1. Introduction

With the continuous depletion of non-renewable resources such as coal, oil and natural gas over the past decades, solar energy will eventually replace other resources to be the main stream. The development of clean renewable energy (RE) has become an inevitable choice for countries to achieve energy restructuring. According to the International Energy Agency (IEA) estimates, the share of RE production in total electricity generation will increase from 21% in 2012 to 33% in 2020 [

1]. Since the 21st century, as a national strategic emerging industry, China’s photovoltaic (PV) industry has developed rapidly. Its capacity and output rank first in the world. However, the unbalanced development of the domestic PV market leads to excess capacity: China’s northwestern region, which is rich in solar energy resources, mainly builds concentrated PVs. However, there is serious solar curtailment phenomenon in Gansu and Xinjiang provinces. Moreover, the demand for electricity in central and eastern regions is large, and solar energy resources are relatively insufficient. In order to accelerate the development of the domestic market and solve the problem of excess production capacity, it is imperative to accelerate the development of distributed photovoltaic (DPV) in the central and eastern regions [

2].

China’s new round of power system reform is focused on energy structural problems, that is, transformation and upgrading. Thus, there is an urgent need to accelerate the construction of new energy power. As a kind of new energy power generation, PV power generation has clean, renewable, energy conservation and emissions reduction advantages and huge potential for development. It is suitable for modern social concept and has received widespread attention in the world today.

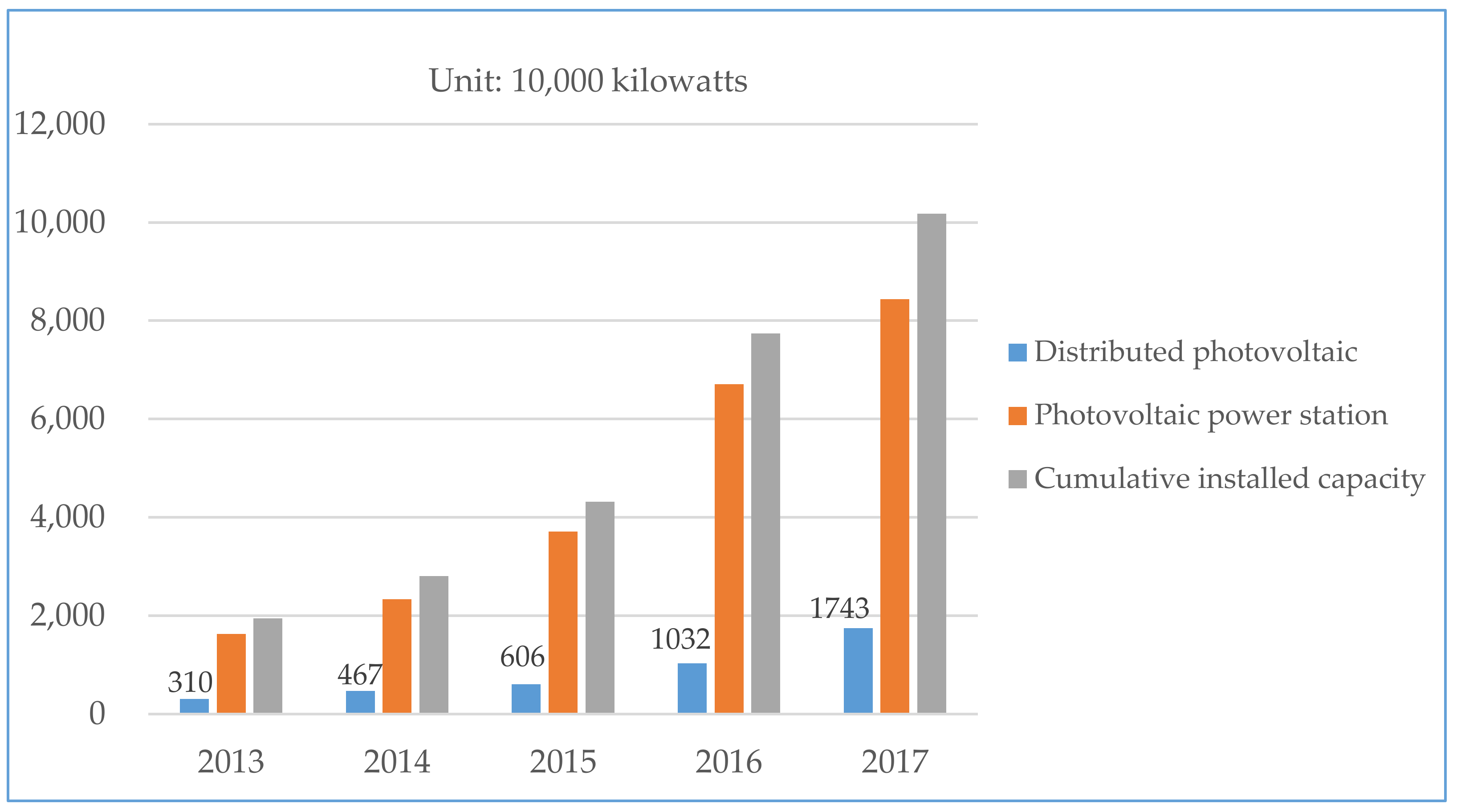

Figure 1 shows the rapid increase of installed PV power generation capacity in China from 2013 to 2017. In particular, in the first half of 2017, China’s newly installed PV power generation capacity was 24.4 million kilowatts, with an increase of 9% year-on-year. The National Energy Administration has adopted a series of measures to promote the implementation of the “leadership” plan for PV power generation and the “leadership base” construction plan. The local government and power grids regard DPV power generation as an assessment indicator for the performance. In addition, with a series of policies such as financial subsidies, acquisition of electricity security, and administrative licensing exemptions, more and more companies have joined the DPV investment. Therefore, how the government should control investment and review projects, especially how investors choose appropriate DPV power generation projects to invest has become a hot issue worth exploring.

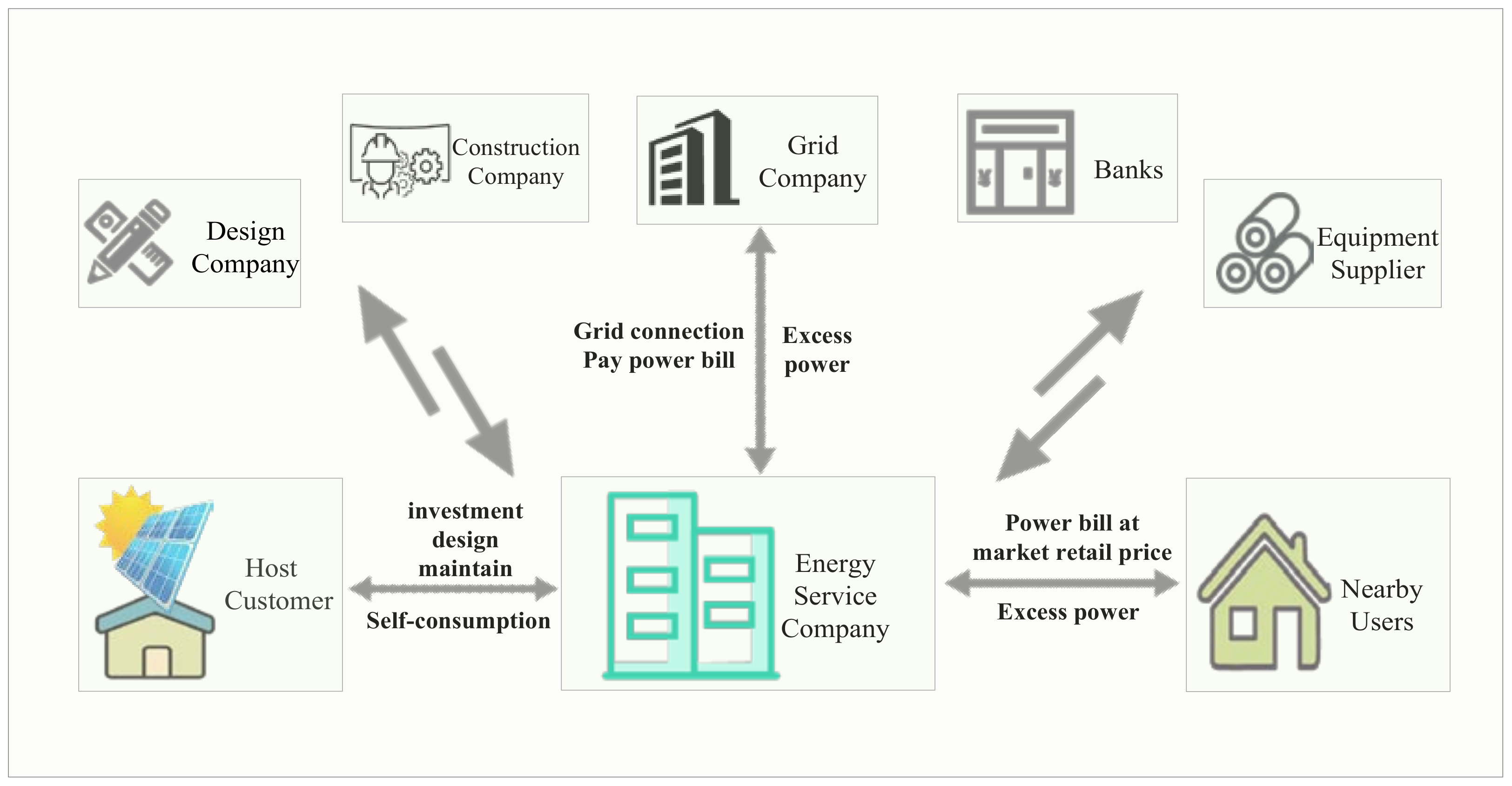

At present, the business models of China’s DPV power generation projects have diversified by introducing pluralistic investment entity. There are mainly three types of operational models, namely energy performance contracting (EPC), lease, and user self-use model. Despite of three models, there are only two types of billing methods with the power grid. One is to use part of the power for contract users themselves, and the remaining power is used for on-grid settlement, the other is the full amount of power generation on-grid settlement.

The essence of the EPC business model is that users have electricity demand, third-party investors who also receive corresponding benefits from project provide users with a complete solution to achieve a win-win goal [

3]. EPC business model is the focus of this paper, which refers to a third-party investor invests in DPV power supply, responsible for project financing, design, construction, maintenance, etc. (

Figure 2) Investors adopt “nearby using the surplus to grid” approach to settlement with the grid power (GC). In addition, under this model, third-party investors act to some extent as the role of power sales companies. This is exactly the direction advocated by the new round of power system reform that China is currently vigorously promoting. The EPC model helps to drive further opening of the power selling side, introducing multiple entities to participate in the competition for power sales. Third-party investors in contract energy management, as power supply service providers, have the natural advantage of becoming power sellers and have enormous potential for development in the future. The investor’s project revenue under EPC model will be introduced in the next chapter.

The main questions studied in this paper are: (1) which factors are influencing investment in DPV power generation projects? In addition, which factors are more important? (2) How the EPC business model has affected the project revenue? (3) What are the differences in decision making after considering the psychological characteristics of risk avoidance and loss of investors?

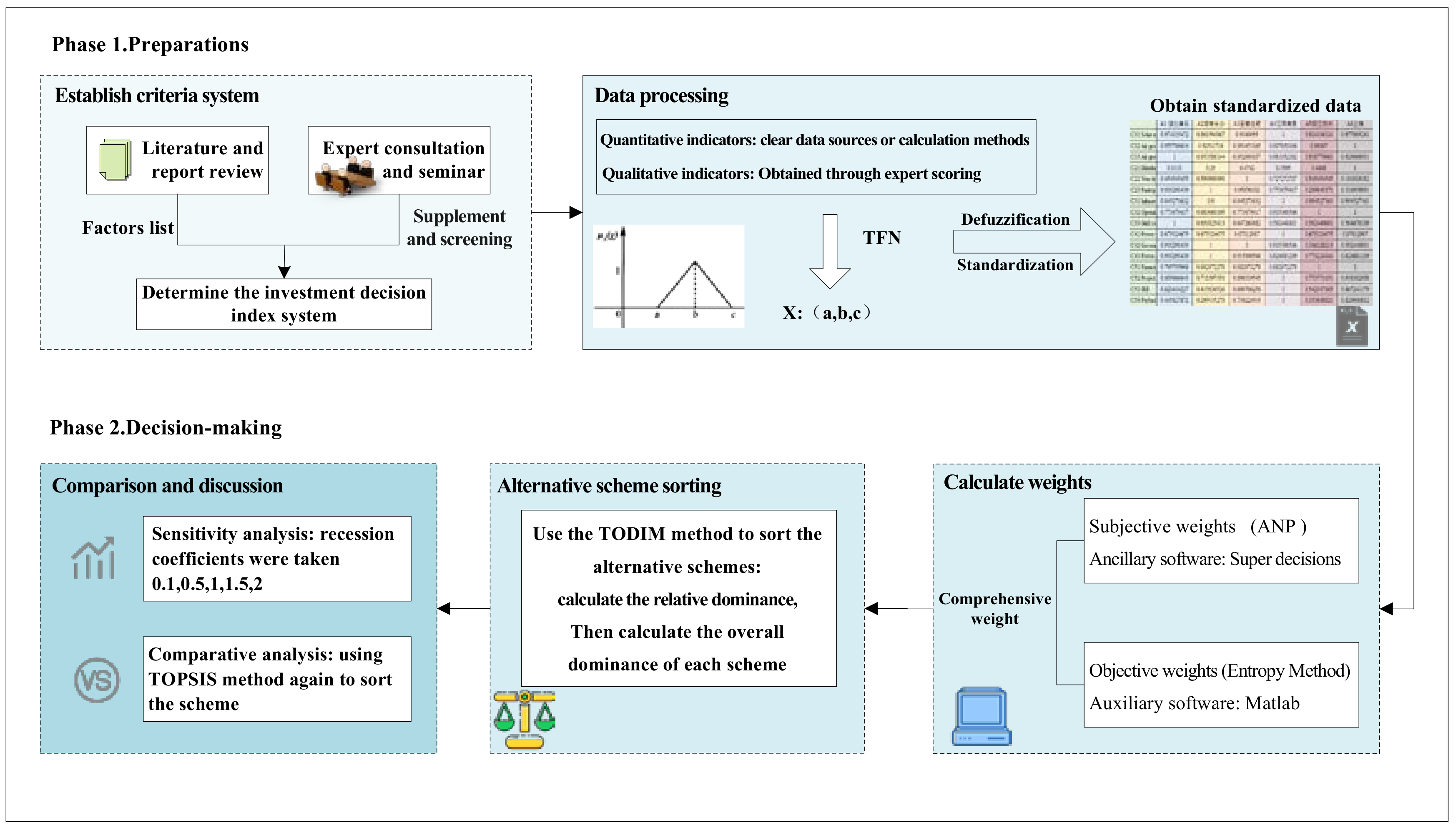

Investment decision plays an important role in the entire life cycle of DPV projects. However, two critical issues have not been solved well by existing researches. Firstly, existing DPV decision frameworks don’t consider that business models can significantly affect the economic performance of the project. Secondly, the decision frameworks don’t take account of investors’ psychology of avoiding risks and losses. To the best of our knowledge, this is the first study to deal with the above two problems simultaneously. The innovations of this study are as follows: first, a comprehensive decision criteria system of DPV projects is established from the perspective of natural, market, technological, policy and competitive, and economic. Second, the framework proposed in this paper considers the impact of business models on project economics and determines the business model is the EPC that is highly respected now and future in China. Third, the TODIM (an acronym in Portuguese of interactive and multicriteria decision making) method is applied to ranking alternatives, which can consider investors’ aversion to risk and loss.

To this end, the paper is organized as follows:

Section 2 provides a comprehensive literature review of DPV project decision methods.

Section 3 establishes an investment decision criteria system for DPV power generation projects based on the EPC business model.

Section 4 introduces the investment decision framework of the DPV power generation project. In the 5th Section, a case study is conducted: 6 schemes of DPV power generation projects distributed in central and eastern China are selected for model validation. Besides, sensitivity analysis is conducted by adjusting the recession coefficient, using the TOPSIS method to conduct a comparative analysis. The last section provides conclusions and recommendations.

2. Literature Review

In recent years, researches on PV investment have mainly focused on the following aspects: (1) Risk analysis of PV power generation projects: analysis of risk factors and establishment of risk assessment models, application of risk models to provide decision-making information for investment decision-makers (DMs) [

4,

5,

6]. Markov, et al. [

7] considered that the physical limitations of the transmission network would pose risks for PV investment. Li et al. [

6] considered extremes natural factors have adverse effects on PV power generation projects; (2) Impact of policies on the deployment and investment construction of DPV power generation projects [

2,

4,

8]; (3) Economic analysis of PV power generation projects, including revenue, cost, net present value (NPV), and internal rate of return (IRR) [

2,

9]. Garcia et al. [

10] proposed a compromise model (CP) model that simulates the agreement between the government that pursues as high a political price (guaranteed price) as possible and the project sponsor who hopes to receive revenue (random cash flow) as high as possible. Zhou [

11] considered the on-grid price adjustment in his PV investment decision and put forward three FIT models, namely fixed feed-in tariffs (FIT) (FFIT), constant premium FIT (CPFIT) and variable premium FIT (VPFIT) models. Fang et al. [

12] obtained the investment cost limit of distributed power generation projects through the application of real options, and then established the option value model of PV power generation investment and analyzed the cost-effective present value and net present value of investment options under the four scenarios; (4) Innovative business models, competitiveness, and market barriers for PV power generation projects [

3,

13]. Markov, et al. [

7] built a four-level NPV model based on the specific case of a small-scale solar PV power station project in Indonesia to discuss the micro-incentive measures for project participants and how to adjust incentives. It can be found that the research on multi-attribute decision making for DPV power generation projects is relatively rare. This paper integrates the key points of the above literature research. In addition, risk factors, competitiveness factors, economic factors, market factors, and policy factors are set as the target attributes of the DPV power generation project. A criteria system is established and a multi-criteria decision-making (MCDM) method is used to make decisions in specific projects.

Practice has proved that the scientific decision-making of DPV power generation projects is crucial to the ultimate success of the projects. Therefore, scholars have conducted a lot of research on the decision-making methods for PV and other RE power generation projects. Lin et al. [

14] obtained the system cost of DPV power generation by establishing an economic analysis model. Jannuzzi and Melo [

15] established a set of technology diffusion models and defined the computer system to be used in Brazil’s PV project evaluation. Miescher, et al. [

16] Used the two indicators Average Electricity Cost (LEC) and NPV to analyze and evaluate the economics of a small DPV system in Brazil. Holdermann et al. [

17] used the cost and income of a typical PV system to evaluate the economics of a DPV power generation system in residential homes and businesses in Brazil. Huang et al. [

18] believed that the investment cost of household DPV power generation projects is still relatively high for individuals, and the investment recovery period is long, but under the current policy subsidies and other incentive policies, the NPV can maintain a positive value. Qiang et al. [

19] insisted that current PV power generation does not have national economic rationality in some regions of China. None of the above economic studies have considered the impact of the business models of DPV power generation projects on economic calculations. Shi [

20] considered the impact of decay rate on the economics of DPV, and put forward an understanding of the EPC model, without considering the calculation of specific economic indicators under the EPC business model yet. Therefore, after considering the specific operating model of DPV power generation projects, this paper will be followed by the establishment of a decision-making criteria system as well as economic calculation.

Technique for Order Preference by Similarity to an Ideal Solution (TOPSIS) is a commonly used decision method that calculates the distance between alternatives and reference plans. Şengül et al. [

21] used fuzzy TOPSIS to rank the RE supply projects in Turkey and proposed the investment projects that are selected by the government through case studies. Investment in wind power is subject to complementarity constraints describing a large number of market clearing conditions. Since the profit as a function of the investment variables has as sufficiently convex envelope, the considered problem can be solved by Benders decomposition. Baringo et al. [

22] based on the BENDERS decomposition algorithm in the mathematical programming model, analyzed and discussed various uncertain scenarios in wind power projects, and selected investment projects with maximized profits. Fetanat [

23] constructed a decision-making criteria system for offshore wind power projects, by using fuzzy analytical network process (ANP) methods to process the chromatographic relationship between decision indicators of offshore wind power projects, DEMATEL is employed in criteria and sub-criteria sections to resolve the influence relationships among indicators, ELECTRE is applied to calculate the decision making matrices of sub-criteria to alternatives. Gazheli and Bergh [

24] studied a community or firm considering to diversify its investment in two distinct RE technologies. A real options approach is applied as it takes into account uncertainty about prices and learning, as well as irreversibility associated with investment decisions. TODIM approach which can capture the DMs psychological behavior, is a recently developed MCDM method. Qin et al. [

25] applied TODIM method to solve a decision-making problem of selecting RE alternatives. Five RE resources as alternative solutions, each type of RE source has its advantages and disadvantages. In summary, Decision methods for RE investment are described in

Table 1.

The existing decision methods for DPV power generation projects are relatively extensive, mainly from economic indicators, real option, best investment value, and maximization of interest. The core of the methods lies in the economy of the project. There are few investment decisions for PDV power generation projects using MCDM methods. In fact, there are many factors affecting DPV power generation projects besides economic. Therefore, DPV power generation projects is essentially a MCDM problem.

In general, scholars have produced more research results on investment decisions for PV projects. However, most of the methods do not consider the important impact of project business models on economic indicators when calculating project economics. There is no obvious compensation among decision-making indicators of DPV power generation projects in this paper. Alternative projects generally do not have strong veto factors. Therefore, this paper does not choose the ELECTRE method and the PROMETHEE method (MCDM) that focused on solving the problem of compensating the indicators of the project plan to sort schemes. In addition, classical methods assume that decisions are conducted in a deterministic environment and decision-makers are completely rational while facing with investment risks. However, these hypotheses are not supported in actual decision. In particular, we should consider the impact of investors’ psychological characteristics of risk and loss avoidance on project selection. TODIM is an abbreviation for Portuguese interactive and multi-criteria decision-making. It has been proved that it can effectively deal with MCDM issues of limited rationality for decision-makers [

29,

30]. The classic TODIM method is proposed by GOMES et al. [

32] based on the prospect theory. Its main idea is to establish the relative dominance function of any scheme relative to other schemes based on the value function of the prospect theory, and then sort the schemes according to the obtained dominance. Therefore, after considering the specific business model and establishing a scientific investment decision criteria system, this paper selects the TODIM method based on prospect theory to make investment decisions.

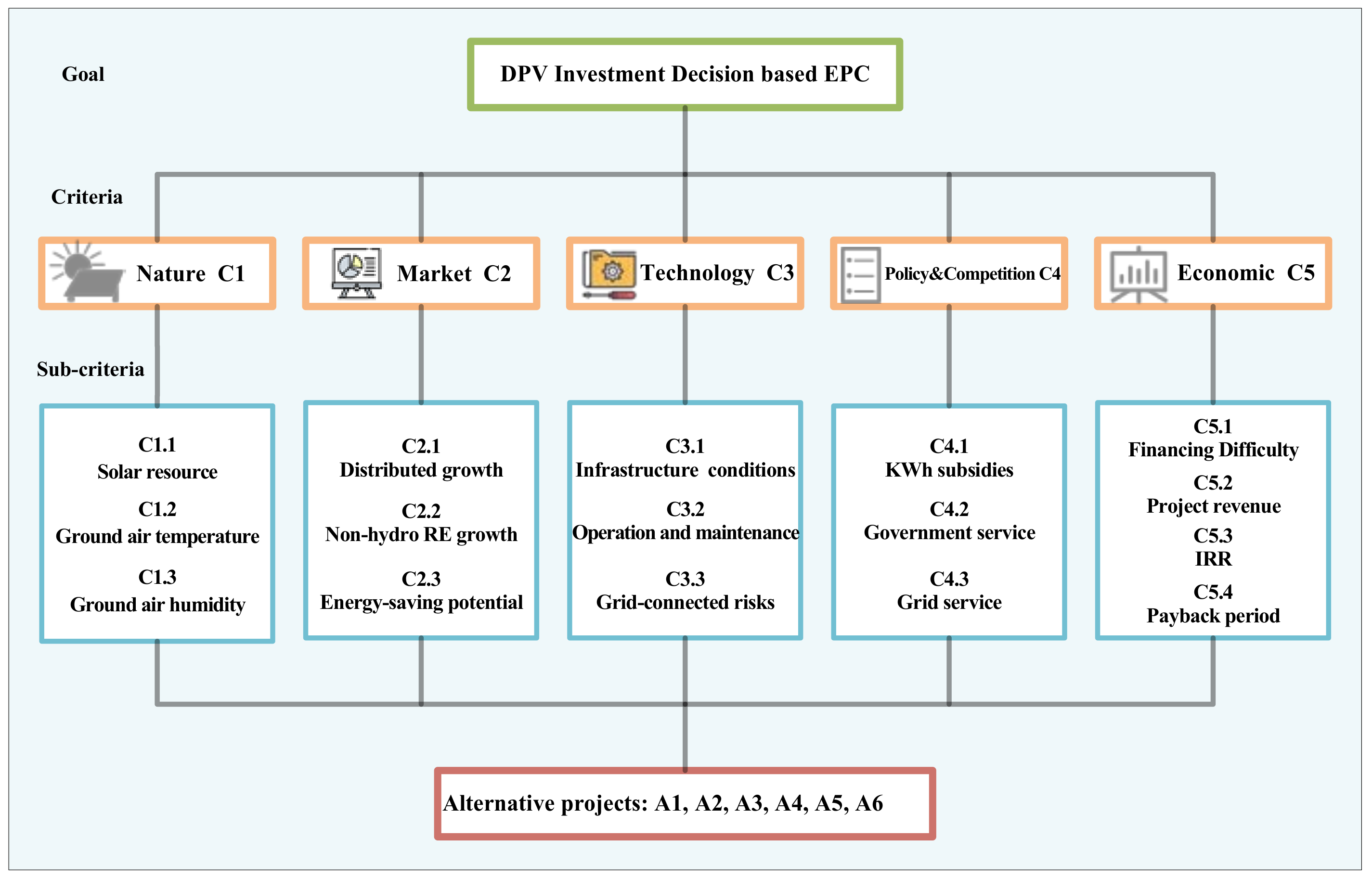

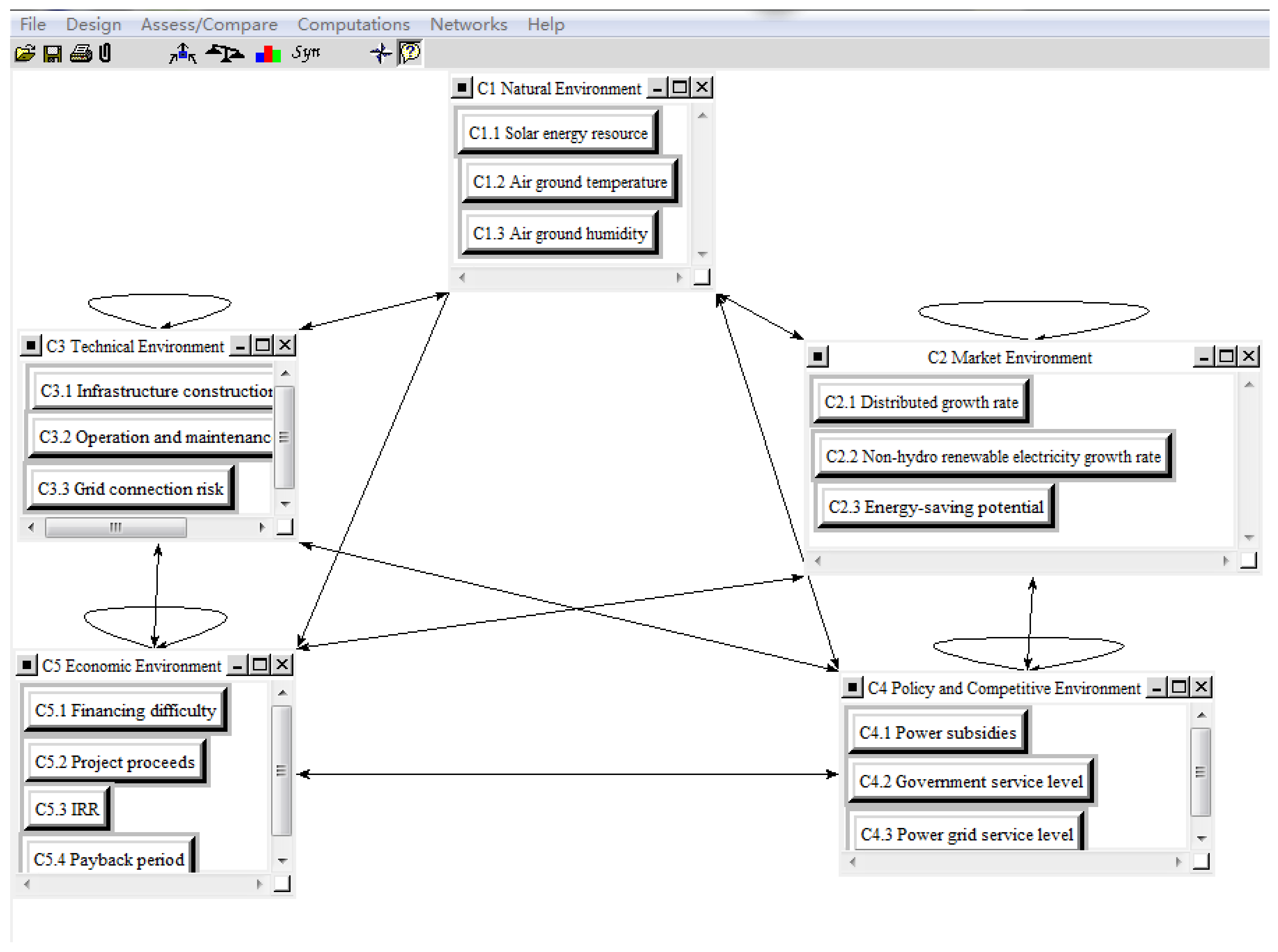

3. Investment Decision Criteria System of EPC-DPV Projects

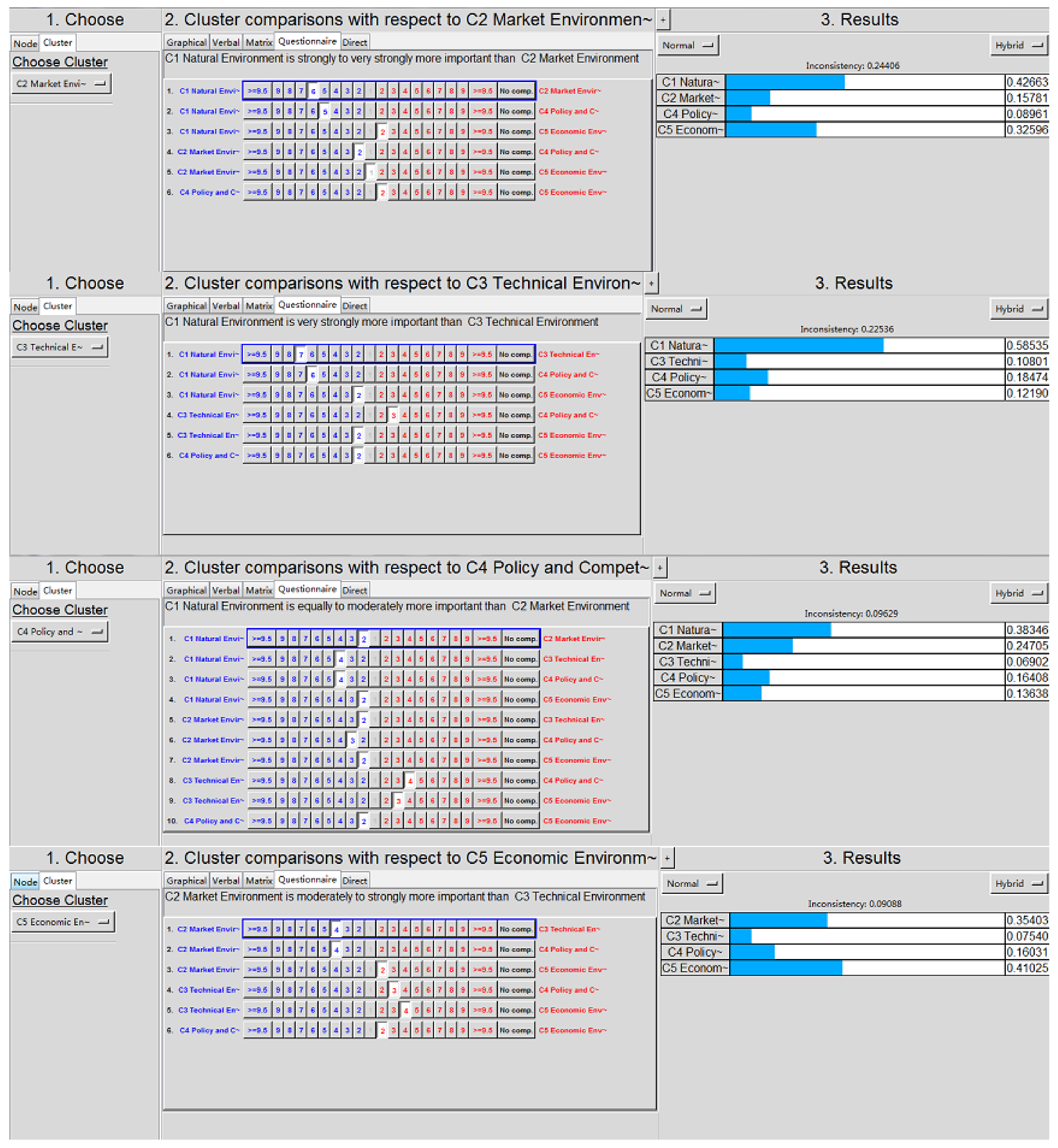

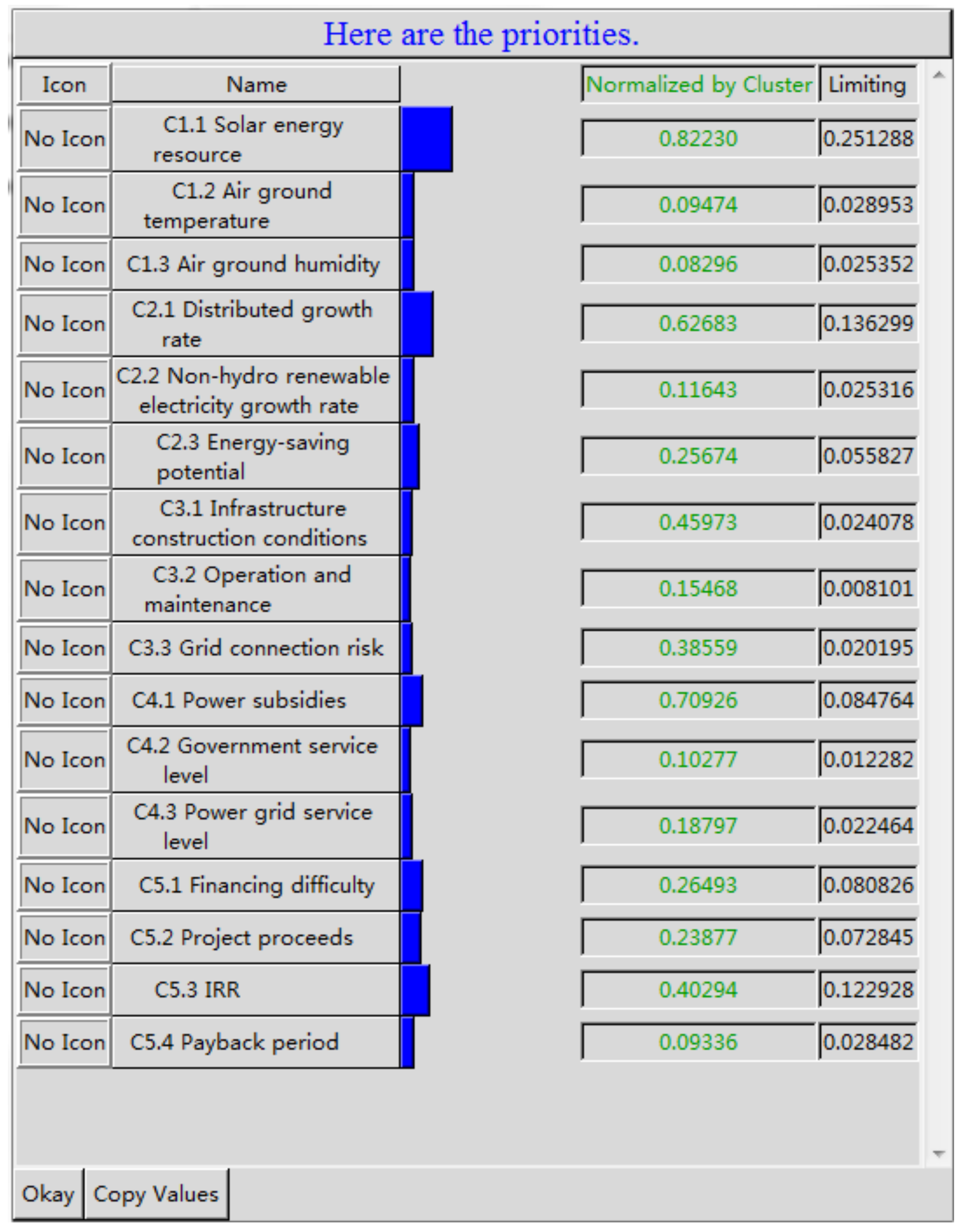

The design of the investment decision-making criteria system for DPV power generation projects is one of the key contents of this paper. This paper carries out investment decision analysis of DPV power generation projects from five aspects: natural environment C1, market environment C2, technological environment C3, policy and competitive environment C4, and economic environment C5. The 9 quantitative indicators include C1.1, C1.2, C1.3, C2.1, C2.2, C4.1, C5.2, C5.3 and C5.4. The 7 qualitative indicators include C2.3, C3.1, C3.2, C3.3, C4.2, C4.3 and C5.1. These 16 indicators constitute these five aspects. The five aspects described are the criteria to be used to evaluate the DPV projects.

3.1. Natural Environment Criteria (C1)

Solar energy resource (C1.1) [

33,

34]. PV power generation has a strong dependence on primary energy sources and is obviously constrained by solar energy resources. A key factor affecting PV power generation is the actual usable amount of solar energy resources.

Ground air temperature (C1.2) [

35,

36]. The electrical performance of solar cells and batteries varies with temperature, which affects the power generation performance of the entire PV system. Currently, large-scale commercial applications are mainly silicon-based solar cells. It mainly reflects that the open circuit voltage drops sharply with the increase of temperature. At the same time, it leads to a serious shift of the charging operating point, which could damage the system easily due to insufficient charging.

Ground air humidity (C1.3) [

6]. Safety and reliability are the main concerns of current and future distributed generation systems. The assessment of relevant risks must take into account the safety and stability of PV equipment in normal weather conditions or accidental events and extreme weather conditions.

3.2. Market Environment Criteria (C2)

3.3. Technical Environment Criteria (C3)

Infrastructure conditions (C3.1) [

39,

40,

41,

42]. The construction of grid-connected DPV requires not only appropriate roof and equipment placement space, but also the convenience of transportation. Whether the construction conditions are allowed and the two parties can cooperate well with the construction will affect the overall progress and cost of the project.

Operation and maintenance (C3.2) [

37,

43,

44]. O&M is the longest period of DPV power generation projects in the entire life cycle. Rational and scientific O & M systems and methods can effectively reduce the related technical risks of PV power generation.

Grid-connected risks (C3.3) [

41,

45,

46]. DPV power generation has inherent characteristics such as volatility, intermittent, and periodicity. When the DPV power supply is integrated into the distribution network, it will have an adverse effect on the distribution network.

3.4. Policy and Competitive Environment Criteria (C4)

kWh subsidies (C4.1) [

47,

48,

49]. The subsidy of DPV power generation by the country, provinces, and regions fully illustrates the importance of RE power generation projects, but the economic development level and subsidy intensity of each region are different. Different subsidies give investors a risk in choosing a DPV project.

Government service (C4.2) [

9,

41,

50]. The government service level in the DPV project location is crucial to the healthy development of the entire project. Whether the local government has formulated and implemented the DPV power generation management rules? Whether the local government can provide investors and users with one-stop market services? Whether there are disguised charges, apportionments, and other actions to increase corporate burden? These issues all reflect the level of policy and competitiveness. The second part of

Appendix A explains the process of obtaining the criteria (C4.2) information.

Grid service level (C4.3) [

9,

41,

50]. The promotion and future operation of the project are closely related to the supporting services of the local grid. Whether the supporting facilities, such as the transformation of the public distribution network line and metering device installation, can be built in time according to the construction period of the PDV project? In particular, whether the revenue of on-grid electricity can be settled in time?

3.5. Economic Environment Criteria (C5)

Financing difficulty (C5.1) [

51]. Most DPV users do not invest directly but participate in DPV power generation projects through EPC and renting out rooftops. According to the statistics of the Energy Bureau, in the first half of 2015, the actual installed capacity of PV was 7.5 GW, of which distributed accounts for 1 GW. In the first half of the year, the overall operating rate of the project was about 40%. The uncompleted projects were mainly affected by the failure of financing.

Project revenue (C5.2) [

52]. The project revenue of DPV power generation is the economic index that investors are most concerned about. Under the EPC model, the income of investors mainly includes the sharing of energy-saving benefits of customers, revenue from electricity sales, income from excess power online, and subsidies.

When making investment decisions, different operating models will affect the policy environment, competitive environment, and economic environment of DPV power generation. However, most studies do not explicitly consider the business model of DPV power generation projects, leading to rough investment analysis. This paper determines the business model is the EPC business model that is highly respected now and future to conduct investment decision analysis, which will make the decision criteria system more reasonable, and rigorous. Project revenue comes from four parts, namely generation allowance income (I1), on-grid income (I2), nearby consumptive income (I3) and energy-saving benefits (I4), respectively.

Table 2 shows the earnings calculations for EPC-based PDV power generation projects, after summarizing the relevant literature and combining China’s EPC operating model [

3,

20].

Internal rate of return (C5.3) [

50,

53,

54]: IRR is defined as the rate at which the total present value of capital inflows is equal to the total value of capital flows, and the discount rate when the net present value is zero. It is an important indicator of investor concern. The formula for calculating this indicator is as follows:

where

CI is the cash inflow volume,

CO is the cash outflow, (

CI−CO)

n is the net cash flow in the

Nth year, and

N represents the life cycle of the project.

Payback period of investment (C5.4) [

50,

53,

54,

55]. The initial investment of the DPV project is large, and the investment return period is long. The long recovery period will increase the probability of system failure. The formula for calculating this indicator is as follows:

where

CI is the cash inflow volume,

CO is the cash outflow, (

CI−CO)

n is the net cash flow in the

Nth year. The investment decision criteria system for EPC-DPV generation projects is shown in

Figure 3.

5. A Case Study of China

5.1. Background Introduction

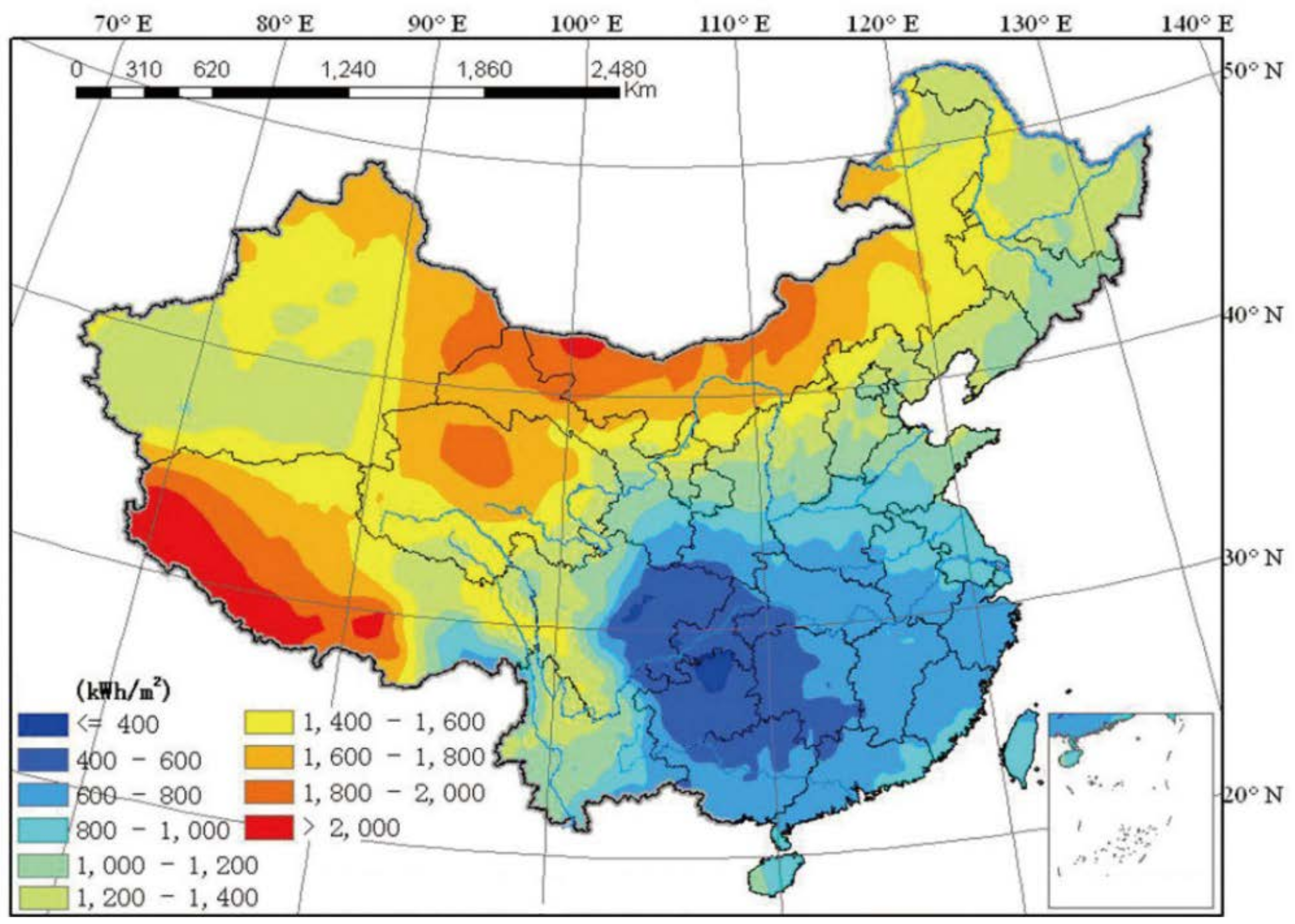

A very important idea in the 13th Five-Year Plan in China is that the development of RE will be more focused on local production and use in the nearest area. PV fully complies with this principle and is the direction of future development. China’s PV power generation presents a pattern of common development in the east, middle and the west. According to the distribution of solar energy resources in China as shown in

Figure 5, concentrated PV power stations are mainly constructed in the western region, and DPV power generation projects are concentrated in the central and eastern provinces. A domestic new energy investment company plans to invest in grid-connected EPC distributed photovoltaic power generation projects. After six alternative projects are initially formed through the preliminary work, the company plans to use investment decision-making model to find a high investment value of the scheme to invest.

The six projects initially selected are located in the central and eastern provinces of China, as shown in

Figure 6. A1 is located in Huangshi City, Hubei Province; A2 is located in Changsha City, Hunan Province; A3 is located in Hefei City, Anhui Province; A4 is located in Nanchang City, Jiangxi Province; A5 is located in Hangzhou City, Zhejiang Province; A6 is located in Shanghai. The installed capacity of the DPV power generation system is set to 1000 KW. The PV power generation system is installed on the roof of the industrial and commercial enterprise’s plant in the municipal district. The areas where these six projects are located are all suitable for the development of DPV power generation projects, with the conditions for DPV power generation to be consumed nearby, and the remaining amount of access to the grid.

However, these six projects differ in market environment, policy subsidies, competitive environment and so on, which brings obstacles for the investors to choose which projects to invest in. In order to maximize economic and social benefits, the company decided to invite experts in the field of DPV power generation to form an assessment committee to help them select the most suitable project for investment. The committee is composed of three main experts, all of whom are professors. Expert E1 is an outstanding scholar in the field of new energy project management and has a solid foundation for theoretical research. The research direction of expert E2 is investment decision. He has been responsible for the investment decision analysis of power grid and government projects on many occasions. Expert E3 has many years of experience in power engineering construction. The three experts have certain understanding of the investment environment and policies for new energy projects.

5.2. Alternative Data Sources

The evaluation criteria system in the investment decision model consists of nine quantitative indicators and seven qualitative indicators. The details are described in the previous section. The data values of the nine quantitative indicators have clear data sources and calculation methods (

Table 3).

The data values of qualitative indicators are obtained through questionnaire surveys and the holding of expert seminars. Using very poor (1), poor (3), general (5), good (7), very good (9), these five language scales describe the attribute of project indicators. Finally, the scores of three experts are counted to determine the score. The data values are first described in terms of TFNs. Through defuzzification and normalization processing, the attribute values of the indicators all lie within the range of 0–1.

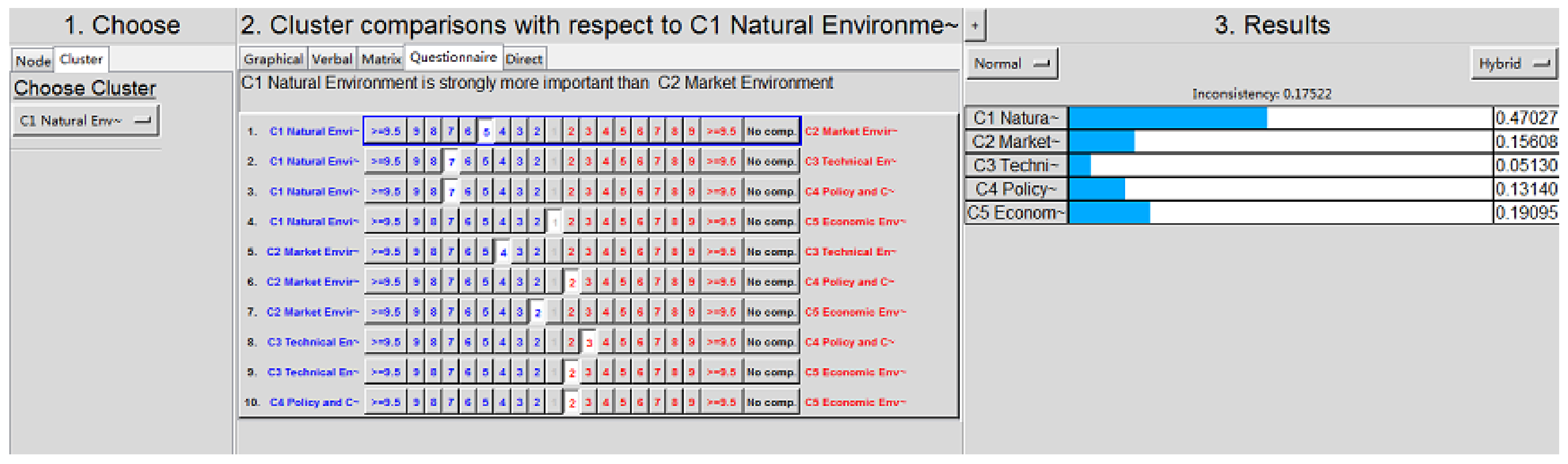

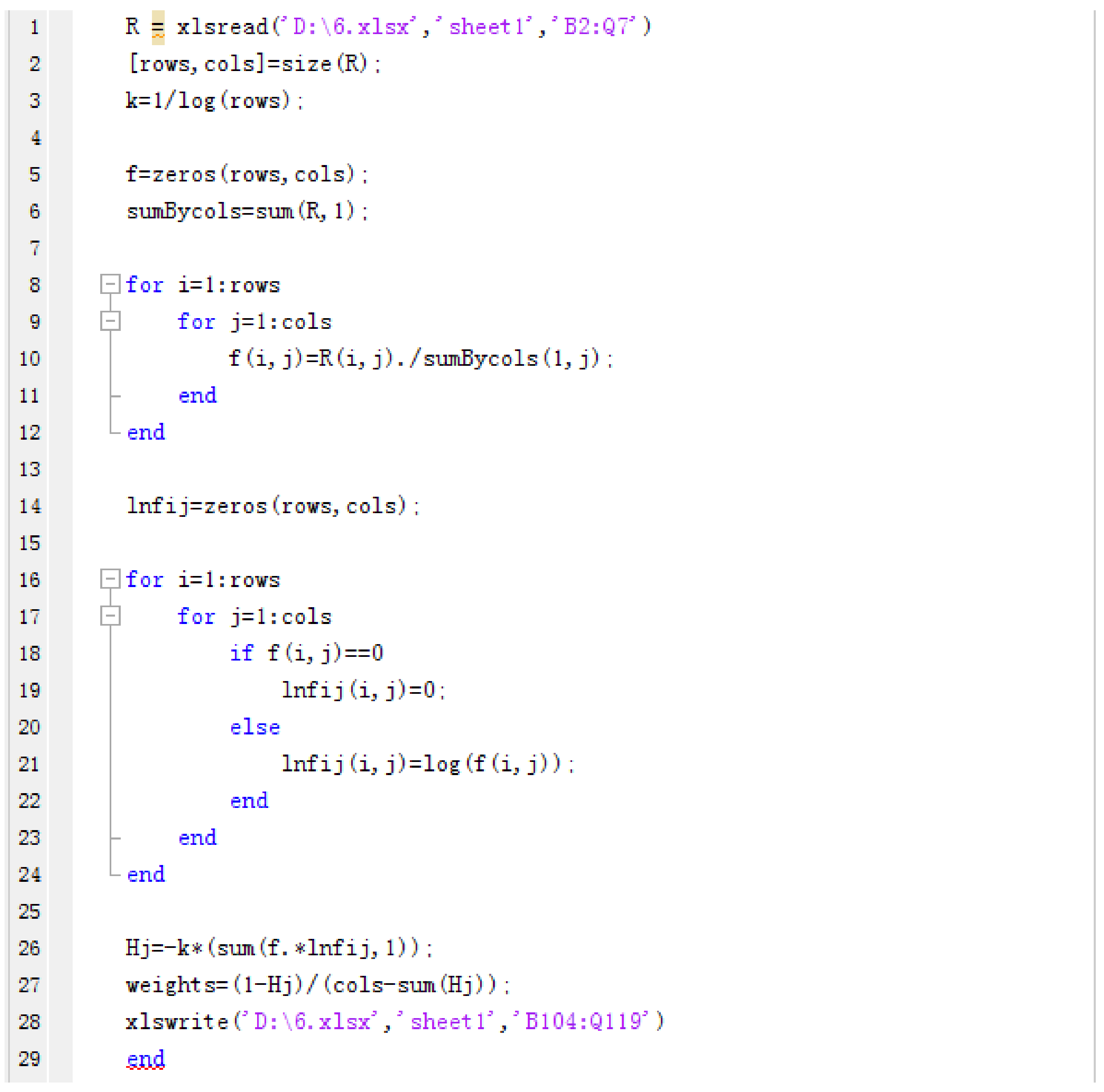

5.3. Weight Calculation

This section is based on the ANP method and entropy method described in 4.3 to determine the subjective weights and objective weights of the indicators, and finally get the comprehensive weights. The three indicators C1.1, C1.2, and C1.3 in the natural environment take their minimum, average, and maximum values as the numerical source of the TFN; Under the economic environment, the three indicators C5.2, C5.3, and C5.4 use the on-grid values of 30%, 50%, and 70% of the total power generation as the source of the number of TFNs. The on-grid values settings here are obtained through the interviews’ questionnaire. (Part 3 of

Appendix A) The attribute value of the TFN of the qualitative indicator is composed of the minimum value, the average value, and the highest value scored by the experts. The titles of the three experts are professors. When expert opinions are assembled, they are considered to have the same weight.

When calculating subjective weights, the most important step is to analyze the relevance of the indicators. The final mutual influence concern of the factors is shown in

Table 4. The symbol “√” means that the criterion in the row would have an effect on the factor in the column.

Set equal shares of the subjective weight and the objective weight to calculate comprehensive weights. Investors consider that both weights are equally important when there are many attributes and large uncertainties. The final results are shown in the

Table 5.

The market environment and economic environment account for a relatively high proportion. Due to the little difference in solar energy resources, the weight of environmental indicators is not prominent.

Figure 7 shows the intuitive proportions of indicators at all levels.

5.4. Applying TODIM Method for Ranking

By the above calculation (Equations (5) and (6)), the normative decision matrix

can be obtained. The relative weight of indicator

Cj is

wjr = wj/

wr, where

is the reference weight. Due to the large number of decision indicators, only the dominance matrix

under indicator C1.1 is listed here as an example (

Table 6).

According to the steps described in

Section 4.4, compute the dominance matrix Φ

j for each indicator

Cj, then summarize the dominance of the 16 indicators to get the overall dominance matrix of the project, as shown in

Table 7.

According to the Equations (8) and (9), calculate the comprehensive sorting value of the solution. The result is shown in

Table 8.

Based on the calculation results, the order of alternative items can be determined as follows: . Therefore, the company should give priority to investing in Project A4, which meets the requirements of DPV power generation technology and has good economic, environmental, and social benefits. The result is an optimal project plan that reflects the investor’s certain psychological, i.e., the recession coefficient θ = 1.

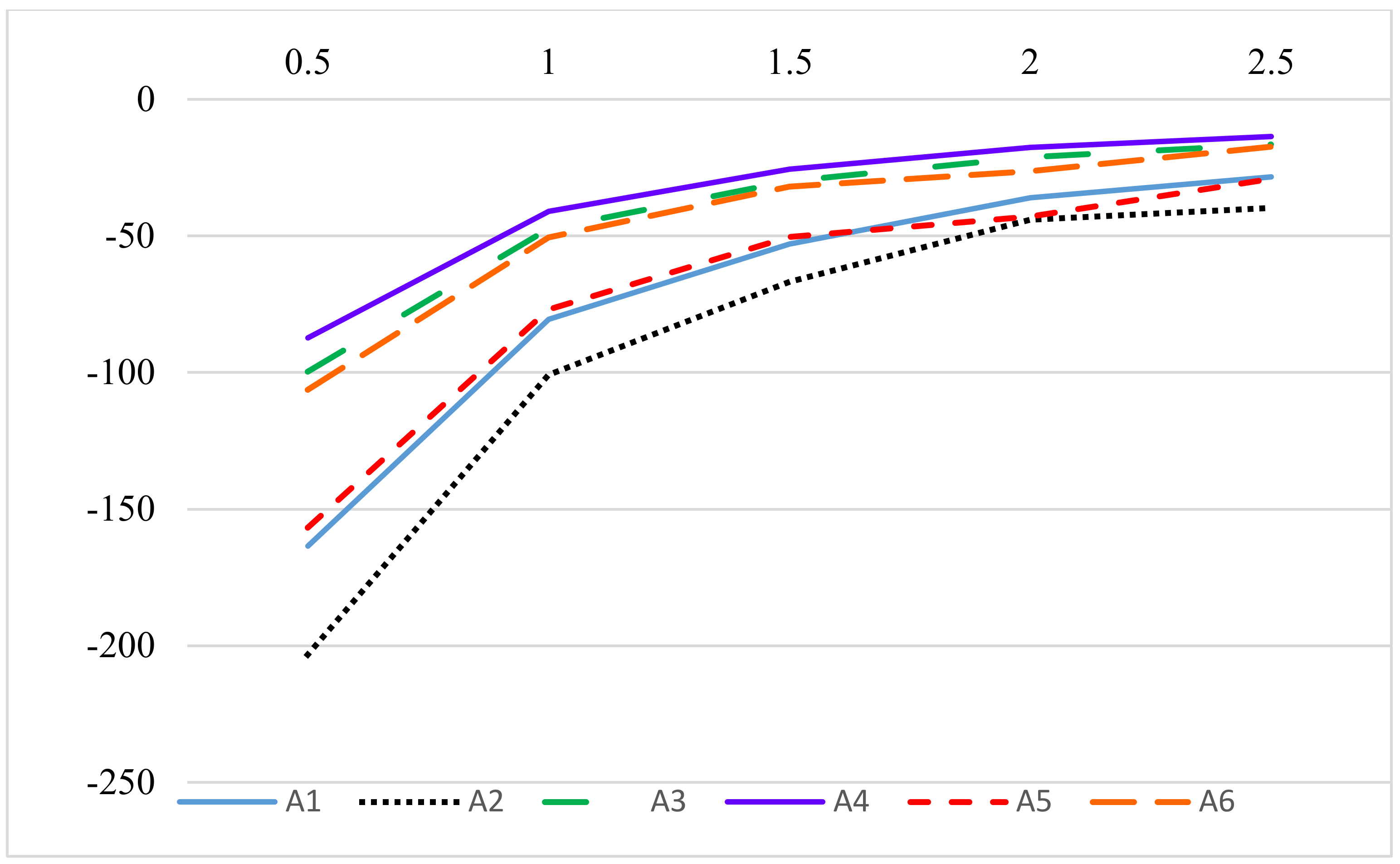

5.5. Sensitivity Analysis

In the existing studies, the two values

θ = 1 and

θ = 2.5 are used at the most [

30,

31]. The sensitivity analysis in this part sets the recession coefficients to 0.1, 0.5, 1, 1.5, 2, and 2.5 respectively. Then the overall dominance and ranking of each scheme is calculated (

Table 9).

According to

Figure 8, the smaller the value of θ, the higher the degree of evasion of the decision makers on the loss, the more sensitive to the loss, the smaller the overall dominance of the program; As the value of θ becomes larger, the gap between the overall dominance of the schemes becomes smaller; In addition, the value of θ will also affect the ranking of the scheme: Regardless of changes in the value of θ, scheme

A4 is always the optimal solution. However, it can be seen that the ranking results of schemes 1 and 2 have changed as the value changes from 1.5 to 2, which shows that the decision maker’s psychology will have an impact on the ranking result.

This part also further analyzes the sensitivity to verify the stability of decision results. Sensitivity analysis is made for parameters mentioned in

Appendix A part 3. We assumed that the project’s on-grid electricity is 30%, 50%, 70% respectively to make sensitivity analysis (

Table 10) and parameter a (the contracted revenue ratio) is set to 0.1, 0.3, 0.5, 0.7, 0.9 for sensitivity analysis (

Table 11). In addition, the share of subjective weight is set to 0.1, 0.3, 0.5, 0.7, 0.9 respectively (

Table 12).

The change of on-grid electricity can affect the economic change of the alternatives, but there is no change in the other aspects of the decision criteria system, which leads to no change in the final ranking results. That is to say, economy is only one of the important aspects of decision-making that is not able enough to change the results.

Similar to the situation in

Table 10, the final ranking results have not changed, and the economic changes in the alternative project lead to a slight change in the overall dominance, but not enough to change the results.

It can be seen that with the increase of the proportion of subjective weight, the ranking results of alternative projects have changed. The projects that rank second and third changed the order, and the ranking results of other projects did not change. This shows that the proportion of subjective and objective weight will have an impact on the ranking results. Its impact on the whole decision criteria is enough to influence the final ranking results to a certain extent.

5.6. Comparative Analysis

The results of comparative analysis using the TOPSIS method are shown in the following table. The ranking results obtained by the TOPSIS method is shown in

Table 13. It can be seen that the optimal alternative obtained by the TOPSIS is different from the TODIM method. Except the A4, the ranking results of other schemes are not very different besides the order exchange between the two ranking adjacent schemes. It’s worth noting that the ranking of scheme A4 changes from fourth to first. The TOPSIS method places more emphasis on the distance between alternative and best reference scenarios while the TODIM method focuses on the impact of the disadvantages of the alternatives in the decision making.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}