A Study of Financial Literacy of Investors—A Bibliometric Analysis

Department of Finance, College of Administrative and Financial Sciences, Saudi Electronic University, Riyadh 13316, Saudi Arabia

*

Authors to whom correspondence should be addressed.

Int. J. Financial Stud. 2022, 10(2), 36; https://doi.org/10.3390/ijfs10020036

Submission received: 26 March 2022

/

Revised: 12 May 2022

/

Accepted: 13 May 2022

/

Published: 16 May 2022

Abstract

:The present study investigates a conceptual research framework on financial literacy in various investment planning and decision-making stages. The study comprises a review of 2182 articles published in peer-reviewed journals from 2001 to 2022 (January). The study employed bibliometric techniques such as citation network analysis, co-citation analysis, content analysis, publication trends, and keyword analysis to analyze the literature on financial literacy. The study aims to add to the literature on financial literacy by proposing ten clusters to improve research on financial literacy in order to help investors learn better. Financial literacy has evolved from a fledgling discipline to a significant teaching and research tool. Therefore, it is vital to investigate and identify current research trends in this field. The results are essential to the financial community, given that institutions and society are increasingly emphasizing financial literacy to strengthen individual citizens’ responsibilities in designing their investment strategies.

1. Introduction

Financial knowledge is one’s understanding of financial matters. Several studies have used “financial knowledge” and “financial literacy” interchangeably. Different authors have conceptualized financial literacy as comprising financial awareness, abilities, and attitudes affecting people’s financial behavior Lusardi and Mitchell (2011). People with financial literacy can better manage their finances, save for emergencies, plan for their children’s education, and plan for their post-retirement years. Its continuing importance and people’s failure to fulfil even minimal criteria have pushed it to policy discussions Sevcík (2015).

Financial literacy, as defined by Mitchell and Lusardi (2011) is “knowledge of basic financial concepts and the ability to perform simple computations.” According to Huston (2010), financial literacy is personal finance knowledge and application. We link other concepts such as financial capability, education, and awareness to financial literacy. Basic financial concepts are futile unless reflected in financial behavior Atkinson and Messy (2012). “Financial literacy” and “financial capability” are synonymous terms Kempson et al. (2006). People can be financially literate if they have the knowledge, understanding, and skills to manage their finances, but they can not be called financially capable unless their behavior reflects this. Financial literacy is a broad concept and includes research centres on analyzing financial literacy outcomes, assessing levels among various population cohorts, variables impacting financial literacy, and the impact of financial education on improving financial literacy.

The present study analyzes financial literacy research and current trends using bibliometric methods. The study investigates financial literacy’s intellectual status, extracting the most recent research trends from analyzing the field’s most recent publications. Prior to this review, only a few literature reviews on specific themes of financial literacy had been published in the past two decades.

Using a bibliometric method, Ahmed et al. (2022) reviewed the artificial intelligence (AI) and machine learning (ML) literature in the finance industry. By inferring the thematic structure of AI and ML research in finance, Goodell et al. (2021) presents an overview of AI and ML research in finance using co-citation and bibliometric-coupling analysis. Patel et al. (2022) used a bibliometric citation meta-analysis to review the literature on financial market integration. Alshater et al. (2021) examines the Journal of Sustainable Finance and Investment from a bibliometric perspective. Alshater et al. (2021) employed the bibliometric approach to describe and analyze the evolution of the published literature on zakat and its different co-relations. Most of the reviews are focused on a single topic like financial clusters Khan et al. (2021), Islamic microfinance Hassan et al. (2021), and waqf literature Alshater et al. (2021).

None of them aspires to encompass the whole extent of financial knowledge. Furthermore, we could not locate any work analyzing the conceptual and intellectual combinations underlying this growing research area. Such limitations pushed us to combine quantitative and qualitative methodologies to compile the existing literature and give a roadmap for future research. This is the first comprehensive review-cum-bibliometric analysis of financial literacy. This review encapsulates the most recent advancements in the field, intending to assist practitioners, policymakers, educators, and academics eventually.

The present study analyzes financial literacy research and current trends using bibliometric methods. The study investigates financial literacy’s intellectual status, extracting the most recent research trends from analyzing the field’s most recent publications. Finally, it sums up its key findings and its conclusions and prospects.

In this context, the research questions addressed in this study are as follows:

RQ1: What is the distribution of financial literacy research based on the number of citations and publications per year, and research areas from 2002 to 2022?

RQ2: Which are the influential authors, institutions, countries, top journals, and top publications in the research field of financial literacy?

RQ3: How have co-citation studies advanced, resulting in meaningful clusters with a specific research focus?

RQ4: What are the topmost active areas, recent research trends, and emerging themes in the research field of financial literacy?

This research finds the contributions of researchers, institutions, countries, scientific journals, and studies to financial literacy research. Furthermore, ten identified clusters highlights the importance of financial literacy research and its future scope. Finally, the study highlights the research field’s most active areas, recent research trends, and emerging themes.

The rest of this paper is designed as follows: Section 2 delineates materials and methods of analysis and data search. Section 3 covers results on publication trends, citation network analysis, co-citation analysis, topmost active areas, recent research trends, and emerging themes. Section 4 includes the discussion. Section 5 suggests future research avenues in reference to theory, methods, and contexts. The study is concluded in Section 6.

2. Materials and Methods

In order to analyze the literature on financial literacy and provide insights, the current study used bibliometric techniques such as citation network analysis, co-citation analysis, clustering, content analysis, publication trends, and keyword analysis. Bibliometrics is the most widely used method for tracing a study field’s knowledge of anatomy Wu and Wu (2017). It is also used to analyze research themes Blanco-Mesa et al. (2017). Thus, the bibliometric analysis provides scholars with a powerful tool to study a specific research area, analyze the literature on financial literacy and provide insights. The current study used bibliometric techniques such as citation network analysis, co-citation analysis, clustering, content analysis, publication trends, and keyword analysis. In this paper, data for this study were retrieved from Clarivate Analytics’ Web of Science core collection, the world’s premier database for published articles and citations. By focusing on the database itself, Li et al. (2018) conducted a pioneer empirical analysis of the Web of Science between 1997 and 2017. They uncovered the characteristics of the academic use of WoS across countries/regions, institutions, and knowledge domains. Moreover, to depict the non-transparent use of WoS, Liu (2019) also finds that many papers have mentioned WoS in their topic field.

The study started in January 2021 and collected data from January 2002 to January 2022. The study began with a search term in the “Topic” field of the Web of Science (WoS) database: “financial literacy” OR “investor financial knowledge” OR “financial education,” yielding 2368 initial results. To ensure the inclusion of relevant articles, articles related to financial literacy or financial education, financial knowledge, and articles dealing with a relatively broader and closely related topic were shortlisted for final analyses. Furthermore, only scientific articles published in peer-reviewed journals were considered, excluding proceedings papers, book chapters, working papers, communications, and conferences, to ensure the inclusion of top-tier publications Liu et al. (2015). To avoid possible consequences, duplicate articles were removed. The search was then refined to include articles written in English, yielding 2182 results. After going through the abstracts, 2182 full-length papers were separated for further analysis.

The VOSviewer software version 1.6.17 (Leiden University, Leidon, The Netherlands) Van Eck and Waltman (2010) was used to perform citation network analysis and keyword analysis that provides scholars with a powerful tool to study a specific research area, analyzing citations, geographical distribution, and keyword analysis. CiteSpace software version 5.8.R3 Chen (2014) was used to conduct co-citation, clustering, content analysis, and recent research trends.

3. Results

3.1. General Descriptive Statistics

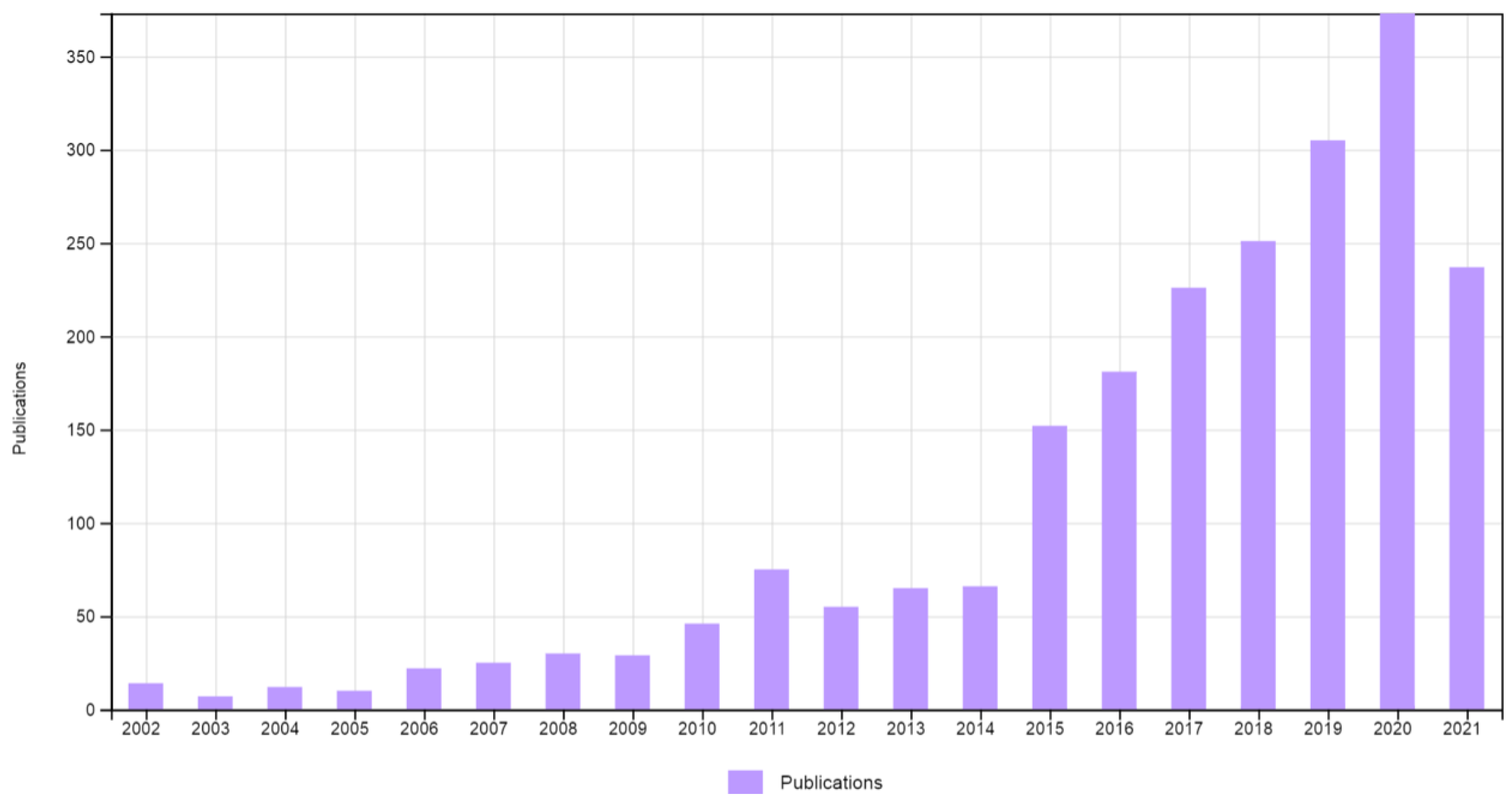

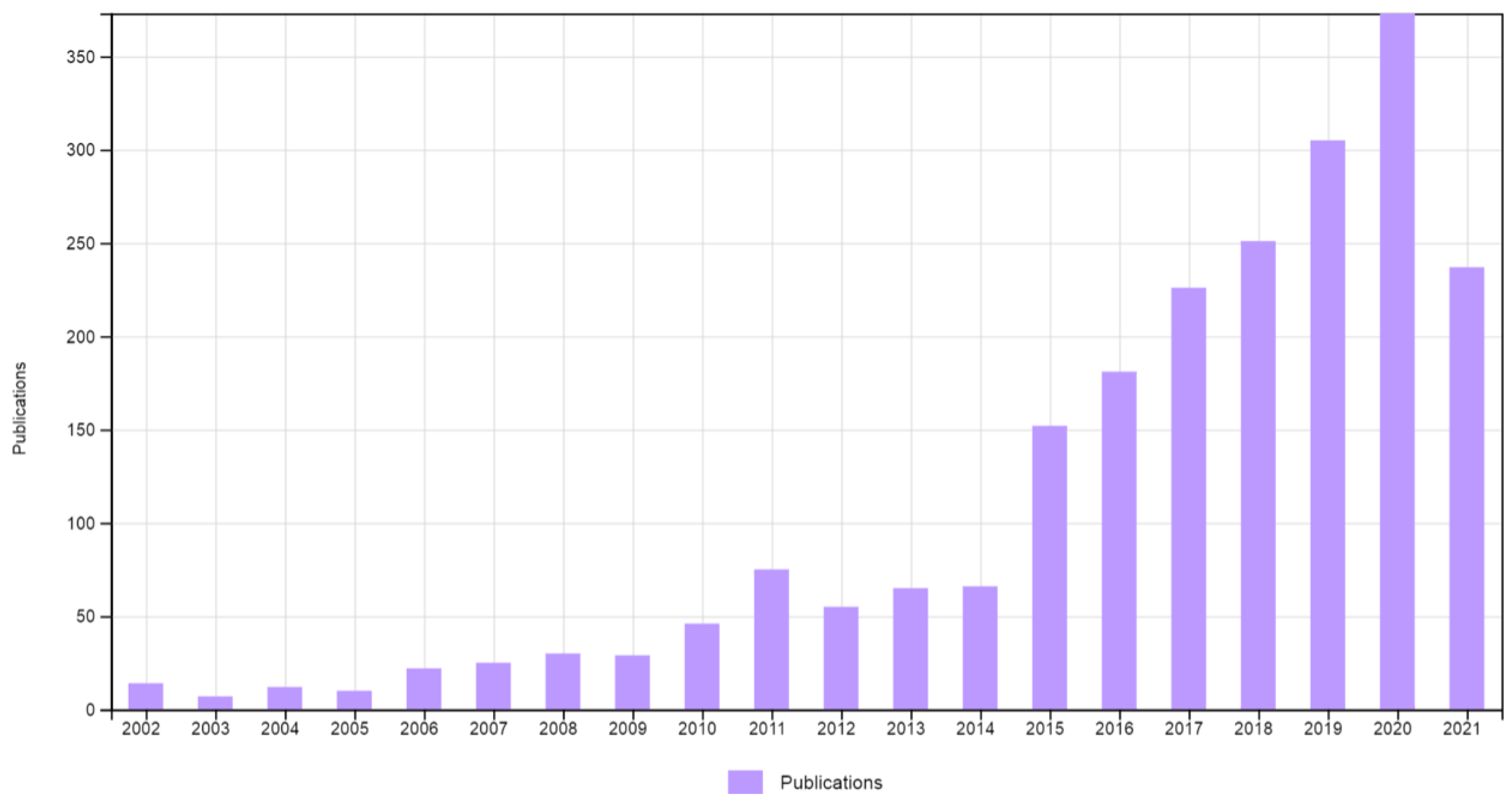

The distribution of financial literacy research is presented in Figure 1 and Figure 2 based on the number of annual citations and publications per year. The number of academic articles published in financial literacy steadily increases, with even more citations than the previous year. It determines the relevance of the study. After a detailed examination, it was found that financial literacy articles were published in 106 countries, including the United States, England, Australia, the People’s R China, Germany, and Malaysia.

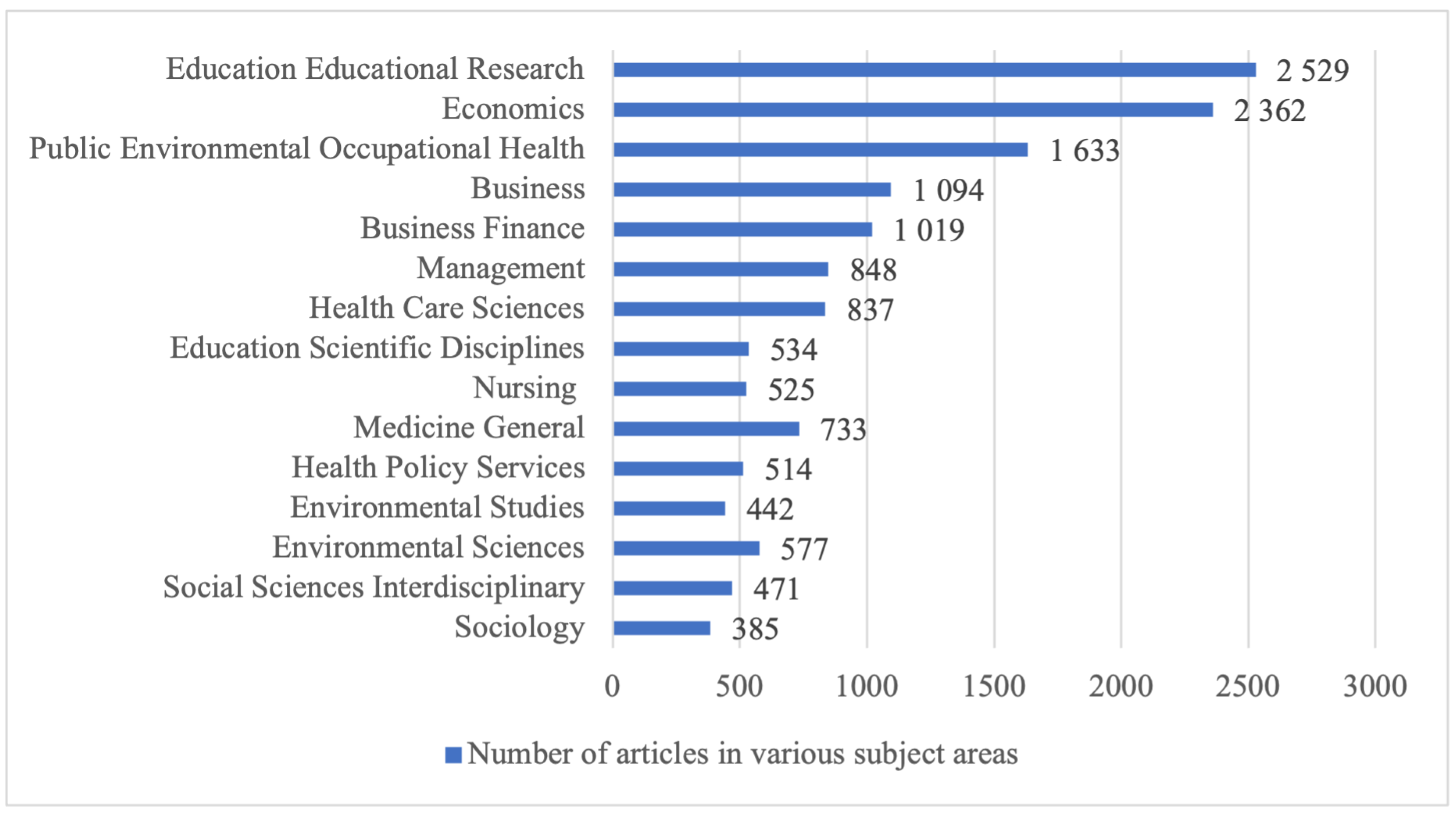

Figure 3 shows the top research areas with more than eight articles published on financial literacy. Financial literacy is connected well to economics, business, finance, management, and other fields. It implies that the topic is multidisciplinary. Surprisingly, there is a lack of study in different areas, particularly interdisciplinary sociology and social sciences.

3.2. Citation Network Analysis

Authors who have made a substantial contribution in the field were analyzed using citation analysis. The top authors in this field are shown in Table 1. According to our dataset, 5227 authors affiliated with 2188 organizations in 106 countries published articles on financial literacy. With 14 publications, Annamaria Lusardi is first on the list, followed by Olivia S. Mitchell with 11 studies. Annamaria Lusardi and Olivia S. Mitchell also receive the highest citations, 1833 and 870. The two authors are experts in financial literacy, education, and social security. They have written several papers on these topics.

Citation analysis was then conducted to identify the top 15 contributing institutions for paper contribution. The University of Pennsylvania with 25 articles, George Washington University with 18 publications, and Tilburg University with, 17 publications, are the most active universities working on financial literacy. These institutions are in the United States, proving that financial literacy research is concentrated in Western countries, showing a wider gap between research in the United States and research in other parts of the world. Table 1 also shows the top 15 countries with the most articles on this topic, with the United States (586 articles), England (193 articles), and Australia (171 articles) ranking first, second, and third, respectively.

Journals that have contributed to publishing research on this subject were also examined using citation analysis. Many journals have contributed to financial literacy, demonstrating how widespread the topic is in the literature. The 2182 publications analyzed are dispersed across 534 journals. It was discovered that 132 journals out of 534 had published at least five studies in this field. Table 2 lists the 15 most prominent journals publishing on financial literacy. The most prolific platform is the Journal of Pension Economics and Finance, with 45 articles published, followed by the Social Indicators Research.

Citation analysis of documents was further conducted to explore the most influential studies on financial literacy. Out of 2182 articles, 127 studies are based on citations with a threshold of a minimum of 50 citations. The top 15 contributing studies are listed in Table 3. Fernandes et al. (2014) top the list with 487 citations, followed by Van Rooij et al. (2011) with 437 and Lusardi and Mitchell (2011) with 421 citations. Fernandes et al. (2014) analyzed 168 publications covering 201 studies to determine the relationship between financial literacy and financial education. They found that partial effects of financial literacy are drastically reduced when psychological features missed in previous studies are controlled or a financial literacy instrument is used to adjust for omitted variables. Van Rooij et al. (2011) found that many respondents have basic financial knowledge, including understanding interest compounding, inflation, and the time value of money. Lusardi and Mitchell (2011) found that financial literacy is critical to retirement security.

3.3. Co-Citation Analysis

A co-citation links two items that are both cited by the same document. The frequency with which one paper cites two other articles is known as co-citation Small (1973). Co-citations indicate that the two articles are closely related in their broader scientific field of study Culnan (1987). Citespace software is used to perform co-citation analysis, identifying the most influential publications in an area of research and the intellectual structure of the topic.

3.3.1. Clustering

Clustering enables thematic analysis of the co-citation network Xu et al. (2018). To focus our study on the most important articles in the field, we chose a co-citation threshold of 20 papers. CiteSpace software identified ten clusters during the clustering process, as shown in Figure 4. The quality of a clustering setup is measured by its silhouette Chen et al. (2010). The silhouette value for each point measures how similar that point is to points in its cluster compared to points in other clusters. The silhouette value ranges from −1 to +1. A high silhouette value indicates that it is well-matched and poorly matched to neighboring clusters. The clustering solution is appropriate if most points have a high silhouette value. If many points have a low or negative silhouette value, the clustering solution may have too many or too few clusters Madureira et al. (2017). The cluster homogeneity is shown in the Silhouette column depicted in Figure 4. If the clusters in comparison have comparable sizes, the higher the silhouette score, the more consistent the cluster members are. A high homogeneity does not mean much if the cluster size is small. For example, clusters #22 and #25 have six members and silhouettes of 1.00, indicating that all six references are likely citation references from the same underlying author.

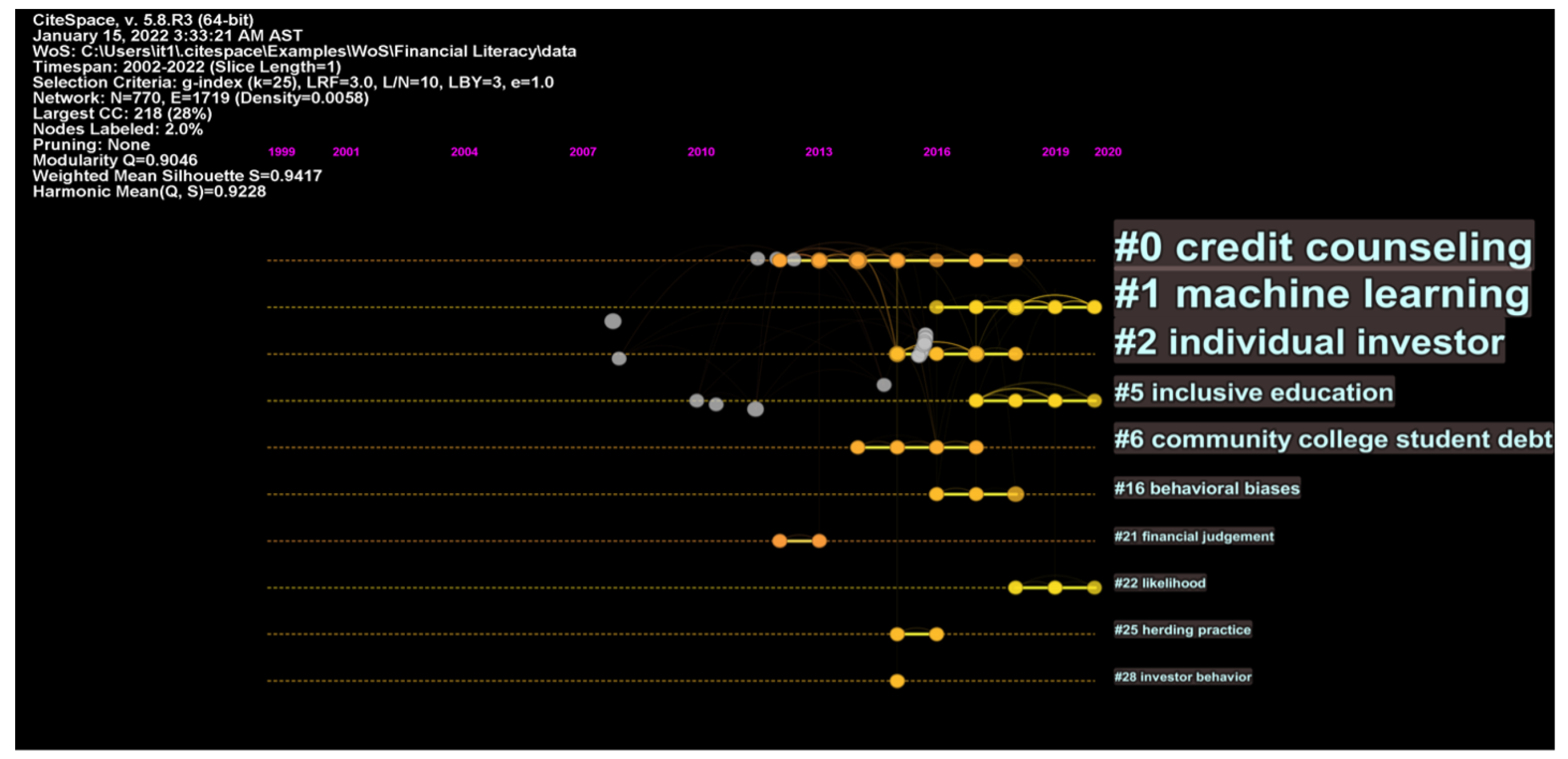

In a timeline view, a co-citation map of co-cited references is displayed based on the citing behaviors of the authors who published the sampled articles. On a horizontal timeline, each cluster is arranged. The arrow of time points to the right Chen (2014). In Figure 5, the network’s signature in the top left corner shows the modularity and silhouette scores. The modularity of a network refers to how easily it can be decomposed into multiple components or modules. This metric serves as a reference point for the overall clarity of a network decomposition Chen et al. (2010). The modularity Q and the mean silhouette scores are two necessary measures that tell us about the network’s overall structural properties Chen (2014). The modularity Q of 0.9046 is relatively high, so the network is reasonably divided into loosely coupled clusters. The mean silhouette value of 0.9417 shows that these clusters are highly homogeneous. A cluster’s average year of publication indicates that it is composed of most recent or mostly old papers Chen (2014).

The clusters are numbered in descending order of cluster size, as shown in Figure 5, starting with the biggest cluster #0, the second-largest #1, etc. Credit counseling appears to be the most prominent (cluster #0 has the most member references). Machine learning (Cluster #1) is the second largest. Individual investor (Cluster #2) is the third type. The fourth (Cluster #5) is inclusive education, and the fifth (Cluster #6) is community college student debt. The smaller clusters are behavioral biases, financial judgment, likelihood, herding practice, and investor behavior. Thus, we now have a general idea of what financial literacy research appeared like between 2002 and 2022.

3.3.2. Content Analysis

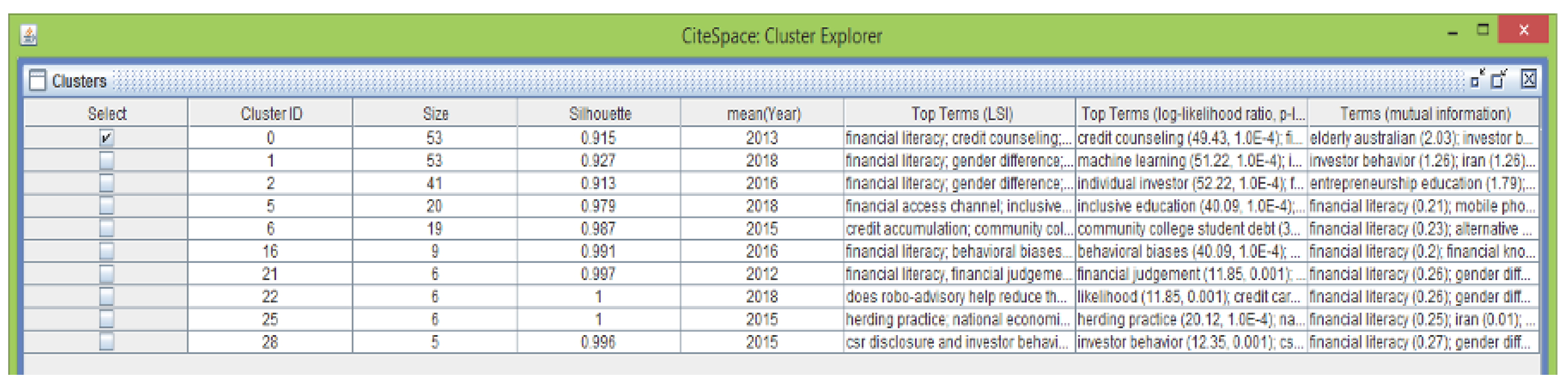

A detailed content analysis of ten clusters was conducted. CiteSpace’s cluster explorer (Figure 6) enables us to explore further into these clusters. CiteSpace extracted the most representative sentences from the abstracts of the citing articles to each cluster based on a sentence with a high degree of centrality. They can tell us about the most common contexts in which they are cited.

Larger nodes represent more cited papers, and a thicker link means that connected nodes are cited more often. In addition, 770 nodes, 1719 links, and 10 clusters are represented on the map (Figure 5). Initially, there were 244 clusters, but ten were identified after a qualitative evaluation based on content analysis. Clusters #22 and #25 were not included in the content analysis due to the high Silhouette value of 1. In other words, clusters #22 and #25 may reflect a single paper’s citation behaviors, making them less representative.

Cluster #0: Credit Counseling

Out of the 218 studied articles, 53 papers were categorized in Cluster #0, the largest cluster comprising the most documents. As observed in the cluster, the focus of this research was on credit counseling. Financial literacy is essential since it lowers the barriers to purchasing complex derivatives. In addition, household wealth, gender, residence, and information sources affect participation rates in derivatives markets Hsiao and Tsai (2018). Shen et al. (2016) investigate that more financially literate people have fewer financial problems. Gender, work status, and household income significantly affect the likelihood of a financial dispute. Financial literacy and social training can substantially improve children’s savings attitudes and behaviors Supanantaroek et al. (2017).

Cluster #1: Machine Learning

With 53 papers, Cluster #1 is the second largest of the ten clusters. The cluster’s focal point is machine learning in financial literacy related to investment return, information provision, student outcomes, behavioral aspects, and risky asset behavior. The cluster focuses on various theories and models such as the Bayesian two-part latent variable model, multinomial logistic regression, SmartPLS technique, regression analysis, meta-analysis, serial mediation model, and automated financial advisors (Robo-advisors).

Cluster #2: Individual Investor

Cluster #2 has 41 documents. The focus of this cluster is on the individual investor, family communication pattern, investment decision, and assessment of consumer literacy. It is followed by an analysis of how illiteracy affects economic decisions and suggested corrective actions to bridge the literacy gap. Jiang and Lim (2018) analyzes how those who have a higher level of trust have a lower risk of defaulting on household debt and higher net worth. Clark et al. (2017) found that the most financially knowledgeable investors: (a) held 18% more stock; (b) could expect to earn eight basis points per month more in excess returns; (c) had 40% higher portfolio volatility, and (d) had portfolios with about 38% less idiosyncratic risk.

Cluster #5: Inclusive Education

The focus of Cluster #5 was to provide a framework for financial literacy and acceptance in the educational sector. It consists of 20 publications emphasizing various dimensions of financial literacy, such as inclusive education, knowledge economy development, economic participation for all, and mobile access to financial channels Ali et al. (2020); Asongu and Kuada (2020); Tchamyou (2020). As a result, it can be inferred that research emphasis in this cluster is on more discussed and specialized areas of study.

Cluster #6: Community College Student Debt

Cluster #6 has 19 documents related to college student debt behavior and related issues such as credit accumulation, loan repayment burden, student loan design, and borrowing outcome. Furquim et al. (2017) examine each of the steps that lead to student debt: applying for aid, borrowing, and deciding how much to borrow. At each step of the student borrowing process, they find significant differences by the generational process. According to Kaiser and Menkhoff (2017), financial education has a significant impact on financial behavior and, to a more considerable extent, financial literacy. Chapman and Dearden (2017) show that Stafford loans are associated with challenging financial circumstances for a low minority of loan recipients in the United States. In addition to it, higher financial literacy and knowledge of federal student loans are related to lower loan aversion for education Boatman and Evans (2017).

Cluster #16: Behavioral Biases

The relationship between demographics and individual behavioral biases was the focus of Cluster #16 with nine documents. Baker et al. (2019) evaluated the influence of age, gender, and education on investing decisions. Furthermore, investing decisions are also influenced by emotion, overconfidence, and herd behavior. Lim et al. (2018) discovered significant mediating effects of risk perception and attitude in the sequential positive relationship between financial knowledge and financial behavioral intention to invest. Boutsouki (2019) explores the influence of the environment on consumers’ impulsive behavior during a financial crisis, and the characteristics of specific consumer segments.

Cluster #21: Financial Judgment

Financial literacy, financial judgment, and retirement self-efficacy among older trustees of self-managed superannuation funds were the focus of Cluster #21.

Cluster #28: Investor Behavior

In Cluster #28, Riviere-Giordano et al. (2018) and Gödker and Mertins (2018) highlight the need to provide a robust framework for CSR disclosure and investing behavior. The cluster also explains the determinants of young adults’ subjective and objective risk attitudes in theoretical and real-world financial decisions. Compared to older adults, young adults generally show a similar degree of personal risk aversion Oehler et al. (2018).

3.4. Topmost Active Areas, Recent Research Trends, and Emerging Themes

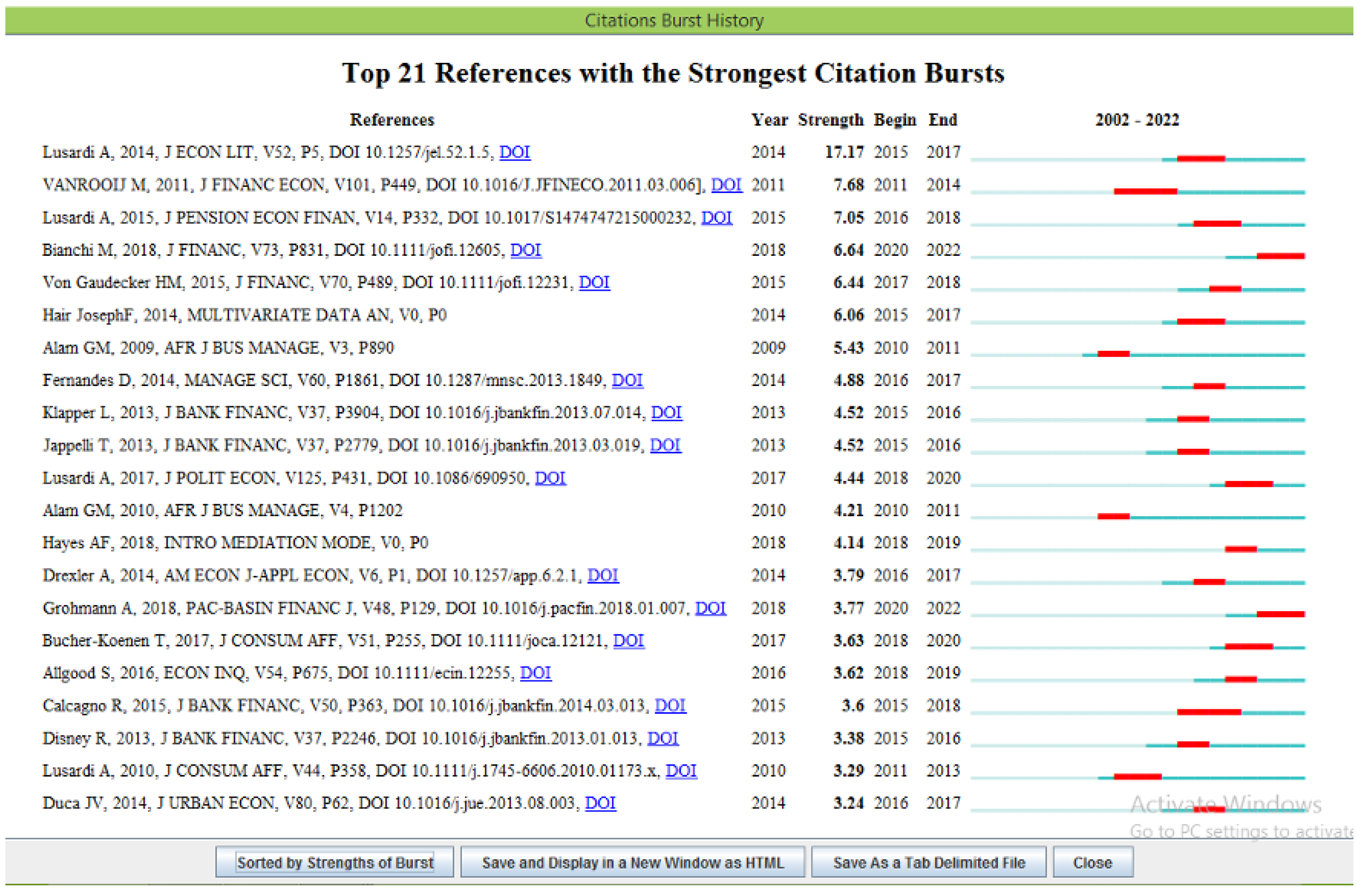

Citation burst is another indicator of an active area of research. Citation burst refers to detecting a burst event that might last multiple years or a single year. A citation bursting is evidence that the publication is associated with a rise in citations. In other words, the paper has attracted the scientific community’s attention. Furthermore, if a cluster has several nodes with high citation bursts, the cluster represents an active study area or a recent trend Chen (2014). Citation Burst History can generate a list of publications associated with citation bursts. Figure 7 represents which references would have the most citation bursts, and the periods during which the bursts occurred. For example, in the list, Lusardi and Mitchell (2014) has the most bursts among publications on financial literacy published since 2014. It is also interesting to note that Van Rooij et al. (2011) had the second-highest citation burst between 2011 and 2014. The other references in the list are Lusardi and Tufano (2015); Bianchi (2018); Von Gaudecker (2015); Hair et al. (2014); Alam (2009); Fernandes et al. (2014); Klapper et al. (2013); Tullio and Mario (2013); Lusardi et al. (2017); Alam and Hoque (2010); Hayes (2018); Drexler et al. (2014); Grohmann (2018); Bucher-Koenen and Lusardi (2011); Allgood and Walstad (2016); Calcagno and Monticone (2015); Disney and Gathergood (2013); Lusardi et al. (2010), and Duca and Kumar (2014).

In order to determine the most recent research trends and hottest topics, we have analyzed the contents of the articles about the topics published in 2019 and 2021 (January to December), extracting the main research lines and summing them up in Table 4.

The author keywords represent the themes of the research articles Comerio and Strozzi (2019). 8538 keywords were identified in 2182 publications—the top keywords used in financial literacy research from 2002 to 2022. “Financial literacy” is the most frequently used keyword, with 348 occurrences, indicating that this word alone is used as a concept in the literature.The other three most used keywords are “performance” (233 occurrences), “education” (249 occurrences), and “impact” (186 occurrences).

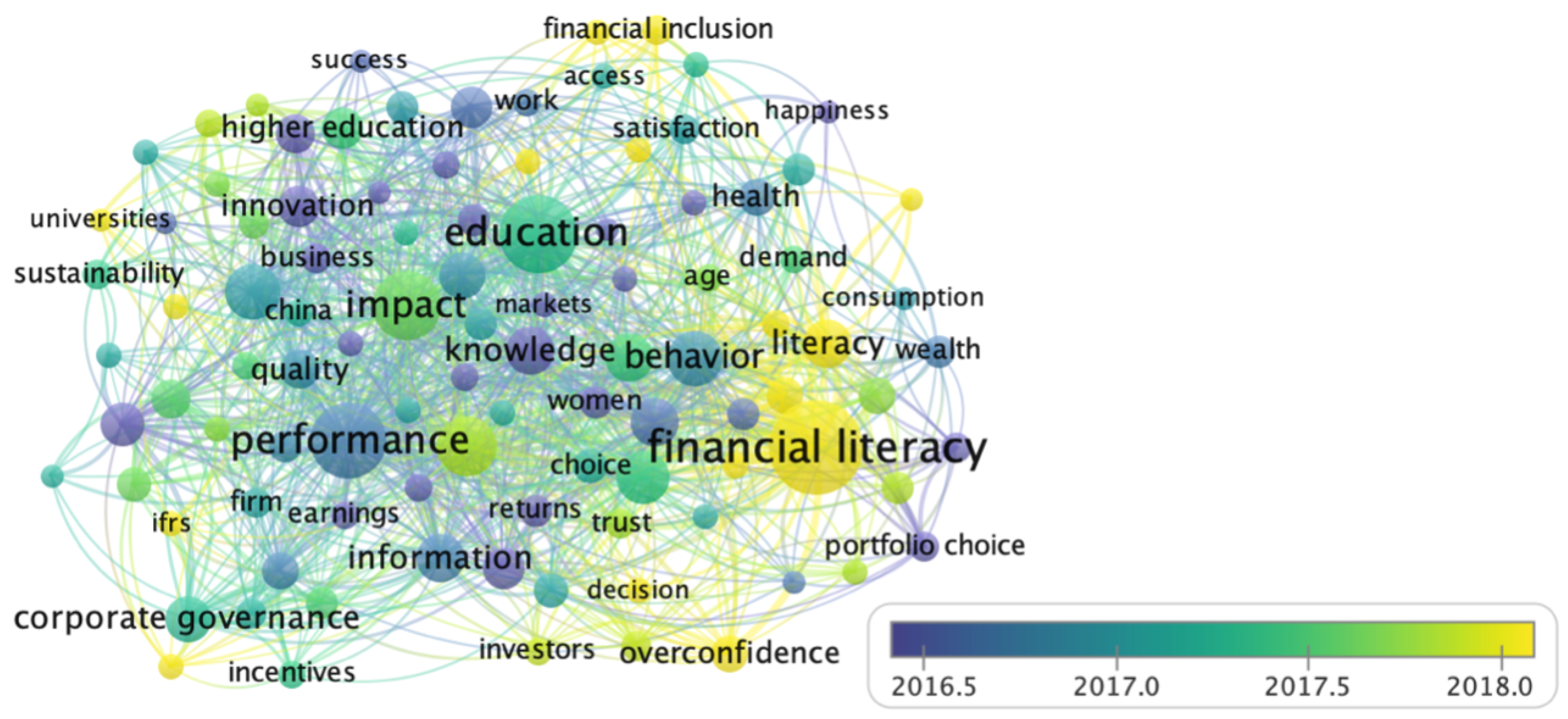

In the co-occurrence analysis, keywords that occurred ten times in the studies were used. A total of 300 keywords met this criterion, from which we selected the top 100 and grouped them into five clusters. By looking at the overlay visualization map of keyword co-occurrence analysis, it is clear that these keyword clusters give a notion of the subject linkages that are common in research projects. From Figure 8, it is evident that the clusters are connected and that the circles are close to each other, which indicates the researchers in related clusters are more likely to be cited in a similar situation. The overlay visualization map of keyword co-occurrence analysis identifies the year’s trending research topics. Financial literacy trends are shifting towards household finance, accounting education, financial capability, financial advice, financial behavior, financial well-being, overconfidence, and financial inclusion Calcagno and Monticone (2015).

4. Discussion

The current study looks at a theoretical research framework for financial literacy in various investment planning and decision-making stages. It contributes to the scientific literature on financial literacy in the finance and education sectors and expands on previous opinions. It suggests and performs bibliometric analysis to find the most important studies (citations, co-citations).

Our first research question was about the distribution of financial literacy research based on the number of citations and publications per year, and research areas from 2002 to 2022. It was found that the number of academic articles published on financial literacy each year steadily increases, with even more citations explaining the relevance of the study. Financial literacy is connected well to different research areas and implies that the topic is multidisciplinary. The second research issue is citation network analysis. According to our result, Annamaria Lusardi is the most influential author, with 14 publications. The topmost institution is the University of Pennsylvania, with 25 articles. The United States, with 586 articles, is the top country contributing to financial literacy. Financial literacy articles are found in both finance and economic journals. Hence, researchers should take interdisciplinary approaches to financial literacy research and development to synthesize information from both areas. Citation analysis of documents was further conducted to explore the most influential studies on financial literacy. Fernandes et al. (2014) and Van Rooij et al. (2011) from Europe top the list with 487 and 437 citations, respectively; and Lusardi and Mitchell (2011) with 421 citations.

The third research question was to find how to have co-citation studies advanced, resulting in meaningful clusters. Ten clusters have been found in thematic analysis, each focusing on a different aspect of financial literacy, from conceptualization to methodologies and application of financial literacy in the financial system. It also shows the relationships between the clusters and argues that better approaches would lead to better financial literacy applications in both financial and educational contexts. The fourth research issue was about the topmost active areas, recent research trends, and emerging themes in the research field of financial literacy. There are various active areas of research, recent research trends, and emerging themes that have been identified as household finance, accounting education, financial capability, financial advice, financial behavior, financial well-being, overconfidence, and financial inclusion. The overlay visualization map of keyword co-occurrence analysis identifies the year’s trending research topics. The authors also contend that the financial literacy and education industry have gotten a lot of attention from researchers throughout the time. This study reveals an opportunity for institutions and researchers to collaborate to improve the working of financial and educational sectors. Researchers are making significant attempts to learn more about the subject in general. There is a lot of scope for theoretical advancement, contextual coverage, and methodological improvements. Financial literacy is a topic with far-reaching implications for economic health, and its advancement can pave the way for more competitive and stable economies.

5. Limitations and Future Research

The limitations of the study are as follows:

- The study was based on a review of 2182 publications published in the last two decades on financial literacy in the financial sector. The study adopted a combination of keywords, and various keyword combinations may have shown different results.

- To better understand the topic, future studies should include all ten clusters. Because of these findings, this field requires more in-depth research.

6. Conclusions

The study employed bibliometric analysis to review the literature on financial literacy for 20 years (2002–2022). New scientific studies on financial literacy are produced every year, with citations indicating the study’s relevance. Financial literacy is multidisciplinary and is significantly linked to various academic disciplines. The contributions of researchers, institutions, countries, scientific journals, and studies to financial literacy research in the financial and educational sectors are explored in detail. It also provides financial literacy researchers opportunities to study the gaps in knowledge, technical expertise, skill sets, innovation, and implementation. Finally, exploring all ten identified clusters of financial literacy—viz., credit counseling, machine learning, individual investor, inclusive education, community college student debt, behavioral biases, financial judgment, likelihood, herding practice, and investor behavior—is pivotal to providing as many options to investors as possible. These clusters emphasize the significance of financial education and the consistency of current research at higher education institutions that focus on learning and individual efficiency. Finally, the study highlights the topmost active areas, recent research trends, and emerging themes in the research field.

This paper persuades scholars to perform scientific literature reviews, including bibliometric techniques, meta-analysis, and literature reviews. In this study, our approach was to explore the scope of financial literacy and the benefits of financial knowledge and technology in the financial industry. It is also important to note that, as technology advances, the current focus on how investors adapt to emerging innovations will continue. Because financial literacy is so important in society, further research is needed. All government initiatives that included financial literacy training could be given directly to individuals or through educational institutions. The financial literacy program offers a constructive solution to obvious shortcomings in financial decision-making.

Author Contributions

Y.A. conceptualization, methodology, writing—original draft, review and editing, and analyzed the findings, Y.A. and M.S.A. conceptualization, formal analysis, software, visualization, writing—review and editing, N.S. and A.A. writing—data curation, methodology, resources, validation, M.S.A. supervised and reviewed the entire study. All authors have read and agreed to the published version of the manuscript.

Funding

This research was funded by the Deputyship for Research & Innovation, Ministry of Education in Saudi Arabia, Grant No. 8027. The APC was funded by the Deputyship for Research & Innovation, Ministry of Education, Saudi Arabia.

Institutional Review Board Statement

Not applicable.

Acknowledgments

We thank Raed Ibrahim Alhamad, Dean of Scientific Research, Saudi Electronic University, for providing grant assistance in this paper. We are also indebted to all the text authors, research papers and articles, and websites we have referred to.

Conflicts of Interest

The authors declare no conflict of interest.

Abbreviations

The following abbreviations are used in this manuscript:

| TC | Total Citations |

| TP | Total Publications |

References

- Ahmed, Shamima, Muneer M. Alshater, Anis El Ammari, and Helmi Hammami. 2022. Artificial intelligence and machine learning in finance: A bibliometric review. Research in International Business and Finance 61: 101646. [Google Scholar] [CrossRef]

- Alam, Gazi Mahabubul. 2009. Can governance and regulatory control ensure private higher education as business or public goods in bangladesh? African Journal of Business Management 3: 890–906. [Google Scholar]

- Alam, Gazi Mahabubul, and Kazi Enamul Hoque. 2010. Who gains from brain and body drain business-developing/developed world or individuals: A comparative study between skilled and semi/unskilled emigrants. African Journal of Business Management 4: 534–48. [Google Scholar]

- Ali, Mohammad Mahbubi, Abrista Devi, Hafas Furqani, and Hamzah Hamzah. 2020. Islamic financial inclusion determinants in indonesia: An anp approach. International Journal of Islamic and Middle Eastern Finance and Management 13: 727–47. [Google Scholar] [CrossRef]

- Allgood, Sam, and William B. Walstad. 2016. The effects of perceived and actual financial literacy on financial behaviors. Economic Inquiry 54: 675–97. [Google Scholar] [CrossRef]

- Alshater, Muneer M., Osama F. Atayah, and Allam Hamdan. 2021. Journal of sustainable finance and investment: A bibliometric analysis. Journal of Sustainable Finance & Investment 2021: 1–22. [Google Scholar]

- Alshater, Muneer M., M. Kabir Hassan, Mamunur Rashid, and Rashedul Hasan. 2021. A bibliometric review of the waqf literature. Eurasian Economic Review 2021: 1–27. [Google Scholar] [CrossRef]

- Alshater, Muneer M., Ram Al Jaffri Saad, Norazlina Abd Wahab, and Irum Saba. 2021. What do we know about zakat literature? a bibliometric review. Journal of Islamic Accounting and Business Research 12: 544–63. [Google Scholar] [CrossRef]

- Asongu, Simplice A., and John Kuada. 2020. Building knowledge economies in africa: An introduction. Contemporary Social Science 15: 1–6. [Google Scholar] [CrossRef]

- Atkinson, Adele, and Flore-Anne Messy. 2012. Measuring Financial Literacy: Results of the OECD/International Network on Financial Education (INFE) Pilot Study (OECD Working Papers on Finance, Insurance and Private Pensions, No. 15). Paris: OECD Publishing. [Google Scholar] [CrossRef]

- Baker, H. Kent, Satish Kumar, Nisha Goyal, and Vidhu Gaur. 2019. How financial literacy and demographic variables relate to behavioral biases. Managerial Finance 45: 124–46. [Google Scholar] [CrossRef]

- Banks, James, and Zoë Oldfield. 2007. Understanding pensions: Cognitive function, numerical ability and retirement saving. Fiscal Studies 28: 143–70. [Google Scholar] [CrossRef] [Green Version]

- Bianchi, Milo. 2018. Financial literacy and portfolio dynamics. The Journal of Finance 73: 831–59. [Google Scholar] [CrossRef] [Green Version]

- Blanco-Mesa, Fabio, José M. Merigó, and Anna M. Gil-Lafuente. 2017. Fuzzy decision-making: A bibliometric-based review. Journal of Intelligent & Fuzzy Systems 32: 2033–50. [Google Scholar]

- Boatman, Angela, and Brent J. Evans. 2017. How financial literacy, federal aid knowledge, and credit market experience predict loan aversion for education. The ANNALS of the American Academy of Political and Social Science 671: 49–68. [Google Scholar] [CrossRef] [Green Version]

- Boutsouki, Christina. 2019. Impulse behavior in economic crisis: A data driven market segmentation. International Journal of Retail & Distribution Management 47: 974–96. [Google Scholar]

- Brenner, Lukas, and Tobias Meyll. 2020. Robo-advisors: A substitute for human financial advice? Journal of Behavioral and Experimental Finance 25: 100275. [Google Scholar] [CrossRef]

- Brown, Meta, John Grigsby, Wilbert van der Klaauw, Jaya Wen, and Basit Zafar. 2016. Financial education and the debt behavior of the young. The Review of Financial Studies 29: 2490–522. [Google Scholar] [CrossRef] [Green Version]

- Bucher-Koenen, Tabea, and Annamaria Lusardi. 2011. Financial literacy and retirement planning in Germany. Journal of Pension Economics & Finance 10: 565–84. [Google Scholar]

- Calcagno, Riccardo, and Chiara Monticone. 2015. Financial literacy and the demand for financial advice). Journal of Banking & Finance 50: 363–80. [Google Scholar]

- Chapman, Bruce, and Lorraine Dearden. 2017. Conceptual and empirical issues for alternative student loan designs: The significance of loan repayment burdens for the united states. The ANNALS of the American Academy of Political and Social Science 671: 249–68. [Google Scholar] [CrossRef]

- Chen, Chaomei. 2014. The citespace manual. College of Computing and Informatics 1: 1–84. [Google Scholar]

- Chen, Chaomei, Fidelia Ibekwe-SanJuan, and Jianhua Hou. 2010. The structure and dynamics of cocitation clusters: A multiple-perspective cocitation analysis. Journal of the American Society for Information Science and Technology 61: 1386–409. [Google Scholar] [CrossRef] [Green Version]

- Christiansen, Charlotte, Juanna Schröter Joensen, and Jesper Rangvid. 2008. Are economists more likely to hold stocks? Review of Finance 12: 465–96. [Google Scholar] [CrossRef] [Green Version]

- Clark, Robert, Annamaria Lusardi, and Olivia S. Mitchell. 2014. Financial knowledge and 401 (k) investment performance: A case study. Journal of Pension Economics & Finance 16: 324–47. [Google Scholar]

- Cobb-Clark, Deborah A., Sonja C. Kassenboehmer, and Mathias G. Sinning. 2016. Locus of control and savings. Journal of Banking & Finance 73: 113–30. [Google Scholar]

- Cole, Shawn, Anna Paulson, and Gauri Kartini Shastry. 2014. Smart money? the effect of education on financial outcomes. The Review of Financial Studies 27: 2022–51. [Google Scholar] [CrossRef] [Green Version]

- Comerio, Niccolò, and Fernanda Strozzi. 2019. Tourism and its economic impact: A literature review using bibliometric tools. Tourism Economics 25: 109–31. [Google Scholar] [CrossRef]

- Culnan, Mary J. 1987. Mapping the intellectual structure of mis, 1980–1985: A co-citation analysis. MIS Quarterly 11: 341–53. [Google Scholar] [CrossRef]

- Disney, Richard, and John Gathergood. 2013. Financial literacy and consumer credit portfolios. Journal of Banking & Finance 37: 2246–54. [Google Scholar]

- Drexler, Alejandro, Greg Fischer, and Antoinette Schoar. 2014. Keeping it simple: Financial literacy and rules of thumb. American Economic Journal: Applied Economics 6: 1–31. [Google Scholar] [CrossRef] [Green Version]

- Duca, John V., and Anil Kumar. 2014. Financial literacy and mortgage equity withdrawals. Journal of Urban Economics 80: 62–75. [Google Scholar] [CrossRef] [Green Version]

- Feng, Xiangnan, Bin Lu, Xinyuan Song, and Shuang Ma. 2019. Financial literacy and household finances: A bayesian two-part latent variable modeling approach. Journal of Empirical Finance 51: 119–37. [Google Scholar] [CrossRef]

- Fernandes, Daniel, John G. Lynch, and Richard G. Netemeyer. 2014. Financial literacy, financial education, and downstream financial behaviors. Management Science 60: 1861–83. [Google Scholar] [CrossRef]

- Furquim, Fernando, Kristen M. Glasener, Meghan Oster, Brian P. McCall, and Stephen L. DesJardins. 2017. Navigating the financial aid process: Borrowing outcomes among first-generation and non-first-generation students. The ANNALS of the American Academy of Political and Social Science 671: 69–91. [Google Scholar] [CrossRef]

- Gödker, Katrin, and Lasse Mertins. 2018. Csr disclosure and investor behavior: A proposed framework and research agenda. Behavioral Research in Accounting 30: 37–53. [Google Scholar] [CrossRef]

- Goodell, John W., Satish Kumar, Weng Marc Lim, and Debidutta Pattnaik. 2021. Artificial intelligence and machine learning in finance: Identifying foundations, themes, and research clusters from bibliometric analysis. Journal of Behavioral and Experimental Finance 32: 100577. [Google Scholar] [CrossRef]

- Grohmann, Antonia. 2018. Financial literacy and financial behavior: Evidence from the emerging asian middle class. Pacific-Basin Finance Journal 48: 129–43. [Google Scholar] [CrossRef] [Green Version]

- Hair, Joseph F., Jr., William C. Black, Barry J. Babin, Rolph E. Anderson, and Ronald L. Tatham. 2014. Pearson new international edition. In Multivariate Data Analysis, 7th ed. Essex: Pearson Education Limited Harlow. [Google Scholar]

- Hassan, M. Kabir, Muneer M. Alshater, Rashedul Hasan, and Abul Bashar Bhuiyan. 2021. Islamic microfinance: A bibliometric review. Global Finance Journal 49: 100651. [Google Scholar] [CrossRef]

- Hayes, Andrew F. 2018. Partial, conditional, and moderated moderated mediation: Quantification, inference, and interpretation. Communication Monographs 85: 4–40. [Google Scholar] [CrossRef]

- Hsiao, Yu-Jen, and Wei-Che Tsai. 2018. Financial literacy and participation in the derivatives markets. Journal of Banking & Finance 88: 15–29. [Google Scholar]

- Huston, Sandra J. 2010. Measuring financial literacy. Journal of Consumer Affairs 44: 296–316. [Google Scholar] [CrossRef]

- Jiang, Danling, and Sonya S. Lim. 2018. Trust and household debt. Review of Finance 22: 783–812. [Google Scholar] [CrossRef]

- Kaiser, Tim, and Lukas Menkhoff. 2017. Does financial education impact financial literacy and financial behavior, and if so, when? The World Bank Economic Review 31: 611–30. [Google Scholar] [CrossRef]

- Kempson, Elaine, Sharon Collard, and Nick Moore. 2006. Measuring financial capability: An exploratory study for the financial services authority. Consumer Financial Capability: Empowering European Consumers 2006: 39. [Google Scholar]

- Khan, Ashraf, John W. Goodell, M. Kabir Hassan, and Andrea Paltrinieri. 2021. A bibliometric review of finance bibliometric papers. Finance Research Letters 2021: 102520. [Google Scholar] [CrossRef]

- Klapper, Leora, Annamaria Lusardi, and Georgios A. Panos. 2013. Financial literacy and its consequences: Evidence from russia during the financial crisis. Journal of Banking & Finance 37: 3904–23. [Google Scholar]

- Kurowski, ukasz. 2021. Household’s overindebtedness during the COVID-19 crisis: The role of debt and financial literacy. Risks 9: 62. [Google Scholar] [CrossRef]

- Li, Jianjun, Qize Li, and Xu Wei. 2020. Financial literacy, household portfolio choice and investment return. Pacific-Basin Finance Journal 62: 101370. [Google Scholar] [CrossRef]

- Li, Kai, Jason Rollins, and Erjia Yan. 2018. Web of science use in published research and review papers 1997–2017: A selective, dynamic, cross-domain, content-based analysis. Scientometrics 115: 1–20. [Google Scholar] [CrossRef] [Green Version]

- Lim, Thien Sang, Rasid Mail, Mohd Rahimie Abd Karim, Zatul Karamah Ahmad Baharul Ulum, Junainah Jaidi, and Raman Noordin. 2018. A serial mediation model of financial knowledge on the intention to invest: The central role of risk perception and attitude. Journal of Behavioral and Experimental Finance 20: 74–79. [Google Scholar] [CrossRef]

- Lin, Xi, Aaron Bruhn, and Jananie William. 2019. Extending financial literacy to insurance literacy: A survey approach. Accounting & Finance 59: 685–713. [Google Scholar]

- Liu, Weishu. 2019. The data source of this study is Web of Science Core Collection? Not enough. Scientometrics 121: 1815–24. [Google Scholar] [CrossRef]

- Liu, Zhigao, Yimei Yin, Weidong Liu, and Michael Dunford. 2015. Visualizing the intellectual structure and evolution of innovation systems research: A bibliometric analysis. Scientometrics 103: 135–58. [Google Scholar] [CrossRef]

- Lusardi, Annamaria, Olivia S. Mitchell, and Vilsa Curto. 2010. Financial literacy among the young. Journal of Consumer Affairs 44: 358–80. [Google Scholar] [CrossRef]

- Lusardi, Annamaria, and Olivia S. Mitchell. 2011. Financial literacy and retirement planning in the United States. Journal of Pension Economics & Finance 10: 509–25. [Google Scholar]

- Lusardi, Annamaria, and Olivia S. Mitchell. 2014. The economic importance of financial literacy: Theory and evidence. Journal of Economic Literature 52: 5–44. [Google Scholar] [CrossRef] [Green Version]

- Lusardi, Annamaria, and Peter Tufano. 2015. Debt literacy, financial experiences, and overindebtedness. Journal of Pension Economics & Finance 14: 332–68. [Google Scholar]

- Lusardi, Annamaria, Pierre-Carl Michaud, and Olivia S. Mitchell. 2017. Optimal financial knowledge and wealth inequality. Journal of Political Economy 125: 431–77. [Google Scholar] [CrossRef] [Green Version]

- Madureira, Bruno, Tiago Pinto, Filipe Fernandes, and Zita Vale. 2017. Context analysis in energy resource management residential buildings. Paper presented at 2017 IEEE Manchester PowerTech, Manchester, UK, June 18–22; pp. 1–6. [Google Scholar]

- Metawa, Noura, M. Kabir Hassan, Saad Metawa, and M. Faisal Safa. 2019. Impact of behavioral factors on investors’ financial decisions: Case of the egyptian stock market. International Journal of Islamic and Middle Eastern Finance and Management 12: 30–55. [Google Scholar] [CrossRef]

- Mitchell, Olivia S., and Annamaria Lusardi. 2011. Financial literacy around the world: An overview. Journal of Pension Economics and Finance 10: 497–508. [Google Scholar]

- Oehler, Andreas, Matthias Horn, and Florian Wedlich. 2018. Young adults’ subjective and objective risk attitude in financial decision-making: Evidence from the lab and the field. Review of Behavioral Finance 10: 274–94. [Google Scholar] [CrossRef]

- Parise, Gianpaolo, and Kim Peijnenburg. 2019. Non-cognitive abilities and financial distress: Evidence from a representative household panel. The Review of Financial Studies 32: 3884–919. [Google Scholar] [CrossRef]

- Patel, Ritesh, John W. Goodell, Marco Ercole Oriani, Andrea Paltrinieri, and Larisa Yarovaya. 2022. A bibliometric review of financial market integration literature. International Review of Financial Analysis 80: 102035. [Google Scholar] [CrossRef]

- Pham, Mia Hang. 2020. In law we trust: Lawyer ceos and stock liquidity. Journal of Financial Markets 50: 100548. [Google Scholar] [CrossRef]

- Rahman, Mahfuzur, Nurul Azma, Md Masud, Abdul Kaium, and Yusof Ismail. 2020. Determinants of indebtedness: Influence of behavioral and demographic factors. International Journal of Financial Studies 8: 8. [Google Scholar] [CrossRef] [Green Version]

- Rivière-Giordano, Géraldine, Sophie Giordano-Spring, and Charles H. Cho. 2018. Does the level of assurance statement on environmental disclosure affect investor assessment? an experimental study. Sustainability Accounting, Management and Policy Journal 9: 336–60. [Google Scholar] [CrossRef]

- Salem, Razan. 2019. Examining the investment behavior of arab women in the stock market. Journal of Behavioral and Experimental Finance 22: 151–60. [Google Scholar] [CrossRef]

- Sevcík, Karel. 2015. Pisa 2012 results: Students and money: Financial literacy skills for the 21st century (volume vi). Pedagogická Orientace 25: 632. [Google Scholar]

- Shen, Chung-Hua, Shih-Jie Lin, De-Piao Tang, and Yu-Jen Hsiao. 2016. The relationship between financial disputes and financial literacy. Pacific-Basin Finance Journal 36: 46–65. [Google Scholar] [CrossRef]

- Small, Henry. 1973. Co-citation in the scientific literature: A new measure of the relationship between documents. Journal of the American Society for Information Science 24: 265–69. [Google Scholar] [CrossRef]

- Stolper, Oscar. 2018. It takes two to tango: Households’ response to financial advice and the role of financial literacy. Journal of Banking & Finance 92: 295–310. [Google Scholar]

- Supanantaroek, Suthinee, Robert Lensink, and Nina Hansen. 2017. The impact of social and financial education on savings attitudes and behavior among primary school children in Uganda. Evaluation Review 41: 511–41. [Google Scholar] [CrossRef] [PubMed]

- Tchamyou, Vanessa Simen. 2020. Education, lifelong learning, inequality and financial access: Evidence from African countries. Contemporary Social Science 15: 7–25. [Google Scholar] [CrossRef] [Green Version]

- Tullio, Jappelli, and Padula Mario. 2013. Investment in financial literacy and saving decisions. Journal of Banking & Finance 37: 2779–92. [Google Scholar]

- Van Eck, Nees, and Ludo Waltman. 2010. Software survey: Vosviewer, a computer program for bibliometric mapping. Scientometrics 84: 523–38. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Van Rooij, Maarten, Annamaria Lusardi, and Rob Alessie. 2011. Financial literacy and stock market participation. Journal of Financial Economics 101: 449–72. [Google Scholar] [CrossRef] [Green Version]

- Von Gaudecker, Hans-Martin. 2015. How does household portfolio diversification vary with financial literacy and financial advice? The Journal of Finance 70: 489–507. [Google Scholar] [CrossRef]

- Wu, Yen-Chun Jim, and Tienhua Wu. 2017. A decade of entrepreneurship education in the Asia Pacific for future directions in theory and practice. Management Decision 55: 1333–50. [Google Scholar] [CrossRef]

- Xu, Shuo, Junwan Liu, Dongsheng Zhai, Xin An, Zheng Wang, and Hongshen Pang. 2018. Overlapping thematic structures extraction with mixed-membership stochastic blockmodel. Scientometrics 117: 61–84. [Google Scholar] [CrossRef]

Figure 1.

The annual citations between the period 2002–2022 retrieved from WOS.

Figure 2.

The annual publication of papers between the period 2002–2022 retrieved from WOS.

Figure 3.

Top research areas with more than eight published articles on financial literacy retrieved from WOS.

Figure 3.

Top research areas with more than eight published articles on financial literacy retrieved from WOS.

Figure 4.

A summary table of ten clusters according to silhouette value prepared using CiteSpace software.

Figure 4.

A summary table of ten clusters according to silhouette value prepared using CiteSpace software.

Figure 5.

A timeline view of the clusters during 2001–2022 prepared using CiteSpace software.

Figure 6.

A summary table of cluster explorer extracted from the abstracts of the articles prepared using CiteSpace software.

Figure 6.

A summary table of cluster explorer extracted from the abstracts of the articles prepared using CiteSpace software.

Figure 7.

Citation bursts history during the period 2002–2022 prepared using CiteSpace software.

Figure 8.

Keywords co-occurrence overlay visualization map according to year (prepared using VOSviewer software).

Figure 8.

Keywords co-occurrence overlay visualization map according to year (prepared using VOSviewer software).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Table 1.

Top authors, affiliated institutions, and countries publishing on financial literacy prepared using VOSviewer software.

Table 1.

Top authors, affiliated institutions, and countries publishing on financial literacy prepared using VOSviewer software.

| Top Authors | Top Institutions | Top Countries | ||||||

|---|---|---|---|---|---|---|---|---|

| Author | TP | TC | Institution | TP | TC | Country | TP | TC |

| Annamaria Lusardi | 14 | 1833 | University of Pennsylvania | 25 | 1493 | USA | 586 | 14,865 |

| Olivia S. Mitchell | 11 | 870 | George Washington University | 18 | 1478 | England | 193 | 3217 |

| Paul Gerrans | 7 | 59 | Tilburg University | 17 | 504 | Australia | 171 | 1763 |

| Satish Kumar | 7 | 44 | National Bureau of Economic Research | 16 | 808 | Peoples R China | 140 | 1747 |

| Kelmara Mendes Vieira | 5 | 69 | Erasmus University | 15 | 660 | Germany | 103 | 1623 |

| Tobias Meyll | 5 | 46 | World Bank | 13 | 651 | Malaysia | 95 | 423 |

| ACG Potrich | 4 | 69 | Tsinghua University | 12 | 253 | Italy | 88 | 1462 |

| Roy Kouwenberg | 4 | 80 | University Western Australia | 12 | 202 | India | 85 | 407 |

| Mario Padula | 4 | 191 | Harvard University | 11 | 1221 | Canada | 77 | 1278 |

| Andreas Walter | 4 | 29 | University of Oxford | 11 | 292 | Netherlands | 58 | 2158 |

| Jing Jian Xiao | 4 | 204 | Centre for Economic Policy Research | 10 | 77 | France | 50 | 643 |

| Alex Yue Feng Zhu | 4 | 10 | University of California | 9 | 289 | Taiwan | 45 | 513 |

| Elsa Fornero | 4 | 129 | University of Groningen | 8 | 603 | Sweden | 37 | 640 |

| Susan Thorp | 4 | 24 | University of Rhode Island | 5 | 206 | Portugal | 34 | 917 |

| CAB Van der Cruijsen | 4 | 44 | University of Colorado | 5 | 521 | Scotland | 34 | 439 |

Table 2.

Leading journals publishing on financial literacy prepared using VOSviewer software.

| Journal | Publisher | TP | TC |

|---|---|---|---|

| Journal of Pension Economics and Finance | Cambridge University Press | 45 | 1863 |

| Social Indicators Research | Springer International Publishing | 44 | 614 |

| Journal of Behavioral and Experimental Finance | Elsevier | 40 | 250 |

| Journal of Banking and Finance | Elsevier | 37 | 1385 |

| Journal of Risk and Financial Management | MDPI | 24 | 75 |

| Pacific-Basin Finance Journal | Elsevier | 21 | 149 |

| Journal of Behavioral Finance | Taylor and Francis Ltd. | 20 | 200 |

| Accounting and Finance | Wiley-Blackwell | 19 | 157 |

| Review of Financial Studies | Oxford University Press | 16 | 609 |

| Journal of Financial Economics | Elsevier | 15 | 1088 |

| European Journal of Finance | Routledge | 15 | 53 |

| Review of Finance | Oxford University Press | 12 | 215 |

| Management Science | Institute for Operations Research and the Management Sciences | 12 | 1158 |

| Journal of Finance | Wiley-Blackwell | 9 | 495 |

| World Bank Economic Review | Oxford University Press | 9 | 365 |

Table 3.

Top publications based on citation count prepared using VOSviewer software.

| Reference | Article Title | Journal | Times Cited, (WoS) |

|---|---|---|---|

| Fernandes et al. (2014) | Financial Literacy, Financial Education, and Downstream Financial Behaviors | Management Science | 487 |

| Van Rooij et al. (2011) | Financial Literacy and Stock Market Participation | Journal of Financial Economics | 437 |

| Lusardi and Mitchell (2011) | Financial Literacy Around the World: An Overview | Journal of Pension Economics and Finance | 421 |

| Mitchell and Lusardi (2011) | Financial Literacy and Retirement Planning in the United States | Journal of Pension Economics and Finance | 227 |

| Lusardi and Tufano (2015) | Debt Literacy, Financial Experiences, and Over-indebtedness | Journal of Pension Economics and Finance | 214 |

| Tullio and Mario (2013) | Investment in Financial Literacy and Savings Decisions | Journal of Banking and Finance | 161 |

| Cole et al. (2014) | Smart Money? The Effect of Education on Financial Outcome | Review of Financial Studies | 158 |

| Von Gaudecker (2015) | How does Household Portfolio diversification vary with Financial Literacy and Financial Advice? | Journal of Finance | 132 |

| Banks and Oldfield (2007) | Understanding Pensions: Cognitive Function, Numerical Ability, and Retirement Saving | Fiscal Studies | 124 |

| Klapper et al. (2013) | Financial Literacy and Its Consequences: Evidence from Russia during the Financial Crisis | Journal of Banking and Finance | 109 |

| Calcagno and Monticone (2015) | Financial Literacy and the Demand for Financial Advice | Journal of Banking and Finance | 109 |

| Christiansen and Rangvid (2008) | Are Economists more Likely to Hold Stocks? | Review of Finance | 78 |

| Brown et al. (2016) | Financial Education and the Debt Behavior of the Young | Review of Financial Studies | 67 |

| Kaiser and Menkhoff (2017) | Does Financial Education Impact Financial Literacy and Financial Behavior and If Thus, When? | World Bank Economic Review | 56 |

| Cobb-Clark et al. (2016) | Locus of Control and Savings | Journal of Banking and Finance | 54 |

Table 4.

Recent research trends and hottest topics in financial literacy during 2019 and 2021.

| S. No. | Reference | Objective |

|---|---|---|

| 1. | Feng et al. (2019) | Investigate the impacts of financial literacy on both sides of the household balance sheet, namely, household debt and assets, using a national sample from the China Household Finance Survey. |

| 2. | Lin et al. (2019) | Investigate factors that may influence individuals’ insurance decision-making. |

| 3. | Stolper (2018) | Homophily has a strong positive impact on the chance of adopting financial advice. |

| 4. | Baker et al. (2019) | Examine how financial literacy and demographic variables are related to behavioral biases. |

| 5. | Boutsouki (2019) | Apply cluster analysis to identify homogeneous subgroups among impulse buyers based on their demographic characteristics and their preference for atmospheric elements. |

| 6. | Metawa et al. (2019) | Investigate the relationship between investors demographic characteristics and their investment decisions through behavioral factors as mediator variables in the Egyptian stock market. |

| 7. | Salem (2019) | Investigate the investment behavior of Arab women on risk tolerance, investment confidence, investment literacy levels, and herding behavior. |

| 8. | Parise and Peijnenburg (2019) | Provides evidence of how non-cognitive abilities affect financial distress. |

| 9. | Li et al. (2020) | Investigates the impact of financial literacy on Chinese households’ portfolio decisions and financial market investment performance. |

| 10. | Rahman et al. (2020) | Design a particular determinants model to investigate the impact of behavioral and demographic variables on indebtedness. |

| 11. | Pham (2020) | Highlights the importance of CEO characteristics in enhancing financial market quality. |

| 12. | Brenner and Meyll (2020) | Investigate whether automated financial advisers (Robo-advisors) reduce demand for human financial advice from financial service providers. |

| 13. | Ali et al. (2020) | Uncover the determinants of Islamic financial inclusion in Indonesia. |

| 14. | Tchamyou (2020) | The impact of financial access on modulating the effect of education and lifelong learning on inequality is examined in 48 African countries from 1996 to 2014. |

| 15. | Asongu and Kuada (2020) | Provides a context for understanding the importance of building knowledge economies in Africa and summarises the main contributions to the themed issue. |

| 16. | Kurowski (2021) | Examine if households with greater financial and debt literacy have better budget management skills, reducing the risk of individuals failing to repay their loans in the crisis. |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Ansari, Y.; Albarrak, M.S.; Sherfudeen, N.; Aman, A. A Study of Financial Literacy of Investors—A Bibliometric Analysis. Int. J. Financial Stud. 2022, 10, 36. https://doi.org/10.3390/ijfs10020036

AMA Style

Ansari Y, Albarrak MS, Sherfudeen N, Aman A. A Study of Financial Literacy of Investors—A Bibliometric Analysis. International Journal of Financial Studies. 2022; 10(2):36. https://doi.org/10.3390/ijfs10020036

Chicago/Turabian StyleAnsari, Yasmeen, Mansour Saleh Albarrak, Noorjahan Sherfudeen, and Arfia Aman. 2022. "A Study of Financial Literacy of Investors—A Bibliometric Analysis" International Journal of Financial Studies 10, no. 2: 36. https://doi.org/10.3390/ijfs10020036

Note that from the first issue of 2016, this journal uses article numbers instead of page numbers. See further details here.