1. Introduction

Extensive research has delved into the consequences of oil price shocks on a nation’s economy. This includes analyzing the impact of oil price shocks on economic growth, as evidenced in works by Hamilton [

1], Mork et al. [

2], and Baek and Young [

3]. Similarly, scholars have probed the correlation between oil shocks and inflation, as highlighted by the studies conducted by Darby [

4], Hooker [

5], and Salisu et al. [

6]. Additionally, there has been scrutiny of the consequences of oil shocks on exchange rates, as exemplified in research by Krugman [

7], Amano and Van Norden [

8], and Baek and Kim [

9]. Furthermore, investigations have explored how oil price shocks impact external balances, as demonstrated in the scholarly contributions of Svensson [

10], Backus and Crucinic [

11], and Baek and Kwon [

12].

However, conventional empirical research in this area faces certain limitations. One limitation is related to the persistent treatment of crude oil prices as exogenously determined with respect to the global economy, even though it is clear that global macroeconomic fluctuations have a significant impact on them. Another limitation arises from the assumption that the consequences of an exogenous shift in oil prices remain constant, regardless of the specific demand or supply shocks in the global oil market responsible for triggering such changes. This assumption lacks credibility due to the historical reality that oil price shocks have historically stemmed from various combinations of oil demand and supply shocks, resulting in distinct effects during different time periods.

In the scope of this research, we aim to directly address these concerns and conduct a rigorous empirical analysis of the impact of oil demand and supply shocks on the Alaskan economy, with particular emphasis on scrutinizing their influence on the production of crude oil within the state. At the outset, it is important to mention that Kilian’s groundbreaking 2009 [

13] research has unveiled that shifts in historical oil prices have primarily been shaped by a combination of oil supply shocks and two types of demand-side shocks, namely global demand shocks and oil-specific demand shocks. Consequently, subsequent studies have taken Kilian’s pioneering work as a starting point and have gone on to explore these dynamics more deeply by employing different data sources and various estimation techniques. Notable researchers contributing to this area of study include Hu et al. [

14], Guerrero-Escobar et al. [

15], and Baek [

16,

17], among others. Our current research is a part of this emerging literature.

The Alaskan economy is heavily reliant on crude oil production, and the oil industry stands as its primary source of funding for the state’s budget. This sector alone contributes almost 90 percent of the state’s unrestricted general fund, resulting in a total state revenue of more than USD 180 billion since Alaska became a state. These oil revenues also empower Alaska’s residents to generate the highest per capita state spending in the United States, and the state imposes neither personal income nor sales taxes as a result. Additionally, the Alaska Permanent Fund (APF), a diversified investment fund, was created by the state government in the wake of the construction of the Trans-Alaska Pipeline System (TAPS) in 1976. The majority of the returns generated from the APF are distributed directly to Alaska’s residents as Permanent Fund Dividends (PFD). Since the inaugural distribution in 1982, the annual PFD amounts have fluctuated, with payments ranging from approximately USD 500 to USD 3000. This distribution has totaled over USD 25 billion disbursed to residents over the years. Moreover, while direct employment in the oil industry comprised less than 10% of the total workforce in Alaska (for instance, around 15,800 jobs in 2020), each job in the oil sector leads to the creation of numerous positions in support industries and beyond. Notably, according to the Alaska Oil and Gas Association (2020), it is estimated that as many as half of all jobs in Alaska are intertwined with the existence of in-state oil operations. Considering the significant role that oil production plays in Alaska’s economic landscape, it becomes important from both a policy and empirical perspective to examine how oil price shocks have affected the state’s oil production. Alaska serves as a noteworthy case study, and the primary findings we uncover hold relevance for other developed nations engaged in oil production.

To thoroughly investigate our research objective, we have developed a threefold approach to empirical analysis. Initially, we utilize a structural vector autoregression (VAR) technique to disentangle crude oil price fluctuations into shocks arising from supply-related and demand-driven factors. Next, we apply the autoregressive distributed lag (ARDL) method, as outlined by Pesaran et al. [

18], to reveal both the short-term and long-term effects of distinct components of oil shocks on oil production within the context of Alaska. Lastly, we employ the nonlinear autoregressive distributed lag (NARDL) approach, introduced by Shin et al. [

19], to identify any asymmetrical responses resulting from positive and negative shocks stemming from various aspects of oil shocks.

To date, several research studies have examined the impacts of oil price shocks on Alaska’s economy. Prominent examples of such investigations encompass the study conducted by Tappen and Baek [

20], which delved into the influence of oil prices on oil production, as well as the research by Bocklet and Baek [

21], which focused on the relationship between oil prices and unemployment. Additionally, Kaczmarski and Baek [

22] undertook research concerning the effects of oil prices on oil revenues in Alaska. Nevertheless, these studies have generally overlooked the potential consequences of different types of oil price shocks in their analyses of this subject. It is worth noting that Sadik-Zada et al. [

23] explored production linkages and fiscal employment effects within the extractive industries in Azerbaijan, while Sadik-Zada [

24] focused on the growth and employment impacts of these industries in Kazakhstan. Given that both of these studies investigate the influence of commodity and/or petroleum sectors on a nation’s economy, our current article falls within the purview of these recent empirical works. Additionally, Sadik-Zada’s [

25] research, which examines the connection between natural resources and economic growth, is relevant to our current study. This is particularly important because Alaska, being heavily reliant on oil, could potentially experience the resource curse phenomenon, as proposed by Corden and Neary [

26], due to the significant role of oil in Alaska’s export composition.

The subsequent sections of the article are structured as follows: In

Section 2, we delve into a detailed discussion of the empirical methodology employed. In

Section 3, we provide details about the data sources employed in our analysis. Moving on to

Section 4, we outline the outcomes of our analyses, and finally,

Section 5 brings the article to a conclusion.

2. Methodology

2.1. The Approach of SVAR

To determine whether variations in oil prices are attributed to changes in oil supply or changes in oil demand, we employ a structural VAR model that makes use of monthly data for the vector

)′, where

represents global crude oil production,

stands for a measure of global economic activity, and

signifies the real price of crude oil. The SVAR model is outlined as follows:

The vector

represents a set of uncorrelated and independently distributed white noise error terms. In this context, we assume that

exhibits a recursive structure, enabling the breakdown of the reduced errors

in the manner

. Following this, we ascribe the fluctuations in oil prices to three distinct structural shocks: (i)

accounts for disruptions in oil supply; (ii)

encompasses shocks impacting the global demand for all industrial commodities, referred to as aggregate demand shocks, and (iii)

stands for demand shocks exclusive to the global oil market, known as oil-specific demand shocks.

Equation (2) posits that the short-term supply curve for crude oil is perfectly inelastic. When shifts in the demand curve occur due to either of two distinct demand shocks, oil prices undergo immediate adjustments as they move along the supply curve. Similarly, unforeseen oil supply shocks lead to changes in oil prices by shifting the vertical supply curve along the demand curve.

The rationale behind the constraints imposed on is as follows. is presumed to remain unresponsive to and within the same month. This assumption appears reasonable because, in practice, oil-producing nations typically exercise prudence and gradual adjustments when changing their oil production levels in response to shifts in oil demand. Additionally, is assumed to reflect the idea that global economic activity does not immediately react to changes in oil prices caused by oil-specific demand shocks. Instead, it is believed to display a delayed response, with at least a one-month lag in its reaction to oil price fluctuations. Finally, is considered to capture variations in oil prices that cannot be explained solely by and . It represents shifts in the precautionary demand for oil, driven by uncertainties about future oil supply.

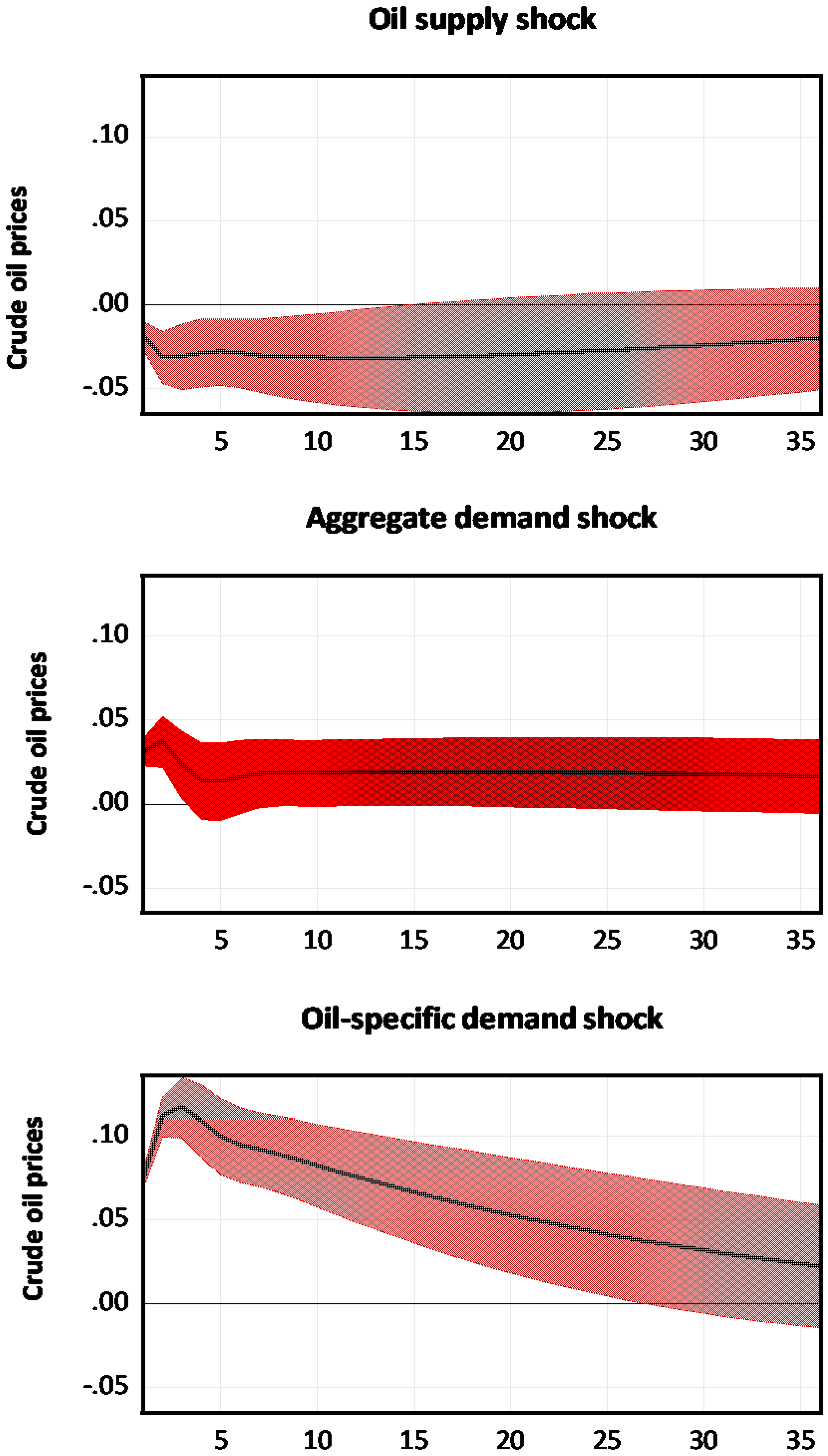

Figure 1 presents the changes in the real oil price in response to the three structural shocks, as depicted by impulse response functions (IRFs). An unexpected increase in global crude oil production leads to an immediate decrease in the real oil price. This decrease, although statistically significant, is short-lived, lasting for about 10 months. When there is an unexpected rise in aggregate demand, it causes an immediate but brief statistically significant increase in oil prices that lasts for approximately three months. On the other hand, an escalation in an oil-specific demand shock triggers an immediate, substantial, and significantly prolonged surge in oil prices, characterized by pronounced overshooting. Thus, the responses to oil price shocks appear to vary depending on the type of shock, although all three responses are ultimately temporary.

2.2. The Approach of ARDL/NARDL

To investigate how various components of oil shocks influence the fluctuating levels of oil production in Alaska, we have made modifications to the empirical framework originally proposed by Baek [

16]. In this context, we establish Alaska’s oil production level (

) as being dependent on various factors, encompassing oil supply shocks (

), aggregate demand shocks (

), oil-specific demand shocks (

), and interest rates (

):

The variables

,

, and

are obtained from the estimated residuals in Equation (2).

Figure 2 illustrates the three identified oil shocks over the period from 1994 to 2022. If increased oil shocks result in higher oil prices and greater oil production in Alaska, we anticipate that the estimates for

,

, and

will be positive. On the other hand, if a rise in interest rates leads to increased investment costs in the oil and gas industry, causing a reduction in oil production levels, we expect the estimate for

to be negative.

Our next modeling step involves converting Equation (3) into an error correction presentation. This allows us to examine the short-term and long-term effects of exogenous variables on Alaska’s oil production level simultaneously. To achieve this, we adopt the ARDL approach as presented by Pesaran et al. [

18], which offers a unique advantage in this context:

Upon estimating Equation (4), the Σ estimates represent the short-term impacts, whereas the

estimates signify the long-term effects. To verify these long-term effects, Pesaran et al. [

18] introduce two cointegration tests. The first test is a

t-test, which assesses the significance of

, and the second test is an

F-test, employed to determine the combined significance of lagged-level variables.

Up until this point, we have been working under the assumption that Equation (4) reflects a symmetrical response for Alaska’s oil production level to the three shocks. However, if it turns out that these shocks have an asymmetric impact on oil production, estimating Equation (4) might lead to misleading findings. In line with the nonlinear ARDL approach presented by Shin et al. [

19], we adjust Equation (4) to incorporate asymmetric analysis. This adjustment involves dividing the changes in the three oil shocks into two distinct sets of time-series variables for each of them: one set represents only positive shock changes (

) and the other set represents only negative shock changes (

). Typically, this is accomplished using the partial sum technique. As an example for oil supply shocks,

is calculated as

and

is computed as

. By substituting Equation (4) with these two sets of partial sum variables for the three shocks, Equation (4) is modified accordingly:

Similar to the ARDL approach, we can uncover both short-term and long-term relationships and verify the presence of cointegration. When we estimate Equation (5), we utilize the Wald statistic to detect asymmetry. Using oil supply shocks as an example, if the Wald statistic rejects the null hypothesis of , we can establish evidence of a long-term asymmetric effect. Conversely, if the Wald statistic rejects the null hypothesis of , we can conclude that there are asymmetric short-term effects.

3. Data

Our analysis relies on a variety of data sources. We use global oil production, measured in millions of barrels per day, which we obtain from the United States Energy Information Administration (EIA), as a representation of worldwide oil supply. To gauge global economic activity, we utilize the OECD total industrial production index, sourced from OECD Statistics, as a proxy. For the price of crude oil, we rely on data from the EIA, specifically the U.S. crude oil import acquisition cost in USD per barrel. To account for inflation, we adjust the nominal price using the U.S. Consumer Price Index (CPI), which we extract from the IFS. Additionally, we consider Alaska’s crude oil production, measured in thousands of barrels per day, which we obtain from the EIA. Finally, for the interest rate, we use the effective federal funds rate, sourced from the Federal Reserve Bank of St. Louis (FRED), as a proxy. Our dataset comprises 350 monthly observations, spanning from January 1994 (1994:M1) to March 2023 (2023:M3).

At this point, it is important to acknowledge several limitations in this study that emanate from both the quality and scope of the data employed, as well as the selection of the proxies. The outcomes and conclusions presented here are contingent upon the dataset available, spanning from January 1994 to March 2023. While this dataset offers a substantial timeframe for analysis, its constraints may influence the extent to which our results can be applied to different time periods or economic contexts. Additionally, as we endeavored to dissect oil price fluctuations into oil supply and oil demand shocks using a structural VAR model, we opted to utilize the OECD total industrial production index as a substitute for measuring global economic activity, departing from the Kilian index employed in Kilian’s seminal work in 2009. This substitution may introduce variations in the results due to disparities in the indicators chosen to represent economic activity. Moreover, we opted to use the U.S. crude oil import acquisition cost in dollars per barrel as a surrogate for oil prices, diverging from the more commonly employed benchmarks such as WTI and Brent. Although this choice was influenced by prior research, it is vital to acknowledge that it may impact the comparability of our findings with studies employing alternative oil price benchmarks. In light of these limitations, readers are encouraged to interpret our results with due consideration for the data constraints and proxy choices and to exercise caution when generalizing the findings to different data ranges or when comparing them to research employing alternative datasets or proxies.

4. Results

In this section, we employ ARDL to estimate the linear model described in Equation (4) and NARDL for the nonlinear model outlined in Equation (5). Both modeling methods assume the absence of serial correlation in the errors. To ensure this, we need to determine the suitable lag order for eliminating serial correlation. After setting the lag order to three months, the null hypothesis of homoscedasticity cannot be rejected based on LM statistics. Thus, we utilize AIC while constraining the maximum lag to three months to identify the optimal lag order for each of the two modeling processes.

Let us begin by examining the outcomes of the ARDL modeling, as presented in

Table 1. In the context of short-term findings, we see that there is statistical significance in at least one of the variables

and

and that this significance is observed at a minimum level of 10%. This implies that the shocks in both oil supply and aggregate demand play a substantial role in affecting Alaska’s short-term oil production. In contrast, the estimates of

and

do not demonstrate statistical significance, even at a significance level of 10%. This implies that oil-specific demand shocks and interest rates have minimal impact on Alaska’s short-term oil production.

What do the outcomes reveal when we delve into the long-term perspective? When we shift our attention to the long-term discoveries, none of the explanatory variables show statistical significance, even when considering the 10% significance threshold. This suggests that both the three oil shocks and the interest rate do not exert substantial effects on Alaska’s oil production over the long term. It is crucial to highlight that for the long-term relationship depicted in Equation (4) to be valid, substantial evidence of cointegration among the four variables is necessary. Unfortunately, both the

F- and

t-statistics fail to exhibit significance, suggesting a lack of cointegration. Consequently, it raises doubts about the reliability of the long-term estimates in Equation (4). Hence, it becomes apparent that the ARDL method may not be a suitable modeling approach for effectively uncovering the short-term and long-term impacts of various aspects of oil shocks on oil production within the context of Alaska. While there are no studies specifically analyzing the effects of various oil price shocks on oil production, we can draw parallels between our findings and those of similar studies that examine the influence of external oil shocks on a nation’s economy. From this perspective, our long-term results contrast with those reported by Adelegan et al. [

27] and Wang et al. [

28]. For instance, Adelegan et al. [

27] highlight the direct impact of oil price shocks on oil revenue in Nigeria, whereas Wang et al. [

28] demonstrate that oil price shocks significantly contribute to fluctuations in unemployment rates in Russia and Canada.

Could the NARDL method generate results that differ from those of the ARDL method? To explore this possibility, we will now analyze the findings derived from the NARDL modeling, as detailed in

Table 2. We will begin by delving into the short-term results, following a similar approach to our examination in the ARDL modeling. Starting with the impact of oil supply shocks, it becomes apparent that both

and

display statistical significance, highlighting the notable influence of oil supply shocks on short-term oil production in Alaska. When we shift our attention to the shocks related to aggregate demand and oil-specific demand, we observe that at least one of the coefficients for

and

is statistically significant, while none of the coefficients for

and

demonstrate statistical significance. This underscores the substantial influence of aggregate demand shocks on Alaska’s short-term oil production, while the impact of oil-specific demand shocks is minimal. These findings align with the results obtained from the ARDL modeling. Finally, it is worth noting that the coefficient linked to

has now been found to be significant. This signifies that interest rates do indeed play a noteworthy role in impacting the level of oil production in Alaska, which differs from what was observed in the ARDL modeling results.

We now focus on the long-run results. We note that both and yield statistical significance with positive values. This suggests that an unexpected rise (decline) in oil supply shocks appears to significantly increase (decrease) Alaska’s oil production in the long run. One way to interpret this finding is that an unforeseen surge in oil supply shocks frequently coincides with periods of global economic growth and heightened demand for oil. As a result, this gradual increase in demand leads to a steady growth in Alaska’s oil production over an extended period. In relation to the impacts of aggregate demand shocks, it is noticeable that both and yield positive estimates. However, significance is observed solely for , indicating that only positive aggregate demand shocks appear to significantly increase Alaska’s oil production. This could be attributed to the fact that a positive aggregate demand shock serves as a stimulus for the global economy, leading to higher oil prices and consequently driving up oil production in Alaska over the long term. Upon investigating the influence of oil-specific demand shocks, neither the positive shock () nor the negative shock () achieves statistical significance, even when considering a significance level of 10%. Thus, aggregate demand shocks exert a relatively limited effect on Alaska’s long-term oil production.

When we incorporate the asymmetrical assumption, it becomes apparent that a higher interest rate has a notably positive impact on Alaska’s oil production in the long term, similar to the short-run findings. This suggests that an increase in interest rates is associated with an increase in Alaska’s oil production. This finding may appear counterintuitive since higher interest rates are typically linked to reduced investments in the oil and gas sectors that could theoretically lead to a decline in Alaska’s oil exploration activities. However, one credible explanation for this phenomenon might be the frequent alignment of higher interest rates with a stringent monetary policy during phases of economic growth in the United States. This U.S. economic expansion typically fosters global economic growth and results in elevated oil prices, factors that are likely to play a role in driving up Alaska’s oil production.

Once again, it is essential to emphasize that for the long-term relationship described in Equation (5) to remain valid, we require a compelling case for the cointegration of the seven variables. In contrast to the ARDL model, both the F- and t-statistics are highly significant, even at the 5% level, providing robust evidence of cointegration. Consequently, the long-term estimates in Equation (5) appear to be reliable. Therefore, utilizing the NARDL model with the incorporation of the asymmetrical assumption proves to be a more suitable modeling approach for effectively understanding both the short-term and long-term impacts of various elements of oil shocks on oil production in the context of Alaska.

The utility of employing the NARDL modeling lies In uncovering potential asymmetry within the three oil shocks. This is driven by the observation that the estimated coefficients for the three positive shocks differ from those associated with the three negative shocks in both short- and long-term outcomes, raising suspicion about potential short- and long-term asymmetry. However, to validate the reliability of this observation, conducting the Wald test becomes essential. The results of this test reveal that, while there is no evidence of short-run asymmetry for any of the three oil shocks, long-run asymmetry is present in the case of shocks related to aggregate demand and oil-specific demand. These findings suggest that Alaska’s oil production responds differently to positive and negative oil shocks in the context of aggregate demand and oil-specific demand over the long term. Once again, although we cannot directly compare this finding to other studies due to the absence of asymmetry in various oil prices, it shares similarities with the work of Olayungbo and Umechukwu [

29]. They also highlight the significance of long-term asymmetry in oil demand shocks, showcasing the asymmetric effects of oil price shocks on output in Algeria and Egypt.

As we near the conclusion of this section, it is crucial to underscore that while our research findings stem from the distinctive context of Alaska’s oil production, they offer valuable insights with potential applicability to other developed nations that share similarities in their oil sectors. The notable impact of oil supply and aggregate demand shocks on Alaska’s oil production, contrasted with the limited influence of oil-specific demand shocks, implies the relevance of these dynamics in analogous regions. However, it is imperative to account for the specific economic, geographical, and regulatory variations among oil-producing areas, which may affect the degree of generalizability. Nevertheless, the importance of interest rates in comprehending fluctuations in oil production, along with the identification of long-term asymmetrical effects, presents a valuable framework for policymakers and researchers in comparable oil-producing regions to investigate and tailor to their specific contexts.

5. Concluding Remarks

This research conducts a comprehensive empirical investigation to explore the relationship between oil price shocks and oil production levels in Alaska. It specifically examines the significant roles played by both oil supply and demand shocks in influencing the fluctuations in Alaska’s oil production, considering both symmetric and asymmetric scenarios. To achieve this objective, the study utilizes a variety of analytical methods, including the structural vector autoregression (SVAR), autoregressive distributed lag (ARDL), and nonlinear autoregressive distributed lag (NARDL) models. By integrating these diverse methodologies, this paper offers a comprehensive and in-depth understanding of the complex dynamics between oil price shocks and oil production in Alaska.

From a methodological standpoint, our analysis demonstrates that employing the NARDL model with the inclusion of the asymmetric assumption is a more appropriate modeling approach for gaining a comprehensive understanding of the short-term and long-term effects of different components of oil shocks on oil production in the context of Alaska.

From a policy standpoint, the NARDL model reveals that both oil supply and aggregate demand shocks exert substantial influence on Alaska’s oil production, impacting both short-term and long-term dynamics. In contrast, oil-specific demand shocks exhibit minimal impact on the fluctuations in Alaska’s oil production in both the short and long term. Additionally, our analysis identifies asymmetrical effects in the long run, particularly in the case of aggregate demand and oil-specific demand shocks influencing Alaska’s oil production. However, no asymmetric effects are observed in the three oil shocks in the short term. Lastly, our findings emphasize the substantial role played by interest rates in understanding fluctuations in Alaska’s oil production, whether in the short or long term.

Our empirical findings carry important policy implications. Firstly, the Alaskan government needs to recognize that there is no one-size-fits-all solution for managing oil production in response to oil price fluctuations. The impact of these shocks on oil production varies depending on the specific nature of the shock. Consequently, policies should be tailored to address the particular type of shock influencing the state’s oil production. Secondly, given that demand-side shocks exhibit asymmetric effects on long-term oil production fluctuations, the Alaskan government must prioritize the incorporation of long-term fiscal planning into policymaking. Through strategic fiscal measures, the government can implement safeguards and enhance economic growth in response to adverse demand-side shocks, fostering a stable and sustainable economic expansion. Finally, acknowledging the crucial influence of interest rates in explaining changes in Alaska’s oil production, policymakers may consider approaches to promote investment in the oil sector while mitigating the impact of interest rate fluctuations. For instance, the government could introduce tax incentives and deductions for companies involved in oil sector investments. This would effectively lower borrowing costs, incentivizing businesses to launch new projects or expand existing ones, even during periods of elevated interest rates.

Our empirical results also carry substantial environmental and social implications. Starting with the environmental aspect, the findings underscore the critical need for sustainable resource management practices in Alaska’s oil industry. With significant impacts observed from supply and demand shocks over both short and long periods, it becomes imperative to develop and implement environmental management strategies that can withstand such fluctuations. For example, sudden increases in production due to supply shocks may necessitate heightened environmental monitoring to mitigate potential ecological impacts, such as increased emissions or habitat disruption. Similarly, long-term impacts resulting from aggregate demand shocks may call for comprehensive sustainability assessments to ensure responsible resource extraction. These findings emphasize the importance of aligning oil production with environmental stewardship to minimize ecological risks while capitalizing on economic benefits. Turning to the social dimension, our findings highlight the necessity of pursuing a more diversified economic strategy within the state. While the oil industry provides substantial revenues and employment opportunities, overreliance on it can make the economy vulnerable to oil market fluctuations. Socially, this means that efforts to diversify the economy, such as investing in alternative industries like renewable energy, tourism, or technology, are crucial for enhancing resilience and reducing the impact of potential economic downturns caused by oil shocks. Such diversification initiatives can lead to a more balanced and sustainable economic landscape, ensuring the well-being and livelihoods of Alaskan residents are less susceptible to the volatile nature of the oil industry.

In conclusion, this paper has provided an extensive analysis of the impact of various oil shocks on Alaska’s oil production, shedding light on both the short- and long-term effects within symmetric and asymmetric scenarios. However, beyond the empirical findings, it is crucial to recognize that Alaska’s oil production operates within a multi-faceted geopolitical and economic context that extends far beyond the scope of this study. Alaska’s substantial oil reserves and production activities hold a pivotal role in shaping energy policies and trade relationships, not only within its own state but also on regional, national, and international scales. Geopolitically, Alaska’s role in oil production contributes significantly to North America’s energy security, and its stability and consistency in oil supply are of strategic importance in a global energy landscape marked by uncertainty. Moreover, as the world grapples with pressing environmental concerns and the transition to cleaner energy sources, Alaska’s oil production intersects with broader discussions on climate change mitigation and sustainable energy practices. Understanding how Alaska navigates this evolving energy landscape is crucial for assessing the adaptability of oil-dependent economies in an era characterized by shifting global energy priorities. Furthermore, Alaska’s oil production is intricately linked to international energy markets by influencing pricing mechanisms and trade dynamics, making it a key player in the global energy trade network. In light of these complexities and considerations, this research serves as a valuable contribution to the understanding of Alaska’s oil production dynamics and underscores the broader implications of these findings within the geopolitical and economic context of the global energy landscape. It is our hope that this study not only enhances academic understanding but also informs policy discussions surrounding energy security, economic resilience, and sustainable practices in the face of evolving energy dynamics. However, while our empirical model provides a focused examination of the core variables, we understand the merit of expanding our discussion to encompass the broader geopolitical and economic landscape. In future work, we aim to incorporate these factors more explicitly, recognizing their interplay with the elements of our model. This will allow us to provide a more comprehensive understanding of Alaska’s oil production dynamics within the context of a complex and interconnected world.

{kind=link}

{kind=link}