Real Estate Valuations with Small Dataset: A Novel Method Based on the Maximum Entropy Principle and Lagrange Multipliers

Abstract

:1. Introduction

2. Literature Review

3. Methodology

- market analysis for the identification of recent sales of similar properties;

- verification of information, considering whether the observed prices adhere to the definition of the market value estimation criterion, and whether the transactions belong to the specific market segment to which the property being appraised belongs;

- selection of elements of comparison (property features);

- definition of the objective function based on Shannon’s Entropy, capable of incorporating the sum of products between the optimal weights of property features and the corresponding prices from the estimated sample data;

- setting variability and normalization constraints, as well as moments of consistency for real estate variables;

- definition of the Lagrangian function that includes the specified constraints, followed by the redefinition of the objective function that returns the sum of the Lagrangians;

- processing the solution and optimal value of the objective function, with the definition of weights for each optimal solution.

4. Empirical Demonstration: Materials and Results

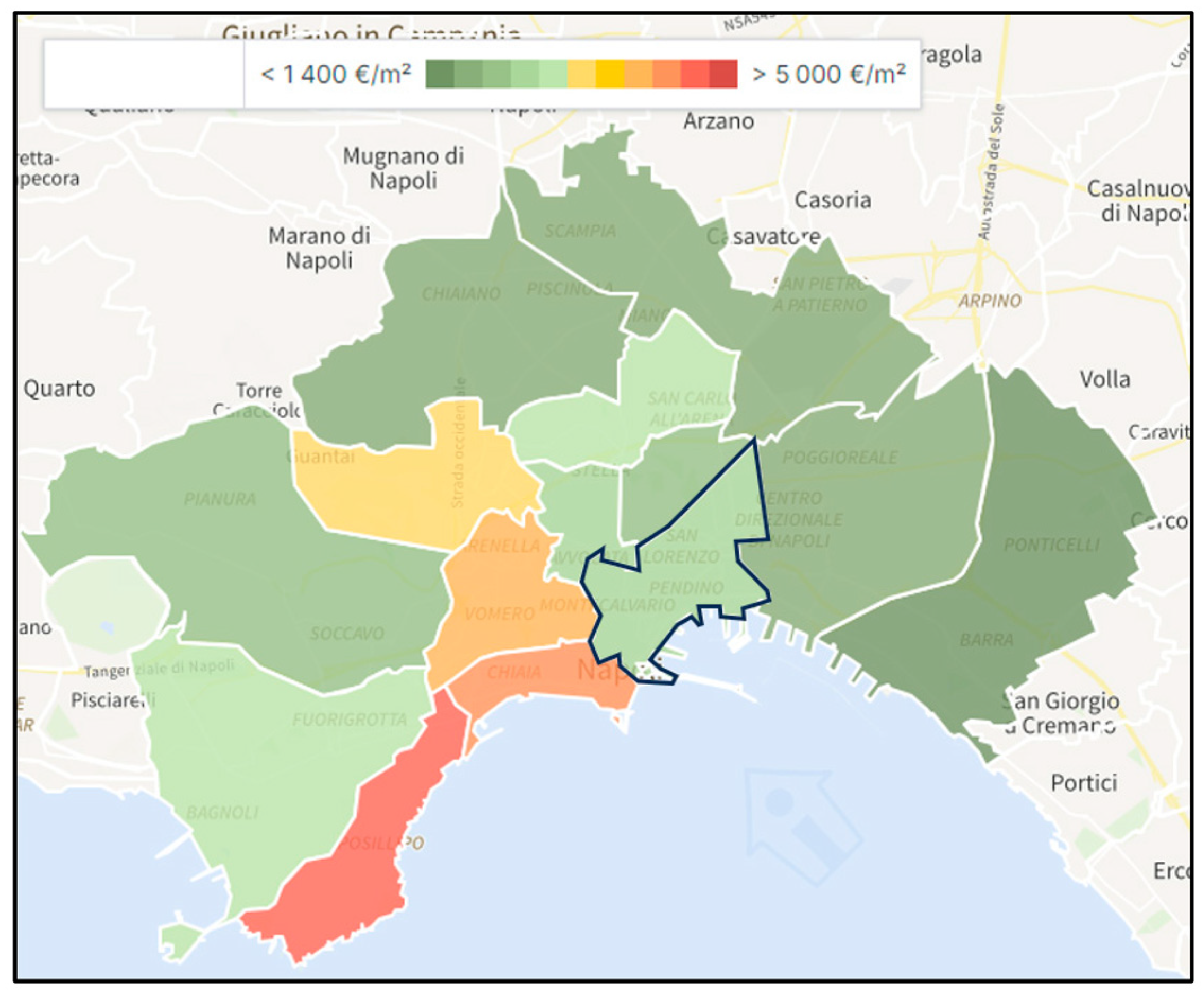

4.1. Context of the Dataset

4.2. Data Specification

- real estate sale price expressed in euro (PRICE);

- commercial area of housing unit expressed in square meters, i.e., the sum of the internal area plus eventual other secondary areas virtualized through specific coefficients used in the respective real estate market (SUR);

- number of floor levels of housing units (LEV);

- maintenance status (MAIN) expressed with a score scale: two if the housing unit is in optimal condition, one if maintenance status is good, and zero otherwise (mediocre status);

- number of rooms constituting the housing unit (ROOMS);

- number of bathrooms in the housing unit (BATH).

4.3. Results

5. Discussion

6. Conclusions

Funding

Data Availability Statement

Conflicts of Interest

References

- Del Giudice, V.; Manganelli, B.; De Paola, P. Hedonic Analysis of Housing Sales Prices with Semiparametric Methods. Int. J. Agric. Environ. Inf. Syst. 2017, 8, 65–77. [Google Scholar] [CrossRef]

- De Paola, P.; Previtera, S.; Manganelli, B.; Forte, F.; Del Giudice, F.P. Interpreting Housing Prices with a MultidisciplinaryApproach Based on Nature-Inspired Algorithms and Quantum Computing. Buildings 2023, 13, 1603. [Google Scholar] [CrossRef]

- Shannon, C.E. A Mathematical Theory of Communication. Bell Syst. Techn. J. 1948, 27, 379–423. [Google Scholar] [CrossRef]

- Jaynes, E.T. Information Theory and Statistical Mechanics. Phys. Rev. Ser. 1957, 106, 620. [Google Scholar] [CrossRef]

- Jaynes, E.T. Where do we stand on maximum entropy? In The Maximum Entropy Formalism; Levine, R.D., Tribus, M., Eds.; MIT Press: Cambridge, MA, USA, 1978; pp. 15–118. [Google Scholar]

- Jaynes, E.T. On the rationale of maximum-entropy methods. Proc. IEEE 1982, 70, 939–952. [Google Scholar] [CrossRef]

- Smith, H.C.; Belloit, J.D. Real Estate Appraisal; Century VII Publishing Company: Los Angeles, CA, USA, 1987; ISBN 9780939787012. [Google Scholar]

- Clausius, R. Abhandlungen uber die Mechanische Warmetheorie; F. Vieweg und Sohn: Braunschweig, Germany, 1864. [Google Scholar]

- Gibbs, J.W. On the equilibrium of heterogeneous substances. Trans. Conn. Acad. Arts Sci. 1879, 3, 108–248. [Google Scholar] [CrossRef]

- Boltzmann, L. Über die Beziehung zwischen dem zweiten Hauptsatze der mechanischen Wärmetheorie und der Wahrscheinlichkeitsrechnung respektive den Sätzen über das Wärmegleichgewicht. Wien. Ber. 1877, 76, 373–435. [Google Scholar]

- Özdilek, Ü. The Role of Thermodynamic and Informational Entropy in Improving Real Estate Valuation Methods. Entropy 2023, 25, 907. [Google Scholar] [CrossRef]

- Golan, A. Information and entropy econometrics: A review and synthesis. Found. Trends Econ. 2006, 2, 1–145. [Google Scholar] [CrossRef]

- Bretó, C.; Espinosa, P.; Hernández, P.; Pavía, J.M. An Entropy-Based Machine Learning Algorithm for Combining Macroeconomic Forecasts. Entropy 2009, 21, 1015. [Google Scholar] [CrossRef]

- Dyer, J.A.; Sarin, R.K. Measurable multi-attribute value functions. Oper. Res. 1979, 27, 810–822. [Google Scholar] [CrossRef]

- Zanakis, S.H.; Solomon, A.; Wishart, N.; Dublish, S. Multi-attribute decision making: A simulation comparison of select methods. Eur. J. Oper. Res. 1998, 107, 507–529. [Google Scholar] [CrossRef]

- Grossman, S.; Stiglitz, J. On the impossibility of informationally efficient markets. Am. Econ. Rev. 1980, 70, 393–408. [Google Scholar]

- Fama, E.F. The Behavior of Stock-Market Prices. J. Bus. 1965, 38, 34–105. [Google Scholar] [CrossRef]

- Ivkovic, Z.; Weisbenner, S. Local does as local is: Information content of the geography of individual investors’ common stock investments. J. Financ. 2005, 60, 267–306. [Google Scholar] [CrossRef]

- Molgedey, L.; Ebeling, W. Local order, entropy and predictability of financial time series. Eur. Phys. J. B 2000, 107, 733–737. [Google Scholar] [CrossRef]

- Bentes, S.; Menezes, R.; Mendes, D.A. Long memory and volatility clustering: Is the empirical evidence consistent across stock markets? Phys. A 2008, 387, 3826–3830. [Google Scholar] [CrossRef]

- Zhou, R.; Cai, R.; Tong, G. Applications of Entropy in Finance: A Review. Entropy 2013, 15, 4909–4931. [Google Scholar] [CrossRef]

- Schrödinger, E. What Is Life? And Mind and Matter; Cambridge University Press: Cambridge, UK, 1967. [Google Scholar]

- Jeffery, K.; Pollack, R.; Rovelli, C. On the Statistical Mechanics of Life: Schrödinger Revisited. Entropy 2019, 21, 1211. [Google Scholar] [CrossRef]

- Applebaum, D. Probability and Information, an Integrated Approach; Cambridge University Press: Cambridge, UK, 1996. [Google Scholar]

- Georgescu-Roegen, N. The Entropy Law and the Economic Process; Harvard University Press: Cambridge, MA, USA, 1971. [Google Scholar]

- Brown, R.J. Entropy–what kind of bet is real estate–really? J. Prop. Invest. Financ. 2017, 35, 341–351. [Google Scholar] [CrossRef]

- Chen, Y.; Cai, Y.; Zheng, C. Efficiency of Chinese Real Estate Market Based on Complexity-Entropy Binary Causal Plane Method. Complexity 2020, 2020, 2791352. [Google Scholar] [CrossRef]

- Lam, K.C.; Yu, C.Y.; Lam, K.Y. An Artificial Neural Network and Entropy Model for Residential Property Price Forecasting in Hong Kong. J. Prop. Res. 2008, 25, 321–342. [Google Scholar] [CrossRef]

- Ge, X.J.; Du, Y. Main variables influencing residential property values using the entropy method–The case of Auckland. In Proceedings of the 5th International Structural Engineering and Construction Conference; Springer Nature; Berlin/Heidelberg, Germany, 2007. [Google Scholar]

- Lam, K.C.; Yu, C.Y.; Lam, K.Y. Support vector machine and entropy based decision support system for property valuation. J. Prop. Res. 2009, 26, 213–233. [Google Scholar] [CrossRef]

- Zhou, S.; Wang, F.; Zhang, Z. Evaluation of Real Estate Venture Capital Based on Entropy Double Base Points Method. In Proceedings of the 2009 International Conference on Electronic Commerce and Business Intelligence, Beijing, China, 6–7 June 2009. [Google Scholar]

- Salois, M.J.; Moss, C.B. An Information Approach to the Dynamics in Farm Income: Implications for Farmland Markets. Entropy 2011, 13, 38–52. [Google Scholar] [CrossRef]

- Gnat, S. Measurement of entropy in the assessment of homogeneity of areas valued with the Szczecin Algorithm of Real Estate Mass Appraisal. J. Econ. Manag. 2019, 38, 89–106. [Google Scholar] [CrossRef]

- Kostic, Z.; Jevremovic, A. What Image Features Boost Housing Market Predictions? IEEE Trans. Multimed. 2020, 22, 1904–1916. [Google Scholar] [CrossRef]

- Basse, T.; Desmyter, S.; Saft, D.; Wegener, C. Leading indicators for the US housing market: New empirical evidence and thoughts about implications for risk managers and ESG investors. Int. Rev. Financ. Anal. 2023, 89, 102765. [Google Scholar] [CrossRef]

- The MathWorks Inc. MATLAB Version: 9.0.0 (R2016a); The MathWorks Inc.: Natick, MA, USA, 2023; Available online: https://www.mathworks.com (accessed on 20 December 2023).

- Zhao, Q.; Kurata, H. Use of maximum entropy principle with Lagrange multipliers extends the feasibility of elementary mode analysis. J. Biosci. Bioeng. 2010, 110, 254–261. [Google Scholar] [CrossRef]

- ISTAT. Monthly Demographic Balance for the Year 2023. Available online: https://www.istat.it (accessed on 4 October 2023).

- Municipality of Naples. Available online: https://www.comune.napoli.it (accessed on 20 December 2023).

- Immobiliare.it. Available online: https://www.immobiliare.it (accessed on 20 December 2023).

- Simonotti, M.; Salvo, F.; Ciuna, M.; De Ruggiero, M. Measurements of Rationality for a Scientific Approach to the Market-Oriented Methods. J. Real Estate Lit. 2016, 24, 403–427. [Google Scholar] [CrossRef]

- Del Giudice, V.; Salvo, F.; De Paola, P. Resampling Techniques for Real Estate Appraisals: Testing the Bootstrap Approach. Sustainability 2018, 10, 3085. [Google Scholar] [CrossRef]

- Bambagioni, G. Codice delle Valutazioni Immobiliari-Italian Property Valuation Standard 2018; Tecnoborsa: Rome, Italy, 2018; ISBN 978-88-943158-0-6. [Google Scholar]

{kind=link}

| Comparable | ROOMS | BATH | SUR | LEV | MAIN | PRICE |

|---|---|---|---|---|---|---|

| No. 1 | 4 | 1 | 130 | 3 | 2 | 490,000 |

| No. 2 | 5 | 3 | 130 | 2 | 2 | 530,000 |

| No. 3 | 5 | 2 | 125 | 1 | 1 | 595,000 |

| No. 4 | 4 | 2 | 122 | 4 | 2 | 530,000 |

| No. 5 | 5 | 1 | 150 | 2 | 1 | 560,000 |

| No. 6 | 3 | 3 | 160 | 2 | 1 | 635,000 |

| No. 7 | 4 | 2 | 110 | 3 | 1 | 530,000 |

| No. 8 | 4 | 2 | 120 | 4 | 1 | 520,000 |

| Index | ROOMS | BATH | SUR | LEV | MAIN | PRICE |

|---|---|---|---|---|---|---|

| Mean | 4.25 | 2.00 | 130.88 | 2.63 | 1.38 | 548,750.00 |

| Std. Error | 0.25 | 0.27 | 5.80 | 0.38 | 0.18 | 16,386.79 |

| Median | 4.00 | 2.00 | 127.50 | 2.50 | 1.00 | 530,000.00 |

| Std. Deviation | 0.71 | 0.76 | 16.40 | 1.06 | 0.52 | 46,348.83 |

| Kurtosis | −0.23 | −0.70 | 0.14 | −0.94 | −2.24 | 0.52 |

| Asimmetry | −0.40 | 0.00 | 0.88 | 0.04 | 0.64 | 0.95 |

| Minimum | 3.00 | 1.00 | 110.00 | 1.00 | 1.00 | 490,000.00 |

| Maximum | 5.00 | 3.00 | 160.00 | 4.00 | 2.00 | 635,000.00 |

| Confidence Level (95.0%) | 0.59 | 0.63 | 13.71 | 0.89 | 0.43 | 38,748.59 |

| Comparable | Optimal Weights (wi) | Optimal Solution (Oi) | Comparable Sale Price (Pi) | Contribution to the Estimated Value (Oi∙Pi) | ||||

|---|---|---|---|---|---|---|---|---|

| ROOMS | BATH | SUR | LEV | MAIN | ||||

| 8 | 0.0067 | 0.0235 | 0.0000 | 0.0078 | 0.0229 | 0.0610 | €520,000.00 | €31,720.00 |

| 2 | 0.0235 | 0.0826 | 0.0000 | 0.0275 | 0.0806 | 0.2143 | €530,000.00 | €113,579.00 |

| 3 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | €595,000.00 | €0.00 |

| 4 | 0.0078 | 0.0275 | 0.0000 | 0.0092 | 0.0269 | 0.0714 | €530,000.00 | €37,842.00 |

| 5 | 0.0229 | 0.0806 | 0.0000 | 0.0269 | 0.0787 | 0.2091 | €560,000.00 | €117,096.00 |

| 6 | 0.0151 | 0.0531 | 0.0000 | 0.0177 | 0.0518 | 0.1377 | €635,000.00 | €87,439.50 |

| 7 | 0.0336 | 0.1182 | 0.0000 | 0.0394 | 0.1153 | 0.3065 | €530,000.00 | €162,445.00 |

| Estimated Value for Comparable no. 1 (Sum of contributions Oi∙Pi) | €550,121.50 | |||||||

| Optimal Value of objective function | −2.75 × 106 | |||||||

| Comparable | Optimal Weights (wi) | Optimal Solution (Oi) | Comparable Sale Price (Pi) | Contribution to the Estimated Value (Oi∙Pi) | ||||

|---|---|---|---|---|---|---|---|---|

| ROOMS | BATH | SUR | LEV | MAIN | ||||

| 1 | 0.0555 | 0.0737 | 0.0555 | 0.0171 | 0.0166 | 0.2184 | €490,000.00 | €107,016.00 |

| 8 | 0.0737 | 0.0978 | 0.0737 | 0.0227 | 0.0220 | 0.2898 | €520,000.00 | €150,696.00 |

| 3 | 0.0555 | 0.0737 | 0.0555 | 0.0171 | 0.0166 | 0.2184 | €595,000.00 | €129,948.00 |

| 4 | 0.0171 | 0.0227 | 0.0171 | 0.0053 | 0.0051 | 0.0673 | €530,000.00 | €35,669.00 |

| 5 | 0.0166 | 0.0220 | 0.0166 | 0.0051 | 0.0049 | 0.0652 | €560,000.00 | €36,512.00 |

| 6 | 0.0358 | 0.0475 | 0.0358 | 0.0110 | 0.0107 | 0.1408 | €635,000.00 | €89,408.00 |

| 7 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | €530,000.00 | €0.00 |

| Estimated Value for Comparable no. 2 (Sum of contributions Oi∙Pi) | €549,249.00 | |||||||

| Optimal Value of objective function | −2.75 × 106 | |||||||

| Comparable | Optimal Weights (wi) | Optimal Solution (Oi) | Comparable Sale Price (Pi) | Contribution to the Estimated Value (Oi∙Pi) | ||||

|---|---|---|---|---|---|---|---|---|

| ROOMS | BATH | SUR | LEV | MAIN | ||||

| 1 | 0.0716 | 0.0573 | 0.0823 | 0.0000 | 0.0268 | 0.2381 | €490,000.00 | €116,669.00 |

| 2 | 0.0573 | 0.0459 | 0.0659 | 0.0000 | 0.0215 | 0.1905 | €530,000.00 | €100,965.00 |

| 8 | 0.0823 | 0.0659 | 0.0946 | 0.0000 | 0.0308 | 0.2736 | €520,000.00 | €142,272.00 |

| 4 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | €530,000.00 | €0.00 |

| 5 | 0.0268 | 0.0215 | 0.0308 | 0.0000 | 0.0101 | 0.0892 | €560,000.00 | €49,952.00 |

| 6 | 0.0412 | 0.0329 | 0.0473 | 0.0000 | 0.0154 | 0.1368 | €635,000.00 | €86,868.00 |

| 7 | 0.0216 | 0.0173 | 0.0249 | 0.0000 | 0.0081 | 0.0719 | €530,000.00 | €38,107.00 |

| Estimated Value for Comparable no. 3 (Sum of contributions Oi∙Pi) | €534,833.00 | |||||||

| Optimal Value of objective function | −2.67 × 106 | |||||||

| Comparable | Optimal Weights (wi) | Optimal Solution (Oi) | Comparable Sale Price (Pi) | Contribution to the Estimated Value (Oi∙Pi) | ||||

|---|---|---|---|---|---|---|---|---|

| ROOMS | BATH | SUR | LEV | MAIN | ||||

| 1 | 0.0178 | 0.0349 | 0.0008 | 0.0000 | 0.0431 | 0.0966 | €490,000.00 | €47,334.00 |

| 2 | 0.0349 | 0.0684 | 0.0015 | 0.0000 | 0.0843 | 0.1891 | €530,000.00 | €100,223.00 |

| 3 | 0.0008 | 0.0015 | 0.0000 | 0.0000 | 0.0019 | 0.0042 | €595,000.00 | €2499.00 |

| 8 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | €520,000.00 | €0.00 |

| 5 | 0.0431 | 0.0843 | 0.0019 | 0.0000 | 0.1040 | 0.2332 | €560,000.00 | €130,592.00 |

| 6 | 0.0260 | 0.0509 | 0.0011 | 0.0000 | 0.0628 | 0.1408 | €635,000.00 | €89,408.00 |

| 7 | 0.0621 | 0.1215 | 0.0027 | 0.0000 | 0.1498 | 0.3361 | €530,000.00 | €178,133.00 |

| Estimated Value for Comparable no. 4 (Sum of contributions Oi∙Pi) | €548,189.00 | |||||||

| Optimal Value of objective function | −2.74 × 106 | |||||||

| Comparable | Optimal Weights (wi) | Optimal Solution (Oi) | Comparable Sale Price (Pi) | Contribution to the Estimated Value (Oi∙Pi) | ||||

|---|---|---|---|---|---|---|---|---|

| ROOMS | BATH | SUR | LEV | MAIN | ||||

| 1 | 0.0654 | 0.0677 | 0.0188 | 0.0000 | 0.0586 | 0.2106 | €490,000.00 | €103,194.00 |

| 2 | 0.0677 | 0.0701 | 0.0195 | 0.0000 | 0.0607 | 0.2179 | €530,000.00 | €115,487.00 |

| 3 | 0.0188 | 0.0195 | 0.0054 | 0.0000 | 0.0168 | 0.0605 | €595,000.00 | €35,997.50 |

| 4 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | €530,000.00 | €0.00 |

| 8 | 0.0586 | 0.0607 | 0.0168 | 0.0000 | 0.0525 | 0.1887 | €520,000.00 | €98,124.00 |

| 6 | 0.0421 | 0.0436 | 0.0121 | 0.0000 | 0.0377 | 0.1355 | €635,000.00 | €86,042.50 |

| 7 | 0.0580 | 0.0600 | 0.0167 | 0.0000 | 0.0520 | 0.1867 | €530,000.00 | €98,951.00 |

| Estimated Value for Comparable no. 5 (Sum of contributions Oi∙Pi) | €537,796.00 | |||||||

| Optimal Value of objective function | −2.69 × 106 | |||||||

| Comparable | Optimal Weights (wi) | Optimal Solution (Oi) | Comparable Sale Price (Pi) | Contribution to the Estimated Value (Oi∙Pi) | ||||

|---|---|---|---|---|---|---|---|---|

| ROOMS | BATH | SUR | LEV | MAIN | ||||

| 1 | 0.0099 | 0.0198 | 0.0045 | 0.0216 | 0.0270 | 0.0827 | €490,000.00 | €40,523.00 |

| 2 | 0.0198 | 0.0396 | 0.0090 | 0.0431 | 0.0539 | 0.1654 | €530,000.00 | €87,662.00 |

| 3 | 0.0045 | 0.0090 | 0.0020 | 0.0098 | 0.0123 | 0.0376 | €595,000.00 | €22,372.00 |

| 4 | 0.0216 | 0.0431 | 0.0098 | 0.0470 | 0.0588 | 0.1804 | €530,000.00 | €95,612.00 |

| 5 | 0.0270 | 0.0539 | 0.0123 | 0.0588 | 0.0736 | 0.2256 | €560,000.00 | €126,336.00 |

| 8 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | €520,000.00 | €0.00 |

| 7 | 0.0369 | 0.0737 | 0.0168 | 0.0804 | 0.1006 | 0.3083 | €530,000.00 | €163,399.00 |

| Estimated Value for Comparable no. 6 (Sum of contributions Oi∙Pi) | €535,904.00 | |||||||

| Optimal Value of objective function | −2.68 × 106 | |||||||

| Comparable | Optimal Weights (wi) | Optimal Solution (Oi) | Comparable Sale Price (Pi) | Contribution to the Estimated Value (Oi∙Pi) | ||||

|---|---|---|---|---|---|---|---|---|

| ROOMS | BATH | SUR | LEV | MAIN | ||||

| 1 | 0.0760 | 0.0714 | 0.0316 | 0.0000 | 0.0421 | 0.2211 | €490,000.00 | €108,339.00 |

| 2 | 0.0714 | 0.0670 | 0.0297 | 0.0000 | 0.0395 | 0.2075 | €530,000.00 | €109,975.00 |

| 3 | 0.0316 | 0.0297 | 0.0131 | 0.0000 | 0.0175 | 0.0919 | €595,000.00 | €54,680.50 |

| 4 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | €530,000.00 | €0.00 |

| 5 | 0.0421 | 0.0395 | 0.0175 | 0.0000 | 0.0233 | 0.1224 | €560,000.00 | €68,544.00 |

| 6 | 0.0468 | 0.0439 | 0.0194 | 0.0000 | 0.0259 | 0.1360 | €635,000.00 | €86,360.00 |

| 8 | 0.0760 | 0.0714 | 0.0316 | 0.0000 | 0.0421 | 0.2211 | €520,000.00 | €114,972.00 |

| Estimated Value for Comparable no. 7 (Sum of contributions Oi∙Pi) | €542,870.50 | |||||||

| Optimal Value of objective function | −2.71 × 106 | |||||||

| Comparable | Optimal Weights (wi) | Optimal Solution (Oi) | Comparable Sale Price (Pi) | Contribution to the Estimated Value (Oi∙Pi) | ||||

|---|---|---|---|---|---|---|---|---|

| ROOMS | BATH | SUR | LEV | MAIN | ||||

| 1 | 0.0622 | 0.0739 | 0.0051 | 0.0000 | 0.0546 | 0.1958 | €490,000.00 | €95,942.00 |

| 2 | 0.0739 | 0.0879 | 0.0060 | 0.0000 | 0.0649 | 0.2328 | €530,000.00 | €123,384.00 |

| 3 | 0.0051 | 0.0060 | 0.0004 | 0.0000 | 0.0045 | 0.0160 | €595,000.00 | €9520.00 |

| 4 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | €530,000.00 | €0.00 |

| 5 | 0.0546 | 0.0649 | 0.0045 | 0.0000 | 0.0479 | 0.1718 | €560,000.00 | €96,208.00 |

| 6 | 0.0429 | 0.0509 | 0.0035 | 0.0000 | 0.0376 | 0.1349 | €635,000.00 | €85,661.50 |

| 7 | 0.0790 | 0.0939 | 0.0065 | 0.0000 | 0.0693 | 0.2487 | €530,000.00 | €131,811.00 |

| Estimated Value for Comparable no. 8 (Sum of contributions Oi∙Pi) | €542,526.50 | |||||||

| Optimal Value of objective function | −2.71 × 106 | |||||||

| Comparable | σ = €5000 | σ = €10,000 | σ = €20,000 | |||

|---|---|---|---|---|---|---|

| Estimated Value | % Error | Estimated Value | % Error | Estimated Value | % Error | |

| 1 | €557,444.00 | 13.76% | €557,859.00 | 13.85% | €558,570.00 | 13.99% |

| 2 | €551,786.00 | 4.11% | €552,190.00 | 4.19% | €552,852.50 | 4.31% |

| 3 | €542,508.00 | −8.82% | €542,801.00 | −8.77% | €543,568.00 | −8.64% |

| 4 | €551,787.00 | 4.11% | €552,144.50 | 4.18% | €552,860.50 | 4.31% |

| 5 | €547,492.50 | −2.23% | €547,805.00 | −2.18% | €548,520.50 | −2.05% |

| 6 | €536,946.50 | −15.44% | €661,361.50 | 4.15% | €806,879.50 | 27.07% |

| 7 | €551,781.50 | 4.11% | €552,141.50 | 4.18% | €552,913.00 | 4.32% |

| 8 | €553,210.50 | 6.39% | €553,517.00 | 6.45% | €554,237.00 | 6.58% |

| Comparable | Sale Price | Maximum Entropy Basic Model | Best Fit (Basic/σ Upper Limit) | ||

|---|---|---|---|---|---|

| % Error | Estimated Value | % Error | Estimated Value | ||

| 1 | €490,000 | 12.27% | €550,121.50 | 12.27% | €550,121.50 |

| 2 | €530,000 | 3.63% | €549,249.00 | 3.63% | €549,249.00 |

| 3 | €595,000 | −10.11% | €534,833.00 | −8.64% | €543,568.00 |

| 4 | €530,000 | 3.43% | €548,189.00 | 3.43% | €548,189.00 |

| 5 | €560,000 | 3.43% | €537,796.00 | −2.05% | €548,520.50 |

| 6 | €635,000 | −15.61% | €535,904.00 | 4.15% | €661,361.50 |

| 7 | €530,000 | 2.43% | €542,870.50 | 2.43% | €542,870.50 |

| 8 | €520,000 | 4.33% | €542,526.50 | 4.33% | €542,526.50 |

| Mean absolute % error | 6.91% | Mean absolute % error | 5.12% | ||

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

De Paola, P. Real Estate Valuations with Small Dataset: A Novel Method Based on the Maximum Entropy Principle and Lagrange Multipliers. Real Estate 2024, 1, 26-40. https://doi.org/10.3390/realestate1010003

De Paola P. Real Estate Valuations with Small Dataset: A Novel Method Based on the Maximum Entropy Principle and Lagrange Multipliers. Real Estate. 2024; 1(1):26-40. https://doi.org/10.3390/realestate1010003

Chicago/Turabian StyleDe Paola, Pierfrancesco. 2024. "Real Estate Valuations with Small Dataset: A Novel Method Based on the Maximum Entropy Principle and Lagrange Multipliers" Real Estate 1, no. 1: 26-40. https://doi.org/10.3390/realestate1010003

APA StyleDe Paola, P. (2024). Real Estate Valuations with Small Dataset: A Novel Method Based on the Maximum Entropy Principle and Lagrange Multipliers. Real Estate, 1(1), 26-40. https://doi.org/10.3390/realestate1010003