Abstract

This research aimed to identify and understand the key factors influencing the effectiveness of online learning, with a specific focus on accounting courses. To achieve this goal, the study relied on the assessments and perceptions of students in the accounting department engaged in online learning. This study provided a model example to uncover the key factors and connections between the quality of online learning and its advantages in accounting education. The research was organized into three main phases: initially presenting the research concept, defining the goals and the essential components of the study. Subsequently, the research continued with a review of the literature, integrating scientific contributions from around the world and linking them to the research hypotheses. The research revealed three key factors in the quality of online learning: Factor 1, Access and communication between students and professors in online learning, emphasizing the importance of interaction and accessibility in this context; Factor 2, The security of platforms and the content of electronic learning, identifying the significance of technology safety and content security; and Factor 3, The ease of use and flexibility of access in online learning, improving student autonomy and global access to content. Hypothesis 1 confirmed that the factors of online learning quality were influenced by the context and the structure of online learning, including specific requirements. Hypothesis 2 asserted that the advantages of online learning were linked to the acceptability of electronic assistance, self-efficiency, and students’ intention to use electronic learning. Hypothesis 3 confirmed that quality factors had a strong correlation with the advantages of online learning in the field of accounting. This research, through student feedback and perspectives, contributed to a deeper understanding of online learning and the importance of quality factors in promoting it in the accounting field. In summary, this research highlights the crucial link between quality attributes and the benefits of online learning in accounting education. It is recommended that educators and institutions prioritize these attributes to enhance the effectiveness of online education, offering valuable insights for the development of more efficient and advantageous online learning environments.

1. Introduction

Information and communication technology (ICT), with a specific focus on e-learning, has emerged as a transformative educational approach that has greatly enhanced teaching and learning processes worldwide. This impact extends to the field of accounting, a critical domain that plays a key role in shaping future generations for both the economy and the academic realm. E-learning has revolutionized teaching methods by shifting the traditional paradigm (Akinyi and Oboko 2020). However, it is essential to acknowledge that e-learning presents certain challenges, and many nations face difficulties in implementing advanced electronic learning systems (Pham et al. 2019). This complexity often arises from issues such as inadequate technological infrastructure, insufficient maintenance, and challenges related to teacher training, which can manifest during online learning sessions (Al-Emran and Teo 2020). E-learning, according to various studies, refers to the delivery of educational content and knowledge through the utilization of diverse electronic devices. It involves harnessing information and communication technology to cater to people’s learning needs and aspirations (Al-Nimer and Alsheikh 2021). Under the umbrella of remote education, e-learning encompasses a wide array of technological applications and learning methodologies, including computer-based learning, internet-driven education, and virtual classrooms (Alkindi et al. 2022). Therefore, online e-learning in higher education contexts prioritizes the cultivation of metacognitive, reflective, and collaborative learning, transcending the confines of structured subject-based education to emphasize the value of self-directed, incidental learning that enhances performance (Bajaj et al. 2021). A significant body of prior research has demonstrated the myriad advantages of e-learning for students, emphasizing its ability to enhance student focus, flexibility, and communication between professors and students (Chen 2009).

Universities worldwide dedicate substantial efforts to maintaining current and consistent course content, fostering robust inter-academic communication, and incorporating valuable insights from their students, particularly the younger generation (Chen 2009). In contrast to traditional learning methods, the administrative responsibilities within universities become notably more pronounced in the development of specialized structures and processes within online environments. The shift from traditional pedagogical methods to online teaching and learning environments necessitates faculty to adapt and significantly transform their instructional approaches to cater to the unique learning requirements of online students. This transformation encompasses not only the acquisition of technical skills related to online learning but also a shift in pedagogical methodologies (Connolly et al. 2020).

In the context of higher education, my research delves into a critical facet of online learning, specifically within the domain of accounting education and its distinctive characteristics. In this context, I have structured my research around key factors related to online learning, including the advantages of e-learning, the perceived usefulness of e-learning, self-efficacy in using e-learning, the perceived ease of using e-learning, and the targeting of e-learning usage behavior, drawing upon a condensed data structure. In Kosovo, our country, significant investments have been made in online learning infrastructure over the past several years. These investments encompassed the training of teaching staff, procurement of essential equipment, and the execution of pilot projects with the support of the European Union and the USA.

The principal aim of this study is to recognize and gain a comprehensive understanding of the crucial elements that impact the efficiency of online learning, particularly in the context of accounting courses. This inquiry revolves around the viewpoints and appraisals of students who are part of the accounting department and have actively participated in online learning sessions. Their assessments form the cornerstone for revealing the fundamental factors that promote the enduring progress of online learning within the domain of accounting education. The research has been meticulously structured to unfold in several phases. The initial segment of the paper introduces the research concept, laying the groundwork for the subsequent exploration. It sets the stage by outlining the primary components of the study and establishing the research’s objectives. Moving forward, the literature review section delves into the scholarly contributions of experts from around the world. This segment establishes a connection between the research’s hypotheses and previous scientific investigations. By doing so, it creates a hierarchical and integrated comparison for each hypothesis, enabling readers to identify the commonalities between this study and other notable works published in reputable journals. In essence, this research aims to illuminate the factors that underpin effective online learning in the field of accounting, leveraging the feedback and perspectives of students to build a comprehensive understanding of the subject. The structured approach of this paper, with its well-defined phases, ensures that the study is firmly grounded in both the existing literature and the empirical insights provided by students, facilitating a comprehensive exploration of this important aspect of contemporary education.

2. Theoretical Framework and Research Hypotheses

The literature is provided with a focus on the notion of hypotheses, presenting the aspects most relevant to my study with the goal of assuring the accuracy of the review and demonstrating the significance they have for the topic of my research.

Hypothesis 1.

The quality factors of online learning in the accounting course are determined by the context of the learning requirements and the structure of the online learning.

Due to its adaptability for student accessibility across various devices and its notable attributes like efficiency and ease of access, e-learning has garnered significant attention within the higher education sector. This interest persists even after traditional lectures (Dangi and Saat 2021). E-learning is also undergoing a transformation into a more inclusive, global form of education encompassing a wide array of academic disciplines. Student engagement is regarded as a measure of e-learning success, while effective administration is recognized as another advantageous aspect of e-learning that profoundly influences the learning process (Eom and Ashill 2018). Self-efficacy, learning styles, student motivation, metacognition, and active participation in learning are among the factors associated with the success of electronic learning, as indicated in a study (Grabinski et al. 2020). Furthermore, e-learning offers students an opportunity for self-regulation by allowing them to plan their assignments and exercise control over learning activities through the regulation of cognition and metacognitive experiences (Söllner et al. 2018). This is particularly pertinent in the context of accounting majors. The quality of e-learning is believed to be influenced by student self-regulation, which is considered an integral component of electronic learning. In another context, we observe how information technology has spurred progress in various industries, including business, banking, healthcare, and education. This surge in educational growth, driven by the fusion of education and technology, has established e-learning as a powerful educational tool (Letseka 2021). E-learning has gained widespread acceptance in higher education, especially within economics and accounting disciplines, a trend noted by several academics (Valencia-Arias et al. 2019). It is suggested that substantial research has been conducted to optimize the effectiveness of these systems, primarily focusing on the quality of e-learning systems. Numerous researchers have sought to identify the success factors of e-learning, often concentrating on the criteria and circumstances surrounding e-learning development, particularly with regard to lecture content (Heald 2018). Generally, these studies have concentrated on the individual components of critical success factors for e-learning systems while overlooking the synergistic interactions among these success factors (Söllner et al. 2018).

This connection aligns with Hypothesis 1, which asserts that the quality factors of online learning in accounting courses are influenced by the specific learning requirements and the structural framework of online learning.

Hypothesis 2.

The advantages of online learning are determined through quality factors such as the perceived usefulness of e-learning, self-efficacy, perceived ease, and behavioral intention of using e-learning.

Various aspects of the benefits of quality are evident in multiple ways, commencing with the advantages of e-learning, self-efficacy, and accessibility, all of which are presented as integral components of the quality of e-learning. According to Söllner et al. (2018), the perceived usefulness exerts statistically significant effects on students’ attitudes towards e-courses, encompassing both their willingness to engage with electronic resources and their behavioral intention to utilize them. Consequently, it has been established that perceived utility significantly influences students’ behavioral intentions. Researchers have consistently found in various studies that students have already integrated the internet into their daily lives, simplifying the incorporation of internet-based platforms for e-learning into their academic routines (Santhanam et al. 2008). Studies suggest that students themselves can foster a supportive environment that cultivates a positive outlook towards online platforms, which, in turn, aids students in acquiring valuable knowledge and skills through these platforms (Tahoon 2021). Moreover, it seems to have a statistically significant impact on the behavioral intention to use, attitude, perceived usability, and perceived ease of use. In essence, it pertains to how students embrace e-learning and rely on their overall perspective (Tibaná-Herrera et al. 2018) (Ali et al. 2018).

The internet has profoundly transformed remote education on a global scale. E-learning is a modern form of learning that already embodies all the characteristics of traditional education. Current research is discussing the shift in paradigm from conventional education to this new model (Lee et al. 2022). Worldwide, distance learning has consistently expanded with the assistance of technology, influencing the overall quality of education. Other studies have revealed that e-learning enhances skills and fosters social and economic development through various avenues. Online education represents an innovative format that affords tremendous flexibility in utilizing technological resources, including diverse communication channels (Ali et al. 2018). Numerous instances attest to e-learning’s contribution to social and economic advancement, underscoring the reciprocal relationship where economic growth significantly impacts capital investments, which subsequently translate into high-quality learning outcomes. This aligns with the research hypothesis, yet it is noteworthy that many scholarly works emphasize that the benefits of online learning are contingent upon pre-established conditions and perceptions, particularly in terms of social aspects (Palvia et al. 2018). Many educators globally advocate and continue to champion this form of education, advocating for the complete replacement of traditional education with e-learning, especially in subject areas where online learning can be more effective (Nugroho et al. 2018).

This connection relates to Hypothesis 2, which posits that the advantages of online learning are determined by quality factors such as the perceived usefulness of e-learning, self-efficacy, perceived ease, and the behavioral intention to engage with e-learning.

Hypothesis 3.

There is a significant correlation between the quality factors and the advantages of online learning.

In addition to other aspects of online accounting education, there are several connections between distance learning and academic achievement that have been elaborated (Sadeghi 2019). This concept is seen as a contemporary reality, offering both opportunities and challenges for educational institutions. It empowers students with more flexibility in terms of when, where, how, and from whom they acquire knowledge. Additionally, it enhances accessibility to education for an ever-expanding population (Sarker et al. 2019). Consequently, the current state of online education and student perspectives are influenced by the interrelation of various elements within higher education, particularly e-learning (Narh et al. 2019) (Gentile et al. 2020).

Lectures can be attended from anywhere, irrespective of geographical location, thanks to the direct connection of online education with flexible modes of utilization. This underscores a robust positive association, ultimately granting users of e-learning platforms more autonomy (Al-Fraihat et al. 2020). (Eze et al. 2020). E-learning systems offer a wide array of advantages to students, commencing with control over the curriculum and learning pace, making it possible to tailor the learning process to meet their specific needs and academic objectives (Liu 2020). This profoundly influences the dynamics between university professors and students. Despite the challenges that may emerge during online lectures, e-learning has the potential to enhance students’ learning experiences, which aligns with the core aim of e-learning (Tere et al. 2020) (Krasodomska and Godawska 2021).

Within the realm of e-learning, several factors can be perceived as obstacles to learning, including decreased student motivation, delays in receiving assistance, and the sense of isolation that students may feel due to the absence of physical peer presence. This connection ties into Hypothesis 3, which postulates a substantial correlation between the quality attributes of online accounting education and the benefits of online learning.

3. Methodology

The research presents students’ perception of the importance and influence of quality factors in the teaching of accounting subjects during online learning, a concept unknown to us until now. The research was carried out from January 2022 until 31 May 2022, with accounting students. The research has lasted longer since the data were sent to a large number of students, and 240 students of different accounting years responded to the research. The instrument for collecting students’ opinions was prepared through a Google form, which was sent directly after the online lectures. Their completion represents the opinion of the students regarding the importance of online learning, namely what are the main factors, and how these factors affect the quality of accounting courses during online learning. The main variables of the research are the advantages of online learning in the role of the dependent variable, while the variables such as perceived usefulness of e-learning, perceived self-efficacy of using e-learning, perceived ease of using e-learning, and intention of e-learning usage behavior in the role of independent variables. The literature applied during the review was selected from the world’s most renowned and reliable databases, such as MDPI, Scopus, Web of Science, and Web Direct, which were classified based on the applied methodology, research structure, and keywords (E-learning, Accountability, Quality factors, Accounting lectures, Online learning).

The structure of the statistical analysis is based on the hierarchical concept of the presentation of the results, where I started with the presentation of the descriptive results and performed the normality and reliability test to increase the reliability of the questionnaire. To validate the hypotheses, I applied the factorial analysis, the test of multiple linear regression, and the Spearman correlation matrix. The results of the analyses are presented in tabular form and interpreted within the statistical concept and logical effects within the variables used in the research. Below, I have presented the statistical concepts based on which I treated the data of my research, the econometric model, and the research concept.

Normality test:

W = (∑ni = 1aix(i))2/∑ni = 1(xi − x)2

Factorial analysis:

Factor analysis is a method of investigating whether some variables of interest Y1, Y2, Yl, are linearly related to a smaller number of unobservable factors F1, F2, Fk.

Regression analysis:

Yi = β0 + β1xi + ui

Correlation matrix:

rs(X,Y) or ρ(X,Y)

i.e., If Rx = Ranks of X and Ry = Ranks of Y, then rs (X,Y) = r(Rx,Ry)

3.1. Reasonableness of Applying Statistical Tests

- The application of the normality test W = (∑ni = 1aix(i))2/∑ni = 1(xi − x)2 has enabled me to determine the distribution of the data I have collected, proving that they have non-parametric distribution. Based on this, I was instructed to apply non-parametric tests to increase the reliability of the results and the research in general.

- Through the Alpha Cronbach’s test Y1, Y2, Yl, I have validated my data, offering the readers data of a high level of reliability.

- Factor analysis has enabled me to present the factors influencing the advantages of online learning, evaluating in detail each variable, which provides a high level of reliability and quality of the research.

- Through multiple regression analysis, I presented the dependence of online learning, testing exactly which factors have an impact on the increase in online learning preferences.

- Correlation matrix analysis determines the relationships between variables, offering another perspective on the correlation between independent and dependent variables.

3.2. The Econometric Model

Yi,t = β0 + β1 DPMi,t + β2 VFP,t + β3 LPP i,t + β4 SSP i,t ꜫi,t

DPM—Perceived usefulness of e-learning

VFP—Perceived self-efficacy of using e-learning

LPP—Perceived ease of use of e-learning

SSP—Behavioral Intention of E-Learning Use

Y—PMO

β0—Beta;

ꜫ—Error term.

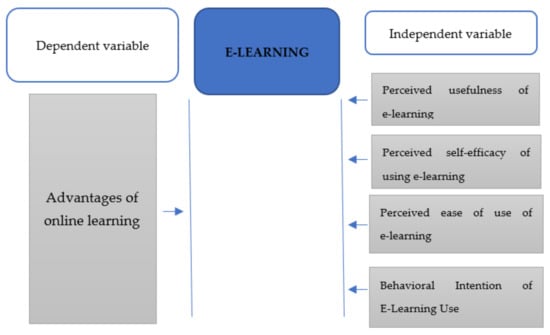

Figure 1 illustrates the conceptual model of the study, source by author.

Figure 1.

Conceptual model of the study.

3.3. Variables Included in the Research

In the framework of the applied variables, I also presented their scientific importance in my research and indicated which variables contain important elements that make them significant in determining their effects and connections in the research. In this context, five main variables are presented, such as the advantages of online learning in the role of the dependent variable, while variables such as perceived usefulness of e-learning, perceived self-efficacy of using e-learning, perceived ease of e-learning use, and intention of e-learning use behavior in the role of independent variables. Table 1 shows the importance of the variable, source by author.

Table 1.

Importance of the variable.

4. Results

The results of the research are organized in a hierarchical form, starting from the presentation of descriptive data, normality test, reliability, factor analysis, regression test, and correlation matrix. The results are presented in tables and interpreted according to the statistical and conceptual aspects of the study issue.

4.1. Descriptive Results

A total of 240 students participated in the research, of whom 93 were male, or 38.8%, and 147 were female, or 61.3%. Regarding age, 135 were from the age group 18–22 years, or 56.3%, 63 from the age group of 23.28 years, or 26.3%, 35 from the age group of 29–35 years, or 14.6%, five from the age group of 36–45 years, or 2.1% and two others in the 46–55 age group, or 0.8%. There were 186 bachelor-level students, or 77.5%, and 54 master-level students, or 22.5%. Table 2 below shows the descriptive results of respondents, source by author.

Table 2.

Descriptive results of respondents.

4.2. Test of Normality

The normality data show that we have a non-parametric distribution, which obliges me to use statistical tests that belong to non-parametric tests, such as factorial analysis, regression, and the Spearman correlation for the correlation matrix. Table 3 below shows the results of Normality test, source by author.

Table 3.

Normality test.

4.3. Reliability Test

Based on the following data, we understand that the data have high statistical reliability, i.e., 80% of the reliability level, which is considered a high level of reliability, and in this case, I conclude that the data are reliable for the inter-predictions of the following. Table 4 below shows the results of reliability test, source by author.

Table 4.

Reliability test results.

4.4. Factor Analysis

The factorial analysis presents the importance of the variables, which then determine the important factors in the context of the electronic learning of accounting. These parameters define the conditions in which e-learning takes place in the Republic of Kosovo, a country that has undergone a post-war transition, and which is now in a political and economic transition. Based on the following results, we have KMO = 0.947, Bartlet test = 3.880, df = 276, and p-value = 0.000, which determines that the data are reliable, and I can continue with their statistical interpretation. Table 5 shows the results for KMO and Bartlett’s Test, source by author.

Table 5.

Results for KMO and Bartlett’s Test.

Based on the table below, we understand that the data are classified into three main factors since only three of them have exceeded the Eigenvalue of 1. Table 6 shows the results for the Eigenvalue table, source by author.

Table 6.

Eigenvalue table.

First, it is necessary to clarify the process of selecting variables. Variables have been chosen based on their coefficient values, with those exceeding 0.60 being separated into distinct categories. This division serves the purpose of defining two groups of variables. In the first factor, variables have been classified into two groups: the first group (with values between 0.60 and 0.70) includes variables related to adapting to different learning styles (0.600), the ability to work with e-learning (0.611), and access to higher education for all students (0.695). The second group (with values exceeding 0.70) encompasses variables such as using study resources effectively (0.720), providing quick feedback (0.724), promoting a wide variety of interactions among students (0.727), and creating opportunities for collaboration and interaction among students (0.747).

The second factor involves the following variables: the first group (0.60–0.70) includes intentions to use e-learning to enhance learning (0.602), alignment of the e-learning service with personal learning styles (0.614), feeling secure while using the e-learning system (0.626), belief in the simplification of the learning process through e-learning (0.647), perceived user-friendliness of e-learning platforms (0.652), intentions to use e-learning as an autonomous learning tool (0.670), and feeling secure when using e-learning features (0.692). In the second group (with values exceeding 0.70), the variable relates to feeling secure when using online learning content (0.714).

The third factor encompasses variables in two groups. The first group (0.60–0.70) focuses on the ease and rapid distribution of educational materials (0.637), the availability of electronic tools for interactive communication between professors and students without face-to-face meetings (0.651), and the presence of technologies for taking tests and submitting assignments electronically (0.667). In the second group (with values exceeding 0.70), the variable pertains to the capacity of e-learning to enable students to study from anywhere in the world (0.720).

These variable groupings and their coefficient values relate to the research hypotheses:

Hypothesis 1 posits that the quality factors of online learning in accounting courses are influenced by the specific learning requirements and the structural framework of online learning.

Hypothesis 2 suggests that the advantages of online learning are determined by quality factors, such as the perceived usefulness of e-learning, self-efficacy, perceived ease, and behavioral intention to use e-learning.

Hypothesis 3 proposes that there is a significant correlation between the quality factors of online accounting learning and the benefits of online learning.

This categorization of variables and their relationship with the hypotheses helps to analyze the impact of these factors on the quality and advantages of online learning in accounting courses. Table 7 shows the results for factor analysis, source by author.

Table 7.

Factor analysis.

The variables within the first factor, specifically the first group, pertain to aspects associated with the approach and opportunities offered by e-learning. This category is referred to as the “approach to online learning”. In contrast, the second group of variables within this factor deals with different forms of interaction between students and professors, denoted as “mutual communication between professors and students”. Within the second factor, the variables in the first group focus on ensuring the safety and security of utilizing various online learning platforms. This category is designated as “safety aspects”. Conversely, the second group of variables in this factor concentrates on the security aspects concerning the content of e-learning, denominated as “safety with e-learning content”. In the third factor, the variables in the first group are associated with the ease of using e-learning, labeled as “ease of use”. On the other hand, the variables in the second group of this factor are centered around the flexibility of accessing e-learning from anywhere in the world, categorized as “flexibility of e-learning access”. Considering these findings, it can be deduced that the critical factors in the context of online learning in accounting, as perceived by students, are closely linked to aspects related to secure access, flexibility, secure e-learning content, and the ability to access from various locations globally, along with pedagogical considerations.

These Observations Have Relevance to the Research Hypotheses as Follows

In summary, the variables under investigation were categorized into three distinct factors. The first factor consisted of two groups, with the first group focusing on the approach and opportunities associated with e-learning, labeled as the “approach to online learning”. Meanwhile, the second group within this factor revolved around various forms of interaction between students and professors, termed “mutual communication between professors and students”. Moving on to the second factor, the variables in the first group were dedicated to ensuring the safety and security of using different online learning platforms, referred to as “safety aspects”. In contrast, the second group of variables in this factor centered on the security of e-learning content, designated as “safety with e-learning content”.

The third factor included variables in the first group related to the ease of utilizing e-learning, coined as “ease of use”. Conversely, the variables in the second group of this factor revolved around the flexibility of accessing e-learning from various global locations, categorized as “flexibility of e-learning access”. In light of these findings, it is evident that the key factors in the realm of online learning in accounting, from the perspective of students, are closely intertwined with aspects concerning secure access, flexibility, secure e-learning content, and the ability to access content from diverse global locations, all within a pedagogical context. Furthermore, these observations have notable implications for the research hypotheses: Hypothesis 1 posits that the quality factors of online learning in accounting courses are influenced by specific learning requirements and the structural framework of online learning. Hypothesis 2 suggests that the advantages of online learning are determined by quality factors such as the perceived usefulness of e-learning, self-efficacy, perceived ease, and behavioral intention to use e-learning. Lastly, Hypothesis 3 proposes a significant correlation between the quality factors of online accounting learning and the advantages of online learning.

4.5. Multiple Regression Results

Based on the findings from the multiple regression analysis, we can discern that the regression analysis can be compartmentalized into three distinct models. In the first model, we exclusively consider the perceived ease of using e-learning, which exhibits a regression value of 0.676, a beta coefficient of 0.743, and a statistically significant p-value of 0.000. The overall model demonstrates an elevated regression value of 0.552, with an associated F value of 293.073. The perceived ease of using electronic learning emerges as a pivotal factor in the normal progression of online learning. Its pronounced effects are clearly reflected in the elevated priority attributed to online learning. Therefore, it is evident that e-learning is an integral component of learning, embodying elements of perceived facilitation when used.

Within the framework of the second model, we identify two critical factors that exert influence on the advantages of online learning in the field of accounting. These factors specifically pertain to the perceived usefulness of electronic learning, which exhibits a regression value of 0.299, a beta coefficient of 0.287, and a statistically significant p-value of 0.000. Additionally, the perceived ease of using e-learning within this model is characterized by a regression value of 0.497, a beta coefficient of 0.546, and a statistically significant p-value of 0.000. The model as a whole demonstrates a squared regression value of 0.595, with a corresponding F value of 174.420.

These two factors, namely the perceived usefulness of e-learning and the ease of its utilization, play a pivotal role in the advancement of online learning. They significantly shape the level of student satisfaction during the e-learning process. In the third model, we identify three factors that exert influence on the advantages of online learning. In addition to the perceived ease of using e-learning and the perceived usefulness of e-learning, self-efficacy emerges as another crucial element in the regular evolution of online learning. Self-efficacy within this model is characterized by a regression value of 0.203, a beta coefficient of 0.228, and a statistically significant p-value of 0.000. Meanwhile, the other two factors exhibit relatively similar effects.

In conclusion, the multiple regression analysis reveals the significance of these factors in the context of online learning in accounting. Perceived ease of use, perceived usefulness, and self-efficacy are all integral elements that significantly influence the advantages and quality of online learning. Table 8 shows the results about regression analysis, source by author.

Table 8.

Regression results.

These findings suggest that the benefits of online learning are contingent upon several key factors. Primarily, the perceived usefulness of e-learning plays a pivotal role. This encompasses considerations related to the methodology of learning, the ability to learn from anywhere in the world, and the availability of technologies and electronic tools for effective communication between professors and students. Additionally, the perceived self-efficacy in the utilization of e-learning systems is of significant importance. This pertains to the assurance of safety when using various online learning platforms, their functionality, and the quality of content they provide. Furthermore, the perceived ease of using e-learning is a critical determinant.

4.6. Correlation Matrix

The analysis of the correlation matrix shows that strong significant relationships have been found between the factors that make up the electronic learning of the accounting field. This correlation was carried out to see the significant relationships between them, through Spearman’s Correlation. Table 9 shows the results about correlation analysis, source by author.

Table 9.

Correlations results.

The correlation analysis reveals significant associations between various factors. There is a strong correlation between the priority given to online learning and the perceived usefulness of e-learning (rho = 0.621**, p-value = 0.000), as well as with the perceived efficiency of using e-learning (rho = 0.632**, p-value = 0.000), the ease of utilizing e-learning (rho = 0.683**, p-value = 0.000), and the behavioral intention to use e-learning (rho = 0.586**, p-value = 0.000). Furthermore, the perceived usefulness of e-learning displays a notable correlation with self-efficacy (rho = 0.610**, p-value = 0.000), the perceived ease of using e-learning (rho = 0.636**, p-value = 0.000), and the behavioral intention to use e-learning (rho = 0.673**, p-value = 0.000). Self-efficacy also demonstrates a strong correlation with ease of use (rho = 0.696**, p-value = 0.000) and the behavioral intention to utilize e-learning (rho = 0.631**, p-value = 0.000). Likewise, the perceived ease of using e-learning is highly positively correlated with the behavioral intention to use e-learning (rho = 0.741**, p-value = 0.000).

These findings are pertinent to the research hypotheses as follows:

Hypothesis 1 postulates that the quality factors of online learning in accounting are influenced by the specific learning requirements and the structural framework of online learning.

Hypothesis 2 posits that the advantages of online learning are determined through quality factors, encompassing the perceived usefulness of e-learning, self-efficacy, perceived ease, and behavioral intention to use e-learning.

Hypothesis 3 postulates that there is a significant correlation between the quality factors of online accounting learning and the advantages of online learning.

The strong correlations observed between these factors validate the interconnectedness of quality and advantages in the context of online learning in accounting, supporting the research hypotheses.

5. Discussion

The research is focused on identifying factors related to online learning, its advantages, and the correlation between quality factors and the benefits of online learning. A discussion of these hypotheses and their connections follows:

- First hypothesis postulates that the quality of online learning in accounting courses is influenced by specific learning requirements and the structure of online learning. The text supports this by mentioning the adaptability of e-learning for students, its efficiency, and ease of access. It also emphasizes the importance of student self-regulation, which is a significant factor in the quality of online learning. The research seems to be examining how these contextual and structural elements impact the effectiveness of online learning in the field of accounting.

- Second hypothesis indicates that the benefits of online learning are associated with various quality factors, including the perceived usefulness of e-learning, self-efficacy, perceived ease, and the intention to use e-learning. The text discusses how students’ attitudes and behavioral intentions towards e-courses are influenced by their perceived usefulness. It also highlights the impact of student self-regulation and motivation on the quality of online learning. The hypothesis suggests that these factors are interconnected and contribute to the overall advantages of online learning.

- Third hypothesis proposes that there is a strong correlation between the quality attributes of online accounting education and the benefits of online learning. The text supports this by emphasizing the flexibility and accessibility of online learning, which enhances students’ autonomy and positively influences their learning experiences. It also acknowledges potential challenges but suggests that the advantages of online learning can outweigh these obstacles. The hypothesis implies that the quality factors directly contribute to the benefits of online learning in the context of accounting education.

The factor analysis categorizes variables into three distinct factors, and it relates these findings to the research hypotheses. The key findings and their connections to the hypotheses are broken down as follows:

Factor 1: Approach to Online Learning and Mutual Communication Between Professors and Students

The first group of variables in Factor 1 includes aspects related to the approach and opportunities offered by e-learning.

The second group of variables in Factor 1 deals with different forms of interaction between students and professors.

These findings suggest that the first factor relates to how students perceive the approach and interactions in online learning.

Safety Aspects and Safety with E-Learning Content. The first group of variables in Factor 1 focuses on ensuring the safety and security of utilizing various online learning platforms.

The second group of variables in Factor 2 concentrates on the security aspects concerning the content of e-learning.

This factor highlights the importance of safety and security in online learning, both in terms of the platforms used and the content being accessed.

Factor 3: Ease of Use and Flexibility of E-Learning Access

The first group of variables in Factor 3 is associated with the ease of using e-learning.

The second group of variables in Factor 3 is centered around the flexibility of accessing e-learning from various global locations.

Factor 3 emphasizes the importance of ease of use and flexibility in online learning, enabling students to access content from anywhere in the world.

These findings are connected to the research hypotheses as follows:

The categorization of variables in Factors 1 and 3 aligns with Hypothesis 1, which suggests that the quality factors of online learning in accounting courses are influenced by specific learning requirements and the structural framework of online learning. The variables in these factors reflect the students’ perception of the approach, interaction, ease of use, and flexibility, all of which are elements of the learning environment’s structural framework.

Posits that the advantages of online learning are determined by quality factors, such as perceived usefulness, self-efficacy, perceived ease, and behavioral intention to use e-learning. The findings in the text suggest that students place importance on security, safety, and ease of use, which are components of perceived usefulness and self-efficacy. These elements also relate to the students’ intention to use e-learning. Suggests a significant correlation between the quality factors of online accounting learning and the benefits of online learning. The factors extracted from the analysis, including approach, interaction, security, and flexibility, are closely related to the quality and benefits of online learning in the context of accounting education. The multiple regression analysis and correlation matrix findings provide valuable insights into the relationships between various factors related to online learning in the field of accounting.

Findings in the context of the research hypotheses:

Hypothesis 1.

The results from the multiple regression analysis confirm that the perceived ease of using e-learning plays a significant role in the normal progression of online learning. It is evident that e-learning embodies elements of perceived facilitation during its usage. This aligns with the idea that factors related to ease of use are integral to the quality of online learning, which is in line with Hypothesis 1.

The correlation analysis further reveals strong associations between various factors, indicating that there is a relationship between the structural framework of online learning (e.g., ease of use) and the quality of the online learning experience, supporting the hypothesis.

Hypothesis 2.

The multiple regression analysis identifies two critical factors, the perceived usefulness of e-learning and the ease of using e-learning, that significantly shape the level of student satisfaction during the e-learning process. These factors play a pivotal role in the advancement of online learning, supporting Hypothesis 2.

The correlation analysis confirms strong correlations between the perceived usefulness of e-learning, self-efficacy, and ease of use with the priority given to online learning and the behavioral intention to use e-learning. This indicates that perceived usefulness, self-efficacy, and ease of use are indeed important quality factors that contribute to the advantages of online learning.

Hypothesis 3.

The strong correlations observed between various factors, as highlighted in the correlation matrix, validate the interconnectedness of quality factors and advantages in the context of online learning in accounting. These findings provide support for Hypothesis 3, indicating that there is indeed a significant correlation between the quality factors of online accounting learning and the advantages of online learning.

6. Conclusions

The goal of the research is to better understand the important variables that affect online learning in the context of accounting education, the benefits that result from these variables, and the relationship that exists between these quality features and the advantages of online learning. To accomplish this, three hypotheses were formulated and examined, shedding light on the intricate relationship between various elements that shape the landscape of online education.

This hypothesis emphasizes the importance of specific learning requirements and the structural framework in influencing the quality of online learning. The text underscores the adaptability of e-learning for students, its efficiency, and ease of access. Furthermore, it highlights the crucial role of student self-regulation in the quality of online learning. The research investigates how these contextual and structural elements impact the effectiveness of online learning in accounting.

This hypothesis contends that the benefits of online learning are intricately linked to various quality factors. The text discusses how students’ attitudes and intentions toward e-courses are influenced by their perception of usefulness, underlining the significance of self-efficacy and motivation in the quality of online learning. The hypothesis argues that these factors are interconnected and contribute to the overall advantages of online learning.

This hypothesis posits that there is a strong relationship between the quality attributes of online accounting education and the benefits of online learning. The text supports this by emphasizing the flexibility and accessibility of online learning, which enhances students’ autonomy and positively influences their learning experiences. It acknowledges potential challenges but indicates that the advantages of online learning can outweigh these obstacles. The hypothesis implies that the quality factors directly contribute to the benefits of online learning in the context of accounting education.

The factor analysis further breaks down the variables into three distinct factors and connects these findings to the research hypotheses:

Factor 1 relates to the approach to online learning and mutual communication between professors and students. It encompasses aspects of how students perceive the approach and interactions in online learning. This aligns with Hypothesis 1, which suggests that the quality of online learning is influenced by the structural framework and learning requirements.

Factor 2 centers on safety aspects and safety with e-learning content, focusing on the security of using various online learning platforms and the security of e-learning content. This factor underscores the importance of safety and security in online learning, which is connected to Hypothesis 2 regarding the perceived usefulness and self-efficacy in online learning.

Factor 3 emphasizes the ease of use and the flexibility of e-learning access. It highlights the significance of ease of use and the ability to access e-learning content from anywhere in the world. These factors align with Hypothesis 1, underlining the importance of the structural framework in shaping the quality of online learning.

In summary, the research findings provide compelling evidence that supports all three hypotheses. The quality factors of online learning in accounting courses are indeed influenced by specific learning requirements and the structural framework of online learning, as indicated by Hypothesis 1. Furthermore, the advantages of online learning are intricately tied to quality factors, including perceived usefulness, self-efficacy, and ease of use, validating Hypothesis 2. Lastly, the research demonstrates that there is indeed a significant correlation between the quality factors of online accounting learning and the benefits of online learning, confirming Hypothesis 3. This comprehensive analysis underscores the interconnectedness of quality and benefits in the context of online learning, supporting the notion that the effectiveness and advantages of online education are deeply rooted in various quality attributes and the contextual and structural framework in which learning takes place.

Author Contributions

Conceptualization, S.A. and N.B.V.; methodology, S.A. and N.B.V.; software, S.A.; validation, S.A. and N.B.V.; formal analysis, S.A. and N.B.V.; investigation, S.A. and N.B.V.; resources, S.A. and N.B.V.; data curation, S.A. and N.B.V.; writing—original draft preparation, S.A. and N.B.V.; writing—review and editing, S.A. and N.B.V.; visualization, S.A. and N.B.V.; supervision, N.B.V.; project administration, S.A. and N.B.V.; funding acquisition, S.A. and N.B.V. All authors have read and agreed to the published version of the manuscript.

Funding

This research received no external funding.

Informed Consent Statement

Not applicable.

Data Availability Statement

Data are contained within the article.

Conflicts of Interest

The authors declare no conflict of interest.

References

- Akinyi, Grace L., and Recheal R. Oboko. 2020. Proposed self-regulation model for collaborative E-learning systems in Kenyan public universities. American Journal of Engineering and Applied Sciences 13: 37–48. [Google Scholar] [CrossRef][Green Version]

- Al-Emran, Mohammed, and Timothy Teo. 2020. Do knowledge acquisition and knowledge sharing affect e-learning adoption? An empirical study. Education and Information Technologies 25: 1983–98. [Google Scholar] [CrossRef]

- Al-Fraihat, Dimah, Mike Joy, Ra’Ed Masa’Deh, and Jane Sinclair. 2020. Evaluating E-learning systems success: An empirical study. Computers in Human Behavior 102: 67–86. [Google Scholar] [CrossRef]

- Ali, Sardar, Muhammad Aamir Uppal, and Stephen R. Gulliver. 2018. A conceptual framework highlighting e-learning implementation barriers. Information Technology & People 31: 156–80. [Google Scholar]

- Alkindi, Mohammed Z., Ali D. Hafiz, Ekhlas Abulibdeh, Ghassan Almurshidi, and Ahmed Abulibdeh. 2022. Moderating Effect of Faculty Status in the Relationship between Attitude, Perceived Usefulness, Perceived Ease of Use, Behavioral Intention, Subjective Norms on Mobile Learning Applications. Journal of Positive School Psychology 6: 5359–79. [Google Scholar]

- Al-Nimer, Munther, and Ghassan Alsheikh. 2021. Unleashing the role of e-learning in student engagement practices and accounting professional competencies. Journal of Applied Research in Higher Education 14: 829–51. [Google Scholar] [CrossRef]

- Bajaj, Niharika, Juan R. Carrión, Francesco Bellotti, Riccardo Berta, and Alessandro De Gloria. 2021. Analysis of Factors Affecting the Auditory Attention of Non-native Speakers in e-Learning Environments. Electronic Journal of e-Learning 19: 159–69. [Google Scholar] [CrossRef]

- Chen, Chih-Ming. 2009. Personalized E-learning system with self-regulated learning-assisted mechanisms for promoting learning performance. Expert Systems with Applications 36: 8816–29. [Google Scholar] [CrossRef]

- Connolly, Michael, Frances Browne, Gerard Regan, and Marian Ryder. 2020. Stakeholder perceptions of curriculum design, development and delivery for continuing e-learning for nurses. British Journal of Nursing 29: 1016–22. [Google Scholar] [CrossRef]

- Dangi, Mahesh Raj, and Mohamad Muda Saat. 2021. 21st Century Educational Technology Adoption in Accounting Education: Does Institutional Support Moderates Accounting Educators Acceptance Behaviour and Conscientiousness Trait towards Behavioural Intention? International Journal of Academic Research in Business and Social Sciences 11: 304–33. [Google Scholar]

- Eom, Sean B., and Nicholas J. Ashill. 2018. A system’s view of the e-learning success model. Decision Sciences Journal of Innovative Education 16: 42–76. [Google Scholar] [CrossRef]

- Eze, Samuel C., Victoria C. Chinedu-Eze, Chukwunonso K. Okike, and Adebowale O. Bello. 2020. Factors influencing the use of e-learning facilities by students in a private Higher Education Institution (HEI) in a developing economy. Humanities and Social Sciences Communications 7: 1–15. [Google Scholar] [CrossRef]

- Gentile, Teresa A., Riccardo Reina, Emanuele De Nito, Damjan Bizjak, and Patrizia Canonico. 2020. E-learning design and entrepreneurship in three European universities. International Journal of Entrepreneurial Behavior & Research 26: 1547–66. [Google Scholar]

- Grabinski, Karol, Malgorzata Kedzior, Joanna Krasodomska, and Agnieszka Herdan. 2020. Embedding E-learning in accounting modules: The educators’ perspective. Education Sciences 10: 97. [Google Scholar] [CrossRef]

- Heald, Sarah M. 2018. Exploring the Implementation of Synchronous Student Support Sessions and Student Retention in an Online Course. Ph.D. dissertation, The University of the Rockies, Denver, CO, USA. [Google Scholar]

- Krasodomska, Joanna, and Justyna Godawska. 2021. E-learning in accounting education: The influence of students’ characteristics on their engagement and performance. Accounting Education 30: 22–41. [Google Scholar] [CrossRef]

- Lee, Kyungmee, Zawacki-Richter Olaf, and Cefa Berrin Sari. 2022. A systematic literature review on technology in online doctoral education. Studies in Continuing Education, 1–27. [Google Scholar] [CrossRef]

- Letseka, Moeketsi. 2021. Stimulating ODL research at UNISA: Exploring the role and potential impact of the UNESCO Chair. Open Learning: The Journal of Open, Distance and e-Learning 36: 133–48. [Google Scholar] [CrossRef]

- Liu, Chen. 2020. The adoption of e-learning beyond MOOCs for higher education. International Journal of Accounting & Information Management 29: 217–27. [Google Scholar]

- Narh, Nartey, Richmond Boateng, Emmanuel Afful-Dadzie, and Akwasi Owusu. 2019. Platforms: Assessing the Challenges of E-Learning In Ghana. AMCIS 2019 Proceedings. 21. Available online: https://aisel.aisnet.org/amcis2019/is_education/is_education/21 (accessed on 14 October 2023).

- Nugroho, Mochamad Agung, Puspita Wahyu Dewanti, and Budi Tri Novitasari. 2018. The impact of perceived usefulness and perceived ease of use on student’s performance in mandatory e-learning use. Paper presented at 2018 International Conference on Applied Information Technology and Innovation (ICAITI), Padang, Indonesia, September 3–5; pp. 26–30. [Google Scholar]

- Palvia, Shailendra, Pradeep Aeron, Partha Gupta, Dillip Mahapatra, Rashmi Parida, Rachelle Rosner, and Shvetha Sindhi. 2018. Online education: Worldwide status, challenges, trends, and implications. Online Education: Worldwide Status, Challenges, Trends, and Implications 21: 233–41. [Google Scholar] [CrossRef]

- Pham, Linh, Yam B. Limbu, Trung Kien Bui, Hien T. Nguyen, and Hieu T. Pham. 2019. Does e-learning service quality influence e-learning student satisfaction and loyalty? Evidence from Vietnam. International Journal of Educational Technology in Higher Education 16: 7. [Google Scholar] [CrossRef]

- Sadeghi, Mohammad. 2019. A shift from classroom to distance learning: Advantages and limitations. International Journal of Research in English Education 4: 80–88. [Google Scholar] [CrossRef]

- Santhanam, Radhika, Sudha Sasidharan, and Jane Webster. 2008. Using self-regulatory learning to enhance e-learning-based information technology training. Information Systems Research 19: 26–47. [Google Scholar] [CrossRef]

- Sarker, Md. Faruque, Rafiul Al Mahmud, Md. Shahadat Islam, and Md. Kamrul Islam. 2019. Use of e-learning at higher educational institutions in Bangladesh: Opportunities and challenges. Journal of Applied Research in Higher Education 8: 457–64. [Google Scholar] [CrossRef]

- Söllner, Matthias, Peter Bitzer, Andreas Janson, and Jan Marco Leimeister. 2018. The process is king: Evaluating the performance of technology-mediated learning in vocational software training. Journal of Information Technology 33: 233–53. [Google Scholar] [CrossRef]

- Tahoon, Rania. 2021. Effects of Test Anxiety, Distance Education on General Anxiety and Life Satisfaction of University Students. Psycho-Educational Research Reviews 10: 107–17. [Google Scholar]

- Tere, Taufiq, Henki Bayu Seta, Achmad Nizad Hidayanto, and Zaenal Abidin. 2020. Variables affecting E-learning services quality in Indonesian higher education: Students’ perspectives. Journal of Information Technology Education. Research 19: 259. [Google Scholar]

- Tibaná-Herrera, Gloria, María Teresa Fernández-Bajón, and Félix de la Moya-Anegón. 2018. Global analysis of the E-learning scientific domain: A declining category? Scientometrics 114: 675–85. [Google Scholar] [CrossRef]

- Valencia-Arias, Alejandro, Santiago Chalela-Naffah, and Juan Bermúdez-Hernández. 2019. A proposed model of e-learning tools acceptance among university students in developing countries. Education and Information Technologies 24: 1057–71. [Google Scholar] [CrossRef]

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).