The Role of Distributed Energy Resources and Associated Business Models in the Decentralised Energy Transition: A Review

1

Curtin Sustainability Policy Institute, Curtin University, Bentley 6102, Australia

2

University of Adelaide, Adelaide 5005, Australia

*

Author to whom correspondence should be addressed.

Energies 2023, 16(10), 4231; https://doi.org/10.3390/en16104231

Submission received: 24 December 2022

/

Revised: 11 May 2023

/

Accepted: 12 May 2023

/

Published: 21 May 2023

(This article belongs to the Topic Distributed Energy Systems and Resources)

Abstract

:The shift from large-scale centralised energy systems to smaller scale decentralised systems based on Distributed Energy Resources (DER) is likely to cause a sector-wide replacement of current electricity management practices and business models—creating a new energy paradigm. If handled well, such a transition will not be inherently disruptive; however, it can cause major disruption if long-held views and assumptions are not rapidly reconsidered and renewed, and new supporting structures are not swiftly put in place—hence, if disruption is experienced it will be due to a lack of strategic responses rather than the nature of the technology. This paper clarifies the nature of DERs and outlines key issues and opportunities associated with a range of associated service configurations and business models. The paper outlines key factors affecting the viability of such approaches and identifies leverage points for accelerating uptake. The paper concludes by considering how shifting landscape factors and related opportunities in the coming decades will shape the transition to a decentralised energy system. This paper contains findings from research performed at the Renewable, Affordable, Clean Energy Cooperative Research Centre (RACE CRC) in Australia.

1. Introduction

As part of the transition from a centralised, fossil-fuel-based energy system to a decentralised, net-zero emissions system, electricity networks are now using a range of new forms of energy generation and storage that need to be integrated into established systems [1]. Options for renewable energy generation (such as solar PV and wind turbines) allow for smaller dispersed sites that are focused on meeting relatively local demand rather than being centrally located in extensive transmission and distribution networks. The economics of such systems is encountering a significant increase in the number of small- and medium-sized energy generators dispersed across the electricity system, which are classified as ‘Distributed Energy Resources’ or DERs [2].

These distributed forms of renewable energy generation provide a cost-effective source of electricity; however, intermittency needs to be managed through the use of energy storage and smart loads (controllable loads that can be switched on or off as needed to stabilise demand–supply operations) [3]. A range of energy storage types and various forms of smart loads are being used in electricity systems worldwide, including in Australia, USA, and Europe [4,5,6]. Such DER solutions are uniquely able to match local electricity generation with demands while accommodating variable electricity-use behaviour within associated governing policies and tariff structures.

A combination of factors needs to be considered when developing business models to facilitate DER uptake, operation, and maintenance [7]. These include incumbent utility practices; government planning and policies; system operator constraints and preferences; consumer behaviour; investment criteria; economic factors; environmental considerations; and social equity issues [8]. The transition to a DER-dominated energy system is being slowed by incumbents seeking to maintain the status quo, while also being driven by early adopters keen to take advantage of the new system. Hence, it is typical for governments to receive mixed signals for action, which can slow updates to crucial policies needed to facilitate the new options, causing mounting anxiety for the system [9].

Along with the need to upgrade infrastructure and update policies and regulatory frameworks, a further complicating factor is that energy consumers are now seeing themselves as energy producers keen to secure cheaper energy costs. These ‘prosumers’ present a challenge to existing energy markets accustomed to a limited number of energy generation sites and well-established customer relations. This new class of energy entity is changing the face of the sector with the proliferation of small and micro energy generation and storage sites across traditionally centralised energy networks. This is creating both challenges and opportunities for those that seek to prepare the energy system for such a transition [1].

This paper introduces various types of DERs and clarifies terminology used for their configuration within energy systems, and then presents and discusses combinations of DERs that together form new business models. The resulting business models are then presented and discussed for their influences, attributes, and impacts. This review uses papers and literature from 2002 onwards, which progressively describe increasingly developed system processes with newer literature. The review was performed using the strategic literature review principles. It does not follow PRISMA in full detail, because the research focuses on industry practice-orientated projects, but rather as a purely academic exercise.

2. Types of Distributed Energy Resources and Configurations

The world is increasingly recognising the potential for Distributed Energy Resources (DERs) to reduce costs associated with a shift towards a clean and reliable electricity grid, as well as creating a growing number of new ways to generate revenue, both for traditional and new business and parties [10]. However, this transition is proving difficult in the early stages as the new business cases are not yet properly understood and involve a number of factors that are not informed by periods of precedent [11,12,13,14]. At their core, such business cases include the combination of a number of DER options for energy generation and storage with appropriate business models, with types of DERs [11] including:

- Solar Photovoltaic Panels (rooftop PV);

- Wind Turbines (both small scale for urban applications and large scale for rural and offshore applications);

- Battery (Chemical) Energy Storage (at a range of scales from household storage to transmission grid storage);

- Thermal Energy Storage;

- Electric Vehicles (storage capacities ranging from 65 kWh to 150 kWh for passenger vehicles and 250kWh to 500 kWh for buses and other large vehicles);

- Co-Generation and Tri-Generation Units;

- Biomass Energy Generators;

- Open- and Closed-Cycle Gas Turbines;

- Diesel and Gasoline Generators;

- Hydroelectric Generators and Storage;

- Fuel Cells.

As a result of the rapid uptake of many of these types of technologies—particularly solar photovoltaics and wind turbines—there is new potential to develop viable business models, for both the incumbent and new electricity system participants that harness DERs. Such business models will involve a range of customers, including regulated utility customers; commercial, institutional, and municipal organisations; and DER technology and service providers. New DER business cases are developing in a number of themes [8], including:

- Individual Distributed Energy Generation (such as private rooftop solar that supplies residential homes or commercial buildings);

- Aggregated Distributed Energy Generation (both co-located in physical precincts and virtually across various locations);

- Distributed Energy Storage (such as batteries or electric vehicles storing excess renewable energy for use during evening peak periods, and back-up power);

- Aggregated Distributed Energy Storage (both co-located and across various locations to provide energy supply, frequency control, and ancillary services).

This report provides a structure (in the form of a taxonomy) to explore specific DER business cases and compare them to current and perceived future landscape conditions. The intention is to better inform those entering the DER field and assist regulators, utilities, and retailers to navigate these changing conditions.

3. Terminology Related to Distributed Energy Resources

With the rise of clean, renewable, and affordable small-scale energy generation and storage technologies (such as rooftop solar panels and batteries), electricity system operation models are shifting away from centralised generation delivered to customers through a distribution network [15,16]. Previous energy generation technology, such as coal-fired power stations, presented environmental, health, and safety risks and should not be co-located with communities, and hence needed to be located away from consumers [17]. The more recent proliferation of clean, small-scale, nonfossil-fuel-based technologies enables more electricity to be generated locally safely (and quietly) and stored locally, which will cause fundamental changes to physical infrastructure and services across the grid. In the early stages of understanding the implications of this shift, the focus has been on the distinction between ‘centralised’ and ‘decentralised’ energy generation and storage options as shown in Figure 1 [18,19], where:

- A ‘Centralised’ system involves a minimum number of large-scale energy generation options that are used to supply the majority of electricity needs across the grid, such as a large coal-fired power plant supplemented with gas turbines to meet varying demand.

- A ‘Decentralised’ system involves a number of small- to medium-scale energy generation and storage options, such as standalone gas turbines, wind farms, battery storage, hydroenergy storage, and solar arrays, which are located at various points in the electricity network and can be aggregated to deliver services such as Virtual Power Plants (VPP) [19].

Despite this distinction explaining the shift away from a centralised electricity grid dominated by fossil-fuel generation, further classification is needed to begin exploring the various types of business models that will be viable in a decentralised system. Important distinctions in electricity management systems are those in which energy assets are situated in a distribution network for consideration of control and authority [20].

- ‘Front-of-Meter’ (FoM): Assets-situated FoM in distribution networks are the responsibility of Distributed Network Service Providers (DNSP) and the stakeholders involved in facilitating the asset and resource, such as a community battery being owned and operated by DNSPs and municipalities [21].

- Behind-the-Meter (BtM): Conversely, assets-situated BtM are the responsibility of the particular metered customer and are located onsite. BtM DERs can interact with distribution and transmission networks under appropriate agreements to provide energy arbitrage and Frequency Control and Ancillary Services (FCAS) [22,23]. The physical distinction between FoM and BtM is outlined in Figure 2 [23].

It is likely that a combination of the two options will provide the most efficient and affordable option for electricity supply to cities around the world, requiring the development of new and appropriate business cases. Despite historical monopolies by distributers and electricity providers, electricity service roles will need to be re-envisioned over time as more energy is generated, stored, and used behind meters. A key element of this transition will be the balance between over-sizing local equipment to meet peak periods and relying on grid electricity to ensure reliability [24], namely [25,26]:

- Over-sizing: If an over-sizing approach is taken, this will result in over-investment as onsite technology is sized to eliminate the need for connection to the grid. However, a level of over-sizing can provide a revenue stream with electricity generation excess to local demands being sold to the grid at strategic times.

- Right-sizing: If a right-sizing approach is taken, then this will result in onsite investment being matched to most local needs with a service provision relationship formed with the grid to ensure reliability.

It is likely that in the early stages of the transition to DERs there will be greater demand for excess generation, which may lead to over-sizing; however, as DERs proliferate and the cost of onsite energy storage declines, there will likely be diminishing demand for purchasing excess from others and onsite systems will trend towards being right-sized [27].

4. Taxonomy for DER Business Cases

4.1. Elements of a DER Business Case

Traditionally, the approach used in the energy sector for the provision of electricity has been based on a form of large-scale and dispatchable centralised electricity generation—typically fossil-fuel based—that does not include energy storage and exports electricity to the transmission grid. With the advent of small-scale and cost-effective clean electricity generation and storage options, this centralised model is being disrupted, and requiring a number of new approaches both for business models and governance arrangements [28,29]. As the following section shows, the shift to decentralised energy generation and storage will create a range of new business opportunities, which will each warrant careful consideration as to how they can be implemented and supported.

The transition to a system dominated by distributed energy resources will require new business models, business types, regulatory controls, finance models, and training [30]. Previous revenue models based on direct sales to customers will need to make way for new models that include processes for direct sales, equipment installation and maintenance, storage, various opportunities for energy systems consultants (i.e., intermediaries between generation and storage, and consortiums and purchase advisors), Frequency Control Ancillary Services (FCAS), and cybersecurity for integrated smart systems [31]. There will be a need for a comprehensive review of the energy regulatory ecosystem as the transition to decentralisation continues [32]. In this new multivariate energy ecosystem, it is not entirely clear what rules are needed and who should decide on them and enforce them [33]. The continued innovation of energy generation and storage technologies that are presenting new revenue-raising opportunities are not only a disruption to the status quo, but a major opportunity for those who act early in the transition.

To provide a structure for investigation, it is assumed that a DER business case can be created through the combination of two elements, namely a ‘DER Service Configuration’ and a ‘Business Model’. The following section provides taxonomy for both the service configuration of DERs and of associated business models. This research has identified sixteen ‘DER Service Configurations’ and has selected seven ‘Business Models’, with some service configurations appropriate for more than one business model.

A DER business case can be described as:

DER Business Case = DER Service Configuration + Business Model

4.2. Types of DER Service Configurations

To provide clarity around the specific application of distributed energy resources, a framework, described below, has been created with a focus on the physical fundamentals of distributed energy systems: electricity generation, electricity storage, and electricity usage and final sale [34,35]. As can be seen from Table 1, the combination of options creates 16 unique DER service configurations. Although this list is not exhaustive, it does present the core configurations [8,36,37].

- 1.

- Where is the electricity generated?

- (a)

- No electricity generation (can only receive energy via the grid).

- (b)

- A dedicated facility on a site with no demand (such as a wind/solar farm).

- (c)

- An individual site with demand and excess production (such as a household).

- (d)

- A cluster of sites with demand and excess production (such as a microgrid or VPP).

- 2.

- Where is the electricity stored?

- (e)

- Stored onsite (such as in batteries in the building or as part of the microgrid).

- (f)

- No storage option (can only sell at time of generation).

- 3.

- Where is the electricity used/sold?

- (g)

- Used and sold to onsite demand (such as using rooftop solar in the building it is located on).

- (h)

- Used and sold to ongrid demand (such a feed-in tariff or virtual power plant arrangement).

Using these three levels of service options creates a set of 16 configurations, as shown in Table 1.

Hence, using the potential combinations presented in Table 1, the following ‘DER Service Configurations’ can be made:

- Local Big Storage: An energy storage facility that sources electricity from the grid for local use.

- Grid Big Storage: An energy storage facility that buys and sells electricity from the grid.

- Local Energy Farm: A dedicated generation facility with onsite storage that produces excess for the grid.

- Grid Energy Farm: A dedicated generation facility with onsite storage that only sells to the grid.

- Local Solar Only: An individual generator with no storage that uses electricity onsite.

- Grid Solar Only: An individual generator with no storage that produces excess for the grid.

- Local Solar + Storage: An individual generator with onsite storage that primarily uses electricity onsite.

- Grid Solar + Storage: An individual generator with onsite storage that produces excess for the grid.

- Local Microgrid: A physical cluster of generators with no storage that uses electricity onsite.

- Grid Microgrid: A physical cluster of generators with no storage that produces excess for the grid.

- Local Micro + Storage: A physical cluster of generators with onsite storage that uses electricity onsite.

- Grid Micro + Storage: A physical cluster of generators with no storage that produces excess for the grid.

- Local VPP Only: A virtual cluster of generators with no storage that primarily uses electricity onsite.

- Grid VPP Only: A virtual cluster of generators with no storage that produces excess for the grid.

- Local VPP + Storage: A virtual cluster of generators with onsite storage that uses electricity onsite.

- Grid VPP + Storage: A virtual cluster of generators with onsite storage that produces excess for the grid.

4.3. Types of DER Business Models

Each of these service configurations can generate revenue in a range of ways, such as in the following business models [8,38,39,40,41,42,43,44], namely:

- Product: This involves the sale of a tangible item that has value to a customer (such as selling electricity from the distribution network to a household customer).

- Service: The provision of assistance for a fee, which may involve servicing physical equipment or software (such as selling the service of frequency control and ancillary services).

- Shared Assets: This involves customers paying for the privilege to use a shared asset in which volume and quality need to be balanced (such as a community battery).

- Subscription: This involves users paying a recurring fee for access to benefits (such as a utility-owned solar panel on a residential building).

- Lease/Rental: This involves leasing an asset for a discrete period of time for an agreed fee (such as leasing a portable battery storage device).

- Reselling: This involves purchasing of a product or asset to on-sell for a premium (such as buying electricity wholesale from the grid to then sell to industrial precinct tenants).

- Agency/Promotion: This involves fee-based marketing of an asset that is not owned for ensuring the generation of transactions (such as the use of a shared battery).

Hence, for each service configuration, as appropriate, there may be the potential for applying up to seven business models for revenue generation. This presents a long list of business cases to choose from; the next section provides an initial way to short-list such cases.

5. Key Factors Affecting Viability of DERs

For the purpose of this paper, rather than outline the possible combinations of the application for each of the business models to each of the service configurations, we identify specific service configurations that have high value potential, should the associated business models be implemented. In order to consider the relative value of each service configuration and associated barriers, the following categories have been selected:

- Scale: When considering the installation of DERs across the energy grid, an important aspect is scale, in particular the relative size of DERs at specific locations. For example, a higher number of small energy storage options spread across a network area may provide greater levels of system reliability compared to a lower number of larger storage resources with equivalent capacity. This then becomes a barrier if the current regulatory environment does not afford small- to medium-scale DERs the same rights as is offered to larger scale options [45,46].

- Grid Capacity: A barrier to the installation of DERs—especially a combination of DERs on a single site—can be the capacity of the infrastructure connecting the site to the electricity grid. For example, a large commercial rooftop solar array may not be able to export its intended level of generation if the grid cannot accommodate it at that point. So, to enable export to the grid there may be a need to upgrade infrastructure. It is not clear who is responsible for the cost of this; however, it is often applied to the site rather than the grid operator [47].

- Hybridisation: It is often the case that a single site will install a number of types of DER behind the meter in order to take advantage of both energy generation and storage opportunities [48]. Such an approach provides the potential for better utilisation of the connection to the network, allowing greater functionality; however, it presents a challenge to regulators who currently find it difficult to register and value such ‘hybrid’ systems due to lack of visibility behind the meter [49].

- Control: Owing to the emergent nature of DERs and the risks associated with a lack of appropriate control, there is hesitancy to recognise nontraditional methods of control, such as solid-state systems, which are often cheaper and offer greater functionality. This often leads to a new DER system with modern control methods being treated as being ‘uncontrolled’ and not rewarding the ability for controllability. One element of this hesitancy is the lack of trust in electronic controls over traditional physical controls, given that they can be reprogrammed remotely, and hence may introduce risk into the control of the system compared to a physical switch or breaker. It is also unclear how owners or DERs—both residential and commercial—will respond to control methods that are intended to enhance the functioning of the grid [48,50,51].

- Aggregation: The decentralised nature of DERs calls for new forms of management with the role of an ‘aggregator’ likely to be required to manage a grid of grids. An aggregator provides a single point of contact for a group of DERs in order to interact with the grid and associated energy markets. Effectively, an aggregator can act as a broker between such a group and energy utilities, pooling the utility of a group of smaller DERs to act as a larger combined entity. Given that the decentralisation of the energy sector is in its early stages, this role is yet to be acknowledged and supported. However, they will likely play a critical role in bringing trust and control to distributed systems, requiring a review of current regulations and other restrictions that are hindering such efforts [52,53,54].

How these factors and associated barriers relate to DER service configurations is shown in Table 2.

6. Landscape Conditions Affecting DER Business Cases

6.1. Overview of Landscape Conditions

To complement the consideration of current barriers to the implementation of specific high-value DER service configurations and business models, overarching landscape conditions and their influence through time need to be considered [33]. For instance, as the transition to a decentralised energy system progresses—mainly due to customer purchasing [55]—it is likely that government support will increase to involve revisions and updates to existing policy positions, regulatory frameworks, and fiscal policies [56]. It is likely that there will be a reduced level of resistance through time from incumbents that stand to benefit from prolonging the centralised fossil-fuel-based system, as either their ability to influence decreases or they begin to transition and integrate themselves into the new system [57]. An example in Western Australia where Perth is part of the world’s largest, most isolated electricity grid (spanning 7750 km of transmission lines and 93,350 km of distribution lines). It is undergoing a rapid transition to a more distributed system as rooftop solar is replacing conventional centralised fossil fuels in the grid. Over 40 percent of households in this grid have rooftop behind-the-meter solar systems, totalling 1700 MW of generation power. The ability for grid generation varies throughout the periods of days and seasons, and hence there are some scenarios where this system takes 70 percent of its generation power from the solar energy generated by these distributed rooftop systems. This grid is in a transitioning stage, as it is dependent on conventional centralised generators amongst the varying solar power [53,58,59].

The transition to a decentralised grid may take decades and hence it is likely that different business cases will be appropriate at different times [60]. For instance, a business case based on the generation of excess solar energy for sale to the grid may have diminishing returns as the uptake of solar and local energy storage increases, reducing the demand for excess onsite generation. For better management, a distinction must be made between landscape conditions that are either in front of or behind the meter [61,62]. For example, a key landscape condition behind the meter will be consumer choice and the rate at which consumers—both residential and commercial—purchase local energy generation and storage equipment, with forecasts sometimes under-estimating or inaccurate [63].

Landscape factors that stand to affect the viability of DER business cases in front of the meter include [60,64]:

- Availability and maturity of technology—both hardware and software (likely to increase);

- Cost of technology (likely to decrease);

- The marginal cost of energy generation (likely to decrease as part of the shift to small, local, and renewable options);

- Level of government financial support (likely to increase as DER deployment continues to increase);

- Level of policy and regulatory change (likely to increase; however, likely to be slower than financing);

- Incumbent resistance (likely to ramp-up in short term then reduce over time);

- Level of overall support and political will (likely to increase as more investment is made in DERs).

Landscape factors that stand to affect the viability of DER business cases behind the meter include [65,66]:

- The ad hoc manner in which consumers will continue to drive the uptake of a range of DERs in the short term, such as rooftop solar.

- The likely shift to greater electrification of homes and businesses to take advantage of local energy generation.

6.2. Considering a Spectrum of DER Opportunities

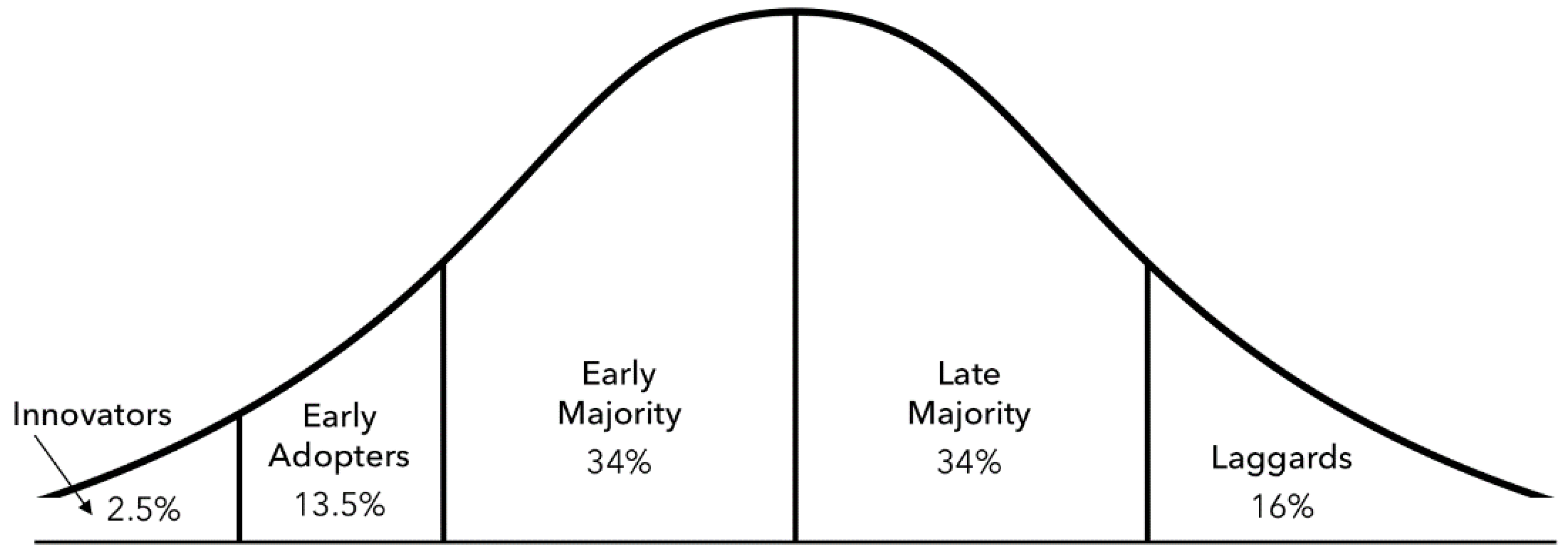

Given the many and varied landscape conditions, it is likely that there will be a spectrum of opportunity as part of the transition to a decentralised energy system. In practice, this is likely to mean that business cases that are viable in one part of the transition are not as viable in others. This approach is complicated by the fact that a number of the landscape conditions are difficult to foresee or anticipate. For the purpose of this discussion, it is assumed that the transition to DERs will follow a standard innovation diffusion curve, namely, moving from innovator to early adopter, to early majority, to late majority, then to laggards, as shown in Figure 3 [67].

Although there are a number of discrete DER types that will each have its own diffusion curve, the aggregation of the curves will likely follow an overall diffusion curve given the complementary nature of DERs. It is likely that each stage will experience a different set of landscape conditions and this will have a direct influence on the viability of associated DER business cases.

- Innovator Stage: In the early stages of the DER transition, the business cases focused on residential rooftop solar and the sale of solar panels and associated equipment, spurred on by attractive feed-in tariffs [68].

- Early Adopter Stage: During the early adopter stage the focus remained on rooftop solar, and numerous businesses were created around the installation and maintenance of associated equipment intended mainly for local electricity provision with some sale of excess electricity generation to the grid. During this stage, the development of home energy storage and electric vehicle technology was ongoing with prices nonconducive to early adoption.

- Early Majority Stage: It is likely that 2022 will be seen as the beginning of the early majority stage of the DER transition. With the now rapid uptake of rooftop solar (first in the residential then the commercial sectors), there is a growing focus on local storage to maximise the benefits in the face of reducing feed-in tariffs and the suggestion of future network use fees [69]. Still, at the beginning of this stage, home storage and EVs are price-prohibitive; however, costs are decreasing and are likely to be affordable in the near future. Alongside cost, the driving range of EVs has substantially increased between 2017 and 2022, reducing concerns of range capacity between chargers, leading to reconsideration for the role of public charging facilities [70]. This stage will also experience a rapid increase in microgrids and precinct systems that seek to cluster DERs behind a connection (behind the meter) to the grid, to take advantage of local generation and storage technologies [71]. It is likely that given the lack of suitable investment in grid-scale renewable generation and energy storage, this focus on local grids will dominate the late majority stage of the DER transition. However, it may be the case that the late majority stage involves a shift towards grid scale that makes very small scale localised use of generation and storage technology not cost effective. A lack of anticipatory planning including all stakeholders creates this uncertainty [9].

- Late Majority Stage: Once the early majority of consumers have equipped themselves with rooftop solar, local storage, and potentially an electric vehicle, in order to reduce energy costs, it is likely that the focus will shift to additional benefits. Hence, this will call for DER business cases such as the provision services associated with mitigating the effect of variability in generation and demand (including frequency and ancillary services) and other essential system services, and services associated with taking advantage of energy markets (such as purchasing energy when it is cheap to store and then sell during high-price periods). This may also include an increase in opportunities around consultant businesses assisting clients to determine how best to service their energy needs, mediating between different energy purchasers and sellers, managing energy clusters, and advising on cybersecurity of digital control systems [72].

- Laggard Stage: Once DERs are firmly established and a range of services are available and supported by policy and regulatory frameworks, it is likely that opportunities will focus mainly on local generation, storage, and use of electricity with the value of exporting and or storing excess generation diminished given that only a small number of consumers will choose not to or will be unable to access such options.

6.3. Further Research

It is important to consider likely landscape conditions and their implications for DER business opportunities [9]. This discussion may be informed through the development of a range of likely service configuration scenarios in order to investigate how likely landscape conditions will affect viability at different stages of the diffusion curve. If done effectively, this approach may reduce the potential for measures such as curtailment to be implemented due to a lack of adequate understanding of the shifting conditions. A key element will be consideration of precinct-scale DER deployment and how such ‘local grids’ function as part of a larger grid, given the customer-driven nature of the transition [73]. Hence, it is clear that during the DER transition there will be times when different business cases have greater or lesser viability depending on a range of factors. In order for the transition to accelerate (to rapidly transition away from fossil-fuel energy and the associated greenhouse gas emissions and air pollution), careful consideration will need to be made for how unpredictable changes in landscape conditions can inform efforts to underpin new and emerging DER business cases. As it is still too early for tangible data in this area of research, this paper does not review the actual case studies of DER that are now happening around the world. In a few years, it will be possible to review how some grids have become dominated by DER systems, and these will lend themselves to a larger review.

7. Conclusions

It is clear that the shift from large-scale centralised energy systems to medium- and small-scale distributed systems (a DER based system) presents much more than simply a technology disruption. In reality, this transition is likely to bring with it sector-wide replacement of many current practices and models, in effect creating a completely new energy paradigm. If handled well, such a transition will minimise disruption; however, it can be severely disruptive if long-held views and assumptions are not rapidly reconsidered and renewed, and new supporting structures are not swiftly put into place. Hence, if disruption is experienced, it is most likely caused by the lack of strategic response rather than the new technology itself, as with historical waves of innovation.

Despite this change in energy paradigm having been long forecast, it has largely been poorly prepared for and even avoided, resulting in a largely consumer-driven transition based on ad hoc purchasing behaviours. In a business-as-usual scenario, the energy sector would largely ignore the impending change in paradigm and assume that control can be maintained with small changes to the current system and greater enforcement of the old ways. The difficulty with this approach is that the technology to generate and store renewable energy at household and precinct scales is now affordable, profitable, and easily accessible, making the transition inevitable.

However, simply because it is now affordable does not mean that we know the best way to harness the greatest value and reduce the degree of disruption from the transition. Given the level of uncertainty around the many landscape conditions affecting the transition, previously held levels of assurance concerning future economic, consumer, and government conditions in the energy sector are no longer valid. It may be the case that understanding how to build effective DER business models at the start of the transition is actually premature, given the level of uncertainty, and may even cause a hindrance to new paradigm thinking, hence requiring a new approach. It is likely that understanding the most appropriate business models in a DER energy system calls for the real-world implementation of a range of DER service configurations under controlled conditions in order to learn from practice and build effective business models that can be rolled out across the energy system—such as the research being undertaken by the Australian Cooperative Research Centre for Renewable, Affordable and Clean Energy (RACE for 2030).

It is likely that such implementation projects would need to be afforded specific permissions to act in a manner that is not currently allowed by regulation or market rules, in order to demonstrate the viability and capability for the service configurations to generate successful business models. Such temporary permissions would likely be targeted around addressing the key barriers to high-value DER service configurations identified in the previous section, namely, scale issues, grid capacity issues, projects that involve hybridisation, lack of rewards for control, and projects that require aggregation. Rather than it being the case that the energy sector is not capable of designing DER business models, it may not be possible to predict the future with enough certainty to design a suitable model before such projects start.

Obviously, the macrobusiness considerations of cost, minimum return, and liability need to be addressed in order to secure a pilot project,; however, only items that are crucial to the initiation of projects should be considered as part of the pilot, with additional business implications and opportunities emerging from the process. The challenge is that although it is logical that old paradigm models are unlikely to be relevant in the new paradigm, it is also the case that new paradigm models are unlikely to be assessable using old paradigm approaches, and doing so may actually stifle innovation.

The key is to find ways to allow innovative DER projects to be collaboratively initiated, with the understanding that uncertainty will need to be navigated as the projects progress from design to construction, and to operation. In short, it will not be clear from the start what the detail of the best business model(s) will be until the service configuration is established and operating. Such projects would be implemented with special consideration and approvals linked to a baseline business case with the understanding that implementation will clarify how to give life to the model—rather than expecting the model to be clear at the start. In effect, a detailed scoping of likely revenue from the project requires a level of certainty that is not going to be available to the energy sector for at least a decade, and bold early steps need to be informed and taken to avoid disruption to the sector. The uncertainty will need to be navigated in real time to allow for specific barriers and challenges to be presented and responded to via collaborative, innovative solutions.

Author Contributions

Conceptualization, K.H., B.J., J.L. and P.N.; methodology, K.H., B.J., J.L. and P.N.; validation, K.H., B.J., J.L. and P.N.; formal analysis, K.H., B.J., J.L. and P.N.; investigation, K.H., B.J., J.L. and P.N.; resources, K.H., B.J., J.L. and P.N.; data curation, K.H., B.J., J.L. and P.N.; writing—original draft preparation, K.H., B.J., J.L. and P.N.; writing—review and editing, K.H., B.J. and P.N.; visualization, K.H., B.J., J.L. and P.N.; supervision, K.H. and P.N.; project administration, K.H.; funding acquisition, K.H. and P.N. All authors have read and agreed to the published version of the manuscript.

Funding

This research was funded by the RACE for 2030 Cooperative Research Centre, Australia.

Acknowledgments

The authors would like to thank the industry partners that participated in discussion with the research team to inform this project, in particular, Richard Romanowski from Planet Ark Power and Brian Innes from Starling Energy.

Conflicts of Interest

The authors declare no conflict of interest.

References

- Parag, Y.; Sovacool, B. Electricity Market Design for the Prosumer Era. Nat. Energy 2016, 1, 16032. [Google Scholar] [CrossRef]

- Van de Ven, D.J.; Capellan-Peréz, I.; Arto, I.; Cazcarro, I.; de Castro, C.; Patel, P.; Gonzalez-Eguino, M. The potential land requirements and related land use change emissions of solar energy. Nature 2021, 11, 2907. [Google Scholar] [CrossRef] [PubMed]

- Kaka, M.; Pendlebury, R. Turning Point for Incentives to Invest in Residential Batteries. Australian Energy Market Commission. Available online: www.aemc.gov.au (accessed on 3 March 2023).

- Frontier. Update on the Australian Battery Storage Sector; Frontier: Melbourne, VIC, Australia, 2022. [Google Scholar]

- Green Energy Markets. Final 2021 Projections for Distributed Energy Resources—Solar PV and Stationary Energy Battery Systems; Green Energy Markets Pty Ltd.: Hawthorn, VIC, Australia, 2021. [Google Scholar]

- World Economic Forum. A Vision for a Sustainable Battery Value Chain in 2030; World Economic Forum: Cologny, Switzerland; Geneva, Switzerland, 2019. [Google Scholar]

- Kubli, M.; Puranik, S. A typology of business models for energy communities: Current and emerging design options. Renew. Sustain. Energy Rev. 2023, 176, 113165. [Google Scholar] [CrossRef]

- Burger, S.; Luke, M. Business models for distributed energy resources: A review and empirical analysis. Energy Policy 2017, 109, 230–248. [Google Scholar] [CrossRef]

- Riedy, C.; Economou, D.; Koskinen, I.; Dargaville, R.; Gui, E.; Niklas, S.; Nagrath, K.; Wright, S.; Hargroves, C.; Newman, P.; et al. Anticipatory Planning for the Energy Transition: Final Report; RACE for 2030 Cooperative Research Centre: Haymarket, NSW, Australia, 2022. [Google Scholar]

- IEA. Unlocking the Potential of Distributed Energy Resources; International Energy Agency: Paris, France, 2022.

- Zakeri, B.; Gissey, G.; Dodds, P.; Subkhankulova, D. Centralized vs. distributed energy storage—Benefits for residential users. Energy 2021, 236, 121443. [Google Scholar] [CrossRef]

- Adinolfi, G.; Cigolotti, V.; Graditi, G.; Ferruzzi, G. Grid integration of distributed energy resources: Technologies, potentials contributions and future prospects. In Proceedings of the 2013 International Conference on Clean Electrical Power (ICCEP), Alghero, Italy, 11–13 June 2013. [Google Scholar]

- Office of Energy Efficiency and Renewable Energy. Distributed Wind. USA Government, n.d. Available online: www.energy.gov (accessed on 3 March 2023).

- Australian Energy Market Commission. Distributed Energy Resources. Australian Government, n.d. Available online: www.aemc.gov.au (accessed on 28 February 2023).

- Allan, G.; Eromenko, I.; Gilmartin, M.; Kockar, I.; McGregor, P. The economics of distributed energy generation: A literature review. Renew. Sustain. Energy Rev. 2015, 42, 543–556. [Google Scholar] [CrossRef]

- Energy Networks Australia (ENA); Commonwealth Scientific and Industrial Research Organisation (CSIRO). Electricity Network Transformation Roadmap; Energy Networks Australia (ENA): Melbourne, VIC, Australia; Commonwealth Scientific and Industrial Research Organisation (CSIRO): Canberra, ACT, Australia, 2016.

- Shiraki, H.; Ashina, S.; Kameyama, Y.; Hashimoto, S.; Fujita, T. Analysis of optimal locations for power stations and their impact on industrial symbiosis planning under transition toward low-carbon power sector in Japan. J. Clean. Prod. 2016, 114, 81–94. [Google Scholar] [CrossRef]

- Horowitz, K.; Peterson, Z.; Coddington, M.; Ding, F.; Sigrin, B.; Saleem, D.; Baldwin, S. An Overview of Distributed Energy Resource (DER) Interconnection: Current Practices and Emerging Solutions; National Renewable Energy Laboratory: Golden, CO, USA, 2019.

- Kholkin, D.; Chausov, I.; Burdin, I.; Rybushkina, A. Internet of Distributed Energy Architecture; National Technology Initiative Center: Moscow, Russia, 2021. [Google Scholar]

- Lantz, E.; Sigrin, B.; Gleason, M.; Preus, R.; Baring-Gould, I. Assessing the Future of Distributed Wind: Opportunities for Behind-the-Meter Projects; National Renewable Energy Laboratory: Golden, CO, USA, 2016.

- Energy Innovation Toolkit. Community Batteries. Australian Government, n.d. Available online: www.energyinnovationtoolkit.gov.au (accessed on 28 February 2023).

- Western Power. What Is the Difference between an ‘In Front of the Meter’ Battery and a ‘Behind the Meter’ Battery? Available online: www.westernpower.com.au (accessed on 1 March 2023).

- Kiesner, S. Key Electric Industry Trends; Edison Electric Institute: Washington, DC, USA, 2018. [Google Scholar]

- Blaabjerg, F.; Yang, Y.; Yang, D.; Wang, X. Distributed Power-Generation Systems and Protection. Proc. IEEE 2017, 105, 1311–1331. [Google Scholar] [CrossRef]

- Yang, Y.; Bremner, S.; Menictas, C.; Kay, M. Battery energy storage system size determination in renewable energy systems: A review. Renew. Sustain. Energy Rev. 2018, 91, 109–125. [Google Scholar] [CrossRef]

- Philibert, C. Solar Integration. Econ. Energy Environ. Policy 2012, 1, 37–46. [Google Scholar] [CrossRef]

- Sharma, V.; Haque, M.; Aziz, S. Energy cost minimization for net zero energy homes through optimal sizing of battery storage system. Renew. Energy 2019, 141, 278–286. [Google Scholar] [CrossRef]

- Bouffard, F.; Kirschen, D. Centralised and distributed electricity systems. Energy Policy 2008, 36, 4504–4508. [Google Scholar] [CrossRef]

- Brisbois, M. Decentralised energy, decentralised accountability? Lessons on how to govern decentralised electricity transi-tions from multi-level natural resource governance. Glob. Transit. 2020, 2, 16–25. [Google Scholar] [CrossRef]

- Schmeling, L.; Schönfeldt, P.; Klement, P.; Wehkamp, S.; Hanke, B.; Agert, C. Development of a Decision-Making Framework for Distributed Energy Systems in a German District. Energies 2020, 13, 552. [Google Scholar] [CrossRef]

- Kaminski Küster, K.; Rasi Aoki, A.; Lambert-Torres, G. Transaction-based operation of electric distribution systems: A review. Int. Trans. Electr. Energy Syst. 2019, 30, e12194. [Google Scholar]

- Chmutina, K.; Wiersma, B.; Goodier, C.; Devine-Wright, P. Concern or compliance? Drivers of urban decentralised energy initiatives. Sustain. Cities Soc. 2014, 10, 122–129. [Google Scholar] [CrossRef]

- Ambrosio-Albalá, P.; Bale, C.; Pimm, A.; Taylor, P. What Makes Decentralised Energy Storage Schemes Successful? An Assessment Incorporating Stakeholder Perspectives. Energies 2020, 13, 6490. [Google Scholar] [CrossRef]

- Jafari, M.; Korpas, M.; Botterud, A. Power system decarbonization: Impacts of energy storage duration and interannual renewables variability. Renew. Energy 2020, 156, 1171–1185. [Google Scholar] [CrossRef]

- Krishan, O.; Suhag, A. An updated review of energy storage systems: Classification and applications in distributed generation power systems incorporating renewable energy resources. Int. J. Energy Res. 2018, 43, 6171–6210. [Google Scholar] [CrossRef]

- Borges, C.L.T. An overview of reliability models and methods for distribution systems with renewable energy distributed generation. Renew. Sustain. Energy Rev. 2012, 16, 4008–4015. [Google Scholar] [CrossRef]

- Bouzid, A.; Guerrero, J.; Cheriti, A.; Bouhamida, M.; Sicard, P.; Benghanem, M. A survey on control of electric power distributed generation systems for microgrid applications. Renew. Sustain. Energy Rev. 2015, 44, 751–766. [Google Scholar] [CrossRef]

- Kavadias, S.; Ladas, K.; Loch, C. The Transformative Business Model—How to tell if you have one. Harv. Bus. Rev. 2016, 89, 113–117. [Google Scholar]

- Mont, O.K. Clarifying the concept of product–service system. J. Clean. Prod. 2002, 10, 237–245. [Google Scholar] [CrossRef]

- Hannon, M.J. Co-Evolution of Innovative Business Models and Sustainability Transitions: The Case of the Energy Service Company (ESCo) Model and the UK Energy System. Ph.D. Thesis, The University of Leeds, Leeds, UK, 2012. [Google Scholar]

- Boons, F.; Montalvo, C.; Quist, J.; Wagner, M. Sustainable innovation, business models and economic performance: An overview. J. Clean. Prod. 2013, 45, 1–8. [Google Scholar] [CrossRef]

- Sioshansi, F. Distributed Generation and Its Implications for the Utility Industry; Academic Press: Oxford, UK, 2014. [Google Scholar]

- Shaw, M. Community Batteries: A Cost/Benefit Analysis; The Australian National University: Canberra, ACT, Australia, 2021. [Google Scholar]

- Goebel, C.; Jacobsen, H.-A. Bringing Distributed Energy Storage to Market. IEEE Trans. Power Syst. 2016, 31, 173–186. [Google Scholar] [CrossRef]

- Kim, J.; Dvorkin, Y. A P2P-Dominant Distribution System Architecture. IEEE Trans. Power Syst. 2020, 35, 2716–2725. [Google Scholar] [CrossRef]

- Li, X.; Wang, S. Energy management and operational control methods for grid battery energy storage systems. CSEE J. Power Energy Syst. 2021, 7, 1026–1040. [Google Scholar]

- Mahmud, K.; Khan, B.; Ravishankar, J.; Ahmadi, A.; SIano, P. An internet of energy framework with distributed energy resources, prosumers and small-scale virtual power plants: An overview. Renew. Sustain. Energy Rev. 2020, 127, 109840. [Google Scholar] [CrossRef]

- Kim, D.; Fischer, A. Distributed Energy Resources for Net Zero: An Asset or a Hassle to the Electricity Grid? International Energy Agency. 2021. Available online: www.iea.org (accessed on 1 March 2023).

- Smith, J.; Rylander, M.; Rogers, L.; Dugan, R. It’s All in the Plans: Maximizing the Benefits and Minimizing the Impacts of DERs in an Integrated Grid. IEEE Power Energy Mag. 2015, 13, 20–29. [Google Scholar] [CrossRef]

- Kumar, N.; Chand, A.; Malvoni, M.; Prasad, K.; Mamun, K.; Islam, F.; Chopra, S. Distributed Energy Resources and the Application of AI, IoT, and Blockchain in Smart Grids. Energies 2020, 13, 5739. [Google Scholar] [CrossRef]

- Kumar, B.A. Solid-State Circuit Breakers in Distributed Energy Resources. In Proceedings of the IEEE 16th International Conference on Smart Cities: Improving Quality of Life Using ICT & IoT and AI, Charlotteville, NC, USA, 6–9 October 2019. [Google Scholar]

- Obi, M.; Slay, T.; Bass, R. Distributed energy resource aggregation using customer-owned equipment: A review of literature and standards. Energy Rep. 2020, 6, 2358–2369. [Google Scholar] [CrossRef]

- Green, J.; Newman, P. Transactive Electricity Markets: Transactive Electricity: How decentralized renewable power can create security, resilience and decarbonization. In Intelligent Environments 2—Advanced Systems for a Healthy Planet; Elsevier: Amsterdam, The Netherlands, 2022. [Google Scholar]

- Hellstrom, M.; Tsvetkova, A.; Gustafsson, M.; Wikstrom, K. Collaboration mechanisms for business models in distributed energy ecosystems. J. Clean. Prod. 2015, 102, 226–236. [Google Scholar] [CrossRef]

- Sadimenko, I. What Does a Customer-Led Energy Transition Mean for Australian Energy? Ernest and Young. 2022. Available online: www.ey.com (accessed on 2 March 2023).

- Cantley-Smith, R.; Kallies, A.; Briggs, C.; Kraal, D.; Khalilpour, K.; Dwyer, S.; Hargroves, K.; Liebman, A.; Ben-David, B. Opportunity Assessment—Theme N4: DSO and Beyond—Optimising Planning and Regulation for DM and DER; RACE for 2030 Cooperative Research Centre: Haymarket, NSW, Australia, 2023. [Google Scholar]

- Heiskanen, E.; Apajalahti, E.; Matschoss, K.; Lovio, R. Incumbent energy companies navigating energy transitions: Strategic action or bricolage? Environ. Innov. Soc. Transit. 2018, 28, 57–59. [Google Scholar] [CrossRef]

- AEMO. About the Wholesale Electricity Market (WEM). Australian Energy Market Operator. Available online: https://aemo.com.au/ (accessed on 3 March 2023).

- Parkinson, G. Rooftop Solar Smashes Demand and Supply Records in World’s Biggest Isolated Grid. Renew Economy. 2022. Available online: https://reneweconomy.com.au/ (accessed on 3 March 2023).

- Stephens, J.; Wilson, E.; Peterson, T.; Meadowcroft, J. Getting Smart? Climate Change and the Electric Grid. Challenges 2013, 4, 201–216. [Google Scholar] [CrossRef]

- Murphy, C.A.; Schleifer, A.; Eurek, K. A taxonomy of systems that combine utility-scale renewable energy and energy storage technologies. Renew. Sustain. Energy Rev. 2021, 139, 110711. [Google Scholar] [CrossRef]

- Charbonnier, F.; Morstyn, T.; McCulloch, M.D. Coordination of resources at the edge of the electricity grid: Systematic review and taxonomy. Appl. Energy 2022, 318, 119188. [Google Scholar] [CrossRef]

- Willems, N.; Sekar, A.; Sigrin, B.; Rai, V. Forecasting distributed energy resources adoption for power systems. iScience 2022, 25, 104381. [Google Scholar] [CrossRef] [PubMed]

- Jones, K.; Curtis, T.; Thege, M.; Sauer, D.; Roche, M. Distributed Utility: Conflicts and Opportunities between Incumbent Utilities, Suppliers, and Emerging New Entrants. In Future of Utilities Utilities of the Future; Institute for Energy and the Environment, Vermont Law School: South Royalton, VT, USA, 2016; pp. 399–415. [Google Scholar]

- Griffith, S. The Big Switch; Black Inc.: Collingwood, VIC, Australia, 2022. [Google Scholar]

- Zinaman, O.; Bowen, T.; Aznar, A. An Overview of Behind-the-MeterSolar-Plus-Storage Regulatory Design; National Renewable Energy Laboratory: Golden, CO, USA, 2020.

- Rogers, E. Diffusions of Innovations, 5th ed.; The Free Press: New York, NY, USA, 2003. [Google Scholar]

- Dijkgraaf, E.; van Dorp, T.; Maasland, E. On the effectiveness of feed-in tariffs in the development of solar photovoltaics. Energy J. 2018, 39, 81–100. [Google Scholar] [CrossRef]

- Ma, R.; Cai, H.; Ji, Q.; Zhai, P. The impact of feed-in tariff degression on R&D investment in renewable energy: The case of the solar PV industry. Energy Policy 2021, 151, 112209. [Google Scholar]

- Hargroves, K.; James, B. Perception and Capacity Factors affecting the Uptake of Electric Vehicles in Australia; Sustainable Built Environment National Research Centre (SBEnrc): Bentley, WA, Australia, 2021. [Google Scholar]

- Rajakaruna, S.; Ghosh, A.; Pashajavid, E.; Economou, D.; Bandara, T.; Ragab, Z.; Dwyer, S.; Dunstall, S.; Wilkinson, R.; Kallies, A.; et al. Opportunity Assessment—Theme N3: Local DER Network Solutions; RACE for 2030 Cooperative Research Centre: Haymarket, NSW, Australia, 2023. [Google Scholar]

- Mouritz, M.; Silva, A.; Economou, D.; Hargroves, K.; Inchauspe, J.; Akimov, A.; Stegen, S.; Nutkani, I.; Vahidnia, A.; McGrath, B. Business Models and the Energy Transition; RACE for 2030 Cooperative Research Centre: Haymarket, NSW, Australia, 2022. [Google Scholar]

- Curtis, S.K.; Mont, O. Sharing economy business models for sustainability. J. Clean. Prod. 2020, 266, 121519. [Google Scholar] [CrossRef] [PubMed]

Figure 1.

A comparison of architecture for a centralised (conventional) system versus a decentralised general electricity system. Red and blue arrows denote electricity and system management data flows, respectively [19].

Figure 1.

A comparison of architecture for a centralised (conventional) system versus a decentralised general electricity system. Red and blue arrows denote electricity and system management data flows, respectively [19].

Figure 2.

Depicting electricity stakeholders located front-of-meter and behind-the-meter. Note that stakeholders behind-the-meter can be an individual or a group [23].

Figure 2.

Depicting electricity stakeholders located front-of-meter and behind-the-meter. Note that stakeholders behind-the-meter can be an individual or a group [23].

Figure 3.

Depicting the population phases of new innovation adoption [67].

Figure 3.

Depicting the population phases of new innovation adoption [67].

{kind=link}

{kind=link}

{kind=link}

Table 1.

Summary of DER service configurations.

| 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 | 11 | 12 | 13 | 14 | 15 | 16 | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Generation | ||||||||||||||||

| No Generation | ✓ | ✓ | ||||||||||||||

| Dedicated Site | ✓ | ✓ | ||||||||||||||

| Individual Site | ✓ | ✓ | ✓ | ✓ | ||||||||||||

| Physical Cluster | ✓ | ✓ | ✓ | ✓ | ||||||||||||

| Virtual Cluster | ✓ | ✓ | ✓ | ✓ | ||||||||||||

| Storage | ||||||||||||||||

| Onsite | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | |||||||

| No storage | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | |||||||||

| Usage | ||||||||||||||||

| Onsite | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | |||||||||

| Grid | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | |||||||

Table 2.

Mapping DER service configurations to selected categories of current barriers.

| Key Industry-Identified Barriers | ||||||

|---|---|---|---|---|---|---|

| DER Service Configuration | Potential Value | Scale Issues | Grid Capacity Issues | Involves Hybrids | Unrewarded Control | Requires an Aggregator |

| Low | ✓ | ✓ | ✕ | ✓ | ✕ |

| High | ✓ | ✓ | ✕ | ✓ | ✕ |

| Medium | ✕ | ✓ | ✕ | ✓ | ✕ |

| High | ✓ | ✓ | ✕ | ✓ | ✕ |

| Medium | ✕ | ✕ | ✕ | ✓ | ✕ |

| High | ✓ | ✓ | ✕ | ✓ | ✕ |

| Medium | ✕ | ✕ | ✓ | ✓ | ✓ |

| High | ✓ | ✓ | ✓ | ✓ | ✓ |

| Medium | ✓ | ✕ | ✓ | ✓ | ✓ |

| High | ✓ | ✓ | ✓ | ✓ | ✓ |

| Medium | ✓ | ✕ | ✓ | ✓ | ✓ |

| High | ✓ | ✓ | ✓ | ✓ | ✓ |

| Medium | ✓ | ✕ | ✓ | ✓ | ✓ |

| High | ✓ | ✓ | ✓ | ✓ | ✓ |

| Medium | ✓ | ✕ | ✓ | ✓ | ✓ |

| High | ✓ | ✓ | ✓ | ✓ | ✓ |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Hargroves, K.; James, B.; Lane, J.; Newman, P. The Role of Distributed Energy Resources and Associated Business Models in the Decentralised Energy Transition: A Review. Energies 2023, 16, 4231. https://doi.org/10.3390/en16104231

AMA Style

Hargroves K, James B, Lane J, Newman P. The Role of Distributed Energy Resources and Associated Business Models in the Decentralised Energy Transition: A Review. Energies. 2023; 16(10):4231. https://doi.org/10.3390/en16104231

Chicago/Turabian StyleHargroves, Karlson, Benjamin James, Joshua Lane, and Peter Newman. 2023. "The Role of Distributed Energy Resources and Associated Business Models in the Decentralised Energy Transition: A Review" Energies 16, no. 10: 4231. https://doi.org/10.3390/en16104231

Note that from the first issue of 2016, this journal uses article numbers instead of page numbers. See further details here.