Influence of Real Exchange Rate on the Finance-Growth Nexus in the West African Region

Abstract

:1. Introduction

2. Data and Methodology

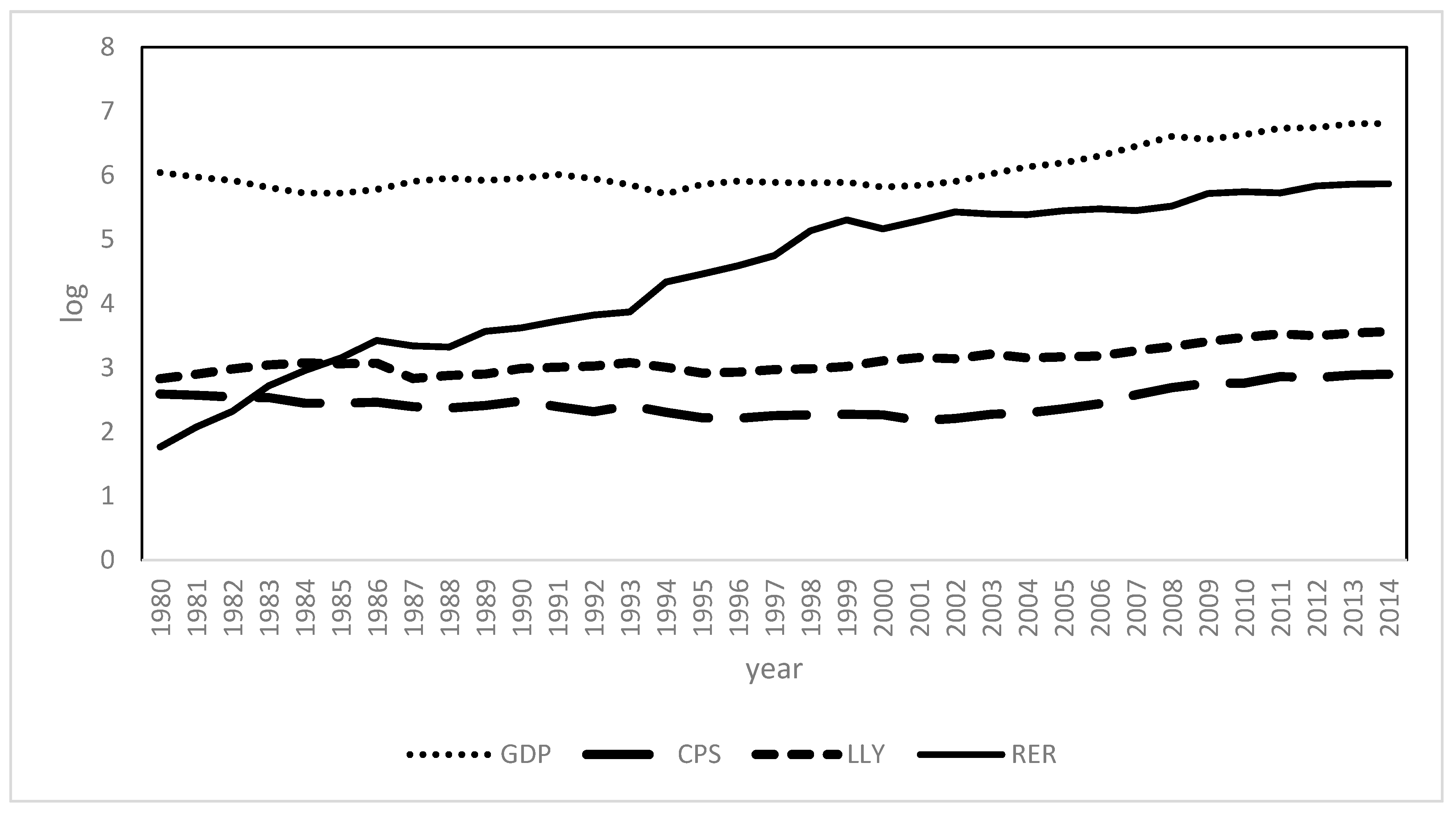

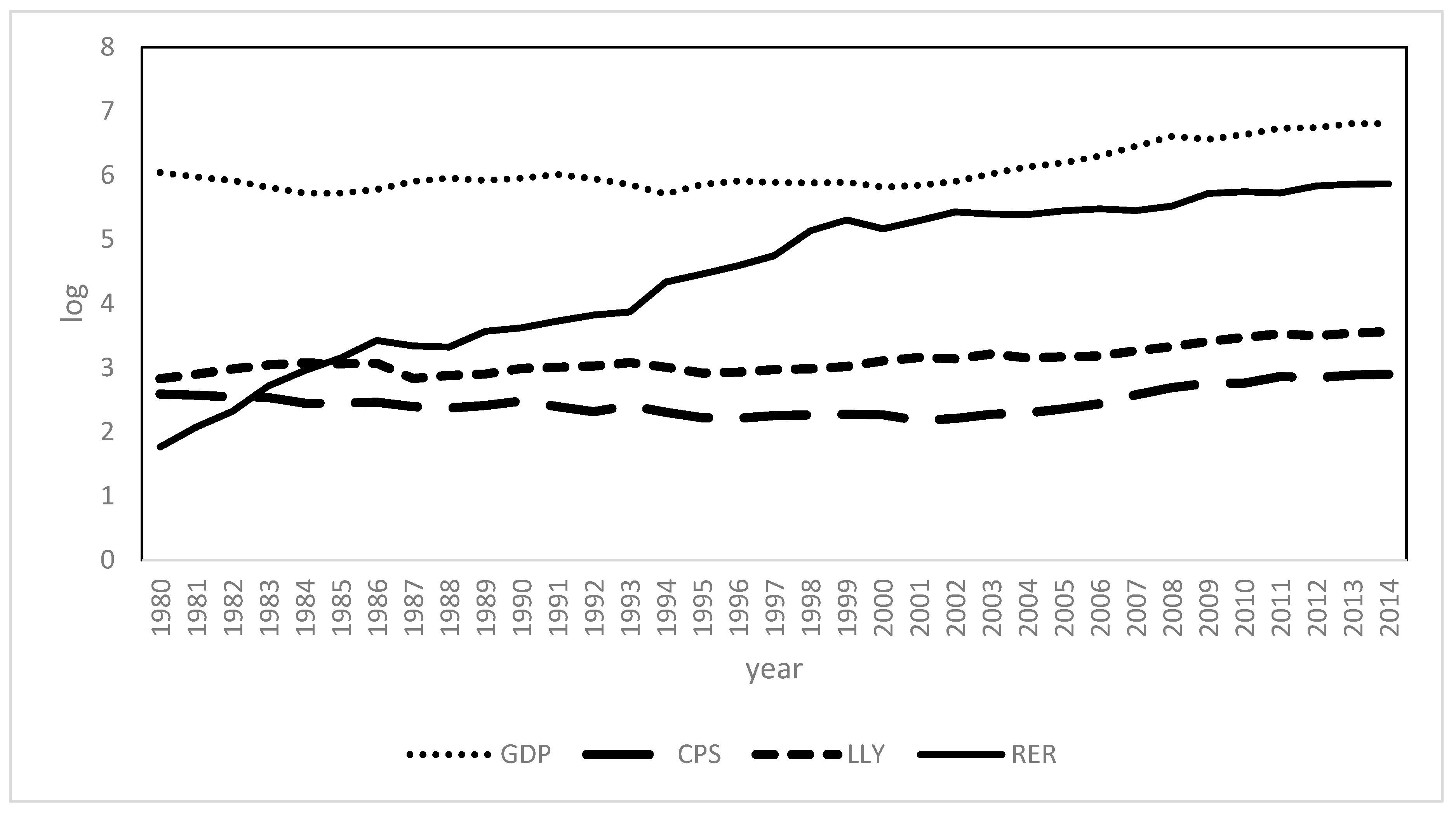

2.1. Data Description

2.2. Model Specification

2.3. Justification of the Variables in the Model

2.4. Estimation Techniques

3. Empirical Results

3.1. Preliminary Data Analysis

3.1.1. Summary of Descriptive Statistics and Correlations

3.1.2. Panel Unit Root Tests

3.2. Estimation Results

3.2.1. Panel Estimation Results

3.2.2. Robustness Checks

3.2.3. SUR Estimation Results for Individual Country

4. Discussion and Policy Implications

5. Conclusions

Author Contributions

Funding

Conflicts of Interest

References

- Aghion, Philippe, Philippe Bacchetta, Romain Ranciere, and Kenneth Rogoff. 2009. Exchange Rate Volatility and Productivity Growth: The Role of Financial Development. Journal of Monetary Economics 56: 494–513. [Google Scholar] [CrossRef]

- Arcand, Jean, Enrico Berkes, and Ugo Panizza. 2015. Too much finance? Journal of Economic Growth 20: 105–48. [Google Scholar] [CrossRef]

- Asongu, Simplice. 2014. Law, Finance and Investment: Does legal origin matter in Africa? The Review of Black Political Economy 41: 145–75. [Google Scholar] [CrossRef]

- Bai, Jushan, and Pierre Perron. 2003. Computation and analysis of multiple structural change models. Journal of Applied Econometrics 18: 1–22. [Google Scholar] [CrossRef] [Green Version]

- Beck, Thorsten, Ross Levine, and Norman Loayza. 2000. Finance and the Sources of Growth. Journal of Financial Economics 58: 261–300. [Google Scholar] [CrossRef]

- Bittencourt, Manoel. 2011. Inflation and Financial Development: Evidence from Brazil. Economic Modelling 28: 91–99. [Google Scholar] [CrossRef]

- Bleaney, Michael, and David Greenaway. 2001. The impact of terms of trade and real exchange rate volatility on investment and growth in sub-Saharan Africa. Journal of Development Economics 65: 491–500. [Google Scholar] [CrossRef]

- Brambor, Thomas, William Clark, and Matt Golder. 2006. Understanding interaction models: Improving empirical analyses. Political Analysis 14: 63–82. [Google Scholar] [CrossRef]

- Comunale, Mariarosaria. 2017. Dutch disease, real effective exchange rate misalignments and their effect on GDP growth in EU. Journal of International Money and Finance 73: 350–70. [Google Scholar] [CrossRef]

- Conrad, Daren, and Jaymieon Jagessar. 2018. Real Exchange Rate Misalignment and Economic Growth: The Case of Trinidad and Tobago. Economies 6: 52. [Google Scholar] [CrossRef]

- Demetriades, Panicos, and Hook Siong Law. 2006. Finance, institutions and economic development. International Journal of Finance and Economics 11: 245. [Google Scholar] [CrossRef]

- Economic Data. 2016. Published by the Federal Reserve Bank of St Louis, USA. Available online: https://fred.stlouisfed.org (accessed on 20 October 2016).

- Ehigiamusoe, Kizito Uyi, and Hooi Hooi Lean. 2018. Finance-growth nexus: New insights from West African Region. Emerging Markets Finance and Trade 54: 2596–613. [Google Scholar] [CrossRef]

- Ehigiamusoe, Kizito Uyi, Hooi Hooi Lean, and Chien-Chiang Lee. 2018. Moderating effect of inflation on the finance–growth nexus: Insights from West African countries. Empirical Economics, 1–24. [Google Scholar] [CrossRef]

- Elbadawi, Ibrahim, Linda Kaltani, and Raimundo Soto. 2012. Aid, Real Exchange Rate Misalignment, and Economic Growth in Sub-Saharan Africa. World Development 40: 681–700. [Google Scholar] [CrossRef]

- Fujiwara, Ippei, and Yuki Teranishi. 2011. Real exchange rate dynamics revisited: A case with financial market imperfections. Journal of International Money and Finance 30: 1562–89. [Google Scholar] [CrossRef]

- Gala, Paulo. 2008. Real exchange rate levels and economic development: Theoretical analysis and econometric evidence. Cambridge Journal of Economics 32: 273–88. [Google Scholar] [CrossRef]

- Gries, Thomas, Manfred Kraft, and Daniel Meierrieks. 2009. Linkages between financial deepening, trade openness, and economic development: causality evidence from Sub-Saharan Africa. World Development 37: 1849–60. [Google Scholar] [CrossRef]

- Habib, Maurizio, Elitza Mileva, and Livio Stracca. 2017. The real exchange rate and economic growth: Revisiting the case using external instruments. Journal of International Money and Finance 73: 386–98. [Google Scholar] [CrossRef]

- Hassan, Kabir, Benito Sanchez, and Jung Yu. 2011. Financial Development and Economic Growth: New Evidence from Panel Data. The Quarterly Review of Economics and Finance 51: 88–104. [Google Scholar] [CrossRef]

- Human Development Reports. 2015. Human Development Reports 2015 published by the United Nations Development Programme. Available online: http://hdr.undp.org/sites/default/files/2015_human_development_report.pdf (accessed on 20 October 2016).

- Im, Kyung So, Hashem Pesaran, and Yongcheol Shin. 2003. Testing for unit roots in Heterogeneous Panels. Journal of Econometrics 115: 53–74. [Google Scholar] [CrossRef]

- IMF. 2014. World Economic Outlook Database of the International Monetary Fund. Available online: http://www.imf.org/external/pubs/ft/weo/2015/02/weodata/index.aspx (accessed on 20 October 2016).

- Iyke, Bernard. 2018. The real effect of currency misalignment on productivity growth: evidence from middle-income economies. Empirical Economics 55: 1637–59. [Google Scholar] [CrossRef]

- Jayashankar, Malepati, and Badri Narayan Rath. 2017. The dynamic linkage between exchange rate, stock price and interest rate in India. Studies in Economics and Finance 34: 383–406. [Google Scholar] [CrossRef]

- Kar, Muhsin, Saban Nazlıoglu, and Huseyin Agır. 2011. Financial development and economic growth nexus in the MENA countries: Bootstrap panel granger causality analysis. Economic Modelling 28: 685–93. [Google Scholar] [CrossRef]

- Karimo, Tari, and Oliver Ogbonna. 2017. Financial deepening and economic growth nexus in Nigeria: Supply-leading or demand-following? Economies 5: 4. [Google Scholar] [CrossRef]

- Katusiime, Lorna. 2018. Private Sector Credit and Inflation Volatility. Economies 6: 1. [Google Scholar] [CrossRef]

- Katusiime, Lorna. 2019. Investigating Spillover Effects between Foreign Exchange Rate Volatility and Commodity Price Volatility in Uganda. Economies 7: 1. [Google Scholar] [CrossRef]

- Khan, Moshin, and Abdelhak Senhadji. 2003. Financial development and economic growth: A review and new evidence. Journal of African Economies 12: 89–110. [Google Scholar] [CrossRef]

- King, Robert, and Ross Levine. 1993. Finance, Entrepreneurship and Growth: Theory and Evidence. Journal of Monetary and Economics 32: 513–42. [Google Scholar] [CrossRef]

- La Porta, Rafael, Florence Lopez-de-Silanes, Andrei Shleifer, and Robert Vishny. 1997. Legal Determinants of External Finance. Journal of Finance 52: 1131–50. [Google Scholar] [CrossRef]

- Law, Siong Hook, and Nirvikar Singh. 2014. Does too much Finance Harm Economic Growth? Journal of Banking and Finance 41: 36–44. [Google Scholar] [CrossRef]

- Law, Siong Hook, Ali Kutan, and Ahmad Mohd Naseem. 2018. The role of institutions in finance curse: Evidence from international data. Journal of Comparative Economics 46: 174–91. [Google Scholar] [CrossRef]

- Levin, Andrew, Chien-Fu Lin, and Chia-Shang Chu. 2002. Unit Root Tests in Panel Data: Asymptotic and Finite-sample Properties. Journal of Econometrics 108: 1–24. [Google Scholar] [CrossRef]

- Levine, Ross, and Sara Zervos. 1998. Stock Markets, Banks and Economic Growth. American Economic Review 88: 537–58. [Google Scholar]

- Levine, Ross, Norman Loayza, and Thorsten Beck. 2000. Financial Intermediation and Growth: Causality and Causes. Journal of Monetary Economics 46: 31–77. [Google Scholar] [CrossRef]

- Lin, Shu, and Haichun Ye. 2011. The role of financial development in exchange rate regime choices. Journal of International Money and Finance 30: 641–59. [Google Scholar] [CrossRef]

- Loayza, Norman, and Romain Ranciere. 2006. Financial development, financial fragility, and growth. Journal of Money, Credit and Banking 38: 1051–76. [Google Scholar] [CrossRef]

- Maddala, Gangadharrao, and Shaowen Wu. 1999. A comparative study of unit root tests with panel data and a new simple test. Oxford Bulletin of Economics and Statistics 61: 631–52. [Google Scholar] [CrossRef]

- Pesaran, Hashem. 2006. Estimation and inference in large heterogeneous panels with a multifactor error structure. Econometrica 74: 967–1012. [Google Scholar] [CrossRef]

- Pesaran, Hashem. 2007. A simple panel unit root test in the presence of cross-section dependence. Journal of Applied Econometrics 22: 265–312. [Google Scholar] [CrossRef] [Green Version]

- Pesaran, Hashem, and Ron Smith. 1995. Estimating long-term relationships from dynamic heterogeneous panels. Journal of Econometrics 68: 79–113. [Google Scholar] [CrossRef]

- Pesaran, Hashem, Yongcheol Shin, and Ron Smith. 1999. Pooled mean group estimation of dynamic heterogeneous panels. Journal of the American Statistical Association 94: 621–34. [Google Scholar] [CrossRef]

- Rapetti, Martin, Peter Skott, and Arslan Razmi. 2012. The real exchange rate and economic growth: are developing countries different? International Review of Applied Economics 26: 735–53. [Google Scholar] [CrossRef]

- Ratsimalahelo, Zaka, and Mamadou Barry. 2010. Financial development and economic growth: Evidence from West Africa. Economics Bulletin 30: 2996–3009. [Google Scholar]

- Rautava, Jouko. 2004. The role of oil prices and the real exchange rate in Russia’s economy—A cointegration approach. Journal of Comparative Economics 32: 315–27. [Google Scholar] [CrossRef]

- Razmi, Arslan, Martin Rapetti, and Peter Skott. 2012. The real exchange rate and economic development. Structural Change and Economic Dynamics 23: 151–69. [Google Scholar] [CrossRef]

- Rioja, Felix, and Neven Valev. 2004. Finance and the sources of growth at various stages of economic development. Economic Inquiry 42: 127–40. [Google Scholar] [CrossRef]

- Rodriguez, Cesar. 2017. The growth effects of financial openness and exchange rates. International Review of Economics and Finance 48: 492–512. [Google Scholar] [CrossRef]

- Rodrik, Dani. 2008. The real exchange rate and economic growth. Brookings Papers on Economic Activity 2: 365–412. [Google Scholar] [CrossRef]

- Rousseau, Peter, and Paul Wachtel. 2002. Inflation thresholds and the finance–growth nexus. Journal of International Money and Finance 21: 777–93. [Google Scholar] [CrossRef]

- Samargandi, Nahla, Jan Fidrmuc, and Sugata Ghosh. 2015. Is the relationship between financial development and economic growth monotonic? Evidence from a sample of middle-income countries. World Development 68: 66–81. [Google Scholar] [CrossRef]

- Sanogo, Vassiki, and Richard Moussa. 2017. Financial reforms, financial development, and economic growth in the Ivory Coast. Economies 5: 1. [Google Scholar] [CrossRef]

- Serenis, Dimitrios, and Nicholas Tsounis. 2013. Exchange rate volatility and foreign trade: The case for Cyprus and Croatia. Procedia Economics and Finance 5: 677–85. [Google Scholar] [CrossRef]

- Sharifi-Renani, Hosein, and Maryam Mirfatah. 2012. The impact of exchange rate volatility on foreign direct investment in Iran. Procedia Economics and Finance 1: 365–73. [Google Scholar] [CrossRef]

- Tang, Bo. 2015. Real Exchange Rate and Economic Growth in China: A Cointegrated VAR Approach. China Economic Review 34: 293–310. [Google Scholar] [CrossRef]

- Tang, Xiaobo, and Xingyuan Yao. 2018. Do financial structures affect exchange rate and stock price interaction? Evidence from emerging markets. Emerging Markets Review 34: 64–76. [Google Scholar] [CrossRef]

- Tarawalie, Abu. 2010. Real exchange rate behaviour and economic growth: evidence from Sierra Leone. South African Journal of Economic and Management Sciences 13: 8–25. [Google Scholar] [CrossRef]

- Vieira, Flavio, Marcio Holland, Cleomar da Silva, and Luiz Bottecchia. 2013. Growth and Exchange Rate Volatility: A Panel Data Analysis. Applied Economics 45: 3733–41. [Google Scholar] [CrossRef]

- Wallack, Jessica. 2003. Structural breaks in Indian macroeconomic data. Economic and Political Weekly 38: 4312–15. [Google Scholar]

- World Development Indicators. 2016. Published by the World Bank. Available online: https://datacatalog.worldbank.org/dataset/world-development-indicators (accessed on 20 October 2016).

- World Economic Outlook. 2015. Published by the International Monetary Fund. Available online: https://www.imf.org/external/pubs/ft/weo/2016/01/weodata/index.aspx (accessed on 20 October 2016).

- Zellner, Arnold. 1962. An efficient method of estimating seemingly unrelated regressions and tests for aggregation bias. Journal of American Statistical Association 57: 348–68. [Google Scholar] [CrossRef]

| 1 | We attempt to use different frequency data such as quarterly or monthly data to check the robustness of our annual data; unfortunately, the quarterly or monthly data for all variables in our model are unavailable for the sample period. When the quarterly or monthly data become readily available in the future, further research could utilize them for comparison. |

| 2 | The real exchange rate between West Africa currencies and the United States dollar is the product of the nominal exchange rate (the units of West Africa currencies given up for one United States dollar) and the ratio of consumer price index between West Africa and United States. The core equation is RER = eP*/P, where e = the nominal West Africa currencies − US dollar exchange rate, P* = the consumer price index in West Africa, and P = the consumer price index in the United States. |

| 3 | We thank the anonymous reviewer for this comment. We are aware that, at a low level of financial development (proxy by credit to the private sector relative to GDP), an increase in credit to the private sector could suggest a higher financial development and probably greater economic growth. However, at a high level of financial development, an increase in credit to the private sector (e.g., from 150% to 200% of GDP) may not indicate a positive development in the financial sector, rather it might probably suggest that the financial sector could undermine economic growth (see Arcand et al. 2015; Law and Singh 2014; Samargandi et al. 2015; Law et al. 2018). Specifically, Arcand et al. (2015) showed that the impact of financial development on economic growth turns negative when financial development (proxy by credit to the private sector) reaches 100% of GDP. However, our study focuses on developing economies of the West African region with a relatively low level of financial development as indicated in Table 1. It shows that the average credit to the private sector relative to GDP was 15.4%, while liquid liabilities relative to GDP were 25.6% during the 1980–2014 period. Therefore, financial system development in the West African region has not reached the level of excessive financial development, which could undermine economic growth in the region. |

| 4 | Although credit to the private sector relative to GDP and liquid liabilities relative to GDP are the two most commonly used proxies of financial development in the literature, but unavailability of data on other proxies (e.g., stock market indicators, commercial-central bank assets, etc.) in the West African region limited our choice of proxies. |

| 5 | Hence, the results of the MG model are not presented to conserve space but available upon request. |

| 6 | The results are not reported to conserve space, but available upon request. |

| 7 | The results of the SUR model with the linear real exchange rate are not reported to conserve space, but available upon request. The results are similar to the ones presented in Table 6, as the interaction term enters with a negative coefficient in 12 countries. |

| 8 | The approach employed in this study is to examine the impact of real exchange rate and its volatility on the finance-growth nexus in the West African region. It is not proposed for forecasting. |

{kind=link}

| Variables | Y | CPS | LLY | GOV | TOP | HCA | INF | RER | RERV |

|---|---|---|---|---|---|---|---|---|---|

| Minimum | 64.810 | 0.802 | 0.416 | 3.542 | 6.320 | 0.400 | −35.525 | 0.001 | 0.535 |

| Mean | 566.729 | 15.432 | 25.642 | 14.807 | 68.979 | 2.602 | 11.858 | 1144.32 | 61.667 |

| Maximum | 3766.11 | 65.278 | 83.026 | 54.515 | 321.63 | 7.004 | 178.70 | 88103.8 | 3939.1 |

| Standard Dev. | 527.875 | 10.774 | 12.759 | 5.926 | 34.172 | 1.481 | 19.030 | 5281.9 | 412.87 |

| CPS | 0.630 *** | ||||||||

| LLY | 0.692 *** | 0.696 *** | |||||||

| GOV | 0.112 ** | 0.390 *** | 0.172 *** | ||||||

| TOP | 0.112 ** | 0.217 *** | 0.244 *** | 0.145 *** | |||||

| HCA | 0.370 *** | 0.200 *** | 0.275 *** | −0.200 *** | 0.301 *** | ||||

| INF | −0.187 *** | −0.295 *** | −0.267 *** | −0.295 *** | −0.036 | 0.074 | |||

| RER | −0.066 ** | −0.172 *** | −0.132 *** | −0.156 *** | −0.124 *** | −0.058 | 0.054 | ||

| RERV | −0.078 ** | −0.059 | −0.046 | −0.054 | 0.129 *** | −0.097 ** | 0.105 ** | −0.031 |

| Variables | ADF–Fisher | PP–Fisher | LLC | IPS | Pesaran |

|---|---|---|---|---|---|

| Y | 12.068 | 9.606 | 2.203 | 3.183 | −1.457 * |

| CPS | 27.357 | 27.059 | −1.109 | −0.059 | −0.541 |

| LLY | 33.193 | 31.748 | 0.317 | 0.215 | −2.662 ** |

| RER | 48.882 ** | 92.522 *** | −4.376 *** | −2.224 ** | −2.549 ** |

| RERV | 55.457 *** | 44.719 * | −2.788 *** | −3.102 *** | −0.793 |

| GOV | 78.280 *** | 84.061 *** | −2.533 *** | −1.361 * | −3.235 *** |

| TOP | 54.206 *** | 55.684 *** | −1.511 * | −2.265 ** | −1.496 * |

| HCA | 9.365 | 11.915 | −0.553 | 5.817 | 4.443 |

| INF | 122.431 *** | 174.348 *** | −7.999 *** | −7.612 *** | −6.787 *** |

| ∆Y | 179.439 *** | 276.720 *** | −9.498 *** | −11.005 *** | −10.704 *** |

| ∆CPS | 180.387 *** | 363.000 *** | −10.724 *** | −10.873 *** | −9.191 *** |

| ∆LLY | 184.236 *** | 286.182 *** | −11.242 *** | −11.267 *** | −9.709 *** |

| ∆RER | 169.106 *** | 257.976 *** | −8.619 *** | −10.494 *** | −8.912 *** |

| ∆RERV | 122.787 *** | 250.541 *** | −8.368 *** | −7.903 *** | −8.647 *** |

| ∆GOV | 228.511 *** | 403.824 *** | −12.234 *** | −13.619 *** | −10.520 *** |

| ∆TOP | 213.345 *** | 366.959 *** | −10.752 *** | −12.801 *** | −9.818 *** |

| ∆HCA | 149.526 *** | 306.169 *** | −3.248 *** | −8.169 *** | −2.831 *** |

| ∆INF | 350.181 *** | 507.739 *** | −16.868 *** | −19.922 *** | −16.381 *** |

| Variables | (1) | (2) | (3) | (4) | (5) |

|---|---|---|---|---|---|

| Long-term coefficients | |||||

| CPS | 0.213 *** (0.047) | 0.615 *** (0.183) | 0.189 (0.436) | 0.423 *** (0.049) | 0.570 *** (0.055) |

| RER | −0.026 (0.261) | ||||

| CPS*RER | −0.049 (0.035) | −0.031 (0.070) | |||

| RERV | 0.079 (0.022) | ||||

| CPS*RERV | −0.001 (0.001) | −0.022 ** (0.009) | |||

| GOV | 0.296 *** (0.107) | −0.099 (0.144) | −0.131 (0.191) | 0.244 ** (0.123) | 0.212 ** (0.116) |

| TOP | 0.447 *** (0.118) | 0.653 *** (0.155) | 0.538 *** (0.206) | 0.829 *** (0.131) | 0.671 *** (0.116) |

| HCA | 0.586 *** (0.195) | −0.164 (0.279) | −0.267 (0.393) | 0.357 ** (0.192) | 0.664 *** (0.219) |

| INF | −0.003 (0.002) | 0.089 *** (0.018) | 0.144 *** (0.039) | 0.003 (0.003) | −0.002 (0.003) |

| Convergence coefficient | −0.224 *** (0.035) | −0.090 *** (0.019) | −0.062 *** (0.013) | −0.228 *** (0.043) | −0.227 *** (0.056) |

| Short-term coefficients | |||||

| ∆CPS | −0.086 (0.048) | 0.644 *** (0.234) | 0.694 (0.482) | −0.061 (0.048) | −0.094 ** (0.049) |

| ∆RER | −0.082 (0.189) | ||||

| ∆CPS*RER | −0.154 *** (0.030) | −0.161 ** (0.069) | |||

| RERV | −0.021 (0.026) | ||||

| ∆CPS*RERV | −0.001 (0.001) | 0.007 (0.009) | |||

| ∆GOV | 0.037 (0.049) | 0.017 (0.049) | 0.018 (0.044) | 0.055 (0.076) | 0.088 (0.073) |

| ∆TOP | −0.301 *** (0.073) | −0.184 *** (0.063) | −0.139 ** (0.067) | −0.304 *** (0.083) | −0.283 *** (0.087) |

| ∆HCA | −0.283 *** (0.108) | −0.237 *** (0.079) | −0.265 *** (0.098) | −0.344 ** (0.147) | −0.439 *** (0.122) |

| ∆INF | −0.001 (0.001) | −0.001 (0.001) | −0.002 (0.001) | −0.002 (0.001) | −0.002 (0.002) |

| Time trend | 0.005 *** (0.001) | 0.006 *** (0.001) | 0.004 *** (0.001) | 0.003 ** (0.002) | 0.002 (0.002) |

| Constant | −0.829 (0.573) | −1.854 *** (0.529) | −1.506 *** (0.376) | −0.905 (0.656) | −0.339 (0.740) |

| Hausman test | 3.47 | 5.90 | 10.41 | 5.20 | 2.07 |

| Log Likelihood | 473.64 | 625.73 | 648.89 | 467.007 | 498.619 |

| Marginal effects | |||||

| Minimum | 1.332 | 0.642 | 0.422 | 0.558 | |

| Mean | 0.397 *** | 0.051 | 0.361 | −0.787 | |

| Maximum | 0.057 | −0.164 | −3.516 | −86.089 | |

| Variables | (1) | (2) | (3) | (4) | (5) |

|---|---|---|---|---|---|

| CPS | 0.339 *** (0.058) | 0.289 *** (0.067) | 0.311 ** (0.133) | 0.502 *** (0.077) | 0.481 *** (0.077) |

| RER | 0.033 (0.032) | ||||

| CPS*RER | −0.006 (0.005) | −0.002 (0.018) | |||

| RERV | −0.002 (0.003) | ||||

| CPS*RERV | −0.001 (0.001) | −0.001 (0.001) | |||

| GOV | −0.148 * (0.089) | −0.119 (0.092) | −0.087 (0.093) | −0.232 * (0.126) | −0.258 * (0.139) |

| TOP | −0.078 (0.072) | −0.072 (0.072) | −0.105 (0.094) | −0.085 (0.115) | −0.168 (0.102) |

| HCA | 0.453 *** (0.035) | 0.476 *** (0.036) | 0.518 *** (0.037) | 0.359 *** (0.067) | 0.422 *** (0.056) |

| INF | −0.006 *** (0.002) | −0.005 *** (0.001) | −0.005 ** (0.001) | −0.005 ** (0.002) | −0.006 ** (0.003) |

| Time Trend | −0.001 *** (0.001) | −0.001 *** (0.001) | −0.001 *** (0.001) | −0.001 *** (0.001) | −0.001 *** (0.001) |

| Constant | 5.963 *** (0.300) | 5.899 *** (0.306) | 5.834 *** (0.188) | 5.941 *** (0.511) | 6.341 *** (0.528) |

| F-test | 1.02 | 7.08 *** | 1.87 * | 6.502 *** | 5.536 *** |

| Eigenvalue stat. | 51.62 *** | 52.28 *** | 64.69 *** | 50.647 *** | 49.332 *** |

| Marginal effects | |||||

| Minimum | 0.377 *** | 0.340 | 0.501 *** | 0.480 *** | |

| Mean | 0.262 *** | 0.302 *** | 0.440 *** | 0.419 *** | |

| Maximum | 0.221 *** | 0.288 | −3.437 *** | −3.458 |

| Variables | (1) | (2) | (3) | (4) | (5) |

|---|---|---|---|---|---|

| Long-term coefficients | |||||

| LLY | 0.566 *** (0.087) | 0.236 (0.259) | −1.735 *** (0.567) | 0.631 *** (0.081) | 0.564 *** (0.082) |

| RER | −1.090 *** (0.271) | ||||

| LLY*RER | 0.071 (0.060) | 0.395 (0.102) | |||

| RERV | −0.009 (0.016) | ||||

| LLY*RERV | −0.001 * (0.001) | 0.003 (0.005) | |||

| GOV | 0.144 (0.106) | −0.273 (0.184) | −0.356 ** (0.149) | 0.286 ** (0.135) | 0.229 ** (0.137) |

| TOP | 0.464 *** (0.117) | 0.427 *** (0.194) | 0.470 *** (0.155) | 0.658 *** (0.146) | 0.789 *** (0.155) |

| HCA | 0.688 *** (0.209) | 0.319 (0.384) | 0.460 (0.307) | 0.627 ** (0.257) | 0.606 ** (0.248) |

| INF | −0.004 (0.002) | 0.115 ** (0.026) | 0.081 *** (0.017) | 0.003 (0.003) | −0.006 ** (0.003) |

| Convergence coefficient | −0.199 *** (0.037) | −0.068 *** (0.016) | −0.093 *** (0.019) | −0.205 *** (0.039) | −0.197 *** (0.040) |

| Short-term coefficients | |||||

| ∆LLY | −0.288 *** (0.037) | 0.431 ** (0.227) | −0.237 (0.780) | −0.241 *** (0.076) | −0.236 *** (0.086) |

| ∆RER | −0.312 (0.428) | ||||

| ∆LLY*RER | −0.135 *** (0.028) | −0.034 (0.132) | |||

| ∆RERV | −0.126 (0.107) | ||||

| ∆LLY*RERV | −0.002 (0.001) | 0.038 (0.035) | |||

| ∆GOV | 0.085 (0.057) | 0.043 (0.049) | 0.051 (0.049) | 0.025 (0.076) | 0.042 (0.078) |

| ∆TOP | −0.331 *** (0.075) | −0.183 *** (0.071) | −0.199 *** (0.068) | −0.229 ** (0.091) | −0.251 *** (0.090) |

| ∆HCA | −0.288 *** (0.084) | −0.305 *** (0.088) | −0.295 ** (0.072) | −0.358 ** (0.145) | −0.327 *** (0.116) |

| ∆INF | −0.002 (0.002) | −0.001 (0.001) | −0.001 (0.001) | −0.002 (0.002) | −0.002 (0.002) |

| Time trend | 0.003 (0.002) | 0.003 *** (0.001) | 0.003 *** (0.001) | 0.002 (0.002) | 0.002 (0.002) |

| Constant | −0.686 (0.723) | −0.865 (0.445) | −0.164 (0.449) | −0.817 (0.859) | −0.491 (0.823) |

| Hausman test | 4.80 | 5.47 | 3.70 | 5.30 | 3.83 |

| Log Likelihood | 491.06 | 631.62 | 653.93 | 472.231 | 493.481 |

| Country | CPS | CPS*RER | GOV | TOP | HCA | INF | Constant | R2 | Marginal Effects | ||

|---|---|---|---|---|---|---|---|---|---|---|---|

| Minimum | Mean | Maximum | |||||||||

| Benin | 0.346 ** (0.148) | −0.017 (0.022) | −0.166 (0.122) | 0.233 * (0.129) | 0.585 *** (0.050) | −0.004 (0.003) | 4.629 *** (0.605) | 0.809 | 0.259 | 0.242 | 0.234 |

| Burkina Faso | 0.771 *** (0.183) | −0.001 (0.028) | 0.505 *** (0.110) | 0.525 *** (0.135) | −1.475 (1.979) | 0.001 (0.004) | 0.747 (0.659) | 0.790 | 0.766 | 0.765 | 0.764 |

| Cape Verde | 1.790 *** (0.289) | −0.296 *** (0.063) | 0.515 (0.464) | 0.319 (0.230) | 0.246 (0.574) | −0.022 *** (0.007) | 2.774 (1.835) | 0.905 | 0.718 | 0.520 | 0.364 |

| Cote d’Ivoire | 0.588 *** (0.103) | −0.088 *** (0.023) | −0.018 (0.117) | 0.463 *** (0.116) | 0.403 *** (0.065) | −0.002 (0.003) | 4.281 *** (0.687) | 0.659 | 0.152 | 0.067 | 0.010 |

| Gambia | −0.245 *** (0.041) | −0.046 *** (0.012) | 0.029 (0.055) | −0.583 *** (0.083) | 0.262 ** (0.106) | −0.009 *** (0.001) | 9.342 *** (0.316) | 0.871 | −0.191 | −0.332 | −0.422 |

| Ghana | 0.122(0.139) | 0.051 *** (0.014) | 0.454 *** (0.147) | −0.554 ** (0.117) | 1.128 ** (0.518) | −0.002 (0.001) | 5.534 *** (0.726) | 0.751 | −0.624 | −0.101 | 0.173 |

| Guinea | 0.306 *** (0.109) | −0.023 *** (0.008) | 0.089 (0.074) | −0.129 (0.109) | 0.558 *** (0.190) | −0.003 *** (0.001) | 5.954 *** (0.429) | 0.187 | 0.238 | 0.154 | 0.092 |

| Guinea-Bissau | −0.329 *** (0.108) | 0.051 *** (0.019) | −0.141 (0.115) | −0.086 (0.225) | 1.486 (1.392) | −0.005 *** (0.002) | 5.319 *** (1.566) | 0.494 | −0.231 | −0.069 | 0.007 |

| Liberia | 0.088 (0.116) | 0.178 *** (0.019) | −0.262 * (0.146) | 0.197 ** (0.099) | −2.811 *** (0.337) | −0.018 (0.017) | 7.065 *** (0.628) | 0.657 | 0.010 | 0.451 | 0.917 |

| Mali | 0.637 *** (0.146) | −0.096 *** (0.019) | −0.065 (0.075) | −0.339 *** (0.101) | 0.701 *** (0.032) | −0.002 (0.002) | 7.255 *** (0.476) | 0.913 | 0.124 | 0.052 | 0.004 |

| Mauritania | −0.766 *** (0.177) | −0.012 (0.018) | −0.196 *** (0.049) | 0.081 (0.073) | 0.808 *** (0.204) | −0.001 (0.005) | 8.653 *** (0.682) | 0.825 | −0.806 | −0.820 | −0.835 |

| Niger | 0.842 *** (0.143) | −0.101 *** (0.025) | 0.008 (0.113) | 0.487 *** (0.098) | 0.150 *** (0.056) | −0.003 (0.002) | 3.187 *** (0.548) | 0.789 | 0.312 | 0.228 | 0.175 |

| Nigeria | −0.018 (0.241) | 0.026 ** (0.012) | 0.342 (0.225) | −0.501 ** (0.256) | 8.809 *** (3.268) | −0.012 *** (0.004) | −6.583 (5.959) | 0.591 | −0.151 | 0.013 | 0.121 |

| Senegal | 1.333 *** (0.230) | −0.099 *** (0.030) | −1.394 *** (0.307) | −0.341 ** (0.147) | 0.585 *** (0.116) | 0.001 (0.003) | 8.739 *** (0.892) | 0.663 | 0.822 | 0.732 | 0.676 |

| Sierra Leone | 0.626 *** (0.122) | −0.025 ** (0.013) | 0.146 (0.239) | −0.301 ** (0.136) | 0.717 *** (0.229) | −0.001 (0.001) | 5.492 *** (0.632) | 0.676 | 0.625 | 0.431 | 0.341 |

| Togo | 0.697 *** (0.147) | −0.067 *** (0.022) | −0.179 (0.140) | 0.140 (0.106) | 0.421 *** (0.081) | −0.001 (0.002) | 4.304 *** (0.453) | 0.634 | 0.360 | 0.300 | 0.258 |

| LM Test | 466.287 *** | ||||||||||

| Country | CPS | CPS*RERV | RERV | GOV | TOP | HCA | INF | Constant | R2 | Marginal Effects | ||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Minimum | Mean | Maximum | ||||||||||

| Benin | 0.426 *** (0.069) | −0.072 *** (0.016) | 0.164 *** (0.037) | 0.049 (0.126) | 0.134 (0.092) | 0.678 *** (0.052) | −0.008 *** (0.002) | 3.919 *** (0.384) | 0.922 | 0.362 | 0.179 | −0.432 |

| Burkina Faso | 1.145 *** (0.139) | −0.152 *** (0.029) | 0.327 *** (0.073) | −0.145 (0.192) | 0.336 *** (0.106) | −3.656 *** (1.312) | 0.001 (0.003) | 3.151 *** (0.686) | 0.885 | 1.025 | 0.736 | −0.077 |

| Cape Verde | 0.529 *** (0.072) | −0.101 *** (0.027) | 0.208 *** (0.068) | −0.212 (0.315) | 0.455 ** (0.207) | 0.655 (0.581) | −0.002 (0.008) | 3.666 ** (1.507) | 0.746 | 0.424 | 0.333 | 0.144 |

| Cote d’Ivoire | 0.481 ** (0.190) | −0.025 (0.087) | 0.079 (0.238) | −0.042 (0.132) | 0.583 *** (0.193) | 0.457 *** (0.113) | −0.008 ** (0.004) | 2.552 ** (1.188) | 0.772 | 0.462 | 0.418 | 0.278 |

| Gambia | −0.132 * (0.072) | 0.001 ** (0.001) | −0.001 *** (0.001) | 0.269 *** (0.074) | −0.222 * (0.128) | −0.142 (0.103) | −0.017 *** (0.003) | 7.087 *** (0.552) | 0.900 | −0.131 | 0.548 | 3.807 |

| Ghana | 0.586 *** (0.138) | −0.009 (0.010) | 0.029 (0.028) | 0.659 *** (0.147) | −1.354 *** (0.156) | 1.904 *** (0.411) | −0.002 (0.002) | 5.747 *** (0.716) | 0.896 | 0.573 | 0.378 | −0.463 |

| Guinea | 0.216 * (0.121) | −0.039 (0.025) | 0.054 (0.035) | 0.131 (0.088) | −0.309 *** (0.113) | 0.383 ** (0.197) | 0.002 (0.002) | 6.538 *** (0.409) | 0.219 | 0.172 | −0.100 | −0.597 |

| Guinea-Bissau | 0.059 (0.056) | 0.003 (0.004) | −0.016 (0.011) | 0.695 *** (0.176) | −0.016 (0.205) | 3.449 *** (1.335) | 0.001 (0.002) | 1.171 (1.566) | 0.484 | 0.060 | 0.085 | 0.165 |

| Liberia | −0.164 (0.236) | −0.002 ** (0.001) | 0.003 ** (0.001) | 0.247 (0.269) | −0.001 (0.231) | 0.492 (0.563) | −0.059 ** (0.029) | 5.137 *** (1.119) | 0.241 | −0.165 | −0.447 | −1.669 |

| Mali | 0.249 (0.182) | 0.002 (0.037) | 0.007 (0.095) | −0.007 (0.175) | −0.803 *** (0.186) | 0.568 *** (0.070) | −0.002 (0.004) | 8.372 *** (0.861) | 0.852 | 0.250 | 0.254 | 0.264 |

| Mauritania | −0.906 ** (0.474) | −0.069 (0.296) | 0.144 (0.985) | −0.398 *** (0.071) | 0.384 *** (0.094) | 0.272 (0.184) | −0.006 (0.005) | 8.918 *** (1.722) | 0.871 | −0.942 | −1.067 | −1.241 |

| Niger | 0.427 *** (0.059) | −0.021 (0.018) | 0.049 ** (0.026) | 0.219 ** (0.109) | 0.221 ** (0.104) | 0.242 *** (0.086) | −0.007 ** (0.003) | 3.225 *** (0.522) | 0.863 | 0.410 | 0.368 | 0.236 |

| Nigeria | −0.079 (0.262) | −0.004 ** (0.002) | 0.007 (0.005) | 0.607 ** (0.303) | −0.092 (0.264) | 14.96 *** (3.156) | −0.006 (0.042) | −18.35 *** (5.631) | 0.606 | −0.081 | −0.429 | −1.931 |

| Senegal | 0.726 *** (0.130) | −0.025 (0.038) | 0.081 (0.105) | 0.409 * (0.229) | 0.689 *** (0.191) | 0.392 *** (0.102) | −0.007 ** (0.003) | −0.135 (1.054) | 0.823 | 0.711 | 0.660 | 0.516 |

| Sierra Leone | 0.468 *** (0.157) | −0.016 * (0.009) | 0.011 (0.011) | −0.132 (0.232) | −0.069 (0.132) | 0.753 *** (0.205) | −0.001 (0.001) | 5.216 *** (0.625) | 0.767 | 0.404 | 0.223 | −0.281 |

| Togo | 0.601 *** (0.136) | −0.139 * (0.081) | 0.393 * (0.232) | −0.018 (0.130) | 0.195 ** (0.103) | 0.202 * (0.111) | −0.002 (0.003) | 3.112 *** (0.535) | 0.707 | 0.476 | 0.211 | −0.679 |

| LM Test | 358.366 *** | |||||||||||

© 2019 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Ehigiamusoe, K.U.; Lean, H.H. Influence of Real Exchange Rate on the Finance-Growth Nexus in the West African Region. Economies 2019, 7, 23. https://doi.org/10.3390/economies7010023

Ehigiamusoe KU, Lean HH. Influence of Real Exchange Rate on the Finance-Growth Nexus in the West African Region. Economies. 2019; 7(1):23. https://doi.org/10.3390/economies7010023

Chicago/Turabian StyleEhigiamusoe, Kizito Uyi, and Hooi Hooi Lean. 2019. "Influence of Real Exchange Rate on the Finance-Growth Nexus in the West African Region" Economies 7, no. 1: 23. https://doi.org/10.3390/economies7010023

APA StyleEhigiamusoe, K. U., & Lean, H. H. (2019). Influence of Real Exchange Rate on the Finance-Growth Nexus in the West African Region. Economies, 7(1), 23. https://doi.org/10.3390/economies7010023