Brand and Firm Value: Evidence from Arab Emerging Markets

Abstract

:1. Introduction

2. Literature Review

2.1. Brand–Share Return Relationship

2.2. The Moderating Role of Agency Costs

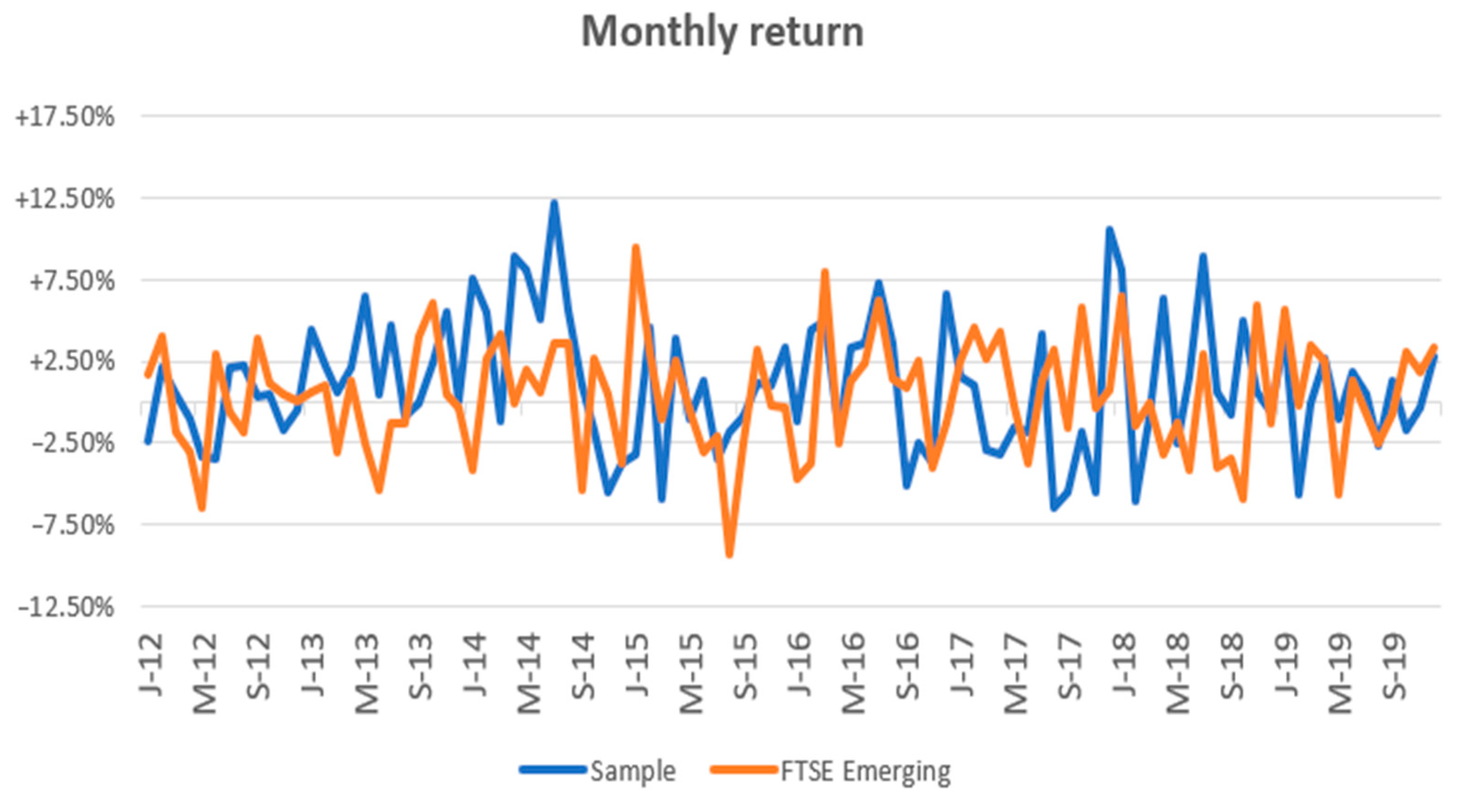

3. Data and Methodology

- Company has accounting data for consecutive years between 2010 and 2019.

- The accounting period ends on 31 December.

- The company is considered within the FTSE Emerging Index constituents for a minimum of four periods.

- The book value is positive for all series years.

- The company has a clear branded product or service, and operates in a competitive market, that is, it does not have an absolute monopoly position.

4. Results and Discussion

4.1. Descriptive Statistics

4.2. Regression Results and Hypotheses Test

5. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

Appendix A

{kind=link}

| Variable | Code | Description | Recourse |

|---|---|---|---|

| Return | − | − ) + D]/ − where = annual closing price in period t. = annual closing price in period t − 1. D = dividends = risk-free return measured by the yield on government bonds for ten years | Own calculation based on Thomson Reuters DataStream |

| Abnormal return | operational earnings per share less the normal earning , where = risk free return, = book value of previous year | Own calculation based on Thomson Reuters DataStream | |

| Brand equity | {Total revenue − total marketing cost}/WACC Marketing cost = general administrative expenses (SG&A) minus research and development (R&D) expenses. WACC: weighted average cost of capital = WACC = VE × Re + VD × Rd × (1 − Tc) where Re = cost of equity calculated by Capital Asset Pricing Model (CAPM) r = () = the return of the market portfolio systematic risk factor calculated using moving five years’ window (60 months or at least 36) through regression estimation between monthly return of share and market index. = slop (,) Rd = cost of debt measured by debt interest rate E = market value of the firm’s equity D = market value of the firm’s debt V = E + D = total market value of the firm’s financing E/V = percentage of financing that is equity D/V = percentage of financing that is debt Tc = corporate tax rate | Own calculation based on Thomson Reuters DataStream | |

| Agency cost | AGCO | Asset utilization ratio = sales/total assets | Own calculation based on Thomson Reuters DataStream |

| Size | Size | Ln (total assets) | Thomson Reuters DataStream |

| Oil | Oil | Annual closing price of Brent crude price | Thomson Reuters DataStream |

References

- Aaker, David. 1996. Building Strong Brands. New York: The Free Press. [Google Scholar]

- Abratt, Russell, and Geoffrey Bick. 2003. Valuing Brands and Brand Equity: Methods and Processes. Journal of Applied Management and Entrepreneurship 8: 21–39. [Google Scholar]

- Anderson, Justin. 2011. Measuring the financial value of brand equity: The perpetuity perspective. Journal of Business Administration Online 10: 1–11. [Google Scholar]

- Ang, James S., Rebel A. Cole, and James Wuh Lin. 2000. Agency costs and ownership structure. Journal of Finance 1: 81–106. [Google Scholar] [CrossRef]

- Arellano, Manuel, and Stephen Bond. 1991. Some tests of specification for panel data: Monte Carlo evidence and an application to employment Equations. The Review of Economic Studies 58: 277–97. [Google Scholar] [CrossRef] [Green Version]

- Badenhausen, Kurt. 2012. Apple tops list of the world’s most powerful brands. Forbes 10. Available online: https://www.forbes.com/sites/kurtbadenhausen/2012/10/02/apple-tops-list-of-the-worlds-most-powerful-brands/?sh=63cab693cc9a (accessed on 10 March 2020).

- Bahadir, S. Cem, Sundar G. Bharadwaj, and Rajendra K. Srivastava. 2008. Financial value of brands in mergers and acquisitions: Is value in the eye of the beholder? Journal of Marketing 72: 49–64. [Google Scholar] [CrossRef]

- Bank, Semra, Evrim Yzar, and Ugur Sivri. 2020. The portfolios with strong brand value: More returns? Lower risk? Borsa Istanbul Review 20: 64–79. [Google Scholar] [CrossRef]

- Barniv, Ran, and Mark Myring. 2006. An international analysis of historical and forecast earnings in accounting-based valuation models. Journal of Business Finance & Accounting 33: 1087–109. [Google Scholar] [CrossRef]

- Belo, Frederico, Xiaoji Lin, and Maria Ana Vitorino. 2014. Brand capital and firm value. Review of Economic Dynamics 17: 150–69. [Google Scholar] [CrossRef]

- Ben Cheikh, Nidhaleddine, Sami Ben Naceur, Oussama Kanaan, and Christophe Rault. 2008. Oil Prices and GCC Stock Markets: New Evidence from Smooth Transition Models. IMF Working Paper, WP/18/98. Washington, DC: International Monetary Fund. [Google Scholar] [CrossRef] [Green Version]

- Bharadwaj, Sundar G., Kapil R. Tuli, and Andrea Bonfrer. 2011. The impact of brand quality on shareholder wealth. Journal of Marketing 75: 88–104. [Google Scholar] [CrossRef]

- Billet, Matthew T., Zhan Jiang, and Lopo L. Rego. 2014. Glamour brands and glamour stocks. Journal of Economic Behavior & Organization 107: 744–59. [Google Scholar] [CrossRef]

- Chan, Louis, Joseph Lakonishok, and Theodore Sougiannis. 2001. The stock market valuation of research and development expenditures. The Journal of Finance 56: 2431–56. [Google Scholar] [CrossRef]

- Chandler, Nicholas Guy. 2018. A Symbiotic Relationship: HR and Organizational Culture. In Organizational Behaviour and Human Resource Management. Management and Industrial Engineering. Edited by C. Machado and J. Davim. Cham: Springer. [Google Scholar] [CrossRef]

- Cheng, Ming-Chang S., and Zuawei Ching Tzeng. 2011. The effect of leverage on firm value and how the firm financial quality influence on this effect. World Journal of Management 3: 30–53. [Google Scholar]

- Duqi, Andi, and Giuseppe Torluccio. 2010. R&D Expenditure and Firm Valuation: Evidence from Europe. Paper presented at 23rd Australasian Finance and Banking Conference, Sydney, Australia, December 14; Available online: https://ssrn.com/abstract=1663205 (accessed on 10 July 2020).

- Dutordoir, Marie, Frank M. Verbeeten, and Dominique Beijer. 2015. Stock price reactions to brand value announcements: Magnitude and moderators. International Journal of Research in Marketing 32: 34–47. [Google Scholar] [CrossRef]

- Dutta Anupam, Jussi Nikkinen, and Timo Rothovius. 2017. Impact of oil price uncertainty on Middle East and African stock markets. Energy 123: 189–97. [Google Scholar] [CrossRef]

- El Zein, Samer A., Carolina C. Segura, and Ruben H. Garcia. 2019. The role of sustainability in brand equity value in the financial sector. Sustainability 12: 254. [Google Scholar] [CrossRef] [Green Version]

- Fehle, Frank, Sergey Tsyplakov, and Vladimir Zdorovtsov. 2005. Can Companies Influence Investor Behaviour through Advertising? Super Bowl Commercials and Stock Returns. European Financial Management 11: 625–47. [Google Scholar] [CrossRef]

- Graham, John R., Campbell R. Harvey, and Shiva Rajgopal. 2005. The economic implications of corporate financial reporting. Journal of Accounting and Economics 40: 3–73. [Google Scholar] [CrossRef] [Green Version]

- Hanssens, Dominique M., and Koen H. Pauwels. 2016. Demonstrating the value of marketing. Journal of Marketing 80: 173–90. [Google Scholar] [CrossRef]

- Huu Nguyen, Anh, Duong Thuy Doan, and Linh Ha Nguyen. 2020. Corporate governance and agency cost: Empirical evidence from Vietnam. Journal of Risk and Financial Management 13: 103. [Google Scholar] [CrossRef]

- Jensen, Michael C., and William H. Meckling. 1976. Theory of the Firm: Managerial Behavior, Agency Costs and Ownership Structure. Journal of Financial Economics 3: 305–60. [Google Scholar] [CrossRef]

- Jensen, Michael. 1986. Agency Costs of Free Cash Flow, Corporate Finance, and Takeovers. The American Economic Review 76: 323–29. [Google Scholar]

- Johansson, Johny K., Claudiu V. Dimofte, and Sanal K. Mazvancheryl. 2012. The performance of global brands in the 2008 financial crisis: A test of two brand value measures. International Journal of Research in Marketing 29: 235–45. [Google Scholar] [CrossRef]

- Karuna, Christo. 2007. Industry product market competition and managerial incentives. Journal of Accounting and Economics 43: 275–97. [Google Scholar] [CrossRef]

- Keller, Kevin Lane. 2001. Building Customer-based Brand Equity: A blueprint for Creating Strong Brands. Report No. 01-107. New York: Marketing Science Institute, pp. 1–31. [Google Scholar]

- Kirk, Coleen P., Ipshita Ray, and Berry Wilson. 2013. The impact of brand value on firm valuation: The moderating influence of firm type. Journal of Brand Management 20: 488–500. [Google Scholar] [CrossRef]

- Krajcsák, Zoltán. 2020. Implementing Open Innovation Using Quality Management Systems: The Role of Organizational Commitment and Customer Loyalty. Journal of Open Innovation: Technology, Market, and Complexity 5: 90. [Google Scholar] [CrossRef] [Green Version]

- Laghi, Enrico, Michele Di Marcantonio, Valentina Cillo, and Niccolo Paoloni. 2020. The relational side of intellectual capital: An empirical study on brand value evaluation and financial performance. Journal of Intellectual Capital. [Google Scholar] [CrossRef]

- Lev, Baruch, and Paul Zarowin. 1999. The boundaries of financial reporting and how to extend them. Journal of Accounting Research 37: 353–85. [Google Scholar] [CrossRef] [Green Version]

- Littunen, Hannu. 2000. Entrepreneurship and the characteristics of the entrepreneurial personality. International Journal of Entrepreneurial Behavior & Research 6: 295–310. [Google Scholar] [CrossRef]

- Luo, Xueming. 2008. When marketing strategy first meets Wall Street: Marketing spending and firms’ initial public offerings (IPOs). Journal of Marketing 72: 98–109. [Google Scholar] [CrossRef]

- Maddala, G. S., and Kajal Lehiri. 2009. Introduction to Econometrics, 3rd ed. Hoboken: Wiley, p. 625. [Google Scholar]

- Madden, Thomas J., Frank Fehle, and Susan Fournier. 2006. Brands matter: An empirical demonstration of the creation of shareholder value through brands. Journal of the Academy of Marketing Science 3: 224–35. [Google Scholar] [CrossRef]

- McKnight, Philip, and Weir Charlie. 2009. Agency costs, corporate governance mechanisms and ownership structure in large UK publicly quoted companies: A panel data analysis. The Quarterly Review of Economics and Finance 39: 131–57. [Google Scholar] [CrossRef] [Green Version]

- Mitton, Todd. 2004. Corporate governance and dividend policy in emerging markets. Emerging Markets Review 5: 409–26. [Google Scholar] [CrossRef]

- Mizik, Natalie, and Robert Jacobson. 2009. Valuing branded businesses. Journal of Marketing 73: 137–53. [Google Scholar] [CrossRef]

- Ocean Tomo. 2017. Intangible Assets Market Value Study. Available online: https://www.oceantomo.com/intangible-asset-market-value-study/ (accessed on 2 April 2020).

- Ohlson, James A. 1995. Earnings, book values and dividends in equity valuation. Contemporary Accounting Research 11: 661–87. [Google Scholar] [CrossRef]

- Oliveira, Martha Olivia Rovedder, Aline Armanini Stefanan, and Mauri Leodir Lobler. 2018. Brand equity, risk and return in Latin America. Journal of Product & Brand Management 27: 557–72. [Google Scholar] [CrossRef]

- Pham, Thach Ngoc, Vuong Minh Nguyen, and Duc Hong Vo. 2018. The Cross-Section of Expected Stock Returns: New Evidence from an Emerging Market. Emerging Markets Finance and Trade 54: 3566–76. [Google Scholar] [CrossRef]

- Rashid Khan, Haroon-Ur, Waqas Bin Khidmat, Osama Al Hares, Naeem Muhammad, and Kashif Saleem. 2020. Corporate governance quality, ownership structure, agency costs and firm performance. Evidence from an emerging economy. Journal of Risk and Financial Management 13: 154. [Google Scholar] [CrossRef]

- Richardson, Gordon, and Surjit Tinaikar. 2004. Accounting based valuation models: What have we learned. Accounting and Finance 44: 223–55. [Google Scholar] [CrossRef]

- Rust, Roland T., Katherine N. Lemon, and Valarie A. Zeithaml. 2004. Return on marketing: Using customer equity to focus marketing strategy. Journal of Marketing 68: 109–27. [Google Scholar] [CrossRef] [Green Version]

- Ryoo, Juyoun, Jin Q. Jeon, and Cheolwoo Lee. 2016. Do marketing activities enhance firm value? Evidence from M&A transactions. European Management Journal 34: 243–57. [Google Scholar] [CrossRef]

- Singh, Manohar, and Wallace N. Davidson. 2001. Agency costs, ownership structure and corporate governance mechanisms. Journal of Banking & Finance 18: 473–90. [Google Scholar] [CrossRef]

- Singh, Manohar, Sheri Faircloth, and Ali Nejadmalayeri. 2005. Capital market impact of product marketing strategy: Evidence from the relationship between advertising expenses and cost of capital. Journal of the Academy of Marketing 33: 432–44. [Google Scholar] [CrossRef]

- Srivastava, Rajendra K., and Allan D. Shocker. 1991. Brand Equity: A Perspective on Its Meaning and Measurement. Marketing Science Institute Working Paper Series Report. Cambridge: Marketing Science Institute, pp. 91–124. [Google Scholar]

- Srivastava, Rajendra K., Shervani A. Tasadduq, and Liam Fahey. 1998. Market-Based Assets and Shareholder Value: A Framework for Analysis. Journal of Marketing 62: 2–18. [Google Scholar] [CrossRef] [Green Version]

- Star Capital. 2020. Global Stock Market Valuation Ratios. Available online: https://www.starcapital.de/en/research/stock-market-valuation/ (accessed on 2 February 2020).

- Suleimankadieva, Aljanat. E., Valeria I. Pilipenko, and Judit Sági. 2019. Knowledge Company: Approaches to Assessing New Knowledge and Representation it to Society. Procedia Computer Science 150: 730–36. [Google Scholar] [CrossRef]

- Sullivan, Don, and John McCallig. 2009. Does customer satisfaction influence the relationship between earnings and firm value? Marketing Letters 20: 337–51. [Google Scholar] [CrossRef]

- Tasci, Asli D. A. 2020. A critical review and reconstruction of perceptual brand equity. International Journal of Contemporary Hospitality Management. [Google Scholar] [CrossRef]

- Vijayakumaran, Ratnam. 2019. Agency cost, ownership, and internal governance mechanisms: Evidence from Chinese listed companies. Asian Economic and Financial Review 9: 133–54. [Google Scholar] [CrossRef] [Green Version]

- Wang, Kui, and Wei Jiang. 2019. Brand equity and firm sustainable performance: The mediating role of analysts’ recommendations. Sustainability 11: 1086. [Google Scholar] [CrossRef] [Green Version]

- Zimmermannová, Jarmila. 2020. Methods in Microeconomic and Macroeconomic Issues. Spationomy. [Google Scholar] [CrossRef] [Green Version]

| Paper | Market Scope | Methodology | Moderating Variables |

|---|---|---|---|

| Fehle et al. (2005) | Developed market—USA | CAPM three-factor and momentum four-factor | No |

| Kirk et al. (2013) | Developed market—USA | Cross-sectional regression | Firm type |

| Luo (2008) | Three developed markets: USA, UK, and Germany | CAPM three-factor and momentum four-factor | NO |

| Johansson et al. (2012) | Developed market USA | CAPM three-factor | NO |

| Billet et al. (2014) | Developed market USA | CAPM three-factor | NO |

| Bharadwaj et al. (2011) | Developed market USA | CAPM three-factor | Changes in industry concentration |

| Oliveira et al. (2018) | Five emerging markets in Latin America | CAPM three-factor and momentum four-factor | NO |

| Wang and Jiang (2019) | Emerging Market—China | CAPM three-factor | Financial analysts’ recommendations |

| Bank et al. (2020) | Emerging market—Turkey | CAPM three-factor | NO |

| Current paper | Four Emerging Arab markets | Ohlson model | Agency costs |

| N | Mean | Std. Deviation | Minimum | Maximum | |

|---|---|---|---|---|---|

| R | 360 | 0.2090 | 0.6310 | −0.8800 | 8.8770 |

| BRE/USD M | 360 | 8,133 | 5,522 | 491 | 73,640 |

| B | 360 | 1.1725 | 0.9060 | 0.0700 | 5.8200 |

| X | 360 | 0.0700 | 0.3020 | −0.6000 | 2.5300 |

| AGCO | 360 | 0.2290 | 0.3271 | 0.0050 | 2.2000 |

| Age | 360 | 26.39 | 17.15 | 3.00 | 67.00 |

| Beta | 360 | 0.8377 | 0.5468 | −0.9000 | 2.4400 |

| P/B | 360 | 1.5697 | 0.9310 | 0.2600 | 6.6500 |

| Variable | Coefficient | Std. Error | t-Statistic | Prob. |

|---|---|---|---|---|

| C | 0.162988 | 0.015143 | 10.76358 | 0.0000 |

| 0.080932 | 0.053339 | 1.517318 | 0.0303 | |

| 3.350713 | 1.221071 | 2.753886 | 0.0063 | |

| 0.250784 | 0.072821 | 3.443856 | 0.0007 | |

| 0.334040 | 0.061452 | 5.435805 | 0.0000 | |

| Weighted Statistics | ||||

| R-squared | 0.234363 | Mean dependent var | 0.224118 | |

| Adjusted R-squared | 0.129222 | S.D. dependent var | 0.594155 | |

| S.E. of regression | 0.554792 | Sum squared resid | 87.41353 | |

| Durbin–Watson stat | 1.928109 | J-statistic | 284.0000 | |

| Variable | Coefficient | Std. Error | t-Statistic | Prob. |

|---|---|---|---|---|

| C | 0.137739 | 0.016340 | 8.429398 | 0.0000 |

| 0.092680 | 0.055358 | 1.674178 | 0.0452 | |

| 6.931407 | 2.806108 | 7.069977 | 0.0000 | |

| 0.255507 | 0.073526 | 3.475053 | 0.0006 | |

| 0.341708 | 0.064580 | 5.291196 | 0.0000 | |

| −0.509158 | 0.288937 | −1.762175 | 0.0291 | |

| Weighted Statistics | ||||

| R-squared | 0.339707 | Mean dependent var | 0.214671 | |

| Adjusted R-squared | 0.241016 | S.D. dependent var | 0.591428 | |

| S.E. of regression | 0.517187 | Sum squared resid | 75.16261 | |

| Durbin-Watson stat | 2.030494 | J-statistic | 281.0000 | |

| Variable | Coefficient | Std. Error | t-Statistic | Prob. |

|---|---|---|---|---|

| C | −0.633603 | 0.628525 | −1.008079 | 0.3141 |

| −0.131992 | 0.053696 | −2.458123 | 0.0145 | |

| 7.166510 | 8.196501 | 7.998904 | 0.0000 | |

| 0.345222 | 0.071958 | 3.407869 | 0.0007 | |

| −0.389212 | 0.064280 | −6.054927 | 0.0000 | |

| −0.509158 | 0.288937 | −1.762175 | 0.0291 | |

| Weighted Statistics | ||||

| R-squared | 0.286994 | Mean dependent var | 0.214671 | |

| Adjusted R-squared | 0.272782 | S.D. dependent var | 0.212352 | |

| S.E. of regression | 0.491734 | Sum squared resid | 72.78248 | |

| Durbin-Watson stat | 1.838339 | J-statistic | 301.0000 | |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Mousa, M.; Sági, J.; Zéman, Z. Brand and Firm Value: Evidence from Arab Emerging Markets. Economies 2021, 9, 5. https://doi.org/10.3390/economies9010005

Mousa M, Sági J, Zéman Z. Brand and Firm Value: Evidence from Arab Emerging Markets. Economies. 2021; 9(1):5. https://doi.org/10.3390/economies9010005

Chicago/Turabian StyleMousa, Musaab, Judit Sági, and Zoltán Zéman. 2021. "Brand and Firm Value: Evidence from Arab Emerging Markets" Economies 9, no. 1: 5. https://doi.org/10.3390/economies9010005

APA StyleMousa, M., Sági, J., & Zéman, Z. (2021). Brand and Firm Value: Evidence from Arab Emerging Markets. Economies, 9(1), 5. https://doi.org/10.3390/economies9010005