Forecasting Commodity Prices: Looking for a Benchmark

Abstract

:1. Introduction

2. Futures Prices as a Benchmark for Nominal Prices

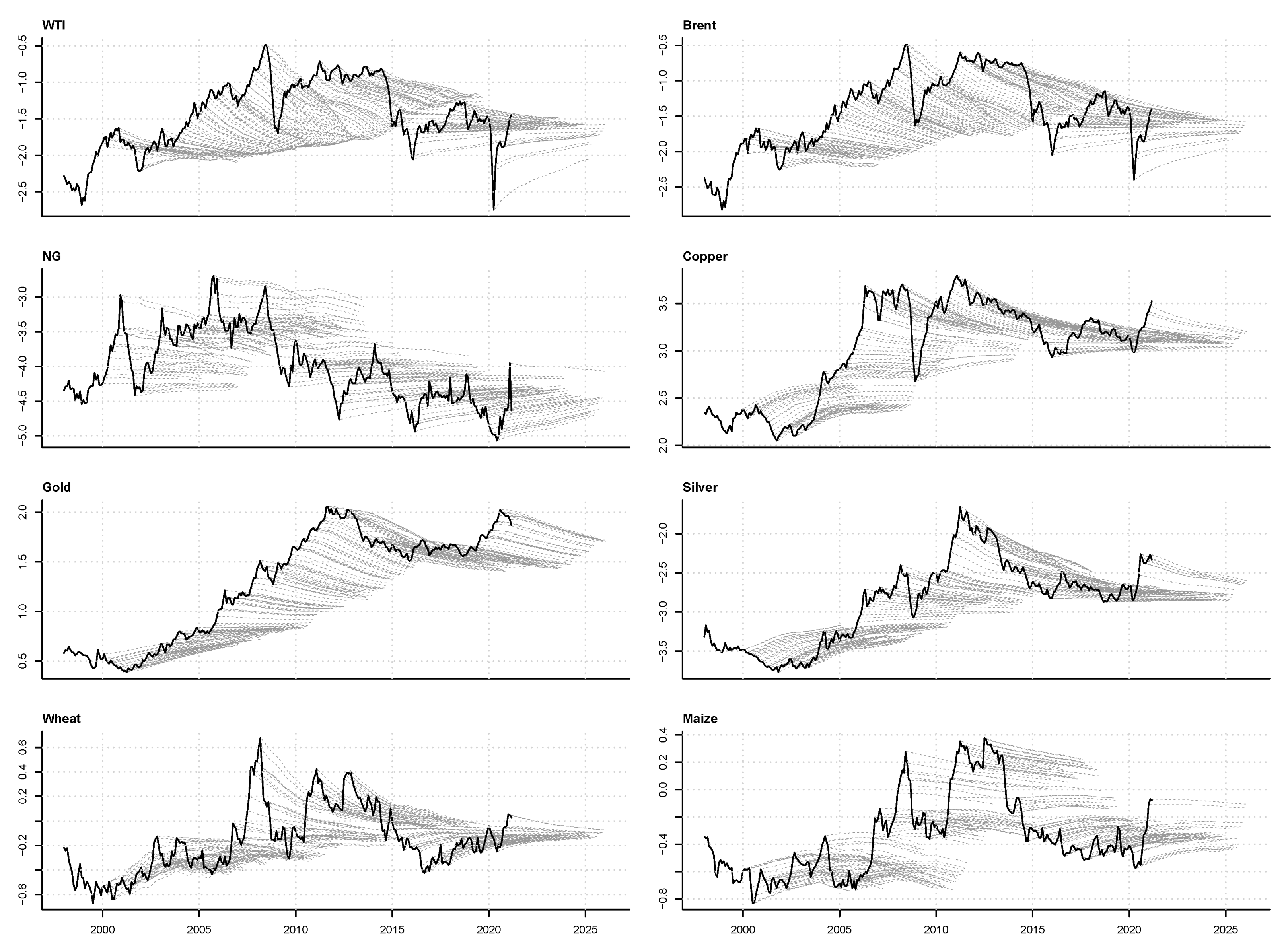

3. Local Projection as a Benchmark for Real Commodity Forecasts

4. Conclusions

Author Contributions

Funding

Data Availability Statement

Acknowledgments

Conflicts of Interest

Abbreviations

| MDPI | Multidisciplinary Digital Publishing Institute |

| DOAJ | Directory of open access journals |

| RW | Random Walk |

| LP | Local Projection |

References

- Basse, T.; Friedrich, M. Asset management in an inflationary environment—Are commodities a useful hedge? Z. Die Gesamte Versicherungswissenschaft 2010, 98, 653–661. [Google Scholar] [CrossRef]

- Zaremba, A.; Umar, Z.; Mikutowski, M. Inflation hedging with commodities: A wavelet analysis of seven centuries worth of data. Econ. Lett. 2019, 181, 90–94. [Google Scholar] [CrossRef]

- Working, H. Price Relations between July and September Wheat Futures at Chicago Since 1885; Wheat Studies of the Food Research Institute, Stanford University: Stanford, CA, USA, 1933. [Google Scholar]

- Fama, E.F.; French, K.R. Commodity Futures Prices: Some Evidence on Forecast Power, Premiums, and the Theory of Storage. J. Bus. 1987, 60, 55–73. [Google Scholar] [CrossRef]

- Geman, H.; Ohana, S. Forward curves, scarcity and price volatility in oil and natural gas markets. Energy Econ. 2009, 31, 576–585. [Google Scholar] [CrossRef] [Green Version]

- Symeonidis, L.; Prokopczuk, M.; Brooks, C.; Lazar, E. Futures basis, inventory and commodity price volatility: An empirical analysis. Econ. Model. 2012, 29, 2651–2663. [Google Scholar] [CrossRef] [Green Version]

- Fernandez, V. Further evidence on the relationship between spot and futures prices. Resour. Policy 2016, 49, 368–371. [Google Scholar] [CrossRef]

- Fernandez, V. Futures markets and fundamentals of base metals. Int. Rev. Financ. Anal. 2016, 45, 215–229. [Google Scholar] [CrossRef]

- Huang, B.N.; Yang, C.; Hwang, M. The dynamics of a nonlinear relationship between crude oil spot and futures prices: A multivariate threshold regression approach. Energy Econ. 2009, 31, 91–98. [Google Scholar] [CrossRef]

- Gulley, A.; Tilton, J.E. The relationship between spot and futures prices: An empirical analysis. Resour. Policy 2014, 41, 109–112. [Google Scholar] [CrossRef]

- Fernandez, V. Spot and Futures Markets Linkages: Does Contango Differ from Backwardation? J. Futur. Mark. 2016, 36, 375–396. [Google Scholar] [CrossRef]

- Almansour, A. Convenience yield in commodity price modeling: A regime switching approach. Energy Econ. 2016, 53, 238–247. [Google Scholar] [CrossRef]

- Shrestha, K. Price discovery in energy markets. Energy Econ. 2014, 45, 229–233. [Google Scholar] [CrossRef]

- Chang, C.P.; Lee, C.C. Do oil spot and futures prices move together? Energy Econ. 2015, 50, 379–390. [Google Scholar] [CrossRef]

- Modjtahedi, B.; Movassagh, N. Bias and backwardation in natural gas futures prices. J. Futur. Mark. 2005, 25, 281–308. [Google Scholar]

- Modjtahedi, B.; Movassagh, N. Natural-gas futures: Bias, predictive performance, and the theory of storage. Energy Econ. 2005, 27, 617–637. [Google Scholar] [CrossRef]

- Coppola, A. Forecasting oil price movements: Exploiting the information in the futures market. J. Futur. Mark. 2008, 28, 34–56. [Google Scholar] [CrossRef]

- Reichsfeld, D.A.; Roache, S.K. Do Commodity Futures Help Forecast Spot Prices? 2011; Unpublished work. [Google Scholar]

- Alquist, R.; Kilian, L. What do we learn from the price of crude oil futures? J. Appl. Econ. 2010, 25, 539–573. [Google Scholar] [CrossRef] [Green Version]

- Alquist, R.; Kilian, L.; Vigfusson, R.J. Chapter 8—Forecasting the Price of Oil. In Handbook of Economic Forecasting; Elliott, G., Timmermann, A., Eds.; Elsevier: Amsterdam, The Netherlands, 2013; Volume 2, Part A; pp. 427–507. [Google Scholar] [CrossRef]

- Chinn, M.D.; Coibion, O. The Predictive Content of Commodity Futures. J. Futur. Mark. 2014, 34, 607–636. [Google Scholar] [CrossRef] [Green Version]

- Fernandez, V. A historical perspective of the informational content of commodity futures. Resour. Policy 2017, 51, 135–150. [Google Scholar] [CrossRef]

- Pak, A. Predicting crude oil prices: Replication of the empirical results in “What do we learn from the price of crude oil?”. J. Appl. Econ. 2018, 33, 160–163. [Google Scholar] [CrossRef]

- Ellwanger, R.; Snudden, S. Futures Prices are Useful Predictors of the Spot Price of Crude Oil; Working Paper 2021-4; Laurier Centre for Economic Research and Policy Analysis, Wilfrid Laurier University: Waterloo, ON, Canada, 2021. [Google Scholar]

- Manescu, C.; Van Robays, I. Forecasting the Brent Oil Price: Addressing Time-Variation in Forecast Performance; ECB Working Paper Series 1735; European Central Bank: Frankfurt, Germany, 2014. [Google Scholar]

- Coroneo, L.; Iacone, F. Comparing Predictive Accuracy in Small Samples; Discussion Papers 15/15; Department of Economics, University of York: York, UK, 2015. [Google Scholar]

- Reeve, T.A.; Vigfusson, R.J. Evaluating the Forecasting Performance of Commodity Futures Prices; International Finance Discussion Papers 1025; Board of Governors of the Federal Reserve System (U.S.): Washington, DC, USA, 2011.

- Pesaran, M.H.; Timmermann, A. A Simple Nonparametric Test of Predictive Performance. J. Bus. Econ. Stat. 1992, 10, 461–465. [Google Scholar]

- Tilton, J.; Humphreys, D.; Radetzki, M. Investor demand and spot commodity prices. Resour. Policy 2011, 36, 187–195. [Google Scholar] [CrossRef]

- Lin, J.B.; Liang, C.C. Testing for threshold cointegration and error correction: Evidence in the petroleum futures market. Appl. Econ. 2010, 42, 2897–2907. [Google Scholar] [CrossRef]

- Mamatzakis, E.; Remoundos, P. Testing for adjustment costs and regime shifts in BRENT crude futures market. Econ. Model. 2011, 28, 1000–1008. [Google Scholar] [CrossRef] [Green Version]

- Beckmann, J.; Belke, A.; Czudaj, R. Regime-dependent adjustment in energy spot and futures markets. Econ. Model. 2014, 40, 400–409. [Google Scholar] [CrossRef]

- Rubaszek, M.; Karolak, Z.; Kwas, M.; Uddin, G.S. The role of the threshold effect for the dynamics of futures and spot prices of energy commodities. Stud. Nonlinear Dyn. Econom. 2020, 24, 1–20. [Google Scholar] [CrossRef]

- Deaton, A.; Laroque, G. Competitive Storage and Commodity Price Dynamics. J. Political Econ. 1996, 104, 896–923. [Google Scholar] [CrossRef] [Green Version]

- Fattouh, B.; Kilian, L.; Mahadeva, L. The Role of Speculation in Oil Markets: What Have We Learned So Far? Energy J. 2013, 34, 7–33. [Google Scholar] [CrossRef] [Green Version]

- Dvir, E.; Rogoff, K. Demand effects and speculation in oil markets: Theory and evidence. J. Int. Money Financ. 2014, 42, 113–128. [Google Scholar] [CrossRef] [Green Version]

- Dvir, E.; Rogoff, K.S. Three Epochs of Oil; NBER Working Papers 14927; National Bureau of Economic Research, Inc.: Cambridge, MA, USA, 2009. [Google Scholar]

- Kruse, R.; Wegener, C. Time-varying persistence in real oil prices and its determinant. Energy Econ. 2020, 85, 104328. [Google Scholar] [CrossRef]

- Adewuyi, A.O.; Wahab, B.A.; Adeboye, O.S. Stationarity of prices of precious and industrial metals using recent unit root methods: Implications for markets’ efficiency. Resour. Policy 2020, 65, 101560. [Google Scholar] [CrossRef]

- Wang, D.; Tomek, W.G. Commodity Prices and Unit Root Tests. Am. J. Agric. Econ. 2007, 89, 873–889. [Google Scholar] [CrossRef]

- Ghoshray, A. Are Shocks Transitory or Permanent? An Inquiry into Agricultural Commodity Prices. J. Agric. Econ. 2019, 70, 26–43. [Google Scholar] [CrossRef]

- Baumeister, C.; Kilian, L. Real-Time Forecasts of the Real Price of Oil. J. Bus. Econ. Stat. 2012, 30, 326–336. [Google Scholar] [CrossRef] [Green Version]

- Baumeister, C.; Kilian, L. Forecasting the Real Price of Oil in a Changing World: A Forecast Combination Approach. J. Bus. Econ. Stat. 2015, 33, 338–351. [Google Scholar] [CrossRef] [Green Version]

- Kilian, L.; Murphy, D.P. The Role Of Inventories And Speculative Trading In The Global Market For Crude Oil. J. Appl. Econ. 2014, 29, 454–478. [Google Scholar] [CrossRef]

- Funk, C. Forecasting the real price of oil. Time-variation and forecast combination. Energy Econ. 2018, 76, 288–302. [Google Scholar] [CrossRef]

- Snudden, S. Targeted growth rates for long-horizon crude oil price forecasts. Int. J. Forecast. 2018, 34, 1–16. [Google Scholar] [CrossRef]

- Degiannakis, S.; Filis, G. Forecasting oil prices: High-frequency financial data are indeed useful. Energy Econ. 2018, 76, 388–402. [Google Scholar] [CrossRef]

- Rubaszek, M. Forecasting crude oil prices with DSGE models. Int. J. Forecast. 2021, 37, 531–546. [Google Scholar] [CrossRef]

- Dooley, G.; Lenihan, H. An assessment of time series methods in metal price forecasting. Resour. Policy 2005, 30, 208–217. [Google Scholar] [CrossRef]

- Rubaszek, M.; Karolak, Z.; Kwas, M. Mean-reversion, non-linearities and the dynamics of industrial metal prices. A forecasting perspective. Resour. Policy 2020, 65, 101538. [Google Scholar] [CrossRef]

- Kwas, M.; Paccagnini, A.; Rubaszek, M. Common Factors and the Dynamics of Cereal Prices. A Forecasting Perspective; CAMA Working Papers 2020-47; Centre for Applied Macroeconomic Analysis: Canberra, Australia, 2020. [Google Scholar]

- Jorda, O. Estimation and Inference of Impulse Responses by Local Projections. Am. Econ. Rev. 2005, 95, 161–182. [Google Scholar] [CrossRef]

- Ca’ Zorzi, M.; Rubaszek, M. Exchange rate forecasting on a napkin. J. Int. Money Financ. 2020, 104, 102168. [Google Scholar] [CrossRef]

- Benmoussa, A.A.; Ellwanger, R.; Snudden, S. The New Benchmark for Forecasts of the Real Price of Crude Oil; Staff Working Papers 20–39; Bank of Canada: Ottawa, ON, Canada, 2020. [Google Scholar]

- Chen, Y.C.; Rogoff, K.S.; Rossi, B. Can Exchange Rates Forecast Commodity Prices? Q. J. Econ. 2010, 125, 1145–1194. [Google Scholar] [CrossRef] [Green Version]

- Gargano, A.; Timmermann, A. Forecasting commodity price indexes using macroeconomic and financial predictors. Int. J. Forecast. 2014, 30, 825–843. [Google Scholar] [CrossRef]

- Ciner, C. Predicting white metal prices by a commodity sensitive exchange rate. Int. Rev. Financ. Anal. 2017, 52, 309–315. [Google Scholar] [CrossRef]

- Pincheira-Brown, P.; Hardy, N. Forecasting base metal prices with the Chilean exchange rate. Resour. Policy 2019, 62, 256–281. [Google Scholar] [CrossRef]

- West, K.D.; Wong, K.F. A factor model for co-movements of commodity prices. J. Int. Money Financ. 2014, 42, 289–309. [Google Scholar] [CrossRef]

- Nakov, A.; Nuno, G. Saudi Arabia and the Oil Market. Econ. J. 2013, 123, 1333–1362. [Google Scholar] [CrossRef]

- Nakov, A.; Pescatori, A. Oil and the great moderation. Econ. J. 2010, 120, 131–155. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

| Commodity | Forecasting Horizon in Months | ||||

|---|---|---|---|---|---|

| 1 | 3 | 6 | 9 | 12 | |

| WTI | 0.979 | 0.951 | 0.958 | 0.947 | 0.936 |

| Brent | 0.990 | 0.973 | 0.972 | 0.962 | 0.962 |

| NG | 0.940 *** | 0.931 ** | 0.916 ** | 0.896 ** | 0.914 |

| Copper | 1.010 | 1.008 | 1.024 | 1.043 | 1.066 |

| Gold | 0.994 * | 0.976 ** | 0.940 ** | 0.905 ** | 0.869 ** |

| Silver | 0.998 | 0.994 | 0.988 | 0.981 | 0.975 |

| Wheat | 1.034 | 1.089 | 1.105 | N/A | N/A |

| Maize | 0.997 | 1.021 | 0.950 | 0.880 | N/A |

| Commodity | Forecasting Horizon in Months | ||||

|---|---|---|---|---|---|

| 1 | 3 | 6 | 9 | 12 | |

| WTI | 0.529 | 0.534 | 0.584 ** | 0.623 *** | 0.648 *** |

| Brent | 0.490 | 0.506 | 0.572 *** | 0.636 *** | 0.656 *** |

| NG | 0.565 *** | 0.561 *** | 0.588 *** | 0.628 *** | 0.652 *** |

| Copper | 0.510 | 0.557 | 0.572 * | 0.534 | 0.525 |

| Gold | 0.537 | 0.605 | 0.668 | 0.709 | 0.738 |

| Silver | 0.510 | 0.549 | 0.548 | 0.579 ** | 0.594 ** |

| Wheat | 0.525 * | 0.557 | 0.568 ** | N/A | N/A |

| Maize | 0.541 ** | 0.565 ** | 0.580 ** | 0.644 *** | N/A |

| Forecasting Horizon in Months | |||||||

|---|---|---|---|---|---|---|---|

| Commodity | 1 | 3 | 6 | 12 | 24 | 36 | 60 |

| WTI | 1.001 | 1.001 | 1.010 | 1.034 | 1.114 | 1.184 | 1.226 |

| Brent | 0.999 | 0.995 | 0.995 | 1.003 | 1.034 | 1.084 | 1.177 |

| NG | 0.998 * | 0.995 * | 0.991 * | 0.979 ** | 0.971 ** | 1.000 | 0.962 |

| Copper | 0.999 | 0.992 | 0.977 | 0.955 | 0.896 ** | 0.866 ** | 0.819 ** |

| Gold | 1.000 | 1.005 | 1.011 | 1.038 | 1.072 | 1.058 | 0.993 |

| Silver | 0.999 | 0.998 | 0.993 | 0.980 | 0.923 | 0.875 * | 0.790 ** |

| Wheat | 0.994 ** | 0.975 *** | 0.946 *** | 0.908 ** | 0.817 *** | 0.791 *** | 0.819 ** |

| Maize | 0.998 * | 0.993 * | 0.982 ** | 0.970 * | 0.939 ** | 0.919 ** | 0.974 |

| Forecasting Horizon in Months | |||||||

|---|---|---|---|---|---|---|---|

| Commodity | 1 | 3 | 6 | 12 | 24 | 36 | 60 |

| WTI | 0.449 | 0.500 *** | 0.514 *** | 0.523 *** | 0.524 *** | 0.493 *** | 0.451 |

| Brent | 0.520 *** | 0.492 ** | 0.534 *** | 0.531 *** | 0.519 *** | 0.457 *** | 0.426 |

| NG | 0.539 | 0.500 | 0.522 | 0.568 ** | 0.602 *** | 0.434 | 0.564 |

| Copper | 0.516 | 0.552 ** | 0.606 *** | 0.683 *** | 0.714 *** | 0.731 *** | 0.795 *** |

| Gold | 0.520 | 0.437 | 0.470 | 0.527 *** | 0.511 *** | 0.557 *** | 0.641 *** |

| Silver | 0.535 | 0.528 | 0.538 ** | 0.613 *** | 0.610 *** | 0.671 *** | 0.754 *** |

| Wheat | 0.555 ** | 0.571 *** | 0.618 *** | 0.675 *** | 0.727 *** | 0.790 *** | 0.749 *** |

| Maize | 0.516 | 0.552 ** | 0.538 ** | 0.543 ** | 0.645 *** | 0.680 *** | 0.359 |

| Forecasting Horizon in Months | |||||||

|---|---|---|---|---|---|---|---|

| Commodity | 1 | 3 | 6 | 12 | 24 | 36 | 60 |

| WTI | 0.998 | 0.992 | 0.990 | 0.986 | 0.962 | 0.945 | 0.908 |

| Brent | 0.997 | 0.990 | 0.983 | 0.975 | 0.948 | 0.927 | 0.888 |

| NG | 0.998 * | 0.995 | 0.989 | 0.976 | 0.953 | 0.948 | 0.862 |

| Copper | 0.999 | 0.990 | 0.977 | 0.954 | 0.893 ** | 0.833 ** | 0.737 ** |

| Gold | 1.006 | 1.016 | 1.028 | 1.046 | 1.051 | 1.045 | 1.027 |

| Silver | 1.000 | 0.998 | 0.995 | 0.985 | 0.943 | 0.904 | 0.828 ** |

| Wheat | 0.995 *** | 0.984 *** | 0.968 *** | 0.935 ** | 0.879 ** | 0.820 *** | 0.735 *** |

| Maize | 0.997 | 0.992 | 0.984 * | 0.967 | 0.934 * | 0.900 * | 0.843 ** |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Kwas, M.; Rubaszek, M. Forecasting Commodity Prices: Looking for a Benchmark. Forecasting 2021, 3, 447-459. https://doi.org/10.3390/forecast3020027

Kwas M, Rubaszek M. Forecasting Commodity Prices: Looking for a Benchmark. Forecasting. 2021; 3(2):447-459. https://doi.org/10.3390/forecast3020027

Chicago/Turabian StyleKwas, Marek, and Michał Rubaszek. 2021. "Forecasting Commodity Prices: Looking for a Benchmark" Forecasting 3, no. 2: 447-459. https://doi.org/10.3390/forecast3020027

APA StyleKwas, M., & Rubaszek, M. (2021). Forecasting Commodity Prices: Looking for a Benchmark. Forecasting, 3(2), 447-459. https://doi.org/10.3390/forecast3020027