The Relationship between AI Adoption Intensity and Internal Control System and Accounting Information Quality

Porto Accounting and Business School, Polytechnic of Porto, CEOS.PP, 4465-004 Porto, Portugal

*

Author to whom correspondence should be addressed.

Systems 2023, 11(11), 536; https://doi.org/10.3390/systems11110536

Submission received: 8 October 2023

/

Revised: 26 October 2023

/

Accepted: 27 October 2023

/

Published: 4 November 2023

Abstract

:This study develops an empirical model for accounting information systems’ quality. The paper identifies the manufacturing industry, intensity of artificial intelligence (AI) adoption and internal control system quality as critical factors for the accounting information system quality. It empirically tests their relative importance, as well as the interrelationships between each variable. We use technology domain theory as a theoretical lens because it encompasses key interrelationships between technology, organization science and cognitive processes necessary to explain the complex relationship between different organizational artifacts. A survey was conducted using managers of 381 firms from different economic sectors. The findings demonstrate a statistically significant relationship between the intensity of AI adoption and the manufacturing industry and the internal control system quality, which in turn contributes to the accounting information system quality.

1. Introduction

During the second half of the twentieth century, the outbreak of technology-intensive (TI) industries emphasized the economic importance of industrialization. According to Vaaler and McNamara [1] (p. 271) “TI industry businesses rely more on research and development and network relationships rather than physical assets and proprietary relationships”. Indeed, with technological evolution, companies began to depend heavily on innovative ideas whose origin is strongly associated with science and technology. The Internet’s emergence, combined with computers and TI development, revolutionized industrial structures and reinvented business models, giving rise to the early 21st century 4.0 Digital Economy and Industry. Although sometimes the changing process is told as being disruptive, the general truth is that, as technology advances, organizations tend to adapt, making it imperative to modify the entire organizational chain [2]. Embodying Industry 4.0., there is a wide range of fundamental concepts [3]: (i) Smart factory—the production structure will be fully equipped with sensors, actors, and autonomous systems; (ii) Cyber-physical systems—the physical and digital level merge; (iii) Existing manufacturing systems are becoming increasingly decentralized; (iv) Distribution and procurement will be increasingly individualized; (v) Open innovation approaches and product intelligence, as well as product memory, are of exceptional importance for the development of individualized products; (vi) New manufacturing systems designed to meet human needs, rather than the other way around; and (vii) Sustainability and resource efficiency at the heart of industrial manufacturing processes design. Digital transformation goes far beyond increasing productivity and efficiency, contributing to the achievement of certain social and environmental objectives, with sustainability being one of the most relevant objectives [4]. To better integrate social and environmental priorities with technological innovation, all societies must carry out a forward-looking exercise, i.e., complement and extend the hallmark features of 4.0 Industry to 5.0 Industry [5].

Meanwhile, the digital transformation of society and organizations has created substantial amounts of data that continue to grow rapidly while becoming more diverse in form, making big data ever larger, broader and faster [6]. Thus, it is not surprising that data have become one of the most valuable assets for modern organizations [7]. However, without analytical tools, data have little or no value [8]. Since AI systems help organizations “to discover complex patterns and provide automated insights drawn from the increasing amounts of data” [9] (p. 8), they are increasingly important for accounting and business management [10]. Indeed, traditional data analysis methods are insufficient and ineffective to help executives, managers and workers make informed business decisions in today’s competitive, complex and uncertain environment [11], driven by 4.0 Industry. Moreover, in a global and digital world, stakeholders require additional corporate reporting and performance information. In this context, AI emerges as a crucial technological infrastructure that helps organizations to manage this increasing amount of data [12] levering digital transformation within all organizations [2], i.e., across all organizational functions, from core production activities to finance function.

AI has several branches, such as “machine learning, deep learning, speech recognition, and cognitive computing” [9] (p. 8) and has led to the development of research in various areas of knowledge. AI systems are increasingly important for business management and accounting [10]. Recently, many accounting field researchers have analyzed advances in AI [13]; although it is a recent topic, there is a growing trend in studies in this area, due to the important impact it could have on the accounting area, as well as on related areas [14,15]. For instances, Li, Haohao and Ming [16] (p. 3) explain that the link between AI and accounting, in addition to considering financial application robots, reflects the evolution of the profession and discipline, which is dependent on advances in AI. Nonetheless, their conception of accounting theories is far from being the consensus in accounting literature. Other studies have verified that accounting information systems quality and, consequently, financial information quality are essential for making economic decisions [2,15,17]. Thus, regarding empirical evidence, the literature gives support to the hypothesis that AI is positively associated with accounting information systems quality and internal control system quality, which is essential to economic decision-making [2,14,17,18].

The multiplicity of demands resulting from the increasing complexity of products and processes, “higher variability in customer demand and preferences, along with relentless competitive pressures from others in the marketplace to remain profitable” offers manufacturers an opportunity for AI’s unique capabilities over conventional tools and approaches [19] (p. 110804-2). Based on the literature, these authors suggest that since manufacturing companies gather large amounts of complex production data, AI is essential to these companies for its ability to transform complex data into actionable and insightful information.

However, it remains unclear whether companies in the manufacturing sector, compared with other sectors’ companies, adopt AI with a different intensity, and whether this intensity has an impact on the accounting information system quality and internal control system quality. This study, therefore, is timely to address this empirical gap in the literature in the Portuguese companies context.

In this study, we focus on manufacturing companies in Portugal due to their relevance in gross domestic product (GDP), as well as the fact that their products are crucial for the supply and technologies that enable or leverage activities in commerce, services, transport or agriculture.

After a topic introduction and research objectives, the theoretical framework and research hypotheses are presented. Section 3 describes the methodologies, approach and procedures, while Section 4 presents and discusses the results. Finally, the main conclusions are presented along with their implications, limitations and future research.

2. Theoretical Approach

In the information systems field, the Design Science approach has been dominant. It is a “problem-solving paradigm” [20]. Design Science seeks solutions to specific problems and applies knowledge to design solutions and, from that point of view, it can be said that design science studies problems and seeks solutions to them; in turn, these solutions are artifacts applicable to a class of problems [21] (p. 228). The study of the “artificial” universe refers to artifacts that are designed by humans, as opposed to universes that occur naturally [22]. The science of artificial universes is concerned with artifacts’ creation that accomplish their functions, achieve goals and adapt to the environment. An artifact can be anything that has been produced or invented by humanity/humankind or suffering interventions from humanity/humankind. Thus, machines, organizations, accounting and other aspects of society can be classified as artifacts. In other words, artifacts are associated with “artificial” factors which are intended to be adjusted or molded to certain objectives and depend on the environment evolution in which one lives [22]. Artifacts in a social context depend on a society’s domain of knowledge [23]. Kouzes and Mico [24] define a domain simply as a sphere of influence or control claimed by a social entity and, on these assumptions, this study will take domain theory as its theoretical lens.

In this paper, AI is interpreted as being the artifact solutions implemented and the manufacturing business processes, accounting systems and internal control systems as domains. According to Hevner [20], artifact evaluation is an important part of the research process, so that certain characteristics such as usefulness, quality and effectiveness are guaranteed. In this paper, we use the perception of companies managers’ perception about the impact of AI adoption intensity on accounting information system quality and internal control system quality and whether AI adoption is influenced by companies belonging to the manufacturing industry. According to Moudud-Ul-Huq [2] (p. 13), expert systems, like those empowered by AI, reduce supervision needs as they allow users substantial control in the search for solutions and discretion in following the system’s recommendations. This research contends that AI artifacts’ evaluation cannot stand in isolation from the organizations’ social dimension. This implies that AI solutions tools would only be advised if they are at least perceived as useful by organization actors. Then, “if the artifacts are useful, they are likely to be used and satisfy the individuals who can then presumably approach tasks with enhanced information” [25] (p. 515).

The core assumption of AI is that machines can mimic human intelligence and behavior. In other words, AI is focused on systems that act in such a way that to any observer appears intelligent [26]. Russell and Norvig [27] (p. 17) assign Alan Turing the gestation of AI, namely due to his lectures on the topic as early as 1947 at the London Mathematical Society and his article “Computing Machinery and Intelligence” in 1950. Nevertheless, Dick [28] explains that the first term use was coined during Dartmouth Summer Research Project on Artificial Intelligence conducted by John McCarthy (Dartmouth College), Marvin L. Minsky (MIT), Nathaniel Rochester (IBM) and Claude Shannon (Bell Laboratories) in 1956. Since then, research in AI has never stopped growing; from medical diagnosis to language processing, research has set out to identify formal processes that constitute intelligent human behavior to reproduce it by machines in automated ways. Nowadays, there is a preference for designing automated systems without a human base, which is expected to achieve a good performance in complex problem domains [29]. Russell and Norvig [27] identify four distinct approaches to AI that have been followed by researchers: the first is to act humanly (Turing test), the second is to think humanly (cognitive modeling), the third is to think rationally (laws of thought) and the last is to act rationally (rational agent). AI researchers intend to seek ways to make machines solve existing difficulties. Thus, researchers observe how humans perform such activities and explore computational methods that humans cannot perform [29]. AI has the potential to improve human cognitive abilities and help humans to become more efficient. For example, AI can help humans to process substantial amounts of data more quickly and accurately. Additionally, AI has the potential to help humans to become better decision-makers by providing them with information that is relevant to the decision at hand.

3. Research Model and Hypotheses

Aggarwal, Mijwil, Al-Mistarehi, Alomari, Gök, Alaabdin and Abdulrhman [30] explain how AI has pervaded people’s daily activities, including industry, agriculture and medicine. The industrial sector is at the forefront of technological evolution. Rizvi, Haleem, Bahl and Javaid [31] argue that AI has encouraged automation and intelligent robots’ use to improve manufacturing processes efficiency, enhance final products quality, reduce errors and facilitate research and development (R&D). Therefore, is not surprising that the world’s annual private investment in AI has grown consistently over the last decade and has been duplicated in 2021 [32]. According to Telles et al. [33], a growth in the use of AI-based industrial automation has a positive impact on companies’ productivity index. Dremel, Herterich, Wulf, Waizmann and Brenner [34] presented the case of traditional manufacturing to demonstrate the importance of business structures and processes news to successful implementation of big data analytics.

Since the future consequences of artificial intelligence and digital technologies are still unclear, and ethical challenges in physical, cognitive, information and governance domains [35] are in their childhood, companies with a high adoption of AI tend to be open to 5.0 Industry concepts like sustainability, responsibility, safety and other development—human-centric orientations [4,33].

The Information and Communications Technology (ICT) sector is naturally the one with the highest penetration of 4.0 and 5.0 generation technologies. However, regarding traditional sectors like manufacturing, commerce, fishing, tourism, transportation and other traditional services, the literature is not clear about which sector is at the forefront. The Digital Economy and Society Index 2022 (DESI 2022), assessed by the European Commission [36], rates the manufacturing industry in sixth place. According to this document from the European Commission [36] (p. 53), “the Path to the Digital Decade target requires that more than 75% of EU companies adopt AI technologies by 2030”. The European Commission [36] shows quite a low uptake of AI technologies in European Union companies, at 8%. Yet Portugal presents 17% of enterprises using AI technologies, thus appearing among the four leading EU countries with AI technologies of more than 10%. When looking at a sectoral overview, manufacturing is behind in leading activities, like ICT and publishing, with only 7% of the Digital Economy and Society Index 2022. However, when comparing manufacturing with other traditional sectors like wholesale and retail trade, transportation and the storage and construction sector, manufacturing presents quite an interesting adoption rate of AI technologies [36] (pp. 53–54). This allows us to assume that industrial companies are on the front line when it comes to the technology adoption domain. Grounded in technology domain theory, the first research hypothesis is formulated:

H1.

Manufacturing companies show the highest intensity in adopting AI.

Research on the relevance of accounting systems in the 5.0 Industry paradigm is scarce. The era of 5.0 industrial revolution emerges “in response to the resolution of industrial revolution 4.0” [37] (p. 4916). “characterized by digitization, information transparency, connectivity, and automatism” [38] (p. 2) and it is “a new system focusing on the interaction of machines as a technology with humans” [37] (p. 4916). This new era has put AI, robotics and BD (among others) at the service of humans, where everything will be connected, and society will have to adapt to this reality.

Industrial revolutions have a significant impact on accounting, changing accounting information processing [39]. The 5.0 Industry poses major challenges for the accounting profession, requiring accountants to understand digital technologies [37] and make use of them. In this regard, Tavares et al. [38] (p. 7) refer that accounting companies and professional associations are recommending that big data, “technology, and information systems to be integrated into accounting courses to provide students the skills and knowledge needed to adapt to the data center environment”.

When incorporated into accounting, AI contributes to the reduction in accounting errors caused by humans while carrying out their functions [39]. Accounting has become a critical source of information for business [40]. Gorla et al. [39] (p. 207) refer that “organizations dependence on information systems drives management attention towards improving information systems’ quality”. Accounting information systems represent a multidimensional concept and, according to Sori [38] (p. 40), it “indicates an integrated framework within an entity (…) that employs physical resources (…) to transform economic data into financial information for; (1) conducting the firm’s operations and activities and (2) providing information concerning the entity to a variety of interested users”. In turn, accounting information system quality depends on its integration with the overall organizational information, to allow data to be obtained, recorded, stored and processed with flexibility, reliability and efficiency for decision-makers [41]. Monteiro et al. [42] (p. 4) defines accounting information system quality “as the capacity of the system to process and convert a large amount of data into quality information (financial and non-financial), with value-relevance to the decision-making process and to development of the company’s activities efficiently and effectively”. Soudani [43] evaluates companies’ accounting information systems by assessing whether they contribute to (1) financial reporting process integrity, (2) data storage in sufficient detail to accurately and fairly reflect the balance sheet value, (3) data collection that saves shareholders time and money, (4) processing data that can make a difference to a decision, helping managers in this process, (5) improving financial reporting quality and streamlining the company’s transaction process and (6) streamlining the generating financial information process, statements and overcoming human weaknesses in data processing through data automation.

The internal control system is defined by Mirnenko et al. [44] as policies, rules and measures implemented by managers, or persons in company charge, which ensure the proper functioning of internal control and aim at achieving goals, strategies, and other company specific objectives. The three main internal control objectives are defined by the COSO as: operations, reporting and compliance. The goal behind internal control systems is to achieve an organization’s overall business objectives and strategy. In this sense, AIs were a crucial part to accounting information system and internal control system quality development [16,45,46]. AI was a key technological driver for a sustainable digital transition and a smart circular economy [47]. One example was Mirzaey et al. [17] study that analyzed the role of artificial neural networks as a powerful tool to analyze complex information for decision-making. In this sense, Mirzaey et al. [17] realized that accounting information systems’ effectiveness is increased with AI. Along the same lines, Mouldud-Ul-Huq [2] mentions several decision-making theories where AI is applied, and which are related to auditing and information assurance problems. Despite this, not all applications used in these areas had the expected positive results, not achieving the desired success in internal control. Nevertheless, Moudud-Ul-Huq [2] concluded that AI improves productivity in accounting works’ auditing, namely auditing tasks and auditing analyses and decisions that include much uncertainty caused by risks and a lack of information. In the same vein, Baldwin et al. [13] report that more complex AI applications can be created to solve some audit problems. Thus, the literature suggests that the intensity of AI adoption impacts accounting information systems’ quality and the quality of internal control systems. In that sense, it seems quite reasonable to assume that AI positively impacts the internal control systems’ quality and the accounting information systems’ quality. In this context, the second and third hypotheses are formulated:

H2.

The intensity of AI adoption determines the internal control system quality.

H3.

The intensity of AI adoption determines the accounting information system quality.

We all agree about the enormous impact of fourth industrial revolution on the way organizations work. Indeed, as mentioned by Breque et al. [5] (p. 5) “sensor technologies, big data and AI are increasingly automating, interconnecting and optimizing a wide range of industrial processes”. However, the intensity of this impact is not the same for all organizations. Even within one organization, we can find some highly digital processes co-existing with rudimentary technology processes. Concerning accounting information systems, the widespread use of the Internet and the digital transformation of society and organizations caused exponential data growth, bringing new challenges to accounting, as mentioned by Gärtner and Hiebl [48]. The main debate across the accounting field, from academic researchers to professional bodies, is whether technology will lead to augmented accounting intelligence and information quality or whether it will lead to the rise of machine automation of accounting processes without any impact on the output quality?

Although the pessimistic predicts of Frey and Osborne [49] and WEF [50] about the threat of accounting profession extinction, the dominant stance in the literature is optimistic. According to Sutton [14] (p. 551), “AI’s greatest impact will not come from replacing jobs with new technologies but from changing what people do”.

Yüksel and Tan [51] predicts real-time access to information with more security, speed and transparency, favorable to large-scale decision-making automation [52,53,54]. Authors like Mosteanu and Faccia [55] argue that technology has led to a reduced risk of error (especially human error), minimal risk of fraud, automation of routine activities, large-scale data analysis, large cost savings, increased reliability of financial reporting and reduced workflow. Still, some authors express their worries about the negative side effects like the increase in the complexity of decision-making and compromise of information quality [56].

Nevertheless, there is a consensus that technology frees up accountants’ time for more value-added tasks [57], thus making them “faster; more efficient and more productive at new tasks” [9] (p. 2). It is expected that AI will help accounts to automate the routine and repetitive activities that are undertaken on a daily, weekly or annual basis, freeing them to address equalities issues and empowering their role in decision-making process [58]. Thus, according to CGMA [9], AI will positively impact the accounting role at several levels.

Internal control monitoring is a key part of the COSO’s Internal Control-Integrated Framework. The internal control system over financial reporting aims, amongst other things, to ensure sufficient confidence in financial reporting’s reliability [59]. The literature suggests that accounting reporting system quality is dependent on internal control system quality [16,18,45,46,60,61]. Indeed, there is extensive literature supporting the idea that internal control quality can impact financial statements users’ decisions, both internal (e.g., managers) and external (e.g., creditors, investors, auditors, financial analysts and other stakeholders such as customers) [62]. For instance, previews of Järvinen and Myllymäki [63] (p. 119) present empirical evidence that companies with effective internal controls have a small tendency to engage in real activities manipulation. Therefore, companies with a weak commitment to providing an effective internal control system and high-quality financial information are related to a tendency to use real methods of results management [63] (p. 119). In the same vein, Lenard, Petruska, Alam and Yu [64] (p. 47) found a “positive relationship between firms reporting internal control weaknesses and real activities manipulation”. Similarly, Clinton, Pinello and Skaife [65] (p. 303) observed that financial analysts’ forecasts tend to be less accurate in companies that reveal less effective internal control. In this regard, Hla and Teru [45] mention that accounting information system quality is influenced by internal control system quality and the existence of robust internal controls. On the other hand, the literature suggests that the IA adoption level contributes to internal control system quality and, in turn, favors accounting information system quality [2,13,16,45,46]. In this context, the fourth and last hypothesis is formulated:

H4.

Internal control system quality is a mediating variable in that it favors accounting information system quality.

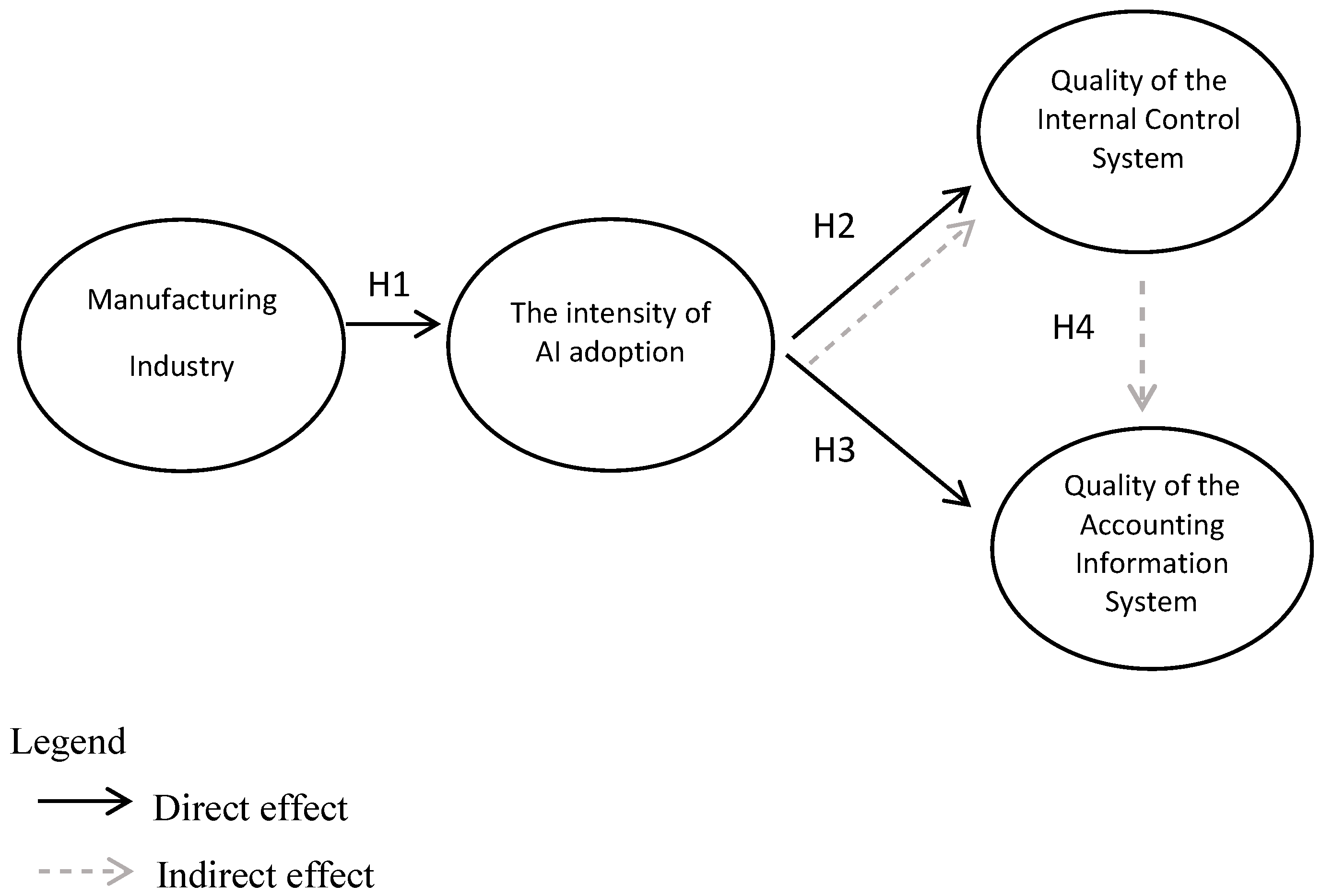

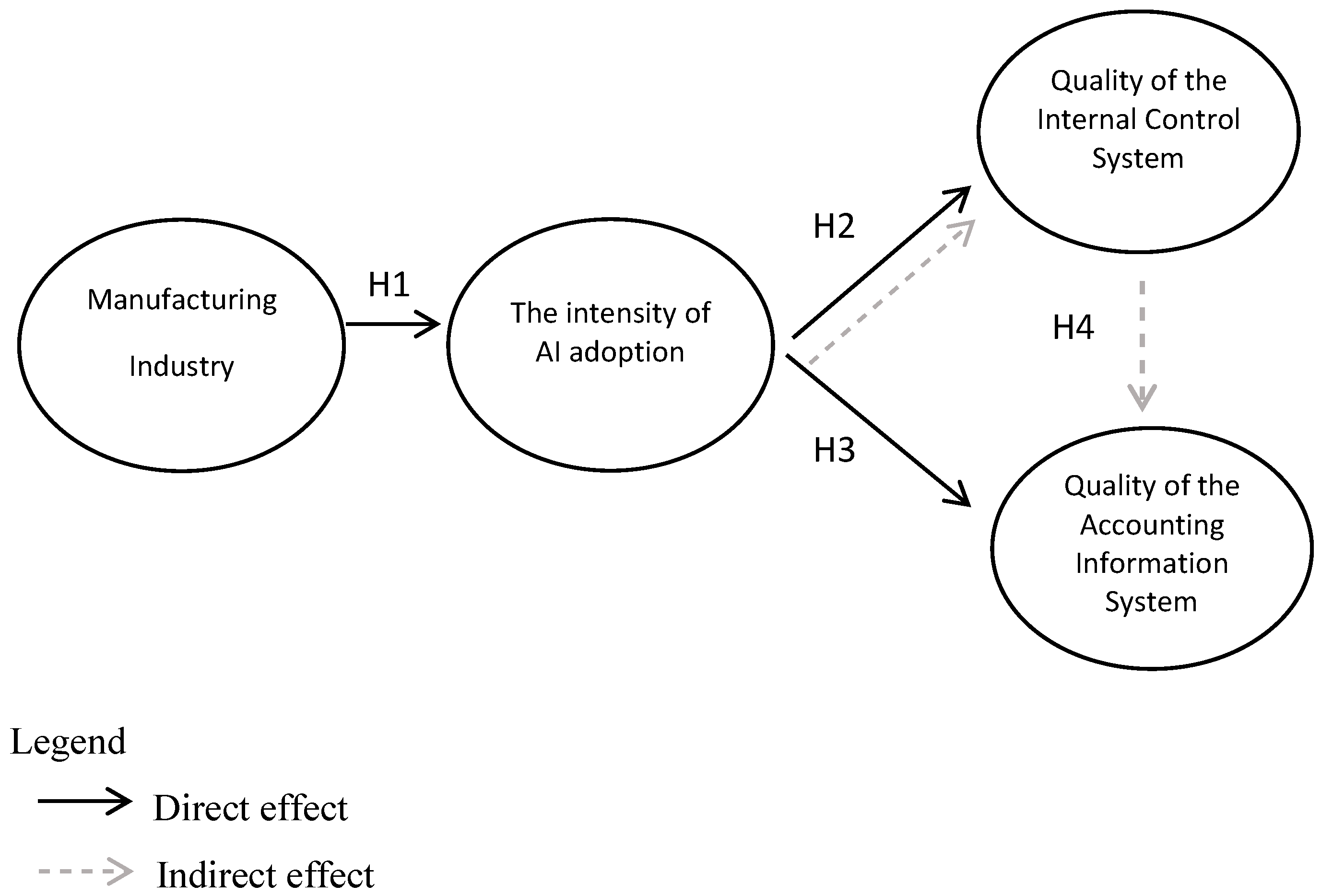

This study assumes the manufacturing industry and intense adoption of AI as antecedents to internal control system quality and accounting information system quality. The manufacturing sector is at the forefront of technological evolution [33]. We draw our research model from previous theoretical and empirical evidence about how variables relate to each other and how they impact accounting information system quality. Figure 1 shows how we find the conceptual models and the main research hypotheses’ representation.

4. Methodology

In this study, of a quantitative nature, an online survey was applied to managers (responsible for the company’s strategy and vision, who could be CEO or general directors) of Portuguese companies to evaluate the proposed theoretical model.

The questionnaire is divided into two parts. The first part includes questions that allow sample characterizing and the second part includes items that allow the evaluation of the three model dimensions (intensity of AI adoption, internal control system quality and accounting information system quality).

In this research, we used scales measured and validated or adapted from previous studies. To measure the intensity of AI adoption, we used the Chen [10] scale. The intensity of AI adoption scale is used to evaluate AI implementation in business processes in general. In assessing accounting information system dimension quality, we used Soudani’s [43] and Kpurugbara et al. [66] scales as references. One item resulted from the pre-test questionnaire (“The company’s accounting information system works efficiently and effectively”). The internal control system quality measurement scale was adopted/adapted from Phornlaphatrachakorn [67]. One item also resulted from the pre-test questionnaire (“The internal control system has quality”). Finally, the industry variable was evaluated as follows: if the company belongs to manufacturing industry sector it was scored with a 1, if it belongs to another sector, the score was 0 (zero).

The target population of this study are Portuguese companies with more than 50 employees because we intend to cover only medium and large Portuguese companies, which are those that produce a large amount of accounting data. Companies’ selection was carried out using the Iberian balance sheet analysis system (SABI) database. Therefore, the option fell to companies whose email address was available, as it was the fastest way to access emails. The SABI database generated 7812 companies. During March 2020, emails were sent, with a link to access the questionnaire, to companies on the list generated by the SABI database. Subsequently, the request for a response to the survey was reinforced with a second email (during the month of March). During the data collection process, 381 complete observations were obtained. Given the high number of existing Portuguese companies with more than 50 employees, a non-probabilistic sample was chosen, following previous studies’ methodology [68,69,70,71].

The proposed theoretical model in this study is evaluated using a structural equation model (SEM) technique. According to Marôco (2010), SEM evaluates hypotheses of causal or associative relationships between latent variables (i.e., variables that are not directly observable). SEM involves different phases in its analysis. The first refers to preliminary data analysis, which is carried out using the SPSS statistical program. This analysis consists of preparing data to be subjected to SEM analysis (analysis of missing data, outliers, data normality, etc.). The second and third phase are the SEM analysis part (measurement model analysis and structural model analysis) [69]. Measurement model analysis consists of validating the model’s constructs in individual terms through confirmatory factor analysis. The measurement scale used for each construct is analyzed in terms of (1) unidimensionality and (2) convergent, discriminate validity. The structural model evaluation consists of assessing relationships between constructs of the proposed theoretical model simultaneously and globally. SEM analysis allows for the obtainment of the model goodness-of-fit to re-specify it to achieve proper goodness-of-fit indicators.

5. Results Presentation and Discussion

5.1. Sample Characteristics

Regarding the companies’ type, according to Table 1, we found that 197 (52%) are public limited companies, 121 (32%) are private limited companies and 17 (4%) are sole proprietorships. However, 46 respondents selected the option “Other”, which represents 12%. Of these, 31 refer that they work in non-profit organizations.

Regarding activity branch, 160 (42%) and 53 (14%) companies are engaged in providing services and commercial activities, respectively, and 126 (33%) belong to the manufacturing industry. Forty two (42) (11%) companies develop activity in other sectors.

As far as size is concerned, 317 (83.2%) companies are medium- and large-sized and 64 (16.8%) are small-sized companies.

5.2. Measurement Model Evaluation

The measurement model results assessment (Table 2) indicated that in the first-order models, all items were significantly related to the factor in terms of loadings, thus confirming the construct unidimensionality. All coefficients have values above 0.60, confirming the convergent constructs’ validity [78]. The average variance extracted (VME) is greater than 0.50, which proves the existence of discriminant validity [79]. Regarding composite reliability, we found that all latent variables have values greater than 0.60, which proves the scales reliability [78]. The Appendix A explains the measurement scales application.

5.3. Structural model Evaluation

The goodness-of-fit measures indicate that the theoretical model has an adequate fit (χ2 = 158.06 (53), p = 0.000; RMSEA = 0.07; GFI = 0.93; NFI = 0.96; CFI = 0.97; PNFI = 0.78).

Figure 2 presents the standardized coefficients and significance level for each hypothesis formulated in the model, as well as the coefficient of determination for each construct. The results show that the manufacturing industry and the intensity of AI adoption are related variables (β = 0.73; p < 0.001), which leads to the support of H1 meeting Saniuk’s [4] rationale. In turn, we find that the intensity of AI adoption contributes positively to the internal control system quality (β = 0.32; p < 0.001) but has no direct relationship with the accounting reporting system quality (p > 0.05), which leads to the support of H2 and rejects H3. However, although the intensity of AI adoption does not directly contribute to the accounting information system quality, this variable is indirectly influenced by the internal control system quality (β = 0.20 (0.32 × 0.61); p < 0.001). These results are in line with the rationale of Hla and Teru [45], Li et al. [16], Bozzolan and Miihkinen [46] and Monteiro et al. [69]. The model variables contribute to 39% of the dependent variable variance of the accounting information system quality.

This research reveals a set of interesting findings that are consistent with other studies. First, the variables in the model explain 39% of the variance in the accounting information system quality. Table 3 shows the summary of estimated coefficients for the structural model and hypothesis.

6. Discussion

Based on a sample of Portuguese companies’ managers, we found that the intensity of AI adoption has a strong connection with the manufacturing industry, meeting the arguments of Saniuk [4] and the European Commission’s [36] results. According to the European Commission [36], the manufacturing industry in Portugal shows a remarkably interesting adoption rate of AI technologies compared to other industries. This empirical evidence shows that industrial companies are the ones that reveal a higher level of IA adoption, which leads to the support of the first research hypothesis. Our results suggest that manufacturing companies, because they gather large amounts of data and complex production data, adopt AI to transform complex data into actionable and insightful information.

In turn, we found that the intensity of AI adoption contributes positively to the internal control system quality. Although some studies have verified audit and information assurance problems with the implementation of AI [2], Baldwin et al. [13] indicate that AI evolution will improve these processes and correct errors, which will contribute to internal control system quality. Thus, the second hypothesis is supported in this study.

On the other hand, the third hypothesis is also supported, as the results indicate that the intensity of AI adoption is a predictive variable of accounting information system quality, where AI improve accounting information system quality and internal control system quality [16,45,46]. In this sense, and according to the foundations existing in the literature, AI adoption should be part of the company’s strategy, as it improves effectiveness and accounting information system quality and consequently the internal control system [2,13,16,45,46]. The results suggest that AI adoption reduces accounting errors committed by humans and contributes to accounting information and internal control systems’ quality [39].

In turn, we also found that internal control system quality favors the relationship between the intensity of AI adoption and accounting information system quality, which supports this study’s last hypothesis. The results are in line with the analyzed literature [2,13,16,45,46].

Thus, considering the technology domain theory, this research reveals that AI intensity adoption is a positive sphere of influence in internal control and accounting information systems in a social entity and, in this sense, it should be used [23].

Since this is the first study exploring the relationship between the activity sector, intensity of AI adoption and accounting information systems quality, our results encourage further investigations.

7. Final Considerations

The impact of the industrial and digital revolution has been substantial in every aspect of our lives, in society, in employment and business. ICT has marked the fourth industrial revolution in the manufacturing industry and other sectors, this revolution has enabled cyber-physical systems’ creation, identical to reality, changing companies’ daily life [4]. The change, via widespread digitization, has encompassed the greater efficiency of processes, greater flexibility of production and the possibility of realizing pro-social and pro-ecological goals, such as sustainable development [4]. This change only becomes possible if companies have an infrastructure with proper information technologies [12].

The industrial sector has contributed much to AI acceleration, but little time has passed between the scaling of 4.0 and 5.0 Industry. Currently, from this escalation, the high autonomy of cyber-physical systems and benefits to society are expected through the inclusion of human factors [4].

This study responds to the recent call for “more AI research in accounting” [14] (p. 68). As accounting has evolved with AI, AI systems have become increasingly important for accounting and business management [10]. Despite this, AI importance for accounting is still not well understood in the literature [13]. With a theoretical lens on technology domain theory, it aimed to develop and evaluate a theoretical model that aims to analyze the relationship between the manufacturing industry, intensity of AI adoption, internal control system quality and accounting information.

This research covers a literature gap, as it relates AI to the manufacturing industry and analyzes its impact on accounting information system quality and internal controls in Portuguese companies. Moreover, this study can help companies to accelerate the digitalization process and contribute to the digitalization of accounting and the economy.

This study is especially relevant for accountants, managers, researchers and workers as it proves the positive benefits of AI implementation in accounting and internal control systems, encouraging its adoption and, at the same time, constant learning taking into account its implementation challenges—challenges that are often not easy, generate errors and in this sense, companies must be resilient, fighting to solve problems.

The study’s results are also important for educational institutions. Considering 5.0 Industry major challenges, in particular AI adoption, it is important that higher education institutions incorporate this theme into accounting and management courses to provide their students with skills in the digital technologies field [38,43].

As for study limitations, the use of convenience and a non-probabilistic sample restricts the results’ generalizability. Regarding future studies, we suggest that the study be applied to other countries and sectors to compare results in similar contexts, despite inherent differences in each country and sector. In addition, we also suggest that this study be applied to accountants to analyze whether there are differences in perception compared to managers. Future research could analyze whether higher education institutions that teach courses in business sciences are reacting to the challenge of adapting to rapid changes brought about by the new era (Industry 5.0). We also suggest applying the same study, on a more longitudinal basis, in order to analyze the AI evolution of application with accounting information systems’ evolution.

Author Contributions

Conceptualization, A.M. and A.C.F.D.S.; data curation, A.M. and J.V.; formal analysis, A.M. and J.V.; investigation, A.M., J.V., A.C.F.D.S. and C.C.; methodology, A.M.; project administration, A.M., J.V., A.C.F.D.S. and C.C.; resources, A.M.; software, A.M.; supervision, A.M., A.C.F.D.S. and C.C.; validation, A.M., J.V., A.C.F.D.S. and C.C.; visualization, A.M., and C.C.; writing—original draft, A.M., J.V., A.C.F.D.S. and C.C.; writing—review and editing, A.M., J.V. and C.C. All authors have read and agreed to the published version of the manuscript.

Funding

This work was financed by Portuguese national funds through FCT—Fundação para a Ciência e Tecnologia, under the project UIDB/05422/2020.

Data Availability Statement

Not applicable.

Conflicts of Interest

The authors declare no conflict of interest. The funders had no role in the design of the study; in the collection, analyses or interpretation of data; in the writing of the manuscript or in the decision to publish the results.

Appendix A. Measurement Scales—Based in Likert Scales of Five Points Where: 1—I Totally Disagree and 2—I Totally Agree

| Constructs | Measurement | References |

| AI adoption intensity | The company has implemented AI in all business processes. | Chen [10] |

| The implementation of AI had a high impact on business operations. | Chen [10] | |

| The implementation of AI, taking into account its potential for the company’s business, was an extensive process. | Chen [10] | |

| The AI implementation allowed business processes to be substantially changed. | Chen [10] | |

| Internal Control System Quality | Internal control system has improved and promoted the company’s operational efficiency and effectiveness. | Phornlaphatrachakorn [67] |

| Internal control system has allowed achieving firms’ business targets, goals and objectives. | Phornlaphatrachakorn [67] | |

| Internal control system has allowed building and creating effective operations, activity and business practices. | Phornlaphatrachakorn [67] | |

| Internal control system has allowed the company to prepare financial information with quality. | Adapted from Phornlaphatrachakorn [67] | |

| Internal control system has allowed the company to prepare non-financial information with quality. | Adapted from Phornlaphatrachakorn [67] | |

| The company complies with all required regulations, i.e., laws, rules, guidelines, standards and other related issues within internal control quality. | Phornlaphatrachakorn [67] | |

| The company’s internal control system has quality. | Pre-test | |

| Accounting Information System Quality | The automated data collection speeds up the process to generate financial statements. | Adapted from Soudani [43] |

| The current accounting information system has improved the quality of non-financial reporting. | Adapted from Soudani [43] | |

| Accounting information system has contributed to the integrity of the financial information reporting process. | Adapted from Soudani [43] | |

| The accounting information system has contributed to the integrity of the non-financial information reporting process. | Adapted from Soudani [43] | |

| The data processing caused the improvement of the quality of the financial reports. | Adapted from Soudani [43] | |

| The automated data collection speeds up the process of non-financial information preparation. | Adapted from Soudani [43] | |

| The automated data collection speeds up the process to generate financial statements and overcome human weaknesses in data processing. | Adapted from Soudani [43] | |

| The automated data collection provides a platform with access to information, which facilitates the use of it. | Adapted from Kpurugbara et al. [66] | |

| The company’s accounting information system works efficiently and effectively. | Pre-test |

References

- Vaaler, P.M.; McNamara, G. Are technology-intensive industries more dynamically competitive? No and yes. Organ. Sci. 2010, 21, 271–289. [Google Scholar] [CrossRef]

- Moudud-Ul-Huq, S. The Role of Artificial Intelligence in the Development of Accounting Systems: A Review. IUP J. Account. Res. Audit. Pract. 2014, 13, 2. [Google Scholar]

- Lasi, H.; Fettke, P.; Kemper, H.G.; Feld, T.; Hoffmann, M. Industrie 4.0. Wirtschaftsinformatik 2014, 56, 261–264. [Google Scholar] [CrossRef]

- Saniuk, S.; Grabowska, S.; Straka, M. Identification of Social and Economic Expectations: Contextual Reasons for the Transformation Process of Industry 4.0 into the industry 5.0 Concept. Sustainability 2022, 14, 1391. [Google Scholar] [CrossRef]

- Breque, M.; De Nul, L.; Petridis, A. Industry 5.0. Towards a Sustainable, Human-Centric and Resilient European Industry. 2021. Available online: https://op.Europe.eu/en/publication-detail/-/publication/468a892a-5097-11eb-b59f-01aa75ed71a1/ (accessed on 15 January 2022).

- Bhimani, A. Digital data and management accounting: Why we need to rethink research methods. J. Manag. Control. 2020, 31, 9–23. [Google Scholar] [CrossRef]

- Redman, T.C. Data Driven: Profiting from Your Most Important Business Asset; Harvard Business Press: Boston, MA, USA, 2008. [Google Scholar]

- Dubey, A.; Rasool, A. Time Series Missing Value Prediction: Algorithms and Applications. In Information, Communication and Computing Technology; Springer: Singapore, 2020; pp. 21–36. [Google Scholar]

- CGMA. CGMA Competency Framework. 2019, pp. 1–78. Available online: https://www.cgma.org/content/dam/cgma/resources/tools/downloadabledocuments/cgma-competency-framework-2019-edition.pdf (accessed on 5 September 2023).

- Chen, J. The Augmenting Effects of Artificial Intelligence on Marketing Performance. Ph.D. Thesis, University of Texas at El Paso, El Paso, TX, USA, 1 January 2019. Available online: https://scholarworks.utep.edu/open_etd/1976 (accessed on 1 October 2022).

- Niu, Y.; Ying, L.; Yang, J.; Bao, M.; Sivaparthipan, C.B. Organizational business intelligence and decision making using big data analytics. Inf. Process. Manag. 2021, 58, 102725. [Google Scholar] [CrossRef]

- Autenrieth, P.; Lörcher, C.; Pfeiffer, C.; Winkens, T.; Martin, L. Current Significance of IT-Infrastructure Enabling Industry 4.0 in Large Companies. In Proceedings of the 2018 IEEE International Conference on Engineering, Technology and Innovation (ICE/ITMC), Stuttgart, Germany, 17–20 June 2018; pp. 1–8. [Google Scholar] [CrossRef]

- Baldwin, A.A.; Brown, C.E.; Trinkle, B.S. Opportunities for artificial intelligence development in the accounting domain: The auditing case. Intell. Syst. Account. Financ. Manag. Int. J. 2006, 14, 77–86. [Google Scholar] [CrossRef]

- Sutton, S.G.; Holt, M.; Arnold, V. “The reports of my death are greatly exaggerated”—Artificial intelligence research in accounting. Int. J. Account. Inf. Syst. 2016, 22, 60–73. [Google Scholar] [CrossRef]

- Nicolaou, A.I. A contingency model of perceived effectiveness in accounting information systems: Organizational coordination and control effects. Int. J. Account. Inf. Syst. 2000, 1, 91–105. [Google Scholar] [CrossRef]

- Li, C.; Haohao, S.; Ming, F. Research on the impact of artificial intelligence technology on accounting. In Proceedings of the 4th International Seminar on Computer Technology, Mechanical and Electrical Engineering (ISCME 2019), Chengdu, China, 13–15 December 2019; Volume 1486, p. 032042. [Google Scholar]

- Mirzaey, M.; Jamshidi, M.B.; Hojatpour, Y. Applications of artificial neural networks in information system of management accounting. Int. J. Mechatron. Electr. Comput. Technol. 2017, 7, 3523–3530. [Google Scholar]

- Monteiro, A.; Cepêda, C. Accounting information systems: Scientific production and trends in research. Systems 2021, 9, 67. [Google Scholar] [CrossRef]

- Arinez, J.F.; Chang, Q.; Gao, R.X.; Xu, C.; Zhang, J. Artificial intelligence in advanced manufacturing: Current status and future outlook. J. Manuf. Sci. Eng. 2020, 142, 110804. [Google Scholar] [CrossRef]

- Hevner, A.R.; March, S.T.; Park, J.; Ram, S. Design science in information systems research. MIS Q. 2004, 75–105. [Google Scholar] [CrossRef]

- Van Aken, J.E. Management research based on the paradigm of the design sciences: The quest for field-tested and grounded technological rules. J. Manag. Stud. 2004, 41, 219–246. [Google Scholar] [CrossRef]

- Simon, H. The Sciences of the Artificial, 3rd ed.; MIT Press: Cambridge, MA, USA, 1996. [Google Scholar]

- Hjørland, B.; Albrechtsen, H. Toward a new horizon in information science: Domain-analysis. J. Am. Soc. Inf. Sci. 1995, 46, 400–425. [Google Scholar] [CrossRef]

- Kouzes, J.M.; Mico, P.R. Domain Theory: An Introduction to Oganizational Behavior in Human Service Organizations. J. Appl. Behav. Sci. 1979, 15, 449–469. [Google Scholar] [CrossRef]

- Frezatti, F. The “economic paradigm” in management accounting: Return on equity and the use of various management accounting artifacts in a Brazilian context. Manag. Audit. J. 2007, 22, 514–532. [Google Scholar] [CrossRef]

- de Almeida Rocha, D.; Duarte, J.C. Simulating human behaviour in games using machine learning. In Proceedings of the 2019 18th Brazilian Symposium on Computer Games and Digital Entertainment (SBGames), Rio de Janeiro, Brazil, 28–31 October 2019; pp. 163–172. [Google Scholar]

- Russell, S.; Norvig, P. Intelligence Artificielle: Avec Plus de 500 Exercices; Pearson Education: France, Paris, 2010. [Google Scholar]

- Dick, S. Artificial intelligence. Harv. Data Sci. Rev. 2019, 1, 1–9. [Google Scholar]

- da Silva, R.J. A inteligência artificial no contexto da ciência da informação: Uma análise de domínio. Mestrado em Ciência da Informação. Master’s Thesis, FEUP, Universidade do Porto, Porto, Portugal, 2021. [Google Scholar]

- Aggarwal, K.; Mijwil, M.M.; Al-Mistarehi, A.H.; Alomari, S.; Gök, M.; Alaabdin, A.M.Z.; Abdulrhman, S.H. Has the Future Started? The Current Growth of Artificial Intelligence, Machine Learning and Deep Learning. Iraqi J. Comput. Sci. Math. 2022, 3, 115–123. [Google Scholar]

- Rizvi, A.T.; Haleem, A.; Bahl, S.; Javaid, M. Artificial intelligence (AI) and its applications in Indian manufacturing: A review. In Current Advances in Mechanical Engineering; Springer: Berlin/Heidelberg, Germany, 2021; pp. 825–835. [Google Scholar]

- NetBase Quid. AI Index Report. 2022. Available online: https://aiindex.stanford.edu/wp-content/uploads/2022/03/2022-AI-Index-Report_Master.pdf (accessed on 18 June 2023).

- Telles, E.S.; Barone, D.A.C.; da Silva, A.M. Inteligência Artificial no Contexto da Indústria 4.0. In Anais do I Workshop Sobre as Implicações da Computação na Sociedade; SBC: Porto Alegre, Brasil, 2020; pp. 130–136. [Google Scholar]

- Dremel, C.; Herterich, M.M.; Wulf, J.; Waizmann, J.-C.; Brenner, W. How AUDI AG established big data analytics in its digital transformation. MIS Q. Exec. 2017, 16, 81–100. [Google Scholar]

- Ashok, M.; Madan, R.; Joha, A.; Sivarajah, U. Ethical framework for Artificial Intelligence and Digital technologies. Int. J. Inf. Manag. 2022, 62, 102433. [Google Scholar] [CrossRef]

- European Commission. The Digital Economy and Society Index (DESI 2022). 2022. Available online: https://digital-strategy.ec.europa.eu/en/library/digital-economy-and-society-index-desi-2022 (accessed on 18 June 2022).

- Zharfan, M.; Hendra, H. Changing role of millennial accountants in the information revolution era (Industry 4.0) and challenges in the society generation scope (Society 5.0). Enrich. J. Manag. 2023, 13, 376–384. [Google Scholar] [CrossRef]

- Tavares, M.C.; Azevedo, G.; Marques, R.P.; Bastos, M.A. Challenges of education in the accounting profession in the Era 5.0: A systematic review. Cogent Bus. Manag. 2023, 10, 2220198. [Google Scholar] [CrossRef]

- Schwartz, M.S. Ethical Decision-Making Theory: An Integrated Approach. J. Bus. Ethics 2016, 139, 755–776. [Google Scholar] [CrossRef]

- Sori, Z.M. Accounting information systems (AIS) and knowledge management: A case study. Am. J. Sci. Res. 2009, 4, 36–44. [Google Scholar]

- Nguyen, H.T.; Nguyen, A.H. Determinants of Accounting Information Systems Quality: Empirical Evidence from Vietnam. Accounting 2020, 6, 185–198. [Google Scholar] [CrossRef]

- Monteiro, A.P.; Vale, J.; Leite, E.; Lis, M.; Kurowska-Pysz, J. The impact of information systems and non-financial information on company success. Int. J. Account. Inf. Syst. 2022, 45, 100557. [Google Scholar] [CrossRef]

- Soudani, S.N. The usefulness of an accounting information system for effective organizational performance. Int. J. Econ. Financ. 2012, 4, 136–145. [Google Scholar] [CrossRef]

- Mirnenko, V.I.; Tkach, I.M.; Potetiuieva, M.V.; Mechetenko, M.Y.; Tkach, M.Y.; Holota, O. Analysis of approaches to assessing effectiveness of the system of internal control of the military organization as the element of public internal financial control of Ukraine. Espacios 2020, 41, 14–20. [Google Scholar]

- Hla, D.; Susan, P.T. Efficiency of Accounting Information System and Performance Measures-Literature’ ‘Review’. Int. J. Multidiscip. Curr. Res. 2015, 3, 976–984. [Google Scholar]

- Bozzolan, S.; Antti, M. The Quality of Mandatory Non-Financial (Risk) Disclosures: The Moderating Role of Audit Firm and Partner Characteristics. SSRN Electron. J. 2019, 56, 2150008. [Google Scholar] [CrossRef]

- Fraga-Lamas, P.; Lopes, S.I.; Fernández-Caramés, T.M. Green IoT and edge AI as key technological enablers for a sustainable digital transition towards a smart circular economy: An industry 5.0 use case. Sensors 2021, 21, 5745. [Google Scholar] [CrossRef] [PubMed]

- Gärtner, B.; Hiebl, M.R. Issues with big data. In The Routledge Companion to Accounting Information Systems; Routledge: Abingdon, UK, 2017; pp. 161–172. [Google Scholar]

- Frey, C.B.; Osborne, M.A. The future of employment: How susceptible are jobs to computerisation? Technol. Forecast. Soc. Change 2017, 114, 254–280. [Google Scholar] [CrossRef]

- World Economic Forum. The Future of Jobs Report. Retrieved from Geneva. 2020. Available online: https://www.weforum.org/publications/the-future-of-jobs-report-2023 (accessed on 7 October 2023).

- Yuksel, A.S.; Tan, F.G. DeepCens: A deep learning-based system for real-time image and video censorship. Expert Syst. 2023, e13436. [Google Scholar] [CrossRef]

- Richins, G.; Stapleton, A.; Stratopoulos, T.C.; Wong, C. Big data analytics: Opportunity or threat for the accounting profession? J. Inf. Syst. 2017, 31, 63–79. [Google Scholar] [CrossRef]

- Moll, J.; Yigitbasioglu, O. The role of internet-related technologies in shaping the work of accountants: New directions for accounting research. Br. Account. Rev. 2019, 51, 100833. [Google Scholar] [CrossRef]

- Damerji, H.; Salimi, A. Mediating effect of use perceptions on technology readiness and adoption of artificial intelligence in accounting. Account. Educ. 2021, 30, 107–130. [Google Scholar] [CrossRef]

- Mosteanu, N.R.; Faccia, A. Digital systems and new challenges of financial management–FinTech, XBRL, blockchain and cryptocurrencies. Qual. Access Success J. 2020, 21, 159–166. [Google Scholar]

- Korhonen, T.; Selos, E.; Laine, T.; Suomala, P. Exploring the programmability of management accounting work for increasing automation: An interventionist case study. Account. Audit. Account. J. 2020, 34, 253–280. [Google Scholar] [CrossRef]

- Hoffman, B. Inside Terrorism; Columbia University Press: New York, NY, USA, 2017. [Google Scholar]

- Nayak, Y.D.; Sahoo, A. Towards understanding of artificial intelligence in accounting profession. Int. J. Bus. Soc. Sci. Res. 2021, 2, 1–5. [Google Scholar]

- Rubino, M.; Vitolla, F. Internal control over financial reporting: Opportunities using the COBIT framework. Manag. Audit. J. 2014, 29, 736–771. [Google Scholar] [CrossRef]

- Rashedi, H.; Toraj, D. How Influence the Accounting Information Systems Quality of Internal Control on Financial Reporting Quality. J. Mod. Dev. Manag. Account. 2019, 2, 33–45. [Google Scholar]

- Bauer, A.M.; Darren, H.; Daniel, P.L. Supplier Internal Control Quality and the Duration of Customer-Supplier Relationships. Account. Rev. 2018, 93, 59–82. [Google Scholar] [CrossRef]

- Chalmers, K.; Hay, D.; Khlif, H. Internal control in accounting research: A review. J. Account. Lit. 2019, 42, 80–103. [Google Scholar] [CrossRef]

- Järvinen, T.; Myllymäki, E.R. Real earnings management before and after reporting SOX 404 material weaknesses. Account. Horiz. 2016, 30, 119–141. [Google Scholar] [CrossRef]

- Lenard, M.J.; Petruska, K.A.; Alam, P.; Yu, B. Internal control weaknesses and evidence of real activities manipulation. Adv. Account. 2016, 33, 47–58. [Google Scholar] [CrossRef]

- Clinton, S.B.; Pinello, A.S.; Skaife, H.A. The implications of ineffective internal control and SOX 404 reporting for financial analysts. J. Account. Public Policy 2014, 33, 303–327. [Google Scholar] [CrossRef]

- Kpurugbara, N.; Akpos, Y.E.; Nwiduuduu, V.; Tams-Wariboko, I. Impact of accounting information system on organizational effectiveness-a study of selected small and medium scale enterprises in Woji, Portharcourt. Int. J. Res. Bus. Manag. Account. 2016, 2, 62–72. [Google Scholar]

- Phornlaphatrachakorn, K. Internal control quality, accounting information usefulness, regulation compliance and decision-making success: Evidence from canned and processed foods businesses in Thailand. Int. J. Bus. 2019, 4, 198–215. [Google Scholar]

- Monteiro, A.P.; Vale, J.; Silva, A.; Pereira, C. Impact of the internal control and accounting systems on the financial information usefulness: The role of the financial information quality. Acad. Strateg. Manag. J. 2021, 1–13. [Google Scholar]

- Montenegro, T.M.; Rodrigues, L.L. Determinants of the attitudes of Portuguese accounting students and professionals towards earnings management. J. Acad. Ethics 2020, 18, 301–332. [Google Scholar] [CrossRef]

- Ainur, A.K.; Sayang, M.D.; Jannoo, Z.; Yap, B.W. Sample Size and Non-Normality Effects on Goodness of Fit Measures in Structural Equation Models. Pertanika J. Sci. Technol. 2017, 25, 2. [Google Scholar]

- Byrne, B. Structural Equation Modeling with LISREL, PRELIS and SIMPLIS: Basic Concepts, Applications and Programming; Lawrence Erlbaum Associates: Mahwah, NJ, USA, 1998. [Google Scholar]

- Marôco, J. Análise de Equações Estruturais—Fundamentos Teóricos, Software e Aplicações, 3rd ed.; ReportNumber, Ld.: Pêro Pinheiro, Portugal, 2013; Volume XI (432), p. 24. ISBN 978-989-96763-6. [Google Scholar]

- Siguaw, J.A.; Diamantopoulos, A. Introducing Lisrel: A Guide for the Uninitiated; Introducing LISREL Sage Publications Ltd.: New York, NY, USA, 2000; pp. 1–192. [Google Scholar]

- Directive 2013/34/EU of the European Parliament and of the Council of June 26, 2013, Regarding the Annual Financial Statements, Consolidated Financial Statements and Related Reports of Certain Types of Enterprises, amending Directive 2006/43/EC of the European Parliament and of the Council and Repealing Council Directives 78/660/EEC and 83/349/EEC, Brussels. 2013. Available online: https://eur-lex.europa.eu/legal-content/RO/TXT/?uri=CELEX:32013L0034 (accessed on 4 February 2019).

- Decree-Law No. 98/2015. Alteracões ao Sistema de Normalizacão Contabilístico (Amendments to SNC). Diário República 2015, 8, 106. Available online: http://www.cnc.min-financas.pt/snc2016.html (accessed on 2 April 2023).

- Garver, M.S.; Mentzer, J.T. Logistics research methods: Employing structural equation modeling to test for construct validity. J. Bus. Logist. 1999, 20, 33–57. [Google Scholar]

- Fornell, C.; Larcker, D. Evaluating structural equation models with unobserved variables and measurement error. J. Mark. Res. 1981, 18, 39–50. [Google Scholar] [CrossRef]

- Bagozzi, R.P.; Yi, Y. On the evaluation of the structural equation model. J. Acad. Mark. Sci. 1988, 16, 74–94. [Google Scholar] [CrossRef]

- Makridakis, S. The forthcoming Artificial Intelligence (AI) revolution: Its impact on society and firms. Futures 2017, 90, 46–60. [Google Scholar] [CrossRef]

Figure 1.

Conceptual model.

Figure 2.

Structural model evaluation.

{kind=link}

{kind=link}

Table 1.

The sample characteristics.

| Sample Characteristics | Frequency | Percentage | |

|---|---|---|---|

| Legal form | Public companies | 197 | 52 |

| Private collective companies | 121 | 32 | |

| Individual companies | 17 | 4 | |

| Other | 46 | 12 | |

| Industry | Services | 160 | 42 |

| Industry | 126 | 33 | |

| Commercial | 53 | 14 | |

| Other | 42 | 11 | |

| Size * | Small-sized companies | 64 | 16.8 |

| Large-sized companies | 317 | 83.2 |

According to Directive No. 2013/34/EU [76] and Portuguese Decree-Law No. 98/2015 [77]: * Small- and medium-sized entities are considered: companies that do not exceed two of the three values: balance sheet total EUR 4,000,000 to EUR 20,000,000, turnover EUR 8,000,000 to EUR 40,000,000 and number of employees during the period 50 to 250. Large entities are considered to be companies that exceed the values of medium-sized entities, i.e., companies with a balance sheet total > EUR 40,000,000, turnover > EUR 40,000,000 and number of employees during the period >250.

Table 2.

Measurement model results.

| Construct | Sc |

|---|---|

| AI Adoption Intensity (CR = 0.97, AVE = 0.83) | |

| The company has implemented AI in all business processes. | 0.745 * |

| The AI implementation had a high impact on business operations. | 0.950 * |

| The AI implementation, considering its potential for the company’s business, was an extensive process. | 0.945 * |

| The AI implementation on allowed business processes to be substantially changed. | 0.947 * |

| Accounting Information System Quality (CR = 0.917, AVE = 0.610) | |

| The data processing causes an improvement in the financial report’s quality. | 0.864 * |

| Automated data collection speed up the process to generate financial statements. | 0.758 * |

| Automated data collection speed up the process to generate financial statements and overcome human weaknesses in the data processing. | 0.744 * |

| Automated data collection provides a platform with access to information, which facilitates its use of it. | 0.752 * |

| Internal Control System Quality (CR = 0.97, AVE = 0.83) | |

| The internal control system has improved and promoted the company’s operational efficiency and effectiveness. | 0.904 * |

| The internal control system has allowed the building and creation of effective operations, activities and business practices. | 0.834 * |

| The internal control systems have allowed the company to prepare financial information with quality. | 0.824 * |

| The company complies with all required regulations, i.e., laws, guidelines, standards and other issues related to internal control. | 0.667 * |

Notes: Sc, Standardized coefficients; CR, composite reliability; AVE, average variance extracted. * Correlation is significant at the 0.001 level.

Table 3.

Hypothesis results.

| Hypothesis | Β | p-Value | Results |

|---|---|---|---|

| H1 | 0.73 | <0.001 | ✓ |

| H2 | 0.32 | <0.001 | ✓ |

| H3 | 0.004 | >0.05 | X |

| H4 | 0.61 | <0.001 | ✓ |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Monteiro, A.; Cepêda, C.; Da Silva, A.C.F.; Vale, J. The Relationship between AI Adoption Intensity and Internal Control System and Accounting Information Quality. Systems 2023, 11, 536. https://doi.org/10.3390/systems11110536

AMA Style

Monteiro A, Cepêda C, Da Silva ACF, Vale J. The Relationship between AI Adoption Intensity and Internal Control System and Accounting Information Quality. Systems. 2023; 11(11):536. https://doi.org/10.3390/systems11110536

Chicago/Turabian StyleMonteiro, Albertina, Catarina Cepêda, Amélia Cristina Ferreira Da Silva, and Joana Vale. 2023. "The Relationship between AI Adoption Intensity and Internal Control System and Accounting Information Quality" Systems 11, no. 11: 536. https://doi.org/10.3390/systems11110536

Note that from the first issue of 2016, this journal uses article numbers instead of page numbers. See further details here.