1. Introduction

The economic disruption due to the pandemic has led to tremendous growth in digital financial services and e-commerce as social distancing has taken hold worldwide. According to the World Bank [

1], there are 1.7 billion unbanked individuals worldwide; half of these include women in rural areas or out of the workforce. The toll of the COVID-19 pandemic highlighted the importance of the inclusion and serving of people currently outside financial systems [

2].

According to the 2020 Global COVID-19 FinTech market rapid assessment study [

3], a more significant push towards digitalization during the pandemic was seen in most types of FinTech firms, who reported strong growth in transaction numbers and volumes of 13% and 11%, respectively, for the first half of 2020 compared to the same period in 2019, which was before the pandemic.

FinTech improves activities in finance by using digital technologies. Applying digital methods to traditional financial activities eases the online demands brought by the pandemic. Yet, it still raises concerns about centralization, such as dictatorship, data monopoly, data tampering, and user privacy issues. Blockchain technology, the most practical decentralized solution, has recently attracted much attention. It removes the need for third-party verification for transactions (i.e., the need for centralized exchanges).

In 2019, Gartner estimated that blockchain remains in the “Peak of Inflated Expectation” region, gaining a high interest from investors and consumers with a forecast to reach a plateau in “five to ten years”. The report predicted that blockchains will undergo more mainstream adoption in 2023, thus leading to a generation of

$3.1 trillion [

4] in new business value by 2030.

This growth is partly due to multinational corporations and technology industry giants using blockchain to capture larger market shares.

The adoption of blockchain technology by FinTech companies is inevitable [

5]. In 2021, the Gartner report [

6] categorized decentralized finance in the “innovation trigger” region, meaning that the technology is subject to significant media and industry interest, with a high potential for technology breakthrough. Blockchain-based FinTech solutions can offer financial services at lower costs and a higher level of accessibility [

7] when compared with traditional solutions.

Blockchain technology can provide decentralized, secure, and traceable storage, attracting massive industry investment. There are currently several blockchain applications that span a vast range of industries, including healthcare [

8], IoT [

9], security [

10,

11], data privacy [

12], supply chain and goods tracing [

13,

14], the energy sector [

15], product counterfeiting [

16], etc. Among the various sectors interested in the blockchain industry, FinTech stands out and has become a prevalent topic with great promises.

Financial behaviors such as banking and trading have changed since the emergence of blockchain. Traditional financial institutions are pouring money into FinTech companies and startups to leverage innovation and gain a competitive advantage over their peers [

17]. The FinTech industry incentivizes traditional banking institutions to develop their blockchain infrastructure to seize the market share of FinTech services.

Although there are high-level reviews of blockchain technology [

18,

19,

20,

21], a systematic comparison of blockchain platforms in the context of financial applications is still lacking. There is a considerable gap in investigating how blockchains and distributed ledger technologies are implemented and used for financial services on a technical level for various FinTech Segments. Other studies [

22] have provided an overview of existing fintech platforms from a theoretical lens by presenting a plan for adopting fintech platforms. Others [

23] have investigated digital finance from a business function perspective.

The authors in [

24] investigated FinTech innovations (e.g., ML, blockchain, and alternative finance) and the related regulatory issues. Our paper is solely focused on laying out blockchain-based applications for FinTech segments.

This survey focuses on using blockchains to enhance the way financial services are offered to individuals and businesses by FinTech companies. We discuss how different companies leverage blockchains to realize their goal.

The contributions of this paper can be summarized as follows:

- (1)

This survey provides a thorough and detailed systematization and summary of the most relevant blockchain-based FinTech implementations.

- (2)

We provide an overview of various FinTech Sectors and segments. For each FinTech segment, we map the current blockchain applications and discuss how these implementations contribute to solving the vast majority of problems faced by FinTech companies and users.

- (3)

We also present detailed blockchain-based use-cases to illustrate how different blockchain applications are implemented for various financial services.

- (4)

We provide an overview of some critical challenges in implementing blockchains for FinTech and a summary of related research work.

- (5)

We provide a discussion and SWOT analysis to identify the strengths, weaknesses, opportunities, and threats in this field.

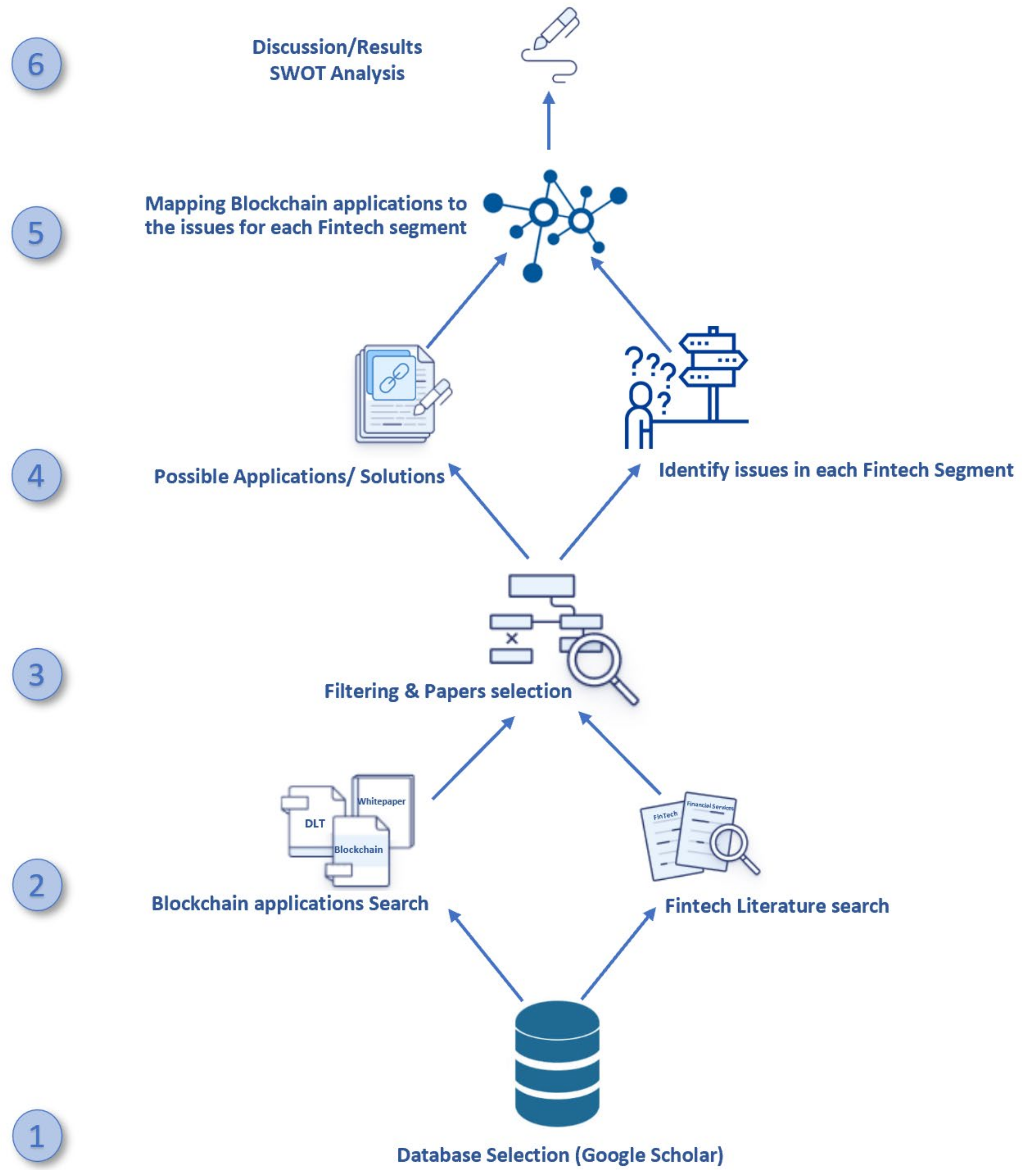

The rest of the paper is organized as follows.

Section 2 provides an overview of the procedures and methodology that we followed in our research.

Section 3 provides a brief background on blockchain architecture, highlights the most popular blockchain implementations’ key characteristics, and introduces smart contracts that enable FinTech companies to provide low-cost, secure, and decentralized applications.

Section 4 introduces the FinTech literature and discusses blockchains’ interaction with banking and their applications within the main three segments of FinTech (Payments, Deposits and Lending, and Investment Management).

Section 5 reviews the Payments segment.

Section 6 reviews the Deposits and Lending segment.

Section 7 discusses the FinTech Investment Management segment.

Section 8 discusses key challenges facing blockchain implementations for FinTech, examines blockchain-based Defi, and provides a SWOT analysis to identify the field’s strengths, weaknesses, opportunities, and threats.

To the best of our knowledge, this is the first mapping study of blockchain applications in solving the issues faced by the Fintech segments from a technical point of view.

3. Blockchain Background

This section starts with an overview of blockchain architecture and smart contracts. A comparison of different open-source blockchain implementations for FinTech is provided. We aim to ensure the readers’ familiarity with blockchain technology and its key characteristics crucial to FinTech.

3.1. Blockchain Architecture

A blockchain can be regarded as an append-only, shared, fault-tolerant, distributed database. A blockchain is immutable because all blocks are connected via hash functions. Any tamper of a block invalidates all the following blocks.

A chain is formed by connecting the blocks. Each block contains the hash value of the block before it (i.e., each block points to its previous block). The blocks consist of several time-stamped transactions collected from users’ broadcasts. Each block also stores the time of creation. Each transaction is verified before its inclusion in a block.

By having the blocks linked to each other, an immutable data chain is prepared, whose copies can be safely kept on distributed network nodes. With a consensus protocol, a decentralized system can be achieved without a centralized authority controlling any data or mechanisms. When a node wants to carry out a transaction within the network, it broadcasts the transaction. Then, several nodes (i.e., Validators) check to ensure that the nodes involved and the transactions are valid, and then a block is made that consists of the valid transactions.

Once the new block is deemed valid, it is added to the database. If the block is not valid, the block is discarded. Therefore, it will not be added to the database. The transactions and the block are signed, so that future transaction revocation or repudiation is impossible. The transactions are bundled in a Merkle tree [

27]. Each block contains the hash of the previous block in the chain. The very first block of the chain is called the genesis block.

By network structure, blockchains can be classified into four categories: public blockchains, private blockchains, consortium blockchains, and hybrid blockchains.

Public blockchains are fully decentralized, permissionless, and public, where everyone can participate. This ensures that there is no centralized entity that controls the network. Therefore, such a network has no single point of failure and no data monopoly. Bitcoin [

28], Ethereum [

29], Litecoin [

30], and USDF [

31] are popular examples of public blockchains. However, this type of blockchain suffers immensely from a scalability issue. Achieving a consensus among a large number of nodes is generally slow.

A private blockchain network implies that the nodes need to be granted access to the network and authenticated, hence “permissioned.” For example, Hyperledger [

32], Quorum [

33], and R3 Corda [

34] are all private blockchains. Many banks are shifting their financial services toward utilizing private blockchains for more secure, faster processing, with more transparent and lower-cost processes than traditional banking [

35]. Although private blockchains can provide more granular control over who belongs to the network, they sacrifice some decentralization by introducing a network administrator to control access. Nonetheless, the distributed data among the participating parties are still traceable and immutable.

Private blockchains are highly scalable, the network size can be customized to match the need, and new nodes can be added to the network as required. However, a centralized identity and access management system is needed to implement access control to the network and the data.

A consortium blockchain is a semi-decentralized blockchain where two or more parties (e.g., financial institutions) manage the blockchain network. Banks and government entities usually utilize this type of blockchain. Examples of this blockchain are CargoSmart [

36] and the Energy Web Foundation (EWF) [

37].

A hybrid blockchain is a combination of private and public blockchains. Only a selected amount of information is allowed to go public while keeping the rest confidential. The idea of incorporating both types is to keep part of the information private while allowing more nodes to join the network for scalability. IBM Food Trust [

38] is an example of a hybrid blockchain.

Note that private blockchains, consortium blockchains, and hybrid blockchains are permissioned blockchains that require authorized permissions to access networks and data.

3.2. Consensus Algorithms

Consensus algorithms are required in distributed ledgers (i.e., blockchains) to get all nodes in the system to agree on the content. When a node appends a block to the chain, the other nodes should also append the same block to maintain blockchain integrity.

For example, in the Proof-of-Work (PoW) algorithm, all nodes complete solving a mathematical puzzle. The puzzle selected by the Bitcoin community is to find a nonce that hashes below a specific value. Whoever solves it first and broadcasts their block has it appended to the chain. The process of verifying the nonce is computationally cheap. Therefore, nodes can verify the new block and append it to their copy of the chain. In PoW, the incentive for mining transactions lies in economic payoffs. Numerous alternative consensus algorithms have been developed for blockchains, namely Proof of Work (PoW), Proof of Stake PoS [

39], Istanbul Byzantine Fault Tolerant (IBFT), leader-free Byzantine consensus [

40], implicit consensus [

41], ELASTICO [

42], Proof of Trust (PoT) [

43], Delegated Byzantine Fault Tolerant (DBFT) [

44], Proof of Participation and Fees (PoPF) [

45], Proof of Vote (PoV) [

46], Delegated Proof of Stake (DPoS) [

47], and Delegated Proof-of-Private-Stake (DPoPS) [

48].

In this subsection, we briefly discuss Proof-of-Work (PoW) [

28], Proof of Stake PoS [

39], Byzantine fault-tolerance (BFT) [

49], and RAFT [

50] to ensure the readers’ familiarity with the consensus algorithms utilized in blockchain-based FinTech Applications.

Proof of Work (PoW): PoW [

28] is the consensus algorithm adopted in the Bitcoin blockchain. Under PoW, nodes (called miners in Bitcoin) solve a computational task to generate a new block. The computational task is finding a value that, when hashed with SHA-256, results in a number beginning with a pre-specified number of zero bits.

The difficulty of the task and the average work required are exponential in the number of zero bits required. The block can be verified by executing a single hash and added to the chain. If most nodes add a block to their copy of the chain and then generate new blocks pointing to it, this indicates a consensus that it is the correct next member of the chain.

Assuming the majority of the nodes in the network are honest, PoW consensus is resistant to Sybil attack [

51], in which an attacker can acquire multiple identities (i.e., nodes) in a distributed system and use them to gain a significant influence (consensus). PoW forces every node on the network, whether it is a malicious or honest node, to carry out an equal amount of computational power. This makes it very difficult for an attacker to alter a past block as they would have to redo the hash pointer of the block and all the subsequent blocks to catch up with and surpass the work of the honest nodes.

A big problem with PoW is that computation of the hash wastes too many computing resources. Many studies [

52,

53] worked on improving the original PoW mechanism. For example, SPECTRE [

54] is a consensus protocol that allows a parallel block creation on the block direct acyclic graph (BlockDAG). This operation improves the transaction throughput and reduces the confirmation time of Bitcoin.

Bitcoin-NG (Next Generation) [

55] is another example of a leader-election PoW consensus protocol. Bitcoin-NG introduces two types of blocks: key blocks and micro blocks. Key blocks are only used for the leader’s election. Once a key block generated by a node is accepted, it becomes the leader. The micro block contains the packaged transaction data and ledger entries. Thus, transactions can be processed continually until the next leader is elected, significantly reducing transaction confirmation time and improving scalability.

The Greedy Heaviest-Observed Sub-Tree (GHOST) [

56] consensus algorithm follows the heaviest sub-tree rule when appending blocks to the chain to eliminate double-spending [

57] attacks on Bitcoin. This rule is more secure than the longest chain rule as it is independent of the size of the blocks or the block creation rate.

Proof of Stake (PoS): In PoS [

39], validators are selected based on the number of coins that the validator stakes. The nodes having more stakes will have a higher opportunity to add the next block to the chain. A new leader is elected using random criteria based on the amount of stakes that a node (i.e., miner) possesses. Ouroboros [

58] and Casper [

59] are examples of PoS algorithms.

Ethereum 1.0 utilized the PoW consensus protocol. Later, in Ethereum 2.0, PoW was replaced by Proof of Stake (PoS) to increase the network’s scalability and power efficiency.

Byzantine fault-tolerance (BFT): BFT [

49] is called Byzantine as the algorithm can cope with some fraction of “Byzantine nodes”—nodes that are faulty and behave arbitrarily. They can lie or intentionally mislead other network nodes, delay message delivery, and cause disruption. Examples of BFT protocols are Trinity [

60] and Exonum [

61].

Reversible Addition-Fragmentation Chain-Transfer (RAFT): The RAFT algorithm [

50] achieves consensus through an elected leader responsible for log replication to the followers, where followers blindly trust their leader. A follower node becomes a leader candidate if it receives no communication from its leader over an election timeout period. Quorum utilizes RAFT as its consensus algorithm.

Istanbul Byzantine Fault Tolerance (IBFT): IBFT [

62] is a proof-of-authority Byzantine fault-tolerant consensus protocol. It uses a group of validators to ensure each proposed block’s integrity. The majority (around 66%) of these validators must sign the block before it can be added to the chain. The group’s leadership also rotates over time, ensuring that a faulty node cannot have long-term effects on the chain. Validators do not assume that all leaders are trustworthy or honest and do multiple rounds of voting to arrive at a consensus.

3.3. Smart Contract

A smart contract is an innovative way to trigger a “contract” program where the deposited cryptocurrency is transferred when a predetermined condition or set of conditions is met. Smart contracts are contractual clauses that have been converted into lines of code that can be run on top of a blockchain.

The purpose is to embed the contractual clauses into a blockchain such that they can be enforced automatically. Smart contracts reduce the risk of contract violation, decrease cost and increase trading efficiency [

63].

Smart contracts adhere to the immutability of the blockchain, meaning that they cannot be altered once issued. Behaviors that violate the contract, such as financial fraud, can be avoided in some cases.

The elimination of a third party allows an automatic settlement of financial transactions, improving businesses’ efficiency in addition to reducing turnaround time and removing the need for reconciliation between parties (i.e., cross-border banks) that speed up transactions and the settlement of trades for FinTech companies.

3.4. Digital Wallets

Digital wallets are financial applications that allow users to store public and private keys for their cryptocurrency transactions. Based on internet connectivity, blockchain-based wallets can be categorized into cold and hot wallets.

A hot wallet is always connected to the internet and cryptocurrency network. It is used for day-to-day transactions. Cold wallets are called “vaults.” They are not connected to the internet and allow users to store cryptocurrencies with a higher level of security. Cold wallets are less convenient for active traders as they have to move the amount of cryptocurrency to a hot wallet or power on cold wallets and connect them to the internet to carry out transactions.

3.5. Blockchain Platforms Adopted in Financial Services

FinTech companies are shifting towards blockchain-based financial services for security, scalability, and efficiency compared with traditional financial services.

Table 1 summarizes the five main properties of blockchains critical to FinTech.

3.6. Description of Blockchain Platforms

In this subsection, we discuss and provide a comparative analysis of the current and most popular open-source blockchain implementations. We start with Bitcoin. Then we discuss Ethereum, Hyperledger Fabric, Quorum, and R3 Corda implementations.

3.6.1. Bitcoin

Bitcoin introduced the concept of blockchain to the world. It was created by Satoshi Nakamoto [

28]. It has been popular since its introduction and has enlightened many derivatives worldwide.

It is a permissionless public ledger record, meaning that the ledger of all Bitcoin transactions is accessible publicly and distributed to nodes worldwide. Since its creation in 2008, many have argued that Bitcoin should be seen as a speculative commodity rather than just a cryptocurrency.

The symbols used for bitcoin are BTC or XBT. BTC is short for Bitcoin. These abbreviations come from the International Standards Organization (ISO), which maintains a list of internationally recognized currencies. The “X” indicates that the currency is not associated with a particular country. Many FinTech applications are built on the Bitcoin distributed ledger, where the transaction records can be easily verified. We discuss these implementations in detail later in this paper.

3.6.2. Ethereum

Ethereum was created as an alternative protocol to Bitcoin and allows for building decentralized applications, writing smart contracts, and managing digital assets. Ethereum is a permissionless, open-source blockchain platform [

67]. Its smart contract implementation and development kits are the most popular blockchain platform for decentralized applications [

68].

Ethereum has a native digital currency called Ether (ETH) that has three primary purposes: to settle transactions through the exchange of ETH and enable network operations by using ETH as currency to pay transaction fees and store value. Ethereum has the largest enterprise ecosystem in the world [

68], with an active technical community of over 300,000 developers and infrastructure experts coordinated by the Enterprise Ethereum Alliance (EEA) [

69], which is dedicated to promoting Ethereum adoption and comprises the world’s largest companies such as Microsoft, JP Morgan, Accenture, ING, Intel, and Cisco.

However, Ethereum has a few limitations in terms of scalability, smart contract volatility, lack of a clear monetary policy, and some uncertainty with Securities and Exchange Commission (SEC) regulations. The momentum of implementing Ethereum for financial services comes from the blockchain’s smart contract capabilities and its heavy involvement in decentralized finance. Ethereum 1.0 utilized Proof of Work (PoW) as its consensus algorithm, resulting in around 40 transactions per second.

Later, Ethereum 2.0 [

70] replaced PoW with Proof of Stake. Ethereum 2.0 has recently become the preferred platform for FinTech because it can handle up to 3000 transactions per second, which is faster and yet more efficient than Bitcoin or Ethereum 1.0.

3.6.3. Hyperledger Fabric

Hyperledger Fabric is an open-source consortium maintained under the Linux Foundation and has more than 200 members from various global companies, including financial services, for example, Visa-integrated Hyperledger Fabric for Business-to-Business (B2B) blockchain payments in 2018 [

52]. Hyperledger Fabric enables blockchain adoption for industrial applications as well.

The Hyperledger Fabric is a permissioned, private blockchain platform where the participating nodes can transfer assets. The transactions are directed by Chaincode [

71]. Chaincode is what executes the functionality of a smart contract within the Hyperledger Fabric framework. The execution of the Chaincode creates the interactions between the nodes and the shared ledger. All nodes within the network need to know and maintain the identity of the other nodes.

There are subnetworks within the larger Hyperledger network, called channels. Channels are restricted to a particular subset of the nodes. A channel can create its own ledger that only maintains a record of its transactions and digital assets and can only be accessed or viewed by nodes in that channel [

35].

Hyperledger supports a Hardware Security Module (HSM) that is vital for managing and protecting the digital keys and its modular architecture, which supports plug-in components [

32]. Hyperledger provides modified and unmodified PKCS #11 for key generation. PKCS #11 [

72] is one of the Public-Key Cryptography Standards (PKCS).

Some implementations may suffer from a lack of transparency. This may lead to data monopoly or tampering, in addition to the limitation in terms of scalability [

73].

3.6.4. Quorum

Quorum is a permissioned version of the Ethereum blockchain. It was developed by JP Morgan and was later acquired by ConsenSys. Since it is a permissioned blockchain, nodes must be verified before entering the Quorum network. The consensus algorithms used by Quorum are RAFT and IBFT in place of the PoW implementation of Ethereum 1.0 and Bitcoin. Privacy is preserved in Quorum as transactions are not visible to members of the larger network. This is similar to Hyperledger’s channels, where some transactions can only be visible to a smaller group of network nodes maintained on a smaller, private ledger. Quorum is referred to as a free gas network, meaning that there is no “mining fee” for transactions, and there are no cryptocurrency costs associated with its transactions (i.e., Gas is set to zero) [

74].

3.6.5. R3 Corda

R3 Corda is a private, permissioned, open-source software project that creates the Corda Network [

21]. The main benefit of Corda is that it eases managing contracts and reaching agreements between parties, especially when there is not enough trust between the parties by using smart contracts. Unlike Hyperledger or Ethereum, to achieve consensus, it uses the idea of notary pools. The details of this consensus method can be found in the introduction to the Corda Platform Whitepaper [

75].

Corda focuses mainly on financial services to create a global independent network and therefore abstracts away many of the typical blockchain structure’s components that cause time and computational overhead. However, the full functionality of the Corda blockchain platform can be achieved by utilizing the components provided by Hyperledger. In addition to the fast operational speeds provided by Corda, it also helps FinTech companies optimize inter-company cooperation’s costs and efficiency, where data can be shared only among permissioned nodes.

Quorum provides the fastest transaction throughput compared with the other blockchains’ original implementations. However, it is less flexible.

Ethereum provides security with limited scalability and is less efficient (i.e., low transactions per second) and thus does not apply to time-critical situations. Hyperledger fabric conducts transactions much faster than Ethereum. This is expected since the latter is based on a permissionless blockchain.

R3 Corda also has higher transaction rates than Ethereum 1.0 but has lower throughput than Hyperledger Fabric. As mentioned before, a Hyperledger Fabric with its “plug-n-play” components can be built to perform similarly to the Corda platform.

However, the highest transaction throughput was reported by Ethereum 2.0. There is no standard yet when it comes to blockchain performance measures. Experiments are limited by resources and often are focused on specific use cases. Therefore, these measurements are not necessarily accurate.

Table 2 provides a comparative summary of the key characteristics of the top five blockchain implementations.

4. Fintech Background

This section discusses the difference between ‘Decentralized Finance’ (DeFi) and centralized finance (CeFi). Later we provide an overview of FinTech evolution.

It is important to differentiate between ‘Decentralized Finance’ (DeFi) and Centralized Finance (CeFi). Traditional finance fundamentally depends on the trust and confidence of the intermediaries that centralize financial functions and resources. It is usually referred to as centralized finance (CeFi). Decentralized finance (DeFi) emerged with the promise of eliminating centralized governance and intermediaries, transforming traditional finance into a trustless and transparent protocol [

81,

82].

Three factors made DeFi possible [

24]. First, Moore’s law is the principle that the amount of data processing grows exponentially. Second, Kryder’s law is the principle that the amount of data storage grows exponentially. Thirdly, there is an advancement in communications bandwidth with a decrease in cost. This allowed advancements in AI, blockchain and distributed Ledgers (DLT), Big data, and Clouds.

Fintech existed before blockchain technology, and the use of this term evolved with time [

83]. This may prove confusing. Fintech can be used for CeFi [

84,

85], utilizing the evolution of traditional finance innovation using technologies such as instant messaging and cloud computing to provide financial services, while others [

86] use the term to indicate the distributed technology (e.g., DLT, blockchains) used to provide DeFi services [

87]. We shall use the latter meaning throughout our paper unless we indicate otherwise.

The development of FinTech experienced several different phases [

88]. Although the roots of FinTech can be traced back to the 19th century, we see that the term only gained traction in the 21st century in concurrence with recent technological advances.

The first age of financial globalization is dated back to 1866, when trans-Atlantic cable was used for the first time to verify signatures in banking transactions operating between Paris and Lyon, France. In the late 1800s, consumers and merchants started to exchange goods using cards for the first time in history. Charga-Plate was an early predecessor of the credit card we know today. Charga-Plate is a small metal card. The transaction record was made using an imprinting machine by pressing an inked ribbon against the card with the embossed transaction information. In 1918, federal reserve banks established Fedwire Funds Service to transfer funds by connecting all Reserve Banks by telegraph using a Morse code system. In 1920, Keynes, in his famous book, “The Economic Consequences of the Peace” [

89], published right after World War I, took the lead in highlighting the inter-linkage between finance and technology. In 1964, the Charg-It card was launched by John C. Beggins to be used in a two-block radius of Flatbush National Bank in Brooklyn, New York.

The second generation of FinTech, ”FinTech 2.0,” was marked by Barclays’ introduction of the first ATM. In 1974, the Equal Credit Opportunity Act was signed by President Gerald Ford, prohibiting and punishing any creditor discrimination against consumers. The year 1982 marked the birth of the first online brokerage, “E-Trade,” which allowed the execution of electronic trades by individual investors.

FinTech 2.0 aimed to seamlessly integrate and combine customers’ financial needs in one place. Fintech 3.0 was born on the heels of the economic recession. The financial crisis of 2007–2008 started the disputable argument about who has the legitimacy to own and provide financial resources. The crisis deteriorated public perception of and trust in banks. The post-crisis strict regulations for FinTech 3.0 opened the market to new providers and allowed open banking, which allows third-party companies access to financial data.

Fintech 3.0 marked the emergence of Bitcoin, followed by other cryptocurrencies using distributed ledger technology (DLT). Distributed ledger technology is also called a shared ledger, where the recording of the transaction of assets is distributed across multiple nodes. Thus, distributed ledgers have no central data store or administration functionality. The challenges brought by the global pandemic in 2019 marked the beginning of FinTech 4.0 [

90].

The COVID-19 pandemic increased the demands for digitization and decentralization. BigTech platforms (e.g., Meta, Google, Amazon) have increased significantly during the COVID-19 pandemic. These platforms have been able to reap the benefit of having a large number of users through online payments, credit, insurance, and digital wallets. Annual FinTech financing and investments by venture capitals, private equity, and cross-border mergers and acquisitions reached

$210 billion by 2021 [

91]. They had been doubling over the preceding years (

$112 Billion by 2018). FinTech companies were brought about due to the surge of the technological age.

Technology companies spotted this need and have jumped in to provide the architecture, software, and services that enable these financial institutions to continue to provide the services on computer-based platforms [

92]. There are currently over 8775 financial services startups in the North American region, 7385 in Europe, the Middle East, and Africa combined, and 4765 in the Asia–Pacific region [

2]. FinTech companies have adopted many technologies, starting with Artificial Intelligence (AI), Machine Learning (ML), Deep Learning (DL), and Blockchain. Blockchain-based FinTech implementation and application are the focus of this survey paper.

Blockchain-based applications for the FinTech sector were motivated by the blockchain’s decentralized potential for finance. In this paper, we study the three main categories of FinTech services [

26]: Payments Services, Deposits and Lending, and finally, Investment Management Services. In this paper, these different services will be described as segments within the FinTech sector.

Figure 2 shows a sample of the current FinTech companies within their assigned FinTech Segment.

The first segment is the Payments segment, which provides new and easier payment methods without centralized authorities. For this reason, the payments segment continues to be the largest segment of the FinTech space. The next most significant segment is the deposits and lending segment. With application processes and background checks already being done online, this was a big avenue in which technology companies could apply big data principles and find a way to streamline the loan and refinancing processes even further to make them more accessible. Following deposits and lending, the investment management space is the next most significant and certainly more blossoming (as of recent times) segment of the FinTech space. More novice investors are putting their money into apps that help them to make investment and trading decisions. Investment management companies allow the investing process to be more tangible and accessible and offer a friendly and straightforward user interface. Each segment can be further broken up and categorized by various companies’ services, goals, and specializations.

For blockchain-based FinTech, it is crucial to understand what exact services a company is attempting to provide in order to understand the core components of these services. By understanding these components, one can formulate a plan to understand the requirements for the technology within this space.

4.1. Payments Segment

Payment is currently the most significant segment that is continually growing larger. A crucial reason for this growth is that access to mobile devices, data networks, and applications has allowed FinTech companies to lure traditional banking customers away from legacy banking platforms. These applications then enable users to interact directly with vendors, removing third-party brokers [

26]. Companies focused on the payments segment are now driving innovation to increase blockchain-based applications’ efficiency and accessibility [

93].

This segment can be broken up into categories that specify what services they offer within the payment realm.

Table 3 discusses the different payment segment categories [

26] and briefly describes the services and companies in each category.

4.2. Deposits and Lending Segment

Deposits and lending is another huge segment in the FinTech space. The purpose of this segment is to simplify the traditional banking flow. This includes storing the money in the bank (i.e., deposits) and building interest on that money. It also incorporates companies that enable people or businesses to obtain loans (i.e., lending) and monitor/collect information about credit. We highlight the top three categories of the deposits and lending [

26] segment and provide exemplary services and companies for each category in

Table 4.

However, some FinTech companies can fit in more than one category based on their services. These companies attempt to simplify the loan process by finding different ways to assess credit risk. They provide various ways for companies to collect data and analytics to simplify the background checking process and shorten the turnover time of loan applications and loan grants/rejections. PeerIQ [

94] is an example of a company that provides risk analytics and decision-making tools to help FinTech lending institutions to analyze, access, and manage lending risk.

4.3. Investment Management Segment

The Investment Management segment of the FinTech sector is mainly comprised of companies that attempt to invest in a simple automated process. These companies ease access to various securities for those less familiar with finance.

Table 5 highlights different segments [

26] of Investment Management companies. Example services and companies for each segment are provided. Still, most FinTech companies provide one or more services and, therefore, can fit within more than one category within the same segment.

Table 5 highlights deposit and lending subsegments.

5. The Payments Sector

The payments sector consists of three segments: retail and consumer payments, point of sale payments, and international money transfers (remittances). This section discusses six FinTech companies (Stellar, Ripple, Algorand, Pundi-X, SureRemit, and Everex), two for each segment. We highlight how blockchain technology is leveraged to solve the sector’s problems.

5.1. Retail and Consumer Payments

This subsection discusses two retail and consumer payments FinTech companies, Ripple and Stellar. With increased users in online shopping, ride-sharing, food delivery, etc., payment methods have now moved away from in-person exchanges of money and gravitated toward digitization.

Oliver Wyman, a leading international management consulting firm, proposed that the payments space has become key for a seamless shopping experience that provides a unique competitive advantage [

95].

The ability to leverage blockchain allows customers to use cryptocurrency in their transactions and allows a faster transaction settlement due to the reduction of centralized verification.

Currently, many transaction fees are associated with traditional banking strategies within the FinTech space. With the rise in payment solutions, technology experts have been trying to leverage different mechanisms to alleviate these fees. For example, merchants send batches of authorized transactions to their payment processors. A payment processor allows merchants to handle customer transactions via various channels such as credit/debit cards or bank accounts.

For every transaction, the card issuer charges the merchant a fee, and the payments processor charges a fee to facilitate all of the background work to perform the transaction. Therefore, the merchant has to pay additional fees to accept a customer’s payment. According to Square, the average cost for payment processing is about 2.87% to 4.35% per transaction [

96].

Along with transaction fees, the intermediaries (i.e., payment processors) create time delays during the transaction. Each intermediary has to process and validate the transaction, then send it to the next intermediary to process. Each intermediary processing the transaction increases the transaction time. This is not only inefficient but also poses a risk for fraud.

Blockchain payment solutions can eradicate transaction fees, allowing customers and merchants to settle transactions without intermediaries. Most existing payment solutions attempt to find the path with the least intermediaries to reduce cost.

Most blockchain payment methods can remove transaction fees by using smart contracts to remove all the intermediaries and decrease the time spent at each intermediary.

Removing all intermediaries (e.g., permissionless blockchain) or reducing the number of intermediaries (e.g., permissioned blockchains) gets rid of high transaction fees and reduces transaction times.

Another challenge in this category is the transaction error rate and lack of transparency. Errors in transactions within payment processing occur for many reasons. Sometimes there can be issues with the physical condition of the card, whether or not there is money in the card holder’s account or even the merchant’s terminal. There can be a lack of authorization, a duplicate charge, or even an incorrect amount charged [

97]. As the transaction passes through so many intermediaries, it is problematic to localize the step where an error occurs and thus troublesome to recover the loss.

Blockchain allows the entirety of the transaction to be transparent and immutable. Therefore, if one of the transaction participants is fraudulent, it is evident and easy to localize the fraudulent transactions.

Furthermore, the consensus mechanism that governs most blockchain payment solutions ensures that errors are minimized or eliminated. A lack of traditional financial services is the main issue that small-to-medium businesses face.

That is because they are not connected to a large financial institution. This is quite common in countries that lack the infrastructure to support large financial institutions but have many small-to-medium banks. These small-to-medium banks lack the same services as their larger counterparts or cannot conduct currency conversion. Without some basic services, merchants have difficulty processing and conducting electronic payments.

Blockchain enables small-to-medium banks to operate internationally by connecting them to larger financial institutions and banks worldwide. This way, when paying with fiat money or cryptocurrency, the transaction can travel through many intermediaries within the blockchain network. Thus, small-to-medium businesses can conduct the same transactions that larger businesses can do with large banks. This has opened up commerce in many areas of the world.

5.1.1. RippleNet

RippleNet is a network of financial entities such as banks, payment providers, and other financial institutions [

64]. RippleNet routes payments among the financial institutions on their network to settle transactions. The network itself is a decentralized global network that uses a Ripple-developed consensus protocol to validate account balances and transactions within the network. The network keeps track of all the transactions that occur and are publicly recorded and viewable. RippleNet uses Ripple Cryptocurrency, XRP. By having banks and payment providers within the network, Ripple removes the fragmentation within the payments processing landscape. Fragmentation results from the lack of interconnection between multiple securities markets. It can reduce the effectiveness of mass marketing techniques, erode brand loyalty, and result in customer orders being directed to markets that do not necessarily offer the best price.

Ripple’s solutions have opened up many services for small-to-medium banks and merchants, especially in countries with little financial infrastructure. RippleNet’s integration allows small banks and merchants to complete transactions.

Access to the network allows these previously challenged companies to complete cross-border transactions and allow different payment services locally. It also allows Ripple’s financial partners to reach many customers that they would not have been able to reach before due to the lack of infrastructure.

5.1.2. Stellar Network

The Stellar Network is a peer-to-peer payments network that originates from the early iterations of the XRP Ledger developed by Ripple. Stellar’s consensus protocol (SCP) utilizes smart contracts to carry out transactions [

98].

It uses the Quorum blockchain to emphasize security and speed up transactions within the network by utilizing the slices. A Quorum slice is a subset of nodes on the network that a given node chooses to trust and depend on [

99].

Stellar allows each node to choose what node is within its “trusted zone” (slice), enabling open participation and more jurisdiction over who is validating the transactions, leveraging the trust built through interpersonal interactions.

Interpersonal interaction is the communication that occurs between interdependent nodes that have some knowledge of each other. However, to reach a global consensus, there have to be intersections between Quorums—meaning that one node in the Quorum slice must also be in another Quorum slice to maintain the integrity of the network. This allows the network to reach a consensus without relying on a centralized/closed system. Quorum slices allow transactions to be accepted quicker by the nodes in the Quorum, thus increasing the speed at which the transactions are carried out.

Since the protocol also allows an open network, there are many ways to decrease the number of intermediaries the money travels through, thus providing shorter options that decrease transaction fees. Quorum slices play a significant role in ensuring the security of each node and the validity of transactions.

Table 6 compares and summarizes the solutions provided by RippleNet and Stellar Network.

5.2. Point of Sale Payments

This segment focuses on the actual place and technology used when a consumer initiates transactions for goods and services provided by a merchant. Point of Sale payments can be online or in-person.

This facilitates the transactional process from customer to merchant. It can also provide order management, inventory tracking, and card payment processing services.

One of the main issues faced by the point-of-sale segment is the high fees. That is because the point of sale systems are often physical devices in stores that can vary from cheap to costly. Whether or not a merchant buys or rents their hardware and software, there is still a non-negligible upfront cost. On top of the existing system, most points of sale vendors charge payment processing fees. Some vendors will allow the merchant to work with a third-party credit processor or require the merchant to pay some fee per transaction.

Other vendors also enforce processing service fees. These fees accumulate over time, and the merchant loses quite a bit of profit to fees. To cover these fees or the cost of the point-of-sale system, merchants often charge the customer a fee for processing the transaction. A point of sale operating within a blockchain framework can prevent processing fees regarding payment. The payment is quickly processed on the network itself. In addition, blockchain provides transparency, so merchants and customers can see all fees associated with the transaction.

Another issue is scalability. Since the point of sale systems tend to have physical devices in stores or online payment systems, the ability to scale is somewhat limited. Merchants fear many taxes and fees associated with credit card providers in addition to the allowed transaction rate in a given time frame. Maintaining large amounts of information is another challenge. Currently, traditional point-of-sale systems are required to maintain several databases and store information of various parties they need to connect with.

The information that needs to be stored relating to customers, such as billing, ratings, and orders, can be stored on individual nodes within a blockchain. Additionally, inventory can be stored on nodes across the chain. Alternatively, the network can be built on top of a decentralized database that can be accessed by nodes when needed. Smart contracts can then trigger processes regarding incoming data and ensure that transactions between existing and new nodes are complete and valid. This ensures security, as there is no one centralized database that can be tampered with [

100].

5.2.1. Algorand Blockchain

The Algorand blockchain is a payment solution with its point-of-sale implementation. Their application acts as a point of sale and communicates with a crypto wallet containing its currency (‘Algo’) through a transaction gateway. The Algorand process starts with an application that captures the transaction details and creates an unsigned transaction that is then sent to the transaction gateway. The transaction gateway forwards it to the wallet. The signing wallet receives the unsigned transaction and waits for approval from the consumer. The transaction gets signed and returned to the gateway if the consumer approves it.

The entire receipt is stored in an off-chain storage system—essentially recording the transaction in an immutable manner so it can be retrieved when needed [

101]. The storage system eliminates the need for data to be managed by the point of sale system/application as it is stored on an off-chain system. That way, all the data can be managed and retrieved at any time. The Algorand blockchain uses a pure PoS consensus algorithm that requires minimal computation.

The Algorand blockchain can handle around 1000 transactions per second [

102]. This increases efficiency, allows the blockchain to scale more rapidly, and significantly reduces settlement times.

Additionally, since the blockchain operates within its own network (from the point of sale application to the gateway into the wallet), there are no outside transaction fees associated with intermediaries in the transaction. The point of sale solution relies entirely on Algorand’s currency, ’Algo.’ Limiting to one currency poses a threat to scaling as it forces consumers to make an initial investment in Algos to carry out the transactions.

5.2.2. Pundi-X

Pundi-X is an end-to-end platform that allows consumers to use cryptocurrency at retail points of sale [

103]. Consumers must have a mobile wallet to use the platform. The mobile wallet maintains the public key encryption behind a standard password-based system to be user-friendly.

The platform also allows for “physical” smart card information to be loaded by the mobile app and allows the currency to be used even without access to a smartphone. Although Visa and Mastercard have networks that enable using cryptocurrency as payment through conversion to a fiat currency, the issue is that not all locations worldwide have access to these services.

Pundi-X targets under-serviced countries where it allows merchants and users to begin to transact more digitally. Pundi-X is currently marketing in Indonesia, giving a hardware device to merchants in retail environments when a smartphone is available. Merchants can carry out their transactions on a smartphone-based application as well.

The merchant sets all the rates required for the transaction at about 1–2%. 65% of that fee is given to the merchant, while the rest is given to Pundi-X or the digital asset issuer. Though this does not eliminate third-party fees, merchants still control the fee being charged.

The merchant is also very aware of who is receiving the fees. With the rise of digital assets, the Pundi-X platform enables people to use some of their investments to pay for goods. Most cryptocurrencies can be used on the Pundi-X platform. The platform is open, allowing digital assets to be submitted and evaluated on the possibility of being used as currency.

This enables long-term scalability as it allows the platform to start incorporating popular digital assets and opens up accessibility to various regions of the world. Furthermore, Merchants can choose whether to accept their payments in fiat currency or a stablecoin. A stablecoin is a crypto asset that is backed one-to-one by the U.S. dollar or other fiat currencies. Therefore, if a consumer chooses to pay with a more volatile coin, the merchant controls the currency in which they receive that payment. This has been very interesting for institutional players as it allows consumers to trade crypto at the institutional level.

A volatile coin is a cryptocurrency whose value and price fluctuate heavily by investor and user sentiments, government regulations, and media hype. On the contrary, stablecoins are unaffected by market volatility.

Pundi-X allows customers to keep their investment in stablecoins that remain in the digital assets space whenever the markets become volatile instead of selling all cryptocurrencies and moving to cash until they return to trading actively.

An issue for scalability may arise as the ledger needs to maintain much more information than just a simple transaction, especially if it is being used to calculate inventory for a merchant. Therefore, this large data storage could affect scalability and transaction time. Additionally, scalability comes into question when it is realized that a physical offline device is needed to scale the platform’s use as a whole. Therefore, since the XPOS machine is acting as a node, there will be slow growth when the adoption process is slow.

Figure 3 summarizes the issues faced by financial institutions within the point-of-sale subsegment. In

Table 7 and

Table 8, we summarize the solutions provided by Algorand and PaundiX.

5.3. International Money Transfer (Remittance)

Blockchain has revolutionized cross-border payments. Several companies (such as Ripple, Everex, SureRemit, etc.) have capitalized on using blockchain for remittance.

This subsection discusses the current issues faced by the remittance international money transfer segment and reviews how Everex and SureRemit solve these issues. Currently, the remittance market is dominated by the Society of Worldwide Interbank Financial Telecommunication (SWIFT).

SWIFT is a network of banks that connects all corners of the world. For a transaction to be completed, the transaction must go through a clearing or settlement center before the transaction is cleared.

SWIFT itself does not settle the transaction. It simply confirms the consumer’s transaction request. It is up to the banks to settle the transaction and relay the confirmation back to SWIFT so both sides can acknowledge the transaction’s completion [

104].

For a cross-border transaction to be executed, it has to pass through several banks because not all banks operate with a large variety of fiat currencies in other countries. Thus, a route between banks must be established to allow currencies to be exchanged into the desired receiving currency.

Blockchain can speed up the cross-border transaction time as a decentralized ledger. The transaction is settled almost as soon as the payment is made. By bypassing third-party intermediaries, sending money globally via blockchain reduces settlement time significantly.

Risk is another major issue while using international currency. The exchange rates for various fiat currencies change quite sporadically. Therefore, the long settlement time poses the risk of changing its value from when it is sent to when it is settled. Furthermore, most banks have a clause in their remittance contract that disclaims liability if the transaction remains incomplete. Thus, the risk is undertaken primarily by the person who initiates the transaction (the sender of the money).

A blockchain architecture mitigates the risk associated with currency exchange rates as the transactions are settled in real-time. Thus, the value sent is likely to be completed with minimal conversion rate changes. The lack of financial inclusion and infrastructure is another issue.

Finding a bank that operates with the desired country’s currency would result in using many intermediary banks that increase the transaction’s cost. Additionally, as some countries do not have the financial infrastructure, some people do not have bank accounts. Without a bank account, it is hard for money to exchange hands without physically handing the money to the desired recipient.

By using blockchain solutions, it does not matter whether or not the country has a bank connected to the rest of the world. It simply relies on the Internet and the conversion between cryptocurrency to the fiat currency of that country. Furthermore, some blockchain companies have taken an interest in the lack of infrastructure in underbanked populations and are finding ways for money to be exchanged and used within the country of that region. The cost of compliance is increasing due to the varying regulatory environments.

Compliance refers to the operational efficiency and reliability of the money being moved safely to the recipient. With the current SWIFT system, it is hard for the sender to track the transaction as it passes through many third-party financial institutions before it reaches the desired recipient. The transparency provided by the blockchain gives the sender the ability to track the transaction’s path.

The interoperability between countries becomes another delay aspect when attempting to complete the transaction. Different countries require different amounts of information for transactions to be processed.

5.3.1. SureRemit

SureRemit [

105] is a blockchain platform started by the makers of Suregifts. SureRemit provides cashless remittance services for cross-border businesses. The Remit token (RMT) can be used within the platform to pay bills and access vouchers. Customers can select the country to which they want the money to be sent, look for the category, and thus create a voucher that can be sent via text and email. These vouchers freeze the tokens. When the voucher is used, the merchant gets paid in their fiat currency or RMT [

105].

The Remit Token is not subject to the volatility of exchange rates; therefore, what the sender sends is what the receiver will receive [

106]. By utilizing vouchers sent over SMS and email, SureRemit breaks through the barriers created due to a lack of financial infrastructure. A customer does not need a bank account in the country of origin to pay and send vouchers. However, one drawback to using RMT vouchers when paying the merchant is that it is required for the merchant to be partnered with SureRemit. This creates an issue in places where merchants are not willing to partner with SureRemit. SureRemit leverages the Stellar platform and also partners with merchants to allow transactions to bypass different regulatory environments, as the RMT tokens can be converted into fiat currency via the Stellar platform. Furthermore, by using the SureRemit blockchain, the sender is cutting out banking intermediaries.

The minimal fees charged by SureRemit are very small compared to SWIFT fees for cross-border money transfers. Additionally, the transaction time is much faster, as Stellar transactions, on average, take 5 s to process without the need to interact with several intermediaries. Thus the risk associated with changing conversion rates does not pose a threat.

5.3.2. Everex

Everex aims to achieve financial inclusion of the underbanked [

107] as it enables wallet-to-wallet interactions through its cryptocurrency ”Cryptocash”. Cryptocash is an Ethereum-based token. Each unit of Cryptocash is backed by the fiat currency it represents. Cryptocash balances are underwritten by third-party cash custodians that allow users to convert their fiat currency into Cryptocash. They then can exchange and transfer the Cryptocash via blockchain. This allows Everex to obtain its goal of financial inclusion and avoid the volatility of current, non-stablecoin cryptocurrencies. Since the Everex token is a “fiat”-pegged stablecoin, the money being transferred is equivalent to the same fiat currency that is being transferred—without needing to be converted multiple times into various currencies. This poses a risk because the conversion from eFiat (Cryptocash) to fiat is subject to conversion rates and can be volatile. Furthermore, for transactions to occur, Everex needs international trusted banking partners to provide a 1:1 conversion rate. This can limit geographical inclusion as it depends on the existing financial infrastructure. If a banking partner does not exist in a region, the eFiat money cannot be redeemed and converted into fiat money.

Summary: This section discusses how blockchains allow Stellar and Ripple to make payments promptly and cost-effectively. We highlighted that RippleNet and the Stellar Network differ in their use cases. The Ripple network was built to provide liquidity solutions to larger institutions, while Stellar’s goal is to provide payment solutions on a smaller scale and facilitate global financial inclusion. The distributed ledger technology enables transparency of transactions and guarantees immutability, leaving a permanent record of transactions that have taken place. This opens up banking services to unbanked populations in certain countries. The Pundi-X and Algorand blockchain implementations leverage the blockchain architecture to have a point-of-sale system for underbanked and under-serviced populations, allowing sales for both merchant and consumer to be more accessible and less costly. The most common problems with remittance are the cost and time it takes for international transactions to complete. SureRemit and Everex solve these problems by utilizing the blockchain architecture and enabling nontraditional ways of sending money. They each approach the issue differently. However, both use the architecture to lower costs due to fees, reduce the time of the transaction, as well as to work around regulatory environments, and serve underbanked populations, which tend to be the main targets of remittance.

Table 9 and

Table 10 compare and summarize the solutions provided by SureRemit and Everex

6. Deposits and Lending

Deposits and Lending is a segment of the FinTech industry that relies on companies enabling people to obtain loans and monitor and collect information about their credit. This section focuses primarily on the Lending aspect of this segment as it has the largest application within the blockchain [

26] and provides an overview of Colendi, Figure, and Celsius Fintech companies.

Blockchain can speed up verification processes by simplifying and breaking down barriers to obtaining a loan and even allowing other people to lend money without the risk of not knowing who they are lending to. Businesses and consumers can use blockchain-aided platforms to initiate transactions and loans guaranteed through the ledger’s transparency and immutability.

Furthermore, blockchain has yet to reach a stage where it can support large business loans. Therefore, blockchain companies specializing in loans and deposits target many small businesses and personal loans. Small business and personal loan companies that utilize blockchain have leveraged the architecture in several ways.

Colendi uses blockchain to perform credit assessments, Figure uses blockchain to provide credit-based loans, and Celsius uses blockchain to provide crypto-based loans. However, within this segment, the problems that are encountered are relatively the same—the solution by each company is what differs.

One of the main issues in the small business and personal loans sector is the high fixed costs. Traditional loan approval is a lengthy process that involves several credit checks, background checks, paperwork, and other processes that often require the use of third-party intermediaries. These third-party intermediaries accrue costs that often have to be paid for by the customer who is taking the loan.

The fees are high, and often personal loans can be a significant barrier because the customer may not be able to afford them. Furthermore, the transaction fees from obtaining the loan and the administration fees associated with the loaner of the money also drive up the overall price of the loan—making the person or customer borrowing responsible for paying back a lot more than the amount that they require in the loan.

Blockchain has the capability of solving these problems by providing a clear and direct translation of the money. Creditworthiness can be tracked by transactions on the blockchain, providing an immutable and transparent account of the person’s financial history. It reduces a lot of the third-party verification needed to approve a loan, thus cutting costs down significantly.

Another main challenge is the lack of information to make a credit decision. The bank’s process of obtaining information about a person or company’s financial history and security to approve or reject the loan is lengthy. Due to the time required to conduct the investigation, many loans take a long time to process.

The information, though through a third party, is not always accurate. Depending on the accuracy, this can pose a risk for both the lender and the borrower. Therefore, there needs to be a transparent way to carry out checks. Blockchain can not only keep a ledger that ensures that financial transactions and trustworthiness can be seen by multiple parties but can also allow this data to be accessed in real-time. Therefore, no large hunt is needed to investigate whether or not the person or company is qualified for the loan. The information lies within the immutable ledger that is fully accessible.

Another component that blockchain allows for is reliance on cryptocurrency as an investment. Now, cryptocurrency can be an asset that is used to back certain loans. One of the largest pain points of loans is the time taken to approve the loan once requested. This is due to the immense amount of third parties that need to either provide information for the approval process or look over the loan application themselves. When evaluating collaterals, many people have to become involved in assessing the worth of the collateral to ensure that it can indeed cover the cost of the loan.

Furthermore, humans are involved heavily in the process. Therefore, time delays occur due to humans’ limited capacity when processing documents. Blockchain architecture enables the possibility of speeding up the process by the utilization of smart contracts and by verifying information via the immutable ledger. Smart contracts allow for agreements to be executed automatically and efficiently, thus reducing the time it takes from one approval action to another.

Furthermore, it reduces costs as legal and administrative fees can be cut. The immutable ledger allows documents and information to be shared via the ledger, thus eliminating the need for an investigation, as it can be inquired of the ledger. All the information is available and easily accessed by those processing the loans. When loans are backed by cryptocurrency, the currency exists on the blockchain. Thus, it is evident that the applicant has collateral funds, reducing any time needed to understand and investigate whether or not the collateral can support the loan.

6.1. Colendi

Colendi is a credit-scoring FinTech company that leverages new sources of information about borrowers to provide new avenues of creditworthiness [

108].

Colendi leverages the Ethereum blockchain and machine learning-based scoring technologies to evaluate user data segments; that is, the process of collecting data related to the transactions, smartphones, social media data, and more than a thousand pieces of personal information to generate a metric called Colendi Score.

This allows underserved and underbanked populations to have the ability to assess the population with less traditional information. Banks create scores dependent on their customers’ records, so the potential borrower is not evaluated based on their characteristics. The customers’ private data shows much more information than the bank can access. Thus Colendi’s goal is to utilize the transparent property of blockchain to create a high standard of evaluation transparency combined with their machine learning algorithms to allow for a comprehensive understanding of the borrower’s full potential.

The blockchain component of the Colendi platform has three main functions: identity management, collecting/storing data, and generating a credit score that can lead to a lending decision based on the stored data.

Due to its significant nature, the data storage combines blockchain and decentralized storage, Storj. The Colendi SDK allows users to interact with Storj without knowing the underlying technology.

The computation of scores is not done on the blockchain itself but rather by the Engima protocol, where data can be split across nodes and used for computation. The score is then relayed back and stored on the blockchain.

Colendi is opening up the opportunity for underbanked populations to gain access to micro-financed loans. If a user does not have enough data to secure a loan, Colendi offers the option for a borrower to stake Colendi tokens.

Though these tokens cannot be used as collateral against a loan, they provide a positive number when it comes to scoring. Furthermore, the data drawn upon goes beyond just traditional assets and bank history by including mobile data, social media data, and external data partners. All information is then stored in decentralized storage and drawn into the Engima protocol to create a score [

109].

All of these processes on the blockchain significantly reduce costs as everything takes place within the Colendi network and does not have to go through several intermediaries.

Furthermore, this reduces time delays as these activities are triggered via smart contracts and are all within the Colendi network. Thus, no time delay is associated with processing information by third-party companies verifying the data. Furthermore, this data is secured as only the Colendi network can access the decentralized storage system.

All that lenders garner is the final score the Colendi protocol produces. The blockchain provides an integral abstracting layer that ensures the protection and confidentiality of the borrowers’ data and information.

6.2. Figure

Figure is a FinTech company leveraging blockchain technology to speed up the loan application process. Figure has its own blockchain platform called Provenance. Provenance is used to store data within the blockchain to ensure that the data is accessible and untampered with.

The data is digitally signed and validated using smart contracts. This inherently reduces the need for third-party companies to verify the data, saving time and cost throughout the loan process. The transactions are granted by the administrator and need to be approved by the stakeholders.

The administrator is a key player in the blockchain as they create and review smart contracts held by the node to process transactions. They are also in charge of determining the cost of the transaction and the amount of stake that each node needs to hold. When a loan originator selects an offer from a consumer’s application for a loan, they generate a ”smart contract” that enables them to provide the amount required in the loan.

Once the loan is funded, the originator can either retain or sell the servicing, meaning that the originator has sold the rights to service the loan (i.e., collect the monthly principal and interest payments). The loan payments are collected through a remittance agent.

The administrator creates smart contracts related to the transactions by taking encrypted data from the member and transforming that information into encrypted data in the blockchain [

110].

Banks on the Omnibus network, called Omnibus banks, are responsible for facilitating fiat settlement on the blockchain.

When fiat is used, the members check to ensure that the Omnibus bank account has enough money. The bank then generates a settlement token backed by the member’s account. Then, the token is passed to the receiving member. This transaction is immutable and present on the blockchain such that it can be referenced later if needed. By performing all of the transactions on the blockchain, Figure cuts out all other intermediary fees, leaving only the origination fee as the primary fee on the blockchain. However, one caveat to using Figure for loans is that they default to traditional methods to determine creditworthiness, primarily a high credit score [

111]. This does not open up Figure to those with no banking infrastructure or to those who do not have a good credit history.

However, since the data is stored on the ledger, the approval time for the application is much faster as the records within the ledger are trusted. Furthermore, smart contracts enable many functions within the entire loan process to be automated and reduce any overhead of maintenance by a person.

6.3. Celsius

Celsius is a FinTech lending platform that leverages blockchain technology to allow people to use cryptocurrencies as collateral for fiat loans. Many people are investing their money into digital assets due to cryptocurrency hype.

They hold onto their digital assets as they invest in cryptocurrency with a long-term mindset. Simply put, they are investing now for significant payoffs in the future.

However, although some businesses and companies allow the use of cryptocurrencies in transactions, crypto assets still do not have a lot of “real value.” The only way to obtain value from them is to sell them—in which case, with such volatile prices, an investor does not know if the sale will be for profit or for a loss.

This is extremely important, as when people need cash instantly, they cannot always wait for the market to regulate such that their coins are valued higher. This often leads people to have to leverage real-world assets to obtain a loan from the bank.

Celsius now offers a platform where people can leverage their cryptocurrency as collateral to secure a loan in fiat currency. Rather than selling the cryptocurrency, members can leverage it while still holding onto that crypto portfolio to obtain future value [

112]. They even take it one step further and allow members to accrue interest on their crypto assets, similar to how money in a bank accrues interest. When asset holders deposit coins on the Celsius Network, they can earn interest on their coin balances.

Celsius token (CEL) is the heart of the blockchain implementation of Celsius. These CEL tokens are Ethereum ERC-20 coins issued on the Ethereum network. Celsius uses these tokens so that the lending and borrowing model is transparent.

The Ethereum platform is leveraged by Celsius such that it can utilize the idea of smart contracts, leverage quick transaction times, and leave a traceable footprint that allows for trade transparency on coin exchanges.

Lenders in the Celsius network can be anyone who deposits crypto assets into the Celsius wallet. These assets are stored in a “Lending Stake Pool” Celsius account. These accounts then transfer the coins to coin exchanges. The lender’s wallet then accrues interest in the form of Celsius tokens.

Lenders also can leverage their crypto assets in exchange for a fiat-based loan. In this instance, the user requests a loan and, in exchange, transfers crypto assets, which are locked. These crypto assets cannot be withdrawn until the loan is paid. The user then receives the fiat loan via a debit card or a direct bank transfer to a Celsius bank account. The payment plan and instructions are also issued at this time. Then, the user pays the loan installments like any other traditional loan. Once a loan is paid, the crypto assets are unlocked, and users may withdraw them as they please. However, if the user fails to pay, Celsius has the authority to sell the crypto assets in exchanges to recover the fiat value and reduce the loan amount. To borrow coins, a borrower deposits a fiat value into a custodian trader account owned by Celsius. To short the crypto asset, the borrower places a limit sell order. This sell order acts as a request that includes conditions of the trade (time and price) and a fee to access the assets.

While the borrower is requesting, the Celsius service checks to ensure the funds that are being requested are available based on the assets from lenders.

If the trade is approved by Celsius, then Celsius issues a sell order of the crypto asset on the exchanges to hold a short position on behalf of the borrower.

Once the crypto assets are sold, Celsius orders exchanges to purchase the crypto assets back. When the Celsius platform and the borrower make a profit off a short, the Celsius master account receives a percentage of that profit in addition to the fees accrued from holding the short position. The money received by the master account from the borrowers is in fiat. Still, the Celsius platform converts this fiat value into CEL tokens and then distributes it back to the lenders’ wallets as a form of daily interest. The amount that is distributed back is contingent on a Proof of Stake consensus.

In other words, the more crypto assets the lender puts into the Celsius Network, the more interest in the form of CEL tokens they accrue.

Lenders then can buy and sell these CEL tokens on exchanges however they wish. Additionally, lenders can pay off their Celsius loans via CEL tokens.

By using the CEL token, not only is Celsius offering a very transparent and efficient method of making exchanges, but it also provides an excellent incentive for people to lend out their crypto assets and use them as collateral for fiat currency while still holding onto them such that they can realize their long-term investments.

The Celsius network leveraging blockchain eliminates any third-party cost as the loans are lent and borrowed within the Celsius platform, effectively making it a P2P loan.

This cuts out any loan application or approval process that requires anybody other than the borrower or lender, making the entire process faster.

It also significantly reduces transaction and administrative costs. The loan is also not based on credit, but it is contingent upon the amount of stake (i.e., the amount of crypto coin) held and put up as collateral.

However, these crypto assets, when used as collateral, are also subject to volatility. Therefore, if the crypto asset loses its value, the Celsius network will require more assets to be put up as collateral.

Furthermore, the transactions all take place on Ethereum, and the ability to use smart contracts enables all internal functions, such as checking the availability of funding or efficiently performing the transactions, significantly reducing the overhead that comes with administrative work for traditional loans.