How Do Urban Land Expansion, Land Finance, and Economic Growth Interact?

Abstract

:1. Introduction

- (1)

- The relationship between urban land expansion and land finance: Some scholars have studied these factors by using the panel Granger causality-test method and found that land development is the Granger causality of the growth in local fiscal revenues [16]; in contrast, only a reverse causal relationship exists in the stage of advanced industrialization [17]. Land-transfer fees significantly encourage urban land expansion, whereas land taxes could theoretically hinder it [18]. Studies on the effects of land finance on urban land expansion have shown that the pursuit of land finance by local governments has encouraged the expansion of urban construction land [19,20,21].

- (2)

- The relationship between urban land expansion and economic growth: The research in this field falls into two categories. The first one focuses on the contribution of land to economic growth. According to the literature, the urban construction land [22], the conversion of rural land to urban use [5], as well as the expansion of construction land [23,24,25], exhibit significant effects on economic growth. Yang et al., (2020) also found a positive relationship between the industrial land-transfer price and economic growth rate [26]. The second category considers economic growth as a driving factor of urban land expansion. Annual growth in GDP per capita drives half of the observed urban land expansion in China [7]. Tan et al. [27] and Liu et al. [28] obtained empirical results and demonstrated that the speed of urban land expansion is closely related to rapid economic development. However, Li et al. found a negative contribution of economic growth to the growth of construction land [29]. Urban spatial expansion arises mainly from the following three powerful forces: growing population, rising incomes, and falling commuting costs [1]. Urban sprawl has been significantly associated with urban population density, GDP per capita, and industrial structure [9].

- (3)

- The relationship between economic growth and land finance: Since the 1990s, land finance has become increasingly important and continues to accelerate China’s urbanization and economic growth [13]. However, sustainable economic growth demands significant investments in infrastructure [30], which are provided as land-based finance to local governments [31,32] through the main channel of land conveyance revenue, which serves as a signal of the credit quality of the local governments [33], who have access to more loans from banks and investments for their economic advancement. Moreover, their reliance on land finance has bolstered the real-estate industry in China, making it a pillar industry [34]. However, Hou et al., (2021) showed that land finance has a significant inhibitory effect on the growth of the green economy [35]. Lin and Zhang (2015) found an inverse U-shaped relationship between the importance of land commodification to municipal finance and the level of urban economic growth [36].

2. Conceptual Framework

- (1)

- To raise land finance, local governments can supply more plots of stock construction and newly expanded land to the market. Stock construction land includes land recovered (retracted) due to the expiry of rights, land requisitioned by the government, and land abandoned voluntarily by enterprises or individuals. The newly expanded land primarily consists of land expropriated from rural collectives. In general, state-run stock urban land plots are relatively close to commercial centers, whose surrounding superior infrastructures and locations offer higher prices than the plots of newly expanded land. Since the reform of the tax-sharing system, local governments have played crucial roles in accumulating land revenues and financing urban expansion by property development, as well as by the subsidization of manufacturing firms in industrial parks, while financing infrastructure extending to the urban fringes [14].

- (2)

- Land finance drives urban land expansion. To obtain more revenue and accelerate economic growth, local governments often supply land to the market in seemingly contradictory ways. Industrial land is usually sold to enterprises at the lowest possible prices. In regions with a stronger dependence on land finance, local governments tend to sell commercial and residential land in highly marketable ways to rapidly compensate for fiscal deficits [39]. The supply of industrial land is conducive to industrialization, thus helping cities to attract more immigrants, develop tertiary industries, and increase the demand for residential and commercial land. Furthermore, urban sprawl in China is manifested in multiple forms, such as leapfrogged industrial parks [21], which, with other industrial land, are distributed in the outskirts of cities, thus directly reflecting the characteristics of urban land expansion.

- (3)

- Economic growth drives urban land expansion by generating demand. Economists believe that population growth, rising household incomes, and transportation improvements are responsible for this spatial growth [42], which can explain urban sprawl in the United States and developing countries, such as China [43]. Economic growth has affected all three variables. First, economic growth drives the development of nonagricultural industries in urban areas, which attracts many rural people to migrate to cities. Furthermore, economic growth promotes scientific and technological progress, increases agricultural labor productivity, and enables surplus laborers in rural areas to seek employment opportunities in cities. Second, economic growth increases household incomes, which foster urban growth because urban residents demand more living spaces as they become more affluent [1]. Finally, only economic growth can help cities to afford better, cheaper, and more convenient public transportation, which leads to the settling of more residents in the outskirts of cities as the optimal choice between transportation and housing costs, thereby stimulating the expansion of the cities.

- (4)

- Urban land expansion promotes economic growth through the contribution of input factors. In neoclassical theories of endogenous economic growth, the roles of scientific and technological progress are valued; however, land is usually not included because of its fixed supply and substitution by other factors. China’s urban economy differs from the developed economy because local governments can sell and lease land-use rights, and then retain revenues. Moreover, they have the right to expropriate rural collective land. The effects of urban land expansion on economic growth through the contribution of inputs are as follows: First, the expansion of urban land leads to the increase in the available spaces for residents and industries, thus concentrating labor, capital, and other factors in urban areas, which benefits the development of industry and promotes economic growth. Second, the expansion of urban land changes economics of scale and agglomeration, which affects land prices and the costs of infrastructure construction, transportation, and public services, thus influencing economic growth [44].

- (5)

- Land finance influences economic growth through investment. In addition to private investment, government investment is also an important driving force. Under financial marketization, the government must find ways to raise large amounts of funds. When obtaining loans from banks, governments should possess assets with strong value preservation and appreciation for collateral value. Land and land revenues owned by local governments are excellent collateral. The continuous growth of land finance and the resultant increase in local financial revenue have contributed to infrastructure construction and the supply of public services, through which local governments have gained significant momentum in accelerating urbanization, attracting more investments, and promoting local economic development [45,46].

- (6)

- Economic growth facilitates the development of the real-estate market in order to increase the scale of land finance. Rapid economic growth has improved the people’s living standards, so that they can afford larger houses, higher-quality commodities, and more luxury goods, which stimulates the demand of enterprises for land. In the case of a relatively short supply of urban land, local governments sell land to obtain as much revenue as possible. Second, hikes in land prices driven by economic growth also increase the prices of buildings, which in turn increase tax revenues on land and building transactions, thereby also increasing land finance.

3. Model Settings and Data Description

3.1. Model Settings

3.2. Data and Variables

4. Empirical Results and Discussion

4.1. Panel Unit-Root Test

4.2. PVAR Model Regression Analysis

4.3. Granger Causality Test

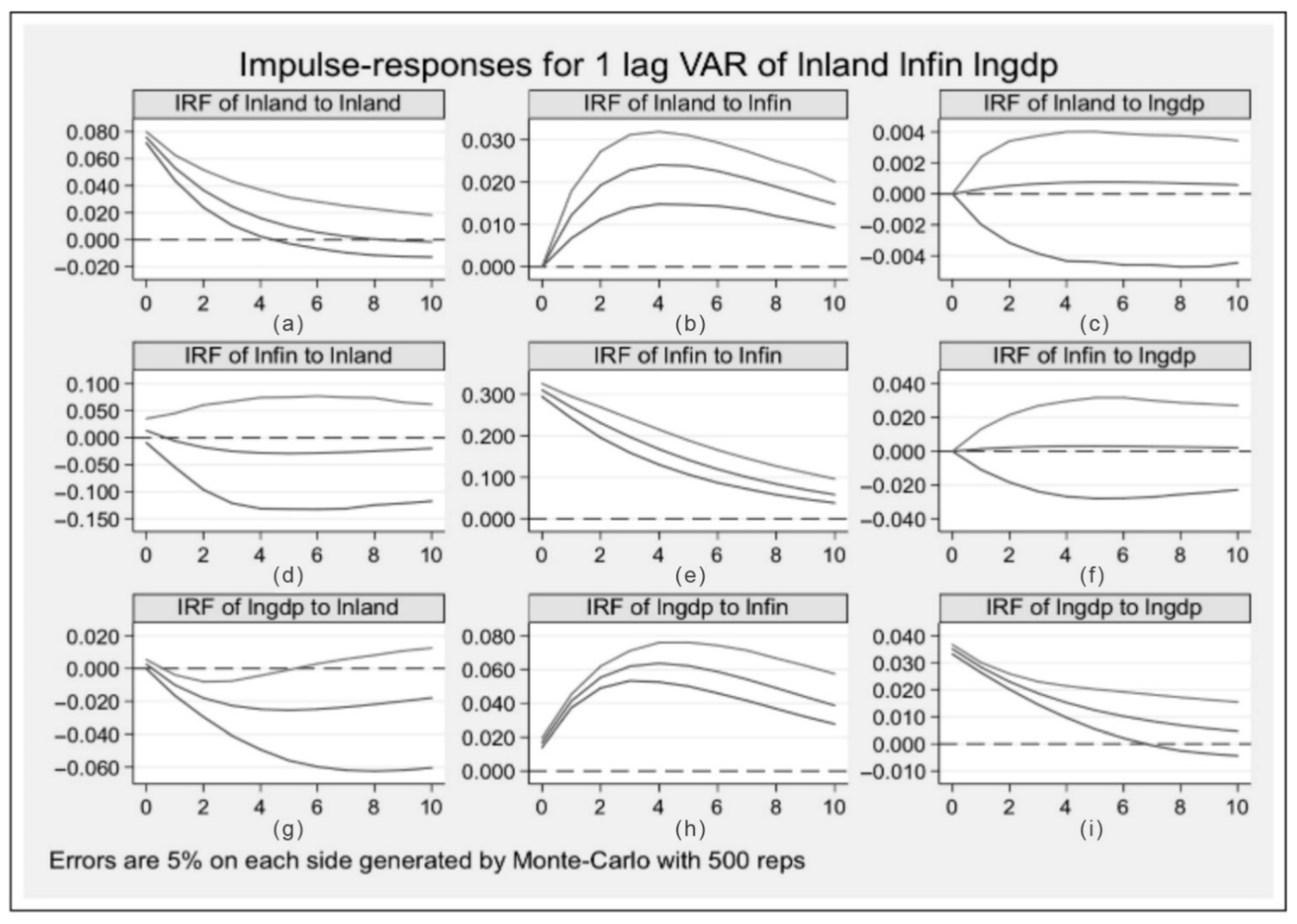

4.4. Impulse-Response Analysis

4.5. Variance Decomposition

5. Conclusions and Policy Implications

- (1)

- Urban land expansion and land finance both affect economic growth. A rational view of the negative externalities accompanied by such expansion should be considered. First, urban land expansion is an inevitable phenomenon resulting from economic development and urbanization. Urban land has a higher efficiency than rural land; therefore, control of this expansion is critical. Regulatory policies should focus on preventing over rapid or excessive expansion and urban sprawl. Second, the dual land-ownership system has made urban expansion achievable through the expropriation of rural collective land. Government’s power to expropriate should be strictly limited to serving the public interest, with farmers and collectives receiving market prices as compensation. The government should not treat all land development as public interest. Third, governments should improve the efficiency of construction land, in particular, industrial land, which should be allocated by market-oriented means, and establish a mechanism for the withdrawals and transfers of rights to industrial land. Finally, public policies’ control of urban size according to the predicted urban population is beneficial because it delineates and implements a moderately flexible urban-growth boundary, as well as establishes a transaction mechanism for new construction-land indicators among the urban governments.

- (2)

- The pursuit of land finance by local governments has driven the expansion of urban land. Therefore, we should dialectically examine the problems faced by local governments that are highly dependent on land finance. With the development of the economy and the reform of the local tax system, the phenomenon of land finance may disappear. However, attention should be paid to the fact that overreliance on land finance in cities leads to the boom of the real-estate industry and spurred market bubbles that drive prices beyond their fair values. Therefore, herein, two suggestions are offered. First, the responsibilities of local governments, in particular, for economic development, should be reduced. Moreover, transfer payments from central governments to local governments should be increased to eliminate the fiscal gap and reduce the incentives for local governments to pursue land finance. Second, taxes and fees should be reformed to increase local government revenues. Lessons can be learnt from the experiences of the United States and other developed countries where property taxes are imposed. Property tax accounts for about more than half of the revenues raised by the local governments. At present, feasible measures include reforming the Chinese property tax system, broadening its base, and raising the ceiling rates.

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- Brueckner, J.K. Urban sprawl: Diagnosis and remedies. Int. Reg. Sci. Rev. 2000, 23, 160–171. [Google Scholar] [CrossRef]

- Seto, K.C.; Kaufmann, R.K.; Woodcock, C.E. Landsat reveals China’s farmland reserves, but they’re vanishing fast. Nature 2000, 406, 121. [Google Scholar] [CrossRef] [PubMed]

- Sahana, M.; Hong, H.; Sajjad, H. Analyzing urban spatial patterns and trend of urban growth using urban sprawl matrix: A study on Kolkata urban agglomeration, India. Sci. Total Environ. 2018, 628–629, 1557–1566. [Google Scholar] [CrossRef] [PubMed]

- Jaeger, J.A.G.; Bertiller, R.; Schwick, C.; Kienast, F. Suitability criteria for measures of urban sprawl. Ecol. Indic. 2010, 10, 397–406. [Google Scholar] [CrossRef]

- Ding, C.; Lichtenberg, E. Land and urban economic growth in China. J. Reg. Sci. 2010, 51, 299–317. [Google Scholar] [CrossRef]

- Zheng, H.; Wang, X.; Cao, S. The land finance model jeopardizes China’s sustainable development. Habitat Int. 2014, 44, 130–136. [Google Scholar] [CrossRef]

- Seto, K.C.; Fragkias, M.; Güneralp, B.; Reilly, M.K. A meta-analysis of global urban land expansion. PLoS ONE 2011, 6, e23777. [Google Scholar] [CrossRef]

- Zimmermann, P.; Tasser, E.; Leitinger, G.; Tappeiner, U. Effects of land-use and land-cover pattern on landscape-scale biodiversity in the European Alps. Agric. Ecosyst. Environ. 2010, 139, 13–22. [Google Scholar] [CrossRef]

- Li, G.; Li, F. Urban sprawl in China: Differences and socioeconomic drivers. Sci. Total Environ. 2019, 673, 367–377. [Google Scholar] [CrossRef]

- Wu, Q.; Li, Y.; Yan, S. The incentives of China’s urban land finance. Land Use Policy 2015, 42, 432–442. [Google Scholar]

- Ding, C. Land policy reform in China: Assessment and prospects. Land Use Policy 2003, 20, 109–120. [Google Scholar] [CrossRef]

- Huang, D.; Chan, R.C. On ‘Land Finance’in urban China: Theory and practice. Habitat Int. 2018, 75, 96–104. [Google Scholar] [CrossRef]

- Zhang, W.; Xu, H. Effects of land urbanization and land finance on carbon emissions: A panel data analysis for Chinese provinces. Land Use Policy 2017, 63, 493–500. [Google Scholar] [CrossRef] [Green Version]

- Peterson, G.E.; Kaganova, O. Integrating Land Financing into Subnational Fiscal Management; World Bank Policy Research Working Paper No.5409; World Bank: Washington, DC, USA, 2010. [Google Scholar]

- Ye, F.; Wang, W. Determinants of Land Finance in China: A Study Based on Provincial-level Panel Data. Aust. J. Public Adm. 2013, 3, 293–303. [Google Scholar]

- Wang, F.; Liu, Y. Panel granger test on urban land expansion and fiscal revenue growth in China’s prefecture-level cities. Acta Geol. Sin. 2013, 68, 1595–1606. (In Chinese) [Google Scholar]

- Zhao, K.; Xu, T.; Li, P.; Zhang, A. Relationship between urban land expansion and land finance at different stages of economic development: An empirical study based on panel data of 264 cities. J. Huazhong Agric. Univ. (Soc. Sci. Ed.) 2015, 4, 95–100. (In Chinese) [Google Scholar]

- Liu, Q.; Ou, M.; Sheng, Y.; Guo, J. Analysis of Relationships between Two Types of Land Finance and Urban Land Expansion: A Panel Co-integration Test of Provincial Level. Chin. J. Popul. Resour. Environ. 2014, 24, 32–37. (In Chinese) [Google Scholar]

- Ye, L.; Wu, A.M. Urbanization, land development, and Land Financing: Evidence from Chinese cities. J. Urban Aff. 2014, 36 (Suppl. 1), 354–368. [Google Scholar] [CrossRef]

- Tian, L. Land use dynamics driven by rural industrialization and land finance in the peri-urban areas of China: The examples of Jiangyin and Shunde. Land Use Policy 2015, 45, 117–127. [Google Scholar] [CrossRef]

- Liu, Y.; Fan, P.; Yue, W.; Song, Y. Impacts of land finance on urban sprawl in China: The case of Chongqing. Land Use Policy 2018, 72, 420–432. [Google Scholar] [CrossRef]

- Wang, J.; Gu, G. Study on contribution of land element to urban economic growth in China. China Popul. Resour. Environ. 2015, 25, 10–17. (In Chinese) [Google Scholar]

- Jiang, H.; Xia, Y.; Qu, F. Research on contribution of construction land expansion to economic growth and its regional difference. China Land Sci. 2009, 23, 6–10. [Google Scholar]

- Xie, H.; Zhu, Z.; Wang, B.; Liu, G.; Zhai, Q. Does the expansion of urban construction land promote regional economic growth in China? evidence from 108 Cities in the Yangtze River Economic Belt. Sustainability 2018, 10, 4073. [Google Scholar] [CrossRef] [Green Version]

- Deng, X.; Huang, J.; Rozelle, S.; Uchida, E. Economic Growth and the Expansion of Urban Land in China. Urban Stud. 2010, 47, 813–843. [Google Scholar] [CrossRef]

- Yang, Z.; Li, C.; Fang, Y. Driving factors of the industrial land transfer price based on a geographically weighted regression model: Evidence from a rural land system reform pilot in China. Land 2020, 9, 7. [Google Scholar] [CrossRef] [Green Version]

- Tan, M.; Li, X.; Xie, H.; Lu, C. Urban land expansion and arable land loss in China—a case study of Beijing–Tianjin–Hebei region. Land Use Policy 2005, 22, 187–196. [Google Scholar] [CrossRef]

- Liu, J.; Zhan, J.; Deng, X. Spatio-temporal patterns and driving forces of urban land expansion in China during the economic reform era. AMBIO J. Hum. Environ. 2005, 34, 450–455. [Google Scholar] [CrossRef]

- Li, Z.; Luan, W.; Zhang, Z.; Su, M. Relationship between urban construction land expansion and population/economic growth in Liaoning Province, China. Land Use Policy 2020, 99, 105022. [Google Scholar] [CrossRef]

- Brown-Luthango, M. Capturing land value increment to finance infrastructure investment—possibilities for South Africa. Urban Forum. 2010, 22, 37–52. [Google Scholar] [CrossRef]

- Zhang, T. Land market forces and government’s role in sprawl. Cities 2000, 17, 123–135. [Google Scholar] [CrossRef]

- Fan, X.; Zheng, D.; Shi, M. How does land development promote China’s urban economic growth? The mediating effect of public infrastructure. Sustainability 2016, 8, 279. [Google Scholar] [CrossRef] [Green Version]

- Mo, J. Land financing and economic growth: Evidence from Chinese counties. China Econ. Rev. 2018, 50, 218–239. [Google Scholar] [CrossRef]

- Chen, Z.; Chen, L. Changes in taxation institution, land finance and economic growth. Financ. Trade Econ. 2011, 12, 24–29. (In Chinese) [Google Scholar]

- Hou, S.; Song, L.; Wang, J.; Ali, S. How land finance affects green economic growth in Chinese cities. Land 2021, 10, 819. [Google Scholar] [CrossRef]

- Lin, G.C.; Zhang, A.Y. Emerging spaces of neoliberal urbanism in China: Land commodification, municipal finance and local economic growth in prefecture-level cities. Urban Stud. 2015, 52, 2774–2798. [Google Scholar] [CrossRef]

- Ewing, R. Is Los Angeles-style sprawl desirable? J. Am. Plan. Assoc. 1997, 63, 107–126. [Google Scholar] [CrossRef]

- Xu, N. What gave rise to China’s land finance? Land Use Policy 2019, 87, 104015. [Google Scholar] [CrossRef]

- Fan, X.; Qiu, S.; Sun, Y. Land finance dependence and urban land marketization in China: The perspective of strategic choice of local governments on land transfer. Land Use Policy 2020, 99, 105023. [Google Scholar] [CrossRef]

- Wang, L.; Wu, H.; Hao, Y. How does China’s land finance affect its carbon emissions? Struct. Chang. Econ. Dyn. 2020, 54, 267–281. [Google Scholar] [CrossRef]

- Li, S.; Luo, B. Estimation of the size of Chinese land finance. J. Cent. Univ. Financ. Econ. 2010, 5, 12–17. [Google Scholar]

- Mieszkowski, P.; Mills, E.S. The Causes of Metropolitan Suburbanization. J. Econ. Perspect. 1993, 7, 135–147. [Google Scholar] [CrossRef] [Green Version]

- Deng, X.; Huang, J.; Rozelle, S.; Uchida, E. Growth, population and industrialization, and urban land expansion of China. J. Urban Econ. 2008, 63, 96–115. [Google Scholar] [CrossRef]

- Zhao, K.; Xu, T.; Zhang, A. Urban land expansion, economic growth, and quality of economic growth. J. Nat. Resour. 2016, 31, 390–401. (In Chinese) [Google Scholar]

- Zhang, B.; Li, J.; Tian, W.; Chen, H.; Kong, X.; Chen, W.; Zhao, M.; Xia, X. Spatio-temporal variances and risk evaluation of land finance in China at the provincial level from 1998 to 2017. Land Use Policy 2020, 99, 104804. [Google Scholar] [CrossRef]

- Zhong, T.; Zhang, X.; Huang, X.; Liu, F. Blessing or curse? Impact of land finance on rural public infrastructure development. Land Use Policy 2019, 85, 130–141. [Google Scholar] [CrossRef]

- Jawadi, F.; Mallick, S.K.; Sousa, R.M. Fiscal and monetary policies in the BRICs: A panel VAR approach. Econ. Model. 2016, 58, 535–542. [Google Scholar] [CrossRef]

- Andrews, D.W.K.; Lu, B. Consistent model and moment selection criteria for GMM estimation with applications to dynamic panel data models. J. Econom. 2001, 101, 123–164. [Google Scholar] [CrossRef]

- Sudhira, H.S.; Ramachandra, T.V.; Jagadish, K.S. Urban sprawl: Metrics, dynamics and modelling using GIS. Int. J. Appl. Earth Obs. Geoinf. 2004, 5, 29–39. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Variable | Measurement | Data Source |

|---|---|---|

| Urban land expansion | Urban construction land area | China Statistical Yearbook and China City Statistical Yearbook |

| Land finance | Land-transfer revenue and land-related tax revenue | China Land and Resources Statistics Yearbook, China Land and Resources Yearbook, and Finance Yearbook of China |

| Economic growth | Real GDP | China Statistical Yearbook and statistical yearbook of each province |

| Series | Test Type | ||||

|---|---|---|---|---|---|

| LLC Test | Breitung Test | IPS Test | Fisher-ADF | Fisher-PP | |

| lnland | −7.3762 *** (0.0000) | 0.8928 (0.8140) | −1.8780 ** (0.0302) | 164.6123 *** (0.0000) | 193.3150 *** (0.0000) |

| lnfin | −4.9013 *** (0.0000) | −0.3642 (0.3578) | −4.3316 *** (0.000) | 161.6238 *** (0.0000) | 155.8744 *** (0.0000) |

| lngdp | −6.1138 *** (0.0000) | 1.1232 (0.8693) | −3.3321 *** (0.0004) | 174.5040 *** (0.0000) | 19.1564 *** (1.0000) |

| Lag | Test Criteria | Conclusion | ||

|---|---|---|---|---|

| AIC | BIC | HQIC | ||

| 1 | −5.2781 | −4.4173 * | −4.9397 * | Lag 1 |

| 2 | −5.2815 * | −4.2953 | −4.8928 | |

| 3 | −4.4025 | −3.2770 | −3.9576 | |

| Coef. | Std. Err. | Z | 95% Conf. Interval | |||

|---|---|---|---|---|---|---|

| lnland | L1.lnland | 0.6954 | 0.0777 | 8.9500 | 0.0000 | (0.5431, 0.8477) |

| L1.lnfin | 0.0387 | 0.0120 | 3.2300 | 0.0010 | (0.0152, 0.0622) | |

| L1.lngdp | 0.0090 | 0.0382 | 0.2300 | 0.8150 | (−0.0659, 0.0838) | |

| lnfin | L1.lnland | −0.2334 | 0.3497 | −0.6700 | 0.5040 | (−0.9189, 0.4519) |

| L1.lnfin | 0.8641 | 0.0488 | 17.7100 | 0.0000 | (0.7685, 0.9597) | |

| L1.lngdp | 0.0399 | 0.1983 | 0.2000 | 0.8410 | (−0.3488, 0.4285) | |

| lngdp | L1.lnland | −0.1761 | 0.0391 | −4.5000 | 0.0000 | (−0.2527, −0.0995) |

| L1.lnfin | 0.0894 | 0.0055 | 16.2600 | 0.0000 | (0.0786, 0.1001) | |

| L1.lngdp | 0.8078 | 0.0210 | 38.4500 | 0.0000 | (0.7666, 0.8490) |

| Dependent Variable | Explanatory Variable | Chi2 | O-Value |

|---|---|---|---|

| Δlnland | Δlnfin | 10.4340 | 0.0000 |

| Δlngdp | 0.0550 | 0.8150 | |

| All | 12.7670 | 0.0020 | |

| Δlnfin | Δlnland | 0.4458 | 0.5040 |

| Δlngdp | 0.0405 | 0.8410 | |

| All | 1.0907 | 0.5800 | |

| Δlngdp | Δlnland | 20.2900 | 0.0000 |

| Δlnfin | 264.5000 | 0.0000 | |

| All | 291.1700 | 0.0000 |

| Response Variable | Period (Years) | Impulse Variable | ||

|---|---|---|---|---|

| lnland | lnfin | lngdp | ||

| lnland | 1 | 1.0000 | 0.0000 | 0.0000 |

| 5 | 0.8690 | 0.1310 | 0.0000 | |

| 10 | 0.7430 | 0.2570 | 0.0000 | |

| 15 | 0.7110 | 0.2890 | 0.0000 | |

| 20 | 0.7050 | 0.2950 | 0.0000 | |

| lnfin | 1 | 0.0020 | 0.9980 | 0.0000 |

| 5 | 0.0070 | 0.9930 | 0.0000 | |

| 10 | 0.0150 | 0.9840 | 0.0000 | |

| 15 | 0.0180 | 0.9810 | 0.0000 | |

| 20 | 0.0190 | 0.9810 | 0.0000 | |

| lngdp | 1 | 0.0040 | 0.1850 | 0.8110 |

| 5 | 0.0890 | 0.7330 | 0.1780 | |

| 10 | 0.1210 | 0.7790 | 0.1000 | |

| 15 | 0.1300 | 0.7830 | 0.0880 | |

| 20 | 0.1320 | 0.7830 | 0.0850 | |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Zhao, K.; Chen, D.; Zhang, X.; Zhang, X. How Do Urban Land Expansion, Land Finance, and Economic Growth Interact? Int. J. Environ. Res. Public Health 2022, 19, 5039. https://doi.org/10.3390/ijerph19095039

Zhao K, Chen D, Zhang X, Zhang X. How Do Urban Land Expansion, Land Finance, and Economic Growth Interact? International Journal of Environmental Research and Public Health. 2022; 19(9):5039. https://doi.org/10.3390/ijerph19095039

Chicago/Turabian StyleZhao, Ke, Danling Chen, Xupeng Zhang, and Xiaojie Zhang. 2022. "How Do Urban Land Expansion, Land Finance, and Economic Growth Interact?" International Journal of Environmental Research and Public Health 19, no. 9: 5039. https://doi.org/10.3390/ijerph19095039

APA StyleZhao, K., Chen, D., Zhang, X., & Zhang, X. (2022). How Do Urban Land Expansion, Land Finance, and Economic Growth Interact? International Journal of Environmental Research and Public Health, 19(9), 5039. https://doi.org/10.3390/ijerph19095039