Non-trivial Factors as Determinants of the Environmental Taxation Revenues in 27 EU Countries

Abstract

:1. Introduction

2. Background

2.1. Environmental Taxation and Economic Growth

2.2. Rule of Law, ICT and Importation

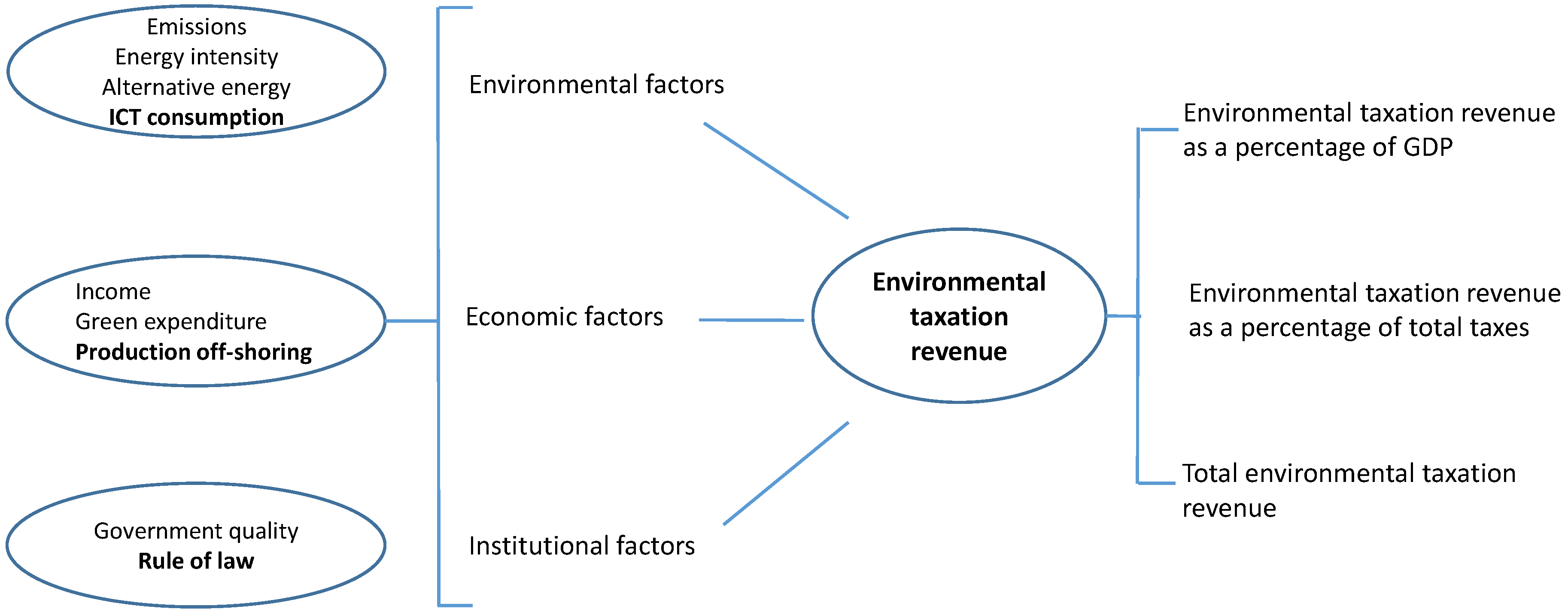

3. Methodology

3.1. Econometric Model

3.2. Data and Descriptive Statistics

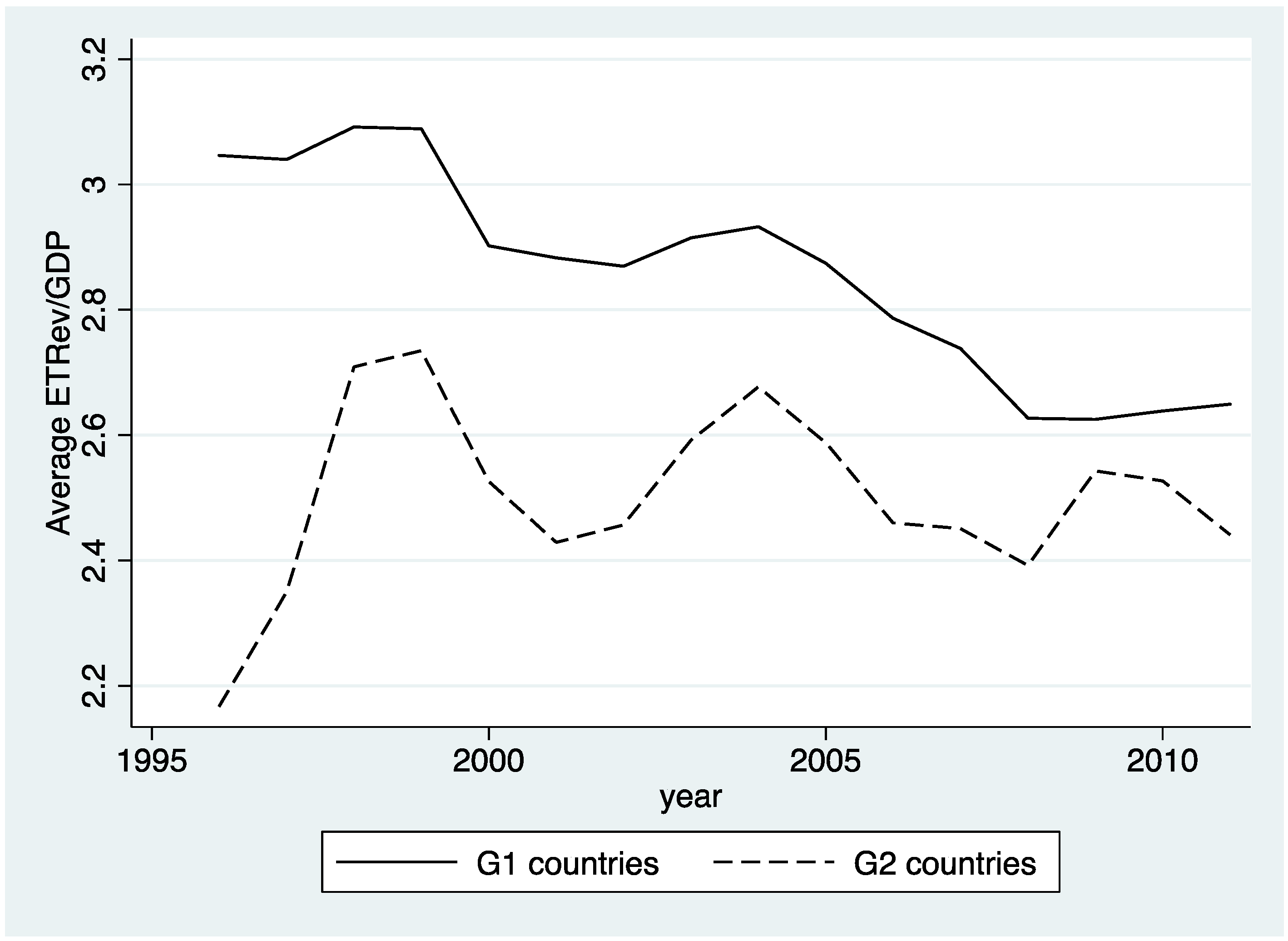

4. Results and Discussion

4.1. Main Results

4.2. Robustness Tests

5. Conclusions

Author Contributions

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

| Variable | Obs | Mean | Std. Dev. | Min | Max |

|---|---|---|---|---|---|

| ETRev_GDP | 448 | 2.730 | 0.676 | 1.180 | 5.170 |

| ETRev_TAX | 476 | 7.529 | 1.807 | 3.720 | 15.390 |

| ETRev_TOT | 444 | 1.25 × 1010 | 1.82 × 1010 | 1.11 × 108 | 7.26 × 1010 |

| RoL | 493 | 6.164 | 0.622 | 4.543 | 7.000 |

| Govern | 493 | 6.230 | 0.675 | 4.377 | 7.357 |

| ICT | 343 | 2.11 × 109 | 1.38 × 1010 | 3.45 × 108 | 1.14 × 1011 |

| IMP | 347 | 1.85 × 1010 | 2.59 × 1010 | 3.45 × 108 | 1.25 × 1011 |

| Pub_exp | 347 | 1.68 × 1011 | 2.21 × 1011 | 3.14 × 109 | 1.27 × 1012 |

| GGEpc | 328 | 14,351.970 | 14,183.610 | 6.236 | 82,806.460 |

| GGEsa | 454 | 0.010 | 0.004 | 0.004 | 0.028 |

| Intensity | 431 | 276.220 | 212.973 | 80.042 | 1411.170 |

| Altern_En | 485 | 14.529 | 14.681 | 0.000 | 50.734 |

| GDP | 489 | 4.86 × 1011 | 7.34 × 1010 | 4.62 × 109 | 3.07 × 1012 |

| GDPpc | 489 | 26,949.78 | 18,227.02 | 2353.987 | 87,716.73 |

| Variable | ETRev_GDP | ETRev_TAX | ETRev_TOT | |||

|---|---|---|---|---|---|---|

| Panel A—G1 group | ||||||

| Govern | 0.500 *** | 0.621 *** | 0.691 *** | 0.764 *** | 0.553 *** | 0.643 *** |

| (0.147) | (0.143) | (0.164) | (0.159) | (0.153) | (0.149) | |

| ICT | 0.060 *** | 0.075 *** | 0.042 | 0.019 * | 0.070 *** | 0.079 *** |

| (0.024) | (0.024) | (0.027) | (0.027) | (0.026) | (0.025) | |

| IMP | −0.113 *** | −0.124 *** | −0.296 *** | −0.281 *** | −0.171 *** | −0.149 ** |

| (0.041) | (0.042) | (0.067) | (0.068) | (0.063) | (0.063) | |

| Pub_exp | −0.080 *** | −0.103 *** | −0.152 *** | −0.162 *** | −0.099 *** | −0.111 *** |

| (0.020) | (0.020) | (0.028) | (0.027) | (0.026) | (0.025) | |

| GGEpc | 0.432 *** | .. | 0.289 *** | .. | 0.393 *** | .. |

| (0.089) | .. | (0.101) | .. | (0.094) | .. | |

| GGEsa | .. | 0.424 *** | .. | 0.271 *** | .. | 0.398 *** |

| .. | (0.089) | .. | (0.110) | .. | (0.103) | |

| Intensity | −0.056 | −0.036 | 0.016 | −0.032 | 0.012 | 0.003 |

| (0.122) | (0.121) | (0.144) | (0.152) | (0.134) | (0.143) | |

| Altern_En | 0.048 ** | 0.051 *** | 0.013 | 0.011 | 0.058 *** | 0.055 *** |

| (0.021) | (0.021) | (0.024) | (0.024) | (0.023) | (0.023) | |

| GDP | .. | .. | 0.760 *** | 0.692 *** | 1.225 *** | 1.104 *** |

| .. | .. | (0.199) | (0.216) | (0.187) | (0.203) | |

| Constant | 4.467 ** | 2.266 | −10.296 ** | −10.517 ** | −0.708 | −0.132 |

| (1.917) | (1.626) | (5.023) | (5.278) | (4.703) | (4.942) | |

| R−sq | 0.67 | 0.67 | 0.61 | 0.61 | 0.56 | 0.56 |

| F−test | 36.38 | 36.02 | 24.74 | 24.11 | 20.01 | 19.44 |

| prob. | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 |

| Obs | 148 | 148 | 148 | 148 | 148 | 148 |

| Panel B—G2 group | ||||||

| Govern | 0.339 | 0.43 | 0.56 | 0.674 | 0.332 | 0.389 |

| (0.524) | (0.482) | (0.497) | (0.471) | (0.526) | (0.504) | |

| ICT | −0.05 | −0.056 | 0.001 | 0.008 | −0.049 | −0.05 |

| (0.052) | (0.051) | (0.050) | (0.050) | (0.053) | (0.054) | |

| IMP | 0.063 | 0.074 | −0.033 | −0.031 | 0.070 | 0.101 |

| (0.090) | (0.095) | (0.119) | (0.109) | (0.127) | (0.115) | |

| Pub_exp | −0.054 *** | −0.052 *** | −0.039 *** | −0.043 *** | −0.054 *** | −0.052 *** |

| (0.017) | (0.017) | (0.016) | (0.016) | (0.017) | (0.017) | |

| GGEpc | 0.087 | .. | −0.088 | .. | 0.092 | .. |

| (0.148) | .. | (0.160) | .. | (0.183) | .. | |

| GGEsa | .. | 0.027 | .. | −0.128 | .. | 0.032 |

| .. | (0.126) | .. | (0.116) | .. | (0.144) | |

| Intensity | −0.075 | −0.057 | −0.023 | 0.005 | −0.08 | −0.058 |

| (0.148) | (0.149) | (0.131) | (0.135) | (0.147) | (0.158) | |

| Altern_En | 0.054 *** | 0.052 *** | 0.035 ** | 0.040 *** | 0.053 *** | 0.055 *** |

| (0.017) | (0.017) | (0.016) | (0.016) | (0.017) | (0.018) | |

| GDP | .. | .. | 0.029 | 0.076 | 0.988 *** | 0.954 *** |

| .. | .. | (0.106) | (0.114) | (0.120) | (0.134) | |

| Constant | 1.096 | 0.262 | 1.097 | −0.25 | 1.27 | 0.681 |

| (3.370) | (2.978) | (2.964) | (3.058) | (3.343) | (3.648) | |

| R−sq | 0.25 | 0.25 | 0.20 | 0.21 | 0.64 | 0.64 |

| Wald(chi)2 | 27.33 | 27.13 | 18.22 | 19.89 | 457.05 | 389.2 |

| prob. | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 |

| Obs | 100 | 100 | 100 | 100 | 100 | 100 |

References

- Al-mulali, Usama, and Low Sheau-Ting. 2014. Econometric Analysis of Trade, Exports, Imports, Energy Consumption and CO2 Emission in Six Regions. Renewable & Sustainable Energy Reviews 33: 484–98. [Google Scholar]

- Anger, Niels, Christoph Bohringer, and Andreas Lange. 2006. Differentiation of Green Taxes: A Political-Economy Analysis for Germany. Centre for European Economic Research Discussion Paper No. 06-003. Mannheim: Centre for European Economic Research. [Google Scholar]

- Bachus, Kris. 2012. Improving the methodology for measuring the greening of the tax system. In Green Taxation and Environmental Sustainability. Edited by Kreiser Lawrence, Ana Yábar Sterling, Pedro Herrera, Janet E. Milne and Hope Ashiabor. Cheltenham: Edward Elgar. [Google Scholar]

- Baek, Jungho, S. Cho Young, and Won W. Koo. 2009. The Environmental Consequences of Globalization: A Country-Specific Time-Series Analysis. Ecological Economics 68: 2255–64. [Google Scholar] [CrossRef]

- Becchetti, Leonardo, David A. Londono-Bedoya, and Luigi Paganetto. 2003. ICT Investment, Productivity and Efficiency: Evidence at Firm Level Using a Stochastic Frontier Approach. Journal of Productivity Analysis 20: 143–67. [Google Scholar] [CrossRef]

- Bento, Antonio M., and Mark R. Jacobsen. 2007. Environmental policy and the “double-dividend” hypothesis. Journal of Environmental Economics and Management 53: 17–31. [Google Scholar] [CrossRef]

- Bhattarai, Madhusudan, and Michael Hammig. 2001. Institutions and the Environmental Kuznets Curve for Deforestation: A Cross-Country Analysis for Latin America, Africa, and Asia. World Development 29: 995–1010. [Google Scholar] [CrossRef]

- BIO Intelligence Service. 2013. Equivalent Conditions for Waste Electrical and Electronic Equipment (WEEE) Recycling Operations Taking Place outside the European Union. Final Report Prepared for European Commission—DG Environment. Brussels: European Commission—DG Environment. [Google Scholar]

- Bluffstone, Randall A. 2003. Environmental Taxes in Developing and Transition Economies. Public Financial Management 3: 143–75. [Google Scholar] [CrossRef]

- Bovenberg, A. Lans, and Ruud de Mooij. 1997. Environmental Tax Reform and Endogenous Growth. Journal of Public Economics 63: 207–37. [Google Scholar] [CrossRef]

- Bovenberg, A. Lans, Lawrence H. Goulder, and Mark R. Jacobsen. 2008. Costs of alternative environmental policy instruments in the presence of industry compensation requirements. Journal of Public Economics 92: 1236–53. [Google Scholar] [CrossRef]

- Brynjolfsson, Erik, and Lorin Hitt. 1996. Paradox Lost? Firm Level Evidence on the Returns to Information Systems Spending. Management Science 42: 541–58. [Google Scholar] [CrossRef]

- Cameron, A. Colin, and Pravin K. Trivedi. 2009. Microeconometrics Using Stata. Texas: College Station. [Google Scholar]

- Castiglione, Concetta. 2012. Technical Efficiency and ICT Investment in Italian Manufacturing Firms. Applied Economics 44: 1749–63. [Google Scholar] [CrossRef]

- Castiglione, Concetta, Davide Infante, and Janna Smirnova. 2012. Rule of law and the environmental Kuznets curve: evidence for carbon emissions. International Journal of Sustainable Economy 4: 254–69. [Google Scholar] [CrossRef]

- Castiglione, Concetta, Davide Infante, and Janna Smirnova. 2014. Is There Any Evidence on the Existence of an Environmental Taxation Kuznets Curve? The Case of European Countries under their Rule of Law Enforcement. Sustainability 6: 7242–62. [Google Scholar] [CrossRef]

- Cole, Matthew A. 2007. Corruption, Income and the Environment: an Empirical Analysis. Ecological Economics 62: 637–47. [Google Scholar] [CrossRef]

- Costantini, Valeria, and Chiara Martini. 2010. A Modified Environmental Kuznets Curve for Sustainable Development Assessment Using Panel Data. International Journal of Global Environmental Issues 10: 84–122. [Google Scholar] [CrossRef]

- Damania, Richard, Per G. Fredriksson, and John A. List. 2003. Trade Liberalization, Corruption, and Environmental Policy Formation: Theory and Evidence. Journal of Environmental Economics and Management 46: 490–512. [Google Scholar] [CrossRef]

- Davis, John. 2003. Regional Economic Integration, the Environment and Community: East Asia and APEC. International Review of Applied Economics 17: 69–83. [Google Scholar] [CrossRef]

- Dutt, Kuheli. 2009. Governance, Institutions and the Environmental-Income Relationship: A Cross-Country Study. Environment, Development and Sustainability 11: 705–23. [Google Scholar] [CrossRef]

- European Environment Agency—EEA. 2005. Market-Based Instruments for Environmental Policy in Europe. Technical Report No. 8. Copenhagen: European Environmental Agency. [Google Scholar]

- Ekins, Paul, and Terry Barker. 2001. Carbon Taxes and Carbon Emissions Trading. Journal of Economic Surveys 15: 325–52. [Google Scholar] [CrossRef]

- Ekins, Paul, Philip Summerton, Chris Thoung, and Daniel Lee. 2011. A Major Environmental Tax Reform for the UK: Results for the Economy, Employment and the Environment. Environmental and Resource Economics 50: 447–74. [Google Scholar] [CrossRef]

- European Commission. 1997. Tax Provisions with a Potential Impact on Environmental Protection. Luxemburg: Office for Official Publications of the European Communities. [Google Scholar]

- European Commission. 2007. A Lead Market Initiative for Europe Explanatory Paper on the European Lead Market Approach: Methodology and Rationale. Commission Staff Working Paper Document SEC (2007) 1730. Brussels: Commission of the European Communities. [Google Scholar]

- Eurostat. 2001. Environmental Taxes. A Statistical Guide. Luxembourg: European Commission. [Google Scholar]

- Eurostat. 2013. Taxation Trends in the European Union: Data for the EU Member States, Iceland, Norway and Luxembourg. Luxembourg: Publications Office of the European Union. [Google Scholar]

- Eurostat. 2014. Environmental Accounts. Available online: http://epp.eurostat.ec.europa.eu/portal/page/portal/environmental_accounts/data/database (accessed on 1 September 2014).

- Fullerton, Don, and Gilbert E. Metcalf. 1997. Environmental Taxes and the Double-Dividend Hypothesis: Did You Really Expect Something for Nothing? NBER Working Paper No. 6199. Cambridge: National Bureau of Economic Research. [Google Scholar]

- Gorbunova, Yulia, Davide Infante, and Janna Smirnova. 2012. New Evidences on FDI Determinants. An Appraisal over the Transition Period. Prague Economic Papers 2: 129–49. [Google Scholar] [CrossRef]

- Gordon, Robert J. 2002. Technology and Economic Performance in the American Economy. NBER Working Paper Series No. 8771. Evanston: Northwestern University. [Google Scholar]

- Goulder, Lawrence H. 2013. Climate change policy’s interactions with the tax system. Energy Economics 40: S3–S11. [Google Scholar] [CrossRef]

- Hall, Bronwyn H., Francesca Lotti, and Jacques Mairesse. 2013. Evidence on the Impact of R&D and ICT Investments on Innovation and Productivity in Italian Firms. Economics of Innovation and New Technology 22: 300–28. [Google Scholar]

- Im, Kyung So, M. Hashem Pesaran, and Yongcheol Shin. 2003. Testing for Unit Roots in Heterogeneous Panel. Journal of Econometrics 115: 53–74. [Google Scholar] [CrossRef]

- Infante, Davide, and Janna Smirnova. 2016. Environmental Technology Choice in the Presence of Corruption and the Rule of Law Enforcement. Transformation in Business & Economics 15: 214–27. [Google Scholar]

- Ivanova, Kate. 2010. Corruption and Air Pollution in Europe. Oxford Economic Papers 63: 49–70. [Google Scholar] [CrossRef]

- Kampas, Athanasios, and Richard Horan. 2016. Second-Best Pollution Taxes: Revisited and Revised. Environmental Economics and Policy Studies 18: 577–97. [Google Scholar] [CrossRef]

- Karydas, Christos, and Lin Zhang. 2017. Green tax reform, endogenous innovation and the growth dividend. Journal of Environmental Economics and Management. [Google Scholar] [CrossRef]

- Kaufmann, Daniel, Aart Kraay, and Massimo Mastruzzi. 2010. The Worldwide Governance Indicators: A Summary of Methodology, Data and Analytical Issues. World Bank Policy Research Working Paper No. 5430. Washington: The World Bank. [Google Scholar]

- Worldwide Governance Indicators. 2014. The Worldwide Governance Indicators (WGI) Project. Available online: http://info.worldbank.org/governance/wgi/#home (accessed on 1 September 2014).

- Kosonen, Katri. 2010. Why Are Environmental Tax Revenues Falling in the European Union? In Critical Issues in Environmental Taxation. Edited by Soares Claudia Dias, Janet Milne, Hope Ashiabor and Kurt Deketelaere. Oxford: Oxford University Press, pp. 37–56. [Google Scholar]

- Lipford, Jody W., and Bruce Yandle. 2010. Environmental Kuznets Curves, Carbon Emissions, and Public Choice. Environment and Development Economics 15: 417–38. [Google Scholar] [CrossRef]

- Luzzati, Tommaso, and Marco Orsini. 2009. Natural Environment and Economic Growth: Looking for the Energy-EKC. Energy 34: 291–300. [Google Scholar] [CrossRef]

- Markandya, Anil, Alexander Golub, and Suzette Pedroso-Galinato. 2006. Empirical Analysis of National Income and SO2 Emissions in Selected European Countries. Environmental and Resource Economics 35: 221–57. [Google Scholar] [CrossRef]

- Muller, Adrian, and Thomas Sterner. 2006. Environmental Taxation in Practice. Abingdon: Taylor & Francis Ltd., Ashgate Publishing Limited. [Google Scholar]

- OECD. 2008. Environmental Outlook to 2030. Paris: OECD. [Google Scholar]

- Panayotou, Theodore. 1997. Demystifying the Environmental Kuznets Curve: Turning a Black Box into a Policy Tool. Environment and Development Economics 2: 465–84. [Google Scholar] [CrossRef]

- Parisi, Maria Laura, Fabio Schiantarelli, and Alessandro Sembenelli. 2002. Productivity, Innovation Creation and Absorption, and R&S: Micro Evidence for Italy. Working Paper in Economics, n.526. Chestnut Hill: Boston College. [Google Scholar]

- Pellegrini, Lorenzo, and Reyer Gerlagh. 2006. Corruption, democracy, and environmental policy. An empirical contribution to the debate. The Journal of Environment and Development 15: 332–54. [Google Scholar] [CrossRef]

- Pereira, Alfredo Marvao, and Rui Marvao Pereira. 2017. Achieving the triple dividend in Portugal: A dynamic general-equilibrium evaluation of a carbon tax indexed to emissions trading. Journal of Economic Policy Reform 20: 1–16. [Google Scholar] [CrossRef]

- Porter, E. Michael, and Claas van der Linde. 1995. Toward a new conception of the Environment-Competitiveness Relationship. The Journal of Economic Perspectives 9: 97–118. [Google Scholar] [CrossRef]

- Scrimgeour, Frank, Les Oxley, and Koli Fatai. 2005. Reducing Carbon Emissions? The Relative Effectiveness of Different Types of Environmental Tax: the Case of New Zealand. Environmental Modelling & Software 20: 1439–48. [Google Scholar]

- Sterner, Thomas, and Gunnar Köhlin. 2003. Environmental Taxes in Europe. Public Finance and Management 3: 117–42. [Google Scholar]

- Taheripour, Farzad, Madhu Khanna, and Carl H. Nelson. 2008. Welfare Impacts of Alternative Public Policies for Agricultural Pollution Control in an Open Economy: A General Equilibrium Framework. American Journal of Agricultural Economics 90: 701–18. [Google Scholar] [CrossRef]

- Takeda, Shiro. 2007. The double dividend from carbon regulations in Japan. Journal of the Japanese and International Economies 21: 336–64. [Google Scholar] [CrossRef]

- Tong, Xin, Jin Shi, and Yu Zhou. 2012. Greening of Supply Chain in Developing Countries: Diffusion of Lead (Pb)-Free Soldering in ICT Manufacturers in China. Ecological Economics 83: 174–82. [Google Scholar] [CrossRef]

- United Nations Environment Programme. 2012. E-Waste. Volume III. WEEE/e-Waste Take Back System. Osaka: United Nations Environmental Programme, Division of Technology, Industry and Economics, International Environmental Technology Centre. [Google Scholar]

- Ward, Hugh, and Xun Cao. 2012. Domestic and International Influences on Green Taxation. Comparative Political Studies 45: 1075–103. [Google Scholar] [CrossRef]

- Warr, Benjamin, and Robert U. Ayres. 2012. Useful work and information as drivers of economic growth. Ecological Economics 73: 93–102. [Google Scholar] [CrossRef]

- Williams, Roberton C. 2002. Environmental Tax Interactions when Pollution Affects Health or Productivity. Journal of Environmental Economics and Management 44: 261–70. [Google Scholar] [CrossRef]

- World Development Indicators. 2014. The World Bank World Development Indicators. Available online: https://data.worldbank.org/products/wdi (accessed on 1 September 2014).

- Yamazaki, Akion. 2017. Jobs and climate policy: Evidence from British Columbia’s revenue-neutral carbon tax. Journal of Environmental Economics and Management 83: 197–216. [Google Scholar]

| Variables | Description | Source |

|---|---|---|

| ETRev_GDP | Total environmental tax revenues as percentage of GDP | Eurostat (2014) |

| ETRev_TAX | Total environmental tax revenues as percentage of total tax revenues | Eurostat (2014) |

| ETRev_TOT | Total environmental tax revenues (constant 2005 US$) | Eurostat (2014) |

| RoL | Rule of Law measured in units ranging from −2.5 to 2.5, with higher values corresponding to better governance outcomes | Worldwide Governance Indicators (2014) |

| Govern | Government Effectiveness measured in units ranging from −2.5 to 2.5, with higher values corresponding to better governance outcomes | Worldwide Governance Indicators (2014) |

| ICT | ICT imports of goods and services (constant 2005 US$) | World Development Indicators (2014) |

| IMP | Imports of goods and services minus ICT imports, (constant 2005 US$) | World Development Indicators (2014) |

| Pub_exp | Per capita environmental protection expenditure (constant 2005 US$) | Eurostat (2014) |

| GGEpc | Greenhouse Gas Emissions (CO2 equivalent), thousands of tonnes per capita | Eurostat (2014) |

| GGEsa | Greenhouse Gas Emissions (CO2 equivalent), thousands of tonnes per surface area | Eurostat (2014) |

| Altern_En | Alternative and nuclear energy (% of total energy use) | World Development Indicators (2014) |

| Intensity | Energy intensity of the economy: gross inland consumption of energy divided by GDP (kg of oil equivalent per 1000 Euro) | Eurostat (2014) |

| GDP | Gross Domestic Product (constant 2005 US$) | Eurostat (2014) |

| GDPpc | Per capita Gross Domestic Product (constant 2005 US$) | Eurostat (2014) |

| Variable | Obs | Mean | Std. Dev. | Min | Max |

|---|---|---|---|---|---|

| G1 group * | |||||

| ETRev_GDP | 288 | 2.86 | 0.69 | 1.57 | 5.17 |

| ETRev_TAX | 306 | 7.45 | 1.92 | 4.08 | 15.39 |

| ETRev_TOT | 284 | 1.84 × 1010 | 2.05 × 1010 | 1.42 × 108 | 7.26 × 1010 |

| RoL | 323 | 6.50 | 0.41 | 5.35 | 7.00 |

| Govern | 323 | 6.59 | 0.47 | 5.21 | 7.36 |

| ICT | 227 | 2.57 × 1010 | 2.94 × 1010 | 4.19 × 108 | 1.25 × 1011 |

| IMP | 227 | 2.36 × 1011 | 2.47 × 1011 | 3.14 × 109 | 1.27 × 1012 |

| Pub_exp | 210 | 19,964.72 | 14,676.38 | 2097.95 | 82,806.46 |

| GGEpc | 294 | 0.01 | 0.00 | 0.01 | 0.03 |

| GGEsa | 294 | 2.06 | 2.16 | 0.13 | 9.71 |

| Intensity | 281 | 154.39 | 39.12 | 80.04 | 280.72 |

| Altern_En | 319 | 14.40 | 16.13 | 0.00 | 50.73 |

| GDP | 319 | 7.02 × 1011 | 8.30 × 1011 | 4.62 × 109 | 3.07 × 1012 |

| GDPpc | 319 | 36,600.06 | 15,223.3 | 12,407.96 | 87,716.73 |

| G2 group * | |||||

| ETRev_GDP | 160 | 2.503 | 0.592 | 1.180 | 5.040 |

| ETRev_TAX | 170 | 7.674 | 1.584 | 3.720 | 13.420 |

| ETRev_TOT | 160 | 1.94 × 109 | 2.11 × 109 | 1.11 × 108 | 1.02 × 1010 |

| RoL | 170 | 5.522 | 0.417 | 4.543 | 6.217 |

| Govern | 170 | 5.549 | 0.431 | 4.377 | 6.190 |

| ICT | 120 | 5.04 × 109 | 5.48 × 109 | 3.45 × 108 | 1.87 × 1010 |

| IMP | 120 | 4.09 × 1010 | 3.50 × 1010 | 4.92 × 109 | 1.71 × 1011 |

| Pub_exp | 118 | 4363.187 | 4507.579 | 6.236 | 20,167.680 |

| GGEpc | 160 | 0.009 | 0.003 | 0.004 | 0.015 |

| GGEsa | 160 | 0.802 | 0.472 | 0.156 | 1.961 |

| Intensity | 150 | 504.452 | 218.151 | 225.804 | 1411.170 |

| Altern_En | 166 | 14.782 | 11.424 | 0.003 | 44.505 |

| GDP | 170 | 7.99 × 1010 | 8.72 × 1010 | 7.54 × 109 | 4.08 × 1011 |

| GDPpc | 170 | 8841.302 | 4196.107 | 2353.987 | 20,706.67 |

| Country | ETRev_GDP (%) | ETRev_TAX (%) | ETRev_TOT (Mln Euro) | |||

|---|---|---|---|---|---|---|

| Mean | Std. Err. | Mean | Std. Err. | Mean | Std. Err. | |

| G1 group * | ||||||

| Austria | 2.461 | 0.041 | 5.732 | 0.097 | 7290 | 232 |

| Belgium | 2.243 | 0.043 | 5.426 | 0.092 | 8140 | 83 |

| Denmark | 4.617 | 0.093 | 9.457 | 0.161 | 11,400 | 230 |

| Finland | 3.054 | 0.059 | 6.858 | 0.102 | 5600 | 132 |

| France | 2.046 | 0.065 | 4.686 | 0.138 | 41,600 | 491 |

| Germany | 2.346 | 0.042 | 5.973 | 0.122 | 64,800 | 1500 |

| Greece | 2.423 | 0.097 | 7.552 | 0.340 | 5240 | 93 |

| Ireland | 2.492 | 0.040 | 8.381 | 0.122 | 4910 | 165 |

| Italy | 2.961 | 0.081 | 7.075 | 0.197 | 51,000 | 823 |

| Luxembourg | 2.749 | 0.050 | 7.221 | 0.124 | 949 | 33 |

| Malta | 3.443 | 0.074 | 11.301 | 0.468 | 201 | 6 |

| Netherlands | 3.866 | 0.027 | 9.598 | 0.072 | 24,100 | 656 |

| Norway | 3.133 | 0.103 | 7.349 | 0.248 | 8970 | 123 |

| Portugal | 2.901 | 0.080 | 9.268 | 0.312 | 5360 | 95 |

| Spain | 1.972 | 0.060 | 5.848 | 0.175 | 20,500 | 380 |

| Sweden | 2.832 | 0.037 | 5.850 | 0.055 | 9880 | 211 |

| United Kingdom | 2.701 | 0.057 | 7.623 | 0.168 | 57,500 | 791 |

| G2 group * | ||||||

| Bulgaria | 2.649 | 0.160 | 8.690 | 0.513 | 738 | 73 |

| Czech Republic | 2.422 | 0.020 | 7.038 | 0.049 | 3000 | 121 |

| Estonia | 2.140 | 0.117 | 6.634 | 0.336 | 269 | 27 |

| Hungary | 2.868 | 0.054 | 7.426 | 0.145 | 2850 | 73 |

| Latvia | 2.336 | 0.079 | 7.939 | 0.290 | 322 | 22 |

| Lithuania | 2.246 | 0.111 | 7.524 | 0.357 | 505 | 24 |

| Poland | 2.342 | 0.082 | 7.026 | 0.298 | 7140 | 550 |

| Romania | 2.354 | 0.157 | 8.358 | 0.477 | 2150 | 79 |

| Slovak Republic | 2.117 | 0.051 | 6.607 | 0.220 | 1260 | 65 |

| Slovenia | 3.554 | 0.155 | 9.443 | 0.422 | 1180 | 37 |

| Variable | ETR_GDP | ETR_TAX | ETR_TOT | |||||

|---|---|---|---|---|---|---|---|---|

| Panel A—G1 group * | ||||||||

| RoL | 0.937 *** | 1.030 *** | 0.899 *** | 0.965 *** | 1.281 *** | 1.370 *** | 0.937 *** | 1.043 *** |

| (0.256) | (0.261) | (0.258) | (0.262) | (0.271) | (0.274) | (0.258) | (0.261) | |

| ICT | 0.059 *** | 0.074 *** | 0.063 *** | 0.077 *** | 0.028 | 0.036 | 0.059 ** | 0.067 *** |

| (0.040) | (0.024) | (0.024) | (0.024) | (0.026) | (0.027) | (0.025) | (0.025) | |

| IMP | −0.152 *** | −0.165 *** | −0.220 *** | −0.253 *** | −0.273 *** | −0.249 *** | −0.152 *** | −0.122 * |

| (0.039) | (0.042) | (0.067) | (0.067) | (0.065) | (0.067) | (0.063) | (0.064) | |

| Pub_exp | −0.084 *** | −0.113 *** | −0.093 *** | −0.121 *** | −0.132 *** | −0.145 *** | −0.084 *** | −0.098 *** |

| (0.020) | (0.020) | (0.021) | (0.020) | (0.028) | (0.028) | (0.026) | (0.026) | |

| GGEpc | 0.476 *** | .. | 0.418 *** | .. | 0.339 *** | .. | 0.476 *** | .. |

| (0.056) | .. | (0.097) | .. | (0.094) | .. | (0.089) | .. | |

| GGEsa | .. | 0.444 *** | .. | 0.370 *** | .. | 0.373 *** | .. | 0.485 *** |

| .. | (0.900) | .. | (0.100) | .. | (0.106) | .. | (0.101) | |

| Intensity | 0.05 | 0.008 | 0.033 | 0.111 | −0.056 | −0.038 | 0.05 | −0.058 |

| (0.122) | (0.123) | (0.138) | (0.136) | (0.139) | (0.150) | (0.131) | (0.143) | |

| Altern_En | 0.075 *** | 0.083 *** | 0.084 *** | 0.094 *** | 0.035 | 0.035 | 0.075 *** | 0.074 *** |

| (0.020) | (0.021) | (0.022) | (0.022) | (0.024) | (0.024) | (0.022) | (0.023) | |

| GDP | .. | .. | .. | .. | 0.475 *** | 0.348 * | 0.999 *** | 0.819 *** |

| .. | .. | .. | .. | (0.188) | (0.207) | (0.179) | (0.197) | |

| GDPpc | .. | .. | 0.296 | 0.395 * | .. | .. | .. | .. |

| .. | .. | (0.237) | (0.236) | .. | .. | .. | .. | |

| constant | 4.862 *** | 2.404 | 2.857 | 0.114 | −3.500 | −2.890 | 4.871 | 6.401 |

| (1.845) | (1.650) | (2.439) | (2.133) | (4.508) | (4.905) | (4.283) | (4.665) | |

| R−sq | 0.68 | 0.66 | 0.68 | 0.67 | 0.62 | 0.61 | 0.55 | 0.55 |

| F−test | 37.1 | 34.76 | 32.8 | 31.21 | 26 | 24.58 | 20.06 | 18.78 |

| prob. | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 |

| Obs | 148 | 148 | 148 | 148 | 148 | 148 | 148 | 148 |

| Panel B—G2 group * | ||||||||

| RoL | 0.592 | 0.705 | 0.692 | 0.687 | −0.248 | −0.045 | 0.086 | 0.314 |

| (0.663) | (0.603) | (0.661) | (0.703) | (0.554) | (0.498) | (0.601) | (0.532) | |

| ICT | −0.052 | −0.059 | −0.051 | −0.052 | −0.024 | −0.028 | −0.046 | 0.314 |

| (0.051) | (0.050) | (0.050) | (0.052) | (0.044) | (0.044) | (0.048) | (0.532) | |

| IMP | 0.069 | 0.072 | 0.054 | 0.092 | −0.024 | −0.072 | −0.086 | −0.056 |

| (0.088) | (0.094) | (0.085) | (0.102) | (0.044) | (0.109) | (0.133) | (0.047) | |

| Pub_exp | −0.059 *** | −0.057 *** | −0.056 *** | −0.059 *** | −0.026 * | −0.026 * | −0.041 *** | −0.036 *** |

| (0.018) | (0.018) | (0.0187 | (0.019) | (0.015) | (0.016) | (0.018) | (0.018) | |

| GGEpc | 0.094 | .. | 0.318 | .. | 0.076 | .. | 0.257 *** | .. |

| (0.167) | .. | (0.244) | .. | (0.113) | .. | (0.110) | .. | |

| GGEsa | .. | 0.045 | .. | 0.001 | .. | 0.012 | .. | 0.164 *** |

| .. | (0.111) | .. | (0.141) | .. | (0.070) | .. | (0.067) | |

| Intensity | −0.055 | −0.04 | −0.315 | −0.001 | −0.056 | −0.022 | −0.142 | −0.097 |

| (0.151) | (0.146) | (0.277) | (0.225) | (0.114) | (0.105) | (0.120) | (0.107) | |

| Altern_En | 0.051 *** | 0.047 *** | 0.057 *** | 0.053 *** | 0.027 ** | 0.024 ** | 0.041 *** | 0.025 ** |

| (0.017) | (0.016) | (0.018) | (0.018) | (0.012) | (0.012) | (0.012) | (0.011) | |

| GDP | .. | .. | .. | .. | 0.087 | 0.066 | 1.103 *** | 1.017 *** |

| .. | .. | .. | .. | (0.085) | (0.083) | (0.092) | (0.087) | |

| GDPpc | .. | .. | −0.242 | 0.011 | .. | .. | .. | .. |

| .. | .. | (0.237) | (0.204) | .. | .. | .. | .. | |

| constant | 0.530 | −0.124 | 5.494 | −1.081 | 4.247 | 3.119 | 3.616 | 3.04 |

| (3.504) | (3.080) | (5.456) | (3.859) | (2.664) | (2.411) | (2.812) | (2.512) | |

| R−sq | 0.25 | 0.25 | 0.23 | 0.26 | 0.12 | 0.13 | 0.61 | 0.60 |

| Wald(chi)2 | 26.9 | 26.42 | 26.57 | 28.07 | 16.45 | 15.79 | 238.46 | 2142.51 |

| prob. | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 |

| Obs | 100 | 100 | 100 | 100 | 100 | 100 | 100 | 100 |

© 2018 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Castiglione, C.; Infante, D.; Smirnova, J. Non-trivial Factors as Determinants of the Environmental Taxation Revenues in 27 EU Countries. Economies 2018, 6, 7. https://doi.org/10.3390/economies6010007

Castiglione C, Infante D, Smirnova J. Non-trivial Factors as Determinants of the Environmental Taxation Revenues in 27 EU Countries. Economies. 2018; 6(1):7. https://doi.org/10.3390/economies6010007

Chicago/Turabian StyleCastiglione, Concetta, Davide Infante, and Janna Smirnova. 2018. "Non-trivial Factors as Determinants of the Environmental Taxation Revenues in 27 EU Countries" Economies 6, no. 1: 7. https://doi.org/10.3390/economies6010007

APA StyleCastiglione, C., Infante, D., & Smirnova, J. (2018). Non-trivial Factors as Determinants of the Environmental Taxation Revenues in 27 EU Countries. Economies, 6(1), 7. https://doi.org/10.3390/economies6010007