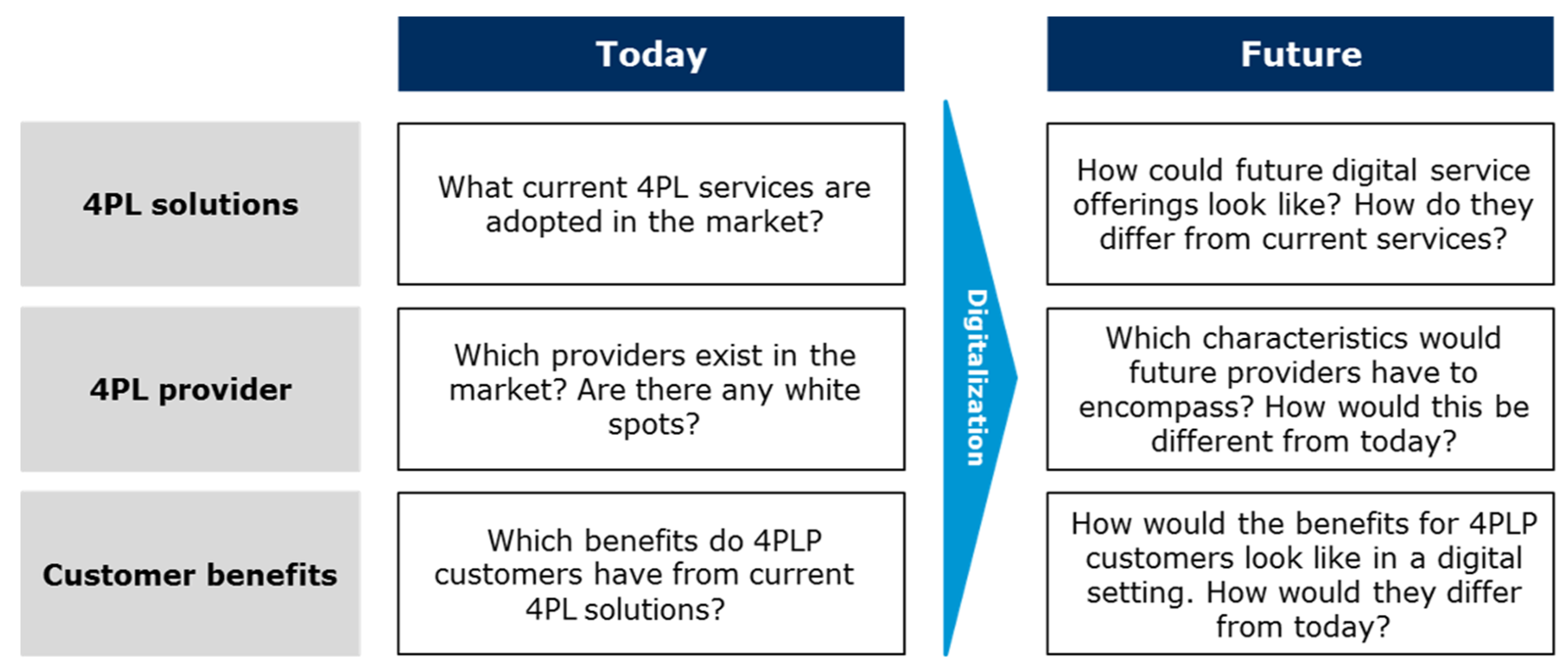

The online questionnaire was open for 39 days and a total of 34 respondents completed the survey. Out of these, no record had to be generally excluded. The questionnaire was accessed at a total of 73 times while most respondents that got beyond the introductory page, also finished the survey. Based on the total of 34 respondents, 14 considered to be potential 4PL clients (41%), 7 logistics service providers (21%), 2 IT providers (6%) and 11 firms providing consultancy services (32%). Most respondents were from manufacturing (29%) or transportation and storage (21%) with the remainder spread over diverse sectors. Regarding firm size, 97% of the participants stated to work in companies with 1000 or more employees and only one person was from a company of less than 50 employees. Similarly, 91% of the companies featured annual sales revenues above €250 m, only two respondents answered to be from a company between €50 m and €250 m and one below €50 m. Thus, it can be concluded that almost all participants are from multinational companies located in the DACH region (i.e., Germany, Austria and Switzerland). Accordingly, a tendency towards European operations can be observed: 21 respondents named a responsibility for operations in Europe and 13 on a global level. Exactly 50% of the respondents work on an operational level or are team leader responsible for one to five other employees. The others follow higher degrees of seniority while 24% of the participants are managers responsible for more than 100 employees. Finally, most respondents work in operations departments (68%). In the following, detailed results from the semi-structured interviews and structured online survey are presented including a comparison with extant literature for each of the three areas of 4PL solutions, 4PL providers and 4PL customer benefits as shown in

Figure 1.

3.1. 4PL Solutions

Firstly, we aimed at assessing 4PL service configurations that are currently offered. To asses this question, both findings from the initial semi-structured interviews as well extant scholarly literature on the 4PL concept were combined.

Looking closer at the extant literature, 4PLPs are regarded to be foremost responsible for selecting suitable logistics service providers to enable the desired transport and logistics operations [

50,

51,

52]. Moreover, 4PLPs are often associated with logistics planning and control activities. Win [

52] argued that inventory management is one of the key 4PL activities. Warehouse management, inventory planning, forecasting activities, customs management, routing operations and network optimization are further activities performed by 4PLPs in this respect [

23,

32,

52]. Additionally, 4PLPs are believed to have a consulting function and provide external expertise to their client company [

32,

46,

50]. They provide such value-added services to the client depending on the companies’ needs [

31,

53]. The 4PLP is also often said to be an intermediary and integrator, thus providing supply chain integration [

32,

54]. In this context, they provide a single interface for the client to communicate with the other actors [

1].

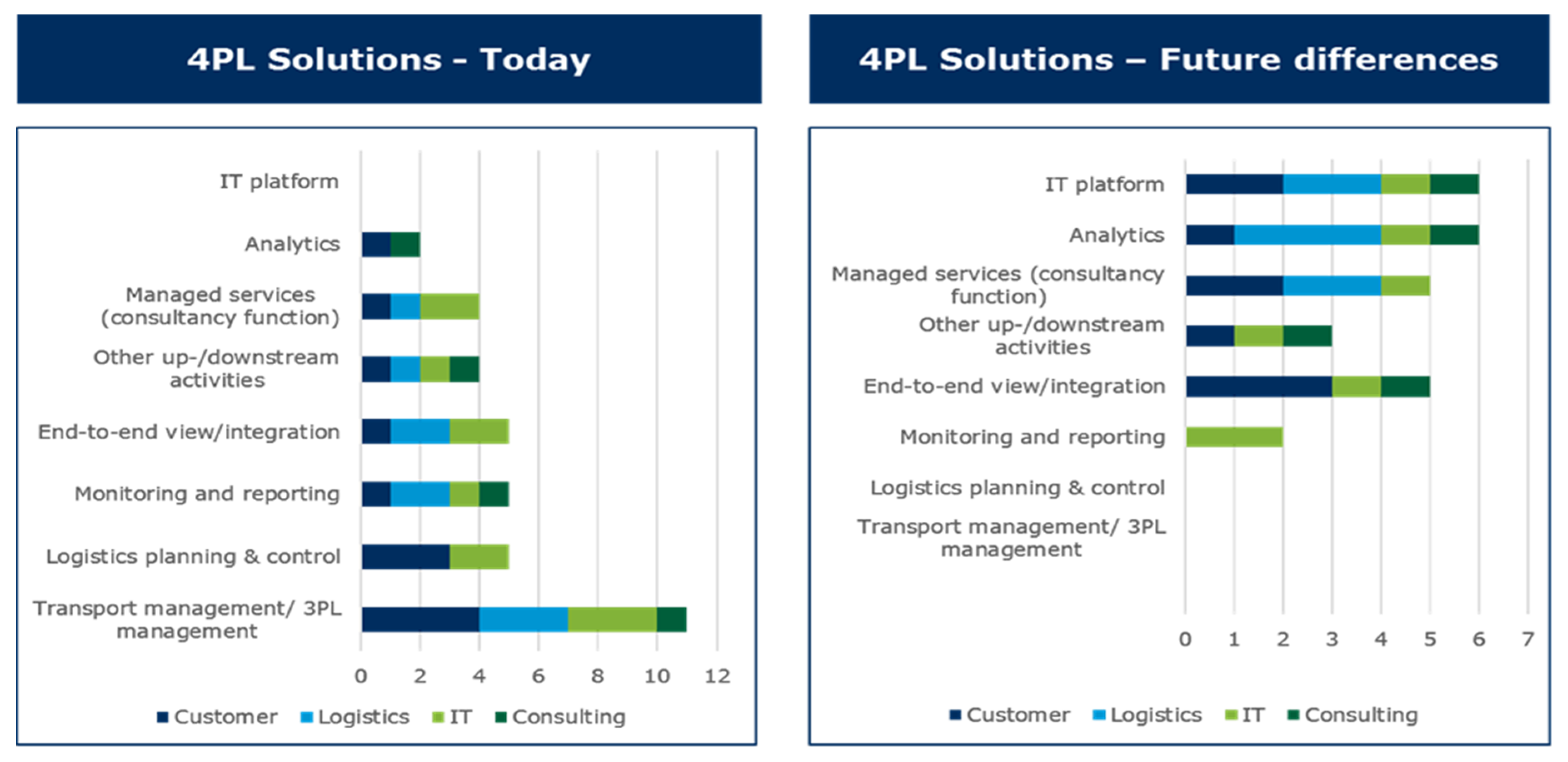

Nonetheless, based on the findings of the semi-structured interviews, it can be argued that in practice, 4PL solutions mainly center around transport management and 3PL selection as these two aspects were mentioned by all interviewees (see left side of

Figure 2). This also includes aspects such as service audits, customs management and ensuring that logistics operations run smoothly. Furthermore, five interviewees named services related to logistics planning and control activities like planning activities, forecasting and inventory control. Additional to these basic service offerings, further services are demanded by clients, most commonly classical logistics planning and control mechanisms similarly to the offerings of traditional 3PLPs. However, depending on the client’s operations, as indicated by some interviewees, a 4PLP may be responsible for a greater set of activities because of the complexity of the client’s operations.

Compared with 4PL services as mentioned in extant literature, it is found that 4PL services mentioned generally correspond. Nevertheless, it is important to state that based on the first 4PL information, its general basic service offerings should reach beyond services 3PLPs usually offer. According to the 4PL concept definition, 4PL services offered should be driven by integrative activities and focus on managing complex supply chains. Even though these aspects are mentioned by the interviewees, they seem not to receive the same broad acceptance today as outlined in extant literature. For the interpretation of these findings, it should be kept in mind that all interviewees have had prior experience with the 4PL concept.

Consequently, based on these findings, it can be suggested that there is no standard 4PL service offering that finds agreement in practice except for basic transport and logistics management services. Furthermore, 4PL services can be manifold and specifically targeted at the client’s needs with different degrees of responsibilities given to 4PLPs. While its personnel may be onsite working directly hand-in-hand with the client, in other settings orders would simply be exchanged by electronic means (for example EDI) to be executed by them.

Thereafter, the possible future for digital 4PL service configurations was examined. Therefore, results from the semi-structured interviews, the expert panel, as well as the structured online survey are jointly taken into account. Generally, there is a definite signal towards 4PLPs making an IT platform available (see right side of

Figure 2). In the semi-structured interviews, providing an IT platform is one of the most-mentioned aspects in the future and in the online questionnaire, the issue whether a 4PLP has to provide an IT platform achieve high consent. Nonetheless, it is not defined whether the 4PLP itself is establishing and hosting such a platform or rather sources it from an external IT provider and then just supervises operations. In any case, it can be argued that having an effective IT platform may positively influence the integration of supply chain partners, especially because it enables information sharing. This is in line with [

24] stating that by using IT systems effectively, transactional cost costs can be reduced by fostering co-operation and reducing complexity.

4PL integrative service activities is another aspect that was further examined in the online questionnaire. There, the respondents supported the observation that a 4PLP will foster integration (see

Table 2). The highest consent can be observed with the 4PL engaging in information sharing activities (INTISH). Nevertheless, importance could also lie in facilitating external integration of suppliers (INTEIS) and customers (INTEIC) as indicated before.

On the contrary, the respondents are rather opposed to a 4PLP managing the companies’ internal integration (INTIIN). This is in line with a low rate of agreement regarding the 4PLP taking care of the clients’ IT infrastructure. Integrative and end-to-end solutions are also aspects pointed out in the semi-structured interviews as; however, the number of observations is higher for current than for future 4PL solutions (see

Figure 2). Because the interviewees were asked about future differences, it is assumed that these aspects were simply not mentioned again.

Additionally, results from the structured online survey show that integration, and especially information sharing between the actors facilitated by the 4PLP positively influence its abilities to provide further 4PL services related to data analysis. Subsequent factor analysis with stepwise linear regression revealed positive effect of 4PL information sharing (INTISH) on 4PL monitoring (EDAMON), a positive influence of INTISH on 4PL analytics (EDAANA) and a positive influence of both INTISH and internal integration (INTIIN) on 4PL planning (EDAPLA) to be confirmed a (all highly statistically significant on a 5% level, see

Appendix A). Overall, a strong positive linear influence of 4PL integration (INT) on 4PL data analysis (EDA) is obvious (

Table 3). In conclusion, RH1 cannot be rejected because of a detected influence of 4PL integration (INT) on 4PL data analysis (EDA).

Analytics, planning and monitoring activities are issues raised in both surveys. Based on the perceptions of the interviewees, planning and monitoring are activities existent in the current 4PL portfolio (see

Figure 2). On the contrary, value-added services like analytics are almost mentioned for future 4PLPs. In the structured online survey, results show greatest consent of analytics with 4PLPs taking care of monitoring activities (see

Table 2). Nonetheless, the agreement with 4PL analytics and planning services is comparably high.

Lastly, it should be noted that one of the major aspects pointed out in the semi-structured interviews is that partnership between 4PLPs and their clients are transferring from operational to more strategic relationships and simultaneously become closer. In the end, managing an effective partnership is the second most mentioned aspect for the future of the 4PL concept (see right side of

Figure 2). This implies that 4PL providers do not only have to focus on presenting a good service portfolio but also need to bother about effectively managing their relationships with their clients ensuring trust.

Moreover, transport services should remain relevant in the future, it can be expected that the 4PL service portfolio will be enhanced with further offers like the provision of an IT platform and resulting possibilities for effective and efficient data analysis. These tools will especially encompass analytics, planning mechanisms as well as monitoring and reporting activities. Providing an IT platform has the potential to get a base product of 4PL services and according to the discussion in the expert panel, this could also be the chance for a company to become a provider of an industry-wide adopted IT platform.

3.2. 4PL Providers

This section points at the existing players in the market and possible white spots in the market. Because of a missing common understanding of 4PL concept, different taxonomies of 4PLPs have been suggested [

23,

32,

52,

55]. Razzaque and Chen Sheng [

55] focused on the difference in an asset basis of the provider. Win [

52] used these asset-basis criteria to differentiate between 3PL and 4PLPs and argues that there is a concern of 3PLPs offering 4PL services, because of their missing independency. Saglietto [

32] identified four general categories of 4PLPs: (s1) 4PLPs that focus on document engineering activities, (s2) 4PLPs that develop integrated supply chain management software, (s3) 4PL subsidiaries of logistics groups with 3PL operations and (s4) pure 4PL players. While (s1) provide very dedicated services, (s2) offer both consultative skills of supply chain modeling and IT skills of infrastructure transformation, (s3) have their strength in offering global logistics solutions. While both entities may belong to logistics groups, they could be legally independent. Finally, (s4) combine different skills and rely on the expertise of their personnel so that they engage in consultative and IT related activities but are also knowledgeable in transport operations [

32]. Pfohl et al. [

23] identified four key players in their study: (p1) logistics system service providers, (p2) pure 4PL players, (p3) IT provider and (p4) consulting companies. Furthermore, they pointed out several advantages and disadvantages of these providers. Nevertheless, a comprehensive market report of 4PLPs in the DACH region similarly to [

32] dealing with 4PLPs in France is virtually unknown to the authors.

Based on the results from our semi-structured interviews, we could identify five distinct categories of 4PLPs, namely (c1) large logistics groups, (c2) pure 4PL players, (c3) niche logistics providers, and (c4) consultancies or (c5) technology providers. For the DACH region, especially the large logistics groups DHL, Kühne+Nagel, DB Schenker and Damco were mentioned. Furthermore, 4Flow (

http://www.4flow.de/en.html) and 4PL Central Station (

http://4plcs.com/en/) were explicitly named as pure 4PL players. For niche logistics players it was pointed out that they are supplying a very specific service. Accenture was regarded as a possible 4PLP from a consultancy perspective but no specific IT company was mentioned. No indications were made on the provider’s market shares or positions in the market. Nevertheless, based on the frequency to which the actors were mentioned, indications can be made on the most well known actors. Notably, all 4PLPs labeled (c1) also offer 3PL and freight forwarding services and this again is in line with pre-existent relationships in a 3PL business area which may facilitate offering additional 4PL services, too [

8,

10,

21,

56,

57,

58,

59]. Furthermore, it can be assumed that (c3) are operating in smaller, particularly specialized areas that may not be exposed to a great change. In sum, it appears that the large logistics groups heavily dominating the current 4PL market, making it especially useful for multinational companies to cooperate with them because of their global reach and well-known portfolio of services.

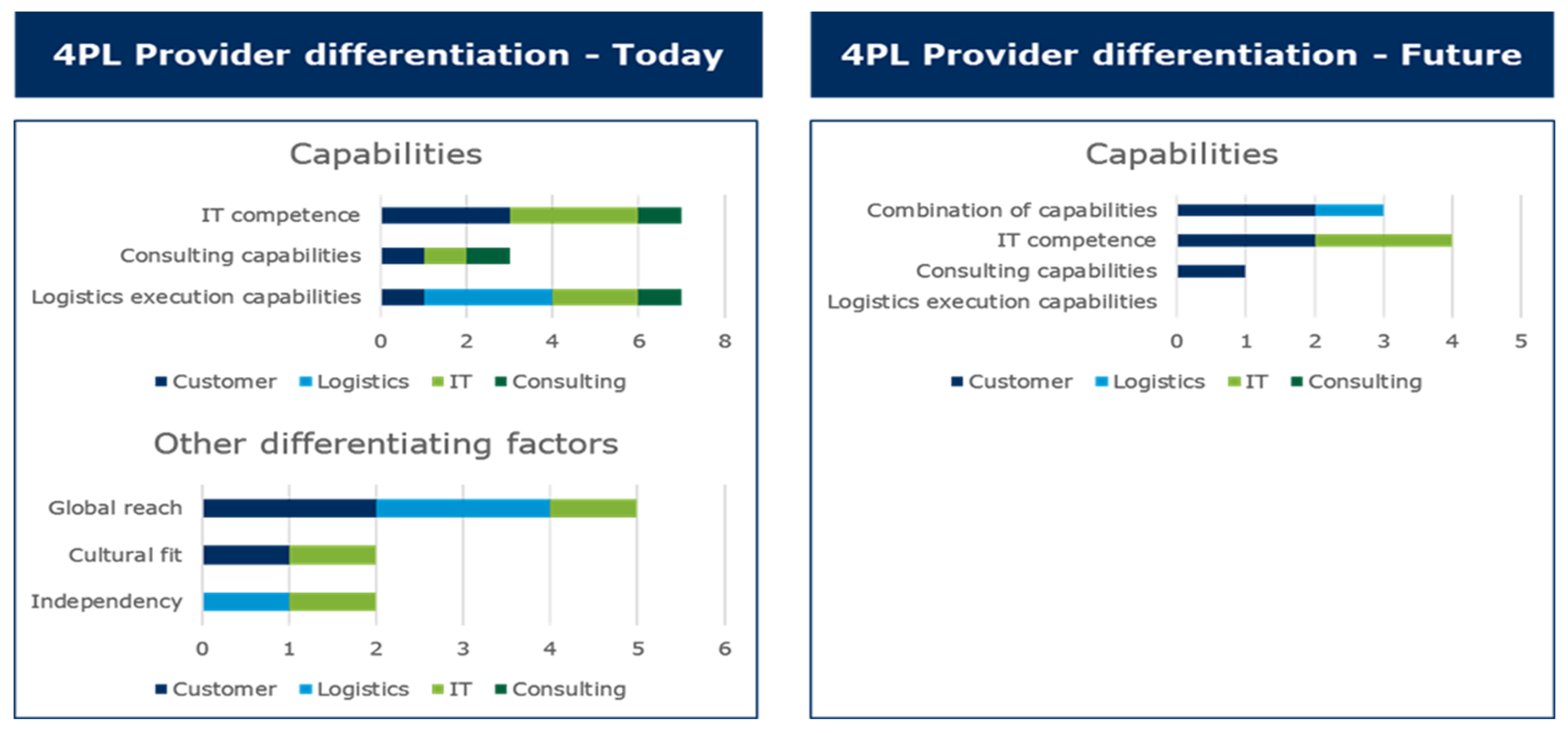

When it comes to the characteristics of future 4PLPs, inferences can be drawn on which companies may succeed in this 4PL market environment. Looking on results from both surveys (see

Figure 3 and

Table 4), it is obvious that IT competence of a 4PLP again plays an important role. As indicated in the previous section, especially providing an IT platform is a crucial future 4PL service. While the agreement for other areas of IT capabilities is lower, there is still a significant consent with the 4PLP being knowledgeable in IT business spanning activities and driving forward technological innovations. Consequently, the future 4PLP must possess own competence in the area of IT and may have choose to cooperate with a strong IT provider as technology partner if their own IT resources are not sufficient.

Concerning the structured online survey, it was expected that a 4PLP requires IT competence in the future because of the uprising trend of digitalization (see

Table 4)—thus, digitalization (DIG) should have a positive influence on 4PL IT competence (ITC). However, factor analysis of both influence of DIG on ITC (see

Table 3) as well as stepwise linear regression of factors of DIG on factors of ITC (see

Appendix A) resulted in an overall low model fit including statistically non-significant factors. Consequently, RH2 has to be rejected so that a straightforward influence of digitalization on IT competence of 4PLPs cannot be confirmed. However, a closer look at the semi-structured interview results unveils further aspects apart from IT competence that may influence the success of the 4PLP positively (see

Figure 3).

Because the 4PLP is considered to still be responsible for transport operations in the future, certain knowledge in logistics operations are a requirement. This fact that a stronger focus is laid on service activities and strategic operations, demanding service qualifications, is a clear indication of the importance of the 4PLP’s consultative function with some interviewees arguing that he has to combine these different capabilities. Furthermore, drivers for choosing a 4PLP today such as the global reach of operations (see

Figure 3) may also remain relevant in the future. Especially when working closely with the 4PLP, it may be beneficial for clients to have only a few 4PLPs that can take care of most of their businesses on a global scale.

Consequently, it can be assumed that the providers’ success is driven by their ability to adapt digital technologies and transfer the advantages to their client’s businesses. As outlined by the participants of the semi-structured interviews and at the expert panel, it remains interesting to see which influence this trend has on larger logistics groups, since these may take longer to adapt to new technological solutions. Nevertheless, participants also argue that 4PL subsidiaries are becoming more independent from their entities, and may thus be able to faster react to change.

3.3. 4PL Customer Benefits

This section points at assessing the benefits from engaging in a 4PL relationship in a current setting. Looking at extant literature, [

7] discussed that 4PL solutions are often applied to reduce logistics cost and direct cost savings can be achieved because a 4PLP is able to realize economies of scale and scope [

51]. Further economic benefits may arise from improved operations [

23] with 4PLPs may conduct logistics activities more effectively and efficiently, and thus achieve cost reductions [

29]. Along with cost reduction, optimized operations may also result in improvements in the services offered to the customers [

1] and better quality [

23]. Furthermore, supply chain utilization could be increased significantly [

60] and this may consequently increase revenue generated by the client [

3]. 4PLPs may additionally support in decreasing supply chain complexity faced by companies [

7,

24,

45,

46] and support with facing globalization challenges [

61]. Moreover, 4PL clients have the possibility to focus on their core competencies and spend less time on non-core activities [

1]. Moreover, 4PLPs provide valuable external expertise [

7] and customers can benefit from an increased flexibility in their operations [

23]. Additionally, Bade and Mueller [

3] argue that using a 4PL service can result in a competitive advantage compared to rivals and consequently, competitiveness [

62], and shareholder value could be increased [

54].

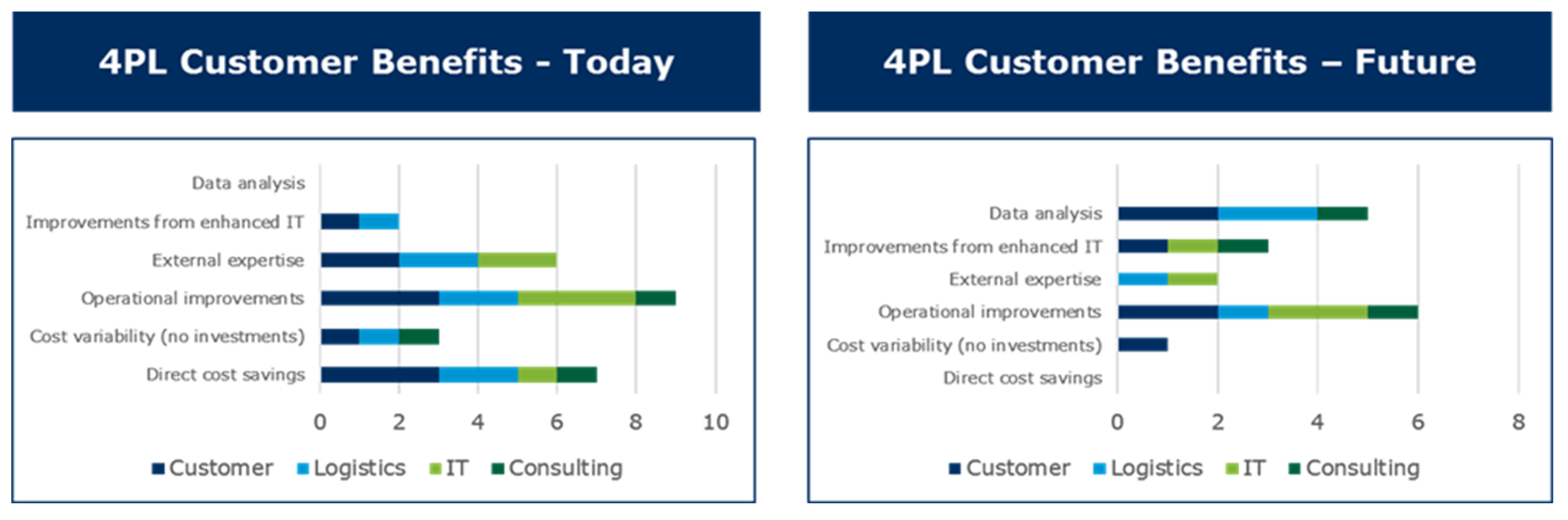

Based on the findings from the semi-structured interviews, both operational improvements as well as direct cost savings were most frequently mentioned advantages (see

Figure 4). Consequently, by cooperating with a 4PLP, a client can achieve directly observable cost reductions. Nonetheless, the interviewees also valued operational improvements a 4PLP brings about, as in the end, further cost decrease may reoccur and additionally, services can be improved. Furthermore, this aspect was actually pointed out more often than direct cost savings and certain interviewees argued that a 4PLP could only be successful when he creates value for the customer beyond directly reducing costs because these savings are most sustainable in the future.

Concerning the 4PL future, both surveys suggest that further service benefits may play a more prominent role in the future (see

Figure 4 and

Table 5). Based on our findings from the online questionnaire, managing, and thus reducing complexity is an important factor for future 4PLPs as they are supposed to manage diversity and higher product volumes and not only to support in reducing uncertainty (see

Table 5). Furthermore, in the expert panel it was argued that there would be a higher amount of smaller transactions in the future that the 4PLPs can support with. This implies that a focus is put on 4PL management services rather than on simple executional tasks. By shifting towards more management services, a higher value is perceived by benefits that can be achieved through these activities.

Factor analysis of both influence of supply chain complexity (SCC) on management of this complexity (MSC, see

Table 3) as well as stepwise linear regression of factors of SCC on the factors of MSC (see

Appendix A) resulted in an overall low model fit. Hence, a straightforward connection between supply chain complexity and its management by 4PLPs cannot be confirmed and so RH3 has to be rejected.

However, while conducting our semi-structured interviews it got also evident that 4PLPs are expected to create further benefits through data analysis resulting in optimized operations. This further backs up our former findings that there is a shift towards more service-oriented benefits. Additionally, it seems that less focus is put on direct cost savings because those were not explicitly mentioned. While cost savings might be important to be achieved as a baseline, it is certainly impossible to continuously drive down cost, for example, for transport activities. To achieve advantages beyond pure economies of scale in procurement, it might be required to optimize the entire transport operations.

Especially through additional benefits of visibility, transparency and flexibility, it may be possible to overcome risks that clients may fear of cooperating with a 4PLP. This may also result in the willingness to give the 4PLP more responsibility. Visibility and transparency could create further trust in their abilities and flexibility could allow for reducing the complexity resulting from cooperating with an outside provider. Through this, the 4PLP could regard more strategic issues instead of trying to achieve further direct cost cuttings in the operational areas.

In conclusion, it can be noted that a shift away from a cost cutting perspective towards a more value-oriented angle can be expected for the 4PL future. 4PLPs would therefore have to focus on further advantages they can achieve rather than direct cost reduction means. This would also allow for great opportunities for the 4PLPs to engage in further fields of operations and reach the full potential of advantages that have been pointed out in extant 4PL literature. In the expert panel, it was also argued that benefits might further increase once a critical mass of partners has been achieved and the 4PLP is operating and optimizing an entire supply chain network.

{kind=link}

{kind=link}

{kind=link}

{kind=link}