1. Introduction

The construction and development of high-tech industry in New Industrializing Countries (NICs) has been an important research topic within development studies, especially concerning the foreign direct investment (FDI) clustering and spillover development. Most literature considers the FDI cluster to support industrial competitiveness and advantage, generating technology spillovers for local domestic firms [

1,

2,

3,

4,

5]. As such, the attractions of FDI clusters are frequently manipulated as an industrial strategy by the governments of NICs to benefit local innovation activity through spillover channels, such as reverse engineering, skilled labor turnovers [

6,

7,

8], demonstration effect, supplier customer relationships [

9,

10,

11], and others. However, the practical results of attracting FDI strategies are ambiguous and sometimes negative. For example, Germidis [

12] finds no evidence of technology learning and transfer from foreign to local firms in the FDI cluster. Even worse, the FDI can even cause negative effects in spillovers [

13,

14,

15,

16]. Furthermore, market stealing may also occur because the foreign-invested firms gain market shares at the expense of domestic firms and force them to reduce production, resulting in higher average cost [

17]. There is, thus, little doubt that the FDI cluster may adversely affect technology learning, and cause negative market effects that can crowd out the development space of domestic firms (also see [

18,

19]). In turn, other studies further contest the reasons for the various results of FDI-led spillovers in the ownership structure of FDI projects, government trade policy,

etc. [

20,

21,

22,

23].

Based on the quantity analysis of panel data sets, many of these studies have advanced our understanding of the technology spillovers of the FDI clusters. They have also touched on the industrial structure, technology learning, market competition, and industrial upgrading topics, which are related to local industrial development in the broader context of globalization. Nevertheless, most studies overemphasize the technology spillovers, playing down the construction and development process of native enterprises in the NICs. In other words, the quantitative research on FDI-led spillovers provides only partial insights for native industrial development within the FDI cluster. These studies also can omit the local quality processes of domestic entrepreneurial construction and development in the FDI clustering, which normally involve government support, strategic linkages of global and local firms, and technology community flows in the fast-changing competitive environment. This is particularly true for the construction and development of the high-tech industry, which involves the intensified and complicated competition strategies of global and local firms, as well as extensively engaging the strategic manipulations of government support.

There is, thus, little doubt that government support for the construction and development of domestic high-tech firms within FDI clusters is not translated into a single path of industrial development. Instead, localities and nationalities have demonstrated context specific paths. The development process of domestic high-tech firms within FDI clusters in the NICs is a local process involving the manipulation of government supports and strategic performances of global and local firms, thereby allowing for a variety of development paths. As a consequence, further research, based on different brick-and-mortar industrial cases in different countries, is required for a better understanding of the sustainable development of domestic high-tech firm and industrial issues within the FDI clusters.

This article, thus, contributes to the FDI cluster debate and attempts to explore the policy lessons for NICs. It presents case studies on the high-tech FDI clusters of Suzhou, Shanghai, and Wuxi, in the Yangtze Delta, and examines their effectiveness and the impact of government support on developing the domestic semiconductor industry. In fact, policies of attracting FDI cluster and of developing indigenous entrepreneurs have been raised as national strategies by the Chinese government to pursue the development of domestic high-tech industries in the globalizing world. In other words, it is through this two-track strategy that the government hopes to develop indigenous high-tech industries by policy supports, while also attracting clusters of foreign investors. As a key component and driver for high-tech developments, the semiconductor industry, in this policy context, constitutes a major sector subject to special support of central and local governments in China. The investment boom of semiconductors since the 1990s has proliferated and is especially clear in Shanghai, Suzhou, and Wuxi of the Yangtze Delta. The temptations of government support have generated different industrial results in developing the native semiconductor industry within the domination of FDI clusters. Accordingly, it is important to explore their differences and detect possible implications of high-tech development policies for the NICs. As such, with reference to the different experiences and challenges of local government supports, the article investigates the industrial possibilities and policy implications for developing the native semiconductor industry in the NICs by examining the cases of Shanghai, Suzhou, and Wuxi, in the Yangtze Delta, China.

Developing a high-tech industry within FDI-dominated clustering is always an extreme challenge for NICs. The first vital question lies in technology acquisition, which is normally regarded as a key component for the sustainable development of native firms in NICs. Nevertheless, technology acquisition is just one element in their development. In some instances, it may be not so critical, because many technologies can be acquired through purchasing and other strategic manipulations, such as the “market for technology” applied in China. The key lies in the technology talents and their capabilities of absorption and learning. Moreover, semiconductor investments are a highly risky business in the intense market competition, with a 12-inch semiconductor firm costing about 2.5 billion US$ and one billion US$ for an eight-inch firm. Beyond technology acquisition, high-tech developments in the NICs also face serious obstacles due to the technology talent shortage, financial risk and market linkages, as well as the huge threat of international competitions [

24].

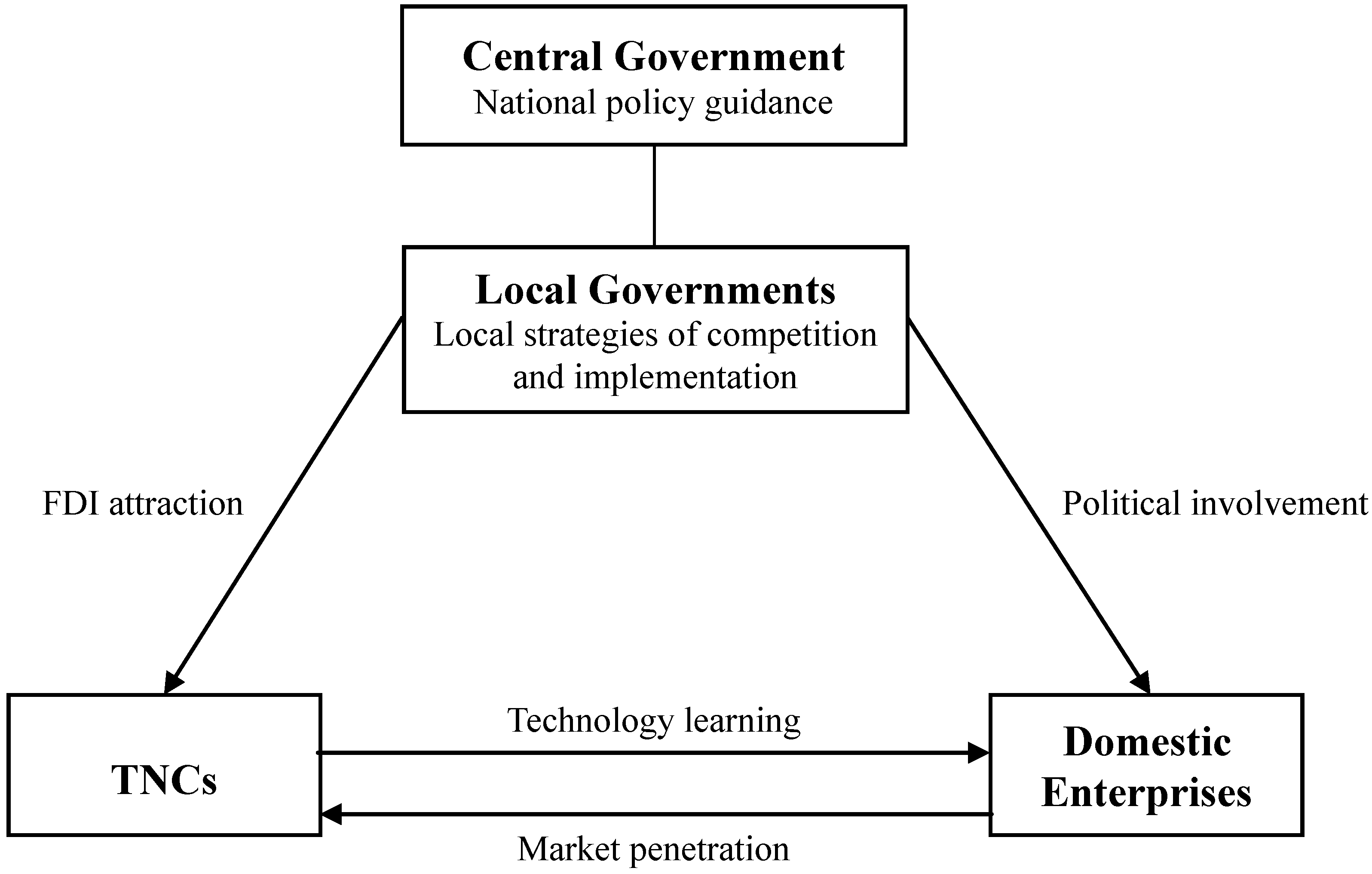

Above all, most cases of indigenous industrial development are normally initiated by government support in NICs. As Dunning [

25,

26,

27] argues, governments may mobilize policies and apply their resources as bargaining chips to harness investment strategies of transnational enterprises for upgrading local industrial structure and technology learning. Coe

et al. [

28] also contend that, within the constant expansion of the global production network (GPN) in the globalizing world, local high-tech industries may be developed, and their success primarily relies on how the government arranges their local industrial assets to reach a complementary interaction with the requirements of FDIs (see

Figure 1). That is, the coherent articulation of the strategic coupling between local industrial assets and foreign investors may generate a successful opportunity for the construction and development of local high-tech industries [

28,

29,

30,

31,

32]. Nevertheless, the sustainable development of local high-tech industries through the strategic coupling of government support still has challenges. In fact, a successful FDI attraction and clustering does not automatically lead to the opportunity and capacity for technological learning and sustainable development by the local indigenous industries. In this condition, it may limit the technical and organizational capabilities of local manufacturers to enter more vulnerable development spaces [

18,

19]. Moreover, the government support to domestic enterprises, generally involved deeply with political purposes and considerations, influences domestic firms’ operation and development strategies. Once the overprotection policy and privileges are manipulated, domestic enterprises’ capability construction of technological learning, market competitiveness and industrial sustainability in the FDI clustering may be jeopardized. As such, the FDI attractions do not imply the opportunity for NICs to construct their own high-tech industries and gain sustainable capacities for further development without challenges.

Figure 1.

Conceptual model of Strategic Coupling.

Figure 1.

Conceptual model of Strategic Coupling.

Based on the case studies of semiconductor developments in the Shanghai, Suzhou, and Wuxi in the Yangtze Delta, this paper, thus, emphasizes the strategic coupling of government support, and attempts to discern possible policy lessons for NICs to construct high-tech industries by exploring the impact of government support on the construction and sustainable development of local high-tech firms, beginning with a discussion of the clustering development of FDI in the Yangtze Delta. Then, the models of government support, and connected impacts on the domestic semiconductors, are identified and investigated to determine which government policy models are more effective. The final section contains conclusions and discussion.

2. High-Tech Clusters of FDI, Government Support and Foreign Semiconductor Firms

High-tech FDI clustering towards the Yangtze Delta was mainly initiated with Deng Xiaoping’s south visit in 1992. They are primarily centralized in the areas of Shanghai, Suzhou, and Wuxi, which is commonly referred to as the manufacturing base of global high-tech industries, especially in the IC and ICT sectors [

33]. This development is primarily a product of national policy. In the early 1990s, the central government put a premium on attracting the FDI to facilitate local development. During the development process of the late 1990s, the targeted industries were dramatically shifted from traditional industries to high-tech ones by the strategic guidance of the ninth Five-Year Plan (1995–2000). This policy transition was particularly presented and constituted in the “Torch Program”, emphasizing the cluster development of foreign enterprises by establishing the Economic and Technology Development Zone (ETDZ) and providing favorable policies.

As declared by Deng, “China must have a place in the world high-tech territory” [

34] (p. 7). It is in this political declaration of having a place in the high-tech arena, the national industrial policy agenda considers that the semiconductor industry in China must develop at any cost [

35]. As a result, the policy ambitions and experiments in developing the domestic semiconductor industry were fostered by the “Project 908” in August 1990 and “Project 909” in September 1995. Two domestic semiconductors,

i.e., the Wuxi Huajung and Shanghai HuaHong NEC [

36], were created as national pioneer projects by the “market for technology” strategy. This policy pledges that the Chinese government will develop native semiconductor industry according to three viewpoints. The first is that semiconductor is a critical industry with a high potential for input-output linkages and spillover effects that can increase national GDP growth. Secondly, China has become a major country for both IC production and consumption; but the self-sufficiency ratio of China’s IC industries is still very low, less than 10% in 2003. In this industrial context, the construction and development of native semiconductors becomes necessary for the sustainable development of high-tech industries in China. Last but not least, the technology community in greater China has been extensively formulated and plays very active roles in the world high-tech territories. With a proper policy of talent attraction, China would stand in a good position to follow the suit of advanced countries, such as the USA and Japan, to construct a full-fledged semiconductor industry and strengthen its sustainable capability of high-tech industries.

For high-tech industrial development, the central government issued “A Series of Policies Encouraging the Development of Software and IC Industries” in 2000, and semiconductors are eligible for the preferential policy of value-added taxes and tariff duty exemptions. Moreover, the policy of “two free, three by half” (

liangmian sanjianban) is applied for attracting high-tech FDI, in which income tax is exempted for the first two years and halved for three subsequent years. Subsequently, the tenth Five-Year Plan (2001–2005) set an ambitious target to speed up semiconductor development by investing RMB 380 billion. Moreover, the policy of “innovation country” was further launched in the eleventh Five-Year Plan (2006–2010) to emphasize indigenous innovation (

zizhu chuangxin) for developing strategic technology and autonomous industrial chains, as well as facilitating native semiconductor construction. In the eleventh Five-Year Plan for High-tech Industries, the cluster policy was further reemphasized to accelerate the high-tech clustering development towards the Yangtze Delta, and to consolidate their industrial chains into a leading high-tech cluster of the world [

37].

Although the cluster policy was initiated by the central government, it is normally realized among the competitions of local governments for attracting FDIs [

38,

39]. In the Yangtze Delta, the local governments of Shanghai, Suzhou, and Wuxi put great efforts in developing huge areas of ETDZ, and in providing special preferences to attract FDI clustering towards their territories [

40]. These major high-tech shifts are often credited with the industrial infrastructures of Shanghai’s Zhangjing Science Park, Suzhou’s New District and Science Park, and Wuxi’s New District [

41,

42]. All of these strategic areas were thus constituted as major regions for FDI clusters. As shown in

Table 1, the growth of high-tech industries on the national development areas had dramatically increased over time and with the local implementation of industrial cluster policy. During the seven-year period from 2000 to 2007, high-tech firms were almost doubled to create triple the growth in employment, produce output value over twice, and generate an export value of more than eight-fold. In particular, the performance of high-tech industrial economies in these three cities were ranked at the top of the nation. In 2007, more than 2000 FDI-led firms were attracted to the development zones of these three cities. They provided 750,000 jobs and created RMB 646.4 billion in output and US$ 50.1 billion in exports, accounting for 29% of the national total.

Table 1.

Economic indicators of high-tech enterprise in development areas 2000, 2007 [

43,

44]

Table 1.

Economic indicators of high-tech enterprise in development areas 2000, 2007 [43,44]

| | 2000 | 2007 |

Number of firms

(unit) | Number of employees

(person) | Output value

(10,000 RMB) | Income value

(10,000 RMB) | Export value

(10,000 USD) | Number of firms

(unit) | Number of employees

(person) | Output value

(10,000 RMB) | Income value

(10,000 RMB) | Export value

(10,000 USD) |

| National total | 20,796 | 2,350,679 | 79,419,852 | 92,092,631 | 1,858,175 | 48,472 | 6,502,370 | 443,769,460 | 549,251,627 | 17,271,217 |

| Shanghai | 438 | 85,146 | 6,747,683 | 7,513,625 | 232,753 | 827 | 241,603 | 26,612,665 | 35,811,713 | 835,646 |

| (9th) | (5th) | (2nd) | (2nd) | (1st) | (10th) | (3rd) | (2nd) | (2nd) | (7th) |

| Suzhou | 236 | 67,084 | 3,462,132 | 3,390,873 | 224,915 | 631 | 278,072 | 16,743,500 | 19,011,390 | 2,596,195 |

| (20th) | (8th) | (5th) | (5th) | (2nd) | (14th) | (2nd) | (6th) | (6th) | (1st) |

| Wuxi | 250 | 31,110 | 2,277,521 | 2,747,891 | 127,031 | 608 | 234,963 | 21,296,699 | 21,667,435 | 1,590,631 |

| (19th) | (33rd) | (8th) | (8th) | (5th) | (17th) | (4th) | (3rd) | (3rd) | (3rd) |

Associated with rapid development of the high-tech FDI clustering, these three cities are geographically translated into a polycentric urban region, connected by a freeway and high-speed railway network. They, thus, form a mega-metropolitan high-tech region and are increasingly considered as one of most dynamic and globalizing areas in China, attracting growth in employment and population. According to the city development plan approved by the central government, Shanghai is designated as the economic powerhouse and gateway city for the Yangtze Delta. Following this development, since the late 1990s this urban region has manifested itself as a spatial division of labor. As our interviewee observes,

“In the Yangtze Delta, cities in the Sunan area, especially the Suzhou and Wuxi, have become Shanghai’s manufacturing bases, while Shanghai serves as the commercial service and marketing center, as well as the outward-looking investment and financing platform related to headquarters and R&D economies”.

The strategic coupling of FDI clustering and the local governments in Suzhou, Shanghai, and Wuxi are discussed as below (

Table 2).

Table 2.

Strategic coupling of foreign direct investment (FDI) clustering and the local governments in the Yangtze Delta.

Table 2.

Strategic coupling of foreign direct investment (FDI) clustering and the local governments in the Yangtze Delta.

| | Shanghai | Suzhou | Wuxi |

|---|

| City status | Municipality | Prefecture-Level city | Prefecture-Level city |

| Industrial clustering | FDI-led R&D, headquarters, advanced manufacturing | ICT manufacturing | ICT manufacturing |

| Development zones | Zhangjiang science Park, Pudong | Suzhou New District

Suzhou Science Park | Wuxi New District |

| FDI preferential policy | Taxation, land and service for global leading firms | Taxation, land and service for FDI especially from Taiwan | Taxation, land and service for FDI especially from from Japan and Korea |

| FDI-led semiconductor examples | IC design: SST, Tridentu, and Taiwan’s VIA and Zhiyuan;

wafer manufacturing: Novellus Systems Inc., Applied Materials Inc., SMIC, TSMC, Charted and Grace;

packing and testing: Intel and ASE | Manufacturing: HeJian (Taiwan), Elpida (Japan)

Testing and packaging: Samsung (Korea), Spansion (USA) | Manufacturing: Hynix Semiconductor (Korea) |

2.1. FDI Clustering and Semiconductor Development in Suzhou

Suzhou is located close to Shanghai. Nevertheless, compared with Shanghai, its urban attractions for the FDI are relative weak in both quality and quantity of industrial infrastructure, urban service, educational resource, labor supply,

etc. Considering the bargaining power of the FDI, the Suzhou city government was forced to target FDIs that had been overlooked by the Shanghai government, in particular, the small-and-medium enterprises (SMEs) of ICT from Taiwan. These generally served as labor-intensive subcontracting manufacturers for Western firms and were extensively stressed by growing labor costs and declining industrial competitiveness in Taiwan. Generous preferential treatment for land supply, infrastructure provisions and tax exemptions were, hence, mobilized by the city government to attract SMEs. More importantly, the operation model of Hsinchu Science Park in Taiwan as a one-stop administrative service system was replicated to create a more Taiwanese industrial atmosphere that would attract Taiwanese investors [

40,

46]. One of Suzhou’s officials pointed out that “One investment project, one policy. Our policy for the FDI is very flexible and very generous; sometimes, very surprising and exciting to the investor” [

47]. As the competition in attracting FDI intensified among local governments on the Yangtze Delta, Suzhou was not only forced to adopt a supply strategy of expanding ETDZ and the land supply to woo investors, but also tailored its services and preferences to meet the needs of Taiwanese firms [

40]. One Taiwanese investor interviewee commented, “the Suzhou government acceded to almost every request to attract Taiwanese IT investors” [

48]. It is within the manipulation of strategic coupling that almost all the leading Taiwanese IT firms—including Compal, Asus, Acer, Mio,

etc.,—had located their manufacturing facilities in Suzhou due to cheaper labor force and larger production space.

In the semiconductor investment, a typical example is the case of HeJian, which was the shadow factory of Taiwan’s UMC because all its engineers were from UMC. In this case, the Suzhou city government provided 200-hectare of free land for HeJian and other preferential policies, including a package of tax exemptions and synchronized construction of relevant infrastructure and dormitories in the surrounding area. In a very similar process of strategic coupling, further FDI in semiconductors also emerged. In 1994, the Korean company Samsung established semiconductor testing and packaging factories in Suzhou Industrial Park. In 2001, the Japanese companies Elpida, Hitachi Semiconductor, and Matsushita PSCSZ located facilities in Suzhou New District. In 2005, American AMD located its subsidiary Spansion in the Suzhou.

2.2. FDI-Led High-Tech Clustering and Semiconductors in Shanghai

In the urban region of the Yangtze Delta, the industrial developments of Shanghai have constantly emphasized its commercial and seaport advantages to develop FDI-led R&D and headquarter economies as its major driving forces for the city’s development. Nevertheless, although the significance of manufacturing sectors has declined, they still play an indispensable and vital role in Shanghai’s development. In fact, since 1978 several ETDZs have been created, including the Pudong New District, Minhang ETDZ, Hongqiao ETDZ, and Caohejing High-Tech Park. As such, a number of international ICT firms have been attracted to Shanghai. With Shanghai’s advantages as the national economic capital city, its FDI policy particularly focused on attracting leading international, capital-intensive firms. To attract Taiwanese, emphasis was put on IT giants, such as Taiwan’s Quanta and TSMC, the largest PC and semiconductor subcontracting firms. The labor intensive sectors of Taiwanese SMEs in the IT industries received relatively little attention.

Obviously, although Shanghai’s urban economic development is overwhelmingly dominated by the commercial sectors, the manufacturing industries were not abandoned, and its industrial policy increasingly emphasized advanced industries. Subsequently, the Shanghai municipal government issued a series of strategies for stimulating manufacturing investment to compete with Suzhou and Wuxi to attract high-tech FDI clustering. In 2002, the industrial policy of “Focus on Zhangjiang” was launched to attract FDI high-tech clustering to Pudong. In 2004, the “Priority Program for Developing the Advanced Manufacturing” was further announced to attract FDI-led semiconductor clusters and develop indigenous high-end semiconductor industry of eight-inch and 12-inch wafer fabrication. Based on these strategic policies, leading global firms were attracted, and a relatively matured semiconductor industrial chain was been formed in Shanghai, including IC design (SST, Tridentu, and Taiwan’s VIA and Zhiyuan); wafer manufacturing (Novellus Systems Inc., Applied Materials Inc., SMIC and Grace); downstream packing and testing (Intel and ASE); and, of course, international ICT R&D institutions.

2.3. Japanese and Korean ICT Clustering and Semiconductors in Wuxi

Wuxi was designated by the central government as a micro-electronics industrial base in 1983. Nevertheless, the FDI-led cluster and domestic investment did not take off until the establishment of the Wuxi New District. As mentioned above, Taiwanese FDI in the Yangtze Delta was mainly centralized in Suzhou. As our interviewee in the Wuxi New District said,

“Most Taiwanese FDI was caught in the development areas of Shanghai and Suzhou, so investors from Taiwan were few in Wuxi. It was for this reason that we turned to attract the Korean and Japanese investors and already had good results”.

The FDI cluster in Wuxi was primarily constituted by three distinct groups—Taiwanese firms, domestic firms, and Korean, and Japanese firms—accounting for 10%, 25%, and 55% respectively [

42]. In 2001, the Wuxi New District was further designated by the central government as the national design base for IC development, and a government-run company was set up to provide services for investors. Furthermore, the city government annually organized a task force of investment promotion targeting Korean and Japanese firms. With its favorable policies on land, taxation, and services, this district has, hence, become a strategic site that attracts FDIs from Japan and Korea. The typical example was the Wuxi Sharp Electronic Components Co. Ltd—a joint venture of Wuxi city government and Japanese Sharp. Moreover, in 2006, Hynix from Korea and STMicroelectronics from Europe set up a joint venture and spent two billion US$ to develop Wuxi into a sophisticated base of 12-inch semiconductor manufacturing in the Yangtze Delta. It is believed that this significant event may reduce the technology gap between semiconductors in China and their international counterparts from 10 years to two to three years. In order to promote its competitive potential, the city largely funded the construction of Thaihu Silicon Valley—a huge modern development area in the New District that is designed to support the construction of a complete semiconductor industrial chain, including wafer fabrication, chip design, packaging and testing, equipment installation, and ancillary services.

2.4. GPN Expansion and Technology Diffusion among Foreign Firms

Propelled by the extensive growth of FDI-led ICT clusters, the global production network has expanded dramatically, and, since 2000, it has stimulated the semiconductor investment in the Yangtze Delta. In other words, with the significant growth of the ICT market, the Yangtze Delta has become a critical area for the leading international semiconductor firms. Moreover, the development was extensively facilitated by the Chinese government’s strategic manipulation of its taxation system. China’s taxation of imported wafers includes tariff duties and value added tax (VAT) of 6% and 17%, respectively. Because the tax base of VAT is the import price plus tariff duty, the actual tax rate reaches about 24%. To avoid such a heavy tax burden, the semiconductor FDI proliferated in the region, and subsequently stimulated a dramatic growth of technology learning and diffusion among the FDI-led firms.

Against this backdrop, Suzhou pulled together major DRAM manufactures, such as Infineon, Elpida, Samsung, Hynix, Spansion, AMD, etc. In addition, SMIC, Kingston, Charted, design centre of AMD, ASE, Intel, etc., also moved to Shanghai. Faced with this intense competition, the Taiwanese government was forced to allow its semiconductor firms to invest in China beginning in 2005. There is no doubt that, apart from tax reduction, the biggest push for the global semiconductor investment in China is the dramatic growth of markets and sales in China. These firms wanted to have a manufacturing base in the Yangtze Delta, because that region is considered the best location to follow the market evolution, consolidate the production network, and gain a stronghold in China’s huge market. Normally, the slotting strategy in the back segment of production chain was adopted by these global firms in attempting to develop their market in China.

For example, the Korean companies Samsung and Hynix upgraded their DRAM production scales in East China in 2005. The DRAM manufacturing of Suzhou Samsung doubled from 25% of the firm’s total production to 50% in 2005. However, since there was no Korean printed circuit board producer to collaborate with in east China, they were forced to collaborate with Taiwanese firms—Tripod Technology and J-THREE. The localized partnership and collaboration was, hence, increasingly formulated among FDI-led firms. Another example is the 2008 joint venture project of 12-inch wafer fabrication between Taiwanese HeJian and Japanese Elpida in Suzhou. In fact, Elpida [

50] had previously developed several Taiwanese semiconductor partners in the Yangtze Delta, including Rexchip Electronics (memory production), which is a subsidiary of Powership Semiconductor, and Powertech Technology, which provides packaging services. Elpida considered that working closely with Taiwanese semiconductors would deepen its strategic alliances and its upgrade market shares in China, thereby giving it an advantage over Samsung to become the global leading firm in the DRAM market.

All of these trends indicate that the FDI-led cluster in Yangtze Delta was increasingly evolving towards capital-intensive and high-end industrial development. More importantly, the expanded scale of the production network has more recently stimulated further investments of their R&D sectors, generating the effect of localized technology learning among FDI firms. The FDI-led R&D investments in the Yangtze Delta are primarily considered to create an effective position to develop that business, and make quick responses and policy decisions to the fast-changing markets for consumer electronics in China and other part of Asia. As one of our interviewees pointed out,

“In the past two decades, the FDI and domestic Chinese firms clustering in the Yangtze Delta had extensively included software and hardware suppliers and the market consumers. The investments of foreign R&D sectors in this region gave the IT firms a great advantage to reduce their cost, shorten the R&D circle and simplify the complicated design works for developing cutting-edge systematic solutions with their clients. At the same time, they also thereby introduced more advanced products for their clients to increases the added-values to the company”.

Undoubtedly, the main function of such research institutions is primarily to develop products specific to the Chinese market [

52]. Nevertheless, this development suggests that the inter-firm relation in the FDI-led clusters has been transformed from the earlier stage of simplified manufacturing linkages into technology learning based on the establishment of regional R&D centers. For example, AMD set up its R&D center in Shanghai. Subsequently, Korean Hyundai Group also set up Hyundai Digital Electronics in Shanghai as its R&D base, one of its five R&D bases across the globe, for a complete series of digital products. The region has, thus, had a great technology boom, fueled first by the government’s strategic manipulation, and recently furthered by the market sales and a growing ecosystem of learning networks among the FDI-led high-tech firms.

3. Insurmountable Challenges of Indigenous Semiconductor Construction in Suzhou Globalism

Associated with the FDI-led clusters, many significant high-tech assets accumulated in Suzhou, including industrial institutions, high-tech labor pools, and, above all—the constant expansion of high-tech GPN and related markets. Nevertheless, it is still questionable whether these developments generated a favorable environment of technology learning for the construction of a domestic semiconductor industry in Suzhou. In particular, the major goal of government support for attracting FDI in Suzhou was overwhelming at facilitating exports and earning foreign reserves, rather than supporting the development of a domestic semiconductor industry. It is in the context of the FDI-dominated cluster that the program to develop an indigenous semiconductor industry was not hashed out in the globalist Suzhou. The insurmountable challenges can be seen from the following limitations of FDI-dominated globalism, high-tech enclave, and policy dilemma.

3.1. FDI-Dominated Globalism in Suzhou

Originally, the industrial policy in Suzhou was primarily intended to attract FDIs and use them to transform its old industrial structure into an export-oriented and high-tech environment. The export and foreign reserve growth were normally considered more important than indigenous high-tech industrial development. This was because the attraction of FDI, export, and GDP growth was the top priority of the government for personal promotion by city governors. As such, the globalist model of Suzhou enjoyed high exports in 2007, which were three times those of Shanghai, accounting for 15% of the national total (see

Table 1). Nevertheless, the globalism favoring FDI has overwhelmingly led to an unfair development environment for domestic firms, and even destroyed the opportunity for developing indigenous high-tech industries. A typical example is presented in Kunsan City, which is part of Suzhou.

According to Chou and Lin [

40], the city had attracted 1407 FDI enterprises, through 225,213 contracts, to invest US$ 12 billion by 2003. Export grew 131-fold, from US$ 55 million to US$ 7.2 billion from 1996 to 2003, making this one of most dynamic economic areas in the Yangtze Delta. In response to the FDI-led success, its industrial structure was substantially upgraded to emphasize foreign enterprises and high-tech industries. The existing domestic firms and industries were extensively attacked during the process. As one interviewee points out,

“The vast majority of state-owned and township enterprises were considered as in the same class as traditional low-tech and high pollution industries with limited contributions to local development, and extensively closed down during the large-scale development process of the EDTZs. Their lands and property were subsequently transferred as industrial assets used to attract the FDI”.

In terms of production values,

Table 3 shows that, as of 2004, foreign enterprises and high-tech industries were responsible for 85% and 44% of the manufacturing sectors in Kunshan, respectively. Shares of state-owned-enterprises, town-village enterprises and local private firms in Kunshan manufacturing sectors were significantly reduced to 3.7%, 7.9%, 17.2% respectively by 2000, and further to 1.0%, 1.0% and 13.1% in 2004. This means that the indigenous firms had become insignificant in the industrial structure. The domestic firms were unable to receive governmental preferences because of their limited contributions to GDP and export. Moreover, they faced unfair competitions from the FDI firms, which enjoyed many kinds of preferential support from the local government. As such, the developments of FDI clustering in Suzhou came at a price: they, not only resulted in dramatically reduced local domestic enterprises, but also stifled the space for future development of domestic industries.

Table 3.

Manufacturing in Kunshan, Suzhou (unit: US$ million) ([

40], p. 1417).

Table 3.

Manufacturing in Kunshan, Suzhou (unit: US$ million) ([40], p. 1417).

| | 2000 | 2004 |

|---|

| Total value of manufacturing sector | 5206.9 (100%) | 19,745.0 (100%) |

| State-own Enterprises (SOEs) | 190.0 (3.65%) | 203.5 (1.03%) |

| Town-Village Enterprises (TVEs) | 410.2 (7.88%) | 189.6 (0.96%) |

| Private Enterprises | 895.3 (17.19%) | 2577.8 (13.06%) |

| Foreign Enterprises | 3711.4 (71.28%) | 16,774.1 (84.95%) |

| High-tech industry | 1140.0 (21.89%) | 8753.1 (44.33%) |

| Non-high-tech industry | 4066.9 (78.11%) | 10,991.9 (55.67%) |

3.2. High-Tech Enclave Limitation

Beyond the decline in domestic enterprises, the FDI-dominated globalism has extensively generated a typical phenomenon of high-tech enclave, stifling the further development of existing indigenous local firms. As mentioned above, although the foreign investors are mostly from the high-tech sector, they are normally formulated as self-sufficient manufacturing groups, which have dramatically reduced the collaboration opportunity for the local domestic firms. In particular, Taiwanese investors normally brought their suppliers to locate in Suzhou and formulated into closed production networks, in which purchasing materials or sub-components from local firms became unnecessary. According to survey of Liu [

54], the collaborations with domestic firms are limited to the subcontracted tasks of printing and packaging, contributing only 15% of the production. This development thus confined their technology learning opportunity. In addition, the opportunity for technical diffusion is further worsened by the intensified policy competition among local governments in Yangtze Delta for attracting FDI, because they have reduced the governmental leverage to press foreign companies to purchase locally and make effective technological transfer to domestic firms [

39].

According to a large-scale survey conducted by Wei

et al. [

55], the spillover of export-oriented FDI cluster in Suzhou was very limited, showing little technology learning benefit to domestic firms. There are several further handicaps factored in the limited technology learning. According to previous research [

56,

57,

58], the joint venture, based on local cheap labor and export market, is normally regarded as having little contribution to knowledge learning and technological upgrading for Chinese firms. This is the case in the FDI-led cluster of Suzhou, overwhelmingly dominated by the export-oriented and labor-intensive sectors and, hence, has little spillover benefit to the local firms. As such, the FDI clustering in Suzhou was normally organized as “pure agglomeration”, drawing on the governmental preferences with little technology learning. It, thus, resulted in a “high-tech enclave” phenomenon, in which the knowledge spillover and learning effect were only moderate. The high-tech enclave limitation was obviously caused by the strategic manipulation of TNCs. Nevertheless, it was more importantly resulted from the government’s over-support strategies for FDI attraction, going against local existing indigenous firms.

3.3. Government Support and Policy Dilemma of Local High-Tech Development

With the strategic guidance of the “innovation country” proposed in the eleventh Five-Year Plan (2006–2010), the Suzhou city government devoted a great deal of effort to fulfill the policy of indigenous innovation (

zizhu chuangxin). However, it, realizing the autonomous innovation policy in the FDI-dominated Suzhou, turned out to be very difficult, and it was necessary to adopt a compromise approach aimed at the technology strategy of “introduction, digestion and re-innovation” when pursuing the policy of autonomous innovation. As noted by an officer from the Suzhou New District [

59]:

“The successful development of ETDZ was entirely attributed to the open development, FDI attraction and connected the high-tech benefits of technology introduction. Today, we emphasize the indigenous innovation and attempt to develop a newly industrializing road for future Suzhou. However, we still need to leverage on the globalizing strategy to extensively absorb the capitalized resources of international science and technology for our own use. So, it is necessary for us to address correctly the dialectical relations of the indigenous innovation with the “introduction, digestion and absorbing”, and amplify FDI attractions on the industrial projects of high-tech, advanced manufacturing and R&D to benefit our regional economic development and ensure the realization of whole-year FDI targets. More importantly, it also needs to use the existing FDI attraction channels to further the R&D attraction of TNCs, enhance high-tech collaborations with the regions abroad and absorb technology-intensive and knowledge-based institutions and enterprises to prompt Suzhou’s economies.”

Clearly, the city government needs to walk a fine line in developing indigenous innovation at the same time as it woos the FDIs. That is one reason why the city government has put their policy emphasis on industrial structure optimization since the mid-2000s, when the labor-intensive FDI was no longer welcomed. Subsequently, the Suzhou Science Park was changed to target the specific segments of FDI that are upstream component business, which perform a complementary function to the current industrial chain, allowing a reduction in industrial external dependence. In terms of the technology digestion and re-innovation, the strategy of “Focus on Suzhou Science City” was pursued in Suzhou New District, and the “China Software and Integrated Circuit Public Service Platform—Jiangsu Sub Centre” also established to accommodate the R&D institutions and technology enterprises of central government, including the Institute of Semiconductors, Institute of Physics in Chinese Academy of Science (CAS), the Electronics Research Institute of Ministry of Industry and Information Technology center of China Electronics Technology Group Corporation, etc. Moreover, with reference to Taiwan’s Industrial Technology Research Institutes (ITRI), the Sunan ITRI was jointly established by Suzhou Science City and CAS to improve the regional learning capacity and promote the indigenous innovation.

Nevertheless, the future of autonomous innovation through these endeavors appears very uncertain because the roles of domestic enterprises in the FDI-led clusters were very limited and they were largely crowed out the market already. All of these developments imply a policy dilemma, in which the Suzhou globalism has done extensive damage to the development opportunity of native high-tech industries, and the indigenous semiconductor has been unable to appear in the policy agenda because the high-tech enclave and huge investment risk is unaffordable for a prefecture-level city (Diji Shi) like Suzhou.

4. Indigenous Semiconductor and Strategic Coupling in Shanghai and Wuxi

As mentioned above, the pioneer programs of “Project 908” and “Project 909” were the first national experiments of the Chinese government in constructing a domestic semiconductor industry. In these programs, Shanghai HuaHong NEC and Wuxi Huajung Microelectronics were constructed through joint ventures of “market for technology” with NEC and Japanese Toshiba, respectively. The operation model of these two firms invariably followed the convention of Integrated Device Manufacturer (IDM) and ran into operation troubles. HuaHong NEC was dragged into a crisis by financial deficits, depending on government support to survive. Wuxi Huajing was even worse, since it was on the verge of bankruptcy because of insufficient operation capability, and factory facilities were entirely idle.

One major reason for the earlier failures rests in the shortage of indigenous technology and operation talent. Nevertheless, with the FDI-led ICT clustering and semiconductor growth in the Yangtze Delta, a semiconductor technology community across the Taiwan Strait was dramatically formulated and played an increasingly critical role in knowledge flow and learning about the construction and development of an indigenous semiconductor industry [

33,

42]. The formation and flow of the technological community have helped to overcome this obstacle of insufficient technology talent. As Zhang Rujing, the CEO of Shanghai SMIC, pointed out in an interview with

Cai Jing [

60] (18 February 2002):

“The significance of the Taiwanese chip industry’s investment in the mainland China does not lie in the capital it brings, but rather, in the talents and technology that come along with the investment….Only talents from Taiwan’s semiconductor industry, as a general force, can drive forward the mainland’s semiconductor industry. In fact, foreign investment has long been involved in the mainland’s chip industry, such as NEC, Motorola, Philips, and Toshiba etc. The biggest difference between these firms and SMIC is that SMIC has a strong technological team that is composed of overseas Chinese, numbering about 400. With respect to about 800 mainland employees, if one guides two, in a few years, we will build up a much bigger and stronger team.”

Obviously, knowledge sharing in the cluster does not necessarily result from official technology transfer among firms in the partnership. A significant part of this knowledge learning and flow takes place in the form of technology personnel moving between different firms and among the technology community [

33,

61]. Against this industrial context, across Taiwan Strait, the two cities of Shanghai and Wuxi have used strategic manipulation to attract semiconductor talent from Taiwan to develop their indigenous semiconductor industry, which have presented different results. In contrast, this personnel moving phenomenon between Taiwanese and domestic Chinese firms did not occur in Suzhou, because there are no domestic semiconductor firms in Suzhou.

4.1. SMIC of Shanghai

With the policy encouragement of central government to promote IC industry, the “Shanghai National Center of IC Design Industrialization” was established as the first IC design base in China. A series of high-tech policies such as the aforementioned “Priority Program for Developing the Advanced Manufacturing” and the “Eleventh Five-Year Plan for High-tech Development” were launched to support the domestic construction of high-end wafer fabrications. The policy goal was to reduce the technology gap between the Chinese semiconductor industry and the leading international firms.

The targeted semiconductor firm is Shanghai Semiconductor Manufacturing International Corporation (SMIC), a company established in 2000 by a Taiwanese operation team led by Zhang Rujing, which recruited hundreds of technicians from the Taiwan Semiconductor Manufacturing Company Limited (TSMC). He raised US$ 1.4 billion in oversea venture capital, together with US$ 450 million from the Shanghai municipal government. A total of US$ 1.8 billion were invested to set up three high-end eight-inch wafer fabrication plants. By introducing the Taiwanese model of foundry operation to replace the prevalent IDM model, SMIC separated chip design from manufacturing and focused on manufacturing.

The Zhangjiang High-tech Park has subsequently been strengthened as the new destination for semiconductor. The global packaging and testing giant, ASE Test, was attracted from Taiwan to relocate next to SMIC. Meanwhile, foreign and domestic IC design firms began to move to Shanghai. Most importantly, SMIC was translated into a state-owned enterprise and designated as Chinese symbol of national high-tech industry, enjoying many tailored preferential policies. First, the Shanghai municipal government not only provided capital investment, but also supported listing on the Hong Kong Stock Exchange to facilitate international financing. Second, the government was engaged in necessary infrastructure construction and preferential policy inputs, especially in free land provision and tax benefits by the “five free and five by half” (wumian wujianban) policy. Third, SMIC also used the policy encouragement of central government to seek opportunities of expanding their factories and branches throughout the country. In 2003, it merged Motorola’s plant in Tianjin and set up a 12-inch wafer fabrication in Beijing. Two years later, 8-inch and 12-inch wafer fabrications were established in Chengdu, Wuhan, and Shenzhen. In practice, SMIC only exported its technology and manager talents, while the real investments of these branches were from the local governments. This expansion model of local funding is referred to as the “SMIC Model”. Starting from 2000, the SMIC has rapidly become the world’s third largest foundry company behind the TSMC and UMC.

4.2. CSMC of Wuxi

Based on the support of “Project 908”, Wuxi Huajing undoubtedly was the first domestic semiconductor in the city. However, it was soon troubled by its business operations and plunged into a deep deficit of RMB 250 million, endangering the entire Huajing Group. In order to deal with the non-profitable assets, Wuxi city government rented out unused buildings and factory equipment with a monthly rental of RMB 51,000 to CSMC Semiconductor, a state-owned-firm registered in Hong Kong and run by the operation team of Chen Zhengyu, a former CEO of Taiwanese semiconductor firm (Mosel Vitelic Inc., Hsinchu, Taiwan). In 1999, CSMC and Huajing jointly set up Wuxi CSMC-HJ Semiconductor, in which CSMC obtained 51% of the stock share for its technology talent inputs and Huajing received 49% for its factory and equipment investments, and then it was reorganized as the China Resources CSMC, enjoying strategic support from the Wuxi city government, such as free land and ensuring water and electricity supply in Wuxi New District. Moreover, as Chou

et al. [

42] has pointed out, local resources were also mobilized to support CSMC operations, including spin-offs from the state-owned enterprises and research institutes. Examples include Wuxi i-CORE Electronics, a spin-off of the No. 58 Research Institute of China Electronics Technology (Group) Corporation, and China Resources Semico, a spin-off of China Resources. In addition, the CSMC and collaborative design firms were authorized by the central government as high-tech firms to enjoy specific subsidies and long-term favorable taxation. The preferential VAT rate for those authorized firms is 3%, instead the national 17%, a substantial 14% tax reduction. Subsequently, CSMC became the largest six-inch wafer foundry in China. CSMC not only earned profits in first year but also promoted the clustering development of domestic semiconductor industry in Wuxi. In terms of market linkage, Wuxi’s design firms were mainly domestic firms, which received business orders from consumer electronics firms in the Pearl River Delta, and the manufacturing order was sub-contracted to CSMS. The testing and packaging works were done by Taiwanese Greatek Electronics in Suzhou, Sigurd Microelectronics in Wuxi and more recently the CSMC-owned subsidiary. The Wuxi New District has, hence, become the development base of domestic semiconductor where the industrial chain is relatively mature, including: IC design, manufacturing of three-inch to six-inch wafers, packing and testing, and downstream consumer electronics chip manufacturing. The region has, thus, enjoyed a small-scale domestic semiconductor boom, fueled by CSMC setting up and a growing domestic market of consumer electronics in China.

5. Government Supports and Sustainability of Indigenous Semiconductors in Shanghai and Wuxi

The development and construction of an indigenous semiconductor industry has not been accidental in Shanghai and Wuxi. Instead, they are growing within a series policy encouragement of central government and developed by different manipulation of local government supports, and have had different trajectories and results. The discussions below thus compare their development trajectories and challenges (

Table 4).

5.1. Nationalist Model of Shanghai

The policy to construct an indigenous semiconductor industry in Shanghai is primarily targeted to catch up the manufacturing technology of world leading firms and, hence, realize the political goal of having a place in the high-tech territory. There is little doubt that the biggest push to be the cornerstone of the indigenous semiconductor industry lies in SMIC. Shanghai, thus, strategized to incorporate the Taiwanese-invested SMIC into a state-owned enterprise so as to shorten the technological learning process and solve the thorny problem of factory operations. Coddled by the almost-automatic provision of government support, would SMIC retain a sustainable capacity to development? Further thorny questions of technology learning and operation cast doubt on SMIC’s ambitious development timelines.

The FDI clustering in the Yangtze Delta does bring SMIC with market opportunity and technology transfer of relatively advanced manufacturing through the technology licensing and manufacturing subcontracting from the world leading firms. In 2001, SMIC became the first eight-inch chip maker in China by technological collaboration with the third largest foundry semiconductor, Singaporean Chartered Semiconductor. Subsequently, it signed a cooperation agreement with Texas Instruments, and acquired technology transfers and subcontracting agreements in 2003 with the world leading firms, including Elpida and Toshiba from Japan and Infineon Technologies from Germany. All of these arrangements presented SMIC with the opportunity to acquire the manufacturing technology, and more importantly access to the subcontracting markets dominated by the leading firms. As such, the options of equity for the technology and manufacturing capacity for subcontracting orders (guquan huan jishu, channeng huan dingdan) are extensively used by SMIC as the development strategy for slotting into the global production networks, which are overwhelmingly dominated by the world leading firms. By 2008, it acquired a substantial amount of technology licensing and subcontracting arrangements with 60 international companies, especially with an eye towards technology transfer, subcontracting works and selling its products to global markets.

Table 4.

Comparison of Government Support Models in Shanghai and Wuxi.

Table 4.

Comparison of Government Support Models in Shanghai and Wuxi.

| | Nationalist Model | Pragmatic Model |

|---|

| City | Shanghai | Wuxi |

| City status | Municipality | Prefecture-Level city |

| Government support and policy goal | Strong government support on financial and infrastructure investments; | Strong government support on infrastructural investments, but relatively weak on financial supports; |

| Political declaration of having a place in high-tech territory by catching up with advanced technology of the world leading firms | Economic temptation to solve the financial crisis of state-owned enterprises caused by the high-tech legacy of “Project 908” |

| Development trajectory | | |

| Targeted domestic firm | SMIC run by Taiwanese semiconductor | CSMC run by Taiwanese semiconductor |

| Market positioning | High-end semiconductors of 8-inch to 12-inch wafers for global high-tech markets | Low-end semiconductors of 3-inch to 6-inch wafers for Chinese home appliances |

| Operation strategies | Equity for the technology and manufacturing capacity for subcontracting orders (guquanhuanjishu, channenghuandingdan) | Complementary linkages with the world leading firms in the market, technology and equipment |

| Sustainable challenges | | |

| Technology learning | Technology learning handicap and institutional inertia | Technology gap between domestic and world leading technology |

| Production operation | High product defect rates and lower product quality | Vertical integration of low-end manufacturing line |

| Financial performance | Financial deficits | Profitable so far |

In turn, the strategic manipulation has accelerated SMIC to become a leading DRAM firm in the world market. Nevertheless, this development was laden with technology learning handicaps and even fell into a learning inertia, blocking its development towards an innovation enterprise. How are the technology-learning handicap and inertia formulated? It needs to be further explained. Firstly, the technology licensing arrangement may be seen as a strategy leveraged by SCMI to introduce advanced technology to its production, but most of the world’s leading firms are normally reluctant to transfer their leading-edge technologies, because of concern with future competition. The progression of technology learning was, hence, limited. Beyond that, a more important question lies in the problems of absorption capability and institutional proximity. In other words, the resultant performance of knowledge learning and flow in the technology licensing primarily hinges on the absorptive capacity of SMIC. As many studies argue [

62,

63,

64], this absorption capacity, however, is primarily determined by the dimension of institutional proximity. As Gertler [

4] points out, the institutional proximity normally includes the common norms, traditions, values and routines that grow out of common experience frameworks and institutions within a national setting (p. 91). Bathelt

et al. [

65] also argues that to successfully establish the external learning linkage requires the development of a shared institutional context which enables effective communication for joint problem-solving, technology learning and knowledge creation (p. 43). As such, it may not be proper for a new company to acquire too much technology licensing with different firms from different countries at one time, because the complicated institutional proximity can handicap the technology absorption and learning performance, resulting in high risks of costly failure in establishing the technology licensing.

These institutional handicaps have drawn SMIC into troubles in the technology learning by establishing too many learning channels from different firms and countries, involving over 60 different global leading firms. It is little wonder that SMIC has constantly been troubled by its higher product defect rate and lower product quality, comparing with its international opponents such as UMC and TSMC from Taiwan. Furthermore, the learning handicap was further worsened into an institutional inertia by its overly parsimonious expenditure on R&D. During the period from 2003 to 2005, its share of R&D investment in total capital expenditures was about 10%, much lower than TSMC’s 30% and UMC’s 25% [

66]. In turn, its manufacturing operations became almost undifferentiated activities, and particularly relied on the existing operation mode of Taiwanese technicians recruited from its opponent, TSMC. As Zhang Rujing, SMIC’s CEO admitted in an open interview [

67],

“The engineers recruited from Taiwan’s TSMC had become accustomed to the operating mode used in TSMC’s production line. So, after arriving in SMIC, they copied the operation manual of our opponents and brought in their intellectual property rights.”

It is for this reason that SMIC has since faced successive lawsuits by TSMC due to technical intrusion. In 2009, it was ultimately forced to pay out huge compensation fee of 200 million US$ and relinquish 8% of SMIC’s equity to TSMC in order to settle the dispute out of court. The result, of course, dramatically damaged its financial health, and the responsible CEO, Zhang Rujing, was forced to resign.

Obviously, the policy goal of having a place in high-tech territory by catching up with advanced technology of the world leading firms has constantly been a major political driving force for the government to support SMIC development. However, the strong support of Shanghai government does not push SMIC to establish a sustainable capacity of technology learning and innovation. On the contrary, the technology learning handicap and inertia was facilitated due to the government support. In fact, the operation of SMIC became unrealistic and different from the Wuxi model, which emphasizes complementary linkages with the world leading firms in the market and equipment. In contrast, as the leading iconic monument of indigenous semiconductor manufacturer in China, SMIC, is a firm that has closely followed the international upgrading trend in manufacturing. That is, in order to reduce the technology distance with the leading firm, SMIC is forced to follow the global upgrading in the risky investments of high-end semiconductors from eight-inch to 12-inch wafer production. As a national report comments on the development strategy of SMIC,

“Burdened by huge investment expenditure and high asset depreciation rate, SMIC does not have competitive advantages in capital, technology and cost control, over its international counterparts. Moreover, its 8-inch and 12-inch wafer products are normally used in fields like computer and mobile phone, in which the market advantages are overwhelmed by the world leading firms”.

Under fierce competition, the operations of SMIC are normally unprofitable and lack the capacity for substantial development due to the high product defect rates, lower product quality and above all huge expenditures on investment and asset depreciation. As such, SMIC has encountered a series of severe financial deficits. It lost US$102.3 million in 2002 and US$6.61 million in 2003. The SMIC, however, assumes that its huge investment and expansion will give it a scale advantage to fulfill the national policy, and use the government support to stabilize its running costs and deficits. In 2005, SMIC already had four eight-inch wafer production lines and one 12-inch wafer line, but lost 111.5 million US$ in that fiscal year. In order to maintain its position as the symbol of the Chinese indigenous semiconductor industry, the government has provided additional loans of 2.26 billion US$ (including US$ 600 million from Beijing, US$ 600 million from Shanghai, US$ 300 million from Tianjin) as rescue money for SMIC by 2007. During the 2008 financial crisis, it lost a further US$ 800 million and US$ 606 million in 2009. The nationalist model adopted by Shanghai city seems to have run into a vicious circle of expanding investments, operating deficits and growing dependences on government support. It is within the vicious circle that the severe deficit threat has in turn driven SMIC to minimize its R&D budget, and worsened the technology learning inertia into an insurmountable hurdle for the SMIC to create a sustainable development capacity.

5.2. Pragmatic Model of Wuxi

In Wuxi, the CSMC, primarily focuses on the low-end manufacturing of three-inch to six-inch wafers, and it seems to have become the first choice for government bids to construct the indigenous semiconductor industry in a city looking to fulfill its autonomous innovation policy, because of the infrastructure legacy advantage of “Project 908” and the cost-prohibitive limitation of high-end semiconductor investments for a prefecture-level city, such as Wuxi. In fact, the intervention of the Wuxi city government in developing the indigenous semiconductor primarily results from the economic temptation to solve the financial crisis of state-owned enterprises caused by the high-tech legacy of “Project 908”. As a prefecture-level city, the government has no extra money to pour into the risky investment of indigenous semiconductor firms, and, hence, imposes no extra policy requirements upon the semiconductor development, allowing the pragmatic model of CSMC to grow in Wuxi.

The pragmatic model has provided a vivid display of what is already possible to construct the indigenous semiconductor within the FDI-dominated cluster. In contrast to SMIC’s focus on the global high-tech markets, the operation of CSMC mainly produces for the domestic market of technologically mature six-inch wafers, which is generally ignored by the leading international firms, even though it is widely utilized in TVs, audio systems, DVDs, MP3 players, electronic game players, communication devices, and other Chinese home appliances.

Thanks to the rise of the home alliance industry, especially in the Pearl Delta, the low-end wafer demands have increased dramatically, at a high rate of 23.8%, which has been a great benefit to the growth of CSMC. Apart from the market complementarities, the pragmatic Wuxi model has also presented a further advantage in the complementary linkages of technology and equipment with the leading international firms. In fact, CSMC began from the low-end manufacturing of three-inch, four-inch, five-inch and six-inch wafers, and developed on the basis of matured technology and second-hand equipments. As the CEO of CSMC, Chen Zhengyu, said in the interview of

21st Century Business Herald [

68],

“To reduce capital expenses, the CSMC purchased second-hand 6-inch wafer manufacturing equipment from Singapore Chartered Semiconductor, saving 2/3 of the cost for constructing factories. Since the manufacturing equipment costs makes up 70%–80% of overall investments in a wafer fabrication planet, the equipment expenditure is usually a heavy burden on a company. Due to high equipment depreciation rate, it normally takes at least 5 years for a new wafer fabrication planet to balance its fiscal investments. With the worsening competition in the international semiconductor market, significant international semiconductor companies have closed down their low-end wafer fabrication planets and shifted to the high-end market. Subsequently, they also gave up the manufacturing of low-end products that were still in demand. This trend presented a much-needed development opportunity for China’s semiconductor industry.”

In fact, a successful cluster of firms typically has global connections through which knowledge and technology can be effectively attained. Most researchers agree that the global external connections undoubtedly constitute a critical element in successful firm development [

63,

64,

69]. However, the key point for this does not rest in the connection, but rather in the kind of linkages and the relationships. As Bresnahan

et al. [

70] point out in their cluster research, the complementarities of market linkages are of particular importance to nascent technology firms, as it is unlikely that these firms will directly challenge the market advantages of the world leading firms. The external linkages, however, are multi-faceted ones, which not only include market linkages, but also contain complementary flows of technology, equipment-embodied knowledge and managerial labor. As Chou

et al. [

42] observe, what CSMC gained through the equipment linkage was far more than cost saving, because through purchasing the second-hand equipment, they also obtained the learning effect of equipment-embodied technology transmission, consumer base and market share. In other words, the acquisition of old equipment, and connected technology licenses, customer resources and market shares, especially from the Singapore Chartered Semiconductor, thus enabled CSMC to build up its overseas connections and test platform for furthering market expansion. These paired relations of multi-external complementarities and connections are thus constituted as opportunity structures for the CSMC to succeed. They are also fundamental to the transmission of technology and knowledge in the local milieu, especially for those germinating regions lacking local industrial infrastructure, technology, talents, and business services. As such, this was a different story in contrast to the above Shanghai case. The foreign technology and licenses purchased by SMIC did not bring it with a good performance on the learning and overseas connections, because SMIC produced similar products and extensively competed with TNCs, leading the learning and licenses to became unrealistic (see above discussions for details).

Though still far from the mainstream, CSMC has grown well so far to infer its intrinsic value. As Chou

et al. [

42] further add, it retains in Wuxi the value it creates in the form of profit, which in turn reinforces itself and Wuxi’s semiconductor industrial chain as a whole, further supporting the local development. That is, CSMC has subsequently facilitated a vertical integration strategy by expanding its operations from the wafer manufacturing to the designing and packaging sectors by further establishing the China Resources Semico, CSMC six-inch wafer foundry and CSMC ANST Technologies. In the 2008 global financial crisis year, its production capacity was further upgraded and expanded by purchasing an eight-inch wafer manufacturing line from Korean Hynix in Wuxi. As such, the pragmatic model has increasingly consolidated its development with the domestic markets, allowing CSMC to strengthen its operation team, construct the technology capacity, and it ultimately may be translated into a constant force to stimulate the development of domestic semiconductor industries in Wuxi.

6. Discussion and Conclusions

With reference to the local experiments by the cities of Suzhou, Shanghai and Wuxi in Yangtze Delta, this paper demonstrates the local varieties of development paths to the possibility of indigenous semiconductor construction by government supports within the FDI-dominated clusters. Based on the different experiences of these clusters, there are two important lessons for the NICs. The first policy lesson is that the government may apply its policy support to attract FDI for high-tech clustering, but this may not bring the opportunity and have a positive impact on industrial sustainability for the indigenous enterprises. It is found that, in the globalization process of high-tech industries, the three local governments of Yangtze Delta have extensively mobilized their policy resources to attract a large number of FDIs and ICT clustering towards their territories. Subsequently, the international heavyweight semiconductors follow their footsteps in order to avoid heavy taxation, deliver just-in-time services, and provide quick response to problem-solving requests from local clients. It is within this intensified competition that the foreign firms recently have accelerated their inter-firm collaboration networks in the Yangtze Delta, through which the technological learning and knowledge diffusion are extensively generated among the FDI-led firms. This clustering evolution of FDI from manufacturing to technological learning is also deepened by further deployment of international R&D institutions. Nevertheless, the FDI-dominated networks in Yangtze Delta do not necessarily bring the opportunities of production collaboration and technological learning for the indigenous firms. Instead, the technological enclaves were created as close partnerships among FDIs’ firms have excluded the indigenous participation in their production networks. A typical example is presented in the case of Suzhou.

The second policy lesson for the NICs is that sustainable development of indigenous semiconductor industries with the FDI-dominated cluster may start from following three interrelated elements—(1) a pragmatic goal of government support; (2) complementarities with the international leading firms in the market, technology, and equipment linkages; and (3) sustainable capacity of technological learning to drive local developments. Among these, how the government defines an appropriate policy to facilitate sustainable capacity of domestic local firms in technology learning and cooperative operation, and subsequently promotes local industry to achieve the goals of sustainable development is a key influence. In other words, the most vital aspect is the pragmatic support of government, because this creates an institutional possibility for the indigenous firm to construct complementary linkages with the international leading firms in the market, technology and equipment, and develop sustainable capacity of technological learning to pragmatically drive local developments.

In fact, the different models and consequences of local semiconductor industries experimented in the FDI-dominated clusters largely result from the different operations of government support. Nevertheless, this discrepancy does not lie in the differences in the strategic attractions to FDI, because the multi-pronged initiatives of land provision, tax benefits, bank loans and technological talent attraction are commonly launched to boost the clustering development. Their difference is determined on whether the policy goal of government support is sufficiently realistic and pragmatic. In particular, the government support to domestic enterprises is deeply involved with political purposes and considerations, which may result in unrealistic policy goal as well as affect domestic enterprises’ operation and development strategies. Above all, once the policy privileges are manipulated to overprotect the domestic enterprises, their capability construction of technological learning, market competitiveness and industrial sustainability in the FDI clustering may be jeopardized.

In Suzhou, the government support was primarily targeted to attract FDI to stimulate the growth of exports and foreign reserves. It is for this reason that the technology enclaves are created and the development opportunity in building indigenous semiconductors has been stifled. In contrast, as a municipal city with high financial strength, Shanghai is extensively driven by the high-tech nationalism of “having a place in high-tech world” to emphasize its policy goal of supporting indigenous semiconductors for reducing their technology distance from the leading semiconductor manufacturers. The government support, although it promoted SMIC as a high-tech icon and political symbol of the Chinese indigenous semiconductor industry, did not push the SMIC to construct a sustainable capacity of technology learning. Instead, the SMIC was entrapped in the institutional handicap and inertia of technology learning. However, the technology problem is just one of many challenges. Intensified stress from the equipment depreciation, high production cost, competition from the world leading firms—and worsened fiscal crisis of the firm operation—could warp its future in a Gordian knot. As entrapped within the vicious circle of long-term operating loss, reliance on government financial support and worsening the technology learning inertia, the SMIC demonstrated a limited contribution to the sustainable developments of indigenous semiconductor industries within the FDI cluster.

In contrast, the performance of pragmatic model experimented in Wuxi seems to present a different story from the nationalist Shanghai model in developing a sustainable indigenous semiconductor industry. The complementary advantage with the world leading firms is gained by the CSMC in that its manufacturing has focused on low-end products and domestic markets neglected by the world leading firms. Subsequently, the use of second-hand equipment has reduced production costs, and, recently, the manufacturing technology and equipment have been upgraded to the more advanced products of eight-inch chips. The pragmatic model adopted by Wuxi has laid down a foundation for the domestic semiconductor industries. Nevertheless, lower end technology means that there is still a technology gap between domestic and overseas technology which focuses on higher end. Thus, the Wuxi pragmatic model can prevent domestic technology to catch up with the world leading technology. Its sustainability for further development remains in challenge.

{kind=link}