1. Introduction

The global economy has faced a sequence of serious challenges in the 21st century. Even though globalisation brought benefits to most stakeholders, the increased interconnectedness of the global economy correspondingly caused several issues. Some of these problems are of a short-term nature (such as the global financial crisis from 2008), while some have long-term features (such as global inequality, sustainable development or terrorism). At the same time, the global economy is predominantly driven by two phenomena, tourism and FDI. The recent decades have seen a powerful boom in touristic development and tourism has been recognised as a global economic driver and one of the fastest growing sectors of the global economy (

UNWTO 2017). FDI has also experienced strong growth and is one of the drivers of economic growth as well and also one of the most salient aspects of globalization (

Li 2008). In addition, the globalization of tourism is occurring simultaneously with the globalization of the world economy predominantly characterised by international capital movements, most notably in the dimension of its external flow and activity. According to the

UNWTO (

2018) World Tourism Barometer, arrivals grew by 7% in 2017 and reached a total of 1.322 billion. This number is expected to reach 1.8 billion by 2030. Tourism accounts for 10.4% of the global GDP and 313 million jobs, i.e., 9.9% total employment in 2017 (

WTTC 2018). Regarding FDI in tourism from 2003 to 2016,

$325 billion in capital expenditure was spent on tourism, and out of 39 sectors, tourism is in tenth place (

Shehadi 2017). However, since 2008 greenfield FDI in tourism has constantly been in decline. From 2003 to 2008 the average greenfield FDI in tourism was

$33.3 million, and since then it has dropped to

$18.9 million (

Shehadi 2017). The brand value of all top ten hotel chains dropped significantly during 2016, and this has been attributed to the rise of the sharing economy (

Atherton 2016). Companies such as Airbnb have made tourism cheaper and easier, but probably at the cost of FDI in tourism (

Shehadi 2017) so they are a threat to the global hospitality industry. Regarding M&A in tourism, the average number of deals in the period from 2012 to 2017 was 327, while the average value was

$78.15 billion (

Haddad 2018). The peak was reached in 2015 with 385 deals and a value of

$200.3 billion (

Haddad 2018). In the context of this paper, it is important to emphasize that the total FDI is more than double in very peaceful countries (

IEP 2018).

The last decade has seen a mild but steady decline in global peace. The number of terrorist incidents has risen nearly 200% since 2011, while casualties resulting from terrorist activities, and casualties caused by terrorism in OECD member states, have increased by 900% since 2007 (

IEP 2018). According to the Global Peace Index (

IEP 2018), the global economic impact of violence increased by 2.1% from 2016 to 2017, equivalent to 12.4% of the global GDP, or

$1988 per person.

Given the strength that tourism has in economic terms at local and global level, the prospect of it being a generator of peace in the world and the fact that tourism development is often associated with the struggle against poverty (

Holden 2013), it is essential to ensure the development of its key elements. This primarily pertains to capital, infrastructure, knowledge and disposal of international marketing and distribution networks whose most efficient developmental driver is FDI in tourism (

Barrowclough et al. 2007). FDI in tourism is especially important for less developed destinations, especially when it comes to investing in human resources and skills (

Shehadi 2017). FDI in tourism has an effect on international tourist arrivals (

Bezić et al. 2010;

Perić and Nikšić Radić 2016;

Selvanathan et al. 2012;

Tang et al. 2007;

Zhang et al. 2011) and thus significantly affects economic growth. Even though FDI in tourism has not until recently been emphasized as a key sector of investment promotional agencies of particular countries, today it plays a key role in their plans and is one of the pillars of sustainable development of the global economy (

Fingar 2017).

FDI, tourism and terrorism have some dominant common features. They surpass national borders, involve stakeholders of different nationalities and are mutually intertwined. FDI and tourism are strongly linked to terrorism because terrorism affects both the movement of tourists and the movement of FDI. Because of its significant role in job creation, tax revenue contribution, and overall impact on economic growth, FDI is a logical choice for attacks (

Lutz and Lutz 2017). International hotels are symbolic targets of western wealth and influence which attract exactly the type of militants who aim to remove foreigners, business travellers, tourists and local elites (

Bharwani and Mathews 2012). Tourists also often become targets of terrorism as they are in a way considered as ambassadors of their countries and easy targets, as well as symbolic indirect representatives of enemy governments. Attacks on foreign tourists and international businesses, i.e., citizens of other countries, guarantees greater media attention to terrorists.

Given the scarcity of existing research and the absence of research involving a causal link between the subject variables, the current study aims to address this research gap. The aim of this paper is to research the causal relationship between terrorism and FDI in tourism on a panel of 50 countries for the period from 2000 to 2016 modelled on research of

Nikšić Radić (

2018). Additionally, in order to ensure the reliability of the research results, certain specific control variables will be included in the testing of causality between the mentioned variables. The authors’ starting point is that terrorism does not affect FDI in tourism. There are several arguments in favour of this. Firstly, the last decade has seen a change in consumer and corporation mentality as they started to behave ‘normally’ as a response to terrorism (

Oaten et al. 2015). One example of the broadening of the global portfolio in times of growing terrorist threats is the

Hongkong and Shanghai Hotels (

2016), which point out that ‘It is an unfortunate reality in today’s world that one can never be 100% protected against terrorists in a free and open society’. Smith Travel Research (STR) data suggested that hotel performances in affected destinations typically started to return to normal three months after an attack, as long as there were no further attacks (

Doggrell 2017). According to

Harper (

2017) head of property services for Hotel Partners Africa, the impact of terror attacks across the world is lessening and, in general, international tourism is resilient to terrorism, recovery times for all types of locations are improving and have shortened significantly over the last 15 years (

Oaten et al. 2015).

The main contribution of this paper is that, for the first time, to the best of the authors’ knowledge, a causality analysis is used to examine the relationship between FDI in tourism and terrorism on a panel of countries. Another contribution of this paper is that it is not based on the premise that terrorism affects FDI in tourism. The third contribution, and the most important one in the authors’ opinion, is that the results of the research point to the fact that, despite the rising nationalist and populistic excesses around the world promoting closing borders because of the fear of spreading terrorism via migration channels, terrorism does not affect FDI in tourism. Terrorism has become one of today’s threats with which life is still normal, either in terms of tourism or in terms of tourism investment and should be treated like this. Like any other threat to global development, it is necessary to approach it with preventive measures to keep it under control in the long term. This article is composed of five sections. After the introduction,

Section 2 presents an overview of the most recent theory on the subject matter.

Section 3 describes the data and methodological framework, whereas

Section 4 focused on the analysis of the results. As a final point, the conclusions and implications for policies are presented in

Section 4.

2. Overview

At the start of the 21st century terrorism became a burning international political problem and it is likely to remain a potential threat to global business (

ATKearney 2015;

EIU 2008). Terrorism asserts insecurity on individuals and governments. Terror attacks have severe consequences on economic activity (gross domestic product, fixed capital formation, export, consumption expenditure) (

Eckstein and Tsiddon 2004), and also on life. The incidence of terrorism appears to be associated with a change in spending from investment towards government expenditures (

Blomberg et al. 2004). In addition, larger economies appear to be less likely to suffer from terrorism attacks (

Kumar and Liu 2015).

Due to the globalisation process, global companies have at least one common feature with terrorism—they are present everywhere (

Krug and Reinmoeller 2003). According to

Mazzarella (

2005), a decline in investment and operations in high-risk regions is the cost of terrorism which companies face. There are also corporations targeting terroristically high-risk countries, i.e., some investment choices may even be motivated by higher yields because of the higher risk the investments are based on (

Asongu et al. 2015).

The relationship between FDI and the political environment is very complex. Political risk affects pre-investment activities of foreign investors and existing FDI (

Feinberg and Gupta 2009). According to

Vargas and Sommer (

2015), political instability occurs through the interaction between three dimensions of political risk—economic instability, institutional instability and ethnic/religious diversity.

Political risk has mostly been equated with political instability and radical political changes in the host country (

Green 1974;

Thunell 1977). Every country showing unequal characteristics presents political risk and potential instability (

Jarvis and Griffiths 2007). The two terms are, however, different. Instability is a characteristic of the general environment, while risk has a somewhat narrower focus that directly affects a foreign corporation or specific project (

Kobrin 1979,

1980). There, the event itself is not important, the event’s effect on business is important (

Chermak 1992). Political stability is not in itself a guarantee for tourism or any other type of industry, especially when there is a lack of favourable economic conditions (

Levis 1979).

When political risk is considered in the context of FDI it can be defined as ‘the probability that political decisions, events or conditions will significantly affect the profitability of a business actor or the expected value of given economic action’ (

Matthee 2011, pp. 2010–11). Contemporary FDI theories treat political risk as the most significant political force affecting patterns in international capital flows, especially in developing countries (

Barry and DiGiuseppe 2018). The term political risk was created within the scope of country risk with the aim of considering the type of insolvency in the country, and it is not directly related to financial or economic factors (

Sottilotta 2017). The effect of political risk varies depending on the industry FDI is oriented towards (

Barry and DiGiuseppe 2018). Research aimed at differences between sectors is scarce and points to the specificities of particular industries (

Blanton and Blanton 2012;

Dunning 1981).

After the 2001 terrorist attack in the USA terrorism became a source of concern for international investors and entered the scene as a type of political risk (

Berry 2007;

Lee 2017). Furthermore, terrorism can be viewed as a category of political violence (

Latif et al. 2017). Political violence is not a homogenous category. According to

Witte et al. (

2017), terrorism represents a discontinuous risk with a high level of impact. Similarly,

Steiner (

2010) views terrorism as violent political unrest when conceptualising dimensions of political risk. There is a well-established strong link between political instability and terrorism (

Sonmez and Graefe 1998). Political stability is one of the key factors in attracting FDI while economic and political shocks are a deterrent (

Metaxas and Kechagia 2017).

Latif et al. (

2017) argue that continuous terrorist attacks probably increase political instability and decrease investments. Terrorist incidents increase risks associated with political instability and through this channel deter FDI (

Bandyopadhyay et al. 2014).

It has already been emphasized that this research does not take as a postulate the necessity of a negative influence of terrorism on FDI in tourism. There are several reasons the authors assumed this stance. Firstly, in an earlier overview of research on political risk,

Kobrin (

1979) concluded that the empirical evidence is inconsistent and presents mixed results regarding the effect of political instability on FDI stocks or flow. Secondly, already in 1983, it was indicated that terrorism in general does not significantly affect FDI, even though it had significant localised effects in places such as the Basque region in Spain or in Northern Ireland (

Crenshaw 1983, p. 6). Ultimately, all subsequent research casts doubt on such a postulate, as displayed in the table below.

As can be seen from

Table 1, available empirical studies have recognized different results considering the relationship between political instability, political risk or just terrorism and FDI.

Schneider and Frey (

1985),

Nigh (

1985),

Globerman and Shapiro (

2003),

Enders et al. (

2006),

Abadie and Gardeazabal (

2008) and

Powers and Choi (

2012) argued that political instability, political risk or terrorism negatively influenced the FDI inflows. Interestingly, certain researches such as

Fatehi-Sedeh and Safizadeh (

1989),

Olibe and Crumbley (

1997),

Li and Resnick (

2003),

Sethi et al. (

2003),

Li (

2006),

Kolstad and Villanger (

2008),

Steiner (

2010),

Blonigen and Piger (

2014) and

Nikšić Radić (

2018) provided evidence that observed variables did not have a significant impact on FDI. Most interesting of all, certain researches such as

Loree and Guisinger (

1995),

Mihalache (

2010),

Tosun et al. (

2014) and

Lutz and Lutz (

2017) provided evidence that observed variables could even contribute to FDI. Research closely related to the impact of terrorism on FDI in tourism is very scarce.

Steiner (

2010) is the only one which links terrorism and FDI in tourism and concludes that a clear link between the observed variables cannot be determined, and

Nikšić Radić (

2018) is the only one which found that terrorism is not significant for attracting FDI in tourism. Bearing in mind the diverse results of research related to the impact of observed variables on the total FDI inflows into the economy, and focusing narrowly on the scarcity of research related to the impact of terrorism on FDI in tourism, it is justified not to start from the premise that terrorism necessarily affects FDI in tourism.

FDI holders take into account political instability when making investment decisions (

Li 2006). When considering the relationship between FDI and terrorism, it should be borne in mind that a foreign investor has a long-term business horizon. Thus, FDI itself becomes a barrier to exit because if the investor decides to disinvest, they cannot do it at no extra cost (

Rivoli and Salorio 1996). This implies that the exit barrier makes the investor anticipate the political and economic development of a potential country or region, including potential political violence and terrorism (

Li 2006). The fact that investors take political instability into account when making investment decisions is further shown in research by

Bass et al. (

1977) and

Porcano (

1993). The level of terrorism risk may influence future business, i.e., expected profit and growth potential. This leads to the conclusion that the scope of the effect of a terrorist attack is not what matters, but the scope of the unexpected effects of that attack (

Hallberg 2016). A large anticipated attack will ultimately become internalised and have less consequences, while a small unanticipated attack will have more severe consequences because it will not be internalised (

Li 2006). FDI in tourism is mostly oriented towards large hotel complexes (

Barrowclough et al. 2007), so it is likely that such investments take into account the long-term business horizon and that market risk analyses definitely consider potential political instability, including possible terrorist attacks in that country. Terrorist attacks are one of the external risks which particularly affect the hotel business (

Bharwani and Mathews 2012).

4. Research Results

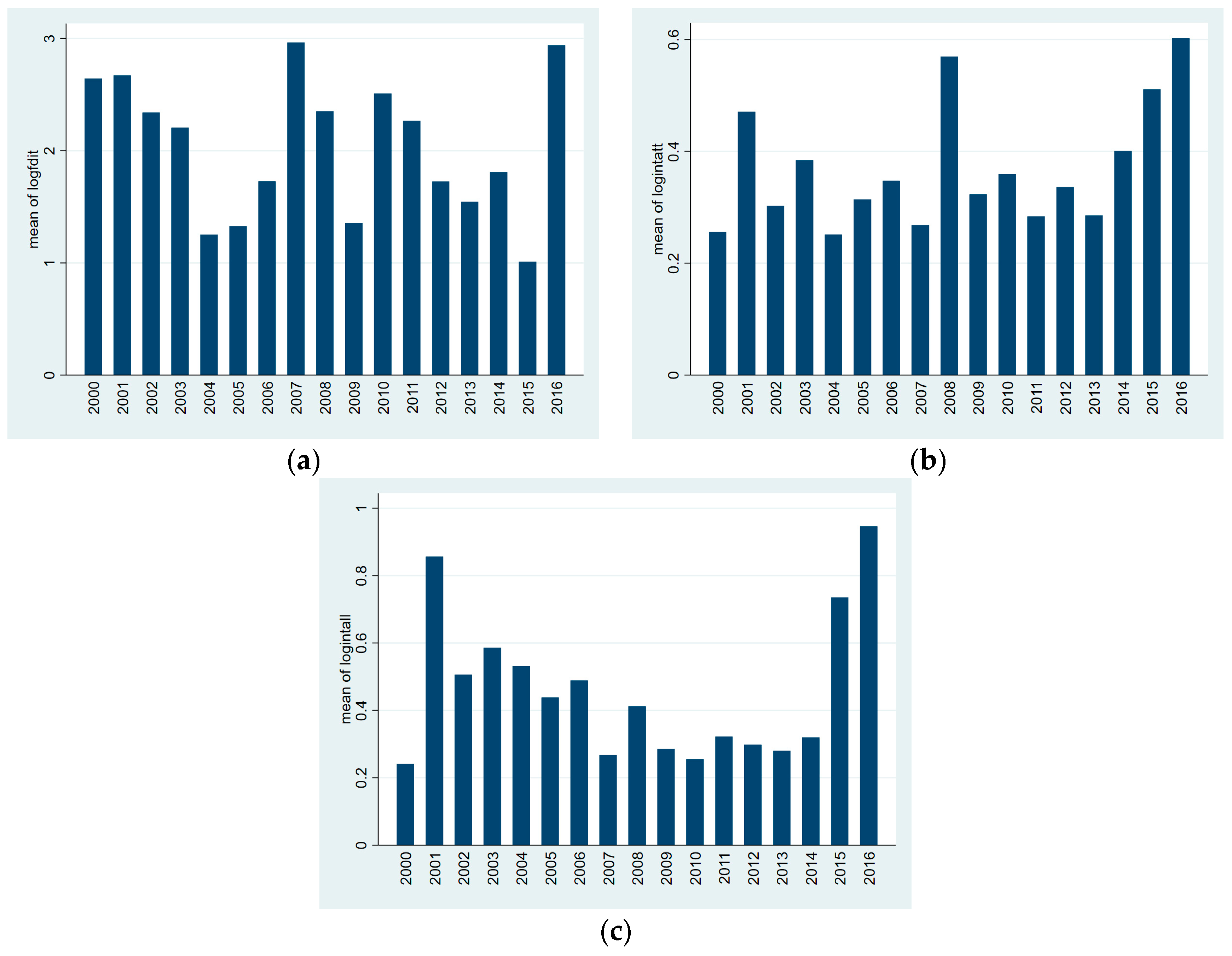

In adherence with the earlier-described research methodology, a panel unit root test is employed to determine whether there is a unit root present. The only variable where a time trend and drift term were included was for the international arrival per capita variable. Stationarity of the variables was tested for all time series, and the results of the unit root test indicate that all series are stationary in level, which is evident from the

Table 2 (the graphs of the observed time series averaged of main variables of interest, across countries, can be found in the

Appendix A,

Figure A1).

Thus, it is possible to conclude that all the observed series do not contain the unit root given that the null hypothesis for non-stationarity has been rejected.

To ensure the reliability of the VAR model, the next step was to choose the optimal lag length of the VAR models. The panel VAR used the first four lags of FDI in tourism and international terrorist attack, FDI in tourism and total international casualties as instruments, respectively. The optimal number of lags was chosen with the help of the usual information criteria, such as Hansen J test, Akaike information criterion (MAIC), the modified Bayesian information criterion (MBIC) and the modified Hannan-Quinn information criterion (MQIC). Based on the above-mentioned criterion, as optimal lag length, 1 is selected.

As suggested by

Abrigo and Love (

2015) a first-order panel VAR model is fitted with the same specification of instruments as above using GMM estimation. Since the database comprises missing values this research further follows

Holtz-Eakin et al. (

1988). The “GMM-style” instruments are used to replace instrument lags with missing values with zeroes. The consequence of such an approach is a larger sample of estimates and estimates that are more reliable.

The next step was to test the Granger causality relationship. Classic Granger causality involves performing the Wald test for the first p parameters of other variables in the VAR model, and, if the Wald test was significant, rejecting the null hypothesis of no causality. The results of the test are shown in

Table 3.

The results of the Granger test indicate that the total casualties in international terrorist attacks and the number of international attacks do not affect FDI in tourism. The results remain the same when control variables are implemented in testing. It may be concluded that all the null hypotheses could not be rejected. The situation is the same the other way around. FDI in tourism does not affect international terrorist attacks or the total number of casualties from international terrorist attacks in any way.

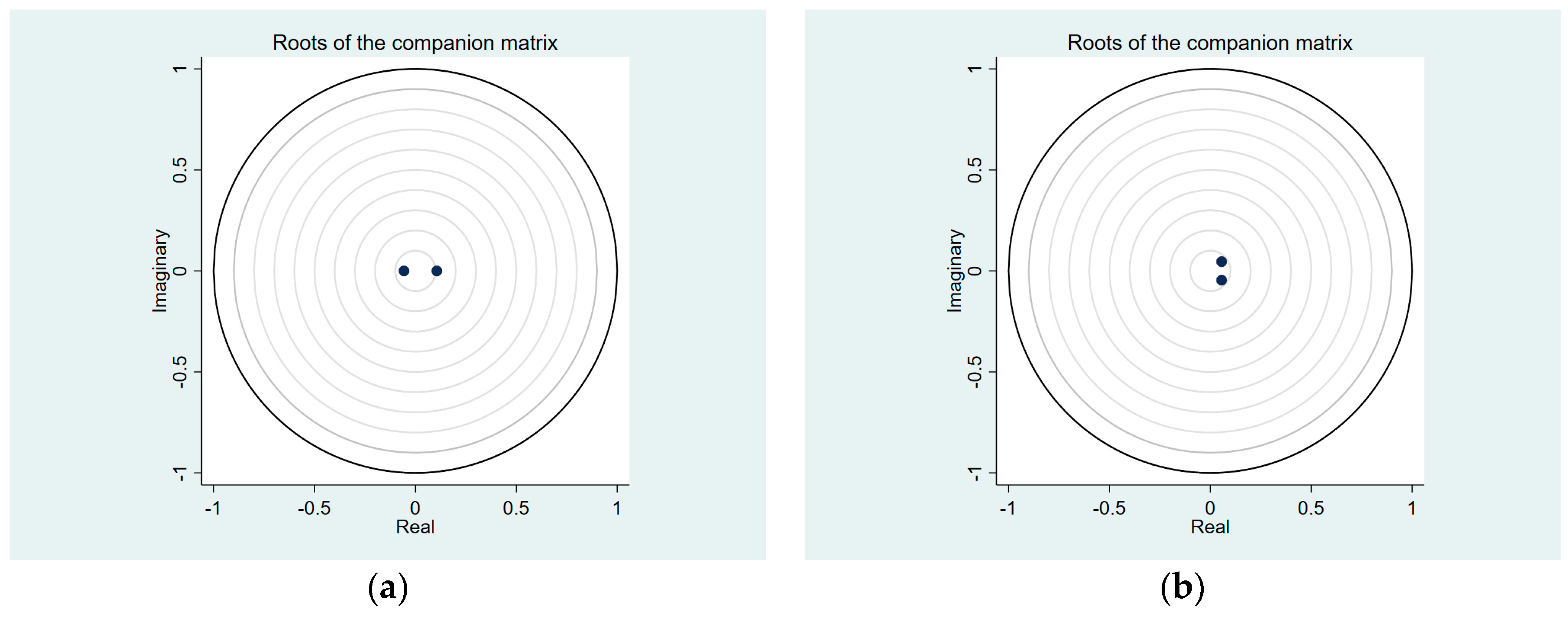

Prior to estimation of impulse-response functions (IRFs) and variance decompositions (FEVD), the stability condition of the estimated panel was checked. The dynamic stability of the VAR models is shown in

Figure 1.

According to

Lutkepohl (

2005) and

Hamilton (

1994), a VAR model is stable if all the roots are strictly less than one. None of the roots is outside of the circles so it is possible to conclude that the VAR models are stable. In other words, the outcomes and conclusions following from this analysis are not questionable.

The variance decomposition of the first pair of variables, logfdit and logintatt, and the second pair of variables, logfdit and logintall, is shown in

Appendix A (

Table A3). The analysis was conducted for the prognostic period of the next 10 years. The variance decomposition shows the relative share of individual variables in the explanation of the variance of the second variable in the following periods. All the variables almost fully explain their prognostic errors as far as the prognostic period is concerned. Following

Abrigo and Love (

2015) the IRF confidence intervals are computed using 200 Monte Carlo simulations based on the estimated model.

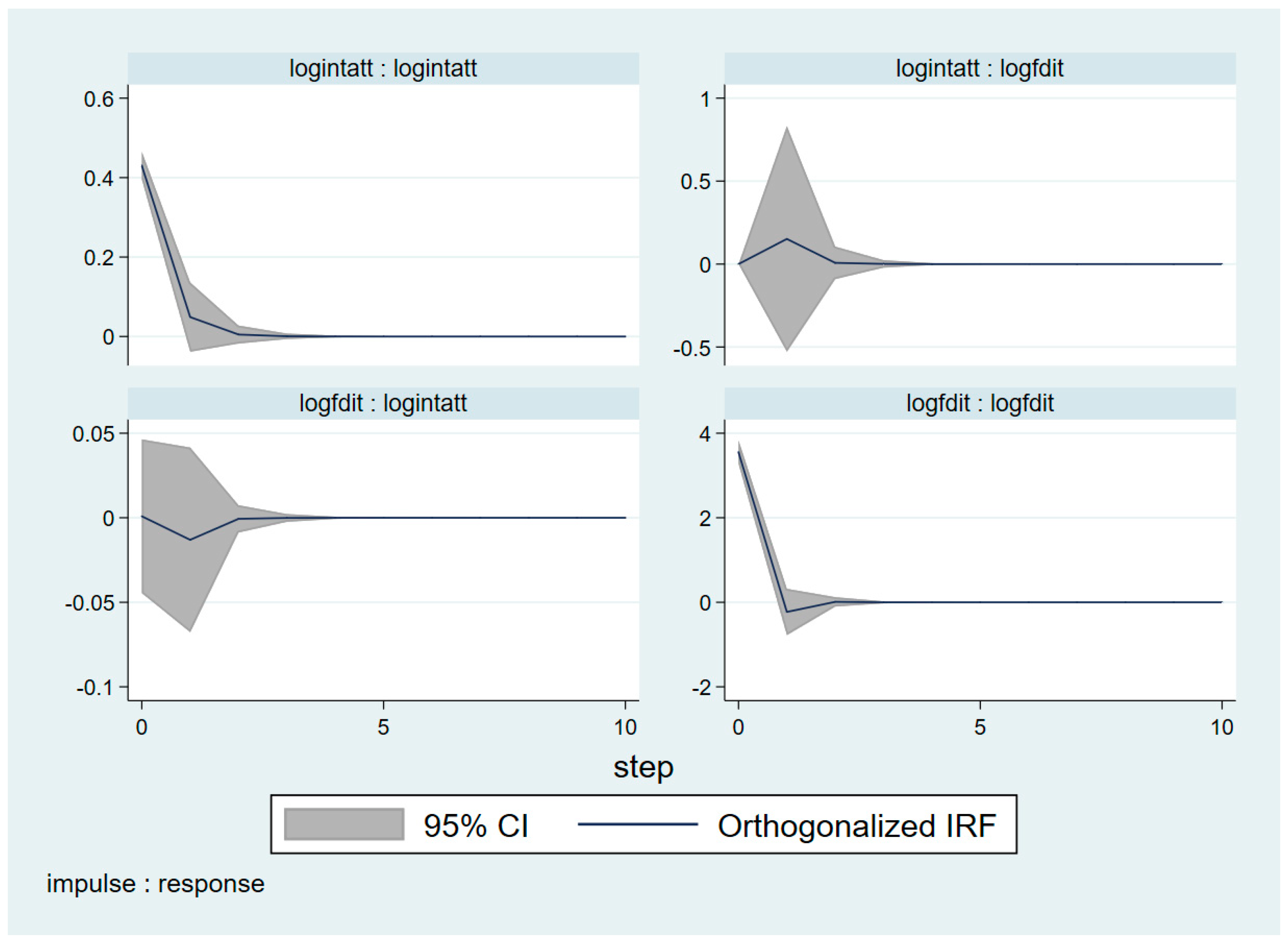

Finally, impulse response functions are calculated as the reaction of each endogenous variable to unit shock in system variables. The analysis was conducted for the prognostic period of 10 years.

The results of the Impulse response function (IRF) from the Cholesky decomposition in

Figure 2 concerning international terrorism attacks and FDI in tourism endorse the results obtained from the Granger causality test. The shock of a one standard deviation change in logintatt has a practically neutral influence on logfdit. In addition, the shock of one standard deviation in logfdit has a neutral influence on logintatt.

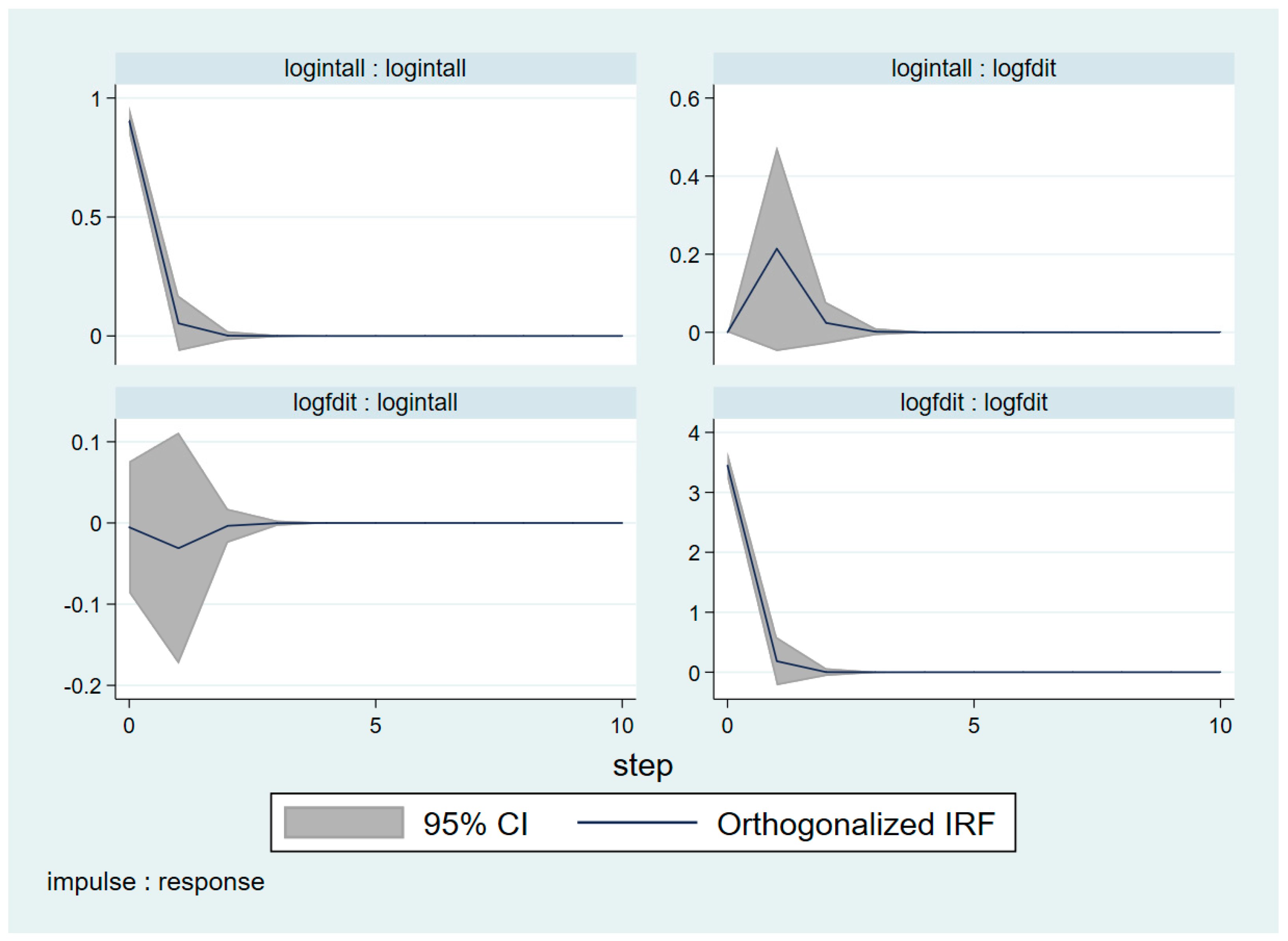

The situation is the same with the other pair of variables. The results from the impulse-response function in

Figure 3 regarding international terrorism death and injures and FDI in tourism confirm the results obtained from the Granger causality test. The shock of a one standard deviation change in logintall has an almost neutral influence on logfdit. In addition, the shock of a one standard deviation in logfdit has a neutral influence on logintall.

The implementation of Granger’s causality test, variance decomposition analysis and impulse response functions lead to the same result. The example of the panel of countries proves that there is no causal relationship between terrorism and FDI in tourism. The variables of terrorism fully explain their prognostic mistakes and the increase in terrorism for one standard deviation does not lead to a decrease in FDI in tourism.

5. Concluding Remarks

The results of the conducted research have confirmed the justification of the established research ground. The example of a panel of countries has shown that there is no causality between terrorism and FDI in tourism in the Granger sense. Such a result was expected. Firstly, terrorism does not considerably influence the long-term behaviour of tourists. According to the WTTC study, it takes 13 months for tourism to make progress from a terrorist attack (

Zillman 2015). Considering that tourist demand elicits tourist supply, it is logical to expect that investors in tourism will act in accordance with that trend. Secondly, global companies were conscious that terrorist threats raised business costs even in the 1980s. The risk of terrorism was then the second most substantial impediment to global business (

Ryans Jr and Shanklin 1980). The risk of terrorism is one of the external risks that corporations take into count when making plans and expanding business to a selected investment location, and they operate in the long-term. The market data also indicate that hotel corporations are recovering faster from terrorist attacks (

Oaten et al. 2015).

Such research results have significant political implications. The fact is that open borders make it easier for terrorists to move around and engage in terrorist activities. On the other hand, open borders also enable FDI to enter a country, as well as countries to get actively involved in globalisation processes. Open borders also allow for tourists to travel more easily and enjoy the benefits of tourism in particular economies. On the one hand, FDI in tourism can attract terrorist attacks, but it can also have a beneficial effect on political instability in a country. Large foreign corporations act as a sort of magnet for terrorists as they symbolise western values, i.e., everything that terrorist attacks focus on. Such attacks on objects full of tourists also attract heavy media attention, which works in favour of causing terror, that being one of the goals of terrorist attacks. However, when taking market trends into account, it is more likely that FDI affects the political stability of a country. A large presence of foreign investors in a country is a symbol of the country’s economic maturity and inclusion in globalisation processes. It seems appropriate to quote

Friedman (

1996), who pointed out in 1996 that ‘No two countries that both have a McDonald’s have ever fought a war against each other’. It may also be useful to bear in mind a research which proved that economic globalisation has an indirect negative effect on transnational terrorism, considering that FDI and international exchange affect economic development (

Li and Schaub 2004).

In view of the various nationalist and populist appearances that are rapidly spreading around the world and calling for the closure of borders, such scientific research is needed. It points to the fact that terrorism has so many negative long-term consequences and that it has become one of the threats of today with which life is still normal. It is also important to emphasize that most terrorist attacks in the world do not actually cause deaths or injuries, as the violence involves property rather than people (

Stohl 2003, p. 86). The further development of countries must be based on active participation in globalization processes, and that is only possible through open economies. Furthermore, the bearers of political authority are currently mostly busy putting out fires and enacting various security measures. However, political activities need to be oriented towards preventative antiterrorist measures, as they are the only thing which can secure long-term safety from terrorism (

De Silva 2017). According to

UNESCO (

2017), appropriate, inclusive and unbiased quality education precludes youth from assembling violent fanatical groups.

The authors believe that the results presented in this research paper should be treated as a starting point for future research on the effects of terrorism on FDI in tourism. These results should be further validated on the level of each country, perhaps by using quarterly data, because each country has its own peculiarities.

{kind=link}

{kind=link}

{kind=link}

{kind=link}