A Bibliometric Analysis of Fintech Trends: An Empirical Investigation

by

, , , ,

, , , ,

Girish Garg

1,

Mohd Shamshad

1,

Nikita Gauhar

1,

Mosab I. Tabash

2,* ,

,

Basem Hamouri

3 and

Linda Nalini Daniel

4

1

School of Finance & Commerce, Galgotias University, Greater Noida 201310, India

2

College of Business, Al Ain University, Al Ain P.O. Box 64141, United Arab Emirates

3

Department of Finance and Banking Sciences, Amman University College of Financial and Administrative Science, Al-Balqa Applied University, Al-Salt P.O. Box 19117, Jordan

4

Faculty of Business, Higher Colleges of Technology, Abu Dhabi P.O. Box 41012, United Arab Emirates

*

Author to whom correspondence should be addressed.

Int. J. Financial Stud. 2023, 11(2), 79; https://doi.org/10.3390/ijfs11020079

Submission received: 10 April 2023

/

Revised: 18 May 2023

/

Accepted: 14 June 2023

/

Published: 19 June 2023

(This article belongs to the Special Issue Literature Reviews in Finance)

Abstract

:Financial technology, or Fintech, has captured the attention of scholars, students, and institutions across worldwide for over a decade. With a plethora of new financial services, products, and innovative methods to engage with clients, the impact of technology on the financial sector has been extensively studied. This research paper provides a summary of scientific research on FinTech by using bibliometric analysis. Using the Scopus database, the paper analyzed 665 publications and identified research gaps and new study topics through “VOS-Viewer” software and “Biblioshiny” using RStudio. The study focused on FinTech’s functions and research constraints in digital finance by assessing citation links between the most significant articles. The findings provide a starting point for further investigation and offer opportunities for researchers to expand their expertise in exciting and innovative studies. Overall, this study seeks to help researchers discover new avenues for exploration in Fintech while advancing their present understanding. There exists much scope in the area of Digital Lending, Supply Chain Finance, the Internet of Things, and RoboAdvisers.

1. Introduction

FinTech (abbreviation for financial technology, as an emerging technical term) is driven by a variety of emerging frontier technologies. It is a series of new business models, new technology applications, and new products and services that have a significant impact on the financial market and supply of financial services. It has attracted wide attention because of the following advantages: improving the efficiency of operations, reducing operating costs effectively, disrupting the existing industry structures, blurring industry boundaries, facilitating strategic disintermediation, providing new gateways for entrepreneurship, and democratizing access to financial services (Li and Xu 2021). Due to financial technology, the financial sector has experienced a constant growth in its services (Brandl and Hornuf 2020; Kanungo and Gupta 2021). This development improves client communication and back-office data processing. Focus on financial innovation has shifted from boosting existing occupations to creating new jobs and business strategies for financial services companies (Gomber et al. 2017), Gomber et al. (2017), and Ozili (2018) offer new financial goods, companies, programs, and consumer interactions (Anjum et al. 2017; Azizi et al. 2021). Financial and information systems research examine these shifts and the financial industry’s impact on technology. Shao et al. (2022) argued that financial technology, like the fast Internet speed and connection changes, plays a big part in getting people to buy insurance plans. Machine learning is an easy-to-understand type of financial technology used in insurance practises to help salespeople learn new habits, build client-friendly strategies, and create the best situation for clients, firms, and salespeople (Chen et al. 2022). AI and data technology transform insurance business models. Some incumbent insurers strive to do the same better, while others adapt to take advantage of new technology and users. Meanwhile, tech-savvy outsiders are destabilising the market. However, this turmoil is leading to a business strategy that works (Zarifis and Cheng 2021).

As the banking sector adapts to the modern digital world, Fintech has become more vital. Some key elements of today’s financial technology landscape include but not limited to the following: People are shifting from using cash and checks to digital payment services provided by fintech businesses. The widespread use of mobile payment programs such as Paytm, PhonePe, and Gpay has made it simpler than ever to exchange funds digitally. One way that fintech firms are shaking up the financial services sector is through online lending platforms, which provide borrowers with convenient and speedy access to credit. These online marketplaces utilize computer algorithms to evaluate applicants’ credit and risk, streamlining the loan process and making it available to more people. Robo-advisors are one example of how Fintech has simplified investing & insurance for the regular consumer (Zarifis et al. 2021). Algorithms power the financial advice and portfolio management functions of these digital hubs. The development of financial technology has also contributed significantly to the expansion of blockchain and cryptocurrencies. The distributed ledger technology known as blockchain has the potential to alter the way monetary transactions are recorded and processed completely. The usage of cryptocurrencies like Bitcoin and Ethereum in online transactions is also growing in popularity. As a whole, Fintech is revolutionizing the financial sector and altering how individuals handle their finances. We may anticipate that Fintech will develop and play an increasingly important role in determining the future of finance as technology progresses.

Digital transformation is crucial to any company’s operations. The adoption of mobile internet has resulted in a better-informed civic society. Cloud computing has lowered scaling complexity and matched digital infrastructure costs. Blockchain, AI/ML, IoT, big data, and 5G is acquiring business headway. The decentralized financial revolution could enhance the power of transactions’ fairness, openness, efficiency, and reliability. AI is changing education, healthcare, security, and agriculture. 5G will connect billions of gadgets, making homes, businesses, and factories “smarter” and improving data availability.

Digital finance pressurized the banks and insurers. Due to rising competition from Financial Technology companies, employers can reach out to more creative and young technical clients (Arner et al. 2015; Joshi 2020; Wang et al. 2021). Traditional financial intermediaries argue about managing Financial Technology and whether acquisitions or engaging those firms as service providers are compatible with their business models (Lai 2020; Suprun et al. 2020; Vučinić 2020). Technology allows them to remain competitive while delivering new and innovative customer offerings.

2. Literature Review

New financial goods, new financial services, new manufacturing methods, or new organizational structures are all examples of innovation in the financial sector (Frame and White 2004). It is an unavoidable consequence of the progress made in information technology regarding the financial sector. Banks, which serve as the foundation of the whole financial system, are constantly innovating new approaches to providing financial services. The growth of information technology assists banks in constructing a credit system, and innovations in communication technology make it possible for financial operations to take place regardless of physical location. Despite this, the research done so far has yet to be able to provide a definitive conclusion about the impact of financial innovation on banks. On the one hand, there is the traditional innovation-growth view, which posits that financial innovation increases the diversity of banking services (Berger 2002), strengthens banks’ risk-sharing ability and improves resource allocation efficiency. On the other hand, the ‘innovation-fragility’ hypothesis states that financial innovation improves banks’ ability to bear risks, which results in excessive credit expansion in financial markets and leads to financial crises. This hypothesis was developed in response to the ‘innovation-stability’ hypothesis, which was developed in response to the ‘innovation-stability’ hypothesis. According to Frame and White (2004), “Everyone speaks about financial innovation, but (nearly) nobody experimentally examines assumptions about it.” This is something that has been seen. Therefore, it is essential for a nation’s economic and financial development to be able to adapt the innovations in the financial sector by improving its operating performance, offering a wider variety of financial services at lower costs, and increasing the competitiveness of its industries. As a result, conducting research into the effects that financial innovation has on the operational efficiency of banks is of utmost importance both to the economy and to public policy. FinTech encompasses finance (crowdfunding, crowd lending, crowd investing), asset management (Robo advising, social trading, factoring), and payments (cryptocurrencies, alternative payment methods) (e.g., search engines, infrastructure providers). FinTech start-ups and market volume surged in all four categories in the past decade (Brandl and Hornuf 2020). As digitalization increasingly affects the financial services sector, financial technology and “Fintech” topics have received the increase attention (Nicoletti 2017; Leong and Sung 2018). Most financial services processes, such as trading on an online platform, are done online (Karagiannaki et al. 2017). Both financial service providers and their consumers must be digitalized to alter the value chain. The word “Fintech” comes from the phrase “financial technology.” Citicorp chairman John Reed probably coined the term in the early 1990s, when a new group called the “Smart Card Forum” started (Puschmann 2017). In the digital age, FinTech applications changed how we think about products to include new ecosystems. When designers of financial services focus on hybrid and incompatible ways for customers to interact with them, it can make some channels unnecessary (Gill et al. 2015). Bibliometrics is one of the most widely used quantitative methods in analyzing literature (Fairthorne 1969; Pritchard 1969). Hood and Wilson (2001), Osareh (1996a, 1996b), and Tsay (2005) found three bibliometric rules. Lotka’s law (Lotka 1926) is the earliest and oldest. It shows author-article links. Bradford’s law (Bradford 1934) involves placing scientific articles in distinct journals. Zipf (1949) about frequency. The basic aim of a bibliometric analysis is to collect previous literature and related topics on the underlying research subject to form objective findings that can be tested and replicated. It aims to both categorize previous studies and offer a rigorous methodological examination of the research results (Tepe et al. 2021).

3. Objectives

- To find the most influential authors in the Fintech field in banking and insurance.

- To find out which country does the most research in the Fintech domain in banking and insurance?

- To find out the gaps in Fintech Domain in banking and insurance.

4. Research Methodology

4.1. Data Collection

Despite the fact that digital finance is increasingly important and relevant, research in this domain is still in its infancy stage. Academic research on digital finance has only increased in recent years, and most publications are empirical research (Zou et al. 2023). Data were extracted from the Scopus database between the years 2017 and 2022. A total of 665 research publications were taken into consideration for this investigation. It was discovered that the Fintech industry gained momentum at the beginning of 2018, and much effort has been made so far because when we extracted data from the Scopus database, we found only 85 articles from 2008 to 2016, while in 2017, we found 114 articles, and in 2018 we found 305 documents, which is just a triple of the previous year.

PRISMA is an acronym for “Prevention and Recovery Information System for Monitoring and Analysis.” Figure 1 illustrates this acronym’s network. It assists us in defining how we have limited the articles, what screening factors are included, and how we recognize the research materials. Documents are reviewed for inclusion in the research at the very end. We have located 3403 research papers in the Scopus database that meet the criteria of year, publication stage, document type, keyword, topic area, and language. These records have been narrowed down using the characteristics mentioned earlier. Since the data were only obtained from 2017 to 2022, 83 publications are disqualified due to the year parameter. This is because papers published before 2017 are disqualified from consideration. We are only allowed to take into account complete articles that have been published and must disregard studies that are either in the communication stage or are currently being prepared for publication. This results in the elimination of 154 different papers. Articles were considered, and we eliminated patents, book chapters, and other documents. This resulted in the elimination of 1569 publications. We excluded 597 articles because of the author keyword; we were only interested in the FinTech keyword publications for our analysis. Because we were only regarded as being in business, economics, and social science, 318 articles were not accepted due to the topic area criteria. Since we were only interested in papers written in English at this level, we had to exclude 17 reports based on the language they were written in. As a result of the filtering out 3403 publications described above, 2738 papers were eliminated from consideration for this research, and we ended up focusing our efforts on 665 articles.

4.2. Methodology

This study employed a bibliometric approach using VOSviewer software, and biblioshiny using R Studio. It helps us to determine who is the most influential author is on a certain subject, and it will also assist scholars in identifying knowledge gaps (Aria and Cuccurullo 2017). Over the past five years, the bibliometric approach has gained popularity. It can be used to conduct systematic literature reviews, the foundation of any good research. It also enables us to determine the country-by-country research conducted on a specific topic and assists countries still needing such a study. For this research topic, the importance is helping people understand secondary data and existing research.

5. Result Analysis and Interpretation

5.1. Descriptive Statistics

Elsevier’s Scopus database is mined for collecting published research papers on financial technology (FinTech). As can be seen in Table 1, there were 665 research papers spread out for six years. In this part, numerical expressions are applied to describe the database used for bibliometric analysis or previous studies on a subject pertaining to FinTech. In addition, the earlier publication is shown in Figure 2. In the year 2017, there were 15 articles published; in the year 2018, there were 54 pieces published; in 2019, there were 61 articles published; in 2020, there were 160 articles published; in 2021, there were 180 articles published; and in 2022, there were 173 articles published. The Year 2020 onwards, there was a boom in research paper publication in FinTech areas because during these years, there was much technological advancement that changed the operation of businesses and every other industry because everyone wanted to take advantage of this advancement and do work in a simple and sophisticated manner. In addition, there was much technological advancement that changed the operation of businesses and every other industry because there was a lot of technological advancement that changed the operation of businesses. During the COVID-19 epidemic, we saw the rapid development of technology in India in the form of virtual meetings, digital payments, digital campaigning, and many other examples.

5.2. Documents Per Year by Source

We found documents per year by source from 2017 to 2022. As can be seen in Figure 3, Sustainability Switzerland and Technology Forecasting and Social Change have a maximum of 22 papers. The Financial Research Letter Journal has 17 documents from 2017 to 2022 in the Fintech domain. Electronic Commerce Research and Application and Financial Innovation both have 14 articles. These were the prominent journals in the Fintech domain. It was noticed that Financial Innovation and Electronic Ecommerce Research and Applications were the oldest journals. In contrast, Financial Research Letter, Technological Forecasting, and Social Change started functioning in the year 2020 onwards.

5.3. Author Wise Publication and Author Network

The author-wise articles and author network are displayed in Figure 4 and Figure 5, respectively. The authors with the most research articles in the FinTech field are Wojcik, D., Barber, H, & Ozili, P. K., with the most vital total links. The authors above must be cited in future studies by researchers who wish to work in Fintech. Prospective researchers get good insight while reviewing these prominent authors’ works. It helps them to understand the subject in a better way and think about the methodology of their study.

5.4. Country Wise Publication

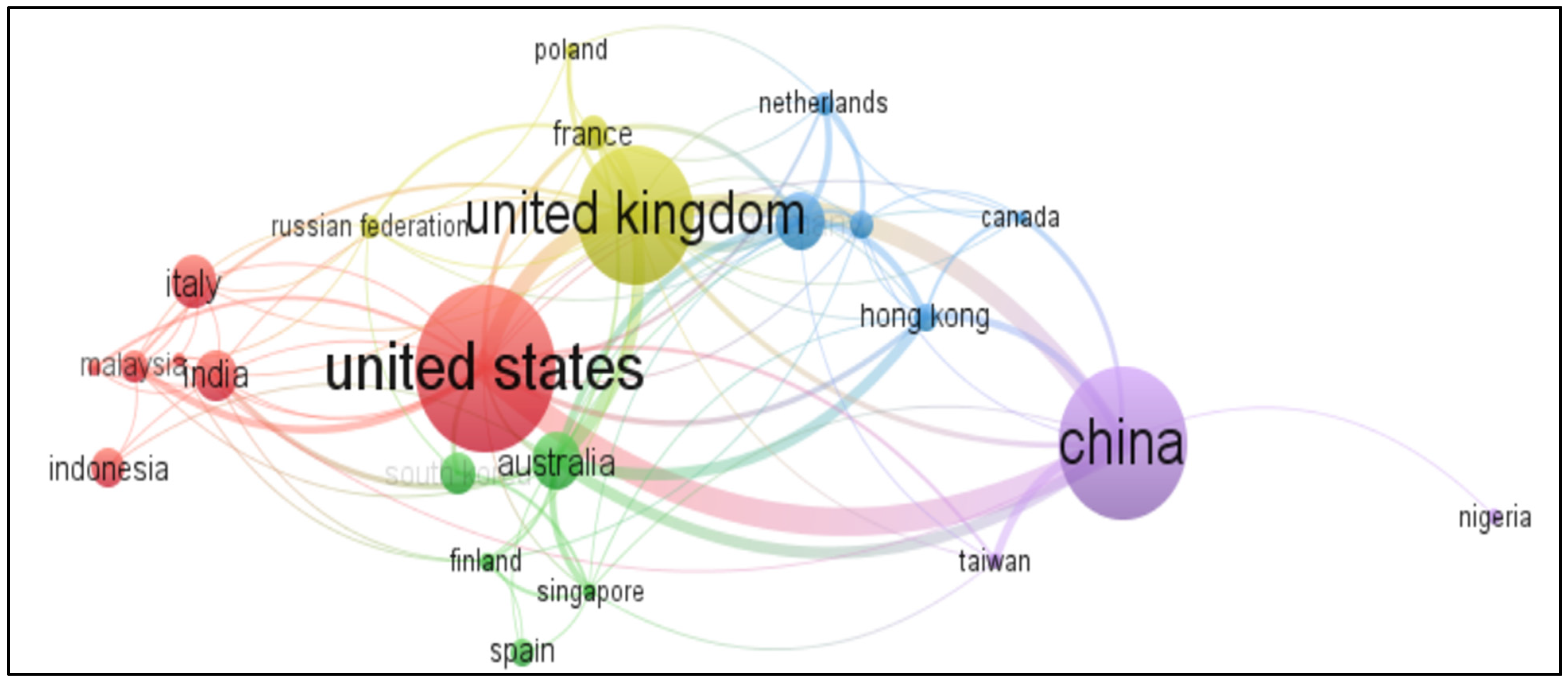

The United States has the most articles published on FinTech, totalling 108 as mentioned in Figure 6. It also has the most citations of any country globally, with 2078. China is the second in the number of articles, while the United Kingdom is the second in the number of citations. India is in the seventh place when it comes to the number of articles. A total of five clusters were found country-wise in the network. In the first cluster, the United States, India, Indonesia, Italy, and Malaysia worked together on the FinTech area, and there was a collaboration among the authors of these countries. In the second cluster, the United Kingdom, France, Poland, and Russia worked together and cooperated as mentioned in Figure 7; the authors were very excited about their work. In the third cluster, China, Taiwan, and Nigeria work together. In the fourth cluster, Hong Kong, Canada, and the Netherlands worked together, and there was a lot of potential for further work in these FinTech areas. In the fifth cluster, Australia, Finland, Singapore, and Spain are working together, and much potential is also available there.

5.5. Citation

Table 2 and Figure 8 show citations and citations network. We have found that Author Gomber P has the most citations, 547, and has two articles in the FinTech field. The author R. J. Kauffman has four articles in the FinTech domain, which puts him in second place in terms of citations. If one wants to do research in the FinTech field, he/she should look at the articles of the author listed above. There are other authors as well.

5.6. Keywords

We have conducted the co-occurrence analysis using the author keywords and identified seven main clusters of FinTech literature, as shown in Figure 9. It shows that Fintech appears 506 times overall under author keywords, which is the most and has the most robust total links. Financial technology, financial inclusion, and blockchain appeared 84, 63, and 58 times, respectively. The researcher can identify research gaps using the keywords network. Digital lending, supply chain finance, the internet of things, and Robo advisors all have much room for more study. Keyword network diagrams assist researchers in identifying barren research areas.

5.7. Affiliation

Figure 10 displays papers by affiliation and reveals that the University of New South Wales, Sydney has the most research articles in the FinTech area, followed by the University of Hong Kong with eight research articles. These allowed potential researchers to connect with the university and research with them.

5.8. Documents by Funding Sponsor

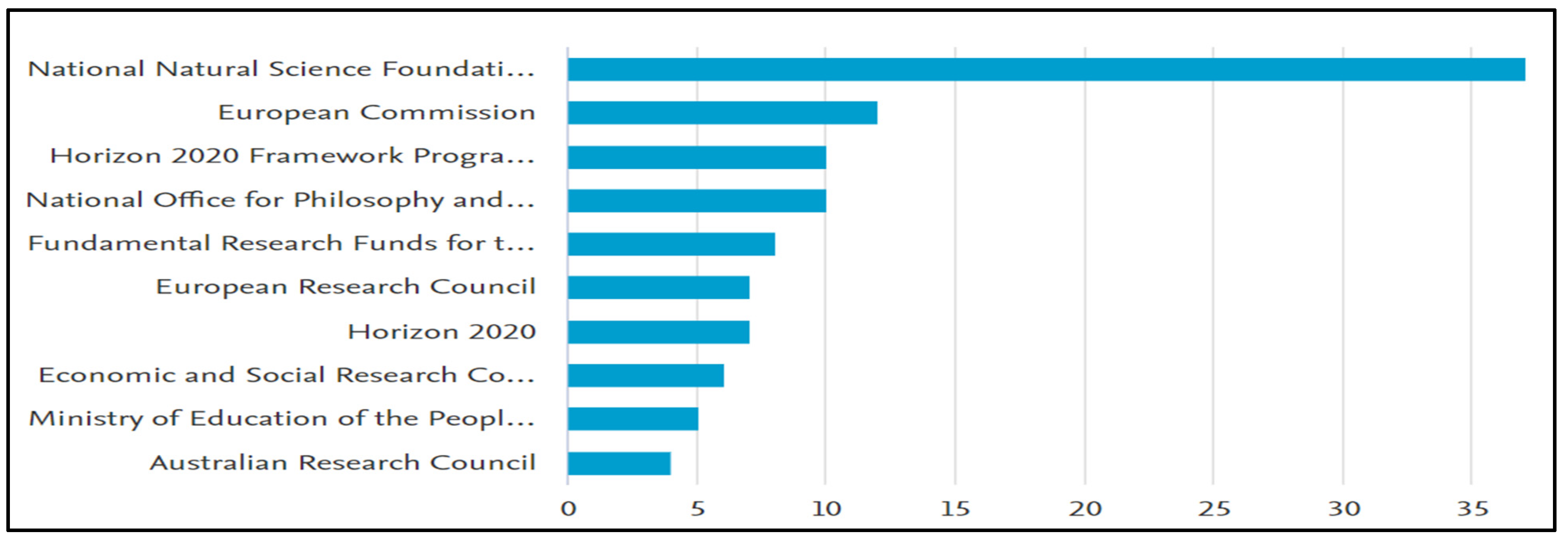

Figure 11 displays documents by funding source. The National Natural Science Foundation of China financed a maximum of 37 research articles in the FinTech domain, whereas the European Commission funded a total of 13 research articles. Researchers who wish to undertake FinTech-related topics will submit funding proposals to these organizations. Now, reputable journals need a hefty article publishing price (APC), making it difficult for researchers to publish in reputable journals.

5.9. Different Types of Indexes

Table 3 shows different types of indexes. Technological Forecasting and Social Change have the highest H-index and G-index, which have a value of 12 and 21 respectively. The H index measures how many documents have been published, and how many times they have been cited. It denotes the reputation of a journal. The G-index is the unique largest number such that the top G articles received at least G2 citations.

5.10. Bradford’s Law

Figure 12 shows Bradford’s Law defines the statistical distribution of scientific or technical knowledge in an area. The Bradford core, a small group of journals, will have the most publications on a subject, while a more extensive group will have fewer. In 1934, British librarian Samuel C. Bradford created the legislation. Bradford observed the logarithmic distribution of articles in his 1933 citation research. He found that the number of journals publishing papers in an area was generally related to the number of pieces. Still, the number of journals needed to account for a certain percentage of articles declined as the proportion rose. It was found that Sustainability Switzerland has the highest reputed journal in the FinTech domain.

5.11. Lotka’s Law

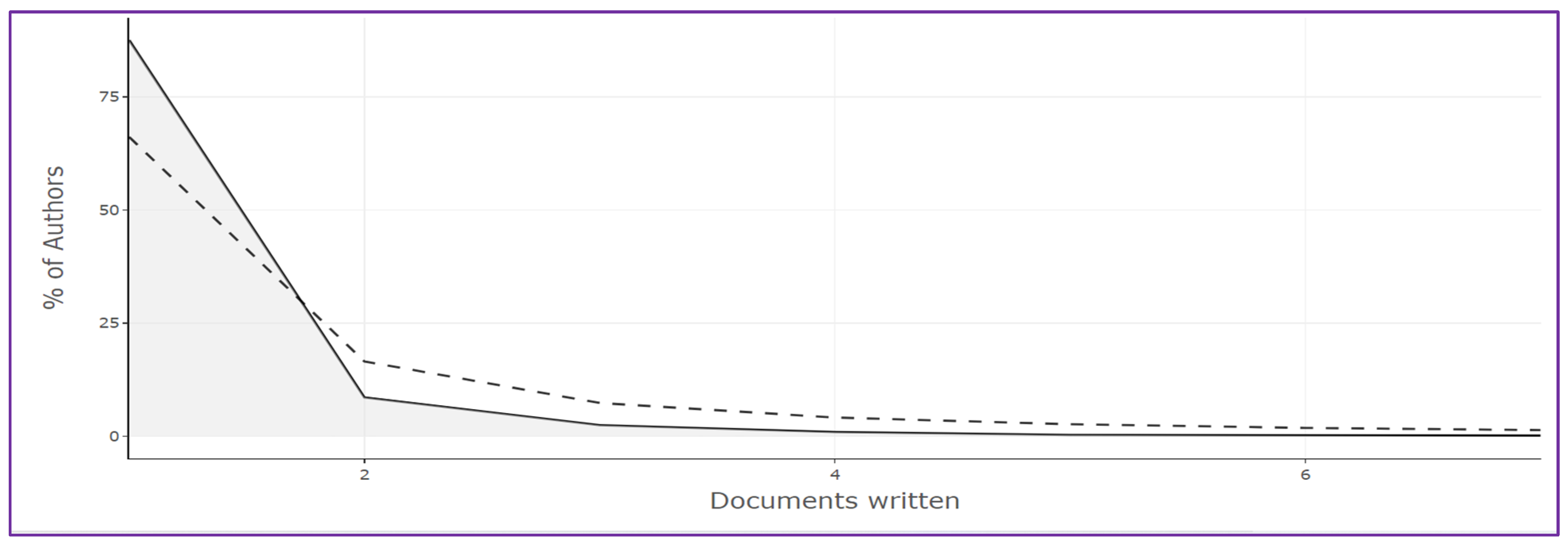

Figure 13 shows the Lotka’s law which describes the frequency of publication by authors in any given field. It was found that an author published on average two research papers on FinTech domain. Lotka’s Law states that the number of authors who have published one article is proportional to 1/n2, the number who have published two papers is proportional to 1/n3, and so on. As the number of publications grows, the number of authors who have published that number falls exponentially. Physics, biology, and social sciences all follow this rule. It can also measure a scientific community’s production and anticipate new writers. The rule is based on statistical observations and does not account for individual research interests, talent, or opportunity. We show the best fit for a power law distribution with sloid black line and power law with cutoff by dotted black line.

5.12. World Map

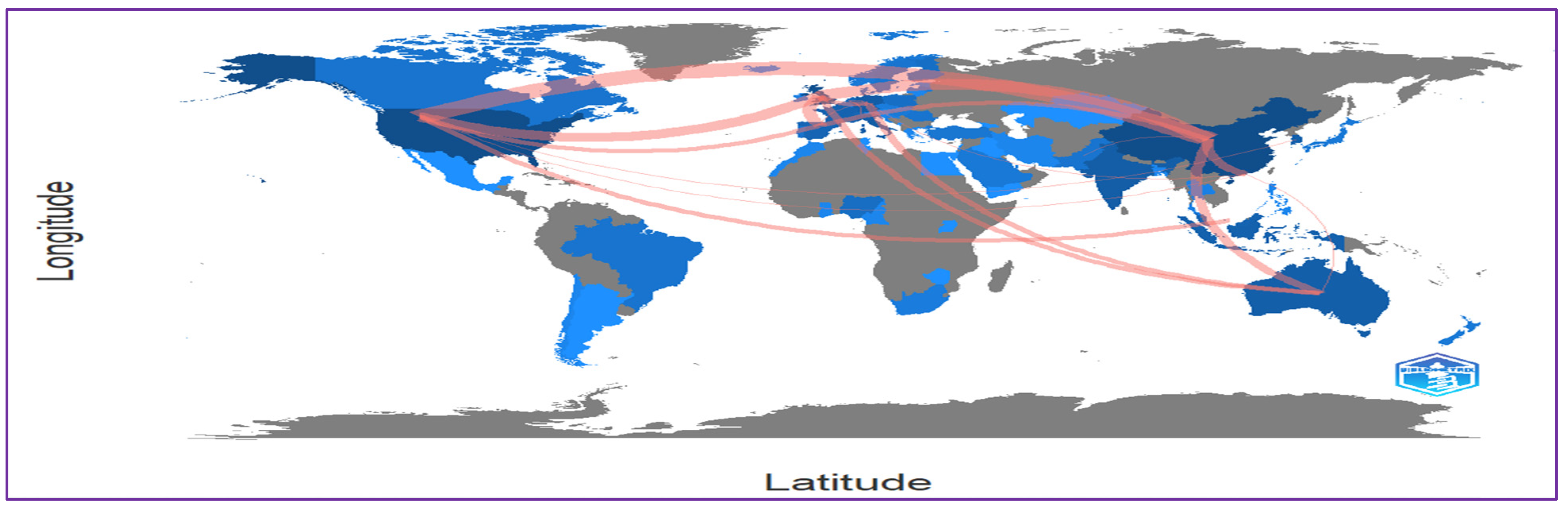

Figure 14 shows a collaboration world map, and it was found that the USA and China have maximum collaboration in the FinTech domain. The USA also partners with Australia, European countries, and India. Using a collaborative world map in the bibliometric analysis may provide a mechanism to investigate the geographical distribution of research publications or citations visibly and interactively. This may assist you in locating new options for study, avenues for cooperation, and sources of financing. Collaboration globe maps can also compare research projects in different countries or regions. By mapping where research papers or citations come from, you can reach the activity levels in other places. This allows you to identify areas in which additional research is required.

6. Conclusions

Researchers benefit from bibliometric analysis by learning which authors, countries, organisations, financial sponsors, and keywords are most often used in the literature around a certain issue. All of these features are being used in the current studies by the researchers. Using bibliometric analysis, they learn about emerging tendencies and patterns in the studied subjects. It provides a basis for the creation of new theoretical frameworks and statistical tools for authors. Bibliometric analysis has gained prominence in the past decade, and numerous studies have been published using this methodology. It aids in comprehending essential factors in any particular research subject. In this study, we identified the significant authors and countries with the help of citation and co-citation analyses that have conducted research in the FinTech industry. These two items also fulfilled the study’s first two objectives. It was found that the consequences of FinTech are full of controversies, which are part of broader, long-standing debates on the role of finance in the economy and society and need to be approached from geographical perspectives. The intense fusion of finance and technology, arguably accelerated by the COVID-19 pandemic, complicates and elevates these controversies to a new level. The co-occurrence analysis enables us to identify research gaps in the FinTech domain. The third goal is also met, and there exists much scope in the area of Digital Lending, Supply Chain Finance, the Internet of Things, and Robo Advisers.

7. Limitations

This research paper is based on information taken from the Scopus database, so it did not look at other well-known journals outside the Scopus database. Here, we focus on FinTech that can be used in business, finance, and insurance. However, many multidisciplinary journals have published research articles in all fields excluded from this study. We limited ourselves to Vosviewer and Biblioshiny software for co-citation analysis, co-occurrence analysis, and network diagrams, while many other software options are available.

8. Implications

Bibliometric analysis is a quantitative method for analysing publication patterns, citations, and collaboration in scientific literature. It has numerous implications for the evaluation and management of scientific research. Bibliometric analysis can evaluate the impact of research and individual researchers by analysing their publication and citation records. This method can also identify highly cited papers and influential researchers in a specific field. Bibliometric analysis can help identify research trends and the development of scientific fields over time. It can be helpful for policymakers, funding agencies, and researchers to make informed decisions about research funding and direction.

Additionally, bibliometric analysis can provide insights into the structure and dynamics of research networks by identifying patterns of collaboration and co-authorship between researchers and institutions. This method can help measure the productivity of researchers and institutions by analyzing their publications output over time and identifying gaps in research, such as under-researched topics or areas where there needs to be more consensus or conflicting results. Finally, bibliometric analysis can provide valuable information for strategic decision-making in research institutions, funding agencies, and governments, informing decisions about research priorities, funding allocation, and developing new research programs.

Author Contributions

Conceptualization, G.G., M.S., M.I.T.; methodology, G.G., B.H., M.I.T.; software, G.G., L.N.D.; validation, G.G., M.S. and N.G.; formal analysis, M.I.T.; investigation, B.H.; resources, L.N.D.; data curation, G.G.; writing—original draft preparation, G.G.; writing—review and editing, M.I.T., G.G., B.H.; visualization, G.G., L.N.D. All authors have read and agreed to the published version of the manuscript.

Funding

This research received no external funding.

Informed Consent Statement

Not applicable.

Data Availability Statement

Data is available based on reasonable request.

Conflicts of Interest

The authors declare no conflict of interest.

References

- Anjum, Muhammad Naeem, Xiuchun Bi, Jaffar Abbas, and Shuguang Zhang. 2017. Analyzing predictors of customer satisfaction and assessment of retail banking problems in Pakistan. Cogent Business & Management 4: 1338842. [Google Scholar] [CrossRef]

- Aria, Massimo, and Corrado Cuccurullo. 2017. Bibliometrix: An R-tool for comprehensive science mapping analysis. Journal of Informetrics 11: 959–75. [Google Scholar] [CrossRef]

- Arner, Douglas W., Janos Nathan Barberis, and Ross P. Buckley. 2015. The Evolution of Fintech: A New Post-Crisis Paradigm? SSRN Electronic Journal 47: 1271. [Google Scholar] [CrossRef] [Green Version]

- Azizi, Mohammad Reza, Rasha Atlasi, Arash Ziapour, Jaffar Abbas, and Roya Naemi. 2021. Innovative Human Resource Management Strategies during the COVID-19 Pandemic: A Systematic Narrative Review Approach. Heliyon 7: e07233. [Google Scholar] [CrossRef]

- Berger, Allen N. 2002. The Economic Effects of Technological Progress: Evidence from the Banking Industry. SSRN Electronic Journal 35: 141–76. [Google Scholar] [CrossRef] [Green Version]

- Bradford, S. C. 1934. Sources of Information on Specific Subjects. Engineering 137: 85–86. [Google Scholar]

- Brandl, Barbara, and Lars Hornuf. 2020. Where Did FinTechs Come From, and Where Do They Go? The Transformation of the Financial Industry in Germany After Digitalization. Frontiers in Artificial Intelligence 3: 8. [Google Scholar] [CrossRef] [Green Version]

- Chen, You-Shyang, Chien-Ku Lin, Yu-Sheng Lin, Su-Fen Chen, and Huei-Hua Tsao. 2022. Identification of Potential Valid Clients for a Sustainable Insurance Policy Using an Advanced Mixed Classification Model. Sustainability 14: 3964. [Google Scholar] [CrossRef]

- Fairthorne, Robert A. 1969. Empirical Hyperbolic Distributions (Bradford-Zipf-Mandelbrot) for Bibliometric Description and Prediction. Journal of Documentation 25: 319–43. [Google Scholar] [CrossRef]

- Frame, W. Scott, and Lawrence J. White. 2004. Empirical Studies of Financial Innovation: Lots of Talk, Little Action? Journal of Economic Literature 42: 116–44. [Google Scholar] [CrossRef] [Green Version]

- Gill, Asif, Deborah Bunker, and Philip Seltsikas. 2015. Moving Forward: Emerging Themes in Financial Services Technologies’ Adoption. Communications of the Association for Information Systems 36: 12. [Google Scholar] [CrossRef]

- Gomber, Peter, Jascha-Alexander Koch, and Michael Siering. 2017. Digital Finance and FinTech: Current research and future research directions. Journal of Business Economics 87: 537–80. [Google Scholar] [CrossRef]

- Hood, William W., and Concepción S. Wilson. 2001. The Literature of Bibliometrics, Scientometrics, and Informetrics. Scientometrics. Scientometrics 52: 291–314. [Google Scholar] [CrossRef]

- Joshi, Vasant Chintaman. 2020. Digital Finance, Bits and Bytes. Singapore: Springer. [Google Scholar]

- Kanungo, Rama Prasad, and Suraksha Gupta. 2021. Financial inclusion through digitalisation of services for well-being. Technological Forecasting and Social Change 167: 120721. [Google Scholar] [CrossRef]

- Karagiannaki, Angeliki, Georgios Vergados, and Konstantinos Fouskas. 2017. The Impact of Digital Transformation in the Financial Services Industry: Insights from an Open Innovation Initiative in Fintech in Greece. Paper presented at the Mediterranean Conference on Information Proceedings 2. (MICS), Genoa, Italy, September 4–5; Available online: http://aisel.aisnet.org/mcis2017/2 (accessed on 15 February 2023).

- Lai, K. P. Y. 2020. FinTech. In The Routledge Handbook of Financial Geography. Abingdon-on-Thames: Routledge, pp. 440–57. [Google Scholar] [CrossRef]

- Leong, Kelvin, and and Anna Sung. 2018. FinTech (Financial Technology): What is It and How to Use Technologies to Create Business Value in Fintech Way? International Journal of Innovation, Management and Technology 9: 74–78. [Google Scholar] [CrossRef]

- Li, Bo, and Zeshui Xu. 2021. Insights into financial technology (FinTech): A bibliometric and visual study. Financial Innovation 7: 69. [Google Scholar] [CrossRef]

- Lotka, Alfred J. 1926. The Frequency Distribution of Scientific Productivity. Journal of Washington Academic and Science 16: 317–23. [Google Scholar]

- Nicoletti, Bernardo. 2017. Future of FinTech. Basingstoke: Palgrave Macmillan. [Google Scholar]

- Osareh, Farideh. 1996a. Bibliometrics, Citation Analysis and Co-Citation Analysis: A Review of Literature I. Libri 46: 149–58. [Google Scholar] [CrossRef]

- Osareh, Farideh. 1996b. Bibliometrics, Citation Anatysis and Co-Citation Analysis: A Review of Literature II. Libri 46: 217–25. [Google Scholar] [CrossRef]

- Ozili, Peterson K. 2018. Impact of digital finance on financial inclusion and stability. Borsa Istanbul Review 18: 329–40. [Google Scholar] [CrossRef]

- Pritchard, A. 1969. Statistical Bibliography or Bibliometrics. Journal of Documentation 25: 348–49. [Google Scholar]

- Puschmann, Thomas. 2017. Fintech. Business & Information Systems Engineering 59: 69–76. [Google Scholar] [CrossRef]

- Shao, Min, Wenxin Jiang, and Chao Ma. 2022. Research on Internet Use and Family Commercial Health Insurance Purchase Behavior: Evidence from China. Paper presented at the ICMSSE 2022, AHCS 12, Chongqing, China, December 12; pp. 374–80. [Google Scholar] [CrossRef]

- Suprun, Anatoly, Tetiana Petrishina, and Iryna Vasylchuk. 2020. Competition and cooperation between fintech companies and traditional financial institutions. E3S Web of Conferences 166: 13028. [Google Scholar] [CrossRef]

- Tepe, Gencay, Umut Burak Geyikci, and Fatih Mehmet Sancak. 2021. FinTech Companies: A Bibliometric Analysis. International Journal of Financial Studies 10: 2. [Google Scholar] [CrossRef]

- Tsay, R. S. 2005. Analysis of Financial Time Series, 3rd ed. Hoboken: John Wiley and Sons. [Google Scholar]

- Vučinić, Milena. 2020. Fintech and Financial Stability Potential Influence of FinTech on Financial Stability, Risks and Benefits. Journal of Central Banking Theory and Practice 9: 43–66. [Google Scholar] [CrossRef]

- Wang, Chunlei, Dake Wang, Jaffar Abbas, Kaifeng Duan, and Riaqa Mubeen. 2021. Global Financial Crisis, Smart Lockdown Strategies, and the COVID-19 Spillover Impacts: A Global Perspective Implications from Southeast Asia. Frontiers in Psychiatry 12: 643783. [Google Scholar] [CrossRef]

- Zarifis, Alex, and Xusen Cheng. 2021. Evaluating the new AI and data driven insurance business models for incumbents and disruptors: Is there convergence? Paper presented at the 24th International Conference on Business Information Systems (BIS 2021), Hannover, Germany, June 15–17; pp. 199–208. [Google Scholar]

- Zarifis, Alex, Peter Kawalek, and Aida Azadegan. 2021. Evaluating if trust and personal information privacy concerns are barriers to using health insurance that explicitly utilizes AI. Journal of Internet Commerce 20: 66–83. [Google Scholar] [CrossRef]

- Zipf, George Kingsley. 1949. Human Behavior and the Principle of Least Effort. Boston: Addison-Wesley Press. [Google Scholar]

- Zou, Zongsen, Xindi Liu, Meng Wang, and Xinze Yang. 2023. Insight into digital finance and fintech: A bibliometric and content analysis. Technology in Society 73: 102221. [Google Scholar] [CrossRef]

Figure 1.

PRISMA Flow Chart. Source: Author’s Contribution.

Figure 2.

Documents Year Wise. Source: Author’s Contribution.

Figure 3.

Documents per year by source. Source: Author’s Contribution.

Figure 4.

Documents by Author. Source: Author’s Contribution.

Figure 5.

Author Network. Source: Author’s Contribution.

Figure 6.

Country-wise Publication. Source: Author’s Contribution.

Figure 7.

Country-wise network. Source: Author’s Contribution.

Figure 8.

Citation Network. Source: Author’s Contribution.

Figure 9.

Keywords Network. Source: Author’s Contribution.

Figure 10.

Documents by Affiliation. Source: Author’s Contribution.

Figure 11.

Documents by Funding Sponsor. Source: Author’s Contribution.

Figure 12.

Clustering through Bradford’s Law. Source: Author’s Contribution.

Figure 13.

Author Productivity through Lotka’s Law. Source: Author’s Contribution.

Figure 14.

Collaboration World Map. Source: Author’s Contribution.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Table 1.

Citation.

| Author | Documents | Citations | Total Link Strength |

|---|---|---|---|

| Gomber P. | 2 | 547 | 75 |

| Kauffman R.J. | 4 | 357 | 42 |

| Shin Y.J. | 2 | 303 | 58 |

| Ozili P.K. | 5 | 212 | 18 |

| Giudici G. | 2 | 208 | 26 |

| Martinazzi S. | 2 | 208 | 26 |

| Brooks’ S. | 2 | 200 | 23 |

| Hornuf L. | 2 | 154 | 35 |

| Tan B. | 5 | 139 | 52 |

| Sun Y. | 4 | 130 | 48 |

| Leong C. | 3 | 126 | 42 |

| Tan F.T.C. | 2 | 126 | 36 |

| Jagtiani J. | 5 | 124 | 53 |

| Lemieux C. | 2 | 113 | 47 |

| Langley P. | 2 | 108 | 15 |

| Leyshon A. | 2 | 108 | 15 |

| Rabbani M.R. | 6 | 107 | 18 |

| Chang V. | 3 | 106 | 4 |

| Belanche D. | 2 | 103 | 6 |

| Casaló L.V. | 2 | 103 | 6 |

Source: Author’s Contribution.

Table 2.

Keywords.

| Keyword | Occurrences | Total Link Strength |

|---|---|---|

| Fintech | 506 | 1783 |

| Blockchain | 84 | 382 |

| Financial Inclusion | 63 | 260 |

| Financial Technology | 58 | 201 |

| Finance | 51 | 301 |

| Financial Services | 47 | 269 |

| Banking | 46 | 265 |

| Innovation | 45 | 279 |

| Artificial Intelligence | 40 | 193 |

| China | 37 | 180 |

| Cryptocurrency | 37 | 161 |

| Bitcoin | 32 | 135 |

| Crowdfunding | 32 | 127 |

| Financial Market | 27 | 182 |

| Big Data | 24 | 99 |

| Financial System | 22 | 174 |

| Regtech | 22 | 93 |

| Peer-to-Peer Lending | 21 | 81 |

| Technology | 20 | 109 |

| COVID-19 | 18 | 67 |

Source: Author’s Contribution.

Table 3.

Different Types of Indexes.

| Element | H-Index | G-Index |

|---|---|---|

| TECHNOLOGICAL FORECASTING AND SOCIAL CHANGE | 12 | 21 |

| SUSTAINABILITY (SWITZERLAND) | 10 | 14 |

| ELECTRONIC COMMERCE RESEARCH AND APPLICATIONS | 9 | 13 |

| JOURNAL OF OPEN INNOVATION: TECHNOLOGY, MARKET, AND COMPLEXITY | 7 | 8 |

| ENVIRONMENT AND PLANNING A | 6 | 6 |

| EUROPEAN BUSINESS ORGANIZATION LAW REVIEW | 6 | 9 |

| FINANCIAL INNOVATION | 6 | 10 |

| INDUSTRIAL MANAGEMENT AND DATA SYSTEMS | 6 | 8 |

| FINANCE RESEARCH LETTERS | 5 | 9 |

| ELECTRONIC MARKETS | 4 | 4 |

Source: Author’s Contribution.

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Garg, G.; Shamshad, M.; Gauhar, N.; Tabash, M.I.; Hamouri, B.; Daniel, L.N. A Bibliometric Analysis of Fintech Trends: An Empirical Investigation. Int. J. Financial Stud. 2023, 11, 79. https://doi.org/10.3390/ijfs11020079

AMA Style

Garg G, Shamshad M, Gauhar N, Tabash MI, Hamouri B, Daniel LN. A Bibliometric Analysis of Fintech Trends: An Empirical Investigation. International Journal of Financial Studies. 2023; 11(2):79. https://doi.org/10.3390/ijfs11020079

Chicago/Turabian StyleGarg, Girish, Mohd Shamshad, Nikita Gauhar, Mosab I. Tabash, Basem Hamouri, and Linda Nalini Daniel. 2023. "A Bibliometric Analysis of Fintech Trends: An Empirical Investigation" International Journal of Financial Studies 11, no. 2: 79. https://doi.org/10.3390/ijfs11020079

Note that from the first issue of 2016, this journal uses article numbers instead of page numbers. See further details here.