The Evolving Research of Customer Adoption of Digital Payment: Learning from Content and Statistical Analysis of the Literature

Abstract

:1. Introduction

2. Methodology

3. Results

3.1. Theories Applied in the Literature

3.1.1. Technology Acceptance Model (TAM)

3.1.2. The Unified Theory of Acceptance and Use of Technology (UTAUT)

3.1.3. Innovation Diffusion Theory (IDT)

3.1.4. Unified Theory of Acceptance and Use of Technology Two (UTAUT2)

3.1.5. Other Theoretical Perspectives

3.2. Research Settings and Geographic Distribution of the Literature

3.3. Thematic Analysis

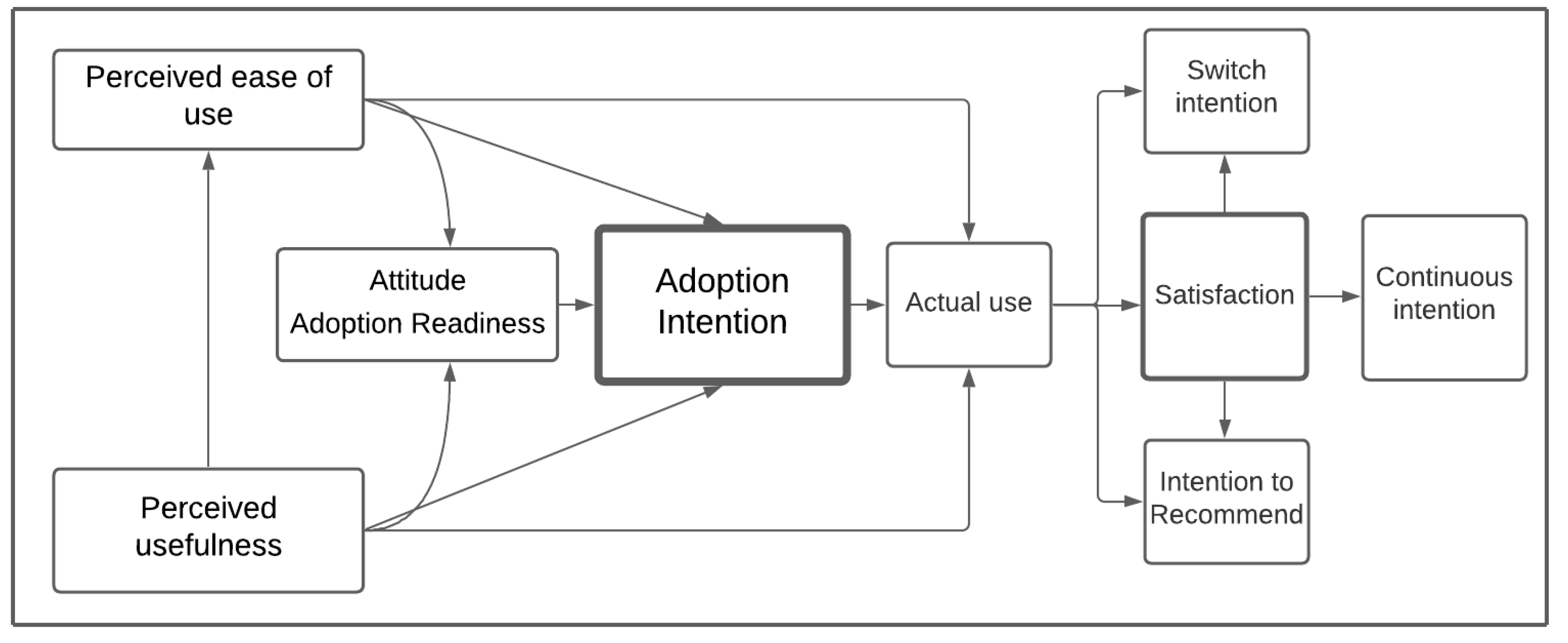

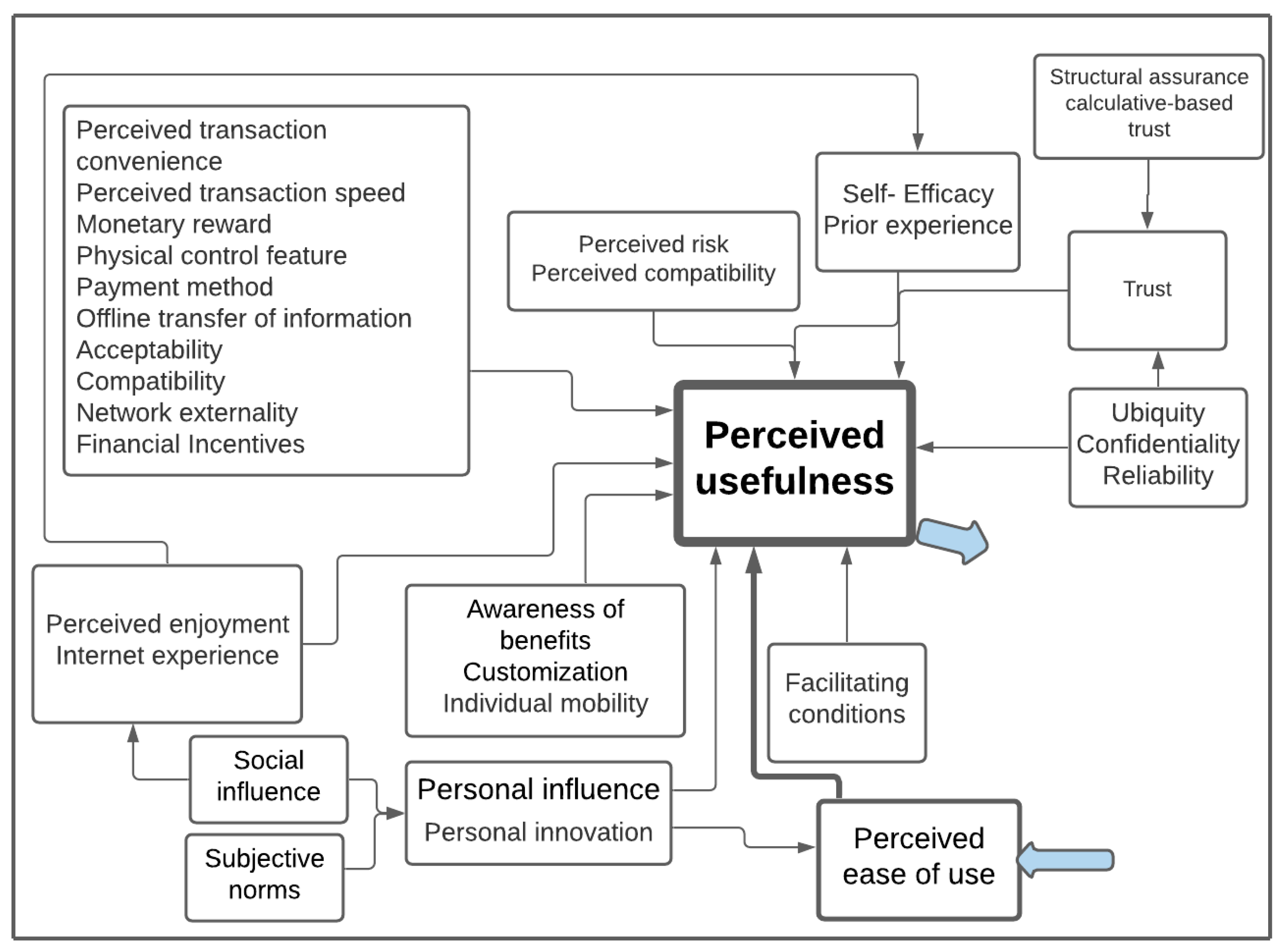

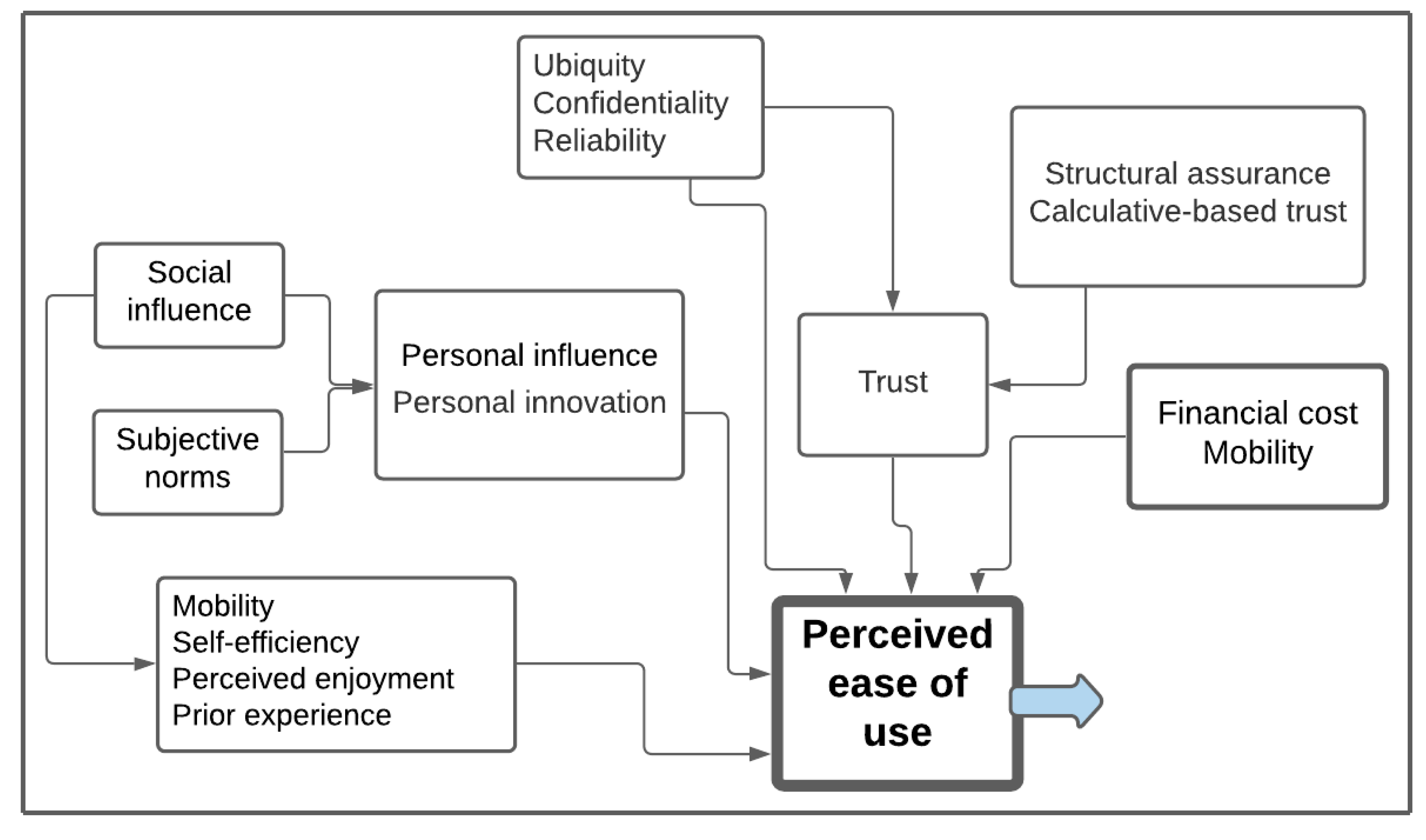

3.3.1. Adoption Attention Factors (Acceptance/Use Behavior/Usage)

3.3.2. Actual Usage Factors

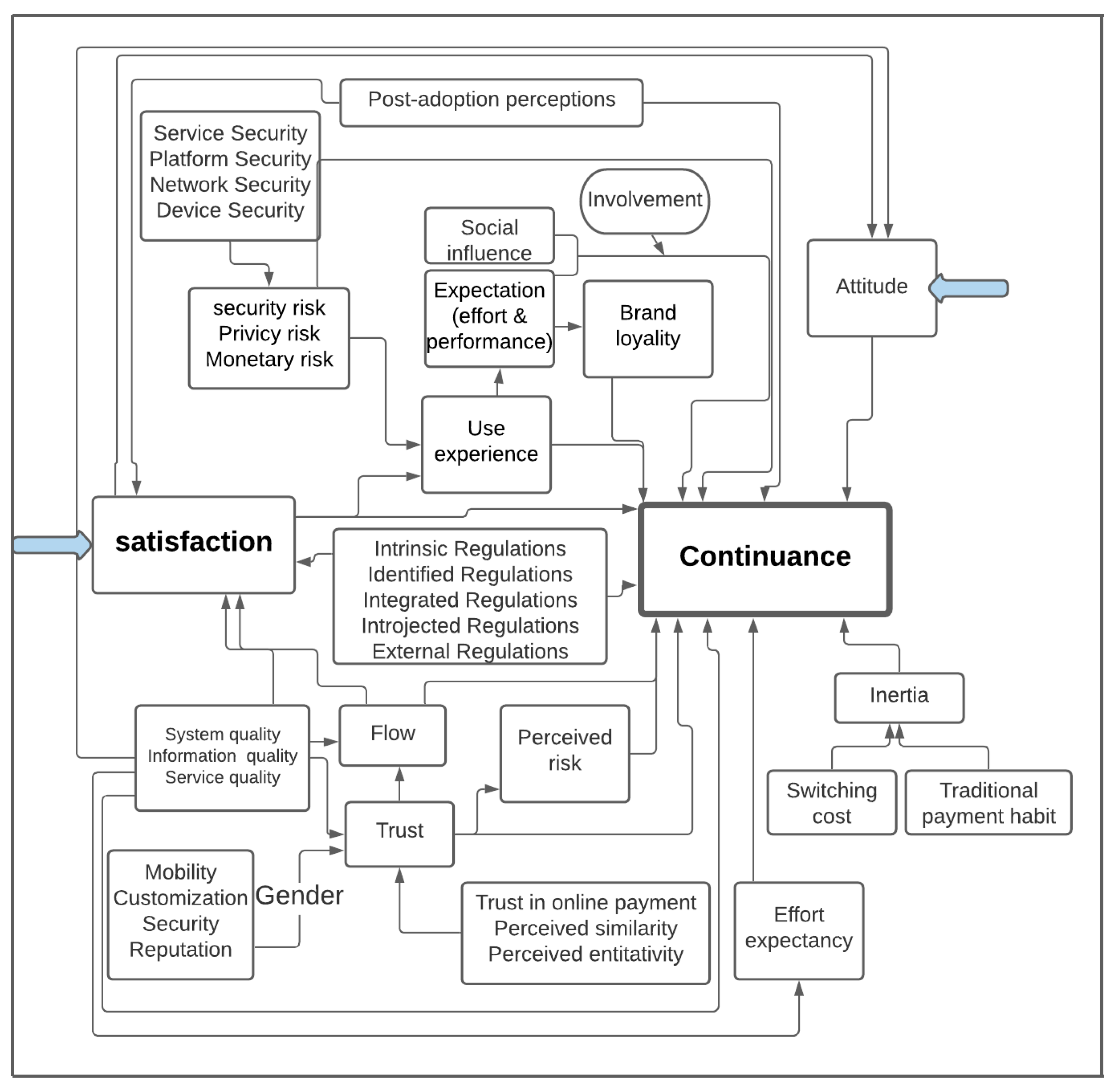

3.3.3. Satisfaction Factors

3.3.4. Continuance Factors

3.3.5. Switch or Recommend Factors

4. Discussion and Future Research Suggestions

5. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Journal Name | Number of Articles |

|---|---|

| International Journal of Bank Marketing | 19 |

| Electronic Commerce Research and Applications | 15 |

| Journal of Retailing and Consumer Services | 13 |

| International Journal of Information Management | 8 |

| Information Systems Frontiers | 8 |

| Technology in Society | 7 |

| Computers in Human Behavior | 7 |

| International Journal of e-Business Research | 6 |

| International Journal of Mobile Communications | 5 |

| Internet Research | 5 |

| Industrial Management and Data Systems | 5 |

| Information Systems and e-Business Management | 5 |

| Information and Management | 4 |

| International Journal of Electronic Finance | 3 |

| Journal of Computer Information Systems | 3 |

| Service Industries Journal | 3 |

| International Journal of Retail and Distribution Management | 3 |

| International Journal of Contemporary Hospitality Management | 2 |

| Journal of Indian Business Research | 2 |

| Economic Research-Ekonomska Istrazivanja | 2 |

| Total | 125 |

References

- Loh, X.M.; Lee, V.H.; Tan, G.W.H.; Ooi, K.B.; Dwivedi, Y.K. Switching from cash to mobile payment: What’s the hold-up? Internet Res. 2021, 31, 376–399. [Google Scholar] [CrossRef]

- Balakrishnan, V.; Shuib, N.L.M. Drivers and inhibitors for digital payment adoption using the Cashless Society Readiness-Adoption model in Malaysia. Technol. Soc. 2021, 65, 101554. [Google Scholar] [CrossRef]

- Teng, S.; Khong, K.W. Examining actual consumer usage of E-wallet: A case study of big data analytics. Comput. Hum. Behav. 2021, 121, 106778. [Google Scholar] [CrossRef]

- Kim, C.; Tao, W.; Shin, N.; Kim, K.S. An empirical study of customers’ perceptions of security and trust in e-payment systems. Electron. Commer. Res. Appl. 2010, 9, 84–95. [Google Scholar] [CrossRef]

- Lee, J.M.; Lee, B.; Rha, J.Y. Determinants of mobile payment usage and the moderating effect of gender: Extending the UTAUT model with privacy risk. Int. J. Electron. Commer. Stud. 2019, 10, 43–64. [Google Scholar] [CrossRef]

- Yang, Y.; Liu, Y.; Li, H.; Yu, B. Understanding perceived risks in mobile payment acceptance. Ind. Manag. Data Syst. 2015, 115, 253–269. [Google Scholar] [CrossRef]

- Apanasevic, T.; Markendahl, J.; Arvidsson, N. Stakeholders’ expectations of mobile payment in retail: Lessons from Sweden. Int. J. Bank Mark. 2016, 34, 37–61. [Google Scholar] [CrossRef]

- Al-Okaily, M.; Lutfi, A.; Alsaad, A.; Taamneh, A.; Alsyouf, A. The Determinants of Digital Payment Systems’ Acceptance under Cultural Orientation Differences: The Case of Uncertainty Avoidance. Technol. Soc. 2020, 63, 101367. [Google Scholar] [CrossRef]

- Bagla, R.K.; Sancheti, V. Gaps in customer satisfaction with digital wallets: Challenge for sustainability. J. Manag. Dev. 2018, 37, 442–451. [Google Scholar] [CrossRef]

- Gupta, S.; Xu, H. Examining the relative influence of risk and control on intention to adopt risky technologies. J. Technol. Manag. Innov. 2010, 5, 22–37. [Google Scholar] [CrossRef] [Green Version]

- Johnson, V.L.; Kiser, A.; Washington, R.; Torres, R. Limitations to the rapid adoption of M-payment services: Understanding the impact of privacy risk on M-Payment services. Comput. Hum. Behav. 2018, 79, 111–122. [Google Scholar] [CrossRef]

- Sinha, M.; Majra, H.; Hutchins, J.; Saxena, R. Mobile payments in India: The privacy factor. Int. J. Bank Mark. 2019, 37, 192–209. [Google Scholar] [CrossRef]

- See-To, E.W.K.; Ho, K.K.W. A study on the impact of design attributes on E-payment service utility. Inf. Manag. 2016, 53, 668–681. [Google Scholar] [CrossRef]

- Makki, A.M.; Ozturk, A.B.; Singh, D. Role of risk, self-efficacy, and innovativeness on behavioral intentions for mobile payment systems in the restaurant industry. J. Foodserv. Bus. Res. 2016, 19, 454–473. [Google Scholar] [CrossRef]

- Kapoor, K.K.; Dwivedi, Y.K.; Williams, M.D. Examining the role of three sets of innovation attributes for determining adoption of the interbank mobile payment service. Inf. Syst. Front. 2015, 17, 1039–1056. [Google Scholar] [CrossRef] [Green Version]

- Dahlberg, T.; Guo, J.; Ondrus, J. A critical review of mobile payment research. Electron. Commer. Res. Appl. 2015, 14, 265–284. [Google Scholar] [CrossRef]

- Dahlberg, T.; Mallat, N.; Ondrus, J.; Zmijewska, A. Past, present and future of mobile payments research: A literature review. Electron. Commer. Res. Appl. 2008, 7, 165–181. [Google Scholar] [CrossRef] [Green Version]

- Taylor, E. Mobile payment technologies in retail: A review of potential benefits and risks. Int. J. Retail Distrib. Manag. 2016, 44, 159–177. [Google Scholar] [CrossRef]

- Alkhowaiter, W.A. Digital payment and banking adoption research in Gulf countries: A systematic literature review. Int. J. Inf. Manag. 2020, 53, 102102. [Google Scholar] [CrossRef]

- Khatib, S.F.A.; Nour, A.-N.I. The Impact of Corporate Governance on Firm Performance during the COVID-19 Pandemic: Evidence from Malaysia. J. Asian Financ. Econ. Bus. 2021, 8, 0943–0952. [Google Scholar] [CrossRef]

- Vargo, D.; Zhu, L.; Benwell, B.; Yan, Z. Digital technology use during COVID-19 pandemic: A rapid review. Hum. Behav. Emerg. Technol. 2021, 3, 13–24. [Google Scholar] [CrossRef]

- Kraenzlin, S.; Meyer, C.; Nellen, T. COVID-19 and regional shifts in Swiss retail payments. Swiss J. Econ. Stat. 2020, 156, 14. [Google Scholar] [CrossRef]

- Khatib, S.F.A.; Abdullah, D.F.; Elamer, A.A.; Abueid, R. Nudging toward diversity in the boardroom: A systematic literature review of board diversity of financial institutions. Bus. Strateg. Environ. 2021, 30, 985–1002. [Google Scholar] [CrossRef]

- Hazaea, S.A.; Zhu, J.; Al-Matari, E.M.; Senan, N.A.M.; Khatib, S.F.A.; Ullah, S. Mapping of internal audit research in China: A systematic literature review and future research agenda. Cogent Bus. Manag. 2021, 8, 1938351. [Google Scholar] [CrossRef]

- Zamil, I.A.; Ramakrishnan, S.; Jamal, N.M.; Hatif, M.A.; Khatib, S.F.A. Drivers of corporate voluntary disclosure: A systematic review. J. Financ. Report. Account. 2021, in press. [Google Scholar] [CrossRef]

- Zhao, J.; Xue, F.; Khan, S.; Khatib, S.F.A. Consumer behaviour analysis for business development. Aggress. Violent Behav. 2021, 101591, in press. [Google Scholar] [CrossRef]

- Hazaea, S.A.; Zhu, J.; Khatib, S.F.A.; Bazhair, A.H.; Elamer, A.A. Sustainability assurance practices: A systematic review and future research agenda. Environ. Sci. Pollut. Res. 2021, 1–22. [Google Scholar] [CrossRef]

- Khatib, S.F.A.; Abdullah, D.F.; Elamer, A.; Yahaya, I.; Owusu, A. Global trends in board diversity research: A bibliometric view. Meditari Account. Res. 2021. [Google Scholar] [CrossRef]

- Khatib, S.F.A.; Abdullah, D.F.; Hendrawaty, E.; Elamer, A.A. A bibliometric analysis of cash holdings literature: Current status, development, and agenda for future research. Manag. Rev. Q. 2021, 1–38. [Google Scholar] [CrossRef]

- Kaur, P.; Dhir, A.; Singh, N.; Sahu, G.; Almotairi, M. An innovation resistance theory perspective on mobile payment solutions. J. Retail. Consum. Serv. 2020, 55, 102059. [Google Scholar] [CrossRef]

- Gong, X.; Zhang, K.Z.K.; Chen, C.; Cheung, C.M.K.; Lee, M.K.O. Transition from web to mobile payment services: The triple effects of status quo inertia. Int. J. Inf. Manag. 2020, 50, 310–324. [Google Scholar] [CrossRef]

- Teo, A.C.; Tan, G.W.H.; Ooi, K.B.; Lin, B. Why consumers adopt mobile payment? A partial least squares structural equation modelling (PLS-SEM) approach. Int. J. Mob. Commun. 2015, 13, 478–497. [Google Scholar] [CrossRef]

- Verkijika, S.F. An affective response model for understanding the acceptance of mobile payment systems. Electron. Commer. Res. Appl. 2020, 39, 100905. [Google Scholar] [CrossRef]

- Mouakket, S. Investigating the role of mobile payment quality characteristics in the United Arab Emirates: Implications for emerging economies. Int. J. Bank Mark. 2020, 38, 1465–1490. [Google Scholar] [CrossRef]

- Morosan, C.; DeFranco, A. It’s about time: Revisiting UTAUT2 to examine consumers’ intentions to use NFC mobile payments in hotels. Int. J. Hosp. Manag. 2016, 53, 17–29. [Google Scholar] [CrossRef]

- De Luna, I.R.; Liébana-cabanillas, F.; Sánchez-fernández, J.; Muñoz-leiva, F. Mobile payment is not all the same: The adoption of mobile payment systems depending on the technology applied. Technol. Forecast. Soc. Chang. 2019, 146, 931–944. [Google Scholar] [CrossRef]

- Barkhordari, M.; Nourollah, Z.; Mashayekhi, H.; Mashayekhi, Y.; Ahangar, M.S. Factors influencing adoption of e-payment systems: An empirical study on Iranian customers. Inf. Syst. E-Bus. Manag. 2017, 15, 89–116. [Google Scholar] [CrossRef]

- Madan, K.; Yadav, R. Behavioural intention to adopt mobile wallet: A developing country perspective. J. Indian Bus. Res. 2016, 8, 227–244. [Google Scholar] [CrossRef]

- Davis, F.D. Perceived Usefulness, Perceived Ease of Use, and User Acceptance of Information Technology. MIS Q. 1989, 13, 319. [Google Scholar] [CrossRef] [Green Version]

- Brohi, I.A. Factors Affecting the Acceptance of Near Field Communication Enabled Mobile Payments: An Empirical Study of Pakistan; International Islamic University Malaysia: Kuala Lumpur, Malaysia, 2019. [Google Scholar]

- Venkatesh, V.; Morris, M.G.; Davis, G.B.; Davis, F.D. User Acceptance of Information Technology: Toward a Unified View. MIS Q. 2003, 27, 425. [Google Scholar] [CrossRef] [Green Version]

- Khalilzadeh, J.; Ozturk, A.B.; Bilgihan, A. Security-related factors in extended UTAUT model for NFC based mobile payment in the restaurant industry. Comput. Hum. Behav. 2017, 70, 460–474. [Google Scholar] [CrossRef]

- Soomro, Y.A. Understanding the adoption of sadad e-payments: UTAUT combined with religiosity as moderator. Int. J. E-bus. Res. 2019, 15, 55–74. [Google Scholar] [CrossRef]

- Rogers, E.M. Diffusion of Innovations: Modifications of a Model for Telecommunications. In Die Diffusion von Innovationen in der Telekommunikation; Springer: Berlin/Heidelberg, Germany, 1995; pp. 25–38. [Google Scholar]

- Ram, S. A model of innovation resistance. ACR N. Am. Adv. 1987, 4, 208–212. [Google Scholar]

- Rogers, E.M. Diffusion of Innovations, 5th ed.; The Free Press: New York, NY, USA, 2003. [Google Scholar]

- Matemba, E.D.; Li, G. Consumers’ willingness to adopt and use WeChat wallet: An empirical study in South Africa. Technol. Soc. 2018, 53, 55–68. [Google Scholar] [CrossRef]

- Yang, S.; Lu, Y.; Gupta, S.; Cao, Y.; Zhang, R. Mobile payment services adoption across time: An empirical study of the effects of behavioral beliefs, social influences, and personal traits. Comput. Hum. Behav. 2012, 28, 129–142. [Google Scholar] [CrossRef]

- Venkatesh, V.; Thong, J.Y.L.; Xu, X. Consumer Acceptance and Use of Information Technology: Extending the Unified Theory of Acceptance and Use of Technology. MIS Q. 2012, 36, 157. [Google Scholar] [CrossRef] [Green Version]

- Singh, N.; Sinha, N.; Liébana-Cabanillas, F.J. Determining factors in the adoption and recommendation of mobile wallet services in India: Analysis of the effect of innovativeness, stress to use and social influence. Int. J. Inf. Manag. 2020, 50, 191–205. [Google Scholar] [CrossRef]

- Singh, N.; Sinha, N. How perceived trust mediates merchant’s intention to use a mobile wallet technology. J. Retail. Consum. Serv. 2020, 52, 101894. [Google Scholar] [CrossRef]

- Fishbein, M.; Ajzen, I. Belief, Attitude, Intention, and Behavior: An Introduction to Theory and Research; Addison-Wesley Publishing Company: Reading, MA, USA, 1975. [Google Scholar]

- Chin, A.G.; Harris, M.A.; Brookshire, R. An Empirical Investigation of Intent to Adopt Mobile Payment Systems Using a Trust-based Extended Valence Framework. Inf. Syst. Front. 2020, 1–19. [Google Scholar] [CrossRef]

- Koenig-Lewis, N.; Marquet, M.; Palmer, A.; Zhao, A.L. Enjoyment and social influence: Predicting mobile payment adoption. Serv. Ind. J. 2015, 35, 537–554. [Google Scholar] [CrossRef]

- Venkatesh, V.; Bala, H. Technology Acceptance Model 3 and a Research Agenda on Interventions. Decis. Sci. 2008, 39, 273–315. [Google Scholar] [CrossRef] [Green Version]

- Thakur, R.; Srivastava, M. Adoption readiness, personal innovativeness, perceived risk and usage intention across customer groups for mobile payment services in India. Internet Res. 2014, 24, 369–392. [Google Scholar] [CrossRef]

- Sripalawat, J.; Thongmak, M.; Ngramyarn, A. M-banking in metropolitan bangkok and a comparison with other countries. J. Comput. Inf. Syst. 2011, 51, 67–76. [Google Scholar] [CrossRef]

- Leong, L.Y.; Hew, T.S.; Ooi, K.B.; Wei, J. Predicting mobile wallet resistance: A two-staged structural equation modeling-artificial neural network approach. Int. J. Inf. Manag. 2020, 51, 102047. [Google Scholar] [CrossRef]

- Goyal, A.; Maity, M.; Thakur, R.; Srivastava, M. Customer usage intention of mobile commerce in India: An empirical study. J. Indian Bus. Res. 2013, 5, 52–72. [Google Scholar] [CrossRef]

- Nel, J.; Boshoff, C. Traditional-bank customers’ digital-only bank resistance: Evidence from South Africa. Int. J. Bank Mark. 2020, 39, 429–454. [Google Scholar] [CrossRef]

- Ryan, R.M.; Deci, E.L. Self-determination theory and the facilitation of intrinsic motivation, social development, and well-being. Am. Psychol. 2000, 55, 68–78. [Google Scholar] [CrossRef]

- Liu, R.; Wu, J.; Yu-Buck, G.F. The influence of mobile QR code payment on payment pleasure: Evidence from China. Int. J. Bank Mark. 2021, 39, 337–356. [Google Scholar] [CrossRef]

- Kim, H.-W.; Kankanhalli, A. Investigating User Resistance to Information Systems Implementation: A Status Quo Bias Perspective. MIS Q. 2009, 33, 567. [Google Scholar] [CrossRef] [Green Version]

- Kuo, R.-Z. Why do people switch mobile payment service platforms? An empirical study in Taiwan. Technol. Soc. 2020, 62, 101312. [Google Scholar] [CrossRef]

- Boden, J.; Maier, E.; Wilken, R. The effect of credit card versus mobile payment on convenience and consumers’ willingness to pay. J. Retail. Consum. Serv. 2020, 52, 101910. [Google Scholar] [CrossRef]

- Iman, N. Is mobile payment still relevant in the fintech era? Electron. Commer. Res. Appl. 2018, 30, 72–82. [Google Scholar] [CrossRef]

- Ramadan, R.; Aita, J. A model of mobile payment usage among Arab consumers. Int. J. Bank Mark. 2018, 36, 1213–1234. [Google Scholar] [CrossRef]

- Sun, S.; Law, R.; Schuckert, M. Mediating effects of attitude, subjective norms and perceived behavioural control for mobile payment-based hotel reservations. Int. J. Hosp. Manag. 2020, 84, 102331. [Google Scholar] [CrossRef]

- Khan, A.N.; Cao, X.; Pitafi, A.H. Personality traits as predictor of M-payment systems: A sEM-neural networks approach. J. Organ. End User Comput. 2019, 31, 89–110. [Google Scholar] [CrossRef] [Green Version]

- Mallat, N. Exploring consumer adoption of mobile payments—A qualitative study. J. Strateg. Inf. Syst. 2007, 16, 413–432. [Google Scholar] [CrossRef]

- Kazancoglu, I.; Aydin, H. An investigation of consumers’ purchase intentions towards omni-channel shopping: A qualitative exploratory study. Int. J. Retail Distrib. Manag. 2018, 46, 959–976. [Google Scholar] [CrossRef]

- O’Neill, J.; Dhareshwar, A.; Muralidhar, S.H. Working Digital Money into a Cash Economy: The Collaborative Work of Loan Payment. Comput. Support. Coop. Work CSCW Int. J. 2017, 26, 733–768. [Google Scholar] [CrossRef]

- Kim, M.; Kim, S.; Kim, J. Can mobile and biometric payments replace cards in the Korean offline payments market? Consumer preference analysis for payment systems using a discrete choice model. Telemat. Inform. 2019, 38, 46–58. [Google Scholar] [CrossRef]

- Kar, A.K. What Affects Usage Satisfaction in Mobile Payments? Modelling User Generated Content to Develop the “Digital Service Usage Satisfaction Model”. Inf. Syst. Front. 2020, 1–21. [Google Scholar] [CrossRef]

- Chang, W.L.; Chen, L.M.; Hashimoto, T. Cashless Japan: Unlocking Influential Risk on Mobile Payment Service. Inf. Syst. Front. 2021, 1–14. [Google Scholar] [CrossRef] [PubMed]

- Phonthanukitithaworn, C.; Sellitto, C.; Fong, M.W.L. An investigation of mobile payment (m-payment) services in Thailand. Asia-Pac. J. Bus. Adm. 2016, 8, 37–54. [Google Scholar] [CrossRef]

- Hampshire, C. A mixed methods empirical exploration of UK consumer perceptions of trust, risk and usefulness of mobile payments. Int. J. Bank Mark. 2017, 35, 354–369. [Google Scholar] [CrossRef] [Green Version]

- Rouibah, K.; Lowry, P.B.; Hwang, Y. The effects of perceived enjoyment and perceived risks on trust formation and intentions to use online payment systems: New perspectives from an Arab country. Electron. Commer. Res. Appl. 2016, 19, 33–43. [Google Scholar] [CrossRef]

- Pousttchi, K.; Schiessler, M.; Wiedemann, D.G. Proposing a comprehensive framework for analysis and engineering of mobile payment business models. Inf. Syst. E-Bus. Manag. 2009, 7, 363–393. [Google Scholar] [CrossRef]

- Liu, Z.; Ben, S.; Zhang, R. Factors affecting consumers’ mobile payment behavior: A meta-analysis. Electron. Commer. Res. 2019, 19, 575–601. [Google Scholar] [CrossRef]

- Al-Saedi, K.; Al-Emran, M.; Ramayah, T.; Abusham, E. Developing a general extended UTAUT model for M-payment adoption. Technol. Soc. 2020, 62, 101293. [Google Scholar] [CrossRef]

- Zhao, H.; Anong, S.T.; Zhang, L. Understanding the impact of financial incentives on NFC mobile payment adoption: An experimental analysis. Int. J. Bank Mark. 2019, 37, 1296–1312. [Google Scholar] [CrossRef]

- Singh, N.; Srivastava, S.; Sinha, N. Consumer preference and satisfaction of M-wallets: A study on North Indian consumers. Int. J. Bank Mark. 2017, 35, 944–965. [Google Scholar] [CrossRef]

- Gao, S.; Yang, X.; Guo, H.; Jing, J. An Empirical Study on Users’ Continuous Usage Intention of QR Code Mobile Payment Services in China. Int. J. E-Adopt. 2018, 10, 18–33. [Google Scholar] [CrossRef]

- Yu, L.; Cao, X.; Liu, Z.; Gong, M.; Adee, L. Understanding mobile payment users’ continuance intention: A trust transfer perspective. Internet Res. 2016, 28, 456–476. [Google Scholar] [CrossRef]

- Zhou, T. The effect of initial trust on user adoption of mobile payment. Inf. Dev. 2011, 27, 290–300. [Google Scholar] [CrossRef]

- Leong, L.Y.; Hew, T.S.; Tan, G.W.W.H.; Ooi, K.B. Predicting the determinants of the NFC-enabled mobile credit card acceptance: A neural networks approach. Expert Syst. Appl. 2013, 40, 5604–5620. [Google Scholar] [CrossRef]

- Phonthanukitithaworn, C.; Sellitto, C.; Fong, M. User intentions to adopt mobile payment services: A study of early adopters in Thailand. J. Internet Bank. Commer. 2015, 20. Available online: https://www.icommercecentral.com/open-access/user-intentions-to-adopt-mobile-payment-services-a-study-of-early-adopters-in-thailand-.php?aid=50545&view=mobile (accessed on 24 November 2021).

- Ramos-de-Luna, I.; Montoro-Ríos, F.; Liébana-Cabanillas, F. Determinants of the intention to use NFC technology as a payment system: An acceptance model approach. Inf. Syst. E-Bus. Manag. 2016, 14, 293–314. [Google Scholar] [CrossRef]

- Su, P.; Wang, L.; Yan, J. How users’ Internet experience affects the adoption of mobile payment: A mediation model. Technol. Anal. Strateg. Manag. 2018, 30, 186–197. [Google Scholar] [CrossRef] [Green Version]

- Kumar, A.; Adlakaha, A.; Mukherjee, K. The effect of perceived security and grievance redressal on continuance intention to use M-wallets in a developing country. Int. J. Bank Mark. 2018, 36, 1170–1189. [Google Scholar] [CrossRef]

- Oney, E.; Guven, G.O.; Rizvi, W.H. The determinants of electronic payment systems usage from consumers’ perspective. Econ. Res. Istraz. 2017, 30, 394–415. [Google Scholar] [CrossRef] [Green Version]

- Schierz, P.G.; Schilke, O.; Wirtz, B.W. Understanding consumer acceptance of mobile payment services: An empirical analysis. Electron. Commer. Res. Appl. 2010, 9, 209–216. [Google Scholar] [CrossRef]

- Liébana-Cabanillas, F.; Sánchez-Fernández, J.; Muñoz-Leiva, F. Antecedents of the adoption of the new mobile payment systems: The moderating effect of age. Comput. Hum. Behav. 2014, 35, 464–478. [Google Scholar] [CrossRef]

- Liébana-Cabanillas, F.; Sánchez-Fernández, J.; Muñoz-Leiva, F. The moderating effect of experience in the adoption of mobile payment tools in Virtual Social Networks: The m-Payment Acceptance Model in Virtual Social Networks (MPAM-VSN). Int. J. Inf. Manag. 2014, 34, 151–166. [Google Scholar] [CrossRef]

- Lwoga, E.T.; Lwoga, N.B. User Acceptance of Mobile Payment: The Effects of User-Centric Security, System Characteristics and Gender. Electron. J. Inf. Syst. Dev. Ctries. 2017, 81, 1–24. [Google Scholar] [CrossRef] [Green Version]

- Liébana-Cabanillas, F.; de Luna, I.R.; Montoro-Ríosa, F. Intention to use new mobile payment systems: A comparative analysis of SMS and NFC payments. Econ. Res. Istraz. 2017, 30, 892–910. [Google Scholar] [CrossRef]

- Francisco, L.C.; Francisco, M.L.; Juan, S.F. Payment systems in new electronic environments: Consumer behavior in payment systems via SMS. Int. J. Inf. Technol. Decis. Mak. 2015, 14, 421–449. [Google Scholar] [CrossRef]

- Liébana-Cabanillas, F.J.; Sánchez-Fernández, J.; Muñoz-Leiva, F. Role of gender on acceptance of mobile payment. Ind. Manag. Data Syst. 2014, 114, 220–240. [Google Scholar] [CrossRef]

- Slade, E.L.; Dwivedi, Y.K.; Piercy, N.C.; Williams, M.D. Modeling Consumers’ Adoption Intentions of Remote Mobile Payments in the United Kingdom: Extending UTAUT with Innovativeness, Risk, and Trust. Psychol. Mark. 2015, 32, 860–873. [Google Scholar] [CrossRef]

- Patil, P.; Tamilmani, K.; Rana, N.P.; Raghavan, V. Understanding consumer adoption of mobile payment in India: Extending Meta-UTAUT model with personal innovativeness, anxiety, trust, and grievance redressal. Int. J. Inf. Manag. 2020, 54, 102144. [Google Scholar] [CrossRef]

- Shaw, B.; Kesharwani, A. Moderating Effect of Smartphone Addiction on Mobile Wallet Payment Adoption. J. Internet Commer. 2019, 18, 291–309. [Google Scholar] [CrossRef]

- Gupta, K.; Arora, N. Investigating consumer intention to accept mobile payment systems through unified theory of acceptance model: An Indian perspective. South Asian J. Bus. Stud. 2020, 9, 88–114. [Google Scholar] [CrossRef]

- Jun, J.; Cho, I.; Park, H. Factors influencing continued use of mobile easy payment service: An empirical investigation. Total Qual. Manag. Bus. Excell. 2018, 29, 1043–1057. [Google Scholar] [CrossRef]

- Shankar, A.; Datta, B. Factors Affecting Mobile Payment Adoption Intention: An Indian Perspective. Glob. Bus. Rev. 2018, 19, S72–S89. [Google Scholar] [CrossRef]

- Humbani, M.; Wiese, M. A Cashless Society for All: Determining Consumers’ Readiness to Adopt Mobile Payment Services. J. Afr. Bus. 2018, 19, 409–429. [Google Scholar] [CrossRef] [Green Version]

- Pham, T.T.T.; Ho, J.C. The effects of product-related, personal-related factors and attractiveness of alternatives on consumer adoption of NFC-based mobile payments. Technol. Soc. 2015, 43, 159–172. [Google Scholar] [CrossRef]

- Mombeuil, C. An exploratory investigation of factors affecting and best predicting the renewed adoption of mobile wallets. J. Retail. Consum. Serv. 2020, 55, 102127. [Google Scholar] [CrossRef]

- Plouffe, C.R.; Vandenbosch, M.; Hulland, J. Intermediating technologies and multi-group adoption: A comparison of consumer and merchant adoption intentions toward a new electronic payment system. J. Prod. Innov. Manag. 2001, 18, 65–81. [Google Scholar] [CrossRef]

- Abdul-Hamid, I.K.; Shaikh, A.A.; Boateng, H.; Hinson, R.E. Customers’ perceived risk and trust in using mobile money services-an empirical study of Ghana. Int. J. E-Bus. Res. 2019, 15, 1–19. [Google Scholar] [CrossRef]

- Handarkho, Y.D.; Harjoseputro, Y. Intention to adopt mobile payment in physical stores: Individual switching behavior perspective based on Push–Pull–Mooring (PPM) theory. J. Enterp. Inf. Manag. 2020, 33, 285–308. [Google Scholar] [CrossRef]

- Chan, F.T.S.T.S.; Niu, B.; Pu, X.; Chan, F.T.S.T.S.; Chong, A.Y.L.; Niu, B. The adoption of NFC-based mobile payment services: An empirical analysis of Apple Pay in China. Int. J. Mob. Commun. 2020, 18, 343. [Google Scholar] [CrossRef]

- Arvidsson, N. Consumer attitudes on mobile payment services—Results from a proof of concept test. Int. J. Bank Mark. 2014, 32, 150–170. [Google Scholar] [CrossRef]

- Shin, D.H. Towards an understanding of the consumer acceptance of mobile wallet. Comput. Hum. Behav. 2009, 25, 1343–1354. [Google Scholar] [CrossRef]

- Liébana-Cabanillas, F.; Muñoz-Leiva, F.; Sánchez-Fernández, J. A global approach to the analysis of user behavior in mobile payment systems in the new electronic environment. Serv. Bus. 2018, 12, 25–64. [Google Scholar] [CrossRef]

- Chawla, D.; Joshi, H. Consumer attitude and intention to adopt mobile wallet in India—An empirical study. Int. J. Bank Mark. 2019, 37, 1590–1618. [Google Scholar] [CrossRef]

- Chen, K.Y.; Chang, M.L. User acceptance of “near field communication” mobile phone service: An investigation based on the “unified theory of acceptance and use of technology” model. Serv. Ind. J. 2013, 33, 609–623. [Google Scholar] [CrossRef]

- Shin, D.H. Modeling the interaction of users and mobile payment system: Conceptual framework. Int. J. Hum. Comput. Interact. 2010, 26, 917–940. [Google Scholar] [CrossRef]

- Flavian, C.; Guinaliu, M.; Lu, Y. Mobile payments adoption—Introducing mindfulness to better understand consumer behavior. Int. J. Bank Mark. 2020, 38, 1575–1599. [Google Scholar] [CrossRef]

- Di Pietro, L.; Guglielmetti Mugion, R.; Mattia, G.; Renzi, M.F.; Toni, M. The Integrated Model on Mobile Payment Acceptance (IMMPA): An empirical application to public transport. Transp. Res. Part C Emerg. Technol. 2015, 56, 463–479. [Google Scholar] [CrossRef]

- Ooi, K.B.; Tan, G.W.H. Mobile technology acceptance model: An investigation using mobile users to explore smartphone credit card. Expert Syst. Appl. 2016, 59, 33–46. [Google Scholar] [CrossRef]

- Lew, S.; Tan, G.W.H.; Loh, X.M.; Hew, J.J.; Ooi, K.B. The disruptive mobile wallet in the hospitality industry: An extended mobile technology acceptance model. Technol. Soc. 2020, 63, 101430. [Google Scholar] [CrossRef]

- Oztruk, A.B. Customer acceptance of cashless payment systems in the hospitality industry. Int. J. Contemp. Hosp. Manag. 2016, 28, 1–23. [Google Scholar] [CrossRef]

- Sharma, S.K.; Sharma, H.; Dwivedi, Y.K. A Hybrid SEM-Neural Network Model for Predicting Determinants of Mobile Payment Services. Inf. Syst. Manag. 2019, 36, 243–261. [Google Scholar] [CrossRef]

- Kalinić, Z.; Liébana-Cabanillas, F.J.; Muñoz-Leiva, F.; Marinković, V. The moderating impact of gender on the acceptance of peer-to-peer mobile payment systems. Int. J. Bank Mark. 2020, 38, 138–158. [Google Scholar] [CrossRef]

- Liu, Y.; Wang, M.; Huang, D.; Huang, Q.; Yang, H.; Li, Z. The impact of mobility, risk, and cost on the users’ intention to adopt mobile payments. Inf. Syst. E-Bus. Manag. 2019, 17, 319–342. [Google Scholar] [CrossRef]

- Pal, A.; Herath, T.; De, R.; Rao, H.R. Is the Convenience Worth the Risk? An Investigation of Mobile Payment Usage. Inf. Syst. Front. 2020. [Google Scholar] [CrossRef]

- Thakur, R. Customer Adoption of Mobile Payment Services by Professionals across two Cities in India: An Empirical Study Using Modified Technology Acceptance Model. Bus. Perspect. Res. 2013, 1, 17–30. [Google Scholar] [CrossRef] [Green Version]

- Sivathanu, B. Adoption of digital payment systems in the era of demonetization in India: An empirical study. J. Sci. Technol. Policy Manag. 2019, 10, 143–171. [Google Scholar] [CrossRef]

- Lim, S.H.; Kim, D.J.; Hur, Y.; Park, K. An Empirical Study of the Impacts of Perceived Security and Knowledge on Continuous Intention to Use Mobile Fintech Payment Services. Int. J. Hum. Comput. Interact. 2019, 35, 886–898. [Google Scholar] [CrossRef]

- Humbani, M.; Wiese, M. An integrated framework for the adoption and continuance intention to use mobile payment apps. Int. J. Bank Mark. 2019, 37, 646–664. [Google Scholar] [CrossRef]

- Kumar, R.R.; Israel, D.; Malik, G. Explaining customer’s continuance intention to use mobile banking apps with an integrative perspective of ECT and Self-determination theory. Pac. Asia J. Assoc. Inf. Syst. 2018, 10, 79–112. [Google Scholar] [CrossRef]

- Zhou, T. An empirical examination of continuance intention of mobile payment services. Decis. Support Syst. 2013, 54, 1085–1091. [Google Scholar] [CrossRef]

- Chen, X.; Li, S. Understanding continuance intention of mobile payment services: An empirical study. J. Comput. Inf. Syst. 2017, 57, 287–298. [Google Scholar] [CrossRef]

- Gupta, A.; Yousaf, A.; Mishra, A. How pre-adoption expectancies shape post-adoption continuance intentions: An extended expectation-confirmation model. Int. J. Inf. Manag. 2020, 52, 102094. [Google Scholar] [CrossRef]

- Park, M.; Jun, J.; Park, H. Understanding mobile payment service continuous use intention: An expectation—Confirmation model and inertia. Qual. Innov. Prosper. 2017, 21, 78–94. [Google Scholar] [CrossRef] [Green Version]

- Shao, Z.; Zhang, L.; Li, X.; Guo, Y. Antecedents of trust and continuance intention in mobile payment platforms: The moderating effect of gender. Electron. Commer. Res. Appl. 2019, 33, 100823. [Google Scholar] [CrossRef]

- Talwar, S.; Dhir, A.; Khalil, A.; Mohan, G.; Islam, A.K.M.N. Point of adoption and beyond. Initial trust and mobile-payment continuation intention. J. Retail. Consum. Serv. 2020, 55, 102086. [Google Scholar] [CrossRef]

- Raman, P.; Aashish, K. To continue or not to continue: A structural analysis of antecedents of mobile payment systems in India. Int. J. Bank Mark. 2021, 39, 242–271. [Google Scholar] [CrossRef]

- Wang, L.; Luo, X.; Yang, X.; Qiao, Z. Easy come or easy go? Empirical evidence on switching behaviors in mobile payment applications. Inf. Manag. 2019, 56, 103150. [Google Scholar] [CrossRef]

- Zhou, T. An empirical examination of users’ switch from online payment to mobile payment. Int. J. Technol. Hum. Interact. 2015, 11, 55–66. [Google Scholar] [CrossRef] [Green Version]

- Zhang, K.Z.K.; Gong, X.; Chen, C.; Zhao, S.J.; Lee, M.K.O. Spillover effects from web to mobile payment services: The role of relevant schema and schematic fit. Internet Res. 2019, 29, 1213–1232. [Google Scholar] [CrossRef]

- Zhou, T. Understanding the determinants of mobile payment continuance usage. Ind. Manag. Data Syst. 2014, 114, 936–948. [Google Scholar] [CrossRef]

- Esfahani, S.S.; Bulent Ozturk, A. The influence of individual differences on NFC-based mobile payment adoption in the restaurant industry. J. Hosp. Tour. Technol. 2019, 10, 219–232. [Google Scholar] [CrossRef]

- Choi, H.; Park, J.; Kim, J.; Jung, Y. Consumer preferences of attributes of mobile payment services in South Korea. Telemat. Informatics 2020, 51, 101397. [Google Scholar] [CrossRef]

| Theory Name | Pre–2005 | 2006–2010 | 2011–2015 | 2016–2021 | Total |

|---|---|---|---|---|---|

| Technology acceptance model | 0 | 3 | 19 | 40 | 62 |

| Unified theory of acceptance and use of technology | 0 | 2 | 11 | 31 | 44 |

| Innovation diffusion theory | 1 | 2 | 12 | 28 | 43 |

| Unified theory of acceptance and use of technology (2) | 0 | 4 | 26 | 30 | |

| Technology acceptance model (2) | 0 | 5 | 15 | 20 | |

| Theory of reasoned action | 0 | 2 | 4 | 12 | 18 |

| Theory of planned behaviour | 0 | 2 | 2 | 12 | 16 |

| Technology acceptance model (3) | 0 | 11 | 11 | ||

| Expectation confirmation theory | 0 | 6 | 6 | ||

| Innovation resistance theory | 0 | 1 | 3 | 4 | |

| Self-determination theory | 0 | 3 | 3 | ||

| Social cognitive theory | 0 | 3 | 3 | ||

| Status quo bias theory | 0 | 3 | 3 | ||

| The theory of perceived risk | 0 | 1 | 2 | 3 | |

| Other theories (two times) * | 0 | 2 | 2 | 14 | 18 |

| Other theories (one time) ** | 0 | 2 | 2 | 29 | 33 |

| No theory | 1 | 2 | 3 | 11 | 17 |

| Item | Pre–2005 | 2006–2010 | 2011–2015 | 2016–2021 | Total |

|---|---|---|---|---|---|

| Methods ─ | |||||

| Quantitative | 3 | 8 | 34 | 109 | 154 |

| Mix method | 2 | 9 | 11 | ||

| Non-empirical | 4 | 3 | 4 | 11 | |

| Review and Meta-analysis | 3 | 3 | 4 | 10 | |

| Qualitative and Case study | 2 | 5 | 7 | ||

| Countries ─ | |||||

| India | 1 | 4 | 28 | 33 | |

| China | 1 | 1 | 7 | 20 | 29 |

| The USA | 3 | 12 | 15 | ||

| Spain | 4 | 8 | 12 | ||

| Malaysia | 4 | 7 | 11 | ||

| Korea | 3 | 5 | 8 | ||

| Taiwan | 1 | 5 | 6 | ||

| Thailand | 3 | 3 | 6 | ||

| South Africa | 5 | 5 | |||

| The UK | 2 | 2 | 4 | ||

| Germany | 1 | 2 | 3 | ||

| Cross-country | 2 | 6 | 8 | ||

| Other countries * | 2 | 1 | 11 | 22 | 36 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Sahi, A.M.; Khalid, H.; Abbas, A.F.; Khatib, S.F.A. The Evolving Research of Customer Adoption of Digital Payment: Learning from Content and Statistical Analysis of the Literature. J. Open Innov. Technol. Mark. Complex. 2021, 7, 230. https://doi.org/10.3390/joitmc7040230

Sahi AM, Khalid H, Abbas AF, Khatib SFA. The Evolving Research of Customer Adoption of Digital Payment: Learning from Content and Statistical Analysis of the Literature. Journal of Open Innovation: Technology, Market, and Complexity. 2021; 7(4):230. https://doi.org/10.3390/joitmc7040230

Chicago/Turabian StyleSahi, Alaa Mahdi, Haliyana Khalid, Alhamzah F. Abbas, and Saleh F. A. Khatib. 2021. "The Evolving Research of Customer Adoption of Digital Payment: Learning from Content and Statistical Analysis of the Literature" Journal of Open Innovation: Technology, Market, and Complexity 7, no. 4: 230. https://doi.org/10.3390/joitmc7040230