1. Introduction

The last decades have seen a continuous debate globally, notably at the United Nations on social and environmental issues (

UNWCED 1987;

UN 2015,

2016). Furthermore, more specifically, on the fact that companies are more committed to social responsibility and include the impacts of their activities on these issues in their operational management and global strategy. This means that, in addition to generating profit, they are expected to create value and contribute to the global value chain. In this context, the role of accounting in promoting sustainable development has gained in relevance (

Bebbington and Unermen 2018). In conceptual terms, social accounting is covered in Social and Environmental Accounting (SEA). The SEA is implicitly linked to companies’ contribution to present and future sustainability on a global level. Thus, social issues, among others, have begun to be included in the sustainable development agenda, which has led most companies to adopt the integration and dissemination of sustainability practices in their strategy, based on the triple bottom line (economic, social, and environmental dimension). In this context, many companies have integrated environmental and social management policies into their management accounting systems and have increased their disclosure practices (

Larrinaga-González and Bebbington 2001). This propensity/trend towards implementing new specific fields of management accounting and its dissemination to all interested parties has sparked greater interest from social science researchers since the early 1970s (

Bebbington and Gray 2001). In the 1990s, interest in social accounting reemerged, with significant concern in the public sector (government) and the private sector (business) with the global social impacts and the environment, such as human rights, ethics, conduct, and values and quality of life. In this context, several proposals have emerged for social accounting to be integrated into companies and other organizations’ accounting and management systems. In addition, the attitude of companies towards the disclosure of this type of non-financial information may be related to the organizational culture and type of activity, as well as to existing legislation, since the disclosure of social sustainability reports represents a means of managing and meeting the expectations of stakeholders in general (

Rodrigues and Mendes 2018). So, current trends indicate that companies are choosing a new way to communicate social and environmental issues (

Bebbington and Gray 2001;

Larrinaga et al. 2002). Given this scenario, the Social Accounting disseminated by

Ramanathan (

1976) stands out, which postulates the disclosure of relevant information on the company’s objectives, its economic and financial performance, policies, and social contributions and advocates this through reports that observe the relationship between the cost and benefit of disclosure, prioritizing the mitigation of asymmetry of information between users (

Niyama and Silva 2014).

The theoretical framework of this theme is essentially focused on three theories: the theory of legitimacy, the theory of stakeholders (stakeholders’ theory) and institutional theory, all of which are widely used in social accounting research, namely, to explain what drives organizations to disclose social and environmental information (

Deegan 2014).

Stakeholder theory has been one of the most widely used social accounting theories (

Gray 2010). There are two strands to this theory, a normative strand that prescribes how companies/organizations should interact with their stakeholders and a managerial strand that seeks to explain how companies/organizations interact effectively with their stakeholders (

Deegan 2014). In the first strand, it is considered that organizations must be accountable to their stakeholders. In the second, the organization must first define who the most important stakeholders are, control the resources, and then make efforts to provide them with the necessary information. In other words, organizations tend not to care about the least essential stakeholders (

Deegan 2014). Like the stakeholder theory, the theory of legitimacy considers the organization part of a comprehensive social system (

Deegan 2019).

However, while the theory of legitimacy is concerned with the expectations of society at large, it sees a social pact between the organization and the society in which it operates (

Deegan 2002). Stakeholder theory focuses on stakeholder groups. Thus, according to the legitimacy theory, companies/organizations survive if the society in which they operate realizes that they contribute to society’s global value creation chain (

Gray et al. 1996). This theory is based on the concept of organizational legitimacy. This means that legitimacy is a general assumption that an entity’s actions/attitudes can be appropriated to society by building a system of norms, values, and boundaries according to the system of that society (

Suchman 1995). Therefore, the theory of legitimacy allows explaining and understanding why companies adopt the practice of disclosing their social information, either in social reports or as part of their annual financial reports. Society is an interested party in companies’ sustainable behavior and, as such, exerts pressure for them to adopt good practices to obtain external and internal legitimacy and, thus, continue to develop their activities successfully. The theory of legitimacy has similarities with institutional theory. Some authors (

Deegan 2014) even claim that institutional theory provides additional insight into how organizations understand and respond to changes brought about by social and institutional pressures and expectations. Stakeholder and legitimacy theories suggest that organizations carefully and deliberately plan to disseminate information to meet more powerful stakeholders or the wider community’s expectations. Institutional theory, in turn, suggests that, in the absence of a clear justification for doing so, firms disseminate information because their peers do so or because it has become a common practice in the contexts in which they operate, thus introducing a process of homogenization of practices through institutional isomorphism (

DiMaggio and Powell 1983). Thus, the institutional theory makes it possible to understand why the dissemination of information happens and how it happens (

Higgins and Larrinaga 2014). It also makes it possible to relate organizational practices to the values of the society in which the organization operates and the need to maintain organizational legitimacy. Thus, according to

Deegan (

2014), institutional theory complements the explanations given by the theories of related parts and legitimacy, allowing the explanation of some asymmetry of information that was still occurring in the elaboration of social reports.

As for the topicality and timeliness of this work, they stem from several reasons. Firstly, the research carried out on this theme showed that, although three articles reviewed the literature, none of them included the dissemination of social information in the themes addressed. Secondly, it was found that most of the literature on the theme under study is scattered and, consequently, in need of systematization. Finally, given the role that social accounting plays in the current business environment, namely, in the international context, its study becomes relevant also in academic terms. This scarcity of studies on disseminating social accounting is the driving force in the first stage of theoretical development on a topic since literature reviews aim to provide in-depth research on a specific field (

Mentzer and Kahn 1995;

Seuring and Müller 2008).

Accounting research has been fertile in bibliometric analyses, for example

Merigó and Yang (

2017) proceeded to systematize the state of the art in accounting, in which it identified research that addressed social accounting in its various aspects. Another study mapped the literature on social responsibility in the mining industry (

Rodrigues and Mendes 2018);

Erkens et al. (

2015) thoroughly analyzed non-financial information;

Kulevicz et al. (

2020) studied how sustainability reports address socio-environmental and business issues;

Sikacz (

2017) systematized the publications on corporate social responsibility (CSR) reporting.

However, previous studies on the dissemination of social accounting have not included the epistemological paradigms that guide them, so the objectives of this article are to map the literature on social accounting and its dissemination, use the bibliometric method, and identify the main theoretical currents and the research paradigms used and frame them in the taxonomy of

Hopper and Powell (

1985). In accordance with Hopper and Powell’s taxonomy (

Hopper and Powell 1985) which, based on the epistemological and ontological assumptions of the researcher, points to three distinct research paradigms in management accounting, which are: positivist research (mainstream), interpretative research and critical research.

Following this brief introduction, the literature review, methodology, results and conclusions are presented.

2. Literature Review

Accounting can be used to communicate a company’s performance to all stakeholders (

Riahi-Belkaoui 2004). This information can be reported through formal and/or informal accounting mechanisms, whether formal reports (financial reports) or informal/voluntary reports (sustainability reports) (

Buhr and Reiter 2006). Accounting is only one and, in this context, it is difficult to draw a line between financial accounting, social accounting, and environmental accounting (

Cooper et al. 2005). However, with social and environmental impacts becoming more evident, the role played by sustainability has become hardcore in several contexts. In this sense, sustainability research has emerged significantly in academia, so

Bebbington and Larrinaga-González (

2014) have explored the possibilities of building a sustainability-driven accounting system, suggesting two lines of research: sustainability and total cost accounting, and sustainable consumption/production. Historically,

Bebbington and Gray (

2001) noted that social accounting became an emerging research topic from the 1970s, reflecting its importance for economic growth (

Jones 2003). In addition, social and environmental issues and their performance, have begun to be taken into account in corporate management strategies (

Gray 2002). However, during the 1980s and 1990s, interest in social and environmental reporting increased (

Adams 2002). It has been found that internal factors, such as ethics and transparency, influence the type of information disclosed in companies. In this period, some regulation on these issues has emerged that has institutionally obliged companies to report information on their social and environmental policies (

Adams 2002).

These regulations are intended to establish some standardization in corporate reports, so

Bebbington et al. (

2012) carried out a comparative study between two countries (Spain and the United Kingdom), with different regulations, which concluded that the legitimacy provided by-laws is crucial for the construction of standardization, and also provided a more subtle set of considerations for understanding the role of regulation in these reports. In this area, the literature has focused on some specific themes, such as social and environmental accounting (e.g.,

Herbohn 2005;

Larrinaga-González et al. 2001), the impacts of legislation (e.g.,

Deegan and Blomquist 2006;

Larrinaga et al. 2002), the dissemination of social and environmental information (e.g.,

Patten 2005), and the relationship between the dissemination of such information and performance (e.g.,

Adams 2004). For

Moser and Martin (

2012), many companies are trying to project an image of commitment to social accounting by voluntarily including additional information in their annual financial reports and demonstrating that they create value for all stakeholders and not just the shareholder. This issue arises mainly in large economic groups. The transfer of social accounting practices between countries voluntarily, with differentiated regulations, implies financial investment, an alignment of values, with added advantages for host countries (

Bansal 2005). The advantages inherent in this situation are visible in the strengthening of the transparency, reputation and legitimacy of these economic groups in the global business environment (

Bansal 2005) and improving the relationship with all stakeholders.

In this context, organizations must communicate information according to stakeholders and show that their information systems, particularly their accounting systems, are appropriate for providing final outputs on social accounting (

de Lima Voss et al. 2017). The dimensions included in social accounting (SEA) reflect that businesses contribute to a country’s wealth and economic growth and its social and environmental sustainability (

Dahlsrud 2008). Thus, for

Jennifer Ho and Taylor (

2007), there is an awareness that large economic groups of the imperative need to report on these issues and their social performance, whether through voluntary or mandatory disclosure. Social accounting issues can thus be seen from two perspectives. The first relates to the fulfilment of the subsequent responsibilities and obligations of companies.

In contrast, the second relates to the management of the interests of the various stakeholders and represents a means of obtaining internal and external legitimacy (

Murray et al. 2006). On the other hand, social accounting has more impact. It is better evidenced in companies carrying out activities with adverse effects on society in general and the environment (

Liu and Anbumozhi 2009), as they have greater public exposure (

Reverte 2009). However, other factors influence social reporting. Some authors (

Lu and Abeysekera 2014;

Van de Burgwal and Vieira 2014;

Huang and Kung 2010) have shown that the size of the company, its financial profitability, the influence of stakeholders, external controls (audits), influence the implementation of a social accounting information system.

In short, social accounting is a broad term, including concepts such as corporate social responsibility (CSR), social responsibility accounting (CRA), SEA, reporting and its disclosure, as well as its auditing (

Gray et al. 2009). This means that companies tend to promote strategies that incorporate social accounting (SEA) in conjunction with CSR as part of their objectives (

Brown and Fraser 2006). However, in terms of practical actions in the surrounding environment and society, these tend to be barely visible (

Sikka 2010). This argument does not prevent social accounting from fostering dialogue and commitment with all stakeholders, and there must be a common language and plurality of issues to be discussed (

Bebbington et al. 2007;

O’Dwyer 2005). Recently, some authors (

Adedeji et al. 2018) have argued that it is crucial to determine the influence of corporate governance on companies’ sustainability through the initiatives they implement and their association with performance. This means that social accounting is gaining importance for companies. However, most of the evidence gathered in the articles reviewed by

Patten and Shin (

2019) suggests that sustainability disclosure remains incomplete, biased, and driven by legitimacy concerns. These authors argue that better regulation is needed, including implementing the disclosure of entities’ social and environmental information.

Finally,

Table 1 shows the studies considered essential/gurus when researching social accounting.

The most studied themes in the 1970s to 1990s are theorization/conceptualization around social accounting, the disclosure of its information and the motivations for doing so. These themes show a cause–effect relationship between them, which means that firstly, it is necessary to define the concepts inherent to social accounting, understood as a new area of accounting. Next, it is necessary to understand how important it is for companies to obtain legitimacy before all stakeholders, which has a positive effect on its disclosure (voluntary or otherwise) and on the motivation of managers/companies to include it in their social performance reports. Nevertheless, these remain of exponential interest to academics, as it is intended to demonstrate in the following sections.

3. Methods

This article’s research methodology consists of a bibliometric review (analysis of co-citations) using the R software. Bibliometrix (

Aria and Cuccurullo 2017). It is a study based on co-citation networks and content analysis (by reading all articles). This type of approach has as its unit of analysis the scientific articles (in this case, the research focused only on scientific articles) and consists of a grouping of documents with a common goal and hardcore (

Grácio 2016). This type of analysis provides the identification, evaluation, and analysis of content in specific areas and systematization of concepts, theories, and practices (

Rowley and Slack 2004). Content analysis is a research tool aimed at analyzing and systematizing data for replication, with the selection of the data to be analyzed being crucial (

Krippendorff 1980) and data collection in this study, followed the common research procedures, through the ISI Web of Science (WoS) search engine to ensure their reliability, since this engine ensures real-time data availability (

Krippendorff 2004,

2012). This means that it is a compilation of scientific documents and their contributions, as it brings critical added value and provides a synthesis of the literature on the topic under study and the identification of relevant gaps and clues for future research purposes. Its main objective is to contribute to the advancement of scientific knowledge on this topic by identifying patterns of subtopics, authors, scientific journals, citations, co-citations, keywords, among others (

Prasad and Tata 2005;

Treinta et al. 2014); and conceptual contents (

Seuring and Müller 2008).

This analysis also followed the methodological procedures defined by

Tranfield et al. (

2003): planning; development; and presentation of results. In this context, the bibliometric analysis of a specific area of research implies adopting a methodical and structured research strategy for the selection of the documents to be included in the respective literature systematization. Thus, it is crucial to define the criteria and keywords to be used in the process of enquiry and specification of documents (

Bandara et al. 2011), and therefore the delimitation of the literature search process is fundamental to obtain an appropriate link between the main topic and subtopics and then proceed to their descriptive analysis (

Quesado and Silva 2021;

Treinta et al. 2014).

Table 2 presents the criteria used in the October 2020 survey.

After obtaining the final version of the scientific articles database, the analysis developed through the following steps:

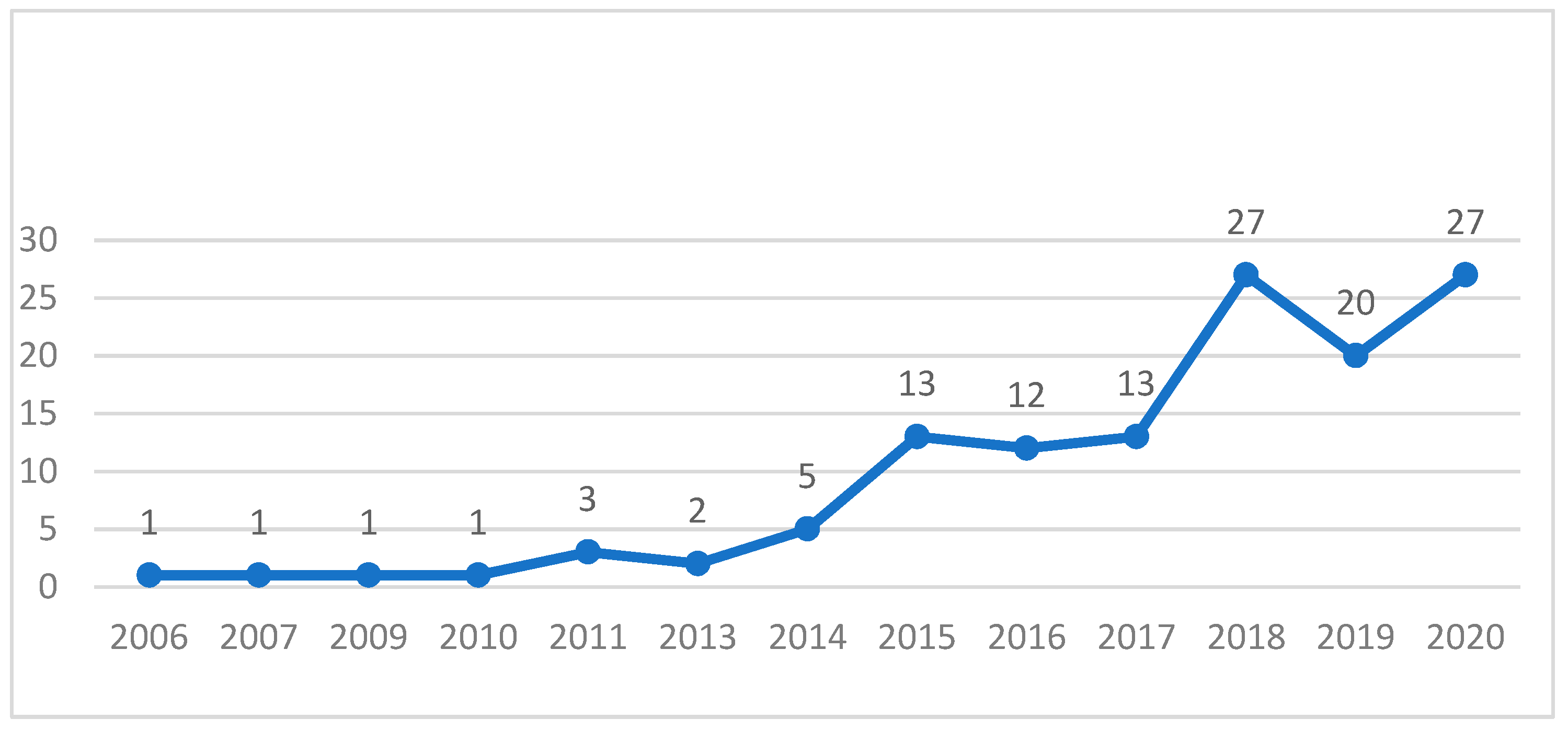

Export to BIBText of all the bibliographical data in order to prepare the descriptive analysis of the 126 scientific articles identified on the subject (

Table 1), in terms of the type of document, number of citations, distribution by year of publication, authors, countries, research areas, and titles of sources.

The bibliometric analysis was performed using the R Bibliometrix software (

Aria and Cuccurullo 2017). A set of tools was used to process all data on serial publications for analysis (126 documents). From this processing several outputs can be extracted (e.g., on authors, number of publications, networks, couplings) (

Ekundayo and Okoh 2018), which result from procedures for standardizing similarity of publications (

Aria and Cuccurullo 2017). The R Bibliometrix software is a package for bibliometric analysis written in R. According to

Derviş (

2019), R is open-source software, which means that it operates in an integrated environment that consists of open libraries, open algorithm and open graphic software. This tool’s other strengths are potent and effective statistical algorithms, access to high-quality numerical routines, and integrated data visualization tools (

Aria and Cuccurullo 2017). The R Bibliometrix software can be used to analyze and map bibliographic data simultaneously (

Derviş 2019). Compared with other open-access programs such as VOSviewer, Bibliometrix focuses on not only data visualization but also the accuracy and statistical robustness of results (

Derviş 2019).

Enrichment of the bibliometric analysis, through the integration of a content analysis of the 126 selected documents, aiming to systematize the topics/subjects of research most studied by the scientific community and that originated the clusters (

Spens and Kovács 2006;

Seuring and Gold 2012). However, this analysis of content is somewhat subjective, given its qualitative character. However, this does not impugn the validity of its inferences and their rigor (

Becker et al. 2012), so a structured and systematic approach has been adopted to overcome this limitation, as recommended by

Tranfield et al. (

2003) and

Seuring and Gold (

2012).

5. Concluding Remarks

In the study developed, bibliometric techniques helped us map the literature and understand the evolution of research on the dissemination of information on social accounting. This research work allows us to conclude that social accounting is an attractive research area since the year 1970 due to the discussion about sustainable development issues and research contributions to sustainability, with effects in the present and the future.

To provide answers to the objectives initially defined, it is concluded that at the level of social accounting great emphasis has been given to its dissemination, which is evidenced by the results obtained in cluster 2 of the published articles. Cluster 1, on the other hand, makes it possible to argue that the theory of legitimacy is one of the most widely used frameworks in studies on social accounting.

However, Cluster 3, in association with Cluster 1, reveals that dissemination is still a controversial issue in information content. Thus, it can be seen that social accounting still has some limitations in its implementation and interconnection with “traditional” accounting. On the other hand, being its disclosure understood as a voluntary practice for companies/economic groups to obtain/maintain their external and internal legitimacy before all interested parties, there is still some heterogeneity in the information disclosed.

Considering that the search for institutional legitimacy is directly related to institutional theory, the latter is appropriate for work that focuses on a specific company’s structure or the adoption of information dissemination practices by similar organizations (mimetic isomorphism). Thus, it can be seen that in work in this area. At the same time, legitimacy theory and institutional theory are used to study specific organizations, and stakeholder theory allows the analysis of interactions between groups of stakeholders or between organizations.

There are, however, pressures for actors in the international context to implement accounting practices that are socially and ethically responsible, in addition to accounting practices that can only be considered in the environmental approach. These practices should be embedded in traditional accounting systems and information should be disclosed in social reports to promote transparency, credibility and enable sustainable performance, thus demonstrating a proactive attitude in this area.

In parallel with the analysis of these theoretical implications, a descriptive mapping of the literature on this subject (figures, charts, and tables) was carried out, systematizing the information and helping future research on the subject, with an indication of the topics that have most aroused the interest of the academic world.

In addition to this, a summary of the paradigmatic plurality revealed by research in social accounting in recent years has been presented. It is noted that positivist research is no longer predominant, giving way to interpretative research and critical research.

Mathews (

1997) argues that the traditional paradigm no longer meets the needs of research, and many of the studies undertaken no longer fit the assumptions of the traditional model. In interpretative research, the researcher seeks to study a social phenomenon in a particular context and may become involved in the phenomenon, and tries to interpret the results in the light of the theories that support it. In critical research, the researcher seeks to understand the social world better and promote the necessary social change. He or she seeks to emancipate the individual, freeing him or her from excessively influential discourses that may restrict his or her ability to reflect (

Gendron 2018). For example,

Kamla et al. (

2012) studied the social accounting perceptions of Syrian accounting professionals and concluded that the sociopolitical and socio-economic context had slowed social accounting development in Syria. This means that, like traditional accounting, social accounting research has shifted from theoretical questions, processes, and norms to focus on social phenomena.

In short, in addition to the mapping of literature in elite journals, another theoretical contribution was the identification of the paradigms and research approaches underlying this theme. Thus, it was concluded that social accounting is a multifaceted area that allows research methodologies, and the paradigms used, to be varied and, as such, allow for a greater theoretical and practical deepening of the analyzed themes. Some critical research, associated with social and environmental responsibility, stands out here on which there is still a strong debate. This means that the study of social accounting can also be approached critically, when trying to respond to the challenges of sustainability imposed by climate change or, carbon emissions, among many other aspects.

It is also important to note some academic and management implications. Academically, this study suggests that this theme is still emerging and current since the dissemination of social accounting still needs to be improved, namely, the inclusion of more information on actions in the local community and the implementation of measures that minimize the negative impacts of some of the strategies followed. Further, the motivation for disclosure should not be used as a tool to entice stakeholders for the sake of convenience, but because they actually want to be socially responsible. This means, in management terms, that this disclosure should not be driven by mere compliance with the law, on the contrary, it should be with a view to generating internal and external added value. A further implication for theory and practice is that it has been shown that in any type of research on in social accounting research, any of the research paradigms can be used without jeopardizing the robustness and quality of the studies carried out, whether theoretical or practical. On the other hand, this plurality shows the variety in the epistemological, ontological and methodological assumptions of researchers and studies. The interpretive paradigm involves greater subjectivity, because when the intention is to answer the how and why, the researcher’s involvement is unquestionable; however, this does not jeopardize the validity, reliability, quality, and contribution of these studies to the development of scientific knowledge.

Like any research work, this study has some limitations, notably, because it has been limited to the Web of Science database. However, this is one of the most widely recognized in the scientific and academic community. Regarding this limitation, it should be added that the same research was carried out in the Scopus database, and it was found that articles not common to both databases did not influence the final result significantly. Similarly, the analysis of paradigms confined only to articles included in clusters represents a limitation.

Finally, and as topics for future research, it is suggested to study the regulations on the type of information to be included in disseminating social reports and its standardization concerning the Global Reporting Index (GRI) standards. It would also be important to search in other relevant academic databases for articles related to the topic under analysis and add them to the final base to be analyzed in Rstudio, and thus enrich the knowledge of this topic, which suggests another future track. Furthermore, broadening the search terms used in this study is another future clue, since the topic of social accounting can be developed at various levels, for instance to include “sustainability reports”, “non-financial information”, and other similar ones.

,

,

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}