1. Introduction

China has now become the largest CO

2 emitter in the world [

1]. Based on the International Energy Agency (IEA), CO

2 emissions caused by fuel combustion in China increased to 9134.9 Mt in 2014, 333% growth compared with 1990. Especially, power generation from coal combustion was responsible for 47% total CO

2 emissions. Referring to the China Electricity Council, the generation capacity of coal-fired power plants in 2016 was 4288.6 TWh, accounting for 71.6% of the whole generation capacity [

2]. In general, the development tendency of coal-fired power is still steadily rising. It is believed that this trend is expected to last owing to increasing energy consumption [

3,

4,

5,

6].

Currently, developing renewable energy is the mainstream method for achieving emission reduction. Most renewable energy could be considered clean because of no direct carbon emissions during its using process. According to statistics by National Energy Administration, while using renewable energy generates electricity instead of coal, each 1 kWh can reduce CO

2 emissions by 0.7–0.85 kg. During 12th Five-Year period, there are 7 billion tons of emission reduction achieved by renewable energy power generation, which is expected to be 14 billion tons with generating totally 1.9 trillion kWh electricity by renewable energy (hydro, wind, solar and biomass energy) during the 13th Five-Year period [

7]. Although the carbon reduction effect with renewable energy is obvious, they fail to substitute for fossil energy absolutely due to technical limitation, resource endowment and large energy demand: development of new energy resources such as solar energy, wind energy and biomass energy are always restricted by technology and environmental conditions as well as low efficiency and high cost; the scale of hydropower is limited by environmental conditions and safety issues [

8]. Given the potential huge power energy demand, Intergovernmental Panel on Climate Change (IPCC) and IEA both consider carbon capture and storage (CCS) technology as the critical mitigation measure in both developed and developing countries that highly depend on fossil fuels [

9]. CCS technology has the advantage because of its non-intricate business relationship and almost zero emission compared with contract energy management and electric vehicles [

8]. With the coal share of electricity mix being 60% in 2020, CCS retrofit has been deemed as an attractive emission mitigation alternative for coal-fired power industry [

10]. There is great potential for CCS implementation in China including immense government support [

3,

11], coal-dominated energy structure [

12] and large geological storage capacity [

13].

Many scholars have paid attention to the overall circumstances for development tendency, benefits and problems of CCS implementation. Ming et al. [

8] used SWOT (Strengths, Weaknesses, Opportunities and Threats) method to demonstrate that CCS technology was a sound and workable way to curtail CO

2 emissions with the huge market and imperfect policy. Huaman and Jun [

14] analyzed global CCS technology activities such as Large Scale Integrated Projects (LSIP) and showed the urgency of CCS demonstration in the world. Li et al. [

15] elaborated on technology maturity and sustainability, and external factors of carbon capture, utilization, and storage (CCUS) in China. Lai et al. [

16] studied the CCS innovation system, demonstrating knowledge development of CCS performed well in China, but technology diffusion and market creation were relatively weak.

Considering strengths and weaknesses, power enterprises are faced with irreversibility, uncertainty and flexibility of CCS investment [

17]. The irreversibility means the CCS project will be transferred into huge sunk cost once carried out. As CCS is still in the early stage of technological development, the investment in it possesses considerable uncertainties. The high uncertainty from the CCS investment denotes volatile CO

2 prices and fuel prices, electricity tariff, power plant lifetime, investment cost, operation and maintenance (O&M) cost, government incentive, technological feasibility, etc., all of which affect investment to different degrees [

18,

19]. Flexibility means the timing of CCS retrofit investment is flexible, which has an economic value during the decision-making period [

3]. Therefore, it is crucial to have a thorough grasp of investment condition and select an appropriate decision-making approach to reduce risk.

There exist many traditional methods to assess renewable energy projects, including net present value (NPV), internal rate of return (IRR), return on investment, payback period, benefit–cost ratio, etc., of which the NPV method is commonly used to evaluate these investments [

20]. Specifically, many scholars used net present value (NPV) method to evaluate CCS retrofit investment previously [

9,

21,

22,

23,

24,

25,

26,

27]. The NPV means the sum of the present value of all cash flows produced by the project, and the decision criterion to implement the project is NPV>0. Nevertheless, it could be non-profitable under NPV rules when neglecting the irreversibility of sunk-cost, the uncertainty related to future cash flows, and the flexible opportunity of CCS retrofit timing, which would underrate the investment value based on static information [

17,

28]. Thus, traditional valuation methods are unsuitable for evaluating power generation investments [

20]. Different from above methods, real options approach (ROA) remedies intrinsic deficiencies of NPV method and is appropriate for various energy projects with the following characteristics: (1) high uncertainty; (2) great managerial flexibility; and (3) NPV near zero [

29]. The ROA reformulates the NPV so that the scenarios of great uncertainty, which compose the investments, are considered. The total investment value (TIV) considering real options is the sum of the static NPV and the value caused by management flexibility. The decision criterion of ROA is TIV > 0.

ROA considers investors’ choice subject to flexibility when uncertainty and irreversibility exist. Enterprises have the right to decide whether to invest CCS, so reducing risk and obtaining additional value of uncertainty [

20]. Heydari et al. [

30] developed a real options model in either full CCS or partial CCS retrofits taking uncertain electricity, CO

2 and coal prices into account and concluded the optimum stopping boundaries were dramatically sensitive to carbon price volatility. Eckhause and Herold [

31] employed a stochastic dynamic programming to obtain optimal funding schemes for project option of full-scale carbon capture plants in EU. By using dynamic programming and Monte Carlo simulation, Zhou et al. [

3] discussed policy uncertainty described by stochastic carbon price under three representative types of technology to determine the best strategy for investing CCS in China. Chen et al. [

4] obtained impacts of subsidy for electricity on CCS investment and coactions between carbon market and subsidy policy under uncertainties of carbon, coal and electricity prices based on Monte Carlo simulation. The investment irreversibility in CCS retrofit implies an option to defer, similar to an American financial call option. On this occasion, discrete real options model, i.e., binomial or multinomial lattice model has an advantage over continuous model due to its greater application for American options and other more complex types of options, and is usually employed to assess CCS investment [

17,

19,

32,

33].

Reviewing existing literature, research on CCS retrofit valuation under ROA has been mainly conducted on the single option model for the carbon capture phase and only considered as a call option. In reality, CCS retrofit is a series of investment decision-making processes including initial demonstration project stage and subsequent commercial operation stage, with obvious multi-stage characteristics [

34,

35,

36,

37]. Each stage contains diverse kinds of options, with each option having a certain spatial and temporal structure of dynamic correlation and mutual influence [

38,

39,

40]. Sequential investment decisions consist of a series of real options with embedded managerial flexibility. These multi-stage compound real options are comprised of mutually related investment opportunities: the early upstream investment engenders potential downstream investment opportunity; meanwhile, the downstream investment opportunity demands the acceptance of the upstream investment [

41]. Each option in different stages is interrelated, and the total value of the project investment cannot be equal to the simple addition of the individual option values [

42].

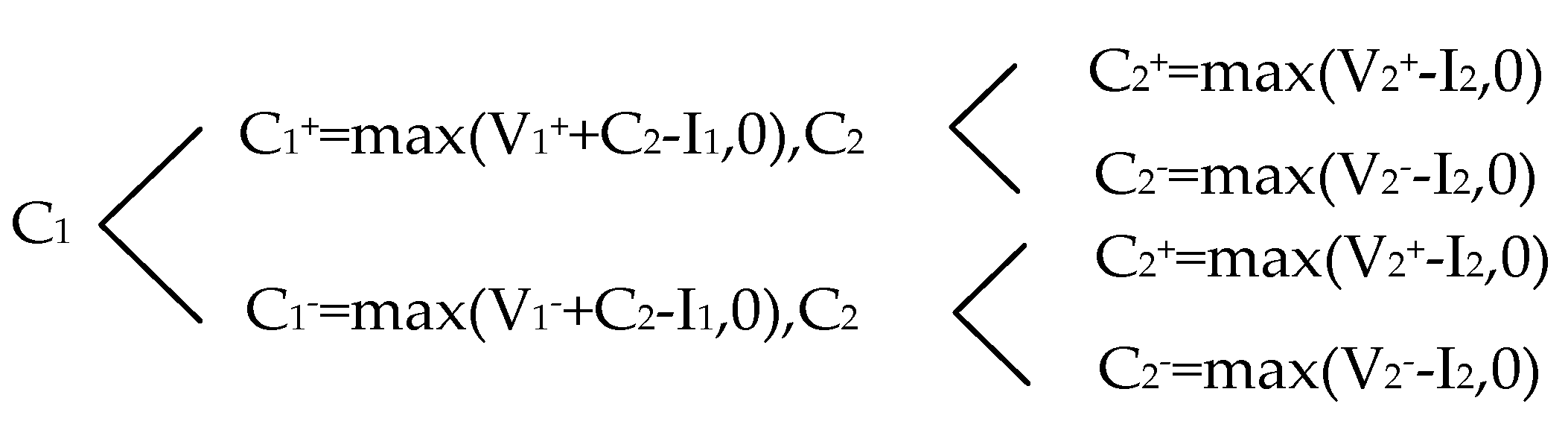

Specifically, the CCS investment decision-making is a dynamic sequential process [

43]. These two stages of CCS retrofit investment are independent and interrelated. The power enterprise should decide whether to continue or change the scale of investment after each stage of investment is completed [

44]. It is apparent that CCS retrofit investment project has strong characteristics of compound real options. Therefore, it is beneficial and necessary to assess CCS retrofit project with compound ROA to conduct a more comprehensive evaluation. However, to the authors’ best knowledge, there is no previous work employing a compound real options model to evaluate CCS retrofit investment.

Moreover, all of the previous studies use different emission factors to estimate certified emission reductions (CERs), critical data in the evaluation model, based on different power generation unit types (for example, 900 g/kWh [

4,

18], 893 g/kWh [

10,

17], and 762 g/kWh [

19]). However, this will fail to consider discrepancies in CO

2 emissions caused by a specific coal-fired power plant using different kinds of fuel and accounting ways, and CO

2 emissions generated from desulfurization process may be neglected. Therefore, it is necessary to use special calculation method of CERs considering specific power plants, to make the whole investment feasibility analysis results more accurate.

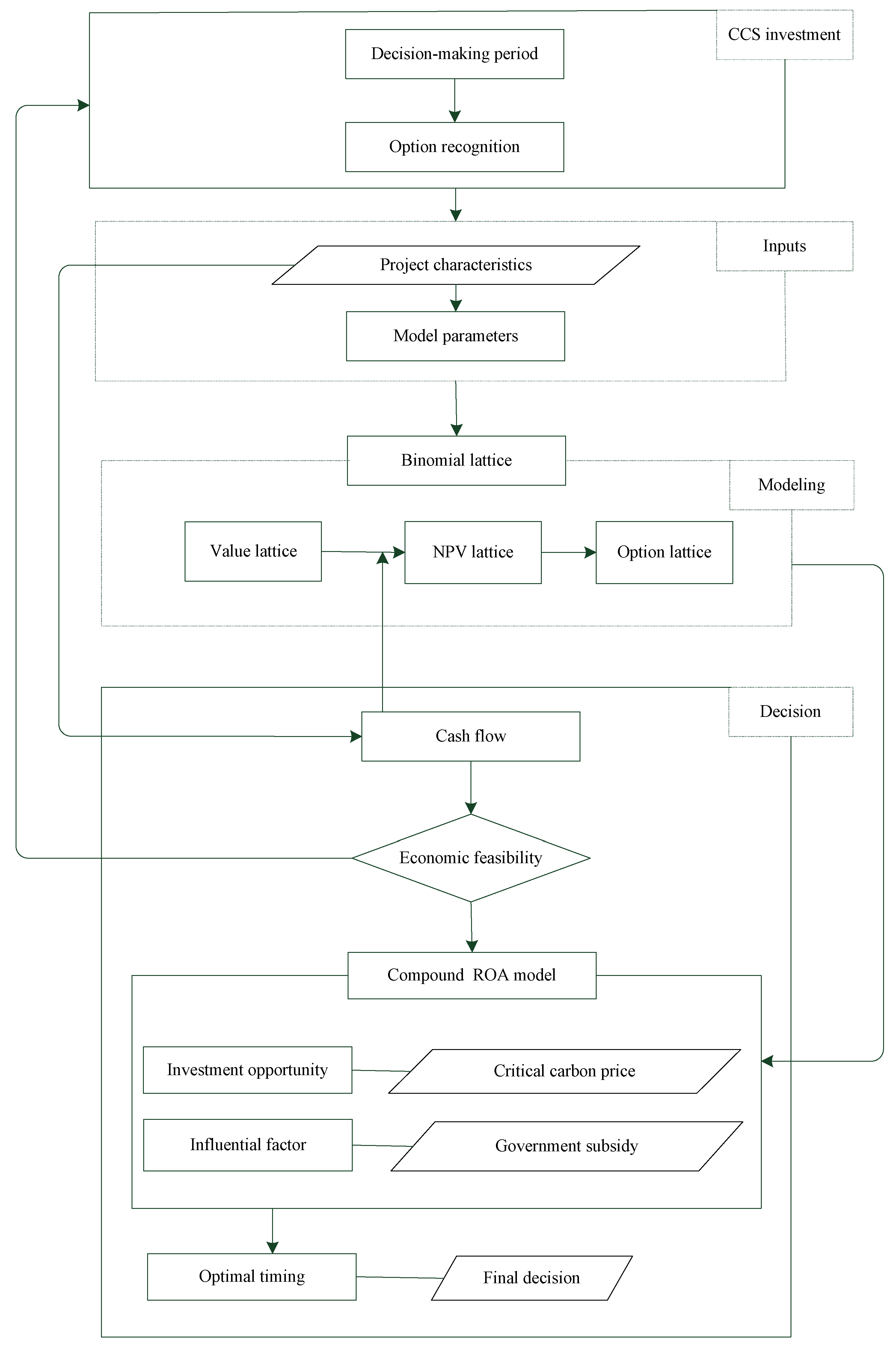

To contribute to filling the gaps in the existing studies, we conducted this study from the following aspects. Firstly, a sequential two-stage compound real options model using binomial lattice method was established to value the CCS retrofit investment in an existing coal-fired power plant in China. Three types of CO2 emission accounting approaches based on diverse conditions were proposed to calculate CERs instead of estimate, which make the options model more realistic and results obtained more precise. Secondly, we considered the uncertainties not only from external factors but also from technology itself including: government subsidy, carbon price, coal price, investment and O&M cost. Finally, the model considered the value of total options. Here, we discuss the impacts of government subsidy under different scenarios at each stage on the critical carbon price to invest in CCS project, which is helpful to the determination of when and whether to invest. Moreover, the focus was on determining respective decisive influential factors of initiating the CCS investment at each period. This can be instructive to formulate corresponding policy to offer an incentive to invest.

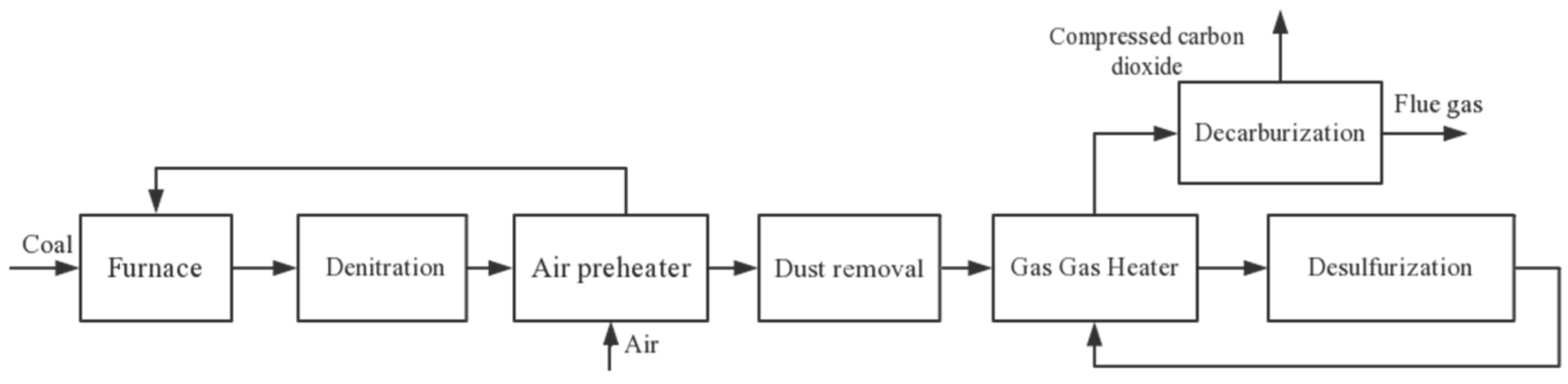

Therefore, this paper sheds light on the current research in following points. It is the first try to establish a compound real options model to evaluate CCS investment feasibility for power plants, which has the typical two-stage investment characteristics, to conduct a more comprehensive and suitable evaluation than previous single option models. Second, by exploring the relationship between two options and their mutual influence on investment decision-making, we first determine respective decisive factors of initiating CCS retrofit investment at each stage. Then, we discuss the impact of subsidy policy on total investment value and critical carbon prices in different scenarios of government subsidies. Third, we present a brief flue gas treatment process equipped with a post-combustion CCS system in a coal-fired power unit. The highlight is that calculation approaches of CERs under different conditions using the thermodynamics principle are distinguished from previous estimation methods for CERs to make analysis results more accurate. The results obtained would be particularly useful in providing appropriate timing for investment decisions under uncertainty as well as information for power enterprises’ CCS technology evaluation and related policy-making.

3. Data Collection and Case Study

Currently, diverse power generation techniques exist among pulverized coal (PC) plants in China. Ultra-supercritical PC and supercritical PC plants are strategically selected by the power sector for new capacity additions coupled with pollution control technologies. Based on the national industry policy, 600 MW and larger-capacity units are required for thermal power generation in the future. A developing trend of clean and high-efficiency power generation technologies is inevitable [

50]. Therefore, we choose supercritical PC as the representative technology for the conventional coal-fired power plant.

An existing 630 MW supercritical coal-fired power generation unit located in China with post-combustion capture technology was an applied case of CCS retrofitting evaluation. Technological parameters of power generation for accounting CO

2 emissions and performance of CCS system were from internal observed data and experimental results of this power plant. Other critical data such as carbon and coal prices, investment cost and returns and the rest necessary parameters, were obtained from previous research or set by this paper. The investor considers retrofitting the CCS system in 2017, with the time step being one year. Meanwhile, the lifetime of the power plant is assumed to be 40 years, 15 years for the demonstration phase and the remaining 25 years for the commercial phase [

4]. To simplify the analysis, it was assumed that emission reductions obtained from CCS system are CERs [

17,

19]. In addition, the electric production was assumed unchanged after CCS retrofit [

10].

According to the parameters provided (

Table 2), the volatile content of coal and other industrial data are not measured by the power plant except for the low calorific value of coal, so Equation (3) can be applied to calculate CO

2 emissions from coal combustion.

Table 3 shows the accounting results of the CO

2 emissions from one power unit in 2016.

Since 2013, China has opened seven carbon trading pilot cities, and the nation-wide carbon trading market was formed at the end of 2017 [

51]. However, China’s carbon trading market is not yet mature, with existing deficiencies: the exchange platform between these seven cities are independent of each other, with no unified market pricing mechanism; and the scale of the pilot market is unbalanced [

46]. For this reason, the CERs from power plants due to CCS retrofit are mainly traded at European Climate Exchange, the largest carbon trading market over the world, through the CDM under the Kyoto Protocol. That is, if the CO

2 emissions of power plants are below the required level, the CERs can be sold to the international market [

19]. Here, the European carbon prices are used to estimate relevant parameters. As for another uncertainty, fuel prices, Bohai-rim steam-coal prices are known as “coal price wind vane” in China. Thus, this kind of steam coal with calorific value of 5500 kcal/kg, having great transit and trading volume in the Bohai Sea ports, is representative of countrywide coal price [

19]. Based on equations calculating the drift and volatility [

17], the concerning parameters of carbon prices and coal prices are obtained:

= 47.978 (the daily average price of 6.222 €/ton from 30 August 2012 to 25 August 2017 was used as the initial carbon price; here, 1 € is equal to 7.711 RMB according to the average exchange rate of the euro to the RMB during this period, i.e., 47.978 RMB/ton) RMB/ton,

= −0.087965, and

= 0.6359663;

= 479.592 (we considered the weekly average price of Bohai-rim steam-coal with calorific value of 5500 kcal/kg during the period from 22 March 2015 to 12 September 2017 as the initial coal price) RMB/ton,

= −0.079779353, and

= 0.092909373.

We collected technological data from related techno-economic assessment literature. These parameters are shown in

Table 4, showing the fundamental parameters of the model in this paper.

6. Policy Implications

First, the development of CCS technology should be vigorously promoted for the purpose of reducing investment cost. Currently, the main obstacle to the application of CCS technology is the high cost. The introduction of foreign advanced technology, equipment and operational experience can accelerate the CCS advance in promotion and application process of China’s coal-fired power plants, but inevitably will bring additional considerable cost. Hence, both the government and the power enterprises should pay attention to independent research and development of CCS technology, to implement independent intellectual property rights and truly drive a significant reduction in carbon capture cost.

Second, because of great cost and low current carbon prices, investment in CCS can mainly be achieved with strong financial support from government including: investment subsidy and clean electricity tariff. However, investment subsidy will bring high financial expenses for the government, which can be decreased by tax transfer strategy. Currently, there has been no carbon tax mechanism in China. The tax charged can be used as subsidy for CCS investment. As for clean electricity tariff for decarbonization in power plants, it has not existed in China until now. Consequently, the government should formulate an efficacious subsidy policy, a reasonable clean electricity price system, and an effective carbon tax mechanism to improve the enthusiasm from power enterprises.

Third, carbon trading scheme should be perfected. Investment in CCS project will produce many CERs, which can bring substantial benefits offsetting part of investment cost. Meanwhile, high volatility of carbon prices can also cause investment postponement under large investment uncertainty. Hence, the government should develop efficacious carbon trading market, improving bargaining power at the market to enhance carbon prices for power enterprises, while lessening the volatility of carbon prices to alleviate investment pressure. Given the nation-wide carbon trading market has been formed recently, in the future, the investment environment for CCS project will be improved in China.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}