Integrated Supervision of the Financial Market without the UK?

Law Faculty, Masaryk University, Brno 611 80, Czech Republic

Int. J. Financial Stud. 2018, 6(1), 20; https://doi.org/10.3390/ijfs6010020

Submission received: 8 December 2017

/

Revised: 20 January 2018

/

Accepted: 25 January 2018

/

Published: 9 February 2018

(This article belongs to the Special Issue Financial Economics)

Abstract

:This paper analyses the integration of financial market supervision at international level, particularly focusing on EU law and the actual processes taking place in this area considering Brexit as its part. Current legislative action at EU level has a significant impact on legislation in all member countries of European Union. This paper seeks, among other things, to find the causes of the increasingly ongoing process of integration of financial market supervision and determine whether or not the direction in which the international integration is going is the right one. The objective of this paper is to determine whether or not the process of integration increases the efficiency of financial market supervision itself and helps to develop the European single market, while simultaneously reducing systemic risk to financial market stability.

JEL Classification:

K221. Introduction

The aim of this article is not merely to analyze the current status of financial market supervision, but is also to propose a possible outcome to the current process that could happen in the near future to adjust supervision of the financial market. Financial system development in recent decades has brought numerous new products, possibilities and ways of operating with financial instruments within the financial market. One of the obvious results of this development is the globalization of the financial market. In the author’s opinion, there are no longer any local or national financial markets; the majority is at supranational level. In Europe, this is already the well established and could be described as the supranational financial market, which functions alongside the existence of a banking union. The banking union is quite a new project and remains still not yet fully operational, but already leads the way of supervision within Europe. There is an interesting question of where Brexit will leave the economic status of the EU, including financial market supervision of the UK. Is it going to assume the position of another country in the agreement of the European Economic Area (the EEA)1 besides Norway, Iceland and Lichtenstein, or something else?

2. Beginning of Integrated Supervision

This section is divided by subheadings. It will provide a concise and precise description of experimental results, their interpretation as well as the experimental conclusions that can be drawn. Banking union is an institutional and functional response to the financial crisis experienced since 2008. Banking union was preceded by another reform known as the European System of Financial Supervision2 (ESFS) where the single market was presented as one of the goals of the European Union. One of the key resources for operational functioning of the single market is single and centralized supervision.3 Centralized supervision is built upon two levels of supervision—macroprudential and microprudential. The goal of macroprudential supervision/code of practice is the stability of the EU financial system with soft law (non-binding competences, recommendations etc.). The aim of microprudential supervision, on the other hand, is operation with legally binding decision-making competences.4

Macroprudential supervision is represented by the European Systemic Risk Board (ESRB). Microprudential supervision is represented by the European Supervisory Authorities (ESAs), which means that this supervisory pillar is not carried out by a set of EU bodies.

2.1. Macroprudential Supervision

The ESRB is an EU-level body responsible for macroprudential supervision. The ESRB’s mission is to prevent, or at least mitigate, systemic risks that threaten to disrupt financial stability (Verhelst 2011).

This organization is based on Article 114 of the Treaty of the Functioning of the European Union (TFEU). It is not a European agency, as it has no legal status and no legal authority. It is something akin to a soft-law organization with a good reputation influencing recipients by means of its decisions or recommendations.

It must be established that the structure, staff and proceedings of the ESRB are such that they instill confidence in its ability to: (a) make independent judgments; (b) produce high-quality analyses; and (c) reach sharp, clear conclusions (Goldby and Keller 2010).

This unit collects and analyses relevant information and data from all EU member countries and evaluates such information for the purpose of identifying systemic risks. The most useful tools are warnings and recommendations issued by the ESBR when needed. They are addressed to the EU as a whole or to one or more member states, ESAs, or national supervisory authorities, and recommendations are addressed specifically to the European Commission. As mentioned previously, none of the tools used by the ESRB are legally binding, but recommendations operate through an “act or explain”5 and “naming and shaming”6 mechanism, aiming at compliance. These mechanisms serve the aim that addressees concur with recommendations. If they do not, they have to provide substantive reasons for deviation from the ESBR recommendation (in certain cases in the public domain) (Ferran and Alexander 2011).

Rising private sector debt may also trigger a fiscal bailout that spills over to peripheral Euro-area countries, even if the government had very low government debt before the bailout (for example, Spain). In such a case, more scrutiny by a centralized financial supervision can be crucial, only that this time it would concentrate on macro and systemic risk (as the macroprudential supervision so far attached to the ECB in the form of ESRB) (Blessing 2013). The centralization of financial supervision is the key point to prevent systemic risk, although systemic risk itself will never vanish completely.

The disadvantage of the ESBR is the fact that its data sources come from local national databases and some countries might not wish to admit some irregularity of the system or individual institutions. The possible problem for confirming the high reputation of the ESBR could be the problem of identifying threats. In cases where the threat is not identified or is assessed incorrectly, consequences similar to those brought about out by the financial crisis might occur. On the other hand, threats that are not real might be identified. Every single false warning might cause a reduction in credibility and reputation, because most of the accepted warnings bring extra costs for some of the competing financial institutions. This is just a question of sensitive application for the ESBR, which must deal with the situation successfully.

2.2. Microprudential Supervision

The European Supervisory Authorities are probably the most important part of the ESFS. The responsibility of the ESAs has increased significantly and received defined, legally binding tools, greater autonomy and broader competence as a result of reform (Rodriguez 2009).

The ESAs consist of three supervisory agencies,7 the Joint Committee of the ESA and the Board of Appeal. All three ESAs agencies have practically the same organizational structure: (a) Board of Supervisors; (b) Management Board; (c) Chairperson; (d) Executive Director; (e) Joint Committee; (f) Board of Appeal (The Joint Committee and the Board of Appeal operate within the ESA in an institutionalized form, as a common unit of the ESA); and (g) Stakeholder groups.8

The three European Supervisory Authorities have rule-making, decision-making and supervisory powers, but the ESMA is the only agency with direct enforcement powers over (private) financial market participants (Scholten and Luchtman 2017).9

The main decision-making body is the Board of Supervisors, whose members hold the right to vote and are the chairmen of national supervisors who decide by simple majority. Because of the large number of members of this body, it is not sufficiently operational, and for this reason, there is an executive body, the Management Board, within which operates a chairman and six other members. The Management Board is the main bearer and executor of the objectives and tasks entrusted to the ESA. Members of the Board of Supervisors with a voting right are the ones who are elected from among themselves, the members of the Management Board as well as the Chairperson and Executive Director of the ESAs. In this manner, through the chairmen of the national supervisory authorities, member states are an influence in their decision-making.

When mention is made of the ESAs’ competences, it is very important to clarify that these agencies do not work as day-to-day supervisory bodies of financial institutions. This task remains in the hands of national supervisors.10 The ESAs operate with soft-law instruments and legally binding authority. All the ESAs have very similar tasks; only ESMA has the one extra competence of forbidding certain financial activities when necessary.

The particular tasks and tools of the ESAs could be divided into 3 sections (see Table 1 bellow). Those are quasi-regulatory competences, supervisory competences and legally binding decisions in the form of law enforcement. The fundamental focus of the ESAs is precisely on having this third group of tools at their disposal. As such, these tools are the essential factors that have brought about this reform of supervision.

2.3. Single Rulebook

One of the main objectives of the ESAs is to work on the single rulebook. ESA Regulation does not define exactly what is meant by such a code. The Council of Ministers described the single rulebook as a basic set of rules and standards across the EU that are directly applicable to all financial institutions operating in the single market (Council of the European Union 2009). However the fact remains that even this statement is not an unequivocal determinant of what a single rulebook is, and for this reason there is ample room for interpretation by the ESAs, who, on the other hand, can also generate contradictions between supervisors.

However, the single rulebook does not include a complete harmonization of the rules applicable to financial institutions that should lead to less contradictory financial legislation in all member states. This results in fewer opportunities to resolve regulatory dispute (regulatory arbitrage)11 and a reduction in gold-plating12 issues (Verhelst 2011).

In general, supervisory practices vary from one member state to another and regulatory arbitrage arises in cases when a contradiction between member states brings efficiency losses for a single market. The ESAs should, therefore, have the necessary powers to effectively coordinate supervisory actions carried out by national supervisory authorities both when authorizing or registering an undertaking and as part of an ongoing review of supervisory practices.

A possible solution for avoiding regulatory arbitrage is to centralize powers in the hands of ESAs. One of the first steps could be found in the enforcement powers of the ESMA’s for credit rating agencies (CRAs) and trade repositories (TRs). When there are more financial market institutions under the direct supervision of ESAs, there is no place for conflicting legislation in Member states. One possible way could be seen in the new proposed practice of ESMA considering certain types of prospectuses with a cross-border dimension, where their approval is centralized at the level of the ESMA.13 The centralization of their approval, as well as all related supervisory and enforcement activities at the level of the ESMA, will enhance the quality, consistency and efficiency of supervision in the union, create a level playing field for issuers and lead to a reduction of the timeline for approvals. It will eliminate the need to choose a “Home Member State” and prevent forum-shopping (European Parliament 2017).

The other possible solution is to produce more detailed harmonization of the rules applicable to financial institutions for the single rulebook. These rules should allow less space for conflicting financial legislation in member states and therefore fewer regulatory arbitrages.

ESAs have two tools to reach the goals mentioned above. The first tool is non-binding regulatory recommendations and guidelines.14 An ESA can address these recommendations and guidelines to national supervisors as well as individual financial institutions. These recipients should comply with such recommendations and guidelines. In cases where they fail to do so, it is necessary for the supervisor to sufficiently justify such action. However, this only applies to financial institutions and only if the recommendation or guideline explicitly expresses such a request.

The second tool is the regulation and implementation of technical standards.15 Implementing standards ensures uniform implementation of EU law without legislative changes. Regulatory standards supplement or amend legislation, but only elements that are non-essential.16

ESAs make “only” draft standards for the European Commission, which is the body that decides on their approval. By the same token, the recommendations and guidelines are not legally binding, and from this we can deduce its “quasi” nature, because ESAs do not in fact have regulative competences.17

On the other hand, the ability of the European Commission in relation to draft standards is limited in terms of their change. The European Commission may intervene in drafts only if ESAs fail to provide adequate drafts within the stipulated deadline. In practice, the Commission only endorses the drafts of ESAs in exceptional cases, and that therefore gives added value to the quasi-regulative competence of ESAs.

It follows from the above that the drafts of technical standards have a greater impact on the harmonization of legislation in the financial market than guidelines and recommendations (as a soft-law tool). At first sight, quasi-regulative competences seem almost powerless, but upon closer examination, it is indeed a regulative competence. In particular, the fact that, in the case of ESAs technical standards drafts, the European Commission practically does not interfere shows that the entity that forms these standards is currently the ESAs.

The ESFS could be seen as a real initial step to the single market with single and unified supervision, which has followed the banking union. It is one of the reactions to/consequences of the financial crisis of 2008. For legal and political reasons, only competencies that allow direct intervention in the operation of the financial market were endowed as a last resort for intervention in this first step of creating new supervisory bodies (which have been created within the ESFS).

A result that had come from the establishment of the ESFS brought the maximum possible effect achievable at that time. It was the first “curtailment” of some degree of sovereignty and exclusive powers of the supervisory authorities of member states. As such, a new direction can then move forward and supervisory powers could be even further (but not entirely) centralized, in the name of “public interest”.

However, the current model of sector supervision of three European supervisory authorities could be changed in order to achieve better coordination and cooperation of ESAs sectors. The one-peak model could be more beneficial than just merging supervision over credit institutions and insurance companies (the twin-peak model) due to possible improvements in the coordination of ESAs’ work and outputs, the deepening interdependence of individual financial market segments and potential savings of the ESAs’ activities.

In general, ESAs’ priority should focus on resolving real problems and ambiguities regarding the implementation of new regulations; but on the other hand, it should also be an authority with more centralized power over the financial market to be able to act as a supranational authority in certain cases. Only this could bring efficiency of supervision in the single market.

3. Banking Union

The process of integration of financial market supervision could be described as a process of changes in the supervisory system of the financial market as a response to the financial crisis. The first step for system changes was analyzed above, based on the Larosiér report. This step was a preparatory stage for real integration. The legal power of ESFS authorities has been greatly reduced, and the direct application of competences conferred on the ongoing activities in the financial market were perceived as final and somewhat extreme solutions. However, the first step was a major impetus for dynamic, real and direct supervision at the European level. The reform of the supervision system proceeds to the second step, which already leads to the formation of direct supervision implemented at the European level, which is referred to as a banking union.

As the financial crisis evolved and turned into the Eurozone debt crisis, it became apparent that a deeper integration of the banking system was necessary for countries that shared the Euro and were even more interdependent. Consequently, on the basis of the European Commission roadmap for the creation of a banking union, the EU institutions agreed to establish a Single Supervisory Mechanism and a Single Resolution Mechanism for banks. The banking union applies to countries in the Euro area. Non-Euro-area countries may join as well.

Prior to the creation of the banking union, prudential rules took place at the level of the local supervisory agencies, and this led to the diversity in supervision among the member states. The internal financial market was thus prevented from being realized, with the real possibility easing potential risks (Wyemersch 2012). The banking union is thus potentially a much stronger move towards the integration of financial market supervision.

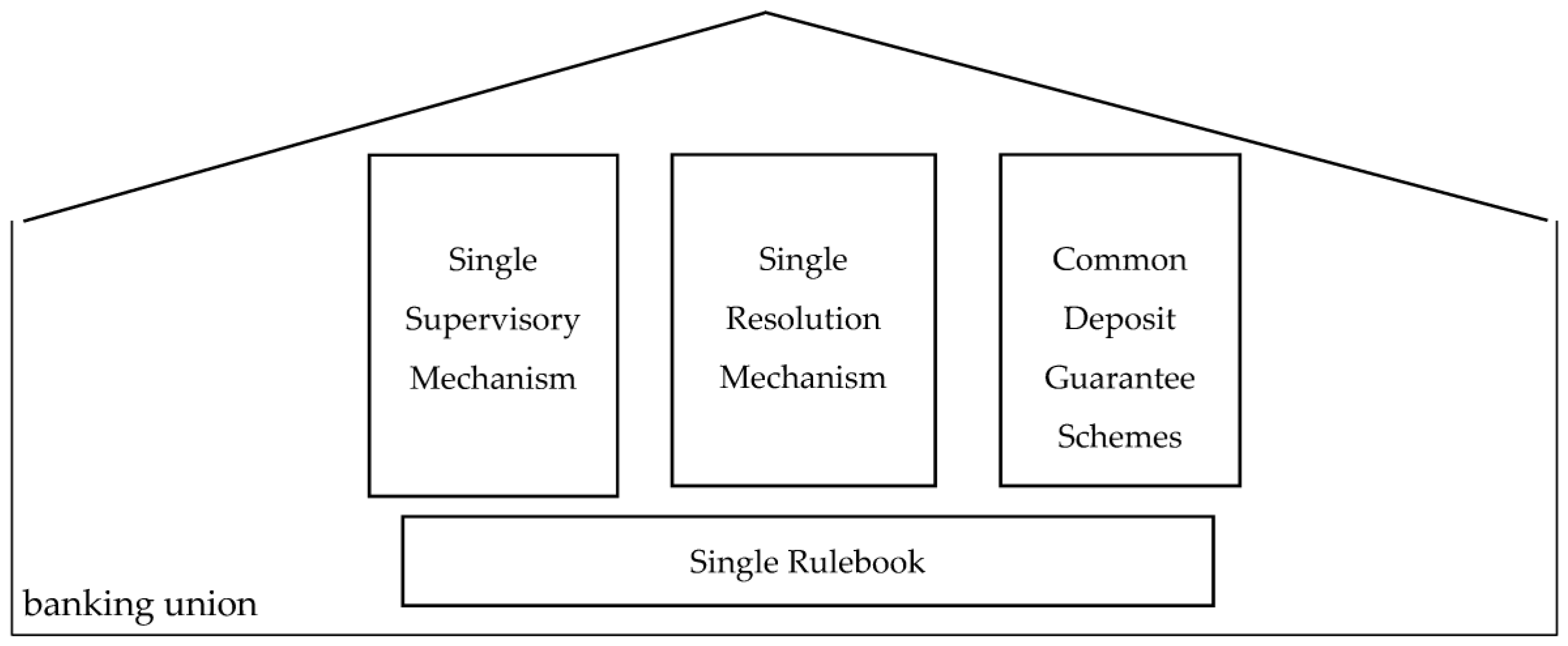

The banking union is essentially an integrated financial framework resting upon three pillars. The first pillar is the Single Supervisory Mechanism (SSM), the second is the Single Resolution Mechanism (SRM), and finally, the third pillar is the Common Deposit Guarantee Scheme (CDGS), which is based on several European directives and regulations.18

These three pillars are supplemented by a single rulebook that provides a single set of harmonized prudential rules that need be respected by all institutions within the EU. It is then a unified aggregate of norms for the banking sector. It consists of Union regulations and directives accompanied by harmonizing and implementing technical norms approved by the European Commission and prepared by the EBA (Kalman 2014).

In the author’s opinion, the prudential rules of the single rulebook are evident in several areas of the banking union. They include the capital requirements for banking institutions (in particular, the CRR, CRD IV, and Basel III), the aim of which is to strengthen the ability of the EU banking sector to survive periods of economic uncertainty, to improve risk management, and to ensure standard lending during periods of economic recession. They also include recovery and resolution mechanisms for the crisis management of credit institutions according to the BRRD Directive. Last but not least, there is also a system of deposit insurance, which is compulsory for all EU member states. All the rules are accompanied by technical norms (the RTS and the ITS) drawn up by the EBA and approved by the European Commission, along with general rules of the EBA and supplementary documents. These are arguably the most important European rules applied in all EU countries (i.e., not only in the Eurozone or just the banking union). Needless to say, the single aggregate of rules is one method of ensuring consistent application of the legislative framework for banking regulation across the EU. Ideally, it should ultimately bring about financial (economic) stability within the EU.

The author does not consider the single rulebook as another (fourth) pillar of the banking union;19 it seems to be a structure of rules that are applicable inside as well as outside the three established pillars of the banking union (see Scheme 1 bellow).

The purpose of this article is not to go deeply into each of the three pillars of the banking union. The fundamental reason is that this topic is too broad and should be the subject of a separate article. The substance of this article is a review of the relationship between EU and non-Eurozone countries and non-EU countries. It is topical at the time of Brexit, when nothing is sure and all actions in this matter will be carried out for the first time in history of the EU. What are the consequences and outcomes of these relationships?

3.1. Banking Union and Non-Eurozone Countries

Eurozone countries are those with a fully operational banking union; together with some specific parts and “details” of the second pillar, the first pillar is most relevant for these countries.

3.1.1. Area of Single Supervisory Mechanism

The Single Supervisory Mechanism (SSM) proposition presumed that the complete banking system of the Eurozone countries will be realized under the direct supervision of the ECB, which would, however, have been unacceptable for the majority of the countries involved. There was a compromise to be arrived at—the direct supervision of the ECB will be realized only over systemically important financial institutions, or rather important20 credit institutions (banks), which, however, cover over 85% of the banking assets21 in the Eurozone by means of 123 banking groups (Nouy 2015) anyway. Supervision over the other banks will be carried out by national supervisory authorities with the option to delegate the power to the ECB, if it accepts it. The EU emergency funds are supposed to offer help directly to banks in trouble, and the ECB assumes the main supervisory tasks such as granting and revoking the license, supervising risk transactions, issuing directives and recommendations, issuing binding decisions along with effective supervision, monitoring and enforcing the observation of capital requirements for banks according to the CRD Directives,22 performing supervision on a consolidated basis and sharing supplementary supervisory tasks through financial conglomerates. The ECB also possesses a relatively wide range of investigative competence, as it can impose administrative sanctions, assess mergers and credit institutions acquisitions.23

National supervisory authorities are responsible for the less important supervisory tasks such as day-by-day supervision, consumer protection, supervision over money laundering, payment services and setting up branches from third countries—they must comply with the directives and regulations issued by the ECB.

The EBA also plays an important role under the SSM, because it ensures effective and consistent implementation of the single set of rules in the banking sector. Moreover, it co-prepares stress testing for banks carried out by the ECB, which co-ordinates stress testing in the entire EU.

3.1.2. Area of Single Resolution Mechanism

The participants of the second pillar are basically all EU countries, but the main important difference could be found in the Single Resolution Fund (SRF), which is set up for Eurozone countries and their national funds. Countries out of the Eurozone collect a contribution from credit institutions to their own national resolution funds, and when there is a need to start a resolution mechanism, it gets financial support only from this national source. The question to be asked here is what is better, more operative and reasonable in a case in which a resolution mechanism is started.

This authority—SRF is financed by banking institutions—and its creation will last for eight years (i.e., it is completion is planned for 2024). Every year, the participating countries should pay one-eighth of the total amount attributable to each country. The funds available in the SRF should reach at least 1 % of the covered deposits of all credit institutions of the banking union members. It is expected that the fund will have about 55 billion EUR at its disposal. The individual contributions of each credit institution is calculated according to the ratio between the total amount of its liabilities (excluding the capital and covered deposits) and the aggregate liabilities (again excluding the capital and covered deposits) of all the credit institutions authorized in the participating member states. The calculation process will also take into consideration the risks taken by the given institution (European Council 2014).

The contributions from credit institutions will be received by the participating member states through their national funds and then transferred to the SRF, which will be activated. The finance can only be used if the principles stipulated in the BRRD Directive and the SRM Regulation are observed and if shareholders and private creditors take part in the recovery plans. During the eight-year transition period, these national funds should gradually merge while the contributions collected by each national fund will be shared as well. This transfer and sharing of finance from the national resolution funds is regulated by the above-mentioned Intergovernmental Agreement (the IGA). Before the SRF has enough financial means, the system of financing is ensured during the transition period by means of domestic funds based on banking contributions, alternatively from the European Stability Mechanism. Another option is to transfer the money from one national resolution fund to another; if that happens, the help is financed from the banking sector contributions.

Since the beginning of 2016, one-eighth of the contributions has been transferred to the SRF. All countries participating in banking union have contributed, with the exception of Portugal, Spain, Greece and Italy. These countries have no money in their national funds due to the fact that they have financed the recovery of their local banks (mostly a prohibited way of part bail-out financing). A decision as to what the next step for the European Commission will be has not been reached yet; in the author’s view, there is no other option for the Commission but to take legal action against these countries if they fail to transfer the money even in the extra time provided.

This is maybe one of the negative points of the supranational Single Resolution Fund in cases where there are no contributions from some countries. The solidarity and motivation might not be very stable in these situations for countries that contribute properly when they realize that some countries simply do not. The national fund might be bit faster in activation, but on the other hand it is just smaller.

Besides these facts, the author does not have any other opinion about the positives and negatives of the supranational fund as compared to national ones, because some years of practice with these funds are needed to find out what might be a smarter solution for a resolution.

3.1.3. General Part

The possibility of entering the voluntarily banking union for non-Eurozone countries should be mentioned as well. Romania and Bulgaria will do so, and Denmark has declared it as well.

What are the main differences for non-Eurozone countries in comparison with Eurozone ones?

By entering the banking union, the author means primarily centralized supervision, especially for major credit institutions, from participating states associated, inter alia, with a major administrative shift of supervision. Entering the banking union voluntarily will bring about the transfer of substantial supervision agenda to the capacity of the ECB, i.e., it will result in a so-called regime of close cooperation between the national supervisor and the ECB. This shift of supervision would apply particularly to important credit institutions whose supervision would take over the ECB. The supervision of smaller credit institutions would be kept by a national supervisor, but it would have to follow the instructions and regulations of the ECB, to ensure a coherent approach to supervision in all countries with an emphasis on the period of potential instability. If a non-Eurozone country enters a banking union before it becomes part of the Eurozone, the ECB will conduct supervision through a national supervisory authority, because the ECB has no direct competence in relation to institutions outside the Eurozone. This also means that any country that is not in the Eurozone must produce adequate legislative measures to ensure that the national supervisory authority will be able to comply with the ECB measures and adopt these measures.

From the political point of view, the benefit of entering a banking union comes along with an official declaration of participation in the euro integration. This could subsequently result in a higher potential in promoting national strategic interests at the EU level, and it would also strengthen the competitiveness of local credit institutions in the European financial market. Other more general contributions should consist in strengthening the stability of the local financial markets.

The main reason for the “holding attitude” of non-entering the SSM is a fear of losing supervisory powers over large credit institutions. There is also a potential increase in the risk of the spread of financial instability to the local subsidiaries of international holdings without an effective possibility for the national supervisory authority to perform and adopt its own solution. One of the other reasons is mandatory participation in financing the supervision of the ECB.

There are some other more political aspects together with the holding position of most of the non-Eurozone countries, because they all wait for and see what is going to happen and whether some positive outcome will be proven. It is all still very new and untested.

On the other hand, the fear of international financial instability spreading is not the real reason. It is complete nonsense to have a stable financial market at the local level when there is instability in an important part of the EU, because there is nothing resembling a local financial market anymore. The financial market is very international and so interconnected, and institutions operating in different countries are fundamentally linked to their parent companies. That is the reason why the single supervisory mechanism is the most important and primary one. Local—the daily supervision of the functioning of the individual subsidiary entities and affiliates—is still very important, but it is a secondary concern from a global point of view.

3.2. Financial Market of EU and EFTA Countries

There are a few reasons why the author has chosen this article comparison of the relation between the EU and three non-EU countries in this area. These three countries are member states of the Agreement on the European Economic Area24 (the EEA) and also participate in the European Free Trade Association25 (the EFTA).

One of the reasons is that Norway is the first European country to have introduced integrated supervision over the financial market, so it is interesting to find out whether their pioneering decision brought about any particularities or differences in comparison with the method or the system of supervision in the EU. Moreover, Norwegian banks are very busy in cross-border business with EU members, particularly in Scandinavia. The Financial Stability Board list mentions Nordea26 as a global systemically important bank. These reasons, including the closely intertwined business relations, make the relation between the EFTA and the EU worthwhile.

Because of the existence of the Agreement on the EEA and because of the fact that the single financial market evidently falls within the four freedoms this agreement helps to establish, it is clear that financial market regulation and supervision in all EFTA countries is legislatively extremely similar to the system in the EU—in fact, they are based on it.

Essentially, the EU regulations become part of the legal system of EFTA countries only after they have become integrated into the agreement on the EEA. All supervisory authorities in these countries are part of the EFTA Working Group on Financial Services, which is a group coordinating the opinions of EFTA countries on the integration of basic financial legal norms into the Agreement on the EEA.

The basic tenet of the Agreement on the EEA is its flexibility and, to a certain extent, homogeneity with the EU single market. Amendments that are made to EU legislation and are relevant to the EEA are gradually implemented into the Agreement on the EEA via the decisions of the EEA Joint Committee27 and the subsequent ratification of these decisions in national legal systems. Since 1994, more than 7000 EU legal regulations have been implemented in this way (Fredriksen and Franklin 2015). For example, it is immensely interesting that the legal system in Norway is very pragmatic as far as foreign languages and legislation are concerned—a large number of EU regulations become part of Norwegian law even before they have been translated into the Norwegian language.28

All EFTA countries participate in EU authorities, such as the highly relevant ESA authorities. The reason is that the secondary legislation of the EU (which is, among other things, produced by the ESA authorities) is incorporated into the EEA Agreement through a rather complicated procedure in case the legislation is relevant to the principles and rules stipulated in the Agreement (in other words, if it is EEA relevant). There is no denying that in the financial market area, most regulations are EEA relevant—they then get through the EEA Agreement into the legal system of EFTA countries.

In the financial market area, the co-operation between EFTA countries and the EU is extremely close, since both parties are keen to make sure that the operation of the financial market is as effective as possible. The ESA authorities are essentially fundamental European authorities producing relevant regulations and the fact that EFTA countries do not have the full membership of these authorities causes considerable problems. These authorities adopt various EEA relevant decisions and regulations that are later adopted by EFTA countries as well, but, crucially, they have no fully-fledged representative there (it only has a kind of an observer), and it therefore cannot voice its opinion regarding the adopted acts—the capacity of EFTA representatives is solely advisory. Another obstacle is the fact that once the EEA Joint Committee decides to implement an act into the EEA Agreement, it must then be adopted via the legislative procedure into national law—Constitutions of EFTA countries do not allow for any other option. Such a process of implementation is rather awkward, and it causes a great many problems. The biggest problem, however, is the delay in implementing EU acts in the EEA Agreement and, subsequently, into individual national legal systems—this may lead to considerable overload on the EEA Joint Committee; more often than not, the delay is caused by one country that obstructs or intentionally impedes the process of transposition in the EEA Joint Committee.29 EFTA countries have attempted to solve the problem several times by accepting unilateral transposition of some regulations into their national legal systems, but these are nothing more than provisional solutions with a rather unclear legal foundation.30

The easiest option is the acceptance of EFTA countries’ representatives as fully-fledged members of the ESA authorities, including a voting and decision-making right. From the perspective of constitutional law, this enables the possibility to transfer the sovereignty to authorities that could be accepted as joint EEA authorities (Fredriksen and Franklin 2015).31

This solution appears to have been applied on 30 September 2016, when the EEA Joint Committee decided to implement the directives establishing the ESA Authorities (EBA, EIOPA, ESMA and the ESBR)32; that problem left EFTA countries in a tight spot to a certain extent. However, the parallel structures (the EU and the EEA) created problems not only for EFTA countries, but also for the financial institutions of the countries that conduct business with EFTA countries.

In June 2017, the EEA Joint Committee adopted a package of decisions to incorporate 31 EU legal norms establishing the European Financial Supervisory Authorities, including the regulations establishing ESA authorities.

The issues surrounding the EEA Agreement and European legislation (and its implementation in EFTA countries) is naturally a much deeper phenomenon that far exceeds the scope of this article.

It seems that the solution to the most pressing problem outlined above has perhaps been found. The solution should be acceptable to all EEA Agreement members.

I am certain that there was no possible solution other than to make the representatives of EFTA countries equal to their European counterparts in order to prevent any delays in the transposition of EU norms into national legal systems while enabling EFTA representatives to take part in the very creation of these norms (issued by authorities such as the ESA). However, secondary problems of the constitutional orders of EFTA countries fall under the competence of individual countries—so they need to tackle the problem of setting the system of accepting EU norms when its members have become fully-fledged members of the ESA authorities.

All EEA Agreement countries are interested in a fully operational single market to which the EEA Agreement contributes; that is why all parties involved (including the EU member countries) benefit from co-operation being as effective as possible also at the EEA level. I am certain that the close cooperation and the relatively prompt implementation of the EEA relevant regulations bring Europe (closer) to a single market.

As far as EU supervisory colleges are concerned, what is worth pointing out is the intersection of EU law with Norwegian supervision, for Finanstilsynet33 is the main supervisory authority in the DNB supervisory college—the DNB is a Norwegian bank operating internationally, including the EU (the majority shareholder is the state, which is an enormous advantage given the bank’s rating). The main task of the college is the preparation of a common assessment of risk and capital for the entire DNB Group, and the college is also responsible for the application of recovery plans that deal with capital adequacy and liquidity failures and proposing measures in compliance with the BRRD Directive. Recovery plans and their application must be assessed by the college, which may result in further comments and statements. Also, this supervisory authority is involved in nine supervisory colleges for foreign banks active in Norway.

Here we can see the evident interconnection between member and non-member EU countries. The financial market (and its institutions) is so interconnected internationally that the question of whether or not a specific country is an EU member is not of such great importance—a financial institution licensed in a country such as that is usually active in other countries as well, and that is why it is beneficial to cooperate internationally and to unify supervisory rules to a certain extent. In this case, a supervisory authority outside the EU is the main authority in one supervisory college and a member of other supervisory colleges whose other members are predominantly from the EU, which brings about the acceptance and harmonization of EU rules in a non-EU zone as well. The crucial aspect is the existence of the EEA Agreement between EFTA and EU countries, which means that most financial market regulations are EEA relevant; as a consequence, EFTA countries are obliged to implement such regulations into their own legal systems.

3.3. EFTA—EU Summary

The EEA Agreement34 defines the form and mechanism of acceptance and subsequent application of EU norms and regulations in the law of EFTA countries (if they are EEA relevant). The legislation of these countries includes widely transposed EU legislation (since it is mostly EEA relevant), which is yet further proof of international harmonization (even outside the EU) and the importance of a Europe-wide (not just EU-wide) single market. We might say that a national financial market does not really exist (given the intertwined international structure of the economy and the financial market being a part of it as well); hence the need to perceive the financial market as a global entity comprised of national financial markets. The author is sure that any other method of regulation and supervision35 in member or non-member countries is neither suitable nor feasible, because at present, a national financial market cannot operate in a way that is isolated from the financial markets in other countries. EFTA countries contribute not only to their own financial stability, but also to international financial stability due to the high number of supranational interconnections in the financial market that simply fail to respect borders, whether they be those of the EU, Europe, or indeed, the entire world.

The above-mentioned statement is basically the author’s opinion based on an international point of view of the economy. Financial institutions play a very important role in the economic system and systemically important institutions are those with cross-border activities. There is no border for these institutions, just administrative barriers, which should be removed (if possible) when the single market is the goal.

4. Conclusions

Even in its current, incomplete form, the banking union presents a radical change that profoundly modifies the nature of European integration and the balance between member states and European institutions. Its full impact has yet to be appreciated, as there is a complex mixture of healthy skepticism, misguided cynicism and indolent inattention (Veron 2015). The internal market is the real goal for the integration of the financial market, and supervision integration is only one aspect of this. In recent years, significant progress towards this goal has been achieved in the project of the banking union and its single supervision mechanism and single resolution mechanism.

The basis of the banking union can be seen in the 2013–2014 European legislation. The first step was the assessment of 130 banks in the Eurozone and the subsequent takeover of the basic supervisory authority by the ECB on 4 November 2014. The process through which supervision is to be transitioned is incomplete as of yet, and it is thus currently very difficult to assess the banking union; any attempt to do so must inevitably be rather premature. The process reached its peak in January 2016—the resolution board acquired the power to issue binding decisions, including the discretionary power to impose a specific resolution instrument; furthermore, the bail-in instrument of the BRRD Directive became applicable: the instrument that makes shareholders, creditors and uninsured depositors carry the burden of financial loss of an insolvent bank. Even after this date, it will take some time before things settle down and we can assess the structural organization of the banking Union. Moreover, a supranational single resolution fund is still being built from the original form of equal national resolution funds—this process should be completed by 2024. Although the process of building the banking union started three years ago, it is still in its early stages.

In a way, every financial crisis (or even an unpleasant situation) purifies the system from undesirable features. How negative the impact of a crisis seems to be a question of legislation, preventive measures and public attitude towards it. What it surely brings about is a reaction in the form of new instruments and measures that aim to cushion the damage that has been already caused and to prevent such a crisis in the future. This chapter on the European integration of regulation and supervision leading to the foundation of the banking union describes processes that clearly exemplify it. The banking union is by far the deepest and most comprehensive legal framework of the entire financial market, not only in terms of regulation and supervision. As to its imperfections, one example is the lack of a fiscal union in the EU. Such a union would bring the single market project much closer to its ultimate goal.

It is not yet possible to evaluate the banking union and its effectiveness, and it will remain as such at least until the SSM and the SRM become fully operational and until they are given sufficient time to show the results of their activities. The trend that had been set before the banking union was established has now intensified thanks to the banking union and its involvement in the area of regulation and supervision of financial institutions—the issue to be resolved is the ideal proportion of regulation and supervision in relation to the administrative demands and expenses of financial institutions, which is then reflected in the services and their prices (e.g., banking fees). In the area of supervision and regulation, we have not witnessed any liberalization attempts; i.e., attempts that would make legislation less strict, at least. Is it at all possible that we see a complete reversal of the trend though? In the authors mind, general liberalization of supervision and regulation is not really viable; yet, I the author am convinced that legislation will stabilize itself as the effects of the recent financial crisis wear off and economic growth becomes positively stable. It is uncertain whether this stabilization will come after the banking union becomes fully operational; the author presumes that it will take a little longer and probably “only” until another crisis arises—this crisis will inevitably happen, but we might feel optimistic that its impact will be much less severe.

It is going to be very interesting to monitor upcoming actions connected with Brexit in relation to the banking union. The UK is not part of the Eurozone, so the SSM is not very relevant, but SRM is in some aspects. The UK, however, proceeds in accordance with the Single Resolution Authority, and the National Resolution Fund fills up in the same way as the other member states. Formally, the UK is still part of the EU, and individual obligations must be respected.

The future is, however, very uncertain and still unpredictable, and it is also very possible that the UK will join the current EFTA countries with economic collaboration (no longer politically) with the EU. When the UK becomes one of the EFTA countries, some of the issues in EFTA countries under the EEA Agreement mentioned above will become topical for the UK.

What are the other options for the UK from the economic point of view? One of them is certainly a complex group of multilateral contracts with the EU or other countries, similar to Switzerland. There are some differences compared to the EEA Agreement, but basically, the goal is the same—easier cross-border economic collaboration. The costs of this might be higher (longer administration procedure including acceptance and implementation of the local government), but there should be greater legislative freedom.

The other option that was recently raised is Nafta (North American Free Trade Agreement), but in the author’s opinion, it would not make sense to join Nafta given that the UK is geographically somewhere else. What could the advantage of such an agreement be? It is hard to find any, especially in a situation where the reality and future of Nafta is very unstable.

The question regarding economic collaboration between the EU and the UK is not “if at all”, but rather “how and when”.

However, this is unlikely to be known until the UK leaving of the EU becomes a final fact and reality. Then, we might find the way for economic collaboration and a legal framework between the EU and the UK. It is certainly needed for both parties. Based on the author’s opinion, the best solution for both parties is a situation in which the UK becomes an EFTA country, and that is the reason why an important part of this article deals with EFTA countries and the EEA Agreement.

A very fitting comment was made by Jurgen Habermas, who said: “Without a common financial and economic policy, the national economies of pseudo-sovereign member states will continue to drift apart in terms of productivity. No political community can sustain such tension in the long run. At the same time, by focusing on the avoidance of open conflict, the EU’s institutions are preventing the political initiatives necessary for expanding the currency union into a political union. Only the government leaders assembled in the European Council are in a position to act, but precisely they are the ones who are unable to act in the interest of a joint European community, because they think mainly of their national electorate. We are stuck in a political trap. […] Over the course of the crisis, the European executive has accrued more and more authority. Key decisions are being taken by the council, the commission and the ECB—in other words, the very institutions that are either insufficiently legitimated to take such decisions or lack any democratic basis. […] The currency union must gain the capacity to act at the supra-national level. In view of the chaotic political process triggered by the crisis in Greece, we can no longer afford to ignore the limits of the present method of intergovernmental compromise.” (Oltermann 2015).

This comment shows something what is much needed also for integrated financial supervision—centralized institutions must gain the real and full capacity to act at the supranational level. The author does not see any possible way other than the centralization of powers and competences in order to bring about a real single market with the same rules and same supervision within the EU.

In conclusion, the author would like to state that having carried out considerable research, he is now utterly convinced that the integration of supervision is a process tried and tested to a large extent over the years, and it is also the right trend in supervision in view of the interconnectedness of international financial markets. New activities in the EU (the creation of the banking union, in particular) represent more concentrated efforts to integrate supervision. It is still in it the early stages, and every detail has not been specified and successfully dealt with yet; it will also take some time before the banking union is in its final form and fully operational. Prior to that, it would be unfair and unprofessional to pass judgment. The author can still conclude that banking union is not the final and ultimate solution for complete and integrated supervision within the EU, but it is another step forward. So many competences were relocated from the national to the supranational level, and it was all unimaginable 20 years ago, so it means a lot, but still more competences must be centralized to fulfill the goal. The whole process of integrated supervision and the banking union must be completed with a common financial and economic policy directing towards political union. Probably only political union could justify the complete centralization of important competences to the supranational level.

One conclusion is very clear: integrated supervision without the UK is possible and Brexit does not change anything in the current process.

The reasons outlined above justify the continuation of the process not only in the EU, but also globally; it is in our best interests to keep supporting and developing the integration of financial market supervision and to keep harmonizing the practices and mechanisms of supervision. Ideally, all should actively participate in this process.

Conflicts of Interest

The author declares no conflict of interest.

References

- Blessing, Martin. 2013. Financial and Fiscal Stability beyond the Crisis Years: Two Paradigm Shifts and their Consequences. In Stability of the Financial System: Illusion or Feasible Concept? Edited by Andreas Dombret and Otto Lucius. Cheltenha: Edward Elgar Publishing. [Google Scholar]

- Council of the European Union. 2009. Agreed Council Conclusions on Strengthening EU Financial Supervision. Brussels: Council of the European Union, p. 5. [Google Scholar]

- Emmenegger, Susan. 2010. Procedural Consumer Protection and Financial Market Supervision. EUI Working Papers Law No. 2010/05. p. 7. Available online: http://papers.ssrn.com/sol3/papers.cfm?abstract_id=1616322 (accessed on 8 June 2017).

- European Parliament. 2017. Proposal for a Regulation of the European Parliament and of the Council. Com(2017) 536 final. Brussels 20.9.2017. Brussels: European Parliament, p. 8. [Google Scholar]

- Ferran, Eilis, and Kern Alexander. 2011. Can Soft Bodies Be Effective? Soft Systemic Risk Oversight Bodies and the Special Case of European System Risk Board. University of Cambridge Faculty of Law Research Paper No. 36/2011. pp. 30–64. Available online: http://papers.ssrn.com/sol3/papers.cfm?abstract_id=1676140 (accessed on 7 August 2017).

- Ferran, Eilis, and Valia S. G. Babis. 2013. The European Single Supervisory Mechanism. University of Cambridge Faculty of Law Research Paper 10/2013. Available online: http://ssrn.com/abstract=2224538 (accessed on 10 August 2017).

- Fredriksen, Halvard Haukeland, and Christian N. K. Franklin. 2015. Of pragmatism and principles: The EEA Agreement 20 years on. Common Market Law Review 52: 629–84. [Google Scholar]

- Goldby, Miriam, and Anat Keller. 2010. The Commission’s proposal for a new European Systemic Risk Board: An evolution. Law and Financial Market Review 4: 51. [Google Scholar] [CrossRef]

- House of Lords. 2009. The Future of EU Financial Regulation and Supervision, Volume I: Report. London: Authority of the House of Lords, p. 12. Available online: http://www.publications.parliament.uk/pa/ld200809/ldselect/ldeucom/106/10604.htm (accessed on 5 January 2017).

- Kalman, Janos. 2014. The reform of financial supervisory system of the European Union. International Relations Quarterly 5: 9. [Google Scholar]

- Moloney, Niamh. 2011. The European Securities and Markets Authority and institutional design for the EU financial market—A tale of two competences: Part (1) Rule-Making. European Business Organization Law Review 12: 41–86. [Google Scholar] [CrossRef]

- Niknejad, Mandana. 2014. European Union towards the Banking Union, Single Supervisory Mechanism and Challenges on the Road Ahead. European Journal of Legal Studies 7: 92–124. Available online: http://www.ejls.eu/15/186UK.htm (accessed on 25 May 2017).

- Norges Bank. 2012. Report from a Working Group Consisting of Representatives from Norges Bank, the Financial Supervisory Authority of Norway. Oslo: Finanstilsynet and the Ministry of Finance, p. 12. [Google Scholar]

- Nouy, Danièle. 2015. The European Banking Landscape—Initial Conclusions after Four Months of Joint Banking Supervision and the Main Challenges Ahead. Paper presented at ‘SZ Finance Day’ in Frankfurt, Frankfurt, Germany, 17 March. [Google Scholar]

- Oltermann, Philip. 2015. Jürgen Habermas’s Verdict on the EU/Greece Debt Deal—Full Transcript. THE GUARDIAN Interview with Habermas, J. Published 16th July. Available online: http://www.theguardian.com/commentisfree/2015/jul/16/jurgen-habermas-eu-greece-debt-deal (accessed on 17 January 2018).

- Pfalzer, Juliette J. W. 2014. Naming and shaming in financial market regulations: A violation of the presumption of innocence? Utrecht Law Review 10: 134–48. [Google Scholar] [CrossRef]

- Rodriguez, Pablo Iglesias. 2009. Towards a New European Financial Supervision Architecture. Columbia Journal of European Law Online 16: 1–6. Available online: http://papers.ssrn.com/sol3/papers.cfm?abstract_id=1518062 (accessed on 5 November 2017).

- Scholten, Miroslava, and Michiel Luchtman. 2017. Law Enforcement by EU Authorities: Implications for Political and Judicial Accountability. Cheltenham: Edward Elgar Publishing, p. 55. [Google Scholar]

- European Council. 2014. Single Resolution Mechanism. Available online: http://www.consilium.europa.eu/cs/policies/banking-union/single-resolution-mechanism/ (accessed on 6 June 2016).

- Tabellini, G. 2008. Why Did Bank Supervision Fail? The First Global Financial Crisis of the 21st Century. Vox Publication, Centre for Economic Policy Research, pp. 45–47. Available online: http://www.voxeu.org/sites/default/files/First_global_crisis.pdf (accessed on 29 June 2017).

- Tomsik, Vladimír. 2012. Banking Union: One Size Fits All? p. 13. Available online: http://www.cnb.cz/cs/verejnost/pro_media/konference_projevy/vystoupeni_projevy/download/tomsik_20121029_cep.pdf (accessed on 2 April 2017).

- Verhelst, Stijn. 2011. Renewed Financial Supervision in Europe—Final or Transitory. Egmont paper No. 44. Gent: Academia Press, p. 40. [Google Scholar]

- Veron, Nicolas. 2015. Europe’s Radical Banking Union. Bruegel Essay and Lecture Series; Brussels: Bruegel, p. 10. [Google Scholar]

- Wyemersch, Eddy. 2012. The European Banking Union, a First Analysis. Financial Law Institute Working Paper Series WP 2012-07. p. 3. Available online: http://papers.ssrn.com/sol3/papers.cfm?abstract_id=2171785 (accessed on 27 July 2017).

| 1 | The Agreement was signed on the 1st January 2004 by the European Commission, EU member countries and three EFTA countries that wished to participate in the European Free Trade Association. The main objective of the EEA Agreement is to ensure in all 31 states free movement of goods, persons, services and capital—the ‘four freedoms’. As a result of this agreement, Union law is, as far as the four freedoms are concerned, implemented into the national legal system of EFTA countries. All new relevant EU legal regulations are also implemented into the EEA Agreement so they apply to the entire EEA area (not just the EU) and they ensure a unified application of legal norms relating to a single market. In this case, we refer to the norms as EEA relevant. EFTA countries are, however, not fully responsible, unlike the EU member countries. |

| 2 | ESFS was based on the Larosiére report and caused EU financial supervisory system’s reform, which is built on macro and micro prudential pillar. |

| 3 | Legislatively new supervisors were established by a Regulation of the European Parliament and the European Council.

|

| 4 | Macro prudential supervision is the analysis of trends and imbalances in the financial system and the detection of systemic risk that these trends, may pose to financial institutions and the economy. The focus of macro prudential supervision is the safety of the financial and economic system as a whole, the prevention of systemic risk. See (House of Lords 2009). |

| 5 | The addresses shall communicate to the ESBR and the Council the actions undertaken as a reflection for recommendation or shall explain any inaction. |

| 6 | It refers the activity of saying publicly that addresses, has behaved in a bad or illegal way. It could mean bad publicity for that addresses which didn’t follow compliance of recommendation. (Detailed description of naming and shaming mechanism see (Pfalzer 2014)). |

| 7 | European Banking Authority—EBA; European securities and markets authority—ESMA; European insurance and Occupational pensions authority. |

| 8 | Stakeholder groups includes for example group Securities and Markets Stakeholder Group (Stakeholder group of Securities and Markets) to which the ESMA should consult the preparation of technical standards and regulations to create a set of common rules (common rulebook). This group is composed of 30 members, representing in balanced proportions EU financial market participants, their employees as well as consumers, investors and users of financial services. Similarly, in case of EBA and EIOPA Stakeholder Groups. (See. Article 37 of the ESA Regulation and (Emmenegger 2010)). |

| 9 | ESMA’s responsibilities and powers in this context are provided by CRA Regulation (EC) no. 1060/2009 and Delegated Regulation no 946/2012, EMIR regulation no. 648/2012 and Delegated Regulation no. 667/2014. |

| 10 | See recital 9 of the EBA and ESMA Regulation and recital 8 of EIOPA Regulation. |

| 11 | Regulatory arbitrage—Differences in financial regulation created incentives for “regulatory arbitrage”, i.e., Situation where financial institutions seek regulatory framework as considerate as possible. Member States that feared—or vice versa tried to benefit from—regulatory arbitrage, recommends to reduce the level of regulatory requirements. (For more details, see (Tabellini 2008)). |

| 12 | This is a situation where Member States may introduce stricter regulatory rules if they want. |

| 13 | These are the wholesale non-equity prospectuses offered only to qualified investors, the prospectuses which relate to specific types of complex securities, such as asset backed securities, or which are drawn up by specialist issuers and the prospectuses drawn up by third country issuers entities in accordance with Regulation (EU) 2017/1129. |

| 14 | Article 16 of the ESA Regulation. |

| 15 | Article 10–15 ESA Regulation. |

| 16 | Article 290–291 of Treaty on the Functioning of the European Union (TFEU), OJ C 83, 30.3.2010, pp. 1–388. |

| 17 | For more details see (Moloney 2011). |

| 18 | Council Regulation (EU) No. 1024/2013 of 15th October 2013 conferring specific tasks on the European Central Bank concerning policies relating to the prudential supervision of credit institutions (hereinafter the ‘SSM Regulation’)

|

| 19 | A different opinion is voiced by e.g., (Tomsik 2012). He says here that the Single Rulebook created by the EBA is the fourth pillar of the banking union. I believe though it includes more single rules than just those created by the EBA and all these rules blend with the other three pillars. |

| 20 | The notion of importance is linked with the size of the bank—the number of assets, its influence on the EU as well as the national economy, the importance of cross-border transactions etc. More specifically direct supervision will be realized in case one of the following criteria is met: the total number of assets is worth 30 billion EUR; the ratio of total assets to the GDP of an EU member is higher than 20% (not applicable if the total number of assets is worth less than 5 billion EUR); Having notified the national supervisory authority the ECB labels a particular bank as important; the ECB upon its own initiative labels a bank as important if the bank has subsidiaries in more EU countries and cross-border assets or bonds form the majority if their assets or bonds; if a bank has asked for or received financial support from the EFSF or the ESM; or, regardless of the criteria above, a bank is one of three biggest banks in a particular member country. |

| 21 | The criterion of total assets suggests that 32% of the banks are French, 22% are German, 14% are Spanish, 10% are Italian and Dutch and 13% are from the remaining Eurozone countries. There are 3520 less important banks, 48% of which are German (1688), 16% are Austrian, and 15% are Italian banks. (Veron 2015). |

| 22 | The setting of higher or supplementary capital buffers according to Basel III or the CRD IV: systemic risk buffer and counter-cyclical buffer. |

| 23 | See more about SSM (Ferran and Babis 2013; Niknejad 2014). |

| 24 | The Agreement was signed on the 1st January 2004 by the European Commission, EU member countries and three EFTA countries that wished to participate in the European free trade association. The main objective of the EEA Agreement is to ensure in all 31 states the free movement of goods, persons, services and capital—the ‘four freedoms’. As a result of this agreement, Union law is, as far as the four freedoms are concerned, implemented into the national legal system of EFTA countries. All new relevant EU legal regulations are also implemented into the EEA Agreement so they apply to the entire EEA area (not just the EU) and they ensure a unified application of legal norms relating to a single market. In this case we refer to the norms as EEA relevant. EFTA countries are, however, not fully responsible, unlike the EU member countries. |

| 25 | European Free Trade Association ‘EFTA’ includes Norway, Iceland, and Lichtenstein. |

| 26 | It is a Nordic financial group active mainly in the North of Europe. This bank is a product of mergers and acquisitions of Finland, Danish, Norwegian and Swedish banks Merita Bank, Unibank, Kreditkassen (Christiania Bank) and Nordbanken, which took place from 1997 to 2000. The Baltic countries and Poland are today also considered to be part of the domestic market. The largest shareholder of Nordea is Sampo, a Finnish insurance company with around 20% of the shares. Nordea is listed on the stock exchanges in Copenhagen, Helsinki, and Stockholm. Nordea’s headquarters is in Stockholm and it has more than 1400 branches. The bank is present in 19 countries all over the world and it operates through full service branches, subsidiaries and representative offices. Source: wikipedia.org. |

| 27 | The EEA Joint Committee is in charge of the execution of the EEA Agreement. It holds regular meetings six (or eight) times a year. It is a forum where problems are discussed and decisions are accepted on the basis of a consensus regarding the implementation of EU norms into the EEA Agreement. Before the Treaty of Lisbon was signed, the EEA Joint Committee was comprised of representatives of EEA and EFTA countries and the European Commission. In agreement with the Treaty of Lisbon, responsibility for the co-ordination of EEA issues was transferred from the European Commission to the European External Action Service after this institution was created on the 1st December 2010. |

| 28 | In view of the fact that such norms are at that time published in English and Swedish; both languages are well understood by everyone in Norway. In Norway the only legal language is not Norwegian. The EEA Agreement lacks a provision as the one found in Article 297 of the TFEU (procedure for the adaption of acts), so the decisions made by the EEA Joint Committee can come into effect even before their legal translations is published in Norwegian or Icelandic in the EEA Official Journal, where all new legislation of the EEA is published (like the norms of the EU). |

| 29 | EFTA countries can delay the effect of the implementation of Union norms even after an agreement has been reached in the EEA Joint Committee. The can do so by claiming that they need to implement the norm into their own constitution (e.g., by means of parliamentary ratification). Subsequently, the transposition deadline is six months; yet, if it is announced that the time needed is going to be longer than six months, the EEA Joint Committee’s decision remains ineffective. |

| 30 | Mainly because they do not guarantee that the EU and member countries accept such acts as equal to the legally binding EU/EEA norms; likewise, they do not grant economic entities from EFTA any rights they could claim within the EU pillar regarding the EEA. |

| 31 | In this case, there would have to be solution to the problem concerning what to do in cases when the European Commission or the Council can influence the decision making of the EU authorities; most probably the best option is to transfer this competence to the EEA Joint Committee. Event his would not be far from ideal, particularly in urgent situations when national interests at are stake—yet, one can hardly find a better alternative in the structures of the EEA. |

| 32 | However, this solution addresses to a certain extent, only the problems associated with ESA authorities, but there are many more EU authorities and agencies. A more comprehensive solution is needed—one that involves all EU authorities that make decisions and are EEA relevant. |

| 33 | This body performs micro-prudential supervision over individual financial institutions with particular focus on analyses of economic shocks that may wreak havoc on the financial sector. Currently the biggest risks are connected with the so-called ‘bubbles’ in the credit and property markets. The monitoring is predominantly based on a group of indicators and analyses covering six main categories and capturing micro as well as macro factors. See Macro prudential supervision of the financial system—organization and instruments (Norges Bank 2012). |

| 34 | The author is certain, that one of the greatest incentives for the EEA Agreement is strong European interconnection and close co-operation as well as the existence of a supranational financial market and an enormous Europe-wide demand for a single market in accordance with the four freedoms of the EEA Agreement. |

| 35 | The other methods are all those decentralized. In these cases, when countries protect their own market with certain rules, legislation and customs we cannot find any future economic growth or financial stability in globalized economy, which is present reality. |

Scheme 1.

Banking union and its pillars.

{kind=link}

Table 1.

Tools and tasks of the ESAs.

| Quasi-regulatory competences | Preparation of technical standards—regulatory and implementing | |

| Recommendations and guidelines for identical and correct application of EU law | ||

| Supervisory Competences | Micro | Supporting and monitoring the efficient, effective and consistent functioning of colleges of supervisors |

| Support coordination between supervisory authorities in specific situations | ||

| Carrying out regular analyses of the mutual evaluation (peer reviews) some or all of the activities of international supervisors | ||

| Monitoring and assessment of market developments and, if necessary, informing other ESAs, the ESBR, the European Parliament, the Council and the Commission on the current micro-prudential trends, risks and vulnerable areas | ||

| Building of and support for common EU supervisory culture | ||

| Macro | Cooperation with the ESRB and the follow-up to its warnings and recommendations in the matter of systemic risk (risk dashboard) | |

| Indicators and criteria for assessing systemic risk and an adequate stress testing regime | ||

| Making the necessary supplementary guidelines and recommendations for key financial institutions while taking into account the systemic risk they pose | ||

| Inquiry of financial activities, type of product or conduct and subsequent recommendations for action to the competent authorities concerned | ||

| Legally binding decisions (law enforcement) | In the case of a breach of EU law, issuing specific recommendations to the national supervisory authorities | |

| Action in critical situations addressed to financial institutions | ||

| Legally binding decisions made during the settlement of disagreements between competent authorities in cross-border situations | ||

| The enforcement powers of ESMA’s for Credit Rating Agencies (CRAs) and Trade Repositories (TRs) | ||

Source: author’s own processing.

© 2018 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Janovec, M. Integrated Supervision of the Financial Market without the UK? Int. J. Financial Stud. 2018, 6, 20. https://doi.org/10.3390/ijfs6010020

AMA Style

Janovec M. Integrated Supervision of the Financial Market without the UK? International Journal of Financial Studies. 2018; 6(1):20. https://doi.org/10.3390/ijfs6010020

Chicago/Turabian StyleJanovec, Michal. 2018. "Integrated Supervision of the Financial Market without the UK?" International Journal of Financial Studies 6, no. 1: 20. https://doi.org/10.3390/ijfs6010020

Note that from the first issue of 2016, this journal uses article numbers instead of page numbers. See further details here.