Examining the Factors Affecting the Adoption of Blockchain Technology in the Banking Sector: An Extended UTAUT Model

Institute of Management Technology, Nagpur 440013, India

Int. J. Financial Stud. 2022, 10(4), 90; https://doi.org/10.3390/ijfs10040090

Submission received: 17 August 2022

/

Revised: 23 September 2022

/

Accepted: 26 September 2022

/

Published: 30 September 2022

Abstract

:Technology innovation has dramatically transformed banks over time. Digital innovation in the banking sector began with the introduction of money to replace barter systems, and then gradually replaced wax seals with digital signatures. One such disruptive innovation that is transforming the banking sector around the world is blockchain technology (BCT). The banking sector in India has also started adopting blockchain technology in various financial transactions. However, they are encountering some difficulties in adapting to and implementing this new technology. The successful and speedy adoption of blockchain in banking largely depends on the users’ intention to use the services. Therefore, this study extended “the unified theory of acceptance and use of technology” (UTAUT) to understand the significant predictors of the bankers’ intention to use blockchain technology. The data was collected from leading banking institutions and FinTech firms in the country to empirically test and validate the extended model. The results found that facilitating conditions, performance expectancy, and initial trust, are the significant antecedents to predicting the bankers’ intention to use blockchain in banking transactions. The study also established the significant mediating role of initial trust in predicting usage intention to use blockchain. This study’s results would help government authorities, decision-makers, and technocrats to improve banking instructions for the speedy and smooth adoption of blockchain technology. The study suggested an extended UTAUT model that incorporates contextual factors based on the scope and usage of blockchain in Indian banking activities. The study helped to identify the key factors influencing blockchain adoption among Indian bankers. The proposed model and the findings make more sense in promoting the adoption of blockchain in the Indian banking sector.

1. Introduction

Banks started their journey toward information technology with the introduction of standalone PCs, followed by the computer network, and the adoption of core banking. The main objective behind technology adoption is to enable banking possible through ‘anywhere-anytime banking’. Furthermore, IT-enabled services such as e-banking, electronic funds transfer, interconnectivity among bank branches, and ATM (Automatic Teller Machine) implementation have significantly altered the banking working system. On the other hand, there is remarkable progress in the development of innovative IT and communication technologies. Innovation like blockchain technology, artificial intelligence technologies, and process automation, etc., has the capability of changing the banking structure and working principles drastically (Ahmed et al. 2022b; Cucari et al. 2022; Gupta and Gupta 2018; Karim et al. 2022; Kumari and Devi 2022c; Patki and Sople 2020). Banks are now eagerly adapting to the technological changes, particularly blockchain technology, to be a part of a global force of technology disruption. Blockchain technology is now becoming a major factor in the fourth industrial revolution. Blockchain technology appears to be an innovation that promises a major change in banking services.

1.1. Blockchain and Banking

The major activities of banks are to conduct asset transformation, store liquidity, and utilize economies of scale to provide banking services (Bunea et al. 2016). Banks use a centralized intermediary to facilitate the storage of assets for the use and sources of funding with different mechanisms for stakeholders (MacDonald et al. 2016). Therefore, all banking activities are operated as a set of centralized ledgers of transactions for payments, storage, and services revolving around the stakeholders’ assets (Frame et al. 2018). The banking system can transition from centralized to distributed control with the use of blockchain technology (Patel et al. 2022). Blockchain technology is centered on having a decentralized ledger that is open to all users and easily accessible, allowing for the establishment of trust in unsafe environments without the need for a middleman. The ledger includes an immutable log of all previous transactions, as well as the shared and agreed-upon state of the blockchain. The rise of blockchain technology coincided with the banking and financial industry’s transition to mobile payments, branchless banking, and digital-value exchange, portending a global rupture of financial systems. Several studies (Frame et al. 2018; Zaina Kawasmi et al. 2020) have observed that the merging of traditional financial systems with blockchain-enabled systems will help both banked and unbanked consumers around the world get better services. Blockchain technology can help banks and financial institutions with Bitcoin trading, bond transactions, currency swaps, check issuance, improved KYC, improved settlement, loan granting, remittances, smart contracts, trade finance, and other activities. Additionally, blockchain can be used in conjunction with other technologies, such as identity management, encryption, and business rules, to adapt technology to the problems at hand (Osmani et al. 2020). Blockchain concepts and applications, as well as various frameworks, are being debated in research communities. Blockchains are now being used in a wide range of banking applications, including financial asset settlement, business-related services, economic transactions, and market forecasting (Haferkorn and Quintana Diaz 2014). Blockchain is expected to be essential for long-term, worldwide economic growth in the future, which will benefit society and consumers in general (Nguyen 2016). Studies have shown that digital payments, settlement, derivatives, securities, commercial banking processes, processes for loan management, auditing, and digital currencies, etc., can make the financial markets much more efficient and effective (Cucari et al. 2022; Gupta and Gupta 2018; Karim et al. 2022; Kumari and Devi 2022b; Osmani et al. 2020; Patki and Sople 2020).

The government of India’s Ministry of Electronics and Information Technology (MeitY) has designated blockchain technology as one of the key research areas with potential applications in a variety of fields, including governance, banking and finance, cyber security, and other sectors. Blockchain technology is being used by many Indian banks, including the State Bank of India, ICICI Bank, Yes Bank, Kotak Mahindra Bank, and Axis Bank, in a variety of banking and financial services, such as vendor financing and financing foreign trade. Blockchain transactions are being used by many banks in India to digitize loan sanctions, cross-border remittances, asset registries, and vendor financing. In 2017, the State Bank of India (SBI) established a financial blockchain consortium with 10 commercial banks, making it the first Indian bank to do so. The consortium members communicate know your customer (KYC), anti-money laundering (AML), and combating the financing of terrorism (CTF) information among themselves using blockchain technology. However, blockchain adoption in Indian banking and financial transactions is still in its early stages. The wide adaptation of blockchain technology in Indian banking and financial services depends on the bankers’ intention to use blockchain in their job profile. Using the technology acceptance model, the main goal of the study is to find out if bankers plan to use blockchain in banking services.

1.2. Technology Adaption Model

Technology creation must coexist with user acceptability for the rapid development of society (Taherdoost 2018). The rate of technology adoption aids decision-makers in advancing technology for the benefit of society. As a result, researchers are researching whether or not people adopt new technology, as well as the causes and effects of that. These study findings can assist various stakeholders in advancing technology adoption by guiding their actions (Taherdoost 2017, 2018, 2022). In parallel, various models and frameworks have been created to look at the factors that influence technology adoption in various fields. Acceptance depends on many factors. Such as the users’ thinking processes, trust, beliefs, attitudes, confidence levels, and support systems (Jevsikova et al. 2021). A proper technology acceptance model is needed to find out if bankers want to use blockchain systems for banking transactions. This will help explain the effects and importance of these different factors (Gupta et al. 2022).

In the past, various studies have utilized different technology acceptance models such as the Theory of Reasoned Action (TRA) (Fishbein and Ajzen 1977), the Technology Acceptance Model (TAM) (Davis 1987), the Theory of Planned Behavior (TPB) (Ajzen 1985), and the Unified Theory of Acceptance and Use of Technology (UTAUT) (Venkatesh et al. 2003). These models give a theoretical foundation for forecasting an individual’s acceptance and use of technology, as well as explanations for technology acceptance and usage based on various technological qualities and contextual circumstances. All these models have their advantages and disadvantages, but UTAUT has proven to be highly effective for measuring technology acceptance in different domains (Chao 2019; Jevsikova et al. 2021; Venkatesh et al. 2003; Wijaya et al. 2022). Users of digital technologies have frequently been forced to accept and use a particular technology almost immediately in order to adjust to the new reality. The UTAUT model is one of the most widely and frequently used theories to explain how people use and adopt technologies in organizational and individual settings (Chao 2019; Venkatesh 2022). UTAUT has served as a primary model for accepting various technologies in both organizational and non-organizational settings (Neirotti et al. 2018; Tamilmani et al. 2019). So, the primary goal of this study was to use the UTAUT to learn more about the important factors that predict whether or not a bank plans to use blockchain technology. Accordingly, the main objectives of this study were: (1) to develop an extended UTAUT model incorporating various contextual constructs to predict usage intention towards blockchain technologies in banking activities; (2) to investigate how significantly the essential factors (performance expectancy, facilitating condition, and initial trust) influence behavioral intention to use blockchain technology in the banking system; (3) to examine whether government regulations and perceived risk moderate the effects of performance expectancy, facilitating condition, and trust on behavioral intention to blockchain technology; and (4) to assess and validate the proposed model empirically.

The remainder of the paper is structured as follows: Section 2 examines previous research in the field. Section 3 presents the proposed theoretical framework. Section 4 explains the methodologies used in this study. The result and analysis section discusses the study findings (i.e., Section 5). Section 6 is devoted to the study’s discussion and implications. Section 7 discusses the limitations and future scope of the study. The study concludes with a conclusion in Section 8.

2. Literature Review

Blockchain will have a significant impact on the banking and financial sectors in the future. Blockchain provides a secure banking system, which reduces time, effort, and cost in banking services. These blockchain-related technologies help to evolve a cashless society. The success of blockchain adoption in banking systems depends on bank employees’ and bank management’s acceptance of using these systems. Acceptance depends on many factors, such as the employees’ thinking processes, trust, beliefs, attitudes, confidence levels, and support systems (Jevsikova et al. 2021). Since the early 1980s, various information system (IS) adoption theories have been created to understand and forecast technology uptake. This section will discuss the studies related to blockchain adoption in the financial and banking sectors. Although there are not many studies conducted to predict the intention of blockchain technology in the banking system, Table 1 summarizes important studies related to various modified and integrated IS models for blockchain adoption in the banking system.

As shown in Table 1, many IS models have been used successfully to find the antecedents of use intention of blockchain technology in financial intuitions and banks across the globe. The TPB adoption model was used by Chang et al. (2020) to examine the adoption of BCT in the financial sector. They identified knowledge-hiding as the most critical factor in the adoption of blockchain technology in financial services. Kawasmi et al. (2020) used a modified TAM to study the acceptance and adoption of the blockchain in the global banking industry. Kawasmi and colleagues studied blockchain adoption in three ways, i.e., supporting, hindering, and circumstantial. They also reported the lack of regulation and the need for the revision of current legislation and regulations. Heidari et al. (2019) integrated the TOE, DOI, and NIP models, to study blockchain adoption in the Iranian financial market. They observed that the blockchain acceptance readiness levels were one of the critical factors for blockchain adoption. Furthermore, Saheb and Mamaghani (2021) used a modified TOE model to study blockchain adoption in banking. They identified the most critical barriers, i.e., thelack of understanding by top managers, marketing noise, and finally compliance and regulatory requirements, for blockchain adoption in the banking sector. Khalil et al. (2021) also studied the significant factors in the adoption of the financial sector by using a moderated mediated model. They found that digital business strategy, business process innovation, and financial performance, are the three important factors for blockchain adoption. Kumari and Devi (2022a) used a decomposed theory of planned behavior (DTPB) model to investigate the factors responsible for the adoption of blockchain technology in investment banking in India. They found that perceived usefulness is an important factor for blockchain adoption in India.

However, the UTAUT framework is the latest and most widely used information system (IS) model to predict the intended and actual use of technology (Venkatesh et al. 2003). Yusof et al. (2018) studied the adoption of blockchain technology in the banking sector using the basic UTAUT model. They found effort expectancy is one of the predictors of blockchain acceptance in the banking sector in Malaysia. Chang et al. (2020) studied the adoption of blockchain in Malaysian Islamic banking using the basic UTAUT model. He found that making things easier is the most important factor in getting Islamic banks to use blockchain. Nazim et al. (2021) integrated basic UTAUT and TOE theory to determine the factors of blockchain technology in banking. They observed that effort expectancy, social influence, and facilitation, are the most important factors for adopting blockchain in the Malaysian baking system. Kumari and Devi (2022b) extended the UTAUT by adding financial literacy and perceived risk factors to study the users’ intention to use blockchain technology in digital banking services. Later, the UTAUT model has been changed many times by adding more contextual and attitude constructs (Ahmed et al. 2022a; Tamilmani et al. 2021; Venkatesh et al. 2012, 2016; Williams et al. 2015) to make it more generalizable and useful.

As discussed above, it is observed that over the past few years, there has been a lot of research on technology adaption in the banking sector. Most of the studies used different technology adoption models (TPB, TAM, DTPB, TOE, and UTAUT) to assess the bankers’ intention to use blockchain. At the same time, the UTAUT model was found to be the most reliable technology adoption model (Ahmed et al. 2022a; Tamilmani et al. 2021; Venkatesh et al. 2016; Williams et al. 2015). However, most of the previous studies used the basic UTAUT model to investigate the bankers’ intention to use blockchain in the banking system. Furthermore, most of the studies are conducted in western countries, and there is still a research gap in predicting blockchain adoption in the banking sector in the Indian context. This research gap could affect the advancement and use of blockchain technology in the banking and financial sectors in India. Because of this, the paper proposes an extended UTAUT model by incorporating different contextual variables to predict the intention of Indian bankers to use blockchain technology. This study will add perspective to evaluating blockchain adoption from a practitioner’s perspective, as prior studies in Indian banking and financial institutions lacked the empirical evidence of determinants of usage intention. The study would help the decision makers involved in the Indian banking sector to enhance the blockchain adoption in banking.

3. Theoretical Ground

Based on the objectives of the study, the theoretical basis of the proposed research framework was adopted from the UTAUT model. Effort expectancy, performance expectancy, social influence, and facilitating conditions, are the four basic predictors of behavioral intention in the original UTAUT model. Many researchers have recently extended the base UTAUT model by adding many new constructs based on the different applications (Han and Conti 2020; Jena 2022). Dwivedi et al. (2021) validated the usage of appropriate constructs in the different versions of the UTAUT model using a meta-analytic evaluation approach. They observe that performance expectancy and facilitating conditions have a substantial direct impact on behavioral intention to use technology. They also saw that the most important UTAUT extensions are trust, personal innovativeness, perceived risk, attitude, and self-efficacy.

Recently, Tamilmani et al. (2021) systematically reviewed the extension of UTAUT models and explained their theory base. They suggested the requirement of a simplified UTAUT prototype that can facilitate researchers making the necessary addition of new constructs and omission of irrelevant constructs based on the context rather than having the obligation to replicate all the constructs in the underpinning model/theory. While studying existing/experienced/specialist users of technology in various developed countries, they discovered that some variables, such as EE, are prone to generating non-significant results, others have a negative impact on others, and some predictors cannot coexist in a research model; for example, EE has been shown to reduce FC’s predictive abilities (Venkatesh et al. 2016). They also had an opinion that researchers should include or exclude the basic and extended UTAUT model constructs based on the study environment and scope. Finally, they arrived at a multi-level framework to facilitate the researchers’ extension of the UTAUT model in future research. The suggested template grouped the variables into four classes, i.e., antecedents, outcomes, mediators, and mediating variables. For this research, PE and FC are taken as antecedents to usage intention in the proposed model (Figure 1).

Further, trust is taken as a mediator in the proposed model. On the other hand, many studies have shown the moderating role of different demographic variables in different situations (e.g., gender, age, and experience) (Venkatesh et al. 2003, 2012). Therefore, instead of these demographic factors, the important contextual moderators, e.g., initial trust and perceived risk, were included in the proposed model.

3.1. Hypothesis Development

Like other studies (Ahmed et al. 2022a; Almisad and Alsalim 2020; Dwivedi et al. 2019; Jevsikova et al. 2021; Raza et al. 2021), this study left out some constructs from the original or extended UTAUT models that were not important or were used extensively in the past. Some contextual constructs, which are essential for explaining the adoption and use of blockchain technology, are added to the proposed framework. Therefore, to study the acceptance of blockchain technology in the banking system, the details of each construct and their relationships are discussed below.

- Usage Intention (UI)

Venkatesh et al. (2003) defined usage intention as “a person’s inclination to engage in a specific behavior and has been found as a sign of actual behavior among users of technology”. Blockchain is a relatively new technology and its adoption behavior has not been explored much in the literature.

- Initial Trust (ITR)

Kim and Prabhakar (2004) defined initial trust as the “willingness of a person to take risks to fulfill a need without prior experience or credible, meaningful information”. In other words, initial trust is formed based on the users’ convenience, flexibility, and perceived benefits of the technology, to their activities (Koufaris and Hampton-Sosa 2004). Furthermore, for new users or less technology-experienced users, initial trust plays an important role in the adoption of new technology like blockchain technology (Franque et al. 2022; Kim and Prabhakar 2004; Oliveira et al. 2014). Initial trust is influenced by the user’s personality, environmental facilitating conditions, performance expectancies of the user, and social influence (Kim and Prabhakar 2004; Oliveira et al. 2017). Trust is a very important factor when using technology, especially in the banking system. After users initially use a system, their further usage will depend on trust-building. A plethora of recent empirical studies has established that initial trust is the most dominant parameter to improve the acceptance of technology in a different context (Kopp et al. 2022; Manchon et al. 2022; Xie et al. 2022). On the contrary, Aljaafreh (2021) in their study revealed that trust has an insignificant or less relevant issue in predicting usage intention. Blockchain is a relatively new technology in banking and financial services. Bankers who lack experience face concerns about risk and lack confidence in using the technology. As the role of initial trust is not conclusive in predicting technology acceptance and blockchain is a new technology, the following hypothesis is posited for this study:

H1.

The bankers’ initial trust in blockchain technology significantly influences the usage intention.

- Facilitating Conditions (FC)

Venkatesh et al. (2012) defined FC as “the user belief that institutional support and infrastructure are available to assist in the use of targeted technology”. From the perspective of the blockchain environment in the bank, facilitating conditions emphasize the availability of technical structure to accept and use the technology (Lai 2020; Raza et al. 2021; Yang et al. 2022). FC is generally influenced by the users’ adequate level of technical, organizational, infrastructural, and human support to use technology. FC enhances the functionality of the technology. Further, FC helps to enhance the users’ initial trust in technology use (Hmoud and Várallyai 2020). Therefore, the following hypotheses are suggested:

H2.

FC positively influences the bankers’ usage intention to use blockchain technology.

H3.

FC significantly influences the bankers’ initial trust to use blockchain technology.

- Performance Expectancy (PE)

Performance expectancy is defined as how individuals perceive that technology will help them gain maximum benefit from their work (Venkatesh et al. 2016). Performance expectancy has been proven to significantly affect behavioral intention (Ayaz and Yanartaş 2020; Nazim et al. 2021). Several studies have also found that PE has a significant impact on trust in technology (Akhtar et al. 2019). Therefore, it is expected that performance expectancy will positively influence the usage intention and initial trust to adopt blockchain technology in this study. Hence, the following hypotheses are proposed:

H4.

PE positively influences the bankers’ usage intention to use blockchain technology.

H5.

PE significantly influences the bankers’ initial trust to use blockchain technology.

3.1.1. Moderating Variables

- Perceived Risk (PR)

When using advanced technology like blockchain in banking transactions, bankers often worry about perceived security risks, such as privacy issues, system errors, losing passwords, incompatibility between operating systems and security software, and low system quality. These security risk factors have a significant impact on the intention to use BCT in banking. Various studies have examined perceived security risk as an external factor influencing the UTAUT model’s variables (Chao 2019; Martins et al. 2014; Thusi and Maduku 2020). They also argued that perceived risk considerably hinders usage intention. Chao (2019) found perceived risk as a significant moderating factor in the extended UTAUT model. Thus, the present study extended the UTAUT model by adding perceived risk as a moderating variable in predicting the intention to use blockchain in banking activities.

H6.

The relationship between performance expectancy and usage intention is moderated by perceived risk.

H7.

Perceived risk moderates the relationship between facilitating conditions and usage intention.

H8.

The perceived risk moderates the relationship between initial trust and usage intention.

- Government Regulation (GR)

Government regulation is concerned with laws that are intended to control people’s behavior. Governments should draught laws to govern blockchain technologies in order to facilitate collaborative peer-to-peer communication among stakeholders, rather than subject them to legal constraints (Tapscott and Tapscott 2016). Proper legislation should be drafted or amended to facilitate the widespread adoption of blockchain technology (Kawasmi et al. 2020). Harwood-Jones (2016) suggested six regulatory/legal challenges to overcome before blockchain technology “e.g., legal nature of blockchain and distributed ledger; recognition of blockchain as immutable, tamper-proof sources of truth; right to be forgotten; legal validity of documents stored in the blockchain; the validity of financial instruments; and using smart contracts”. The government of India is now framing new IT laws and regulations to facilitate the easy adoption of blockchain technology in different sectors, including banking and financial services. No study so far has tested government regulation as a variable to predict blockchain adoption using the UTAUT framework. So, the following hypotheses are made to identify how these rules and regulations are affecting bankers’ plans to use blockchain technology:

H9.

Government regulations moderate the relationship between performance expectancy and usage intention.

H10.

Government regulations moderate the relationship between facilitating conditions and usage intention.

H11.

Government regulations moderate the relationship between initial trust and usage intention.

Further, taking the combined moderating effect of GR and PR on the proposed relationship (Figure 1), the following hypotheses are proposed:

H12.

The impact of performance expectancy on usage intention is moderated by perceived risk and government regulation.

H13.

Perceived risk and government regulation moderate the impact of facilitating conditions on usage intention.

H14.

The combination of perceived risk and government regulation moderates the effect of initial trust on usage intention.

3.1.2. Mediating Variable

Several studies have discovered that trust plays an important role as a mediator between usage intention and its predictors (Burda and Teuteberg 2014; Casey and Wilson-Evered 2012; Chang and Chen 2008; Domingo and Garganté 2016; Ghazizadeh et al. 2012; Giovannini et al. 2015; Hew and Kadir 2016). Burda and Teuteberg (2014) investigated the mediating role of trust between ease of use and the intention to use cloud storage. Their findings established the mediating role of trust. Masrek et al. (2014) developed a conceptual model to investigate the adoption of mobile banking in Malaysia. They found the significant mediating role of initial trust in predicting the intention to use mobile banking. Ghazizadeh et al. (2012) used trust as a mediator to predict the drivers’ intention to use technology-enabled monitoring and feedback systems. The findings showed that trust fully mediates the effect of perceived ease of use on UI. Hew and Kadir (2016) incorporated ITR as a mediator between perceived expectancy and usage intention. The findings showed that trust partially mediates the relationship between perceived expectancy and usage intention. Similarly, Chang and Chen (2008) have proved the significant mediating role of trust in the intention to purchase from an online store. Giovannini et al. (2015) established the partial mediating role of trust in predicting the intention to use m-commerce. On the contrary, Casey and Wilson-Evered (2012) found that trust in technological innovation did not produce significant effects on the intention to use technology. Chaouali et al. (2016) found trust as a strong mediator for using internet banking services. In the field of blockchain adoption, it can be defined as the trust of bankers to accept a disruptive technology. Therefore, in this study, trust in blockchain technology was introduced as a mediating variable to predict intention to use the blockchain. Thus, the following hypotheses are proposed:

H15.

Initial trust in blockchain technology mediates the relationship between performance expectancy and usage intention.

H16.

The relationship between facilitating conditions and usage intention is significantly mediated by the initial trust in blockchain technology.

4. Research Methodology

4.1. Study Instrument

A questionnaire (in Supplementary Information) was designed to collect data for this study. The questionnaire was divided into two sections. In the first section, 32 items were used to measure the seven constructs presented in the proposed research model (Figure 2). The scales for PE, FC, ITR, UI, GR, and PR, were developed after a thorough review of literature related to different IS models. The scale for FC, PE, and UI, was adopted by Venkatesh et al. (2012). The initial trust scales were adapted from Kim and Garrison (2009). The government regulation was measured using four items adapted from Tornatzky et al. (1990). The perceived risk scale was adapted from von Solms and von Solms (2018). All the scales were measured on a 5-point Likert scale. The second part of the instrument was used to gather demographic information about the participant.

A pilot study was conducted before the actual study to improve the readability and validity of the scale. The main objective of the pilot study was to check the accuracy and precision of the items (Hair et al. 2010). In the pilot study, 30 valid responses were received from bankers from Nagpur, India. The Cronbach’s alpha scores of all the variables were between 0.71 and 0.83. The results showed that Cronbach’s alpha values for all variables were higher than 0.7. This showed that all measurement items were reliable (Hair et al. 2010).

4.2. Participants

A cross-sectional survey based on a stratified sampling procedure was used for data collection. The stratification sampling method generally increases the precision of statistical estimates (Creswell and Creswell 2017). The sample size of this study was decided based on the requirements of Structural Equation Modeling (SEM). According to Boomsma and Hoogland (2001), a minimum sample size of 200 is required to minimize the bias in the results in SEM. Schreiber et al. (2006) recommended a ratio of 10 observations per indicator for a good sample size for SEM. In addition, Wolf et al. (2013) recommends that the minimum sample size be at least 10 times the number of free parameters in SEM. Considering the above recommendations, it was assumed that a minimum sample size of at least 200 would be sufficient to reduce bias in the study results. Aiming to receive the required responses, more than 600 questionnaires were distributed among employees of leading banking institutions and FinTech firms all over India, between 15 April 2021 and 15 February 2022. All the participating bankers were middle-to senior-level employees. All participants were informed about the research and assured that their responses would be anonymous and used only for research purposes. A total of 428 responses were collected and, after preliminary screening, only 381 responses were found usable for further analysis. The demographic data revealed that the mean age of the participants was 36.8 years, and approximately two-thirds of the participants were male (74.3%). Furthermore, 56% (approx.) of the participants had more than 12 years of experience in banking. In addition, 38.6% of the sample were from public banks.

5. Results and Analysis

The model was validated using partial least squares (PLS) regression-based structural equation modeling (SEM) techniques in R. PLS regression is very useful for data analysis during the early stages of theory building and validation (Tsang et al. 2021). The PLS model examines and evaluates the measurement model and structural model. In addition to utilizing several data-screening processes for missing values and outlier detection, a common-method variance test and a nonresponse bias test were used to ensure the data quality.

- The Nonresponse Bias Test

Nonresponse bias is a significant problem for data acquired using the ego instrument. In this work, potential nonresponse biases were evaluated using an extrapolation technique suggested by Armstrong and Overton (1977). This method assessed and analyzed the responses of both early and late respondents to determine whether their mean values differed. A t-test was performed to compare the mean values of the first 100 participants to those of the last 100. According to the test results, there was no statistically significant difference between the sample means (t = 11.4, p = 0.03). Consequently, there was no response bias in the data.

- The Common-Method Variance Test

In a cross-sectional study, common-method variance poses a formidable challenge (Hair et al. 2017). Consequently, the solution developed by Podsakoff et al. (2003) was utilized to solve the possible common method variance issue in this investigation. Varimax rotation was employed to treat all 32 components as a single factor. Five iterations later, the one-factor test converged to six factors (FC, PE, ITR, GR, PR, and UI). The test explained 39% of the total variance, which is significantly below the needed 50% threshold (Harman 1976). These results demonstrate that the data does not have a problem with common-method variance.

5.1. Evaluation of Measurement Models

Internal reliability (IR), convergent validity (CV), and discriminant validity (DV), were examined to evaluate the measurement model. The Cronbach’s alpha and composite reliability (CR) values were used to assess internal reliability. The average variance extracted (AVE) was used to assess the CV and DV of the construct (Bagozzi and Yi 2012; Fornell and Larcker 1981; Hair et al. 2010). Table 2 displays the item loading range, Cronbach’s alpha, AVE, and CR results. The estimated significant construct loadings, which are greater than the suggested levels, varied from 0.69 to 0.87. (Hair et al. 2010). The IR of a construct describes how well a construct is assessed using its items and assessed using Cronbach’s alpha and CR. The Cronbach’s alpha values ranged from 0.71 (PE) to 0.77 (GR), and CR values ranged from 0.77 (PE) to 0.82 (GR). For both measures, all constructs exceeded the recommended cutoff of 0.7 (Fornell and Larcker 1981; Hair et al. 2010), thereby suggesting moderate to high internal reliability. The AVE ranged from 0.62 (PE) to 0.68 (GR) and was greater than 0.5 for each construct (Fornell and Larcker 1981), thereby establishing the construct validity.

To evaluate the DV, two criteria (Fornell–Larcker criteria and the Heterotrait-Monotrait (HTMT) criteria) were used. Using the Fornell–Larcker criteria, the results show that the square root of the AVE of each latent construct (presented diagonally with strong bold text) exceeded the inter-construct correlations for each construct, as shown in Table 3, demonstrating an appropriate degree of DV. Additionally, according to the HTMT criterion, all HTMT values (upper diagonal values in Table 3) are below the cutoff of 0.90 (Hair et al. 2017), confirming the discriminant validity of the constructs.

5.2. Model Assessment

To rate the overall effectiveness of the suggested model, the goodness of fit (GoF), path coefficient, and coefficient of determination (R2) were utilized. The geometric mean of the average commonality and average R2 value was used to calculate the GoF (GoF = ) as suggested by Alolah et al. (2014). The recommended threshold value of GoF is 0.36. The GoF value for the proposed model was 0.66, which is more than the threshold value. As a result, the model’s overall quality was satisfactory. The path coefficient and t-statistics were also used to assess the associations between the dependent and independent variables. Finally, the coefficients were found using the bootstrapping resampling method. The number of iterations was set at 1000.

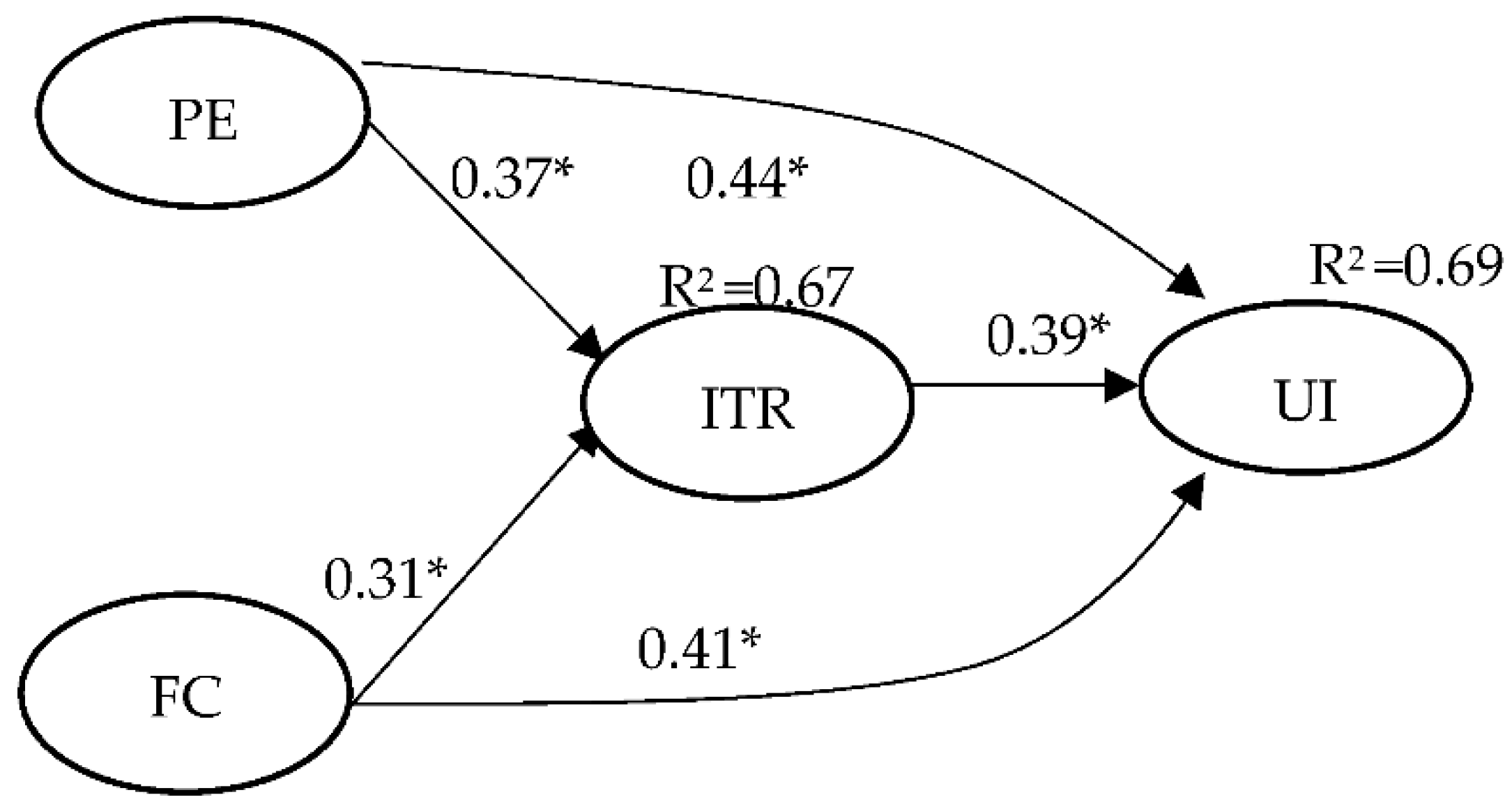

The hypotheses concerning the direct relationship between PE, FC, ITR, and UI, are shown in Figure 2. Considering ITR as a dependent variable, the direct effect of FC and PE are significant, with path coefficients of 0.31 and 0.37, respectively. This demonstrates that FC and PE positively influence bankers’ initial trust using blockchain technology for banking activities. Hence, hypotheses H3 and H5 are supported. Further, ITR (0.39) positively influenced the usage intention to use blockchain technology in banking activities. Therefore, hypothesis H1 is found satisfactory. Further FC (0.41) positively influences the intention to use the blockchain in banking services. Thus, hypothesis H2 is supported. Similarly, PE (0.44) significantly predicts the usage intention to use blockchain. Hence, hypothesis H4 is supported.

So far, from the above findings, it is observed that the proposed structural model has a significant explanatory power (i.e., R2 value is 0.69). However, researchers have ascertained that only R2 is not sufficient to assess the stinginess of a structural model in the PLS-SEM approach (Hair et al. 2016). So, the predictive power of the proposed model was estimated using the Stone-Geisser’s Q2 test (Stone 1974). The Q2 value was calculated by using the Blindfolding procedure. Q2 ≠ 0 indicates a significant predictive relevance for its endogenous variables (Hair et al. 2017). The Q2 value of the proposed model was found at 0.37, which indicates a strong predictive relevance for the bankers’ blockchain technology use in the banking and finance sector.

5.2.1. Mediation Effect

The bootstrapping method was used to assess the mediation effect in the theoretical model. The bootstrapping method is independent of any assumption about the sampling distribution (Hair et al. 2017). The variance accounted for (VAF) was calculated as follows: VAF = Indirect effect/Total effect. According to Hair et al. (2016): “If the VAF value is less than 0.2, there is no mediation; if the value is greater than or equal to 0.2 and less than or equal to 0.8, then there is partial mediation; and if the value is greater than 0.8, there is full mediation”. Mediation results are presented in Table 4. The VAF value for PE→ITR→UI is 0.92, indicating that trust fully mediated the relationship between performance expectancy and usage intention. For the mediation effect of trust on the relationship between facilitating condition and usage intention, the VAF value is 0.93, showing full mediation. Thus, H15 and H16 are supported.

5.2.2. Moderation Effect

The interactions and moderation effects of all dimensions included in the model analysis are presented in Table 5. The results include structural path estimates and explained variations for the dependent variable (usage intention).

It was also discovered that perceived risk has a negative effect on the intention to use blockchain in banking services (β= −0.17, p < 0.05). This implies that the users’ usage intention to use blockchain increases with a decrease in perceived risk. Government regulations, on the other hand, have a positive influence on blockchain usage in the banking sector (β = 0.33, p < 0.01).

The trust was found to significantly (positively) affect usage intention. The relationship between trust and usage intention is significantly moderated by government regulation (β = 0.37, p < 0.05). Hence, hypothesis H11 is supported. Further, the perceived risk did not moderate the relationship between trust and usage intention. Therefore, H8 is not supported. However, the combined moderating effect of PR and GR on ITR→UI is also found to be insignificant. Hence, H14 is not supported.

Government regulation significantly moderates the relationship between PE and usage intention (β = 0.22, p < 0.05). H9 is supported. Again, perceived risk significantly moderates the relationship between PE→UI (β = −0.24, p < 0.01). H6 is supported. The combined (GR and PR) moderating effect on PE→UI is not significant. Hence, H12 is not supported. On the other hand, government regulation is found to significantly moderate the relationship FC→UI (β = 0.25, p < 0.05). Hypothesis H10 is supported. However, the moderating effect of PR on FC→UI is found to be insignificant. Hence, hypothesis H7 is not supported. Thus, the combined moderating effect of PR and GR on FC→UI is significant (β = 0.21, p < 0.05). H13 is supported.

The suggested model explains a significant proportion of the variance in initial trust (67%) and usage intention (69%) (Figure 2). Falk and Miller (1992) state that the coefficient of determination (R2) must be greater than 0.10. Overall, the suggested model can account for more than half of the variance in the dependent variables. These results imply that the proposed model is stable and robust. Table 5 and Figure 2 display all estimated and normalized path coefficients (significant paths are indicated with asterisks). Finally, Table 6 shows the results of the hypothesis test.

6. Discussion

This study seeks to extend the researcher’s understanding of blockchain technology adaptation in banking services by extending UTAUT with contextual variables. The research model in this study enhances the theoretical foundations of UTAUT by incorporating different contextual variables, e.g., trust, government regulation, and perceived risk, shaping the adoption behavior of bankers to use blockchain technology in the banking sector. A high level of trust in blockchain technology will make it easier for bankers to validate the details of blockchain services to evaluate their reality. The study results show the significant effect of trust in blockchain technology on usage intention. The analysis results demonstrate that a high level of trust will increase the bankers’ intention to use blockchain technology in banking services. This result is in line with the argument stated by previous researchers (Saputra and Darma 2022; Vidan and Lehdonvirta 2019). The banker will feel more comfortable using trusted services because there will be no need to check for authenticity and legitimacy (Bianchi and Brockner 2012; Saputra and Darma 2022).

The proposed model validates the relationship between performance expectancy (PE) and initial trust (ITR). This finding is consistent with previous studies in the context of IT-enabled banking services (Kim and Garrison 2009; Oliveira et al. 2014). As discussed, initial trust is formed when the user finds performance gains from using blockchain technology. Thus, when the banking tasks are optimized by blockchain technology, it leads to the initial trust of the banker. Further, this study found that PE is one of the most important predictors of usage intention to use blockchain technology. This finding is also supported by various past studies (Luo et al. 2010; Zhou et al. 2010). It is interesting to note that the banker views performance expectations as one of the most critical aspects of the acceptance of blockchain technology in Indian banking and financial services.

The moderating variable, and perceived risk, failed to moderate the association (FC→UI and ITR→UI). Indeed, blockchain application in banking is the story of the future. When trust in blockchain grows and the enabling conditions improve, bankers will be able to confidently use blockchain in their work. That means when bankers are proficient with the blockchain-enabled banking system, the impact of risk does not seem very significant in moderating the proposed relationship. Further, government regulations and perceived security are proven to be significant mediators in the proposed model. The rules and regulations regarding the use of cryptocurrencies and other financial transactions using blockchain, especially in India, are still unclear. The bankers feel that government regulation does not provide enough support for using blockchain transactions. Besides, the risk of using blockchain in banking services has not been explored enough by government regulation. The lack of clarity in rules and regulations regarding the usage of blockchain technology in banking services will make bankers distrustful in India. Meanwhile, on the security aspect, frequent bugs, and delays in the application, cause bankers to feel insecure when using it. It may be because blockchain applications are very new to the bank, so it needs more development in technology security. In addition, blockchain is a decentralized technology that is always vulnerable to malicious security attacks, resulting in huge value and data theft (Lin and Liao 2017).

6.1. Study Implication

This research makes significant contributions to both research and practice. For researchers, the model provides a holistic approach to examining the factors that predict blockchain adoption in India’s banking sector by cohesively extending the UTAUT model. The study adds to the existing body of knowledge by establishing a link between bankers’ perceptions of blockchain technology and the blockchain’s ability to meet their individual performance expectations in banking activities, facilitating conditions to support the use of blockchain technology, and their initial trust in blockchain services. It provides practitioners with useful insights into the role of advanced technology in banking service delivery. It provides a realistic view of the behavioral and technological factors that influence the decision to use blockchain technology. The study can assist banking and financial institution stakeholders in supporting blockchain initiatives, implementation, and deployment in Indian banks. The theoretical and practical implications will be explained in the next sections.

6.1.1. Theoretical Implications

This paper provides several significant advances in theory. First, to the best of our knowledge, this is an early attempt to analyze blockchain usage intention in Indian banks in a comprehensive manner. Although few prior studies have addressed blockchain adoption using the UTAUT model, the strength of this study lies in extending the UTAUT model by adding contextual behavioral, technological, and environmental variables. This is evidenced by the high explanatory power of our research model (0.69). Second, it is important to point out that the constructs relevant to blockchain adoption are not just FC, but also performance expectancy, initial trust, and the moderating role of government regulation and perceived risk. This warrants the extension of the UTAUT framework by adding contextual constructs to explain the adoption of blockchain in the Indian banking system. Future studies on technology adoption may benefit from this research. This research presents an integrative model for evaluating the impact of behavioral, technological, and environmental aspects on the adoption of new technologies.

6.1.2. Implications for Practice

This study provides a significant hands-on impact on relevant stakeholders, government representatives, industry professionals, and policymakers, involved in implementing and delivering the blockchain service. This study found the direct effects of performance expectancy on initial trust and usage intention. The direct effect of PE on UI shows that the bankers’ intention to use blockchain technology is largely influenced by the benefits (e.g., convenience, economic benefits, satisfaction, etc.) of using technology to carry out banking operations. This means that the banking authorities must provide at least all the required services available through blockchain technology. The facilitating condition is another important determinant of usage intention and creates initial trust among the users of blockchain technology in the banking environment. Therefore, it is recommended that the senior bank authorities and technical support team organize workshops, conferences, and peer-peer discussions, regarding the usage and benefits of different applications to enhance the bankers’ initial trust and usage intention. Further, providing useful suggestions through creating micro-support sites, round-the-clock call centers, and qualified personnel to offer a helping hand, can boost the banker’s trust and usage intention. Furthermore, authorities must provide the necessary infrastructure at both the organizational and technical levels to ensure a seamless blockchain experience for bankers.

Furthermore, government rules and regulations regarding the implementation and use of blockchain technology also influence the trust and intention to use blockchain services. Since 2017, the government of India has started framing rules to make banking transactions seamless and secure using blockchain1. However, the government of India needs more effort to bring user-friendly rules and regulations to influence the bankers’ decision to use blockchain and ensure that the rules optimize the usage of blockchain. Again, the perceived risk of using blockchain services was another observation from the study results. So, ensuring and maintaining information protection guarantees, transaction confidentiality, and service availability, can minimize the reputational risk.

7. Limitations and Future Research

There are certain limitations to this study, as in other studies. Some restrictions are a result of this new technology’s (blockchain) fundamental characteristics. In India, the use of blockchain in banking and financial transactions is a relatively recent service. Although most mobile phone users are aware of the blockchain service’s basic notion, they are generally unaware of its actual capabilities. Over time, bankers will use blockchain more widely, so longitudinal research in the future will help to better understand the acceptance of blockchain technology. Since there has not been much research done on how banks are using blockchain, future research can help us learn more about how users feel about blockchain services in banks, like cryptocurrency payments, and letters of credit (LOC), etc.

It can also be a worthwhile improvement to adjust the research model described in this study to incorporate different contextual moderators, e.g., technology experience, and task-technology fit, etc. Once the new service is used, the foundation of trust shifts, and as time goes on, information quality, security, and availability become the factors that matter (Zahedi et al. 2008). This study can be expanded to include data quality parameters and how they affect blockchain adoption in the face of change in mobile technology and financial service models. Retail banks, commercial banks, community development banks, or any other sort of banking institution, were not distinguished in this study. Therefore, future studies can compare and contrast the intention to adopt blockchain as various banking institutions differ in terms of IT and strategic decisions (Tallon 2010). In the future, researchers could also use other types of analysis, like spatial analysis (Franch-Pardo et al. 2020), to look at how blockchain innovations are spreading in the banking and financial sector.

8. Conclusions

This study formulated and empirically tested an extended UTAUT model to explain the important predictors of Indian bankers’ intention to use blockchain technology at an individual level. The findings of this study indicate that the suggested model has strong explanatory power and is reliable in a variety of situations. Not only is the extension of the UTAUT model with different contextual constructs (initial trust, government regulations, and perceived risk) theoretically appealing, but it is also empirically significant. The study reveals that the most important predictors of an Indian banker’s intention to use blockchain are facilitating conditions (FC), performance expectancy (PE), and initial trust (ITR). The significant moderation effect of government regulation and perceived risk on the intention to use blockchain technology and its predictors also proves the significance of the proposed model. The research proposes a comprehensive strategy for future studies on the adoption of new technologies (e.g., blockchain) by emphasizing the utility of the UTAUT extension by integrating crucial contextual elements. The research provides practitioners with helpful insights that can be used to create and ensure the seamless deployment of blockchain technology within the banking sector.

Supplementary Materials

The following supporting information can be downloaded at: https://www.mdpi.com/article/10.3390/ijfs10040090/s1, Study Instrument.

Funding

This research received no external funding.

Informed Consent Statement

Not applicable.

Data Availability Statement

Data can be provided on request.

Conflicts of Interest

The author declares no conflict of interest.

| 1 | https://bfsi.economictimes.indiatimes.com/news/banking/how-indian-banks-are-leveraging-blockchain-technology/88027231 (assessed on 17 August 2022). |

References

- Ahmed, Rizwan Raheem, Dalia Štreimikienė, and Justas Štreimikis. 2022a. The extended UTAUT model and learning management system during COVID-19: Evidence from PLS-SEM and conditional process modeling. Journal of Business Economics and Management 23: 82–104. [Google Scholar] [CrossRef]

- Ahmed, Shamima, Muneer M. Alshater, Anis El Ammari, and Helmi Hammami. 2022b. Artificial intelligence and machine learning in finance: A bibliometric review. Research in International Business and Finance 61: 101646. [Google Scholar] [CrossRef]

- Ajzen, Icek. 1985. From intentions to actions: A theory of planned behavior. In Action Control. Berlin: Springer, pp. 11–39. [Google Scholar]

- Akhtar, Sadia, Muhammad Irfan, Shamsa Kanwal, and Abdul Hameed Pitafi. 2019. Analysing UTAUT with trust toward mobile banking adoption in China and Pakistan: Extending with the effect of power distance and uncertainty avoidance. International Journal of Financial Innovation in Banking 2: 183–207. [Google Scholar] [CrossRef]

- Aljaafreh, Ali. 2021. Why Students Use Social Networks for Education: Extension of Utaut2. Journal of Technology and Science Education 11: 53–66. [Google Scholar]

- Almisad, Budour, and Monirah Alsalim. 2020. Kuwaiti female university students’ acceptance of the integration of smartphones in their learning: An investigation guided by a modified version of the unified theory of acceptance and use of technology (UTAUT). International Journal of Technology Enhanced Learning 12: 1–19. [Google Scholar] [CrossRef]

- Alolah, Turki, Rodney A. Stewart, Kriengsak Panuwatwanich, and Sherif Mohamed. 2014. Determining the causal relationships among balanced scorecard perspectives on school safety performance: Case of Saudi Arabia. Accident Analysis & Prevention 68: 57–74. [Google Scholar]

- Armstrong, J. Scott, and Terry S. Overton. 1977. Estimating nonresponse bias in mail surveys. Journal of Marketing Research 14: 396–402. [Google Scholar] [CrossRef]

- Ayaz, A., and Mustafa Yanartaş. 2020. An analysis on the unified theory of acceptance and use of technology theory (UTAUT): Acceptance of electronic document management system (EDMS). Computers in Human Behavior Reports 2: 100032. [Google Scholar] [CrossRef]

- Bagozzi, Richard P., and Youjae Yi. 2012. Specification, evaluation, and interpretation of structural equation models. Journal of the Academy of Marketing Science 40: 8–34. [Google Scholar] [CrossRef]

- Bianchi, Emily C., and Joel Brockner. 2012. In the eyes of the beholder? The role of dispositional trust in judgments of procedural and interactional fairness. Organizational Behavior and Human Decision Processes 118: 46–59. [Google Scholar] [CrossRef]

- Boomsma, Anne, and Jeffrey J. Hoogland. 2001. The robustness of LISREL modeling revisited. Structural Equation Models: Present and Future. A Festschrift in Honor of Karl Jöreskog 2: 139–68. [Google Scholar]

- Bunea, Daniela, Polychronis Karakitsos, Niall Merriman, and Werner Studener. 2016. Profit distribution and loss coverage rules for central banks. ECB Occasional Paper 169: 1–56. [Google Scholar] [CrossRef]

- Burda, Daniel, and Frank Teuteberg. 2014. The role of trust and risk perceptions in cloud archiving—Results from an empirical study. The Journal of High Technology Management Research 25: 172–87. [Google Scholar] [CrossRef]

- Casey, Tristan, and Elisabeth Wilson-Evered. 2012. Predicting uptake of technology innovations in online family dispute resolution services: An application and extension of the UTAUT. Computers in Human Behavior 28: 2034–45. [Google Scholar] [CrossRef]

- Chang, Hsin Hsin, and Su Wen Chen. 2008. The impact of online store environment cues on purchase intention: Trust and perceived risk as a mediator. Online Information Review 32: 818–41. [Google Scholar] [CrossRef]

- Chang, Victor, Patricia Baudier, Hui Zhang, Qianwen Xu, Jingqi Zhang, and Mitra Arami. 2020. How Blockchain can impact financial services–The overview, challenges and recommendations from expert interviewees. Technological Forecasting and Social Change 158: 120166. [Google Scholar] [CrossRef] [PubMed]

- Chao, Cheng-Min. 2019. Factors determining the behavioral intention to use mobile learning: An application and extension of the UTAUT model. Frontiers in Psychology 10: 1652. [Google Scholar] [CrossRef]

- Chaouali, Walid, Imene Ben Yahia, and Nizar Souiden. 2016. The interplay of counter-conformity motivation, social influence, and trust in customers’ intention to adopt Internet banking services: The case of an emerging country. Journal of Retailing and Consumer Services 28: 209–18. [Google Scholar] [CrossRef]

- Cheng, Ritchie Jay. 2020. UTAUT implementation of cryptocurrency-based Islamic financing instrument. International Journal of Academic Research in Business and Social Sciences 10: 873–84. [Google Scholar] [CrossRef]

- Creswell, John W., and J. David Creswell. 2017. Research Design: Qualitative, Quantitative, and Mixed Methods Approaches. Thousand Oaks: Sage Publications. [Google Scholar]

- Cucari, Nicola, Valentina Lagasio, Giuseppe Lia, and Chiara Torrier. 2022. The impact of blockchain in banking processes: The Interbank Spunta case study. Technology Analysis & Strategic Management 34: 138–50. [Google Scholar]

- Davis, Fred D. 1987. User Acceptance of Information Systems: The Technology Acceptance Model (TAM). Ann Arbor: University of Michigan. [Google Scholar]

- Domingo, Marta Gómez, and Antoni Badia Garganté. 2016. Exploring the use of educational technology in primary education: Teachers’ perception of mobile technology learning impacts and applications’ use in the classroom. Computers in Human Behavior 56: 21–28. [Google Scholar] [CrossRef]

- Dwivedi, Yogesh K., Elvira Ismagilova, Prianka Sarker, Anand Jeyaraj, Yassine Jadil, and Laurie Hughes. 2021. A meta-analytic structural equation model for understanding social commerce adoption. Information Systems Frontiers 2021: 1–17. [Google Scholar] [CrossRef]

- Dwivedi, Yogesh K., Nripendra P. Rana, Anand Jeyaraj, Marc Clement, and Michael D. Williams. 2019. Re-examining the unified theory of acceptance and use of technology (UTAUT): Towards a revised theoretical model. Information Systems Frontiers 21: 719–34. [Google Scholar] [CrossRef]

- Falk, R. Frank, and Nancy B. Miller. 1992. A Primer for Soft Modeling. Akron: University of Akron Press. [Google Scholar]

- Fishbein, Martin, and Icek Ajzen. 1977. Belief, attitude, intention, and behavior: An introduction to theory and research. Philosophy and Rhetoric 10: 177–88. [Google Scholar]

- Fornell, Claes, and David F. Larcker. 1981. Structural Equation Models with Unobservable Variables and Measurement Error: Algebra and Statistics. Los Angeles: Sage Publications. [Google Scholar]

- Frame, W. Scott, Larry D. Wall, and Lawrence J. White. 2018. Technological Change and Financial Innovation in Banking: Some Implications for Fintech. Available online: https://ssrn.com/abstract=3261732 (accessed on 3 March 2022).

- Franch-Pardo, Ivan, Brian M. Napoletano, Fernando Rosete-Verges, and Lawal Billa. 2020. Spatial analysis and GIS in the study of COVID-19. A review. Science of the Total Environment 739: 140033. [Google Scholar] [CrossRef]

- Franque, Frank Bivar, Tiago Oliveira, and Carlos Tam. 2022. Continuance intention of mobile payment: TTF model with Trust in an African context. Information Systems Frontiers 2022: 1–19. [Google Scholar] [CrossRef]

- Ghazizadeh, Mahtab, Yiyun Peng, John D. Lee, and Linda Ng Boyle. 2012. Augmenting the technology acceptance model with trust: Commercial drivers’ attitudes towards monitoring and feedback. Proceedings of the Human Factors and Ergonomics Society Annual Meeting 56: 2286–90. [Google Scholar] [CrossRef]

- Giovannini, Cristiane Junqueira, Jorge Brantes Ferreira, Jorge Ferreira da Silva, and Daniel Brantes Ferreira. 2015. The effects of trust transference, mobile attributes and enjoyment on mobile trust. BAR-Brazilian Administration Review 12: 88–108. [Google Scholar] [CrossRef]

- Gupta, Abhishek, and Stuti Gupta. 2018. Blockchain technology: Application in Indian banking sector. Delhi Business Review 19: 75–84. [Google Scholar] [CrossRef]

- Gupta, Somya, Wafa Ghardallou, Dharen Kumar Pandey, and Ganesh P. Sahu. 2022. Artificial intelligence adoption in the insurance industry: Evidence using the technology–organization–environment framework. Research in International Business and Finance 5: 101757. [Google Scholar] [CrossRef]

- Haferkorn, Martin, and Josué Manuel Quintana Diaz. 2014. Seasonality and interconnectivity within cryptocurrencies-an analysis on the basis of bitcoin, litecoin and namecoin. International Workshop on Enterprise Applications and Services in the Finance Industry 217: 106–20. [Google Scholar]

- Hair, Joe F., Jr., Lucy M. Matthews, Ryan L. Matthews, and Marko Sarstedt. 2017. PLS-SEM or CB-SEM: Updated guidelines on which method to use. International Journal of Multivariate Data Analysis 1: 107–23. [Google Scholar] [CrossRef]

- Hair, Joseph F., David J. Ortinau, and Dana E. Harrison. 2010. Essentials of Marketing Research. New York: McGraw-Hill/Irwin, vol. 2. [Google Scholar]

- Hair, Joseph F., Jr., G. Tomas M. Hult, Christian M. Ringle, and Marko Sarstedt. 2016. A Primer on Partial Least Squares Structural Equation Modeling (PLS-SEM). Thousand Oaks: Sage Publications. [Google Scholar]

- Han, Jeonghye, and Daniela Conti. 2020. The use of UTAUT and post acceptance models to investigate the attitude towards a telepresence robot in an educational setting. Robotics 9: 34. [Google Scholar] [CrossRef]

- Harman, Harry H. 1976. Modern Factor Analysis. Chicago: University of Chicago Press. [Google Scholar]

- Harwood-Jones, Margaret. 2016. Blockchain and T2S: A Potential Disruptor. London: Standard Chartered Bank. [Google Scholar]

- Heidari, Hamed, Morteza Mousakhani, Mahmood Alborzi, Ali Divandari, and Reza Radfar. 2019. Explaining the Blockchain Acceptance Indices in Iran Financial Markets: A Fuzzy Delphi Study. Journal of Money and Economy 14: 335–65. [Google Scholar]

- Hew, Teck-Soon, and Sharifah Latifah Syed Abdul Kadir. 2016. Predicting instructional effectiveness of cloud-based virtual learning environment. Industrial Management & Data Systems 116: 1557–84. [Google Scholar]

- Hmoud, Bilal Ibrahim, and László Várallyai. 2020. Artificial intelligence in human resources information systems: Investigating its trust and adoption determinants. International Journal of Engineering and Management Sciences 5: 749–65. [Google Scholar] [CrossRef]

- Jena, R. K. 2022. Exploring Antecedents of Peoples’ Intentions to Use Smart Services in a Smart City Environment: An Extended UTAUT Model. Journal of Information Systems 36: 133–49. [Google Scholar] [CrossRef]

- Jevsikova, Tatjana, Gabrielė Stupurienė, Dovilė Stumbrienė, Anita Juškevičienė, and Valentina Dagienė. 2021. Acceptance of distance learning technologies by teachers: Determining factors and emergency state influence. Informatica 32: 517–42. [Google Scholar] [CrossRef]

- Karim, Sitara, Mustafa Raza Rabbani, and Hana Bawazir. 2022. Applications of blockchain technology in the finance and banking industry beyond digital currencies. In Blockchain Technology and Computational Excellence for Society 5.0. Hershey: IGI Global, pp. 216–38. [Google Scholar]

- Kawasmi, Zaina, Evans Akwasi Gyasi, and Deneise Dadd. 2020. Blockchain adoption model for the global banking industry. Journal of International Technology and Information Management 28: 112–54. [Google Scholar]

- Khalil, Mahmoona, Kausar Fiaz Khawaja, and Muddassar Sarfraz. 2021. The adoption of blockchain technology in the financial sector during the era of fourth industrial revolution: A moderated mediated model. Quality & Quantity 56: 2435–52. [Google Scholar]

- Kim, Kyung Kyu, and Bipin Prabhakar. 2004. Initial trust and the adoption of B2C e-commerce: The case of internet banking. ACM SIGMIS Database: The DATABASE for Advances in Information Systems 35: 50–64. [Google Scholar] [CrossRef]

- Kim, Sanghyun, and Gary Garrison. 2009. Investigating mobile wireless technology adoption: An extension of the technology acceptance model. Information Systems Frontiers 11: 323–33. [Google Scholar] [CrossRef]

- Kopp, Tobias, Marco Baumgartner, and Steffen Kinkel. 2022. How Linguistic Framing Affects Factory Workers’ Initial Trust in Collaborative Robots: The Interplay Between Anthropomorphism and Technological Replacement. International Journal of Human-Computer Studies 158: 102730. [Google Scholar] [CrossRef]

- Koufaris, Marios, and William Hampton-Sosa. 2004. The development of initial trust in an online company by new customers. Information & Management 41: 377–97. [Google Scholar]

- Kumari, Anitha, and N. Chitra Devi. 2022a. Blockchain technology acceptance by investment professionals: A decomposed TPB model. Journal of Financial Reporting and Accounting, ahead-of-print. [Google Scholar]

- Kumari, Anitha, and N. Chitra Devi. 2022b. Determinants of user’s behavioural intention to use blockchain technology in the digital banking services. International Journal of Electronic Finance 11: 159–74. [Google Scholar] [CrossRef]

- Kumari, Anitha, and N. Chitra Devi. 2022c. The Impact of FinTech and Blockchain Technologies on Banking and Financial Services. Technology Innovation Management Review. Available online: https://timreview.ca/article/1481 (accessed on 13 June 2022).

- Lai, Horng-Ji. 2020. Investigating older adults’ decisions to use mobile devices for learning, based on the unified theory of acceptance and use of technology. Interactive Learning Environments 28: 890–901. [Google Scholar] [CrossRef]

- Lin, Iuon-Chang, and Tzu-Chun Liao. 2017. A survey of blockchain security issues and challenges. International Journal of Network Security 19: 653–59. [Google Scholar]

- Luo, Xin, Han Li, Jie Zhang, and Jung P. Shim. 2010. Examining multi-dimensional trust and multi-faceted risk in initial acceptance of emerging technologies: An empirical study of mobile banking services. Decision Support Systems 49: 222–34. [Google Scholar] [CrossRef]

- MacDonald, Trent J., Darcy WE Allen, and Jason Potts. 2016. Blockchains and the boundaries of self-organized economies: Predictions for the future of banking. In Banking beyond Banks and Money. Berlin: Springer, pp. 279–96. [Google Scholar]

- Manchon, J.-B., Mercedes Bueno, and Jordan Navarro. 2022. How the initial level of trust in automated driving impacts drivers’ behaviour and early trust construction. Transportation Research Part F: Traffic Psychology and Behaviour 86: 281–95. [Google Scholar] [CrossRef]

- Martins, Carolina, Tiago Oliveira, and Aleš Popovič. 2014. Understanding the Internet banking adoption: A unified theory of acceptance and use of technology and perceived risk application. International Journal of Information Management 34: 1–13. [Google Scholar] [CrossRef]

- Masrek, Mohamad Noorman, Intan Salwani Mohamed, Norzaidi Mohd Daud, and Normah Omar. 2014. Technology trust and mobile banking satisfaction: A case of Malaysian consumers. Procedia-Social and Behavioral Sciences 129: 53–58. [Google Scholar] [CrossRef]

- Nazim, Nur Firas, Nabiha Mohd Razis, and Mohammad Firdaus Mohammad Hatta. 2021. Behavioural intention to adopt blockchain technology among bankers in islamic financial system: Perspectives in Malaysia. Romanian Journal of Information Technology and Automatic Control 31: 11–28. [Google Scholar] [CrossRef]

- Neirotti, Paolo, Elisabetta Raguseo, and Emilio Paolucci. 2018. How SMEs develop ICT-based capabilities in response to their environment: Past evidence and implications for the uptake of the new ICT paradigm. Journal of Enterprise Information Management 31: 10–37. [Google Scholar] [CrossRef]

- Nguyen, Quoc Khanh. 2016. Blockchain-a financial technology for future sustainable development. Paper presented at 2016 3rd International Conference on Green Technology and Sustainable Development (GTSD), Kaohsiung, Taiwan, November 24–25; pp. 51–54. [Google Scholar]

- Oliveira, Tiago, Matilde Alhinho, Paulo Rita, and Gurpreet Dhillon. 2017. Modelling and testing consumer trust dimensions in e-commerce. Computers in Human Behavior 71: 153–64. [Google Scholar] [CrossRef]

- Oliveira, Tiago, Miguel Faria, Manoj Abraham Thomas, and Aleš Popovič. 2014. Extending the understanding of mobile banking adoption: When UTAUT meets TTF and ITM. International Journal of Information Management 34: 689–703. [Google Scholar] [CrossRef]

- Osmani, Mohamad, Ramzi El-Haddadeh, Nitham Hindi, Marijn Janssen, and Vishanth Weerakkody. 2020. Blockchain for next generation services in banking and finance: Cost, benefit, risk and opportunity analysis. Journal of Enterprise Information Management 34: 884–99. [Google Scholar] [CrossRef]

- Patel, Ritesh, Milena Migliavacca, and M. Oriani. 2022. Blockchain in banking and finance: A bibliometric review. Research in International Business and Finance 62: 101718. [Google Scholar] [CrossRef]

- Patki, Aarti, and Vinod Sople. 2020. Indian banking sector: Blockchain implementation, challenges and way forward. Journal of Banking and Financial Technology 4: 65–73. [Google Scholar] [CrossRef]

- Podsakoff, Philip M., Scott B. MacKenzie, Jeong-Yeon Lee, and Nathan P. Podsakoff. 2003. Common method biases in behavioral research: A critical review of the literature and recommended remedies. Journal of Applied Psychology 88: 879. [Google Scholar] [CrossRef]

- Raza, Syed A., Wasim Qazi, Komal Akram Khan, and Javeria Salam. 2021. Social isolation and acceptance of the learning management system (LMS) in the time of COVID-19 pandemic: An expansion of the UTAUT model. Journal of Educational Computing Research 59: 183–208. [Google Scholar] [CrossRef]

- Saheb, Tahereh, and Faranak Hosseinpouli Mamaghani. 2021. Exploring the barriers and organizational values of blockchain adoption in the banking industry. The Journal of High Technology Management Research 32: 100417. [Google Scholar] [CrossRef]

- Saputra, Upayana Wiguna Eka, and Gede Sri Darma. 2022. The Intention to Use Blockchain in Indonesia Using Extended Approach Technology Acceptance Model (TAM). CommIT (Communication and Information Technology) Journal 16: 27–35. [Google Scholar] [CrossRef]

- Schreiber, James B., Amaury Nora, Frances K. Stage, Elizabeth A. Barlow, and Jamie King. 2006. Reporting structural equation modeling and confirmatory factor analysis results: A review. The Journal of Educational Research 99: 323–38. [Google Scholar] [CrossRef]

- Stone, Mervyn. 1974. Cross-validatory choice and assessment of statistical predictions. Journal of the Royal Statistical Society: Series B (Methodological) 36: 111–33. [Google Scholar]

- Taherdoost, Hamed. 2017. Appraising the smart card technology adoption; case of application in university environment. Procedia Engineering 181: 1049–57. [Google Scholar] [CrossRef]

- Taherdoost, Hamed. 2018. A review of technology acceptance and adoption models and theories. Procedia Manufacturing 22: 960–67. [Google Scholar] [CrossRef]

- Taherdoost, Hamed. 2022. A Critical Review of Blockchain Acceptance Models—Blockchain Technology Adoption Frameworks and Applications. Computers 11: 24. [Google Scholar] [CrossRef]

- Tallon, Paul P. 2010. A service science perspective on strategic choice, IT, and performance in US banking. Journal of Management Information Systems 26: 219–52. [Google Scholar] [CrossRef]

- Tamilmani, Kuttimani, Nripendra P. Rana, and Yogesh K. Dwivedi. 2021. Consumer acceptance and use of information technology: A meta-analytic evaluation of UTAUT2. Information Systems Frontiers 23: 987–1005. [Google Scholar] [CrossRef]

- Tamilmani, Kuttimani, Nripendra P. Rana, Naveena Prakasam, and Yogesh K. Dwivedi. 2019. The battle of Brain vs. Heart: A literature review and meta-analysis of “hedonic motivation” use in UTAUT2. International Journal of Information Management 46: 222–35. [Google Scholar] [CrossRef]

- Tapscott, Don, and Alex Tapscott. 2016. Blockchain Revolution: How the Technology behind Bitcoin is Changing Money, Business, and the World. New York: Penguin. [Google Scholar]

- Thusi, Philile, and Daniel K. Maduku. 2020. South African millennials’ acceptance and use of retail mobile banking apps: An integrated perspective. Computers in Human Behavior 111: 106405. [Google Scholar] [CrossRef]

- Tornatzky, Louis G., Mitchell Fleischer, and Alok K. Chakrabarti. 1990. Processes of Technological Innovation. Lanham: Lexington Books. [Google Scholar]

- Tsang, Kwok Kuen, Yuan Teng, Yi Lian, and Li Wang. 2021. School management culture, emotional labor, and teacher burnout in Mainland China. Sustainability 13: 9141. [Google Scholar] [CrossRef]

- Venkatesh, Viswanath. 2022. Adoption and use of AI tools: A research agenda grounded in UTAUT. Annals of Operations Research 308: 641–52. [Google Scholar] [CrossRef]

- Venkatesh, Viswanath, James Y. L. Thong, and Xin Xu. 2012. Consumer acceptance and use of information technology: Extending the unified theory of acceptance and use of technology. MIS Quarterly 36: 157–78. [Google Scholar] [CrossRef]

- Venkatesh, Viswanath, James Y. L. Thong, and Xin Xu. 2016. Unified theory of acceptance and use of technology: A synthesis and the road ahead. Journal of the Association for Information Systems 17: 328–76. [Google Scholar] [CrossRef]

- Venkatesh, Viswanath, Michael G. Morris, Gordon B. Davis, and Fred D. Davis. 2003. User acceptance of information technology: Toward a unified view. MIS Quarterly 27: 425–78. [Google Scholar] [CrossRef]

- Vidan, Gili, and Vili Lehdonvirta. 2019. Mine the gap: Bitcoin and the maintenance of trustlessness. New Media & Society 21: 42–59. [Google Scholar]

- von Solms, Basie, and Rossouw von Solms. 2018. Cybersecurity and information security–what goes where? Information & Computer Security 26: 2–9. [Google Scholar]

- Wijaya, Dennis, Ermi Girsang, Sri Lestari Ramadhani, Sri Wahyuni Nasution, and Ulina Karo Karo. 2022. Influence Of Organizing Functions, Direction Functions And Planning Functions On Nurse Performance At Hospital Royal Prima Medan. International Journal of Health and Pharmaceutical (IJHP) 2: 1–8. [Google Scholar] [CrossRef]

- Williams, Michael D., Nripendra P. Rana, and Yogesh K. Dwivedi. 2015. The unified theory of acceptance and use of technology (UTAUT): A literature review. Journal of Enterprise Information Management 28: 443–88. [Google Scholar] [CrossRef]

- Wolf, Erika J., Kelly M. Harrington, Shaunna L. Clark, and Mark W. Miller. 2013. Sample size requirements for structural equation models: An evaluation of power, bias, and solution propriety. Educational and Psychological Measurement 73: 913–34. [Google Scholar] [CrossRef] [PubMed]

- Xie, Heng, Alsius David, Md Rasel Al Mamun, Victor R. Prybutok, and Anna Sidorova. 2022. The formation of initial trust by potential passengers of self-driving taxis. Journal of Decision Systems 2022: 1–30. [Google Scholar] [CrossRef]

- Yang, Cheng-Chia, Cheng Liu, and Yi-Shun Wang. 2022. The acceptance and use of smartphones among older adults: Differences in UTAUT determinants before and after training. Library Hi Tech, ahead-of-print. [Google Scholar]

- Yusof, Hayati, M. F. M. B. Munir, Zulnurhaini Zolkaply, Chin Li Jing, Chooi Yu Hao, Ding Swee Ying, Lee Seang Zheng, Ling Yuh Seng, and Tan Kok Leong. 2018. Behavioral intention to adopt blockchain technology: Viewpoint of the banking institutions in Malaysia. International Journal of Advanced Scientific Research and Management 3: 274–79. [Google Scholar]

- Zahedi, Fatemeh, Jaeki Song, and Suprasith Jarupathirun. 2008. Web-based decision support. In Handbook on Decision Support Systems 1. Berlin: Springer, pp. 315–38. [Google Scholar]

- Zhou, Tao, Yaobin Lu, and Bin Wang. 2010. Integrating TTF and UTAUT to explain mobile banking user adoption. Computers in Human Behavior 26: 760–67. [Google Scholar] [CrossRef]

Figure 1.

Conceptualized extended UTAUT model.

Figure 2.

Path coefficients (Direct). * p < 0.05.

{kind=link}