A Strategic Analysis of Cargolux Airlines International Position in the Global Air Cargo Supply Chain Using Porter’s Five Forces Model

School of Tourism and Hospitality Management, Suan Dusit University, Hua Hin Prachaup, Khiri Khan 77110, Thailand

Infrastructures 2019, 4(1), 6; https://doi.org/10.3390/infrastructures4010006

Submission received: 28 November 2018

/

Revised: 4 January 2019

/

Accepted: 18 January 2019

/

Published: 18 January 2019

Abstract

:The objective of this research was to examine Cargolux Airlines International’s, one of the world’s major dedicated all-cargo airlines, strategic position in the global air cargo supply chain. To achieve this objective, a qualitative research approach was used. The data gathered for the study was examined by document analysis. The strategic analysis of Cargolux Airlines International was underpinned using Porter’s Five Forces Model. The study found that Cargolux has developed an extensive portfolio of products that satisfy discrete air cargo market segments’ requirements. The airline has also entered strategic partnership agreements with Emirates SkyCargo, Nippon Cargo Airlines (NCA), and Oman Air, which has enabled the partners to expand their route networks and to better optimize their available air cargo capacities. Cargolux has also established Milan-based Cargo Italia, which focuses on serving the important Italian air cargo market. The airline has also developed a successful two hub strategy in conjunction with one of its major shareholders, Henan Civil Aviation and Investment Company (HNCA). In 2017, Cargolux commenced a journey of transformation with the introduction of the “Cargolux 2025 Strategy”. A limitation of the study was that Cargolux’s annual revenues were not available. It was, therefore, not possible to analyze the airline’s revenue performance.

1. Introduction

The world air cargo industry has grown rapidly in recent decades and is now an integral part of the global economy. In 2017, the world’s airlines transported around 52 million metric tons of air cargo, which represented around 35% of the annual world merchandise trade by value [1]. In the global air cargo industry, air cargo capacity is provided by combination passenger airlines. These are airlines that carry passengers on the main deck and air cargo in their passenger aircraft lower lobe belly-holds. Air cargo capacity is also offered by dedicated all-cargo carriers, such as Cargolux International Airlines and Nippon Cargo Airlines (NCA), as well as by the integrators, such as DHL Express, FedEx, and United Parcel Service (UPS) [2]. All-cargo services are operated by dedicated freighter aircraft, where all the available capacity is devoted to the transportation of air cargo [3,4,5]. A freighter aircraft is an aircraft that has been expressly designed for the carriage of air cargo or one which has been converted from a passenger configuration to a freighter aircraft and is subsequently used to transport air cargo, express, and so forth, rather than passengers [6]. According to Boeing Commercial Airplanes {7], around 56% of global air cargo revenue ton kilometres (RTKs) is presently carried in dedicated freighter aircraft [7].

In the global air cargo industry, there are a small number of dedicated all-cargo airlines who offer airport-to-airport air cargo transportation services. These airlines include AirBridgeCargo Airlines, CargoLogicAir, Cargolux International Airlines, Nippon Cargo Airlines (NCA), and Polar Air Cargo Worldwide. The objective of this study is to empirically examine Cargolux Airlines International’s (hereafter Cargolux) strategic position in the global air cargo supply chain using Porter’s Five Forces Model. A secondary aim is to examine the strategies that Cargolux has defined and implemented to capture a competitive advantage. A third aim is to examine the Cargolux product/service portfolio vis-à-vis those of its main competitors to identify any differences, whilst, at the same time, identifying the targeted air cargo market segments for which Cargolux and its competitors have defined and implemented product/service specific offerings. Cargolux was selected as the case firm as the company was the world’s largest non-integrated dedicated all cargo airline in 2017. Cargolux was also the world’s seventh largest air cargo carrying airline, as measured by freight tonne kilometres performed (FTKs), in 2017 [8]. In addition, Cargolux is Europe’s leading air cargo carrier. A further motivation for selecting Cargolux Airlines as the case airline was the ready availability of documentation in the public domain. To address the study’s objectives, the following research questions were empirically examined:

- What is Cargo Airlines International’s competitive position in the global air cargo supply chain?

- What strategic options has Cargolux Airlines International defined and implemented to capture and deliver a competitive advantage in the global air cargo industry?

- Are there any strategic differences between Cargolux Airlines International services/products offerings and those of their principal competitors?

The remainder of the paper is organized as follows. Section 2 sets the contextual setting of the study and presents a brief overview of the global air cargo market, Porter’s Five Forces Model, and Porter’s generic strategies. Section 3 describes the research method used in the study. The case study on Cargolux is presented in Section 4. Section 5 presents the study’s findings.

2. Background

2.1. Porter’s Five Forces Model

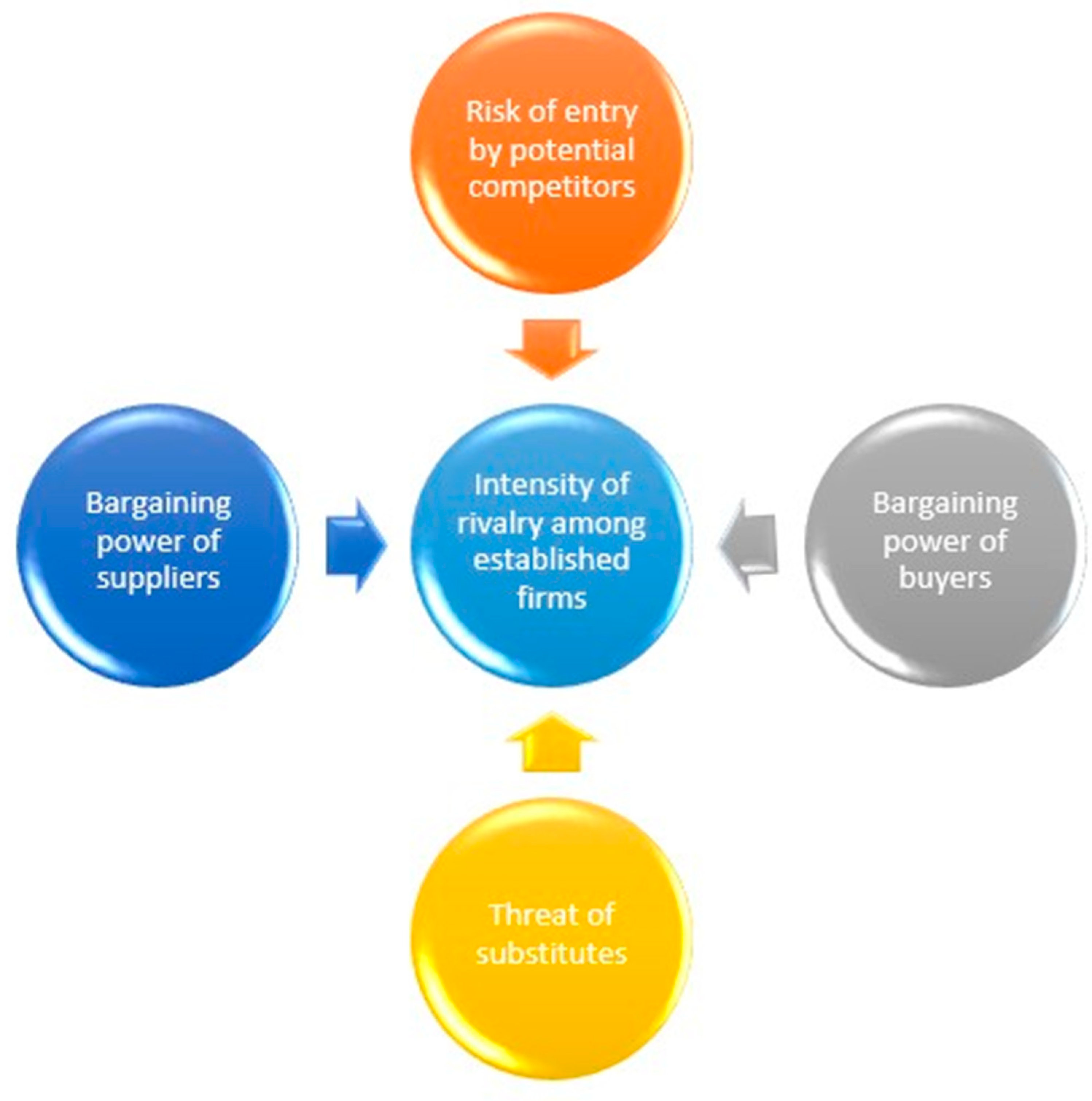

Prior to a firm defining its business level strategy, it must have a comprehensive understanding of what forces influence profits in the industry in which it competes [9]. One tool that is available for conducting this important analysis is “Porter’s Five Forces Model” [10]. Porter’s Five Forces Model is based on industrial organization (IO) economics. This specialty within the economics discipline argues that firms competing in an industry confront forces that significantly influence profitability. If a firm understands these forces, then it can define and implement a business-level strategy that enables the firm to either take advantage of, or protect itself from, these forces. This practice subsequently allows the firm to be consistently profitable. Porter’s model focuses on the five forces in an industry (buyers, suppliers, new entrants, substitution, and rivalry) that impact each other [11]. The collective strength of the five forces determines the ability of a firm competing in an industry to earn, on average, rates of return on investment (ROI) that are higher than the cost of capital [12] (p. 6). The model provides a framework for assessing and evaluating the strength and position of a firm competing in an industry [13,14]. Figure 1 summarizes Porter’s Five Forces Model.

2.1.1. The Intensity of Rivalry among Established Firms

The rivalry amongst firms competing in an industry takes the familiar form of jockeying for position [15]. A high level of rivalry between being existing competitors in an industry can influence the level of profitability generated in the industry. This force can be influenced by a range of factors, which includes the industry growth rate, fixed/storage costs, the number of firms’ competing balance, switching costs between rivals, differentiation, or barriers to market exit [11,15,16,17].

2.1.2. The Bargaining Power of Buyers

Powerful buyers can capture additional value by forcing prices downward and playing incumbents off against each other [18]. Thus, powerful buyers can also drive down the profitability of the industry. The buying power of buyers is high if the buyers are large, they can easily switch to another supplier, and they are few in number [16].

Most of these sources of buyer power can be attributed to consumers’ as a group as well as to industrial and commercial purchasers [11].

2.1.3. The Bargaining Power of Suppliers

Suppliers can exert bargaining power on incumbents in an industry by raising prices or by reducing the quality of the goods and services acquired. Powerful suppliers are therefore able to squeeze profitability out of an industry that is unable to recover cost increases in its own prices. Customers can force prices down, demand higher quality or greater service, and play rivals off against each other. These will occur at the expense of industry profits [11] (p. 28).

2.1.4. The Threat of Substitutes

A substitute threat refers to the risk associated with substitute products. Porter [19] observes that it is necessary to identify whether the other production branches (firms) have products that can perform the same function as the original products of a manufacturer [19]. By placing a ceiling on prices that it can charge, substitute products or services restrict the potential of an industry [20]. Furthermore, substitutes not only restrict profits in normal times; they also reduce the windfall that an industry can reap in boom times [21]. Like the threat of new market entrants, the threat of substitutes is determined by factors that include:

- Brand loyalty of customers;

- close customer relationships;

- customer switching costs;

- the relative price of the substitute’s performance; and

- current industry trends [22].

2.1.5. The Risk of Entry by Potential Competitors

New firms entering an industry bring a new capacity, the desire to gain a market share, and often very substantial resources [23]. Firms diversifying through acquisition into an industry from other markets quite often leverage their resources to cause a shakeup in the industry. The seriousness of the threat of entry is dependent upon the barriers that are present as well as the reaction from existing rivals that new entrants can expect. If the barriers to entry are high and new entrants can expect sharp retaliation from the entrenched rivals, then the new entrants will not pose a serious threat of entering the industry [24].

Porter [19] (pp. 24–25) notes that there are six key sources of barrier to entry: Economies of scale, product differentiation, capital requirements, cost disadvantage independent of size, access to distribution channels, and government policy. The potential rival’s outlook about the reaction of incumbents also will influence its decision on whether to enter the industry. The firm is likely to have second thoughts if incumbents have previously attacked new entrants or if:

- The incumbents possess substantial resources to fight back, including excess cash, productive capacity, or a strong position with distribution channels and customers;

- the incumbents seem likely to reduce prices because of a desire to retain market shares or because of industrywide excess capacity; and

- industry growth is slow. This will influence its ability to absorb the new arrival and probably cause the financial performance of all the parties involved to decline [19] (p. 26).

2.2. Porter’s Generic Strategies

In dealing with the five competitor forces, Porter [23] observes that there are three potential generic strategic approaches available to a firm that would enable it to outperform other firms in an industry: Overall cost leadership, differentiation, and focus. In some cases, the firm can successfully pursue more than one strategic approach as its primary target. Effectively implementing any of these strategic approaches typically requires total commitment as well as supporting organizational arrangements that are diluted if there is more than one principal target. The generic strategies are approaches to outperform rival firms in the industry; in some industries, the structure will mean that all firms are able to earn high returns, whereas in other industries, success with one of the generic strategies may be considered necessary for the firm just to obtain acceptable returns in an absolute sense [23] (p. 35).

2.2.1. Overall Cost Leadership Strategy

This strategic approach is based on the firm being the overall low-cost provider in the industry [24]. This is achieved through a set of functional policies aimed at the basic objective of being the lowest cost provider. A firm using a cost leadership strategy needs to aggressively construct efficient-scale facilities, maintain a vigorous pursuit of cost reductions from experience, tight cost, and overheads control, avoidance of conducting business with marginal customer accounts, and ensure cost minimization in areas, such as service, sales force, and so forth [23].

There are two potential advantages for a firm implementing this strategy. First, as a result of its lower cost structure, the cost leader can charge a lower price than rivals and still earn a profit, or, alternatively, charge the same prices as competitors, thereby earning a higher profit. Second, should there be a situation where a price war ensues, the cost leader will be in a more favorable position to withstand price-driven competition [25].

Attaining a low-cost position typically requires a high market share so that economies of scale can be realized. Emphasis is placed on the reduction of costs at every possible point. Thus, the firm may be required to design products for the ease of manufacture or delivery. Once a low-cost position has been achieved, the profits earned by the firm must often be reinvested in improved processes and technologies that will enable it to further reduce costs so that its cost leadership can be sustained [25].

2.2.2. Differentiation Strategy

Firms pursuing differentiation strategies seek to capture a competitive advantage by developing products or services that are perceived by buyers as being unique and for which buyers are prepared to pay a premium price. Successful differentiation provides the firm with two principal advantages that stem from the uniqueness of its products. First, the firm is able charge a higher price for its products or services. This often enables the firm to earn a higher margin [25]. Second, customers that are willing to pay more for a unique product are often more loyal. This is because their purchase decision is based more on the perceived quality rather than the price [23,25].

For a firm to achieve successful differentiation, a clear understanding of customer requirements and investments in capabilities necessary to satisfy those needs is required. Typically, achieving differentiation requires a trade-off to be made with its cost position, particularly if the activities required to create product uniqueness, for example, market research or quality materials, are themselves costly [25].

2.2.3. Focus or Niche Strategy

Porter’s final generic strategy focuses on a particular buyer group, market segment, or geographical market [23]. According to Griffin [26] (pp. 69–70), “this strategy may have either a differentiation focus, whereby the firm differentiates its products in the focus markets, or an overall cost leadership focus, whereby the firm manufactures and sells its products at low cost in the focus market”. The firm gains a competitive advantage by better serving the requirements of its chosen market segment, whether those requirements be lower cost or differentiating quality [25].

The ability of the firm to better satisfy the requirements of its chosen customers means that it may be able to charge a higher price for its unique products or services. Alternatively, the firm may be able to undercut the cost of the industry-wide cost leader through the application of technologies and processes that are not cost effective at larger scales. In addition, concentration within a protected niche may help the firm to withstand broader competition within the industry as a whole [25].

2.3. Competitive Advantage: A Background Note

Competitive advantages are conditions that enable a firm or country to produce a good or service of equal value at a lower price or in a more desirable fashion. These conditions enable the productive entity to generate more sales or superior margins when compared to its competitors in the market. Competitive advantages are attributed to a variety of factors: Cost structure, branding, the quality of product offerings, the firm’s distribution network, intellectual property, and the level of customer provided. Competitive advantages produce greater value for a business and its shareholders because of certain strengths or conditions. The greater the sustainability of the competitive advantage, the more difficult it is for rivals to neutralize the advantage [27].

3. Research Approach

3.1. Research Method Used in the Study

The research approach in this paper was based on the use of an instrumental case study research approach [28,29]. An instrumental case study is the study of a case, for example, a firm, that provides insights into a specific issue, redraws generalizations, or builds theory [30,31]. The present study was designed around the established theory of “Porter’s Five Forces Model” and Porter’s generic strategies [11,14]. The key issues examined in the present study were twofold. Firstly, the study examined Cargolux strategic position in the global air cargo supply chain based on Porter’s Five Forces Model, and secondly, the study examined the strategies that Cargolux have defined and implemented to capture a competitive advantage. A third aim was to empirically examine the Cargolux product/service portfolio vis-à-vis those of its main competitors and to identify the market segment specific product/service offerings. Thus, as previously noted, Cargolux International Airlines was the case firm examined in the study.

3.2. Data Collection

Data for the study was obtained from a range of documents, Cargolux Airlines International’s company materials available on the internet, airline industry press articles, and media releases. These documents provided the sources of case evidence. The documents collected and examined in the study included Cargolux Airlines’ annual reports, company brochures, media releases, and the airline’s websites. An exhaustive source of the leading air transport and air cargo-related magazines was conducted (Table 1). A search of the SCOPUS and Google Scholar databases was also undertaken in the present study.

The key words used in the database searches included “Cargolux Strategy”, “Cargolux 2025 Strategy”, “Cargolux strategic partnerships”, “Cargolux cooperation agreements”, and “Cargolux airline products”.

Secondary data was therefore used in the study. The three principles of data collection as suggested by Yin [34] were followed: The use of multiple sources of case evidence, creation of a database on the subject, and the establishment of a chain of evidence.

3.3. Data Analysis Process

The empirical data collected for the case studies was examined using document analysis [35,36]. Document analysis is quite frequently used in case studies and focuses on the information and data from formal documents and company records that were gathered in the study [37,38,39]. The documents collected for the present study were examined by four key criteria: Authenticity, credibility, representativeness, and meaning [40,41].

Before proceeding with the formal analysis of the documents that were gathered for the study, the context in which the documents were created was determined and the authenticity of the documents was carefully assessed [42]. Authenticity entails an assessment of the gathered documents for their soundness and authorship. Scott and Marshall [43] (p. 188) note that “soundness refers to whether the document is complete and whether it is an original and sound copy”. Authorship relates to such issues as collective or institutional authorship. In this study, the source of the case study documents was primarily from Cargolux as well as relevant articles published in the leading air transport and air cargo industry-related magazines, for example, Air Cargo World, Air Transport World, Airline Business, Aviation Week and Space Technology, Flight International, and the Journal of Air Transport Management. The documents collected in the study were all readily available in the public domain.

The credibility criterion concerns the accuracy and sincerity of a document [43,44]. In the present study, the evidence for the case study was corroborated using various kinds of documents that were sourced from various sources, for example, company media releases, articles published in the leading air transport industry magazines, and relevant articles published on the Internet [45].

The representativeness criterion involved an assessment of the availability and survival of the documents that were collected for the study. No major difficulties were experienced in obtaining the documents as all the relevant documents could be easily accessed in the public domain. The fourth criterion, meaning, is a very important aspect of document analysis. Meaning occurs at two levels. The first is the literal understanding of a document, that is, its physical readability, the language used, whether it can be read, and the date of the document [43,44]. When conducting document analysis in a study, it is important for the researcher(s) to interpret the understanding and the context within which the document was produced. This enables the researcher(s) to subsequently interpret the meaning of the document. The evidence found in the documents collected and used for the present study were all clear and comprehensible [46].

The document analysis process in the study was undertaken in six distinct phases, which followed the recommendations of O’Leary [47].

- Phase 1: This phase involved planning the types and required documentation and their availability;

- Phase 2: The data collection involved gathering the documents and developing and implementing a scheme for the document management;

- Phase 3: Documents were reviewed to assess their authenticity, credibility, and to identify any potential bias;

- Phase 4: The content of the collected documents was interrogated, and the key themes and issues were identified;

- Phase 5: This phase involved the reflection and refinement to identify and difficulties associated with the documents, reviewing sources, as well as exploring the documents’ content; and

- Phase 6: The analysis of the data was completed in this final phase of the study [47] (p. 179).

Following the guidance of Yin [39], all the collected documents were downloaded and stored in a case study database. The documents collected for the study were all in English. Each document was carefully read, and key themes were coded and recorded. This study also followed the recommendation of van Schoor [46] (p. 94), who has noted that to avoid bias, documents from different sources should also be carefully analyzed in the study. In addition, triangulation was utilized to add discipline to the study. This was achieved by collecting documents from multiple sources. This approach helped verify the themes that were detected in the documents gathered in the study [48].

4. Results

4.1. A Brief Overview of Cargolux Airlines

Cargolux was established in March 1970 to operate world-wide air cargo charters from its home base at Findel Airport, Luxembourg [49]. The airline’s shareholders were Luxembourg’s national airline, Luxair; Swedish shipping line, Salen Shipping Group; Icelandic airline, Loftleider Icelandic; and private interests [50,51]. Luxair, Salen Shipping, and Loftleider Icelandic each held a third of the shares, with the balance held by private interests [52]. Cargolux commenced operations in May 1977 with a single Canadair CL-44D4 aircraft [52,53]. The Canadair CL-44 was manufactured by Montreal, Canada-based Canadair Limited.

In 1973, Cargolux took delivery of its first jet-powered aircraft, a McDonnell Douglas DC8-61F. The McDonnell Douglas DC8-61F was produced by the Douglas Aircraft Company at Long Beach, California, in the United States. In 1979, the airline added its first Boeing 747-200F freighter aircraft, along with two Boeing B707-331 Combi aircraft. The Boeing B707-331 Combi and the 747-200F were manufactured by the Boeing Commercial Airplane Company in Renton, Washington State in the United States. In 1985, Cargolux withdrew its fleet of McDonnell Douglas DC8F and Boeing 707′s, and in the process, became Europe’s first all Boeing 747-200F cargo operator [53].

In 1993, Cargolux took delivery of its first Boeing B747-400 freighter aircraft; this aircraft type provided a better range capability and increased air cargo capacity [53]. Cargolux was the first dedicated all-cargo airline to take delivery of the Boeing B747-400 freighter aircraft, which was manufactured by Boeing Commercial Airplanes, in Renton, Washington State in the United States. Initially, it was envisaged that the Boeing B747-400F would rationalize the Cargolux fleet, permitting the airline to operate its fleet of Boeing B747-200 freighter aircraft on shorter routes and the Boeing 747-400 freighter aircraft on longer routes. However, cost savings arising from the operation of a two-crew cockpit, 18% fuel savings, lower maintenance costs, and greater capacity led to the decision by the company to replace the Boeing 747-200 fleet with the Boeing B747-400 freighter aircraft [54].

Cargolux together with Japan-based Nippon Cargo Airlines (NCA) were the launch customers for the Boeing 747-8 freighter aircraft [55]. Following the orders for 13 Boeing 747-8 freighters by Cargolux and 14 by Nippon Cargo Airlines, Boeing Commercial Airplanes officially launched the 747-8F program in November 2005 [56]. The Boeing 747-8 is manufactured by Boeing Commercial Airplanes at its facilities located in Renton, Washington State in the United States. Cargolux was scheduled to take delivery of its first two Boeing 747-8F freighter aircraft on 19 September 2011 [57], however, the delivery was delayed to October 12, 2011, at which time the airline received its first aircraft [58,59]. At the time of the present study, Cargolux operated a fleet of 14 Boeing 747-8 freighters, 12 Boeing 747-400, and two Boeing B747-400ERF freighter aircraft (this aircraft was also manufactured by Boeing Commercial Airplanes at its Renton, Washington State facilities). The airline’s worldwide route network covers 90 destinations, of which some 70 are served by scheduled all-cargo flights. In addition to its scheduled flights, Cargolux also operates full and part-charter services [60].

Cargolux principally transports perishables, temperature and shock-sensitive goods, supply chain goods, project cargo, finished commodities, live animals, sensitive and high-technology equipment, as well as oversized freight shipments. Cargolux also provides subleasing services. The airline also operates extensive trucking services that consist of road feeder services (RFS) throughout Europe, North and South America, the Middle East, Africa, and within Asia [61]. Road feeder services are used in the air cargo industry for the transportation of air cargo between hub and regional airports [62].

Cargolux also offers third party aircraft maintenance at its maintenance base at Luxemburg Findel Airport. The company is specialized in Boeing B747 line and hanger maintenance up to and including aircraft C-Checks. Also, the company offers a range of specialized maintenance services and holds line maintenance approval for the Boeing 777 aircraft.

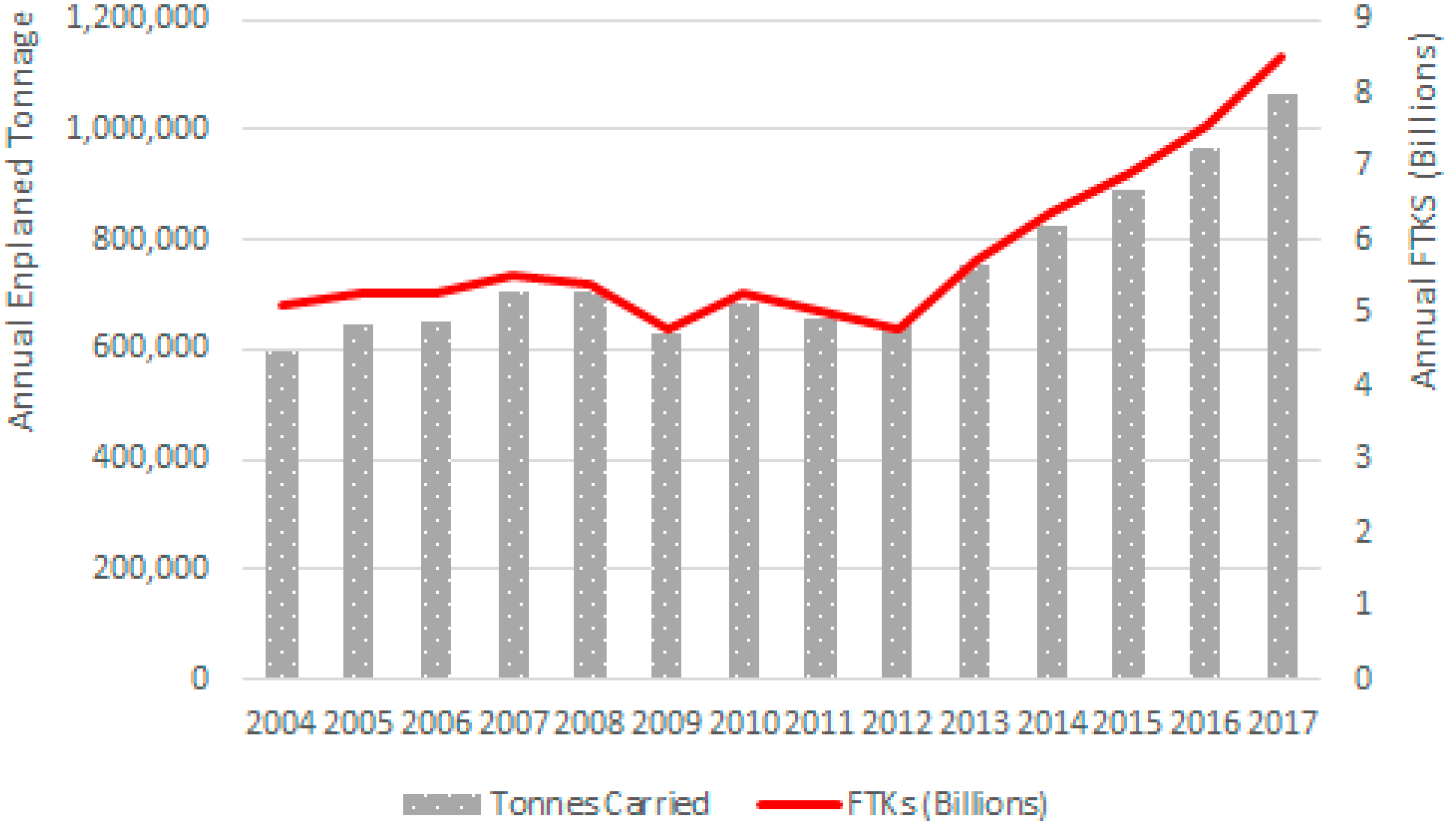

Figure 2 presents Cargolux’s annual enplaned air cargo tonnage and freight tonne kilometres performed (FTKs) for the period of 2004 to 2017. A freight tonne kilometer is defined “as the mass of air cargo multiplied by the distance that the cargo is carried” [63] (p. 36). As can be observed in Figure 2, both the annual enplaned tonnages and FTKs declined in 2009 as the effects of the global financial crisis (GFC) impacted the global air cargo industry. From 2012 to 2017, Cargolux experienced strong growth in both its annual enplaned tonnages and FTKs from 2012 until 2017.

4.2. The Application of Porter’s Five Forces Model to Cargolux Airlines’ International Position in the Global Air Cargo Industry Supply Chain

The attractiveness of the world air cargo industry is determined by five competitive forces: The intensity of the rivalry amongst incumbent competitors, threat of new entrants into the industry, bargaining power of buyers, buying power of suppliers, and the threat of substitute products or services [70].

4.2.1. The Intensity of Rivalry among Established Airlines in the Global Air Cargo Supply Chain

- There are many competitors providing services in the global air cargo supply chain. These carriers typically operate the same aircraft types as Cargolux and their business models are virtually comparable at a global level [10]. Both the combination passenger airlines, who may also operate freighter aircraft in addition to their passenger services, and the dedicated all-cargo airlines, such as Cargolux, Cargo Logic Air, and Nippon Cargo Airlines (NCA), provide airport-to-airport services. These operators principally source their air cargo traffic from International Air Transport Association (IATA) accredited air freight forwarders and third-party logistics providers, for example, DB Schenker, DHL Global Forwarding, and Panalpina. In addition, the major integrated carriers, such as DHL Express, FedEx, and United Parcel Service, also compete strongly in both the global air cargo and air express market segments;

- air cargo capacity can only be introduced in quite large increments. As previously noted, the major global air cargo carrying airlines operate dedicated freighter aircraft, with airlines, such as Cargolux, AirBridge Cargo Logic Air, Cargo Airlines, and Nippon Cargo Airlines, operating fleets of Boeing B747-400 or Boeing 747-8 freighter aircraft. The Boeing B747-400 freighter has a cargo payload of 121.9 tonnes, whilst the Boeing 747-8 freighter has a cargo payload of 132.6 tonnes [71,72]. The Boeing B777-200LRF freighter aircraft is operated by Emirates SkyCargo, Ethiopian Airlines, Etihad Airways, EVA Air Cargo, Korean Air Cargo, Lufthansa Cargo, and Turkish Air Cargo. The Boeing B777-200LRF has a cargo payload of 103.7 tonnes [73]. Cargolux, like other air cargo-carrying airlines, offers large volumes of air cargo capacity when it enters a new market. Thus, detailed planning and market analysis is required prior to deciding whether to add new or additional air cargo capacities;

- the fixed assets that are required by the actors competing in the global air cargo industry, such as aircraft, aircraft unit load devices, and air cargo terminals, can typically only grow in larger and fixed steps [70]. The major assets that Cargolux requires are aircraft, and these are carefully planned for. Air cargo handling at the carrier’s primary hub at Luxemburg Airport is outsourced to LuxairCARGO [74]. In addition, Cargolux’s cargo handling is contracted to cargo handling agents at the various airports that it services on a scheduled and non-scheduled basis. This cargo handling outsourcing strategy eliminates the requirement for Cargolux to invest in costly air cargo terminals, whilst also avoiding the staffing and operating costs associated with the provision of cargo handling services; and

- the barriers for exiting the air cargo market are rated as high. This is due to the specialized means of production (air cargo transportation), fixed costs associated with the retirement of aircraft, and governmental barriers [70]. This factor did not apply to Cargolux Airlines International as the airline is an active competitor in the global air cargo supply chains.

4.2.2. Barriers to Market Entry in the Global Air Cargo Supply Chain

The presence of market entry barriers in the global air cargo industry restricts the number of actors competing in the industry, and hence, influences the rivalry amongst the incumbent competitors [70]. In the world airline industry, there are four discrete types of legal entry barriers: Airline ownership, airline operating licenses, route-specific air services rights, and perimeter rules at airports [75].

Should new airlines enter the air cargo market, the competitive advantages of the incumbent airlines are immediately influenced. This is because the new entrant provides new additional air cargo carrying capacities in the existing market, which typically diminishes the profit margins of all market participants [70]. When the market entry barriers are low, there is a greater threat to the incumbent airlines [24].

There are three other discrete entry barriers in the air cargo industry that are applicable for pure new dedicated cargo airlines. Importantly, these barriers do not apply for the additional air cargo capacity provided by the combination airlines [70].

- Existing incumbent all cargo airlines realize economies of scale by over proportionally decreasing the total cost whilst, at the same time, increasing their production capacity, that is, freight tonne kilometres (FTKs) performed;

- the incumbent airlines may have already attained high brand recognition, intense customer loyalty, or similar marketing targets. For the new entrant to compete in the market, they must incur the costs associated with sales support, advertising, and other marketing initiatives. Cargolux has historically worked very closely with the freight forwarders, and hence, has a strong brand image and customer loyalty; and

- entry into the air cargo market requires substantial investment and capital. In terms of capital expenditure and costs incurred, the risk of a new cargo airline failing (sunk costs) presents a major hurdle for new market entrants [70] (p. 319).

In the global passenger and air cargo transport industry, airport “slots” are viewed as a classic barrier to market entry [76]. A slot is “defined as the concession or entitlement to use runway capacity of a certain airport on a specific date and specific time” [77]. In cases where airport slots continue to be awarded under the “Grandfather Rights” principle, it would then be very difficult for new entrants to obtain access to attractively-timed slots at congested airports. However, the legalization of the so-called “Secondary Slot Trading” does provide new entrants with the possibility of purchasing slots. If they do purchase them, however, they will still need to compete against incumbent airlines who obtained many, or all, of their slots for free [75] (p. 88). As previously noted, Cargolux’s major hub is located at Luxembourg Airport. Thus, a possible future threat would be if the airport become slot constrained at some point in the future.

Governmental policy is also a major entry barrier [24]. In today’s air cargo (and airline) industry, there are stringent security regulations that can pose a barrier to market entry due to the associated costs. Cargolux Airlines International, like the combination and dedicated all-cargo airlines, and the integrated carriers, must comply with all government regulations.

4.2.3. Bargaining Power of Buyers

Customers that have a high level of market power in the air cargo industry can place pressure on air cargo rates, whilst at the same time, these customers often demand higher quality or the extension of a carrier’s existing product/services’ range [70]. Around 90% of global air cargo traffic is provided by freight forwarders and global logistics providers [76]. These firms are powerful because they are often purchasing standardized or undifferentiated services, the costs associated with changing airlines is low, and the products/services provided by airlines are often easily exchanged or substituted [70]. Today, in the global air cargo industry, there are a relatively small number of international freight forwarders or global logistics service providers, such as DHL Global Forwarding, Panalpina, and DB Schenker, who account for a major portion of the industry revenues and employees [76,77]. Indeed, the global air cargo industry has never seen such a high degree of forwarder concentration as that which exists today. Given the large volumes of air cargo traffic that these large firms control, they can have considerable influence over an airline’s routing decisions, and they are using that influence to develop cargo hubs at preferred airports [78] (p. 140). There are also small and mid-sized freight forwarding firms competing in the industry, as they can offer a level of specialization or a combination of scope and flexibility that the large global operators may not be able to provide. As noted, Cargolux has historically worked very closely with the international air freight forwarders and this has resulted in a strong brand and customer loyalty.

Some freight forwarders have extended their service offering beyond merely booking cargo space on behalf of their customer on passenger and freighter services provided by the airlines. They are now offering shippers their own dedicated freighter services. For example, in February 2018, Flexport, an air freight forwarder, announced that beginning April 5 it would offer round-trip flights between Hong Kong and Los Angeles twice per week utilizing a Boeing B747-400F aircraft [79].

4.2.4. Bargaining Power of Suppliers

Within the air cargo industry, suppliers can pose a threat through the increase in their pricing. As such, powerful suppliers could, in this context, reduce the profitability of firms competing in the industry, if they are not able to recoup cost increases through an increase in their pricing. The aircraft manufacturers and aviation fuel companies are considered powerful. This is because these sectors are dominated by several firms, for example, Airbus and Boeing Commercial Airplanes, and they are more concentrated than the airlines. Furthermore, their products that are delivered are vital for the consuming air cargo sector [70]. In the airline industry, there are suppliers who either actually or potentially possess monopoly power. These include air traffic control (ATC) and airport services, with many carriers having to pay whatever ATC and airport services’ charges are levied upon them [76].

Boeing Commercial Airplanes and Cargolux have had a long-standing relationship and have launched new aircraft programs together, for example, as previously mentioned, Cargolux was one of the launch customers for the Boeing 747-8 freighter aircraft [80,81]. Cargolux was also the first airline to operate the Boeing B747-400 freighter aircraft [82].

Cargolux is the major air cargo airline serving Luxemburg Airport and has a long-standing relationship with its cargo handling agent—Luxair CargoCenter. Luxair has a 35% shareholding in Cargolux [83].

As previously noted, Cargolux provides extensive road feeder services to expand its marketable network. These services are provided by contracted trucking companies that serve an extensive surface network throughout Europe to deliver intercontinental air cargo to and from Luxembourg. Temperature-controlled road transport services are also provided to and from the Luxair CargoCenter in Luxembourg Airport [84]. Due to its strong position and ranking in the global air cargo industry, Cargolux is a valuable customer for the road feeder service operators.

Cargolux appears to be in a relatively favorable position vis-à-vis its key suppliers.

4.2.5. The Threat of Substitute Products in the Global Air Cargo Supply Chain

Oedekoven [70] (p. 320) has observed that substitution in the air cargo industry depends upon the specific market segment. Substitution in the air cargo industry is generally greater if the air cargo services being provided can be relatively easily switched from the original product/service to a substitute (low product loyalty). The possibility of buyers making a substitution are made greater if the incurred buyer switching costs are relatively low and if the air cargo rates are relatively high compared to the performance of the substitute product, for example, the slower speeds of ocean transport or by truck, which is considered acceptable to the buyer at the lower price [70]. Often, air cargo transportation confronts challenges from two modes of transport: Railway and road. Railway transport is considerably cheaper than air cargo transport [85]. The supply of air cargo capacity is influenced by the airline’s available capacity, and competition from the surface-based transport modes, particularly maritime container transport. Furthermore, improved trucking reliability and service quality, for instance, the ability of customers to track their consignments in real time, lower theft/damage/pilferage rates, coupled with rates lower than airlines can offer, has put trucking in a position where it both competes with, and complements, air services [79] (p. 143). The rail mode is also emerging as a potential source of competition to air cargo, particularly between China and Europe [86]. Thus, the surface transport modes can pose a competitive threat to air cargo-carrying airlines. The threat of the substitution of ground-based surface transport modes applies to both the combination airlines and the dedicated all-cargo carriers.

Furthermore, in recent times, there has been a modal shift with the loss of global air cargo to ocean freight [87,88]. The decline in the air share is explained by three key factors:

- Commodity mix effect: Higher growth of products that traditionally, and typically, were shipped by ocean freight versus those shipped by the air cargo mode;

- Value effect: There has been a higher growth of the lower end of a product, which has entailed the greater use of ocean freight; and

- Mode shift: This occurs when a product historically transported by the air cargo mode is shipped by ocean freight instead [89] (p. 5).

Cargolux, like all other cargo-carrying airlines, will need to remain mindful of these competitive threats and, in so doing, frame their strategic options accordingly

4.3. Cargolux Airlines’ Strategy

Cargolux has strategically positioned itself as a relatively niche carrier with a niche route network, which includes the world’s largest air cargo markets, and a niche range of products. These are key to the airline’s value premium and have prevented the commoditization of the product/service offering [90].

4.3.1. Cargolux Strengths in the Competitive Global Air Cargo Supply Chain

There are a range of strategic factors that underpin Cargolux’s competitive position in the global air cargo supply chain. The airline operates a homogenous, modern fuel-efficient fleet of Boeing B747-8, Boeing B747-400F, and Boeing B747-400ERF freighter aircraft [68]. The most commonly used metric in the evaluation of aircraft productivity is the daily aircraft utilization rate. The daily aircraft utilization rate is measured in block hours per day and by the aircraft operated by the airline [91]. Thus, the most effective driver of an airline’s aircraft productivity is its aircraft utilization rate, as aircraft do not earn revenue when they are sitting on the ground in between flights [92]. In 2017, the strategic deployment of the Cargolux fleet of aircraft resulted in a daily utilization rate of 14 hrs 51 min per day being achieved [68].

Organizational flexibility is required by firms so that they can adapt rapidly to changing business environments [93]. At a strategic level, there is a great deal of strategic flexibility when the firm can easily change the composition of its product market combinations (PMCs) through the renewal of products, by switching to new markets, by the acquisition of other firms, and via the divestment of unviable business units [94]. An important factor that underpins Cargolux’s competitive strategic position in the global air cargo supply chain is the company’s flexibility to adapt to market changes [90]. Recent changes in the global air cargo market include the rapid volume in perishable items transported by the air cargo mode. This growth is due to the globalization of eating habits [95]. Another market change has been the increase in E-commerce, which has created “a speed to market” customer mentality—the air cargo mode is well suited to satisfy this requirement. Furthermore, in recent years, there has been strong growth in the volume of pharmaceutical products shipped by air cargo. According to the International Air Transport Association [96] (p. 5), the pharmaceutical industry relies on air cargo for its speed and efficiency in transporting high-value, and time and temperature sensitive cargo, particularly vaccines. Other factors that are shaping the air cargo environment include market liberalization, new logistics concepts, new players, and new modes of transport, for example, drones [97]. Cargolux has responded to these changes through the development of its product and services offered as well as through its niche route network.

The other factors that underpin Cargolux’s strengths in the global air cargo supply chain include a lean customer driven organization, a loyal and highly qualified workforce, quick decision making, a team environment, and its in house aircraft maintenance and flight operations departments [69]. Furthermore, niche all-cargo operators can deploy their aircraft to destinations and at times that suit air cargo demand [98]. Cargolux is an example of one such niche operator.

4.3.2. Cargolux Airlines’ International Differentiated Product and Service Range

As a product, air cargo is extremely heterogeneous in nature [99]. Due to air cargo’s heterogeneous nature, a range of different transport solutions must be available for air cargo [100]. The air cargo products offered by airlines (and the integrators) are normally defined in terms of service patterns, such as general, priority, same day, and next day (the latter three are normally time definite services) [101].

Standard air cargo services emanate from the traditional, commodity-like segment of the air cargo market. Industrial and other products are transported by air with limited liability of airlines as to defined delivery times and other product features, for instance, damaged or lost cargo, where airlines offer a limited guarantee to shippers [102]. Cargolux’s standard product for general cargo is called CV Classic. This product satisfies the requirement of any air cargo shipment that requires fast, reliable, and expert handling throughout the transportation chain [103].

Express, time-definite air cargo services are used by shippers who are prepared to pay a premium for transportation services that enable them to minimize product inventory levels by providing time-definite deliveries [104]. Time-definite air cargo services are typically more expensive than general air cargo due to their higher boarding priority. Products shipped by express, time-definite air cargo services are generally very valuable, hence, delivery times are a critical factor [105]. Cargolux offers two discrete products for cargo that has a high degree of urgency: “CV Select and CV Select +.” The minimum shipment size for the CV Select product is 150 kgs [104,106]. The minimum shipment size for CV Select+ is 1650 kgs [107].

The air cargo mode enables shippers to ship highly perishable products to many distant markets that cannot be serviced by surface transport modes (rail/truck) or ocean transport. Hence, the air cargo mode is increasingly being used to transport a diverse range of perishable products, such as high-value horticultural products, including fruits, vegetables, flowers, and fresh cut fruits and vegetables. Chilled and frozen meat, dairy products, fish, and seafood are also commonly shipped by air cargo [108]. Such products require rapid transportation. This is because they are urgently required, or because they may otherwise perish or deteriorate when being transported over long distances [76]. Thus, as previously noted, there are a range of products shipped by air cargo that require cool chain or temperature-sensitive transportation [109]. To avoid physical perishability or spoilage, perishable goods must be shipped as expeditiously as possible to the consumer. Also, the use of air cargo ensures consumers receive the goods prior to the expiration of the good’s commercial life [108]. Cargolux has defined and implemented a special product that focuses on the transportation of perishable items—"CV Fresh” [110].

Prior to examining Cargolux’s pharmaceutical product, it is informative to briefly note the trends in pharmaceuticals shipped by air and their handling requirements. The change in market demographics and the greater accessibility and wider choice of drug products has led to a continued demand for healthcare products around the world. Speed to market is therefore critical and the healthcare industry is increasingly relying upon air cargo to ship their products [111,112]. The pharmaceutical industry markets drugs, which are licensed for use as medications and it is an industry that relies extensively on the air cargo mode to transport its raw products and carry its products to the end consumer [113] (p. 86). Pharmaceutical consignments are typically valuable and sensitive. The high value is due to the large quantities of regulated drugs and one-of-a-kind production batches for research and development (R&D). Importantly, pharmaceuticals are sensitive to temperatures; most drugs and other vaccines lose their effectiveness when exposed to ambient temperatures for too long a time period. In addition, pharmaceutical shipments are often subject to time constraints because of potential spoilage; therefore, they are most often air freighted over longer distances, as the elapsed journey time of ocean freight may be too long. To minimize losses, pharmaceuticals are therefore shipped in a cold chain. In cold chains, each chain actor provides cold storage at all parts of the consignment’s journey. In cold storage, every actor ensures that the temperature remains within a narrow range specified during the booking of the transport. These temperature regulations are most typically quite low (2–5 degrees Celsius), but room temperatures (15–25 degrees Celsius) may also be requested [114]. Handling and quality standards that are uniform across all stages of the supply chain are essential to ensure pharmaceutical products reach their destination in impeccable condition through an unbroken cool chain [114]. Temperature deviations and temperature excursions throughout the transportation cycle requires the establishment of a complete logistics process to maintain the shipment’s integrity [113]. Cargolux’s pharmaceutical product is called “CV Pharma” [115]. Cargolux aims to provide pharmaceutical customers with a complete cool-chain solution and Cargolux was the first airline to receive the Good Distribution Practices (GDP) Certification for Pharmaceuticals. Cargolux’s CV Pharma product is also fully compliant with the International Air Transport Association (IATA) Chapter 17 (Air Transport Logistics for Time and Temperature Sensitive Healthcare Products) regulations [114].

The carriage of live animals by air is a specialized niche of the air cargo industry [115], and it is a growing high value business [116]. Examples of the types of animals transported by air cargo include race horses [117], sharks, lions [118], and live pets [117]. Cargolux has developed a special product for the carriage of live animals—"CV Alive” [119].

Another niche market segment for which Cargolux has developed a specific product is the oversized or outsized air cargo market. Oversized is air cargo that does not fit into an airline’s standard unit load devices (ULDs) or on a specific aircraft [112]. According to Vyshehirsky [120] (pp. 140–141), outsized cargo is a unique good if they satisfy one or more conditions: “Cargo whose transportation is not possible without the development and use of specialist engineering and design solutions; cargo that requires loading and unloading to and from aircraft with the use of non-standard ground and aircraft loading equipment; and the transportation of cargo requiring special preparation of the aircraft and training for the flight crew”. Cargolux’s outsized cargo product is called “CV Jumbo” [121].

The air cargo mode is also used to carry ultra-high value products, for example, artwork, gold, jewelry, and precious stones [98]. Cargolux’s product for the safe carriage of high value goods is called “CV Precious” [122].

Cargolux has also developed a product for items that are powered, for example, cars and aircraft engines. This product is called “CV Power” [123].

The final discrete air cargo product offered by Cargolux is titled “CV Hazmat” [124]. This product is targeted at the carriage of dangerous goods. According to Sales [112] (p. 75), “dangerous goods are articles or substances that are capable of posing a risk to health, safety, and property or the environment and which are shown on the list of dangerous goods in the IATA Dangerous Goods Regulations (DGRs) (dangerous goods regulations) or which are classified according to those regulations”.

Table 2 presents a summary of the Cargolux International Airlines’ services/product offering vis-a-viz its principal all-cargo airline competitors. As can be observed in Table 2, Cargolux and its competitors all offer branded general cargo and pharmaceutical products. CargoLogic Air offers a branded dedicated aerospace and aircraft on ground service, an oil and gas, as well as a special humanitarian branded service offering (Table 1). Cargolux also competes in this market segment with its “CV Power” product. Nippon Cargo Airlines (NCA) is the only carrier that offers a special branded artworks service (Table 2), though the AirBridge Cargo “abc Valuables” service also includes art work consignments. Cargolux and its competitors, except for CargoLogic Air, all offer branded express and oversized cargo products. The hazardous or dangerous goods market segment is served by AirBridge Cargo, Cargolux, Nippon Cargo Airlines (NCA), and Polar Air Cargo. These airlines offer a branded dangerous goods solution that is in full compliance with the international regulations for the carriage of dangerous goods (Table 1). AirBridge Cargo, Cargolux, Nippon Cargo Airlines (NCA), and Polar Air Cargo all offer a branded product that is targeted at the oversize cargo market segment.

4.3.3. Cargolux Italia

In December 2008, Cargolux established a subsidiary, Cargolux Italia, based in Milan, Italy. The motivation for this venture was to capitalize on the reduced operations of Alitalia [146]. In 2009, Cargolux Italia launched its first flights following the approval of commence operations from the Italian civil aviation authority. Initially, the airline planned to operate one Boeing B747-400 freighter, on a twice-weekly Hong Kong and Milan service. This service also made a stop at Dubai on the eastbound service and Baku on the westbound service [147].

In mid-2014, both Cargolux Airlines International and Cargolux Italia were awarded the status of Authorized Economic Operator (AEO). This status was granted by the Luxembourg and Italian customs administrations on behalf of the Directorate General for Taxation and Customs Union of the European Commission. An Authorized Economic Operator (AEO) is recognized by all 28 EU member states as well as by third countries that have a mutual recognition agreement (MRA) with the EU. The AEO status was awarded following an in-depth procedure that included application, qualification, and on-site audit phases during 2013 [148].

In October 2015, Cargolux Italia and Nippon Cargo Airlines (NCA) entered into a strategic partnership agreement that involved code-sharing cargo flights from Milan Malpensa Airport to Osaka’s Kansai International Airport and from Malpensa to Tokyo’s Narita International Airport. The cooperation arrangements between the two airlines represented an improved service offering on the routes between Italy and Japan that also include two weekly flights from Milan Malpensa Airport to Osaka’s Kansai International Airport and four weekly flights from Milan Linate to Tokyo’s Narita International Airport. According to Cargolux Italia, these flights provide another fast and reliable freight lane for shippers in the Tokyo area to Europe [149].

Cargolux Italia operates flights from Milan to various destinations, including Hong Kong, Osaka, Zhengzhou, and Novosibirsk. These destinations are served by a fleet of four Boeing 747-400 freighter aircraft [150].

4.3.4. The Joint Sharing of Air Cargo Capacity with Alliance Partners

On 9 May 2017, Emirates SkyCargo (the air cargo division of Emirates Airline) and Cargolux signed a Memorandum of Understanding (MoU) for a strategic operational partnership in air cargo transportation. This agreement was the first agreement of its kind in the air cargo industry between a full-service network carrier (FSNC) and a specialized dedicated all-cargo airline [151,152]. The MoU allows the strategic cooperation between the two airlines who have complementary strengths and shared values for customer service excellence [153]. Under the agreement, Emirates SkyCargo will have access to Cargolux’s Boeing B747 freighters’ capacity, which will enable it to offer transport of outsized air cargo consignments requiring the nose-loading capability of the Cargolux Boeing B747 freighter aircraft. In addition, the MoU includes block-space and interline arrangements, which enable both partners to expand both their route networks [153]. A block space agreement (BSA) is a contractual arrangement between an airline and another third party, for example, another airline, whereby a specified amount of cargo space is allotted between two or more points on an airline’s network for a given period [154].

In June 2017, Emirates SkyCargo commenced freighter operations to Luxemburg, with the cargo traffic carried on these services to be handled at the same facility as used by Cargolux. Cargolux also announced that it would increase its flight frequencies to Dubai to improve connectivity [151,152]. A further benefit of the MoU for Cargolux was that it gained access to Emirates’ vast passenger belly-hold capacity on its widebody passenger fleet [152].

In October 2017, Cargolux Airlines and Emirates SkyCargo signed a codeshare partnership agreement for air cargo. This agreement allows both airlines to procure air cargo capacity on each other’s flights and subsequently offer it to their customers under their own airway bills and flight numbers. The codeshare agreement was applicable for air cargo capacity on both freighter and Emirates passenger services [155,156]. The new agreement built on the strong collaboration between the two airlines, including cargo handling agreements to facilitate the smooth transition of air cargo consignments between the two airlines hubs in Luxemburg and at Dubai World Central airports [69].

In November 2017, Cargolux and Japan-based Nippon Cargo Airlines (NCA) signed a strategic cooperation agreement that provided access to each carrier’s capacity through code-share and space swap arrangements. Under the terms of the agreement, Cargolux obtained access to NCA’s flights from Frankfurt-Hahn Airport to Tokyo’s Narita International Airport, whilst NCA gained access to Cargolux’s services from Luxembourg to Tokyo’s Narita International Airport. As part of this agreement, Cargolux Italia ceased its services to Narita International Airport, but retained its services to Osaka’s Kansai International Airport. Cargolux also announced its intention to further develop its operations at Komatsu Airport in Japan [157].

4.3.5. Cargolux International Airlines and Oman Air Strategic Cooperation Agreement

On 10 March 2015, Cargolux completed a strategic cooperation agreement with Oman Air. The cooperation agreement provided Cargolux with new sea/air cargo transport opportunities from Oman’s modern port facilities. Cargolux’s freighter aircraft will use Oman Air’s facilities at Muscat Airport. Under the terms of the agreement, Cargolux would introduce full freighter services from Luxembourg to Chennai in India via Oman. The first flight took place on 15 April 2015. The agreement also provided Cargolux with access to the lower-deck belly hold space on Oman Air’s passenger service [158] as well as the use of Oman Air’s facilities at Muscat, Salalah, and Sohar [159].

Due to the successful cooperation between Cargolux and Oman Air on the cargo flights to Chennai, and in the frame of the cooperation agreement signed in 2015, Cargolux and Oman Air introduced an additional destination in India, with two weekly flights to Mumbai, commencing on 8 March 2016 [160]. The extended agreement provided Oman Air with additional air cargo traffic sourced from throughout Cargolux’s extensive global network and Cargolux continued to have greater access to Oman Air’s passenger services [161].

The strategic cooperation agreement between Cargolux and Oman Air has helped Oman Air to expand its air cargo operations and develop the Sultanate’s logistics hub. A further benefit of the agreement is that it will help grow the economy of the Sultanate of Oman [162].

4.3.6. Cargolux International Airlines and Henan Civil Aviation and Investment Company (HNCA)

In 2013, Henan Civil Aviation Development and Investment Co Ltd., a China State-owned company located in the Henan province, purchased a 35% stake in Cargolux Airlines International [163]. Zhengzhou Xinzheng International Airport became Cargolux’s second hub airport [164,165]. The dual hub strategy is a major pillar of the commercial cooperation between Cargolux and HNCA [166] (p. 13).

Following a series of charter flights, Cargolux commenced scheduled services from Luxemburg to Zhengzhou Xinzheng International Airport on 24 April 2014 [166]. By the end of 2015, Cargolux was operating 13 services per week from its Zhengzhou Airport hub, and the airline had launched a trans-Pacific service between Zhengzhou and Chicago [167]. During 2017, Cargolux operated daily flights from Luxemburg to Zhengzhou Airport (and daily flights from Luxemburg to Hong Kong and Shanghai’s Pudong International Airport). The airline also opened two new routes in 2017 from Zhengzhou; Zhengzhou to Atlanta and Zhengzhou to London Stansted Airport. These new routes were designed to cater for the growing demand for trans-Pacific and European connections, respectively [69].

In 2017, Cargolux was the largest cargo airline in its Zhengzhou hub. The airline’s expansion in China also supports the “One Belt, One Road” strategy to promote the air corridor, the “Air Silk Road”, along this important route [69] (p. 8).

4.3.7. Cargolux 2025 Strategy

In 2017, Cargolux commenced a journey of transformation, with the introduction of the “Cargolux 2025 Strategy” [168,169]. This strategy is focusing on ensuring that Cargolux remains a sustainable, relevant, and competitive provider of quality services to its customers [169]. The scheme focuses on ensuring business sustainability through lean and flexible processes together with technological and digital enhancement that are in alignment with the company’s “lean and green” philosophy. The strategy is also focused on the development of people skills to ensure the company always remains financially sustainable. The company’s value offering to its customers is of prime importance and forms a key part of the strategy. Also, of equal importance will be the change associated with the digital revolution and the impact that this will have on Cargolux’s business and that of their customers. In addition, the implementation of the strategy aims to capitalize on and solidify the company’s market presence to ensure that Cargolux is the “Global Cargo Carrier of Choice” [69] (p. 10).

There are three pillars underpinning the “Cargolux 2025 Strategy”: Strategic Measures, Business Process Review, and the Digital Roadmap [69] (p. 11).

- Strategic Measures: The “Cargolux 2025 Strategy” emphasizes the airline having a flexible aircraft fleet that can take advantage of changing market conditions without incurring undue additional costs.

- Business Process Review: During 2017, Cargolux embarked on a company-wide transformation initiative to modernize work processes and to “future proof” the company, thereby ensuring its sustainability. This program contributes to job security and growth and includes training in more efficient work practices (lean). The Business Process Review is thus an important element within the Cargolux 2025 Strategy goals of digitalization and transformation. It highlights the workforce at every level of the organization as they identify small, incremental changes that can make a big difference to the organization. The Business Process Review ensures that Cargolux takes every available opportunity to strengthen the relationships with long-standing customers whilst also creating an unassailable value proposition for new ones.

- Digital Roadmap: An important tool of the Cargolux 2025 Strategy is a review program, which has mobilized staff and management to find better and even more productive methods for executing key business processes. The integrated digitalization of key business processes and the enhanced communication throughout the airline are welcomed by-products of this holistic and systematic review [69] (p. 60). Cargolux [69] (p. 60) have noted that “with each supply chain automation comes an even stronger connection with the customer”. The trend towards supply chain management (SCM) favours freighter aircraft over passenger airlines. This is because freighter aircraft can be more easily scheduled to satisfy the requirements of shippers, that is, for late night departures [170]. For air cargo shippers, services that are scheduled to depart in the late evening and at night tend to be more compatible with the firm’s daily production schedules [171].

4.4. Looking to the Future

The global air cargo industry is forecast to grow at 4.2% over the period of 2018 to 2037 [172]. It is envisaged that the primary drivers of the global air cargo growth will be increasingly driven by E-commerce and world economic growth [173]. According to Boeing [172] (p. 6), “Asia will continue to lead the world in average annual air cargo growth, with domestic China and intra–East Asia markets expanding 6.3 percent and 5.8 percent per year, respectively. Supported by faster-growing economies and growing middle classes, the East Asia–North America and Europe–East Asia markets will grow slightly faster than the world average growth rate. Middle East and Latin America markets connected to Europe and North America will grow at approximately the world average. In the more established and mature trade flows between North America and Europe, growth will be below the world average”. From an airline route network standpoint, freighter routes are highly concentrated on relatively few trade lanes, particularly in the world’s two largest trade routes, East Asia–North America and East Asia–Europe. In contrast, passenger networks are much broader in scope and often include destinations where there is limited or minimal air cargo demand. This difference in the distribution of passenger and cargo traffic explains the considerable load factor difference in the lower deck belly space of passenger services and freighters, which average approximately 30% and 70%, respectively. In addition, range limitations on fully loaded passenger aircraft and restricted passenger services to key air cargo airports make freighter operations essential. For these structural reasons, Boeing [172] has predicted that freighter aircraft will carry more than half of the world’s air cargo for the next 20 years.

In recent times, world air cargo growth has been influenced by the shortening of product life cycles, reductions in the times to ship goods to markets, and the trend towards the global sourcing of products [174]. In addition, more firms are increasingly recognizing that the higher costs of shipping goods by the air cargo mode can be offset by reductions in their inventory holding costs, warehousing, and packaging costs [175]. The rapid rise in e-commerce, and the growing importance of global companies’ supply chain strategies, have continually influenced the growth of the global air cargo market in recent years [176]. Consequently, air cargo also plays a substantial role in the modern-day supply chains [177]. Air cargo-carrying airlines need to remain cognizant of these changing trends and in so doing develop solutions (products/services) that will help them to become integrated into the air cargo supply chain.

5. Discussion

5.1. Findings

The case study has highlighted the various strategic options available to dedicated all-cargo airlines seeking to optimize their value proposition and capture a competitive advantage. The study found that the Cargolux Airlines competes in a very competitive industry and, to optimize its strategic position and satisfy air cargo shippers’ supply chain requirements, the airline has developed and implemented a wide variety of niche products aimed at the discrete air cargo market segments. The airline has in recent times consummated strategic cooperation agreements with Emirates SkyCargo, Nippon Cargo Airlines (NCA), and Oman Air. These agreements have enabled Cargolux to extend its network coverage and obtain access to additional air cargo capacities and destinations served by the Emirates Airline and Oman Air passenger aircraft fleet. Cargolux has also established a subsidiary airline—Cargolux Italia, based in Milan, that has focused on serving the very important Italian air cargo market. Most importantly, following the acquisition of a 35% shareholding in Cargolux by Henan Civil Aviation and Investment Company (HNCA) in 2013, Cargolux has adopted a dual hub strategy—Luxemburg Airport and Zhengzhou Xinzheng International Airport—which has enabled the airline to expand its route network and tap into the increasingly important China air cargo market.

In 2017, Cargolux commenced a journey of transformation with the introduction of the “Cargolux 2025 Strategy”, which is predicated on three pillars: Strategic Measures, Business Process Review, and the Digital Roadmap. A key objective of this strategy is to ensure that Cargolux Airlines International remains a sustainable, relevant, and competitive provider of quality services to its customers, both existing and new.

The case study has shown that to successfully compete in the global air cargo industry supply chain, airlines need to carefully design and offer products that are targeted at specific market segments, for example, the general air cargo market, the perishables, and the pharmaceutical market segments. Products need to satisfy the discrete shipping and handling requirements of the products being shipped by the air cargo mode. From a strategic policy perspective, a competitive advantage will be captured if shippers and customers deem the product/services being offered by an airline as suitable for the product(s) being shipped by the air cargo mode.

Dedicated all-cargo airlines as well as the combination airlines offering air cargo services/products have designed and now offer a range of product/services targeted at discrete market segments. The case study showed that Cargolux and its competitors offer a suite of products/services. Cargolux and its dedicated all cargo airline competitors offer a general cargo air cargo product and, except for CargoLogic Air, these airlines all offer branded express, perishables, and oversized air cargo products. Cargolux and its dedicated all-cargo airline competitors all offer a pharmaceutical cool chain solution. There are, however, other differences between the air cargo product/services offered. CargoLogic Air offers an aerospace and aircraft on ground (AOG), humanitarian aid, and oil and gas product/service. Nippon Cargo Airlines (NCA) offers an artworks product and, as previously noted, the AirBridge Airlines “abcValuables” product includes the handling and transportation of artworks. Cargolux and AirBridge Cargo both offer a valuable air cargo service.

Cargolux’s business success has been due to a range of factors: Achieving high load factors, good air cargo yields, high daily aircraft utilization rates [155], dedicated employees, high customer loyalty [169], nose loading capability of the airlines’ Boeing 747-400 and 747-8 freighter aircraft [90], a diversified product portfolio, partnership agreements with other major air cargo carrying airlines, and a global route network that serves world trade flows. A new all-cargo carrier entering the global air cargo market could incorporate these factors into their business model to ensure their business success.

5.2. Study Limitations

A limitation of the study was that the study focused on Cargolux Airlines’ dedicated all-cargo airline competitors. As noted earlier, around 56% of world air cargo is carried in freighter aircraft, with the balance carried in the lower deck belly-hold compartments on passenger services.

5.3. Future Work

Future work will look at a cross-sectional study to investigate the competitive position of the five leading dedicated all-cargo airlines—AirBridgeCargo Airlines, CargoLogicAir, Cargolux International Airlines, Nippon Cargo Airlines (NCA), and Polar Air Cargo Worldwide, in the global air cargo industry. Another future study will look at a cross-sectional analysis of the combination airlines who operate dedicated freighter aircraft air cargo service/product offering vis-à-vis those offered by dedicate air cargo airlines, including the integrated carriers, such as DHL Express and FedEx.

6. Conclusions

This paper has examined Cargolux Airlines International strategic position in the global air cargo supply chain. Despite the increasing importance of freighter aircraft in the global air cargo industry, there has been relatively limited research undertaken on this phenomenon. Thus, this study adds some valuable insights to the literature. The study was underpinned by a case study protocol and research framework that followed the recommendations of Yin [39] and applied “Porter’s Five Forces Model” for the first time in assessing the strategic position of a dedicated all-cargo airline in the global air cargo supply chain.

As noted in the case study, Cargolux International Airlines is a key player in the global air cargo supply chain. In 2017, the airline was ranked number seven in the world in terms of freight tonnes kilometres performed (FTKs). In addition, Cargolux is one of Europe’s leading all-cargo airlines.

The case study has highlighted the various strategic options available to dedicated all-cargo airlines seeking to optimize their value proposition and capture a competitive advantage. The study found that the Cargolux Airlines competes in a very competitive industry and, to optimize its strategic position and satisfy air cargo shippers’ supply chain requirements, the airline has developed and implemented a wide variety of niche products aimed at the discrete air cargo market segments. The airline has in recent times consummated strategic cooperation agreements with Emirates SkyCargo, Nippon Cargo Airlines (NCA), and Oman Air. These agreements have enabled Cargolux to extend its network coverage and obtain access to additional air cargo capacities and destinations served by the Emirates Airline and Oman Air passenger aircraft fleet. Cargolux has also established a subsidiary airline—Cargolux Italia, based in Milan, that has focused on serving the very important Italian air cargo market. Most importantly, following the acquisition of a 35% shareholding in Cargolux by Henan Civil Aviation and Investment Company (HNCA) in 2013, Cargolux has adopted a dual hub strategy—Luxemburg Airport and Zhengzhou Xinzheng International Airport—which has enabled the airline to expand its route network and tap into the increasingly important China air cargo market.

In 2017, Cargolux commenced a journey of transformation with the introduction of the “Cargolux 2025 Strategy”, which is predicated on three pillars: Strategic Measures, Business Process Review, and the Digital Roadmap. A key objective of this strategy is to ensure that Cargolux Airlines International remains a sustainable, relevant, and competitive provider of quality services to its customers, both existing and new.

As previously noted, Cargolux has defined and implemented a range of strategies that principally focus on niche market segments, for which the airline has developed unique products, the sharing of air cargo capacities with other key airlines, and optimizing its route network by following a two-hub strategy and supplementing flights with extensive road feeder services.

In the global air cargo in recent times, there has been a growing trend by airlines to develop and offer product specific air cargo services. Cargolux and its dedicated all-cargo airline competitors have followed this trend and now offer a portfolio of services to the discrete air cargo market segments. There are, however, differences in these airlines service offerings. CargoLogicAir, for example, offers an aerospace and aircraft on ground, humanitarian aid, and an oil and gas service offering. Japan-based Nippon Cargo Airlines (NCA) offers a unique artwork product solution. Cargolux and its competitors offer a general airport-to-airport air cargo product, a perishable product, and a pharmaceutical product. The airlines also compete in the dangerous goods or hazardous cargo market segment. Another important market is the oversized air cargo market segment; Cargolux AirBridge Cargo, Nippon Cargo Airlines (NCA), and Polar Air Cargo Worldwide all service this market segment with their unique service offerings. Cargolux competes against AirBridge Cargo Airlines in the valuables’ air cargo market segment.

Funding

This research received no external funding.

Conflicts of Interest

The author declares no conflict of interest.

References

- International Air Transport Association. Air Cargo: Enabling Global Trade. Available online: https://www.iata.org/whatwedo/cargo/Pages/index.aspx (accessed on 22 November 2018).

- Baxter, G.S.; Bardell, N.S. Can the renewed interest in ultra-long-range passenger flights be satisfied by the current generation of civil aircraft? Aviation 2017, 21, 42–54. [Google Scholar] [CrossRef]

- Cook, G.N.; Billig, B. Airline Operations and Management: A Management Textbook; Routledge: Abingdon, UK, 2017. [Google Scholar]

- Dresner, M.; Zou, L. Air cargo and logistics. In Air Transport Management: An International Perspective; Budd, L., Ison, S., Eds.; Routledge: Abingdon, UK, 2017; pp. 247–264. [Google Scholar]