Empirical Analysis of Demand for Sukuk in Uzbekistan

Department of Finance, Prince Sultan University, Riyadh 12435, Saudi Arabia

Economies 2024, 12(8), 220; https://doi.org/10.3390/economies12080220

Submission received: 30 June 2024

/

Revised: 8 August 2024

/

Accepted: 20 August 2024

/

Published: 22 August 2024

(This article belongs to the Special Issue Role of Islamic Finance in Modern Economy)

Abstract

:Islamic finance (IF) holds significant potential for economic development and the enhancement of financial inclusion in Uzbekistan. Sukuk, as a key Islamic capital market instrument and Shari’ah-compliant investment alternative, plays an important role in this context. However, the demand for sukuk and its determinants are not well understood by policymakers and industry practitioners in Uzbekistan. This study aims to address this research gap by utilizing an ordinal logit model on primary data collected through a survey of 196 individuals from diverse demographic and professional backgrounds, with varying levels of IF and capital market knowledge and experience. The regression results indicate that factors such as prior investment experience, knowledge of sukuk, and a strong inclination toward Shari’ah-compliant investments positively influence an individual’s intent to buy sukuk. Conversely, we found that residents of Tashkent (the capital city) are less likely to invest in sukuk compared to residents of other regions in Uzbekistan or those residing abroad. Based on this study’s findings, several essential policy and practical recommendations are provided to relevant stakeholders.

1. Introduction

Uzbekistan is considered the fastest-growing Muslim-majority country among the Central Asian nations, accounting for almost half of the region’s population (Statistical Agency of Uzbekistan 2024; Worldometer 2024; Pew Research Center 2009). It is among middle–low-income countries, with an annual GDP per capita slightly over USD 2500, real economic growth of 6%, and inflation curbed at 8.8% as of 2023 (World Bank Group 2024a). The real GDP growth is expected to stay around 5.5% and 5.6% for 2024 and 2025, respectively, while inflation is expected to remain at about the same level for the next two years (Asian Development Bank 2024).

With a current population nearing 37 million, over 96 percent of whom are Muslim, Uzbekistan presents a significant emerging market with high demand for Islamic financial services (Abdullayev et al. 2023; Khusanov 2022; Nusrathujaev 2020; Imamnazarov 2020). With its current economic growth and financial market development trajectory, the country possesses great potential to become a financial hub, especially for Islamic finance (IF), in Central Asia (Botirova 2023; Nizomiddinov 2020; Associated Press of Pakistan 2024). The Islamic capital market (ICM) is particularly promising in Uzbekistan (Asadov et al. 2023, 2024), where an opening economy and new investment opportunities are being warmly received, especially among the younger population. However, this potential is under-researched, particularly from an empirical perspective, and needs closer scrutiny to understand the demand for Islamic capital markets clearly. This understanding will serve as empirical evidence to inform policymakers, attract potential investors, and provide further assurance to future security issuers.

Recent research has discovered the significance of sukuk issuance for the development of the Islamic capital market, emphasizing the enforced adherence of issuers to the moral and ethical principles of Shari’ah (Hassan et al. 2022). When examining the decision of governments on issuing sukuk versus conventional bonds, Boujlil et al. (2020) found that sovereign sukuk is predominantly issued by countries with strong economies, high credit ratings, developed financial markets, and sustainable financial positions. The issuance of Islamic securities has helped these countries further develop and diversify their financial markets. Similarly, another study explored the benefits of introducing retail sukuk alongside retail bonds by the government of emerging markets such as Indonesia (Danila et al. 2023). The study found that offering retail sukuk successfully expanded the investor base for individual investors and benefited them in terms of diversification. All of the information above demonstrates the importance of introducing new Islamic capital market instruments for emerging Muslim-majority countries, such as Uzbekistan.

Since IF began gaining momentum in Uzbekistan after the new government led by President Mirziyoyev came to power in late 2016, studies of the industry have been scarce in the country’s economic literature. With the new government initiating economic reforms and attempting to attract more foreign investments, the topics of financial inclusion and attracting Muslim investors from abroad to the prospective introduction and development of the IF industry have gained importance. As a major component of the industry and a vital element for attracting both local and foreign investment, Islamic capital markets play a crucial role. Unfortunately, despite renewed interest in IF and the government’s openness to introducing legal foundations for its development, progress has been slow (Asadov and Turaboev 2023; Asadov et al. 2023).

Several studies have found a positive impact of sukuk financing on the economic growth of both developing and developed countries that issue sukuk (Ledhem 2022; Echchabi et al. 2018). Nonetheless, it is also important to understand important factors that contributed to the sukuk market development and influenced the demand for security. A study by Smaoui and Khawaja (2017), covering 13 countries between 2001 and 2013 using the GMM procedure, found that a combination of institutional, financial, and structural factors affects the market significantly. Unfortunately, there has been no such study examining the factors influencing sukuk market development or determinants of demand for sukuk conducted for Central Asian countries. This lack of research could be the reason why the sukuk market was slow to take off in some of the countries in the region, such as Kazakhstan and Kyrgyzstan, despite having required legislation and financial regulations in place for several years.

Nonetheless, it is never too early or too late to study the potential of such ICM products and the factors influencing sukuk demand for emerging markets in Central Asia, such as Uzbekistan. Therefore, this study aims to empirically investigate the demand for sukuk in Uzbekistan using an ordinal logit regression model. Analysis of the survey data using the ordinal logit regression technique helped us study the factors directly influencing individuals’ demand for sukuk in the country. Among the explanatory variables, we found that factors such as having investment experience, knowledge of sukuk, and a greater inclination towards Shari’ah-compliant investments positively impact an individual’s intent to buy sukuk if offered in Uzbekistan. Conversely, we also found that residents of Tashkent (the capital city) are less likely to invest in sukuk, possibly due to the availability of other investment alternatives, compared to residents of other regions in Uzbekistan or those residing abroad.

The rest of this paper is organized as follows. The next section provides a brief literature review of recent developments in IF and capital markets in Uzbekistan. Section 3 explains the data and methods used in our analysis of the demand for sukuk in the country.

Section 4 presents the results obtained from the ordinal logit regression and margin plot analysis. The detailed interpretation of the findings, their relation to the existing literature, and practical implications are discussed in Section 5. Finally, Section 6 concludes the paper and provides essential policy recommendations.

2. Literature Review

Despite the recent increase in interest in Islamic finance (IF) in Uzbekistan, driven by the more favorable political environment established by the government that came into power in late 2016, the industry has some early history in the country. Uzbekistan’s first involvement in IF dates back to 2003. As the last Central Asian country to join the Islamic Development Bank (IsDB), Uzbekistan became a member in 2003 with a subscribed capital of 13.4 million Islamic dinars, accounting for a 0.03 percent share in the IsDB’s total capital (Khaki and Malik 2014).

Since becoming a member of the IsDB, Uzbekistan has received approximately USD 2.4 billion in financing. Most of this funding has been directed toward educational, health, agricultural, and electrical development and construction projects. To date, 103 projects have been implemented nationwide, with 49 completed and 54 still ongoing. During this period, the IsDB’s operations in Uzbekistan have been conducted through conventional banking lines based on three main contracts: ijarah, istisna’, and murabahah (Khasanov 2019).

Additionally, in 2004, the Islamic Corporation for the Development of the Private Sector (ICD), a private sector arm of the IsDB, approved Uzbekistan’s membership. From then until 2013, the ICD extended USD 133 million in financing to local banks in Uzbekistan. In 2013 alone, the ICD provided USD 13 million to the state-owned Xalq Banki for refinancing SME projects. Later, in 2021, during the annual meeting of IsDB members held in Uzbekistan’s capital, the ICD signed an agreement with four major banks—Kapitalbank, Trustbank, Orient Finance Bank, and InFinBank—to provide USD 40 million in financing to SMEs in Uzbekistan (ICD 2021).

Overall, from 2005 to the present, Uzbekistan has joined all the sub-organizations of the IsDB, including the ICD, ITFC (International Islamic Trade Finance Corporation), ISFD (Islamic Solidarity Fund for Development), and ICIEC (Islamic Corporation for the Insurance of Investment and Export Credit). However, the internal growth of IF has been slow, with only a few Islamic leasing (ijara) companies and government-level IF activities until recently (Asadov and Nurmukhamedov 2023).

A new wave of optimism emerged with the administration of President Mirziyoyev, who has actively promoted the integration of IF into the country’s financial system since 2017. The president mandated the inclusion of an IF development plan in the government’s strategic development document, with specific action plans outlined in his decree for the development of the IF industry. Despite these efforts to establish a legal and financial infrastructure for Islamic banking and finance, the results have been modest (Asadov and Nurmukhamedov 2023).

The development of IF in Uzbekistan, especially the examination of the current demand for IF products, is relatively scarce. One of the earlier studies in this area was produced by a joint effort of the United Nations Development Program (UNDP) in Uzbekistan, some government agencies, and researchers in 2020. The survey revealed that 30 percent of the population do not use conventional banks’ services due to religious reasons, and 61 percent of businesses and 75 percent of individuals were willing to use Islamic financial services if offered in Uzbekistan (Imamnazarov 2020). The same study also uncovered that 44.4% of commercial bank representatives believe that the introduction of sukuk would be the most effective IF instrument to introduce in the country due to it creating opportunities for the development of capital markets. Nonetheless, the study did not provide specific insights into the conclusions of commercial bank managers or the opinions of individuals about sukuk offerings.

Similarly, the findings of a survey conducted by Abdullayev et al. (2023) to assess the feasibility of introducing IF uncovered the existence of strong demand for the industry’s products in Uzbekistan. Their survey of 240 individuals showed that despite only 18.8% of respondents having used IF services previously, a stunning 86.3% of participants stated that they are very or somewhat likely to use those products if offered in Uzbekistan. Furthermore, 73% of participants believe that the IF industry could positively contribute to the economy of the country. Even though the study uncovers the existence of a strong demand for IF products in general and factors such as Shari’ah compliance and competitive pricing as most important for individuals’ demand for those products, it does not go into closer scrutiny of different sectors of the IF industry.

When it comes to the demand for an Islamic capital market (ICMs) in Uzbekistan, Asadov et al. (2024) studied the feasibility of introducing ICM products in Uzbekistan. The conducted survey of the general public and the interviews with IF and capital market experts confirmed the presence of significant demand and large potential for Islamic capital market products. Similar to the findings of previous studies by Imamnazarov (2020) and Abdullayev et al. (2023) for general IF products, the study also reveals that despite low IF awareness and an underdeveloped capital market, there is strong demand for Islamic capital market products in the country (Asadov et al. 2024). Even though the study narrows down its focus on the ICM segment, it does not examine factors influencing the demand for ICM products in Uzbekistan. Rather, it looks into the prospects and challenges of ICM in the country.

When it comes to hurdles facing the IF industry in Uzbekistan, the academic literature and government officials mention several factors. Some Uzbek government officials cite a lack of IF literacy as the main obstacle to the introduction of IF in the country (Daryo 2021; Kun.uz 2021), and some surveys support these findings (Abdullayev et al. 2023). Nevertheless, some other studies point to the lack of legal foundations, financial infrastructure, and experienced specialists as the main hindrances preventing the industry’s development (Asadov and Turaboev 2023; Imamnazarov 2020). The main barrier preventing the introduction of Islamic capital market products, such as sukuk and Islamic indices, in Uzbekistan is, again, the absence of specific legal frameworks (Asadov et al. 2023).

In terms of accessing international capital markets, Uzbekistan has made some progress recently. The country has already issued Eurobonds, SDG-linked and green bonds, local currency bonds, and conventional bonds. Hence, some market experts believe the issuance of Islamic capital market instruments, such as sukuk, should follow naturally (Jivraj 2024). Sukuk is considered a hybrid instrument that holds a position between bond and equity. It is a Shari’ah-compliant risk-sharing instrument that provides part of the company’s earnings as a reward for the sukuk-holder (unlike the fixed interest return of a conventional bond), but at the same time, it does not dilute the share of the current owners (avoiding the disadvantage of the equity issuance) (Bacha and Mirakhor 2013). These favorable features of sukuk provide a perfect combination for both governments and corporations of developing countries as an external financing alternative, allowing them to avoid the burden of debt while still maintaining their ownership stakes in the entity.

When it comes to the development of sukuk, it first started in Southeast Asia, particularly in Malaysia. The first corporate sukuk was issued in 1990 by Shell MDS Sdn Bhd of Malaysia for the amount of MYR 125 million (USD 33 million), and the first global sovereign sukuk was issued by the Government of Malaysia in 2002 for the amount of USD 600 million (Ahmad and Radzi 2011; Laldin 2008). As of 2022, Malaysia leads the global sukuk market with a total outstanding sukuk value of USD 300 billion, followed by Saudi Arabia and Indonesia, with total sukuk outstanding values of USD 222 billion and USD 95 billion, respectively (ICD and LSEG 2023). Indonesia also takes third place and shows a clear lead in the Southeast Asian region in the global sukuk market. When examining the impact of sukuk financing on the economic growth of three Southeast Asian countries (Malaysia, Indonesia, and Brunei Darussalam) using data from Q4 2013 to Q3 2019, Ledhem (2022) found it to be significant. This indicates the important role of sukuk financing for Muslim-majority countries of the region.

Nevertheless, Malaysia and Indonesia represent only two of the top 10 major sukuk-issuing countries as of 2023. In terms of the number of countries, the Gulf Cooperation Council (GCC) leads as a region. All of the GCC countries except for Oman make it to the top 10 list, with a total value of sukuk outstanding for the region standing at USD 330 billion. Other regions have a much smaller share of the sukuk market, with other Asian regions (including Central Asia) having less than USD 1 billion in total outstanding sukuk value (ICD and LSEG 2023). As for the impact on the economy of the issuing country, a study by Echchabi et al. (2016) examined the impact of sukuk on the economy of 17 major issuing countries covering not only Southeast Asia or the GCC but also East and Central Asia, Europe, and Africa, and found some interesting results. Their findings uncovered the significant influence of sukuk issuance on the gross domestic product (GDP) and gross capital formation (GDF) of those countries when all of them were pooled together. However, no such impact on the economy of a country was found for the GCC members.

With regards to the experience of Central Asian countries besides Uzbekistan on sukuk, two of its neighbors already have both the legal basis and practical experience with the issuance of Islamic bonds. Kazakhstan established legal footing for sukuk issuance in 2010 and placed its first sovereign sukuk in 2012. A 5-year Murabaha sukuk worth MYR 240 million (around USD 75 million) was issued by the Development Bank of Kazakhstan with the assistance of Malaysian investment banks and was subscribed to mostly by Malaysian investors and the pension fund of Kazakhstan (Nagimova 2021). Since then, Kazakhstan has announced a few more intentions to issue a second tranche of sovereign sukuk, but no such issuance has taken place as of today.

The second country that long planned sukuk issuance is Kyrgyzstan, which made amendments to the law ‘On the Securities Market’ in 2016 to accommodate sukuk issuance (Nagimova 2021). However, despite numerous previous plans, the country was only able to issue its first corporate sukuk in April of 2023 by the Hong Kong-based global commodities trading company, Intercascade Group, for the amount of KGS 750 million (USD 8.55 million). The security was set up as a sukuk al-Mudaraba based on a profit-sharing arrangement between the issuer and sukuk-holder (IFN 2023).

From the examples of these two Central Asian countries that adopted legislation to support and had firsthand experience with the issuance of sukuk, we can learn some important lessons. If a country issues sukuk prematurely, as possibly happened in Kazakhstan, or passes a law or makes amendments to legislation with no real intent from the government or corporate entities, as was the case with Kyrgyzstan, both investors and issuers may become disheartened. Therefore, it is better to evaluate the existence of true demand for sukuk in the country initially and understand the triggers that influence the demand to harbor the population’s intent to invest in Islamic bonds. When it comes to factors influencing sukuk market development, a study covering 13 countries between 2001 and 2013 by Smaoui and Khawaja (2017) using the GMM procedure found that a combination of institutional, financial, and structural factors significantly affects the market. The factors that positively affected sukuk market development are a lower level of corruption, an attractive investment profile, a larger proportion of Muslims in the population, and a large economy. On the other hand, a larger interest spread adversely impacted the size of the sukuk market.

As for the Central Asian countries, especially for Uzbekistan, there is no study examining the factors influencing sukuk market development or the determinants of demand for sukuk. Therefore, while Uzbekistan’s government ponders passing sukuk legislation and both the government and corporations are considering sukuk issuance, it becomes vital to study the demand for such Islamic capital market products among the population. Though some studies have conducted legal and market analyses for a general demand for IF products in Uzbekistan, the empirical analysis of demand for sukuk and the factors influencing its demand has not been studied. Hence, it is apparent that there is a research gap to empirically investigate such demand in the country. Since such a study is crucial from both policymaking and practical perspectives, this work aims to address the given research gap. Specifically, we will scrutinize the factors influencing the demand for sukuk in Uzbekistan.

3. Methodology

To achieve the main objective of this study—analyzing the demand for sukuk in Uzbekistan and the factors influencing this demand—a quantitative analysis was employed. Specifically, ordinal logit regression was utilized on primary data collected through a survey conducted by the authors in April 2023. During the survey, respondents were asked several questions related to their demographics, industry of employment, income level, knowledge of and experience with investing in capital markets, knowledge of and preference towards Islamic capital market products, and, finally, their willingness to buy sukuk if offered in Uzbekistan. The last variable was taken as the dependent variable for this study, and the respondents were provided several options following an ordinal structure to choose from for this question. Since the dependent variable follows ordinal categories (converted to values), ordinary least squares (OLS) or other linear regression models used for continuous dependent variables are not suitable. Therefore, the ordered logit model is the most fitting regression model for the given characteristics of the dependent variable.

3.1. Ordered Logit Regression

The ordered (ordinal) logit model is similar to the binary logistic (logit) regression model, which forces the output of the regression to be either 0 or 1 (negative or positive outcome). More specifically, binary logit regression estimates the probability of the dependent variable having a positive outcome (value of 1) for a given combination of independent variables. However, if there are more than two possible outcomes for the dependent variable (y), regular (binary) logit regression cannot be applied, and other alternatives, such as ordered (ordinal) or multinomial logit regressions, should be selected. The multinomial logit model is applicable if there is no defined order for possible outcome categories of the dependent variable, and if such an ordering of dependent variable outcomes exists, then the ordinal logit model is preferable. The ordinal logit model is particularly useful for dealing with ordinal dependent variables, where respondents select only one category among given ordinal values. These categories are termed alternatives and are identified as , following a particular order, with higher values representing higher levels, although the differences in value are not necessarily equal.

An index model for a single latent variable is defined by the following equation (Long and Freese 2014):

where and . denote the sample size, and is the total number of alternatives of the dependent variable. Furthermore, , is a column vector of explanatory variables, is a constant term, is a parameter vector that needs to be estimated, and is the error term of logistic distribution. represents an unknown parameter’s threshold parameters, which are estimated along with . The probability that observation i will select alternative is as follows:

where F represents the standard logistic cumulative distribution function.

Lastly, the marginal effect resulting from an independent variable increase in for the outcome is given by the following equation (Mallick 2009):

3.2. Data

A survey was conducted in April 2023 with the objective of studying the demand for sukuk in Uzbekistan. The questionnaire included several questions to identify the respondents’ personal, employment, residential, and financial characteristics, as well as their experience with capital markets and knowledge of conventional and Islamic capital market products. Additionally, information about their attitudes towards Shari’ah-compliant investments and willingness to invest in sukuk was also obtained.

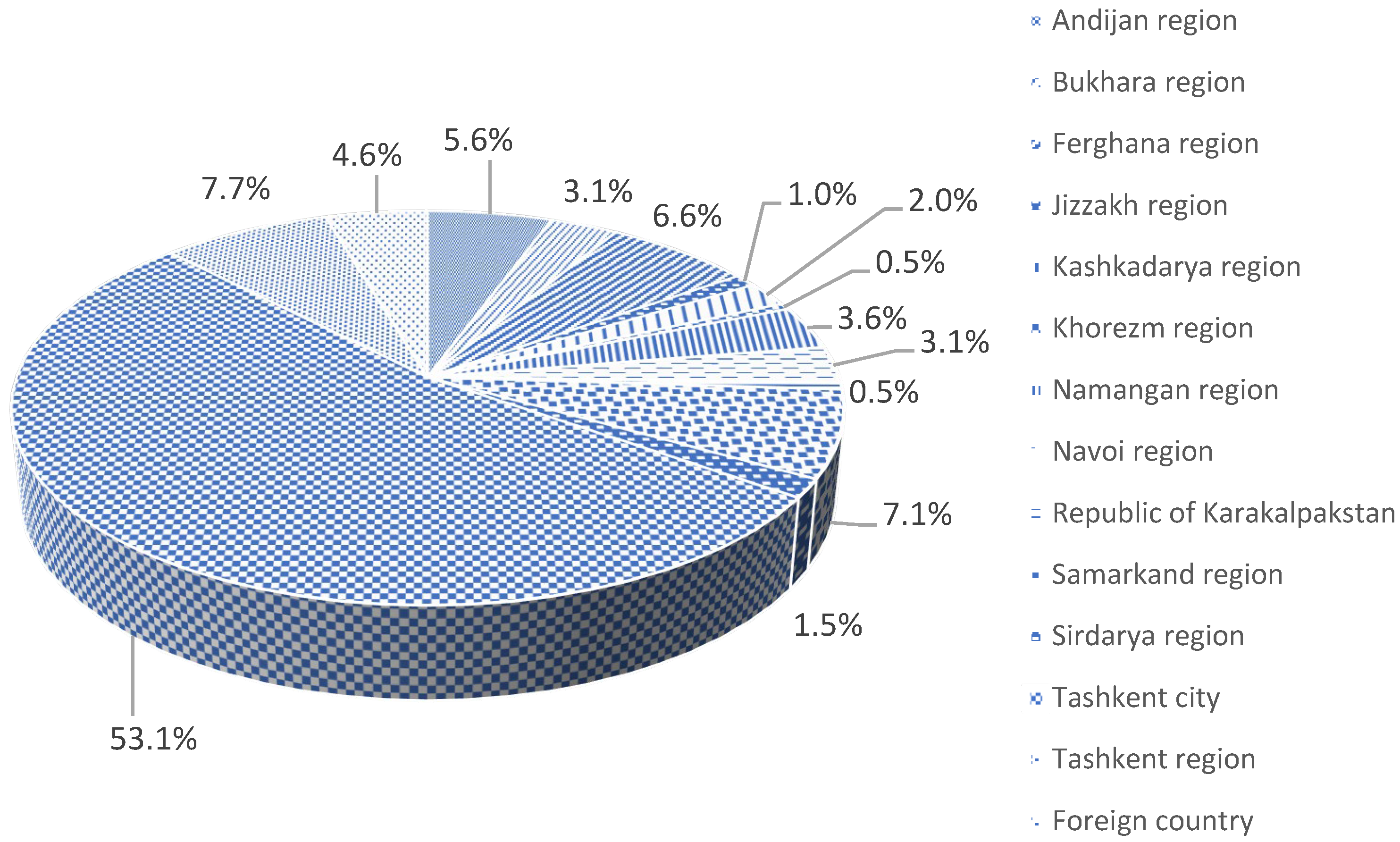

The online survey was distributed via professional contacts, personal networks, and multiple social media channels to ensure wide representation. In April of 2023, we received answers from 196 respondents coming from diverse demographic and professional backgrounds and levels of Islamic finance (IF) and capital markets knowledge and experience1. The respondents’ distribution by place of residence is shown in Figure 1 below.

The summary of other main characteristics of the respondents and their distribution according to their response to the main question of the survey regarding their intent to “buy sukuk if offered in Uzbekistan” is provided in Table 1 below. The respondents’ intent to buy sukuk is divided into four ordinal scales: “Will not buy” if the respondent indicated no interest in buying sukuk if offered in Uzbekistan, “Maybe will buy” if the respondent stated that they may buy depending on its structure or return, “Probably will buy” if the respondent is most likely to buy sukuk or will buy it if offered in smaller denominations, and “Definitely will buy” if the respondent stated they would definitely buy sukuk if offered in Uzbekistan.

As shown in the last row of the table, the largest portion of respondents stated that they “Maybe will buy” (40.31%), followed by those who answered, “Probably will buy” (36.22%) if offered in Uzbekistan. A relatively smaller fraction responded that they “Definitely will buy” (18.37%), and a very small proportion of respondents answered that they “Will not buy” (5.10%) sukuk. This indicates that there is a significantly large demand (94.9% of respondents) for sukuk among the population in Uzbekistan, with the largest portion of respondents (76.53%) showing conditional intent to buy sukuk if offered.

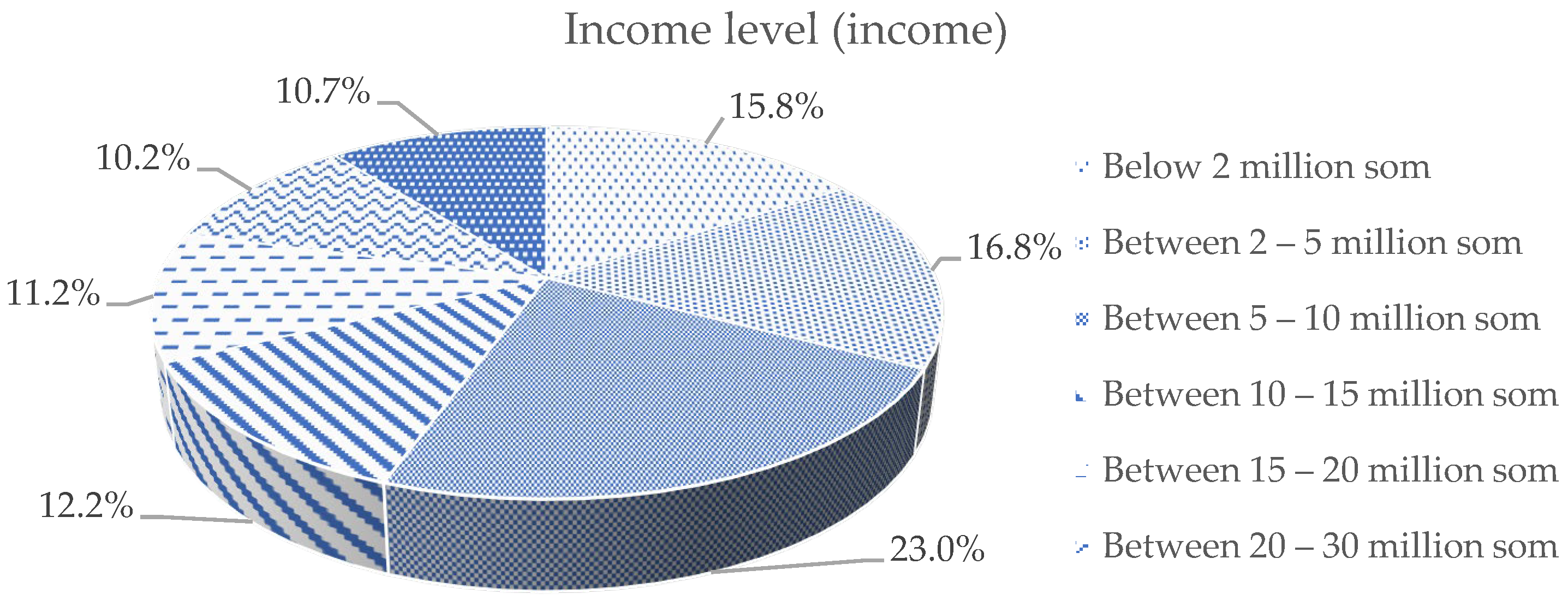

However, some ordinal variables collected during the survey could also influence the respondents’ intent to buy sukuk if offered in Uzbekistan. The summary table listing and showing the distribution of these variables with respect to the “Intent to buy sukuk if offered in Uzbekistan” variable is provided in Table A1 in Appendix A. Furthermore, Figure 2 and Figure 3 belove provide a general idea about the distribution of the respondents according to continuous variables, i.e., age and income of the respondents, respectively.

Overall, the sample of respondents seems to be representative of the general population and those who are actively involved in economic and investment decisions in a typical family in Uzbekistan. The population of Uzbekistan is relatively young, with the median age being 27 years as of 2023 (Worldometer 2023). Considering we only invited adults to participate in the survey, our sample median age of 35 years (see Table 2) seems to be representative of the economically active part of the population. The median salary in Uzbekistan is equal to UZS 4.55 million, with the highest level of income observed in Tashkent city being UZS 7.45 million in 2023 (The Tashkent Times 2024). Since the majority of respondents in our sample come from Tashkent city (see Figure 1) and includes predominantly males (see Table 1), who earn 34% more income compared to females (World Bank Group 2024b), the sample median income of UZS 7.5 million (see Table 2) also seems to be representative. Overall, most of the other characteristics of the sample are in line with those of the general economically active population of Uzbekistan, which is also typical for most developing countries with a Muslim majority.2

Nonetheless, the survey method is not without its limitations. Firstly, it is difficult to obtain a large enough sample size to represent the entire population of a country. Secondly, it may have potential biases, such as capturing more tech-savvy individuals compared to those not familiar with the usage of information technology. Finally, it is very difficult to generalize the findings obtained from survey data to the entire population of Uzbekistan. Despite all of the limitations above, we believe that our sample is representative enough to provide the reader with some general findings and provide a clearer picture of the potential demand for sukuk in Uzbekistan.

4. Empirical Results

4.1. Descriptive Statistics of Variables and Visual Analysis of Demand for Waqf-Based IMF

Understanding the demand for sukuk in Uzbekistan involves examining the factors influencing people’s responses. From the summary tables in Section 3 (Table 1), we can observe the impact of factors such as gender and marital status on the respondents’ decisions. However, the causality is not clear from mere summary observations. Additionally, several continuous and ordinal variables collected during the survey, such as the respondents’ age, monthly income, knowledge of capital markets, sukuk, and Islamic stocks, investment experience, and attitudes towards Shari’ah compliance with stocks, may also contribute to their decision-making. Descriptive statistics for these variables are provided in Table 2, and their correlations are shown in Table 3 below.

The pairwise correlations presented in Table 3 provide some insights about the relationship between the given variables. For brevity, we only focus on those correlations that are significant at a 5% level, mainly between dependent variables and independent variables. There is no significant correlation between the intent to buy sukuk (buysuk) and the age or income of the individual. However, the intent to buy sukuk shows a positive and significant correlation with a person’s capital market knowledge (cmknow), investment experience (invexpr), knowledge of sukuk (sukknow), and knowledge of Islamic stocks (ismstkknow), as well as their attitude towards Shari’ah-compliant investment (stkshrcomp). Among other relationships, we also notice a moderately strong positive (greater than +0.5) and significant correlation between investment experience (invexpr) and capital market knowledge (cmknow), and between sukuk knowledge (sukknow) and Islamic stock knowledge (ismstkknow). These last two relationships indicate a strong overlap between these skill pairs.

We adopted a broad-to-narrow approach for developing our model, starting by including all the relevant independent variables to predict the outcome of the main dependent variable (buysuk) using ordinal logistic regression. As shown in Table 4, the predictor variables included are the age of a person (age), gender dummy (femdum), married dummy (mardum), Tashkent city resident dummy (tashdum), dummy for employees in the education (edudum) and banking and finance industries (findum), monthly income (income) and monthly saving (saving), knowledge of capital markets (cmknow), investment experience (invexpr), knowledge of sukuk (sukknow) and Islamic stocks (ismstkknow), and respondents’ attitudes towards Shari’ah compliance of stocks (stkshrcomp).

Table 4 provides results for three different models (1)–(3) of the intent to buy sukuk (buysuk), following a broad-to-narrow method. In the broad model (Model 1), some variables were found to be insignificant and were removed to develop alternative models (2) and (3), also presented in Table 4. Specifically, age, married dummy (mardum), education industry dummy (edudum), income, capital markets knowledge (cmknow), and knowledge about Islamic stocks (ismstkknow) were found to be insignificant and omitted in further models. Variables with p-values over 0.5 were dropped in Model (2) development.

In Model (2), all the variables were statistically significant at least at the 10% level, except for the female (femdum) and finance industry (findum) dummies. Comparing Model (1) and Model (2) using the Bayesian information criterion (BIC), Model (2) was shown to be a better fit, leading us to focus on it for further analysis. We dropped all the variables not significant in Model (2), except for some categorical variables where some categories had insignificant coefficients (i.e., invexpr and sukknow), as these were focus variables with mostly significant categories.

Model (3), developed based on these criteria, showed almost all the variables to be statistically significant at least at the 10% level, except for some categories of two ordinal variables (invexpr and sukknow), as seen in Model (2). However, compared to Model (2), the Bayesian information criterion (BIC) indicated that Model (3) was the best fit. Thus, we focused on this model for our analysis.

As discussed, all the variables in the final model are significant except for one category each of invexpr and sukknow. For example, for a one-unit increase in tashdum (i.e., going from 0 to 1), we expect a 0.758 decrease in the log odds of being in a higher level of buysuk, assuming all the other variables are unchanged. Alternatively, if investment experience increases by one level from 1 to 2, we expect a 0.897 increase in the log odds of being at a higher level of buysuk. The interpretation of other coefficients follows a similar manner. The cut points indicate three dividing points of the latent variable, making the four groups observed in the data.

Compared to the coefficient values, the odds ratios are easier to interpret. From Table 5 (Model 3), we can conclude that the odds ratio of tashdum indicates Tashkent city residents are 53% less likely to be in a higher category of intent to buy sukuk compared to others. Similarly, a person with investment experience at level 2 is 2.45 times more likely to intend to buy sukuk compared to someone with investment experience at level 1. Overall, the Model (3) outcomes show that except for the Tashkent city dummy (tashdum), increases in the other variables (invexpr, sukknow, and stkshrcomp) positively impact the individuals’ intent to buy sukuk if offered in Uzbekistan. Models (1) and (2) also show that variables such as age, gender, marital status, employment in education or financial industries, and knowledge of capital markets or Islamic stocks do not significantly impact individuals’ willingness to buy sukuk (See Table 4).

To ensure the robustness of the finding for Model (3), in line with some previous studies of ordinal response models (Ananth and Kleinbaum 1997), a simple sensitivity analysis of the model thresholds was conducted by subtracting and adding one standard error for each coefficient of the cut point estimates presented in Table 5. As expected for the ordinal logit model, all the cut points were strictly positive and progressively increased from a lower to a higher threshold. As seen in the sensitivity analysis (the last two columns of Table 5), there is no overlap between the lower and upper bounds of the given cut points, except for a small overlap between the upper bound of cut point 2 (6.008) and the lower bound of cut point 3 (5.841). These findings indicate the general robustness of Model (3)’s results to the sensitivity analysis of the estimated thresholds.

To ensure the assumptions of proportional odds underlying the ordered logistic regression hold (i.e., the relationship between all the pairs of groups is the same), we conducted a likelihood ratio test and the Brant test. Insignificant results from these tests indicate that the proportional odds assumption is not violated. The likelihood ratio test run using the model command in Stata produced Chi-squared test results. The likelihood-ratio chi-squared test with 8 degrees of freedom is 10.88 with a p-value of 0.2084. The Brant test results are provided in Table 6. Both test results confirm that the null hypothesis of proportional odds is not violated, indicating the results obtained in the ordinal logit regression are valid.

4.2. Margin Plot Analysis

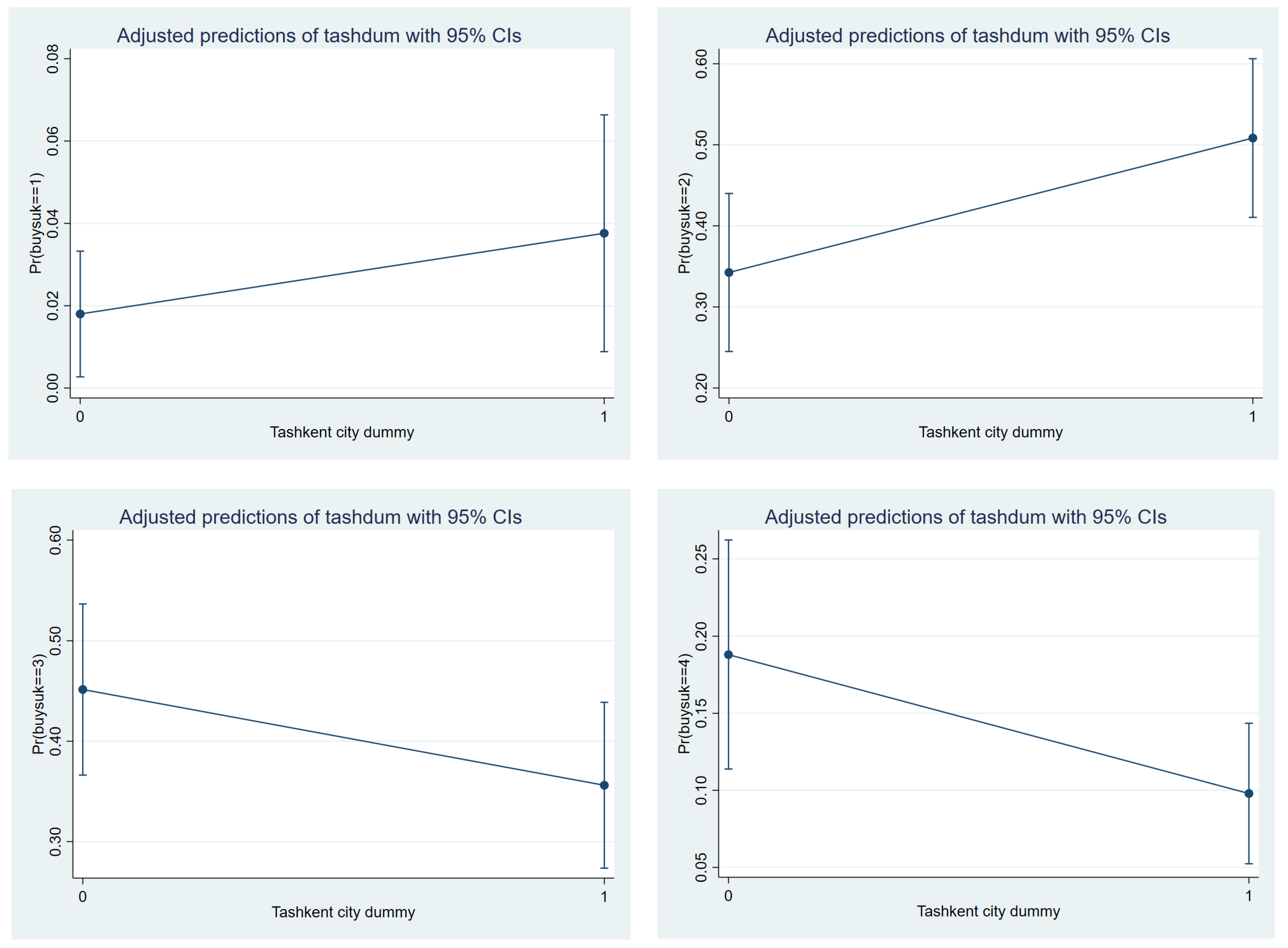

Margin plots provide useful information regarding the predicted probability of dependent variable outcomes. When examining the margin plots of the Tashkent city dummy (tashdum) in Figure 4, a significant difference between Tashkent city and other regions’ residents can be observed regarding their intent to buy sukuk. Specifically, for outcome 1, the mean predicted probability of a Tashkent city resident is about 20% higher than that of other regions’ residents for the intent not to buy sukuk. Conversely, for outcome 4, Tashkent city residents are 10% less likely to buy sukuk.

Margin plots of investment experience and knowledge influencing individuals’ intent to buy sukuk, reflected in Figure 5, clearly indicate a positive influence of investment experience on individuals’ probability of buying sukuk. One thing is evident from these margin plots: individuals with more experience are less likely to be unwilling or hesitant to buy sukuk (outcomes 1 and 2) and more likely to be interested or determined to buy sukuk (outcomes 3 and 4). This highlights the importance of investment experience, knowledge, and willingness in a person’s decision to invest in sukuk.

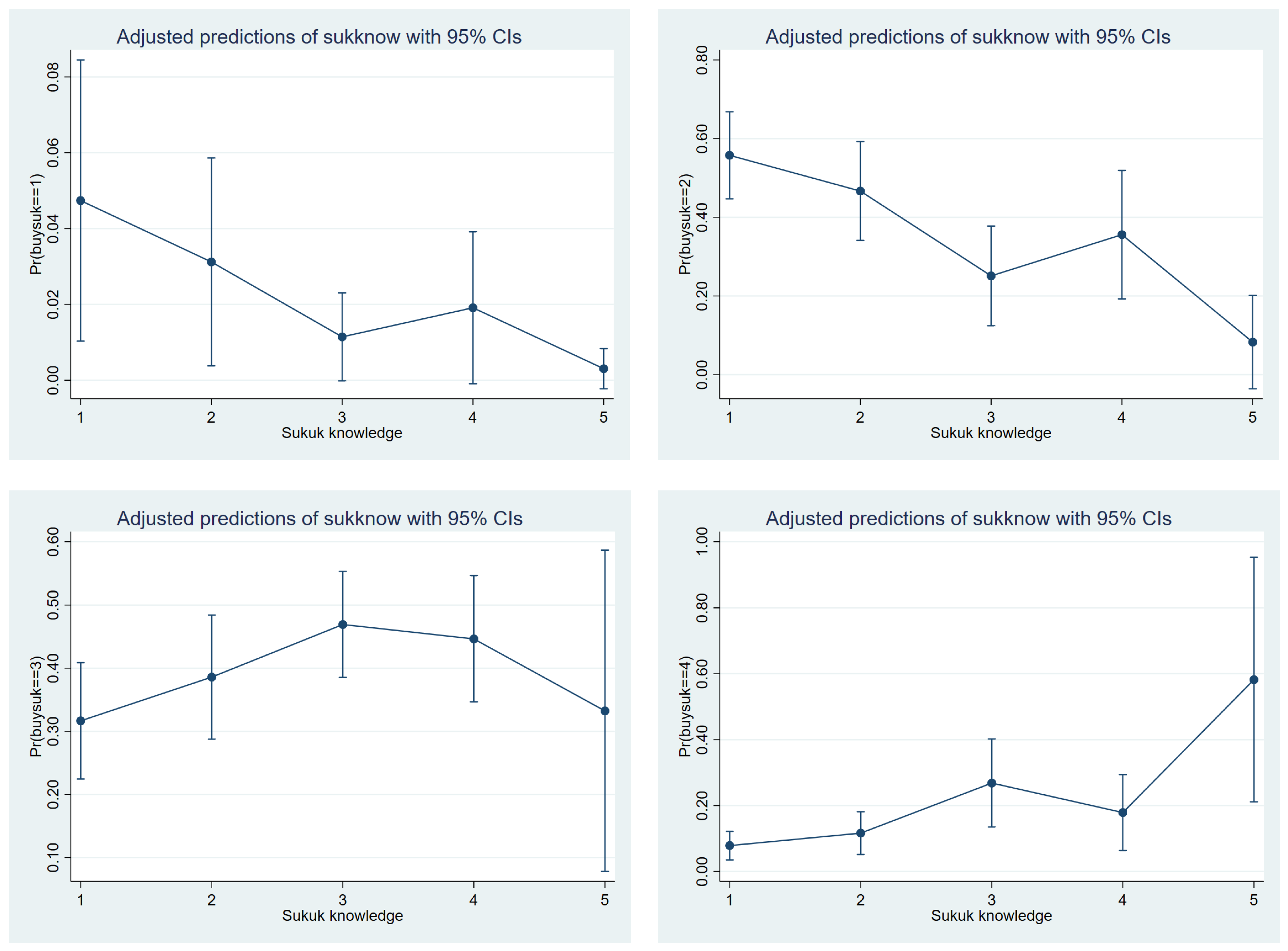

In line with our interpretation of investment experience influencing individuals’ intent to buy sukuk (Figure 5), we observe a similar pattern of influence from sukuk knowledge on individuals’ intent to buy sukuk. Here, too, individuals with more knowledge about sukuk are less likely to be unwilling or hesitant to buy sukuk (outcomes 1 and 2) and more likely to be interested or determined to buy sukuk (outcomes 3 and 4) (See Figure 6). This demonstrates the positive impact of sukuk knowledge on an individual’s intention to buy sukuk.

Finally, the impact of an individual’s attitude towards stock Shari’ah compliance on the intent to buy sukuk appears threefold (Figure 7). First, those least concerned about Shari’ah compliance with stocks are the most unwilling to buy sukuk (outcome 1). Next, individuals in the middle category regarding their attitude towards stock Shari’ah compliance (not very important, relatively important, and important) have the highest probability of being hesitant to buy sukuk (outcome 2). Lastly, individuals who believe that stock Shari’ah compliance is very important are the most likely or determined to buy sukuk (outcomes 3 and 4), followed by the middle category. Individuals least concerned about stock Shari’ah compliance are also least likely to intend to buy sukuk (See Figure 7).

5. Discussion

The findings of the ordinal logit regression provided in the previous section offer some interesting implications that require detailed explanation. Model (1)’s results in Table 4 indicate that demographic factors such as age, gender (femdum), marital status (mardum), industry of employment (edudum and findum), and income level do not have any significant impact on an individual’s intent to purchase sukuk (buysuk). This provides some insight into the overall picture. It seems that these factors are secondary compared to other more directly related and significant factors, such as a person’s investment experience (invexpr) or knowledge of the sukuk concept (sukknow).

Nevertheless, the impact of an individual’s place of residence, especially the finding that Tashkent city residents (tashdum) are 53.1% less likely to be in higher categories of intent to buy sukuk compared to residents of other regions, is striking. This finding can be partially explained by the theory of availability bias, a type of cognitive bias prompting individuals to make fast but sometimes incorrect investment decisions (Kahneman and Tversky 2013). This is typically true for investment decisions of investors in developing countries with low levels of financial literacy, similar to Uzbekistan. For instance, Salman et al. (2021) found that most individual investors in Pakistan are influenced by availability bias when making their investment decisions at the Pakistan Stock Exchange. Furthermore, Sachan and Chugan (2020) found that a relatively larger portion of rural investors are affected by availability bias compared to urban ones when making investment decisions in the Gujarat state of India.

In the case of Uzbekistan, Tashkent city residents, living in the business capital of the country, have more experience and awareness about investing compared to residents of other regions in the country. Therefore, even if Islamic investment alternatives may resonate with positive feelings for both types of residents, Tashkent city residents are likely to be less inclined to make a rush decision to invest in sukuk without any reservations compared to residents of other regions.

The impact of investment experience (invexpr) on an individual’s intent to buy sukuk (buysuk) is found to be positive for all the categories except for the second one. This finding aligns with previous studies on capital market investment decisions of retail investors. Cohen and Kudryavtsev (2012) conducted a survey among MBA students to learn their behavior in terms of investment decisions and loan taking. Their findings reveal that the respondents’ decisions to invest in stocks were influenced by their experience in the capital market and knowledge of and expectations about a particular market index’s performance. The decision to invest in conventional bonds was influenced by individuals’ expectations regarding interest rate changes, as well as their capital market experience.

Our findings related to the positive impact of investment experience on the sukuk purchase decision also align with Krische (2019), who indicated the significant influence of past investment experience in prompting potential investors to scrutinize financial reports of prospective investments before making decisions. Krische’s (2019) study also found that the financial literacy of an investor fosters the role of proper financial reporting on investment-related decisions. This further supports our result showing the positive effect of sukuk knowledge (sukknow) on an individual’s intent to buy sukuk (buysuk). The positive influence of financial literacy on individuals’ decisions to invest in capital market products has been similarly discovered in several other papers (Van Rooij et al. 2011; Sivaramakrishnan et al. 2017). All of the information above indicates that the obtained results related to the impact of sukknow on buysuk are supportive of previous studies on investment decisions, even for conventional capital market investments.

As for the impact of Islamic finance (IF) literacy on Islamic capital market (ICM) investment in the context of a Muslim-majority country (i.e., Indonesia), the findings of Yusfiarto et al. (2023) lend further support to our findings. Their study outcomes show that IF literacy, as well as attitudes and perceived behavioral control, have a significant positive impact on individuals’ intent to invest in ICM products. This supports our finding related to the positive impact of sukuk knowledge (sukknow) on a person’s intent to buy sukuk and also aligns with another finding of our study showing the positive contribution of an individual’s attitude towards Shari’ah-compliant investments (stkshrcomp) on the personal intent to purchase sukuk.

The impact of an individual’s attitude towards Shari’ah-compliant investments (stkshrcomp) on the person’s intent to buy sukuk (buysuk) seems to be the most significant and strongest positive factor influencing the intent to buy sukuk in our model. As can be seen in Table 5, all the coefficients of stkshrcomp are large in magnitude (the minimum being 3.663) and significant at least at the 5% level. Another study of Indonesian investors by Indriani et al. (2020) that explores the behavior of academicians toward ICM investment also arrived at a similar conclusion. Their study found that religious motivation is the most influential factor on an individual’s decision to invest in ICM products. Furthermore, their results indicate that a person’s level of religiosity, as well as awareness of and knowledge about ICM significantly impacted the individual’s attitude towards investing in ICM.

Finally, it is also important to comment on two independent variables that were originally included in Model (1) but were eventually dropped in Model (3) due to their coefficients being mostly insignificant (See Table 4). They are knowledge of capital markets (cmknow) and Islamic stocks (ismstkknow), which were initially believed to be important factors influencing an individual’s intent to invest in sukuk (buysuk). There are two possible explanations for the lack of significant impact of these variables on the decision to buy sukuk. First, both variables have moderate to strong positive and significant correlations with two other variables included in the final model. The correlation between cmknow and investment experience (invexpr) is positive at 0.5440, while the correlation between ismstkknow and sukuk knowledge (sukknow) is positive at 0.7887, both significant at the 5% level (See Table 3). Therefore, the initially tested Model (1) must have suffered from model specification bias, which was corrected when each of the strongly correlated explanatory variables was excluded in Model (3). Secondly, the relation of cmknow and ismstkknow with the dependent variable (buysuk) must be considered. Since the intent to buy sukuk (buysuk) is more likely to be influenced by capital market experience rather than theoretical knowledge of capital markets, and more by an individual’s knowledge of sukuk rather than that of Islamic stocks, these two variables should not have a significant impact. In a sense, the first and the second reasons are interrelated, and the combination of both can also be the true reason for the insignificance of coefficients for variables cmknow and ismstkknow.

6. Conclusions

6.1. Summary of Findings

In this study, we analyzed the potential demand for sukuk if offered in Uzbekistan using primary data collected through a survey conducted in April 2023. The initial scrutiny of the data and the results of the empirical examination through the ordinal logit model reveal some interesting implications. Firstly, the data show that 94.9% of the respondents demonstrate either conditional or unconditional intent to buy sukuk if offered in Uzbekistan. The majority of respondents indicated that they may or probably will buy sukuk, with only 18.4% stating their unconditional intent to buy sukuk. Finally, only a small fraction (5.1%) indicated that they do not intend to buy sukuk if offered in the country.

The outcomes of the ordinal logit model reveal that among the explanatory variables, only the Tashkent (capital) city dummy, investment experience, knowledge of sukuk, and attitude towards Shari’ah-compliant stocks significantly impact an individual’s intent to buy sukuk if offered in Uzbekistan. Specifically, the results show that having more investment experience, possessing knowledge of sukuk, and having a stronger inclination towards Shari’ah-compliant stocks positively impact an individual’s intent to buy sukuk. Conversely, residents of Tashkent are less likely to invest in sukuk (likely due to the availability of other investment alternatives) compared to residents of other regions in Uzbekistan or those residing abroad. Interestingly, the findings indicate that neither knowledge of capital markets nor Islamic stocks plays a significant role in an individual’s intent to invest in sukuk if offered in Uzbekistan. This challenges the claims made by some government officials in Uzbekistan regarding lack of Islamic finance (IF) literacy as a hindrance to the introduction of the industry in the country.

Nevertheless, knowledge of sukuk and experience in investing in capital markets are major determinants of individual demand for sukuk. Therefore, it can be concluded that it is not the general knowledge of the IF industry or capital markets that is important but specific knowledge of the product being offered and some exposure to investing. However, even more important is a person’s attitude towards a product being in line with their personal and religious beliefs, which plays a major role compared to general knowledge of that product category. Finally, the findings also indicate that none of the demographic and personal characteristics of individuals, except for their place of residence, influences their intent to invest in sukuk if offered in Uzbekistan.

6.2. Policy Recommendations

The findings of this study show a high demand for sukuk in Uzbekistan and highlight key factors influencing that demand. The results also provide essential policy recommendations that can assist industry practitioners and policymakers.

- ▪

- Firstly, as previous studies found, it is important to provide a favorable legal infrastructure for the issuance of sukuk by making necessary changes to the capital market regulations in Uzbekistan (Asadov et al. 2023, 2024). These changes should make the investment and issuance of sukuk legal in the country.

- ▪

- Reflecting the high demand for sukuk among the population, the government and businesses should seriously consider issuing Islamic securities. Once the necessary legislative changes are made, more sukuk can be issued for both local and international investors.

- ▪

- Practitioners should focus on specific segments of Uzbekistan’s population that show the highest potential to invest in sukuk. These include residents of regions other than the capital city, individuals with some investing experience and knowledge of sukuk, and those with a strong preference for Shari’ah-compliant investments.

- ▪

- Considering the importance of knowledge of sukuk and investing experience, both issuers of sukuk and government organizations should focus on disseminating knowledge about sukuk among the public. Additionally, promoting investment experience through mobile apps or online simulations would also enhance demand for sukuk in Uzbekistan.

These recommendations aim to support the growth and acceptance of sukuk in Uzbekistan, promoting a robust market for IF products in the country.

6.3. Limitations of the Study and Avenues for Future Research

This study provides important findings relating to factors influencing the potential demand for sukuk in Uzbekistan and offers several vital policies and practical recommendations based on these findings. Nevertheless, it is not without its limitations and cannot be considered a comprehensive analysis of Islamic capital market (ICM) opportunities in Uzbekistan.

Firstly, we only captured one product of the ICM, namely, sukuk, and did not touch upon other products and services, such as Shari’ah-compliant stocks, Islamic stock indexes, or Islamic funds. Therefore, future studies, both theoretical and empirical, can focus on these untapped areas of the ICM in Uzbekistan and provide more insights into this research field.

Furthermore, our findings may not be generalized, especially in the context of countries with different levels of economic and financial market development, as this study covered only Uzbekistan, a single country in Central Asia. Since we relied on survey data for our analysis, the impact of aggregate variables on the results of the regression was not considered. Therefore, it would be interesting to see if similar findings would hold for a country with different demographics and levels of economic and financial market development, such as a developed country with advanced capital markets and a Muslim minority, like the United Kingdom.

Even within the scope of sukuk’s prospects in Uzbekistan, despite the current study’s empirical analysis of its demand and previous studies analyzing the sector from broader industry and legal perspectives, several areas remain unexplored. These include Shari’ah principles, contract structures, and types of sukuk (sovereign, corporate, or retail) most suitable for the region. Hence, any effort to study these areas for Uzbekistan or other Central Asian countries would be a valuable research contribution.

Moreover, there is a notable lack of empirical research on IF in Uzbekistan, despite the existence of several descriptive studies in the field. Therefore, more effort to produce empirical research would benefit academicians, practitioners, and policymakers in making evidence-based decisions in their respective fields. Some potential areas for such empirical research include Islamic banking, Takaful (Islamic insurance), Islamic leasing and investment funds, and Islamic social financing, to name a few. Such studies will not only encourage further development of the IF industry but also promote academic–government and academic–industry collaboration in the field.

To support future research, we are sharing the questionnaire used for this study in hopes of benefiting anyone interested in exploring any of the mentioned research avenues (See Appendix B).

Funding

This research received no funding.

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Data Availability Statement

The raw data supporting the findings of this article will be provided by the author upon request.

Acknowledgments

The author gratefully acknowledges Prince Sultan University for its financial support and for covering the Article Processing Charge (APC) for this publication. Author thanks three anonymous reviewers for their beneficial feedback and comments. I also acknowledge kind assistance of Ikhtiyorjon Turaboev of Tashkent State University of Law and Ramazan Yildirim of Upsite Consulting W.L.L. during the data collection and reviewing of the manuscript.

Conflicts of Interest

The author declares no conflict of interest.

Appendix A. Distribution of Categorical Independent Variable

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Table A1.

Distribution of categorical independent variables according to respondent’s intent to buy sukuk if offered in Uzbekistan (% of survey respondents).

Table A1.

Distribution of categorical independent variables according to respondent’s intent to buy sukuk if offered in Uzbekistan (% of survey respondents).

| Dependent Variable | Intent to Buy sukuk if Offered in Uzbekistan | |||||

|---|---|---|---|---|---|---|

| Variable Names | Variable Category | Will Not Buy (1) | Maybe Will Buy (2) | Probably Will Buy (3) | Definitely Will Buy (4) | Total |

| Capital market knowledge (cmknow) | very familiar (5) | 0.00 | 2.55 | 1.02 | 2.04 | 5.61 |

| familiar (4) | 0.51 | 4.59 | 12.24 | 3.06 | 20.41 | |

| some knowledge (3) | 2.04 | 11.73 | 14.80 | 5.61 | 34.18 | |

| little knowledge (2) | 1.02 | 13.78 | 7.65 | 3.06 | 25.51 | |

| not familiar (1) | 1.53 | 7.65 | 0.51 | 4.59 | 14.29 | |

| Experience investing in securities (invexpr) | do regularly (5) | 0.00 | 0.51 | 0.51 | 1.02 | 2.04 |

| some experience (4) | 1.02 | 3.57 | 7.14 | 4.08 | 15.82 | |

| knowledge no experience (3) | 1.02 | 11.73 | 13.78 | 5.10 | 31.63 | |

| no knowledge but interested (2) | 0.51 | 14.80 | 11.22 | 6.12 | 32.65 | |

| no experience not interest (1) | 2.55 | 9.69 | 3.57 | 2.04 | 17.86 | |

| Sukuk knowledge (sukknow) | very familiar (5) | 0.00 | 0.51 | 1.02 | 2.55 | 4.08 |

| familiar (4) | 0.00 | 3.57 | 8.16 | 2.04 | 13.78 | |

| some knowledge (3) | 0.00 | 3.57 | 8.67 | 4.59 | 16.84 | |

| little knowledge (2) | 0.51 | 12.24 | 9.69 | 2.55 | 25.00 | |

| not familiar (1) | 4.59 | 20.41 | 8.67 | 6.63 | 40.31 | |

| Islamic stock knowledge (ismstkknow) | very familiar (5) | 0.00 | 0.00 | 0.00 | 0.51 | 0.51 |

| familiar (4) | 0.00 | 1.02 | 5.10 | 2.55 | 8.67 | |

| some knowledge (3) | 0.00 | 5.61 | 9.18 | 5.10 | 19.90 | |

| little knowledge (2) | 0.51 | 14.80 | 10.71 | 4.59 | 30.61 | |

| not familiar (1) | 4.59 | 18.88 | 11.22 | 5.61 | 40.31 | |

| Stock’s Shari’ah compliance (stkshrcomp) | very important (5) | 3.57 | 28.57 | 29.08 | 15.82 | 77.04 |

| Important (4) | 0.00 | 7.65 | 5.10 | 2.04 | 14.80 | |

| relatively important (3) | 0.00 | 2.04 | 1.53 | 0.51 | 4.08 | |

| not very important (2) | 0.00 | 1.02 | 0.51 | 0.00 | 1.53 | |

| not important at all (1) | 1.53 | 1.02 | 0.00 | 0.00 | 2.55 | |

| Grand total | Percentage | 5.10 | 40.31 | 36.22 | 18.37 | 100.0 |

| Count | 10 | 79 | 71 | 36 | 196 | |

Note: Notations provided inside the parenthesis in italic font ( ) are either variable names used in the models or their values if they are dummy or ordinal variables.

Appendix B. Survey on the Prospects of Introducing sukuk Securities in Uzbekistan

Dear participant, this survey is for a study on the prospects of introducing sukuk (Islamic bonds) in Uzbekistan. The information entered in the survey is completely anonymous, and no personal information is collected. Therefore, we ask you to answer the questions as honestly as possible. Thank you very much for taking the time to fill out the questionnaire!

- (1)

- Your age

- (a)

- 19 or younger

- (b)

- 20–29 years old

- (c)

- 30–39 years old

- (d)

- 40–49 years old

- (e)

- 50–59 years old

- (f)

- 60 and older

- (2)

- Your gender

- (a)

- Male

- (b)

- Female

- (3)

- Your marital status

- (a)

- Single

- (b)

- Married

- (c)

- Divorced

- (d)

- Widowed

- (4)

- Your place of residence (one of 14 regions or a foreign country)

- ▪

- Andijan region

- ▪

- Bukhara region

- ▪

- Ferghana region

- ▪

- Jizzakh region

- ▪

- Khorezm region

- ▪

- Namangan region

- ▪

- Navoi region

- ▪

- Qashqadarya region

- ▪

- Republic of Karakalpakstan

- ▪

- Samarkand region

- ▪

- Sirdarya region

- ▪

- Surkhandarya region

- ▪

- Tashkent region

- ▪

- Tashkent city

- ▪

- Foreign country

- (5)

- Field of your work

- (a)

- Banking–finance industry

- (b)

- Education (higher education, school, etc.)

- (c)

- Farming and agriculture

- (d)

- Production and construction

- (e)

- Public service

- (f)

- Trade or services industry

- (g)

- Other (please specify)

- (6)

- Your income level

- (a)

- Below 2 million som

- (b)

- Between 2 and 5 million som

- (c)

- Between 5 and 10 million som

- (d)

- Between 10 and 15 million som

- (e)

- Between 15 and 20 million som

- (f)

- Between 20 and 30 million som

- (g)

- Above 30 million som

- (7)

- How much do you know about the activities in the capital markets (stock markets)?

- (a)

- I am very familiar.

- (b)

- I am generally familiar.

- (c)

- I have some knowledge.

- (d)

- I have very little knowledge.

- (e)

- I am not familiar at all.

- (8)

- Do you have experience investing in financial securities (e.g., stocks, bonds, etc.)?

- (a)

- I do it regularly.

- (b)

- I have some experience investing in them.

- (c)

- I have a general understanding and interest but have not invested yet.

- (d)

- I do not think that I have enough experience and understanding, but I am interested.

- (e)

- I do not have any experience, and I am not planning to invest in them.

- (9)

- How much do you know about Islamic bonds (i.e., sukuk)?

- (a)

- I am very familiar.

- (b)

- I am generally familiar.

- (c)

- I have some knowledge.

- (d)

- I have very little knowledge.

- (e)

- I am not familiar at all.

- (10)

- How much do you know about Islamic stocks and stock indexes?

- (a)

- I am very familiar.

- (b)

- I am generally familiar.

- (c)

- I have some knowledge.

- (d)

- I have very little knowledge.

- (e)

- I am not familiar at all.

- (11)

- If you decide to invest in stocks, to what extent is their compliance with Shari’ah (i.e., being Halal) important for you?

- (a)

- Very important

- (b)

- Important

- (c)

- Relatively important

- (d)

- Not very important

- (e)

- Not important at all

- (12)

- Would you buy Islamic bonds (sukuk) if they were issued in Uzbekistan?

- (a)

- Yes, I would definitely buy them.

- (b)

- Probably, I most likely would buy them.

- (c)

- Probably, if they are in smaller denominations (e.g., 5–10 million som).

- (d)

- Maybe, depending on its type (structure and sharia contract).

- (e)

- Maybe, if sukuk provides more return than traditional bonds.

- (f)

- No, I would not buy them at all.

- (13)

- If you have any suggestions and feedback related to introduction and development of sukuk markets in Uzbekistan, please write them below.(Open-ended question)

| 1 | The method of stratified random sampling was used in our survey to ensure that none of the major segments (strata) of the population is underrepresented. Stratified random sampling combines the randomness of pure random sampling with the representativeness of stratified sampling (see Singh and Mangat 1996 for more details). For example, in our sample, we used gender (female dummy) and marital status (married dummy) among the independent variables. While sampling, we ensured that each of their strata (female vs. male or married vs. others) had at least 10% representation in the total sample size (see Table 1). For sample size determination, we followed the rule of thumb suggested by Peduzzi et al. (1996) for logistic regressions, which recommends at least 10 events per variable (EPV) to obtain unbiased regression coefficients. Our sample size of 196 meets this requirement for at least two out of the three models we estimated (see Table 4). Specifically, Model (2) requires a minimum sample size of 150, while Model (3) requires a minimum sample size of 130 observations. Although our sample size falls slightly short for Model (1) when counting each predictor parameter (beta), it overwhelmingly satisfies Model (3)’s requirement of a minimum of 130 observations for 13 predictor parameters, as suggested by Peduzzi et al. (1996). Since we chose Model (3) as our final model and the dropped variables from Models (1) and (2) were largely insignificant, our sample size of 196 is more than adequate. |

| 2 | By just observing our sample, two variables appear to be somewhat biasedly represented. Firstly, Tashkent city residents present a slight majority (53.1%) of the sample. However, this is not surprising and should not be considered an overrepresentation since it is considered both the administrative and business capital of the country, with a much larger economically active population, most of whom come from other regions of the country. Secondly, females represent a relatively small portion (15.3%) of the sample despite our efforts to encourage active participation of both genders in the survey. Again, this should also not be considered a significant misrepresentation because female labor force participation is 29% lower compared to males in Uzbekistan (World Bank Group 2024b). Furthermore, in a typical Uzbek family, males are considered the head of the household and are generally responsible for investment decisions. Both of these factors may explain the low representation of females in the sample. |

References

- Abdullayev, Azamat, Juliana Juliana, and Gulnora Bekimbetova. 2023. Investigating the Feasibility of Islamic Finance in Uzbekistan. Review of Islamic Economics and Finance 6: 63–74. [Google Scholar]

- Ahmad, Wahida, and Rafisah Mat Radzi. 2011. Sustainability of Sukuk and Conventional Bond during Financial Crisis: Malaysia’s Capital Market. Global Economy and Finance Journal 4: 33–45. [Google Scholar]

- Ananth, Cande, and David G. Kleinbaum. 1997. Regression Models for Ordinal Responses: A Review of Methods and Applications. International Journal of Epidemiology 26: 1323–33. [Google Scholar] [CrossRef]

- Asadov, Alam, and Bahodir Nurmukhamedov. 2023. Development of Islamic Finance in CIS Countries: In the Example of Uzbekistan, 1st ed. Riyadh: Obeikan Publishing. [Google Scholar]

- Asadov, Alam, and Ikhtiyorjon Turaboev. 2023. Legal Challenges Hindering the Development of Islamic Finance in Uzbekistan. Access to Justice in Eastern Europe 6: 1–16. [Google Scholar] [CrossRef]

- Asadov, Alam, Ikhtiyorjon Turaboev, and Mohd Zakhiri Md. Nor. 2023. Legal Challenges in Establishing the Islamic Capital Market in Uzbekistan. ISRA International Journal of Islamic Finance 15: 45–63. [Google Scholar] [CrossRef]

- Asadov, Alam, Ikhtiyorjon Turaboev, and Ramazan Yildirim. 2024. Prospects of Islamic Capital Market in Uzbekistan: Issues and Challenges. International Journal of Islamic and Middle Eastern Finance and Management 17: 102–23. [Google Scholar] [CrossRef]

- Asian Development Bank. 2024. Economic Forecasts for Uzbekistan. Asian Development Outlook (ADO). April. Available online: https://www.adb.org/where-we-work/uzbekistan/economy (accessed on 28 July 2024).

- Associated Press of Pakistan. 2024. Uzbekistan Possess Huge Potential to Become Financial Hub for Central Asia. Business. May 3. Available online: https://www.app.com.pk/business/uzbekistan-possess-huge-potential-to-become-financial-hub-for-central-asia/#google_vignette (accessed on 28 July 2024).

- Bacha, Obiyathulla Ismath, and Abbas Mirakhor. 2013. Islamic Capital Markets and Development. In Economic Development and Islamic Finance. Edited by Zamir Iqbal and Abbas Mirakhor. Washington, DC: The World Bank, pp. 253–74. [Google Scholar]

- Botirova, Hulkar Olimjonovna. 2023. Overview of Islamic Finance in Uzbekistan: Challenges and Prospects. European Journal of Economics, Finance and Business Development 1: 20–25. [Google Scholar]

- Boujlil, Rhada, M. Kabir Hassan, and Rihab Grassa. 2020. Sovereign Debt Issuance Choice: Sukuk vs. Conventional Bonds. Journal of Islamic Monetary Economics and Finance 6: 275–94. [Google Scholar] [CrossRef]

- Cohen, Gil, and Andrey Kudryavtsev. 2012. Investor Rationality and Financial Decisions. Journal of Behavioral Finance 13: 11–16. [Google Scholar] [CrossRef]

- Danila, Nevi, Noor Azlina Azizan, and Umara Noreen. 2023. A Comparative Study between Retail Sukuk and Retail Bonds in Indonesia. International Journal of Business and Globalisation 33: 373. [Google Scholar] [CrossRef]

- Daryo. 2021. Ўзбeкиcтoндa Иcлoмий Moлиялaштиpиш Heгa Tўлиқ Aмaлгa Oшиpилмaгaнигa Изoҳ Бepилди (It Was Explained Why Islamic Financing Was Not Fully Implemented in Uzbekistan). Www.Daryo.Uz. September 2. Available online: https://daryo.uz/k/2021/09/02/ozbekistonda-islomiy-moliyalashtirish-nega-toliq-amalga-oshirilmaganiga-izoh-berildi/ (accessed on 3 August 2024).

- Echchabi, Abdelghani, Hassanuddeen Abd Aziz, and Umar Idriss. 2016. Does Sukuk Financing Promote Economic Growth: An Emphasis on the Major Issuing Countries. Turkish Journal of Islamic Economics 3: 63. [Google Scholar] [CrossRef]

- Echchabi, Abdelghani, Hassanuddeen Abd Aziz, and Umar Idriss. 2018. The Impact of Sukuk Financing on Economic Growth: The Case of GCC Countries. International Journal of Financial Services Management 9: 60. [Google Scholar] [CrossRef]

- Hassan, Shafiqul, Mohsin Dhali, Saghir Munir Mehar, and Fazluz Zaman. 2022. Islamic Securitization as a Yardstick for Investment in Islamic Capital Markets. International Journal of Service Science, Management, Engineering, and Technology 13: 1–15. [Google Scholar] [CrossRef]

- ICD, and LSEG. 2023. Islamic Finance Development Report 2023: Navigating Uncertainty. London: LSEG. [Google Scholar]

- Imamnazarov, Jakhongir. 2020. Landscaping Analysis of Islamic Finance Instruments in Uzbekistan. Tashkent, Uzbekistan. Available online: https://www.undp.org/sites/g/files/zskgke326/files/migration/uz/ENG_Landscaping-IF-in-Uzbekistan_final.pdf (accessed on 3 August 2024).

- Indriani, Mirna, Ratna Mulyany, and N. A. Indayani. 2020. Behaviour towards Investments in Islamic Capital Market: An Exploratory Study. International Journal of Trade and Global Markets 13: 454. [Google Scholar] [CrossRef]

- Islamic Corporation for the Development of the Private Sector (ICD). 2021. ICD Signs Line of Finance Agreements with Four Uzbekistan Banks. ICD News. September 4. Available online: https://icd-ps.org/en/news/icd-signs-line-of-finance-agreements-with-four-uzbekistan-banks (accessed on 30 July 2024).

- Islamic Finance News (IFN). 2023. Intercascade Group’s Sukuk: First in Kyrgyzstan. Available online: https://www.islamicfinancenews.com/intercascade-groups-sukuk-first-in-kyrgyzstan.html (accessed on 14 May 2024).

- Jivraj, Hassan. 2024. Challenges Impede Islamic Finance Growth in Central Asia. Salaam Gateway. April 24. Available online: https://salaamgateway.com/story/challenges-impede-islamic-finance-growth-in-central-asia (accessed on 30 July 2024).

- Kahneman, Daniel, and Amos Tversky. 2013. Prospect Theory: An Analysis of Decision Under Risk. In Handbook of the Fundamentals of Financial Decision Making: Part I. Singapore: World Scientific, pp. 99–127. [Google Scholar] [CrossRef]

- Khaki, G N, and Bilal Ahmad Malik. 2014. Islamic Banking and Finance in Post—Soviet Central Asia with Special Reference to Kazakhstan. International Journal of Excellence in Islamic Banking and Finance 4: 1–14. [Google Scholar] [CrossRef]

- Khasanov, Khusan. 2019. Prospects for the Development of Islamic Finance in the Republic of Uzbekistan. In Round Table Meeting on Prospects of Development of Islamic Finance in Uzbekistan. Tashkent: Center for Development Strategy, Uzbekistan. Available online: https://www.researchgate.net/publication/339552084_Prospects_for_the_Development_of_Islamic_Finance_in_the_Republic_of_Uzbekistan (accessed on 23 June 2024).

- Khusanov, Murod. 2022. Uzbekistan Opens for Islamic Finance. Islamic Finance News (IFN). December 16. Available online: https://www.islamicfinancenews.com/uzbekistan-opens-for-islamic-finance.html (accessed on 31 March 2024).

- Krische, Susan D. 2019. Investment Experience, Financial Literacy, and Investment-Related Judgments. Contemporary Accounting Research 36: 1634–68. [Google Scholar] [CrossRef]

- Kun.uz. 2021. Ministerial Official Explains Why Islamic Finance Is Not Fully Introduced in Uzbekistan. Kun.Uz. September 3. Available online: https://kun.uz/en/news/2021/09/03/ministerial-official-explains-why-islamic-finance-is-not-fully-introduced-in-uzbekistan (accessed on 13 May 2023).

- Laldin, Mohamad Akram. 2008. Islamic Financial System: The Malaysian Experience and the Way Forward. Humanomics 24: 217–38. [Google Scholar] [CrossRef]

- Ledhem, Mohammed Ayoub. 2022. Does Sukuk Financing Boost Economic Growth? Empirical Evidence from Southeast Asia. PSU Research Review 6: 141–57. [Google Scholar] [CrossRef]

- Long, J. Scott, and Jeremy Freese. 2014. Regression Models for Categorical Dependent Variables Using Stata, 3rd ed. College Station: Stata Press. [Google Scholar]

- Mallick, Debdulal. 2009. Marginal and Interaction Effects in Ordered Response Models. Munich: MPRA Paper, p. 1332. [Google Scholar]

- Nagimova, Almira. 2021. Islamic Finance in the CIS Countries. Campbell: Academus Publishing. [Google Scholar] [CrossRef]

- Nizomiddinov, Muzaffar. 2020. Uzbekistan Can Become a CIS Leader in Islamic Finance. Kun.Uz. August 4. Available online: https://kun.uz/en/94663863#! (accessed on 28 July 2024).

- Nusrathujaev, Hondamir. 2020. Opportunities and Expectations for Islamic Finance in Uzbekistan (Country Report: Uzbekistan). Islamic Finance News, December. 131. [Google Scholar]

- Peduzzi, Peter, John Concato, Elizabeth Kemper, Theodore R. Holford, and Alvan R. Feinstein. 1996. A Simulation Study of the Number of Events per Variable in Logistic Regression Analysis. Journal of Clinical Epidemiology 49: 1373–79. [Google Scholar] [CrossRef]

- Pew Research Center. 2009. Mapping the Global Muslim Population: A Report on the Size and Distribution of the World’s Muslim Population. Washington, D.C. Available online: https://microdata.worldbank.org/index.php/citations/3606 (accessed on 17 May 2024).

- Sachan, Abhishek, and Pawan Kumar Chugan. 2020. Availability Bias of Urban and Rural Investors: Relationship Study of the Gujarat State of India. Journal of Behavioural Economics, Finance, Entrepreneurship, Accounting and Transport 8: 1–6. [Google Scholar]

- Salman, Muhammad, Bakhtiar Khan, Sher Zaman Khan, and Rafi Ullah Khan. 2021. The Impact of Heuristic Availability Bias on Investment Decision-making: Moderated Mediation Model. Business Strategy & Development 4: 246–57. [Google Scholar] [CrossRef]

- Singh, Ravindra, and Naurang Singh Mangat. 1996. Stratified Sampling. In Elements of Survey Sampling. Edited by Ravindra Singh and Naurang Singh Mangat. Cham: Springer-Science+Business Media, B.V., pp. 102–44. [Google Scholar] [CrossRef]

- Sivaramakrishnan, Sreeram, Mala Srivastava, and Anupam Rastogi. 2017. Attitudinal Factors, Financial Literacy, and Stock Market Participation. International Journal of Bank Marketing 35: 818–41. [Google Scholar] [CrossRef]

- Smaoui, Houcem, and Mohsin Khawaja. 2017. The Determinants of Sukuk Market Development. Emerging Markets Finance and Trade 53: 1501–18. [Google Scholar] [CrossRef]

- Statistical Agency of Uzbekistan. 2024. The Permanent Population in Uzbekistan Increases Daily by an Average of 1.8 Thousand People. Agency News. April 16. Available online: https://stat.uz/en/press-center/news-of-committee/52809-o-zbekisto-nda-doimiy-ah-oli-soni-har-kuni-o-rtacha-1-8-ming-kishiga-oshmoqda-5 (accessed on 17 May 2024).

- The Tashkent Times. 2024. Average Uzbekistan before Tax Salary at US$ 370. The Tashkent Times. January 30. Available online: https://tashkenttimes.uz/national/12411-average-uzbekistan-before-tax-salary-at-us-370 (accessed on 31 July 2024).

- Van Rooij, Maarten, Annamaria Lusardi, and Rob Alessie. 2011. Financial Literacy and Stock Market Participation. Journal of Financial Economics 101: 449–72. [Google Scholar] [CrossRef]

- World Bank Group. 2024a. Uzbekistan: Overview. Uzbekistan Overview. Available online: https://www.worldbank.org/en/country/uzbekistan/overview#context (accessed on 28 July 2024).

- World Bank Group. 2024b. World Bank Country Gender Assessment Report: Uzbekistan. Country Gender Assessment Report. Available online: https://www.worldbank.org/en/country/uzbekistan/publication/country-gender-assessment-2024 (accessed on 31 July 2024).

- Worldometer. 2023. Uzbekistan Demographics 2023 (Population, Age, Sex, Trends). Uzbekistan Demographics 2023. Available online: https://www.worldometers.info/demographics/uzbekistan-demographics/ (accessed on 31 July 2024).

- Worldometer. 2024. Central Asia Population (LIVE). Available online: https://www.worldometers.info/world-population/central-asia-population/ (accessed on 17 May 2024).

- Yusfiarto, Rizaldi, Septy Setia Nugraha, Lu’liyatul Mutmainah, Izra Berakon, Sunarsih Sunarsih, and Achmad Nurdany. 2023. Examining Islamic Capital Market Adoption from a Socio-Psychological Perspective and Islamic Financial Literacy. Journal of Islamic Accounting and Business Research 14: 574–94. [Google Scholar] [CrossRef]

Figure 1.

Respondents’ distribution by place of residence. Note: The order of regions goes clockwise according to the list, with the Andijan region at the 12 o’clock position.

Figure 1.

Respondents’ distribution by place of residence. Note: The order of regions goes clockwise according to the list, with the Andijan region at the 12 o’clock position.

Figure 2.

Age distribution of respondents.

Figure 3.

Income distribution of respondents.

Figure 4.

Margin plots of Tashkent city dummy (tashdum) for all four categories of intent to buy sukuk (buysuk).

Figure 4.

Margin plots of Tashkent city dummy (tashdum) for all four categories of intent to buy sukuk (buysuk).

Figure 5.

Margin plots of investment experience (invexpr) for all four categories of intent to buy sukuk (buysuk).

Figure 5.

Margin plots of investment experience (invexpr) for all four categories of intent to buy sukuk (buysuk).

Figure 6.

Margin plots of sukuk knowledge (sukknow) for all four categories of intent to buy sukuk (buysuk).

Figure 6.

Margin plots of sukuk knowledge (sukknow) for all four categories of intent to buy sukuk (buysuk).

Figure 7.

Margin plots of attitude on stock’s Shari’ah compliance (stkshrcomp) for all four categories of intent to buy sukuk (buysuk).

Figure 7.

Margin plots of attitude on stock’s Shari’ah compliance (stkshrcomp) for all four categories of intent to buy sukuk (buysuk).

Table 1.

Distribution of dummy independent variables according to respondents’ intent to buy sukuk if offered in Uzbekistan (% of survey respondents).

Table 1.

Distribution of dummy independent variables according to respondents’ intent to buy sukuk if offered in Uzbekistan (% of survey respondents).

| Dependent Variables | Intent to Buy sukuk if Offered in Uzbekistan | |||||

|---|---|---|---|---|---|---|

| Names | Categories | (1) | (2) | (3) | (4) | Total |

| Gender (femdum) | Female (1) | 1.02 | 8.67 | 2.55 | 3.06 | 15.31 |

| Male (0) | 4.08 | 31.63 | 33.67 | 15.31 | 84.69 | |

| Married (mardum) | Married (1) | 3.57 | 28.06 | 26.02 | 11.73 | 69.39 |

| Single (0) | 1.53 | 11.73 | 9.69 | 5.61 | 28.57 | |

| Divorced (0) | 0 | 0 | 0.51 | 0.51 | 1.02 | |

| Widowed (0) | 0 | 0.51 | 0 | 0.51 | 1.02 | |

| Tashkent city resident (tashdum) | Yes (1) | 3.57 | 23.98 | 18.88 | 6.63 | 53.06 |

| No (0) | 1.53 | 16.33 | 17.35 | 11.73 | 46.94 | |

| Education industry (edudum) | Yes (1) | 3.06 | 15.31 | 15.82 | 5.61 | 39.8 |

| No (0) | 2.04 | 25 | 20.41 | 12.76 | 60.2 | |

| Financial industry (findum) | Yes (1) | 0 | 7.14 | 6.12 | 3.57 | 16.84 |

| No (0) | 5.1 | 33.16 | 30.1 | 14.8 | 83.16 | |