Attitudes towards Tax Evasion in Turkey and Australia: A Comparative Study

Abstract

:1. Introduction

2. Literature Review

3. Methodology

3.1. Measured Variables

3.2. Descriptive Analysis

4. Results

4.1. Overall Assessment

4.2. Test on Mean Difference and Analysis

4.3. Ranking of the Statements Relative to the Views Regarding the Ethics of Tax Evasion

4.4. Comparative Analysis of the Respondent Groups and Summary of the Main Findings

5. Conclusions

Author Contributions

Conflicts of Interest

References

- Neil Brooks, and Anthony N. Doob. “Tax Evasion: Searching for a Theory of Compliant Behaviour.” In Securing Compliance: Seven Case Studies. Edited by Martin L. Friedland. Toronto: University of Toronto Press, 1990. [Google Scholar]

- Hughlene A. Burton, Stewart S. Karlinsky, and Cynthia Blanthorne. “Perception of White-Collar Crime: Tax Evasion.” Journal of Legal Tax Research 3 (2005): 35–48. [Google Scholar] [CrossRef]

- Gerrit Antonides, and Henry S. J. Robben. “True Positives and False Alarms in the Detection of Tax Evasion.” Journal of Public Psychology 16 (1995): 617–40. [Google Scholar] [CrossRef]

- Ranjana Gupta, and Robert McGee. “Study on Tax Evasion Perceptions in Australasia.” Australian Tax Forum 25 (2010): 507–34. [Google Scholar]

- International Bureau of Fiscal Documentation (IBFD). International Tax Glossary, 4th ed. Amsterdam: IBFD Publications, 2001. [Google Scholar]

- Charles Adams. Fight, Flight and Fraud: The Story of Taxation. Curacao: Euro-Dutch Publishers, 1982. [Google Scholar]

- Charles Adams. For Good or Evil: The Impact of Taxes on the Course of Civilization. London, New York and Lanham: Madison Books, 1993. [Google Scholar]

- Gordon Cohn. “The Jewish View on Paying Taxes.” Journal of Accounting, Ethics & Public Policy 1 (1998): 109–20. [Google Scholar]

- Meir Tamari. “Ethical Issues in Tax Evasion: A Jewish Perspective.” Journal of Accounting, Ethics & Public Policy 1 (1998): 121–32. [Google Scholar]

- Gregory M. A. Gronbacher. “Taxation: Catholic Social Thought and Classical Liberalism.” Journal of Accounting, Ethics & Public Policy 1 (1998): 91–100. [Google Scholar]

- D. Eric Schansberg. “The Ethics of Tax Evasion within Biblical Christianity: Are There Limits to ‘Rendering Unto Caesar’? ” Journal of Accounting, Ethics & Public Policy 1 (1988): 77–90. [Google Scholar]

- Mushtaq Ahmad. Business Ethics in Islam. Islamabad: The International Institute of Islamic Thought & the International Institute of Islamic Economics, 1995. [Google Scholar]

- Ali Reza Jalili. “The Ethics of Tax Evasion: An Islamic Perspective.” In The Ethics of Tax Evasion: Perspectives in Theory and Practice. Edited by Robert W. McGee. New York: Springer, 2012, pp. 167–99. [Google Scholar]

- Sayyid Muhammad Yusuf. Economic Justice in Islam. Lahore: Sh. Muhammad Ashraf, 1971. [Google Scholar]

- Wig DeMoville. “The Ethics of Tax Evasion: A Baha’i Perspective.” Journal of Accounting, Ethics & Public Policy 1 (1998): 356–68. [Google Scholar]

- Gueorgui Smatrakalev. “Walking on the Edge: Bulgaria and the Transition to a Market Economy.” In The Ethics of Tax Evasion. Edited by Robert W. McGee. Dumont: The Dumont Institute for Public Policy Research, 1988, pp. 316–29. [Google Scholar]

- Benno Torgler. Tax Compliance and Tax Morale: A Theoretical and Empirical Analysis. Cheltenham and Northampton: Edward Elgar, 2007. [Google Scholar]

- Vladimir V. Vaguine. “The ‘Shadow Economy’ and Tax Evasion in Russia.” In The Ethics of Tax Evasion. Edited by Robert W. McGee. Dumont: The Dumont Institute for Public Policy Research, 1998, pp. 306–14. [Google Scholar]

- Martin Timothy Crowe. The Moral Obligation of Paying Just Taxes. Washington: The Catholic University of America Press, 1944. [Google Scholar]

- Robert W. McGee. “Is Tax Evasion Unethical? ” University of Kansas Law Review 42 (1994): 411–35. [Google Scholar] [CrossRef]

- Robert W. McGee. “Three Views on the Ethics of Tax Evasion.” Journal of Business Ethics 67 (2006): 15–35. [Google Scholar] [CrossRef]

- Robert W. McGee. The Ethics of Tax Evasion: Perspectives in Theory and Practice. New York: Springer, 2012. [Google Scholar]

- Robert W. McGee, ed. “An Analysis of Some Arguments.” In The Ethics of Tax Evasion: Perspectives in Theory and Practice. New York: Springer, 2012, pp. 47–71.

- Robert W. McGee. Justifiable Homicide. Fayetteville: Create Space, 2014. [Google Scholar]

- Robert W. McGee, and Gordon Cohn. “Jewish Perspectives on the Ethics of Tax Evasion.” Journal of Legal, Ethical and Regulatory Issues 11 (2008): 1–32. [Google Scholar] [CrossRef]

- Lysander Spooner. No Treason: The Constitution of No Authority. Boston: printed by author, 1870. [Google Scholar]

- Robert Nozick. Anarchy, State & Utopia. New York: Basic Books, 1974. [Google Scholar]

- James Alm, and Benno Torgler. “Culture differences and tax morale in the United States and in Europe.” Journal of Economic Psychology 27 (2006): 224–46. [Google Scholar] [CrossRef]

- Robert W. McGee, and Galina G. Preobragenskaya. “The Ethics of Tax Evasion: A Survey of Business Students in Poland.” In Global Economy—How It Works. Edited by Mina Baliamoune-Lutz, Alojzy Z. Nowak and Jeff Steagall. Jacksonville: University of North Florida, 2006, pp. 155–74. [Google Scholar]

- Robert W. McGee, and Zhiwen Guo. “A Survey of Law, Business and Philosophy Students in China on the Ethics of Tax Evasion.” Society and Business Review 2 (2007): 299–315. [Google Scholar] [CrossRef]

- Benno Torgler, Ihsan C. Demir, Alison Macintyre, and Markus Schaffner. “Causes and Consequences of Tax Morale: An Empirical Investigation.” Economic Analysis & Policy 38 (2008): 313–39. [Google Scholar] [CrossRef]

- Sheldon R. Smith, and Kevin C. Kimball. “Tax Evasion and Ethics: A Perspective from Members of the Church of Jesus Christ of Latter-Day Saints.” Journal of Accounting, Ethics & Public Policy 1 (1998): 337–48. [Google Scholar]

- Robert W. McGee, and Marcelo J. Rossi. “A Survey of Argentina on the Ethics of Tax Evasion.” In Taxation and Public Finance in Transition and Developing Economies. Edited by Robert W. McGee. New York: Springer, 2008, pp. 239–61. [Google Scholar]

- Robert W. McGee, and Sanjoy Bose. “The Ethics of Tax Evasion: A Survey of Australian Opinion.” In Readings in Business Ethics. Edited by Robert W. McGee. Hyderabad: ICFAI University Press, 2009, pp. 143–66. [Google Scholar]

- Robert W. McGee, and Carlos Noronha. “The Ethics of Tax Evasion: A Comparative Study of Guangzhou (Southern China) and Macau Opinions.” Euro Asia Journal of Management 18 (2008): 133–52. [Google Scholar] [CrossRef]

- Robert W. McGee, Jaan Alver, and Lehte Alver. “The Ethics of Tax Evasion: A Survey of Estonian Opinion.” In Taxation and Public Finance in Transition and Developing Economies. Edited by Robert W. McGee. New York: Springer, 2008, pp. 461–80. [Google Scholar]

- Robert W. McGee, and Ravi Kumar Jain. “The Ethics of Tax Evasion: A Study of Indian Opinion.” In The Ethics of Tax Evasion: Perspectives in Theory and Practice. Edited by Robert W. McGee. New York: Springer, 2012, pp. 321–36. [Google Scholar]

- Robert W. McGee, Arsen M. Djatej, and Robert H. Sarikas. “The Ethics of Tax Evasion: A Survey of Hispanic Opinion.” Accounting & Taxation 4 (2012): 53–74. [Google Scholar] [CrossRef]

- Robert W. McGee, and Silvia López Paláu. “The Ethics of Tax Evasion: Two Empirical Studies of Puerto Rican Opinion.” Journal of Applied Business and Economics 7 (2007): 27–47. [Google Scholar] [CrossRef]

- Serkan Benk, Robert W. McGee, and Bahadir Yüzbasi. “How Religions Effect Attitudes toward Ethics of Tax Evasion? A Comparative and Demographic Analysis.” Journal for the Study of Religions and Ideologies 14 (2015): 202–23. [Google Scholar]

- Edward G. Carmines, and Zeller A. Richard. Reliability and Validity Assessment. Newbury Park: Sage Publications, 1979. [Google Scholar]

- “Australian Tax Office (ATO). ” Available online: https://www.ato.gov.au/individuals/income-and-deductions/in-detail/how-tax-works/your-notice-of-assessment/ (accessed on 18 September 2015).

{kind=link}

{kind=link}

{kind=link}

| No | Statement |

|---|---|

| 1 | Tax evasion is ethical if tax rates are too high. |

| 2 | Tax evasion is ethical even if tax rates are not too high because the government is not entitled to take as much as it is taking from me. |

| 3 | Tax evasion is ethical if the tax system is unfair. |

| 4 | Tax evasion is ethical if a large portion of the money collected is wasted. |

| 5 | Tax evasion is ethical even if most of the money collected is spent wisely. |

| 6 | Tax evasion is ethical if a large portion of the money collected is spent on projects that I morally disapprove of. |

| 7 | Tax evasion is ethical even if a large portion of the money collected is spent on worthy projects. |

| 8 | Tax evasion is ethical if a large portion of the money collected is spent on projects that do not benefit me. |

| 9 | Tax evasion is ethical even if a large portion of the money collected is spent on projects that do benefit me. |

| 10 | Tax evasion is ethical if everyone is doing it. |

| 11 | Tax evasion is ethical if a significant portion of the money collected winds up in the pockets of corrupt politicians or their families and friends. |

| 12 | Tax evasion is ethical if the probability of getting caught is low |

| 13 | Tax evasion is ethical if some of the proceeds go to support a war that I consider to be unjust. |

| 14 | Tax evasion is ethical if I can’t afford to pay. |

| 15 | Tax evasion is ethical even if it means that if I pay less, others will have to pay more. |

| 16 | Tax evasion would be ethical if I lived under an oppressive regime like Nazi Germany or Stalinist Russia. |

| 17 | Tax evasion is ethical if the government discriminates against me because of my religion, race or ethnic background. |

| 18 | Tax evasion is ethical if the government imprisons people for their political opinions. |

| Turkey (N = 291) | Australia (N = 211) | Turkey & Australia (N = 502) | |

|---|---|---|---|

| Cronbach’s alpha | 0.862 | 0.954 | 0.910 |

| Turkey | Australia | |||

|---|---|---|---|---|

| Sample Size | % | Sample Size | % | |

| Education Level | ||||

| Undergraduate | 291 | 100.0 | 107 | 50.7 |

| Graduate | - | - | 97 | 46.0 |

| Other | - | - | 7 | 3.3 |

| Unknown | - | - | - | - |

| Major | ||||

| Accounting | - | - | 178 | 84.8 |

| Business/Economics | 291 | 100.0 | 19 | 9.0 |

| Theology | - | - | 1 | 0.5 |

| Law | - | - | 5 | 2.4 |

| Other | - | - | 7 | 3.3 |

| Unknown | - | - | 1 | 0.5 |

| Age | ||||

| 15–29 | 268 | 92.1 | 175 | 82.9 |

| 30–49 | 22 | 7.6 | 29 | 13.7 |

| 50+ | - | - | 6 | 2.8 |

| Unknown | 1 | 0.3 | 1 | 0.5 |

| Gender | ||||

| Male | 130 | 44.7 | 108 | 51.2 |

| Female | 160 | 55.0 | 101 | 47.9 |

| Unknown | 1 | 0.3 | 2 | 0.9 |

| Total | 291 | 211 | ||

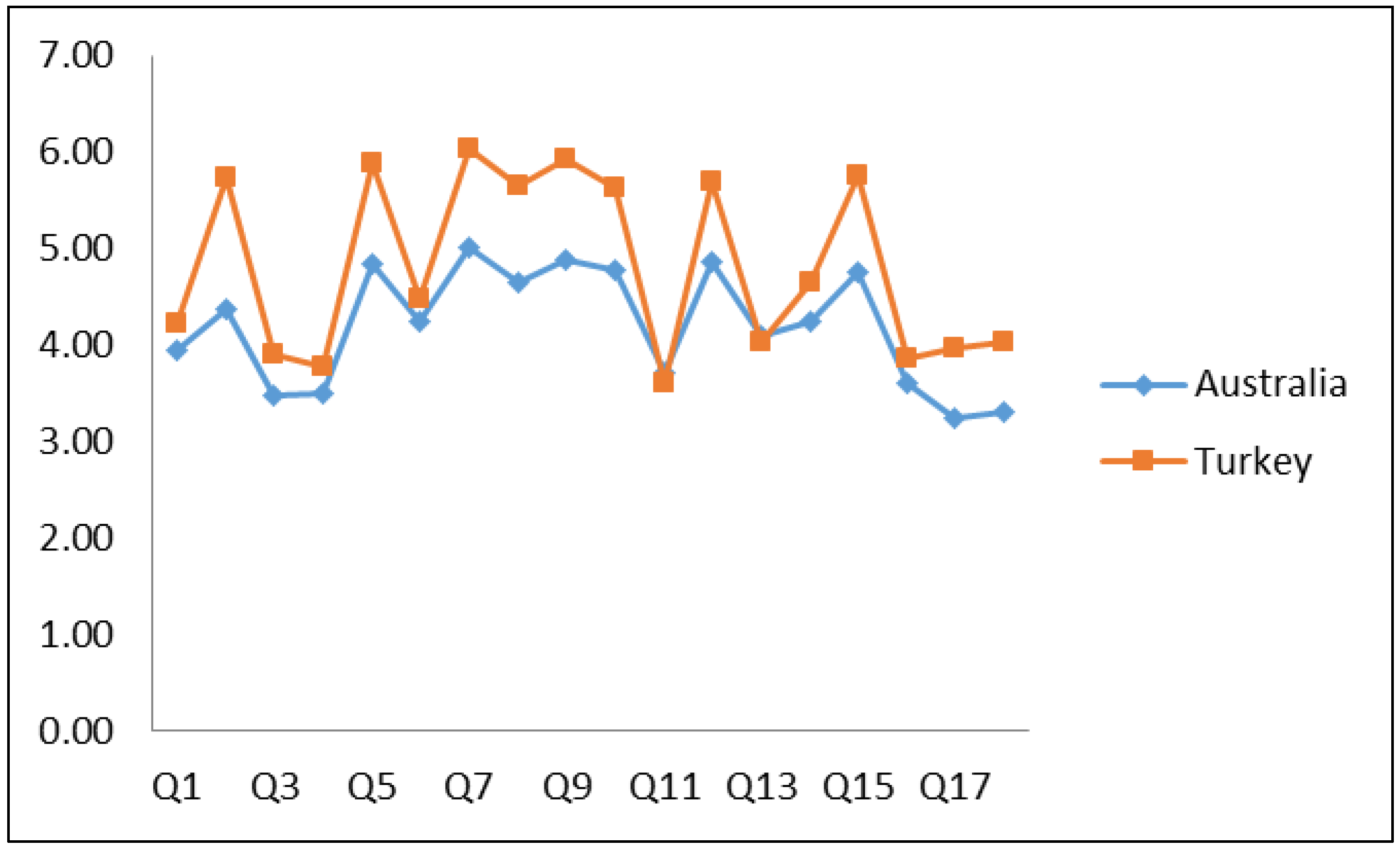

| S# | Turkey | Australia | ||

|---|---|---|---|---|

| Mean | S.D. | Mean | S.D. | |

| 1 | 4.23 | 2.204 | 3.97 | 1.678 |

| 2 | 5.73 | 1.912 | 4.37 | 1.756 |

| 3 | 3.94 | 2.112 | 3.47 | 1.626 |

| 4 | 3.77 | 2.109 | 3.51 | 1.639 |

| 5 | 5.89 | 1.778 | 4.84 | 1.744 |

| 6 | 4.48 | 2.127 | 4.25 | 1.549 |

| 7 | 6.04 | 1.604 | 5.01 | 1.668 |

| 8 | 5.66 | 1.669 | 4.64 | 1.643 |

| 9 | 5.93 | 1.682 | 4.88 | 1.670 |

| 10 | 5.63 | 1.928 | 4.77 | 1.696 |

| 11 | 3.61 | 2.423 | 3.71 | 1.775 |

| 12 | 5.70 | 1.812 | 4.87 | 1.643 |

| 13 | 4.04 | 2.278 | 4.09 | 1.636 |

| 14 | 4.65 | 2.078 | 4.24 | 1.676 |

| 15 | 5.76 | 1.641 | 4.75 | 1.672 |

| 16 | 3.86 | 2.125 | 3.60 | 1.513 |

| 17 | 3.96 | 2.221 | 3.24 | 1.554 |

| 18 | 4.04 | 2.268 | 3.30 | 1.526 |

| Mean | 4.83 | 1.998 | 4.26 | 1.648 |

| S# | (Mann-Whitney U) | (Wilcoxon W) | z-Stat | p-Value |

|---|---|---|---|---|

| 1 | 27973.50 | 49918.50 | −1.429 | 0.153 |

| 2 | 16319.00 | 38474.00 | −9.153 | 0.000 ** |

| 3 | 26879.00 | 49034.00 | −2.215 | 0.027 ** |

| 4 | 29001.50 | 50737.50 | −0.742 | 0.458 |

| 5 | 18814.50 | 40969.50 | −7.651 | 0.000 ** |

| 6 | 27462.00 | 49617.00 | −1.773 | 0.076 |

| 7 | 18064.00 | 40009.00 | −8.071 | 0.000 ** |

| 8 | 18720.50 | 40875.50 | −7.408 | 0.000 ** |

| 9 | 17712.00 | 39448.00 | −8.160 | 0.000 ** |

| 10 | 19760.00 | 40875.00 | −6.476 | 0.000 ** |

| 11 | 28097.50 | 69713.50 | −1.105 | 0.269 |

| 12 | 19820.50 | 41765.50 | −6.772 | 0.000 ** |

| 13 | 29644.50 | 70685.50 | −0.156 | 0.876 |

| 14 | 25068.00 | 45774.00 | −2.786 | 0.005 * |

| 15 | 18245.00 | 38748.00 | −7.201 | 0.000 ** |

| 16 | 28714.50 | 50869.50 | −0.975 | 0.330 |

| 17 | 25021.50 | 46966.50 | −3.140 | 0.002 ** |

| 18 | 25135.50 | 47290.50 | −3.201 | 0.001 ** |

© 2016 by the authors; licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons by Attribution (CC-BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

McGee, R.W.; Devos, K.; Benk, S. Attitudes towards Tax Evasion in Turkey and Australia: A Comparative Study. Soc. Sci. 2016, 5, 10. https://doi.org/10.3390/socsci5010010

McGee RW, Devos K, Benk S. Attitudes towards Tax Evasion in Turkey and Australia: A Comparative Study. Social Sciences. 2016; 5(1):10. https://doi.org/10.3390/socsci5010010

Chicago/Turabian StyleMcGee, Robert W., Ken Devos, and Serkan Benk. 2016. "Attitudes towards Tax Evasion in Turkey and Australia: A Comparative Study" Social Sciences 5, no. 1: 10. https://doi.org/10.3390/socsci5010010