A Real Options Analysis for Renewable Energy Investment Decisions under China Carbon Trading Market

School of Economics and Management, North China Electric Power University, Beijing 102202, China

*

Author to whom correspondence should be addressed.

Energies 2018, 11(7), 1817; https://doi.org/10.3390/en11071817

Submission received: 11 June 2018

/

Revised: 5 July 2018

/

Accepted: 6 July 2018

/

Published: 11 July 2018

(This article belongs to the Special Issue Modeling and Simulation of Carbon Emission Related Issues)

Abstract

:Under the carbon trading mechanism, renewable energy projects can gain additional benefits through Chinese Certified Emission Reduction transactions. Due to the uncertainty of carbon trading system, carbon prices will fluctuate randomly, which will affect the investment timing of renewable energy projects. Thus, the value of the option will be generated. Therefore, renewable energy power generation project investment has the right of option. However, the traditional investment decision-making method can no longer meet the requirements of renewable energy investment in the current stage. In this paper, a real option model considering carbon price fluctuation is proposed as a tool for renewable energy investment. Considering optimal investment timing and carbon price, the model introduces a carbon price fluctuation as part of the optimization, studies the flexibility of enterprises’ delayed investment under the fluctuation of carbon price. A case study is carried out to verify the effectiveness of the proposed real option model by selecting a wind farm in North China. The model is expected to help investors to assess the volatility and risk of renewable energy projects more accurately, and help investors to make a complete plan for the project investment, thus promoting the efficient allocation of resources in the energy industry.

1. Introduction

With the increasingly global climate change, reducing greenhouse gas emissions, optimizing energy structure and decreasing fossil energy consumption have been one of the attentions of the world. The Paris Agreement points out that all sides should strengthen the global response to the threat of climate change. It involves holding on to a clear goal, in this case the 2C limit. China has participated in the cooperation of the climate problem actively, and made solemn commitment to reduce the greenhouse gas emission, that is a decrease in emissions intensity of around 40 percent to 45 percent between 2005 and 2020, at the Copenhagen conference in December 2009. In order to achieve saving energy and reducing emissions, the utilization of renewable energy has great potential for development. Therefore, the 13th Five-Year Plan proposed that the non-fossil energy contributes 15% of primary energy consumption. It is the request of achieving greenhouse gas emission reduction. It means a rare opportunity to invest in renewable energy for power enterprises.

In 2018, China has officially launched the national carbon trading market. As an instrument of policy, carbon trading market can promote the whole society to a low carbon transformation. It also will promote the development of clean energy power generation. Key emission units can reduce carbon emissions by developing clean energy such as photovoltaic and wind power. With the growing size of the market for carbon trading and the development of carbon trading mechanism, more and more enterprises involve in carbon trading. Enterprises will be more active in the use of clean energy, which promotes the development of the renewable energy. Accordingly, the establishment of carbon trading market also brings an opportunity for the investment of renewable energy power generation projects.

Furthermore, with the development of national economy, energy security problem has been an important indicator of future economic development of China. At present, the newly discovered fossil energy resources in China are basically located in remote areas or oceans, and the cost of mining is relatively high. Conversely, renewable energy has no threat of exhaustion, and it is not dependent on import. From the amount of renewable energy reserves in China, renewable energy has good resource conditions, its development potential is huge. Therefore, promoting large-scale investment of renewable energy by power generation enterprises is a feasible and effective measure to ensure China’s energy security.

Therefore, this topic is based on the above realistic background. This paper focuses more on the overall impact of the establishment of carbon trading market on renewable energy power generation projects and studies the optimal investment rule of power generation enterprises under carbon price fluctuation to provide useful reference for enterprise decision-makers and thus promoting renewable energy development, achieving national greenhouse gas emission reduction commitments and ensuring energy security supply.

In this paper, the structure of this paper is as follows. Section 1 introduces the background of the research. Section 2 summarizes the current research status at home and abroad. Section 3 constructs the real option model based on the fluctuation of carbon price and carries out the calculation. Section 4 selects the wind power field in North China for an empirical analysis. The research contents of this paper are summarized in Section 5.

2. Literature Review

2.1. The Generation of Real Option Theory

Net present value is a relatively scientific and relatively simple method of investment evaluation. It is suitable for a relatively stable market situation. However, due to the factors that it considers are simple and lack of reflection on future uncertainty, it is likely to underestimate the true value of investment projects. The volatility of carbon prices and the risk of renewable energy investment increased with the gradual maturity of the international carbon trading market and the establishment of China’s carbon trading market. The traditional investment decision method cannot comply with the trend. Therefore, we can minimize the risk of renewable energy investment projects by introducing the real option method. Real options method is an extension of financial options theory to real assets. The option pricing model was originally applied to asset appraisal in 1973 [1,2], and then applied to investment projects under uncertainty. Amram and Kulatilaka [3] and Copeland and Antikarov [4] evaluated high risk investment projects by Return on Assets, which including petroleum, aviation, medicine and other fields. Then, due to the investment flexibility of the real option method, it was soon applied to all walks of life [5,6].

2.2. The Application of Real Option Theory

At present, more and more foreign scholars begin to study the volatility of renewable energy investment projects caused by uncertainty. Kyeongseok Kim and Hyoungbae Park [7] put forward the corresponding real option model taking the developing countries as the research object. The model is put forward as a tool to evaluate the investment decision of renewable energy, which help investors to efficiently and accurately invest in projects with high carbon price and high risk. Bøckman et al. [8] selected the hydropower project in Norway as a case. The real option model is constructed, and the optimal scale and time of investment for hydropower projects are finally obtained. Kjærland [9] analyzed the potential project value of Norway under different point and different investment behavior, and quantified the value of the project through the construction of real option model, so as to determine the optimal investment behavior. Abadie and Chamorro [10] designed the real option model under the uncertain conditions and analyzed the influence of the three uncertainties including electricity price, electricity generation, and tariff subsidy policy on the investment value of British wind farm projects. Lee [11] demonstrated the effectiveness of the option model through applying real option model to wind power projects in Taiwan. It is found that the electricity price, the expiration time, the risk free interest rate, and the investment value of the project are proportional to the investment value. Martinez-Cesena and Mutale [12] designed a real option model suitable for small wind power projects. Kumbaroğlu et al. [13] proposed the renewable energy investment strategy based on dynamic programming model considering the uncertainty of renewable energy technology. Lena Kitzing and Nina Juul [14] proposed a real option model of wind energy investment to solve the optimal investment time point and optimal capacity.

At present, the research on renewable energy investment is mainly focused on feasibility evaluation and risk assessment. Mahdi Shahnazari and Adam McHugh [15] studied the comprehensive real option model under the interaction of carbon price and renewable portfolio standard (RPS) instruments. Casals [16] studied the feasibility of the renewable energy power generation project and analyzed its technical feasibility in meeting the stability reliability of the system and regional development planning. Ochoa [17] appraised the economic benefit of the renewable energy generation project, and proposed the evaluation model and multi-objective programming model of the economic benefit of the distributed generation. Rothwell [18] evaluated the risk of developing new nuclear power plants by means of real options, and simulated three uncertain factors: price risk, production risk, and cost risk. The risk premium was derived by Monte Carlo simulation. Fleten et al. [19] founded that the use of a random price real option method to analyze the investment of a power plant required a greater return, not just the return value of the traditional net present value balance point.

Domestic scholars are also concerned about the application of real option theory in renewable energy investment. Han Longxi [20] analyzed the opportunities and challenges facing the renewable energy industry in China through Clean Development Mechanism, and suggested that the renewable energy industry should take the lead in the integration of the domestic greenhouse gas emission reduction trading system, and explore the huge benefits of reducing emissions and increasing revenues by market means. Wang Jianbin [21] fully considered the reaction and influence of market participants to investment decision, established a dynamic model of power investment based on real option theory and game theory, and studied the dynamic decision-making problem of electric power project investors under uncertainty and market competition. Xu nuo [22] proposed two basic assumptions when building the mathematical model of power generation investment based on option game theory, that is, the decision-making behavior of the power generation investors in the market will affect each other. The change of load growth is the most important uncertainty factor in the decision-making of the power generation investors. Ren zhi min and Zeng Ming [23] built a non-cooperative game model of power generation investment decision under the condition of building up carbon price based on bidding principle of free competitive power generation market. Gong Piqin and Li Xinyang [24] studied the investment in renewable energy projects under the fluctuation of carbon price and calculated the NPV of three types of renewable energy project investment and its real option value (ROV). Hou Gang [25] and Zhu Zhenyu [26] studied the risk assessment of renewable energy projects, including the determination of risk factors and risk control strategies.

The main problems involved in the previous research are the application of real options model in different industries, the improvement of the evaluation methods of renewable energy projects and the impact of renewable energy technology on project investment. Through the analysis of previous studies, there is a method of cash flow to assess the impact of carbon prices on renewable energy investment, and also to use capacity constraints as a part of the optimization of renewable energy investment to carry out the real option analysis of carbon prices. However, there is a lack of a real option analysis of the dynamic planning and analysis of carbon prices for China’s renewable energy projects. Therefore, this paper attempts to provide an option model for the research of renewable energy investment in China by analyzing the impact of carbon price fluctuation on the investment of renewable energy projects.

On the basis of the above research work, assuming sustainability and scale stability of renewable energy projects the research will introduce the carbon price to build a mathematical model to solve the optimal solution of the carbon price of the renewable energy investment. The study of this paper will fill the gap of optimizing carbon price as an investment value.

3. Methodology

3.1. The Steps of Model for Investment Decisions for Renewable Energy Investment

Although the fixed tariff system provides the guarantee of higher electricity price and power generation capacity, investment in renewable energy generation projects will get CDM support with the fixed price cannot cover the renewable energy project investment and the cost of power generation enterprises. Then, enterprises will obtain carbon emissions subsidies. The uncertainty of carbon price will affect the Investment decision of renewable energy project. It is difficult for investors to accurately evaluate renewable energy investment projects.

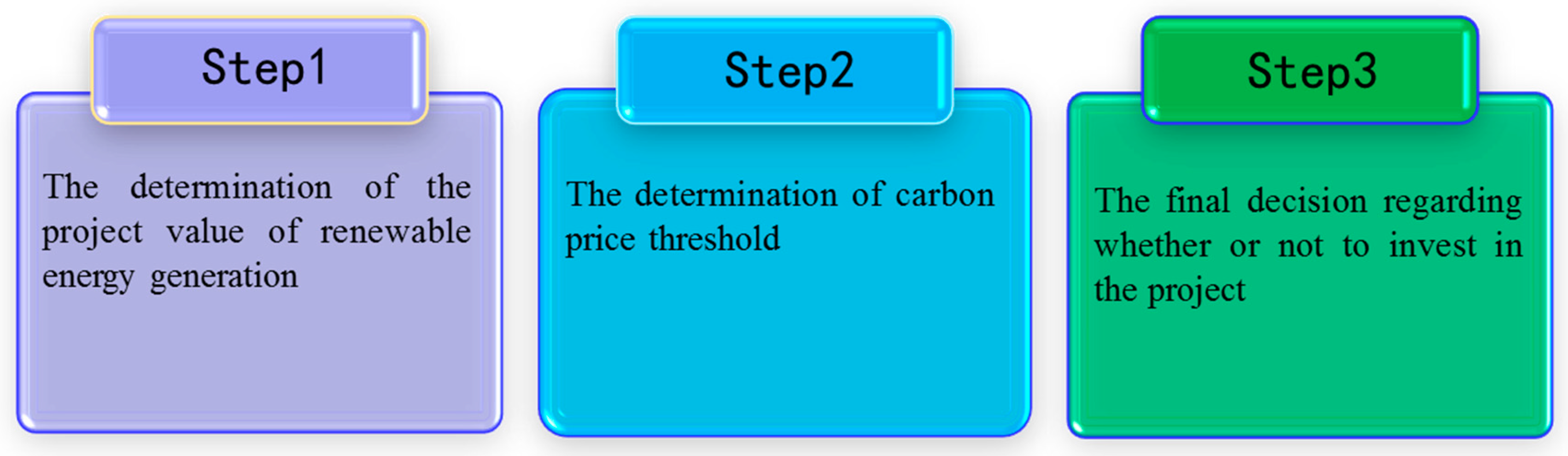

In order to solve these difficulties, this paper proposed a real option model for renewable energy projects. The model is divided into three steps, as shown in Figure 1: values confirmation, determination of carbon price threshold, and investment timing determining. Step 1 is the determination of the project value of renewable energy generation. In this step, the random fluctuation of carbon price is considered. Benefits of renewable energy projects include the revenue from certified emission reduction. Step 2 is the determination of carbon price threshold. The Brownian movement of carbon price is an important type of stochastic process. The uncertainty of the price of carbon produces the value of the option. In this step, the dynamic programming method and Bellman equation are introduced, and then Bellman equation and Ito lemma are used to introduce a famous irreversible investment model. Step 3 is to determine whether renewable energy projects will be invested.

3.2. Model

Considering the volatility of carbon prices and the flexibility of investment time points, the investment problem of renewable energy projects can be considered as a time-lasting real option problem. In regards to uncertainty, the carbon price () is assumed to be governed by a geometric Brownian motion (GBM) , where is the growth rate of carbon price, is the standard deviation of the growth rate, and and are the drift and volatility of the carbon price, and is a standard Brownian motion.

The operational gross margin is influenced by the electricity price (), unit generation cost (c), carbon price, and total output of renewable energy generation, all of which are combined in this single measure .

3.2.1. Value Confirmation

The profit of the renewable energy generation project is composed of two parts of the income of the electricity sales profit and the revenue of the reduced displacement approved by the sales CDM. For given [3], the value of the project refers to the expected discount value of gross profit of the project.

where is the gross profit of the project, and Q is the average production. I denotes investment cost. , C > 0. C refers to the investment cost of project unit output, which is related to the capacity of the project.

The discounted rate (r) refers to the interest rate that can be invested in a certain investment object without any risk. Where T denotes the life cycle of renewable energy generation projects and η denotes the conversion coefficient of certified emission reduction and generating capacity .

The project value of the renewable energy generation project is equal to the discount value of the project profit, and it is a function of the carbon price. The value of the project is:

where denotes the income of the electricity sales profit and denotes the revenue of the reduced displacement approved by the sales CDM, where is a compound index of the value of profit with the random fluctuation of carbon price.

3.2.2. Determination of Carbon Price Threshold

represents investment options for renewable energy projects due to the uncertainty of carbon price fluctuation. Bellman equation is [14]:

satisfies the dynamic programming equation. The ordinary differential equation is [21]:

, . The homogeneous part in the upper form indicates the delayed option value of the power generation enterprise postponing investment. The general solution to the ordinary differential equation is [21] , where and are the two roots of the quadratic equation. Where and are undetermined constant determined by boundary condition:

Since r 0, it is that . Also, since , it is that .

In order to obtain the threshold of carbon price, two conditions must be satisfied. First, if the carbon price is 0, then the option value is 0, then the investment of renewable energy projects will not be optimal. F = 0. . It thus follows that . Second, to determine , the value of the option and the value of the projects are analyzed: They should be equal at , moreover, both functions have the same slope (Smooth pasting condition).

Solving upper formula for , the investment thresholds are derived:

The value of option is determined as:

4. Case Study

4.1. Case Description and Sources of Data

In recent years, the power supply tends to be diversified, and the thermal power generation is becoming cleaner. The proportion of renewable energy is increasing obviously. In 2017, renewable energy accounted for 36.6% of the total installed capacity of China’s electricity industry and 26.4% of the total generating capacity [20]. Renewable energy investment has accounted for 85% of the total investment in the power sector. According to the “energy production and consumption revolutionary strategy (2016–2030)”, by 2030, the proportion of non-fossil energy generated by non-fossil energy, including nuclear energy and renewable energy, will strive to reach 50% of the total power generation [21].

This paper selected the operation of a wind farm in North China and applied the option model, and then solved carbon price threshold, investment time point and investment value by the option model. The source of funds for the project is free financing, and the rest is settled by financing. According to the conditions of wind energy, it is planned to install 33 units of wind turbines with an installed capacity of 49.5 MW, an average annual availability of 2500 h, and a unit generation cost of 0.0728 USD/kwh, with a project period of 20 years. The risk free interest rate R is 0.05 [24]. The electricity price of the Internet is 0.0823 USD/kwh [27]. Table 1 lists the specific data of the case.

is assumed to follow a GBM, it is that . The carbon price is estimated by drift α and volatility σ, and the two parameters are assumed to be constant, indicating that the randomness of carbon price will not change with time.

Carbon emission reduction coefficient is closely related to emission reduction standards, geographical distribution, and technological level. According to the data released by the climate division, the emission reduction coefficient of carbon dioxide in north China in 2015 is 1.0416 t /MWh [15].

Table 2 summarizes the environmental parameters.

4.2. Real Options Analysis

The seasonal changes were not taken into account in the model construction. It is assumed that renewable energy output is considered constant throughout the life cycle of the project.

According to the correlation coefficient of carbon price in the previous article, the Monte Carlo method is used to simulate the random fluctuation of carbon price. The number of simulation times is 100,000 times, and the carbon price threshold of the power generation enterprises under fixed net price is measured, which is 6.78 dollars/ton.

According to the seven major carbon trading market in China in the past year, the price range of quota price has narrowed year by year in the past two years. At present, the price of carbon emissions in Beijing is 4.5–8 dollars/ton, and Shenzhen’s carbon price is 3–5 dollars/ton [28].

According to the above information, the carbon price threshold of the wind power generation project is within the range of domestic carbon price fluctuations, indicating that wind power generation projects can gain revenue through carbon emission reduction transactions. The power generation companies will invest in wind power projects at the level of carbon price higher than 6.78 US dollars/ton.

According to the data of wind power project, the NPV of the wind power project is $330 million. Under the carbon trading mechanism, the investment value of the project with real option value is $460 million because of the uncertainty of carbon price. The total value of the project investment considering the option value is higher than that of the pure present value method. It shows that the renewable energy power generation project can be more comprehensive and flexible to measure the investment value of the project under the carbon trading mechanism.

4.3. Sensitivity Analysis

Sensitivity analysis, that is, using Monte Carlo method to iterate many times, to observe the impact of renewable energy investment options through variable changes. According to the results obtained above, the carbon price threshold of the wind power generation project is of practical significance. Therefore, the sensitivity analysis of carbon price fluctuation of wind power projects is carried out. The effects of carbon price growth rate and volatility of carbon price growth rate on carbon price threshold and investment option value are studied respectively while other parameters remain the same.

- (1)

- The relationship between carbon price growth rate and carbon price threshold and investment options

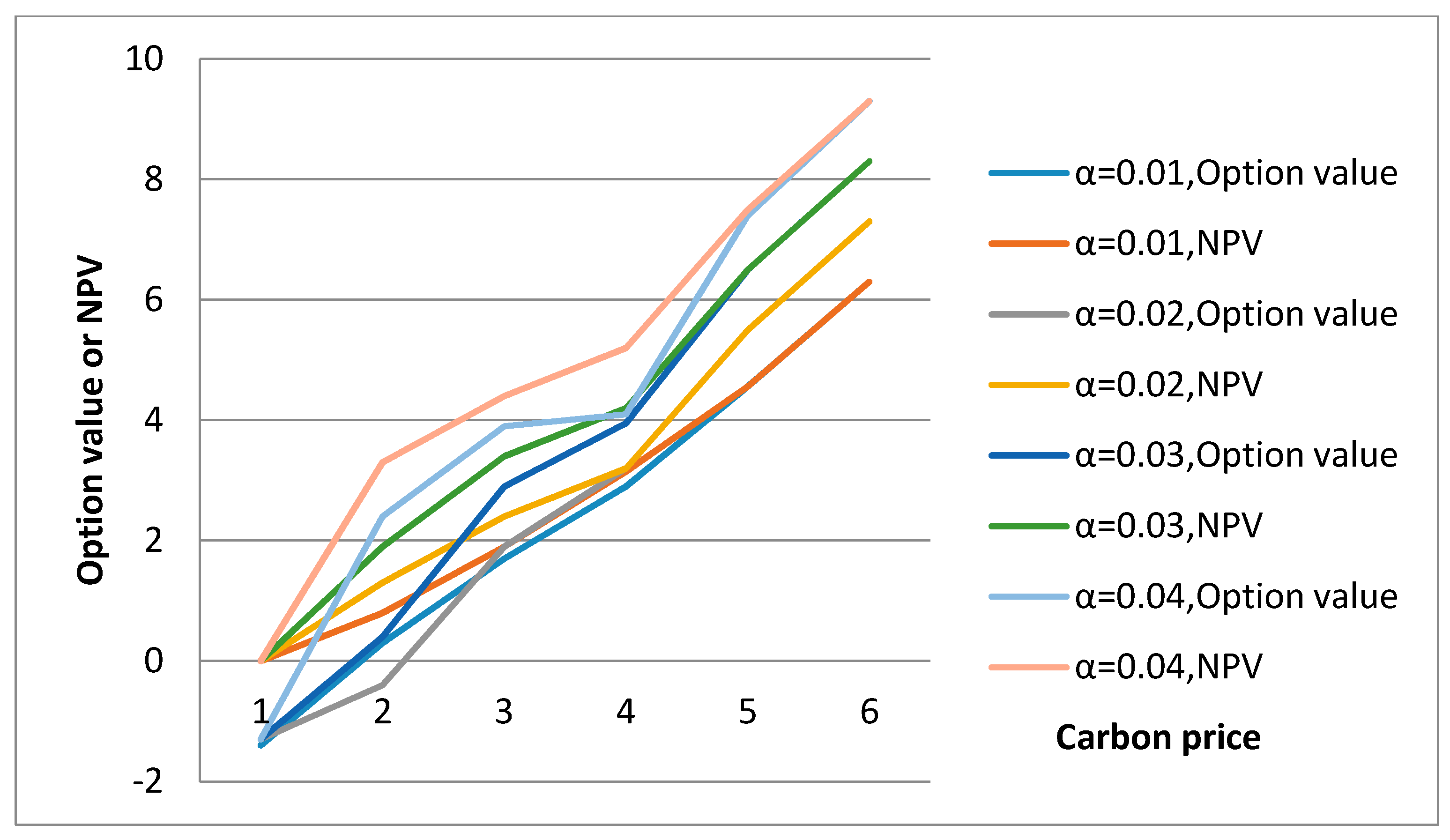

According to Figure 2, the investment option value of power generation enterprises is positively related to the growth rate of carbon price under the condition that other parameters remain unchanged. The higher the carbon price growth rate, the more inclined the power generation companies to wait for the delayed investment, and when the future carbon price reaches a higher level, the investment will get greater returns. However, with the expansion of the carbon emission market, the rate of carbon price growth will be reduced, and the power generation enterprises will invest earlier in the renewable energy generation projects.

- (2)

- The relationship between volatility of carbon price growth rate and carbon price threshold and investment options

As shown in Figure 3, the option value of the power generation enterprise is positively related to the volatility of the carbon price growth rate. This shows that the higher volatility of carbon price increases the value of enterprise investment options, but delays the investment time of enterprises. The reason is that higher volatility shows greater uncertainty, and power generation companies need to wait longer to determine whether the volatility of carbon prices is beneficial to investment. With the continuous improvement of China’s carbon trading system, the volatility of carbon prices will be further stabilized, and the volatility will be reduced, promoting the power generation enterprises to invest in renewable energy projects at a lower carbon price level.

5. Conclusions

The uncertainty of renewable energy investment comes from the volatility of the carbon trading market, the uncertainty of national policies, and the uncertainty of the environment, etc. This paper studies the uncertainty of the stochastic volatility of carbon price to the investment of renewable energy, so as to determine the optimal investment time and option value of renewable energy. The two objectives pursued in this study were: (1) the feasibility of renewable energy investment projects under the uncertainty of carbon price; and (2) the variation of the carbon price threshold was revealed. In order to achieve these two objectives, this paper proposed a real option model considering carbon price fluctuation as a tool to evaluate the investment of renewable energy projects.

A real option model of renewable energy generation investment under the current benchmark electricity price system was constructed. The numerical simulation and sensitivity test of the model were carried out by the Monte-Carlo method. This paper discussed the feasibility of investing in wind power projects under the current net electricity price level in China, analyzed the investment opportunity of the investment in the renewable energy project of wind power generation and revealed the change law of the value of the carbon price gap with the related parameters.

In this paper, a real option model was verified by selecting a case of a wind farm project. The research has somewhat practical significance. Sensitivity analysis was to determine the impact of stochastic characteristics of carbon prices on project value. According to the sensitivity analysis of wind power data, this paper concluded that the higher the rate of carbon price growth and the higher the fluctuation level, the more the power generation enterprises tend to postpone the investment, and these factors have a very significant impact on the return of the enterprise investment.

The future uncertain world carbon trading system will inevitably aggravate the fluctuation of carbon prices. The future research on investment in renewable energy projects will tend to further quantify the uncertainty of projects, which can better control of the high risk of project investment. The uncertainty of the project includes changes in government policies, climate changes, and changes in technology levels. In the construction of real option model, if more scenarios are designed and more detailed data analysis method is adopted, it will be more accurate to analyze the change in investment value of project uncertainty.

Author Contributions

Conceptualization, Methodology: M.W. carried out a real options model in a realistic and easily applicable way as a tool to assess renewable energy investment. Y.L. carried out a general design of the article. Z.L. contributed much in the revised version of our manuscript.

Funding

This research was financed by “Natural Science Foundation of China Project” (Grant No. 71471058), Beijing social science foundation research base project (Grant No. 17JDGLA009).

Acknowledgments

The authors thank the anonymous reviewers for careful reading and many helpful suggestions to improve the presentation of this paper. The authors thanks the anonymous referees for careful reading and many helpful suggestions to improve the presentation of this paper. This paper is supported by “Natural Science Foundation of China Project” (Grant No. 71471058), Beijing social science foundation research base project (Grant No. 17JDGLA009).

Conflicts of Interest

The authors declare that they have no competing interests.

References

- Black, F.; Scholes, M. The pricing of options and corporate liabilities. J. Political Econ. 1973, 81, 637–654. [Google Scholar] [CrossRef]

- Merton, R. An intertemporal capital asset pricing model. Econometric 1973, 41, 867–887. [Google Scholar] [CrossRef]

- Amram, M.; Kulatilaka, N. Real Options; Harvard Business School Press: Boston, MA, USA, 1999. [Google Scholar]

- Copeland, T.E.; Antikarov, V. Real Options: A Practitioner’s Guide; Texere: New York, NY, USA, 2003. [Google Scholar]

- Arrow, K.J.; Fisher, A.C. Environmental preservation, uncertainty, and irreversibility. Q. J. Econ. 1974, 88, 312–319. [Google Scholar] [CrossRef]

- Henry, C. Investment decisions under uncertainty: The irreversibility effect. Am. Econ. Rev. 1974, 64, 1006–1012. [Google Scholar]

- Kim, K.; Park, H. Real options analysis for renewable energy investment decisions in developing countries. Renew. Sustain. Energy Rev. 2017, 75, 918–926. [Google Scholar] [CrossRef]

- Bøckman, T.; Fleten, S.-E.; Juliussen, E.; Langhammer, H.J.; Revdal, I. Investment timing and optimal capacity choice for small hydropower projects. Eur. J. Oper. Res. 2008, 190, 255–267. [Google Scholar] [CrossRef] [Green Version]

- Kjærland, F. A real option analysis of investments in hydropower—The case of Norway. Energy Policy 2007, 35, 5901–5908. [Google Scholar] [CrossRef]

- Abadie, L.M.; Chamorro, J.M. Valuation of wind energy projects: A real options approach. Energies 2014, 7, 3218–3255. [Google Scholar] [CrossRef]

- Lee, S.-C. Using real option analysis for highly uncertain technology investments: The case of wind energy technology. Renew. Sustain. Energy Rev. 2011, 15, 4443–4450. [Google Scholar] [CrossRef]

- Martinez-Cesena, E.A.; Mutale, J. Wind power projects planning considering real options for the wind resource assessment. IEEE Trans. Sustain. Energy 2012, 3, 158–166. [Google Scholar] [CrossRef]

- Venetsanos, K.; Angelopoulou, P.; Tsoutsos, T. Renewable energy sources project appraisal under uncertainty: The case of wind energy exploitation within a changing energy market environment. Energy Policy 2002, 30, 293–307. [Google Scholar] [CrossRef]

- Kitzing, L.; Juul, N. A real options approach to analyze wind energy investments under different support schemes. Appl. Energy 2017, 188, 83–96. [Google Scholar] [CrossRef]

- Shahnazari, M.; McHugh, A. Overlapping carbon pricing and renewable support schemes under political uncertainty: Global lessons from an Australian case study. Appl. Energy 2017, 200, 237–248. [Google Scholar] [CrossRef]

- Casals, X. Technical and economic analysis on the introduction of a high percentage of renewable energy in the Spanish energy system. In Proceedings of the ISES Solar World Congress 2007: Solar Energy and Human Settlement, Beijing, China, 18–21 September 2007. [Google Scholar]

- Ochoa, L. Evaluating distributed generation impacts with a multiobjective index. IEEE Trans. Power Deliv. 2006, 21, 1452–1458. [Google Scholar] [CrossRef]

- Rothwell, G.A. A real options approach to evaluating new nuclear power plants. Energy J. 2006, 27, 37–53. [Google Scholar] [CrossRef]

- Fleten, S.; Maribu, K.; Wangensteen, I. Optimal investment strategies in decentralized renewable power generation under uncertainty. Energy 2007, 32, 803–815. [Google Scholar] [CrossRef] [Green Version]

- Han, L.; Zhai, J.; Zhang, L. The challenges and opportunities of China’s greenhouse gas emission trading on renewable energy. Ecol. Econ. 2015, 31, 31–35. [Google Scholar]

- Wang, J. A dynamic modeling of investments in power generation based on real option theory and game theory. Trans. China Electrotech. Soc. 2007, 22, 163–167. [Google Scholar]

- Xu, N.; Wen, F.; Huang, M. An option-game based approach for generation investment decision-making. Autom. Electr. Power Syst. 2007, 31, 25–30. [Google Scholar]

- Ren, Z.; Zeng, M.; Li, C. Investment decision-making of renewable energy generation with increasing of carbon price. Water Resour. Power 2015, 33, 211–215. [Google Scholar]

- Gong, P.; Li, X. Study on the investment value and investment opportunity of renewable energies under the carbon trading system. China Popul. Resour. Environ. 2017, 27, 22–29. [Google Scholar] [CrossRef]

- Hou, G. Research on the Risk Evaluation and Management of Biomass Energy in China; Northwest Agriculture & Forestry University: Yangling, China, 2009; pp. 43–76. [Google Scholar]

- Zhu, Z. Decision on Investment Risks of solar Photovoltaic Industry in China; China University of Geosciences: Beijing, China, 2010; pp. 83–96. [Google Scholar]

- Polaris Power Network Database. 2017. Available online: http://news.bjx.com.cn/html/20170420/821314.shtml (accessed on 5 May 2018).

- Carbon Emissions Trading Database. 2017. Available online: http://www.tanpaifang.com/ (accessed on 5 May 2018).

Figure 1.

The steps of model for investment decisions for renewable energy projects.

Figure 2.

The relationship between F, Net Present Value and .

Figure 3.

The relationship between F, Net Present Value and σ.

{kind=link}

{kind=link}

{kind=link}

Table 1.

Summary of input parameters in the case study.

| Items | Symbols | Values |

|---|---|---|

| Upper generator capacity | q | 49.5 MW |

| Total project cost | I | 39.17 million USD |

| Concession period | T | 20 Years |

| Annual average production | Q | 1947.72 USD kwh |

| Variable investment cost | C | 0.0728 USD/kwh |

Table 2.

Environmental parameters.

| Items | Symbols | Values |

|---|---|---|

| Risk-free rate interest rate | r | 0.05 |

| Electricity tariff | 0.0823 USD/kwh | |

| Conversion coefficient | 1.0416 t CO2/MWh | |

| The growth rate of carbon price | 0.02 | |

| The standard deviation of | 0.10 |

© 2018 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Li, Y.; Wu, M.; Li, Z. A Real Options Analysis for Renewable Energy Investment Decisions under China Carbon Trading Market. Energies 2018, 11, 1817. https://doi.org/10.3390/en11071817

AMA Style

Li Y, Wu M, Li Z. A Real Options Analysis for Renewable Energy Investment Decisions under China Carbon Trading Market. Energies. 2018; 11(7):1817. https://doi.org/10.3390/en11071817

Chicago/Turabian StyleLi, Yanbin, Min Wu, and Zhen Li. 2018. "A Real Options Analysis for Renewable Energy Investment Decisions under China Carbon Trading Market" Energies 11, no. 7: 1817. https://doi.org/10.3390/en11071817

Note that from the first issue of 2016, this journal uses article numbers instead of page numbers. See further details here.