Electrifying the Last-Mile Logistics (LML) in Intensive B2B Operations—An European Perspective on Integrating Innovative Platforms

Abstract

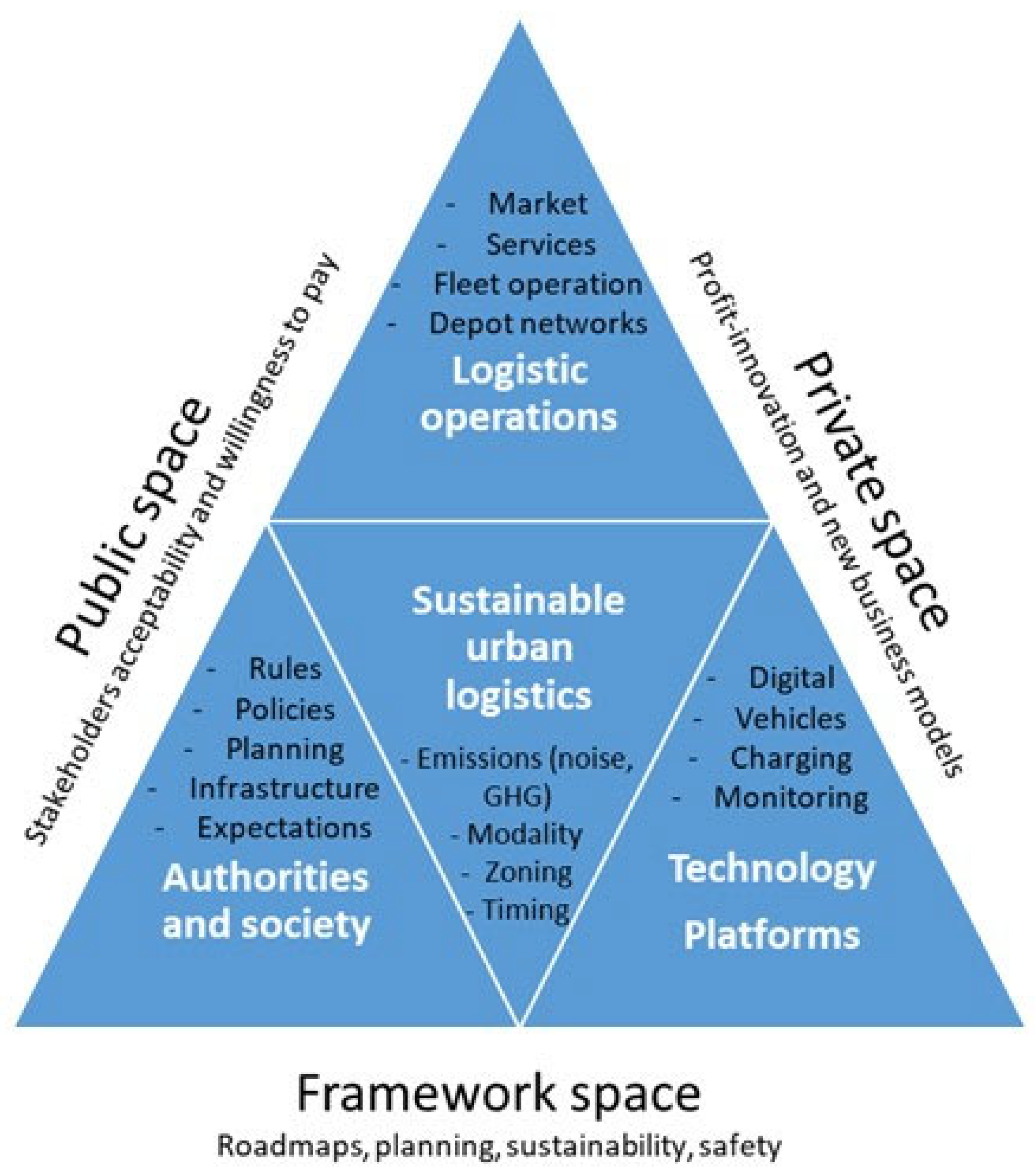

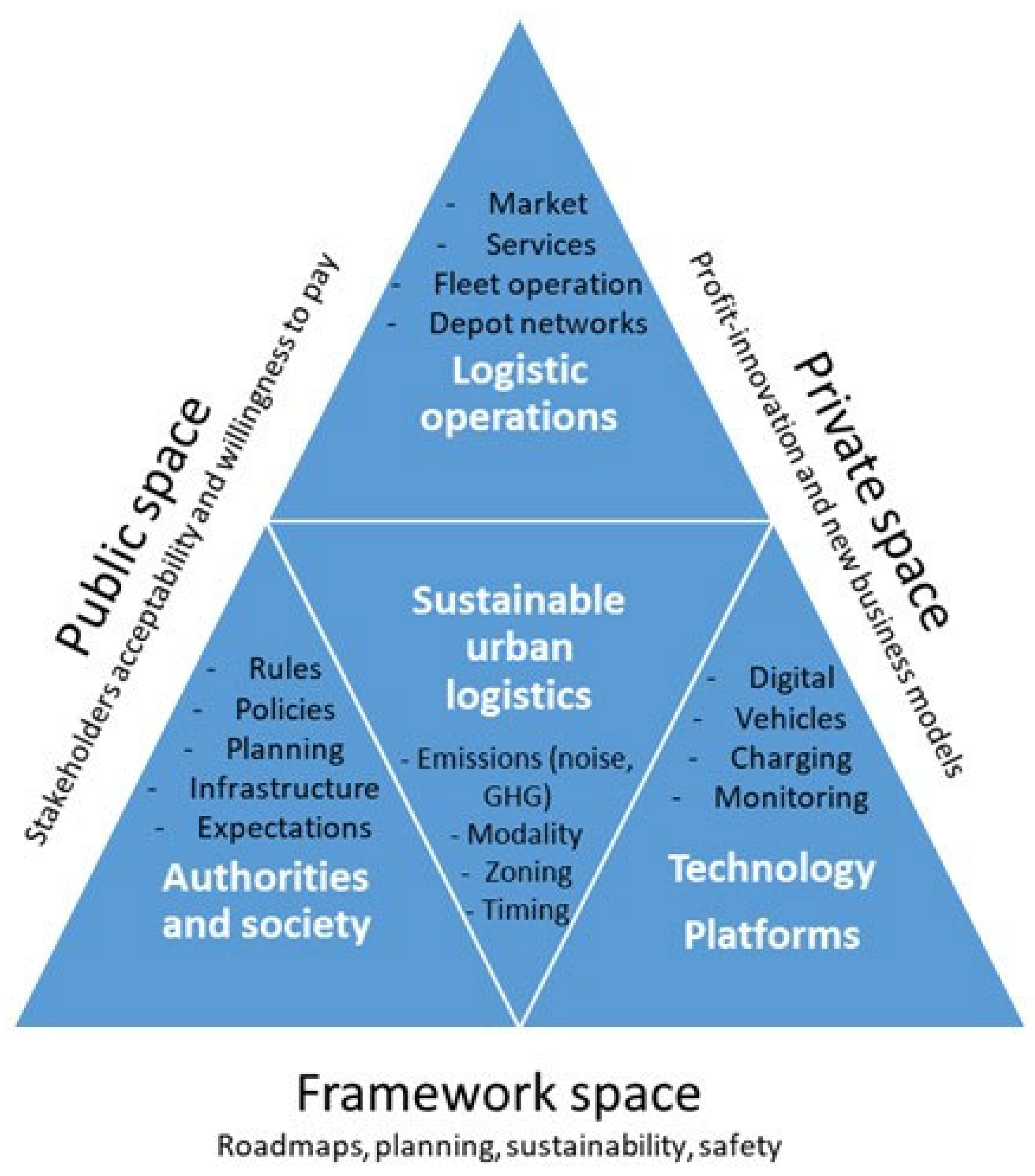

1. Introduction

- RQ1: Is electrification of LML economically viable in a European context?

- RQ2: What is the rationale for using Mobility Service Provider (MSP) cloud software, and how does it impact the profitability of LML?

- RSQ1: Why is charging redundancy needed, and which options are the most economically and functionally compatible?

- RSQ2: Could the digital nature of EVs and their infrastructure open the way for new business models in automotive aftermarket logistics?

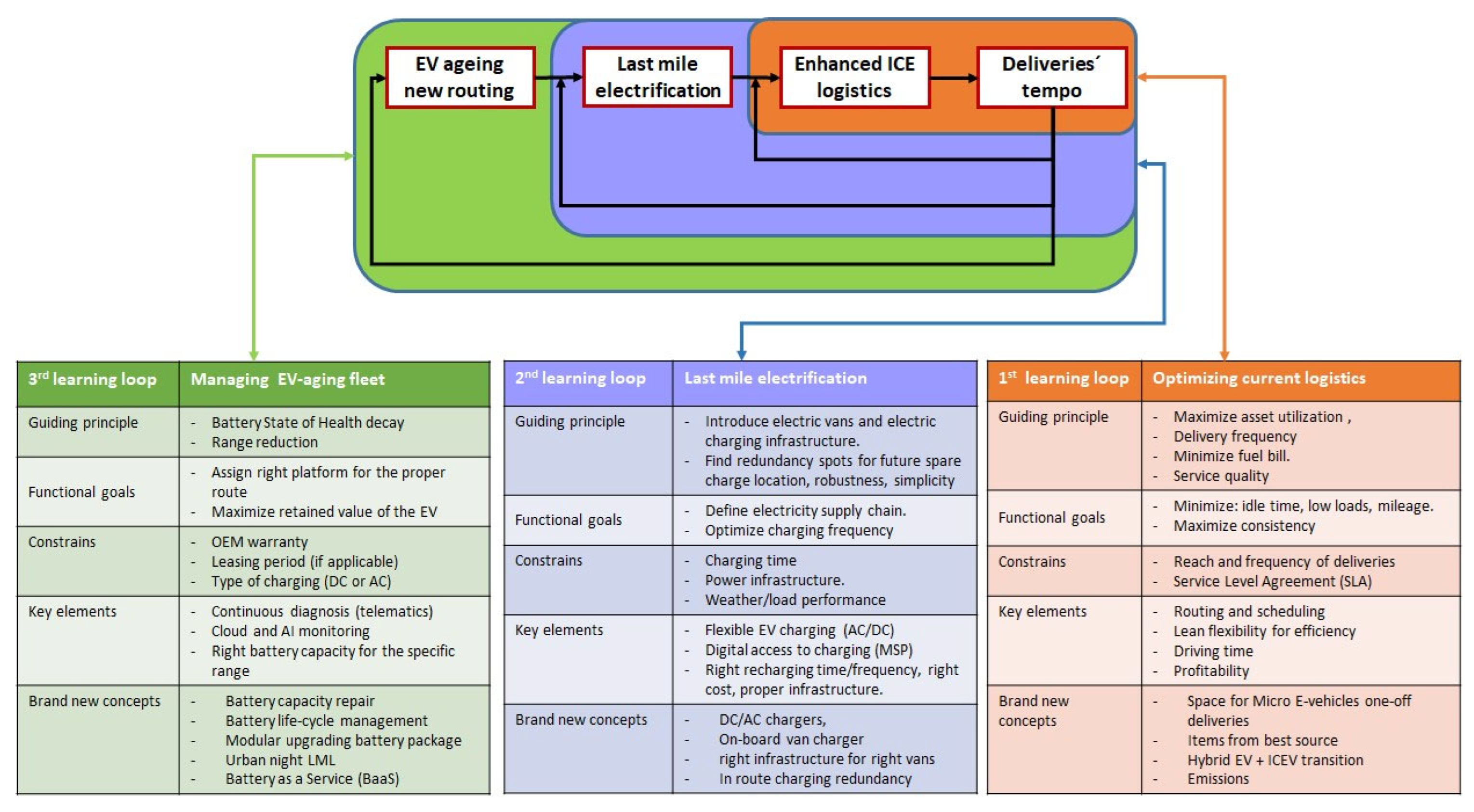

- RSQ3: Which learning processes could be derived for any other logistic operator planning or undergoing the electrification of their LML operations?

2. Materials and Methods

3. Results

- (1)

- Companies (CPOs mainly) that focus exclusively on EV charging must maximize the utilization of their installed assets.

- (2)

- On the other extreme of the spectrum are companies whose core business has nothing to do with EV charging but use it to attract users to their core business (hotels, malls, supermarkets). They need the broadest possible access to the charging assets and various payment methods.

- (3)

- The third category includes the drivers/users. For private users, low-cost access IDs allow them to charge in a very vast charging network at the European level.

4. Discussion and Conclusions

- Not having to invest in its own charging infrastructure

- Using the available parking space available to the original logistic operator

- Benefiting from all the data statistics and dashboards generated by the MSP

- Immediately available infrastructure without the previously mentioned time-costs/delays.

- -

- Charger choice: AC 22 kW

- -

- Charging infrastructure: Proprietary

- -

- Vehicles: compatible with both AC (22 kW) and DC (80 kW) charging

- -

- Battery packs 40–90 kWh (modular if possible)

- -

- Routing avoiding charging deviations and top-ups under control (multi-energy microgrid to incorporate PV in the future)

- -

- Redundancy level: 20%

- -

- MSP and remote EV diagnosis incorporated.

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

References

- Kasarda, J.D. Logistics is about competitiveness and more. Logistics 2017, 1, 1. [Google Scholar] [CrossRef]

- Demir, E.; Syntetos, A.; van Woensel, T. Last mile logistics: Research trends and needs. IMA J. Manag. Math. 2022, 33, 549–561. [Google Scholar] [CrossRef]

- Aljohani, K.; Thompson, R.G. An Examination of Last Mile Delivery Practices of Freight Carriers Servicing Business Receivers in Inner-City Areas. Sustainability 2020, 12, 2837–2858. [Google Scholar] [CrossRef]

- Marcucci, E.; Stathopoulos, A.; Gatta, V.; Valeri, E. A Stated Ranking Experiment to Study Policy Acceptance: The Case of Freight Operators in Rome’s LTZ. Ital. J. Reg. Sci. 2012, 11, 11–30. [Google Scholar] [CrossRef]

- Marcucci, E.; Stathopoulos, A.; Gatta, V.; Valeri, E. A Stated Ranking Experiment to Study Policy Acceptance: The Case of Freight Operators in Rome’s LTZ. Università degli Studi di Roma tre. CREI Centro Ricerca Interdipartamentale di Ecomia delle Instituzioni. CREI Working Paper 4/2011. Available online: http://host.uniroma3.it/centri/crei/pubblicazioni.html (accessed on 15 March 2024).

- Gonzales, J.N.; Garrido, L.; Vasallo, J.M. Exploring stakeholders’ perspectives to improve the sustainability of last mile logistics for e-commerce in urban areas. Res. Transp. Bus. Manag. 2023, 49, 101005. [Google Scholar] [CrossRef]

- Marciani, M.; Cossu, P.; Pompetti, P. How to increase stakeholders’ involvement while developing new governance model for urban logistic: Turin best practice. Transp. Res. Procedia 2016, 16, 343–354. [Google Scholar]

- Dohn, K.; Kramarz, M.; Przybylska, E. Interaction with City Logistics Stakeholders as a Factor of the Development of Polish Cities on the Way to Becoming Smart Cities. Energies 2022, 15, 4103. [Google Scholar] [CrossRef]

- Cebeci, M.S.; de Bok, M.; Tavasszy, L. The changing role and behaviour of consumers in last mile logistics services: A review. J. Supply Chain. Manag. Sci. 2023, 4, 114–138. [Google Scholar] [CrossRef]

- Marcucci, E.; Gatta, V.; Valeri, E.; Stathopoulos, A. Urban Freight Transport Modelling: An Agent-Specific Approach; FrancoAngeli: Milan, Italy, 2013. [Google Scholar]

- Gatta, V.; Marcucci, E.; Le Pira, M.; Stathopoulos, A.; Scaccia, L.; Delle Site, P. Willingness to Pay Measures to Tailor Policies and Foster Stakeholder Acceptability in Urban Freight Transport. Sci. Reg. 2018, 17, 351–370. [Google Scholar]

- Fossheim, K.; Andersen, J. Plan for sustainable urban logistics—comparing between Scandinavian and UK practices. Eur. Transp. Res. Rev. 2017, 9, 52–65. [Google Scholar] [CrossRef]

- Correia, D.; Vagos, C.; Marques, J.L.; Teixeira, L. Fulfilment of last-mile urban logistics for sustainable and inclusive smart cities: A case study conducted in Portugal. Int. J. Logisitcs Res. Appl. 2022, 1–28. [Google Scholar] [CrossRef]

- Aljohani, K.; Thompson, R.G. A Stakeholder-Based Evaluation of the Most Suitable and Sustainable Delivery Fleet for Freight Consolidation Policies in the Inner-City Area. Sustainability 2019, 11, 124–151. [Google Scholar] [CrossRef]

- van Oosterhout, S.A. Infrastructural Opportunities and Barriers for Last-Mile Delivery by Small Electric Distribution Vehicles in Historical City Centres in The Netherlands. Ph.D. Thesis, University of Groningen, Faculty of Spatial Sciences, Groningen, The Netherlands, 2022. [Google Scholar]

- Nordic Innovation. Innovative Sustainable Urban Last Mile. Available online: https://www.nordicinnovation.org/2024/innovative-sustainable-urban-last-mile (accessed on 15 March 2024).

- Bauwens, J.M.O. A Dynamic Roadmap for City Logistics Designing a dynamic roadmap towards 2025 for The Netherlands. Master’s Thesis, Systems Engineering, Policy Analysis and Management at the Faculty of Technology, Policy and Management Delft University of Technology, Delft, The Netherlands, 2015. [Google Scholar]

- Gkoumas, K.; Stepniak, M.; Cheimariotis, I.; Marques dos Santos, F.; Grosso, M.; Pekár, F. Research and Innovation in Urban Mobility and Logistics in Europe; EUR 31197; Publications Office of the European Union: Luxembourg, 2022; ISBN 978-92-76-56341-9. [Google Scholar] [CrossRef]

- Chocholac, J.; Kučera, T.; Sommerauerová, D.; Hruška, R.; Machalík, S.; Křupka, J.; Hyršlová, J. Smart city and urban logistics—Research trends and challenges: Systematic literature review. Oper. Econ. Transp. 2023, 4, A175–A192. [Google Scholar]

- UN-Habitat. World Cities Report—Envisaging the Future of Cities; UN-Habitat: United Nations Human Settlements Programme: Nairobi, Kenya, 2022; pp. 139–175. [Google Scholar]

- Cowie, J.; Fisken, K. Cycle Logistics Sustaining the Last Mile. In The Routledge Handbook of Urban Logistics; Monios, J., Budd, L., Ison, S., Eds.; Taylor & Francis: Oxfordshire, UK, 2023; pp. 59–71. [Google Scholar]

- Available online: https://www.einride.tech/insights/the-physical-and-digital-infrastructure-behind-intelligent-electric-freight (accessed on 15 March 2024).

- Meidute-Kavaliauskiene, I.; Cebeci, H.I.; Ghorbani, S.; Cincikaite, R. An Integrated Approach for Evaluating Lean Innovation Practices in the Pharmaceutical Supply Chain. Logistics 2021, 5, 74–91. [Google Scholar] [CrossRef]

- Silva, V.; Amaral, A.; Fontes, T. Sustainable Urban Last-Mile Logistics: A Systematic Literature Review. Sustainability 2023, 15, 2285–2312. [Google Scholar] [CrossRef]

- Patella, S.M.; Grazieschi, G.; Gatta, V.; Marcucci, E.; Carrese, S. The Adoption of Green Vehicles in Last Mile Logistics: A Systematic Review. Sustainability 2021, 13, 6. [Google Scholar] [CrossRef]

- Maniatis, P. Exploring the Viability of Last-Mile Delivery Solutions for Sustainable Supply Chains. preprints 2023, 2023060982. Available online: https://www.preprints.org/manuscript/202306.0982/v1 (accessed on 15 March 2024).

- Bachofner, M.; Lemardelé, C.; Estrada, M.; Pagès, L. City logistics: Challenges and opportunities for technology providers. J. Urban Mobil. 2022, 2, 10020–11030. [Google Scholar] [CrossRef]

- Wold Economic Forum. The Future of the Last Mile Ecosystem; World Economic Forum: Geneva, Switzerland, 2020. [Google Scholar]

- Macharia, V.M.; Garg, V.K.; Kumar, D. A review of electric vehicle technology: Architectures, battery technology and its management system, relevant standards, application of artificial intelligence, cyber security, and interoperability challenges. IET Electr. Syst. Transp. 2023, 13, e12083. [Google Scholar] [CrossRef]

- Buzoverov, E.; Zhuk, A. Comparative economic analysis for different types of electric vehicles. Int. J. Sustain. Energy Plan. Manag. 2020, 29, 57–68. [Google Scholar]

- Acharige, S.S.G.; Haque, M.D.E.; Arif, M.T.; Hosseinzadeh, N. Review of Electric Vehicle Charging Technologies, Configurations, and Architectures. IEEE Access 2023, 11, 41218–41255. [Google Scholar] [CrossRef]

- Alanazi, F. Electric Vehicles: Benefits, Challenges, and Potential Solutions for Widespread Adaptation. Appl. Sci. 2023, 13, 6016–6030. [Google Scholar] [CrossRef]

- Virmani, N.; Agarwal, V.; Karuppiah, K.; Agarwal, S.; Raut, R.D.; Paul, S.K. Mitigating barriers to adopting electric vehicles in an emerging economy context. J. Clean. Prod. 2023, 414, 137557. [Google Scholar] [CrossRef]

- Pamidimukkala, A.; Kermanshachi, S.; Rossenberger, J.M.; Hladik, G. Evaluation of barriers to electric vehicle adoption: A study of technological, environmental, financial, and infrastructure factors. Transp. Res. Interdiscip. Perspect. 2023, 22, 100962. [Google Scholar] [CrossRef]

- Available online: https://www.iea.org/articles/fuel-economy-in-the-european-union (accessed on 15 March 2024).

- Innovation Outlook. Innovation Outlook: Smart Charging for Electric Vehicles; International Renewable Energy Agency (IRENA): Abu Dhabi, United Arab Emirates, 2019; ISBN 978-92-9260-124-9. Available online: https://www.irena.org/-/media/Files/IRENA/Agency/Publication/2019/May/IRENA_Innovation_Outlook_EV_smart_charging_2019.pdf (accessed on 26 March 2024).

- Polat, H.; Hosseinabadi, F.; Hasan, M.M.; Chakraborty, S.; Geury, T.; El Baghdadi, M.; Wilkins, S.; Hegazy, O. A Review of DC Fast Chargers with BESS for Electric Vehicles: Topology, Battery, Reliability Oriented Control and Cooling Perspectives. Batteries 2023, 9, 121–157. [Google Scholar] [CrossRef]

- Steinstraeter, M.; Heinrich, T.; Lienkamp, M. Effect of Low Temperature on Electric Vehicle Range. World Electr. Veh. J. 2021, 12, 115–141. [Google Scholar] [CrossRef]

- Zhang, X.; Plant, E.; Valantasis Kanellos, N. An Evaluation of Ireland’s Sustainable Freight Transport Policy. Logistics 2022, 6, 65–88. [Google Scholar] [CrossRef]

- Available online: https://allianceautomotivegroup.eu/corporate-responsibility/ (accessed on 15 March 2024).

- Muñoz-Villamizar, A.; Solano-Charris, E.L.; Reyes-Rubiano, L.; Faulin, J. Measuring Disruptions in Last-Mile Delivery Operations. Logistics 2021, 5, 17–26. [Google Scholar] [CrossRef]

- Gilswijk, R.; Paalvast, M.; Ligterink, N.E.; Smokers, R. Real-World Fuel Consumption of Passenger Cars and Light Commercial Vehicles; TNO-R11664; TNO: The Hague, The Netherlands, 2020. [Google Scholar]

- Available online: https://blog.evbox.com/new-electric-light-commercial-vehicles (accessed on 15 March 2024).

- Available online: https://www.cargopedia.net/europe-fuel-prices (accessed on 15 March 2024).

- Available online: https://ec.europa.eu/eurostat/statistics-explained/index.php?title=Electricity_price_statistics#Electricity_prices_for_non-household_consumers (accessed on 15 March 2024).

- Available online: https://www.allego.eu/news/2022/december/charging-tariffs-january-2023 (accessed on 15 March 2024).

- Pavlovic, J.; Tansini, A.; Fontaras, G.; Ciuffo, B. The Impact of WLTP on the Official Fuel Consumption and Electric Range of Plug-in Hybrid Electric Vehicles in Europe. SAE Tech. Pap. 2017, 24, 133–144. [Google Scholar]

- Sarrafan, K.; Sutanto, D.; Muttaqi, K.M.; Town, G. Accurate Range Estimation for an Electric Vehicle Including Changing Environmental Conditions and Traction System Efficiency. Master’s Thesis, University of Wollongong, Wollongong, Australia, 2017. [Google Scholar]

- Available online: https://www.reuters.com/business/autos-transportation/iveco-group-nikola-reshuffle-joint-venture-electric-hybrid-trucks-2023-05-09/ (accessed on 15 March 2024).

- Available online: https://www.scania.com/group/en/home/newsroom/press-releases/press-release-detail-page.html/4271729-scania-and-einride-sign-deal-to-accelerate-electrification-of-road-freight-with-fleet-of-110-trucks (accessed on 15 March 2024).

- Available online: https://insideevs.com/news/565351/nikola-mobile-charging-trailer-explained/ (accessed on 15 March 2024).

- Available online: https://www.chargepoint.com/en-gb/blog/north-drives-electrification-heavy-duty-vehicles (accessed on 15 March 2024).

- UK Government. UK Statutory Instrument: The Public Charge Point Regulations 2023 No. 1168. Available online: https://www.legislation.gov.uk/ukdsi/2023/9780348249873 (accessed on 26 March 2024).

- UK Government. 2021 No. 1467 ROAD TRAFFIC the Electric Vehicles (Smart Charge Points) Regulations 2021 (Coming into Force 30 June 2022). Available online: https://www.legislation.gov.uk/uksi/2021/1467/contents/made (accessed on 26 March 2024).

- UK Government. Office of Product Safety and Standards. Complying with the Electric Vehicles (Smart Charge Points) Regulations 2021, May 2022. Available online: https://assets.publishing.service.gov.uk/media/628ce214e90e071f653a494a/Guide-to-evscp-regulations-2021-V2.1.pdf (accessed on 26 March 2024).

- ElaadNL. Nationale Agenda Laadinfrastructuur. Smart Charging Requirements (SCR). 2020. Available online: https://elaad.nl/wp-content/uploads/downloads/smart-charging-requirements-nl.pdf (accessed on 26 March 2024).

- NKL. Netherlands Knowledge Platform for Public Charging Infrastructure (www.nklnederland.nl). Uniform Standards for Charging Stations from Policy to Realization; NKL Nederland: Utrectht, The Netherlands, 2018. [Google Scholar]

- NAL. Dutch National Charging Infrastructure Agenda. Smart Charging for all 2022-2025 Action Plan, 2022.

- Venselaar, M.; Idema, H.-J.; Endriβ, T. ; Ministry of Foreign Affairs of The Nethelands. German Charging Infrastructure Regulations; Supporting Dutch Companies Understanding the German Framework; Rijksdienst voor Ondernemend Nederland: The Hague, The Netherlands, 2019. [Google Scholar]

- Available online: https://cms.law/en/int/expert-guides/cms-expert-guide-to-electric-vehicles/germany (accessed on 15 March 2024).

- Available online: https://www.euractiv.com/section/electricity/news/ev-chargers-heat-pumps-may-be-curtailed-in-germany-as-of-2024/ (accessed on 15 March 2024).

- Available online: https://www.netzerowatch.com/german-electricity-to-be-rationed-as-evs-and-heat-pumps-threaten-collapse-of-local-power-grids/ (accessed on 15 March 2024).

- Selter, J.-L.; Schmitz, J.; Schramm-Klein, H. Sustainability assessment of last mile electrification: A qualitative study in Germany. Transp. Res. Part D Transp. Environ. 2024, 126, 104019. [Google Scholar] [CrossRef]

- Available online: https://www.reuters.com/business/autos-transportation/eus-electric-dreams-short-circuited-by-ev-charging-gridlock-2023-12-04/ (accessed on 15 March 2024).

- Available online: https://driivz.com/blog/ev-smart-charging-regulations/ (accessed on 15 March 2024).

- Available online: https://www.edf.fr/en/the-edf-group/inventing-the-future-of-energy/electric-mobility-for-today-and-tomorrow/smart-charging (accessed on 15 March 2024).

- Li, Y.; Pei, W.; Zhang, Q. Improved Whale Optimization Algorithm Based on Hybrid Strategy and Its Application in Location Selection for Electric Vehicle Charging Stations. Energies 2022, 15, 7035–7060. [Google Scholar] [CrossRef]

- Chen, J.; Xu, J.; Chen, W.; Song, B. Locating and sizing method of electric vehicle charging station based on Improved Whale Optimization Algorithm. Energy Rep. 2022, 8, 4386–4400. [Google Scholar] [CrossRef]

- Yu, N.K.; Jiang, W.; Hu, R.; Qiang, B.; Wang, L. Learning Whale Optimization Algorithm for Open Vehicle Routing Problem with Loading Constraints. Discret. Dyn. Nat. Soc. 2021, 2021, 8016356. [Google Scholar] [CrossRef]

- Pham, V.H.S.; Nguyen, V.N.; Dang, N.T.N. Hybrid whale optimization algorithm for enhanced routing of limited capacity vehicles in supply chain management. Nat. Portfolio. Sci. Rep. 2024, 14, 793–822. [Google Scholar] [CrossRef] [PubMed]

- Na, H.S.; Kweon, S.J.; Park, K. Characterization and Design for Last Mile Logistics: A Review of the State of the Art and Future Directions. Appl. Sci. 2022, 12, 118–139. [Google Scholar] [CrossRef]

- Phuc, P.N.; Phuong Thao, N.L. Ant Colony Optimization for Multiple Pickup and Multiple Delivery Vehicle Routing Problem with Time Window and Heterogeneous Fleets. Logistics 2021, 5, 28–41. [Google Scholar] [CrossRef]

- Basma, H.; Rodriguez, F.; Hildemeier, J.; Jahn, A. Electrifying Last-Mile Delivery—A Total Cost of Ownership Comparison of Battery-Electric and Diesel Trucks in Europe; ICCT: Washington, DC, USA, 2022; Available online: https://www.raponline.org/knowledge-center/electrifying-last-mile-delivery/ (accessed on 26 March 2024).

- Hildemeier, J.; Jahn, A.; Rodriguez, F. Electrifying EU City Logistics: An Analysis of Energy Demand and Charging Cost. ICCT: The Hague, Netherlands, 2020. [Google Scholar]

- Letnik, T.; Hanžič, K.; Luppino, G.; Mencinger, M. Impact of Logistics Trends on Freight Transport Development in Urban Areas. Sustainability 2022, 14, 16551. [Google Scholar] [CrossRef]

- Kin, B.; Hopman, M.; Quak, H. Different Charging Strategies for Electric Vehicle Fleets in Urban Freight Transport. Sustainability 2021, 13, 13080. [Google Scholar] [CrossRef]

- van der Kam, M.; Bekkers, R. Mobility in the smart grid: Roaming protocols for EV charging. IEEE Trans. Smart Grid 2023, 14, 810–822. [Google Scholar] [CrossRef]

- Hensel Roth, T.; Latham, O.; Glotzer, E.; Tzanetaki, C.A.; Stocker, R.; Caputo, L.; Nobili, F. Competition Analysis of the Electric Vehicle Recharging Market across the EU27 + the UK— Market for the Provision of Publicly Accessible Recharging Infrastructure and Related Service; European Commission Directorate-General for Competition and CRA Associated; Publications Office of the European Union: Luxembourg, 2023; Available online: https://op.europa.eu/en/publication-detail/-/publication/c9f5b4eb-72ee-11ee-9220-01aa75ed71a1 (accessed on 15 April 2024).

- Available online: https://www.statista.com/topics/4226/energy-prices-in-the-eu/#topicOverview (accessed on 15 March 2024).

- Masrur, H.; Shafie-Khah, M.; Hossain, M.J.; Senjyu, T. Multi-Energy Microgrids Incorporating EV Integration: Optimal Design and Resilient Operation. IEEE Trans. Smart Grid 2022, 13, 3508–3518. [Google Scholar] [CrossRef]

- Chowdary, A.; Rao, S.S. Grid-connected photovoltaic-based microgrid as charging infrastructure for meeting electric vehicle load. Front. Energy Res. 2022, 10, 961734. [Google Scholar] [CrossRef]

- Wang, D. Microgrid Based on Photovoltaic Energy for Charging Electric Vehicle Stations: Charging and Discharging Management Strategies in Communication with the Smart Grid. Electric Power. Ph.D. Thesis, Université de Technologie de Compiègne, Compiègne, France, 2021. [Google Scholar]

- Tkac, M.; Kajanova, M.; Bracinik, P. A Review of Advanced Control Strategies of Microgrids with Charging Stations. Energies 2023, 16, 6692. [Google Scholar] [CrossRef]

- International Energy Agency (IEA). Electricity 2024—Analysis and Forecast to 2026; IEA Publications International Energy: Agency, France, 2024. [Google Scholar]

- Mashoodi, B.; Muñoz Unceta, P. Regional allocation of EV chargers’ grid load. Ann. GIS 2023, 29, 227–241. [Google Scholar] [CrossRef]

- Huang, X.; Li, X.; Yuan, X.; He, B.; Li, J. An Economic Evaluation of Electric Vehicle Charging Infrastructure in Public Places in China. IOP Conf. Ser. Earth Environ. Sci. 2018, 168, 12018. [Google Scholar] [CrossRef]

- Pardo-Bosch, F.; Pujadas, P.; Morton, C.; Cervera, C. Sustainable deployment of an electric vehicle public charging infrastructure network from a city business model perspective. Sustain. Cities Soc. 2021, 71, 102957. [Google Scholar] [CrossRef]

- Nigro, N.; Frades, M. Business Models for Financially Sustainable EV Charging Networks; Center for Climate and Energy Solutions (C2ES): Olympia, WA, USA, 2015. [Google Scholar]

- Ma, T.Y.; Fang, Y. Survey of charging management and infrastructure planning for electrified demand-responsive transport systems: Methodologies and recent developments. Eur. Transp. Res. Rev. 2022, 14, 36. [Google Scholar] [CrossRef]

- Nagamitsu, S.; Gondo, R.; Nagaoka, N.; Al-Karakchi, A.A.A.; Putrus, G.; Wang, Y. A Novel Battery Diagnostic Method for Smart Electric Vehicle Charger. In Proceedings of the 2018 53rd International Universities Power Engineering Conference (UPEC), Glasgow, UK, 4–7 September 2018; pp. 978–984. [Google Scholar]

- ISO-IEC ISO 15118-1:2019(E); Road vehicles—Vehicle to Grid Communication Interface—Part 1: General Information and Use-case Definition. International Organization for Standardization: Geneva, Switzerland, 2019; pp. 1–8.

- ISO-IEC ISO 15118-20:2022(E); Road Vehicles—Vehicle to Grid Communication Interface—Part 20: 2nd Generation Network Layer and Application Layer Requirements. International Organization for Standardization: Geneva, Switzerland, 2022; pp. 1–10.

- Rezvanizaniani, S.M.; Liu, Z.; Chen, Y.; Lee, J. Review and recent advances in battery health monitoring and prognostics technologies for electric vehicle (EV) safety and mobility. J. Power Sources 2014, 256, 110–124. [Google Scholar] [CrossRef]

- Frendo, O.; Graf, J.; Gaertner, N.; Stuckenschmidt, H. Data-driven smart charging for heterogeneous electric vehicle fleets. Energy AI 2020, 1, 100007–100019. [Google Scholar] [CrossRef]

- Nait-Sidi-Moh, M.; Ruzmetov, A.; Bakhouya, M.; Naitmalek, Y.; Gaber, J. A Prediction Model of Electric Vehicle Charging Requests. Sci. Direct Procedia Comput. Sci. 2018, 141, 127–134. [Google Scholar] [CrossRef]

- Kostopoulos, E.D.; Spyropoulos, G.C.; Kaldellis, J.K. Real-world study for the optimal charging of electric vehicles. Energy Rep. 2020, 6, 418–426. [Google Scholar] [CrossRef]

- Powell, S.; Vianna Cezar, G.; Min, L.; Azevedo, I.; Rajagopal, R. Charging infrastructure access and operation to reduce the grid impacts of deep electric vehicle adoption. Nat. Energy 2022, 7, 932–945. [Google Scholar] [CrossRef]

- Slávika, R.; Gnap, J. Selected Problems of Night—Time Distribution of Goods within City Logistics. Transp. Res. Procedia 2019, 40, 497–504. [Google Scholar]

- Chowdhury, T.; Vaughan, J.; Saleh, M.; Mousavi, K.; Hatzopoulou, M.; Roorda, M.J. Modeling the Impacts of Off-Peak Delivery in the Greater Toronto and Hamilton Area. Transp. Res. Rec. 2022, 2676, 413–425. [Google Scholar] [CrossRef]

- Sánchez-Díaz, I.; Georén, P.; Brolinson, M. Shifting urban freight deliveries to the off-peak hours: A review of theory and practice. Transp. Rev. 2016, 37, 521–543. [Google Scholar] [CrossRef]

- Kong, C.; Rimal, B.P.; Reisslein, M.; Maier, M.; Bayram, I.S.; Devetsikiotis, M. Cloud-Based Charging Management of Heterogeneous Electric Vehicles in a Network of Charging Stations: Price Incentive Versus Capacity Expansion. IEEE Trans. Serv. Comput. 2022, 15, 1693–1706. [Google Scholar] [CrossRef]

- Klapwijk, P.; Driessen-Mutters, L. Exploring the Public Key Infrastructure for ISO 15118 in the EV Charging Ecosystem; ElaadNL: Arnhem, The Netherlands, 2018. [Google Scholar]

- Kim, T.; Makwana, D.; Adhikaree, A.; Vagdoda, J.S.; Lee, Y. Cloud-Based Battery Condition Monitoring and Fault Diagnosis Platform for Large-Scale Lithium-Ion Battery Energy Storage Systems. Energies 2018, 11, 125. [Google Scholar] [CrossRef]

- Sardar, M.U.; Vaimann, T.; Kütt, L.; Kallaste, A.; Asad, B.; Akbar, S.; Kudelina, K. Inverter-Fed Motor Drive System: A Systematic Analysis of Condition Monitoring and Practical Diagnostic Techniques. Energies 2023, 16, 5628. [Google Scholar] [CrossRef]

- Serrano, A.; Kalenatic, D.; López, C.; Montoya-Torres, J.R. Evolution of Military Logistics. Logistics 2023, 7, 22–46. [Google Scholar] [CrossRef]

- Penge, P. La logistica e l’eterno conflitto fra efficienza ed eficacia. Riv. Ital. Dif. RID 2023, 10, 38–46. [Google Scholar]

- Available online: https://www.energysage.com/local-data/electricity-cost/ (accessed on 25 August 2023).

- Available online: https://ycharts.com/indicators/us_retail_diesel_price# (accessed on 25 August 2023).

- Borlaug, B.; Salisbury, S.; Gerdes, M.; Muratori, M. Levelized cost of charging electric vehicles in the United States. Joule 2020, 4, 1470–1485. [Google Scholar] [CrossRef]

- Schuur, P.C.; Kellersmann, C.N. Improving Transport Logistics by Aligning Long Combination Vehicles via Mobile Hub & Spoke Systems. Logistics 2022, 6, 18. [Google Scholar] [CrossRef]

- Paidi, V.; Nyberg, R.G.; Håkansson, J. Dynamic Scheduling and Communication System to Manage Last Mile Handovers. Logistics 2020, 4, 13. [Google Scholar] [CrossRef]

- Leijon, J.; Boström, C. Charging Electric Vehicles Today and in the Future. World Electr. Veh. J. 2022, 13, 139–154. [Google Scholar] [CrossRef]

- Logistics Trends 2023 | Logistics Industry Trends | Discover DHL. Available online: https://www.dhl.com/discover/en-us/global-logistics-advice/logistics-insights/logistics-and-delivery-trends-2023 (accessed on 26 March 2024).

- Pevec, D.; Babic, J.; Podobnik, V. Electric Vehicles: A Data Science Perspective Review. Electronics 2019, 8, 1190. [Google Scholar] [CrossRef]

- Alaee, P.; Bems, J.; Anvari-Moghaddam, A. A Review of the Latest Trends in Technical and Economic Aspects of EV Charging Management. Energies 2023, 16, 3669. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Van Type | Diesel Average Range (Euro 6) | |

|---|---|---|

| Liters/100 km | km/Liter | |

| Up to L1H1 | 7.1 (peak at 9.3 in city loaded) | 16.4 |

| Up to L3H3 | 8.8 (peak at 10.68) | 12.7 |

| Van Type | Electric average range | |

| kWh/100 km | km/kWh | |

| Up to L1H1 gen.2 | 16.7 | 6 |

| Up to L3H3 gen.1 | 20 | 5 |

| Logistic Type | Routing | Delivery Points | Frequency/Tempo | Response Timing | Fleet Use | Time for Scheduling Planning | Key Metrics |

|---|---|---|---|---|---|---|---|

| Scheduled | Random optimized | Variable (customer and collection points) | As per customer convenience | Planned | Efficient | Medium High | Cost per delivery on right time spot |

| Hybrid (a) | Fixed multi-drop routing | Fixed/known Order–based (b) | High Tempo and frequency | Fast | Medium | Short | Percentage of orders in SLA (c) |

| On-demand | Simple scheduling | Variable | At the earliest | Instant Immediate | Low | Short | Minimum TAT (d) |

| Type | Variable | Rationale |

|---|---|---|

| Included | EV platforms | Analysis based on actual vehicle performance on commercially available platforms (for the same load-carrying and delivery frequencies) |

| AC charging (own or external) and in-route recharging | It is simpler, less expensive, less demanding on the grid, and easier to obtain authorization for installation. Recharging stops are a defining feature of electric last-mile distribution. | |

| Cloud-based access operators | It provides access to other charging operators and controls the fleet’s electricity use, but it can also be a significant cost source. | |

| Leased EV-vehicles | Aging vehicle key variables (range and remaining value) are irrelevant at this stage and simplify the model | |

| Cloud-based telemetry of electric components | More capillary analysis of the effects of charging frequency and power on battery life/performance | |

| Smart charging and diagnosis | Smart charging is mandatory in some geographic areas to share available grid power. The charger network (and redundancy) is set accordingly. | |

| Excluded | DC charging and depot model | More stringent electric requirements, higher maintenance costs, more protracted approvals, and higher electricity costs for the user. |

| Digital e-commerce platform, uncertain customer availability | The distribution networks under study have state-of-the-art e-commerce platforms. The number of reverse logistics due to failure in e-commerce is close to nil. As deliveries occur at the customer workshops (based on a digital order), availability is not uncertain. | |

| New delivery platforms (drones and autonomous vehicles) and fab-shops | Only technology-mature and currently available vehicles for electrifying the last-mile distribution logistics; 3D-printing fab shops (or concurrent manufacturing) are excluded as not yet adequate for high-end (safety-critical) mechanical components | |

| Proximity hubs and collecting points (lockers) | Not part of the current automotive aftermarket business model and the Service Level Agreement (SLA) of the logistic operator with its customers | |

| Owned or outsourced EV platforms | Eliminates the need to optimize the routing to adapt for the range decay with the battery aging. | |

| Reverse logistics and cross-docking | Eliminates the need to optimize the routing to adapt for the range decay with the battery aging | |

| Detour kilometers and scheduling. | Route re-design to provide redundancy between routes but not assume detours due to failing EV platforms or unavailable chargers. Scheduling is unknown (it is order-dependent), but routing is | |

| PV and energy storage | It is already in the company forecast, but the economics still need to mature more for the current model. It can undoubtedly reinforce profitability, but how much or with what payback time still needs to be consolidated. | |

| Public incentive | Any viability of the electrification must be independent of any local (and temporal) public incentive. | |

| Weather and road congestion/works | The same cities and roads, therefore, have the same external disruptions. Same customer dispersion. EV might benefit from city access otherwise closed to ICE vehicles. | |

| Maintenance skills | The operator owns the largest network of EV workshops in Europe and will ensure vehicle availability. Redundancy numbers and service contracts with the provider cover chargers’ availability | |

| Eastern European countries and Iberian peninsula operations | The recently acquired and expanding operations in Eastern Europe and the Iberian peninsula are not as consolidated as the core four European zones (UK, D, F, Benelux) |

| Variables | |||||

|---|---|---|---|---|---|

| Description | Units | Symbol | Remarks | ||

| Number small vans | quantity | ns | Actual values of the electrified LML fleet in the four European countries where LML is electrified | ||

| Number large vans | nl | ||||

| km/year/van (small) | km/y | kms | kms: 40.000 km/y (actual fleet average) | ||

| Km/year/van (large) | kml | kml: 60.000 km/y (actual fleet average) | |||

| Fuel specific consumption | km/L | SFC | Operator Test shows an average diesel range of 13.94 km/L while the larger vans (up L3H3) have an average range of 11.36 km/L. This is in line with [42] | ||

| Electricity specific consumption | km/kWh | SEC | Use actual vehicle specs and cross-check with https://blog.evbox.com/new-electric-light-commercial-vehicles (accessed on 15 March 2024) [43] Light commercial EVs are between 5.5 and 6.6 km/kWh (we used 6 km/kWh) while L3H3 vehicles are around 3.4 and 5.25 kWh7 (we used 4.5 km/kWh) | ||

| Fuel consumption/year | l/y | ly | Based on vehicle specs and actual fleet consumption. Data in line with [35] | ||

| Fuel Price | €/l | Pfuel | From [44] | ||

| Electricity grid price | €/kWh | Pelec | European non-household electricity tariffs [45] | ||

| Public charging price | €/kWh | PPC | Based on actual rates from European charging operators. [46] | ||

| Leasing extra cost | €/van/y | Clease | Actual leasing proposals. Small vans: 1.440 €/y, and large vans: 2.400 €/y | ||

| Chargers cost | €/charger | Pch | Cost of 22 kW AC charger. Different as per country specifications | ||

| Installation cost | €/charger | Pinst | Cost of installing and activating each charger | ||

| Investment | € | ICI | One-off investment covering charger cost + installation | ||

| Number of charger | n.a. | Nc | One charger per van | ||

| Redundancy margin | % | R% | 20% margin on top of the total number of chargers | ||

| Equations | |||||

| Parameter | Formula | units | Remarks | ||

| Fuel cost (per type) | €/y | n and km for the specific country SFC for specific type of van Total fuel cost per country: fuel cost small vans + fuel cost large vans per country | |||

| Electricity cost (own chargers only) | €/y | n and km for the specific country SEC for specific type of van Total electricity cost/country: electricity cost small vans + electricity cost large vans | |||

| Energy margin | Fuel cost—electricity cost | €/y | Different for every country | ||

| Electricity cost public + private charging | €/y | %: percentage of public charging | |||

| Extra leasing cost | €/y | Extra leasing cost based on fleet composition | |||

| Operational margin | Energy margin—extra leasing cost | €/y | Excluding any Mobility Service Provider (MSP) | ||

| Investment | € | Calculation will include high-end and low-end scenarios | |||

| Pay-back period | years | ||||

| Key Variable | Micro EV Delivery Platforms | First and Second Domain of Distribution Chain | Next Frontier Distribution Chain | ||||||

|---|---|---|---|---|---|---|---|---|---|

| First Generation | Second Generation | Third Generation | |||||||

| Up to L1H1 | From L1H1 to L4H3 | Up to L1H1 | From L1H1 to L4H3 | L1H1 | From L1H1 to L4H3 | Trucks | Lorries and Prime Movers | ||

| Battery size, kWh | 5–10 | 35–50 | 35–50 | 35–50 | 35–91 | 37–90 | 70–140 | 110–200 | 350–750 |

| WLTP range, km (a) | 75–110 | 220–280 | 110–135 | 90–250 | 120–250 | 100–325 | 180–340 | 150–225 (f) | 330–530 |

| AC charging | YES | YES | YES | YES | YES | YES | YES | YES | YES |

| Internal charger, kW | 2.3 | 2.3–7.4 | 2.3–7.4 | 11–22 | 11–22 | 22 | 22 | 22 | 22 |

| DC charging | NO | NO | NO | YES | YES | YES and NO | YES (h) | NO | YES |

| Max DC power, kW | 50–80 | 50–80 | 110–170 | 120–150 | 150–350 | ||||

| Type of plug | Type 2 | Type 2 | Type 2 | CCS | CCS | Type 2 or CCS | CCS | Type 2 | CCS |

| AC full charging, h | 4–8 | 4.5–8 | 10–22 | 3.5–5 | 1.5–5 | 1.5–5 | 3–6 | 5–8 | No viable |

| DC full charging, h | 0.4–0.6 | 0.4–1.5 | 0.5–0.9 | 0.5–1 | 1–2 | ||||

| New EV concept | YES | NO | NO | NO | NO | YES | YES | YES | YES |

| Suitable for intensive logistics? | YES (d) | NO (e) | NO (e) | YES | YES | YES | YES | YES | YES |

| Payload, ton (b) | 0.06–0.240 | 0.3–0.75 | 0.7–0.9 | 0.5–0.8 | Up to 1.7 | Up to 1 (g) | Up to 1.7 (g) | 3–10 | 16–18 |

| TRL (c) | 9 | 9 | 9 | 9 | 9 | 8–9 | 8 | 7–8 | 7 |

| Some vehicle models | (i) | (j) | (k) | (l) | (m) | (n) | |||

| General Optimization Criteria | ||

|---|---|---|

| Performance metrics | Operational | Profitability (total cost reduction) |

| Quality and service agreement (time constrains) | ||

| Consistency | ||

| Simplicity | Reducing navigation complexity | |

| Clustering and geometric partitioning | ||

| Compacting | ||

| Minimizing electricity top-up time | ||

| Separation vs. overlapping | ||

| Robustness | Reduce risk of failure | |

| Availability | ||

| Minimum charging redundancy | ||

| Tractable and intractable problems | ||

| External conditioners | Emissions (CO2 and noise) | |

| City access | ||

| Fast charging (DC) networks | ||

| Integration with business | Facilities locations | Depot networks, shops, users |

| Fleet sizing and composition | Numbers, types (size) | |

| Inventory management | Items distribution in depots and interactions with item producers | |

| Specific criteria for the last mile distribution network under study | ||

| Start-end points for the routes | Every route starts and finishes in the same location | At least one charger per EV at those points to ensure overnight charging of all EV platforms. |

| Fixed collecting point for each LML route. Single pick-up and multiple delivery with time window (VRPTW) | ||

| Drivers do not bring EV vans home | ||

| Transition structure from ICEV to EV | Coexistence for some time of two type of vehicles | Complete last mile logistic renewal spread over 4 years |

| Scheduling | Not planned in advance | Multi-drop routing optimized but scheduling is order-dependent |

| Charging infrastructure | Fully owned AC 22 kW chargers | Back up provided either by redundancy chargers or by external providers (Vehicles are DC charging compatible). Cost of purchasing and installation not included |

| Driver | Minimizing unproductive hours | Top-ups during vehicle loading or during lunch pause |

| Minimize detour kilometers | ||

| Private charging facilities with uncompromised access | ||

| Training (vehicle, charging, alternative routing) | ||

| Route distance | Compacting | Increase number of routes that can be covered on a single full charge |

| If modular EV batteries adapt capacity for distance | ||

| Leasing | All vehicles leased. No distance reduction due to battery decay included in the routing solutions | |

| Vehicle—route determination | Semi Heterogeneous VRP | Although heterogeneous VRPs require the joint determination of vehicle and routing, in this deployment vehicles were first selected (based on freight volume/weight) and then route was optimized. |

| Country | Number of Vans | Vans per Country | Kilometers per Year | Kilometers per Day | Average km/day/van | Route Frequency (Rotations per Day) | |||

|---|---|---|---|---|---|---|---|---|---|

| Up to L1H1 | Up to L3H3 | Up to L1H1 | Up to L3H3 | Total km/year | |||||

| France | 990 | 700 | 1690 | 39,600,000 | 35,000,000 | 74,600,000 | 239,103 | 141 | 2–4 |

| Germany | 450 | 1500 | 1950 | 18,000,000 | 75,000,000 | 93,000,000 | 298,077 | 153 | 3–6 |

| UK | 1937 | 750 | 2687 | 77,480,000 | 37,500,000 | 114,980,000 | 368,596 | 137 | 8–10 |

| Benelux | 544 | 328 | 872 | 21,760,000 | 16,400,000 | 38,160,000 | 122,308 | 140 | 6–8 |

| Total EU | 3921 | 3278 | 7199 | 156,840,000 | 163,900,000 | 320,740,000 | 1,028,084 | 143 | |

| Country | (a) Diesel Price (€/l) | Liters Vans up to L1H1 (b) | Liters Vans up to L3H3 | Total Liters per Year | Diesel Cost per Year (€) | CO2 Emissions (Tons/Year) (c) | ||||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Low L1H1 | High LH1 | Low L3H3 | High L3H3 | Low Fleet (d) | High Fleet (d) | |||||||||||||||||||||||

| Diesel fleet | France | 1.665 | 2,840,746 | 3,080,986 | 5,921,732 | 9,859,684 | 4514 | 5148 | 6405 | 8785 | 10,919 | 13,933 | ||||||||||||||||

| Germany | 1.593 | 1,291,248 | 6,602,113 | 7,893,361 | 12,574,124 | 2052 | 2340 | 13,725 | 18,825 | 15,777 | 21,165 | |||||||||||||||||

| UK | 1.798 | 5,558,106 | 3,301,056 | 8,859,163 | 15,928,774 | 8833 | 10,072 | 6863 | 9413 | 15,695 | 19,485 | |||||||||||||||||

| Benelux | 1.499 | 1,560,976 | 1,443,662 | 3,004,638 | 4,503,952 | 2481 | 2829 | 3001 | 4116 | 5482 | 6.945 | |||||||||||||||||

| EU | 1.63av | 9,690,100 | 12,984,155 | 22,674,255 | 38,362,582 | 17,880 | 20,389 | 29,994 | 41,139 | 47,874 | 61,528 | |||||||||||||||||

| Country | Grid price €/kWh) (e) | Public AC (€/kWh) (f) | Public DC €/kWh) | Required kWh/y (g) | Cost (€/y) | |||||||||||||||||||||||

| Up to L1H1 | Up to L3H3 | Total | AC 22 kW | 10% public AC 22 kW | 10% DC 50 kW | 100% public AC 22 kW | ||||||||||||||||||||||

| Electric fleet | France | 0.14 | 0.60 | 0.79 | 6,600,000 | 7,777,778 | 14,377,778 | 2,012,889 | 2,674,267 | 2,947,444 | 8,626,667 | |||||||||||||||||

| Germany | 0.20 | 0.60 | 0.75 | 3,000,000 | 16,666,667 | 19,666,667 | 3,933,333 | 4,720,000 | 5,015,000 | 11,800,000 | ||||||||||||||||||

| UK | 0.17 | 0.52 | 0.99 | 12,913,333 | 8,333,333 | 21,246,667 | 3,611,933 | 4,355,567 | 5,354,160 | 11,048,267 | ||||||||||||||||||

| Benelux | 0.18 | 0.67 | 0.83 | 3,626,667 | 3,644,444 | 7,271,111 | 1,308,800 | 1,665,084 | 1,781,422 | 4,871,644 | ||||||||||||||||||

| EU | 0.17av | 0.60 | 0.84 | 26,140,000 | 36,422,222 | 62,562,222 | 10,866,956 | 13,414,918 | 15,098,027 | 36,346,578 | ||||||||||||||||||

| Country | Fuel vs. kWh (€) | eFleet operation cost saving compared to diesel fleet (€/y) | Extra leasing cost for eVans (Clease) (€/y) (h) | Profit pool deducting the additional lease cost (€/y) | ||||||||||||||||||||||||

| Own AC | 10% public AC | 10% public DC | 100% public AC | L1H1 | L3H3 | Fleet extra lease cost | Own AC 22 kW | 10% public AC | 10% public DC | |||||||||||||||||||

| Cost-profit | France | 1.53 | 7,846,795 | 7,185,417 | 6,912,239 | 1,233,017 | 1,425,600 | 1,680,000 | 3,105,600 | 4,741,195 | 4,079,817 | 3,806,639 | ||||||||||||||||

| Germany | 1.39 | 8,640,791 | 7,854,124 | 7,559,124 | 774,123 | 648,000 | 3,600,000 | 4,248,000 | 4,392,791 | 3,606,124 | 3,311,124 | |||||||||||||||||

| UK | 1.63 | 12,316,841 | 11,573,208 | 10,574,614 | 4,880,507 | 2,789,280 | 1,800,000 | 4,589,280 | 7,727,561 | 6,983,928 | 5,985,334 | |||||||||||||||||

| Benelux | 1.32 | 3,195,152 | 2,838,867 | 2,722,530 | (367,692) | 783,360 | 787,200 | 1,570,560 | 1,624,592 | 1,268,307 | 1,151,970 | |||||||||||||||||

| EU | 1.46 | 31,999,578 | 29,451,616 | 27,768,507 | 6,519,956 | 5,646,240 | 7,867,200 | 13,513,440 | 18,486,138 | 15,938,176 | 14,255,067 | |||||||||||||||||

| Fleet and Grid Parameters | |||||||||

|---|---|---|---|---|---|---|---|---|---|

| Number of Vans | Chargers (a) | Vans Recharging Twice Per Day | Charging Events per Day | Charging Events per Year | Average km per kWh (c) | Distance per Van per Year | Fleet Electricity kWh (d) | EU Grid Cost per kWh (5) | (e) AC 22 kW Euro per kWh |

| 1000 | 1200 | 50% | 1500 | 468,000 (b) | 5 | 50,000 km | 10,000,000 | 0.17 € | 0.40 € |

| MSP yearly fee structure in euro | |||||||||

| Fees | Integrated providers (f) | Charger agnostic providers (g) | |||||||

| Vendor 1 | Vendor 2 | Vendor 3 | Vendor 4 | Vendor 5 | Vendor 6 | Vendor 7 | Vendor 8 | Vendor 9 | |

| Yearly subscription | 15,000 € | 50,000 € | 14,500 € | ||||||

| Roaming (h) | 39,500 € | 13,500 € | 7500 € | ||||||

| number of users (i) | 84 € | 90 | 204 | ||||||

| charging sessions | 0.39 € | 0.3 € | 0.25 € | 0.35 € | |||||

| Per kWh | 0.02 € | ||||||||

| Percentage of charged electricity price | 5% | ||||||||

| Per charging outlet | 96 € | 180 € | 108 € | 26.4 € | 102 € | ||||

| Smart meters (j) | 20% socket price | ||||||||

| Percentage on transaction billing (k) | 7% | ||||||||

| 24/7 service desk (l) | 32,000 € | 23.400 € | 19.500 € | ||||||

| Total MSP | 297,720 € | 300,000 € | 355,400 € | 161,600 € | 271,180 € | 350,780 € | 205,300 € | 202,000 € | 204,000 € |

| Fuel cost ICE vans | 6,560,000 €/year. Assuming 8 l/100 km of diesel (average of Table 1) and a European average diesel price of 1.63 €/liter from Table 8. | ||||||||

| Own AC 22kW charging | 4,000,000 €/year (assuming an average of 5 km/kWh at grid price of 0.17 €/kWh, Table 8). No MSP cost included. Savings compared to ICE option: 2,560,000 €/year | ||||||||

| public AC 22 kW charging | 6,000,000 €/year (average of 5 km/kWh and AC 22 kW public charging rate of 0.6 €/kWh, Table 8). No MSP cost included. Savings compared to ICE option: 560,000 €/year | ||||||||

| Sensitivity Analysis Scenarios (Low, Normal, High) and Basic Assumptions | |||||||||

|---|---|---|---|---|---|---|---|---|---|

| Sensitivity Scenario Level | Number of Chargers | kWh Price (€/kWh) | % of Top-up per Day (a) | Total Charging Events (b) | Transport Diesel Price (€/l) | Fixed Costs (€/y) (c) | Specific Notes on Input Variables | ||

| Low scenario (L) | 1000 | 0.20 | 0 | 312,000 | 1.09 | 0 |

| ||

| Normal Scenario (N) | 1200 | 0.40 | 50% | 468,000 | 1.64 | 30,000 | |||

| High Scenario (H) | 1500 | 0.60 | 100% | 624,000 | 2 | 90,000 | |||

| Constants used in sensitivity analysis | |||||||||

| Numbers of vans/users | km per van per year | Km per year (km/y) | Average km per (kWh) | Electricity (kWh/y) | Diesel km/liter (km) | Fleet diesel (liters/y) | Charging on public chargers | Chargers ownership | Chargers used by 3rd parties |

| 1.000 | 50.000 | 50,000,000 | 5 | 10,000,000 | 12.5 | 4,000,000 | Nil | 100% | Nil (d) |

| Sensitivity analysis MSP providers | |||||||||

| Variation in input | Integrated providers cost euro per year | Charger agnostic providers cost euro per year | |||||||

| Vendor 1 | Vendor 2 | Vendor 3 | Vendor 4 | Vendor 5 | Vendor 6 | Vendor 7 | Vendor 8 | Vendor 9 | |

| Number chargers (L) | 278,520 € | 264,000 € | 355,400 € | 140,000 € | 265,900 € | 326,300 € | 205,300 € | 202,000 € | 204,000 € |

| Number chargers (N) | 297,720 € | 300,000 € | 355,400 € | 161,600 € | 271,180 € | 350,780 € | 205,300 € | 202,000 € | 204,000 € |

| Number chargers (H) | 326,520 € | 354,000 € | 355,400 € | 194,000 € | 279,100 € | 387,500 € | 205,300 € | 202,000 € | 204,000 € |

| Delta high-low | 48,000 € | 90,000 € | 0 | 50,000 € | 13,200 € | 61,200 € | 0 | 0 | 0 |

| kWh price (L) | 297,720 € | 300,000 € | 255,400 € | 161,600 € | 271,180 € | 350,780 € | 205,300 € | 146,000 € | 204,000 € |

| kWh price (N) | 297,720 € | 300,000 € | 355,400 € | 161,600 € | 271,180 € | 350,780 € | 205,300 € | 202,000 € | 204,000 € |

| kWh price (H) | 297,720 € | 300,000 € | 455,400 € | 161,600 € | 271,180 € | 350,780 € | 205,300 € | 258,000 € | 204,000 € |

| Delta high-low | 0 | 0 | 200,000 € | 0 | 0 | 0 | 0 | 106,000 € | 0 |

| Charging events (L) | 236,880 € | 300,000 € | 308,600 € | 161,600 € | 271,180 € | 311,780 € | 150,700 € | 202,000 € | 204,000 € |

| Charging events (N) | 297,720 € | 300,000 € | 355,400 € | 161,600 € | 271,180 € | 350,780 € | 205,300 € | 202,000 € | 204,000 € |

| Charging events (H) | 739,200 € | 300,000 € | 402,200 € | 161,600 € | 271,180 € | 389,780 € | 259,900 € | 202,000 € | 204,000 € |

| Delta high-low | 502,320 € | 0 | 93,600 € | 0 | 0 | 78,000 € | 0 | 0 | |

| Fixed costs (L) | 297,720 € | 300,000 € | 355,400 € | 108,000 € | 226,928 € | 302,880 € | 163,800 € | 202,000 € | 204,000 € |

| Fixed costs (N) | 297,720 € | 300,000 € | 355,400 € | 159,600 € | 256,000 € | 332,380 € | 193,800 € | 202,000 € | 204,000 € |

| Fixed costs (H) | 297,720 € | 300,000 € | 355,400 € | 219,600 € | 316,928 € | 392,880 € | 253, 800 € | 202,000 € | 204,000 € |

| Delta high-low | 0 | 0 | 0 | 111,600 € | 90,000 € | 90,000 € | 90,000 € | 0 | 0 |

| Differentiator | B2B Logistic Fleet (a) | 3rd Party Individual Users |

|---|---|---|

| Number of vehicles/users | Fixed (logistic fleet) | Growing |

| Revenue model | Cost savings due to shifting away from ICE vans | Private users charging at a premium rate |

| Routing | Fixed/repetitive (high frequency) | Random (no routing) |

| MSP need to identify available chargers | Low | High |

| 24/7 service desk | Option | Mandatory |

| Fleet | Owned/rented/leased | 3rd parties |

| Charger use policy | Private (proprietary) | Public |

| Charging frequency | Daily | Variable |

| Average distance per vehicle per day | 143 km/day (50,000–60,000 km/y) (b) | 39 km/day (14,300 km/y) (c) |

| Daily top-ups | Probable | Rare |

| EV-battery SoH assessment while charging (d) | Probable | NO |

| Telematic fleet data management | YES | NO |

| Charger/vehicle ratio | 1.2 | <<1 |

| Charger type | AC (11–22 kW) | AC (22 kW) DC (up to 350 kW) |

| kWh price paid by user | Grid price | Grid price + premium |

| Charger availability uncertainty | Low | Medium |

| Charging criticality | High | Medium |

| Charger usage | Low | Medium–High |

| Who pays for kWh? | Logistic operator | 3rd party customers |

| Compatibility with other B2B logistic operators’ fleet | Probable (in different time windows) | Difficult |

| Compatibility with other B2C customers | Difficult | Standard business model |

| Chargers locations | Industrial and commercial urban areas | High density urban areas (downtown, malls, offices, stadiums, highways) |

| Payback period | Short | Longer (mostly for DC chargers) |

| Limitations imposed by the grid capacity | Some | Large (mostly for DC chargers) |

| Average vehicle retention | Shorter than OEM warranty (e) | Around OEM warranty |

| CPO | Logistic operators and associates | Diverse |

| Charging at other CPO networks | Rare/minimum (f) | Common |

| Charging internationally | Very rare | Possible |

| Country | Total Number of Chargers (a) | Operational Margin per Year (€/Year) (b) | Shortest Payback Period (Years) (c) | Longest Payback Period (Years) (d) |

|---|---|---|---|---|

| France | 2.028 | 4,741,195 | 1.67 | 3.42 |

| Germany (e) | 2.340 | 4,392,791 | 2.08 | 4.26 |

| UK | 3.224 | 7,727,561 | 1.63 | 3.34 |

| Benelux | 1.046 | 1,624,592 | 2.51 | 5.15 |

| Total EU | 8.638 | 18,486,138 | 1.82 | 3.74 |

| MSP Yearly Fee to be Compensated by Letting a 3rd Party Use the Charging Network at Market Price | |||||||||

|---|---|---|---|---|---|---|---|---|---|

| Vendor 1 | Vendor 2 | Vendor 3 | Vendor 4 | Vendor 5 | Vendor 6 | Vendor 7 | Vendor 8 | Vendor 9 | |

| Cost per year (a) | 297,720 € | 300,000 € | 355,400 € | 161,000 € | 271,180 € | 350,780 € | 205,300 € | 202,000 € | 204,000 € |

| kWh (b) | 1,353,273 | 1,363,636 | 1,615,455 | 731,818 | 1,232,636 | 1,594,455 | 933,182 | 918,181 | 927,273 |

| km per year (c) | 6,766,365 | 6,818,180 | 8,077,275 | 3,659,090 | 6,163,180 | 7,972,275 | 4,665,910 | 4,590,905 | 4,861,365 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Sanz, A.; Meyer, P. Electrifying the Last-Mile Logistics (LML) in Intensive B2B Operations—An European Perspective on Integrating Innovative Platforms. Logistics 2024, 8, 45. https://doi.org/10.3390/logistics8020045

Sanz A, Meyer P. Electrifying the Last-Mile Logistics (LML) in Intensive B2B Operations—An European Perspective on Integrating Innovative Platforms. Logistics. 2024; 8(2):45. https://doi.org/10.3390/logistics8020045

Chicago/Turabian StyleSanz, Alejandro, and Peter Meyer. 2024. "Electrifying the Last-Mile Logistics (LML) in Intensive B2B Operations—An European Perspective on Integrating Innovative Platforms" Logistics 8, no. 2: 45. https://doi.org/10.3390/logistics8020045

APA StyleSanz, A., & Meyer, P. (2024). Electrifying the Last-Mile Logistics (LML) in Intensive B2B Operations—An European Perspective on Integrating Innovative Platforms. Logistics, 8(2), 45. https://doi.org/10.3390/logistics8020045