing to the last two, that is accenting on research gaps and informing policy recommendations.

The researcher conducted a document review to analyze and interpret reviewed literature on direct DSTs in Africa. The paper builds on previous studies on digital taxation in developing countries and African nations that have adopted direct DSTs in their tax systems. Some of the publications reviewed were drawn from development research bodies such as the International Centre of Tax and Development (ICTD) and the Institute of Development Studies. The extant literature reviewed is complemented by drawing on the work and documentation on digital taxation from organizations such as the African Tax Administration Forum (ATAF) and the Organization of Economic Co-operation and Development as well as the European Commission. Recent digital tax legislation (Income Tax Acts, Finance Acts, and VAT Acts) and policy initiatives implemented by African countries such as Tunisia, Zimbabwe, Nigeria, and Kenya as well as by other non-African developing countries (Chile, Indonesia, and Argentina) were also assessed. Drawing from these various efforts (multilateral and unilateral), legislative prescriptions and findings from the existing theoretical body of knowledge, this paper addresses the research questions outlined in Section 1 to contribute to both the theoretical body of knowledge on digital taxation and the practical assessments on tax policy on digital taxation in Africa. Mpofu (2021b) and Snyder (2019) encourage authors of review articles to be comprehensive in articulating their review process to enhance the credibility of findings and to inform readers of their sources of information.

Borrowing from the methodology used by Megersa (2020), to understand more on the implications of the implementation of digital taxes, the researcher also reviewed other different types of literature on digital taxation from reports, policy reviews, and blogs by various development agencies and international organizations such as Bloomberg.

The researcher conducted an in-depth review of related literature on direct DSTs to accentuate consistencies and inconsistencies among researchers to bring to light the research gaps in the implementation of direct DSTs in Africa. The literature was collected from the Scopus database, Google Scholar, and EBSCO databases. Xiao and Watson (2019) recommend the Google Scholar database because of its comprehensiveness and the fact that grey literature such as conference proceedings, theses, and working papers can be accessed enhancing diversity. This was critical for this review because of the embryonic nature of the subject area on DSTs. Wee and Banister (2016) submit that a review article must be extensive and focus on relevant literature, with reviewed artless ranging from 50 to 100. To increase the number of papers reviewed after 40 papers were selected articles from the database searches through screening, the researchers conducted forward and backward snowballing as well as citation mining from the reference lists of the selected papers reviewed. The process resulted in some additional papers from the works of scholars such as Rukundo (2017, 2020), Munoz et al. (2022), and Santoro et al. (2022). The paper reviewed a total of 60 articles. These papers were reviewed up to a point of saturation, this being the point where authors found no new information from further reviewing of more articles. The search terms used included “DSTs in Africa”, “Direct digital services taxes in Africa”, “Opportunities of taxing the digital economy through direct DSTs in Africa”, “Challenges of DSTs”, Challenges of administering direct DSTs in Africa”, Implications of implementing or administering direct DSTs in Africa and “Effects of direct DSTs in Africa”. In relation to the exclusion and inclusion, titles, abstracts, keywords, and introductions were used to screen and assess the initial output from the database searches.

Because DSTs are still in their early stages of implementation globally as shown in Table 1, Table 2 and Table 3, most articles accessed and reviewed were from 2015 to date, with most of them being concentrated between 2019 and 2022.

Literature was reviewed under themes that were deduced during the review of literature informed by the research questions Therefore the discussion of findings coalesced on the opportunities, challenges, and implications of the DST policy in Africa. Braun and Clarke (2019) encourage the qualitative researcher to use thematic analysis for ease of analysis and comprehension of their work by readers

4. Discussions of Findings

The benefits, challenges, and implications of implementing digital taxes in developing counties and especially African countries are scarcely explored in literature because the implementation is in its infancy, with only a few countries that have applied these taxes (Kelbesa 2020). The few African countries that have implemented digital taxes have done so in recent years. The challenges due to the lack of proper evaluation of the application of digital taxes are further compounded by the novel nature of the subject area in academic literature, implying that there is a dearth in literature. According to Rukundo (2020), “For African countries, digitalization of the tax base is itself a challenge”, due to weak technical capacities in revenue authorities”.

The review presented a few possible pros and cons of digital taxation implementation in some developing countries and the few African countries that have implemented the taxes. Some of the challenges are also drawn from the critique of the OECD’s two-pillar framework by ATAF in addressing the needs of the African context. ATAF raised several concerns on the applicability and appropriateness of the OECD digital taxation proposals and guidelines for African countries.

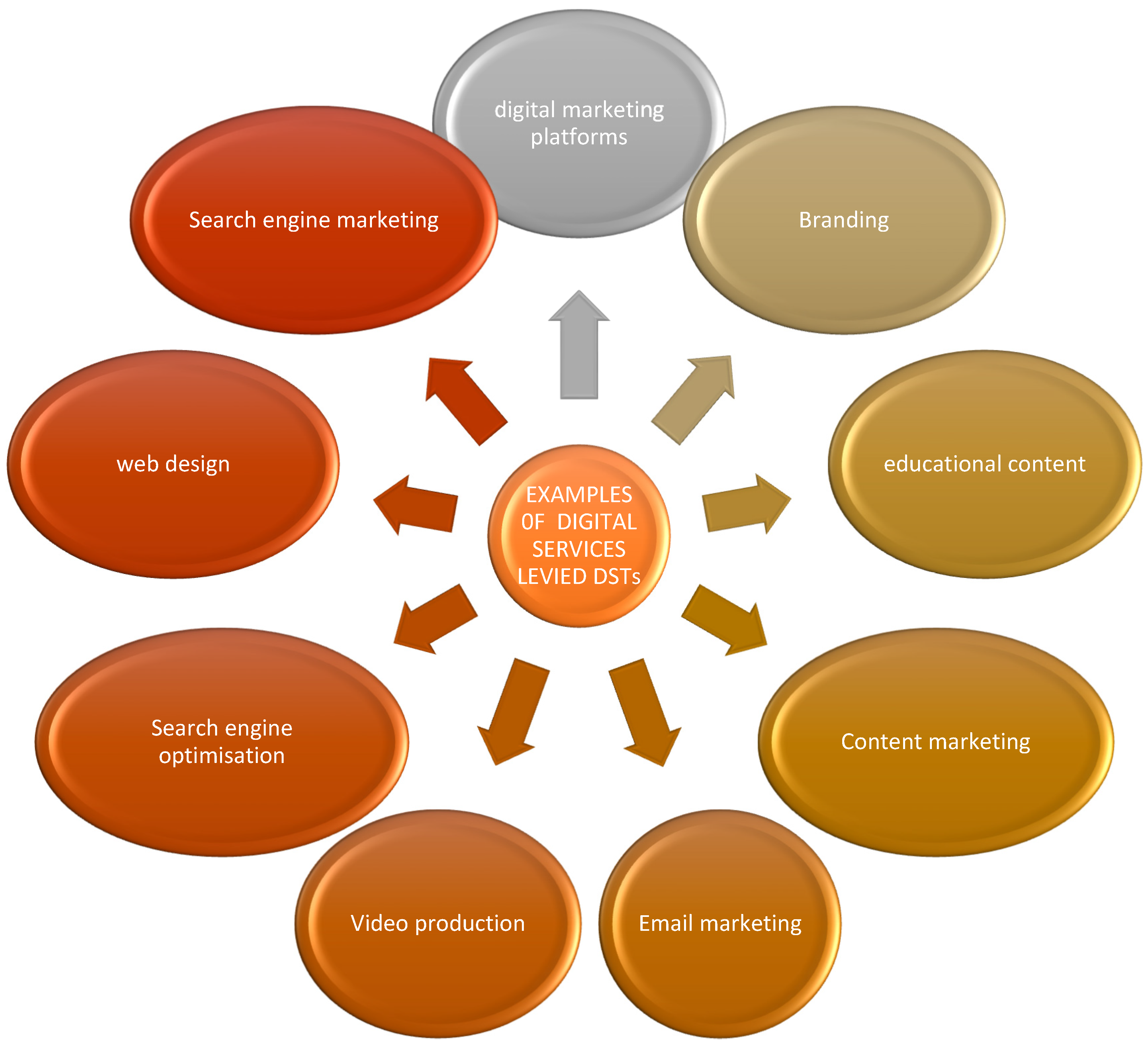

To have a full appreciation of the discussion on the matters relating to the taxation of the digital economy through direct DSTs it is crucial to give a picture of the nature of the services subject to digital services taxes. Understanding these services would show their importance and contribution to economic development and financial inclusion. From the DST policies of the African countries presented above, a collated summary of some of the services levied DSTs is presented below in Figure 1. A better comprehension of the services subject to tax through DSTs will inform a better understanding of the opportunities, challenges, and implications of administering DSTs in African economies.

Figure 1.

Examples of Services Subject to Direct DSTs in African Countries. Source: Author’s Compilation.

The sections that follow summarize the findings of the review. These were discussed under the main subthemes that emerged across the three main themes of opportunities, challenges, and implications of DSTs guiding this review.

4.1. Opportunities from Applying Direct DSTs Taxes in African Countries

African countries are faced with challenges of tapping revenue from the digital economy, yet it has promising outcomes. The key is how to augment the tax bases in these countries without crippling development and the use of technology or hindering the participation of the business community in the growing e-market (Kakungulu-Mayambala and Rukundo 2018; Rukundo 2020). The benefits include an increase in tax revenue.

4.1.1. The Increase in Tax Revenue

In developing countries, researchers have also shown the possibility of enhanced revenue generation. According to Becker (2021), direct digital taxes present an opportunity for African governments to extend revenue mobilization and widen the tax bases. The opportunity is critical, especially for SSA countries with huge and continuously expanding informal economies and narrow tax bases. The informal sector in SSA contributes significantly to GDP in Africa. According to Rogan (2019), the informal sector contributes greatly to employment creation and poverty alleviation in developing countries. In Zimbabwe to be precise Medina and Schneider (2018) estimate the country to have the second largest informal economy in the world contributing 63% of GDP. The reduction in economic activity due to the COVID-19 pandemic has further heightened the challenge of revenue mobilization in SSA especially and the rest of Africa, other developing countries, and developed countries. Digital taxation promises to be a fountain of more tax revenue especially due to the increased digital transformation and the upsurge in the use of the fourth industrial revolution (4IR) tools such as artificial intelligence (IA) in nearly all sectors of the economy and activities such as education, banking trading, and communication. The digital services sector is significantly growing and performing better than other sectors of the economy. According to Gallien et al. (2021, p. 6), “Taxing digital transactions is often a promising way to target tax avoidance by big technology platforms, while recognizing that these have benefited significantly from increasing online transaction in the past years”. If governments could tap tax revenue from this undertaxed sector, revenue mobilization prospects would have a significant boost especially if the envisaged tax revenue estimations materialize.

Despite taxation of digital transactions being seen as a possible option for increased domestic revenue mobilization, other researchers caution on the need for a properly designed digital tax policy, otherwise, the outcomes might be fundamentally pervasive on value creation, internet usage, and even tax revenue generation (Kakungulu-Mayambala and Rukundo 2018; Mpofu 2022; Philip et al. 2021; Rukundo 2020). In concurrence, Ahmed and Gillwald (2020) avow “Poorly designed digital taxes could actually lower domestic tax revenue and impact affordable and meaningful access to the internet and financial inclusion”. In African nations, political agendas and weak capacities affect the development of effective and sound tax legislation and this affects revenue collection efforts. The question is how then African countries design inclusive tax policy and what are the features of that policy. Taxes generally have a twofold effect; they are costly to the business and individuals as well as being an economic tool for revenue mobilization. Government should focus on ensuring equilibrium in these two conflicting roles. Excessive taxation can increase tax revenues in the short run but in the long-term lead to business failure and increased inequality. For corporates increased tax costs lead to a reduction in profits and the failure to fund operational activities, while for individuals it can lead to lower disposable incomes or goods being excessive as companies push the tax burden to consumers at high prices. The results of digital tax policy might be conflicting due to the structure of the tax policy. An opportunity for revenue mobilization if not properly exploited or is overexploited might have negative impacts on economic growth, digital companies’ survival, and digital financial inclusion as well as employment.

Most African countries have high rates of unemployment and rely more on informal activities for subsistence income, funding household expenses as well as to finance education and health. Excessive taxation of the digital economy may thus not only affect sustainable development but also the attainment of the 2030 Sustainable Development Goals (SDGs) such as poverty alleviation (SDG1), Zero hunger (SDG 2), Access to and delivery of quality health services (SDG 3) and access to quality education (SDG 4) among others.

Mpofu and Moloi (2022) encourage African governments to consider the canons of taxation such as economy, fairness, transparency, and simplicity in designing direct DSTs to ensure that digital tax policy does not only accentuate the revenue generation motive at the expense of the other objectives of tax policy. These objectives involve facilitating economic growth, redistribution of resources, and being a governance tool as well as an instrument to reduce. DSTs must adhere to the canons of taxation and strike an equilibrium between domestic revenue mobilization and promotion of international trade as they tend to target large giant tech companies. These companies have not only helped foster economic and financial inclusion but also promote social inclusion through enhancing connectivity through social platforms.

4.1.2. Improved Public Confidence and Trust in the Fairness and Transparency in the Tax System

The taxation of big digital MNEs that have no physical presence in the countries could ameliorate trust in tax administration. The government could be perceived to be fair in its revenue mobilization efforts. Trust, fairness perceptions, and policy acceptance are important variables in tax morale and compliance discussions. For DST policy to gain acceptance it must be seen as fair, enabling fair taxation of both domestic and international companies. The non-taxation of digital international companies, while domestic companies paid the corporate tax, VAT and other levies was unfair and tilted the competition landscape in favor of international tax rules. Traditional international tax laws were based on the physical presence concept, yet digital companies have largely virtual operations. The implementation of DSTs could lead to an increase in public trust could improve tax morale among taxpayers and ultimately enhance tax compliance. This could indirectly translate to increased revenue generation as suggested Sebele-Mpofu (2021) when studying tax morale, tax compliance, and the implicit social contract in Zimbabwe’s informal sector. Generally, people are willing to invest in a government they trust.

4.1.3. Improved Economic Growth and Fulfilment of Government’s Key Objectives

The increase in revenue mobilization implies that government would mobilize funds to fulfill its objectives. The government would have enough funds to invest in infrastructure, education, and health and thus achieve the 2030 SDGs as well as objectives of the Africa Agenda 2063. This would also depend on whether the design of the digital tax policy supports the principles of a good tax system, the capabilities of tax authorities in the country, perceptions of fairness, and tax morale. Otherwise improperly designed tax policy could lead to negative effects on revenue mobilization, sustainable economic growth, and the delivery of the SDGs as highlighted by Mpofu (2022) and Mpofu and Moloi (2022) on mobile money taxes and digital taxes and the principles of taxation respectively

4.1.4. Reduction in Other Taxes

Expansion of the digital economy could earn countries more on VAT cross-border digital transactions all perhaps allowing the government to lower digital taxes and other taxes in the long run (Bunn et al. 2020; Kelbesa 2020). The arguments suggested a possibility of reduction of other tax heads based on the introduction of another tax head are often criticized on the basis that taxes generally have a distortionary effect on the economy and on the spending decision of users. The compensatory effect if ever possible is difficult to ascertain.

4.2. Challenges of Taxing the Digital Economy and Administering DSTs

Several challenges emerged from literature in relation to the administration of DSTs. These challenges were largely connected to the invisible nature of digital services targeted for taxation as outlined in Table 3 and Figure 1, the weak tax administration capacities of African countries, possible welfare loss for consumers, and the embryonic nature of DSTs. Most of the DST policies were introduced between 2019 and 2021 as shown in Table 1, Table 2 and Table 3 (Africa)The subsections that follow articulate and explore some of the challenges in taxing the digital economy using DSTs that became evident from the review process.

4.2.1. Reduction of the Growth of the Digital Sector and Economic Growth in African Countries

The digital economy is seen to be a consequential driver of economic growth and development in Africa (Ahmed et al. 2021; Ahmed and Gillwald 2020). Becker (2021) expostulates that in response to every 10% increase in mobile broadband in internet usage, there is a corresponding increase of around 0.82% to 1.4% in the gross domestic product (GDP) in African countries. Taxation would thus increase the cost of the internet which is already prohibitively high in some African countries. Digital services tax might result in reduced usage of digital services. High costs of internet-connected devices and data limit the use and connectivity of the internet in Africa. Coupled with significant customs duties on digital devices on digital mediums (such as eco-cash in Zimbabwe, and e-wallet in South Africa), digital taxes might have unfavorable effects. Becker (2021) contends, “Poorly designed digital taxes could lower domestic tax revenue and negatively impact affordable and meaningful access to the internet”. This might impede on digital transformation efforts in the various sectors of the economy (Pushkareva 2021; Ndulu et al. 2021), yet the COVID-19 pandemic made it evident that digitalization is key to economic survival and performance during the crisis. Digital financial inclusion might also be negatively affected. To affirm this concern Shipalana (2019), Ojo (2022), and Ozili (2018, 2020) argue that accessible and cheaper digital services are key to financial inclusion. The diminished usage of usage could result in a reduction in the growth of the digital sector and its contribution to economic growth in the African continent, thus compromising the achievement of Sustainable Development Goals such as reduced poverty (SDG 1), addressing gender inequality (SDG 5), ensuring decent work and economic growth (SDG 8) and industry and innovation (SDG 9) among others.

In affirmation of the concerns, Ahmed et al. (2021) argue “There is already considerable evidence that these taxes exacerbate the digital divide and undermine national digital strategies that support inclusive economic development efforts, which will be needed more than ever for post-COVID-19 economic reconstruction”. As highlighted by Bunn et al. (2020) and Megersa (2020), the sector is irrefutably growing significantly and contributing considerably to the GDP of developing economies. Hence, the impact of implementing digital taxes in African countries requires a comprehensive cost-benefit assessment as well as a thorough evaluation of how the implementation will affect consumption taxes such as VAT on digital services, transactions, and equipment.

Contributing to this concern, Becker (2021), asseverates that the proposed digital service taxes and those that have been applied in other African countries are based on the gross turnover. This signals that small companies, those on the launch stage (start-ups), and small and medium enterprises might be negatively affected. In view of this possible unfavorable effect, the ATAF (2020) recommends the use of minimum thresholds or tax bases to guarantee that the targeted businesses for digital taxes are the more profitable digital companies. However, the recommendation is persuasive, but it conflicts with the ability to pay principle, which presupposes that taxpayers must contribute to taxation based on their income earning capacity. The principle of fairness (tax justice, impartiality, and equality in treatment) will be compromised as other businesses are made to contribute to digital taxes while others using the same services are not. The discrimination in terms of size would lead to a perceived unfairness that compromises tax morale, reduces tax morale, and consequently tax compliance and revenue mobilization. The impact of discrimination related to the size of the business was alluded to have a negative effect on tax compliance Sebele-Mpofu (2021) and Mpofu (2021a) while studying presumptive tax compliance in the informal enterprise in Zimbabwe. This might stifle the growth of small and medium firms, as they would want to remain small to avoid reaching the minimum threshold to avoid taxes firms (Mpofu 2021a). Therefore, in as much as the African government and their revenue authorities are looking to the digital economy as a lucrative source of uncollected tax revenue, there is a crucial need for policymakers to strike an equilibrium between revenue mobilization objectives and not curtailing the growth of the digital economy and its contribution to overall economic growth, infrastructural development, and improved communication.

4.2.2. Administrative Challenges and the Infant Nature of DST Legislation

Developing countries’ revenue authorities and particularly African governments are faced with administrative challenges in their tax revenue generation efforts. These challenges include weak legal, technical, and institutional structures and capacities. Capacity building is weak in these counties. The construction and collection of digital taxes especially DSTs implies a reliance on an international specialist to assist in the early stages of design and implementation, yet these specialists are often expensive and difficult to retain (Rukundo 2020). Financial constraints make it difficult to pay competitive remuneration or to engage in intensive training programs or even to second personnel to countries with more developed digital taxes. Similar capacity concerns were raised in relation to transfer pricing legislation enforcement in African countries by Mashiri (2018), Sebele-Mpofu et al. (2021a), and Kabala and Ndulo (2018).

In addition, the intangible and visible nature of digital services requires comprehensive technical skills and capacity as well as investment in technological advancement, purchase of equipment and software, and intensive technical training to be able to tax the sector. African countries suffer from a shortage of financial resources. This has been worsened by the effects of the COVID-19 pandemic on tax collections, prices of minerals and commodities as well as the commitment of significant financial resources to fighting the pandemic.

The nascent nature of Digital service tax policy brings challenges to definitions in tax legislation, or the income tax Acts provision guiding the administration of DSTs. For example, while digital services include some of those listed in Figure 1, the provisions of the Income-tax Acts extracts given in Table 3 are not explicit on the services earmarked for taxation through DSTs. While in Zimbabwe the Act refers to broadcasting services offered through digital platforms and e-commerce services being a targeted for taxation services. The definition of electronic services is not clear. Tunisia alludes to DSTs being levied on the sale of digital services and computer applications and does not elaborate on the digital services. Kenya on the other hand refers to the DSTs being charged on income accruing through a digital marketplace and the marketplace is not fully explained. From the literature review, the uncertainties in definitions coalesce around fundamental terms such as electronic services, digital marketplace, e-commerce activities, digital services, and the supply of digital services. The concerns on the challenging effect of underdeveloped tax legislation in African countries are also alluded to by Taxwatch (2021) and Kabwe and van Zyl (2021). The researchers allude to the ambiguities in definitions in digital taxation frameworks in Africa, pointing out that the definitions are narrow and vague.

The challenges are further worsened by a lack of tax knowledge and awareness on taxation in general (Sebele-Mpofu and Chinoda 2019) and on digital taxes in particular (Ahmed and Gillwald 2020; Philip et al. 2021), considering they are still a novel implementation in developing countries. African countries should bridge the knowledge and awareness gaps through information dissemination, policy briefs, and workshops. Resources can be set aside for capacity building and the secondment of personnel to other countries.

4.2.3. Increased Administration and Enforcement Costs

As earlier outlined that the OECD guidelines are taking a long to finalize and implement, some developing countries including African countries are implementing their own countries’ contextual digital taxes that they would have to repeal later when now adopting the multilateral OECD framework consensus-motivated digital taxes (Becker 2021). The implementation of the country context regulation would culminate in significant tax administration and enforcement costs being incurred as well as other costs for setting up the tax system such as technical training costs, human capital, and technological resources. In some cases, the benefits reaped would not be able to justify the costs incurred in setting up the provisional digital tax systems. The costs would be disproportionate to the revenues collected (Kelbesa 2020). Considering the revenue authorities in African countries are current authorities are currently grappling with auditing and dispute resolution challenges in relation to transfer pricing (Sebele-Mpofu et al. 2021b) and weak legal, administrative, and enforcement capacity to collect revenue from the informal sector (Sebele-Mpofu 2020, 2021), digital taxes might be faced with the same problem. Challenges in tax administration, auditing, monitoring, and enforcement might impede the collection of digital taxes (Kelbesa 2020; Kofler 2021; Kofler and Sinnig 2019).

4.2.4. Increase in Compliance Costs

There are several implications for compliance costs. These costs are likely to soar due to the implementation of digital taxes. Compliance with various and changing requirements in every country where digital companies or MNEs have digital sales would increase compliance burdens significantly. The costs might be very high, consequently becoming prohibitive to the information, communication and technological infrastructure needs as well as updates to meet the evolving legislative requirements. This could also increase operating costs significantly (Bulusu and Ali 2020; Bunn et al. 2020). In addition, the e-invoicing rules could be cumbersome, and increase the workload and volume of transactions, thus bringing complexity to accounting and tax systems. This could be costly and demanding, especially because due to fiscalisation, some revenue authorities require businesses to transmit sales invoices directly to the revenue authorities’ databases as the transaction takes place (Bulusu and Ali 2020; Megersa 2020). African countries must find ways of simplifying the digital taxes system but bearing in mind that issues to do with identifying the location of users, digital revenue, and value creation are problematic

4.2.5. Possible Challenges in Abolishing the Interim Digital Taxes (DSTs)

The construction, implementation, administration, and enforcement of tax policy, especially for a new one takes a great deal of time, money, and effort. Similarly, the implementation of the interim DSTs in some countries, African countries included would take up substantial resources as well as time to bring them to functionality. Therefore, the likelihood of abolishing them is questionable (Kelbesa 2020; Megersa 2020). The general argument is that once taxes are implemented, the taxes are always problematic to abolish. The thought and willingness of repealing the unique country digital tax legislation and implementing a completely new set of legislation when consensus is eventually reached on the application of the consensus-motivated OECD regulation DSTs is controversial (Becker 2021). The implementation of the OECD agreed digital tax regulations implies new additional costs in the form of effort, administration, and enforcement, resources as well as in the form of processes and increased compliance costs. The practicability and feasibility of such a transition are problematic. The cost and benefit evaluation of having the individual country’s digital taxes for a short time and then repealing them raises questions on the prudence of implementing temporary digital taxes in the short term and later the consensus-based one (Kelbesa 2020; Kofler 2021). One could argue that perhaps they are important to collect revenues immediately in the short term while awaiting the finalization of the taxes. Perhaps it is better to tap the revenue now as the digital economy is growing than to wait for an unknown future.

4.2.6. Lack of Co-Operation and Information Asymmetry

Imposing and enforcing tax rules on foreign companies that have a market but are not physically located in the market jurisdiction can prove to be challenging as it requires a high level of cooperation between the countries involved or some sort of contractual agreement to ensure adequate information is shared in a transparent and fair manner (Kelbesa 2020). Otherwise, information asymmetry would impede digital tax legislation application and enforcement, similar to transfer pricing regulation enforcement that is curtailed by lack of cooperation between countries and the developed—developing country power imbalances Similar challenges were pointed out by Mashiri (2018) and Sebele-Mpofu et al. (2021a) when discussing the effectiveness of transfer pricing rules in mitigating tax evasion and avoidance in African countries. The political and economic power imbalances between African states and developed countries such as the United States where most of the big technological giants are based could affect the effectiveness of DSTs. When studying the effectiveness of VAT legislation taxing the digital economy, Kabwe and van Zyl (2021) raise concerns about the ability of the African countries to hold MNEs or their developed country governments to effectively comply with or account for DSTs owing to the economic and political power differences.

To avoid and evade taxes, the companies supplying digital services can choose not to file tax returns in the market jurisdiction or country where their consumers are based if the sales exceed or reach the taxable thresholds to avoid honoring the arising tax obligations. On the other hand, the foreign country (home to the digital company) may not be motivated by anything to assist in enforcing adherence to the tax regulation of the other country or even ensuring that the correct information on sales is disseminated (Kelbesa 2020; Megersa 2021). Contrastingly, many tax authorities in developing especially African countries, lack the capacities and capabilities, and technical competencies to adequately administer tax, let alone the propensity to manage the possibly overwhelming number of digital transactions (Kelbesa 2020; Mekgoe and Hassam 2020). Capacity weaknesses are the biggest challenge for tax administration in Africa (Sebele-Mpofu 2020; Sebele-Mpofu et al. 2021b), coupled with the complexity of tax systems and ambiguous tax laws (Sebele-Mpofu and Chinoda 2019). Digitalization brings significant taxation challenges as it allows countries to have an economic life in other countries with minimal or no tax presence altogether.

In addition to the actual challenges relating to the implementation of digital taxes discussed above risks and threats linked to the possible negative effects of digital taxes are also a reality for African countries to grapple with digital tax administration (de Lima Carvalho 2020; Kelbesa 2020; Kofler and Sinnig 2019). These include the likelihood of overtaxing companies, adverse impact on investment, growth, and innovation, welfare loss, and the possible passing of the tax cost to local customers in high prices (Becker 2021; Ganter 2021; Kofler and Sinnig 2019; Low 2020). These are important possible negative externalities that require consideration because taxation is not only about collecting tax revenue but also about fostering economic growth and reducing inequalities.

4.2.7. Probability of Over-Taxation

In the quest for fairness, equity, or impartiality in digital taxation and in compliance with international agreements, countries might be compelled to levy digital taxes on both citizens and non-residents. This can result in double taxation, especially where a transaction is liable for both digital and corporate taxes. The possibilities of excessive taxation were also raised by Kelbesa (2020) and Kofler (2021). According to Rukundo (2020), digital taxes might lead to increased tax competition that might lead to race-bottom, erode the tax base, and discourage investment. The relationship between digital taxes and the canons of taxation requires due consideration.

4.2.8. Possible Welfare Loss

Taxes normally distort economic decisions (Mpofu 2021a). Companies sometimes take economic decisions that they would not have taken in the absence of tax implications. The production and possibly supply decisions could be compromised or altered and this could lead to overall welfare loss in the economy, productivity, and digitalization (Bunn et al. 2020; Kelbesa 2020). Digital taxes might undermine digital and financial inclusion in African countries through reduced internet usage and funds for development (Ndung’u 2019). According to Stork et al. (2020), digital taxes will not only affect connectivity and affordability (consumption and pricing decisions) but also investment in information technology and the internet value chain (capital investment decisions). These decisions might lead to the loss of household incomes, and business incomes, and ultimately reduced tax revenue. Ahmed and Gillwald (2020) adduce those digital taxes impinge on the universal access to internet efforts by developing countries as well as enfeebling social and economic development efforts. Rukundo (2020) contends that digitalization and information technology are linked to high productivity in developed countries owing to digital dividends. Digital dividends refer to the gains from digitalization such as penetration of new markets, reduced information costs, increased trust, and transparency in transactions. It is important to note that on the other hand, digitalization might increase tax evasion and avoidance due to the ease of concealing digital transactions.

4.2.9. Negative Effect on Investment, Growth, and Innovation

Digital taxes are likely to lead to an increase in the cost of capital for supplying the services. This might reduce the motivation to invest and thus result in a negative effect on the growth of the business and economic growth in general (Kelbesa 2020; Low 2020). The gross tax could further stifle investment in innovation for the companies directly or indirectly affected by the digital taxes. This could increase losses or reduce the profitability of start-up companies and SMEs (Becker 2021; Deloitte 2020). Digitalization spurs innovation and if this innovation is curtailed, the digital economy is adversely affected as well as its growth. The consequences could be loss of employment, reduced chances of employment creation, and lost opportunities to improve the welfare of citizens (through employment and access to digital services) as well as the building up of trade wars.

4.2.10. Possibility of Economic Incidence of Taxes Being Passed to Consumers

The above is contingent on the price elasticity of demand and supply of digital services (buyers and sellers respectively) as well as the market structure. The digital taxes could be wholly or partially passed on to the users (both individuals and businesses) in the form of increased prices. This would reduce the consumption of certain goods and services being expensive thus contributing to welfare loss (Becker 2021; Kelbesa 2020; Low 2020). It is there important to pay due consideration and analysis to the possible treatment and effect of digital taxes (direct taxes and VAT on digital taxes) as these can have substantial effects on the prices of goods and services, consumption patterns, demand, digitalization, and economic growth. Otherwise, ironically, the effort to mobilize more revenue can bring several problems that can end up leading to reduced economic activity and ultimately reduced tax revenue.

4.3. Implications and Lessons Drawn on Digital Taxation in African Countries

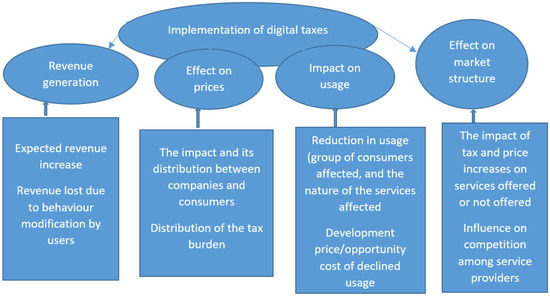

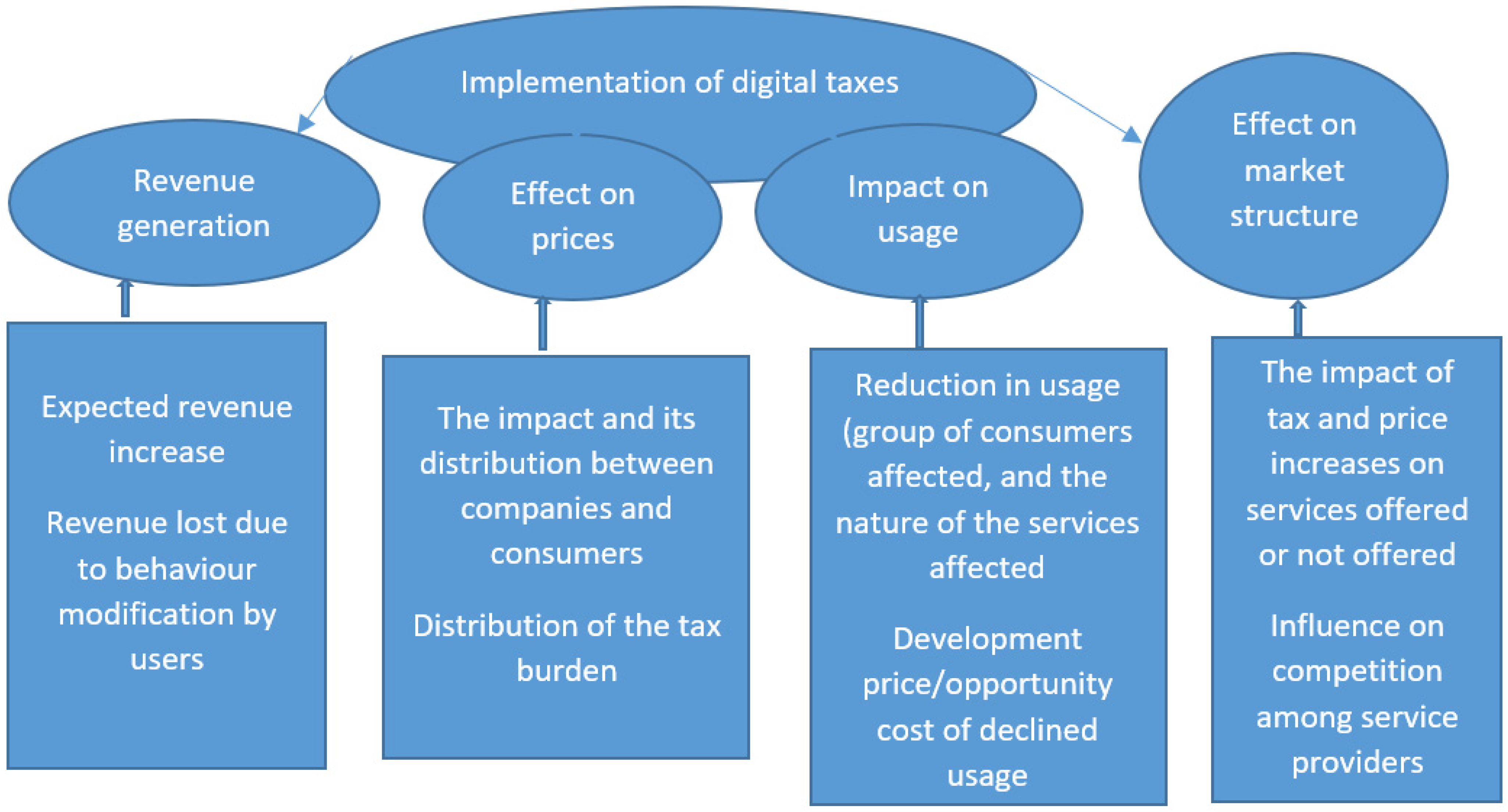

While the diversity of African nations in economic, political, and social environments as well as in the tax administration structures and fiscal capacities and capabilities signal the need to have contextual policy formulation, implications, and recommendations, several lessons and implications can be drawn from the implementation of digital taxes in some African countries that can guide other African countries in pursuit of their tax policy. Building from the literature by Munoz et al. (2022), this study summarizes the implications of administering direct DSTs under four fundamental issues, revenue advantages, price increases, the decline in using digital services, and distortions in the market structure. It is crucial for the design of digital taxes to consider the contradictory impacts of the application of digital taxes on the identified key aspects. Figure 2 foregrounds the discussion of the implications of digital taxes. Figure 2 gives a visual synopsis of the implications, thus aiding readers to quickly scanning through the contents of this section.

Figure 2.

Digital tax implications.

The review established that the implications of digital tax policy are paradoxical. The implications are driven by the possible opportunities and challenges of implementing direct DSTs discussed above. These include the possibility of increased tax revenues. Reduction in tax revenues, the possibility of trade wars, race bottom, and infringement of existing tax treaties and agreements.

4.3.1. Revenue Mobilization, Increased Tax Morale, and Tax Compliance

DSTs can be a tool for maximizing tax revenue collection (Ahmad et al. 2021; Onuoha and Gillwald 2022), but might also give rise to unintended outcomes. These views have been shared by different researchers as they alluded to the likelihood of both favorable and unfavorable consequences such as more revenue, economic recovery, enhanced control, and transparency when dealing with MNEs (Low 2020) and the possibility of disfranchising and increased marginalization of the poor and low-income earners (Becker 2021; Clifford 2020; Munoz et al. 2022). Improved transparency in taxation could help boost the public coffers of African countries that were severely affected by the effects of the COVID-19 pandemic especially the reduction in corporate taxes and other trade taxes such as customs duty. The taxation of non-tax paying digital MNEs could boost tax morale among domestic digital companies that are paying tax. This could increase tax compliance. This could improve revenue mobilization to fund the SDGs. In Uganda, Nicholas et al. (2017) submit evidence that e-commerce activities such as online network marketing enable citizens (employed and unemployed) to earn profits, bonuses, and commissions as well as passive or residual incomes. This contributes to poverty reduction, improving the quality of life of citizens, and to employment creation.

4.3.2. Reduced Usage, Reduction Investment in Digital Services, and Declining Revenue

The reduction in usage or the switch to alternatives could lead to a reduction in usage and possible tax revenues mobilized through various tax heads. If companies can pass the tax to consumers this would impede digitalization, digital transformation, and digital inclusion in the African continent (Saint-Amans 2017). If companies cannot pass the tax on consumers this would reduce investment or drive a capital flight to countries that have not implemented DSTs. This would negatively influence the achievement of SDGs such as those aimed at poverty reduction, reduction of inequality, provision of decent work, and quality education among others. This was also alluded to by Mpofu (2022) in relation to mobile money taxes in Africa.

4.3.3. Race Bottom Tax Competition

DSTs in Africa could possibly lead to race bottom tax competition by tax jurisdictions in Africa with governments and tax authorities offering tax incentives and low taxes to encourage companies to invest. Tax is a cost in addition to other economic costs. Therefore, to be an investment destination of choice, countries might offer tax incentives, deductions, and exemptions that are unsustainable in the long-term and detrimental to revenue mobilization. Tax competition leads to race bottom. In the case of African countries, Oguttu (2018) bemoans the poorly designed tax incentive tax policies and the awarding of excessive tax incentives that erose tax bases. Sebele-Mpofu et al. (2022) affirm the erosion of the tax base through the exploitation of tax incentives by investors and MNEs, with the cost of awarding these incentives exceeding the gains in foreign direct investment. Acknowledging the possibility of negative implications of awarding tax incentives and tax competition, Bahl and Bird (2008), argue that tax competition has a significant influence on sustainable revenue mobilization, sustainable national budgets as well as on sustainable development especially in countries with an overreliance on tax revenues more so on corporate taxes. Kabala and Ndulo (2018) highlight that most African countries overly depend on taxes to raise revenue for the government to fund public expenditure. Ganter (2021) argues that DSTs must be carefully implemented to fund sustainable development initiatives.

4.3.4. Infringement of Tax Agreements

The unilateral taxes’ legal implications might conflict with multilateral tax agreements such as the OECD consensus-based digital taxes and accompanying agreements. There might be double taxation implications where revenue is subjected to both corporate tax and digital taxes. Perhaps giving provisions for crediting digital taxes against corporate taxes might address this problem. Digital taxes might increase the risk of double taxation and income shifting between those countries giving digital taxes as an allowable deduction against corporate tax and those countries levying digital taxes (Kofler 2021).

4.3.5. Conflict and Unfairness Perceptions