1. Introduction

Childhood obesity is of particular concern as overweight and obese children have a high chance of becoming obese adults and have an increased risk of later cardio-metabolic morbidity and premature mortality [

1]. An increase in the total number of years spent in an obese state increases the risk for cardiovascular, cancer and all-cause mortality, emphasising the increased benefits of targeting the prevention of obesity in children and young people [

2]. Importantly, targeting the prevention of obesity in children may be far less expensive than having to treat the consequences of obesity later in life [

3].

Current initiatives to improve food choices in Australia have focussed on voluntary measures in the form of self-regulation of television advertising to children and food labelling [

4,

5,

6]. These measures have been shown to be inadequate with deregulated food markets linked to increased fast food transactions and increasing body mass index (BMI) with the sharpest increases occurring in Canada and Australia (1999–2008) [

7]. In contrast, countries with stringent food market regulation such as Italy, the Netherlands and Greece had relatively small increases in both fast food consumption and BMI [

7]. One regulatory strategy with considerable potential to reduce the consumption of obesogenic foods, and therefore obesity, is taxation [

8,

9]. Using taxation to increase the price of energy-dense nutrient-poor foods is likely to have an impact of food consumption patterns in Australia. However, it is important to first clearly define what categories of food contribute most to weight gain and identify whether a tax on these items is likely to be practical and acceptable.

In 2010, the Australian government commenced the development of a National Food Plan (NFP) aimed at integrating food-related policies in Australia [

10]. The NFP has been criticised as having a strong focus on economic growth and food production rather than on promoting the availability of affordable and nutritious food to help consumers make healthier food choices [

11]. The Independent Panel for the Review of Food Labelling Law and Policy presented a report in which it recommended the development a national nutrition policy to establish monitoring and food labelling systems in Australia [

12]. Although there is strong support for a National Nutrition Policy [

11], some of the key concerns about the policy include the lack of evidence on the effectiveness of the star rating labelling system, the length of time taken to implement the labelling changes and the reliance on food industry to voluntarily implement label changes [

13].

Public engagement in policy decisions is increasingly viewed as an essential part of decision making in the health area given that the public are the key stakeholders of any decisions that are made [

14]. Members of the public can provide their view of the values and priorities of their community. This allows for both improving the trust and confidence in the health system and ensuring that decisions fit with the ideals of a participatory democracy [

15]. Knowing the public viewpoint is also important for policy implementation as Governments are often unwilling to make unpopular decisions, particularly those involving taxes. A Citizens’ Jury is one method of public deliberation that offers a relatively high level of participation by public participants in policy decisions [

16,

17,

18]. It is a well-accepted approach for engaging the public in decision-making on a specific topic, including in the area of health policy [

19,

20,

21,

22,

23]. As a deliberative form of pubic engagement, it is well suited to investigating public opinion around topics that may be sensitive or divisive, such as the role of taxation in obesity prevention. This paper describes the findings and recommendations of a Citizens’ Jury exploring pubic perspectives on taxation of food and drinks as a preventive strategy for childhood obesity.

3. Results and Discussion

3.1. Profile of the Jury

Demographic characteristics of the 13 citizens selected to participate in the Citizens’ Jury are presented in

Table 2. The jurors broadly reflected the diversity in the community and were from a diverse range of ages, family situations, educational, employment and household income levels.

Table 2.

Demographic characteristics of the jurors.

Table 2.

Demographic characteristics of the jurors.

| Demographic Characteristic of Jurors | N (%) |

|---|

| Gender | |

| Male | 5 (38) |

| Female | 8 (62) |

| Age | |

| 18–34 years | 1 (8) |

| 35–44 years | 2 (15) |

| 45–54 years | 3 (23) |

| 55–64 years | 4 (31) |

| <65 years | 3 (23) |

| Children under 18 years living at home | |

| 0 children | 9 (69) |

| 1 child | 1 (8) |

| 2 or more children | 3 (23) |

| Born overseas | 5 (38) |

| Speaks a language other than English at home | 0 (0) |

| Indigenous | 0 (0) |

| Education | |

| Did not complete high school | 2 (15) |

| Up to year 12 | 3 (23) |

| Diploma or trade certificate | 7 (54) |

| Bachelor’s degree or higher | 1 (8) |

| Employment | |

| Full-time | 5 (38) |

| Part-time | 4 (31) |

| Unemployed | 0 (0) |

| Not in labour force/Retired | 4 (31) |

| Annual household income | |

| <$42,000 | 4 (31) |

| $42,000–$130,000 | 7 (54) |

| >$130,000 | 1 (8) |

| Not stated | 1 (8) |

3.2. Jury Verdicts

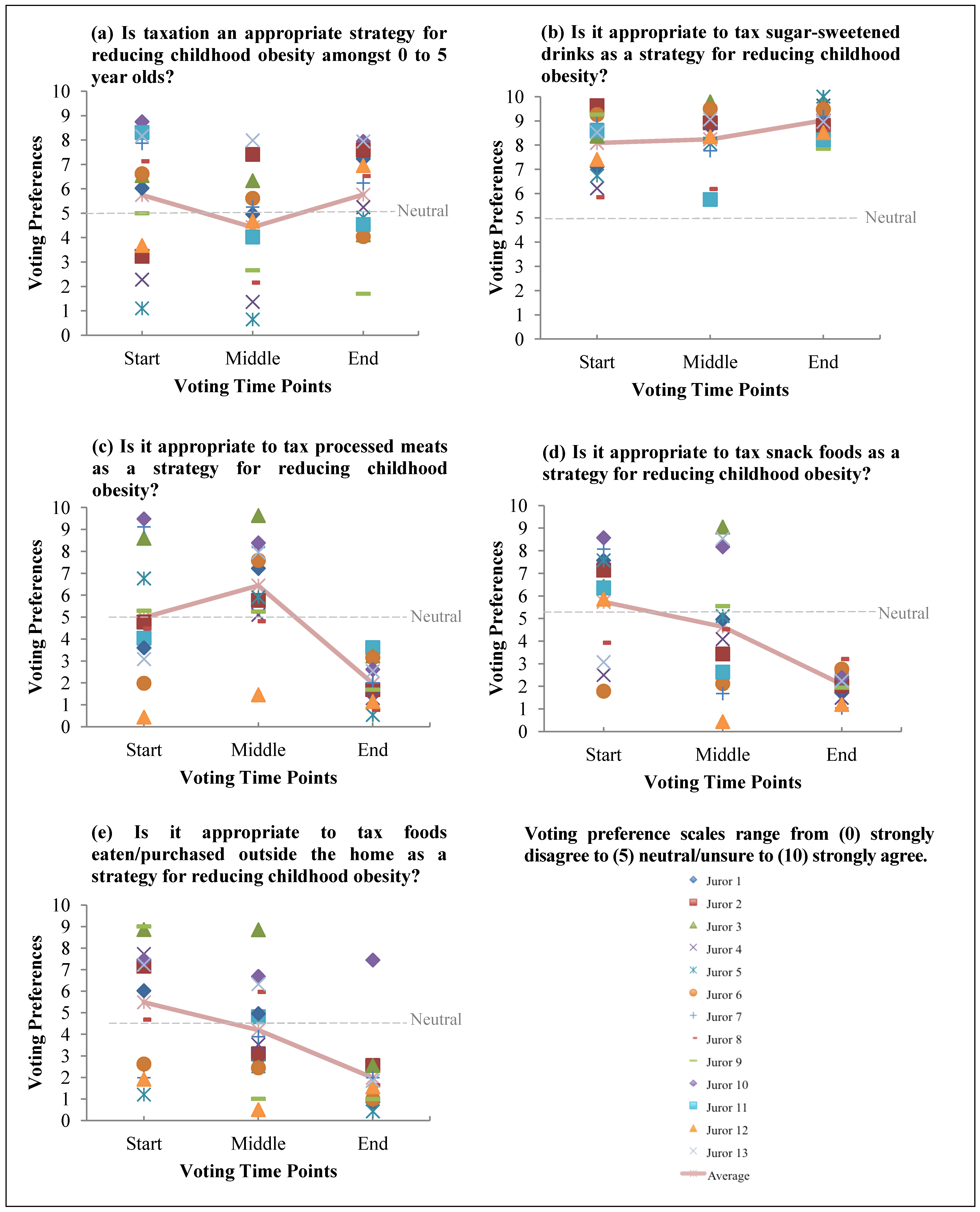

The individual and average voting preferences of the jurors for each of the questions across the three time points are illustrated in

Figure 1 and the verdicts are detailed in the sections below.

3.2.1. Question One: “Is Taxation an Appropriate Strategy for Reducing Childhood Obesity amongst 0 to 5 Year Olds?”

The jurors did not reach a unanimous decision on the overarching question of whether taxation is an appropriate strategy for reducing childhood obesity. Initially, there was wide variation in preferences amongst the jurors; however, by the end of the jury deliberation process half of the jurors were in favour of a tax whilst the remaining jurors were unsure (

Figure 1a). Many of the jurors felt that the question was both complex and ambiguous, that is, it was unclear what foods would be taxed. The jurors also stated that the evidence was insufficient to make a decision.

Whilst the jurors felt that a tax is likely to discourage consumption, and therefore reduce obesity rates in children, a number of concerns were raised. Jurors were most concerned about how the revenue that will be raised from the tax would be used. Jurors were unanimous in wanting all revenue generated from the taxation on food and drinks to be directed towards nutrition education and physical activity interventions for children and subsidies for fresh food. They were also concerned about equity issues and whether such a tax would unfairly disadvantage those on low incomes.

3.2.2. Question Two: “Is It Appropriate to Tax Sugar-sweetened Drinks as a Strategy for Reducing Childhood Obesity?”

All jurors strongly agreed that a tax on sugar-sweetened drinks is appropriate. At the start of the Citizens’ Jury process, the jurors were supportive of a tax on sugar-sweetened drinks and their support appeared to increase and consolidate by the end (

Figure 1b). Jurors without tertiary education had lower scores at the start than those with College education (6.9

vs. 8.8) but they reached consensus by the end (9.1

vs. 9.0). The jurors agreed that sugar-sweetened drinks were easily defined and a major contributor to childhood obesity, therefore taxation was a suitable strategy for these products. The jurors felt that the tax needed to be large enough to change consumer behaviour. The majority agreed that a 50% tax was appropriate and some argued for 100% (or doubling of current prices) with most wanting an immediate introduction of taxation. The jurors did not consider equity for those with low incomes to be an issue as such drinks provide little to no health benefits and therefore can be completely removed from the diet.

The jurors were undecided whether diet drinks should be included in this category. It was however agreed that the consumption of such products should not be promoted as there may be health issues associated (e.g., increased dental caries). The jurors felt that packaged unflavoured water should be reduced in price. There were concerns that the full tax may not be passed on to consumers by companies as they may spread the load across all types of sweetened and non-sweetened drinks or there may be unintended consequences such as heavy promotion of diet drinks and non-sweetened drinks with high levels of naturally occurring sugar (e.g., fruit juices). Consequently, in addition to the taxation on sweetened fruit juices, some of the jurors wanted non-sweetened fruit juice (including 100% fruit juice) to also be included in the tax due to the high levels of naturally occurring sugar in such drinks.

3.2.3. Question Three: “Is It Appropriate to Tax Processed Meats as a Strategy for Reducing Childhood Obesity?”

The jurors opposed a tax on processed meats as they felt that the evidence presented did not conclusively indicate that processed meats were a contributing factor to childhood obesity. The jurors highlighted that there are many different types of processed meats and that some types were healthier than others.

Figure 1.

Individual and average voting preferences at three time points for the five questions: (a) Taxation. (b) Sugar-sweetened drinks. (c) Processed meats. (d) Snack foods. (e) Foods eaten/purchased outside the home.

Figure 1.

Individual and average voting preferences at three time points for the five questions: (a) Taxation. (b) Sugar-sweetened drinks. (c) Processed meats. (d) Snack foods. (e) Foods eaten/purchased outside the home.

As such, the jurors agreed that the types of processed meats that were amenable to taxation were difficult to define and it was, therefore, deemed that taxation was not an appropriate strategy for this category of products. Initially, there was a wide variation in the level of agreement for the introduction of taxation on processed meats with jurors shifting their preference to increased opposition to the tax at the end of the Citizens’ Jury process (

Figure 1c).

The jurors felt that more research into the effects of children consuming processed meats is warranted and they strongly believed that the public should be informed of the health consequences of consuming additives commonly found in processed meats such as salt, fat and preservatives. The jurors recommended that the levels of salt and preservatives in products such as processed meats should be reduced and that more nutritional information including the levels of preservatives contained in the product should be included on the food packaging labels. The jurors also believed that education on the effects of consuming processed meats, and processed foods in general, should be given to children from an early age.

3.2.4. Question Four: “Is It Appropriate to Tax Snack Foods as a Strategy for Reducing Childhood Obesity?”

The jurors unanimously agreed that a tax on snack foods was not an appropriate strategy to reduce childhood obesity. There was a wide variation in the level of agreement for a tax on snack foods at the start of the Citizens’ Jury (

Figure 1d). The jurors’ opposition to the tax on snack foods appeared to both increase and consolidate over the course of the deliberations. At the end of the Citizens’ Jury, the jurors had a moderately strong opposition to the tax as the category of snack foods is not yet well defined. The jurors believed that the current regulation of snack foods is inadequate and emphasised the need for improvements to be made in regards to nutritional labelling and advertising of snack foods to children. Specifically, jurors recommended that nutritional labelling should include more graphical representations of the sugar content as well as the introduction of the use of a “traffic light” labelling system. The jurors believed that these suggested labelling systems would help consumers to identify healthier food choices. In addition, the jurors believed that such regulation would likely lead to food companies improving the recipes and serving sizes of their snack food products. Furthermore, the jurors stated that they were open to a discussion about the possibility of introducing a tax on the unhealthy snack foods as identified through a ‘traffic light’ labelling system. In regards to advertising of snacks foods, the jurors supported increased regulation of all forms of advertising snack foods to children. This included advertising from media sources to sponsorships of children’s activities to shop displays. The jurors felt that there needs to be increased health messages and advertising of healthy food choices for children.

3.2.5. Question Five: “Is It Appropriate to Tax Food Eaten outside the Home (Purchased outside the Home) as a Strategy for Reducing Childhood Obesity?”

The jury did not support taxation on foods eaten/purchased outside the home. The jurors appeared to have held a wide variation in the levels of support for a tax on these foods throughout the Citizens’ Jury process. Following the final deliberations, however, the jurors reported a moderate to strong opposition of a tax on foods eaten/purchased outside the home with the exception of one juror who moderately supported a tax. The jurors opposed this tax as they believed that the current definition was too broad and difficult to define. Specifically, the jurors highlighted that the definition did not account for healthy foods that are eaten/purchased outside the home and for unhealthy foods that are purchased outside the home and eaten inside the home. The jurors believed that regulation in the form of nutritional labelling was appropriate for this category of foods, supporting a “traffic light” labelling system aimed at helping consumers choose healthier food options. Half of the jurors supported a tax on unhealthy foods eaten/purchased away from home as determined by a ‘traffic light’ labelling system.

3.3. Recommendations from the Jurors about Strategies Other Than Taxation

The jurors recognised that food taxation was only one of several strategies necessary to help prevent and reduce childhood obesity in Australia. The jurors proposed a number of strategies that were required in conjunction with taxation to help address childhood obesity as they were reluctant to rely only on taxation noting the importance of informing and supporting healthy consumer decisions. Both education-based strategies and the introduction of regulation were believed to be important in order to help consumers make healthier choices. The types of education-based strategies proposed by the jurors were not specified. The jurors, did, however identify the need for regulation in regards in improved product nutritional labelling and increased access to affordable healthy food options. Specifically, the jurors proposed the introduction of a comprehensive nutritional labelling system, such as “traffic light” labelling, which was regarded as essential in helping consumers identify healthier food options. In addition, the jurors identified the need for clearer labelling of specific nutrients (i.e., sugar, salt, fat, etc.) and recommended pictures to be placed on the front of food packages to show the number of teaspoons of the nutrients contained in the product. Furthermore, the jurors believed that access to affordable healthy food options was important to contain the obesity crisis highlighting the need for increased availability of healthier foods within outlets and the need for healthier foods to be cheaper than, or at least the same price as, unhealthy food options. Half of the jurors suggested the regulation of the distribution of the types of food outlets within a geographical area. The jurors concluded with the recommendation that more research in the area of childhood obesity prevention is required in order to address childhood obesity.

3.4. Discussion

There was strong support for taxation on sugar-sweetened drinks as an obesity-prevention strategy. This support was evident throughout the deliberations and became stronger by the time the final vote was cast. These results suggest that there may be broad support in the community for the introduction of a tax on sugar-sweetened drinks, particularly if the proposal was accompanied by front-of-pack labelling and increased nutrition education initiatives. This information; similar to what was presented to the jurors; would allow citizens to make informed decisions and judgements about the appropriateness of taxation as a strategy to address childhood obesity.

The jurors considered that the likelihood of public support would be increased if taxation revenue was used to promote healthy eating and/or subsidise healthy food alternatives and if the tax was high enough to change consumption patterns of parents. Taxation on sugar-sweetened drinks has already been implemented in a number of countries [

27,

28,

29]. Evidence has suggested that taxes need to be non-trivial in order to change behaviour [

30] and may need to be higher than 10% to have an impact on consumption [

29,

31]. However, even small taxes that may not affect sales raise significant revenues to fund public health activities [

32].

The jury did not support taxation on other categories of food primarily because they included both obesogenic and non-obesogenic options. Jurors acknowledged the difficulties associated with defining healthy and unhealthy foods and the pragmatic implications of this uncertainty for taxation policy. The difficulties associated with taxation of these food categories were highlighted in 2012 when Denmark repealed an unpopular “fat” tax due to public and industry pressure [

33].

There was strong support for other types of regulation to assist parents in making healthy choices for their children, indicating that taxation alone was not considered a sufficient strategy. Clear front-of-pack labelling was presented by one of the expert witnesses and was a key recommendation made by the jury, even though food labelling was not the focus of the Citizens’ Jury. In support of this recommendation, recent research has demonstrated that 96% of Queenslanders were unable to identify healthy and unhealthy food because of confusing and misleading labelling practices [

34]. The jurors believed that a clear labelling system should be developed and implemented in Australia, if parents are to be supported to make healthy choices for their children.

The recommendations made by this jury support previous strategies identified by public health researchers. They described several conditions that needed to be met for taxation to be successful, including making it clear that the aim of taxation is to reduce consumption and that the revenue generated from the taxation should be allocated to publicly-supported health promotion initiatives. Similar conclusions have been drawn in the literature on this topic [

35].

This study is not without limitations. Most notably, there may have been a selection bias in the sample as the jurors were chosen from a pool of individuals that were both interested in participating in the Citizens’ Jury and were available over two days of a weekend. Further, the Citizens’ Jury may not have been representative of the Australian population as all of the jurors resided in the local community. Whilst Citizens’ Juries are a well-accepted approach for engaging the public in decision-making, it is important to note that the findings of the current study are from a small group of jurors and may not reflect the views and opinions of the broader public. Moreover, the method of the presenting information in the form of evidence from expert witnesses is typical of the Citizens’ Jury process however may not be reflective of the usual approach that is adopted when introducing new policies to the general public. Although it is a standard process to present a number of questions to jurors in the Citizens’ Jury [

19], it is possible that the presentation of five questions may have yielded different findings than if the jurors had deliberated on a single question. Views from the peak industry groups in Australia (the Australian Food and Grocery Council and the Australian Beverages Council) were only presented from media sources (previous print and radio interviews) as both groups declined participation in the jury process. Finally, the jurors reported that the expert witnesses needed more time to present the information and that the categories of foods (

i.e., snack foods; and foods eat/purchased outside the home) were too broad and not well defined.

Future Citizens’ Juries on this topic should ensure that expert witnesses are given adequate time to present sufficient evidence to the jurors, to help jurors make improved decisions and to allow for time for questions. In addition, the questions posed to the jurors should be carefully constructed and clearly defined in order to help jurors deliver meaningful verdicts. Clear definitions of obesogenic foods and drinks are essential to assist policy makers in adopting preventive strategies to address childhood obesity. Many of the recommendations from the jurors were outside the scope of the current Citizens’ Jury. As current policies directed at self-regulation of the food industry in Australia appear to be slow and are not designed to take into account public preferences, it may be useful to conduct a Citizens’ Jury specifically on food labelling and other regulation alternatives.

4. Conclusions

In summary, this Citizens’ Jury has suggested that the Australian public would support the introduction of a sugar-sweetened drink taxation. However, the acceptability of such a tax will depend on the way in which proceeds from the taxation revenue are allocated. Importantly, our study has shown that the provision of unbiased expert information about childhood obesity and taxation can increase community support for policy change, even in areas such as taxation on sugar-sweetened drinks that may be sensitive or even divisive. Finally, changes to current food and drink labelling methods were strongly supported by all members of the Citizens’ Jury. These reforms should be considered by government to reduce the future societal costs of obesity.

{kind=link}